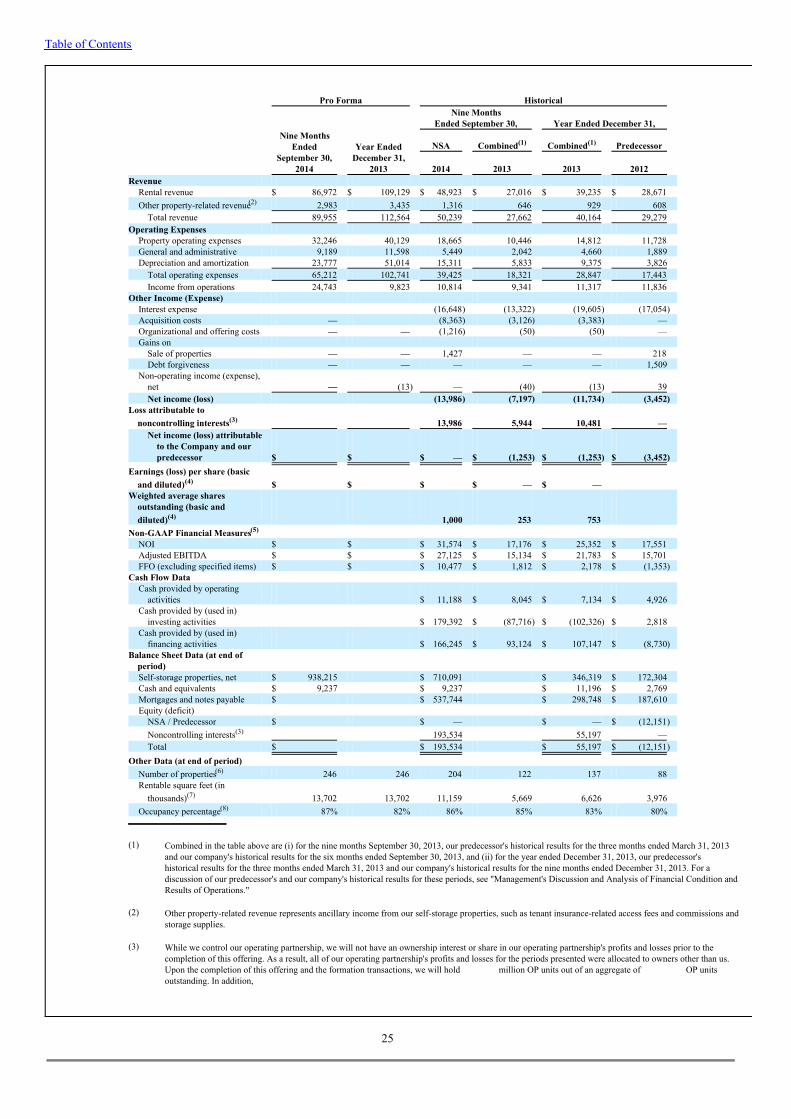

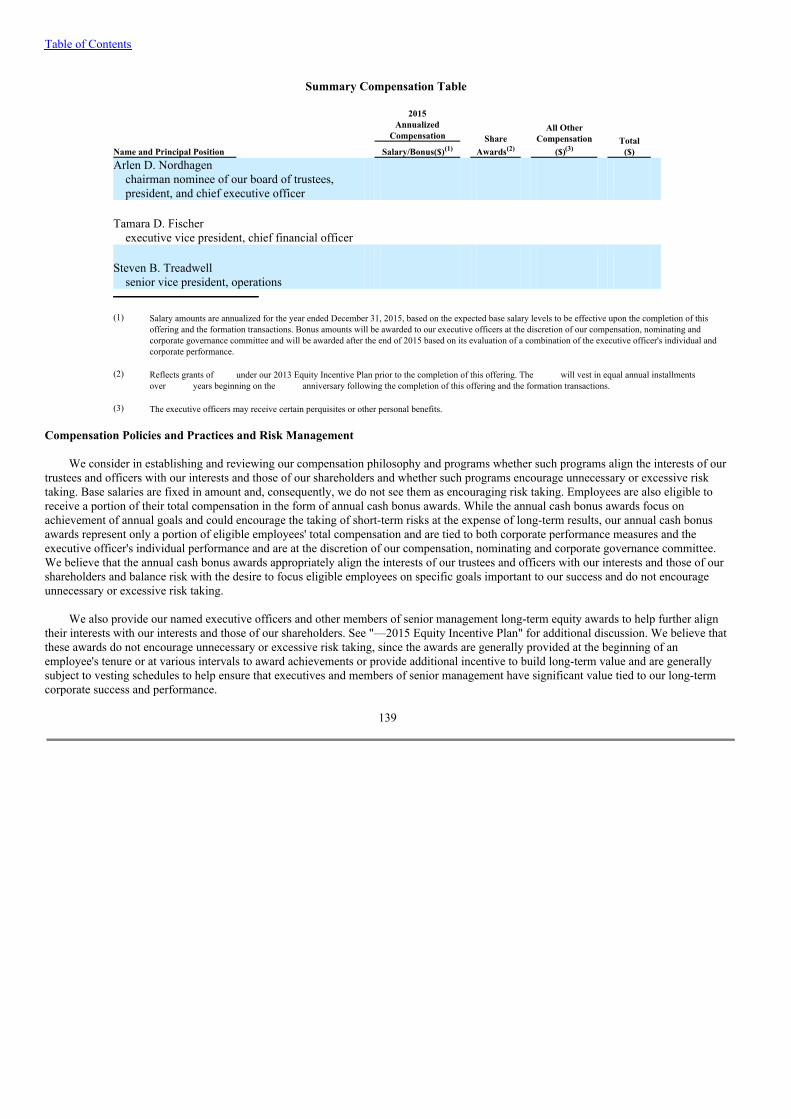

national storage affiliates trust form s-11 securities and exchange...

TRANSCRIPT

Use these links to rapidly review the documentTABLE OF CONTENTS TABLE OF CONTENTS 2

Table of Contents

As filed with the Securities and Exchange Commission on February 13, 2015

Registration Statement No. 333-

SECURITIES AND EXCHANGE COMMISSIONWashington, D.C. 20549

FORM S-11FOR REGISTRATION

UNDERTHE SECURITIES ACT OF 1933

OF CERTAIN REAL ESTATE COMPANIES

National Storage Affiliates Trust(Exact name of registrant as specified in its governing instruments)

National Storage Affiliates Trust5200 DTC Parkway

Suite 200Greenwood Village, Colorado 80111

(720) 630-2600(Address, including Zip Code, and Telephone Number, including Area Code, of Registrant's Principal Executive Offices)

Arlen D. NordhagenChief Executive Officer

National Storage Affiliates Trust5200 DTC Parkway

Suite 200Greenwood Village, Colorado 80111

(720) 630-2600(Name, Address, including Zip Code, and Telephone Number, including Area Code, of Agent for Service)

Copies to:

Jay L. Bernstein, Esq.Andrew S. Epstein, Esq.Clifford Chance US LLP

31 West 52nd StreetNew York, New York 10019

Tel (212) 878-8000Fax (212) 878-8375

Julian Kleindorfer, Esq.

Lewis Kneib, Esq.Latham & Watkins LLP355 South Grand Avenue

Los Angeles, California 90071Tel (213) 485-1234Fax (213) 891-8763

Approximate date of commencement of proposed sale to the public:As soon as practicable after the effective date of this registration statement.

If any of the Securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registrationstatement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number ofthe earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number ofthe earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "largeaccelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o Accelerated filer o Non-accelerated filer ý(Do not check if a

Smaller reporting company o

CALCULATION OF REGISTRATION FEE

Title of each class of securitiesto be registered

Proposed maximumaggregate offering

price(1)(2) Amount of

registration fee(3)

Common shares, $0.01 par value per share $100,000,000 $11,620.00

(1) Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended.

(2) Includes the offering price of common shares that may be sold if the option to purchase additional shares granted by the Registrant to the underwriters is exercised.

(3) Calculated pursuant to Rule 457(o) based on an estimate of the proposed maximum aggregate offering price.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a furtheramendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended,or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

smaller reporting company)

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these common shares until theregistration statement filed with the Securities and Exchange Commission becomes effective. This preliminary prospectus is not anoffer to sell these common shares and it is not soliciting an offer to buy these common shares in any jurisdiction where the offer orsale is not permitted.

Subject to CompletionPreliminary Prospectus, dated , 2015

PROSPECTUS

Shares

National Storage Affiliates TrustCommon Shares of Beneficial Interest

This is our initial public offering. We are offering common shares of beneficial interest, $0.01 par value per share. We expect theinitial public offering price of our common shares to be between $ and $ per share. Prior to this offering, there has been no publicmarket for our common shares. We intend to apply to have our common shares listed on the New York Stock Exchange, under the symbol"NSA."

We are an "emerging growth company" as defined in the Jumpstart Our Business Startups Act of 2012.

We intend to elect and qualify to be taxed as a real estate investment trust, or a REIT, for U.S. federal income tax purposes, commencingwith our taxable year ending December 31, 2015. To assist us in qualifying as a REIT, among other purposes, shareholders are generallyrestricted from owning more than 9.8% by value or number of shares, whichever is more restrictive, of our aggregate outstanding shares ofall classes and series, the outstanding shares of any class or series of our preferred shares or our outstanding common shares. Our declarationof trust contains various other restrictions on the ownership and transfer of our shares, see "Description of Shares of Beneficial Interest—Restrictions on Ownership and Transfer."

Investing in our common shares involves risks that are described in the "Risk Factors" section beginning onpage 28 of this prospectus.

Per share Total

Initial public offering price $ $

Underwriting discount $ $

Proceeds, before expenses,(1) to us $ $

(1) See "Underwriting" for a detailed description of compensation payable to the underwriters.

We have granted the underwriters the option to purchase up to additional common shares from us at the initial public offeringprice, less the underwriting discount, within 30 days after the date of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these shares ordetermined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares sold in this offering will be ready for delivery on or about , 2015.

The date of this prospectus is , 2015

Jefferies Morgan Stanley Wells Fargo Securities

TABLE OF CONTENTS

You should rely only on the information contained in this prospectus, any free writing prospectus prepared by us or informationto which we have referred you. We have not, and the underwriters have not, authorized anyone to provide you with additionalinformation or information different from that contained in this prospectus. We are offering to sell, and seeking offers to buy, ourcommon shares only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurateonly as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of common shares.

i

Market and Industry Data and Forecasts ii Prospectus Summary 1 Risk Factors 28 Forward-Looking Statements 53 Use of Proceeds 55 Distribution Policy 56 Capitalization 57 Dilution 59 Selected Pro Forma and Historical Financial and Operating Data 61 Management's Discussion and Analysis of Financial Condition and Results of Operations 66 Industry Overview and Market Opportunity 99 Business and Properties 106 Our Management 131 The Formation and Structure of Our Company 147 Principal Shareholders 154 Certain Relationships and Related Transactions 156 Description of Shares of Beneficial Interest 160 Certain Provisions of Maryland Law and of Our Declaration of Trust and Bylaws 166 Shares Eligible for Future Sale 173 Limited Partnership Agreement of Our Operating Partnership 176 U.S. Federal Income Tax Considerations 184 ERISA Considerations 209 Underwriting 210 Legal Matters 217 Experts 218 Where You Can Find More Information 219 Index to Financial Statements F-1

Table of Contents

MARKET AND INDUSTRY DATA AND FORECASTS

Certain market and industry data included in this prospectus has been obtained from third-party sources that we believe to be reliable.Market estimates are calculated by using independent industry publications, government publications and third-party forecasts inconjunction with our assumptions about our markets. We have not independently verified such third-party information. While we are notaware of any misstatements regarding any market, industry or similar data presented herein, such data involves risks and uncertainties and issubject to change based on various factors, including those discussed under the headings "Forward-Looking Statements" and "Risk Factors"in this prospectus.

CERTAIN DEFINED TERMS

Except where the context suggests otherwise, references in this prospectus to (1) "NSA," "our company," "we," "us" and "our" refer toNational Storage Affiliates Trust, a Maryland real estate investment trust, together with its subsidiaries, (2) "our operating partnership" or"our operating partnership subsidiary" refer to NSA OP, LP, a Delaware limited partnership, together with its subsidiaries, and (3) "ourpredecessor" refer to the combined subsidiaries of SecurCare Self Storage, Inc. In addition, unless the context otherwise requires, thefollowing terms used throughout this prospectus have the following meanings:

CAD cash available for distribution as defined in the operating partnership agreementcommon shares our company's common shares of beneficial interest, $0.01 par value per sharecontributed portfolio with respect to each PRO, the portfolio of properties that such PRO manages on our behalf, which

were (i) contributed by such PRO to us or (ii) sourced by such PRO from a third-party seller andacquired by us

DownREIT partnerships limited partnership subsidiaries of our operating partnership that issue units of limited partnerinterest intended to be economically equivalent to the OP units and subordinated performance unitsissued by our operating partnership

exclusive MSA an MSA granted to a PRO wherein our operating partnership has agreed not to acquire additionalself-storage properties in such MSA without first offering such PRO the opportunity to co-invest in,and manage, such properties

Guardian Guardian Storage Centers, LLC and its controlled affiliatesin-place portfolio 246 self-storage properties, which includes 225 properties that we currently own, 13 properties that

we expect to acquire prior to or concurrently with the completion of this offering, and eightproperties that we expect to acquire upon the receipt of lender consents, which may occur prior to,concurrently with, or following the completion of this offering. These properties compriseapproximately 13.7 million rentable square feet and are diversified across 16 states in more than100,000 storage units

LTIP units long-term incentive plan units in our operating partnershipMove It Move It Self Storage, LP and its controlled affiliatesMSA metropolitan statistical areaNOI net operating incomenon-exclusive MSA an MSA granted to a PRO that may in the future, at the option of our operating partnership, become

a shared MSA

ii

Table of Contents

Northwest Kevin Howard Real Estate Inc., d/b/a Northwest Self Storage and its controlled affiliatesoperating partnership agreement the Third Amended and Restated Limited Partnership Agreement of our operating partnershipOptivest Optivest Properties, LLC and its controlled affiliatesOP units common equity interests in our operating partnership or DownREIT partnershipspipeline 115 self-storage properties, comprising approximately 7.5 million rentable square feet. Of these,

one is a property that our company has under contract to acquire, 30 are properties in which ourPROs have a controlling ownership interest that we have a right to acquire (i) in the event that ourPRO seeks to transfer such interest or (ii) upon maturity of outstanding indebtedness encumberingsuch property so long as the occupancy of such property is consistent with average local marketlevels at such time, 20 are properties in which our PROs currently have an ownership interest but donot control, and 64 are properties that our PROs manage without an ownership interest. With respectto the 114 properties in our pipeline that are not under contract to be acquired, there can be noassurance that definitive agreements relating to the acquisition of these properties will be enteredinto by our company and the current property owner(s). All such pipeline properties are subject toadditional due diligence by our company, the determination by us to pursue the acquisition of theproperty and the decision of the current owner(s) to contribute the property to our company. Therecan be no assurance that we will be able to acquire any of the properties in our pipeline

PROs our participating regional operators, which currently consist of Guardian, Move It, Northwest,Optivest and SecurCare, and will, upon the completion of this offering and the formationtransactions, also include Storage Solutions

same store portfolio properties owned and operated for the entirety of the applicable periods presentedSecurCare SecurCare Self Storage, Inc. and its controlled affiliatesshared MSA an MSA granted to more than one PRO wherein our operating partnership has agreed not to acquire

additional self-storage properties in such MSA without first offering one of the PROs, in ouroperating partnership's discretion, the opportunity to co-invest in, and manage, such properties, andif such first PRO declines, our operating partnership must offer the same opportunity to a differentPRO assigned to the shared MSA

subordinated performance units subordinated performance units in our operating partnership or DownREIT partnershipsStorage Solutions Arizona Mini Storage Management Company d/b/a Storage Solutions and its controlled affiliates

iii

Table of Contents

PROSPECTUS SUMMARY

This summary highlights some of the information in this prospectus. It does not contain all of the information that you should considerbefore investing in our common shares. You should carefully read the more detailed information set forth under "Risk Factors" and theother information included in this prospectus. Certain technical and other terms used in this prospectus are defined under the heading"Certain Defined Terms" on p. ii above.

Unless otherwise indicated, the information contained in this prospectus assumes that (1) the formation transactions described under"The Formation and Structure of our Company" have been completed, (2) the common shares to be sold in the offering are sold at$ per share, which is the mid-point of the initial public offering price range shown on the cover page of this prospectus, and (3) theunderwriters' option to purchase additional shares is not exercised.

Company Overview

Our Company

National Storage Affiliates Trust is a Maryland real estate investment trust focused on the ownership, operation, and acquisition ofself-storage properties located within the top 100 metropolitan statistical areas, or MSAs, throughout the United States. According to the2014 Self-Storage Almanac, we are the sixth largest owner and operator of self-storage properties and the largest privately-owned operatorof self-storage properties in the United States based on number of properties, units, and rentable square footage. Upon the completion ofthis offering and the formation transactions, our in-place portfolio of 246 self-storage properties will comprise approximately 13.7 millionrentable square feet and will be diversified across 16 states in more than 100,000 storage units. In addition, we have a pipeline of potentialadditional acquisitions consisting of 115 properties, comprising approximately 7.5 million rentable square feet.

Our chief executive officer, Arlen D. Nordhagen, co-founded SecurCare Self Storage, Inc. in 1988 to invest in and manage self-storageproperties. While growing SecurCare to over 150 self-storage properties, Mr. Nordhagen recognized a market opportunity for adifferentiated public self-storage REIT that would leverage the benefits of national scale by integrating multiple experienced regional self-storage operators with local operational focus and expertise. We believe that his vision, which is the foundation of our company, aligns theinterests of regional self-storage operators with those of public shareholders by allowing the operators to participate alongside shareholdersin the financial performance of our company and their contributed portfolios. A key component of this strategy is to capitalize on the localmarket expertise and knowledge of regional self-storage operators by maintaining the continuity of their roles as property managers.

We believe that our structure creates the right financial incentives to accomplish these objectives. We require our participatingregional operators, or PROs, to exchange the self-storage properties they contribute to our company for a combination of common equityinterests, or OP units, and subordinated performance units in our operating partnership or DownREIT partnerships. OP units, which areeconomically equivalent to our common shares, create alignment with the performance of our company as a whole. Subordinatedperformance units, which are linked to the performance of specific contributed portfolios, incentivize our PROs to drive operatingperformance and support the sustainability of the operating cash flow, generated by the contributed self-storage properties that theycontinue to manage on our behalf. Because subordinated performance unit holders receive distributions only after portfolio-specificminimum performance thresholds are satisfied, subordinated performance units play a key role in aligning the interests of our PROs with usand our shareholders. Our structure thus offers PROs a unique opportunity to serve as regional property managers for their contributedproperties and directly participate in the potential upside of those properties while simultaneously diversifying their investment to include abroader portfolio of self-storage properties. We believe our

1

Table of Contents

structure provides us with a competitive growth advantage over self-storage companies that do not offer property owners the ability toparticipate in the performance and potential future growth of their contributed portfolios.

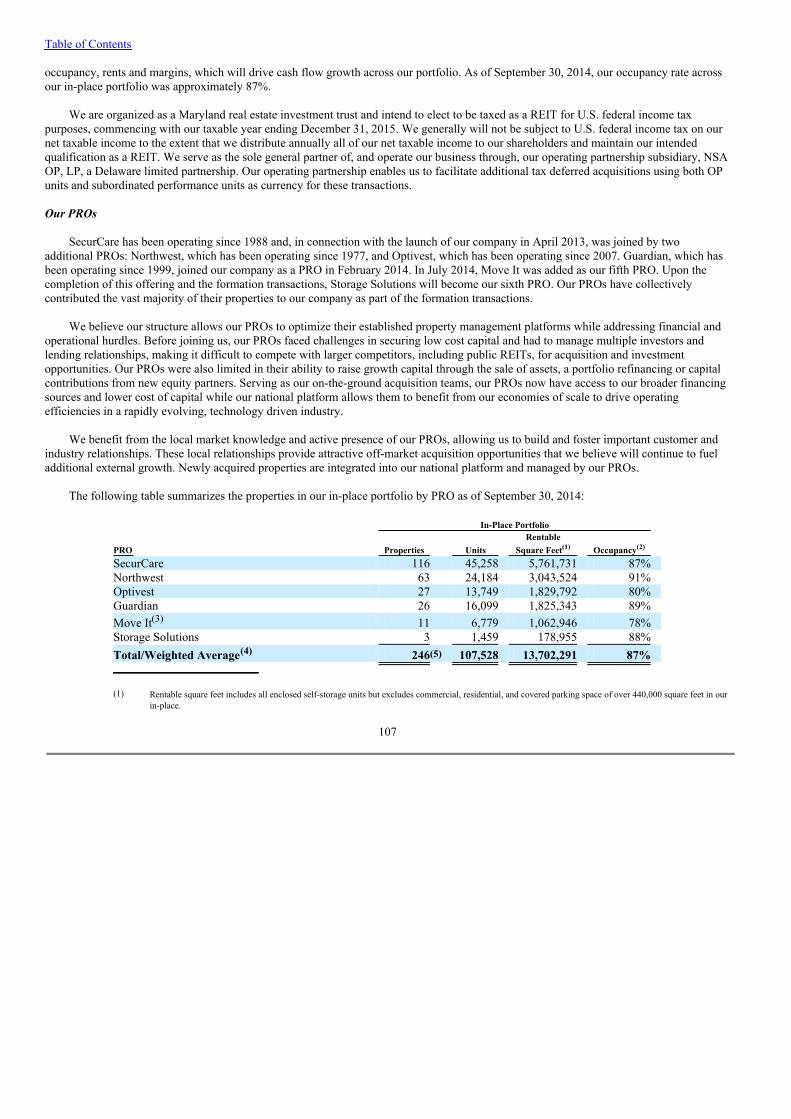

We believe that our national platform has significant potential for external and internal growth. We seek to expand our platform byrecruiting additional established self-storage operators, while integrating our operations through the implementation of centralizedinitiatives, including management information systems, revenue enhancement and cost optimization programs. We are currently engaged inpreliminary discussions with additional self-storage operators and believe that we could add several additional PROs over the next two tothree years. These additional operators will enhance our existing geographic footprint and allow us to enter regional markets in which wecurrently have limited or no market share. In addition, we believe the implementation of best practices across our portfolio and leveragingeconomies of scale will allow us to more effectively grow internally through increased occupancy, rents and margins, which will drive cashflow growth across our portfolio. As of September 30, 2014, our occupancy rate across our in-place portfolio was approximately 87%.

We are organized as a Maryland real estate investment trust and intend to elect to be taxed as a real estate investment trust for U.S.federal income tax purposes, or REIT, commencing with our taxable year ending December 31, 2015. We generally will not be subject toU.S. federal income tax on our net taxable income to the extent that we distribute annually all of our net taxable income to our shareholdersand maintain our intended qualification as a REIT. We serve as the sole general partner of, and operate our business through, our operatingpartnership subsidiary, NSA OP, LP, a Delaware limited partnership. Our operating partnership enables us to facilitate additional taxdeferred acquisitions using both OP units and subordinated performance units as currency for these transactions.

Our PROs

SecurCare has been operating since 1988 and, in connection with the launch of our company in April 2013, was joined by twoadditional PROs: Northwest, which has been operating since 1977, and Optivest, which has been operating since 2007. Guardian, which hasbeen operating since 1999, joined our company as a PRO in February 2014. In July 2014, Move It was added as our fifth PRO. Upon thecompletion of this offering and the formation transactions, Storage Solutions will become our sixth PRO. Our PROs have collectivelycontributed the vast majority of their properties to our company as part of the formation transactions.

We believe our structure allows our PROs to optimize their established property management platforms while addressing financial andoperational hurdles. Before joining us, our PROs faced challenges in securing low cost capital and had to manage multiple investors andlending relationships, making it difficult to compete with larger competitors, including public REITs, for acquisition and investmentopportunities. Our PROs were also limited in their ability to raise growth capital through the sale of assets, a portfolio refinancing or capitalcontributions from new equity partners. Serving as our on-the-ground acquisition teams, our PROs now have access to our broaderfinancing sources and lower cost of capital while our national platform allows them to benefit from our economies of scale to driveoperating efficiencies in a rapidly evolving, technology driven industry.

We benefit from the local market knowledge and active presence of our PROs, allowing us to build and foster important customer andindustry relationships. These local relationships provide attractive off-market acquisition opportunities that we believe will continue to fueladditional external growth. Newly acquired properties are integrated into our national platform and managed by our PROs.

2

Table of Contents

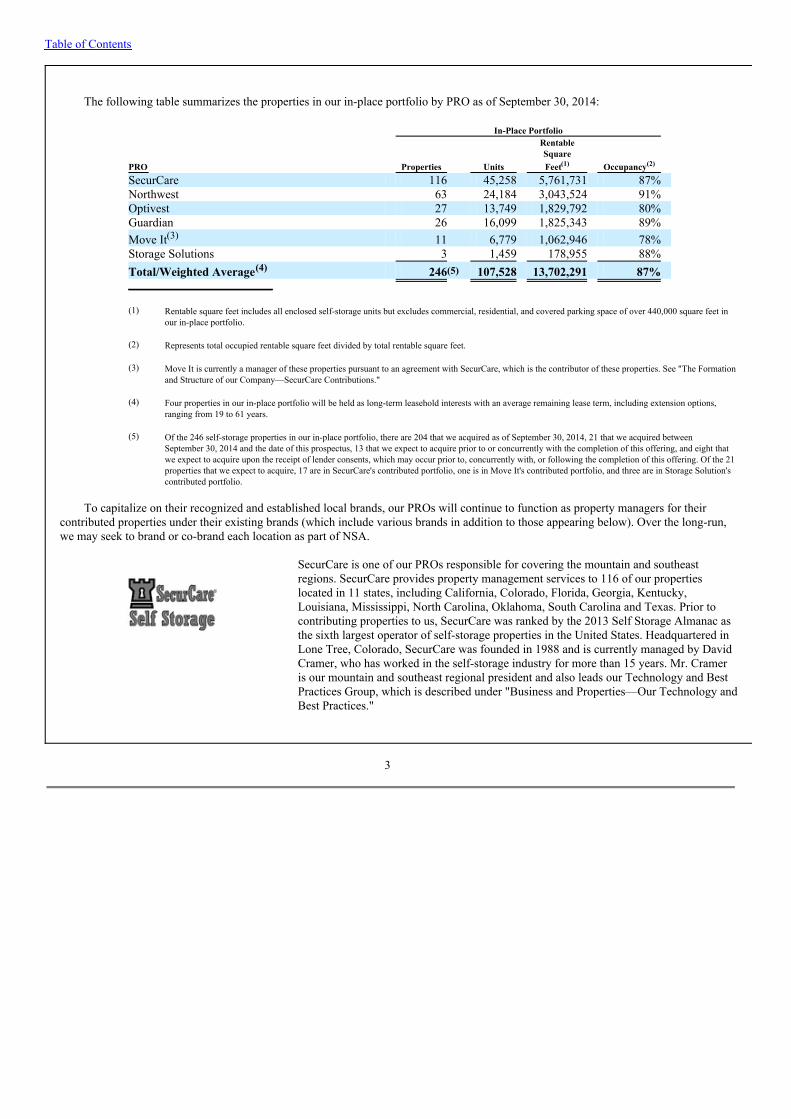

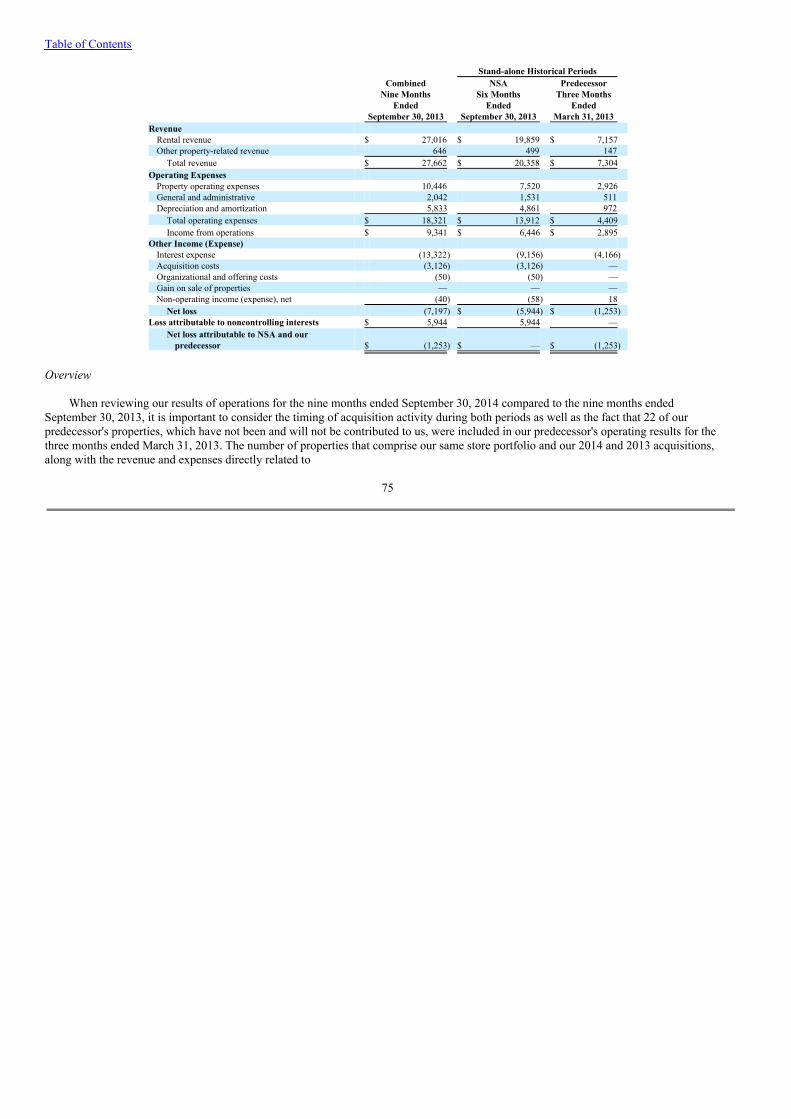

The following table summarizes the properties in our in-place portfolio by PRO as of September 30, 2014:

To capitalize on their recognized and established local brands, our PROs will continue to function as property managers for theircontributed properties under their existing brands (which include various brands in addition to those appearing below). Over the long-run,we may seek to brand or co-brand each location as part of NSA.

SecurCare is one of our PROs responsible for covering the mountain and southeastregions. SecurCare provides property management services to 116 of our propertieslocated in 11 states, including California, Colorado, Florida, Georgia, Kentucky,Louisiana, Mississippi, North Carolina, Oklahoma, South Carolina and Texas. Prior tocontributing properties to us, SecurCare was ranked by the 2013 Self Storage Almanac asthe sixth largest operator of self-storage properties in the United States. Headquartered inLone Tree, Colorado, SecurCare was founded in 1988 and is currently managed by DavidCramer, who has worked in the self-storage industry for more than 15 years. Mr. Crameris our mountain and southeast regional president and also leads our Technology and BestPractices Group, which is described under "Business and Properties—Our Technology andBest Practices."

3

In-Place Portfolio

PRO Properties Units

RentableSquareFeet(1) Occupancy(2)

SecurCare 116 45,258 5,761,731 87% Northwest 63 24,184 3,043,524 91% Optivest 27 13,749 1,829,792 80% Guardian 26 16,099 1,825,343 89% Move It(3) 11 6,779 1,062,946 78% Storage Solutions 3 1,459 178,955 88%

Total/Weighted Average(4) 246(5) 107,528 13,702,291 87%

(1) Rentable square feet includes all enclosed self-storage units but excludes commercial, residential, and covered parking space of over 440,000 square feet inour in-place portfolio.

(2) Represents total occupied rentable square feet divided by total rentable square feet.

(3) Move It is currently a manager of these properties pursuant to an agreement with SecurCare, which is the contributor of these properties. See "The Formationand Structure of our Company—SecurCare Contributions."

(4) Four properties in our in-place portfolio will be held as long-term leasehold interests with an average remaining lease term, including extension options,ranging from 19 to 61 years.

(5) Of the 246 self-storage properties in our in-place portfolio, there are 204 that we acquired as of September 30, 2014, 21 that we acquired betweenSeptember 30, 2014 and the date of this prospectus, 13 that we expect to acquire prior to or concurrently with the completion of this offering, and eight thatwe expect to acquire upon the receipt of lender consents, which may occur prior to, concurrently with, or following the completion of this offering. Of the 21properties that we expect to acquire, 17 are in SecurCare's contributed portfolio, one is in Move It's contributed portfolio, and three are in Storage Solution'scontributed portfolio.

Table of Contents

Northwest is our PRO responsible for covering the northwest region. Northwest providesproperty management services to 63 of our properties located in Oregon and Washington.Prior to contributing properties to us, Northwest was ranked by the 2014 Self StorageAlmanac as the 16th largest operator of self-storage properties in the United States.Headquartered in Portland, Oregon, Northwest is run by Kevin Howard, who founded thecompany over 30 years ago. Mr. Howard is our northwest regional president and isrecognized in the industry for his successful track record as a self-storage specialist in theareas of design and development, operation and property management, consultation, andbrokerage.

Optivest is one of our PROs responsible for covering the southwest region. Based in DanaPoint, California, Optivest currently manages 27 of our properties across five states,including Arizona, California, Nevada, New Hampshire and Texas. Prior to contributingproperties to us, Optivest was ranked by the 2014 Self Storage Almanac as the 21st largestoperator of self-storage properties in the United States. Optivest is run by its co-founder,Warren Allan, who has more than 25 years of financial and operational managementexperience in the self-storage industry. Mr. Allan is our southwest regional president and isrecognized as a self-storage acquisition and development specialist.

Guardian Storage Centers Guardian is one of our PROs responsible for covering portions of the southern Californiaregion and the Arizona market. Based in Irvine, California, Guardian currently manages26 of our properties located in California and Arizona. Prior to contributing properties tous, according to guidance from Guardian, if the 2014 Self Storage Almanac had reportedits size, it would have been ranked as the 36th largest operator of self-storage properties inthe United States. This operator is led by John Minar, who has over 30 years of self-storage acquisition and operational management experience. Mr. Minar is our southernCalifornia regional president and brings close to 40 years of real estate acquisition,rehabilitation, ownership, and development experience to our company.

Move It is one of our PROs responsible for covering certain portions of the Texas market.Based in Addison, Texas, Move It currently manages 11 of our properties in Texas. Priorto contributing properties to us, Move It was ranked by the 2014 Self Storage Almanac asthe 34th largest operator of self-storage properties in the United States. This operator is ledby its founder, Tracy Taylor, who has more than 40 years of experience in self-storagedevelopment, acquisition and management. Mr. Taylor is our Texas market executive vicepresident and is currently on the board of directors for the Large Owners Council of theSelf Storage Association.

4

Table of Contents

Storage Solutions, upon the completion of this offering and the formation transactions,will be our PRO responsible for covering most of the Arizona market. Based in Chandler,Arizona, Storage Solutions manages three of our properties in Arizona. Prior tocontributing properties to us, Storage Solutions was ranked by the 2014 Self StorageAlmanac as the 29th largest operator of self-storage properties in the United States. Thisoperator is led by its founder, Bill Bohannan, who is one of the largest operators inPhoenix and has more than 34 years of self-storage acquisition, development andmanagement experience. Mr. Bohannan is our Arizona market executive vice presidentand is recognized in the industry as a self-storage acquisition, development andmanagement specialist.

Each PRO representative who serves as regional president or executive vice president of our company receives no compensation fromus for serving in these roles.

Our Competitive Strengths

We believe our unique PRO structure allows us to differentiate ourselves from other self-storage operators, and the followingcompetitive strengths enable us to effectively compete against our industry peers:

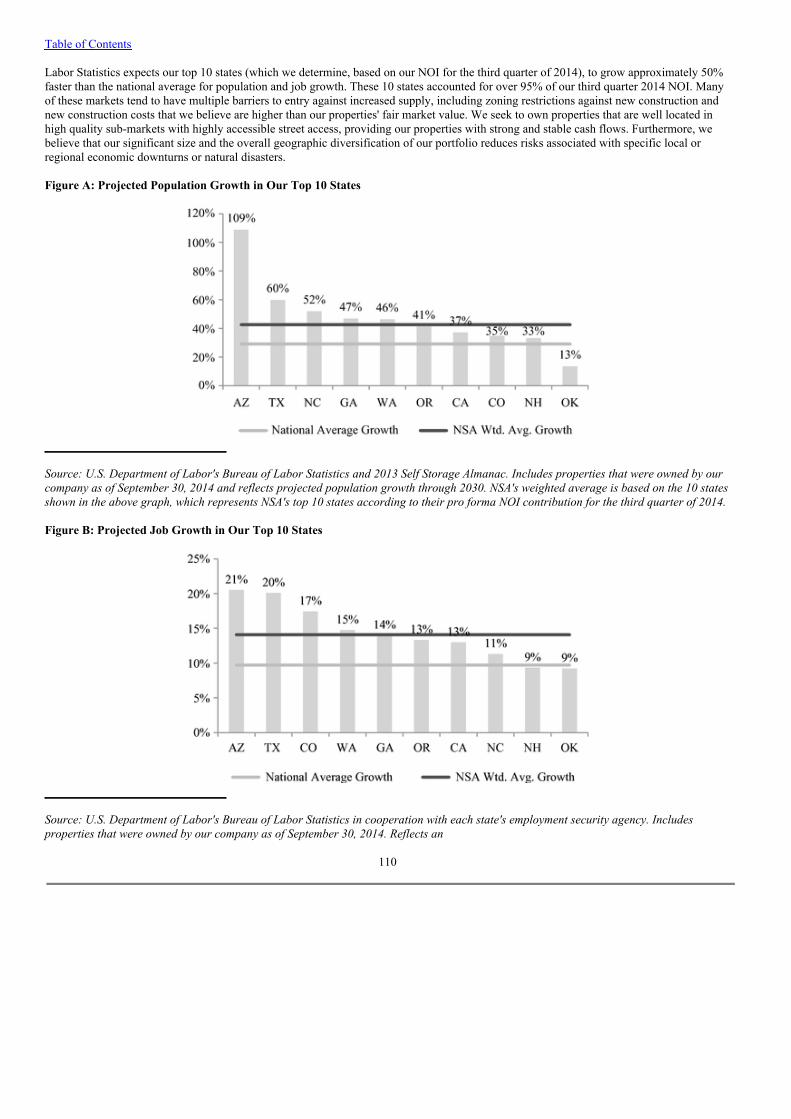

High Quality Properties in Key Growth Markets. Upon the completion of this offering and the formation transactions, we expect toown a large, geographically diversified portfolio of 246 self-storage properties, which includes 225 properties that we currently own, 13properties that we expect to acquire prior to or concurrently with the completion of this offering, and eight properties that we expect toacquire upon the receipt of lender consents, which may occur prior to, concurrently with, or following the completion of this offering.These properties are located in 16 states and over 50 MSAs. Over % of our in-place portfolio is located in the top 100 MSAs based onnet operating income, or NOI, for the third quarter of 2014. We believe that these properties are primarily located in high quality growthmarkets that have attractive supply and demand characteristics and are less sensitive to the fluctuations of the general economy. The U.S.Department of Labor's Bureau of Labor Statistics expects our top 10 states (which we determine based on our NOI for the third quarter of2014), to grow approximately 50% faster than the national average for population and job growth. These 10 states accounted for over 95%of our third quarter 2014 NOI. Many of these markets tend to have multiple barriers to entry against increased supply, including zoningrestrictions against new construction and new construction costs that we believe are higher than our properties' fair market value. We seekto own properties that are well located in high quality sub-markets with highly accessible street access, providing our properties with strongand stable cash flows. Furthermore, we believe that our significant size and the overall geographic diversification of our portfolio reducesrisks associated with specific local or regional economic downturns or natural disasters.

Differentiated, Growth Oriented Strategy Focused on Established Operators. We are a self-storage REIT with a unique structurethat supports our differentiated external growth strategy. Our structure appeals to operators who are looking for access to growth capitalwhile maintaining an economic stake in the self-storage properties that each has contributed to our company and continues to manage onour behalf. These attributes entice operators to join our company rather than sell their properties for cash consideration. Our strategy is toattract operators who are confident in the performance of their properties and desire to participate in the future growth of our company. Weare focused on recruiting established institutional operators across the United States with a history of efficient property management and atrack record of successful acquisitions. Our structure and differentiated strategy

5

Table of Contents

have enabled us to build a substantial pipeline from existing operators as well as potentially create external growth from future operators.

Integrated Platform Utilizing Advanced Technology for Enhanced Operational Performance and Best Practices. Our nationalplatform allows us to capture cost savings through integration and centralization, thereby eliminating redundancies and utilizing economiesof scale across the property management platforms of our PROs. As compared to a stand-alone operator, our national platform has greateraccess to lower-cost capital, reduced Internet marketing costs per customer lead, discounted property insurance expense, and reducedoverhead costs. In addition, our company has sufficient scale for national and bulk purchasing and has centralized various functions,including financial reporting, call center operations, marketing, information technology, legal support, and capital market functions, toachieve substantial cost savings over smaller, individual operators.

Our national platform utilizes advanced technology for Internet marketing, call center operations, financial and property analyticdashboards, revenue optimization analytics and expense management tools to enhance operational performance. These centralizedprograms, which are run through our Technology and Best Practices Group, are positively impacting our business performance, and webelieve that they will be a driver of organic growth going forward. We will utilize our Technology and Best Practices Group to help usbenefit from the collective sharing of key operating strategies among our PROs in areas like human resource management, local marketingand operating procedures.

Aligned Incentive Structure with Shareholder Downside Protection. Our structure promotes operator accountability assubordinated performance units issued to our PROs in exchange for the contribution of their properties are entitled to distributions onlyafter those properties satisfy minimum performance thresholds. In the event of a material reduction in operating cash flow, distributions onour subordinated performance units will be reduced before distributions on our common shares held by our common shareholders. Inaddition, we expect our PROs will generally co-invest subordinated equity in the form of subordinated performance units in eachacquisition that they source, and the value of these subordinated performance units will fluctuate with the performance of their contributedproperties. Therefore, our PROs are incentivized to select acquisitions that are expected to exceed minimum performance thresholds,thereby increasing the value of their subordinated equity stake. We expect that our shareholders will benefit from the higher levels ofproperty performance that our PROs are incentivized to deliver.

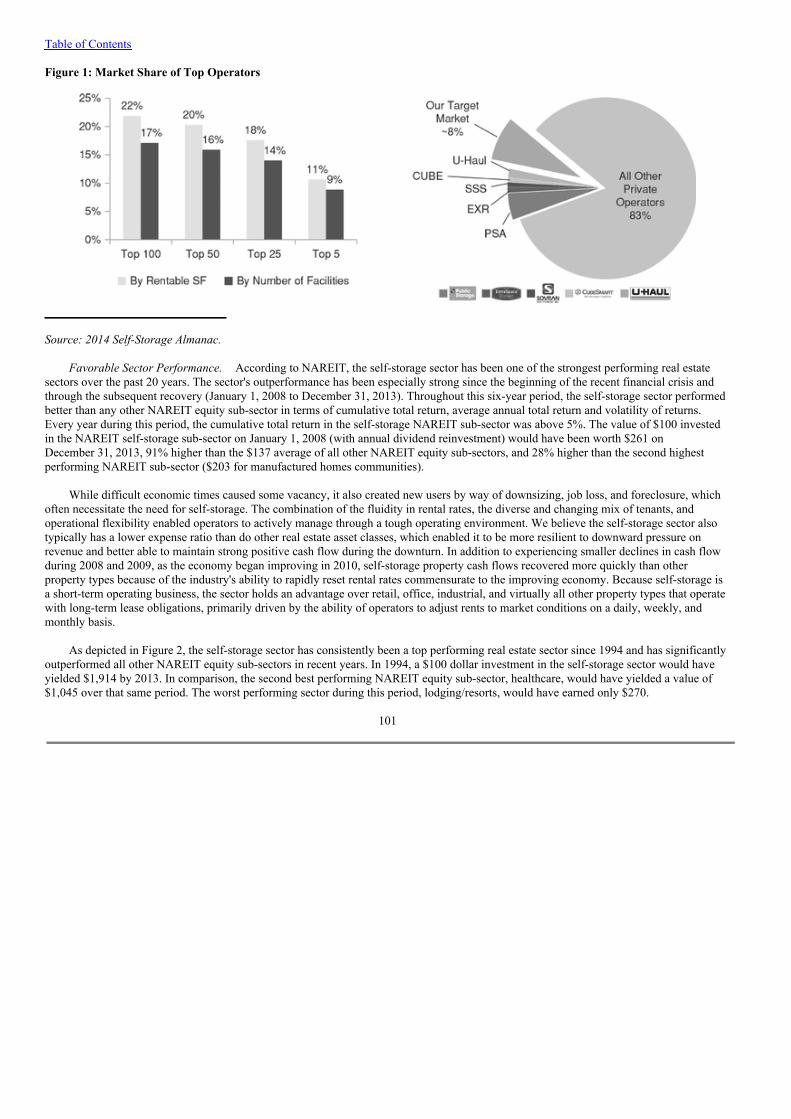

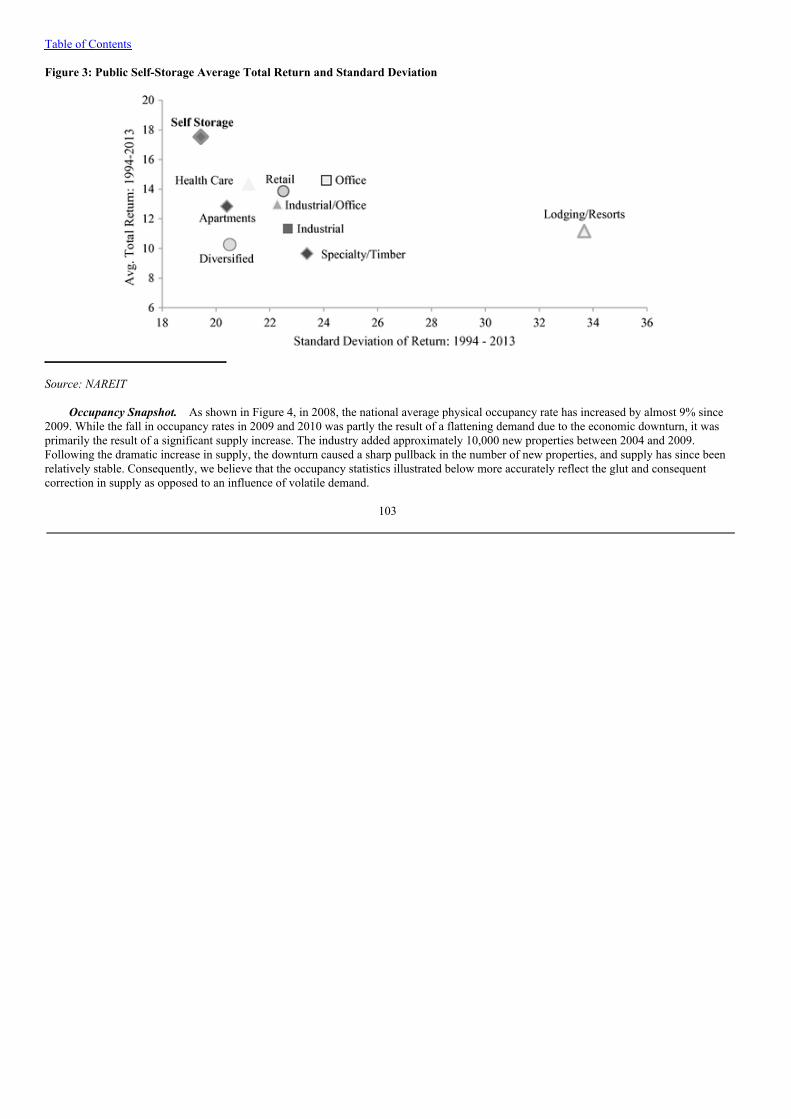

Attractive Sector with Strong Underlying Fundamentals and Historic Outperformance. Self-storage industry fundamentals arerobust, with many properties operating at optimal revenue-producing occupancy and favorable industry dynamics resulting in pricing powerfor self-storage operators. Operators are able to achieve high same-store occupancy levels through a diverse base of customer demand fromindividuals as well as businesses. As of September 30, 2014, according to industry sources, the industry average of same-store occupancywas 85%. Based on these favorable supply and demand dynamics, we believe that disciplined self-storage operators will generate revenuegrowth in the near term and will continue to drive revenue performance throughout various economic cycles. We believe that overheadcosts and maintenance capital expenditures are considerably lower in the self-storage industry as compared to other real estate sectors, andas a result, self-storage companies are able to achieve comparatively higher operating and cash flow margins. The self-storage sector'sfundamentals have consistently established it as one of the strongest performing sectors among all classes of real estate over the last twentyyears. The National Association of Real Estate Investment Trusts, or NAREIT, has tracked total return performance of the real estate equitysector since 1994, and from that time through December 31, 2013, the self-storage equity REIT sector has returned an average of over 17%on an annual total return basis compared to the average annual total return of approximately 12% for all other equity REIT sectors.

Experienced Senior Management Team with Deep Operating and Public Company Experience. Our senior management team hasan established executive leadership track record, aided by their extensive

6

Table of Contents

knowledge of the self-storage sector and experience in the ownership, management, and development of self-storage properties. Our chiefexecutive officer, Arlen D. Nordhagen, and chief financial officer, Tamara D. Fischer, bring accomplished backgrounds with an average of25 years of experience in multiple management capacities at both public and private companies. As a successful entrepreneur involved inthe start-up and growth of several public and private companies, Mr. Nordhagen was one of the founders of SecurCare in 1988 and led thecompany through a period of rapid growth. In addition to SecurCare, Mr. Nordhagen was a founder of MMM Healthcare, Inc., the largestprovider of Medicare Advantage health insurance in Puerto Rico. He has also served as managing member of various private investmentfunds and held various managerial positions at E. I. DuPont De Nemours and Company, or DuPont, and Synthetech, Inc. Ms. Fischer alsobrings substantial managerial and public company experience to us. Prior to joining us, Ms. Fischer was executive vice president and chieffinancial officer of Vintage Wine Trust Inc., a REIT formed for the purpose of providing triple-net lease financing to owners and operatorsof wineries, vineyards, and other wine-related facilities. Ms. Fischer also served as executive vice president and chief financial officer ofChateau Communities Inc., one of the largest public REITs in the manufactured home community sector. In that capacity, Ms. Fischeroversaw the company's initial public offering, multiple merger and acquisition transactions, as well as ongoing capital markets activities,investor relations, financial reporting, and administrative responsibilities. Ms. Fischer remained at Chateau through its sale to HometownAmerica LLC in 2003.

Our seasoned PROs also have highly experienced management teams averaging over 30 years of industry experience as well as deepindustry knowledge of key markets and extensive national networks of industry relationships.

• David Cramer, a principal of SecurCare, joined the company in 1998, and has more than 15 years of experience in the self-storage industry, growing SecurCare's portfolio from 20 properties to over 150 properties during his tenure. He is an activemember of the Large Owners Council of the Self Storage Association and is a board member of FindLocalStorage.com, anindustry digital marketing consortium.

• Kevin Howard, a principal of Northwest, founded the company in 1977 and built it into one of the largest privately-ownedportfolios of self-storage properties in the Pacific Northwest. He was one of the earliest members of the Self StorageAssociation in the mid-1970s, serving on its board of directors during several of the early years of its existence.

• Warren Allan, principal of Optivest, has over 25 years of financial and operational management experience, during whichtime he helped structure over 25 real estate partnerships to acquire self-storage properties in various regions nationwide. Priorto founding Optivest in 2007, Mr. Allan served as both chief operating officer and chief financial officer of another self-storage management company, Platinum Storage, since its founding in 2000.

• John Minar, principal of Guardian, has been involved in the self-storage industry since 1984. Mr. Minar formed Guardian in1999 and is the owner and manager of Guardian's portfolio, which has properties located in southern California and Arizona.Mr. Minar has been involved in the acquisition, rehabilitation, ownership, and development of real estate since 1977, and isactive in the Large Owners Council of the Self Storage Association.

• Tracy Taylor, principal of Move It, has been involved in the self-storage industry for more than 40 years. He founded MoveIt and is the manager of Move It's portfolio, which has properties in Texas, Tennessee and North Carolina. He served on theboard of directors of the Self Storage Association from 2006 through 2011, serving as chairman of the board in 2010. He hasalso served on the board of directors for the Large Owners Council of the Self Storage Association since 2012.

7

Table of Contents

• Bill Bohannan, principal of Storage Solutions, has been involved in the self-storage industry for more than 30 years and isone of the largest operators of self-storage properties in the Phoenix, Arizona MSA. A recognized industry expert,Mr. Bohannan has been a speaker, and has instructed various courses, for the Self Storage Association for several years.

We believe our deep and cohesive management structure has the relevant skills and experience necessary to effectively grow ourcompany. Upon the completion of this offering and the formation transactions, we expect that our senior management team, including ourchief executive officer, representatives of our PROs who serve on our board of trustees and PRO advisory committee, and our chieffinancial officer, will own approximately % of our equity on a fully diluted basis.

Our Business and Growth Strategies

By capitalizing on our competitive strengths, we seek to increase scale, achieve optimal revenue-producing occupancy and rent levels,and increase long-term shareholder value by achieving sustainable long-term growth. Our business and growth strategies to achieve theseobjectives are as follows:

Increase Occupancy of In-Place Portfolio. Existing public self-storage REITs were operating with a weighted average occupancylevel of approximately 92% as of September 30, 2014, which we believe is at or near optimal revenue-producing occupancy. Our in-placeportfolio occupancy was approximately 87% as of September 30, 2014, reflecting a gap of approximately 5% compared to the averageoccupancy of the existing public self-storage REITs. Through utilization of our centralized call centers, integrated Internet marketingstrategies and best practices protocols, we expect our PROs will be able to increase rental conversion rates resulting in increasing occupancylevels. We believe that a 1% improvement in our average occupancy for our in-place portfolio will translate to an approximate $1.3 millionimprovement in revenue. We would expect a similar increase in NOI subject to marginal increases in operating expenses.

Maximize Property Level Cash Flow. We strive to maximize the cash flows at our properties by leveraging the economies of scaleprovided by our national platform, including through the implementation of new ideas derived from our Technology and Best PracticesGroup. We believe that our unique PRO structure, centralized infrastructure and efficient national platform will enable us to achieveoptimal market rents and occupancy, reduce operating expenses and increase the sale of ancillary products and services, including tenantinsurance, rental moving equipment and packing supplies.

Acquire Built-in Pipeline of Target Properties from Existing PROs. We have an attractive, high quality pipeline of 115 self-storageproperties, one of which is a development property under contract comprising approximately 20,000 rentable square feet that we expect toacquire in late 2016 once occupancy reaches average local market levels and financial performance is acceptable. The other 114 propertiesin our pipeline represent potential acquisitions, comprising approximately 7.5 million rentable square feet, that we anticipate will drive ourfuture growth. We consider a property to be in our pipeline if (i) it is under a management service agreement with one of our PROS, (ii) itmeets the property quality criteria described under "The Formation and Structure of our Company—Valuation Methodology forContributed Portfolios," and (iii) it is either required to be offered to us under the applicable facilities portfolio management agreement or aPRO has a reasonable basis to believe that the owner of the property intends to sell the property in the next seven years.

8

Table of Contents

The following table summarizes the properties in our pipeline by PRO as of September 30, 2014:

Our PROs have management service agreements with all of the properties in our pipeline and hold controlling ownership interests in30 of these properties and non-controlling ownership interests in 20 of these properties. With respect to each property in our pipeline inwhich a PRO holds a controlling ownership interest, such PRO has agreed that it will not transfer (or permit the transfer of, to the extentpossible) any interest in such self-storage property without first offering or causing to be offered (if permissible) such interest to us. Inaddition, upon maturity of the outstanding mortgage indebtedness encumbering such property, so long as occupancy is consistent with orexceeds average local market levels, which we determine in our sole discretion, such PRO has agreed to offer or cause to be offered (ifpermissible) such interest to us. With respect to pipeline properties in which our PROs have a non-controlling ownership interest or noownership interest, each PRO has agreed to use commercially reasonable good faith efforts to facilitate our purchase of such property. Wepreserve the discretion to accept or reject any of the properties that our PROs are required to, or elect to, offer (or cause to be offered) to us.See "The Formation and Structure of Our Company—Facilities Portfolio and Asset Management Agreements—Controlled PropertiesPurchase Option Upon PRO Determination to Transfer" and "—Non-Controlled Properties Notice and Facilitation."

The following table summarizes, by each category of property in our pipeline, the years in which we expect to either acquire, have anoffer to acquire, or make an offer to acquire such properties.

We have organized our pipeline into annual time periods in the above table based on our assessment of (i) the pending maturity datesof the mortgages encumbering such properties or when pre-payment of such mortgage is economical, (ii) our PROs' understanding, asmanagers of these

9

Pipeline

PRO Properties Units Rentable

Square Feet(1) SecurCare 25 12,339 1,539,921 Northwest 7 2,170 269,579 Optivest 24 13,531 1,633,331 Guardian 8 6,121 709,825 Move It 21 10,091 1,396,069 Storage Solutions 30 18,095 1,953,818

Total(2) 115 62,347 7,502,543

(1) Rentable square feet includes all enclosed self-storage units but excludes commercial, residential, and covered parking space of over 35,000 squarefeet in our pipeline.

(2) Two properties in our pipeline, if acquired, would be held as long-term leasehold interests.

Pipeline

Under

Contract

PRO ControllingOwnershipInterest(1)

PRO Non-controllingOwnership

Interest

PROwithout

OwnershipInterest Total

2015 — 3 15 20 38 2016 1 10 5 40 56 2017 — 7 — 2 9 2018 and beyond — 10 — 2 12

Total 1 30 20 64 115

(1) Two properties in our pipeline, if acquired, would be held as long-term leasehold interests.

Table of Contents

properties, as to when the owners of the controlling interests in these properties might be interested in selling, and/or (iii) a particularproperty having occupancy consistent with average local market levels, along with acceptable financial performance. For 26 of the 30properties in which our PROs have a controlling ownership interest, properties are organized into annual time periods based primarily onthe pending maturity dates of the underlying mortgages. The remaining four of these 30 properties are development properties that areincluded in annual time periods based on our estimate as to when each such property is expected to have occupancy consistent with averagelocal market levels and acceptable financial performance.

With respect to the 84 pipeline properties in which our PROs have a non-controlling ownership interest or no ownership interest, wehave included 45 of such properties into annual time periods based primarily on the pending maturity dates of their underlying mortgagesand one such development property in an annual time period based on our estimate as to when such property is expected to have occupancyconsistent with average local market levels and acceptable financial performance. The annual time periods for the remaining 38 propertiesare based largely on our PROs' understanding as to when the owners of the controlling interests in these properties might be interested inselling their properties.

For all of the 114 potential acquisitions in our pipeline, we have not entered into negotiations with the respective owners and there canbe no assurance as to whether we will acquire any of these properties or the actual timing of any such acquisitions. Each pipeline propertyis subject to additional due diligence and the determination by us to pursue the acquisition of the property. In addition, with respect to the84 pipeline properties in which our PROs have a non-controlling ownership interest or no ownership interest, the current owner of eachproperty is not required to offer such property to us and there can be no assurance that we will acquire these properties.

Access Additional Off-Market Acquisition Opportunities. Our PROs and their "on-the-ground" personnel have established anextensive network of industry relationships and contacts in their respective markets. Through these local connections, our PROs are able toaccess acquisition opportunities that are not publicly marketed or sold through auctions. Our structure incentivizes our PROs to sourceacquisitions in their markets and consolidate these properties into our company. Other public self-storage companies generally haveacquisition teams located at their central offices, which in many instances are far removed from regional and local markets. We believe ouroperators' networks and close familiarity with the other operators in their markets provide us clear competitive advantages in identifyingand selecting attractive acquisition opportunities. Our PROs have already sourced 47 acquisitions since our inception, comprisingapproximately 3.2 million rentable square feet within our in-place portfolio.

Recruit New PROs in Target Markets. We intend to continue to execute on our external growth strategy through additionalacquisitions and contributions from future PROs in key markets. With the approximately 50,000 total self-storage properties in the UnitedStates owned by over 30,000 operators, we believe there is significant opportunity for growth through consolidation of the highlyfragmented composition of the market. We believe that future operators will be attracted to our unique structure, providing them with lowercost of capital, better economies of scale, and greater operational and overhead efficiencies while preserving their existing propertymanagement platforms. Over ten private operators, each with portfolios of over 20 properties, have expressed interest in exploring thepossibility of joining our company as future PROs. We have not entered into any agreements with these operators in respect of them joiningour company or contributing their properties to us and there can be no assurance that we will enter into any such agreements in the future.We intend to add additional PROs to complement our existing geographic footprint and to achieve our goal of creating a highly diversifiednationwide portfolio of properties in the top 100 MSAs. When considering a PRO candidate, we consider various factors, including the sizeof the potential PRO's portfolio, its market exposure, its operating expertise, its ability to grow its business, and its reputation with industryparticipants. Following our inception, we recruited an additional three PROs who managed 112 self-storage properties across seven

10

Table of Contents

states, 40 of which are part of our in-place portfolio. For example, we recruited Move It, which manages 42 self-storage properties in fourstates. This PRO manages 11 properties in our in-place portfolio and 21 in our pipeline.

Our Technology and Best Practices

Our technology and best practices programs, which are overseen by our Technology and Best Practices Group, are designed to takeadvantage of the scale and sophistication afforded to a large national storage operator while benefiting from the local expertise andrelationships of experienced PROs. These programs deliver value for us and our PROs through a number of methods, tools, and platforms:(1) a common data platform for financial, operational, and marketing data collection, reporting, analysis and dissemination, (2) a commononline marketing platform to deliver economies of scale for Internet search rankings and customer lead generation, (3) a centralized callcenter supporting property operations, (4) a joint purchasing program for products such as property insurance, retail merchandise, officesupplies, merchant credit and debit card processing, and online auction services in order to achieve economies of scale, and (5) a forum forsharing management techniques and engaging in high-level collaboration across decentralized operations.

Our unique structure allows for effective best practices collaboration among our experienced PROs. We provide the methods, tools,and platforms for our PROs to share management techniques and resources with each other in order to promote greater experimentation,faster iteration, and a level of flexibility not easily achieved by large competitors operating in a more monolithic fashion. These techniquesspan the spectrum of property management from employee training, sourcing, and retention to operational audits, selling techniques, dataanalytics, document digitization, and the pursuit of additional revenue streams such as rooftop solar and cellular antenna contracts. Webelieve that over time, the open sharing of best practices will deliver consistent, incremental organic improvements and drive betterfinancial results throughout our portfolio.

The Formation and Structure of Our Company

Upon the completion of this offering and the formation transactions, our in-place portfolio will consist of 246 self-storage propertieslocated in 16 states, comprising approximately 13.7 million rentable square feet. Of these properties, four will be held as long-termleasehold interests with an average remaining lease term, including extension options, ranging from 19 to 61 years.

Acquisition of In-Place Portfolio. For our in-place portfolio, pursuant to separate contribution agreements described under "TheFormation and Structure of our Company—Contribution Agreements," we have issued or expect to issue in connection with the formationtransactions an aggregate of million units of limited partner interest in our operating partnership or in DownREIT partnerships in whichour operating partnership owns a significant investment, consisting of million OP units in our operating partnership, million OPunits in our DownREIT partnerships, million subordinated performance units in our operating partnership, and million subordinatedperformance units in our DownREIT partnerships. The properties included in our in-place portfolio by our PROs were or will becontributed pursuant to a policy adopted by our board of trustees that standardizes the methodology that we use for valuing self-storageproperties that are contributed to us by our PROs. See "The Formation and Structure of our Company—Valuation Methodology forContributed Portfolios." In connection with these transactions, we assumed or will assume an aggregate of approximately $65.8 million ofmortgage indebtedness. In addition, we have acquired an aggregate of 47 properties, which were sourced by our PROs, pursuant to purchaseand sale agreements with certain third-party owners for a combination of cash and OP units totalling approximately $201 million. Inconnection with these acquisitions, we assumed or will assume an aggregate of approximately $34.5 million of mortgage indebtedness. Asof September 30, 2014, our operating partnership had also granted an additional 220,000 LTIP units to a third-party consultant and

11

Table of Contents

1.7 million LTIP units to our PROs under the Prior Incentive Plan. See "Our Management—Prior Incentive Plan."

Facilities Portfolio and Asset Management Agreements. Each self-storage property that was contributed to our operatingpartnership or one of its subsidiaries by a PRO will continue to be managed by the PRO that contributed the property. Each PRO hasentered into a facilities portfolio management agreement with us with respect to its contributed portfolio together with asset managementagreements for each property. We believe this consistency in post-contribution portfolio and property management, together with ourtechnology and best practices programs, will allow us to fully leverage each PRO's local market knowledge and expertise and mitigatetransitional disruptions to operations. Pursuant to the asset management agreements, the PROs receive reimbursements for certain expensesand a market rate supervisory and administrative fee for their services, which in total will be not less than 5% nor more than 6% of grossrevenue generated by each property that they manage for us. Each facilities portfolio management agreement also contains a number ofterms relating to, among other things, exclusivity and non-competition, management and retirement (including the "Key Person Standards"described below under "—Key Person Standards"), and performance. For a further description of the terms of the facilities portfolio andasset management agreements, see "The Formation and Structure of Our Company—Facilities Portfolio and Asset ManagementAgreements."

Assignment of PRO Territories. Our company plans to primarily rely on our PROs to source acquisitions of self-storage propertiesfrom third-party sellers that operate in the same regional and local markets as our PROs. However, under some circumstances, we maylearn about an acquisition opportunity from a source other than a PRO within an exclusive MSA or non-exclusive MSA granted to suchPRO. In such circumstances, pursuant to the facilities portfolio management agreements, our operating partnership has agreed not to acquireadditional self-storage properties without first offering such PRO the opportunity to co-invest in, and manage, the property in its assignedMSA. In shared MSAs, where more than one PRO is assigned, the operating partnership is permitted to choose the PRO that will get the co-investment and management opportunity. This permits us to reward a PRO that sources an acquisition for us. In the event that a PROdetermines not to accept a co-investment and management opportunity, our operating partnership must offer the same opportunity to adifferent PRO assigned to the shared MSA. If all PROs in an MSA decline the opportunity, we are free to enter into alternative co-investment and management arrangements.

• SecurCare is assigned 18 exclusive MSAs within Colorado, Georgia, Louisiana, North Carolina, Oklahoma, South Carolina,and Texas, five shared MSAs within California and Texas, and one non-exclusive MSA within Georgia.

• Northwest is assigned five exclusive MSAs within Oregon and one non-exclusive MSA in Washington.

• Optivest is assigned two exclusive MSAs within Arizona and New Hampshire and seven shared MSAs within Arizona,California, Nevada, and Texas.

• Guardian is assigned one exclusive MSA within California and three shared MSAs within Arizona and California.

• Move It is assigned four exclusive MSAs within Texas, five shared MSAs within Texas, and one non-exclusive MSA withinTennessee.

• Storage Solutions is assigned two shared MSAs within Arizona and Nevada.

Each PRO is prohibited from entering into new agreements or arrangements for self-storage properties that they do not currently ownor manage without our operating partnership's prior written consent. In addition to the reimbursements of expenses and fees paid under theasset management

12

Table of Contents

agreements, we also pay our PROs an insignificant underwriting and due diligence fee in connection with the sourcing of third-partyacquisitions. We do not intend to pay our PROs any other fees.

Company Lock-out Periods. We utilize a number of different lock-out periods with respect to our PROs' equity interests in order tomaintain their long-term incentive to continue to improve and grow the portfolio of properties that they contributed to us.

• Subordinated Performance Unit Conversion. PROs are restricted from converting any of their subordinated performanceunits into OP units for a minimum of two years from the later of the completion of this offering or the initial contribution oftheir properties to us. Following such two-year period, other than in connection with a retirement event, a PRO may onlyconvert subordinated performance units into OP units upon the achievement of certain performance thresholds and at aspecified conversion discount. See "Limited Partnership Agreement of our Operating Partnership—Conversion ofSubordinated Performance Units into OP Units."

• Retirement. PROs are prevented from "retiring" for a minimum of two years from the later of completion of this offering orthe initial contribution of their properties to us. Upon certain retirement events, the management of the properties in suchPRO's contributed portfolio will be transferred to us (or our designee) in exchange for OP units with a value equal to fourtimes the average of the normalized annual EBITDA from the management contracts related to such PRO's contributedportfolio over the immediately preceding 24-month period. See "Formation and Structure of our Company—FacilitiesPortfolio and Asset Management Agreements—Management and Retirement."

• Redemption. Existing holders of OP units in our operating partnership, including our PROs, are restricted from redeemingtheir OP units for a minimum of one year from the completion of this offering. See "Limited Partnership Agreement of ourOperating Partnership—Redemption of OP Units." Existing holders of OP units in our DownREIT partnerships have alonger lock-out period before they can redeem. See "The Formation and Structure of our Company—DownREITPartnerships."

Key Person Standards. Each facilities portfolio management agreement contains provisions, which we refer to as the "Key PersonStandards," which relate to each PRO's key persons (as defined in each facilities portfolio management agreement). Our operatingpartnership, in its sole discretion, may consent to changes in the key persons designated with respect to each PRO from time to time.Pursuant to the facilities portfolio management agreements, each PRO's key persons are required to remain active in and devote a sufficientportion of each such person's business time to the business and affairs of the PRO with respect to such PRO's contributed portfolio which isconsistent with past practice. In addition, other than as a result of death or legal incapacity, at least 50% of the subordinated performanceunits issued in respect of each PRO's contributed portfolio are required to be beneficially owned by such PRO's key persons and such keypersons are required to collectively own at least 50% of the beneficial interest in and control the management company relating to thecontributed portfolio. We may elect to terminate our facilities portfolio and asset management agreements and transfer propertymanagement responsibilities over the properties managed by a PRO to us (or our designee), if, subject to specified cure provisions, a PRObreaches its Key Person Standards. Upon termination of the facilities portfolio management agreement for a PRO in the case of breach ofKey Person Standards, we will be permitted to require that the subordinated performance units issued in respect of such PRO's contributedportfolio be converted into OP units applying a specified conversion penalty on the terms described herein under "Limited PartnershipAgreement of our Operating Partnership—Conversion of Subordinated Performance Units into OP Units." See "The Formation andStructure of our Company—Management and Retirement" and "—Performance."

13

Table of Contents

Registration Rights Agreements. We have granted registration rights to those persons who will be eligible to receive commonshares issuable upon exchange of OP units (or securities exchangeable for OP units) issued in our formation transactions. The registrationrights agreement requires that as soon as practicable after the date on which we first become eligible to register the resale of securities ofour company pursuant to Form S-3 under the Securities Act, but in no event later than 60 calendar days thereafter, we file a shelfregistration statement registering the offer and resale of the common shares issuable upon exchange of OP units (or securities exchangeablefor OP units) issued in our formation transactions on a delayed or continuous basis. See "Shares Eligible for Future Sale—RegistrationRights Agreement."

Our Structure

The following diagram illustrates our anticipated structure upon the completion of this offering and the formation transactions:

(1) In addition to PROs, various third-party investors who do not manage the properties and certain of our trustees and officers will own OP units and subordinated performanceunits in our operating partnership.

(2) OP units in our operating partnership are redeemable for cash or, at our option, exchangeable for common shares on a one-for-one basis, subject to certain adjustments.

(3) As disclosed under "Limited Partnership Agreement of our Operating Partnership—Conversion of Subordinated Performance Units into OP Units," subordinated performanceunits are only convertible into OP units, beginning two years following the completion of this offering and then only upon (i) the achievement of certain performance thresholdsrelating to the properties to which such subordinated performance units relate or (ii) upon a retirement event of a PRO that holds such subordinated performance units.Consequently, subordinated performance units will not initially be taken into account in calculating our earnings allocable to common shareholders or our diluted earnings pershare, and we have not included such subordinated performance units in the percentage calculations included in the above chart. However, if such subordinated performanceunits were convertible into OP units as of September 30, 2014, we estimate that the subordinated performance units outstanding as of that date would convert into anaggregate of OP units. The basis and assumptions underlying this estimate are described under "Limited Partnership Agreement of our Operating Partnership—Conversion of Subordinated Performance Units into OP Units." The actual number of OP units into which

14

Table of Contents

subordinated performance units will become convertible two years after the completion of this offering may vary significantly.

(4) OP units in our DownREIT partnerships are redeemable for cash or, at our option, exchangeable for OP units in our operating partnership on a one-for-one basis, subject tocertain adjustments.

(5) Subordinated performance units in our DownREIT partnerships are exchangeable for subordinated performance units in our operating partnership on a one-for-one basis on theterms set forth in the DownREIT partnership's organizational documents, which are then convertible into OP units in our operating partnership as specified in note 3 to this chartabove.

The diagram above excludes (i) up to common shares that we may issue and sell upon the exercise of the underwriters' optionto purchase additional shares, (ii) common shares available for future issuance under our 2015 Equity Incentive Plan, as describedunder "Our Management—2015 Equity Incentive Plan", (iii) 2.7 million OP units issuable upon conversion of 2.7 million outstanding LTIPunits and (iv) OP units issuable upon conversion of outstanding subordinated performance units. For a description of the termsrelated to the conversion of subordinated performance units into OP units, including the application of the conversion penalty, see "LimitedPartnership Agreement of our Operating Partnership—Conversion of Subordinated Performance Units into OP Units."

We believe that our structure provides meaningful advantages, including the strong alignment of financial incentives between PROsand shareholders, accelerated acquisition growth opportunities and a disciplined approach to new acquisitions.

Our Properties

Our PROs have contributed high quality portfolios of self-storage properties that are designed to offer customers convenient,affordable, and secure storage units. Generally, our properties are in highly visible locations clustered in states or markets with strongpopulation and job growth and are specifically designed to accommodate residential and commercial tenants with features such as securitysystems, electronic gate entry, easy access, climate control, and pest control. Our units typically range from 25 square feet to 300 squarefeet, and some of our properties also offer outside storage for vehicles, boats, and equipment. We provide 24-hour access to many storageunits through computer controlled access systems, as well as alarm and sprinkler systems on many of our individual storage units. Ourportfolio upon the completion of this offering and the formation transactions is expected to have more than 100,000 storage units, almost allof which are leased on a month-to-month basis providing us the flexibility to increase rental rates over time as market conditions permit.

15

Table of Contents

The following map depicts the geographic diversification of our in-place portfolio and pipeline as of September 30, 2014:

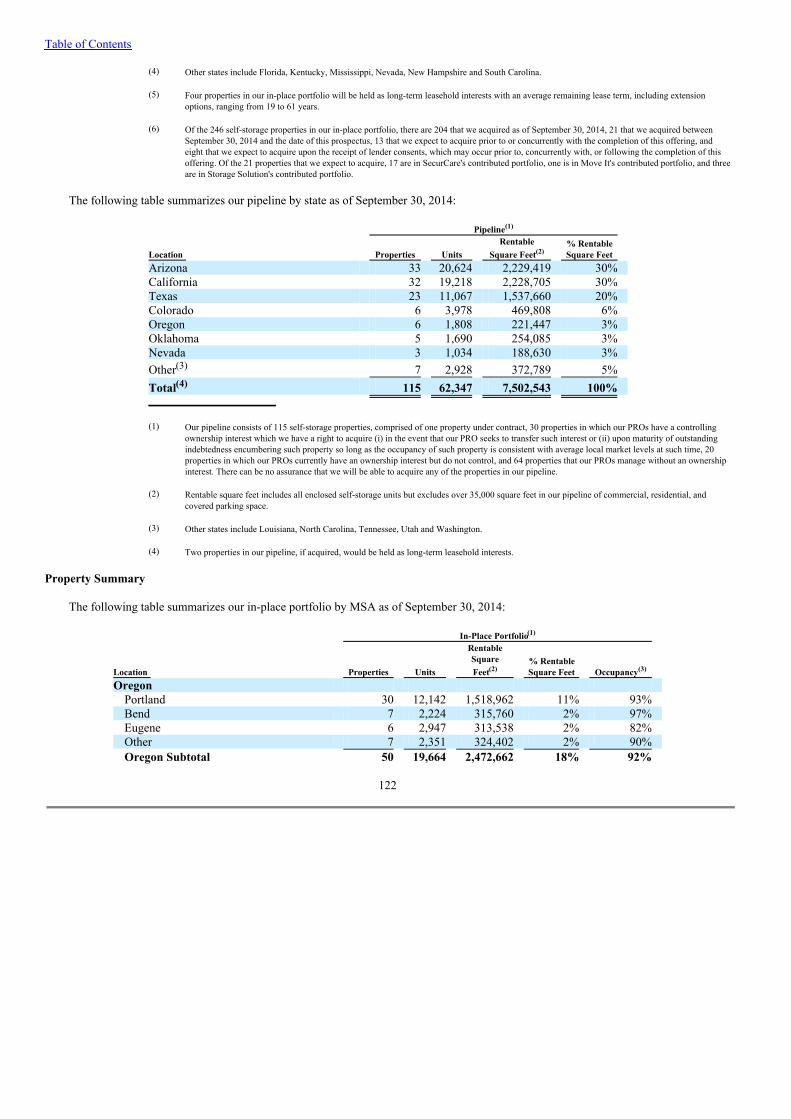

The following table summarizes information about our in-place portfolio by state as of September 30, 2014:

16

In-Place Portfolio

Location Properties Units Rentable

Square Feet(1) % RentableSquare Feet Occupancy(2)

Pro FormaAnnualized

EffectiveRental

Revenue perSquare Foot(3)

Oregon 50 19,664 2,472,662 18% 92% $ 10.86 Texas 46 18,034 2,526,945 18% 83% $ 8.89 California 28 16,597 2,012,570 15% 86% $ 11.95 North Carolina 27 12,273 1,493,619 11% 86% $ 9.43 Oklahoma 26 12,248 1,630,477 12% 87% $ 8.37 Georgia 16 5,305 678,351 5% 85% $ 7.47 Arizona 13 7,337 833,631 6% 84% $ 10.92 Washington 13 4,520 570,862 4% 90% $ 9.52 Colorado 8 3,741 453,166 3% 91% $ 10.98 Louisiana 5 2,281 318,860 2% 85% $ 7.68 Other(4) 14 5,528 711,148 5% 83% $ 8.98

Total/WeightedAverage(5) 246(6) 107,528 13,702,291 100% 87% $ 9.84

(1) Rentable square feet includes all enclosed self-storage units but excludes over 440,000 square feet in our in-place portfolio of commercial, residential, andcovered parking space.

(2) Represents total occupied rentable square feet divided by total rentable square feet.

Table of Contents

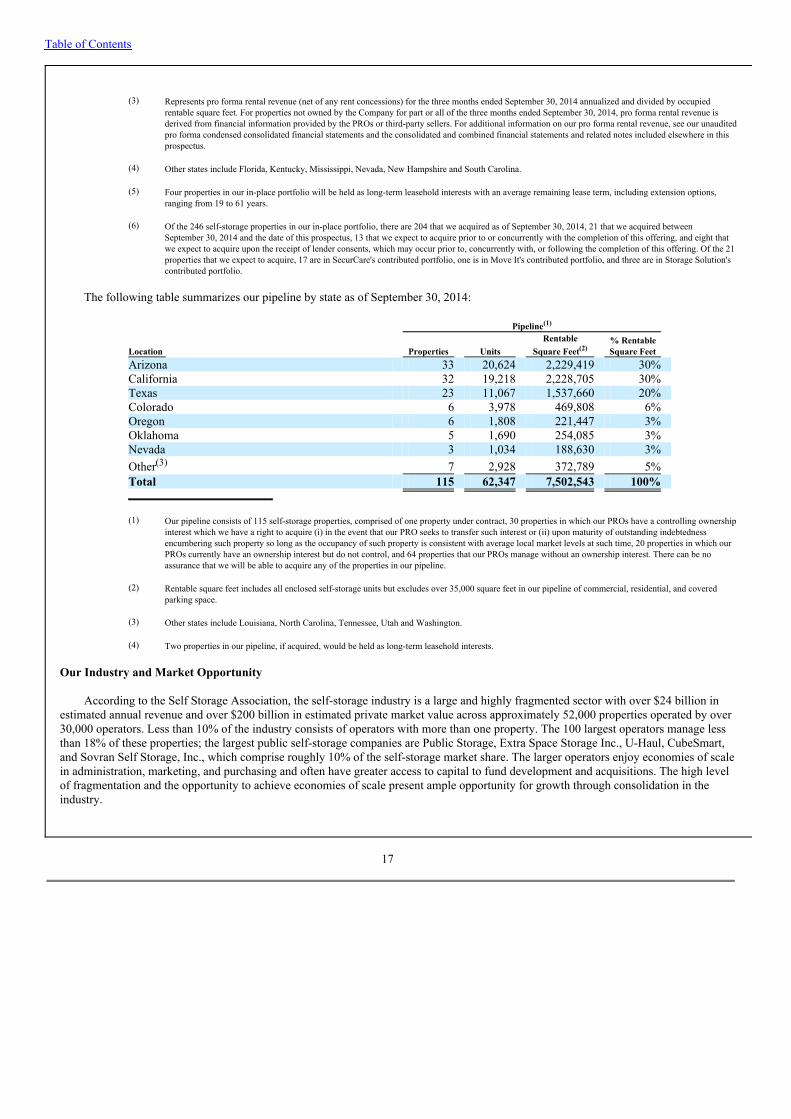

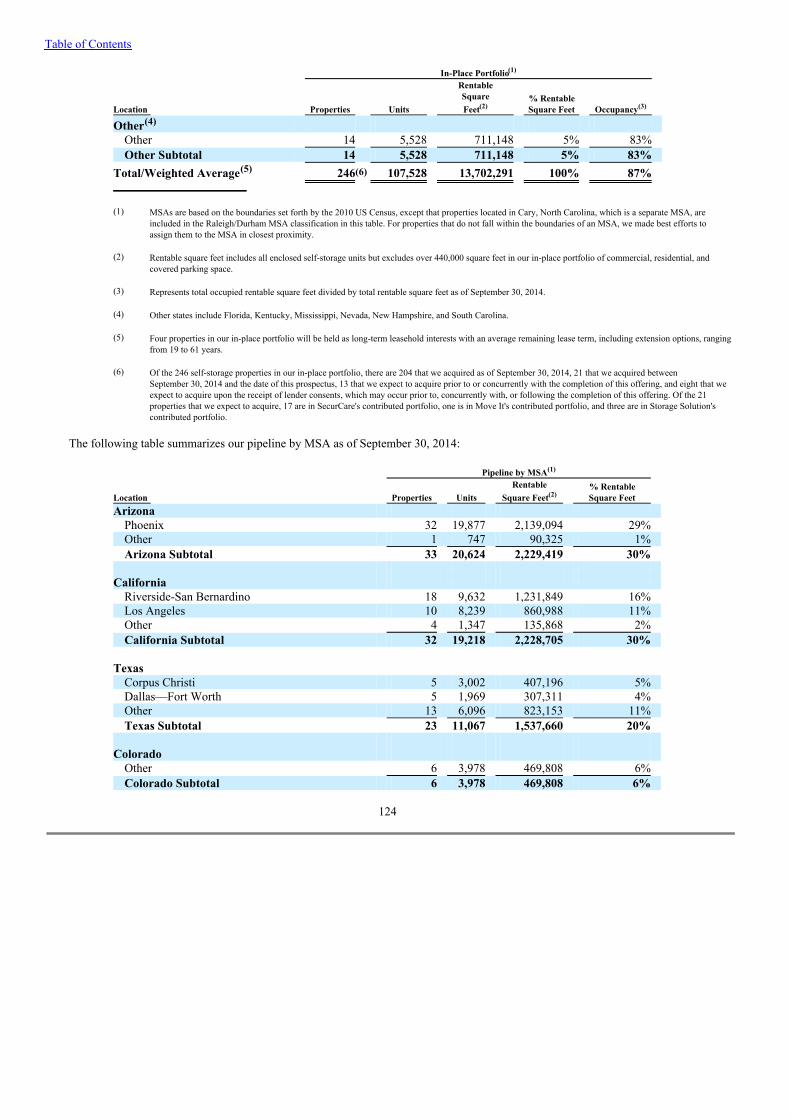

The following table summarizes our pipeline by state as of September 30, 2014:

Our Industry and Market Opportunity

According to the Self Storage Association, the self-storage industry is a large and highly fragmented sector with over $24 billion inestimated annual revenue and over $200 billion in estimated private market value across approximately 52,000 properties operated by over30,000 operators. Less than 10% of the industry consists of operators with more than one property. The 100 largest operators manage lessthan 18% of these properties; the largest public self-storage companies are Public Storage, Extra Space Storage Inc., U-Haul, CubeSmart,and Sovran Self Storage, Inc., which comprise roughly 10% of the self-storage market share. The larger operators enjoy economies of scalein administration, marketing, and purchasing and often have greater access to capital to fund development and acquisitions. The high levelof fragmentation and the opportunity to achieve economies of scale present ample opportunity for growth through consolidation in theindustry.

17

(3) Represents pro forma rental revenue (net of any rent concessions) for the three months ended September 30, 2014 annualized and divided by occupiedrentable square feet. For properties not owned by the Company for part or all of the three months ended September 30, 2014, pro forma rental revenue isderived from financial information provided by the PROs or third-party sellers. For additional information on our pro forma rental revenue, see our unauditedpro forma condensed consolidated financial statements and the consolidated and combined financial statements and related notes included elsewhere in thisprospectus.

(4) Other states include Florida, Kentucky, Mississippi, Nevada, New Hampshire and South Carolina.

(5) Four properties in our in-place portfolio will be held as long-term leasehold interests with an average remaining lease term, including extension options,ranging from 19 to 61 years.

(6) Of the 246 self-storage properties in our in-place portfolio, there are 204 that we acquired as of September 30, 2014, 21 that we acquired betweenSeptember 30, 2014 and the date of this prospectus, 13 that we expect to acquire prior to or concurrently with the completion of this offering, and eight thatwe expect to acquire upon the receipt of lender consents, which may occur prior to, concurrently with, or following the completion of this offering. Of the 21properties that we expect to acquire, 17 are in SecurCare's contributed portfolio, one is in Move It's contributed portfolio, and three are in Storage Solution'scontributed portfolio.

Pipeline(1)

Location Properties Units Rentable

Square Feet(2) % RentableSquare Feet

Arizona 33 20,624 2,229,419 30% California 32 19,218 2,228,705 30% Texas 23 11,067 1,537,660 20% Colorado 6 3,978 469,808 6% Oregon 6 1,808 221,447 3% Oklahoma 5 1,690 254,085 3% Nevada 3 1,034 188,630 3% Other(3) 7 2,928 372,789 5%

Total 115 62,347 7,502,543 100%

(1) Our pipeline consists of 115 self-storage properties, comprised of one property under contract, 30 properties in which our PROs have a controlling ownershipinterest which we have a right to acquire (i) in the event that our PRO seeks to transfer such interest or (ii) upon maturity of outstanding indebtednessencumbering such property so long as the occupancy of such property is consistent with average local market levels at such time, 20 properties in which ourPROs currently have an ownership interest but do not control, and 64 properties that our PROs manage without an ownership interest. There can be noassurance that we will be able to acquire any of the properties in our pipeline.

(2) Rentable square feet includes all enclosed self-storage units but excludes over 35,000 square feet in our pipeline of commercial, residential, and coveredparking space.

(3) Other states include Louisiana, North Carolina, Tennessee, Utah and Washington.

(4) Two properties in our pipeline, if acquired, would be held as long-term leasehold interests.

Table of Contents

According to NAREIT, the self-storage sector has been one of the strongest-performing real estate sectors over the past 20 years. Thesector's outperformance has been especially strong since the beginning of the recent financial crisis and through the subsequent recovery(January 1, 2008 to December 31, 2013). Throughout this six-year period, the self-storage sector performed better than any other NAREITequity sub-sector in terms of cumulative total return, average annual total return and volatility of returns. Every year during this period, thecumulative total return in the self-storage NAREIT sub-sector was above 5%. The value of $100 invested in the NAREIT self-storage sub-sector on January 1, 2008 (with annual dividend reinvestment) would have been worth $261 on December 31, 2013, 91% higher than the$137 average of all other NAREIT equity sub-sectors, and 28% higher than the second highest performing NAREIT sub-sector ($203 formanufactured home communities).

While difficult economic times caused some vacancy, it also created new users by way of downsizing, job loss, and foreclosure, whichoften necessitate the need for self-storage. The combination of the fluidity in rental rates, the diverse and changing mix of tenants, andoperational flexibility enabled operators to actively manage through a tough operating environment. We believe the self-storage sector alsotypically has a lower expense ratio than do other real estate asset classes, which enabled it to be more resilient to downward pressure onrevenue and better able to maintain strong positive cash flow during the downturn. In addition to experiencing smaller declines in cash flowduring 2008 and 2009, as the economy began improving in 2010, self-storage property cash flows recovered more quickly than otherproperty types because of the industry's ability to rapidly reset rental rates commensurate with the improving economy. Because self-storage is a short-term operating business, the sector holds an advantage over retail, office, industrial, and virtually all other property typesthat operate with long-term lease obligations, primarily driven by the ability of operators to adjust rents to market conditions on a daily,weekly, and monthly basis.

Indebtedness Outstanding Upon the Completion of this Offering and the Formation Transactions