national consumer agency market research findings: grocery shopping august 2010

DESCRIPTION

National Consumer Agency Market Research Findings: Grocery Shopping August 2010 Research Conducted by. Amárach Research conducted the research by means of face-to-face interviewing with 1,000 people between the ages of 15-74. - PowerPoint PPT PresentationTRANSCRIPT

National Consumer Agency

Market Research Findings:Grocery Shopping

August 2010Research Conducted by

2

Making Complaints

• Amárach Research conducted the research by means of face-to-face interviewing with 1,000 people between the ages of 15-74.

• In all, 6 comparable “Waves” of Market Research have been completed since November / December 2007.

• To ensure that the data is nationally representative, quotas were applied on the basis of age, gender and social class.

• Interviewing was conducted over a four week period in June 2010.

Research Background and Methodology

Nov/Dec 2007 Aug 2008 Nov/Dec 2008

May/June 2009 Nov/Dec 2009 June 2010

Benchmark

Wave 3 Wave 4

Wave 1 Wave 2

Wave 5

Current Wave

3

Making Complaints

20

41 41

25

47

19

37

9

16

83

204

46

10

54

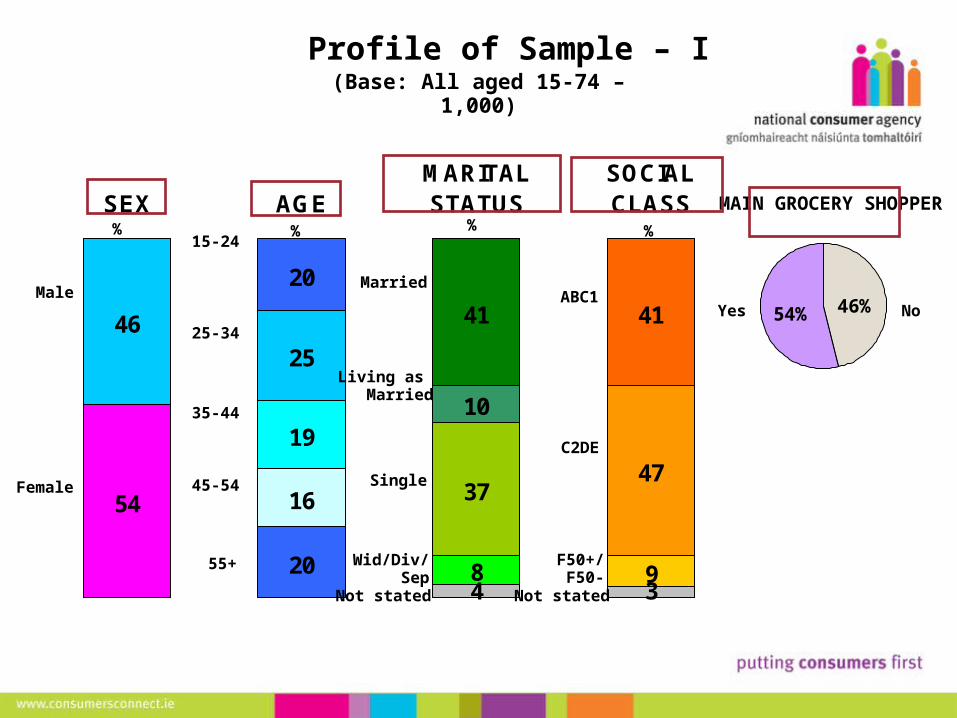

SEX AGEMARITALSTATUS

SOCIALCLASS

Profile of Sample – I(Base: All aged 15-74 – 1,000)

Male

Female

% % % %15-24

25-34

35-44

45-54

55+

Married

Living as Married

Single

Wid/Div/Sep

ABC1

C2DE

F50+/F50-

MAIN GROCERY SHOPPER

Yes No46%54%

Not statedNot stated

4

Making Complaints

5

48 4225

45

25

24

9

20

134

25

4

25

1175

SEX AGEMARITALSTATUS

SOCIALCLASS

Profile of Sample – II – Main Grocery Shoppers(Base: All Mainly Responsible for Grocery Shopping in Home – 535)

Male(46)

Female(54)

% % % %15-24(20)

25-34(25)

35-44(19)

45-54(16)

55+(20)

Married(41)

Living as Married

(10)

Single(37)

Wid/Div/Sep

(8)

ABC1(41)

C2DE(47)

54%

( ) = Total Sample

F50+/F50-(9)

Those who were responsible for the main grocery shop within the household were more likely to be female and over the age of 34.

Not stated Not stated

5

Making Complaints

Section 1:Grocery Shopping

6

Making Complaints

Key Findings

• Price continues to be the key driver of choice of the main grocery shop, followed by convenience – both increasing in importance since the previous wave.

• The number of grocery shoppers that have changed what they buy or where they shop since the start of the year has fallen back to just under 1 in 2.

• Cutting back on treats remains the number one change to the grocery shop since the start of the year although this has fallen back slightly since Nov/Dec 2009. Those responsible for the main grocery shop are now more likely to be spreading their shopping over different stores in order to get the best value – up 12% from the previous wave.

• 4 in 5 consumers responsible for the main grocery shop would prefer to see supermarkets offering more long term lower prices as opposed to regular promotions and special offers.

• 7 in 10 Irish consumers claim to be aware of the prices of everyday goods such as bread, milk and a litre of petrol.

7

Making Complaints

2232 34 38

49

56 55 49

13

5 5 55 4 57 2 2 3

9

Total Wave 5 2010

Wave 4 2009

% % %

(Base: All aged 15-74 – 1,000)

Overall Awareness of the Price of Everyday Goods

All responsible for the main grocery shop – 535 (54%)

71% aware of prices

86% 89%

Very aware of the prices (5)

Fairly aware of the prices (4)

Don't really know the prices (3)

Not at all aware of the prices (1)

Somewhat unaware of the prices (2)

(22)

(48)

(12)

(10)

(8)

( ) = Wave 4 2009Wave 3

2008%

87%

As with the previous wave, 7 in 10 Irish consumers claim to be aware of the prices of everyday goods such as bread, milk and a litre of petrol. Consistently so; the majority of those responsible for the main grocery shop within the household are more likely to be aware (86%) – however this has

fallen back slightly since the previous wave.

8

Making Complaints

60

47

20

15

13

6

6

5

Main Reasons for Choice of Main Grocery Shop

Price

Convenience

Parking

Late night opening

Quality of Product

Loyalty

Support local shops

Other

Main Reasons Wave 2 2008%

54%

58

49

17

8

11

8

6

4

Wave 3 2009%

62

43

18

9

10

10

6

2

Wave 4 2009

%

70

55

20

12

12

10

6

4

Wave 5 2010

%

(Base: All main grocery shoppers – 535)

Price continues to be the key driver of choice of the main grocery shop, followed by convenience – both increasing in importance since the previous wave.

9

Making Complaints

Change in Grocery Shopping Since the Start of the Year

55%45%Yes No

The number of grocery shoppers that have changed what they buy or where they shop since the start of the year has fallen back to just under 1 in 2.

(55%)(45%)

%

Male (45%) 39%Female (58%) 47%

ABC1 (56%) 47%C2DE (59%) 45%

54%

(Base: All main grocery shoppers – 535)

10

Making Complaints

42

40

38

34

26

16

14

12

%

Wave 3 2009

Changes Made to the Grocery Shopping Since the Start of the Year

(Base: All who changed their shopping behaviour since the start of the year – 240)

Cutting back on treats for you/family

Buying cheaper versions of products (e.g. own brands rather than regular)

Taking more advantage of special offers, using coupons, etc.

Buy less

Spreading your grocery shopping over different supermarkets and stores to get the best value

Switched your main grocery shopping from a different retailer to the one you use now

Started shopping up North (across the boarder)

Do without or cut back e.g. buy less meat

Changes to Grocery Shopping

(-8%)

24%

(+14%)

56

36

53

46

23

11

13

12

%

Wave 4 2009

(+14%)

(+15%)

(+12%)

53

36

48

43

35

10

9

14

%

Wave 5 2010

(+12%)

Cutting back on treats remains the number one change to the grocery shop since the start of the year although this has fallen back slightly since Nov/Dec 2009. Those responsible for the main grocery shop are now more likely to be spreading their shopping over different stores in order to get the best value – up 12% from the

previous wave.

11

Making Complaints

81%

2%

17%

Price Cuts & Special Offers -1

(Base: All responsible for the main grocery shop - 535)

Long Term Lower Prices

Regular Promotions & Special Offers

Don’t know

What would you prefer to see more of within supermarkets?

54%

4 in 5 consumers responsible for the main grocery shop would prefer to see supermarkets offering more long term lower prices as opposed to regular promotions and special offers.

(77%)

(7%)(16%)

12

Making Complaints

81

17

2

79

21

81

18

1

82

16

2

82

16

2

82

17

1

82

18

84

14

2

83

15

2

79

20

1

Price Cuts & Special Offers -2(Base: All responsible for the main grocery shop – 535)

* Caution small base size

Male(134)

Total(535)

Female(401)

ABC1(222)

C2DE(240)

25-34(134)

15-24*(24)

35-44(135)

45-54(103)

55+(135)

Long term lower prices

Regular promotions & special offers

Don’t know

Long term lower prices

Regular promotions & special offers

Don’t know – –

–

%%%%%

%%%%%

4 in 5 consumers responsible for the main grocery shop would prefer to see supermarkets offering more long term lower prices as opposed to regular promotions and special offers – this is consistent across all

demographic breaks, with C2DEs and those aged 45-54 slightly more inclined to say so.