negotiable instrument act 1881 unit-3. meaning negotiable means “transferable by delivery”....

TRANSCRIPT

NEGOTIABLE INSTRUMENT ACT 1881

UNIT-3

Meaning

Negotiable means “transferable by delivery”.

Instrument means “written document by which a right is created in favor of some person”.

Thus, a negotiable instrument means ‘a written document transferable by delivery’.By-Akansha Kansal

DefinitionSection – 13 A “negotiable instrument”

means

a promissory note,

bill of exchange or cheque payable either to order or to bearer.

Section 13(2) - A negotiable instrument may be made payable to two or more payees jointly,

or it may be made payable in the alternative to one of two, or one or some of several payees. By-Akansha Kansal

ESSENTIALS OF NEGOTIABLE INSTRUMENTS

Instrument being in writing & signed by its maker.

It contains an unconditional promise or order to pay some money.

It is about a fixed sum of money.

The transferee of a negotiable instrument, receiving it in good faith & for value, has a right to recover the amount mentioned in it. Such a person is called ‘Holder in Due Course’.

The transferee can sue on it in his own name to enforce his rights.

It is based on some presumptions.By-Akansha Kansal

Presumptions about Negotiable Instrument

Consideration- Every NI was made, drawn, accepted for consideration.

Date

Time of acceptance (before maturity).

Proper time of transfer.

Order of endorsements.

Stamp

Holder in due course

Fact of dishonor- through certificate from notary public about fact of dishonour.

By-Akansha Kansal

Kinds of Negotiable InstrumentThere are many kinds of negotiable instrument

but act has taken a specific account of only 3 of these. They are-

1. Promissory note- it is a negotiable instrument which contains an unconditional promise by one person to pay a certain sum of money to another person.

2. Bill of exchange- it is a negotiable instrument which contains an order directing a certain person to pay a certain sum of money to the bearer of the instrument or to a specified person.

3. Cheque- it is a negotiable instrument which contains an unconditional order to a specified banker to pay a certain sum of money to the bearer of instrument or to a specified person.

By-Akansha Kansal

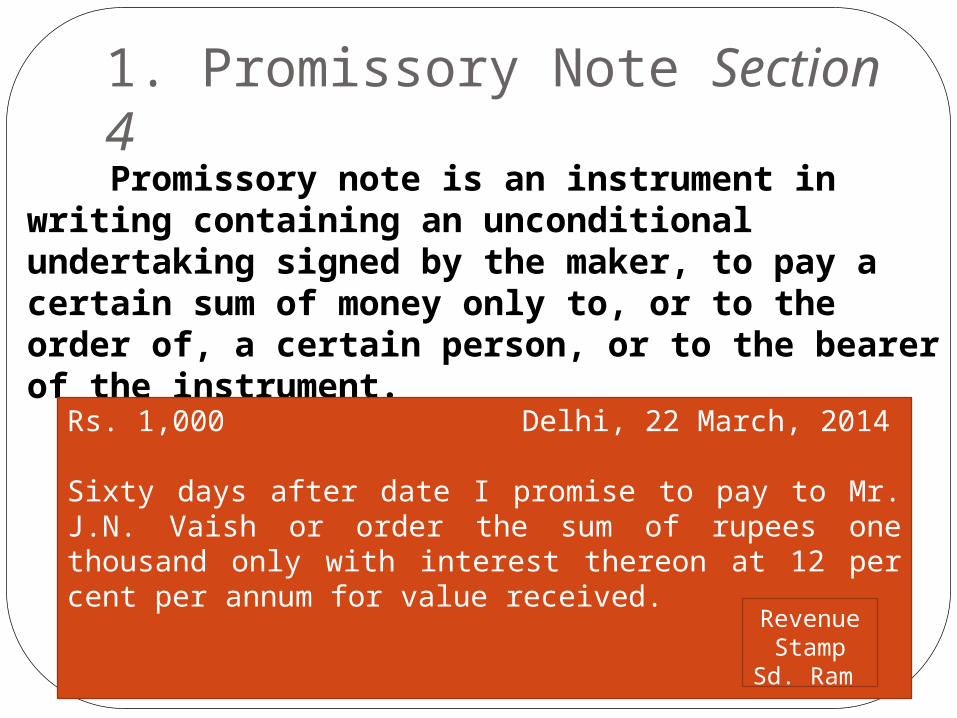

1. Promissory Note Section 4

Promissory note is an instrument in writing containing an unconditional undertaking signed by the maker, to pay a certain sum of money only to, or to the order of, a certain person, or to the bearer of the instrument.

Rs. 1,000 Delhi, 22 March, 2014

Sixty days after date I promise to pay to Mr. J.N. Vaish or order the sum of rupees one thousand only with interest thereon at 12 per cent per annum for value received.

Revenue Stamp

Sd. Ram

Parties to a Promissory Notes

There are 2 parties to a promissory notes-

1. The maker- The person(i.e. Debtor) who makes the promissory note.

1. The payee- The person(i.e. creditor) to whom order the payment is to be made.

By-Akansha Kansal

Essentials of a Promissory Note

It must be in writing

It must contain a promise or undertaking to pay.

The promise to pay must be unconditional.

It must be signed by the maker.

The maker must be a certain person.

The payee must be certain.

The sum payable must be certain.

The amount payable must be in legal tender money of India.

By-Akansha Kansal

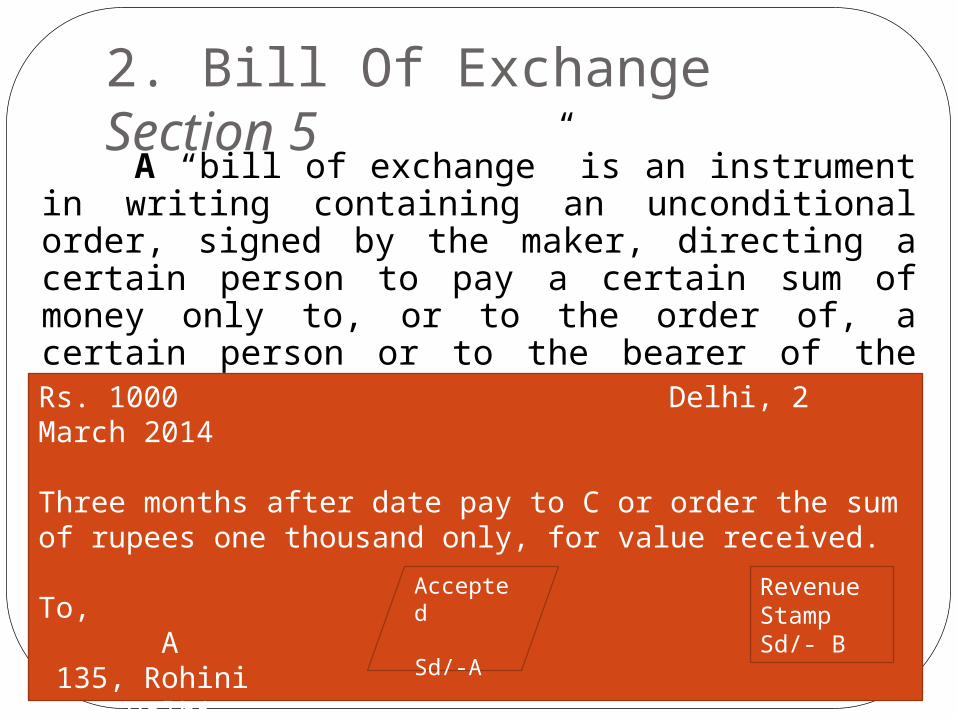

2. Bill Of Exchange Section 5

A “bill of exchange” is an instrument in writing containing an unconditional order, signed by the maker, directing a certain person to pay a certain sum of money only to, or to the order of, a certain person or to the bearer of the instrument.

Rs. 1000 Delhi, 2 March 2014

Three months after date pay to C or order the sum of rupees one thousand only, for value received.

To, A 135, Rohini Delhi

Accepted

Sd/-A

Revenue StampSd/- B

Parties to a Bill of Exchange

There are 3 parties to a Bill of Exchange-

1. Drawer- The person who draws a bill of exchange.

2. Drawee- The person on whom the bill of exchange is drawn. He is also called as an acceptor of the Bill, when he accepts the bill by writing the words ’accepted’ & then signing.

3. Payee- The person named in the instrument to whom or to whose order the money is directed to be paid by the instrument.

By-Akansha Kansal

Essentials of a Bill of Exchange

It must be in writing

It must contain an order to pay.

The order to pay must be unconditional.

It must be signed by the drawee.

The maker must be a certain person.

The drawee, drawer and payee must be certain.

The sum payable must be certain.

The bill must contain an order to pay money only.

By-Akansha Kansal

2. Cheque Section 6

“A cheque is a bill of exchange drawn on a specified banker and not expressed to be payable otherwise than on demand and it includes electronic image of a truncated cheque and a cheque in electronic form”.

By-Akansha Kansal

Parties to a Cheque

There are 3 parties to a cheque-

1. Drawer- The person who draws the cheque.

2. Banker- The bank on which the cheque is drawn.

3. Payee- The person in whose favour the cheque is drawn. The payee may be the third party or the drawer himself.

By-Akansha Kansal

Essentials of a Cheque

The cheque is one form of Bill of Exchange.

It is always drawn on bank.

It may be written on a paper or it may be in the electronic form.

It is always payable on demand.

It may be authenticate by the hand written signature or by digital signature.

By-Akansha Kansal

Section 7 DRAWER, DRAWEE AND PAYEE

The maker of a bill of exchange or cheque is called the “drawer”;

the person thereby directed to pay is called the “drawee”

The person named in the instrument,

to whom,

or to whose order

the money is by the instrument directed to be paid,

is called the “payee”

However, a drawer and payee can be one person as he can order to pay the amount to himself.

By-Akansha Kansal

Cheque Bill of Exchange

1) It must be drawn only on a

banker.

2) The amount is always payable

on demand.

3) The cheque is not entitled to

days of grace.

4) Acceptance is not needed.

5) A cheque can be crossed

6) Notice of dishonour is not

necessary. The parties thereon

remain liable, even if no notice

of dishonour is given.

7) A cheque is not to be noted or

protested in case of dishonour.

8) The protection given to the

paying banker in respect of

crossed cheques is peculiar to

this instrument.

1) It can be drawn on any person

including a banker.

2) The amount may be payable on

demand or af ter a. specified

time.

3) A usance (time) bill is entitled

to three days of grace.

4) A bill payable after sight must

be accepted.

5) Crossing of a bill of exchange is

not possible.

6) Notice of dishonour is necessary

to hold the parties liable

thereon. A party who does not

receive a notice of dishonour

can generally escape its liability

thereon.

7) A bill is noted or protested to

establish dishon our.

8) No such protection is available

in the case of bills.

By-Akansha Kansal

Promissory Note Bill of Exchange

1) There are only two parties – the

maker (debtor) and the payee

(creditor).

2) A note contains an unconditional

promise by the maker to pay the

payee.

3) No prior acceptance is needed.

4) The liability of the maker or

drawer is primary and absolute.

5) No notice of dishonour need be

given.

6) The maker of the note stands in

immediate relation with the

payee.

1) There are three parties – the

drawer, the drawee and the

payee- although any two of these

capacities may be filled by one

and the same person.

2) It contains an unconditional order

to the drawee to pay according to

the drawer`s directors.

3) A bill payable `after sight` must

be accepted by the drawee or his

agent before it is presented for

payment.

4) The liability of the drawer is

secondary and conditional upon

non-payment by the drawee.

5) Notice of dishonour must be given

by the holder to the drawer and

the intermediate endorsers to

hold them liable thereon.

6) The maker or drawer does not

stand in immediate relation with

the acceptor drawee.

By-Akansha Kansal

Topic-2

“HOLDER” AND “HOLDER IN DUE COURSE”

Holder (Section 8)

A person is called holder of a negotiable instrument if he satisfies the following two conditions:

He must entitled to the possession of the instrument in his own name; and

He must be entitled to receive/recover the amount due on the instrument from the parties liable under the instrument.

By-Akansha Kansal

Example:

X advanced Rs. 10,000 to Y who executed a promissory note in the name of Z. On maturity Y failed to pay the amount due and X brought an action against Y. It was held that X could not recovered the amount because he was not entitled to the promissory note in his own name.

By-Akansha Kansal

Holder in Due Course (Sec 9)

He must be a holder.

He must have become, for consideration. Such consideration must not be unlawful and need not be adequate.

He must have obtained the instrument before its maturity.

He must have obtained the instrument in good faith, i.e. without having sufficient cause to believe that any defect existed in the title of the person from whom he derived his title.

He must receive the instrument complete and regular on the face of it.By-Akansha Kansal

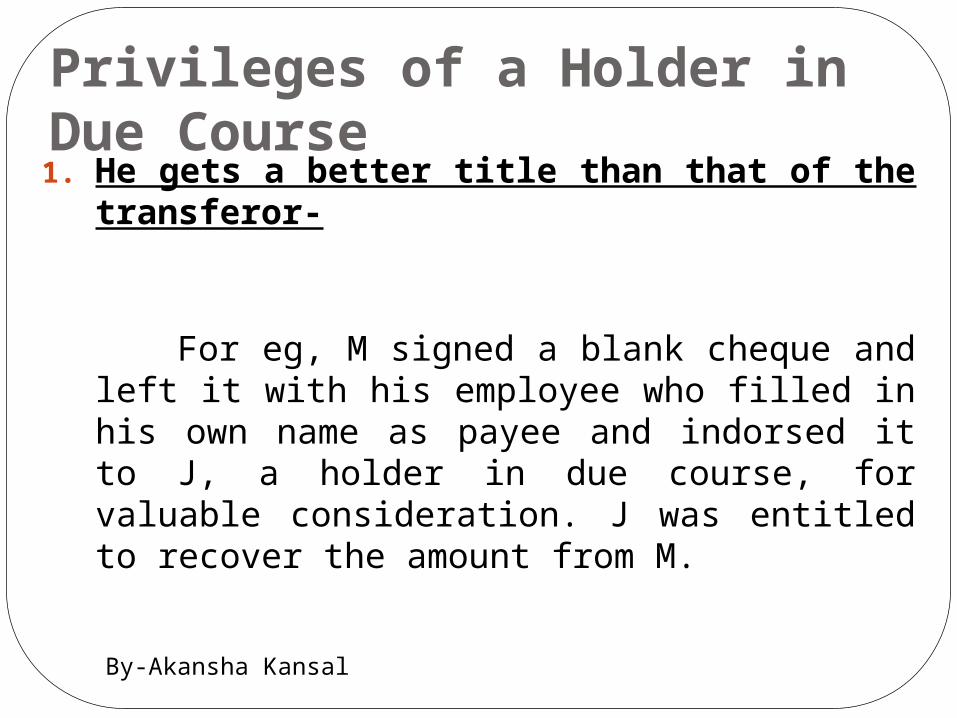

Privileges of a Holder in Due Course1. He gets a better title than that of the

transferor-

For eg, M signed a blank cheque and left it with his employee who filled in his own name as payee and indorsed it to J, a holder in due course, for valuable consideration. J was entitled to recover the amount from M.

By-Akansha Kansal

By-Akansha Kansal

2. Privilege in case of inchoate stamped instruments (Sec. 20)

Inchoate means an instrument that is incomplete in certain respects.

If such an instrument is transferred to a holder in due course, he can claim the whole of the amount so entered provided that the amount is covered by the stamp affixed thereon.

3. Liability of prior parties: All the prior parties to a negotiable instrument continue to remain liable to a holder in due course both only and severally until the instrument is duly satisfied.

4. Privilege in case of fictitious bills: Such a bill is not a good bill and cannot be enforced at law. But the acceptor of such a bill is liable to holder in due course provided the latter can show that the first endorsement on the bill and the signature of the supposed drawer in the same handwriting.

5. Privilege when an instrument delivered conditionally is negotiated. For eg: if I give a cheque to a shopkeeper with the condition that he should not encash the cheque till he supplies me the goods, anybody encashing the cheque before fulfilling the condition is liable to return the money except ‘holder in due course’.By-Akansha Kansal

6. Estoppel against denying original validity of instrument (sec.120) : The plea of original invalidity of the instrument, eg, that no consideration actually passed between the maker & payee, cannot be put forth against the ‘holder in due course’.

7. Estoppel against denying capacity of payee to endorse: A holder in due course can claim payment in his own name despite the payee’s incapacity to endorse the instrument.

By-Akansha Kansal

Difference B/W a Holder and a Holder in Due Course

He may become the possessor or payee of an instrument even without consideration.

He need not become the possessor the maturity of the instrument.

He acquires possession for consideration.

He must become the possessor before the maturity of the instrument.

By-Akansha Kansal

He need not become the possessor in good faith.

He cannot have a better title than that of transferor.

He must become the possessor in good faith i.e. without having sufficient cause to believe that any defect existed in the transferor’s title.

He can have a better title than that of transferor.

By-Akansha Kansal

He cannot enforce his rights against all the prior parties. He can recover the amount from a person who has signed it and also from whom he obtained.

He does not enjoy all the privilege available to holder in due course.

He can enforce his rights against all the prior parties.

He enjoys some privilege under the act, ex under Sections 20,36,42,43,46,58,120,121.

By-Akansha Kansal

Negotiation by endorsement

Topic-3

Negotiation

Where a negotiable instrument is transferred to any person so as to constitute that person the holder thereof, the instrument is said to be negotiated. There are 2 essentials of negotiations.

a) The instrument should be transferred from one person to another.

b) The transfer should be in such a manner so as to constitute the transferee of its holder.

By-Akansha Kansal

Modes of Negotiation

1. Negotiation by delivery : A negotiable instrument payable to the bearer can be transferred by mere delivery and the transferee becomes the holder of the instrument. The transferor need not sign his name on such instrument. E.g. A, a holder of a negotiable instrument payable to bearer, delivers it to B’s agent to keep for B. The instrument has been negotiated.

2. Negotiation by endorsement and delivery : An instrument payable to order is negotiable by the holder by endorsement and delivery thereof.

By-Akansha Kansal

Kinds of Endorsement

1. Blank or general endorsement

2. Full or special endorsement

3. Partial endorsement

4. Restrictive endorsement

5. Conditional or qualified endorsement

6. Sans Recourse endorsement

7. Facultative endorsement

By-Akansha Kansal

1. Blank or general endorsement

A blank or general endorsement is one in which the endorser simply puts down his signature.

The name of the endorsee is not put down.

The effect of such an endorsement is to make the instrument into a bearer instrument. The property in the instrument can now be transferred by mere delivery.

By-Akansha Kansal

2. Special or full endorsement

Special or full endorsement is that which contains not only the name of the endorser but also the name of the endorsee.

For eg, A, the holder of a bill of exchange, wants to make an endorsement in full to B, he would write this: “Pay to B or order, Sd/A.”

After such an endorsement it is only B who is entitled to receive the payment of the instrument & to further negotiate the instrument by his endorsement.

By-Akansha Kansal

3. Partial endorsement

A partial endorsement is one which means to transfer the instrument only for a part of its value.

For instance a cheque for Rs. 500 may be endorsed only for Rs.300. Legally such an endorsement is invalid.

By-Akansha Kansal

4. Restrictive endorsement:

When an endorsement restricts the negotiability or transferability of ownership of an instrument, it is known as restrictive endorsement.

Such an endorsement entitles the endorsee to receive the payment on due date & sue the parties for it but he cannot further negotiate the instrument.

By-Akansha Kansal

5. Conditional or qualified endorsement

If the endorser, by express words in the endorsement, makes his liability, dependent on the happening of a specified event, although such an event may never happen, such endorsement is conditional endorsement.

For eg, “Pay B or order on his marriage”.

But, the endorsee can sue other prior parties, if the instrument is not duly met on maturity, even though the specified event did not happen.By-Akansha Kansal

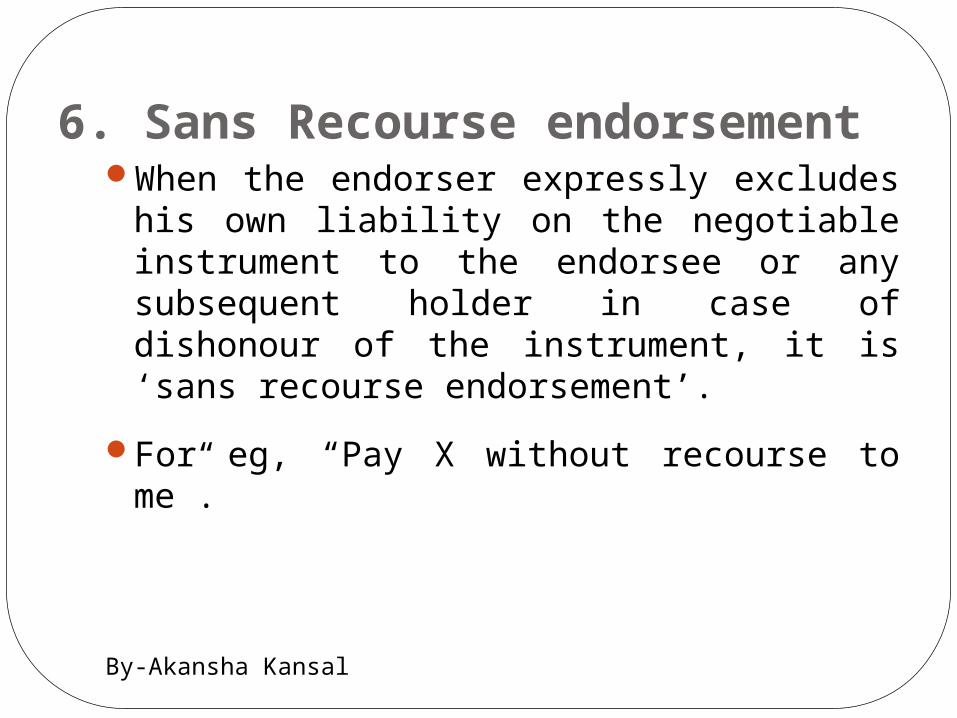

6. Sans Recourse endorsementWhen the endorser expressly excludes his

own liability on the negotiable instrument to the endorsee or any subsequent holder in case of dishonour of the instrument, it is ‘sans recourse endorsement’.

For eg, “Pay X without recourse to me”.

By-Akansha Kansal

7. Facultative endorsement

When an endorser expressly gives up some of his rights under the negotiable instrument, the endorsement is called a ‘facultative’ endorsement.

For eg, “Pay X or order, notice of dishonour waived” is a facultative endorsement,

Facultative means optional or not-compulsory.

By-Akansha Kansal

Topic-4

CROSSING OF CHEQUES

INTRODUCTION

Cheques may be of two types-

1. Open or uncrossed cheques- It is payable at the counter of the drawee bank on the presentation of the cheque.

2. Crossed cheques- it is payable only through a collecting banker & not directly at the counter of the bank.

A cheque is said to be crossed when two parallel transverse lines, with or without any words, are drawn on the left hand top corner of the cheque. Crossing of cheque does not affect its negotiability.

There are 2 types of crossing- A. General crossing and

B. Special crossing.

By-Akansha Kansal

A. GENERAL CROSSING Section 123

Where a cheque bears across its face two parallel transverse lines without any words or with words ‘and company’ or/and ‘not negotiable’ written in between these two parallel lines, it is called general crossing.

By-Akansha Kansal

B. SPECIAL CROSSING Section 124Where a cheque bears across its face an addition of the name of a banker, either with or without the words “not negotiable”, that addition shall be deemed a crossing, and the cheque shall be deemed to be crossed specially, and to be crossed to that banker.

Transverse lines may not be drawn in special crossing.

By-Akansha Kansal

Account Payee or Restrictive CrossingRestrictive crossing can be made in both

general and special crossing by adding the words ‘Account Payee’, Account Payee only’.

The effect is that the collecting banker is supposed to credit the amount of the cheque to the account of the payee only & nobody else.

By-Akansha Kansal

‘NOT NEGOTIABLE’ Crossing Section 130

A person taking a cheque crossed generally or specially, bearing in either case the words “not negotiable”, shall not have, and shall not be capable of giving, a better title to the cheque than that which the person from whom he took it had.

Thus, mere writing words ‘Not negotiable’ does not mean that the cheque is not transferable. It is still transferable, but the transferee cannot get title better than what transferor had.

By-Akansha Kansal

Who may cross a Cheque?

Section 125 permits the crossing being made even after issue of a cheque in the following ways:-

i. Where a cheque is uncrossed, the holder may cross it generally or specially.

ii. Where a cheque is crossed generally, the holder may cross it specially.

iii. Where a cheque is crossed generally or specially, the holder may add the words ‘not negotiable’.

iv. Where a cheque is crossed specially, the banker to whom it is crossed may again cross it specially to another banker as his agent for collection.

By-Akansha Kansal

Topic-5

DISHONOUR OF CHEQUE

Refusal of Payment by the BankerIt is the prime duty of the banker to honor

his customer’s cheque unless there are valid reasons for refusing payment on the same.

In case he dishonors a cheque wrongfully, he is liable to compensate the drawer.

By-Akansha Kansal

When banker ‘Must Refuse’ Payment on ChequesWhen payment is countermanded (stop) by

the customer.

On receipt of a notice of customer’s death.

On customer’s becoming insolvent.

On receipt of a notice of the customer’s insanity.

On receipt of a Garnishee order( prohibiting order from court attaching the money in the customer’s account).

When the banker suspects to believe that the title of the person presenting the cheque is defective.

When the banker receives the notice of lost of a cheque.

When there are unauthorized material alterations done in the cheque.

When signatures does not tally with bank records.

When the bank receives notice of closure of account.

By-Akansha Kansal

When banker ‘May Refuse’ Payment on ChequesWhen funds in the customer’s account are

insufficient.

When the funds in the customer’s account are not applicable for the cheques presented.

When the cheque is presented at the branch other than the branch where the customer who has issued the cheque, has the account.

When the cheque is presented after banking hours.

When the cheque is presented after the 6 months from th date of its issue( i.e. Stale cheques).

When the cheque is presented before the due date on which it is written to be payable.

When the cheque is undated.

By-Akansha Kansal

Penalty in case of dishonour of cheques for insufficiency of funds

If a cheque is dishonored even when presented before expiry of 6 months,

the payee or holder in due course is required to give notice to drawer of cheque within 30 days from receiving information from bank.

The drawer should make payment within 15 days of receipt of notice

If he does not pay within 15 days, the payee has to lodge a complaint with Metropolitan Magistrate or Judicial Magistrate of First Class, against drawer within one month from the last day on which drawer should have paid the amount.

The penalty can be upto two years imprisonment or fine upto twice the amount of cheque or both.

The offense can be tried summarily. Notice can be sent to drawer by speed post or courier.

Offense is compoundable.

By-Akansha Kansal

By-Akansha Kansal