national student financial aid scheme (nsfas) sefako makgatho ... and national student financial aid...

TRANSCRIPT

Performance and Expenditure Review

National Student Financial Aid Scheme (NSFAS)

Final

February 2016

Research commissioned by the National Treasury

FINAL FEBRUARY 2016

Version control of drafts submitted to National Treasury

Date submitted Draft number shown on cover Name of file

2015.10.30 First draft v1 2015 10 30 NSFAS PER Report v.4

2015.11.02 First draft v1 2015 11 01 NSFAS PER Report v.5

2015.11.04 First draft v2 2015.11.04 NSFAS PER Report First Draft v2

2015.11.27 First draft v3 2015.11.27 NSFAS PER Report First Draft v3

2015.12.30 Final draft v1 2015.12.30 NSFAS PER Report Final Draft v1

2016.02.24 Final 2016.02.24 NSFAS PER Report Final

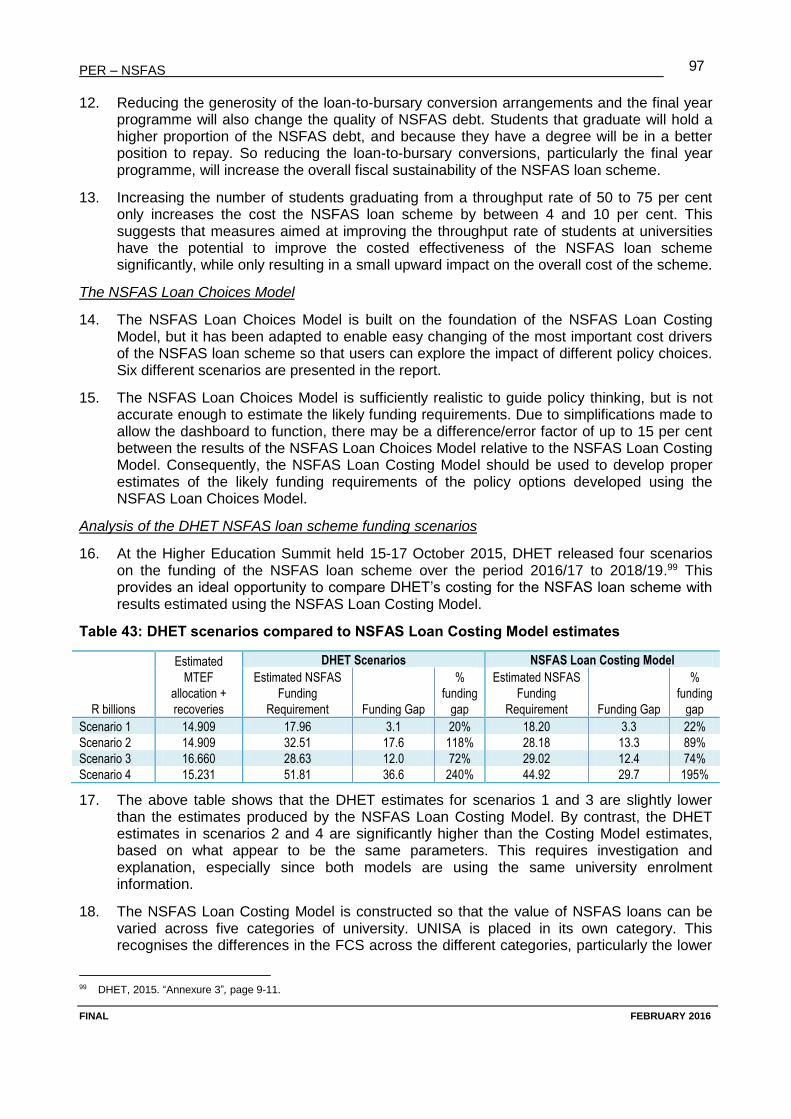

2016.03.18 Final v2 2013.03.18 NSFAS PER Report Final edited v2

Project team –

Jonathan Carter [email protected] Senior Researchers with Conrad Barberton [email protected] Cornerstone Economic Research Carmen Abdoll [email protected] www.cornerstonesa.net Fiona Lewis [email protected] Independent Consultant Charles Sheppard [email protected] Nelson Mandela Metropolitan University

PER – NSFAS – Key PER Observations ~ A ~

FINAL FEBRUARY 2016

PER – NSFAS

FINAL FEBRUARY 2016

i

Table of Contents LIST OF ABBREVIATIONS ........................................................................................................................................... 1

1. INTRODUCTION ................................................................................................................................................ 3

1.1 TOPIC ................................................................................................................................................................ 3 1.2 PURPOSE AND SCOPE ............................................................................................................................................ 3 1.3 KEY QUESTIONS ................................................................................................................................................... 4 1.4 INFORMATION USED IN CONDUCTING THE REVIEW ...................................................................................................... 4 1.5 LIST OF DOCUMENTS THAT MAKE UP THE REVIEW ........................................................................................................ 4

2. FUNDING FRAMEWORK FOR HIGHER EDUCATION ........................................................................................... 4

2.1 THE IMPORTANCE OF NSFAS FUNDING TO UNIVERSITIES AND TVET COLLEGES ................................................................ 6 2.2 THE ROLE OF NSFAS IN THE HIGHER EDUCATION FUNDING FRAMEWORK ........................................................................ 7

3. OVERVIEW OF NSFAS OPERATIONS .................................................................................................................. 8

3.1 THE NATURE OF NSFAS OPERATIONS ....................................................................................................................... 9 3.1.1 Loans for undergraduate study at university (NSFAS loans) ..................................................................... 10 3.1.2 Grants for study at a TVET college ............................................................................................................ 11 3.1.3 Administration of other bursary/grant schemes ...................................................................................... 12 3.1.4 Shortcomings of the old NSFAS administrative system............................................................................. 13

3.2 THE NEW STUDENT CENTRED MODEL .................................................................................................................... 14 3.3 PROPOSALS AND RECENT POLICY DEVELOPMENTS REGARDING NSFAS .......................................................................... 15

4. NSFAS IN THE HIGHER EDUCATION CONTEXT ................................................................................................. 17

4.1 INCREASING ENROLMENT NUMBERS ....................................................................................................................... 18 4.1.1 University enrolment numbers.................................................................................................................. 18 4.1.2 TVET college enrolment numbers ............................................................................................................. 20

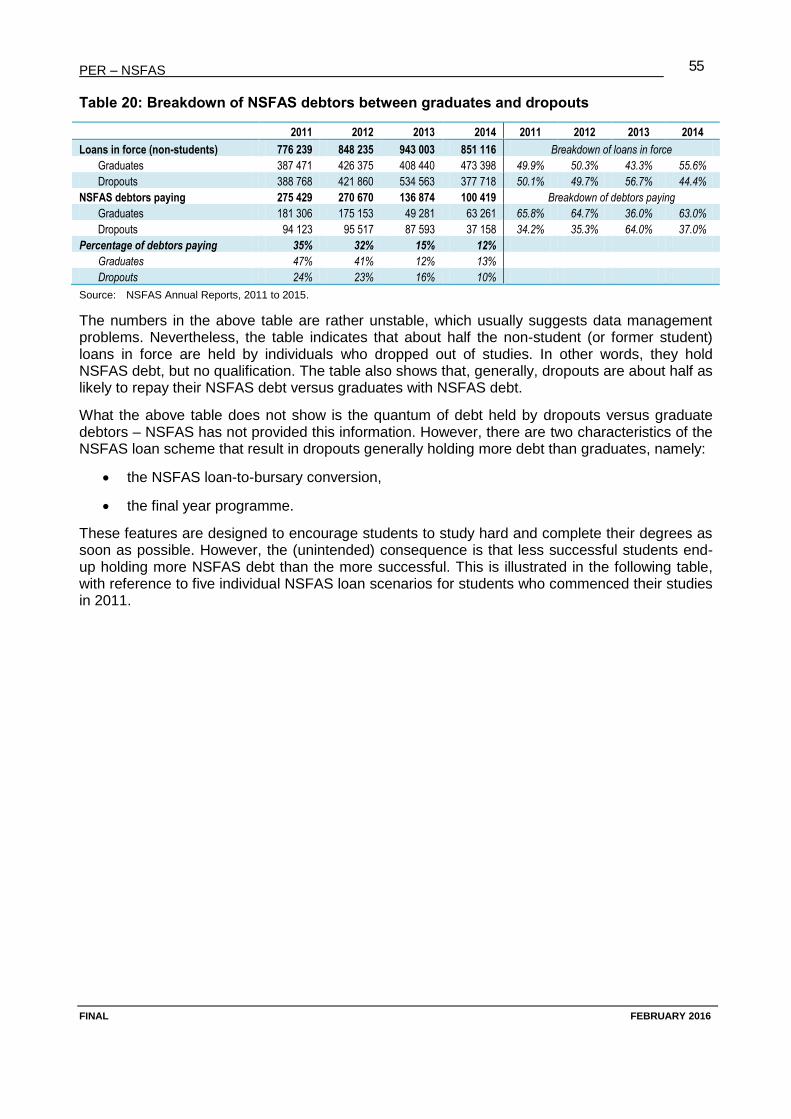

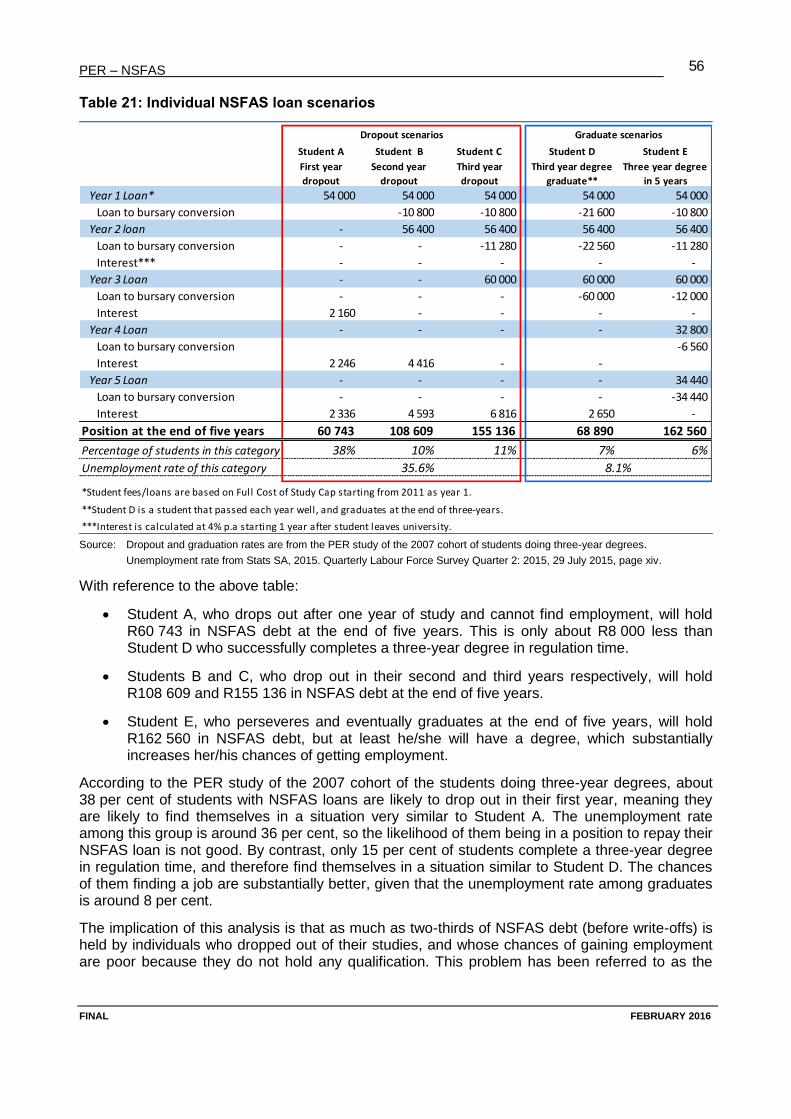

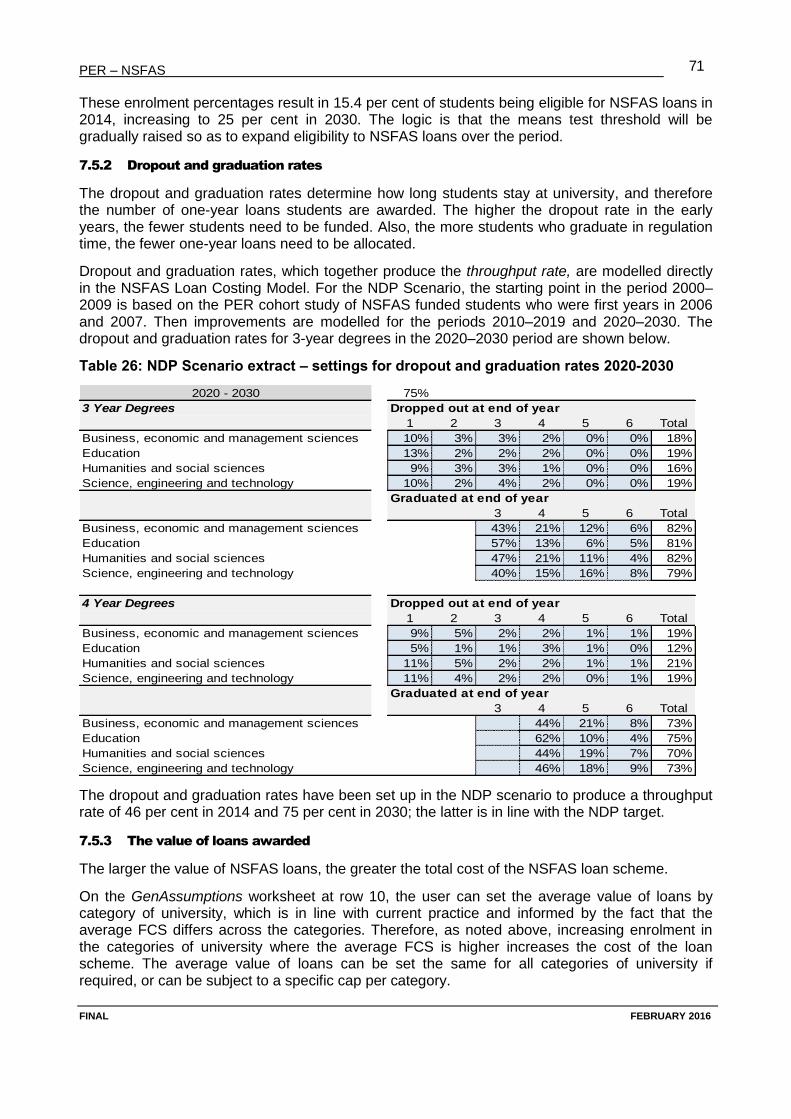

4.2 CHANGING ENROLMENTS IN THE DIFFERENT FIELDS OF STUDY ...................................................................................... 20 4.3 DROPOUT AND GRADUATION RATES ....................................................................................................................... 21

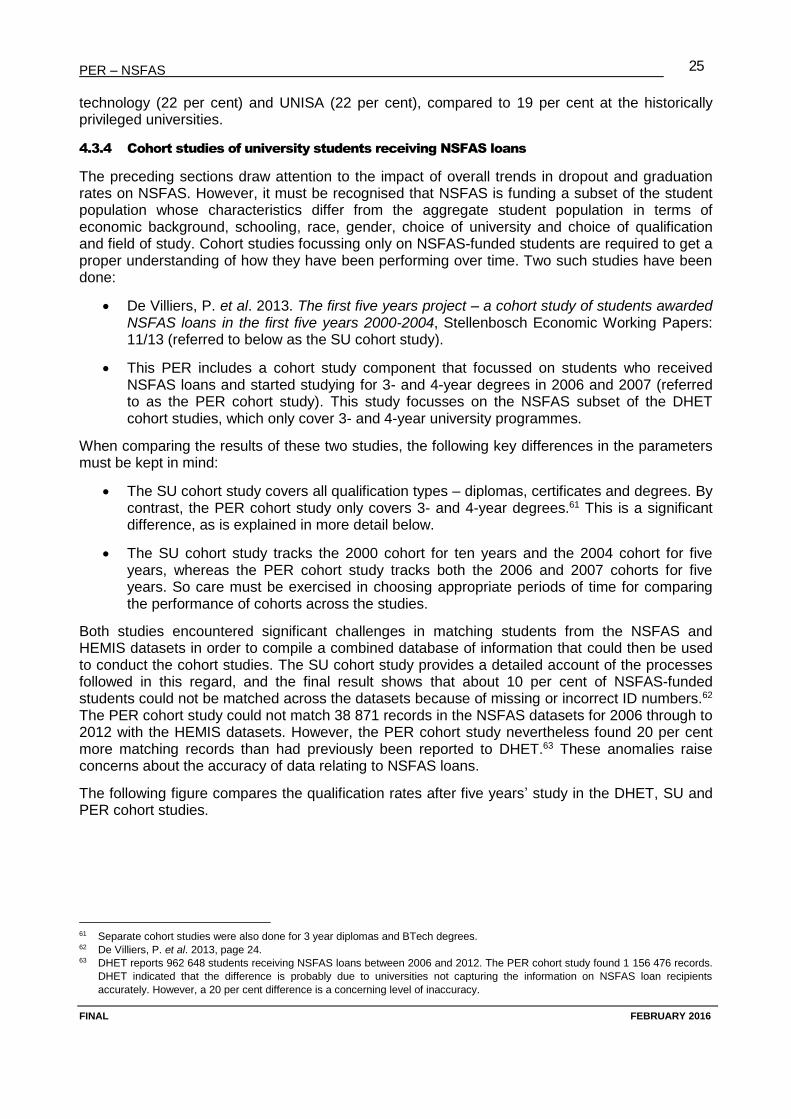

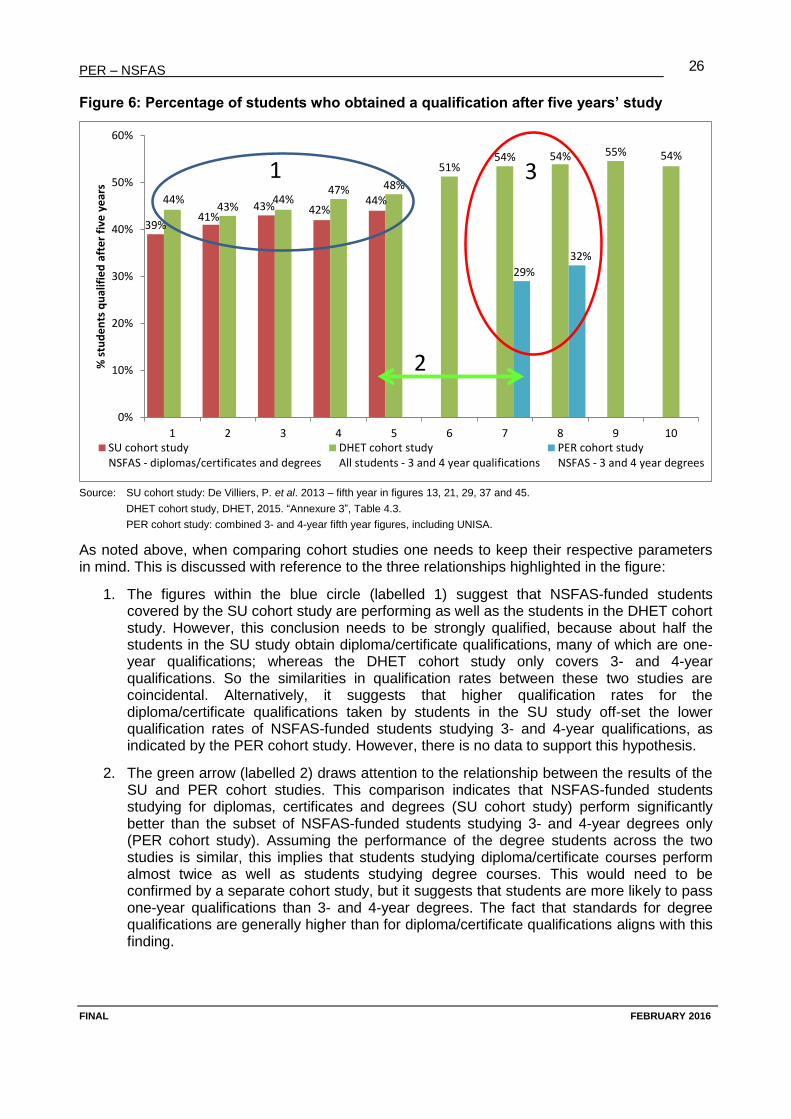

4.3.1 Overall dropout and graduation rates of university students ................................................................... 22 4.3.2 Dropout and graduation rates of university students by race and gender ............................................... 23 4.3.3 Dropout and graduation rates by university ............................................................................................. 24 4.3.4 Cohort studies of university students receiving NSFAS loans .................................................................... 25

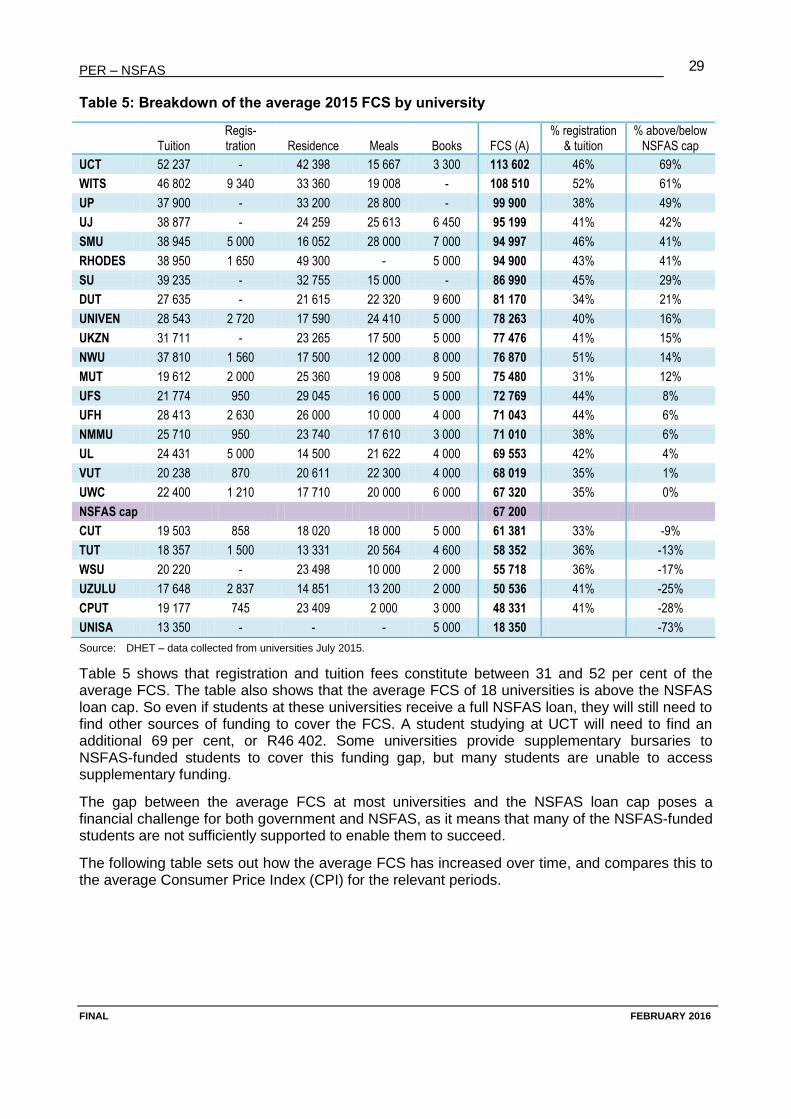

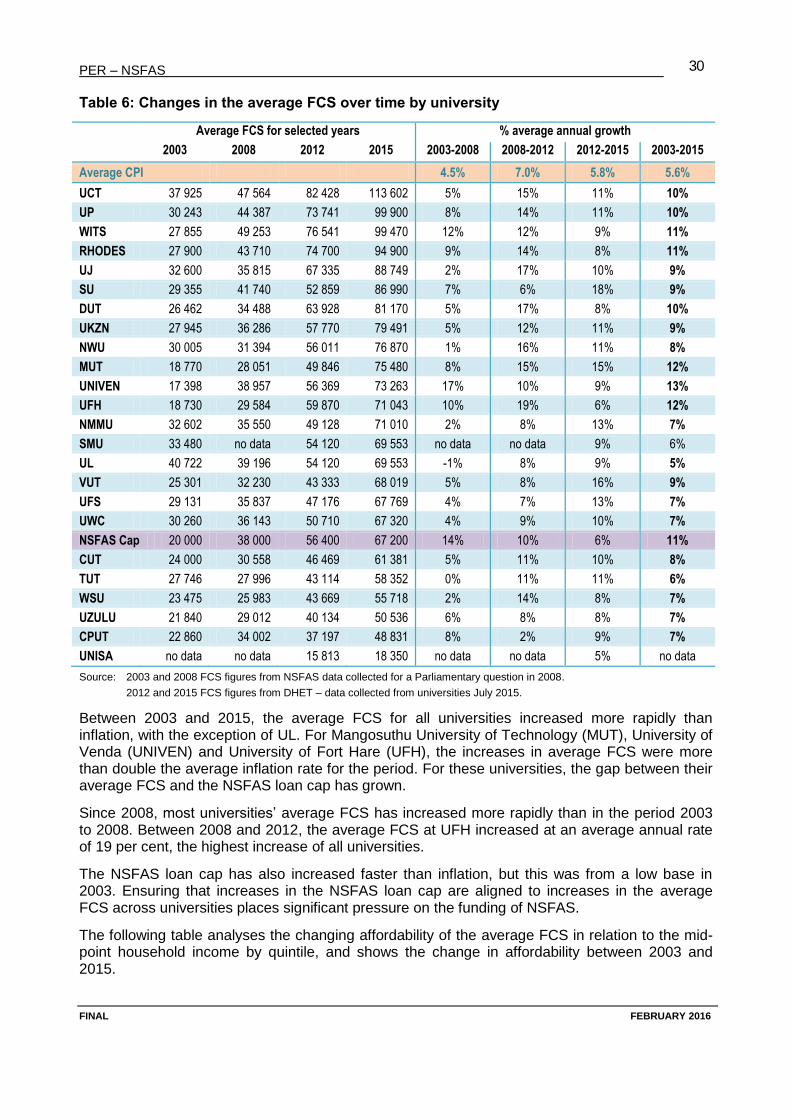

4.4 FULL COST OF STUDY ........................................................................................................................................... 28

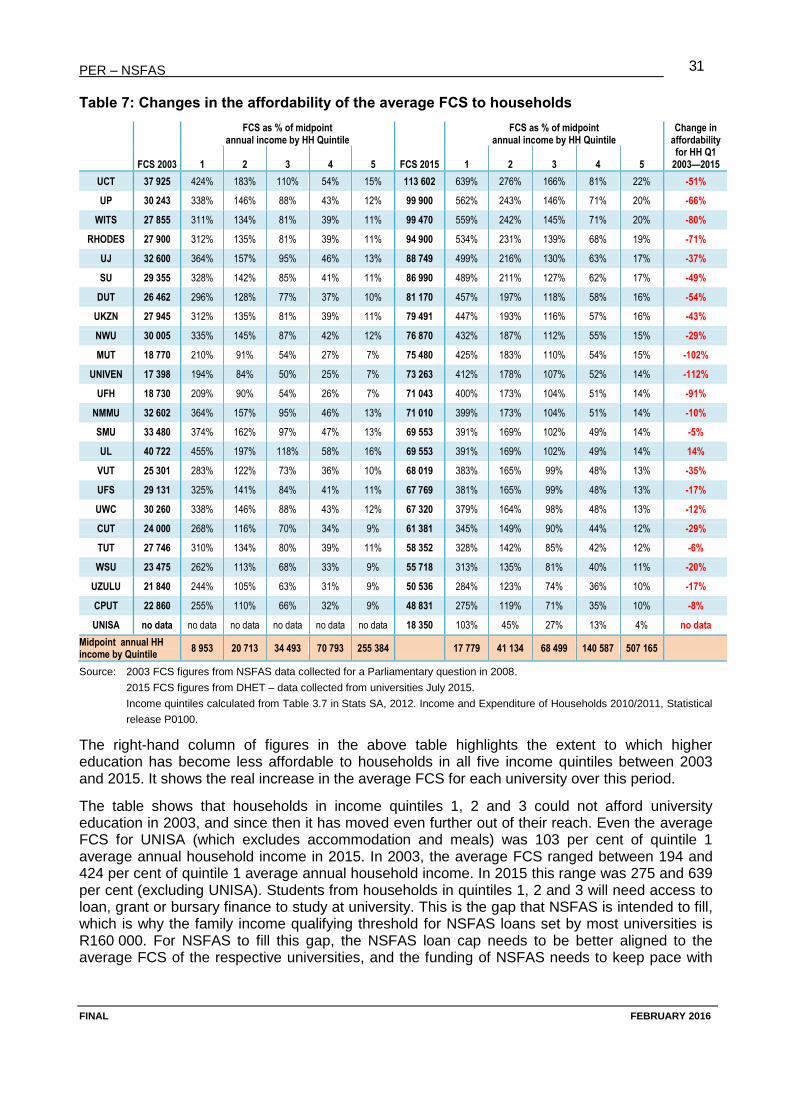

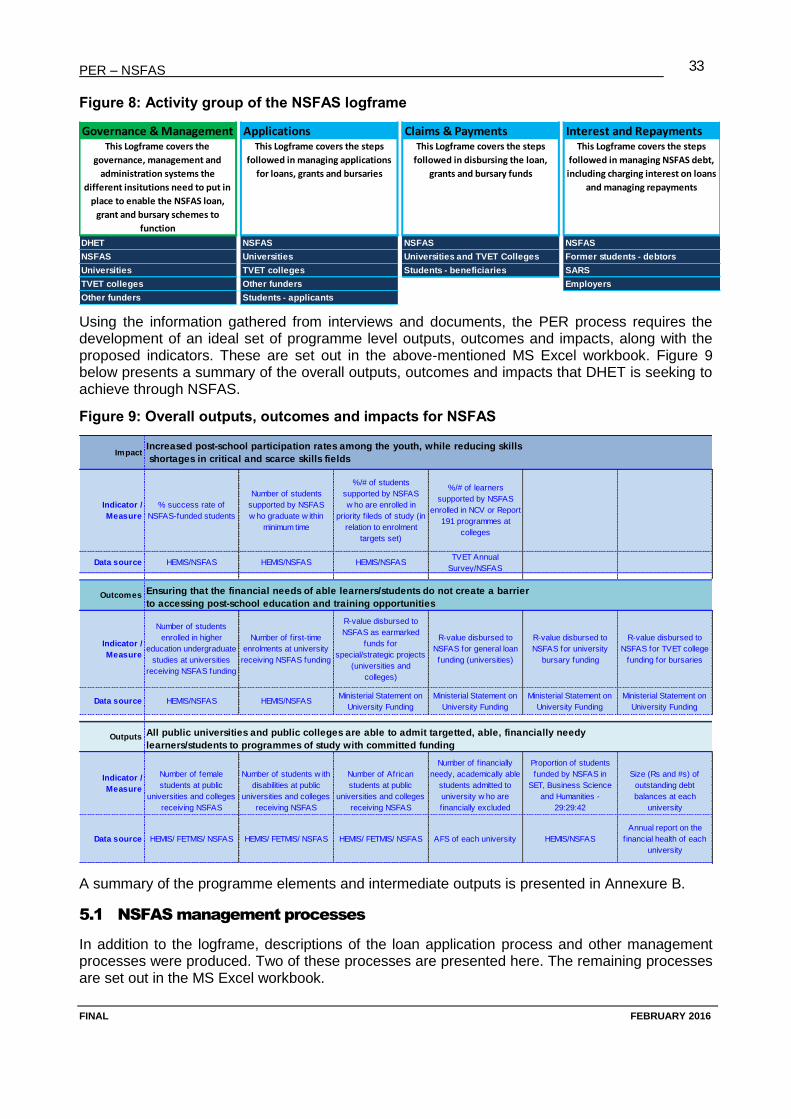

5. PROGRAMME ANALYSIS OF NSFAS PROCESSES .............................................................................................. 32

5.1 NSFAS MANAGEMENT PROCESSES ........................................................................................................................ 33 5.2 KEY FINDINGS OF THE PROGRAMME ANALYSIS .......................................................................................................... 35

6. FINANCIAL AND PERFORMANCE ANALYSIS OF NSFAS .................................................................................... 36

6.1 THE STRUCTURE OF NSFAS FINANCES AND FINANCIAL REPORTING ............................................................................... 36 6.2 NSFAS FUNDING SOURCES .................................................................................................................................. 39 6.3 NSFAS ADMINISTRATIVE INCOME AND EXPENDITURE ................................................................................................ 40 6.4 NSFAS ALLOCATION OF LOANS AND DISBURSEMENT OF GRANTS AND BURSARIES ............................................................ 42 6.5 FINANCIAL ANALYSIS OF THE NSFAS LOAN SCHEME .................................................................................................. 46

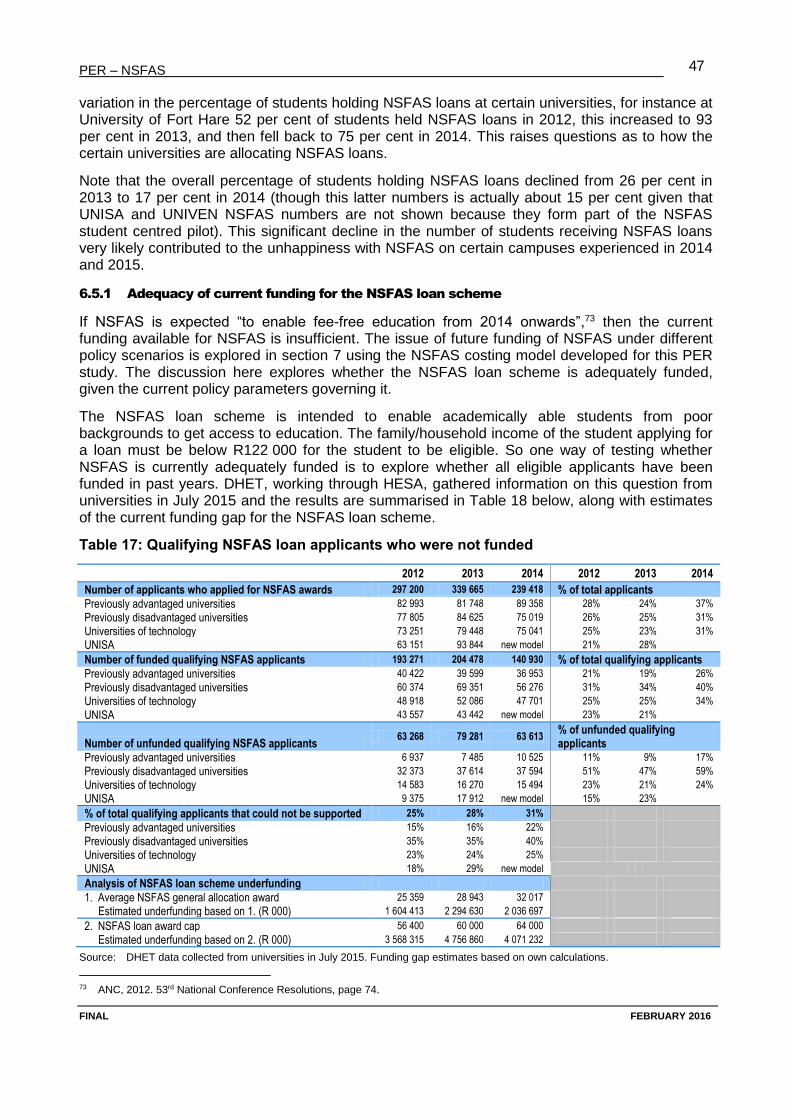

6.5.1 Adequacy of current funding for the NSFAS loan scheme ......................................................................... 47 6.5.2 The conversion of NSFAS loans to bursaries and the final year programme ............................................ 49 6.5.3 Performance of NSFAS loan recoveries ..................................................................................................... 50 6.5.4 The poor quality of NSFAS debt ................................................................................................................ 54

6.6 KEY FINDINGS FROM THE FINANCIAL ANALYSIS .......................................................................................................... 57

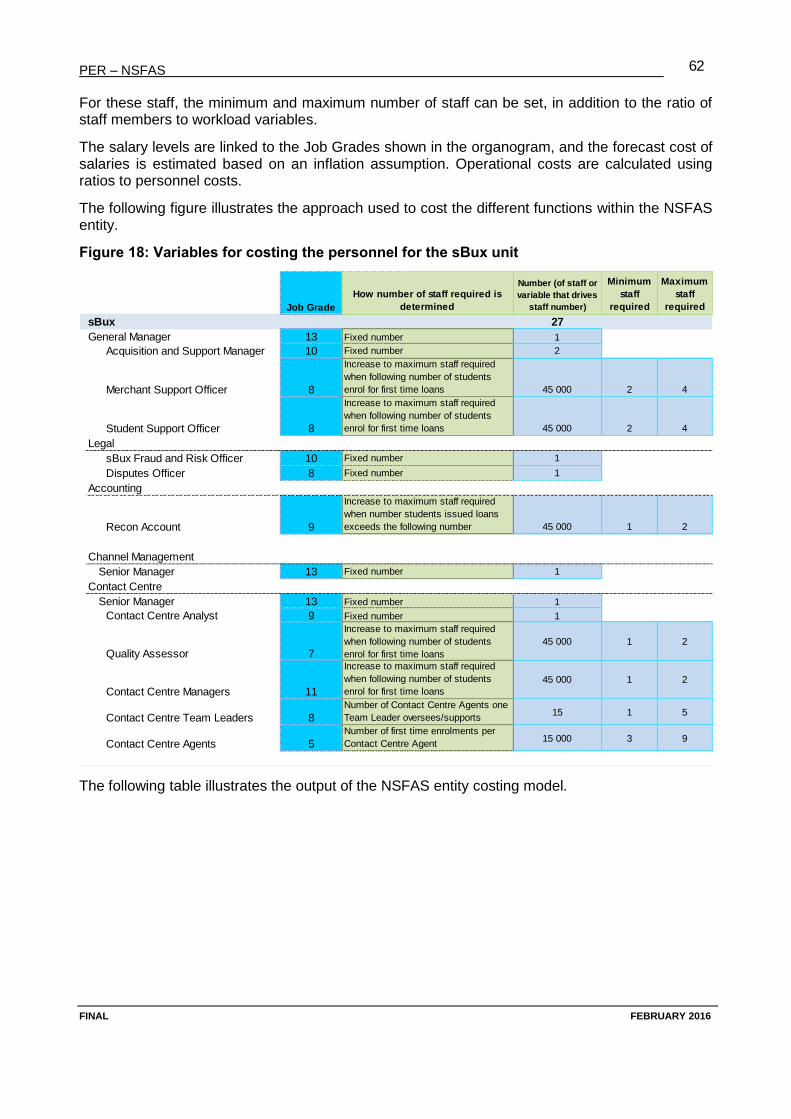

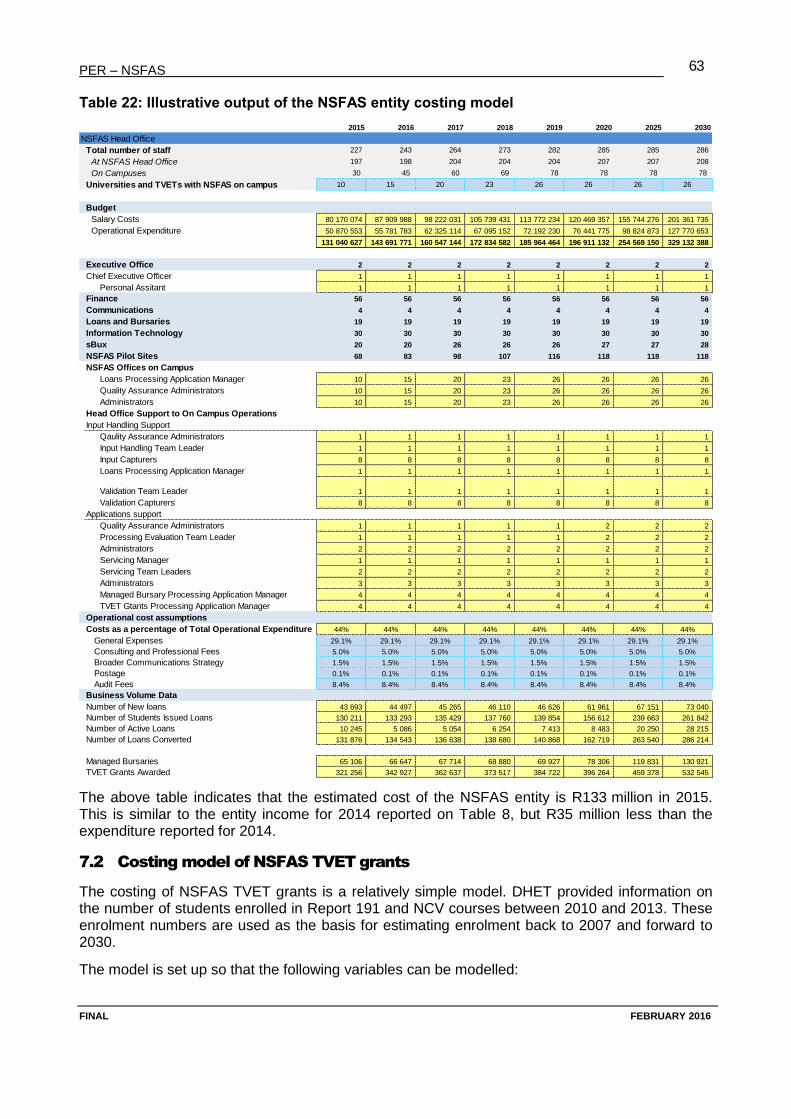

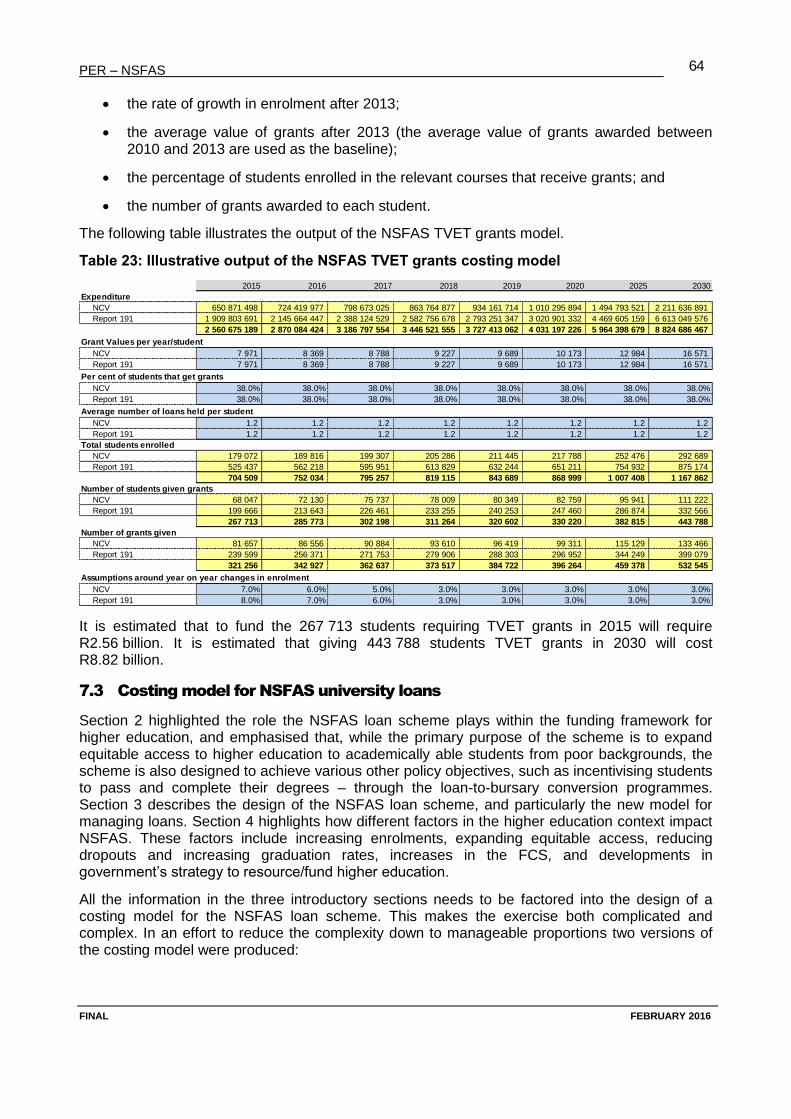

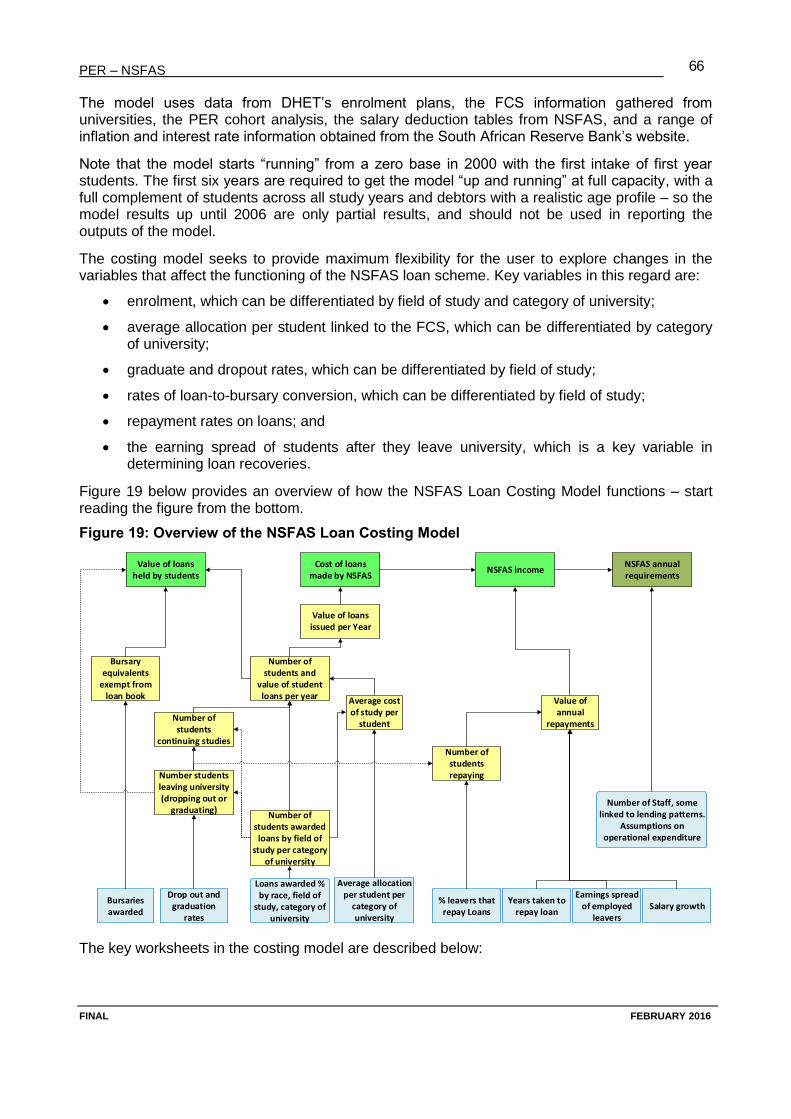

7. COSTING MODELS .......................................................................................................................................... 61

7.1 COSTING MODEL FOR NSFAS THE ENTITY ............................................................................................................... 61 7.2 COSTING MODEL OF NSFAS TVET GRANTS............................................................................................................. 63 7.3 COSTING MODEL FOR NSFAS UNIVERSITY LOANS ..................................................................................................... 64

7.3.1 Calibrating the models against reality ...................................................................................................... 65

PER – NSFAS

FINAL FEBRUARY 2016

ii

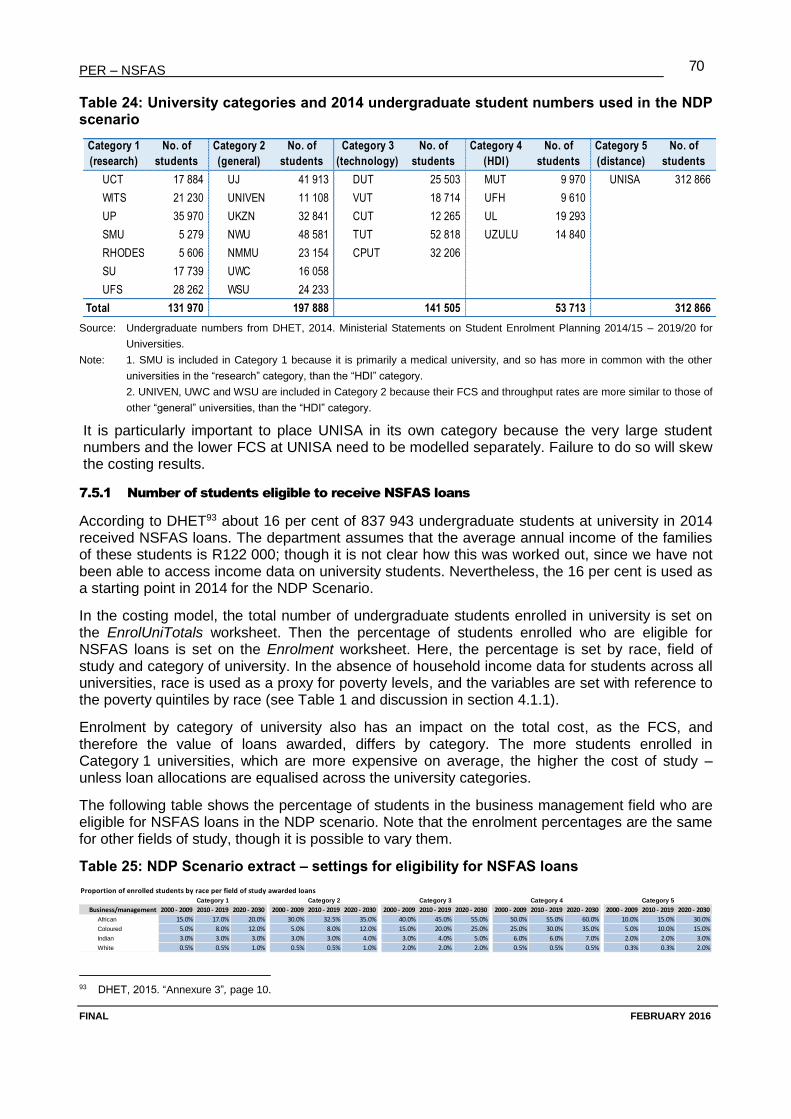

7.4 THE NSFAS LOAN COSTING MODEL – THE FULL AND COMPLICATED COSTING MODEL ..................................................... 65 7.5 THE NSFAS LOAN COSTING MODEL – CALIBRATING THE NDP SCENARIO ..................................................................... 69

7.5.1 Number of students eligible to receive NSFAS loans ................................................................................. 70 7.5.2 Dropout and graduation rates .................................................................................................................. 71 7.5.3 The value of loans awarded ...................................................................................................................... 71 7.5.4 NSFAS loan-to-bursary conversions .......................................................................................................... 73 7.5.5 NSFAS debtors repaying their loans .......................................................................................................... 73 7.5.6 Income tables for debt repayments .......................................................................................................... 74

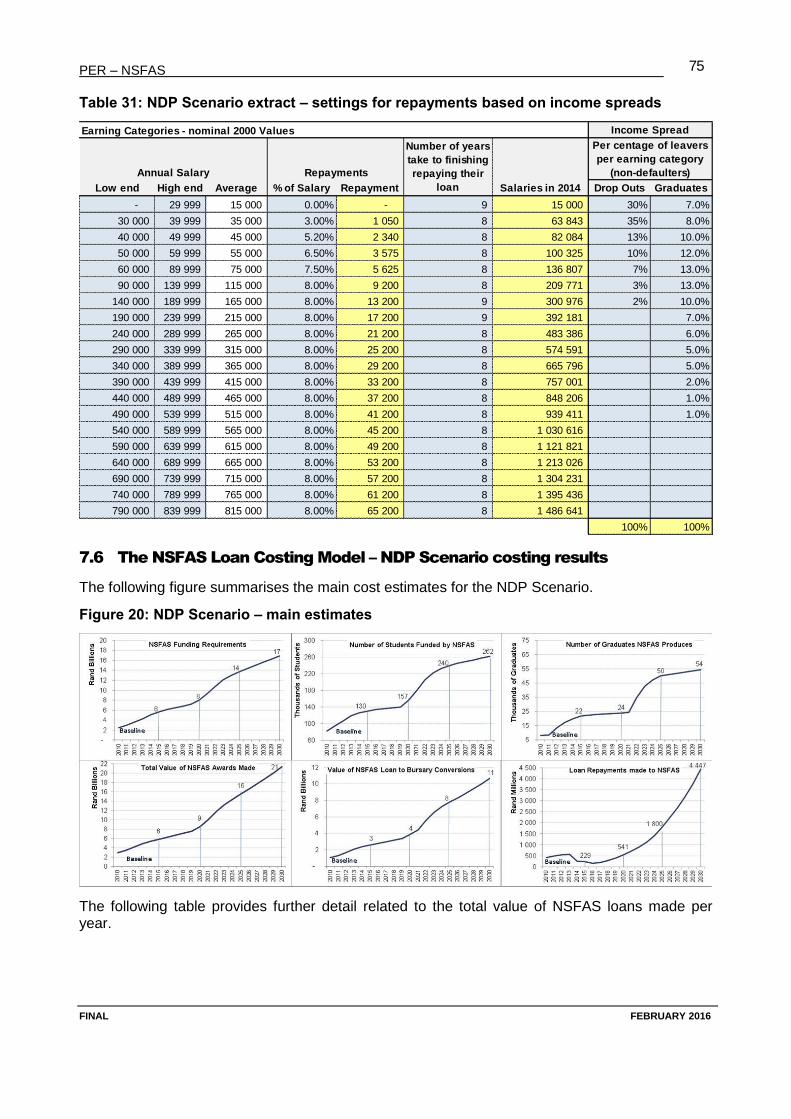

7.6 THE NSFAS LOAN COSTING MODEL – NDP SCENARIO COSTING RESULTS ..................................................................... 75 7.7 EXPLORING THE IMPACT OF THREE KEY NSFAS VARIABLES .......................................................................................... 79

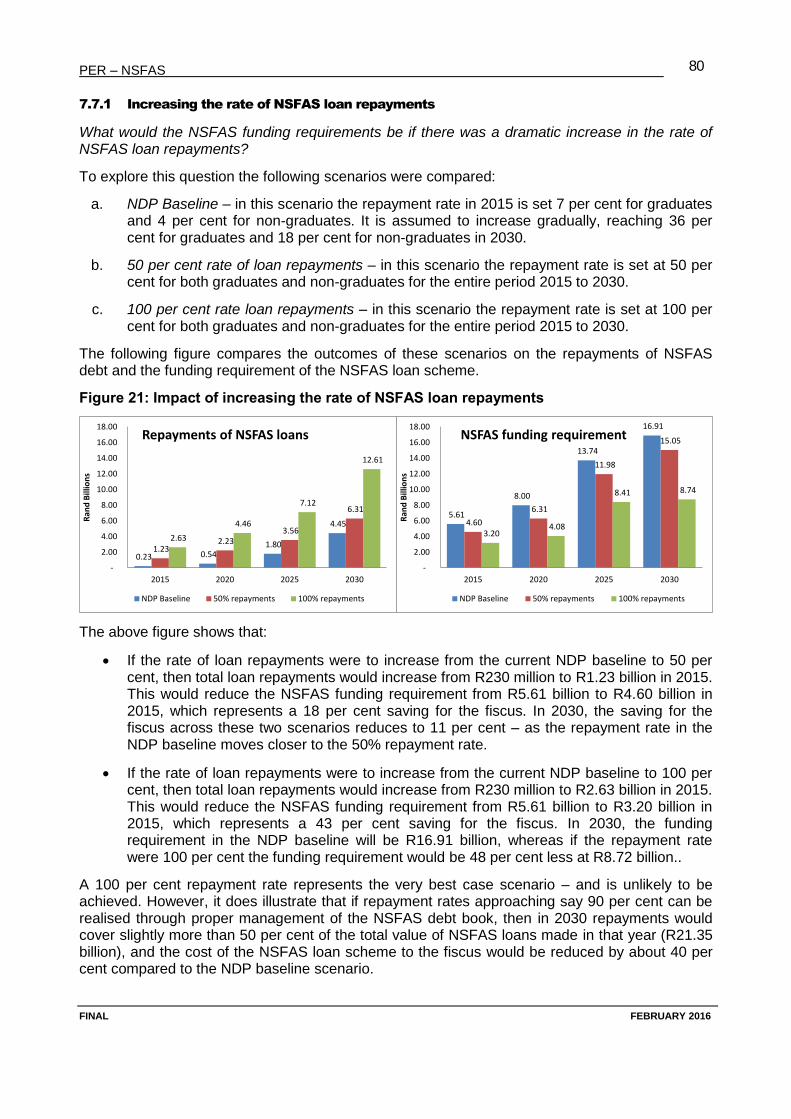

7.7.1 Increasing the rate of NSFAS loan repayments ......................................................................................... 80 7.7.2 Reducing NSFAS loan-to-bursary conversions ........................................................................................... 81 7.7.3 Increasing the student throughput rate .................................................................................................... 83

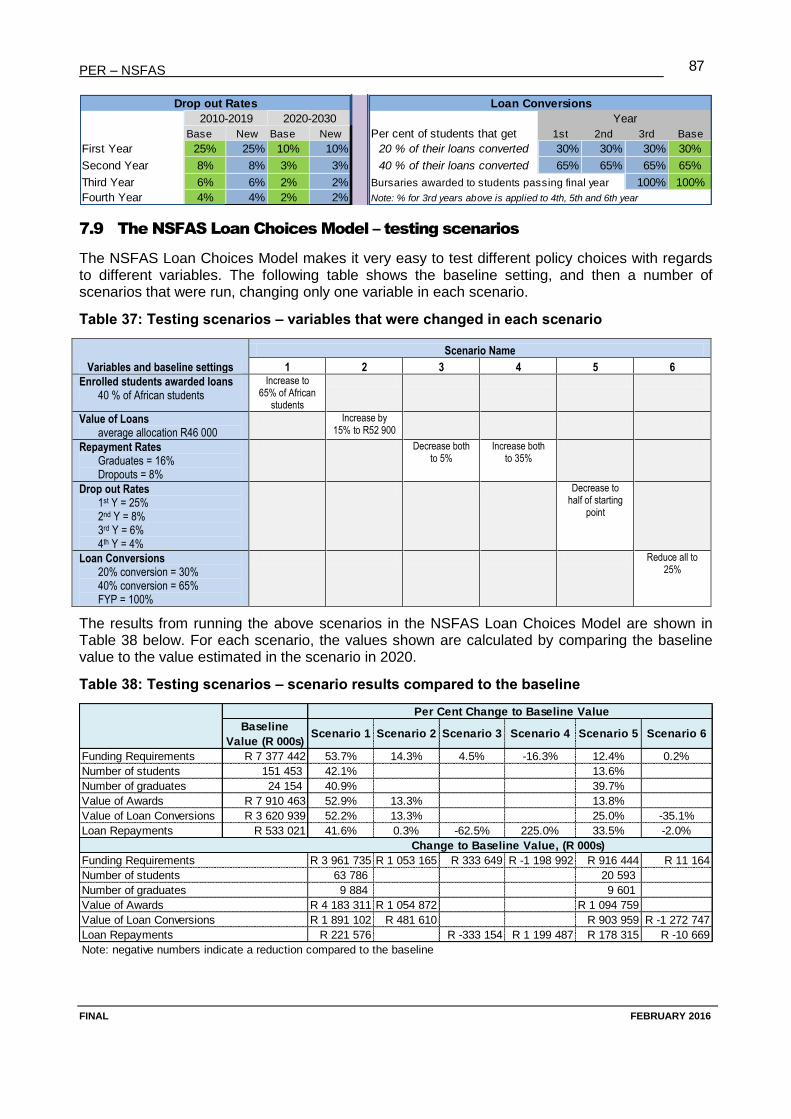

7.8 THE NSFAS LOAN CHOICES MODEL – EASY ACCESS COSTING MODEL ........................................................................... 85 7.9 THE NSFAS LOAN CHOICES MODEL – TESTING SCENARIOS ........................................................................................ 87

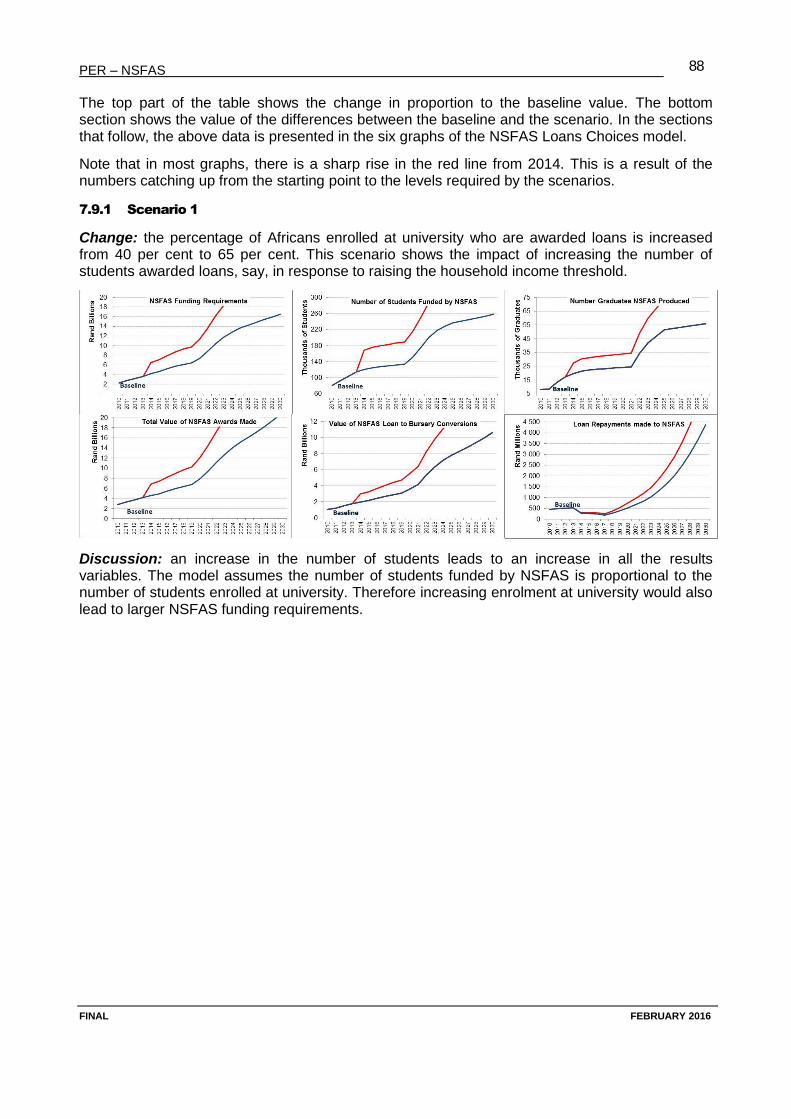

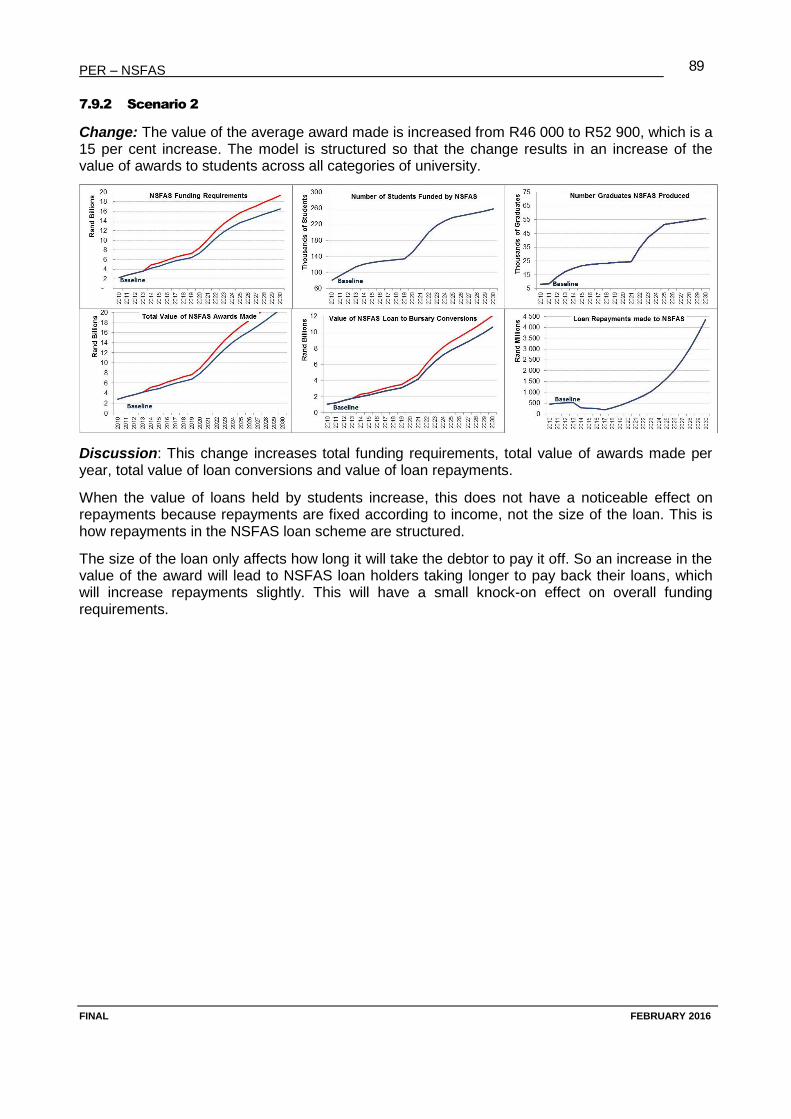

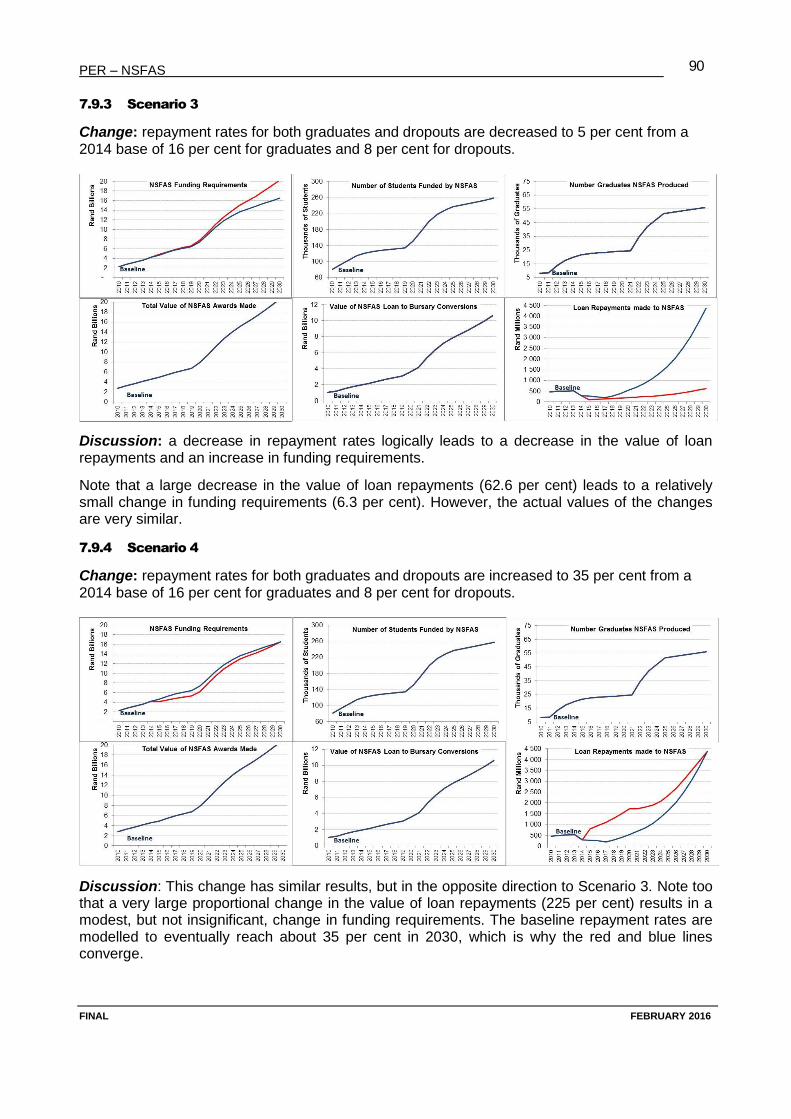

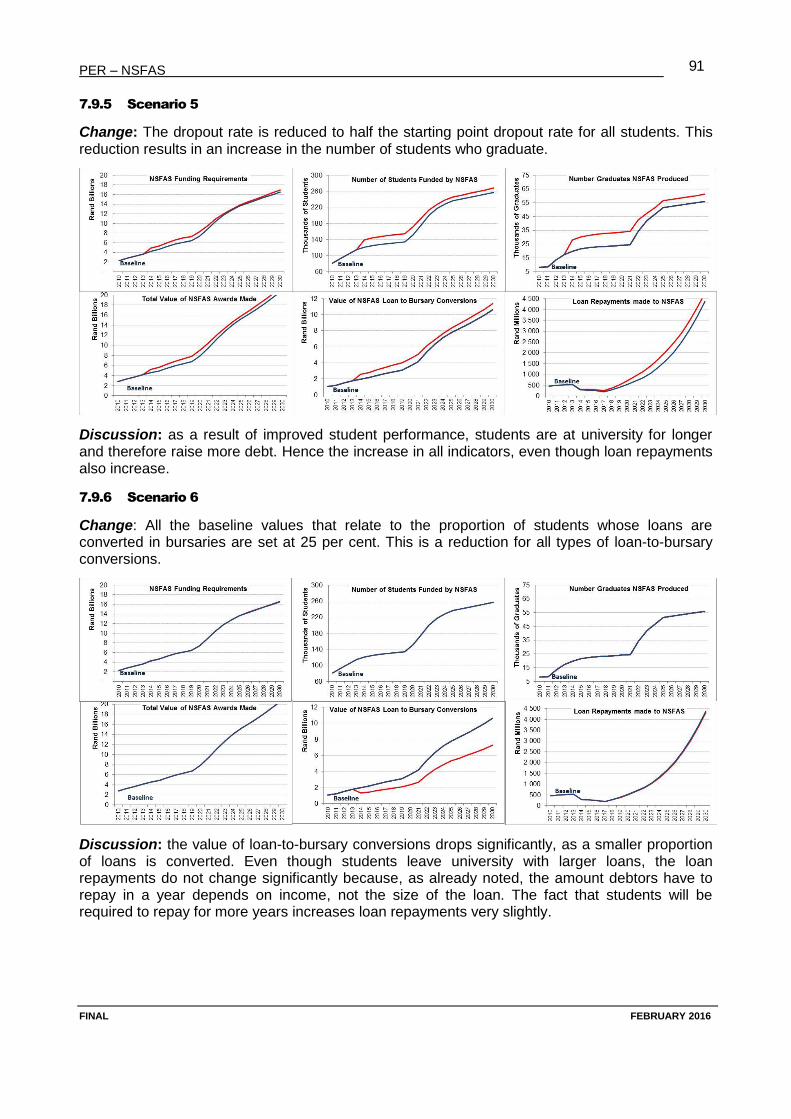

7.9.1 Scenario 1 ................................................................................................................................................. 88 7.9.2 Scenario 2 ................................................................................................................................................. 89 7.9.3 Scenario 3 ................................................................................................................................................. 90 7.9.4 Scenario 4 ................................................................................................................................................. 90 7.9.5 Scenario 5 ................................................................................................................................................. 91 7.9.6 Scenario 6 ................................................................................................................................................. 91

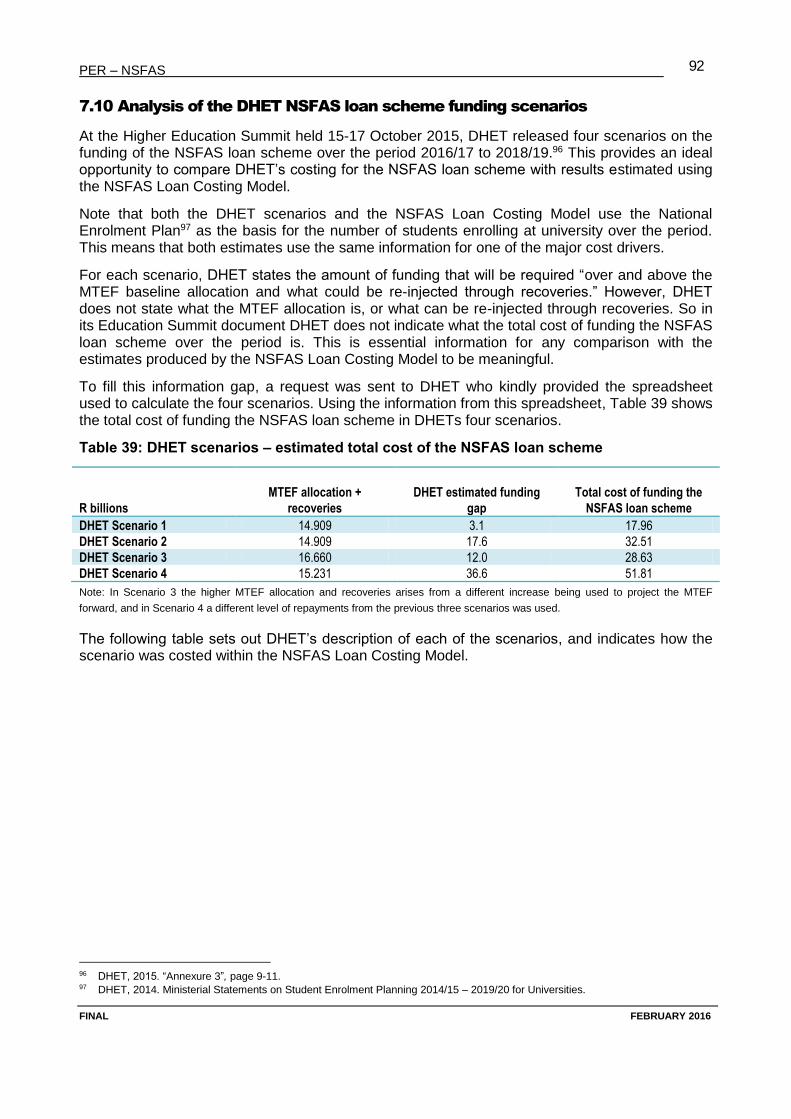

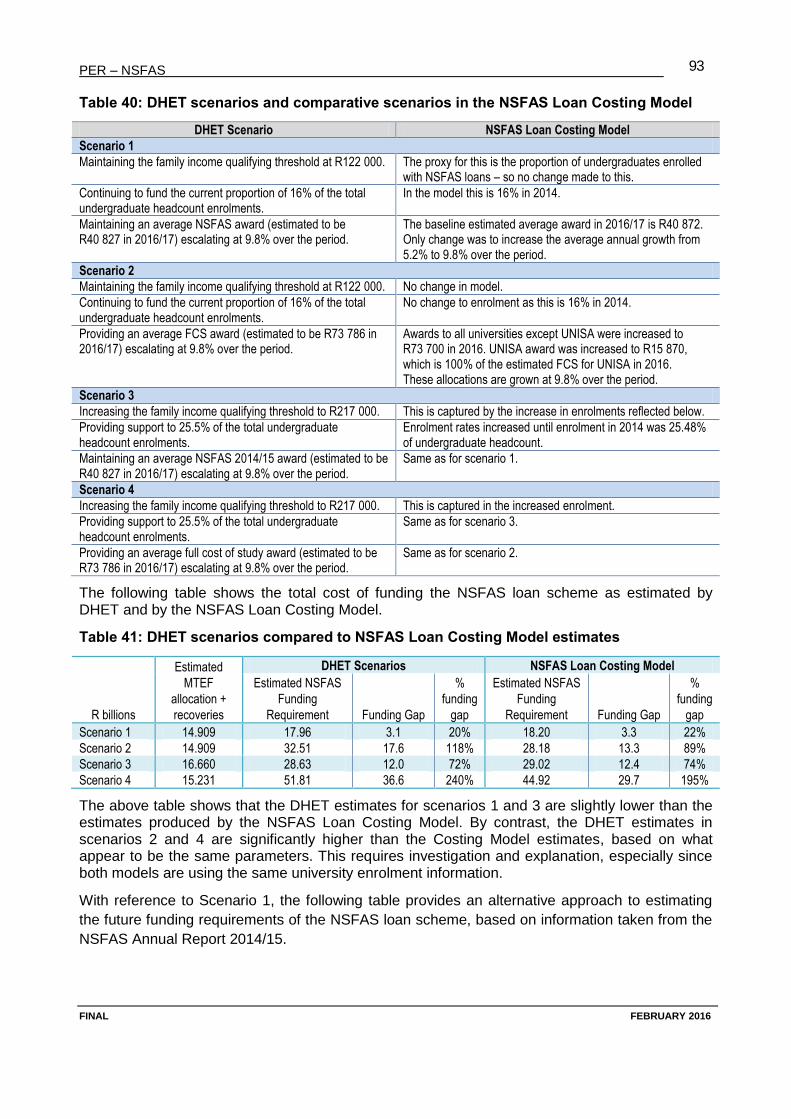

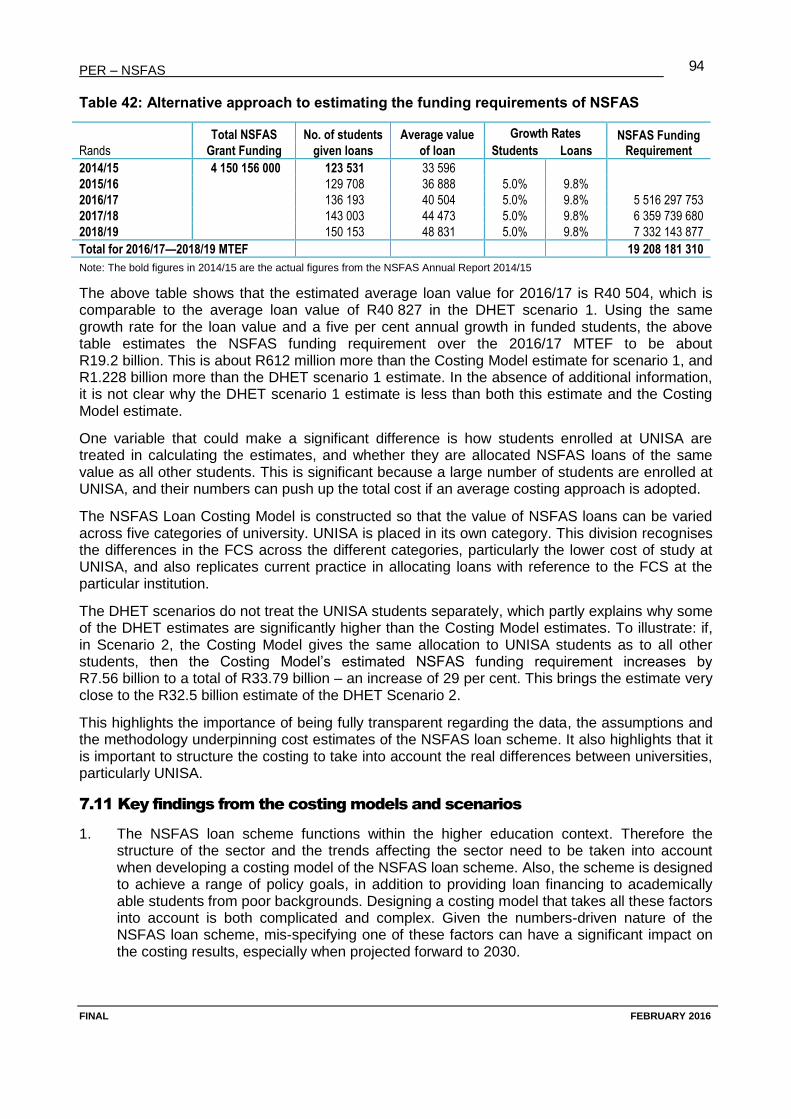

7.10 ANALYSIS OF THE DHET NSFAS LOAN SCHEME FUNDING SCENARIOS ........................................................................... 92 7.11 KEY FINDINGS FROM THE COSTING MODELS AND SCENARIOS ....................................................................................... 94

8. CONCLUSIONS ................................................................................................................................................ 98

ANNEXURE A – NSFAS STUDENT COHORT ANALYSIS ............................................................................................ 101

APPROACH TO DATA ANALYSIS USED FOR THIS PER .............................................................................................................. 101 UNIVERSITY OF STELLENBOSCH’S APPROACH TO DATA ANALYSIS ............................................................................................ 102

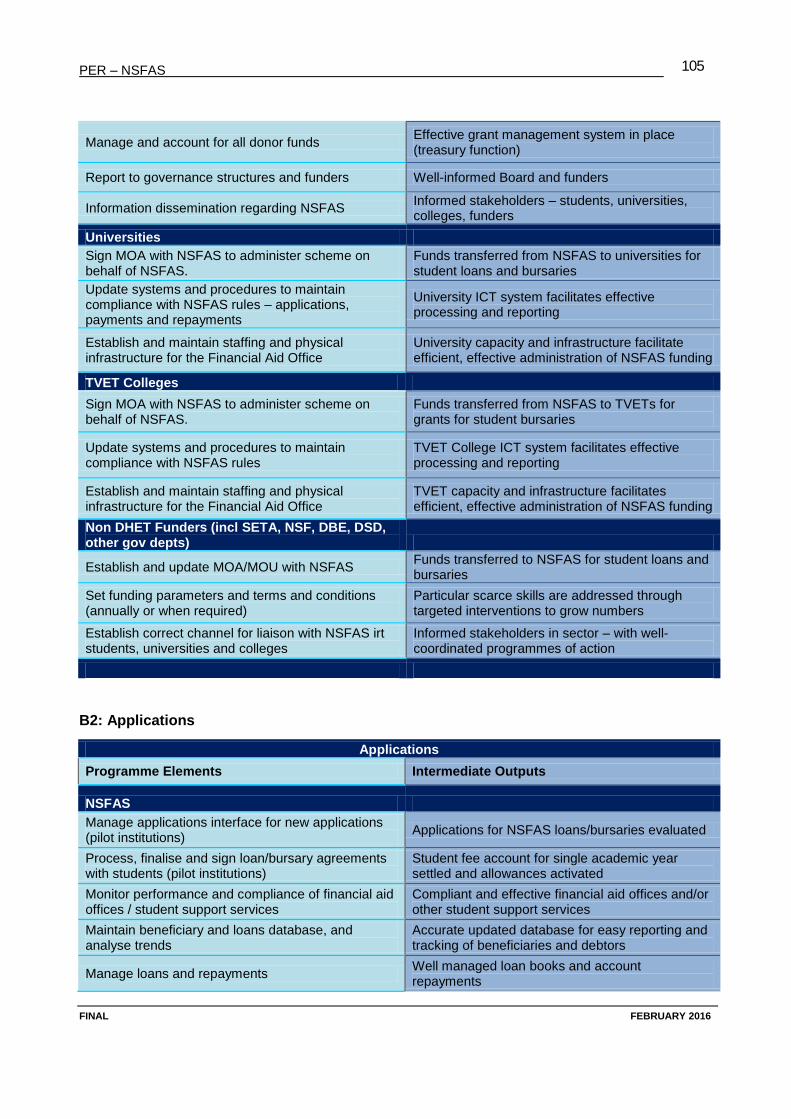

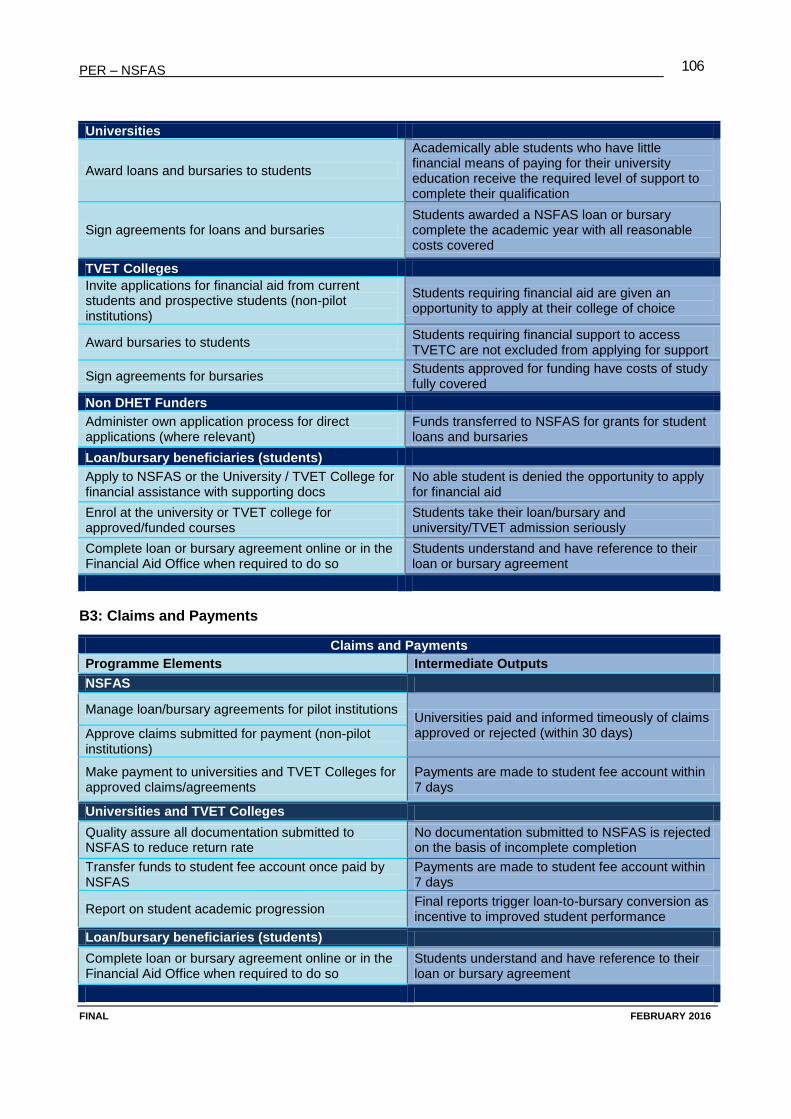

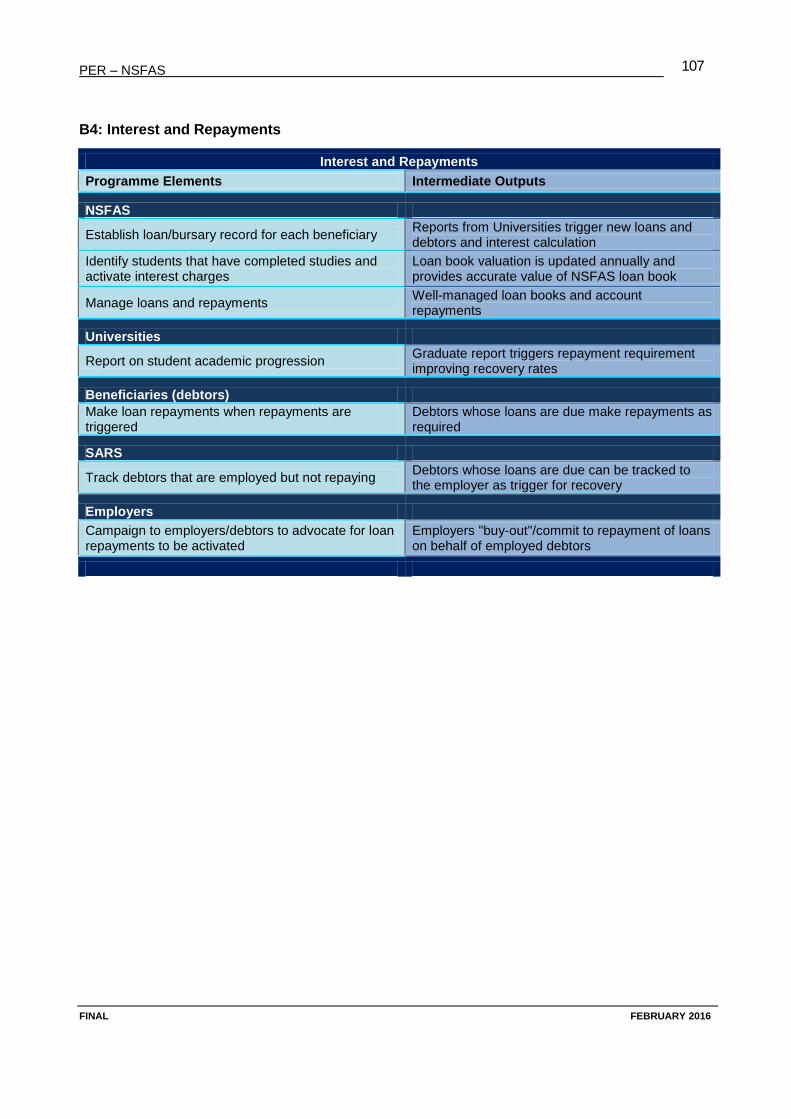

ANNEXURE B – PROGRAMME ELEMENTS AND INTERMEDIATE OUTPUTS ............................................................ 104

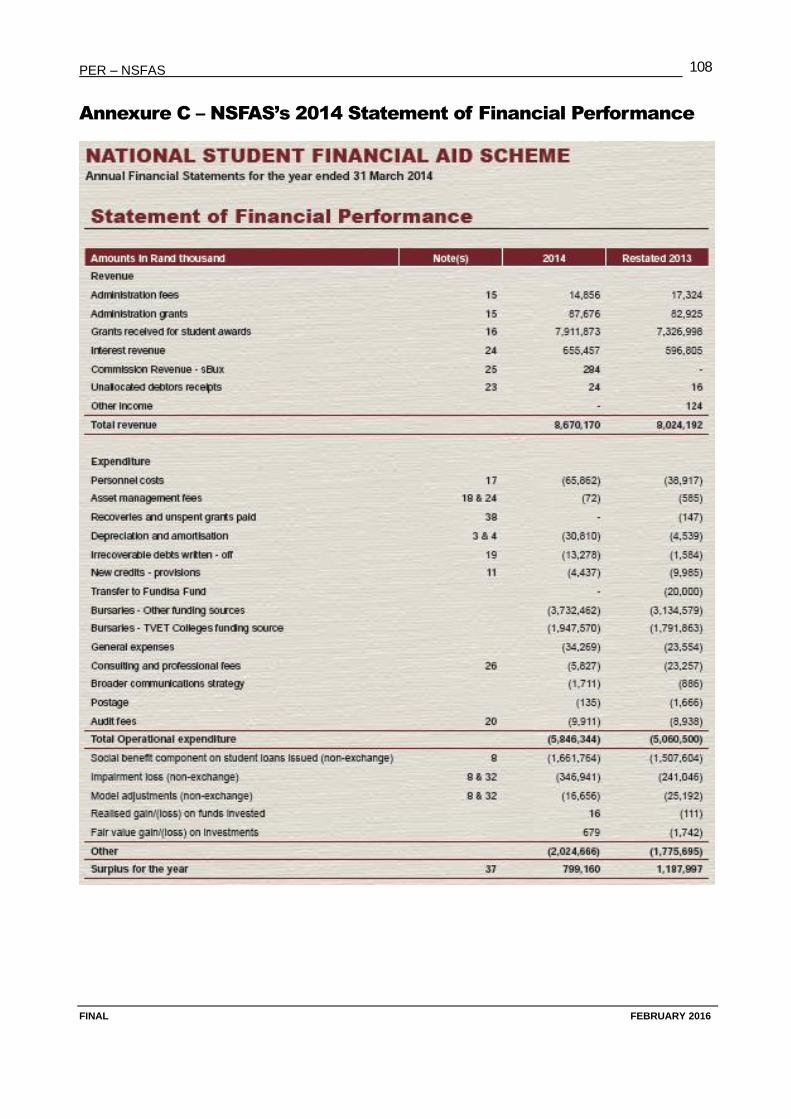

ANNEXURE C – NSFAS’S 2014 STATEMENT OF FINANCIAL PERFORMANCE ........................................................... 108

ANNEXURE D – PEOPLE INTERVIEWED FOR THIS PER............................................................................................ 109

ANNEXURE E – IMPORTANT DOCUMENTS CONSULTED FOR THIS PER .................................................................. 110

ANNEXURE F – UCT’S BURSARY PARAMETERS AND POLICY FOR 2013 .................................................................. 111

PER – NSFAS

FINAL FEBRUARY 2016

1

List of abbreviations

AFS Annual Financial Statement

CESM Classification of Education Subject Material

CPI Consumer Price Index

DBE Department of Basic Education

DHET Department of Higher Education and Training

DSD Department of Social Development

EFC Expected Family Contribution

EFT Electronic Funds Transfer

EMIS Education Management Information System

FCS Full Cost of Study

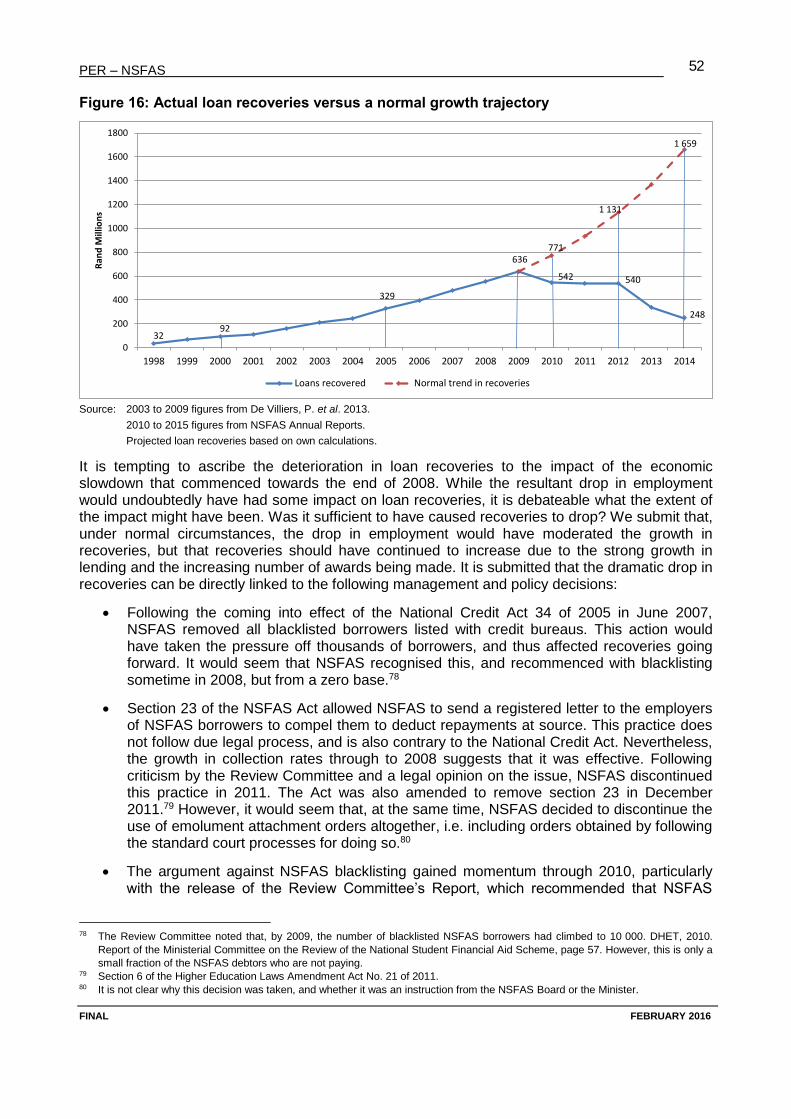

FTE Full Time Equivalent

HDI Historically Disadvantaged Institutions

HEI Higher Education Institutions

HEMIS Higher Education Management Information System

LAF Loan Agreement Form

MOA Memorandum of Agreement

MOU Memorandum of Understanding

NCV National Certificate Vocational

NDP National Development Plan 2030

NMT National Means Test

NRF National Research Foundation

NSF National Skills Fund

NSFAS National Student Financial Aid Scheme

OVC Orphan and Vulnerable Children

PAYE Pay As You Earn

PER Performance and Expenditure Review

SARS South African Revenue Service

SASSA South African Social Security Agency

SET Science, Engineering and Technology

SETA Sector Education and Training Authority

SOP Schedule of Particulars

TEFSA Tertiary Education Fund of South Africa

TVET Technical Vocational Education and Training (colleges)

WDS Weighted number of Disadvantaged Students

PER – NSFAS

FINAL FEBRUARY 2016

2

List of universities

CPUT Cape Peninsula University of Technology

CUT Central University of Technology

DUT Durban University of Technology

MUT Mangosuthu University of Technology

NMMU Nelson Mandela Metropolitan University

NWU North West University

Rhodes Rhodes University

SMU Sefako Makgatho University

SU Stellenbosch University

TUT Tshwane University of Technology

UCT University of Cape Town

UFH University of Fort Hare

UFS University of the Free State

UJ University of Johannesburg

UKZN University of KwaZulu-Natal

UL University of Limpopo

UNISA University of South Africa

UNIVEN University of Venda

UP University of Pretoria

UWC University of the Western Cape

UZULU University of Zululand

VUT Vaal University of Technology

WITS University of the Witwatersrand

WSU Walter Sisulu University

PER – NSFAS

FINAL FEBRUARY 2016

3

1. Introduction

This Performance and Expenditure Review (PER) was commissioned by the National Treasury, working with the Department of Higher Education and Training (DHET) and National Student Financial Aid Scheme (NSFAS). It forms part of a broader initiative to understand the planning, implementation and financing dynamics of some thirty policy initiatives of government. It is envisaged that PER studies such as this will allow for greater value for money in government expenditure and improved implementation of policy initiatives, taking into consideration the objectives of the National Development Plan 2030 (NDP).

1.1 Topic

NSFAS is a large public entity responsible for administering a range of funding programmes to higher education students.

In analysing NSFAS, it is important to distinguish between the administration of NSFAS the entity, and each of the three main streams of student funding NSFAS the entity manages. These distinctions are often not made, which results in a lack of clarity regarding the finances and performance of NSFAS the entity and the funding programmes it manages.

1.2 Purpose and scope

The purpose of this PER is to develop an approach and tools that will enable National Treasury to:

i. understand the costs of the NSFAS administration; and

ii. estimate the optimal funding level for funding the NSFAS loans and Technical Vocational Education and Training (TVET) grants to achieve specific target outcomes.

The target outcomes were not defined in the project terms of reference, but it is understood that they refer to the higher education and training targets set out in the NDP.1 Among these targets, the most important from a NSFAS perspective are:

Increase the throughput rate for degree programmes to more than 75 per cent. The number of graduates will increase from the combined total of 167 469 for private and public higher education institutions to 425 000 by 2030.

Increase the number of masters and PhD students, including by supporting partnerships for research. By 2030, over 25 per cent of university enrolments should be at postgraduate level.

As part of this target, the number of science, technology, engineering and mathematics graduates should increase significantly.

In terms of scope, this PER aims to provide:

a detailed analysis of the organisational and implementation logic of NSFAS, enabling critical performance measures to be developed across all components of the scheme;

an understanding of the current expenditure and financial performance of the NSFAS entity, and each of the funding streams it manages;

a detailed analysis of the cost elements and expenditure drivers of the NSFAS entity and each of the funding streams it manages; and

1 National Development Plan 2030, page 319.

PER – NSFAS

FINAL FEBRUARY 2016

4

proposed improvements for linking policy intent and programmatic design, based on a better understanding of the causal linkages between the higher education environment and NSFAS, and the funding and cost of each of the funding streams managed by NSFAS.

1.3 Key questions

With the above in mind, this project aims to examine the following key questions:

1. What are the costs of administering NSFAS the entity?

2. What are the costs of the NSFAS loan and TVET grant programmes?

3. What is the optimal funding level of the NSFAS loan and TVET grant programmes required to achieve specific target outcomes?

1.4 Information used in conducting the review

Annexures D and E set out the list of the people interviewed and the documents referenced in the course of conducting this study.

1.5 List of documents that make up the review

The project outputs that comprise the review are:

Step 2 and 3 – 2015 02 03 NSFAS PER Step 3 Logframe – Final.xls – sets out a logical framework of NSFAS and presents additional information on the working of the NSFAS loans programme.

Step 4a – a wide range of financial information was analysed, including NSFAS loan data, trial balance information, information on grants to universities, and information from NSFAS’s annual financial statements.

Step 4b – Three MS Excel workbooks cost the different NSFAS components:

2016.02.19 NSFAS Loan Costing Model Final - NDP Scenario.xls – this workbook contains a cost model of the NSFAS entity (administration) and the NSFAS loan scheme.

2015.11.10 NSFAS Loan Choices Model Final.xls – this workbook contains a dashboard users can use to test the impact of different policy choices on the funding needs and performance of the NSFAS loan scheme.

2015.08.14 TVET Grant Model Final.xls – contains a model that costs the TVET grants programme.

Step 5 – 2016.02.23 NSFAS PER Report Final – this report.

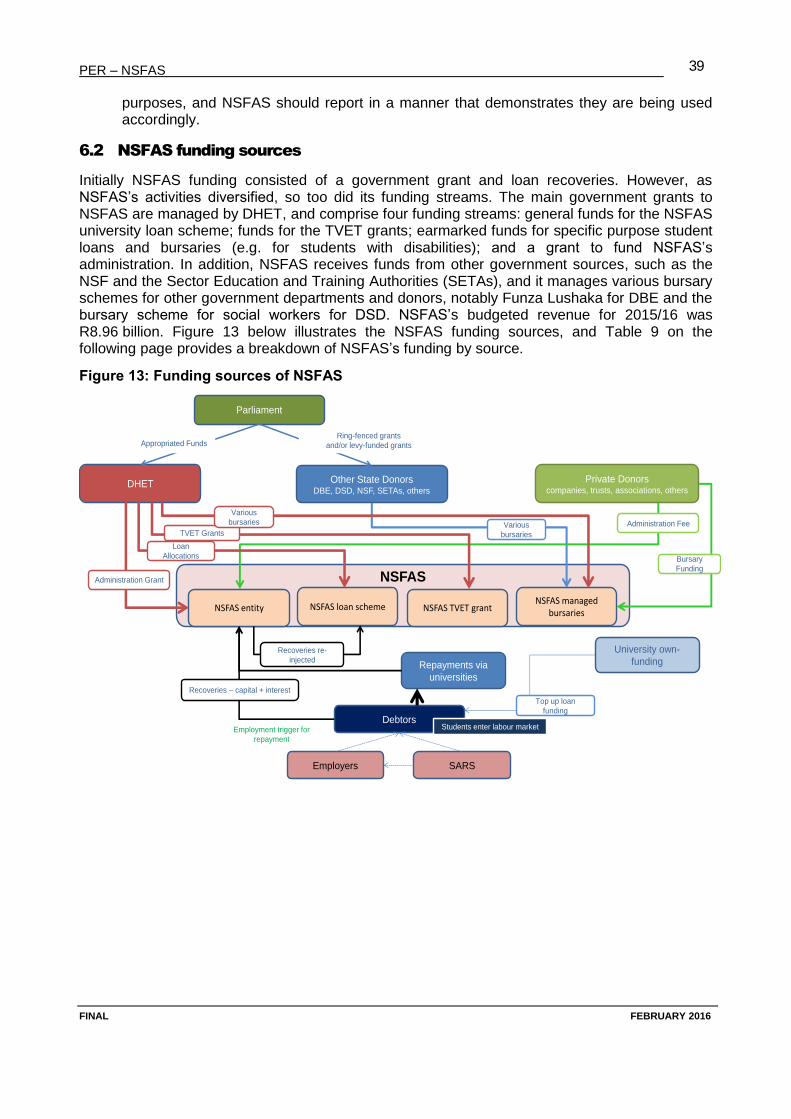

2. Funding framework for higher education

The mechanisms through which governments transfer funds to training institutions are likely to have an important effect on the way in which the funding is used and institutional behaviour.2

2 Ziderman, A. 2001. Financing vocational training to meet policy objectives: sub-Saharan Africa. Human development sector. Africa

Region. World Bank, cited by Sheppard, C. and Ntenga, L. 2013. “Chapter 10: Funding of the South African Further Education and

Training Sector for an Equitable Sharing of National Revenue” in the FFC Submission for 2014/15 Division of Revenue.

PER – NSFAS

FINAL FEBRUARY 2016

5

Consequently, the different components of the higher education funding framework should be designed to serve specific purposes.

The government grants for higher education are structured to achieve particular objectives and incentivise particular behaviours on the part of universities, TVET colleges and students. This is clearly illustrated by the range of earmarked grants, which include the infrastructure grant, clinical training grant, teaching development grant, research development grant, historically disadvantaged institutions (HDI) development grant, and the veterinary sciences grant. It also explains why government funding for NSFAS does not flow directly to universities and TVET colleges: rather it is transferred to NSFAS, which acts as an intermediary to ensure the funding is allocated in line with the objective of expanding access to higher education for academically able students from poor backgrounds.

National Treasury and the DHET have commissioned a separate PER to review the entire funding framework for higher education, which will examine whether the different components of the funding framework are fit for purpose, encouraging internal efficiency, and strengthening demand-driven training and research.

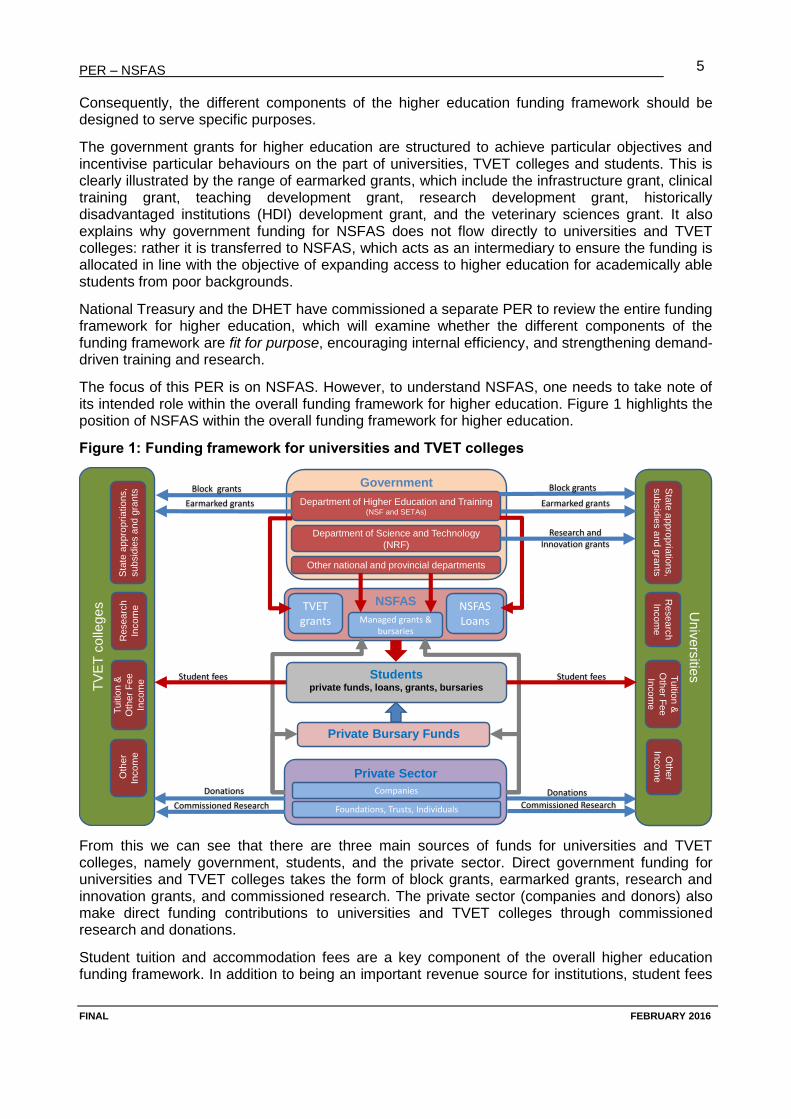

The focus of this PER is on NSFAS. However, to understand NSFAS, one needs to take note of its intended role within the overall funding framework for higher education. Figure 1 highlights the position of NSFAS within the overall funding framework for higher education.

Figure 1: Funding framework for universities and TVET colleges

From this we can see that there are three main sources of funds for universities and TVET colleges, namely government, students, and the private sector. Direct government funding for universities and TVET colleges takes the form of block grants, earmarked grants, research and innovation grants, and commissioned research. The private sector (companies and donors) also make direct funding contributions to universities and TVET colleges through commissioned research and donations.

Student tuition and accommodation fees are a key component of the overall higher education funding framework. In addition to being an important revenue source for institutions, student fees

Un

ive

rsitie

s

Government

Studentsprivate funds, loans, grants, bursaries

Department of Higher Education and Training(NSF and SETAs)

Private Sector

NSFAS

Tuitio

n &

Oth

er F

ee

Incom

e

Sta

te a

ppro

pria

tions,

subsid

ies a

nd g

rants

Researc

h

Incom

e

Department of Science and Technology

(NRF)

Other national and provincial departments

Private Bursary Funds

TVET grants

NSFAS LoansManaged grants &

bursaries

Oth

er

Incom

e

TV

ET

co

lleg

es

Sta

te a

ppro

priations,

subsid

ies a

nd g

rants

Tuitio

n &

Oth

er

Fee

Incom

e

Re

se

arc

h

Incom

e

Oth

er

Incom

e

Earmarked grants

Block grants

Research and Innovation grants

Commissioned Research

Student fees

Donations

Earmarked grants

Block grants

Student fees

Donations

Commissioned Research

Companies

Foundations, Trusts, Individuals

PER – NSFAS

FINAL FEBRUARY 2016

6

serve a number of other purposes. They serve as an incentive for students not to waste their time at university. They are a mechanism for rationing scarce resources – tuition opportunities and student accommodation. They are a type of tax on wealthier families to fund higher education. It is also appropriate that students be expected to pay for tuition and accommodation because of the private benefits they derive – in the short term, their accommodation and tuition for the year, and in the medium term, a qualification that lays the basis for higher future income-earning potential.

However, the downside of tuition and accommodation fees is that they are an obstacle to students from poor and lower middle class backgrounds wishing to access higher education. This undermines government’s efforts to address poverty, inequality and promote economic development. Therefore, to remove or minimise the “obstacle effect” of these fees, government makes funds available for student loans, grants and bursaries, targeting them at academically able students from poor backgrounds. The majority of these funds are DHET grants to NSFAS, but other departments have also set up various bursary programmes – some of which are managed by NSFAS. From the perspective of universities and TVET colleges, the funds that government allocates to NSFAS loans, TVET grants and other bursary programmes are probably best described as indirect earmarked grants, since most of these funds flow to the institutions via students paying their tuition and accommodation fees. DHET refers to these as second stream incomes for the higher education institutions, which is also a useful description.

As shown, the private sector also makes contributions to NSFAS and private bursary funds that fund students’ tuition and accommodation fees, and other study costs.

2.1 The importance of NSFAS funding to universities and TVET colleges

The government and private sector funds that NSFAS manages do not flow directly to universities and TVET colleges, but they are nevertheless an important indirect source of funding as they flow to them via the students that receive the loans, grants and bursaries.

In 2013, NSFAS allocated R6.7 billion in loans and bursaries to university students. Based on the full cost of study (FCS) information presented in section 4.4 below, we can assume that at least 95 per cent, or R6.4 billion, flowed to the universities in the form of registration, tuition, accommodation and meals fees. NSFAS also allocated R1.95 billion in grants to TVET students, all of which flowed to the TVET colleges in registration, tuition and accommodation/meals fees.

The following figure illustrates the contribution that NSFAS funding makes to the funding of four universities.

PER – NSFAS

FINAL FEBRUARY 2016

7

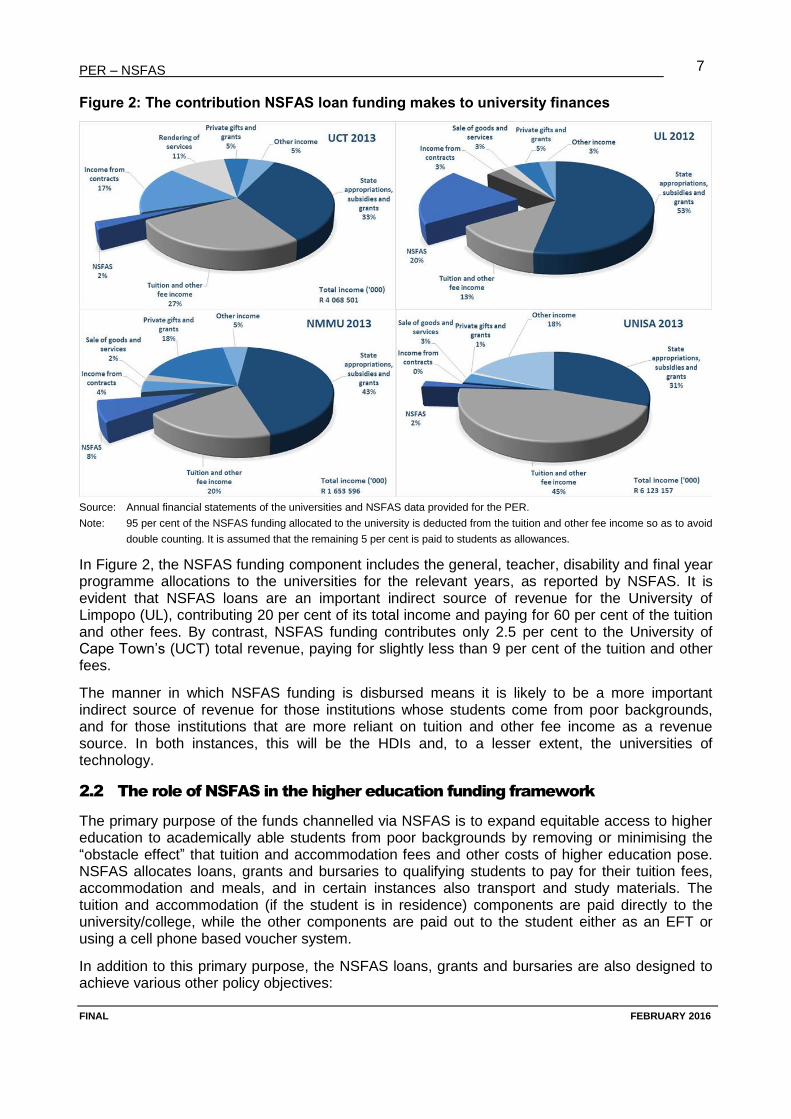

Figure 2: The contribution NSFAS loan funding makes to university finances

Source: Annual financial statements of the universities and NSFAS data provided for the PER.

Note: 95 per cent of the NSFAS funding allocated to the university is deducted from the tuition and other fee income so as to avoid

double counting. It is assumed that the remaining 5 per cent is paid to students as allowances.

In Figure 2, the NSFAS funding component includes the general, teacher, disability and final year programme allocations to the universities for the relevant years, as reported by NSFAS. It is evident that NSFAS loans are an important indirect source of revenue for the University of Limpopo (UL), contributing 20 per cent of its total income and paying for 60 per cent of the tuition and other fees. By contrast, NSFAS funding contributes only 2.5 per cent to the University of Cape Town’s (UCT) total revenue, paying for slightly less than 9 per cent of the tuition and other fees.

The manner in which NSFAS funding is disbursed means it is likely to be a more important indirect source of revenue for those institutions whose students come from poor backgrounds, and for those institutions that are more reliant on tuition and other fee income as a revenue source. In both instances, this will be the HDIs and, to a lesser extent, the universities of technology.

2.2 The role of NSFAS in the higher education funding framework

The primary purpose of the funds channelled via NSFAS is to expand equitable access to higher education to academically able students from poor backgrounds by removing or minimising the “obstacle effect” that tuition and accommodation fees and other costs of higher education pose. NSFAS allocates loans, grants and bursaries to qualifying students to pay for their tuition fees, accommodation and meals, and in certain instances also transport and study materials. The tuition and accommodation (if the student is in residence) components are paid directly to the university/college, while the other components are paid out to the student either as an EFT or using a cell phone based voucher system.

In addition to this primary purpose, the NSFAS loans, grants and bursaries are also designed to achieve various other policy objectives:

PER – NSFAS

FINAL FEBRUARY 2016

8

Recycle funding by requiring students to repay their NSFAS loans once they get employment and earn above a specified income threshold.

Incentivise students to pass – through the loan-to-bursary conversions;

Incentivise students to complete their degrees – the final year loan-to-bursary conversion;

Subsidise priority fields of study: prioritising the allocation of loans to students studying priority courses, targeting the TVET grants to NCV and Report 191 programmes3, and putting in place bursary programmes for specific professions (e.g. teachers and social workers); and

Target specific categories of students, such as those with disabilities.

It is arguable whether these objectives would be achieved through a block grant, or even a direct earmarked grant, to universities and TVET colleges. It is important that the funding be allocated to individual students so as to create a nexus between the student and the funding mechanism, thus creating incentives for the desired behaviour responses – choosing a priority field of study, or working hard to minimise their debt. NSFAS therefore acts as an agent or intermediary for government to ensure the funding is allocated in line with the objectives.

This needs to be kept in mind when analysing the functioning of NSFAS, and particularly when making proposals regarding how the NSFAS entity and the NSFAS loans, TVET grants and the managed bursaries could be better designed or managed.

3. Overview of NSFAS operations

In 1991, the Independent Development Trust established the Tertiary Education Fund of South Africa (TEFSA) as a not-for-profit company to provide loans to students attending higher education institution. The aim was to provide financial aid to poor students, irrespective of race, so that they could access higher education. Recognising the value of this scheme, the government allocated funds for the establishment of NSFAS in 1995 and, because TEFSA already had the necessary infrastructure in place, the government decided to get it to manage the new scheme.

The Education White Paper 3 (1997) endorsed the NSFAS idea, and processes were put in place to formalise its governance arrangements. In 1999, the NSFAS loan scheme was formally established by an Act of Parliament (Act 56 of 1999) and, in 2000, TEFSA was reconstituted as NSFAS (the organisation) – a public entity managed by an executive officer accountable to a Board representing all major stakeholders in higher education, and appointed by the Minister of Higher Education and Training. In addition, there are a number of other role-players involved in the management of the NSFAS loan scheme. Included amongst these are the higher education institutions, which are responsible for managing the loan application and approval processes, and the government entities that contribute funding.

NSFAS is a large public entity, with an administrative budget of about R149 million in 2014, responsible for administering:

the NSFAS loan scheme for university undergraduate students (referred to as “NSFAS loans”);

grants to students at TVET colleges (referred to as “TVET grants”); and

3 The policy document, Formal technical college instructional programmes in the RSA, Report 191 (2001/08), contains the

programme requirements for current technical college education in the Republic of South Africa.

PER – NSFAS

FINAL FEBRUARY 2016

9

a range of other government and private bursary and grants schemes, including the Funza Lushaka Bursary Programme to train teachers (referred to either as “managed bursary/grant programmes” or by the name of the particular bursary/grant programme).

In 2014, NSFAS managed the disbursement of R8.7 billion in loans, bursaries and grants to 416 365 students.4

A word on terminology: loans vs grants vs bursaries

NSFAS administers a range of financial programmes to assist students. Often the terminology used by the

organisation to describe these products is not clear, and results in misunderstandings regarding the nature

of the products. For this PER, we use the following definitions to guide our use of these terms:

A loan is a sum of money lent to a student who meets prescribed requirements. The student is

required to repay the capital and interest on the capital. NSFAS loans have preferential terms, such

as grace periods before interest accrues, and the rate of interest is kept below market values.

A grant is awarded to students who meet prescribed requirements, such as being from a low

income household and having the necessary academic criteria to register for specific qualifications.

A grant does not have to be repaid.

A bursary is awarded to students for good performance. A bursary does not need to be repaid.

However, some bursaries involve a work obligation. A bursary may be awarded up-front for future

studies or, as is the case with NSFAS, a bursary can be awarded retrospectively by converting a

portion of the student’s loan into a bursary.

In many cases, what NSFAS calls a bursary is in fact a grant. It would greatly facilitate discussions if role-

players in the sector were to adopt a consistent approach to naming financial aid products for students in

line with the above definitions.

3.1 The nature of NSFAS operations

Due to the volume of applications, TEFSA used financial aid officers at higher education institutions as local agents for distributing loans. This practice was carried over to NSFAS, and it continues to be a key component of NSFAS operations. NSFAS allocates funds to the institutions for loans and grants. The institutions receive applications for funding from students, assess eligibility, and allocate the loans and grants. They are also responsible for concluding the written loan or grant agreements between the students and NSFAS, and managing the disbursement of the funds to students. They also report to NSFAS on the progress of the funded students.

NSFAS is in the process of introducing a new model, which will shift the responsibility of administering funding from the universities to NSFAS (see further discussion in section 3.2).

Allocation of funds to higher education institutions5

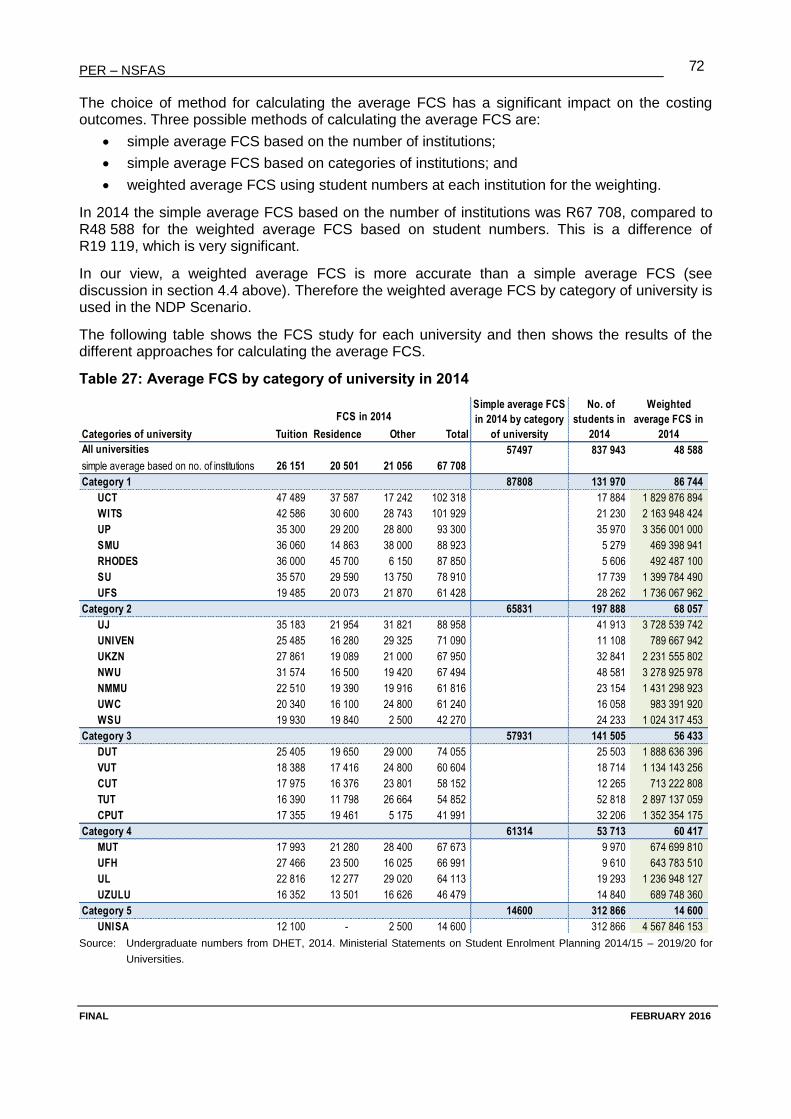

To ensure that the funds for NSFAS loans are equitably divided between the different higher education institutions, the institutional allocations are based on the number of disadvantaged students at the respective institutions, as well as the costs of study (according to study programme) at each institution. The average FCS for all academic programmes at an institution includes registration, tuition, residence and meals. It is not clear whether NSFAS has extended the FCS to cover books and transport as well.6 The weighted number of disadvantaged students (WDS) at each institution is determined using the following formula:

WDS = (FTE enrolled African students × 3) + (FTE enrolled coloured students × 2) + (FTE enrolled Indian students × 1)

4 NSFAS Annual Financial Statements, 2014:53. 5 This description draws on De Villiers, P. et al. 2013, pages 7 and 8. 6 DHET’s position is that the FCS must cover books as well.

PER – NSFAS

FINAL FEBRUARY 2016

10

The WDS and FCS measures for each institution are used to apportion the total NSFAS allocation for a specific financial year between the higher education institutions. The amount that each institution receives is thus solely determined by the racial composition of the students at that institution. However, when allocating NSFAS loans or grants, the institutions do not take race into account. Rather, grants are allocated on the basis of means tests, in which poverty is the main component.

According to NSFAS the above formula was last used in 2011. However, since then the allocations to each university have increased more or less in proportion to the available funding – so in practice the current allocations are still founded on the above race-based formula.

In the new model there is no need for funds to be allocated to institutions, so this allocation process will progressively fall away as the new model is extended to cover more institutions.

3.1.1 Loans for undergraduate study at university (NSFAS loans)

The NSFAS loan scheme is:

a tool government uses to fund/purchase the higher education outcomes the country requires in order to grow the economy and address the challenges of development and inequality;

a scheme for making means-tested allocations to students who meet certain qualifying criteria in order to fund their first qualification at higher education institutions; and

a performance-linked loan and bursary scheme that rewards students who pass their courses or graduate.

Eligibility criteria and means tests

NSFAS has issued guidelines7 for the allocation of NSFAS loans that higher education institutions are expected to follow. These guidelines include:

non-financial eligibility criteria, which include academic criteria;

a National Means Test (NMT) to determine financial eligibility, and the Expected Family Contribution (EFC), issued annually (the majority of universities order the applications according to the EFC and allocate loans from lowest to highest EFC. This means the effective income threshold varies across universities. Some universities set an income threshold of R160 000 as a guide to students making applications); and

a method for calculating the approved cost of study and the NSFAS award.

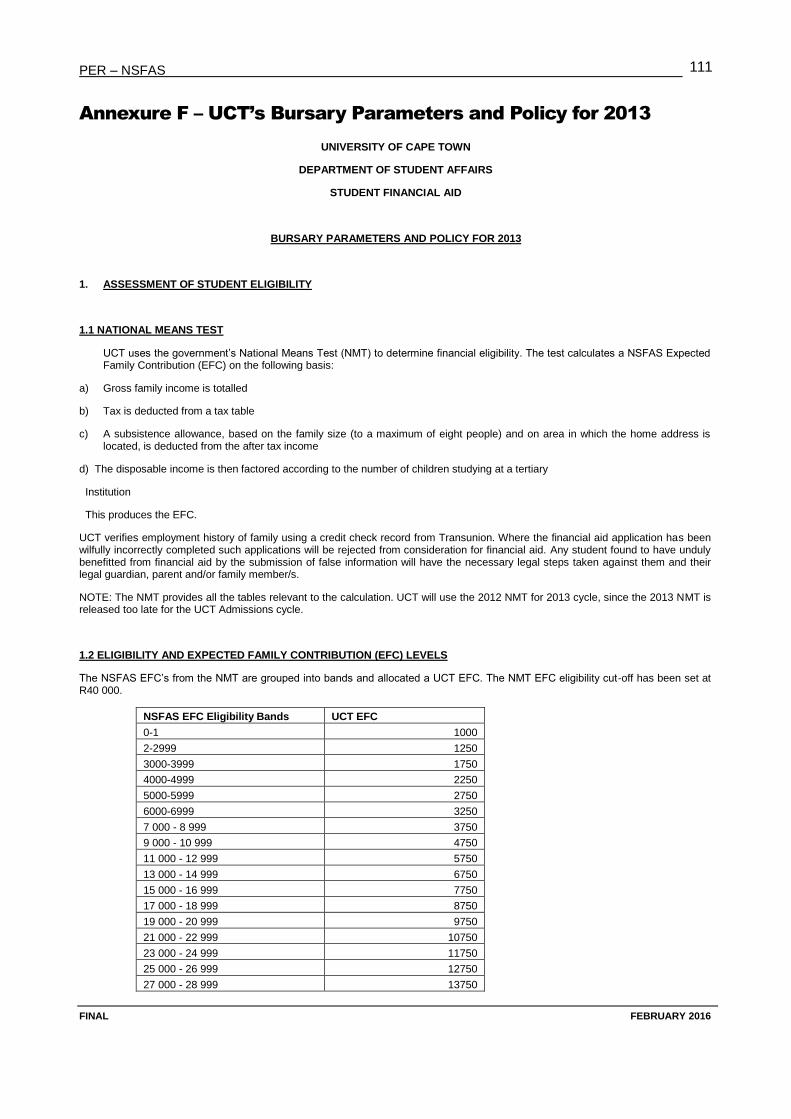

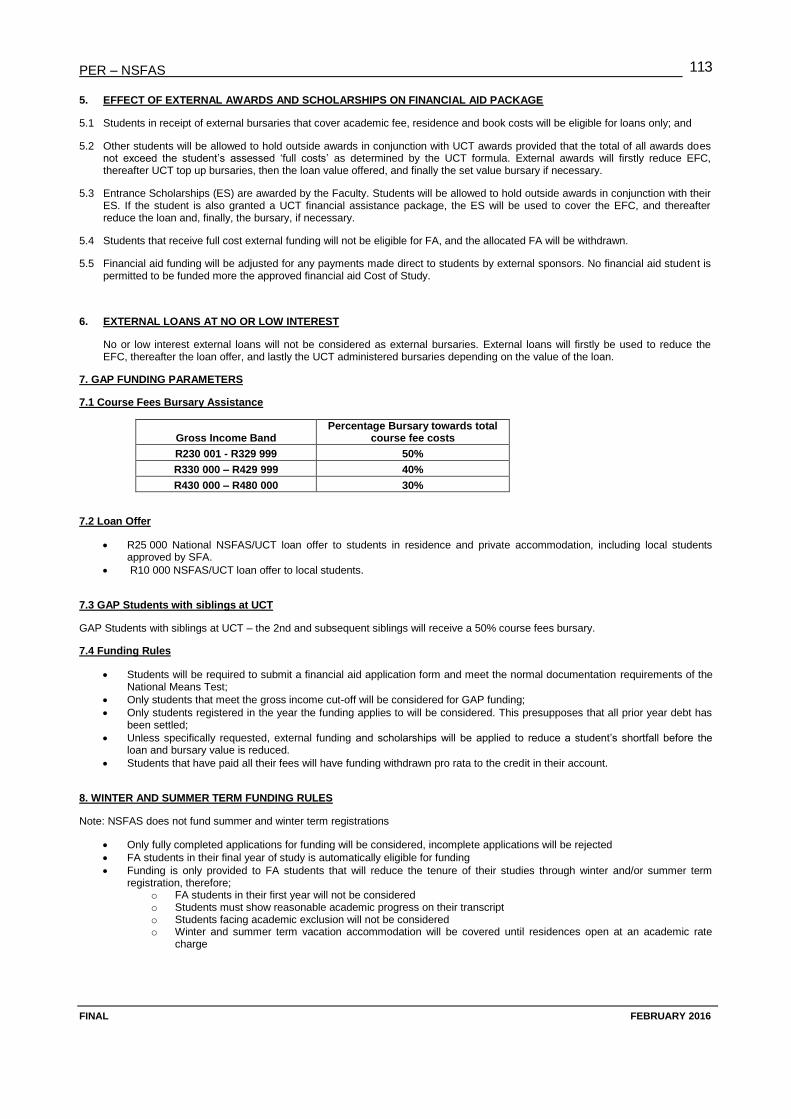

Each higher education institution is expected to issue their own financial awards policy that is aligned to the NSFAS guidelines, but tailored to the institution’s specific circumstances. By way of example, UCT’s Bursary Parameters and Policy for 2013 is attached in Annexure F.

In July 2015, DHET gathered the financial aid policies of universities, and Universities South Africa produced a review of them.8 An important finding was that there is “a very significant amount of variation within the country’s university system” when it comes to managing NSFAS loans. The review concludes by recommending that DHET and Universities South Africa should consider the feasibility of developing a good practice manual for managing financial aid, and specifically NSFAS loans.9 This is rather an unusual recommendation given that NSFAS issued a 7 None of these documents are in the public domain. 8 Universities South Africa, 2015. Student financial aid at South African Universities – Financial aid policies, structures and practices

with regards to NSFAS funding. 9 Universities South Africa, 2015, page 9.

PER – NSFAS

FINAL FEBRUARY 2016

11

guideline for managing NSFAS loans in 2011.10 The continuing variation suggests that the NSFAS guideline was either not suited to most universities situations and so is not widely followed, or it is drafted in such a way as to allow for diversity. The rollout of the new model would make this proposal redundant, as it aims to put in place a single, national system for managing NSFAS loans, grants and bursaries.

NSFAS loan-to-bursary conversion

NSFAS rewards students for passing their courses by converting a portion of their loan into a bursary. If a student passes all their courses in a year, then 40 per cent of their loan for that year will be converted into a bursary. A student who passes half their courses will have 20 per cent of their loan converted into a bursary.

In addition, when students qualify, the full loan amount for their final year of study is converted into a bursary. This “final year programme” was launched by the President in 2011. Students may only benefit from the final year programme once.

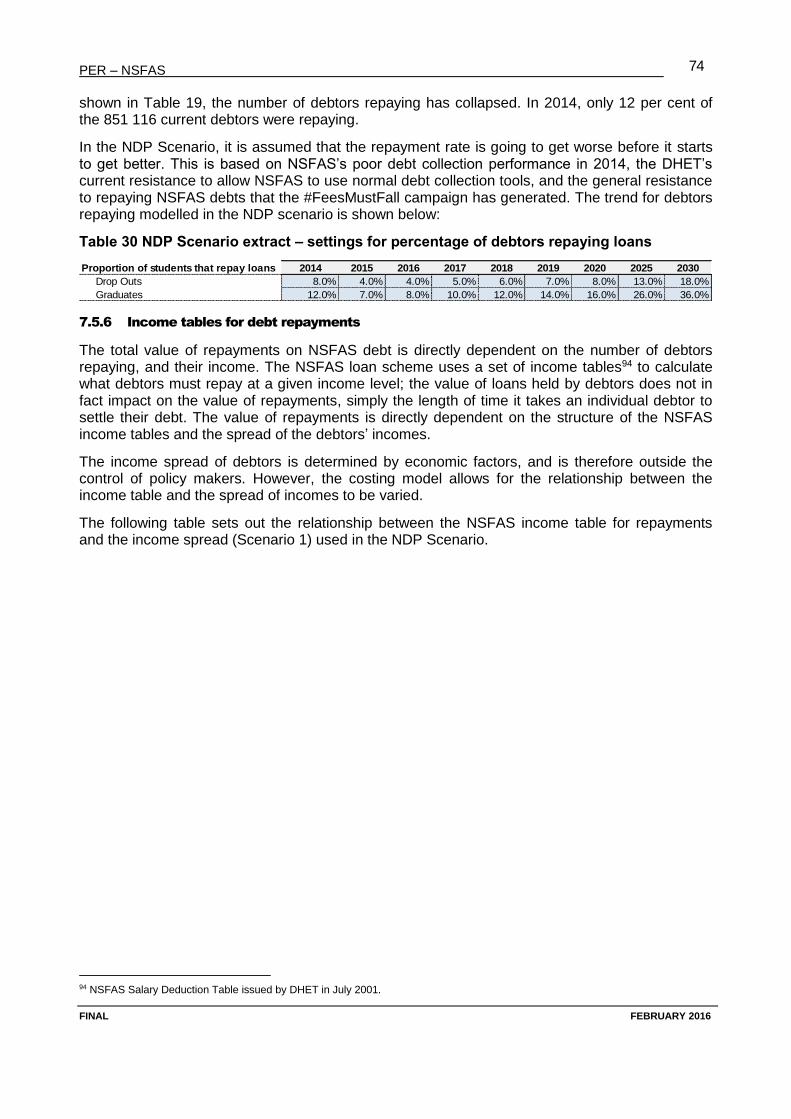

Recovery of NSFAS loans

The NSFAS loan scheme is intended to recycle recovered NSFAS loans to fund future loans. The scheme uses a set of income tables to calculate what debtors must repay at a given income level; This means the value of loans does not impact on the value of repayments, only on the length of time it takes for a loan holder to complete making payments. Loan holders become liable to start repaying their loans once they are employed and earning in excess of R30 000 per annum. A loan holder with an annual salary of R30 000 is required to pay 3 per cent of his or her gross annual salary. This percentage increases as salaries increase, up to a maximum of 8 per cent for gross annual salaries of R65 000 or higher.

Interest on the capital amount of the loan only starts accruing from a year after the student leaves university. If the loan holder starts repaying during the period before the interest begins accruing, those repayments will be 100 per cent capital repayments. Interest on the loans is charged at 80 per cent of the South African Reserve Bank Repurchase Rate as at 1 April. In 2014, the interest rate was pegged at 4.4 per cent.11

Loan holders are required to continue making repayments, based on their salaries, until all interest and capital has been repaid.

The NSFAS Salary Deduction Table was introduced in July 2001 by way of regulation. Since then the Deduction Table has not been revised. In 2000/1 the minimum tax threshold was R21 111.12 This suggests the threshold in the Deduction Table was broadly aligned to the SARS Personal Income Tax threshold in that year. Since then there has been significant “bracket creep”. As salaries have increased over the last 15 years loan holders have moved up the table and consequently those at the lower end of the income spectrum are being required to repay more than would have been the case if the Deduction Table had been properly adjusted for inflation each year or if the alignment with the SARS tax tables had been maintained. In 2014/15 the minimum personal income tax threshold had increased to R70 700.13

3.1.2 Grants for study at a TVET college

DHET facilitates access to vocational education and training at public TVET colleges for able students from poor backgrounds through the NSFAS TVET grant scheme. These grants are only available for full-time studies. The eligibility criteria for these TVET grants are:

10 NSFAS is apparently supposed to issue these guidelines annually, and has commissioned a new guideline to be issued in 2016. 11 NSFAS, 2015. Annual Report 2014/15, page 73. 12 http://www.sataxguide.co.za/south-african-income-tax-rates-from-1981-to-2007/. Accessed 25 November 2016 at 10:30. 13 http://www.sars.gov.za/Tax-Rates/Income-Tax/Pages/Rates%20of%20Tax%20for%20Individuals.aspx. Accessed 25 November

2016 at 10:30.

PER – NSFAS

FINAL FEBRUARY 2016

12

The student must be a South African citizen.

The student must be enrolled or intending to enrol in one of the following programmes:

o NCV.

o Report 191 courses:

N1 – N3, linked to a registered apprenticeship.

N4 – N6.

The student must be in need of financial assistance as determined by a compulsory means test and an income threshold of R122 000 – which was last reviewed by DHET in 2010.

The student must demonstrate potential for academic success.

The grants are paid directly to the TVET college on behalf of the student; they do not receive any funds directly.14 Students are not required to make any repayments on the grants.

3.1.3 Administration of other bursary/grant schemes

NSFAS manages a range of bursary funds for different government institutions:

The Funza Lushaka Bursary Programme to train teachers:15 a multi-year programme of

the Department of Basic Education (DBE) to promote teaching as a profession. Bursaries

are available to enable eligible students to complete a teaching qualification in an area of

national priority, such as mathematics. Recipients of these bursaries are required to teach

at a public school for the same number of years as they received the bursary.

Bursaries for studying social work:16 a programme introduced by the national Department

of Social Development (DSD) to promote social work as a profession, given the national

shortage of social workers. Bursary holders must complete the qualification within the

minimum period as prescribed by the university, and are not permitted to change fields of

study. Recipients of these bursaries are required to work as social workers in the public

sector for the same number of years as they received the bursary.

Bursaries from the National Skills Fund (NSF) for scarce skills:17 bursaries to students

from poor backgrounds, towards qualifications in identified scarce skills, as well as to

students with disabilities, for all fields of study. The fund covers tuition and resident fees,

study materials, and may also include a travel and general allowance depending on

requirements of the student. Each bursary awarded will depend on the financial need of

the student. Students are also encouraged to apply for other funding. Candidates who

receive a bursary will be required to agree to an obligatory work contract within South

Africa after successfully completing their studies. Students will need to successfully pass

each year of their studies towards their first degree. If they fail, funding will be

discontinued and they must re-do the year at their own cost before funding will be re-

instated the following year.

The bursary programme for students with disabilities:18 This bursary programme was

introduced by DHET. The bursary covers tuition and residence fees, meals, study

14 NSFAS states in its Annual Performance Plan 2014/15 that DHET intends “to publish regulations for determining allowances for

travel, accommodation and meals for TVET college students.” 15 http://www.funzalushaka.doe.gov.za/. 16 http://www.dsd.gov.za. 17 http://bursaries-southafrica.co.za/the-national-skills-fund-bursaries/. 18 http://www.isasaschoolfinder.co.za/info/governments-bursary-programme-for-students/, accessed [Fill in date] at [Fill in time].

PER – NSFAS

FINAL FEBRUARY 2016

13

material, transport and assistive devices and/or human support to the student.

Beneficiaries of the bursary are required to work in South Africa for a specified period

upon completion of their studies.

Other bursary schemes include the Military Veterans’ scheme, the Eastern Cape

Provincial Government scheme and the KwaZulu-Natal Provincial Government scheme.

NSFAS also manages various grant and bursary programmes for private institutions

(e.g.Nedbank) on a fee basis.

3.1.4 Shortcomings of the old NSFAS administrative system

The Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme (2010) identified various shortcomings with the current institution-based approach to managing NSFAS funding:

the methodology for dividing funding up between institutions is inequitable as it is based

on race rather than socio-economic status19 (see analysis in section 6.5.1);

lack of consistency across institutions with regards to compliance with the norms and

standards for the NSFAS scheme, especially the application of the means test20 and the

requirement to assess the probability of academic success;

certain institutions are spreading the NSFAS allocations very thinly among students (this

practice is referred to as “top slicing”21), meaning the students either have to find top-up

funding or are unable to complete their studies due to lack of funds;22

the processing of NSFAS loan agreements not meeting good governance or audit

requirements;23

administrative inefficiencies resulting in funds not being effectively applied and universities

not being paid on time;24

susceptibility to fraud and corruption; and

difficulties in recovering loans due to the absence of a direct relationship between NSFAS

and the students – often resulting from institutions capturing/students providing inaccurate

personal and contact information of the student being funded.

Addressing administrative and financial management issues is an ongoing process. NSFAS has

made significant progress in many areas since 2010 which has resulted in the institution receiving

unqualified financial audit opinions from the Auditor-General on its Annual Financial Statements

since 2011 through to 2015. This is a significant achievement. However, as the Auditor-General’s

“emphasis of matter” items in each of these years indicate there are still significant issues that

need to be addressed. In addition, an unqualified financial audit opinion does not mean NSFAS is

functioning optimally, that its data management capabilities are what they need to be, or that

there are no policy issues relating to the NSFAS loan scheme that need to be addressed.

19 DHET, 2010. Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme, page xiv. 20 Universities South Africa, 2015, page 9.

DHET, 2010. Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme, page xv. 21 DHET, 2010. Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme, page xiv. 22 HRDC, 2013. Status of the Bursary/Scholarship Landscape in South Africa, Research Report, page 295. 23 DHET, 2010. Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme, page xiv. 24 DHET, 2010. Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme, page xvii.

PER – NSFAS

FINAL FEBRUARY 2016

14

3.2 The New Student Centred Model

Partly in response to the above short-comings, in October 2013 NSFAS introduced a new administrative model for managing NSFAS loans, grants and bursaries, the new student centred model (hereafter referred to as the new model). The new model shifts the responsibility of administering funding from universities and TVET colleges to NSFAS.

The new model incorporates a range of innovations aimed at improving administration, including:

Students apply once for funding (not one year of study at a time), and their funding is

sustained in subsequent years for as long as they meet academic requirements for

promotion from one year to the next, easing the administrative burden on institutions and

NSFAS.

The financial means test is automated, and linked to other government databases to verify

personal, family, income and employment data, including:

o a link to the social security system to confirm whether the applicants were

beneficiaries of a Child Support Grant;

o a link to Department of Education’s schools’ database to establish whether the

applicant attended a fee free school or was given school fee exemptions;

o a link to Department of Education’s EMIS database allowing a speedy confirmation

of Grade-12 results, which determine whether a student qualifies for initial financial

assistance.

Funding will be allocated using an “all for some” approach according to a national ordered

eligibility queue based on a means test, academic assessment, and scarce skills.

Tuition and residence fees are paid to the university or TVET college at the start of the

academic year, which assists their cash flow.

Allowances for books, food, private accommodation, transport, electronic and assistive

devices are paid directly to student’s cell phones through the sBux voucher system,

ensuring that spending can be monitored and accounted for.

NSFAS has reviewed the operational processes required to implement the new model, and mapped the associated human resource requirements. Consequent to this review, the NSFAS Board has approved an increase in the entity’s headcount from 163 to 299, with a structured implementation plan based on the most critical needs as well as the funding available on a sustainable basis. The majority of new positions are in the operational areas relating directly to students, i.e. the Loans and Bursaries department and the significantly reorganised Contact Centre, as well as in the Information Technology department.25

NSFAS26 planned the phase-in of the new model over three years as follows:

Phase 1 would see seven universities and five TVET colleges participating, which would

cover some 77 000 students, or 20 per cent of all NSFAS-funded students.

Phase 2, anticipated to begin in 2015, would see 80 per cent of university and TVET

college students shifted to the new model.

25 NSFAS, 2014. Annual Report 2013/14, page 51. 26 NSFAS Annual Performance Plan 2014.

PER – NSFAS

FINAL FEBRUARY 2016

15

Phase 3, to have started from the beginning of 2016, would see all students on the new

model.

However, there have been delays in rolling it out. The NSFAS Annual Performance Plan for 2015/16 states NSFAS aim to increase the coverage of the new model to 30 per cent of students by the end of 2015.27 However, in December 2015, the NSFAS website28 only identified six universities and five TVET colleges as being part of the system. In its 2014/15 Annual Report,29 NSFAS acknowledges the challenges by stating that:

In essence, approximately 85% of the student population remains with the old model. Starting new models that are heavily dependent on Information Technology has its own attendant technical challenges.

The 2014/15 Annual Report notes that the Board has decided to have a longer phased-in approach for implementing the new model, and to use the more gradual process to learn from the glitches instead of going for “a big-bang approach that could potentially quadruple the problems that may be encountered in the implementation phase, and thus paralyse the entire system”.30

Clearly, the new model has much to offer in terms of streamlining administrative processes and improving accountability; consequently, the delays in its rollout are a major concern.

3.3 Proposals and recent policy developments regarding NSFAS

In 2010, the Ministerial Committee on the Review of NSFAS published its report,31 which made a range of findings and recommendations regarding the structure and management of NSFAS, many of which continue to be relevant. In addition, there are ongoing discussions between DHET and NSFAS, and within the higher education sector generally, as to how NSFAS can be strengthened and how the funding of academically able students from poor backgrounds can be improved. This section highlights proposals and recent policy developments in these areas:

1. Fee-free university education for the poor. In line with resolution 44 of the ANC’s 52nd National Conference,32 the Review Committee recommended that the higher education funding model should move progressively towards “free higher education to undergraduate level for students from poor and working class communities”33 This continues to be an objective of government. However, the issue of funding remains the primary challenge. In the interim, a number of steps have been taken to move NSFAS in this direction:

the rapid growth in NSFAS general funding, and the addition of other funding streams;

the introduction and expansion of the TVET grant programme;

elimination of the means test in relation to students who qualified to receive a Child Support Grant;

elimination of the means test in relation to students who matriculated from “fee-free schools” or were granted school fee exemptions while at school; and

the introduction of the final year programme, in addition to the loan-to-bursary conversions, for students who pass their courses.

27 NSFAS Annual Performance Plan for the year 2015/16 page 9. 28 http://www.nsfas.org.za/NSFAS/STUDENTS/APPLY, accessed 30 December 2015 at 11.30. 29 NSFAS, 2015. Annual Report 2014/15, page 12. 30 NSFAS, 2015. Annual Report 2014/15, page 12. 31 DHET, 2010. Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme. 32 ANC, 2007. 52nd National Conference: Resolutions, 20 December 2007. http://www.anc.org.za/show.php?id=2536. 33 DHET, 2010. Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme, page 124.

PER – NSFAS

FINAL FEBRUARY 2016

16

2. The means test and the “missing middle”. The Review Committee was very critical of the NSFAS means test because “it excludes children from families who earn above the R122 000 per annum qualification threshold, but who still cannot afford to attend university.”34 The Committee recommended that the higher education funding model should provide student loans on favourable terms to higher education students from lower middle-income families. DHET35 continues to explore this option, as well as other ideas that have been proposed, including:

a graduate tax;

greater contributions from the private sector; and

using the NSFAS grant as collateral to bring national banks and investment corporations (e.g. the Public Investment Corporation) on board to support students.

3. The funding of BTech programmes. According to NSFAS policy, BTech is regarded as a second qualification, and therefore students studying for BTech are not eligible. This leaves a very significant gap in government’s efforts to provide financial assistance to students, especially those studying for qualifications in science, engineering and technology (SET). In February 2015, DHET36 indicated that funding will only be made available for BTech qualifications required for registration with a professional council. Recent information from the Nelson Mandela Metropolitan University (NMMU)37 and the Cape Peninsula University of Technology (CPUT)38 confirms that NSFAS funding will be available for certain BTech qualifications in 2016. However, the lack of funding for the remaining BTech programmes remains a challenge.

4. The FCS and the determination of the approved cost of study. Once a student has been approved for an NSFAS loan, grant or bursary, a process of establishing the approved cost of study relating to that particular student needs to be completed to determine the quantum to be awarded. There are three proposals relating to this issue:

the Review Committee proposed that the practice of top slicing should be eliminated (the full rollout of the new model would achieve this);

the FCS and other approved costs should be extended to cover transport; and

DHET is in the process of preparing regulations for determining allowances for travel, accommodation and meals for TVET college students.39

5. Implementation of the in duplum rule. The Review Committee found that NSFAS was operating on the basis that the in duplum rule, which restricts the amount of interest that may accrue to an amount equal to the original loan, did not apply to it. This was in contravention of both common law and the National Credit Act.40 Consequently, NSFAS has undertaken an extensive exercise to review existing debt and restate the interest on such debt in compliance with the in duplum rule. This has resulted in the value of NSFAS debt being adjusted downwards.

6. Collecting debts that had prescribed. The Review Committee found that NSFAS continued to collect debts that had prescribed.41 It is understood that this practice has been discontinued. However, the broader issue is that NSFAS should manage its debt book in a manner that prevents debts prescribing.

34 DHET, 2010. Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme, page xv. 35 DHET, 2015. “Annexure 3”, page 9-11. 36 DHET, 2015. Presentation to Parliament‘s Portfolio Committee on Higher Education and Training, 18 February 2015. 37 http://finaid.nmmu.ac.za/NSFAS-Loans, accessed 26 October 2015 at 16.45. 38 http://www.cput.ac.za/research/postgraduate/bursaries, accessed 26 October 2015 at 16.45. 39 NSFAS, 2014. Annual Performance Plan, page 11. 40 DHET, 2010. Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme, page xvii. 41 DHET, 2010. Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme, page xviii.

PER – NSFAS

FINAL FEBRUARY 2016

17

7. Blacklisting of NSFAS debtors The NSFAS Act allows NSFAS to blacklist delinquent borrowers after informing them of the intention to do so and giving them an opportunity to settle arrear payments. In August 2011, the Minister of Higher Education and Training instructed NSFAS to discontinue all blacklisting of NSFAS borrowers.42 This closed down an important tool for collecting NSFAS debt, especially from students who are employed but refusing to pay.

8. Extra-judicial emolument attachment orders. Section 23 of the NSFAS Act allowed NSFAS to send a registered letter to the employers of NSFAS borrowers to compel them to deduct repayments at source. This practice does not follow due legal process, and is also contrary to the National Credit Act. Following criticism by the Review Committee, and a legal opinion on the issue, NSFAS discontinued this practice in 2011. However, it would seem that, at the same time, NSFAS decided to discontinue the use of all emolument attachment orders.43 Again, this closed down an important tool for collecting NSFAS debt from students who are employed but refusing to pay.

9. Using SARS to assist with collecting NSFAS debt. A key recommendation of the Review Committee was that government should explore the option of using SARS to collect NSFAS debt by way of a surcharge on the borrower’s PAYE.44 While SARS does provide NSFAS with employer information in terms of the NSFAS Act, there does not appear to have been any further movement in getting SARS to manage NSFAS debt collections.

4. NSFAS in the higher education context

NSFAS is an integral part of the higher education sector; therefore, it is directly affected by key sector trends, namely:

efforts to increase the participation rates in higher education through increasing enrolments;

transformation efforts to ensure equitable access to higher education by academically-able students from poor backgrounds;

efforts to improve the retention and conversion rates (i.e. reducing dropouts and increasing graduation rates);

increasing cost of higher education as represented by the FCS; and

developments in government’s strategy to resource/fund higher education.

For this PER, various data was analysed to get an understanding of these key trends and how they impact upon the different components of NSFAS. The results of this work are presented below and compared with the information from other sources, notably “Annexure 3”45 presented at the Second National Higher Education Summit46 recently hosted by DHET.

42 Timeslive article, “Loan relief for NSFAS students”, 24 August 2011. http://www.timeslive.co.za/local/2011/08/24/loan-relief-for-

nsfas-students accessed 26 October 2015 at 16:45. 43 It is not clear why this decision was taken, and whether it was an instruction by the Board or the Ministers. 44 DHET, 2010. Report of the Ministerial Committee on the Review of the National Student Financial Aid Scheme, page xix. 45 DHET, 2015. “Annexure 3 Are we making progress with systemic structural transformation of resourcing, access, success, staffing

and researching in higher education: What do the data say?” Submission to the Second National Higher Education Summit held in

Durban on 15 to 17 October 2015 are available at http://www.dhet.gov.za/summit/Docs2015.html. Accessed 20 November 2015 at

10:30. 46 Documents presented at the Second National Higher Education Summit held in Durban on 15 to 17 October 2015 are available at

http://www.dhet.gov.za/summit/Docs2015.html. Accessed 20 November 2015 at 10:30.

PER – NSFAS

FINAL FEBRUARY 2016

18

4.1 Increasing enrolment numbers

The National Plan on Higher Education (2001) stated that a participation rate47 in higher education of 20 per cent should be achieved over the following 10-15 years in order to supply the human resources needs of the country. DHET reports that the participation rate has increased from 15.4 per cent in 2003 to 19.5 per cent in 2013. Importantly, the participation rate of African students has increased from 11.1 per cent in 2003 to 16.5 per cent in 2013.48

4.1.1 University enrolment numbers

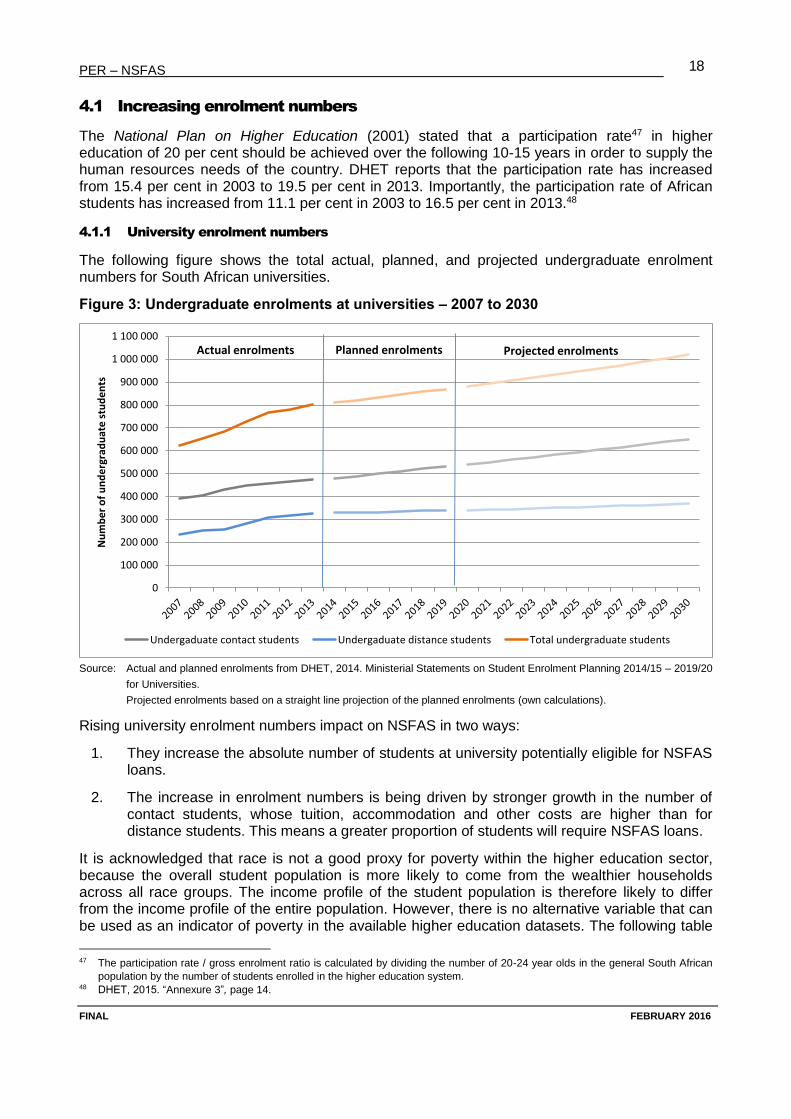

The following figure shows the total actual, planned, and projected undergraduate enrolment numbers for South African universities.

Figure 3: Undergraduate enrolments at universities – 2007 to 2030

Source: Actual and planned enrolments from DHET, 2014. Ministerial Statements on Student Enrolment Planning 2014/15 – 2019/20

for Universities.

Projected enrolments based on a straight line projection of the planned enrolments (own calculations).

Rising university enrolment numbers impact on NSFAS in two ways:

1. They increase the absolute number of students at university potentially eligible for NSFAS loans.

2. The increase in enrolment numbers is being driven by stronger growth in the number of contact students, whose tuition, accommodation and other costs are higher than for distance students. This means a greater proportion of students will require NSFAS loans.

It is acknowledged that race is not a good proxy for poverty within the higher education sector, because the overall student population is more likely to come from the wealthier households across all race groups. The income profile of the student population is therefore likely to differ from the income profile of the entire population. However, there is no alternative variable that can be used as an indicator of poverty in the available higher education datasets. The following table

47 The participation rate / gross enrolment ratio is calculated by dividing the number of 20-24 year olds in the general South African

population by the number of students enrolled in the higher education system. 48 DHET, 2015. “Annexure 3”, page 14.

0

100 000

200 000

300 000

400 000

500 000

600 000

700 000

800 000

900 000

1 000 000

1 100 000

Nu

mb

er

of

un

de

rgra

du

ate

stu

de

nts

Undergaduate contact students Undergaduate distance students Total undergraduate students

Actual enrolments Planned enrolments Projected enrolments

PER – NSFAS

FINAL FEBRUARY 2016

19

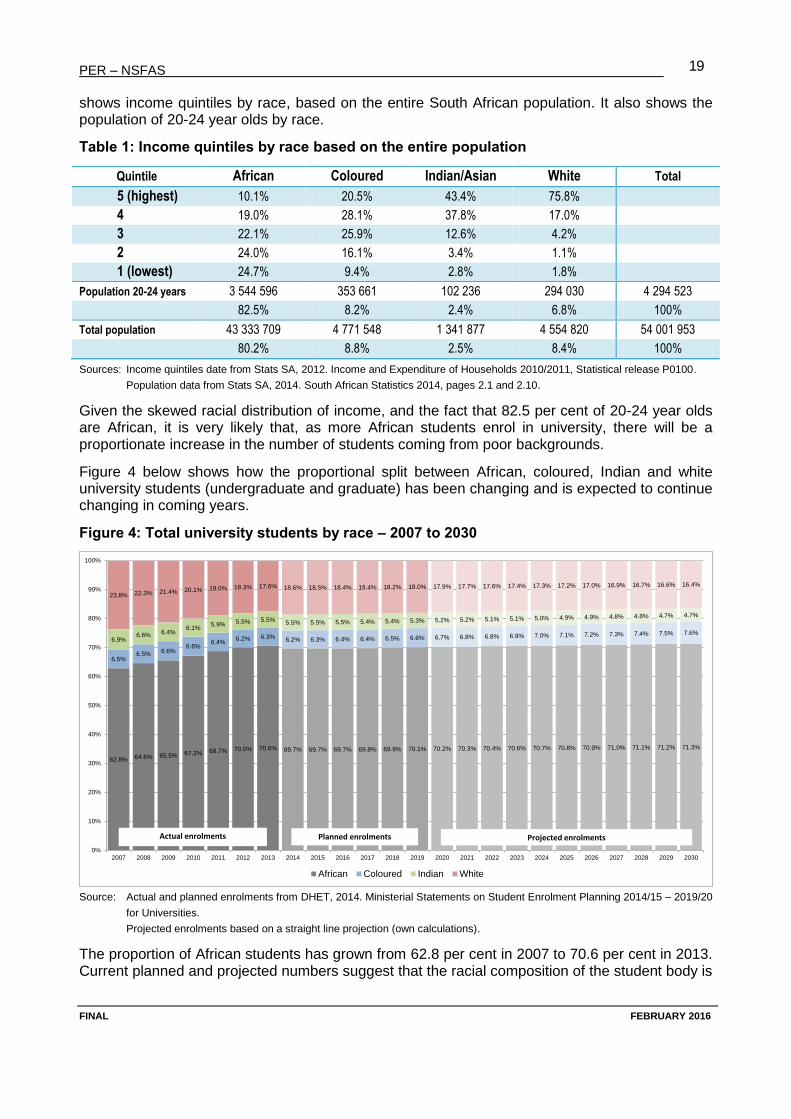

shows income quintiles by race, based on the entire South African population. It also shows the population of 20-24 year olds by race.

Table 1: Income quintiles by race based on the entire population

Quintile African Coloured Indian/Asian White Total

5 (highest) 10.1% 20.5% 43.4% 75.8%

4 19.0% 28.1% 37.8% 17.0%

3 22.1% 25.9% 12.6% 4.2%

2 24.0% 16.1% 3.4% 1.1%

1 (lowest) 24.7% 9.4% 2.8% 1.8%

Population 20-24 years 3 544 596 353 661 102 236 294 030 4 294 523

82.5% 8.2% 2.4% 6.8% 100%

Total population 43 333 709 4 771 548 1 341 877 4 554 820 54 001 953

80.2% 8.8% 2.5% 8.4% 100%

Sources: Income quintiles date from Stats SA, 2012. Income and Expenditure of Households 2010/2011, Statistical release P0100.

Population data from Stats SA, 2014. South African Statistics 2014, pages 2.1 and 2.10.

Given the skewed racial distribution of income, and the fact that 82.5 per cent of 20-24 year olds are African, it is very likely that, as more African students enrol in university, there will be a proportionate increase in the number of students coming from poor backgrounds.

Figure 4 below shows how the proportional split between African, coloured, Indian and white university students (undergraduate and graduate) has been changing and is expected to continue changing in coming years.

Figure 4: Total university students by race – 2007 to 2030

Source: Actual and planned enrolments from DHET, 2014. Ministerial Statements on Student Enrolment Planning 2014/15 – 2019/20

for Universities.

Projected enrolments based on a straight line projection (own calculations).

The proportion of African students has grown from 62.8 per cent in 2007 to 70.6 per cent in 2013. Current planned and projected numbers suggest that the racial composition of the student body is

62.8% 64.6% 65.5% 67.2% 68.7% 70.0% 70.6%

6.5%6.5% 6.6%

6.6%6.4%

6.2% 6.3%6.9%6.6% 6.4%

6.1%5.9% 5.5% 5.5%

23.8% 22.3% 21.4% 20.1% 19.0% 18.3% 17.6%

69.7% 69.7% 69.7% 69.8% 69.9% 70.1%

6.2% 6.3% 6.4% 6.4% 6.5% 6.6%

5.5% 5.5% 5.5% 5.4% 5.4% 5.3%

18.6% 18.5% 18.4% 18.4% 18.2% 18.0%

70.2% 70.3% 70.4% 70.6% 70.7% 70.8% 70.9% 71.0% 71.1% 71.2% 71.3%

6.7% 6.8% 6.8% 6.9% 7.0% 7.1% 7.2% 7.3% 7.4% 7.5% 7.6%

5.2% 5.2% 5.1% 5.1% 5.0% 4.9% 4.9% 4.8% 4.8% 4.7% 4.7%

17.9% 17.7% 17.6% 17.4% 17.3% 17.2% 17.0% 16.9% 16.7% 16.6% 16.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

African Coloured Indian White

Actual enrolments Planned enrolments Projected enrolments

PER – NSFAS

FINAL FEBRUARY 2016

20

likely to remain fairly stable going forward. Nevertheless, increases in the total participation rate will continue to widen access to students from poor backgrounds. Therefore the proportion of students who will be eligible for NSFAS funding will continue to grow.

4.1.2 TVET college enrolment numbers

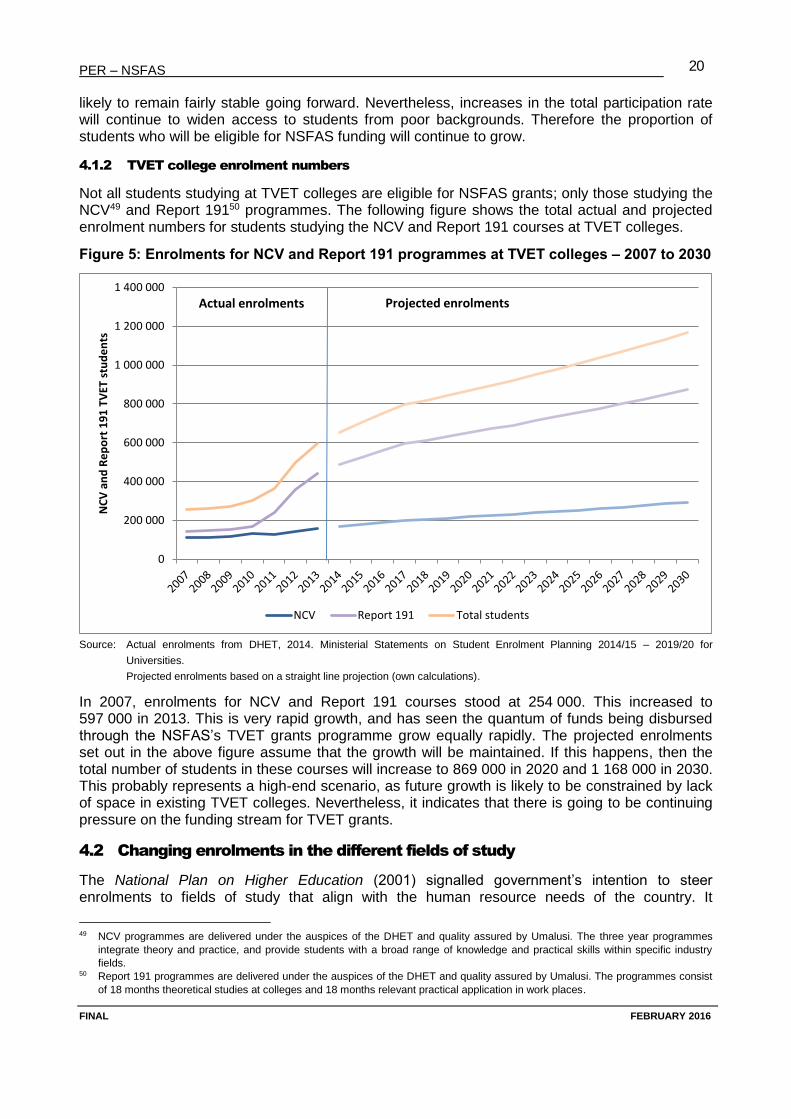

Not all students studying at TVET colleges are eligible for NSFAS grants; only those studying the NCV49 and Report 19150 programmes. The following figure shows the total actual and projected enrolment numbers for students studying the NCV and Report 191 courses at TVET colleges.

Figure 5: Enrolments for NCV and Report 191 programmes at TVET colleges – 2007 to 2030

Source: Actual enrolments from DHET, 2014. Ministerial Statements on Student Enrolment Planning 2014/15 – 2019/20 for

Universities.

Projected enrolments based on a straight line projection (own calculations).

In 2007, enrolments for NCV and Report 191 courses stood at 254 000. This increased to 597 000 in 2013. This is very rapid growth, and has seen the quantum of funds being disbursed through the NSFAS’s TVET grants programme grow equally rapidly. The projected enrolments set out in the above figure assume that the growth will be maintained. If this happens, then the total number of students in these courses will increase to 869 000 in 2020 and 1 168 000 in 2030. This probably represents a high-end scenario, as future growth is likely to be constrained by lack of space in existing TVET colleges. Nevertheless, it indicates that there is going to be continuing pressure on the funding stream for TVET grants.

4.2 Changing enrolments in the different fields of study

The National Plan on Higher Education (2001) signalled government’s intention to steer enrolments to fields of study that align with the human resource needs of the country. It

49 NCV programmes are delivered under the auspices of the DHET and quality assured by Umalusi. The three year programmes

integrate theory and practice, and provide students with a broad range of knowledge and practical skills within specific industry

fields. 50 Report 191 programmes are delivered under the auspices of the DHET and quality assured by Umalusi. The programmes consist

of 18 months theoretical studies at colleges and 18 months relevant practical application in work places.

0

200 000

400 000

600 000

800 000

1 000 000

1 200 000

1 400 000

NC

V a

nd

Re

po

rt 1

91

TV

ET s

tud

en

ts

NCV Report 191 Total students

Actual enrolments Projected enrolments

PER – NSFAS

FINAL FEBRUARY 2016

21

committed government to “shift the balance in enrolments between the humanities, business and commerce and science, engineering and technology (SET) from the 2001 ratio of 49%:26%:25% to a ratio of 40%:30%:30% respectively”51 over the next five to ten years. During the enrolment planning cycle for 2011/12-2013/14, DHET set targets for certain scarce skill areas, namely: engineering sciences; human and animal health; natural and physical sciences; and initial teacher education. These scarce skills fall mainly within the SET field of study.

DHET52 reports that between 2003 and 2013, the SET field of study’s share of total enrolments has increased from 27 per cent to 29 per cent. However, this seemingly small shift has taken place within the context of rapidly growing overall enrolments, meaning that the actual number of students enrolling for SET courses has grown rapidly from 193 864 in 2003 to 283 622 in 2013. Also significant is that the percentage of African enrolments in SET increased from 55 per cent in 2003 to 67 per cent in 2013.

Increasing enrolments in the SET field of study impacts upon NSFAS as follows:

Most SET qualifications require four years regulation time, as opposed to three years for the other two fields of study. Increasing enrolments for SET qualifications means that NSFAS has to fund more students for more years.

Generally, the tuition fees for SET courses are higher than in other fields of study. So if more students who require NSFAS funding enrol for such courses, it will further push up the cost to NSFAS.

There is evidence that the dropout rates in certain SET courses are higher, and graduation rates lower, than in other fields of study.53 If NSFAS funds an increasing number of SET students, the risk of the funds not being effectively spent is greater. Also, if the funding is an NSFAS loan, then a larger number of students will incur debt without obtaining a qualification, which will impact on the recoverability of such debt.

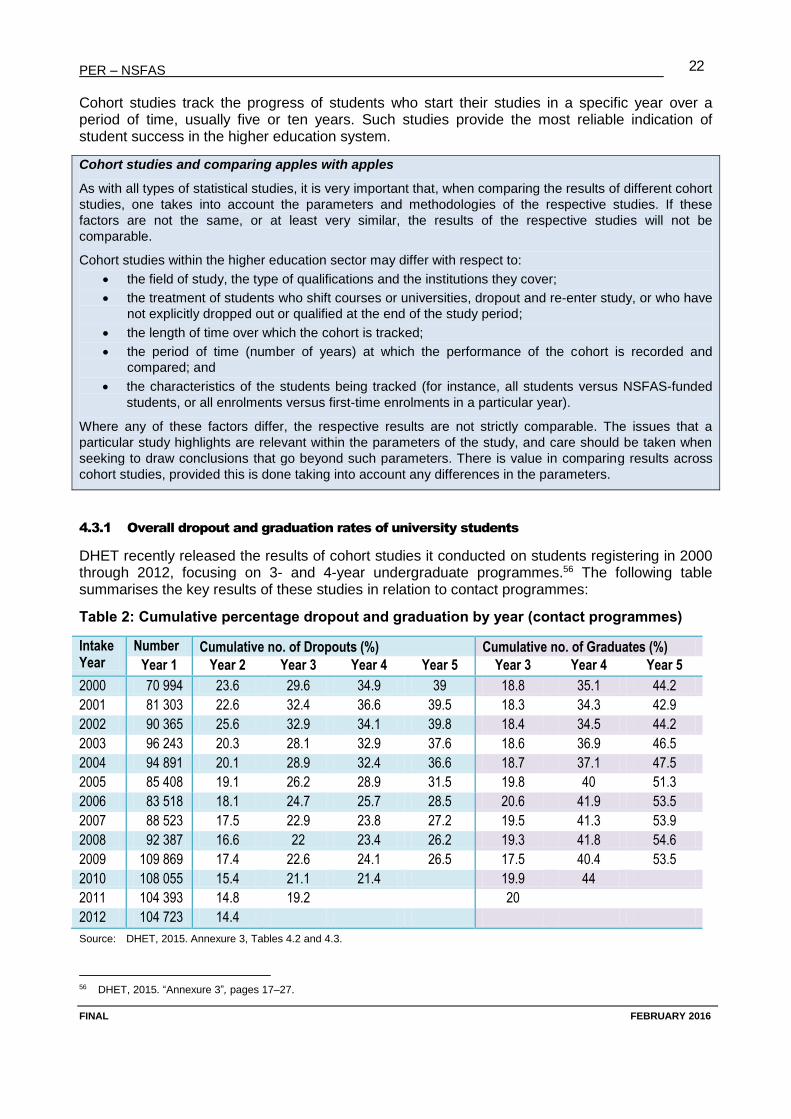

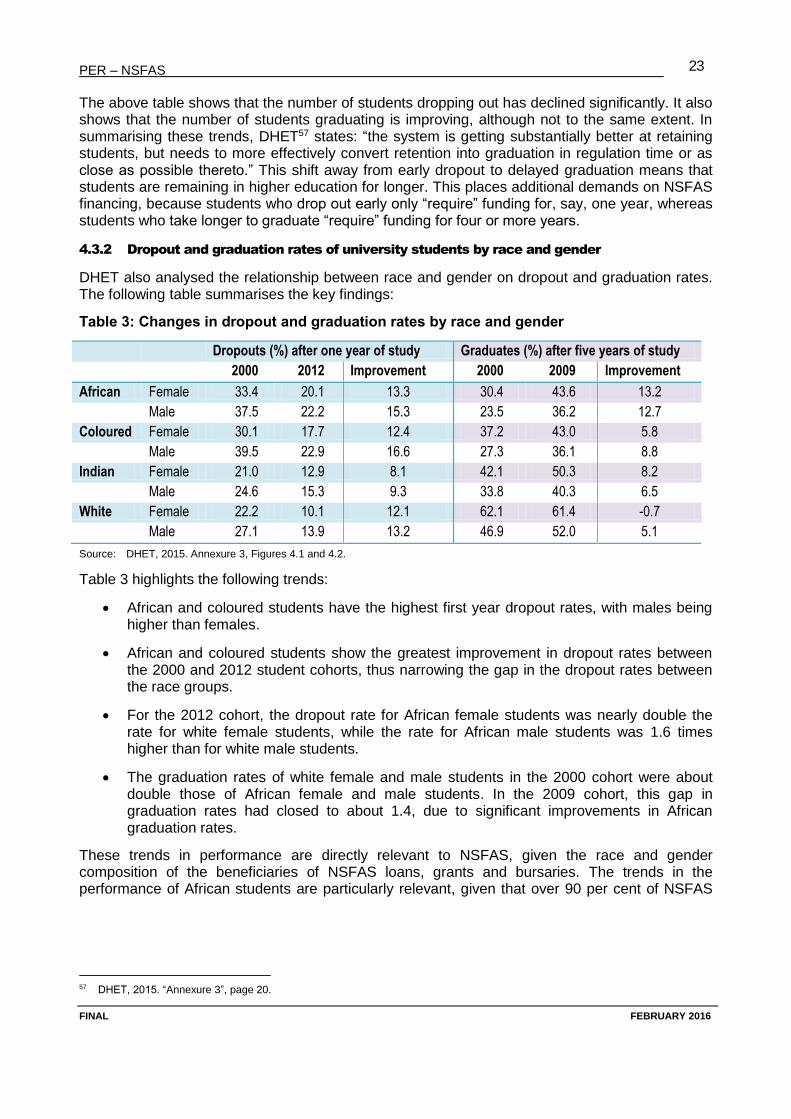

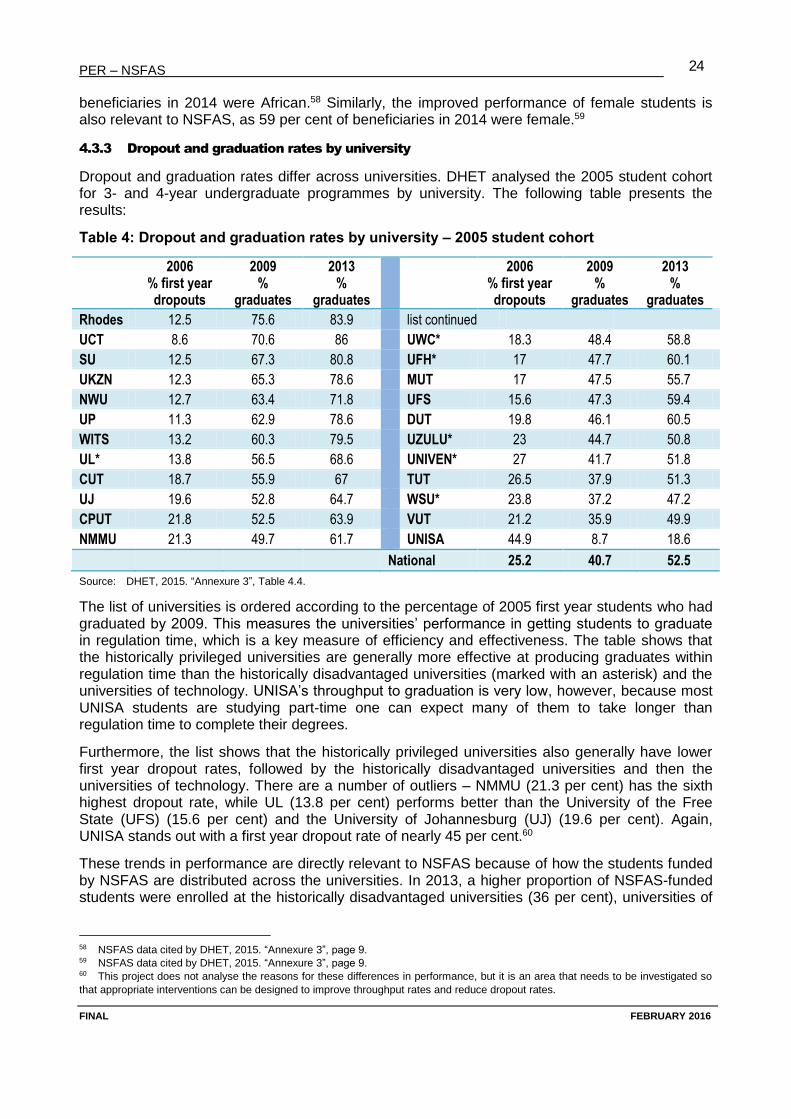

4.3 Dropout and graduation rates

An effective and efficient higher education system is one that minimises the number of dropouts and enables as many students as possible to graduate in regulation time54 or as close to it as possible, obviously without compromising quality.55 The most efficient use of NSFAS funds is to fund students that graduate within regulation time. Therefore the dropout and delayed graduation rates in the higher education system impact directly on the finances of NSFAS in the following ways:

If NSFAS allocates grants or bursaries to students who subsequently dropout, those funds are wasted because they did not purchase the intended qualification.

If NSFAS allocates loans to students that subsequently dropout, it means they will be saddled with NSFAS debt and no qualification. The lack of a qualification reduces their chances of employment and income earning potential, which decreases the likelihood of them being able to repay the NSFAS debt.

If NSFAS funds students who take longer than regulation time to qualify, they will receive more funding from NSFAS than a student who qualifies in regulation time.

51 National Plan on Higher Education, 2001, page 26. 52 DHET, 2015. “Annexure 3”, pages 15 and 16. 53 See the results of the PER cohort study presented in section 4.3.4. 54 For a 3-year contact programme, 3 years would be regulation time, and for a 4-year programme it would be 4 years. 55 DHET, 2015. “Annexure 3”, page 18.

PER – NSFAS

FINAL FEBRUARY 2016

22

Cohort studies track the progress of students who start their studies in a specific year over a period of time, usually five or ten years. Such studies provide the most reliable indication of student success in the higher education system.

Cohort studies and comparing apples with apples

As with all types of statistical studies, it is very important that, when comparing the results of different cohort

studies, one takes into account the parameters and methodologies of the respective studies. If these

factors are not the same, or at least very similar, the results of the respective studies will not be

comparable.

Cohort studies within the higher education sector may differ with respect to:

the field of study, the type of qualifications and the institutions they cover;

the treatment of students who shift courses or universities, dropout and re-enter study, or who have

not explicitly dropped out or qualified at the end of the study period;

the length of time over which the cohort is tracked;