new brunswick public service pension plan (nbpspp)

TRANSCRIPT

1

New Brunswick Public ServicePension Plan (NBPSPP)2020

2

● This presentation is for information purposes only and norights are conferred by this presentation.

● The NBPSPP Document and Funding Policy, the NewBrunswick Pension Benefits Act, and the Income Tax Actsupersede this presentation where discrepancies may occur.

● For authoritative wording regarding this pension plan,please refer to the Plan Document for the NBPSPP.

Disclaimer

3

● Thinking about retirement?

● Mid-way through your career?

● Curious about your pension plan?

● Recently started contributing to the plan?

● Casual or part-time employee?• may be able to purchase when you become eligible to participate

Who is this Presentation for?

4

● Vestcor

● Overview of NBPSPP

● Keeping track of pension

● Provisions upon termination/death

● Factors that may impact pension benefit amount

● Employee benefits provisions upon retirement

Agenda

5

On October 1, 2016● PEBD became Vestcor Pension Services Corporation (VPSC) and NBIMC became Vestcor

Investment Management Corporation (VIMC)● Effective January 1, 2018, VPSC and VIMC became Vestcor

Vestcor is a not-for-profit organization● Administers the day-to-day operation of 11 pension plans as well as employee benefit

programs● Approximately 60,000 active and 36,000 retired members● Parts I, II, III and IV of the provincial government along with several quasi-public

organizations● As of January 1, 2019, NBPSPP membership totals 39,167:

- 18,502 actives- 16,536 retirees and survivors- 4,125 deferred members

We are the public sector’s provider of choice for integrated investment and benefit administration services.

Vestcor

6

A Board of Trustees is responsible for the administration of the NBPSPP.

The Board of Trustees administers the NBPSPP in accordance with:

The Plan Document

The Agreement and Declaration of Trust

The Funding Policy

The Statement of Investment Policy

The Income Tax Act (ITA)

The NB Pension and Benefits Act (PBA)

Governance

7

Pension ContributionsEmployer Contributions● Currently, 12.0% of eligible earnings

Employee Contributions● 7.5% of eligible earnings up to the year’s maximum pensionable

earnings (YMPE)● 10.7% of eligible earnings in excess of YMPE

% of eligible earningon salary accumulation

up to YMPE(Resets in January)

% of eligible earningon salary accumulation

in excess of YMPE(Resets in January)

Note: CPP deductions cease upon reaching the YMPE

8

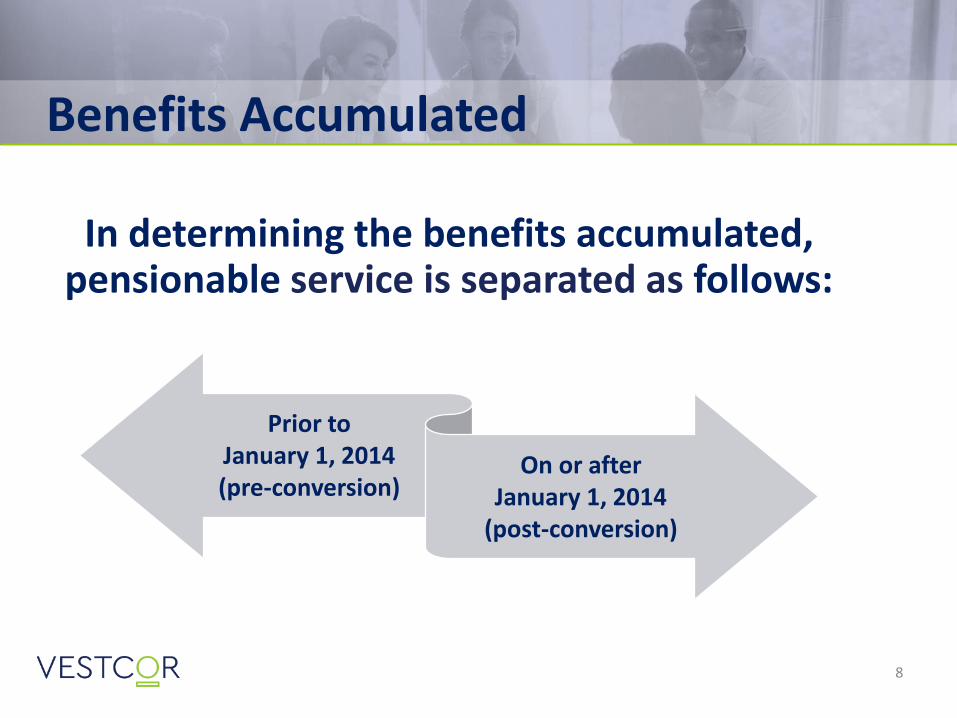

In determining the benefits accumulated, pensionable service is separated as follows:

Benefits Accumulated

Prior toJanuary 1, 2014(pre-conversion)

On or afterJanuary 1, 2014

(post-conversion)

9

Benefits Accumulated

Pensionable service prior to Jan. 1, 2014

Annual Pension Formula Before Age 65

2% XPensionable service up

to Dec. 31, 2013 X Best 5-year average salary up to Dec. 31, 2013

Annual Pension Formula After Age 65

1.3% XPensionable service up

to Dec. 31, 2013 XBest 5-year average salary up to the average Year's

Maximum Pensionable Earnings (YMPE) up toDec. 31, 2013 (3-year avg. YMPE)

P L U S

2% XPensionable service up

to Dec. 31, 2013 XBest 5-year average salary in excess of the average

YMPE at Dec. 31, 2013 (3-year avg. YMPE)

Note: Calculation prior to any early retirement factors and Cost of Living adjustment

10

Benefits Accumulated

Note: Calculation prior to any early retirement factors and Cost of Living adjustment

For each year (or part year) of service on or after Jan. 1, 2014

Annual Pension Formula Before Age 65

2% XAnnualized Pensionable

earnings for the year X % of full-time annual employment

Annual Pension Formula After Age 65

1.4% XAnnualized Pensionable

earnings up to the YMPE for the year

X % of full-time annual employment

P L U S

2% XAnnualized Pensionable

earnings in excess of the YMPE for the year

X % of full-time annual employment

11

Entitlement to pension benefits

Vesting under NBPSPP occurs upon the completion of the earlier of:

● Five years of continuous employment; or

● Two years of pensionable service in NBPSPP [including pensionable service in the Public Service Superannuation Act (PSSA)]; or

● Two years of membership in the NBPSPP, including membership in any of the following predecessor pension plans:• The Pension Plan for Part-Time and Seasonal Employees of the

Province of NB (PT&S); or• The PSSA

Vesting

Keeping track ofmy pension benefit

12

13

Employee Statement

14

Employee Statement

15

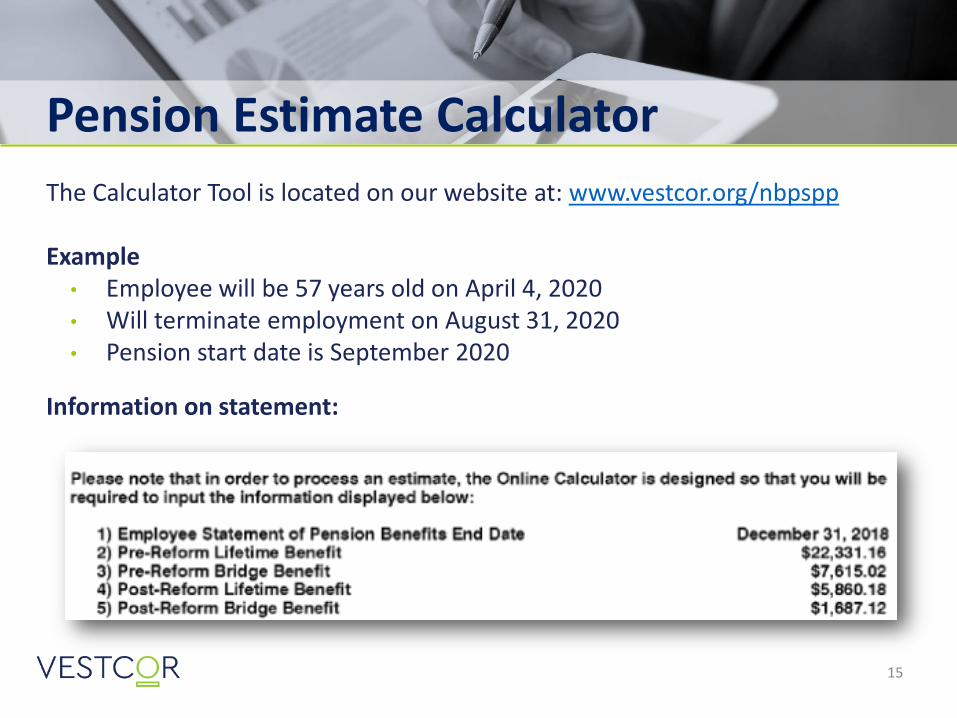

Pension Estimate Calculator

The Calculator Tool is located on our website at: www.vestcor.org/nbpspp

Example• Employee will be 57 years old on April 4, 2020• Will terminate employment on August 31, 2020• Pension start date is September 2020

Information on statement:

16

Pension Estimate Calculator

17Note: Calculation based on normal form of pension

Pension Calculator

Benefits payable upon termination or death

18

19

Termination Benefits

Not Vested Vested Prior to Age 55 Vested After Age 55

● Receives refund of contributions plus interest

● Amount is payable in cash or transferred into an RRSP

● Defer commencement of pension between age 55-65; or

● Transfer termination value into a locked in retirement account

● Begin receiving pension immediately; or

● Defer pension until any age between age 55-65 (reduced pension)

● Defer pension until age 65 (unreduced pension)

Election to transfer Termination value must be made within 90 days of the date indicated on the cover letter, otherwise

pension will be deemed deferred

20

Death Benefits

Active Not Vested Active Vested Pensioner

Refund of member’s contributions with

interest to member’s surviving spouse or

beneficiary if there is no spouse

A monthly benefit of 50% of the pension will be payable to the

spouse or to designated eligible dependent children if there is no

spouse

OR

Termination value will be paid as a lump-sum amount to the member’s

spouse – if there is no spouse, amount will be paid to designated

beneficiary or the estate

The death benefit will be paid in accordance with

the form of pension benefit the member elected at retirement

Note: The entitlement of the spouse shall supersede the entitlement of any beneficiary designation, unless the appropriate waiver form is completed and delivered to Vestcor

21

● A member may designate a beneficiary or beneficiaries to receive any benefit which may be payable to a beneficiary under the terms of the NBPSPP upon the death of the member.

● Upon the death of the member, if there is no spouse, eligible dependent or designated beneficiary, any death benefits will be payable to the member’s estate.

● If an active or deferred member designates a person other than his/her spouse as a beneficiary, the entitlement of the spouse shall supersede the entitlement of the beneficiary to a pre-retirement death benefit unless the spouse has signed a PBA Form 9.

Designated Beneficiary

22

PBA Form 9: Pre-Retirement Death Benefit Waiver

● Pension plan members now have a way to designate a beneficiary other than their spouse or common law partner to receive a pre-retirement death benefit.

● The spouse or common law partner of the plan member would need to waive his/her entitlement to the pre-retirement death benefit by completing a waiver called PBA Form 9.

● PBA Form 9 needs to be signed by the spouse and received by Vestcor before the death of the member.

Note: The waiver can be revoked by completing PBA Form 10. PBA Form 10 must be signed by both the plan member and the spouse or common law partner and received by Vestcor before the death of the member

Designated Beneficiary

Starting my pension

23

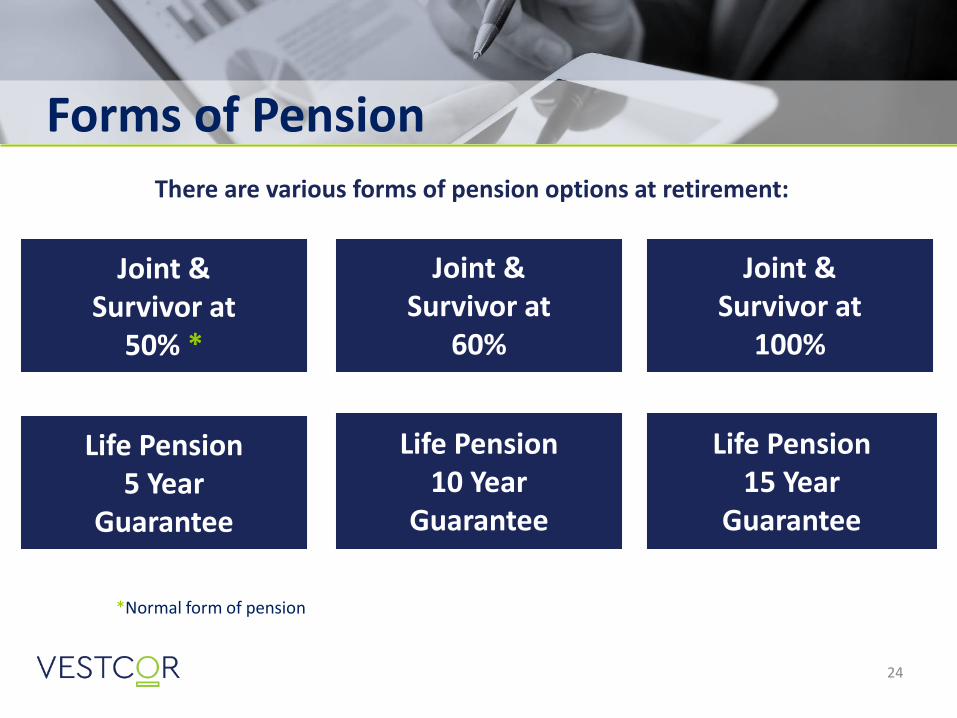

24

There are various forms of pension options at retirement:

*Normal form of pension

Forms of Pension

Life Pension15 Year

Guarantee

Joint &Survivor at

50% *

Joint &Survivor at

60%

Joint &Survivor at

100%

Life Pension10 Year

Guarantee

Life Pension5 Year

Guarantee

25

Forms of PensionJoint and Survivor at 50%

● Payments made during lifetime of retiree.

● If retiree dies before spouse, payments continue to spouse (spouse at date of death) for remainder of spouse’s life.

● 50% of pension amount at age 65 (before application of any early retirement reductions) payable to spouse, or eligible dependent if spouse dies or no spouse.

Note: If member has a spouse, a Joint and Survivor Pension Waiver form must be completed by the member’s spouse at time of retirement

26

Forms of PensionJoint and Survivor at 60% or 100%

● Payments made during lifetime of retiree.

● If retiree dies before spouse, payments continue to spouse (spouse at date of retirement) for remainder of spouse’s life.

● 60% or 100% of pension amount at age 65 (after application of any early retirement reductions) is payable to spouse.

● If no spouse or if spouse dies, 50% of pension amount at age 65 (beforeapplication of any early retirement reductions) is payable to eligible dependent.

27

Forms of PensionLife Pension Guarantee (5, 10 or 15 Years)

● Payments made during lifetime of retiree.

● If retiree dies before end of guarantee period, the Designated Beneficiary receives the remaining pension payments (pension payable at age 65, after application of any early retirement reductions) through monthly installments.

Note: If member has a spouse, a Joint and Survivor Pension Waiver form must be completed by the member’s spouse at time of retirement

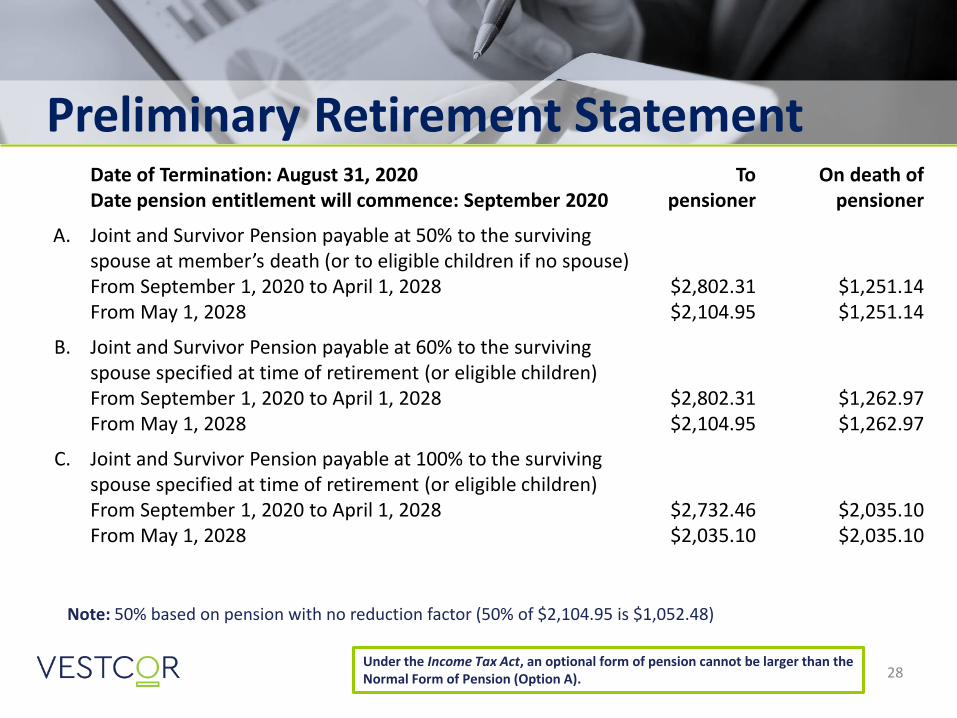

28Under the Income Tax Act, an optional form of pension cannot be larger than the Normal Form of Pension (Option A).

Preliminary Retirement StatementDate of Termination: August 31, 2020Date pension entitlement will commence: September 2020

To pensioner

On death of pensioner

A. Joint and Survivor Pension payable at 50% to the surviving spouse at member’s death (or to eligible children if no spouse)From September 1, 2020 to April 1, 2028From May 1, 2028

$2,802.31$2,104.95

$1,251.14$1,251.14

B. Joint and Survivor Pension payable at 60% to the surviving spouse specified at time of retirement (or eligible children)From September 1, 2020 to April 1, 2028From May 1, 2028

$2,802.31$2,104.95

$1,262.97$1,262.97

C. Joint and Survivor Pension payable at 100% to the surviving spouse specified at time of retirement (or eligible children)From September 1, 2020 to April 1, 2028From May 1, 2028

$2,732.46$2,035.10

$2,035.10$2,035.10

Note: 50% based on pension with no reduction factor (50% of $2,104.95 is $1,052.48)

29Under the Income Tax Act, an optional form of pension cannot be larger than the Normal Form of Pension (Option A).

Preliminary Retirement StatementDate of Termination: August 31, 2020Date pension entitlement will commence: September 2020

To pensioner

On death of pensioner

D. Life Pension with Guaranteed Period of 5 YearsFrom September 1, 2020 to April 1, 2025From September 1, 2025 to April 1, 2028From May 1, 2028

n/an/an/a

n/an/an/a

E. Life Pension with Guaranteed Period of 10 YearsFrom September 1, 2020 to April 1, 2028From May 1, 2028 to August 1, 2030From September 1, 2030

$2,802.31$2,104.95$2,104.95

$2,104.95$2,104.95

$0.00

F. Life Pension with Guaranteed Period of 15 YearsFrom September 1, 2020 to April 1, 2028From May 1, 2028 to August 1, 2035From September 1, 2035

$2,796.16$2,098.80$2,098.80

$2,098.80$2,098.80

$0.00

30

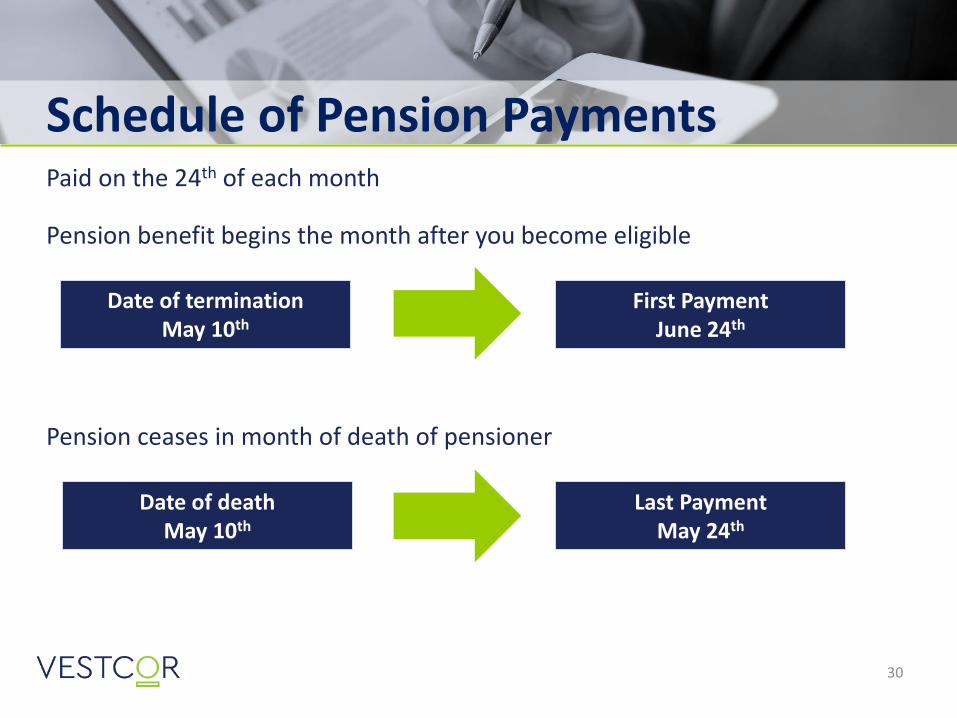

Paid on the 24th of each month

Pension benefit begins the month after you become eligible

Pension ceases in month of death of pensioner

Schedule of Pension Payments

Date of terminationMay 10th

First Payment June 24th

Date of deathMay 10th

Last PaymentMay 24th

Factors that impact my pension benefit amount

31

32

● In September of 1966, the Canada Pension Plan (CPP) was implemented, which resulted in the provincial and federal plans being integrated. As such, all provincially sponsored pension plans became integrated with the CPP.

● Integration means that both your contribution rate and the level of benefits under the NBPSPP are reduced because you are also contributing to the CPP*.

● Regardless of when you start receiving your CPP (can be taken at age 65 unreduced or as early as age 60 reduced), your NBPSPP pension benefit is only reduced by CPP integration at age 65.

* This is reflected on the pension contributions slide

Integration

33

* Benefit amounts shown are for illustration purposes only

Integration

34

* Benefit amounts shown are for illustration purposes only

Integration

35

● Each year, based on the funding level of the NBPSPP, the pension plan’s Board of Trustees will determine whether the plan is able to provide indexation – also known as Cost of Living Adjustments (COLA).

● COLA may be provided up to the average change in Consumer Price Index (CPI).

● When COLA is provided, it will apply to all NBPSPP members(i.e. active employees, retirees and deferred members).

Cost of Living Adjustments

36

55 56 57 58 59 60 61 62 63 64 65

15% 12% 9% 6% 3% 0% 0% 0% 0% 0% 0%

55 56 57 58 59 60 61 62 63 64 65

50% 45% 40% 35% 30% 25% 20% 15% 10% 5% 0%

Years of Service prior to January 1, 2014

Years of Service on or after January 1, 2014Age

Age

Reduction

Reduction

3/12% per month (3% per year)Between 55 and 60

No reduction at age 60

5/12% per month (5% per year)Between 55 and 65

No reduction at age 65

Early Retirement Reduction Factor

37

A member may be able to purchase the following periods of service (certain restrictions apply):

● Previously refunded service

● Authorized leave without pay (e.g., maternity)

● Prior Non-Contributory (part-time, casual or temporary)

● Long Term Disability Waiting Period

● MLA Service

Note: The cost to purchase service varies depending on the type of service being purchased

Purchase of Pensionable Service

38

● Reciprocal Transfer Agreement (RTA)• permits the portability of pension benefits between pension plans

● Marriage Breakdown• permits the division of pension assets

● Pre-Retirement Work Reduction Program *• reduction in hours for maximum of 5 years with full-time service

credited

*Subject to employer approval and CRA limitations

Other Provisions

Employee benefit provisions upon retirement

39

40

Health, Travel and Dental Benefits

● Transfer from Active Plan to Retiree Plan● You are eligible to transfer your current or lower coverage to the retiree

plan

*Co-payment $15.00/prescription**Must have Health to have Travel coverage

Retiree Monthly Premiums(December 2019 Rates)

Coverage Single Family

Health* $147.53 $295.06

Travel** $18.29 $36.59

Dental $31.95 $63.89

Retiree Benefits

41

Group Life Insurance Ends at retirement but employee may request information on conversion

Accidental Death and Dismemberment (AD&D)

Ends at retirement

Long Term Disability Ends at retirement or 4 months prior to age 65

Retiree Benefits

42

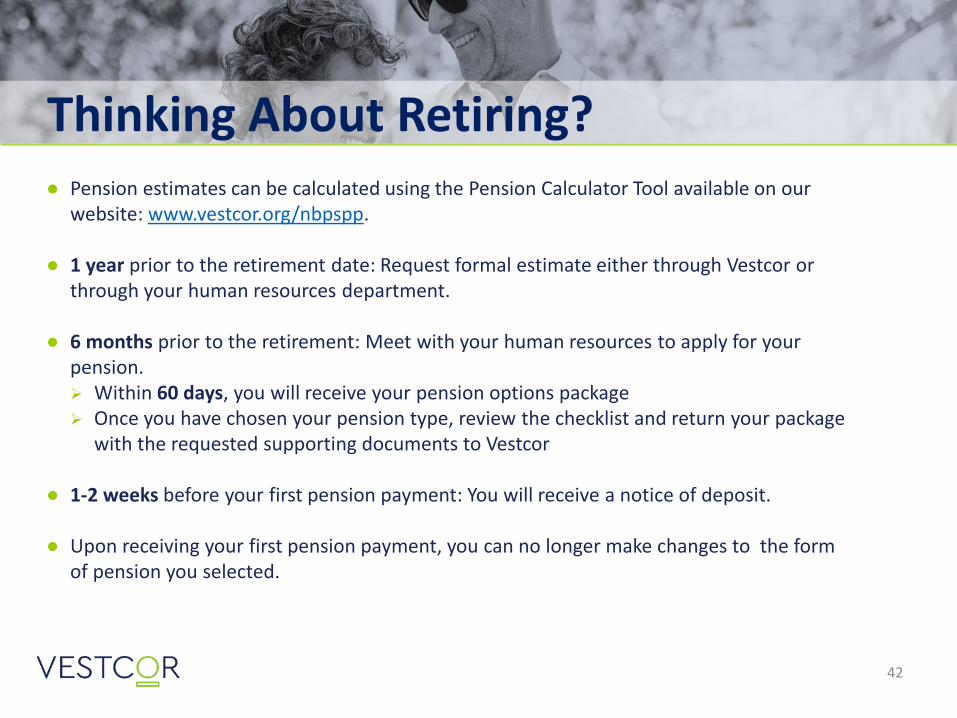

● Pension estimates can be calculated using the Pension Calculator Tool available on our website: www.vestcor.org/nbpspp.

● 1 year prior to the retirement date: Request formal estimate either through Vestcor or through your human resources department.

● 6 months prior to the retirement: Meet with your human resources to apply for your pension.➢ Within 60 days, you will receive your pension options package➢ Once you have chosen your pension type, review the checklist and return your package

with the requested supporting documents to Vestcor

● 1-2 weeks before your first pension payment: You will receive a notice of deposit.

● Upon receiving your first pension payment, you can no longer make changes to the form of pension you selected.

Thinking About Retiring?

43

Notice of Deposit

44

How to Stay Informed

Check out the NBPSPP, and many more documents and forms, on our website atwww.vestcor.org/nbpspp

A newsletter is published and distributed to all plan members twice a year

45

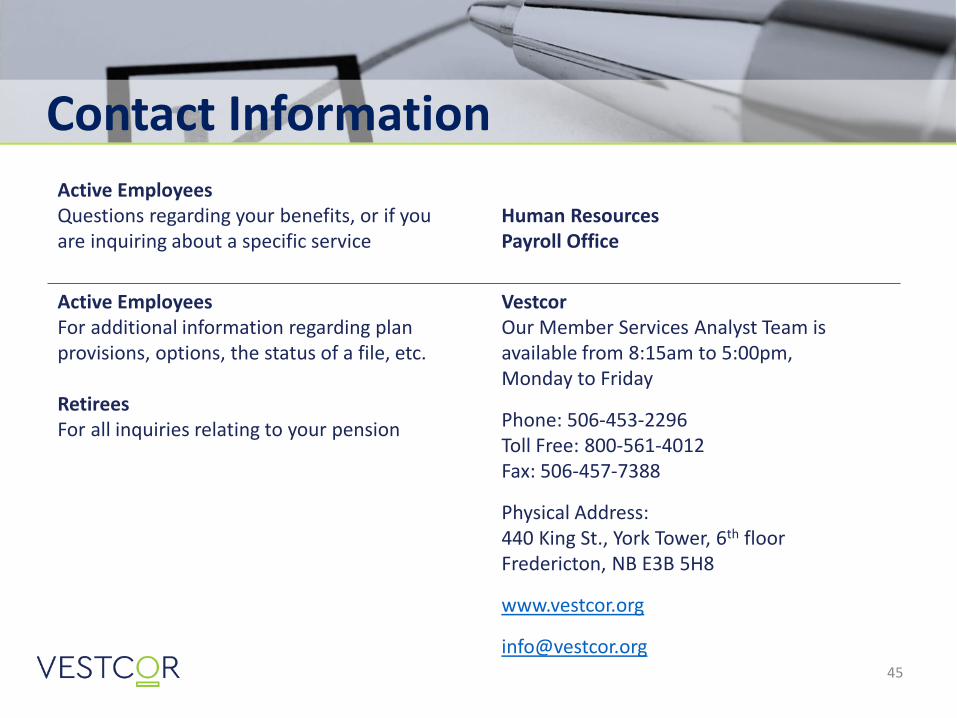

Contact Information

Active EmployeesQuestions regarding your benefits, or if youare inquiring about a specific service

Human ResourcesPayroll Office

Active EmployeesFor additional information regarding plan provisions, options, the status of a file, etc.

Retirees For all inquiries relating to your pension

VestcorOur Member Services Analyst Team is available from 8:15am to 5:00pm, Monday to Friday

Phone: 506-453-2296Toll Free: 800-561-4012Fax: 506-457-7388

Physical Address:440 King St., York Tower, 6th floorFredericton, NB E3B 5H8

www.vestcor.org

46

Canada Pension Plan and Old Age Security

Service Canada800-277-9914 (English)800-277-9915 (French)

Website: http://www.servicecanada.gc.ca

Income Tax Act

Canada Revenue Agency800-959-8281 (English)800-959-7383 (French)

Website: https://www.canada.ca/en/revenue-agency.html

Additional Information

THANK YOU! QUESTIONS?

47

Have you contacted our office in the past year?Yes – please complete the table on next page

No

Satisfaction SurveyBased on the presentation, please indicate whether you agree or

disagree with the statements listed in the table below:

Strongly Agree

Agree Neutral DisagreeStrongly Disagree

I have a better understanding of the pension plans and/or benefits following the presentation.

The presentation material was clear and easy to understand.

The presenter was knowledgeable about the subject matter and presented well.

The room and set-up were appropriate for the presentation.

I would recommend this presentation to a colleague.

In what year were you born? _________ (for demographic purposes) In what year did you join the plan? ________ (please estimate if you are unsure)

Satisfaction Survey – page 1 of 2 Section available for your comments on next page

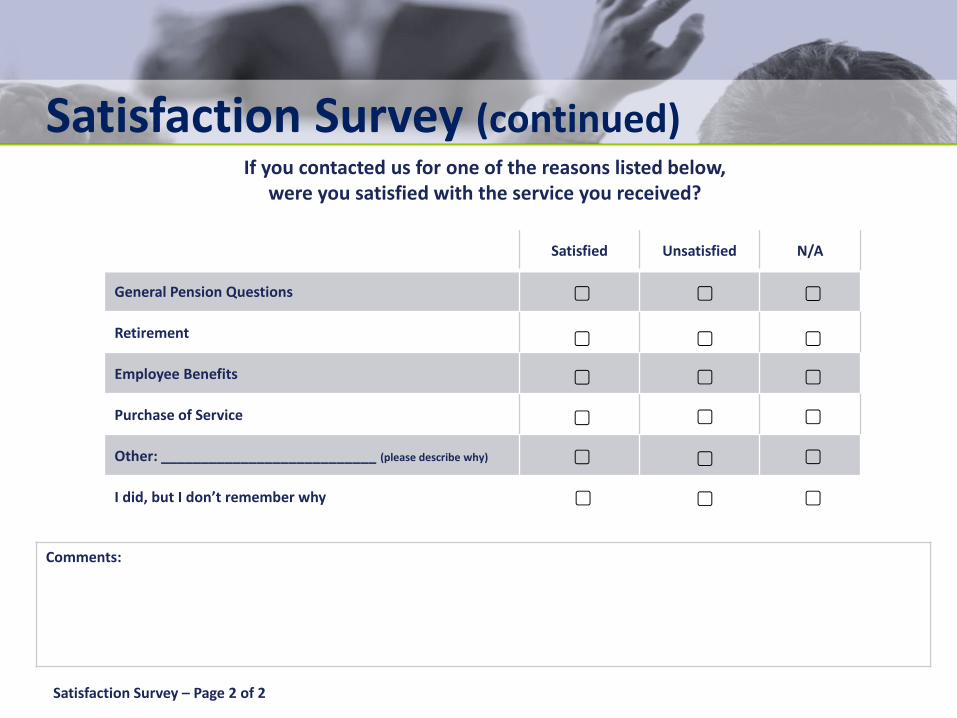

Satisfied Unsatisfied N/A

General Pension Questions

Retirement

Employee Benefits

Purchase of Service

Other: ___________________________ (please describe why)

I did, but I don’t remember why

49

Satisfaction Survey (continued)If you contacted us for one of the reasons listed below,

were you satisfied with the service you received?

Comments:

Satisfaction Survey – Page 2 of 2