national philanthropy day state laws that charitable organizations should know november 1, 2012 hugh...

TRANSCRIPT

National Philanthropy DayNational Philanthropy Day

State Laws that CharitableState Laws that Charitable

Organizations Should KnowOrganizations Should Know

November 1, 2012

Hugh R. Jones

Tax & Charities Division

There are Various Sources of the There are Various Sources of the AG’s Authority in this AreaAG’s Authority in this Area

Common LawCommon Law State Statutes:State Statutes:

Ch. 414D: Hawaii Nonprofit Corp. ActCh. 414D: Hawaii Nonprofit Corp. Act Ch. 467B: Charitable Solicitation ActCh. 467B: Charitable Solicitation Act Ch. 517E: UPMIFACh. 517E: UPMIFA Ch. 323D: Hospital AcquisitionsCh. 323D: Hospital Acquisitions Ch. 431: Charitable Gift AnnuitiesCh. 431: Charitable Gift Annuities Ch. 554 Trust ProceedingsCh. 554 Trust Proceedings

Common Law AuthorityCommon Law Authority

Common Law AuthorityCommon Law Authority

Common Law Authority: Hawaii Common Law Authority: Hawaii Statement of the LawStatement of the Law

The function of the attorney general, as parens The function of the attorney general, as parens patriae of charitable trusts, is to oversee the patriae of charitable trusts, is to oversee the activities of the trustees to the end that the trust is activities of the trustees to the end that the trust is performed and maintained in accordance with the performed and maintained in accordance with the provisions of the trust document, and to bring any provisions of the trust document, and to bring any abuse or deviation on the part of the trustees to the abuse or deviation on the part of the trustees to the attention of the court for correction attention of the court for correction Hite v. Queen's Hospital, 36 Haw. 250, 262 (1942)Hite v. Queen's Hospital, 36 Haw. 250, 262 (1942). The . The authority of the attorney general over charitable authority of the attorney general over charitable trusts does not extend beyond the performance of trusts does not extend beyond the performance of that function. M. R. Fremont-Smith, Foundations and that function. M. R. Fremont-Smith, Foundations and Government, 198 (1965). Government, 198 (1965).

Midkiff v. KobayashiMidkiff v. Kobayashi, 54 Haw. 299 (1973), 54 Haw. 299 (1973)

Standing to Enforce Charitable Standing to Enforce Charitable TrustsTrusts

Generally, only the Attorney General has Generally, only the Attorney General has standing to enforce the terms of a standing to enforce the terms of a charitable trust.charitable trust.

The Hawaii Supreme Court adopted a The Hawaii Supreme Court adopted a narrow exception in the case:narrow exception in the case: Where a breach of trust Where a breach of trust Kapiolani Park TrustKapiolani Park Trust is is

brought to the attention of the AG and the AG brought to the attention of the AG and the AG does not bring the breach to the court’s does not bring the breach to the court’s attention for correction, the Court will recognize attention for correction, the Court will recognize the standing of a third party as a “relator.”the standing of a third party as a “relator.”

Common Law AuthorityCommon Law Authority

Its generally accepted that the Attorney Its generally accepted that the Attorney General is the only person with legal General is the only person with legal standing to enforce a charitable gift or a standing to enforce a charitable gift or a donor restricted giftdonor restricted gift

Generally donors and third parties do not Generally donors and third parties do not have standinghave standing

Corporate Charities (Not Trusts)Corporate Charities (Not Trusts)

The State’s nonprofit corporation act gives The State’s nonprofit corporation act gives the Attorney General significant oversight the Attorney General significant oversight tools over charities that exist in corporate tools over charities that exist in corporate form (“Public Benefit Corporations”).form (“Public Benefit Corporations”). Power to seek judicial removal of directors who Power to seek judicial removal of directors who

have breached their duties or where the have breached their duties or where the corporation is no longer able to perform its corporation is no longer able to perform its functions. HRS 414D-140functions. HRS 414D-140

The AG has power to review “Conflicts’ The AG has power to review “Conflicts’ transactions. HRS sec. 414D-150transactions. HRS sec. 414D-150

Corporate Charities (Not Trusts)Corporate Charities (Not Trusts)

Public Benefit Corporations must give notice of Public Benefit Corporations must give notice of their intent to dissolve to the Attorney General. their intent to dissolve to the Attorney General. HRS sec. 414D-233HRS sec. 414D-233

Public Benefit Corporations must give notice of Public Benefit Corporations must give notice of their intent to sell or transfer substantially all their intent to sell or transfer substantially all their assets. HRS sec. 414D-222their assets. HRS sec. 414D-222

Public Benefit Corporations must give notice of Public Benefit Corporations must give notice of their intent to Merge to the Attorney general if their intent to Merge to the Attorney general if the survivor of the merger will into be another the survivor of the merger will into be another Public Benefit Corporation. HRS sec. 414D-211Public Benefit Corporation. HRS sec. 414D-211

Private Foundations

Hawaii’s nonprofit corporation’s act provides that a private foundations must not:

Subject the foundation to the tax under IRC section 4942 Non engage in any act of self-dealing as defined in IRC section

4941(d) Not retain any excess business holdings as defined in IRC

section 4943(c) Not make any investments in such manner to subject the

corporation to tax under section 4944 (Jeopardy Investments) Not make any taxable expenditures as defined in IRC section

4945(d)(Lobbying, political intervention, grants to individuals)

Loans to Officers and Directors

Hawaii’s nonprofit corporation’s act prohibits loans to officers and directors:

§414D-151 Loans to or guaranties for directors and officers. (a) A corporation may not lend money to or guaranty the obligation of a director or officer of the corporation.

(b) The fact that a loan or guaranty is made in violation of this section shall not affect the borrower's liability on the loan.

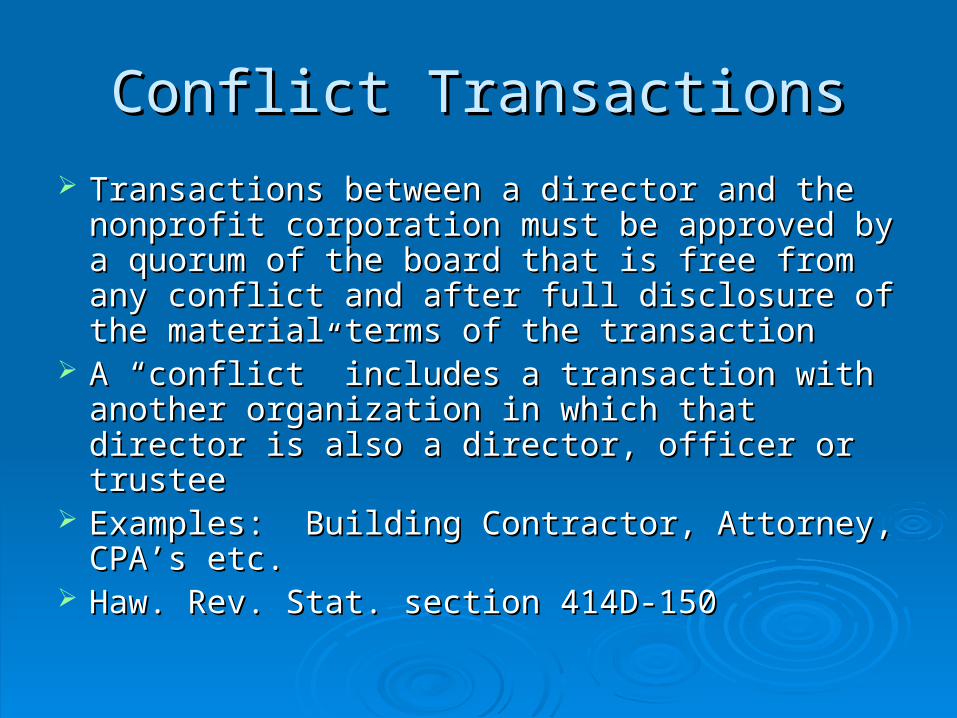

Conflict TransactionsConflict Transactions

Transactions between a director and the Transactions between a director and the nonprofit corporation must be approved by a nonprofit corporation must be approved by a quorum of the board that is free from any conflict quorum of the board that is free from any conflict and after full disclosure of the material terms of and after full disclosure of the material terms of the transactionthe transaction

A “conflict” includes a transaction with another A “conflict” includes a transaction with another organization in which that director is also a organization in which that director is also a director, officer or trusteedirector, officer or trustee

Examples: Building Contractor, Attorney, CPA’s Examples: Building Contractor, Attorney, CPA’s etc.etc.

Haw. Rev. Stat. section 414D-150Haw. Rev. Stat. section 414D-150

Uniform Prudent Management of Uniform Prudent Management of Institutional Funds Act (UPMIFA)Institutional Funds Act (UPMIFA)

Chapter 517E, HRSChapter 517E, HRS Applies to “Endowments”Applies to “Endowments”

Ex. I give $100,000 to the UH Foundation, Ex. I give $100,000 to the UH Foundation, the Income of the Income of whichwhich is to be used to endow a chair at the School of is to be used to endow a chair at the School of Veterinary Medicine.Veterinary Medicine.

UMPIFA allow the appropriation of “corpus” if the UMPIFA allow the appropriation of “corpus” if the Trustees act prudently.Trustees act prudently.

UPMIFA allows for “non judicial cy pres” with AG UPMIFA allows for “non judicial cy pres” with AG Consent where the size of the fund is less than Consent where the size of the fund is less than $250,000. HRS sec. 517E-6$250,000. HRS sec. 517E-6

Otherwise must seek judicial approval of release of Otherwise must seek judicial approval of release of restrictionrestriction

Hospital AcquisitionsHospital Acquisitions Ch. 323D, HRSCh. 323D, HRS In the 1980’s there was a wave of acquisitions of In the 1980’s there was a wave of acquisitions of

nonprofit hospitals by large hospital chainsnonprofit hospitals by large hospital chains Acquisition of Blue Cross Blue Shield Plans and Acquisition of Blue Cross Blue Shield Plans and

Managed Care SystemsManaged Care Systems Purpose of Oversight is to Insure that Charitable Purpose of Oversight is to Insure that Charitable

Assets Remain Protected by the Sale and Continue to Assets Remain Protected by the Sale and Continue to be Devoted to Charitybe Devoted to Charity

Some of these transactions involved Golden Some of these transactions involved Golden Parachutes and other Excessive Benefits to Insiders.Parachutes and other Excessive Benefits to Insiders.

Usually results in the formation of a Foundation to Usually results in the formation of a Foundation to hold the Sale Proceedshold the Sale Proceeds

Hospital AcquisitionsHospital Acquisitions

§323D-72 Acquisition of hospital. §323D-72 Acquisition of hospital. (a) (a) No person shall engage in the acquisition No person shall engage in the acquisition of a hospital without first:of a hospital without first:

(1) Applying for and receiving the (1) Applying for and receiving the approval of the agency; andapproval of the agency; and

(2) Notifying the attorney general and, (2) Notifying the attorney general and, if applicable, receiving approval from the if applicable, receiving approval from the attorney general pursuant to this part.attorney general pursuant to this part.

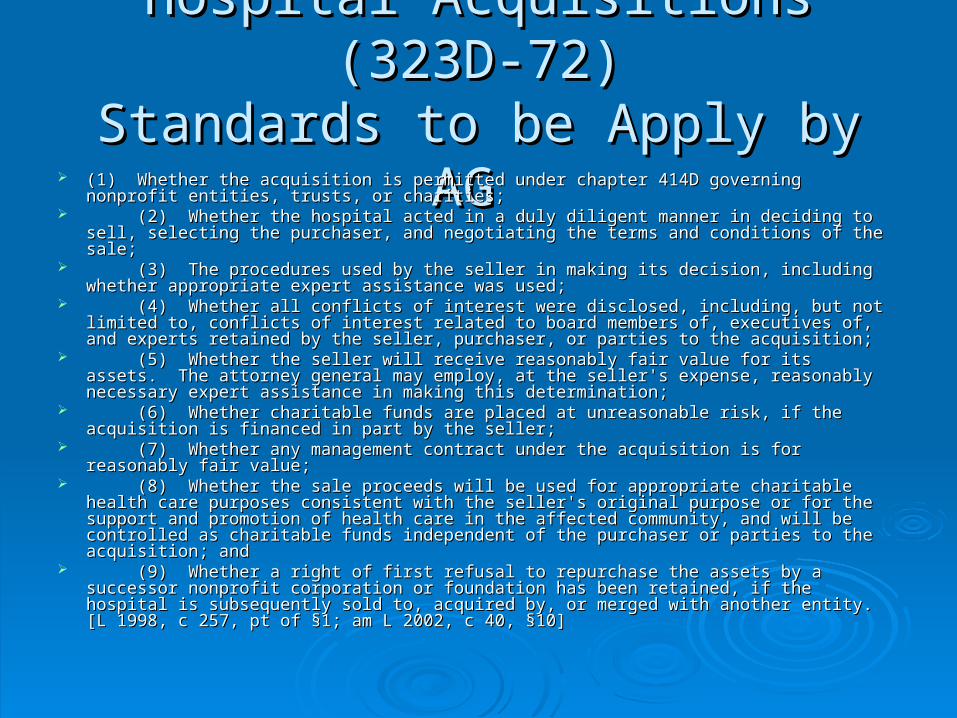

Hospital Acquisitions (323D-72)Hospital Acquisitions (323D-72)Standards to be Apply by AGStandards to be Apply by AG

(1) Whether the acquisition is permitted under chapter 414D governing nonprofit entities, (1) Whether the acquisition is permitted under chapter 414D governing nonprofit entities, trusts, or charities;trusts, or charities;

(2) Whether the hospital acted in a duly diligent manner in deciding to sell, selecting (2) Whether the hospital acted in a duly diligent manner in deciding to sell, selecting the purchaser, and negotiating the terms and conditions of the sale;the purchaser, and negotiating the terms and conditions of the sale;

(3) The procedures used by the seller in making its decision, including whether (3) The procedures used by the seller in making its decision, including whether appropriate expert assistance was used;appropriate expert assistance was used;

(4) Whether all conflicts of interest were disclosed, including, but not limited to, conflicts (4) Whether all conflicts of interest were disclosed, including, but not limited to, conflicts of interest related to board members of, executives of, and experts retained by the seller, of interest related to board members of, executives of, and experts retained by the seller, purchaser, or parties to the acquisition;purchaser, or parties to the acquisition;

(5) Whether the seller will receive reasonably fair value for its assets. The attorney (5) Whether the seller will receive reasonably fair value for its assets. The attorney general may employ, at the seller's expense, reasonably necessary expert assistance in general may employ, at the seller's expense, reasonably necessary expert assistance in making this determination;making this determination;

(6) Whether charitable funds are placed at unreasonable risk, if the acquisition is (6) Whether charitable funds are placed at unreasonable risk, if the acquisition is financed in part by the seller;financed in part by the seller;

(7) Whether any management contract under the acquisition is for reasonably fair (7) Whether any management contract under the acquisition is for reasonably fair value;value;

(8) Whether the sale proceeds will be used for appropriate charitable health care (8) Whether the sale proceeds will be used for appropriate charitable health care purposes consistent with the seller's original purpose or for the support and promotion of purposes consistent with the seller's original purpose or for the support and promotion of health care in the affected community, and will be controlled as charitable funds health care in the affected community, and will be controlled as charitable funds independent of the purchaser or parties to the acquisition; andindependent of the purchaser or parties to the acquisition; and

(9) Whether a right of first refusal to repurchase the assets by a successor nonprofit (9) Whether a right of first refusal to repurchase the assets by a successor nonprofit corporation or foundation has been retained, if the hospital is subsequently sold to, corporation or foundation has been retained, if the hospital is subsequently sold to, acquired by, or merged with another entity. [L 1998, c 257, pt of §1; am L 2002, c 40, §10]acquired by, or merged with another entity. [L 1998, c 257, pt of §1; am L 2002, c 40, §10]

Charitable Gift AnnuitiesCharitable Gift Annuities

HRS sec. 431-1-201HRS sec. 431-1-201 Imposes certain minimum asset and Imposes certain minimum asset and

operating and reserve requirements on operating and reserve requirements on charities that issue CGI’s or they are treated charities that issue CGI’s or they are treated as life insurance productsas life insurance products

Requires Annual Certification of compliance Requires Annual Certification of compliance with the AG.with the AG.

The Form is on the AG’s Charities website.The Form is on the AG’s Charities website.

Charitable Charitable Solicitation/RegistrationSolicitation/Registration

Chapter 467B, HRS requires registration Chapter 467B, HRS requires registration by:by:

• Charities that solicit contributionsCharities that solicit contributions

• Professional Solicitors Professional Solicitors (Telemarketers/Direct Mailers)(Telemarketers/Direct Mailers)

• Professional Fundraising CounselsProfessional Fundraising Counsels

• Commercial Co-VenturersCommercial Co-Venturers

Charitable Charitable Solicitation/RegistrationSolicitation/Registration

Financial Reporting by Charities and Paid Financial Reporting by Charities and Paid Solicitors is required.Solicitors is required.

Charity Registration is done electronically Charity Registration is done electronically via the Internet.via the Internet.

The AG receives registration statements The AG receives registration statements through via a system developed by the through via a system developed by the Urban Institute (home of the Nat.’l Center Urban Institute (home of the Nat.’l Center for Charitable Statistic)for Charitable Statistic)

State Charity Regulators Have Access to Reporting Features

This report shows Users with the name “Wish” in their organizational names

Hawaii Charity RegistryHawaii Charity Registry

XML and PDF files received through the XML and PDF files received through the Fed/State Backend are transferred using a Fed/State Backend are transferred using a FTP protocol to the administrator of the FTP protocol to the administrator of the State’s Internet PortalState’s Internet Portal

Ehawaii.gov constructed a publicly Ehawaii.gov constructed a publicly searchable registry for these registrations searchable registry for these registrations and 990 Formsand 990 Forms

AG pays Ehawaii.gov a portion of annual AG pays Ehawaii.gov a portion of annual fees to develop and maintain the registry.fees to develop and maintain the registry.

The AG’s Charity Resources The AG’s Charity Resources Website Provides a Wealth of Website Provides a Wealth of

InformationInformation Financial reporting by professional solicitorsFinancial reporting by professional solicitors Donor Education ToolsDonor Education Tools Guides for Nonprofit Directors and BoardsGuides for Nonprofit Directors and Boards All our FormsAll our Forms Model Policies for Nonprofit OrganizationsModel Policies for Nonprofit Organizations Other Guides for Directors and Officers and Other Guides for Directors and Officers and

the Publicthe Public

www.hawaii.gov/ag/charitieswww.hawaii.gov/ag/charities

In Addition to Registration We Do In Addition to Registration We Do Investigation/Enforcement/SanctionInvestigation/Enforcement/Sanction We investigate and enforce prohibited We investigate and enforce prohibited

practices in soliciting charitable practices in soliciting charitable contributionscontributions

We may suspend or revoke the We may suspend or revoke the registration of charities and professional registration of charities and professional fundraisersfundraisers

We may impose civil penalties for We may impose civil penalties for violationsviolations

..

In Addition to Registration AG Does In Addition to Registration AG Does Investigation/Enforcement/SanctionsInvestigation/Enforcement/Sanctions

We may issue cease and desist ordersWe may issue cease and desist orders Administrative actions are subject to the Administrative actions are subject to the

right to a contest case hearing.right to a contest case hearing. We may seek and obtain injunctive and We may seek and obtain injunctive and

other relief.other relief.

Case Studies in Governance Failures .

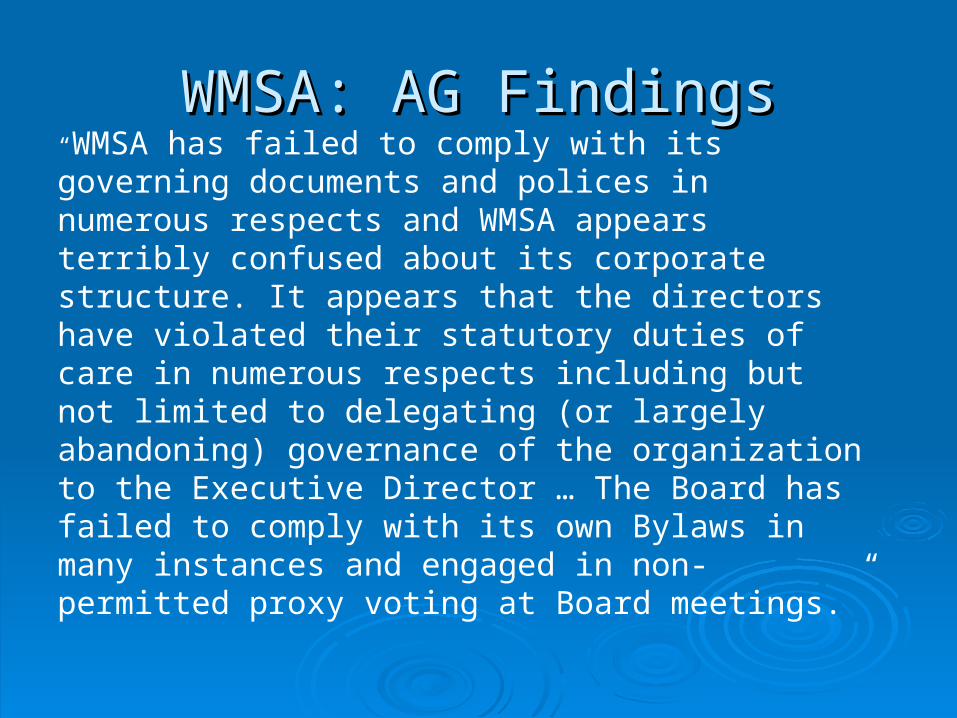

“WMSA has failed to comply with its governing documents and polices in numerous respects and WMSA appears terribly confused about its corporate structure. It appears that the directors have violated their statutory duties of care in numerous respects including but not limited to delegating (or largely abandoning) governance of the organization to the Executive Director … The Board has failed to comply with its own Bylaws in many instances and engaged in non-permitted proxy voting at Board meetings.”

WMSA: AG FindingsWMSA: AG Findings

WMSA: AG FindingsWMSA: AG Findings“[T]he Board has failed to formally adopt fundamental polices to protect the organization from risk and threats despite informing the Internal Revenue Service (“IRS”) it has done so, putting the organization’s valuable tax exempt status at risk. WMSA’s 2009 and 2010 IRS Form 990 [tax return] appears inaccurate in several material respects and WMSA has engaged in prohibited political intervention by making an illegal campaign contribution.”

WMSA: AG FindingsWMSA: AG Findings•“WMSA itself has no records to substantiate how it allocated its functional expenses among program services, management and general, and fundraising on its IRS Form 990 for 2010 but reports $154,000 in program related services.”• “The other senior employee of WMSA is the Executive Director’s daughter who has been employed by WMSA for fifteen years an an Accountant/Office Manager and was hired ‘at the recommendation of the CPA’ in violation of WMSA’s anti-nepotism policy (the Board retroactively modified its anti-nepotism policy after her date of hire).”

WMSA: AG FindingsWMSA: AG Findings

No Evaluation of Executive Director since 2009No Evaluation of Executive Director since 2009 No Strategic PlanNo Strategic Plan Part IV, line 3 of WMSA’s IRS Form 990 for Part IV, line 3 of WMSA’s IRS Form 990 for

2010 states that it does not engage in lobbying. 2010 states that it does not engage in lobbying. However, WMSA frequently testifies before the However, WMSA frequently testifies before the County Council in support of or against specific County Council in support of or against specific legislation and WMSA staff expends time legislation and WMSA staff expends time preparing the written testimony and meeting with preparing the written testimony and meeting with Council members, their staffs and Council members, their staffs and subcommittees. Such activities constitute ‘direct subcommittees. Such activities constitute ‘direct lobbying’ under applicable Treasury regulations lobbying’ under applicable Treasury regulations

Private FoundationsPrivate Foundations

The AG receives IRS Form 990PFsThe AG receives IRS Form 990PFs The AG regularly reviews 990PF’s The AG regularly reviews 990PF’s

submitted by Hawaii private foundationssubmitted by Hawaii private foundations These 990PF reviews often generate AG These 990PF reviews often generate AG

inquiries about matters reported on the inquiries about matters reported on the 990PF990PF

Private Foundation InquiryPrivate Foundation Inquiry

Foundation “A” has two directors Foundation “A” has two directors “C” and “D” who are attorneys“C” and “D” who are attorneys

Foundation has $134 million in assets.Foundation has $134 million in assets. C’s law firm rents space in Foundation A’s C’s law firm rents space in Foundation A’s

officesoffices Director C negotiated the lease for the law firm.Director C negotiated the lease for the law firm. Directors C&D billed the foundation at their Directors C&D billed the foundation at their

attorney rates for doing “director related” attorney rates for doing “director related” services and what appears to be non legal services and what appears to be non legal servicesservices

Private Foundation InquiryPrivate Foundation Inquiry Directors C and D are engaged in a conflict transactions Directors C and D are engaged in a conflict transactions

with Foundation A on whose board they sit.with Foundation A on whose board they sit. Section 414D-150 defines “indirect conflict of interest” as Section 414D-150 defines “indirect conflict of interest” as

follows:follows:1.1. (c) For purposes of this section, a director of the corporation (c) For purposes of this section, a director of the corporation

has an indirect interest in a transaction if:has an indirect interest in a transaction if: (1) Another entity in which the director has a material interest or (1) Another entity in which the director has a material interest or

in which the director is a general partner is a party to in which the director is a general partner is a party to the transaction;the transaction;

The lease to C’s law firm and payment of attorneys fees The lease to C’s law firm and payment of attorneys fees qualify as indirect conflicts under (c)(1) abovequalify as indirect conflicts under (c)(1) above

Private Foundation InquiryPrivate Foundation Inquiry Directors C and D are disqualified persons and receive Directors C and D are disqualified persons and receive

approximately $140,000 in compensation as directorsapproximately $140,000 in compensation as directors If compensation is not necessary and reasonable, it may If compensation is not necessary and reasonable, it may

expose the directors to the excise tax on self dealing expose the directors to the excise tax on self dealing transactions by foundation managers.transactions by foundation managers.

As a matter of State law, nonprofit corporation may not As a matter of State law, nonprofit corporation may not engage in a self-dealing excise tax transactionengage in a self-dealing excise tax transaction

C&D’s Law firms is also potentially a disqualified person C&D’s Law firms is also potentially a disqualified person depending on the extent of C&D’s ownership in the depending on the extent of C&D’s ownership in the partnershippartnership

Payments made to C&D’s law firms totaled nearly Payments made to C&D’s law firms totaled nearly $533,000 in 2008 and it included time spent performing $533,000 in 2008 and it included time spent performing work as directors.work as directors.

Questions?????Questions?????