new issue rating: s&p aaa book-entry only see “bond …book-entry only see “bond rating”...

TRANSCRIPT

NEW ISSUE Rating: S&P AAA BOOK-ENTRY ONLY See “BOND RATING” herein. In the opinion of Gilmore & Bell, P.C., Bond Counsel, under existing law and assuming continued compliance with certain requirements of the Internal Revenue Code of 1986, as amended (the “Code”), (1) the interest on the Bonds is excludable from gross income for federal income tax purposes and is not an item of tax preference for purposes of the federal alternative minimum tax imposed on individuals and corporations, (2) the interest on the Bonds is exempt from Missouri income taxation by the State of Missouri, and (3) the Bonds have not been designated as “qualified tax-exempt obligations” within the meaning of Section 265(b)(3) of the Internal Revenue Code of 1986, as amended. See “TAX MATTERS” herein.

$9,905,000 ROCKWOOD R-6 SCHOOL DISTRICT

ST. LOUIS COUNTY, MISSOURI GENERAL OBLIGATION REFUNDING BONDS

SERIES 2011 Dated: Date of Delivery Due: February 1, as shown on the inside cover

The General Obligation Refunding Bonds, Series 2011 (the “Bonds”) will be issued by the Rockwood R-6 School District, St. Louis County, Missouri (the “District”) for the purposes of providing funds to (1) crossover refund certain maturities of the District’s General Obligation Bonds, Series 2006 as further described herein under the section captioned “PLAN OF FINANCING – Refunding of the Refunded Bonds,” (2) pay a portion of the interest on the Bonds and (3) pay costs of issuance related to the Bonds. The Bonds will be issued as fully registered bonds without coupons in the denomination of $5,000 or integral multiples thereof. Principal on the Bonds will be payable annually on February 1, commencing on February 1, 2015. Interest on the Bonds is payable semiannually on each February 1 and August 1, commencing February 1, 2012, by check or draft mailed (or by wire transfer in certain circumstances as described herein) to the persons who are the registered owners of the Bonds as of the close of business on the 15th day of the month preceding the applicable interest payment date.

The Bonds will not be subject to optional redemption.

THE BONDS AND INTEREST THEREON WILL CONSTITUTE GENERAL OBLIGATIONS OF THE DISTRICT, PAYABLE FROM AD VALOREM TAXES WHICH MAY BE LEVIED WITHOUT LIMITATION AS TO RATE OR AMOUNT UPON ALL OF THE TAXABLE TANGIBLE PROPERTY, REAL AND PERSONAL, WITHIN THE TERRITORIAL LIMITS OF THE DISTRICT. The Bonds are offered when, as and if issued by the District and accepted by the Underwriter, subject to the approval of validity by Gilmore & Bell, P.C., St. Louis, Missouri, Bond Counsel, and subject to certain other conditions. It is expected that the Bonds will be available for delivery through the facilities of The Depository Trust Company in New York, New York on or about July 27, 2011.

The date of this Official Statement is July 14, 2011.

$9,905,000 ROCKWOOD R-6 SCHOOL DISTRICT

ST. LOUIS COUNTY, MISSOURI GENERAL OBLIGATION REFUNDING BONDS

SERIES 2011

MATURITY SCHEDULE

Due

(February 1)

Principal Amount

Interest Rate

Yield

Price

CUSIP

2015 $1,520,000 2.00% 1.00% 103.441% 791434 WC3 2015 1,500,000 4.00 1.00 110.325 791434 WE9 2016 6,885,000 4.00 1.25 112.025 791434 WD1

ROCKWOOD R-6 SCHOOL DISTRICT ST. LOUIS COUNTY, MISSOURI

111 East North Street

Eureka, Missouri 63025 (636) 458-7337

BOARD OF EDUCATION

Steve Smith, President

Janet Strate, Vice President Stephen Banton, Director Peggy Devoy, Director

Matt Doell, Director Matthew Fitzpatrick, Director

Keith Kinder, Director Kathy M. Chitwood, Secretary of the Board of Education

DISTRICT ADMINISTRATION

Dr. Bruce T. Borchers, Superintendent

Mr. Randall Smasal, Associate Superintendent of Learning Ms. Shirley Broz, CPA, Chief Financial and Legislative Affairs Officer

Mr. Steven Beatty, Chief Information Officer Mr. Dennis F. Griffith, Assistant Superintendent - Administrative Services

Dr. Kelvin McMillin, Assistant Superintendent - Human Resources Ms. Kim Cranston, Chief Communications Officer

PAYING AGENT

UMB Bank, N.A. St. Louis, Missouri

BOND COUNSEL

Gilmore & Bell, P.C. St. Louis, Missouri

UNDERWRITER

Piper Jaffray & Co. St. Louis, Missouri

REGARDING USE OF THIS OFFICIAL STATEMENT

____________________________

THE BONDS HAVE NOT BEEN REGISTERED WITH THE SECURITIES AND EXCHANGE COMMISSION UNDER THE SECURITIES ACT OF 1933, AS AMENDED, IN RELIANCE UPON THE EXEMPTION CONTAINED IN SECTION 3(a)(2) OF SUCH ACT. The information set forth herein has been obtained from the District and other sources which are deemed to be reliable, but is not guaranteed as to accuracy or completeness by, and is not to be construed as a representation by, the District. The Underwriter has provided the following sentence for inclusion in this Official Statement. The Underwriter has reviewed the information in this Official Statement in accordance with, and as part of, its responsibilities to investors under the federal securities laws as applied to the facts and circumstances of this transaction, but the Underwriter does not guarantee the accuracy or completeness of such information. No dealer, broker, salesperson or any other person has been authorized by the District to give any information or make any representations, other than those contained in this Official Statement, in connection with the offering of the Bonds, and if given or made, such other information or representations must not be relied upon as having been authorized by the foregoing. This Official Statement does not constitute an offer to sell or the solicitation of an offer to buy, nor shall there be any sale of the Bonds by any person in any state in which it is unlawful for such person to make such offer, solicitation or sale. The information herein is subject to change without notice, and neither the delivery of this Official Statement nor the sale of any of the Bonds hereunder shall under any circumstances create any implication that there has been no change in the affairs of the District or the other matters described herein since the date hereof. IN CONNECTION WITH THE OFFERING OF THE BONDS, THE UNDERWRITER MAY OVER-ALLOT OR EFFECT TRANSACTIONS WHICH STABILIZE OR MAINTAIN THE MARKET PRICE OF SUCH BONDS AT A LEVEL ABOVE THAT WHICH MIGHT OTHERWISE PREVAIL IN THE OPEN MARKET. SUCH STABILIZING, IF COMMENCED, MAY BE DISCONTINUED AT ANY TIME.

(i)

TABLE OF CONTENTS Page Page INTRODUCTION ................................................. 1

General .............................................................. 1 Purpose of the Bonds ........................................ 1 Security for the Bonds....................................... 1 Continuing Disclosure ....................................... 1

THE BONDS .......................................................... 2 General .............................................................. 2 Book-Entry Only System .................................. 2 Registration, Transfer and Exchange of Bonds

Upon Discontinuance of Book-Entry Only System ........................................................ 4

No Redemption of Bonds .................................. 4 SECURITY FOR THE BONDS ........................... 5

General .............................................................. 5 Sources and Uses of Funds ............................... 6

VERIFICATION OF MATHEMATICAL COMPUTATIONS ......................................... 6

THE DISTRICT ..................................................... 6 LEGAL MATTERS ............................................... 7

BOND RATING ..................................................... 7 TAX MATTERS ..................................................... 7

Opinion of Bond Counsel .................................. 8 Other Tax Consequences ................................... 8

CONTINUING DISCLOSURE UNDERTAKING ............................................. 9

ABSENCE OF LITIGATION ............................. 10 UNDERWRITING ............................................... 10 CERTAIN RELATIONSHIPS ............................ 11 MISCELLANEOUS ............................................. 11 APPENDIX A - INFORMATION REGARDING

THE DISTRICT APPENDIX B - INDEPENDENT AUDITORS’ REPORT AND AUDITED FINANCIAL STATEMENTS OF THE DISTRICT FOR THE FISCAL YEAR ENDED JUNE 30, 2010

(THIS PAGE LEFT BLANK INTENTIONALLY)

OFFICIAL STATEMENT

$9,905,000 ROCKWOOD R-6 SCHOOL DISTRICT

ST. LOUIS COUNTY, MISSOURI GENERAL OBLIGATION REFUNDING BONDS

SERIES 2011

INTRODUCTION The following introductory information is subject in all respects to more complete information contained elsewhere in this Official Statement. The order and placement of materials in this Official Statement, including the appendices hereto, are not to be deemed to be a determination of relevance, materiality or relative importance, and this Official Statement, including the cover page and appendices should be considered in its entirety. The offering of the Bonds to potential investors is made only by means of the entire Official Statement. General This Official Statement, including the cover page and appendices hereto, is furnished to prospective purchasers in connection with the offering and sale of $9,905,000 aggregate principal amount of General Obligation Refunding Bonds, Series 2011 (the “Bonds”) by the Rockwood R-6 School District, St. Louis County, Missouri (the “District”). The issuance and sale of the Bonds is authorized by a resolution of the Board of Education of the District adopted on July 14, 2011 (the “Resolution”). All capitalized terms used herein and not otherwise defined herein have the meanings assigned to those terms in the Resolution. Purpose of the Bonds The Bonds are being issued for the purposes of providing funds to (1) crossover refund the District’s General Obligation Bonds, Series 2006 maturing in the years 2015 and 2016, outstanding in the aggregate principal amount of $10,100,000 (the “Refunded Bonds”), (2) pay interest on the Bonds to and including February 1, 2014 (the “Crossover Date”) and (3) pay the costs of issuing the Bonds. See the section herein captioned “PLAN OF FINANCING.” Security for the Bonds The Bonds will constitute general obligations of the District and will be payable as to both principal and interest from ad valorem taxes, which may be levied without limitation as to rate or amount upon all the taxable tangible property, real and personal, within the territorial limits of the District. See the section herein captioned “SECURITY FOR THE BONDS - General.” Continuing Disclosure The District has covenanted in a Continuing Disclosure Undertaking to provide certain financial information and to provide notices of material events with the Municipal Securities Rulemaking Board, all in compliance with Rule 15c2-12 promulgated by the Securities and Exchange Commission. See the caption “CONTINUING DISCLOSURE UNDERTAKING” herein.

-2-

THE BONDS General The Bonds are being issued in the aggregate principal amount of $9,905,000. The Bonds are dated as of the date of original delivery of and payment for such Bonds and the principal is payable on February 1 in the years and in the principal amounts set forth on the inside cover page. Interest on the Bonds is calculated at the rates per annum set forth on the inside cover page, computed on the basis of a 360-day year of twelve 30-day months. The Bonds shall consist of fully registered bonds without coupons in denominations of $5,000 or any integral multiple thereof and shall be numbered from 1 consecutively upward, with the number on each Bond preceded by the letter “R.” Interest on the Bonds is payable from the date thereof or the most recent date to which said interest has been paid and is payable semiannually on February 1 and August 1 in each year, beginning February 1, 2012. Payment of the interest on the Bonds will be made to the person in whose name such Bond is registered on the registration books (the “Bond Register”) at the close of business on the 15th day (whether or not a Business Day) of the calendar month next preceding an interest payment date (the “Record Date”). Interest on the Bonds will be paid to the Registered Owners thereof by check or draft mailed by UMB Bank, N.A. (the “Paying Agent”) to each Owner at the address shown on the Bond Register or at such other address as is furnished to the Paying Agent in writing by such Registered Owner, or in the case of an interest payment to any Registered Owner of $500,000 or more in aggregate principal amount of Bonds, by electronic transfer to such Registered Owner upon written notice signed by such Registered Owner and given to the Paying Agent not less than 15 days prior to the Record Date for such interest payment, containing the electronic transfer instructions including the name and address of the bank (which shall be in the continental United States), the ABA routing number and the account number to which such Owner wishes to have such transfer directed. Principal of the Bonds will be paid by check or draft to the Registered Owner of such Bond at the maturity of such Bond or otherwise, upon presentation and surrender of such Bond at the payment office of the Paying Agent in St. Louis, Missouri or at such other payment office as designated by the Paying Agent. Book-Entry Only System

General. The Bonds are available in book-entry only form. Purchasers of the Bonds will not receive certificates representing their interests in the Bonds. Ownership interests in the Bonds will be available to purchasers only through a book-entry system (the “Book-Entry System”) maintained by The Depository Trust Company (“DTC”), New York, New York. The following information concerning DTC and DTC’s book-entry system has been obtained from DTC. The District takes no responsibility for the accuracy or completeness thereof, and neither the Indirect Participants nor the Beneficial Owners should rely on the following information with respect to such matters, but should instead confirm the same with DTC or the Direct Participants, as the case may be. There can be no assurance that DTC will abide by its procedures or that such procedures will not be changed from time to time. DTC will act as securities depository for the Bonds. The Bonds will be issued as fully-registered securities registered in the name of Cede & Co. (DTC’s partnership nominee) or such other name as may be requested by an authorized representative of DTC. One fully-registered Bond will be issued for each maturity of the Bonds, each in the aggregate principal amount of such maturity and will be deposited with DTC. DTC and its Participants. DTC, the world’s largest securities depository, is a limited-purpose trust company organized under the New York Banking Law, a “banking organization” within the meaning of the New York Banking Law, a member of the Federal Reserve System, a “clearing corporation” within the

-3-

meaning of the New York Uniform Commercial Code, and a “clearing agency” registered pursuant to the provisions of Section 17A of the Securities Exchange Act of 1934. DTC holds and provides asset servicing for over 3.5 million issues of U.S. and non-U.S. equity issues, corporate and municipal debt issues, and money market instruments (from over 100 countries) that DTC’s participants (“Direct Participants”) deposit with DTC. DTC also facilitates the post-trade settlement among Direct Participants of sales and other securities transactions in deposited securities, through electronic computerized book-entry transfers and pledges between Direct Participants’ accounts. This eliminates the need for physical movement of securities certificates. Direct Participants include both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, clearing corporations, and certain other organizations. DTC is a wholly-owned subsidiary of The Depository Trust & Clearing Corporation (“DTCC”). DTCC is the holding company for DTC, National Securities Clearing Corporation and Fixed Income Clearing Corporation, all of which are registered clearing agencies. DTCC is owned by the users of its regulated subsidiaries. Access to the DTC system is also available to others such as both U.S. and non-U.S. securities brokers and dealers, banks, trust companies, and clearing corporations that clear through or maintain a custodial relationship with a Direct Participant, either directly or indirectly (“Indirect Participants”). DTC has Standard & Poor’s highest rating: AAA. The DTC Rules applicable to its Participants are on file with the Securities and Exchange Commission. More information about DTC can be found at www.dtcc.com and www.dtc.org. Purchases of Ownership Interests. Purchases of Bonds under the DTC system must be made by or through Direct Participants, which will receive a credit for the Bonds on DTC’s records. The ownership interest of each actual purchaser of each Bond (“Beneficial Owner”) is in turn to be recorded on the Direct and Indirect Participants’ records. Beneficial Owners will not receive written confirmation from DTC of their purchase. Beneficial Owners are, however, expected to receive written confirmations providing details of the transaction, as well as periodic statements of their holdings, from the Direct or Indirect Participant through which the Beneficial Owner entered into the transaction. Transfers of ownership interests in the Bonds are to be accomplished by entries made on the books of Direct and Indirect Participants acting on behalf of Beneficial Owners. Beneficial Owners will not receive certificates representing their ownership interests in the Bonds, except in the event that use of the book-entry system for the Bonds is discontinued. Transfers. To facilitate subsequent transfers, all Bonds deposited by Direct Participants with DTC are registered in the name of DTC’s partnership nominee, Cede & Co., or such other name as may be requested by an authorized representative of DTC. The deposit of Bonds with DTC and their registration in the name of Cede & Co. or such other DTC nominee do not effect any change in beneficial ownership. DTC has no knowledge of the actual Beneficial Owners of the Bonds; DTC’s records reflect only the identity of the Direct Participants to whose accounts such Bonds are credited, which may or may not be the Beneficial Owners. The Direct and Indirect Participants will remain responsible for keeping account of their holdings on behalf of their customers. Notices. Conveyance of notices and other communications by DTC to Direct Participants, by Direct Participants to Indirect Participants, and by Direct Participants and Indirect Participants to Beneficial Owners will be governed by arrangements among them, subject to any statutory or regulatory requirements as may be in effect from time to time. Beneficial Owners of Bonds may wish to take certain steps to augment the transmission to them of notices of significant events with respect to the Bonds, such as tenders, defaults, and proposed amendments to the Bond documents. For example, Beneficial Owners of Bonds may wish to ascertain that the nominee holding the Bonds for their benefit has agreed to obtain and transmit notices to Beneficial Owners. In the alternative, Beneficial Owners may wish to provide their names and addresses to the registrar and request that copies of notices be provided directly to them. Voting. Neither DTC nor Cede & Co. (nor any other DTC nominee) will consent or vote with respect to Bonds unless authorized by a Direct Participant in accordance with DTC’s MMI Procedures. Under its usual procedures, DTC mails an Omnibus Proxy to the District as soon as possible after the record date. The

-4-

Omnibus Proxy assigns Cede & Co.’s consenting or voting rights to those Direct Participants to whose accounts Bonds are credited on the record date (identified in a listing attached to the Omnibus Proxy). Payments of Principal and Interest. Payment of principal of and interest on the Bonds will be made to Cede & Co., or such other nominee as may be requested by an authorized representative of DTC. DTC’s practice is to credit Direct Participants’ accounts upon DTC’s receipt of funds and corresponding detail information from the District or the Paying Agent, on the payment date in accordance with their respective holdings shown on DTC’s records. Payments by Participants to Beneficial Owners will be governed by standing instructions and customary practices, as is the case with securities held for the accounts of customers in bearer form or registered in “street name,” and will be the responsibility of such Participant and not of DTC, the Paying Agent or District, subject to any statutory or regulatory requirements as may be in effect from time to time. Payment of principal of and interest on the Bonds to Cede & Co. (or such other nominee as may be requested by an authorized representative of DTC) is the responsibility of the District or Paying Agent, disbursement of such payments to Direct Participants will be the responsibility of DTC, and disbursement of such payments to the Beneficial Owners will be the responsibility of Direct and Indirect Participants. Discontinuation of Book-Entry System. DTC may discontinue providing its services as depository with respect to the Bonds at any time by giving reasonable notice to the District or the Paying Agent. Under such circumstances, in the event that a successor depository is not obtained, Bond certificates are required to be printed and delivered. The Direct Participants holding a majority position in the Bonds may decide to discontinue use of the system of book-entry only transfers through DTC (or a successor securities depository). In that event, Bond certificates will be printed, registered in the name of DTC’s partnership nominee, Cede & Co. (or such other name as may be requested by an authorized representative of DTC), and delivered to DTC (or a successor securities depository), to be held by it as securities depository for Direct Participants. If, however, the system of book-entry only transfers has been discontinued and a Direct Participant has elected to withdraw its Bonds from DTC (or such successor securities depository), Bond certificates may be delivered to Beneficial Owners in the manner described in the Resolution. Registration, Transfer and Exchange of Bonds Upon Discontinuance of Book-Entry Only System The Paying Agent will keep or cause to be kept the Bond Register at its principal payment office or such other office designated by the Paying Agent. Upon surrender of any Bond at the principal payment office of the Paying Agent, the Paying Agent shall transfer or exchange Bonds as provided in the Resolution. Any Bond may be transferred upon the Bond Register by the person in whose name it is registered and shall be accompanied by a written instrument or instruments of transfer or authorization for exchange, in a form and with guarantee of signature satisfactory to the Paying Agent, duly executed by the Registered Owner thereof or by the Registered Owner’s duly authorized agent. The Owner requesting such transfer or exchange will be required to pay any additional costs or fees that might be incurred in the secondary market with respect to such exchange. In the event any Registered Owner fails to provide a correct taxpayer identification number to the Paying Agent, the Paying Agent may make a charge against such Registered Owner sufficient to pay any governmental charge required to be paid as a result of such failure. No Redemption of Bonds The Bonds are not subject to optional redemption prior to maturity.

-5-

SECURITY FOR THE BONDS General Pledge of Full Faith and Credit. The Bonds will constitute general obligations of the District and will be payable as to both principal and interest from ad valorem taxes, which may be levied without limitation as to rate or amount upon all the taxable tangible property, real and personal, within the territorial limits of the District. Levy and Collection of Annual Tax. Under the Resolution, there is levied upon all of the taxable tangible property within the District a direct annual tax sufficient to produce the amounts necessary for the payment of the principal of and interest on the Bonds as the same become due and payable in each year. Such taxes shall be extended upon the tax rolls in each year, and shall be levied and collected at the same time and in the same manner as the other ad valorem taxes of the District are levied and collected. The proceeds derived from said taxes shall be deposited in the Debt Service Fund, shall be kept separate and apart from all other funds of the District and shall be used solely for the payment of the principal of and interest on the Bonds as and when the same become due and the fees and expenses of the Paying Agent.

PLAN OF FINANCING

Refunding of the Refunded Bonds A portion of the proceeds of the Bonds will be used for the purposes of (a) paying interest on the

Bonds to and including the Crossover Date and (b) redeeming and paying the Refunded Bonds on the Crossover Date at a redemption price of 100% of the principal amount thereof.

The District will enter into an Escrow Trust Agreement dated as of July 1, 2011 (the “Escrow Trust

Agreement”), with UMB Bank, N.A., St. Louis, Missouri, as escrow agent (the “Escrow Agent”). Pursuant to the Escrow Trust Agreement, the District will transfer a portion of the proceeds of the Bonds to the Escrow Agent for deposit in the Escrow Fund (the “Escrow Fund”) established under the Escrow Trust Agreement to purchase direct obligations of, or obligations the principal of and interest on which are unconditionally guaranteed by, the United States of America (the “Escrowed Securities”). The Escrowed Securities will mature in such amounts and at such times as shall be sufficient, together with interest to accrue thereon and any cash deposit to the Escrow Fund, to (a) pay interest on the Bonds to and including the Crossover Date and (b) redeem and pay the principal of the Refunded Bonds on the Crossover Date.

Robert Thomas CPA, LLC, Shawnee Mission, Kansas (the “Escrow Verifier”), a firm of independent

certified public accountants, will provide a report to the effect that the principal of and interest income on the Escrowed Securities, together with any cash deposit in the Escrow Fund, will provide sufficient moneys to make the required payments in accordance with the District’s refunding plan as set forth herein. See the section herein captioned “VERIFICATION OF MATHEMATICAL COMPUTATIONS.”

-6-

Set forth below is a description of the Refunded Bonds being refunded pursuant to the Resolution:

Maturity Date (February 1)

Principal Amount

Interest Rate

CUSIP Number

Redemption Date

Redemption Price

2015 $3,100,000 4.125% 791434 TY9 February 1, 2014 100% 2016 7,000,000 4.125 791434 TZ6 February 1, 2014 100

$10,100,000

Sources and Uses of Funds

The sources and uses of the proceeds of the Bonds are as follows:

Sources of Funds: Par Amount of Bonds $9,905,000.00 Plus: Reoffering Premium 1,035,099.45 Total $10,940,099.45

Uses of Funds: Deposit to Escrow Fund $10,867,729.59 Underwriter’s Discount 39,620.00 Deposit to Costs of Issuance Fund 32,749.86 Total $10,940,099.45

VERIFICATION OF MATHEMATICAL COMPUTATIONS Upon delivery of the Bonds, the Escrow Verifier will deliver to the District and the Underwriter a report indicating that such firm has examined, in accordance with standards established by the American Institute of Certified Public Accountants, the information and assertions provided by the Underwriter and the District and its representatives. Included in the scope of its examination will be a verification of the mathematical accuracy of (a) the adequacy of the maturing principal amount of the Escrowed Securities held in the Escrow Fund, interest earned thereon and certain uninvested cash to (i) pay the interest on the Bonds to and including the Crossover Date and (ii) redeem and pay the principal of and redemption premium, if any, on the Refunded Bonds on the Crossover Date (as described under the caption “PLAN OF FINANCING – Refunding of the Refunded Bonds”), and (b) the mathematical computations supporting the conclusion that the Bonds are not “arbitrage bonds” under Section 148 of the Code. Such verification of the accuracy of the computations will be based upon information supplied by the Underwriter and on interpretations of the Internal Revenue Code of 1986, as amended, provided by Bond Counsel.

THE DISTRICT The District is located in the western portion of St. Louis County, Missouri and the northern portion of Jefferson County, Missouri and covers approximately 150 square miles. The District serves all or part of Ballwin, Chesterfield, Clarkson Valley, Ellisville, Eureka, Fenton, Manchester and Wildwood, Missouri. The District has a population of approximately 116,321. See “APPENDIX A - INFORMATION REGARDING THE DISTRICT” for further information regarding the District.

-7-

LEGAL MATTERS

Legal matters with respect to the authorization, execution and delivery of the Bonds are subject to the approval of Gilmore & Bell, P.C., St. Louis, Missouri, Bond Counsel, whose approving opinion will be available at the time of delivery of the Bonds. The various legal opinions to be delivered concurrently with the delivery of the Bonds express the professional judgment of the attorneys rendering the opinions as to the legal issues explicitly addressed therein. By rendering a legal opinion, the opinion giver does not become an insurer or guarantor of that expression of professional judgment, of the transactions opined upon, or of the future performance of parties to such transaction, nor does the rendering of an opinion guarantee the outcome of any legal dispute that may arise out of the transaction.

BOND RATING Standard & Poor’s, a Division of The McGraw-Hill Companies, Inc. (the “Rating Agency”) has assigned a rating to the Bonds of “AAA” based on the underlying credit of the District. The rating reflects only the view of the Rating Agency at the time such rating is given, and the Underwriter and the District make no representation as to the appropriateness of such rating. An explanation of the significance of such rating may be obtained from the Rating Agency. The District has furnished the Rating Agency with certain information and materials relating to the Bonds and the District that have not been included in this Official Statement. Generally, rating agencies base their ratings on the information and materials so furnished and on investigations, studies and assumptions made by the rating agencies. There is no assurance that a particular rating will be maintained for any given period of time or that it will not be lowered or withdrawn entirely if, in the judgment of the rating agency originally establishing such rating, circumstances so warrant. Neither the Underwriter nor the District has undertaken any responsibility to bring to the attention of the holders of the Bonds any proposed revision or withdrawal of the rating of the Bonds or to oppose any such proposed revision or withdrawal. Any such revision or withdrawal of the ratings could have an adverse effect on the market price and marketability of the Bonds.

TAX MATTERS The following is a summary of the material federal and State of Missouri income tax consequences of holding and disposing of the Bonds. This summary is based upon laws, regulations, rulings and judicial decisions now in effect, all of which are subject to change (possibly on a retroactive basis). This summary does not discuss all aspects of federal income taxation that may be relevant to investors in light of their personal investment circumstances or describe the tax consequences to certain types of owners subject to special treatment under the federal income tax laws (for example, dealers in securities or other persons who do not hold the Bonds as a capital asset, tax-exempt organizations, individual retirement accounts and other tax deferred accounts, and foreign taxpayers), and, except for the income tax laws of the State of Missouri, does not discuss the consequences to an owner under any state, local or foreign tax laws. The summary does not deal with the tax treatment of persons who purchase the Bonds in the secondary market. Prospective investors are advised to consult their own tax advisors regarding federal, state, local and other tax considerations of holding and disposing of the Bonds.

-8-

Opinion of Bond Counsel In the opinion of Gilmore & Bell, P.C., Bond Counsel, under the law existing as of the issue date of the Bonds: Federal and Missouri Tax Exemption. The interest on the Bonds is excludable from gross income for federal income tax purposes and is exempt from income taxation by the State of Missouri. Alternative Minimum Tax. Interest on the Bonds is not an item of tax preference for purposes of computing the federal alternative minimum tax imposed on individuals and corporations, but is taken into account in determining adjusted current earnings for the purpose of computing the alternative minimum tax imposed on certain corporations. Bank Qualification. The Bonds have not been designated as “qualified tax-exempt obligations” within the meaning of Section 265(b)(3) of the Internal Revenue Code of 1986, as amended (the “Code”).

Bond counsel’s opinions are provided as of the date of the original issue of the Bonds, subject to the condition that the District comply with all requirements of the Code that must be satisfied subsequent to the issuance of the Bonds in order that interest thereon be, or continue to be, excludable from gross income for federal income tax purposes. The District has covenanted to comply with all such requirements. Failure to comply with certain of such requirements may cause the inclusion of interest on the Bonds in gross income for federal and Missouri income tax purposes retroactive to the date of issuance of the Bonds. Bond Counsel is expressing no opinion regarding other federal, state or local tax consequences arising with respect to the Bonds but has reviewed the discussion under the heading “TAX MATTERS.” Other Tax Consequences Original Issue Premium. If a Bond is issued at a price that exceeds the stated redemption price at maturity of the Bond, the excess of the purchase price over the stated redemption price at maturity constitutes “premium” on that Bond. Under Section 171 of the Code, the purchaser of that Bond must amortize the premium over the term of the Bond using constant yield principles, based on the purchaser’s yield to maturity. As premium is amortized, the owner’s basis in the Bond and the amount of tax-exempt interest received will be reduced by the amount of amortizable premium properly allocable to the owner. This will result in an increase in the gain (or decrease in the loss) to be recognized for federal income tax purposes on sale or disposition of the Bond prior to its maturity. Even though the owner’s basis is reduced, no federal income tax deduction is allowed. Prospective investors should consult their own tax advisors concerning the calculation and accrual of bond premium.

Sale, Exchange or Retirement of Bonds. Upon the sale, exchange or retirement (including

redemption) of a Bond, an owner of the Bond generally will recognize gain or loss in an amount equal to the difference between the amount of cash and the fair market value of any property received on the sale, exchange or retirement of the Bond (other than in respect of accrued and unpaid interest) and such owner’s adjusted tax basis in the Bond. To the extent a Bond is held as a capital asset, such gain or loss will be capital gain or loss and will be long-term capital gain or loss if the Bond has been held for more than 12 months at the time of sale, exchange or retirement.

Reporting Requirements. In general, information reporting requirements will apply to certain

payments of principal, interest and premium paid on the Bonds, and to the proceeds paid on the sale of the Bonds, other than certain exempt recipients (such as corporations and foreign entities). A backup withholding tax will apply to such payments if the owner fails to provide a taxpayer identification number or certification of foreign or other exempt status or fails to report in full dividend and interest income. The amount of any

-9-

backup withholding from a payment to an owner will be allowed as a credit against the owner’s federal income tax liability.

Collateral Federal Income Tax Consequences. Prospective purchasers of the Bonds should be aware that ownership of the Bonds may result in collateral federal income tax consequences to certain taxpayers, including, without limitation, financial institutions, property and casualty insurance companies, individual recipients of Social Security or Railroad Retirement benefits, certain S corporations with “excess net passive income,” foreign corporations subject to the branch profits tax, life insurance companies, and taxpayers who may be deemed to have incurred or continued indebtedness to purchase or carry or have paid or incurred certain expenses allocable to the Bonds. Bond Counsel expresses no opinion regarding these tax consequences. Purchasers of Bonds should consult their tax advisors as to the applicability of these tax consequences and other federal income tax consequences of the purchase, ownership and disposition of the Bonds, including the possible application of state, local, foreign and other tax laws.

CONTINUING DISCLOSURE UNDERTAKING

The District will covenant in the Continuing Disclosure Undertaking to file certain financial information and operating data relating to the District (updated within not later than 180 days following the end of its fiscal year, which currently ends June 30) (the “Annual Report”) commencing with the Annual Report for the fiscal year ending June 30, 2011, and to file notices of the occurrence of certain enumerated events, if material. The Annual Report shall be filed by or on behalf of the District with the Municipal Securities Rulemaking Board (the “MSRB”) through the Electronic Municipal Market Access system (“EMMA”). The Annual Report shall include:

(a) The audited financial statements of the District for the prior fiscal year, prepared in accordance with general accounting principles.

(b) Information relating to the District and its operations set forth in the tables under the

following sections in Appendix A of this Official Statement: “THE DISTRICT – History of Enrollment” and “PROPERTY TAX INFORMATION – Property Valuations,” “– Tax Rates” “– Tax Collections” and “– Major Taxpayers” and information with respect to litigation if, in the judgment of the District, such litigation would have a material adverse affect on the financial condition of the District.

Within 10 business days after the occurrence of any of the following events, the District shall give, or

cause to be given to the MSRB through EMMA, notice of the occurrence of any of the following events with respect to the Bonds (“Material Events”):

(1) principal and interest payment delinquencies; (2) non-payment related defaults, if material; (3) unscheduled draws on debt service reserves reflecting financial difficulties; (4) unscheduled draws on credit enhancements reflecting financial difficulties; (5) substitution of credit or liquidity providers, or their failure to perform; (6) adverse tax opinions; the issuance by the Internal Revenue Service of proposed or final

determinations of taxability, Notices of Proposed Issue (IRS Form 570-TEB) or other material notices or determinations with respect to the tax status of the Bonds, or other material events affecting the tax status of the Bonds;

(7) modifications to rights of bondholders, if material; (8) bond calls, if material, and tender offers; (9) defeasances;

-10-

(10) release, substitution or sale of property securing repayment of the Bonds, if material; (11) rating changes; (12) bankruptcy, insolvency, receivership or similar event of the District; (13) the consummation of a merger, consolidation, or acquisition involving the District or the sale

of all or substantially all of the assets of the District, other than in the ordinary course of business, the entry into a definitive agreement to undertake such an action or the termination of a definitive agreement relating to any such actions, other than pursuant to its terms, if material; and

(14) appointment of a successor or additional trustee or the change of name of the Paying Agent, if material.

Nothing in the Continuing Disclosure Undertaking shall be deemed to prevent the District from disseminating any other information using the means of dissemination set forth in the Continuing Disclosure Undertaking, or any other means of communication, or including any other information in any Annual Report or notice of occurrence of a Material Event, in addition to that which is required by the Continuing Disclosure Undertaking. If the District chooses to include any information in any Annual Report or notice of occurrence of a Material Event in addition to that which is specifically required, the District shall have no obligation to update such information or include it in any future Annual Report or notice of occurrence of a Material Event. These covenants have been made in order to assist the Underwriter in complying with Rule 15c2-12 promulgated by the Securities and Exchange Commission.

The District has made a similar undertaking with respect to its outstanding general obligation bonds to file an Annual Report for each fiscal year of the District. The District covenanted to include in its Annual Report the District’s audited financial statements for the previous year in addition to updated information relating to the District and its operations. The District is not now and has never been in default with respect to any continuing disclosure obligation of the District under Rule 15c2-12.

ABSENCE OF LITIGATION

As of the date hereof, there is no controversy, suit or other proceeding of any kind pending or, to the

District’s knowledge, threatened wherein or whereby any question is raised or may be raised, questioning, disputing or affecting in any way the legal organization of the District or its boundaries, or the right or title of any of its officers to their respective offices, or the legality of any official act in connection with the authorization, issuance and sale of the Bonds, or the constitutionality or validity of the Bonds or any of the proceedings had in relation to the authorization, issuance or sale thereof, or the levy and collection of a tax to pay the principal and interest thereof, or which might affect the District’s ability to meet its obligations to pay the Bonds.

UNDERWRITING Piper Jaffray & Co. Incorporated (the “Underwriter”), has agreed to purchase the Bonds at a price of $10,900,479.45 (which is equal to the aggregate original principal amount of the Bonds, less an underwriting discount of $39,620.00 plus original issue premium of $1,035,099.45). The Underwriter is purchasing the Bonds for resale in the normal course of the Underwriter’s business activities. The Underwriter reserves the right to offer any of the Bonds to one or more purchasers on such terms and conditions and at such price or prices as the Underwriter, in its discretion, shall determine.

-11-

The Underwriter has entered into an agreement (the “Distribution Agreement”) with Advisors Asset Management, Inc. (“AAM”) for the distribution of certain municipal securities offerings allocated to the Underwriter at the original offering prices. Under the Distribution Agreement, if applicable to the Bonds, the Underwriter will share with AAM a portion of the fee or commission, exclusive of management fees, paid to the Underwriter.

CERTAIN RELATIONSHIPS

Gilmore & Bell, P.C., Bond Counsel, has represented the Underwriter and the Paying Agent in

transactions unrelated to the issuance of the Bonds, but is not representing the Underwriter or the Paying Agent in connection with the issuance of the Bonds.

MISCELLANEOUS The references, excerpts and summaries of all documents referred to herein do not purport to be complete statements of the provisions of such documents, and reference is made to all such documents for full and complete statements of all matters of fact relating to the Bonds, the security for the payment of the Bonds and the rights of the Owners thereof. During the period of the offering, copies of drafts of such documents may be examined at the offices of the Underwriter; following delivery of the Bonds, copies of such documents may be examined at the principal payment office of the Paying Agent. The information contained in this Official Statement has been compiled from official and other sources that are deemed to be reliable, and while not guaranteed as to completeness or accuracy, is believed to be correct as of this date. Any statement made in this Official Statement involving matters of opinion or of estimates, whether or not expressly so stated, are set forth as such and not as representations of fact, and no representation is made that any of the estimates will be realized. The information and expressions of opinion herein are subject to change without notice and neither the delivery of this Official Statement nor any sale made hereunder shall, under any circumstances, create any implication that there has been no change in the information presented herein since the date hereof. This Official Statement is not to be construed as a contract or agreement between the District, the Paying Agent, or the Underwriter and the purchasers or Owners of any Bonds. The District has duly authorized the delivery of this Official Statement.

ROCKWOOD R-6 SCHOOL DISTRICT, ST. LOUIS COUNTY, MISSOURI By: /s/Steve Smith President of the Board of Education

(THIS PAGE LEFT BLANK INTENTIONALLY)

APPENDIX A

INFORMATION REGARDING THE DISTRICT

TABLE OF CONTENTS PAGE

THE DISTRICT .............................................................................................................................................. A-1

General ....................................................................................................................................................... A-1 Board of Education .................................................................................................................................... A-1 Administration ........................................................................................................................................... A-1 Professional Staff ....................................................................................................................................... A-2 Employee Relations ................................................................................................................................... A-2 History of Enrollment ................................................................................................................................ A-3 School Rating and Accreditation ............................................................................................................... A-3 Educational Programs and Services ........................................................................................................... A-4 Educational Facilities ................................................................................................................................. A-4

ECONOMIC INFORMATION CONCERNING THE DISTRICT ........................................................... A-7 Commerce, Industry and Employment ...................................................................................................... A-7 Population and Other Statistics .................................................................................................................. A-9

FINANCIAL INFORMATION CONCERNING THE DISTRICT ......................................................... A-11 Accounting, Budgeting and Auditing Procedures .................................................................................... A-11 Sources of Revenue .................................................................................................................................. A-12 Local Revenue ......................................................................................................................................... A-13 State Revenue ........................................................................................................................................... A-14 Federal Revenue ....................................................................................................................................... A-15 Tax Limitation Provisions ........................................................................................................................ A-15 Fund Placement and Expenditure Restrictions ......................................................................................... A-16 Summary of Revenues, Expenditures and Fund Balances ....................................................................... A-18 Property and Liability Insurance .............................................................................................................. A-18 Pension and Employee Retirement Plans ................................................................................................. A-19

PROPERTY TAX INFORMATION .......................................................................................................... A-19 Property Valuations ................................................................................................................................. A-19 Tax Rates ................................................................................................................................................. A-20 Tax Collections ........................................................................................................................................ A-21 Major Property Taxpayers ....................................................................................................................... A-22 Tax Abatement and Tax Increment Financing ......................................................................................... A-23

DEBT STRUCTURE OF THE DISTRICT ................................................................................................ A-23 Debt Ratios and Related Information ....................................................................................................... A-23 General ..................................................................................................................................................... A-24 General Obligation Indebtedness ............................................................................................................. A-24 Overlapping General Obligation Indebtedness ........................................................................................ A-25 Legal Debt Capacity................................................................................................................................. A-25 Debt Service Requirements for General Obligation Bonds Outstanding ................................................. A-26 Operating Leases ...................................................................................................................................... A-26 No Prior Defaults ..................................................................................................................................... A-27 Future Plans ............................................................................................................................................. A-27

THE DISTRICT

General The Rockwood R-6 School District, St. Louis County, Missouri (the “District”) encompasses approximately 150 square miles and is located in the western portion of St. Louis County, Missouri and a small portion of the District is located in northern Jefferson County, Missouri. The District serves all or part of Ballwin, Chesterfield, Clarkson Valley, Ellisville, Eureka, Fenton, Manchester and Wildwood, Missouri. For the 2010-2011 school year there were 22,480 students enrolled. The District’s average cost per ADA (average daily attendance) for the 2009-2010 school year was $9,451 compared with the Missouri average of $9,751. Board of Education The District is governed by a seven-director Board of Education (the “Board of Education”). The directors are elected for staggered three-year terms. The key roles and responsibilities of the Board of Education are to establish policies for the District, to provide for the general operation and personnel of the District and to oversee the property and affairs of the District. The Board of Education elects a President and Vice President for one-year terms. The Secretary and Treasurer are appointed by the Board of Education.

The present members and officers of the Board of Education are as follows:

Year Current

Name and Title First Elected Term Expires Steve Smith, President and Member 1989 2014 Janet Strate, Vice President and Member 2004 2013 Stephen Banton, Member 1998 2013 Peggy Devoy, Member 2006 2012 Matthew Fitzpatrick, Member 2009 2012 Keith Kinder, Member 2011 2014 Matt Doell, Member 2011 2014

The Board of Education has appointed Shirley Broz, Chief Financial and Legislative Affairs Officer of the District, to serve as Treasurer of the Board of Education and Kathy Chitwood to serve as Secretary of the Board of Education. Administration

The Board of Education appoints the Superintendent of Schools, who is the chief executive officer of the District responsible for carrying out the policies set by the Board of Education. Additional members of the administrative staff and all other employees are appointed by the Board of Education upon recommendation by the Superintendent.

Dr. Bruce T. Borchers. Dr. Borchers was appointed to serve as Superintendent of the District in 2010.

Dr. Borchers has a total of 22 years of experience in education and has previously held the position of Associate Superintendent of Secondary Schools for Anoka-Hennepin Schools in Coon Rapids, Minnesota. Dr. Borchers received a bachelor’s degree in Education from Morningside College, a Master’s degree in Educational Administration from the University of South Dakota, a Master’s degree in Secondary Guidance Counseling from Wayne State College, and a Doctorate in Educational Administration from the University of Minnesota.

A-1

Ms. Shirley Broz. Ms. Broz was appointed to serve as Chief Financial and Legislative Affairs Officer

of the District in 2009 and has been with the District since 1996. Ms. Broz is a certified public accountant, and received a bachelor’s degree in Business Administration from Lindenwood University and a Master’s degree in Business Administration from Webster University.

Professional Staff

The District has 3,316 employees, including 118 administrative personnel, 1,590 teachers, librarians and counselors and 1,608 support staff. The average years of teaching experience for the 2009-10 school year was 12.5 years. Approximately 73% of the teaching staff have master’s degrees. Approximately 80% of the staff is tenured.

The starting teacher’s salary for the 2009-10 school year is $38,250 with an average teacher salary of $52,828.

The District has a maximum class size goal of 23 students for grades K-2, 25 students for grades 3-5, 28 students for grades 6-8 and 30 students for grades 9-12. The current average student-teacher ratio for the District is 18 to 1.

Employee Relations Teaching staff are reviewed after the first year of employment, and thereafter on an annual basis until they achieve tenure. Thereafter, tenured teachers are reviewed every third year. During the initial five years of employment, teaching staff are retained on a probationary basis. Teaching staff may join professional groups or associations. The District, pursuant to State law, conducts a meet and confer process with the representative teacher organization. The Superintendent of the District believes that employee relations are excellent.

[Remainder of Page Intentionally Left Blank.]

A-2

History of Enrollment Listed below are the District’s Fall enrollment figures for the preceding three school years and the current school year:

Grade 2006-07 2007-08 2008-09 2009-10

K 1,427 1,442 1,381 1,390 1st 1,605 1,495 1,504 1,479 2nd 1,578 1,658 1,504 1,571 3rd 1,628 1,633 1,691 1,554 4th 1,662 1,692 1,676 1,753 5th 1,641 1,724 1,696 1,698 6th 1,797 1,710 1,777 1,748 7th 1,716 1,844 1,735 1,778 8th 1,817 1,742 1,836 1,760 9th 1,984 1,958 1,944 2,048

10th 1,848 1,969 1,928 1,868 11th 1,775 1,716 1,887 1,837 12th 1,685 1,749 1,670 1,834

Total 22,163 22,332 22,229 22,318

Source: District’s reports of Fall enrollment data filed with Missouri Department of Elementary and Secondary Education and

the District. School Rating and Accreditation Missouri law requires the Department of Elementary and Secondary Education (“DESE”) to regularly evaluate each public school district. DESE has assigned the District “accredited” status, the highest accreditation status given by DESE. The process of accrediting school districts is mandated by State law, and the specific responsibilities are outlined both by rules of the State Board of Education and in Section 161.092 of the Revised Statutes of Missouri, as amended. Under DESE’s current accreditation system, school districts are evaluated every five years based on DESE standards in three areas: resource standards, educational process standards and performance standards. Districts receive an evaluation judgment for each of the three sets of standards and an overall evaluation, which evaluations are in one of three categories: “accredited,” “provisionally accredited” or “unaccredited.” As of July 2008, 513 (97.9%) of all school districts in the State were “accredited,” 7 (1.3%) were “provisionally accredited,” 1 (0.2%) was “interim” credited and 3 (0.6%) were “unaccredited” under the Missouri School Improvement Program (“MSIP”) rating system. The District’s 2009-10 MSIP review resulted in accreditation once again. Annually, DESE gives special recognition to certain school districts that have demonstrated outstanding academic performance and consistent progress in the areas that are measured by the State’s school-accreditation standards. For the 2009-2010 school year, DESE awarded the District the prestigious “Distinction in Performance Award” for the eighth consecutive year. The award is based on the same 14 academic standards used in the accreditation review process. To receive the award, a school district must meet 13 out of the 14 standards, including all of the Missouri Assessment Program based measures. The District met all 14 standards and received the “High Achievement” level of Distinction in Performance Award.

A-3

Educational Programs and Services The District is proud of the programs and services it provides and the quality of students it educates. Outlined in the following paragraphs are selected programs and activities offered by the District. Early Childhood Development The District operates a comprehensive Early Childhood Development program designed to assist parents and children from birth through five years of age. The Parents As Teachers program is a free parent education and support program for new and expecting parents in skills related to child development and parenting. The Early Childhood Special Education program provides services to preschool children who have significant development delays. The District also provides developmental screening which measures a child’s development in the areas of speech and language skills, motor skills, general knowledge, hearing and vision. The District also offers Preschool and Mini-Preschool to children three to five years of age. Accelerated Programs The Center for Creative Learning (grades K-5), Academic Stretch (grades 6-8), and the Secondary Gifted Program (grades 9-12) comprise the District’s program for academically gifted students. All students involved in this program meet criteria set forth by the District and approved by the Missouri Department of Elementary and Secondary Education. The District’s high schools offer numerous Advanced Placement and college credit courses. Special Education Programs The District is a component district of the Special School District of St. Louis County. The District’s special education for its students is supplied by the Special School District of St. Louis County. Extracurricular Activities The District has a full program of extracurricular activities for high school students. The athletic program includes fall, winter and spring sports for both boys and girls. Some interscholastic teams include both underclass and varsity level competition. An intramural program offers recreational opportunities for students interested in exercise and leisure time pursuits. Clubs and organizations ranging from athletic support groups to music, journalism, drama, yearbook and student council are also available. At the intermediate schools, students have the opportunity to participate in intramurals, student council, drama and music. The District is committed to encouraging students to take advantage of the opportunities offered by its program of extracurricular activities. Voluntary Transfer Student The District participates in a Voluntary Transfer Student program in which St. Louis City resident African-American students volunteer to transfer to the District’s schools. As of September 2010, this K-12 program represented approximately 8.6% of the District’s population. Educational Facilities

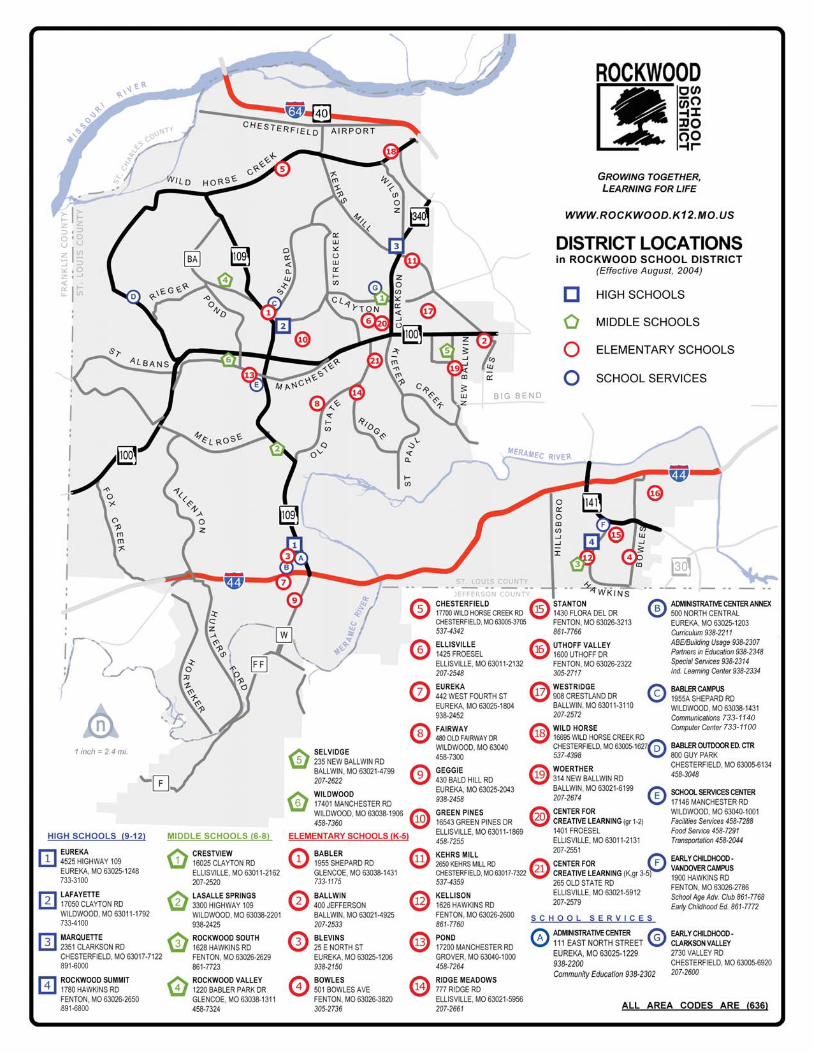

The District currently operates 33 schools, including 2 preschools, 19 elementary schools, 6 middle schools, 4 high schools, 2 Centers for Creative Learning (gifted K-5) and the Individualized Learning Center located at the District’s Administrative Center for students at risk of not graduating high school.

A-4

Information about the District’s school facilities is listed below:

Schools

Location

Grades

Approx. Enrollment

Eureka Senior High School 4525 Highway 109

Eureka, Missouri 63025 9-12 1,918

Lafayette Senior High School 17050 Clayton Road

Ballwin, Missouri 63011 9-12 2,013

Marquette Senior High School 2351 Clarkson Road

Chesterfield, Missouri 63017 9-12 2,215

Rockwood Summit Senior High School 1780 Hawkins Road

Fenton, Missouri 63026 9-12 1,301

Crestview Middle School 16025 Clayton Road

Ellisville, Missouri 63011 6-8 1,211

LaSalle Springs Middle School 3300 Highway 109

Wildwood, Missouri 63038 6-8 929

Rockwood South Middle School 1628 Hawkins Road

Fenton, Missouri 63026 6-8 1,006

Rockwood Valley Middle School 1220 Babler Park Drive

Wildwood, Missouri 63038 6-8 768

Selvidge Middle School 235 New Ballwin Road

Ballwin, Missouri 63021 6-8 691

Wildwood Middle School 17401 Manchester Road

Wildwood, Missouri 63038 6-8 764

Babler Elementary School 1955 Shepard Road

Wildwood, Missouri 63038 K-5 573

Ballwin Elementary School 400 Jefferson

Ballwin, Missouri 63021 K-5 558

Blevins Elementary School 25 E. North Street

Eureka, Missouri 63025 K-5 497

Bowles Elementary School 501 Bowles Avenue

Fenton, Missouri 63026 K-5 327

Chesterfield Elementary School 17700 Wild Horse Creek Road

Chesterfield, Missouri 63005 K-5 540

Ellisville Elementary School 1425 Froesel

Ellisville, Missouri 63011 K-5 570

A-5

Eureka Elementary School 442 W. Fourth Street Eureka, Missouri 63025

K-5 308

Fairway Elementary School 480 Old Fairway Drive Wildwood, Missouri 63040

K-5 556

Geggie Elementary School 430 Bald Hill Road

Eureka, Missouri 63025 K-5 555

Green Pines Elementary School 16543 Green Pines Drive

Ellisville, Missouri 63011 K-5 472

Kehrs Mill Elementary School 2650 Kehrs Mill Road

Chesterfield, Missouri 63017 K-5 622

Kellison Elementary School 1626 Hawkins Road

Fenton, Missouri 63026 K-5 461

Pond Elementary School 17200 Manchester Road

Wildwood, Missouri 63040 K-5 449

Ridge Meadows Elementary School 777 Ridge Road

Ellisville, Missouri 63021 K-5 503

Stanton Elementary School 1430 Flora Del Drive

Fenton, Missouri 63026 K-5 539

Uthoff Valley Elementary School 1600 Uthoff Drive

Fenton, Missouri 63026 K-5 531

Westridge Elementary School 908 Crestland

Ballwin, Missouri 63011 K-5 421

Wild Horse Elementary School 16695 Wild Horse Creek Road

Chesterfield, Missouri 63005 K-5 573

Woerther Elementary School 314 New Ballwin Road

Ballwin, Missouri 63021 K-5 565

Center for Creative Learning 1401 Froesel

Ellisville, Missouri 63011 1-2 N/A(1)

Center for Creative Learning 265 Old State Road

Ellisville, Missouri 63021 K, 3-5 N/A(1)

Early Childhood – Clarkson Valley 2730 Valley Road

Chesterfield, Missouri 63005 PK 43/193(2)

Early Childhood – Vandover Campus 1900 Hawkins Road

Fenton, Missouri 63026 PK 25/136(2)

(1) The Center for Creative Learning offers programs for academically gifted students in grades K-5 whose enrollment is counted in their respective elementary school. (2) Enrollment in full-day program/half-day program.

A-6

ECONOMIC INFORMATION CONCERNING THE DISTRICT

Commerce, Industry and Employment Major Employers. Listed below are the major employers located in the St. Louis metropolitan area and the approximate number of employees employed by each: Name Product or Service Employment 1. Boeing Integrated Defense Systems Space and Defense Production 15,500 2. SSM Health Care Health Care 11,951 3. Schnucks Markets Inc. Grocery Store 10,800 4. St. John’s Mercy Health Care Health Care 8,042 5. Special School District Education 5,789 6. Dierberg’s Markets Grocery Store 5,000 7. Edward Jones Financial Services 4,844 8. Enterprise Rent-A-Car Auto Rental and Leasing 3,500 9. Washington University Education 3,175 10. St. Louis County Government Government 4,114 Source: St. Louis Regional Chamber and Growth Association. Unemployment. The following table sets forth estimates of the unemployment rates for St. Louis County, the State of Missouri and the United States for 2002 through 2010:

Unemployment Rates

St. Louis

County ** State of Missouri

United States

4.8% 5.2% 5.8% 5.2 5.6 6.0 5.5 5.8 5.5 5.1 5.4 5.1 4.7 4.8 4.6 4.9 5.1 4.6 5.9 6.1 5.8 9.0 9.3 9.7 9.4 9.6 9.6

Source: U.S. Department of Labor, Bureau of Labor Statistics. *Figures are averages for the year

A-7

The following table represents workforce by occupation in the District, St. Louis County and the State of Missouri according to the 2000 Census:

District St. Louis County State of Missouri Occupation Number Percent Number Percent Number Percent Management, professional and related occupations 26,807 48.1% 210,366 41.6% 836,005 31.4% Service 5,677 10.2 63,158 12.5 399,052 15.0 Sales and office 16,253 29.2 148,738 29.4 714,303 26.9 Farming, fishing and forestry 83 0.1 513 0.1 17,240 0.6 Construction, extraction and maintenance 3,361 6.0 32,105 6.4 259,266 9.8 Production, transportation and material moving 3,556 6.4 50,370 10.0 432,058 16.3 Total 55,737 100.0% 505,250 100.0% 2,657,924 100.0%

Source: U.S. Bureau of the Census (2000 Census). The following table represents employees by industry in St. Louis County and the State of Missouri according to the 2000 Census

St. Louis County

State of Missouri

Industry Number Percent Number Percent Agriculture, forestry, fishing, hunting and mining 1,146 0.2% 58,415 2.2% Construction 24,817 4.9 182,858 6.9 Manufacturing 64,212 12.7 393,440 14.8 Wholesale trade 21,290 4.2 97,021 3.7 Retail trade 57,061 11.3 315,872 11.9 Transportation and warehousing and utilities 27,141 5.4 150,641 5.7 Information 19,021 3.8 80,623 3.0 Finance, insurance, real estate, and rental and leasing 45,603 9.0 177,651 6.7 Professional, scientific, management, administrative and waste management services 56,101 11.1 198,547 7.5 Educational, health and social services 109,440 21.7 541,715 20.4 Arts, entertainment, recreation, accommodation and food services 38,345 7.6 206,295 7.8 Other services (except public administration) 24,398 4.8 132,940 5.0 Public administration 16,675 3.3 121,906 4.6 Total 505,250 100.0% 2,657,924 100.0%

Source: U.S. Bureau of the Census (2000 Census).

A-8

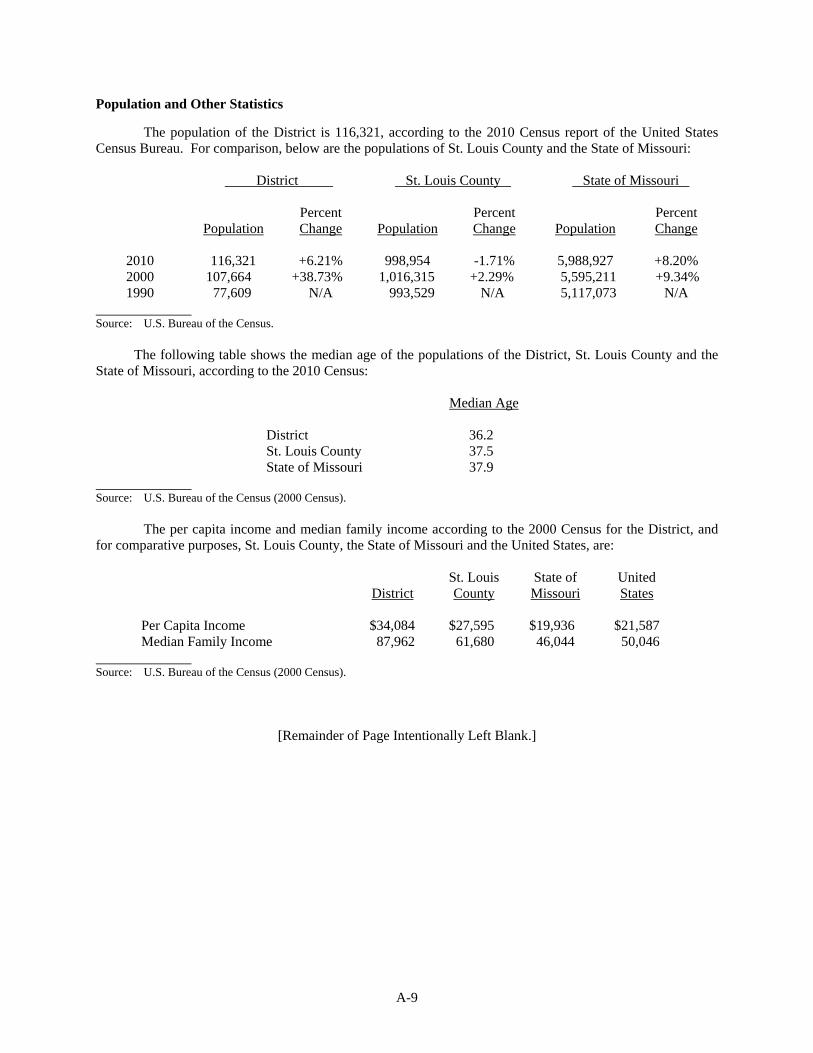

Population and Other Statistics

The population of the District is 116,321, according to the 2010 Census report of the United States Census Bureau. For comparison, below are the populations of St. Louis County and the State of Missouri:

District St. Louis County State of Missouri

Population Percent Change

Population

Percent Change

Population

Percent Change

2010 116,321 +6.21% 998,954 -1.71% 5,988,927 +8.20% 2000 107,664 +38.73% 1,016,315 +2.29% 5,595,211 +9.34% 1990 77,609 N/A 993,529 N/A 5,117,073 N/A

Source: U.S. Bureau of the Census.

The following table shows the median age of the populations of the District, St. Louis County and the

State of Missouri, according to the 2010 Census:

Median Age

District 36.2 St. Louis County 37.5 State of Missouri 37.9

Source: U.S. Bureau of the Census (2000 Census).

The per capita income and median family income according to the 2000 Census for the District, and for comparative purposes, St. Louis County, the State of Missouri and the United States, are:

District

St. Louis County

State of Missouri

United States

Per Capita Income $34,084 $27,595 $19,936 $21,587 Median Family Income 87,962 61,680 46,044 50,046

Source: U.S. Bureau of the Census (2000 Census).

[Remainder of Page Intentionally Left Blank.]

A-9

The following table represents the distribution of household income for the District, St. Louis County and the State of Missouri according to the 2000 Census:

District St. Louis County State of Missouri Income

Number

Percent

Number

Percent

Number

Percent

Under $10,000 1,040 2.8% 23,049 5.7% 221,242 10.1% $10,000 to $14,999 651 1.7 18,211 4.5 154,370 7.0 $15,000 to $24,999 1,890 5.1 43,402 10.7 319,986 14.6 $25,000 to $34,999 2,358 6.3 49,378 12.2 314,611 14.3 $35,000 to $49,999 4,091 11.0 65,737 16.2 385,315 17.5 $50,000 to $74,999 7,673 20.5 85,179 21.1 415,772 18.9 $75,000 to $99,999 6,575 17.6 48,720 12.0 193,561 8.8 $100,000 to $149,999 7,415 19.9 42,141 10.4 125,566 5.7 $150,000 or more 5,634 15.1 28,790 7.1 66,791 3.0 Total 37,327 100.0% 404,607 100.0% 2,197,214 100.0%

Source: U.S. Bureau of the Census (2000 Census).

The following table sets forth per capita personal income for St. Louis County and the State of

Missouri for 2001 through 2008, the most recent years for which figures are available:

St. Louis County

State of Missouri

Year

Per Capita Personal Income(1)

% Change

Per Capita Personal Income(1)

% Change

2001 $40,031 N/A $27,816 N/A 2002 41,760 4.32% 28,385 2.05% 2003 43,075 3.15 29,122 2.60 2004 44,888 4.21 30,283 3.99 2005 2006

46,361 48,848

3.28 5.36

31,202 32,514

3.03 4.20

2007 51,710 5.86 33,964 4.46 2008 No Data 35,228 3.72

(1) Per Capita Personal Income is the annual total Personal Income of residents divided by resident population as of July 1.

“Personal Income” is the sum of Net Earnings by place of residence, rental income of persons, personal dividend income, personal interest income, and transfer payments. “Net Earnings” is earnings by place of work — the sum of wage and salary disbursements (payrolls), other labor income, and proprietors’ income — less personal contributions for social insurance, plus an adjustment to convert earnings by place of work to a place-of-residence basis. Personal income is measured before the deduction of personal income taxes and other personal taxes and is reported in current dollars (no adjustment is made for price changes).

Source: U.S. Department of Commerce - Bureau of Economic Analysis.

A-10

Set forth below are the median (owner-occupied) house values according to the 2000 Census for the District, and for comparative purposes, St. Louis County, the State of Missouri and the United States.

Median House Value District $191,485 St. Louis County 116,600 State of Missouri 89,900 United States 119,600

Source: U.S. Bureau of the Census (2000 Census). The value of specified owner-occupied housing units of the District, St. Louis County and the State of Missouri was, according the 2000 Census, as follows: District St. Louis County State of Missouri Value

Number

Percent

Number

Percent

Number

Percent

Under $50,000 209 0.7% 20,167 7.2% 198,814 16.7% $50,000 to $99,999 3,061 10.1 97,337 34.8 491,675 41.4 $100,000 to $149,999 6,516 21.5 64,418 23.1 262,103 22.1 $150,000 to $199,999 6,336 21.0 38,491 13.8 117,791 9.9 $200,000 to $299,999 8,034 26.6 32,423 11.6 74,880 6.3 $300,000 or more 6,075 20.1 26,505 9.5 43,179 3.6 Total 30,231 100.0% 279,341 100.0% 1,188,442 100.0% Source: U.S. Census Bureau (2000 Census).

FINANCIAL INFORMATION CONCERNING THE DISTRICT Accounting, Budgeting and Auditing Procedures General. The District’s financial statements include all funds, account groups, departments, agencies, boards, commissions and other organizations over which the District is financially accountable.

Accounts are organized on the basis of funds or groups of accounts, each of which is considered to be a separate set of self-balancing accounts which comprise its assets, liabilities, fund balances, revenues, expenditures and expenses. Following are the funds and account groups used by the District:

General (Incidental) Fund – This fund is used to account for general activities of the District, including expenditures for noncertified employees, pupil transportation costs, plant operation, fringe benefits, student body activities, community services, food service and any expenditures not required or permitted to be accounted for in other funds.

Special Revenue (Teachers’) Fund – This fund is used to account for expenditures for certified employees involved in administration and instruction. It includes revenues restricted by the State and the local tax levy for the payment of teacher salaries and certain employee benefits.

Debt Service Fund – This fund is used to account for the accumulation of resources for, and the payment of, principal, interest and fiscal charges on long-term debt.

Capital Projects Fund – This fund is used to account for the proceeds of long-term debt, taxes and other revenues to be used for the acquisition or construction of major capital assets.

A-11

Basis of Accounting. Basis of accounting refers to when revenues and expenditures are recognized in the accounts and reported in the financial statements. The District’s accounting system for governmental funds reflect the modified accrual basis of accounting. At the end of the year, the governmental funds are converted from the modified accrual basis to the accrual basis for presentation in District-wide financial statements. Under the accrual basis of accounting, the current year’s revenues and expenses are recognized regardless of when cash is received or paid.

Budgets and Budgetary Accounting. The District follows these procedures in establishing the budgetary data reflected in the financial statements: 1. In accordance with Chapter 67 of the Revised Statutes of Missouri, as amended, the District

adopts a budget for each fund. 2. Prior to July, the Chief Financial Officer, who serves as the budget officer, submits to the

Board of Education a proposed budget for the fiscal year beginning on the following July 1. The proposed budget includes estimated revenues and proposed expenditures for all District funds. Budgeted expenditures cannot exceed beginning available monies plus estimated revenues for the year.

3. A public hearing is conducted to obtain taxpayer comments. Prior to its approval by the

Board of Education, the budget document is available for public inspection. 4. Prior to July 1, the budget is approved by a vote of the Board of Education. 5. Subsequent to its formal approval of the budget, the Board of Education has the authority to

make necessary adjustments to the budget by formal vote of the Board. Adjustments made during the year are reflected in the budget information included in the financial statements.

The financial records of the District are audited annually by an independent public accountant in accordance with generally accepted auditing standards. The most recent annual audit has been performed by Kerber, Eck & Braeckel LLP, Certified Public Accountants, St. Louis, Missouri. A copy of the audit for the fiscal year ended June 30, 2010, is included in this Official Statement as Appendix B. A summary of significant accounting policies of the District is contained in this Official Statement in the Notes accompanying the financial statements in Appendix B. Sources of Revenue

Missouri school districts finance their operations through the local property tax levy, State sales tax, State Aid, federal grant programs and miscellaneous sources including State Aid for Transportation, State Aid for Handicapped Students, a State sales tax on cigarettes (“fair share revenues”) and a pro rata share of interest income from the counties in which each school district operates. Debt service is financed primarily through local property taxes.

A-12

The following table shows the allocation of the District’s revenue from the various sources for the fiscal year ended June 30, 2010.

Revenue Source % of Total Local Revenue 81.56% County Revenue 1.26 State Revenue 11.93 Federal Revenue 4.95 Other Revenue 2.90

Total 100.00% Source: Comprehensive Annual Financial Report for the Fiscal Year ended June 30, 2010.

The following table shows the District’s sources of revenues for the five fiscal years shown:

Fiscal

Year Ended

June 30

Property

Taxes

Other Local

County

Revenue

State

Revenue

Federal Revenue

Other

Revenue

Total

Revenue