nerctranslate this page of trustees governance dl...%pdf-1.6 %âãÏÓ 2875 0 obj > endobj xref...

TRANSCRIPT

116-390 Village Blvd. Princeton, NJ 08540

609.452.8060 | www.nerc.com

1

Agenda Corporate Governance and Human Resources Committee February 11, 2008 | 7:30–9 a.m. Arizona Grand Resort 8000 South Arizona Grand Parkway Phoenix, Arizona 877-800-4888

OPEN SESSION Introductions and Announcements ⎯ John Q. Anderson, Chairman Antitrust Compliance Guidelines 1. Minutes from October 22, 2007 Open and Closed Meetings (attached) — Approve 2. Calendar of CGHRC Responsibilities (attached) — Review

3. Human Resources Report (attached) — Julie Morgan

a. Cafeteria Plan

4. Committee Memberships for 2008 — Strawman Attached

5. Committee Mandates (draft mandates attached) ⎯ Review

6. Trustee Conflicts of Interest ⎯ Discussion

7. Conflict of Interest Guidelines for Trustees / Business Ethics Guidelines ⎯ (attached) ⎯ Discussion

8. 2007 Discretionary Contribution to Savings and Investment Plan (attached) ⎯

Approve

9. Board Self-Assessment (attached) — Review 10. Committee Self-Assessment (attached) — Review

11. Board Compensation

a. Formalize policy regarding laptops for trustees

116-390 Village Blvd. Princeton, NJ 08540 609.452.8060 | www.nerc.com

Agenda Item 1 CG&HR Agenda February 11, 2008

Corporate Governance and Human Resources Committee

October 22, 2007 Dallas, Texas

Draft Minutes — Open Session

Chairman John Q. Anderson called to order the duly noticed meeting of the North American Electric Reliability Corporation Corporate Governance and Human Resources Committee on October 22, 2007 at 11:25 a.m., CDT, and a quorum was declared present. The agenda and list of attendees are attached as Exhibits A and B. NERC Antitrust Compliance Guidelines Chairman Anderson directed participants’ attention to the NERC Antitrust Compliance Guidelines included in the agenda. Minutes The committee approved the draft minutes of the July 31, 2007 meeting (Exhibit C). Fourth Quarter Calendar of CGHRC Responsibilities Chairman Anderson reviewed with the committee the fourth quarter calendar of CGHRC responsibilities which included:

• Completing a self-assessment annually to determine how effectively the CGHRC is meeting its responsibilities,

• Reviewing self-assessments of other board committees to assure that they are being done on a consistent basis, and

• Monitoring the membership of the board to ensure their independence, that qualifications under any applicable laws are maintained, and that specific situations of conflict of interest are avoided, and periodically reviewing the criteria for independence set out in the bylaws and recommending changes to the board, as appropriate.

Staff will send self-assessment forms to committee members by December 1. Results will be available for the February 2008 meeting. David Cook will send conflicts of interest questionnaires to board members by December 1.

-2-

Human Resources Report Julie Morgan, manager of human resources, reported that in addition to the recruiting efforts, the human resources department is working on anti-harassment training, 360 degree reviews, and a new code of conduct policy. Ms. Morgan informed the committee she would send them a copy of their mandate for review and comments prior to the February meeting. The open session of the committee adjourned at 11:35 a.m. Submitted by,

David N. Cook Secretary

116-390 Village Blvd. Princeton, NJ 08540 609.452.8060 | www.nerc.com

Corporate Governance and Human Resources Committee

October 22, 2007 Dallas, Texas

Draft Minutes — Closed Session

Chairman John Q. Anderson called to order a duly noticed closed meeting of the Corporate Governance and Human Resources Committee at 11:35 a.m. on October 22, 2007. A copy of the meeting agenda is attached as Exhibit A. Minutes The committee approved the draft minutes of the July 31, 2007 closed session (Exhibit B). Personnel The committee discussed various personnel matters associated with NERC management team. There being no further business, Chairman Anderson terminated the meeting at 11:45 a.m. Submitted by, John Q. Anderson Chairman

Agenda Item 2 CG&HR Agenda February 11, 2008

116-390 Village Blvd. Princeton, NJ 08540

609.452.8060 | www.nerc.com

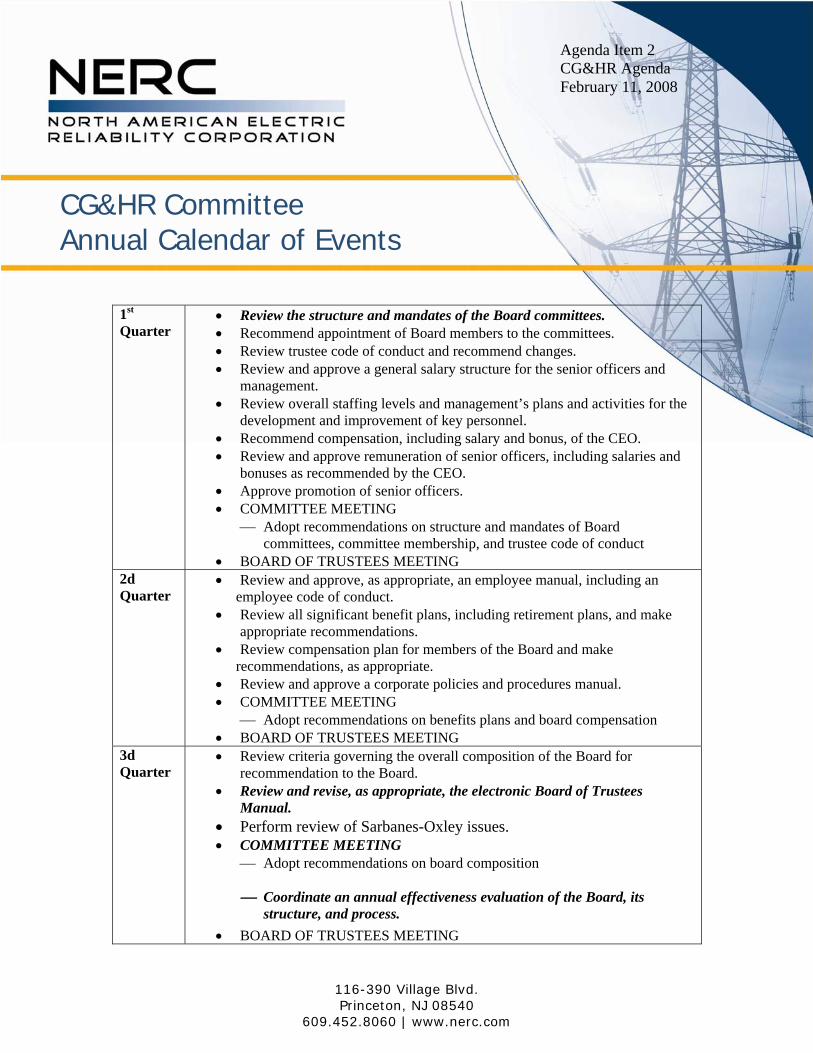

CG&HR Committee Annual Calendar of Events

1st Quarter

• Review the structure and mandates of the Board committees. • Recommend appointment of Board members to the committees. • Review trustee code of conduct and recommend changes. • Review and approve a general salary structure for the senior officers and

management. • Review overall staffing levels and management’s plans and activities for the

development and improvement of key personnel. • Recommend compensation, including salary and bonus, of the CEO. • Review and approve remuneration of senior officers, including salaries and

bonuses as recommended by the CEO. • Approve promotion of senior officers. • COMMITTEE MEETING

⎯ Adopt recommendations on structure and mandates of Board committees, committee membership, and trustee code of conduct

• BOARD OF TRUSTEES MEETING 2d Quarter

• Review and approve, as appropriate, an employee manual, including an employee code of conduct.

• Review all significant benefit plans, including retirement plans, and make appropriate recommendations.

• Review compensation plan for members of the Board and make recommendations, as appropriate.

• Review and approve a corporate policies and procedures manual. • COMMITTEE MEETING

⎯ Adopt recommendations on benefits plans and board compensation • BOARD OF TRUSTEES MEETING

3d Quarter

• Review criteria governing the overall composition of the Board for recommendation to the Board.

• Review and revise, as appropriate, the electronic Board of Trustees Manual.

• Perform review of Sarbanes-Oxley issues. • COMMITTEE MEETING

⎯ Adopt recommendations on board composition

⎯ Coordinate an annual effectiveness evaluation of the Board, its structure, and process.

• BOARD OF TRUSTEES MEETING

Corporate Governance and Human Resources Committee Revised October 14, 2004

2

4th Quarter

• Complete committee self-assessment • Review self-assessments of other Board committees to assure that they are

being done on a consistent basis. • Monitor the membership of the Board to ensure their independence, that

qualifications under any applicable laws are maintained, and that specific situations of conflict of interest are avoided.

• COMMITTEE MEETING • BOARD OF TRUSTEES MEETING

As needed

• Develop recommendations regarding Trustee succession policy. • Approve hiring of senior officers. • Review with CEO essential elements of senior management succession

planning.

Agenda Item 3 CG&HR Agenda February 11, 2008

Human Resources Report Committee Action Required Recommend Board of Trustees approval to terminate existing Cafeteria Plan (flexible spending account). Background NERC needs to adopt a new flexible spending account plan to comply with IRS regulations. To facilitate the development of the new plan, NERC recommends the committee seek Board approval to terminate the existing plan, effective immediately. NERC will propose a new plan as well as the possibility of outsourcing the plan’s administration to our health insurance provider or similar vendor in the near future. During the course of the year, NERC will review its other benefits plans and recommend any necessary changes to the committee. Staffing Updates We have filled the following positions since your last meeting: Chief Financial Officer — Bruce Walenczyk. Bruce was the CFO and Treasurer of IDT Spectrum, a start-up subsidiary of IDT Corporation, a NYSE listed international media and telecommunications company. Bruce also worked for Allegheny Energy as senior vice president and chief financial officer. Prior to Allegheny, he was vice president-finance at PSEG Energy Holdings Inc. Bruce holds an MBA in Finance from Fairleigh Dickinson University and a Bachelor of Science in Economics/Finance from St. John’s University. Canadian Affairs Representative — Ric Cameron. Ric will be a contractor rather than a full-time NERC employee. Ric has 35 years experience in the Public Service of Canada. He was the senior vice president of the Canadian International Development Agency supporting the federal and Canadian interests in international development in a variety of domestic and international fora. Ric was also the assistant deputy minister of the energy sector for Natural Resources Canada. Ric holds a Bachelor of Arts in Political Science from Carleton University, and is fluent in English and French. Manager of Regional Standards — Stephanie Monzon. Stephanie is responsible for providing oversight, guidance, and coordination of the regional standards development programs. Prior to NERC, Stephanie worked as a senior engineer for PJM Interconnection. She held several roles within system operations and the NERC and regional coordination divisions. Stephanie began her career as a consultant with Accenture in the wholesale power industry. Stephanie received her Bachelor of Science degree in Mechanical Engineering from the Cooper Union in her native New York City.

2

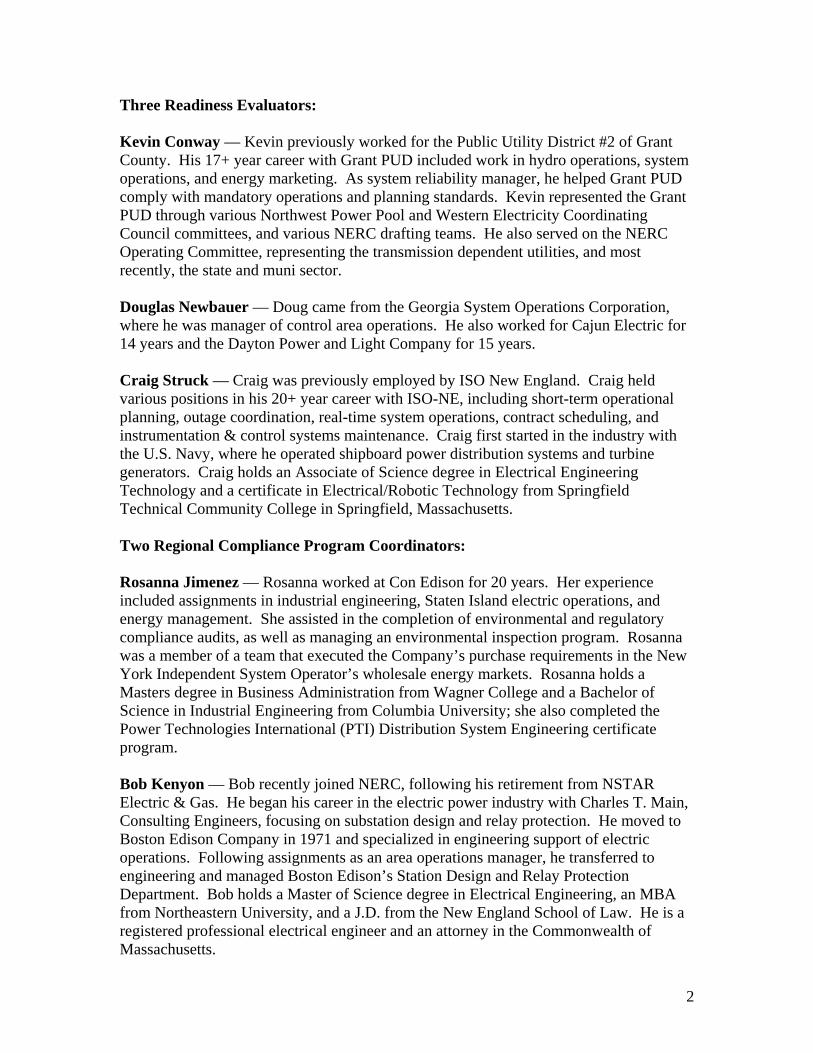

Three Readiness Evaluators: Kevin Conway — Kevin previously worked for the Public Utility District #2 of Grant County. His 17+ year career with Grant PUD included work in hydro operations, system operations, and energy marketing. As system reliability manager, he helped Grant PUD comply with mandatory operations and planning standards. Kevin represented the Grant PUD through various Northwest Power Pool and Western Electricity Coordinating Council committees, and various NERC drafting teams. He also served on the NERC Operating Committee, representing the transmission dependent utilities, and most recently, the state and muni sector. Douglas Newbauer — Doug came from the Georgia System Operations Corporation, where he was manager of control area operations. He also worked for Cajun Electric for 14 years and the Dayton Power and Light Company for 15 years. Craig Struck — Craig was previously employed by ISO New England. Craig held various positions in his 20+ year career with ISO-NE, including short-term operational planning, outage coordination, real-time system operations, contract scheduling, and instrumentation & control systems maintenance. Craig first started in the industry with the U.S. Navy, where he operated shipboard power distribution systems and turbine generators. Craig holds an Associate of Science degree in Electrical Engineering Technology and a certificate in Electrical/Robotic Technology from Springfield Technical Community College in Springfield, Massachusetts. Two Regional Compliance Program Coordinators: Rosanna Jimenez — Rosanna worked at Con Edison for 20 years. Her experience included assignments in industrial engineering, Staten Island electric operations, and energy management. She assisted in the completion of environmental and regulatory compliance audits, as well as managing an environmental inspection program. Rosanna was a member of a team that executed the Company’s purchase requirements in the New York Independent System Operator’s wholesale energy markets. Rosanna holds a Masters degree in Business Administration from Wagner College and a Bachelor of Science in Industrial Engineering from Columbia University; she also completed the Power Technologies International (PTI) Distribution System Engineering certificate program. Bob Kenyon — Bob recently joined NERC, following his retirement from NSTAR Electric & Gas. He began his career in the electric power industry with Charles T. Main, Consulting Engineers, focusing on substation design and relay protection. He moved to Boston Edison Company in 1971 and specialized in engineering support of electric operations. Following assignments as an area operations manager, he transferred to engineering and managed Boston Edison’s Station Design and Relay Protection Department. Bob holds a Master of Science degree in Electrical Engineering, an MBA from Northeastern University, and a J.D. from the New England School of Law. He is a registered professional electrical engineer and an attorney in the Commonwealth of Massachusetts.

3

Standard Development Coordinator — Darrel Richardson. Prior to joining NERC, Darrel worked for Illinois Power for 30+ years. In his last position as manager of compliance, Darrel was responsible for ensuring Illinois Power’s compliance with FERC, NERC, MAIN, and ISO policies and procedures. Among some of the other positions held were director of generation control, manager of power marketing and trading, and senior regional marketing director. Administrative Assistant — Monica Benson. Monica is the administrative assistant to the Compliance Department. Before NERC, Monica worked as an administrative assistant at ALK Technologies, Inc. Promotions: Susan Morris was recently promoted to manager of regional compliance program oversight. Susan joined NERC as a regional compliance program coordinator in January 2007. She has over 19 years experience in power system operations and planning, having worked at Tennessee Valley Authority, GridSouth, and SERC Reliability Corporation. Susan has a Bachelor of Science degree in Electrical Engineering from the University of Tennessee at Chattanooga. She currently serves on the College of Engineering and Computer Science Advisory Board, University of Tennessee at Chattanooga. Ellen Oswald was also recently promoted to manager of compliance program interfaces. Ellen joined NERC as a regional compliance program coordinator in January 2007. She was a 15-year veteran of Exelon Corporation. She held key management positions, such as delivery duty officer and director of generation dispatch, where she was responsible for strategic and real-time electric system operations. Ellen also held various positions at the ComEd control area. Ellen has a Bachelor of Science degree in Business Administration and Mechanical Engineering from Marquette University. Additional Changes: Dave Nevius is now responsible for coordinating NERC’s relationship and delegation agreements with the eight regional entities. Larry Kezele has assumed responsibility of the NERC Operating Committee. Transmission Owners & Operators Forum — The Transmission Forum hired Don Benjamin as its first full-time staff member. Don is the Forum’s vice president. Don LeKang joined the Forum staff on February 4 as director of operations. Don has been the acting director of FERC’s division of reliability and engineering services. Prior to FERC, he worked for CSA Energy Consultants. Resignations/Retirements — Cherie Broadrick, manager of regional compliance program oversight resigned, effective January 11. Cherie accepted a position with ICF Consulting in Houston. Ron Dmytrow, information technology specialist and a 28-year veteran, announced his retirement, effective at the end of February.

4

Staffing Census — The 2008 Business Plan and Budget projects NERC to grow to 101.5 employees. Management has identified three additional positions necessary to meet the goals of the ERO. The additional positions are: manager of regional standards (filled); manager of regional compliance program interfaces (filled); and manager of alerts.

STAFFING CENSUS Program Where We Are Today Projected for 2008

Standards 13 13 Readiness 9 11 Training 6 6 Forums 2 2 Compliance 18 27 Assessments 11 13 Executive 4 4 Situation Awareness 5 6 Information Technology 7 8 Inter-governmental Relations 2 2 Legal 4 4 Human Resources 3.5 3.5 Finance 4 5 88.5 104.5 Staff Development Working with the training department, human resources will create a staff development training plan and deliver four activities by year-end. The 360-degree review results triggered a request from management for executive-level training on time management and career mentoring.

1

Strawman - Board Committees 2008

Compliance CommitteePaul Barber, ChairJim GoodrichTom Berry Fred GorbetBruce Scherr

Technology CommitteeJim Goodrich, ChairPaul BarberSharon NelsonKen Peterson

Corporate Governance & Human Resources Committee

John Anderson, ChairTom Berry [Janice Case]Sharon Nelson

Nominating CommitteeJohn Q. Anderson Paul BarberTom BerryJim GoodrichFred GorbetSharon Nelson[Janice Case] (plus MRC reps)

Finance and Audit CommitteeBruce Scherr, ChairJohn Anderson Fred Gorbet[Janice Case]Ken Peterson

Dan Skaar

Agenda Item 4CG&HR AgendaFebruary 11, 2008

116-390 Village Blvd. Princeton, NJ 08540

609.452.8060 | www.nerc.com

1

Agenda Item 5 CG&HR Agenda February 11, 2008

Board of Trustees Compliance Committee Mandate Approved: XX

1. The Compliance Committee (CC) shall be composed of not less

than three and not more than six members of the Board of Trustees (board). 2. The members of the CC shall be appointed or reappointed by the board at the regular

meeting of the board immediately following each Annual Meeting of the Members Committee. Each member of the CC shall continue to be a member thereof until a successor is appointed, unless a member resigns or is removed or ceases to be a trustee of the corporation. Where a vacancy occurs at any time in the membership of the CC, it may be filled by the board.

3. The chairman of the board shall appoint a chair from among the CC members.

NERC’s director of compliance shall serve as the non-voting secretary. 4. The CC shall meet monthly by conference call or in person. Meetings may occur at

the same place in conjunction with the regular board meetings of the corporation, or as determined by the members of the CC, using the same meeting procedures established for the board.

5. The compensation of the members of the CC, including the chair of the CC, shall be

the same as established by the board for the other committees of the board. 6. The CC shall be responsible for audits of the NERC Compliance Monitoring and

Enforcement Program to meet board and governmental authority requirements on a three year basis. The audit shall evaluate the success and effectiveness of the NERC Compliance Monitoring and Enforcement Program in achieving its mission.

7. The CC shall review the violations, regardless of their status, of the most recent

month, known to the Compliance Monitoring and Enforcement Program staff as reported by regional entities, discovered by the NERC staff, or discovered from any other source.

8. The CC shall review and advise the board on the progress of individual operating

entities in mitigating confirmed violations.

Board of Trustees Compliance Committee Mandate Approved: XX

2

9. The CC shall review the progress of regional entities in processing all allegations of violations of NERC reliability standards in accordance with the NERC Rules of Procedure.

10. The CC shall serve as the appeal body for any appeals of compliance violations,

penalties, or sanctions.

11. The CC shall serve as the appeal body for any appeals of findings resulting from audits of the regional entity implementation of the NERC Compliance Monitoring Enforcement Program heard by the NERC Compliance and Certification Committee.

12. The CC shall review all Notice of Penalty or Sanction, Settlement Agreement, and

Remedial Action Directive documents and direct NERC staff to file with FERC and other governmental authorities or remand to the appropriate regional entity.

13. The CC shall hear any challenges by candidates for inclusion on the compliance

registry. 14. The CC shall be responsible for audits of the NERC Organization Registration and

Certification Program on a three year basis. The audit shall evaluate the success and effectiveness of the NERC Organization Registration and Certification Program in achieving its mission.

15. The CC shall report to the board at each regularly scheduled meeting of the board. 16. The CC shall recommend to the board such actions as may further the purposes of

the NERC Compliance Monitoring and Enforcement Program and Organization Registration and Certification Program.

17. The CC shall review this mandate annually and recommend to the board Corporate

Governance and Human Resources Committee any changes to it that the CC considers advisable.

18. The CC shall complete a self-assessment annually to determine its effectiveness. 19. The CC shall perform such other functions as may be delegated from time to time by

the board.

116-390 Village Blvd. Princeton, NJ 08540

609.452.8060 | www.nerc.com

1

Board of Trustees Compliance Committee Mandate Approved: XX

1. The Compliance Committee (CC) shall be composed of not less

than three and not more than six members of the Board of Trustees (board). 2. The members of the CC shall be appointed or reappointed by the board at the regular

meeting of the board immediately following each Annual Meeting of the Members Committee. Each member of the CC shall continue to be a member thereof until a successor is appointed, unless a member resigns or is removed or ceases to be a trustee of the corporation. Where a vacancy occurs at any time in the membership of the CC, it may be filled by the board.

3. The chairman of the board shall appoint a chair from among the CC members.

NERC’s director of compliance shall serve as the non-voting secretary. 4. The CC shall meet monthly by conference call or in person. Meetings may occur at

the same place in conjunction with the regular board meetings of the corporation, or as determined by the members of the CC, using the same meeting procedures established for the board.

5. The compensation of the members of the CC, including the chair of the CC, shall be

the same as established by the board for the other committees of the board. 6. The CC shall be responsible for audits of the NERC Compliance Monitoring and

Enforcement Program to meet board and governmental authority requirements on a three year basis. The audit shall evaluate the success and effectiveness of the NERC Compliance Monitoring and Enforcement Program in achieving its mission.

7. The CC shall review the violations, regardless of their status, of the most recent

month, known to the Compliance Monitoring and Enforcement Program staff as reported by regional entities, discovered by the NERC staff, or discovered from any other source.

Deleted: and time as

Deleted: submitted

Deleted: the regions, developed

Deleted: discovered through the Readiness Audit Program,

Board of Trustees Compliance Committee Mandate Approved: XX

2

8. The CC shall review and advise the board on the progress of individual operating entities in mitigating confirmed violations.

9. The CC shall review the progress of regional entities in processing all allegations of

violations of NERC reliability standards in accordance with the NERC Rules of Procedure.

10. The CC shall serve as the appeal body for any appeals of compliance violations,

penalties, or sanctions.

11. The CC shall serve as the appeal body for any appeals of findings resulting from audits of the regional entity implementation of the NERC Compliance Monitoring Enforcement Program heard by the NERC Compliance and Certification Committee.

12. The CC shall review all Notice of Penalty or Sanction, Settlement Agreement, and

Remedial Action Directive documents and direct NERC staff to file with FERC and other governmental authorities or remand to the appropriate regional entity.

13. The CC shall hear any challenges by candidates for inclusion on the compliance

registry. 14. The CC shall be responsible for audits of the NERC Organization Registration and

Certification Program on a three year basis. The audit shall evaluate the success and effectiveness of the NERC Organization Registration and Certification Program in achieving its mission.

15. The CC shall report to the board at each regularly scheduled meeting of the board. 16. The CC shall recommend to the board such actions as may further the purposes of

the NERC Compliance Monitoring and Enforcement Program and Organization Registration and Certification Program.

17. The CC shall review this mandate annually and recommend to the board Corporate

Governance and Human Resources Committee any changes to it that the CC considers advisable.

18. The CC shall complete a self-assessment annually to determine its effectiveness. 19. The CC shall perform such other functions as may be delegated from time to time by

the board.

Deleted: the regions and

Deleted: The CC shall review the progress of the regions in dealing with all probable violations evolving from the readiness audits and submitted to the regions

Deleted: ¶<#>The CC shall review the progress of the regions and their members in implementing all recommendations evolving from the readiness audits.¶

Deleted: Readiness Audit

Approved by Board of Trustees

116-390 Village Blvd. Princeton, NJ 08540

609.452.8060 | www.nerc.com

1

Board of Trustees Corporate Governance and Human Resources Committee Mandate Approved: XX

1. The Corporate Governance and Human Resources Committee (the “CGHRC”) shall

be composed of not less than three and not more than six trustees. 2. The members of the CGHRC shall be appointed or reappointed by the board at the

regular meeting of the board immediately following each annual meeting of the Member Representatives Committee. Each member of the CGHRC shall continue to be a member thereof until his or her successor is appointed, unless he or she shall resign or be removed or shall cease to be a trustee of the corporation. Where a vacancy occurs at any time in the membership of the CGHRC, it may be filled by the board.

3. The Board of Trustees or, in the event of the board’s failure to do so, the members

of the CGHRC, shall appoint a chair from among their members. The CGHRC shall appoint a secretary who need not be a trustee.

4. The date and place of meetings of the CGHRC and the procedure at such meetings

shall be the same as for regular Board of Trustees’ meetings of the corporation, or as determined from time to time by the members of the CGHRC, provided that:

(a) A quorum for meetings shall be a majority of the number of members of the

CGHRC. (b) The CGHRC shall meet as required and at least twice a year.

5. The compensation of members of the CGHRC and chair shall be the same as

established by the board for its other committees.

6. The CGHRC shall be responsible for:

(a) Developing criteria governing the overall composition of the board for recommendation to the board.

Approved by Board of Trustees

2

(b) Monitoring the membership of the board to ensure their independence, that qualifications under any applicable laws are maintained, and that specific situations of conflict of interest are avoided, and periodically reviewing the criteria for independence set out in the bylaws and recommending changes to the board, as appropriate.

(c) Recommending to the board the appointment of board members to each of the

committees.

(d) Coordinating an annual effectiveness evaluation of the board, its structure, and process.

(e) Reviewing annually the compensation plan for members of the board and

making recommendations to the board, as appropriate.

(f) Completing a self-assessment annually to determine how effectively the CGHRC is meeting its responsibilities.

(g) Reviewing the self-assessments of the board committees to assure that they

are being done on a consistent basis.

(h) Reviewing annually the structure of the committees, and together with the committee chairs, the mandate of each committee, and recommending changes to the board, as appropriate.

(i) Ensuring the meaningfulness and timeliness of support, information, and

documentation from management to the board.

(j) Developing a trustee code of conduct for adoption by the board and periodically reviewing the code of conduct and recommending changes, as appropriate.

(k) )Developing recommendations for the board regarding trustee succession

policy.

(l) Approving the hiring or promotion of senior officers.

(m) Regularly reviewing the performance of the chief executive officer (CEO) and providing feedback as appropriate.

(n) Recommending to the board the compensation, including salary and bonus, of

the CEO.

Approved by Board of Trustees

3

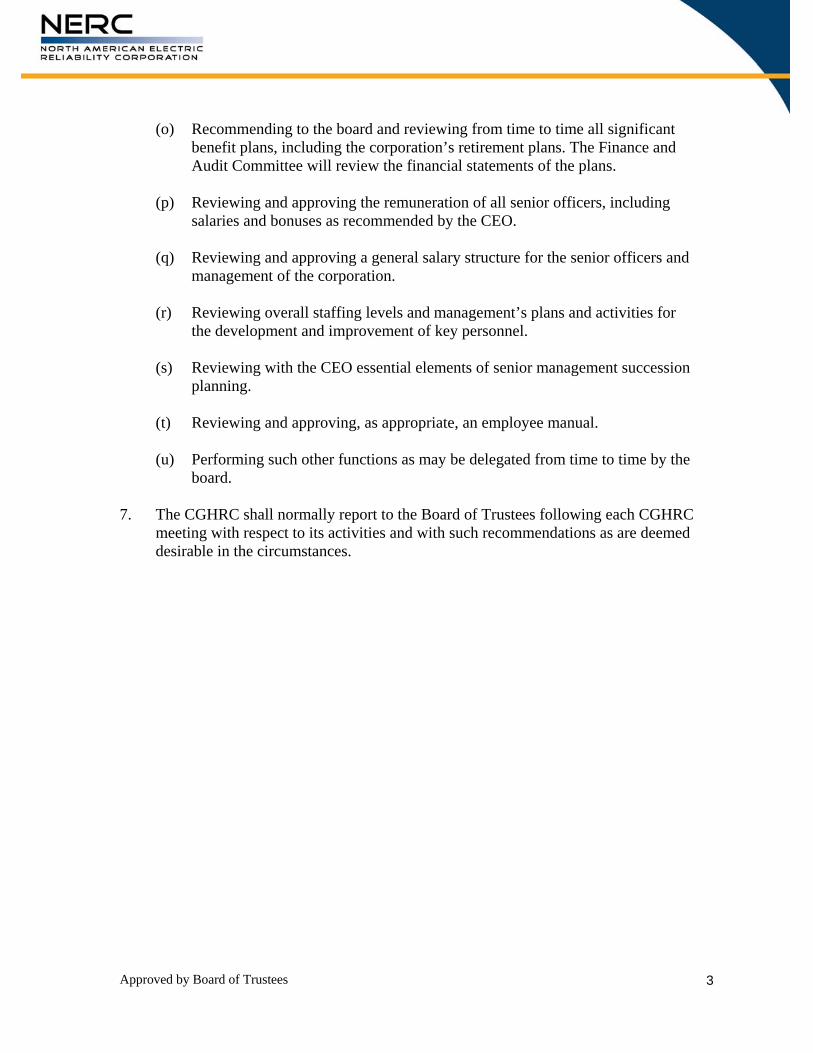

(o) Recommending to the board and reviewing from time to time all significant benefit plans, including the corporation’s retirement plans. The Finance and Audit Committee will review the financial statements of the plans.

(p) Reviewing and approving the remuneration of all senior officers, including

salaries and bonuses as recommended by the CEO.

(q) Reviewing and approving a general salary structure for the senior officers and management of the corporation.

(r) Reviewing overall staffing levels and management’s plans and activities for

the development and improvement of key personnel.

(s) Reviewing with the CEO essential elements of senior management succession planning.

(t) Reviewing and approving, as appropriate, an employee manual.

(u) Performing such other functions as may be delegated from time to time by the

board.

7. The CGHRC shall normally report to the Board of Trustees following each CGHRC meeting with respect to its activities and with such recommendations as are deemed desirable in the circumstances.

Approved by Board of Trustees

116-390 Village Blvd. Princeton, NJ 08540

609.452.8060 | www.nerc.com

1

Board of Trustees Corporate Governance and Human Resources Committee Mandate Approved: XX

1. The Corporate Governance and Human Resources Committee (the “CGHRC”) shall

be composed of not less than three and not more than six trustees. 2. The members of the CGHRC shall be appointed or reappointed by the board at the

regular meeting of the board immediately following each annual meeting of the Member Representatives Committee. Each member of the CGHRC shall continue to be a member thereof until his or her successor is appointed, unless he or she shall resign or be removed or shall cease to be a trustee of the corporation. Where a vacancy occurs at any time in the membership of the CGHRC, it may be filled by the board.

3. The Board of Trustees or, in the event of the board’s failure to do so, the members

of the CGHRC, shall appoint a chair from among their members. The CGHRC shall appoint a secretary who need not be a trustee.

4. The date and place of meetings of the CGHRC and the procedure at such meetings

shall be the same as for regular Board of Trustees’ meetings of the corporation, or as determined from time to time by the members of the CGHRC, provided that:

(a) A quorum for meetings shall be a majority of the number of members of the

CGHRC. (b) The CGHRC shall meet as required and at least twice a year.

5. The compensation of members of the CGHRC and chair shall be the same as

established by the board for its other committees.

6. The CGHRC shall be responsible for:

(a) Developing criteria governing the overall composition of the board for recommendation to the board.

Formatted: Indent: Left: -0.63"

Deleted: ¶

Deleted: Stakeholders

Approved by Board of Trustees November 1, 2006February 12, 2008

2

(a) Developing criteria governing the overall composition of the board for recommendation to the board.

(b) Monitoring the membership of the board to ensure their independence, that

qualifications under any applicable laws are maintained, and that specific situations of conflict of interest are avoided, and periodically reviewing the criteria for independence set out in the bylaws and recommending changes to the board, as appropriate.

(c) Recommending to the board the appointment of board members to each of the

committees.

(d) Coordinating an annual effectiveness evaluation of the board, its structure, and process.

(e) Reviewing annually the compensation plan for members of the board and

making recommendations to the board, as appropriate.

(f) Completing a self-assessment annually to determine how effectively the CGHRC is meeting its responsibilities.

(g) Reviewing the self-assessments of the board committees to assure that they

are being done on a consistent basis.

(h) Reviewing annually the structure of the committees, and together with the committee chairs, the mandate of each committee, and recommending changes to the board, as appropriate.

(i) Ensuring the meaningfulness and timeliness of support, information, and

documentation from management to the board.

(j) Developing a trustee code of conduct for adoption by the board and periodically reviewing the code of conduct and recommending changes, as appropriate.

(k) Reviewing and revising, as appropriate, the electronic Board of Trustees

Manual. (l) Developing recommendations for the board regarding trustee succession

policy.

(m) Reviewing and approving a corporate policies and procedures manual.

(n) Approving the hiring or promotion of senior officers.

Approved by Board of Trustees November 1, 2006February 12, 2008

3

(o) Regularly reviewing the performance of the chief executive officer (CEO) and providing feedback as appropriate.

(p) Recommending to the board the compensation, including salary and bonus, of

the CEO.

(q) Recommending to the board and reviewing from time to time all significant benefit plans, including the corporation’s retirement plans. The Finance and Audit Committee will review the financial statements of the plans.

(r) Reviewing and approving the remuneration of all senior officers, including

salaries and bonuses as recommended by the CEO.

(s) Reviewing and approving a general salary structure for the senior officers and management of the corporation.

(t) Reviewing overall staffing levels and management’s plans and activities for

the development and improvement of key personnel.

(u) Reviewing with the CEO essential elements of senior management succession planning.

(v) Reviewing and approving, as appropriate, an employee manual, including an

employee code of conduct.

(w) Performing such other functions as may be delegated from time to time by the board.

7. The CGHRC shall normally report to the Board of Trustees following each CGHRC

meeting with respect to its activities and with such recommendations as are deemed desirable in the circumstances.

116-390 Village Boulevard, Princeton, New Jersey 08540-5721

Phone: 609.452.8060 ▪ Fax: 609.452.9550 ▪ www.nerc.com

Board of Trustees Finance and Audit Committee Mandate Approved: XX

1. The Finance and Audit Committee (FAC) shall be composed of not less than three and not

more than six trustees. 2. The members of the FAC shall be appointed or reappointed by the board at the regular

meeting of the board immediately following each annual meeting of the Member Representatives Committee. Each member of the FAC shall continue to be a member thereof until his/her successor is appointed, unless he/she shall resign or be removed or shall cease to be a trustee of the corporation. Where a vacancy occurs at any time in the membership of the FAC, it may be filled by the Board of Trustees. The president of the corporation shall not be eligible for appointment to the FAC.

3. The Board of Trustees or, in the event of their failure to do so, the members of the FAC, shall

appoint a chair from among their members. The FAC shall also appoint a secretary who need not be a trustee.

4. The place of meetings of the FAC and the procedures at such meetings shall be the same as

for regular board meetings of the corporation, or as determined by the members of the FAC, provided that:

(a) A quorum for meetings shall be a majority of the number of members of the FAC.

(b) The FAC shall meet as required and at least twice a year. 5. The compensation of the members of the FAC and chair shall be the same as established by

the board for its other committees. 6. The objectives of the FAC are as follows:

(a) To assist the board in the discharge of its responsibility to monitor the component parts of the audit process and the integrity of the corporation’s financial reporting.

(b) To receive reports from the external auditor and to provide independent communication between the board and the external auditor.

(c) To monitor the independence of the external auditor and to ensure that the external auditor remains ultimately accountable to the board and the FAC.

Finance and Audit Committee Mandate 2 Approved by Board of Trustees: XX

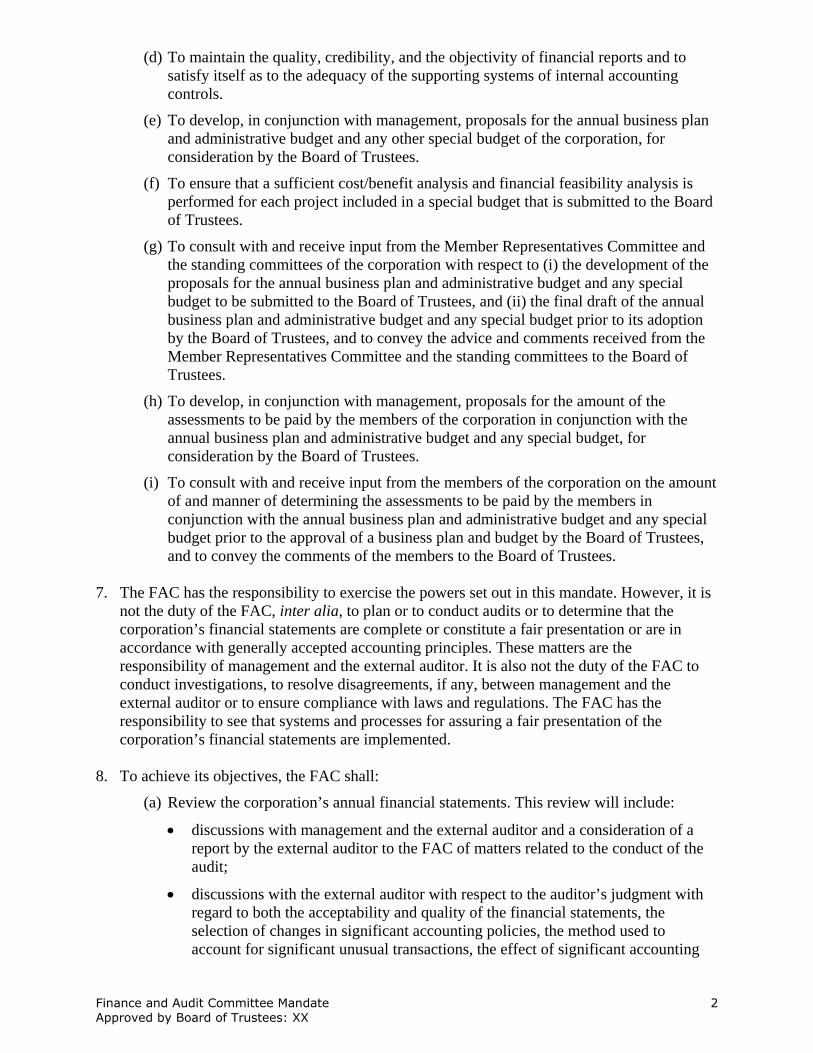

(d) To maintain the quality, credibility, and the objectivity of financial reports and to satisfy itself as to the adequacy of the supporting systems of internal accounting controls.

(e) To develop, in conjunction with management, proposals for the annual business plan and administrative budget and any other special budget of the corporation, for consideration by the Board of Trustees.

(f) To ensure that a sufficient cost/benefit analysis and financial feasibility analysis is performed for each project included in a special budget that is submitted to the Board of Trustees.

(g) To consult with and receive input from the Member Representatives Committee and the standing committees of the corporation with respect to (i) the development of the proposals for the annual business plan and administrative budget and any special budget to be submitted to the Board of Trustees, and (ii) the final draft of the annual business plan and administrative budget and any special budget prior to its adoption by the Board of Trustees, and to convey the advice and comments received from the Member Representatives Committee and the standing committees to the Board of Trustees.

(h) To develop, in conjunction with management, proposals for the amount of the assessments to be paid by the members of the corporation in conjunction with the annual business plan and administrative budget and any special budget, for consideration by the Board of Trustees.

(i) To consult with and receive input from the members of the corporation on the amount of and manner of determining the assessments to be paid by the members in conjunction with the annual business plan and administrative budget and any special budget prior to the approval of a business plan and budget by the Board of Trustees, and to convey the comments of the members to the Board of Trustees.

7. The FAC has the responsibility to exercise the powers set out in this mandate. However, it is

not the duty of the FAC, inter alia, to plan or to conduct audits or to determine that the corporation’s financial statements are complete or constitute a fair presentation or are in accordance with generally accepted accounting principles. These matters are the responsibility of management and the external auditor. It is also not the duty of the FAC to conduct investigations, to resolve disagreements, if any, between management and the external auditor or to ensure compliance with laws and regulations. The FAC has the responsibility to see that systems and processes for assuring a fair presentation of the corporation’s financial statements are implemented.

8. To achieve its objectives, the FAC shall:

(a) Review the corporation’s annual financial statements. This review will include:

• discussions with management and the external auditor and a consideration of a report by the external auditor to the FAC of matters related to the conduct of the audit;

• discussions with the external auditor with respect to the auditor’s judgment with regard to both the acceptability and quality of the financial statements, the selection of changes in significant accounting policies, the method used to account for significant unusual transactions, the effect of significant accounting

Finance and Audit Committee Mandate 3 Approved by Board of Trustees: XX

policies in controversial or emerging areas, the degree of aggressiveness or conservation, as the case may be, of the accounting policies adopted by the corporation, the process used by management in formulating particularly significant accounting estimates, and the basis for the external auditor’s conclusions regarding the reasonableness of those estimates;

• a review of significant adjustments arising from the audit;

• a review of disagreements with management over the application of accounting policies and the disclosures in the financial statements;

• a review of the external auditor’s suggestions for improvements to the corporation’s operations and internal controls;

• compliance with various covenants; and

• the selection of and changes in accounting policies and consideration of the appropriateness of such selections and changes.

(b) Determine, based on its review and discussion, whether to recommend the acceptance by the board of such audited financial statements.

(c) Review with management, the external auditor and legal counsel, the corporation’s procedures to ensure compliance with applicable laws and regulations, and any significant litigation, claim, or other contingency, including tax assessments, that would have a material effect upon the financial position or operating results of the corporation and the disclosure or impact on the results of these matters in the annual financial statements.

(d) Review and approve estimated and actual audit fees and expenses for the current years.

(e) At least once each year:

• Meet privately with management to assess the performance of the external auditor.

• Meet privately with the external auditor, amongst other things, to inquire about time pressures on the external auditor, to understand any restrictions placed on them or other difficulties encountered in the course of the audit, including restrictions on the scope of their work and access to requested information and the level of cooperation received from management during the performance of their work and their evaluation of the corporation’s financial, accounting, and personnel systems.

(f) Evaluate the performance of the external auditor, and if so determined, recommend that the board propose to the members of the corporation reappointment of the external auditor or steps to replace the external auditor.

(g) Obtain from the corporation’s external auditor the major audit findings and internal control recommendations reported during the period under review, the response of management to those recommendations, and review the follow-up performed by management in order to monitor whether management has implemented an effective system of internal accounting control.

(h) Annually obtain a report of management assessing the corporation’s internal controls.

Finance and Audit Committee Mandate 4 Approved by Board of Trustees: XX

(i) Review significant emerging accounting and reporting issues, including recent professional and regulatory pronouncements, and assess their impact on the corporation’s financial statements.

(j) Review policies for approval of senior management expenses, including those of the chief executive officer.

(k) Review with management the corporation’s computer systems, including procedures to keep the systems secure and contingency plans developed to deal with possible computer failures.

(l) Whenever it may be appropriate to do so, to retain and receive advice from experts, including independent legal counsel and independent public accountants, and to conduct or authorize the conduct of investigations into any matters within the scope of the responsibility of the FAC as the FAC may consider appropriate.

(m) Develop, in conjunction with management, a schedule for the preparation and development of the annual business plan and administrative budget and each special budget that provides sufficient time for preliminary development by management, review by the FAC, consideration and submission of input by the Member Representatives Committee and the standing committees of the corporation, consideration of the proposed business plan and budget by the Board of Trustees, review and submission of comments by the Member Representatives Committee and the standing committees on the final draft of a proposed business plan and budget prior to its final approval by the Board of Trustees, and final approval of the annual business plan and budget or special budget by the Board of Trustees, in accordance with the overall business plan and budget cycle established by the Board of Trustees.

(n) Review the financial statements of NERC’s retirement and related plans and report, as appropriate, to the Corporate Governance and Human Resources Committee.

(o) Develop, in conjunction with management, a schedule for the development of proposed assessments to be paid by the members of the corporation in conjunction with the annual business plan and budget and each special budget that provides sufficient time for preliminary development by management, review by the FAC, consideration and submission of input by the members of the corporation, consideration of the proposed assessments by the Board of Trustees, review and submission of comments by the members on the final draft of the proposed assessments prior to final approval by the Board of Trustees, and final approval of the assessments by the Board of Trustees, in accordance with the overall business plan and budget cycle established by the Board of Trustees.

(p) Develop, in conjunction with management, a system of reporting to the FAC and to the Board of Trustees that provides for the tracking of actual expenditures against the amounts approved in the annual administrative budget and each special budget.

(q) Report regularly to the board on the activities, findings, and conclusions of the FAC.

(r) Review this mandate on an annual basis and recommend to the board Corporate Governance and Human Resources Committee any changes to it that the FAC considers advisable.

(s) Complete a self-assessment annually to determine how effectively the FAC is meeting its responsibilities.

(t) Perform such other functions as may be delegated from time to time by the board.

116-390 Village Boulevard, Princeton, New Jersey 08540-5721

Phone: 609.452.8060 ▪ Fax: 609.452.9550 ▪ www.nerc.com

Mandate of the Finance and Audit Committee

1. The Finance and Audit Committee (FAC) shall be composed of not less than three and not more than six trustees.

2. The members of the FAC shall be appointed or reappointed by the board at the regular meeting of the board immediately following each annual meeting of the StakeholdersMember Representatives Committee. Each member of the FAC shall continue to be a member thereof until his/her successor is appointed, unless he/she shall resign or be removed or shall cease to be a trustee of the corporation. Where a vacancy occurs at any time in the membership of the FAC, it may be filled by the Board of Trustees. The president of the corporation shall not be eligible for appointment to the FAC.

3. The Board of Trustees or, in the event of their failure to do so, the members of the FAC, shall appoint a chair from among their members. The FAC shall also appoint a secretary who need not be a trustee.

4. The place of meetings of the FAC and the procedures at such meetings shall be the same as for regular board meetings of the corporation, or as determined by the members of the FAC, provided that:

(a) A quorum for meetings shall be a majority of the number of members of the FAC.

(b) The FAC shall meet as required and at least twice a year.

5. The compensation of the members of the FAC and chair shall be the same as established by the board for its other committees.

6. The objectives of the FAC are as follows:

(a) To assist the board in the discharge of its responsibility to monitor the component parts of the audit process and the integrity of the corporation’s financial reporting.

(b) To receive reports from the external auditor and to provide independent communication between the board and the external auditor.

(c) To monitor the independence of the external auditor and to ensure that the external

auditor remains ultimately accountable to the board and the FAC.

(d) To maintain the quality, credibility, and the objectivity of financial reports and to satisfy itself as to the adequacy of the supporting systems of internal accounting controls.

Finance and Audit Committee Mandate 2 Approved by Board of Trustees: February 7, 2005

(e) To develop, in conjunction with management, proposals for the annual business plan and administrative budget and any other special budget of the corporation, for consideration by the Board of Trustees.

(f) To ensure that a sufficient cost/benefit analysis and financial feasibility analysis is performed for each project included in a special budget that is submitted to the Board of Trustees.

(g) To consult with and receive input from the StakeholdersMember Representatives Committee and the standing committees of the corporation with respect to (i) the development of the proposals for the annual business plan and administrative budget and any special budget to be submitted to the Board of Trustees, and (ii) the final draft of the annual business plan and administrative budget and any special budget prior to its adoption by the Board of Trustees, and to convey the advice and comments received from the StakeholdersMember Representatives Committee and the standing committees to the Board of Trustees.

(h) To develop, in conjunction with management, proposals for the amount of the assessments to be paid by the members of the corporation in conjunction with the annual business plan and administrative budget and any special budget, for consideration by the Board of Trustees.

(i) To consult with and receive input from the members of the corporation on the amount of and manner of determining the assessments to be paid by the members in conjunction with the annual business plan and administrative budget and any special budget prior to the approval of a business plan and budget by the Board of Trustees, and to convey the comments of the members to the Board of Trustees.

7. The FAC has the responsibility to exercise the powers set out in this mandate. However, it is not the duty of the FAC, inter alia, to plan or to conduct audits or to determine that the corporation’s financial statements are complete or constitute a fair presentation or are in accordance with generally accepted accounting principles. These matters are the responsibility of management and the external auditor. It is also not the duty of the FAC to conduct investigations, to resolve disagreements, if any, between management and the external auditor or to ensure compliance with laws and regulations. The FAC has the responsibility to see that systems and processes for assuring a fair presentation of the corporation’s financial statements are implemented.

8. To achieve its objectives, the FAC shall:

(a) Review the corporation’s annual financial statements. This review will include:

• discussions with management and the external auditor and a consideration of a report by the external auditor to the FAC of matters related to the conduct of the audit;

• discussions with the external auditor with respect to the auditor’s judgment with regard to both the acceptability and quality of the financial statements, the selection of changes in significant accounting policies, the method used to account for significant unusual transactions, the effect of significant accounting policies in controversial or emerging areas, the degree of aggressiveness or conservation, as the case may be, of the accounting policies adopted by the corporation, the process used by management in formulating particularly significant accounting estimates, and the

Finance and Audit Committee Mandate 3 Approved by Board of Trustees: February 7, 2005

basis for the external auditor’s conclusions regarding the reasonableness of those estimates;

• a review of significant adjustments arising from the audit;

• a review of disagreements with management over the application of accounting policies and the disclosures in the financial statements;

• a review of the external auditor’s suggestions for improvements to the corporation’s operations and internal controls;

• compliance with various covenants; and

• the selection of and changes in accounting policies and consideration of the appropriateness of such selections and changes.

(b) Determine, based on its review and discussion, whether to recommend the acceptance by the board of such audited financial statements.

(c) Review with management, the external auditor and legal counsel, the corporation’s procedures to ensure compliance with applicable laws and regulations, and any significant litigation, claim, or other contingency, including tax assessments, that would have a material effect upon the financial position or operating results of the corporation and the disclosure or impact on the results of these matters in the annual financial statements.

(d) Review and approve estimated and actual audit fees and expenses for the current years.

(e) At least once each year:

• Meet privately with management to assess the performance of the external auditor.

• Meet privately with the external auditor, amongst other things, to inquire about time pressures on the external auditor, to understand any restrictions placed on them or other difficulties encountered in the course of the audit, including restrictions on the scope of their work and access to requested information and the level of cooperation received from management during the performance of their work and their evaluation of the corporation’s financial, accounting, and personnel systems.

(f) Evaluate the performance of the external auditor, and if so determined, recommend that the board propose to the members of the corporation reappointment of the external auditor or steps to replace the external auditor.

(g) Obtain from the corporation’s external auditor the major audit findings and internal control recommendations reported during the period under review, the response of management to those recommendations, and review the follow-up performed by management in order to monitor whether management has implemented an effective system of internal accounting control.

(h) Annually obtain a report of management assessing the corporation’s internal controls.

(i) Review significant emerging accounting and reporting issues, including recent professional and regulatory pronouncements, and assess their impact on the corporation’s financial statements.

Finance and Audit Committee Mandate 4 Approved by Board of Trustees: February 7, 2005

(j) Review policies for approval of senior management expenses, including those of the chief executive officer.

(k) Review with management the corporation’s computer systems, including procedures to keep the systems secure and contingency plans developed to deal with possible computer failures.

(l) Whenever it may be appropriate to do so, to retain and receive advice from experts, including independent legal counsel and independent public accountants, and to conduct or authorize the conduct of investigations into any matters within the scope of the responsibility of the FAC as the FAC may consider appropriate.

(m) Develop, in conjunction with management, a schedule for the preparation and development of the annual business plan and administrative budget and each special budget that provides sufficient time for preliminary development by management, review by the FAC, consideration and submission of input by the StakeholdersMember Representatives Committee and the standing committees of the corporation, consideration of the proposed business plan and budget by the Board of Trustees, review and submission of comments by the StakeholdersMember Representatives Committee and the standing committees on the final draft of a proposed business plan and budget prior to its final approval by the Board of Trustees, and final approval of the annual business plan and budget or special budget by the Board of Trustees, in accordance with the overall business plan and budget cycle established by the Board of Trustees.

(n) Review the financial statements of NERC’s retirement and related plans and report, as appropriate, to the Corporate Governance and Human Resources Committee.

(o) Develop, in conjunction with management, a schedule for the development of proposed assessments to be paid by the members of the corporation in conjunction with the annual business plan and budget and each special budget that provides sufficient time for preliminary development by management, review by the FAC, consideration and submission of input by the members of the corporation, consideration of the proposed assessments by the Board of Trustees, review and submission of comments by the members on the final draft of the proposed assessments prior to final approval by the Board of Trustees, and final approval of the assessments by the Board of Trustees, in accordance with the overall business plan and budget cycle established by the Board of Trustees.

(p) Develop, in conjunction with management, a system of reporting to the FAC and to the Board of Trustees that provides for the tracking of actual expenditures against the amounts approved in the annual administrative budget and each special budget.

(q) Report regularly to the board on the activities, findings, and conclusions of the FAC.

(r) Review this mandate on an annual basis and recommend to the board Corporate Governance and Human Resources Committee any changes to it that the FAC considers advisable.

(s) Complete a self-assessment annually to determine how effectively the FAC is meeting its responsibilities.

(t) Perform such other functions as may be delegated from time to time by the board.

116-390 Village Blvd. Princeton, NJ 08540

609.452.8060 | www.nerc.com

Board of Trustees Nominating Committee Mandate Approved: XX

1. The Nominating Committee (the “NC”) shall be composed of those trustees whose terms do not expire in the coming year and at least three representatives of the Member Representatives Committee.

2. The trustee members of the NC shall be appointed or reappointed by the board at

the regular meeting of the board immediately following each annual meeting of the Member Representatives Committee. Each trustee member of the NC shall continue to be a member thereof until his or her successor is appointed, unless he or she shall resign or be removed or shall cease to be a trustee of the corporation.

3. The Member Representatives Committee representatives shall be appointed by the

chairman of the Member Representatives Committee following the annual meeting of the Member Representatives Committee. Each stakeholder representative of the NC shall continue to be a member thereof until his or her successor is appointed, unless he or she shall resign or be removed. Where a vacancy occurs at any time in the stakeholder representatives, it may be filled by the chairman of the Member Representatives Committee.

4. The Board of Trustees or, in the event of the board’s failure to do so, the members

of the NC, shall appoint a chair from among the trustee members. The NC shall appoint a secretary who need not be a trustee.

5. The date and place of meetings of the NC and the procedure at such meetings

shall be the same as for regular Board of Trustees’ meetings of the corporation, or as determined from time to time by the members of the NC, provided that:

(a) A quorum for meetings shall be a majority of the number of members

of the NC.

(b) The NC shall meet as required and at least twice a year.

6. The compensation of trustee members of the NC and chair shall be the same as established by the board for its other committees.

Approved by Board of Trustees June 10, 2003

2

7. The NC shall be responsible for:

(a) Recommending to the Member Representatives Committee candidates for election as trustees.

(b) Implementing the board composition provisions of the bylaws and the

board’s conflict of interest policy and trustee succession policy in making its recommendations.

(c) Completing a self-assessment annually to determine how effectively

the NC is meeting its responsibilities.

(d) Performing such other functions as may be delegated from time to time by the board.

116-390 Village Blvd. Princeton, NJ 08540

609.452.8060 | www.nerc.com

Nominating Committee Mandate

1. The Nominating Committee (the “NC”) shall be composed of those trustees whose terms do not expire in the coming year and at least three representatives of the Member Representatives Committee.

2. The trustee members of the NC shall be appointed or reappointed by the board at

the regular meeting of the board immediately following each annual meeting of the Member Representatives Committee. Each trustee member of the NC shall continue to be a member thereof until his or her successor is appointed, unless he or she shall resign or be removed or shall cease to be a trustee of the corporation.

3. The Member Representatives Committee representatives shall be appointed by the

chairman of the Member Representatives Committee following the annual meeting of the Member Representatives Committee. Each stakeholder representative of the NC shall continue to be a member thereof until his or her successor is appointed, unless he or she shall resign or be removed. Where a vacancy occurs at any time in the stakeholder representatives, it may be filled by the chairman of the Member Representatives Committee.

4. The Board of Trustees or, in the event of the board’s failure to do so, the members

of the NC, shall appoint a chair from among the trustee members. The NC shall appoint a secretary who need not be a trustee.

5. The date and place of meetings of the NC and the procedure at such meetings

shall be the same as for regular Board of Trustees’ meetings of the corporation, or as determined from time to time by the members of the NC, provided that:

(a) A quorum for meetings shall be a majority of the number of members

of the NC.

(b) The NC shall meet as required and at least twice a year.

6. The compensation of trustee members of the NC and chair shall be the same as established by the board for its other committees.

Deleted: Stakeholders

Deleted: Stakeholders

Deleted: Stakeholders

Deleted: Stakeholders

Deleted: Stakeholders

Deleted: Stakeholders

Deleted:

Approved by Board of Trustees June 10, 2003

2

7. The NC shall be responsible for:

(a) Recommending to the Member Representatives Committee candidates for election as trustees.

(b) Implementing the board composition provisions of the bylaws and the

board’s conflict of interest policy and trustee succession policy in making its recommendations.

(c) Completing a self-assessment annually to determine how effectively

the NC is meeting its responsibilities.

(d) Performing such other functions as may be delegated from time to time by the board.

Formatted: Indent: Left: 72 pt

Formatted: Bullets and Numbering

Formatted: Bullets and Numbering

Formatted: Bullets and Numbering

Deleted: Stakeholders

116-390 Village Blvd. Princeton, NJ 08540

609.452.8060 | www.nerc.com

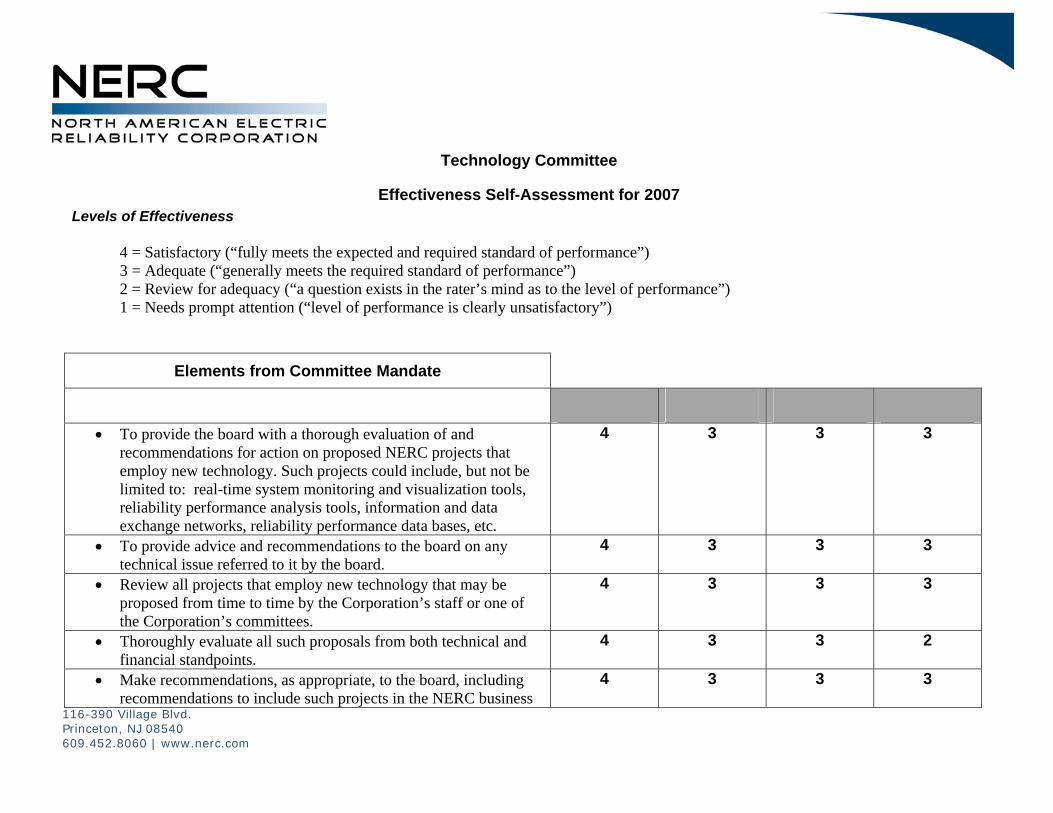

Board of Trustees Technology Committee Mandate Approved: XX

1. The Technology Committee (TC) shall be composed of not less than three and not more

than six Trustees. 2. The members of the TC shall be appointed or reappointed by the Board at the regular

Meeting of the Board immediately following each Annual Meeting of the Member Representatives Committee. Each member of the TC shall continue to be a member thereof until his/her successor is appointed, unless he/she shall resign or be removed or shall cease to be a Trustee of the Corporation. Where a vacancy occurs at any time in the membership of the TC, it may be filled by the Board of Trustees.

3. The Board of Trustees or, in the event of their failure to do so, the members of the TC,

shall appoint a Chair from among their members. The TC shall also appoint a Secretary who need not be a Trustee.

4. The place of meeting of the TC and the procedures at such meeting shall be the same as for

regular Board meetings of the Corporation, or as determined by the members of the TC, provided that:

(a) A quorum for meetings shall be a majority of the number of members of the TC.

(b) The TC shall meet as required and at least twice a year. 5. The compensation of the members of the TC and Chair shall be the same as established by

the Board for its other committees. 6. The objectives of the TC are as follows:

(a) To provide the board with a thorough evaluation of and recommendations for action on proposed NERC projects that employ new technology. Such projects could include, but not be limited to: real-time system monitoring and visualization tools, reliability performance analysis tools, information and data exchange networks, reliability performance data bases, etc.

(b) To provide advice and recommendations to the board on any technical issue referred to it by the board.

Board of Trustees Technology Committee Mandate Approved by the NERC Board of Trustees February 13, 2007

2

7. To achieve its objectives, the TC shall:

(a) Review all projects that employ new technology that may be proposed from time to time by the Corporation’s staff or one of the Corporation’s committees;

(b) Thoroughly evaluate all such proposals from both technical and financial standpoints;

(c) Make recommendations, as appropriate, to the board, including recommendations to include such projects in the NERC business plan and budget;

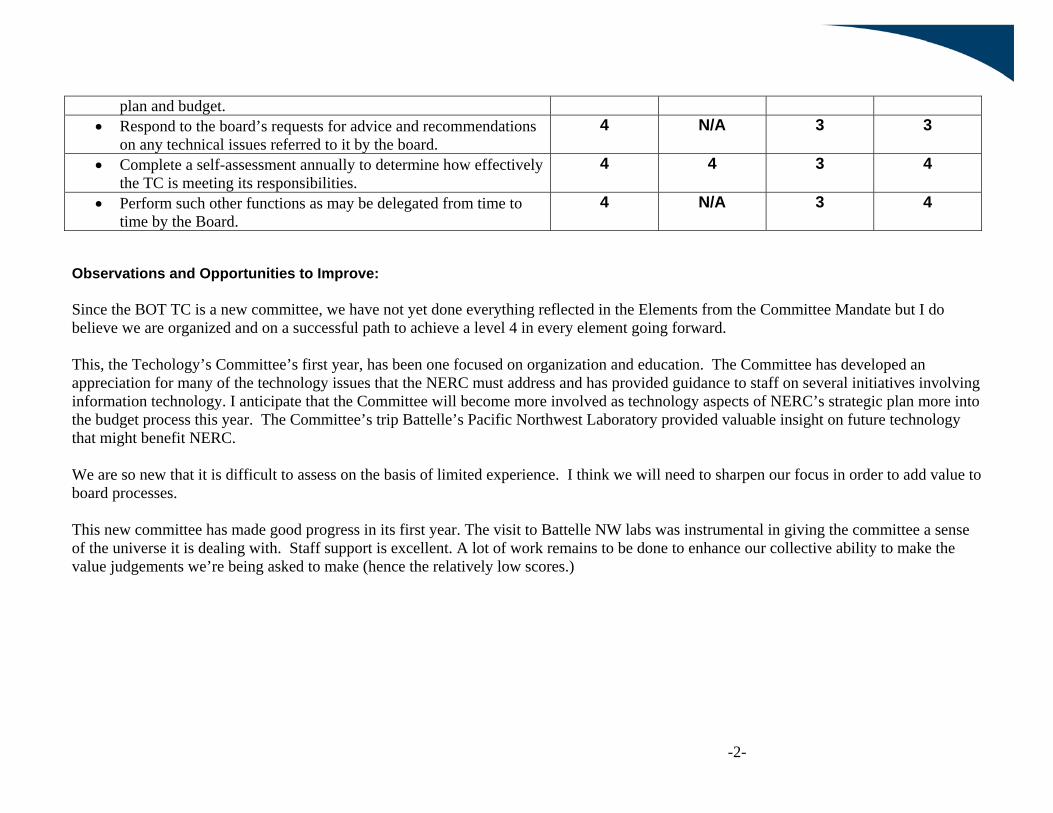

(d) Respond to the board’s requests for advice and recommendations on any technical issues referred to it by the board.

(e) Complete a self-assessment annually to determine how effectively the TC is meeting its responsibilities; and

(f) Perform such other functions as may be delegated from time to time by the board.

Conflict of Interest Guidelines for Trustees, Officers and Employees Business Ethics Guidelines

Committee Action Required Discuss objectives of business ethics principles to be considered at the May 2008 committee meeting. Background As the designated “electric reliability organization,” NERC has vital responsibilities within the electricity industry. Stakeholders, governmental authorities, and the industry in general must be able to have confidence that NERC is carrying out those responsibilities in an independent, fair and impartial manner. Management believes it is imperative to have guidance in place to help NERC representatives maintain the highest levels of professional and ethical conduct.

NERC’s consideration of guidelines for business ethics proceeds from two core concepts:

• NERC representatives must not use their position at NERC for private gain, and • NERC representatives must act impartially and not give preferential treatment to

any particular organization or individual.

To ensure that stakeholders, governmental authorities, and the industry in general have confidence in how NERC is carrying out its responsibilities, NERC representatives must also strive to avoid any action that would create the appearance they are violating the law or ethical standards. NERC’s “Conflict of Interest Guidelines for Trustees, Officers, and Employees” (attached) address the financial aspects of conflicts of interest, but do not address gifts, favors, entertainment and payments given or received by NERC representatives. Discussion The following draft guideline should serve as a basis for committee discussion and the questions that follow are included to guide the discussion.

NERC Representatives shall not give, solicit, or accept gifts from any person or organization that regulates NERC or is subject to regulation by NERC, that participates or seeks to participate in NERC activities, or that does or seeks to do business with NERC, except such commonly accepted courtesies as are usually associated with sound business practices.

“Gift” is defined as any gratuity, favor, discount, entertainment, hospitality, loan, or other similar item having monetary value.

Agenda Item 7 CG&HR Agenda February 11, 2008

NERC should offer guidance in interpreting the general statement, especially as to what constitutes a gift and what is included within “commonly accepted courtesies.” The following questions are offered to assist a discussion of what that guidance should include. Questions: 1. Should the guidelines include an absolute prohibition on certain kinds of gifts

(e.g., cash or cash equivalents)? 2. Should the guidelines include a dollar limit on gifts? 3. Should the guidelines on “commonly accepted courtesies” include an element

of reciprocity (i.e., one should not accept a gift he or she is not in a position to give in return) and mutuality (not one-way giving or receiving)?

4. Should the guidelines include a list of acceptable/unacceptable examples?

a. Meals with users, owners, and operators; b. Meals with vendors and would-be vendors; c. Pre-existing relationships; d. How to deal with inappropriate gifts e. Others

2007 Discretionary Contribution Savings & Investment Plan Committee Action Required Recommend to the board that the annual discretionary contribution equal to 10% of eligible compensation to the Savings and Investment Plan for all eligible employees be authorized for the plan year ending December 31, 2007. Background When the NERC Defined Benefit Plan was terminated in 2003, the board passed a resolution to put in place an annual discretionary contribution equal to 10% of eligible compensation to the NERC Savings and Investment Plan for all eligible employees. As part of the audit that was performed on the NERC Savings and Investment Plan in 2006, the Mercadien Group made the following observation and recommendation: “Currently, the 10% profit sharing match is recurring and does not have to be approved annually. We recommend that the Board of Trustees or Finance and Audit Committee approve the profit sharing match annually as part of its fiduciary responsibility.” The board’s approval of this item will implement the recommendation from Mercadien Group.

Agenda Item 8 CG&HR Committee Meeting February 11, 2008

116-390 Village Blvd. Princeton, NJ 08540 609.452.8060 | www.nerc.com

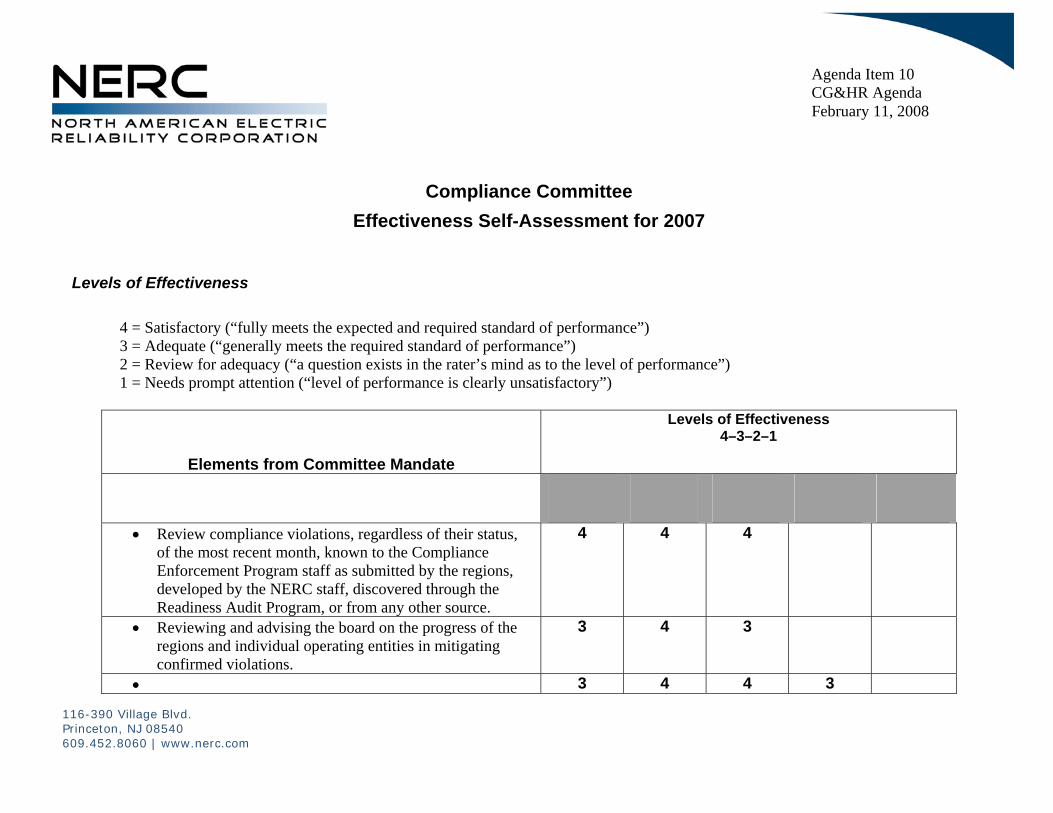

NERC Board of Trustees Effectiveness Self-Assessment for 2007

Levels of Effectiveness 4 = Satisfactory (“fully meets the expected and required standard of performance”) 3 = Adequate (“generally meets the required standard of performance”) 2 = Review for adequacy (“a question exists in the rater’s mind as to the level of performance”) 1 = Needs prompt attention (“level of performance is clearly unsatisfactory”)

I. Discharge of Responsibilities

A. Has the board addressed its responsibilities to ensure the affairs of the corporation are conducted in an ethical and moral manner?

4 4 4 4 4 4 4 4 4

B. Is the board sufficiently involved to ensure a viable strategic plan and effectively monitor the implementation and results of the strategic plan?

4 4 4 4 4 4 4 4 4

C. Is the board satisfied that senior management is competent and well motivated?

4 4 4 4 4 4 4 4 4

D. Does the Board assure itself that proper development and succession plans are in place for the CEO and senior management?

4 4 4 3 3 4 3 4 3

Agenda Item 9 CG&HR Agenda February 11, 2008

-2-

E. Is the board process, through the

CGHRC, for reviewing the Chief Executive Officer’s performance, effective and meaningful?

4 4 4 4 N/A 4 4 4 4

F. Are reliability and integrity of corporate internal control procedures and management information systems monitored to assure the underlying asset base is not eroded?

4 4 4 4 4 3 3 4 4

G. Is the board satisfied with management’s representations?

4 4 4 4 4 4 4 4 4

H. Does the board make sufficient use of internal and/or external auditors?

4 4 4 4 4 2 3 4 3

I. Does the board assure itself that the rules of timely disclosure are observed?

4 4 4 NA 4 4 4 3 4

J. Does the board conduct effective communication with all stakeholders?

4 4 4 3 3 4 3 3 4

K. Is the board sufficiently involved in the annual budgeting process?

4 4 4 4 4 4 4 4 4

II. Composition and Structure

A. Is the board the right size? 4 4 4 4 4 4 4 4 4 B. Do the board members have a mix, in

terms of diversity of backgrounds, personal qualities and traits, competencies and experience?

3 4 4 4 4 4 3 3 4

C. Has the board formed the appropriate committees in the necessary disciplines?

4 4 4 4 4 4 4 4 4

D. Do these committees have suitable mandates and membership?

4 4 4 4 4 4 4 4 4

E. Is there a suitable director nomination process?

4 4 4 4 4 4 4 4

F. For new board members, how would you rate the orientation and education program that was provided to you?

N/A N/A N/A N/A N/A 4 N/A 4 3

-3-

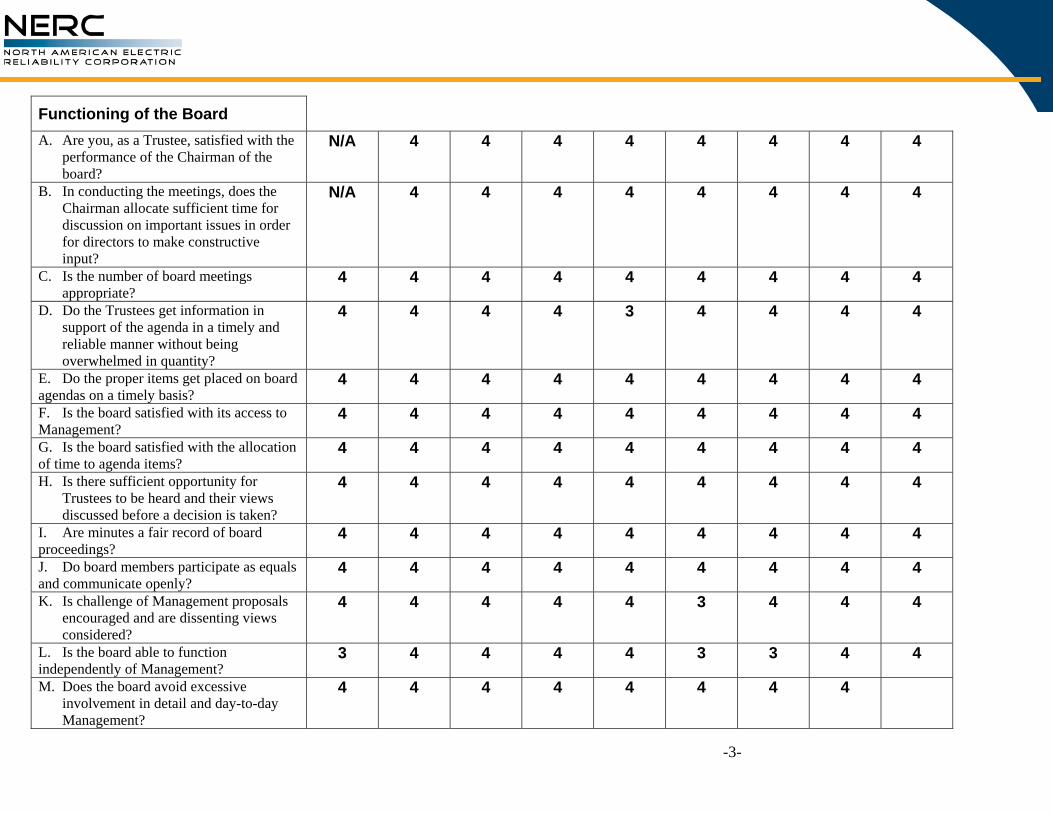

Functioning of the Board A. Are you, as a Trustee, satisfied with the

performance of the Chairman of the board?

N/A 4 4 4 4 4 4 4 4

B. In conducting the meetings, does the Chairman allocate sufficient time for discussion on important issues in order for directors to make constructive input?

N/A 4 4 4 4 4 4 4 4

C. Is the number of board meetings appropriate?

4 4 4 4 4 4 4 4 4

D. Do the Trustees get information in support of the agenda in a timely and reliable manner without being overwhelmed in quantity?

4 4 4 4 3 4 4 4 4

E. Do the proper items get placed on board agendas on a timely basis?

4 4 4 4 4 4 4 4 4

F. Is the board satisfied with its access to Management?

4 4 4 4 4 4 4 4 4

G. Is the board satisfied with the allocation of time to agenda items?

4 4 4 4 4 4 4 4 4

H. Is there sufficient opportunity for Trustees to be heard and their views discussed before a decision is taken?

4 4 4 4 4 4 4 4 4

I. Are minutes a fair record of board proceedings?

4 4 4 4 4 4 4 4 4

J. Do board members participate as equals and communicate openly?

4 4 4 4 4 4 4 4 4

K. Is challenge of Management proposals encouraged and are dissenting views considered?

4 4 4 4 4 3 4 4 4

L. Is the board able to function independently of Management?

3 4 4 4 4 3 3 4 4

M. Does the board avoid excessive involvement in detail and day-to-day Management?

4 4 4 4 4 4 4 4

-4-

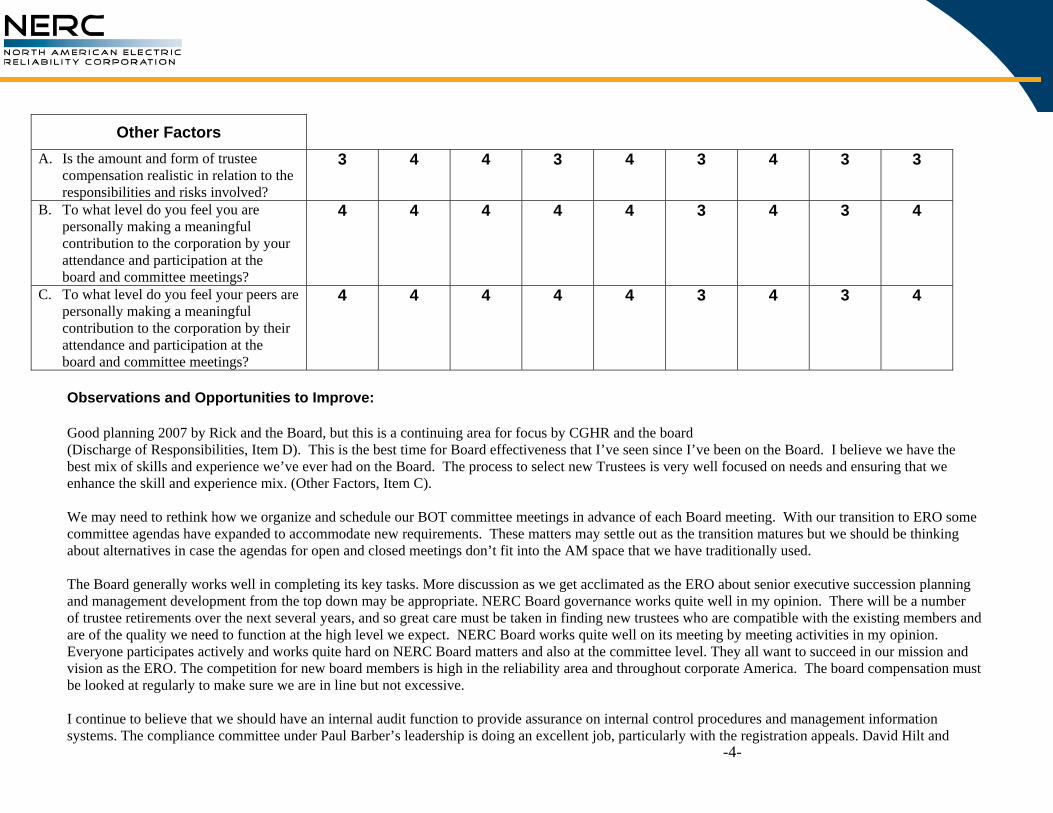

Other Factors A. Is the amount and form of trustee

compensation realistic in relation to the responsibilities and risks involved?

3 4 4 3 4 3 4 3 3

B. To what level do you feel you are personally making a meaningful contribution to the corporation by your attendance and participation at the board and committee meetings?

4 4 4 4 4 3 4 3 4

C. To what level do you feel your peers are personally making a meaningful contribution to the corporation by their attendance and participation at the board and committee meetings?

4 4 4 4 4 3 4 3 4

Observations and Opportunities to Improve: Good planning 2007 by Rick and the Board, but this is a continuing area for focus by CGHR and the board (Discharge of Responsibilities, Item D). This is the best time for Board effectiveness that I’ve seen since I’ve been on the Board. I believe we have the best mix of skills and experience we’ve ever had on the Board. The process to select new Trustees is very well focused on needs and ensuring that we enhance the skill and experience mix. (Other Factors, Item C). We may need to rethink how we organize and schedule our BOT committee meetings in advance of each Board meeting. With our transition to ERO some committee agendas have expanded to accommodate new requirements. These matters may settle out as the transition matures but we should be thinking about alternatives in case the agendas for open and closed meetings don’t fit into the AM space that we have traditionally used. The Board generally works well in completing its key tasks. More discussion as we get acclimated as the ERO about senior executive succession planning and management development from the top down may be appropriate. NERC Board governance works quite well in my opinion. There will be a number of trustee retirements over the next several years, and so great care must be taken in finding new trustees who are compatible with the existing members and are of the quality we need to function at the high level we expect. NERC Board works quite well on its meeting by meeting activities in my opinion. Everyone participates actively and works quite hard on NERC Board matters and also at the committee level. They all want to succeed in our mission and vision as the ERO. The competition for new board members is high in the reliability area and throughout corporate America. The board compensation must be looked at regularly to make sure we are in line but not excessive. I continue to believe that we should have an internal audit function to provide assurance on internal control procedures and management information systems. The compliance committee under Paul Barber’s leadership is doing an excellent job, particularly with the registration appeals. David Hilt and

-5-