new partnership models between oil & gas, oilfield services … kingsley petrofac... · new...

TRANSCRIPT

New partnership models between oil & gas,

oilfield services and engineering companies

Mark Kingsley, SVP, Petrofac 7 November 2012

North Africa Oil & Gas Summit 2012, Vienna

• Shifting focus and evolving partnerships

• Working with NOCs

• Working with local partners

• Capability development

• Creative strategic alliances

1

Overview

2

Shifting Focus

IOCs

• Not about finance

• About technology – moving into ultra deepwater, Arctic, GTL, FLNG etc

• R&D advancement – IOC’s fund over a third of global energy-related global R&D

NOCs

• Share of industry growing

• Wish to retain ownership of resources

• Well financed in many cases but can be resource constrained, especially people

• Open to, and initiators of, new commercial business models

Oilfield Service Companies (OFS)

• Expanding their capability offering

• Taking risk on subsurface – traditionally a no-go area

• Putting up significant capital but no desire to own / book reserves

Working with National Oil Companies

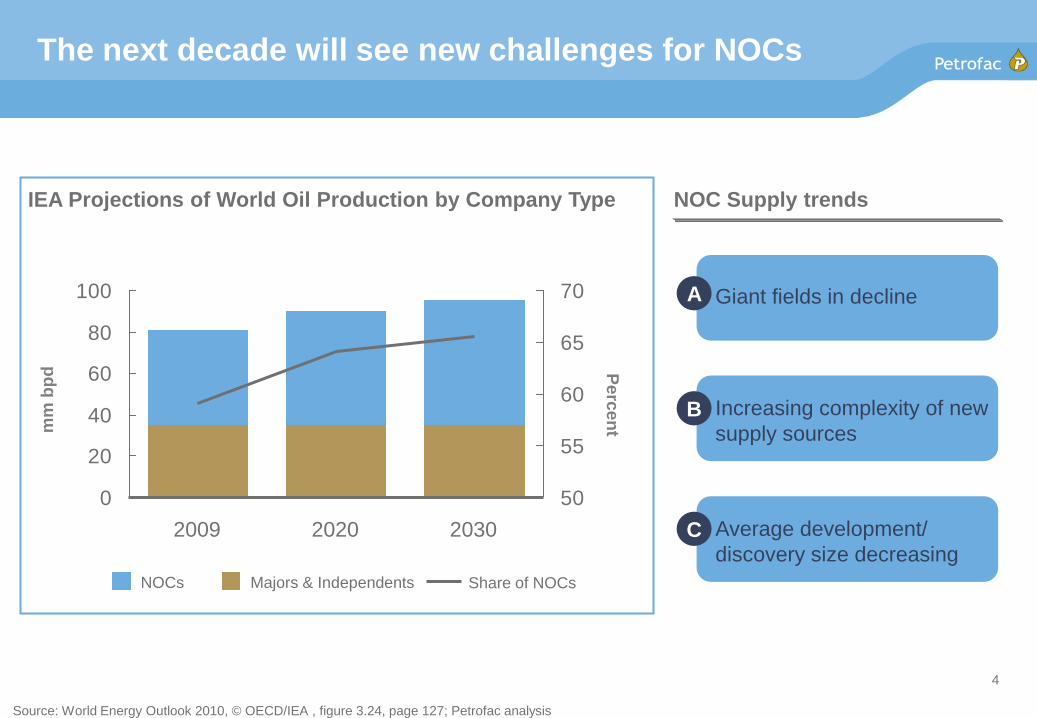

The next decade will see new challenges for NOCs

0

20

40

60

80

100

50

55

60

65

70

P

erc

en

t mm

bp

d

2030 2020 2009

Majors & Independents NOCs

A Giant fields in decline

B Increasing complexity of new

supply sources

C Average development/

discovery size decreasing

Source: World Energy Outlook 2010, © OECD/IEA , figure 3.24, page 127; Petrofac analysis

IEA Projections of World Oil Production by Company Type NOC Supply trends

Share of NOCs

4

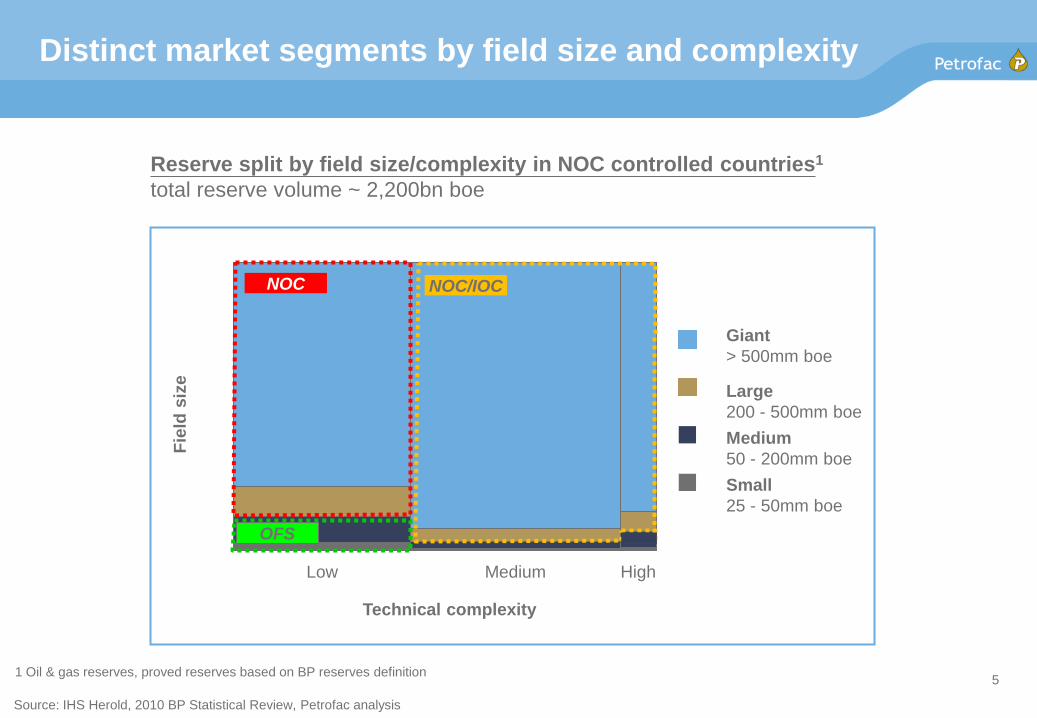

Reserve split by field size/complexity in NOC controlled countries1

total reserve volume ~ 2,200bn boe

Distinct market segments by field size and complexity

1 Oil & gas reserves, proved reserves based on BP reserves definition

Source: IHS Herold, 2010 BP Statistical Review, Petrofac analysis

High Medium Low

Fie

ld s

ize

Technical complexity

Small

25 - 50mm boe

Large

200 - 500mm boe

Medium

50 - 200mm boe

Giant

> 500mm boe

NOC NOC/IOC

OFS

5

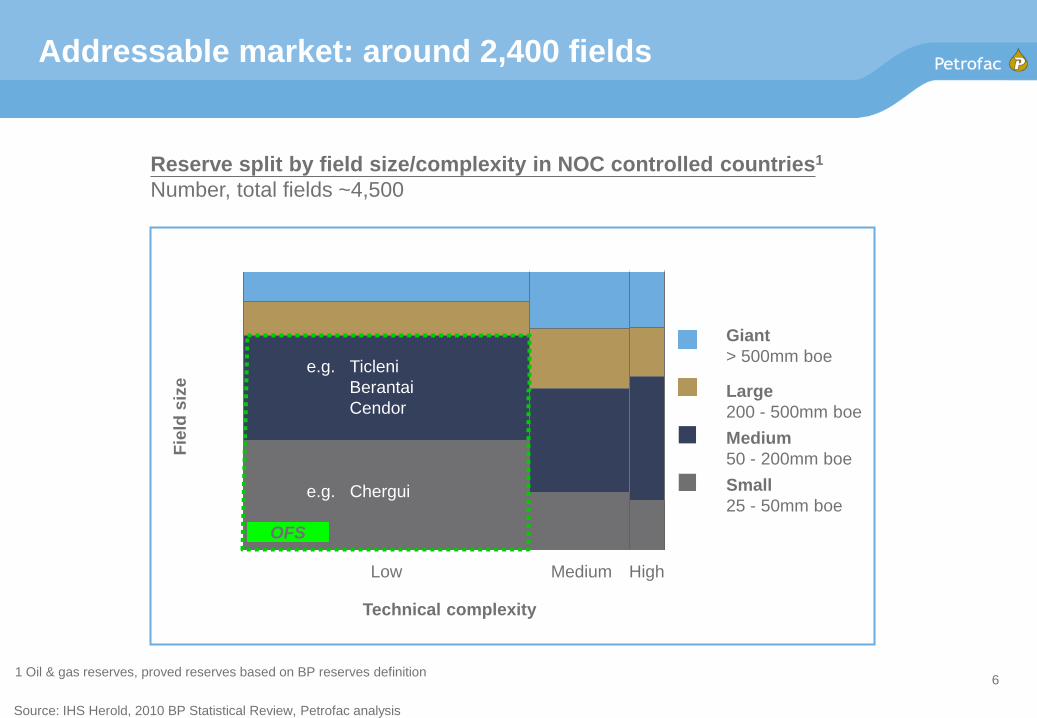

Addressable market: around 2,400 fields

Reserve split by field size/complexity in NOC controlled countries1

Number, total fields ~4,500

High Medium Low

OFS

e.g. Chergui

Fie

ld s

ize

Technical complexity

1 Oil & gas reserves, proved reserves based on BP reserves definition

Source: IHS Herold, 2010 BP Statistical Review, Petrofac analysis

Ticleni

Berantai

Cendor

e.g.

Small

25 - 50mm boe

Large

200 - 500mm boe

Medium

50 - 200mm boe

Giant

> 500mm boe

6

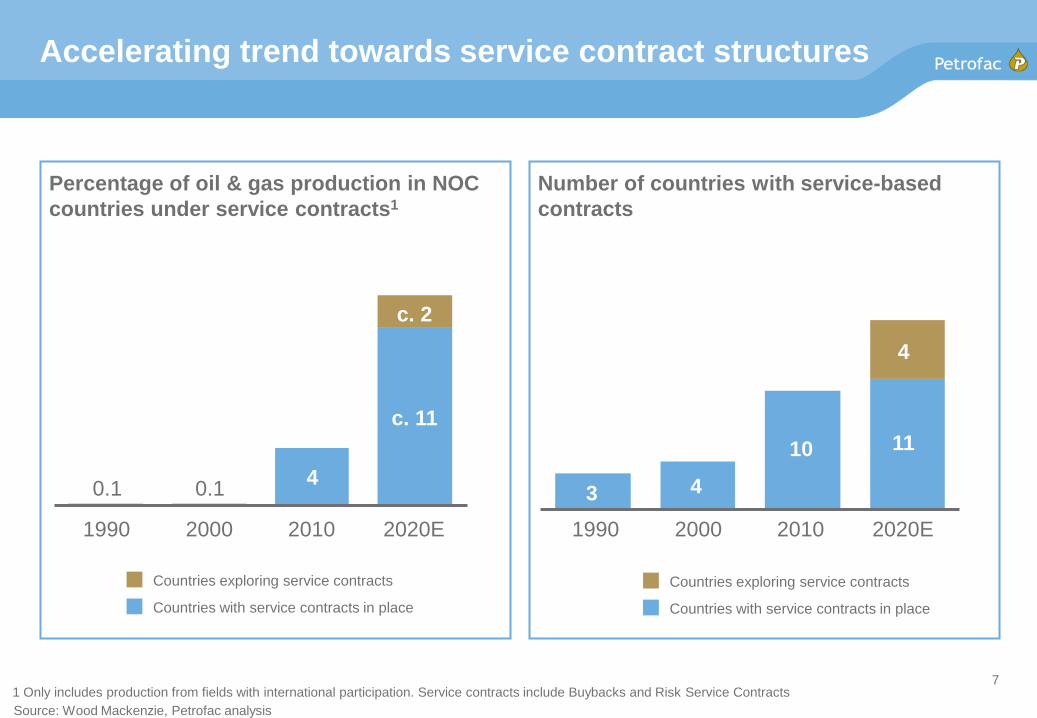

Accelerating trend towards service contract structures

43

2020E

11

4

2010

10

2000 1990 2020E

c. 11

c. 2

2010

4

2000

0.1

1990

0.1

Countries with service contracts in place

Countries exploring service contracts

1 Only includes production from fields with international participation. Service contracts include Buybacks and Risk Service Contracts

Source: Wood Mackenzie, Petrofac analysis

Percentage of oil & gas production in NOC

countries under service contracts1

Number of countries with service-based

contracts

Countries with service contracts in place

Countries exploring service contracts

7

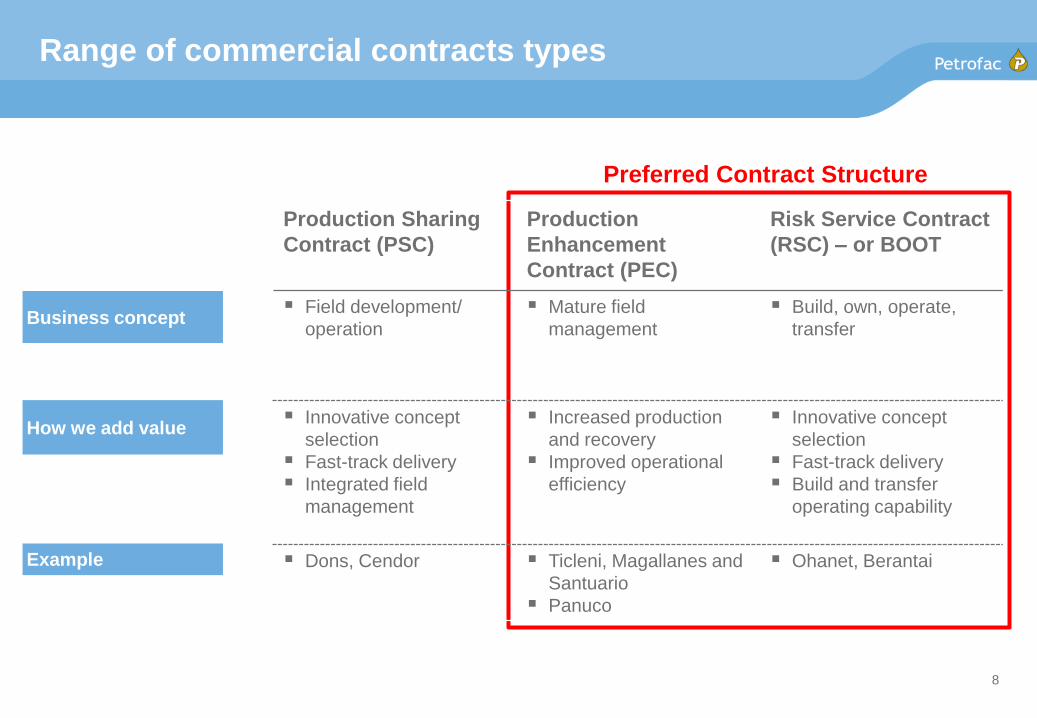

Range of commercial contracts types

Production Sharing

Contract (PSC)

Production

Enhancement

Contract (PEC)

Risk Service Contract

(RSC) – or BOOT

Field development/

operation

Mature field

management

Build, own, operate,

transfer

Innovative concept

selection

Fast-track delivery

Integrated field

management

Increased production

and recovery

Improved operational

efficiency

Innovative concept

selection

Fast-track delivery

Build and transfer

operating capability

Dons, Cendor Ticleni, Magallanes and

Santuario

Panuco

Ohanet, Berantai

Business concept

How we add value

Example

Preferred Contract Structure

8

Enhancing production for NOCs

Production Enhancement Contracts (PECs)

• PECs are used to increase the production from mature fields

– Integration of new technologies, work practices and enhanced recovery techniques

• Petrofac

– Commits to minimum work programmes and capital expenditures

– Funds capex and opex investments

• Contract duration is usually long term

15+ years

• A Joint Management Committee guides

and directs

• Control and all reserves and production

remain with the asset owner

10

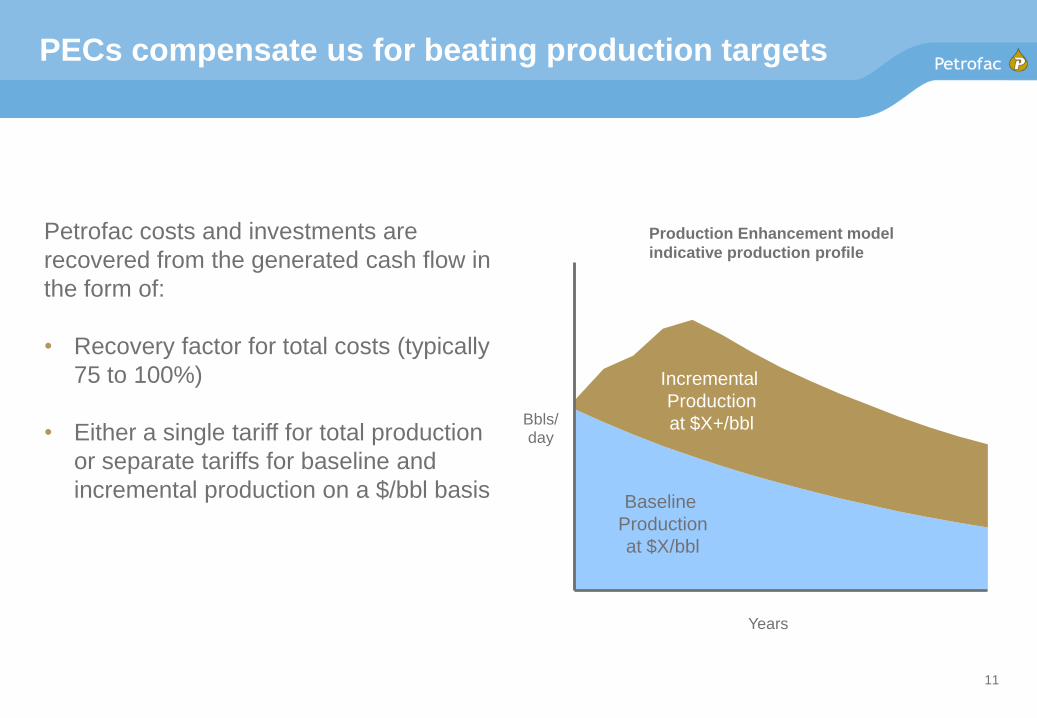

PECs compensate us for beating production targets

Bbls/ day

Years

Incremental

Production

at $X+/bbl

Baseline

Production

at $X/bbl

Petrofac costs and investments are

recovered from the generated cash flow in

the form of:

• Recovery factor for total costs (typically

75 to 100%)

• Either a single tariff for total production

or separate tariffs for baseline and

incremental production on a $/bbl basis

11

Production Enhancement model

indicative production profile

Production Enhancement Contract with OMV Petrom

Award of 15 year PEC for Ticleni oilfields

• 9 commercial fields

• >1200 wells – 450 currently active

Preparation of Field Development Plan

• Reservoir modelling

• Optimization activities modelled

Capital investment commitment

Baseline and incremental tariffs

OMV Petrom retains:

• License for exploitation

• Title to reserves, production, and the

concession

Halted and reversed long term decline

• 2011 production exceeded 2010

production year-on-year

• Have delivered incremental production

every month

12

Challenges:

• Maturity and condition of fields and facilities

• Minimizing the production decline in depleted reservoirs

• Available data is of varying quality

• Identifying behind pipe opportunities

• Investment needed – facilities, well workovers, well reactivation and new wells

• Update and revise work practices

Our Focus:

• We are applying our capability to grow production via:

– Optimizing artificial lift

– Well workovers, re-drills, new wells

– Repair and reactivate shut-in wells

– Water flood program

– Automation

– Facility upgrades

• Our interests with OMV Petrom are aligned as we are paid on a tariff basis for every

barrel produced

• We add value for OMV Petrom by increasing production, allowing them to focus on

Romania’s largest fields

Ticleni PEC

13

Working with local partners

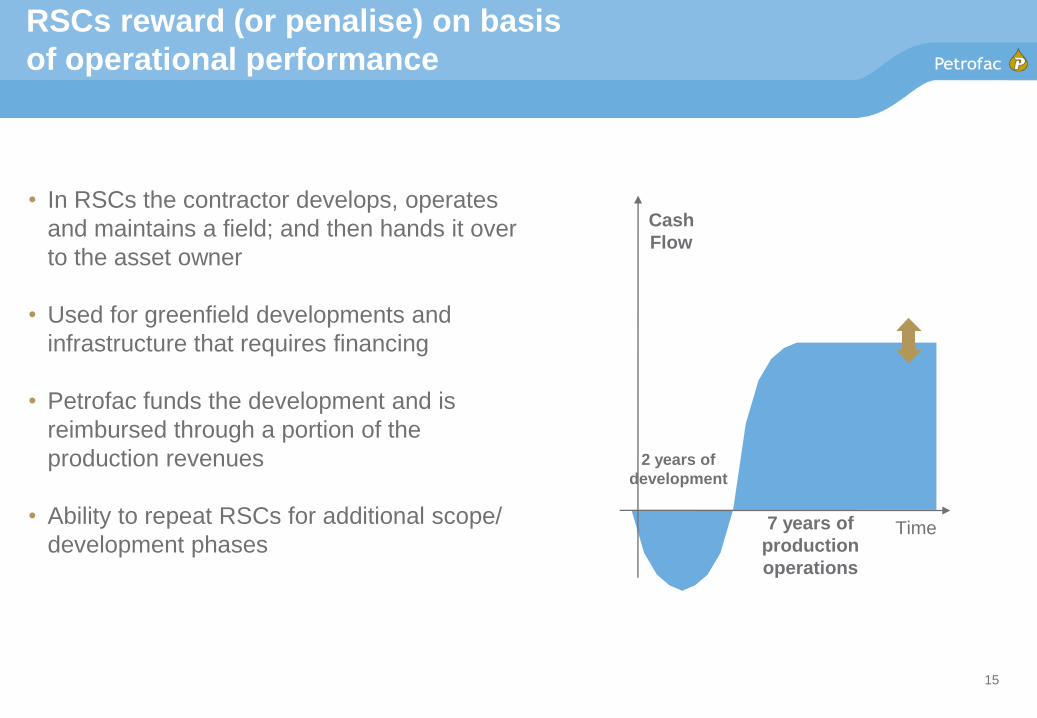

RSCs reward (or penalise) on basis

of operational performance

• In RSCs the contractor develops, operates

and maintains a field; and then hands it over

to the asset owner

• Used for greenfield developments and

infrastructure that requires financing

• Petrofac funds the development and is

reimbursed through a portion of the

production revenues

• Ability to repeat RSCs for additional scope/

development phases

2 years of

development

7 years of

production

operations

Cash

Flow

Time

15

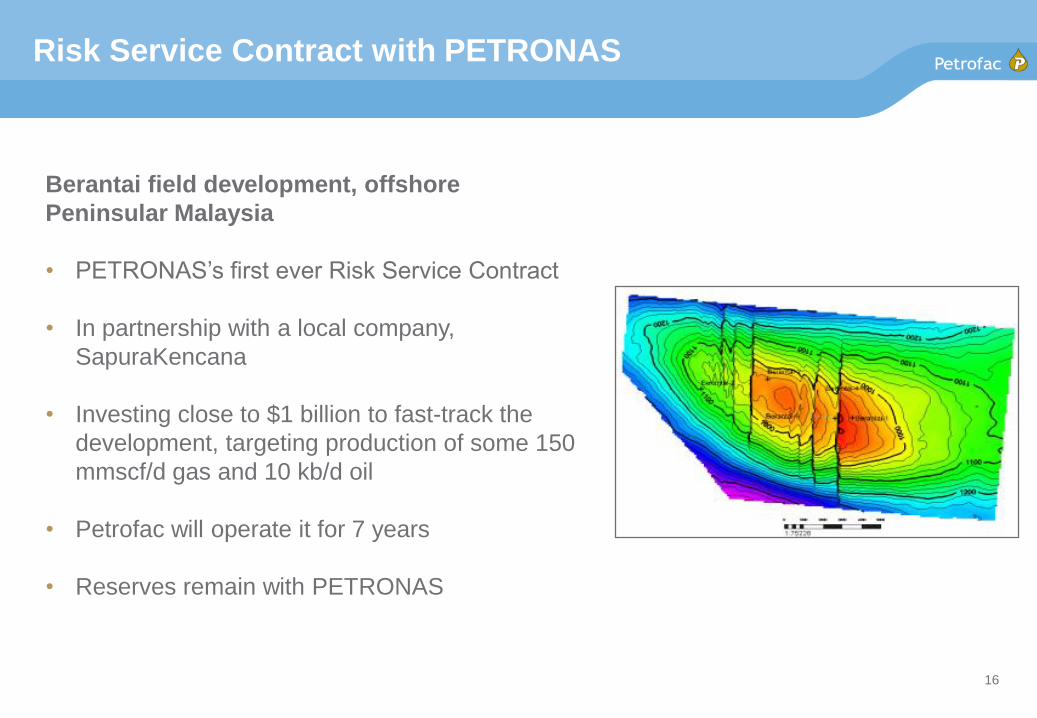

Risk Service Contract with PETRONAS

Berantai field development, offshore

Peninsular Malaysia

• PETRONAS’s first ever Risk Service Contract

• In partnership with a local company,

SapuraKencana

• Investing close to $1 billion to fast-track the

development, targeting production of some 150

mmscf/d gas and 10 kb/d oil

• Petrofac will operate it for 7 years

• Reserves remain with PETRONAS

16

Why Berantai will work

On track to achieve 1st gas in Q4:

• WHP installation in October 2011

• Drilling commenced immediately after installation of WHP

• FPSO on site early September

• Drilling results ahead of expectation

Partners supportive, with secondees embedded into the development team

Project execution:

• Record time for FPSO conversion

• 5.3MM man-hours without an LTI

First RSC in Malaysia

• PETRONAS and Petrofac both going

up a learning curve

• Has demonstrated that RSCs can

work in Malaysia

17

18

NOCs: Capability development

Training as a differentiator

Emergency Response & Crisis

Management simulator- USA / UK /

Singapore / UAE Survival, Fire and Marine Training - UK

Chemical Process Technology Centre

(CPTC) - Singapore

BP Caspian Technical Training Centre

(CTTC) - Baku

Sakahalin Technical Training Centre

(STTC) - Sakhalin

60,000 delegates went through Petrofac training in 2011

19

CPTC is the first training centre in the

world to contain an industry-scale

petrochemical process plant

Designed to operate as an actual

production unit in a typical commercial

plant to allow trainees to experience real

operations, enhancing the training

experience under safe and controlled

conditions

20

Singapore: Petrofac Live Plant Training Centre Chemical Process Technology Centre (CPTC)

Strategic partnerships

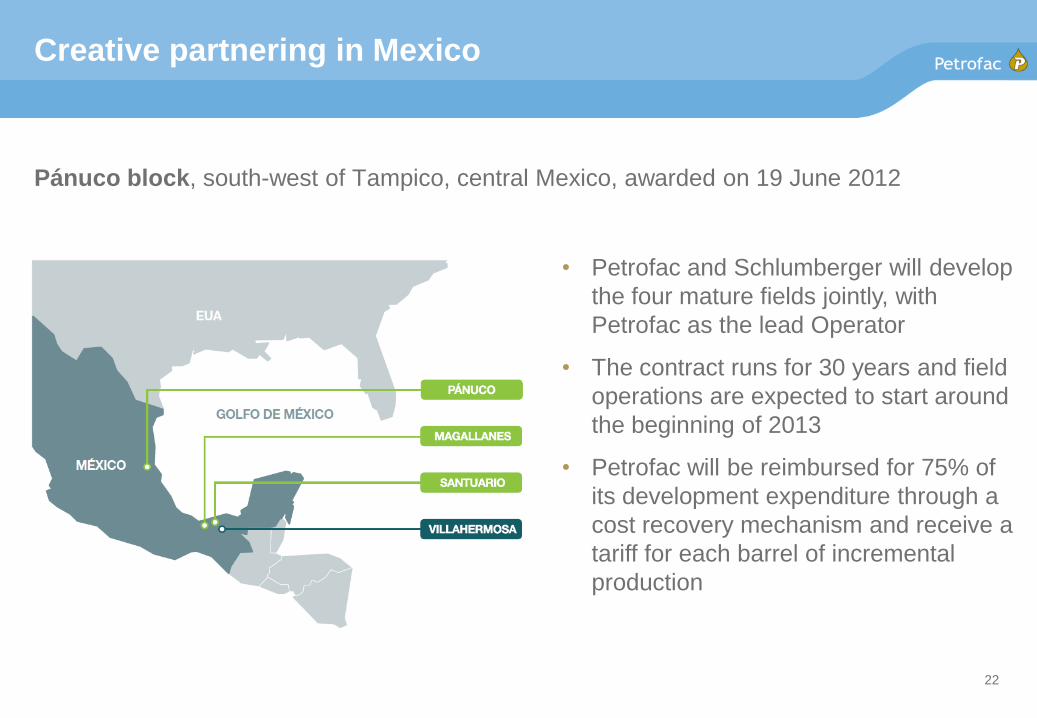

Creative partnering in Mexico

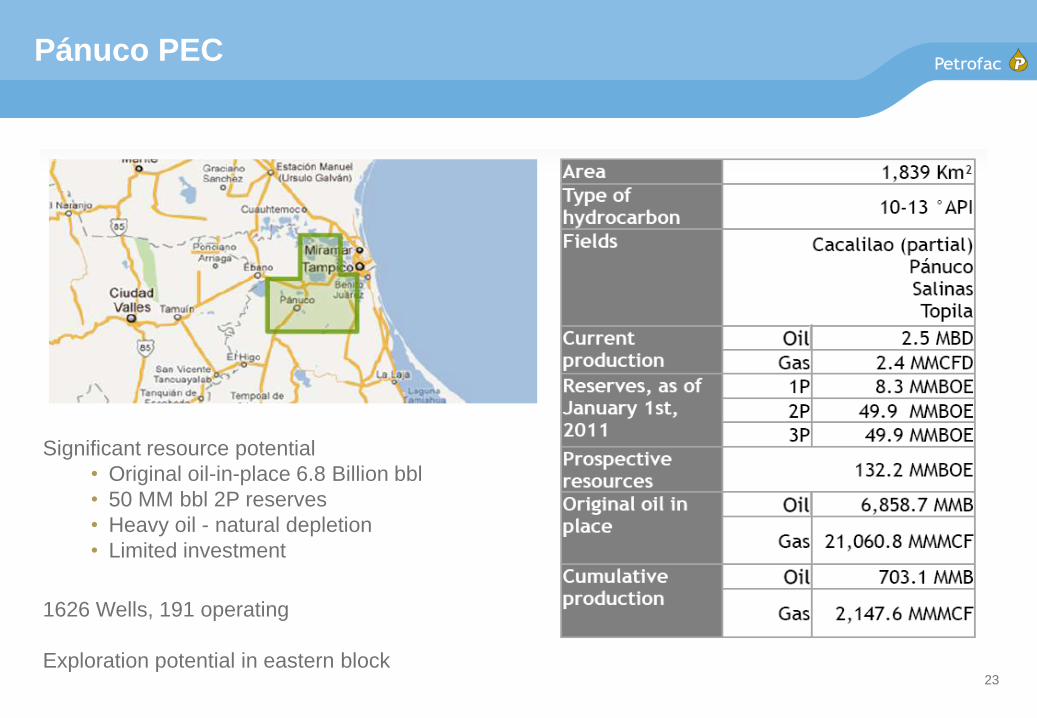

Pánuco block, south-west of Tampico, central Mexico, awarded on 19 June 2012

22

• Petrofac and Schlumberger will develop

the four mature fields jointly, with

Petrofac as the lead Operator

• The contract runs for 30 years and field

operations are expected to start around

the beginning of 2013

• Petrofac will be reimbursed for 75% of

its development expenditure through a

cost recovery mechanism and receive a

tariff for each barrel of incremental

production

Significant resource potential

• Original oil-in-place 6.8 Billion bbl

• 50 MM bbl 2P reserves

• Heavy oil - natural depletion

• Limited investment

1626 Wells, 191 operating

Exploration potential in eastern block

23

Pánuco PEC

Closing remarks

Summary

Fundamental shift in the industry

• Resource nationalism

• Capability has become the issue

• Maturing industry resource base

Roles of traditional players are changing

Strategic partnerships help to fill skills gaps

25

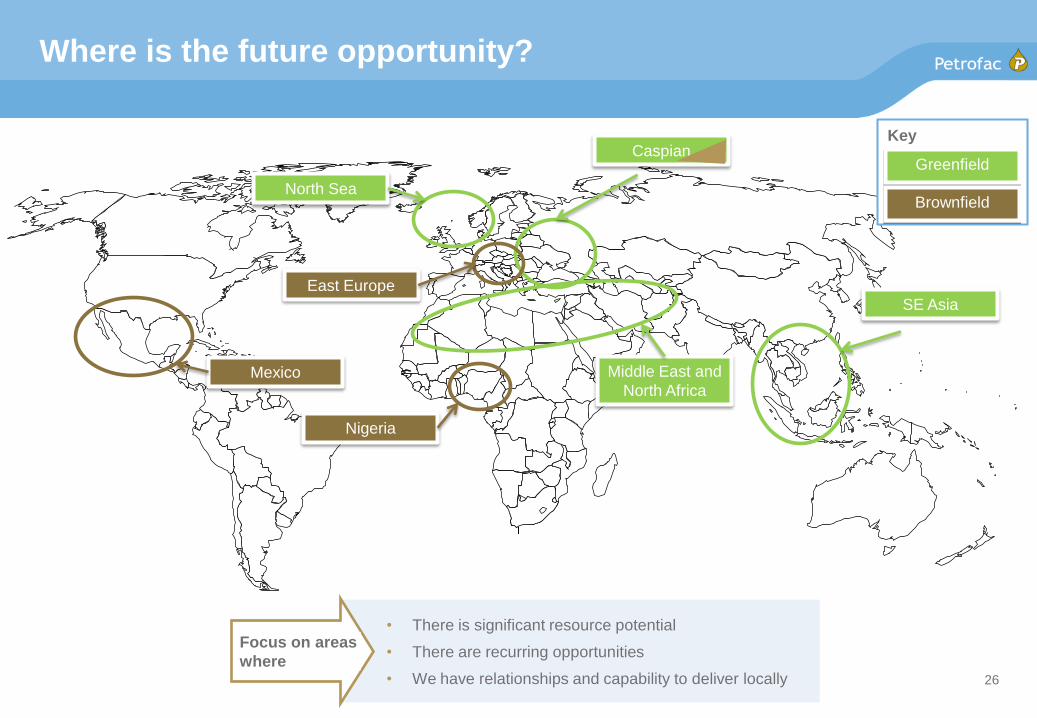

Where is the future opportunity?

North Sea

Caspian

Middle East and

North Africa

SE Asia

East Europe

Mexico

Nigeria

Greenfield

Brownfield

Key

Greenfield

Brownfield

Key

Focus on areas

where

• There is significant resource potential

• There are recurring opportunities

• We have relationships and capability to deliver locally 26

Thank you Petrofac

117 Jermyn Street

2nd Floor

London SW1Y 6HH

Tel +44 207 811 4700

www.petrofac.com