national association of black accountants, inc. m ney $ense naba - money $ense

TRANSCRIPT

National Association of National Association of Black Black

Accountants, Inc.Accountants, Inc.

M ney M ney $$enseense

NABA - Money $enseNABA - Money $ense

Money Mindsets

““The only way to not think about money is to have a great The only way to not think about money is to have a great deal of it.”deal of it.”

Edith WhartonEdith Wharton

Money Mindsets (cont’d)

““The safest way to double your money is to fold it over and The safest way to double your money is to fold it over and put it in your pocket.” put it in your pocket.”

Kin HubbardKin Hubbard

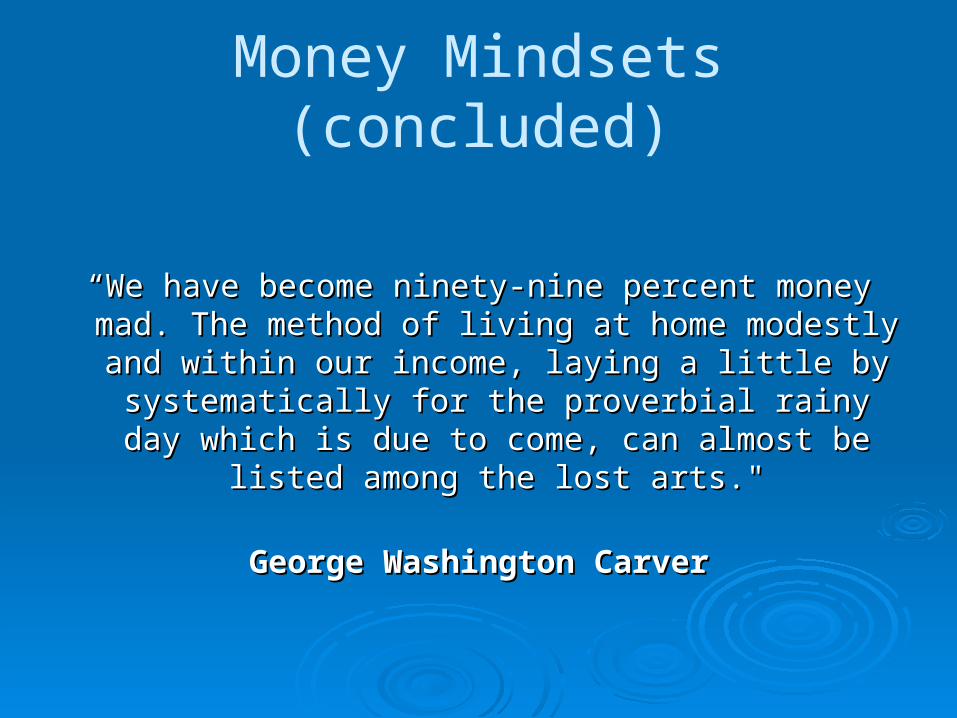

Money Mindsets (concluded)

““We have become ninety-nine percent money mad. The We have become ninety-nine percent money mad. The method of living at home modestly and within our method of living at home modestly and within our

income, laying a little by systematically for the proverbial income, laying a little by systematically for the proverbial rainy day which is due to come, can almost be listed rainy day which is due to come, can almost be listed

among the lost arts."among the lost arts."

George Washington CarverGeorge Washington Carver

How does money play into your How does money play into your life?life?

Have you thought about your relationship Have you thought about your relationship with money?with money?

Money should not influence your self-Money should not influence your self-esteemesteem

Your value as a person does not come Your value as a person does not come from moneyfrom money

NABA - Money $enseNABA - Money $ense

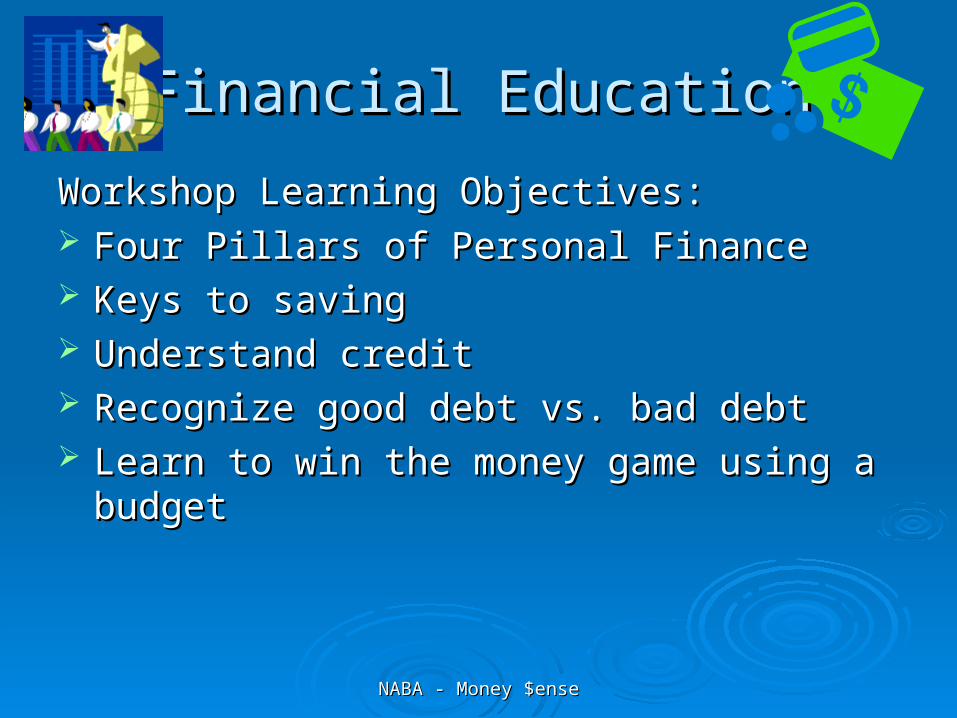

Financial EducationFinancial Education

Workshop Learning Objectives:Workshop Learning Objectives: Four Pillars of Personal FinanceFour Pillars of Personal Finance Keys to savingKeys to saving Understand creditUnderstand credit Recognize good debt vs. bad debtRecognize good debt vs. bad debt Learn to win the money game using a budgetLearn to win the money game using a budget

NABA - Money $enseNABA - Money $ense

Four Pillars of Personal FinanceFour Pillars of Personal Finance

1.1. SavingsSavings• You are worth every penny of your moneyYou are worth every penny of your money

• Pay Yourself First and Pay Yourself OftenPay Yourself First and Pay Yourself Often

2.2. Handling Credit and DebtHandling Credit and Debt• Knowledge is PowerKnowledge is Power

• Know your credit score and how to raise itKnow your credit score and how to raise it• Know the power and pitfalls of credit/debtKnow the power and pitfalls of credit/debt

NABA - Money $enseNABA - Money $ense

Four Pillars of Personal FinanceFour Pillars of Personal Finance

3.3. BudgetingBudgeting• Know where your money is going or it’s Know where your money is going or it’s

going to go places without you going to go places without you • Know your budget, update your budget, be Know your budget, update your budget, be

flexible with your budgetflexible with your budget

4.4. InvestingInvesting• Know what you want and use patience to Know what you want and use patience to

get thereget there• Invest based on your goals, risk tolerance, Invest based on your goals, risk tolerance,

and timeand time

Pillar One: Savings

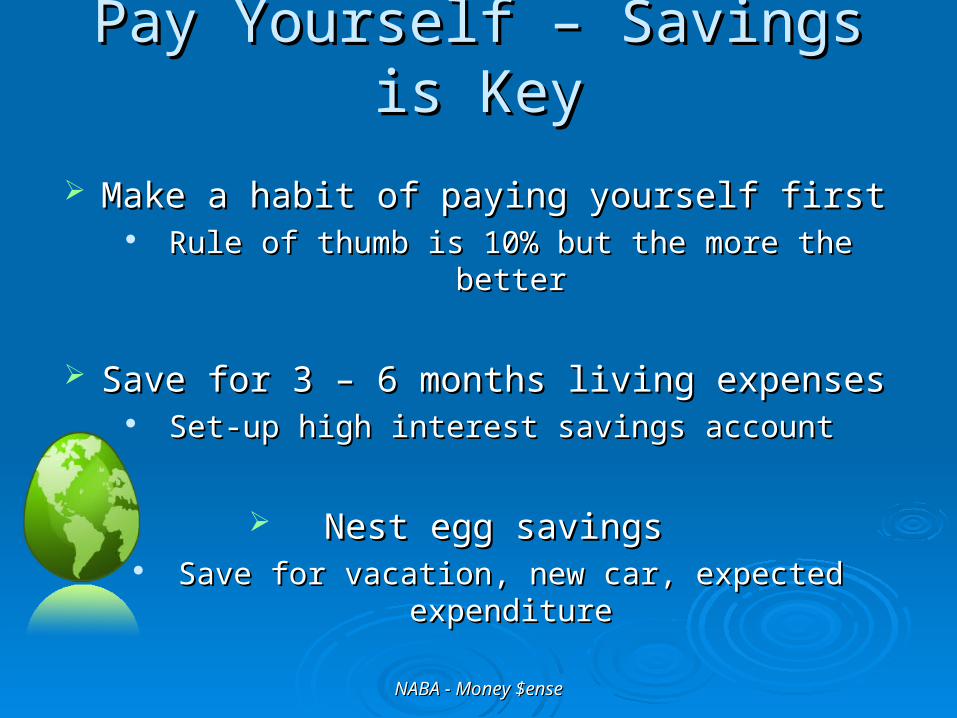

Pay Yourself – Savings is KeyPay Yourself – Savings is Key

Make a habit of paying yourself firstMake a habit of paying yourself first Rule of thumb is 10% but the more the betterRule of thumb is 10% but the more the better

Save for 3 – 6 months living expensesSave for 3 – 6 months living expenses Set-up high interest savings account Set-up high interest savings account

Nest egg savingsNest egg savings Save for vacation, new car, expected Save for vacation, new car, expected

expenditureexpenditure

NABA - Money $enseNABA - Money $ense

Pillar Two: Managing Debt and Credit

Credit in a Nutshell

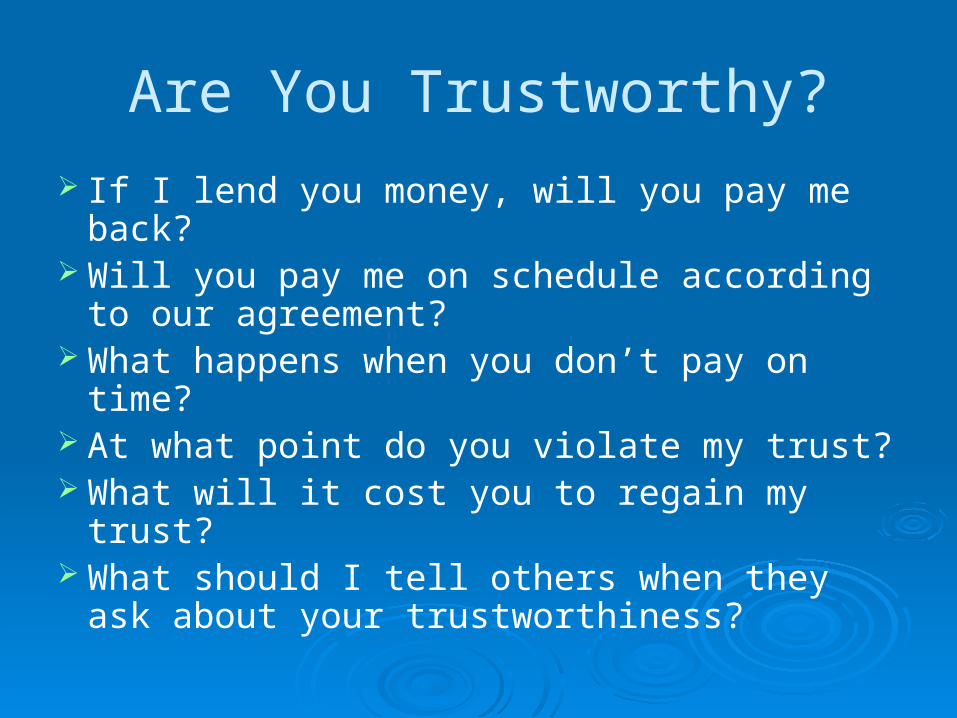

Are You Trustworthy?

Are You Trustworthy?

If I lend you money, will you pay me back? Will you pay me on schedule according to

our agreement? What happens when you don’t pay on

time? At what point do you violate my trust? What will it cost you to regain my trust? What should I tell others when they ask

about your trustworthiness?

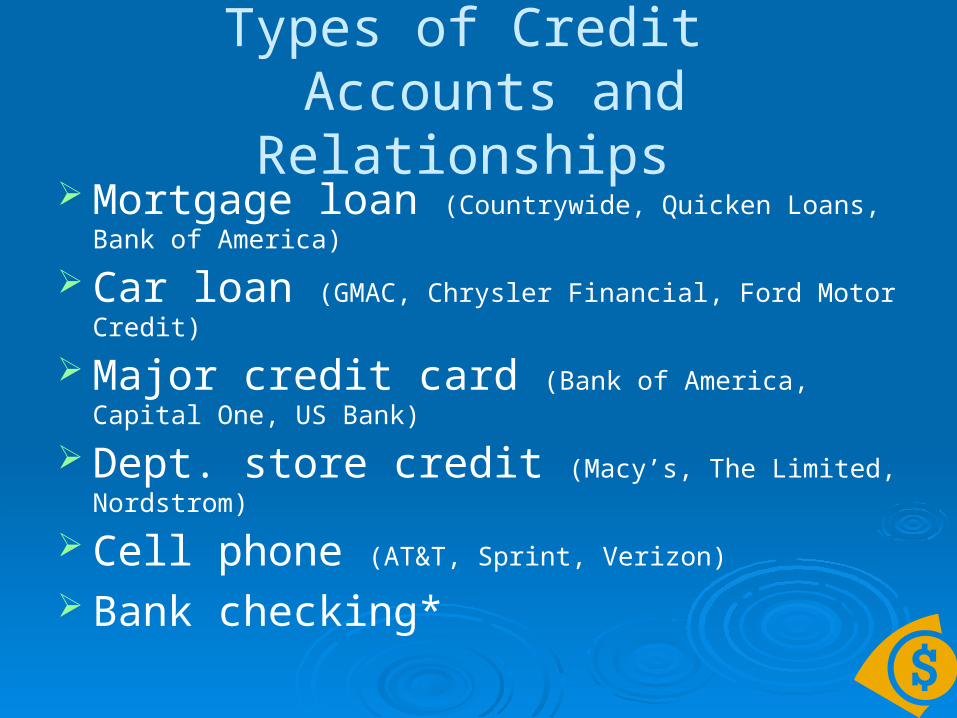

Types of Credit Accounts and Relationships

Mortgage loan (Countrywide, Quicken Loans, Bank of America)

Car loan (GMAC, Chrysler Financial, Ford Motor Credit)

Major credit card (Bank of America, Capital One, US Bank)

Dept. store credit (Macy’s, The Limited, Nordstrom)

Cell phone (AT&T, Sprint, Verizon)

Bank checking*

Type of Credit Lender Advantages Disadvantages

HOME MORTGAGE • Commercial bank

• Savings and loan

• Credit union

• Homes often increase in value.

• Interest rates for mortgages are relatively low

• The interest paid is tax-deductible.

• Mortgages are long-term commitments.

• Obtaining a home loan involves extensive credit checks.

CAR LOANS • Commercial bank

• Savings and loan

• Credit union

• Consumer finance company

• Cars can make it easier to work and earn an income.

• Cars lose their value relatively quickly. The car you purchase may have little value when the last payment is made.

COLLEGE LOANS • Commercial bank

• Savings and loan

• Credit union Federal governmentFederal government

• A college education is a good borrow investment. necessary.

• Interest rates can be relatively low.

• Students sometimes borrow more than necessary.

• New graduates can face difficulty in repaying large loans.

PERSONAL LOANS • Commercial bank

• Savings and loan

• Credit union

• Consumer finance company

• Personal loans allow individuals to purchase today that boat or vacation they want.

• Personal loans have relatively high interest rates.

• Some young people may borrow more than their income allows.

CREDIT CARDS • Commercial bank

• Savings and loan

• Department store

• Oil companies

• Other financial institutions, e.g., American Express

• Credit cards are convenient to use and useful in an emergency.

• Credit cards provide a record of charges.

• Credit cards have relatively high interest rates.

• Some young people may borrow more than their income allows.

NABA - Money $enseNABA - Money $ense

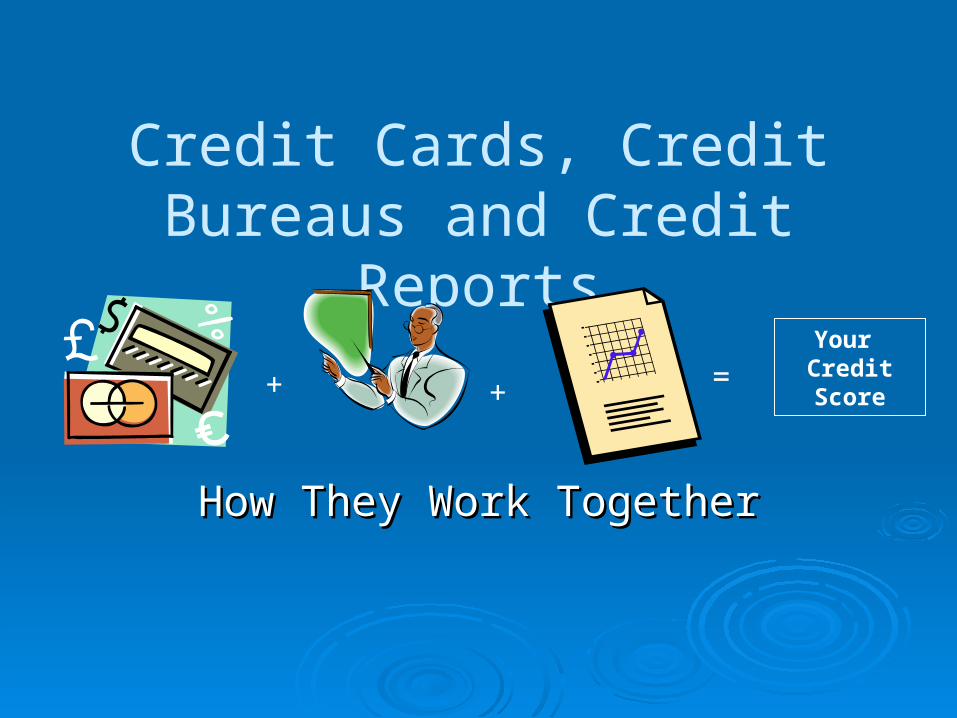

Credit Cards, Credit Bureaus and Credit Reports

How They Work TogetherHow They Work Together

+ + =Your CreditScore

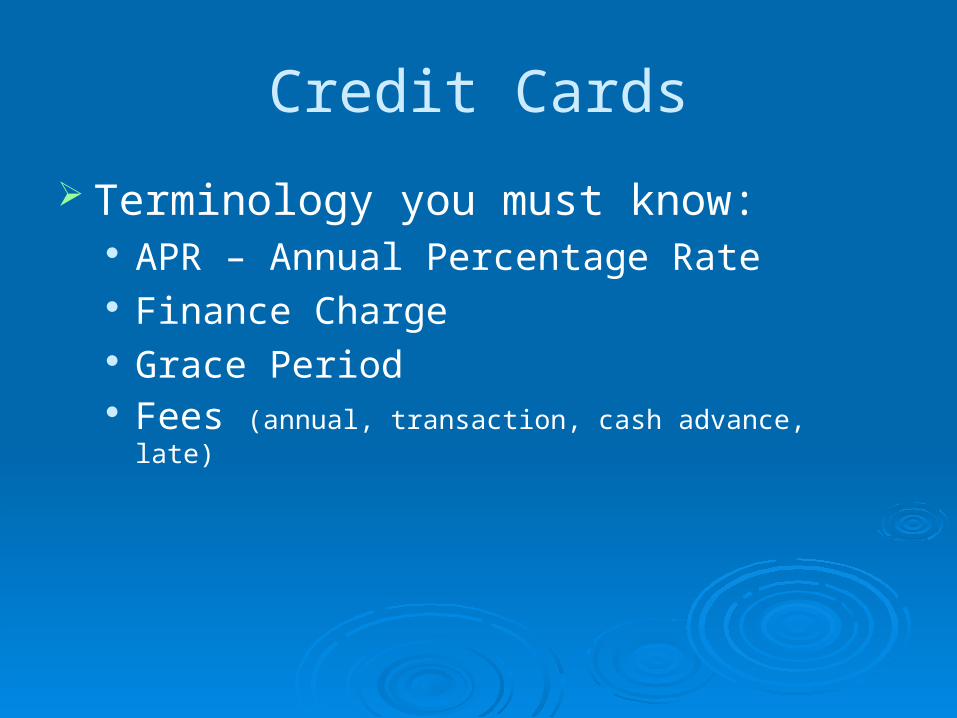

Credit Cards

Terminology you must know: APR – Annual Percentage Rate Finance Charge Grace Period Fees (annual, transaction, cash advance, late)

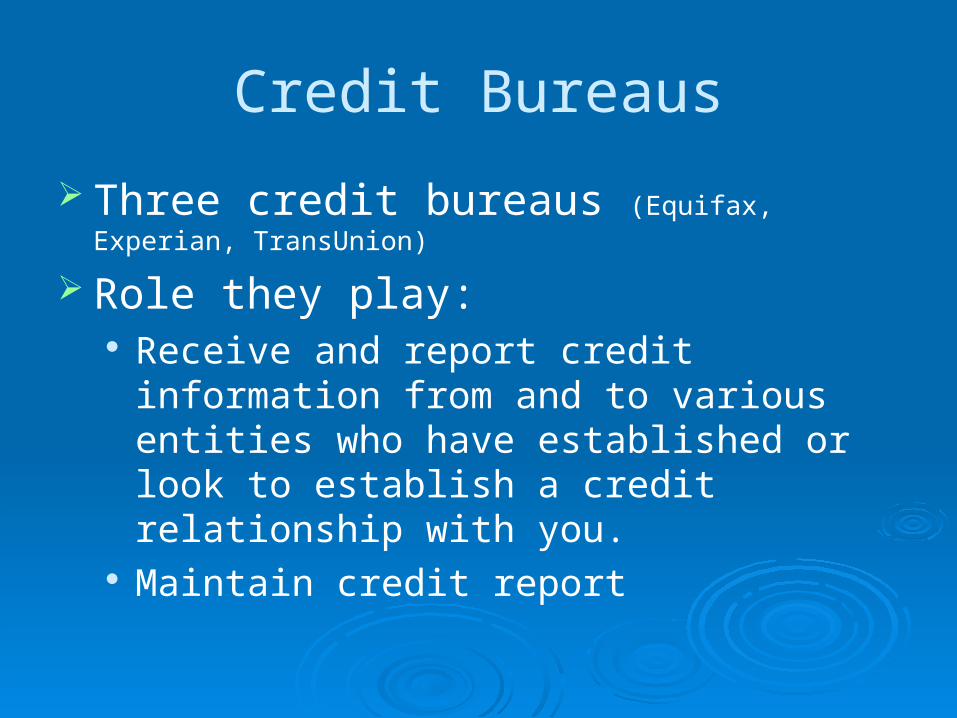

Credit Bureaus

Three credit bureaus (Equifax, Experian, TransUnion)

Role they play: Receive and report credit information from

and to various entities who have established or look to establish a credit relationship with you.

Maintain credit report

Credit Reports

What is reported? Name of creditor Length of credit history Amount of credit outstanding and borrowing capacity Status of payment on account: current or late Inquiries on account Other information Credit score*

How do you obtain a copy of report? FREE at www.annualcreditreport.com

Credit Score

Why is it important? Measurement of creditworthiness Basis for creditor’s lending decision Determines cost of borrowing (i.e. interest rate) Employers may pull it when evaluating potential candidates for hire

How is it calculated? Payment history – Payment history – (35%)(35%) Debt to credit limit – Debt to credit limit – (30%)(30%) Length of credit history – Length of credit history – (15%)(15%) New accounts and recent applications for credit – New accounts and recent applications for credit – (10%)(10%) Mix of credit cards and loans – Mix of credit cards and loans – (10%)(10%)

Credit Cards – Terms to KnowCredit Cards – Terms to KnowAPR: the amount it costs annually when you decide to carry a balance (not pay off your credit

card in full) each month. Can range from 0 to as high as 25% annually

Finance Charge: Actual dollar cost of using credit

Grace Period: the number of days you have to pay your bill in full before incurring finance charges (typically 25 days).

Beware of cards with no grace period! Interest accrues from the moment you charge an item. You don’t get a grace period when you carry a balance.

Annual Fee: the amount you pay annually as a credit cardholder for the privilege of using credit If you pay your balance each month, you should avoid cards with an annual fee. Some annual fee cards have lower interest rates, so if you carry a balance each month you may

actually save money with an annual fee card.Transaction Fees: You may be charged additional fees for ATM cash advances, balance transfers,

late charges and exceeding your credit limit. Some cards also charge a monthly fee for not using the card!

Late Fee: If your payment is not processed by the due date, you may be assessed a late fee of up to $35.

Avoid this expense by mailing timely payments. Remember, creditors must receive a payment at least every 30 days.

NABA - Money $enseNABA - Money $ense

Debt: Friend or Foe?Debt: Friend or Foe?

Good Debt vs. Bad Debt Good Debt vs. Bad Debt Buying a home vs. buying an expensive vacationBuying a home vs. buying an expensive vacation

How much debt can you handleHow much debt can you handle A conservative rule of thumb: the “20-10 Rule” A conservative rule of thumb: the “20-10 Rule”

• Total household debt including your housing payments Total household debt including your housing payments shouldn’t exceed 20% of your net household incomeshouldn’t exceed 20% of your net household income

How to handle debtHow to handle debt Have a planHave a plan

• Know how much you owe, know the interest and Know how much you owe, know the interest and repayment terms, set a plan, and stick to itrepayment terms, set a plan, and stick to it

NABA - Money $enseNABA - Money $ense

Pillar Three: Budgeting

Get in the Money Game!

The Money Game

How Do You Play?

Three Ways to Play

1. Getting Ahead – You make more money than you spend. Therefore, you have money at end of month that can be saved or invested.

2. Breaking Even – You spent everything you had –no more, no less

3. Falling Behind – You spent more than you had using borrowed funds.

BUDGET SCORECARD

CategoryGetting Ahead

BreakingEven

Falling Behind

Monthly INCOME: Wages/Income $1600 $1600 $1600 Interest Income $10 $10 $10 INCOME SUBTOTAL $1,610 $1,610 $1610 Monthly EXPENSES: Taxes $250 $250 $250 Rent/Mortgage $500 $600 $750 Utilities $100 $100 $100 Groceries/Food $250 $300 $350 Clothing $100 $100 $200 Shopping $75 $75 $100 Entertainment $100 $160 $200 Miscellaneous/Other $25 $25 $50 EXPENSES SUBTOTAL $1,400 $1610 $2000 NET INCOME (Income - Expenses) $210 $0 $(390)

NABA - Money $enseNABA - Money $ense

Benefits of Budgeting

Evaluate source (s) of income – explore ways to increase this amount

Evaluate expenditures and where money goes – identify opportunities to reduce this amount

Save, invest, pay down debt faster

Cash Flow Equation:(+) Revenue or Source

of Income

(-) Less: Expense or

Use of Income _______________(=) Net Cash Flow

Budgeting Basics

1.1. Save at least 10% of income through automatic Save at least 10% of income through automatic payroll deduction (when available) payroll deduction (when available)

2.2. Create a contingency fund for unexpected Create a contingency fund for unexpected expenditures (minimum 6 months of salary) expenditures (minimum 6 months of salary)

3. Track your spending your spending Itemize necessities first and foremostItemize necessities first and foremost Update your budget monthlyUpdate your budget monthly Add new information timelyAdd new information timely Print it out and post it as a daily visual reminderPrint it out and post it as a daily visual reminder

4.4. Pay down expensive / excessive debt.Pay down expensive / excessive debt.

NABA - Money $enseNABA - Money $ense

Pillar Four: Investing

Make Your Money GrowMake Your Money Grow

TIMETIME

NO INTERESTNO INTEREST 5% DAILY5% DAILYCOMPOUNDINGCOMPOUNDING

Year 1Year 1 $ 365$ 365 $ 374$ 374

Year 5Year 5 $ 1,825$ 1,825 $ 2,073$ 2,073

Year 10Year 10 $ 3,650$ 3,650 $ 4,735$ 4,735

Year 30Year 30 $10,950$10,950 $25,415$25,415

Money that is invested will grow!Money that is invested will grow!

NABA - Money $enseNABA - Money $ense

What if you saved $1 per day for 30 years?What if you saved $1 per day for 30 years?

What Did You Learn?

New Mindset, New HabitsNew Mindset, New Habits Take the First Step:Take the First Step:

Step 1Step 1• I have taken control of my financial futureI have taken control of my financial future• I am committed to achieving financial freedom I am committed to achieving financial freedom

Step 2Step 2• I have a budget and I review my budget regularlyI have a budget and I review my budget regularly• I save 10% or more of my incomeI save 10% or more of my income• I have 6-9 months of living expenses saved as an emergency fundI have 6-9 months of living expenses saved as an emergency fund• I know how much debt I have and the related interest ratesI know how much debt I have and the related interest rates• I know my credit scoreI know my credit score

Step 3Step 3• I have a 401(k) or similar retirement account that I contribute to I have a 401(k) or similar retirement account that I contribute to

regularlyregularly• I have an investment plan that considers my goals and risk toleranceI have an investment plan that considers my goals and risk tolerance

NABA - Money $enseNABA - Money $ense

Thank You!Thank You!

National Association of Black Accountants, National Association of Black Accountants, Inc.Inc.

M ney $enseM ney $ense

For more information visit www.nabainc.orgFor more information visit www.nabainc.orgNABA - Money $enseNABA - Money $ense