navigating the indirect cost rate maze - ncma boston€¦ · is considered an intermediate pool,...

TRANSCRIPT

Navigating the Indirect CostRate Maze

Chad Braley Marie Salamone

Value Proposition

Capital Edge is the country’s largest independent consulting firm focusing solely on the U.S. Government contracting market.

2

Who We Work WithAll entities receiving Federal funding

3

The Solution Model

4

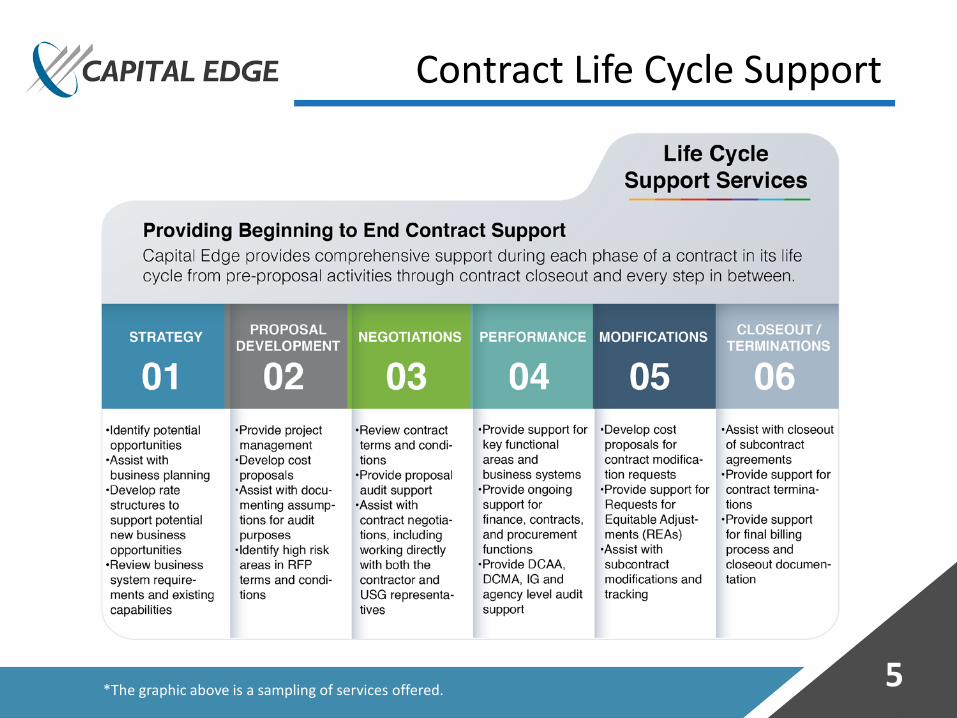

Contract Life Cycle Support

*The graphic above is a sampling of services offered. 5

Course Outline

• Indirect Rates – The Basics• Indirect Rate Composition Options• Indirect Rates throughout Contract Life Cycle• Establishing and Understanding Corporate Strategic

Objectives• Challenges Developing Indirect Cost RatesMergers and AcquisitionsIndirect Rate Changes under CAS Covered ContractsTo Silo or Not to SiloDecentralized OrganizationsCorporate Culture Hurdles

6

Indirect Rates –The Basics

Three Questions…

8

What is Cost Allowability?Reasonable Allowable Allocable

What is Cost Allocation?Pools Allocation Base

What is Cost?Direct Indirect

Composition of Total Cost — FAR 31.201-1

9= Total Cost

Direct CostsCosts directly associated with production of a product or service

(aka “Variable Costs”)

Indirect CostsCosts required to support production and/or normal business

operations(aka “Fixed Costs”)

+

+Cost of Money

The imputed cost of investment in the business

Applicable Credits-

Typical Direct & Indirect Costs

Direct Costs

Subcontracts

Material

Direct Labor

10

Indirect Costs

Rent

Utilities

Indirect Labor

Direct & Indirect Costs

• The regulations do not provide explicit criteria for the types of direct and indirect costs

• It is up to your company to define the costs that are direct vs. indirect as long as company parameters: can meet direct/indirect regulatory definitions, and ensure that costs are treated consistently as direct/indirect in like

circumstances (CAS 402 Guidance)

• Depending on industry type, make-up of company costs, company size, etc., costs that are treated as direct by one company may be treated as indirect by another

11

Major Concepts –Indirect Cost Pools

12

Homogeneous Pools

Beneficial or Causal Relationships

• Homogeneous Indirect pools must contain costs with common links• Base used to allocate those pooled cost must benefit from or

demonstrate to have caused the indirect costs to be incurred• Allocability — FAR 31.201-4• Normally expressed as a percentage (i.e., “Pool Expenses” is the

numerator and “Allocation Base” is the denominator)

Typical Indirect Pools and Allocation Bases

13

Fringe Pool

Overhead Pool

G&A

Total Labor

Vacation RetirementHealth Insurance

Direct Labor

Utilities RentIndirect Labor

Total Cost Input

Finance CEOHuman Resources

Value Added Input Baseor

Full Absorption Costing

14

Product Cost

Direct Labor

Material / Subcontracts

Overhead

Period Cost

Selling

General

Administrative

Total Project Costs

Allowable Cost Criteria FAR 31.201-2

15

“A cost is allowable only when the cost complies with all of

the following requirements”

Reasonable

Allocable

Complies with terms of the contract

FAR 31.2 criteria and limitations

CAS/GAAP Compliant

Risks of double and treble damages, plus interest for failure to comply!

What is Cost Allowability?

Costs the Government is willing to pay

for!

Indirect Rate Composition Options

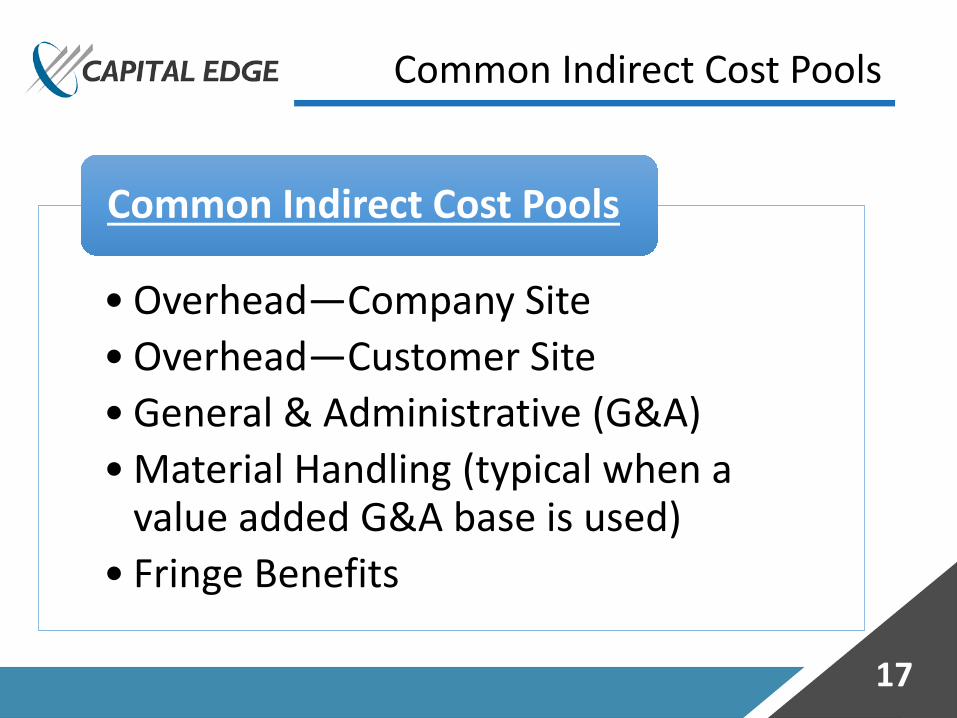

Common Indirect Cost Pools

17

• Overhead—Company Site• Overhead—Customer Site• General & Administrative (G&A)• Material Handling (typical when a

value added G&A base is used)• Fringe Benefits

Common Indirect Cost Pools

Intermediate Cost Pools

• Fringe benefits -- Total labor• Facilities – Square footage or headcount• IT Service Center -- Usage or headcount• Payroll Service Center -- Paychecks or headcount• Overhead Service Center -- Direct Labor & Fringe• Human Resources -- Headcount

Typical Intermediate Cost Pools & Bases

18

These can be found in Schedule D of the ICS

Two Tiers• Fringe is considered an

intermediate pool, allocated based on direct labor Allocated out to G&A and

Overhead pools as part of their rates

• Overhead includes fringe on direct labor Overhead is applied on direct

labor only

• G&A applied to the total cost input

Three Tiers• Fringe is a final indirect rate pool,

applied to total labor Applied first before Overhead

and G&A rates applied

• Overhead is applied on Direct Labor plus fringe on Direct Labor

• G&A is applied to the total cost input

Two Tiers vs. Three Tiers

19

Fringe

Overhead direct labor

G&Atotal cost input

Two Tier Indirect Rate

Structure

Two Tiers vs. Three Tiers

20

(allocated based on % of Total labor)

Three Tier Indirect Rate

Structure

Two Tiers vs. Three Tiers

21

Fringe• Total Labor

Overhead

• Direct Labor + Direct Labor Fringe

G&A

• Direct Labor + DL Fringe + Overhead + ODC’s +Subcontracts

Two Tiers vs. Three Tiers

• The G&A rate will always be the same, because it is applied to the same base (total cost input) regardless of the structure

Similarities

•Overhead rate will be higher using two-tier system, because fringe costs are in the pool instead of the base

Differences

22

*How to decide: How many times have you heard a customer say your O/H rate is too high? How many times have you heard a customer say to cut benefits b/c your fringe is too high? Definitely worth consideration.

G&A Allocation Bases

• Companies can choose between three types of G&A allocation bases: Total Cost Input includes all contract costs except G&A,

including direct labor, fringe, overhead, subcontracts, materials, and other ODC’s

• Method used most oftenValue-Added does not include direct material and

subcontracts costs• Useful when there is a significant amount of

subcontract costs and/or materialsSingle Input Base

• Typically direct labor and less frequently used

23

Strategy Considerations

24

What is important to your organization?

Want a Lower Pass Thru on

SubK?

High number of subcontractors / material costs?

Consider a Material Handling

Rate

Want a Lower Overhead Rate?

Consider moving from a 2 Tier to a

3 Tier Fringe Structure

Review costs which could be claimed as Fringe rather than Overhead

Common Pitfalls to Avoid

• When changing G&A allocation bases, you must consider the impact of rate changes on existing contracts

• When creating a customer site O/H, be aware of the impact to your contractor site work

• Creating new O/H pools for new contracts or new work sites can be very dangerousThe administrative and systemic burdens often outweigh the

benefitsThis process can also create numerous small pools and bases that

may fluctuate significantly

• Be wary of your contract type mix when making changesHow will this effect the entire contract population?

25

Indirect Rates Throughout Contract Life

Cycle

Types of Indirect Rates

27

Types of Indirect Rates (Cont.)

• Forward Pricing Rates - FAR 42.17 allows for the establishment of mutually agreed to Forward Pricing Rates between the Contracting Officer and ContractorEstablished long-term rates for use in contractor pricing effortsBased on the Contractor’s long range plans and budgetsMay be continuously negotiated/updated based on availability of

most current, accurate, and complete dataAdequacy Check List available at DCAA.mil

• Budgeted RatesApproved internally for management purposes and as a

basis for pricing products and servicesDCAA expects rates are prepared annually

28

Types of Indirect Rates (Cont.)

• Provisional or Contract Rates (FAR 42.704)Approval by the contracting officer or CFAORates established based on information from recent

review, previous rate audits or experienceAuditor assurance that rates are as close as possible to

final indirect cost rates anticipatedRevision by mutual agreement (AT ANY TIME), to prevent

substantial over/underpaymentTypically based on a contractor’s budget rates

29

Types of Indirect Rates (Cont.)

• ICS Rates (Final Indirect Cost Rate Proposal)Unaudited year end rates based on actual costs incurredSubject to audit by DCAA or Contracting Officer’s

designeeRequired within six months of Contractor’s fiscal year

end FAR 52.216-7 (d)(2)(i) - Allowable Cost and Payment FAR 52.232-7(b)(4) & (b)(5) - Payments under T&M and Labor-

Hour ContractsFAR 42.704 allows for ICS rates to become provisional

rates for the fiscal period until the Contractor’s ICS can be audit and rates finalized

30

Types of Indirect Rates (Cont.)

• Final Rates - FAR 42.705 requires final determination of rates by either the Contractor officer or his assigned representative (auditor)Adjusted for questioned/unallowable costs identified by

the auditor and Subject to Negotiation

31

Life Cycle of Indirect Rates

32

33

Acquisition Cycle - Indirect Rates

Establishing and Understanding

Corporate Strategic Objectives

Organizational Considerations

• What type of industry?GoodsServices

• How large is your organization?SmallMediumLarge

• Does your organization have many people and facilities in multiple locations?

• Do you have a large number of subcontractors?

35

Considerations – Industry (Cont.)

• GoodsDo you have multiple product lines requiring differing

support functions?Do you have manufacturing facilities in multiple

locations?

• ServicesDo you have a large number of employees working at

client/customer sites?Do you have different service offerings requiring

different support functions?Are your employee’s located both domestically and

internationally?

36

Compliant Rate Structure Benefits

• Facilitates Decision MakingHow is the company structured?Is the company structure changing?

• Improves Competitive Advantage in Market PlaceIndirect Rate Structure positioned to win the work

• Capitalizes on Thorough Budgeting ProcessHopefully already in existence…

• Ensures Allowable Cost RecoveryAnd maybe even some profit!

Rate Structure MUST mirror the Organization, not limited by accounting software, customer or govt.

37

Indirect Cost Rate Challenges

Challenge No. 1 –Mergers and Acquisitions

• Due DiligenceHas proper due diligence been performed on existing government

contracts? Are there rate caps? Are there CAS covered contracts? Are there unsubmitted/late incurred cost submission years? Are there inadequate incurred cost submissions? Are costs owed to the government on flexibly priced contracts?

• Incorporate or SegregateWill the acquired company be folded into the existing company? How will the acquisition impact the existing rate structure?

• Allowable vs. Unallowable CostsAre M&A costs captured to properly segregate allowable from

unallowable?39

Challenge No. 2 – Rate Changes under CAS Covered Contracts

• Fully CAS Covered Contracts require disclosure to accounting practices including indirect rate structures

• Changes to disclosed practices (including changes to rates) require cost impact proposals

• Two types of cost impact proposalsGeneral Dollar Magnitude (GDM) Proposal (FAR 52.230-6d)Detailed Cost Impact (DCI) Proposal (FAR 52.230-6e)

40

For Companies without CAS Covered Contracts:1. Keep changes to a minimum - makes good business sense2. Change rates to maintain compliance with standards3. Cost become material because of change in business4. If changes are necessary, change ahead of anticipation of

receiving a CAS covered contract

Challenge No. 3 –To Silo or Not to Silo

Advantages• Limits Compliance to Government Business• Limits Audits and Oversight to Government Business

Disadvantages• Disruption to current operations• Corporate culture resistance to change• Sometimes difficult to get buy in until work volume

increases

41

Challenge No. 4 –Decentralized Organizations

• Lines of business can analyze profitability in a vacuum

• Bid on new work using rates which are not the most current, accurate and complete

• Win contracts with significantly low rate caps• Bill contracts with unapproved provisional rates

resulting…High contract overbillings resulting in paying $$ back to

the government ORHigh contract underbillings resulting in poor cash flow to

the organization

42

Challenge No. 5 –Corporate Culture Hurdles

• Establishing or changing allocation bases can impact lines of businesses differentlyExample: Use of headcount for IT vs. Use of No. of

Licenses

• Allocating costs on budgeted data without using actual base dataActual data is difficult to obtain or no longer tracked

• Communication Challenges Between DepartmentsContracts and Accounting/FinanceBusiness Development and Compliance

43

National Coverage in Satellite Offices

Phoenix, AZ • Los Angeles, CA San Diego, CA • San Francisco, CADenver, CO • Melbourne, FL Tampa, FL • Dayton, OH • Pittsburgh, PAPhiladelphia, PA

CONTACT US

CORPORATE HEADQUARTERS8200 Greensboro Drive

Suite 401McLean, Virginia 22102

www.capitaledgeconsulting.com