napa economic summit: the economy 2012: napa, north bay and beyond napa, caoctober 28, 2011 robert...

TRANSCRIPT

Napa Economic Summit:The Economy 2012: Napa, North Bay and Beyond

Napa, CA October 28, 2011

Robert Eyler, Ph.D.Professor, Economics

Frank Howard Allen Economics Research FellowDirector, Executive MBA Program

Sonoma State [email protected]

1

Current State of Affairs• 2011 was a year of mixed signals • Global: Europe, geopolitical uncertainty

– May change tourism over time

• National: Recovery underway, slow from jobs weakness– May change both wine sales and tourism

• State: Revenue generation and public workers• Local: Recovery slow and needs a jump start

Policy Issues• How do we create jobs through Congress?

– Temporary versus permanent job creation– Cost recovery versus investment

• Credit Supply Issues: reticence to lend– Riskiness in Europe not helping

• Credit Demand Issues: reticence to borrow– Interest rates low and stable as a result

• FED declaration on rates only as good as expected inflation

3

Excess Reserves at U.S. Banks (Loanable Funds Not Lent), 2008$Jan 2000 - Aug 2008

0

2

4

6

8

10

12

14

16

18

Month

Bil

lio

ns

of

$

4Source: Federal Reserve Board

0

200

400

600

800

1000

1200

1400

1600

1800

Billi

ons

of $

Excess Reserves at U.S. Depository Institutions (Loanable Funds Not Lent)2008$, Jan 2008 - Present

5Source: Federal Reserve Board

6Source: Federal Reserve Board

0

200

400

600

800

1000

1200

1400

1600

1800

Jan-

97M

ay-9

7Se

p-97

Jan-

98M

ay-9

8Se

p-98

Jan-

99M

ay-9

9Se

p-99

Jan-

00M

ay-0

0Se

p-00

Jan-

01M

ay-0

1Se

p-01

Jan-

02M

ay-0

2Se

p-02

Jan-

03M

ay-0

3Se

p-03

Jan-

04M

ay-0

4Se

p-04

Jan-

05M

ay-0

5Se

p-05

Jan-

06M

ay-0

6Se

p-06

Jan-

07M

ay-0

7Se

p-07

Jan-

08M

ay-0

8Se

p-08

Jan-

09M

ay-0

9Se

p-09

Jan-

10M

ay-1

0Se

p-10

Jan-

11M

ay-1

1Se

p-11

Bil

lio

ns o

f 2008$

Month

Excess Reserves at U.S. Depository Institutions (Loanable Funds Not Lent)2008$, Jan 1997 - Present

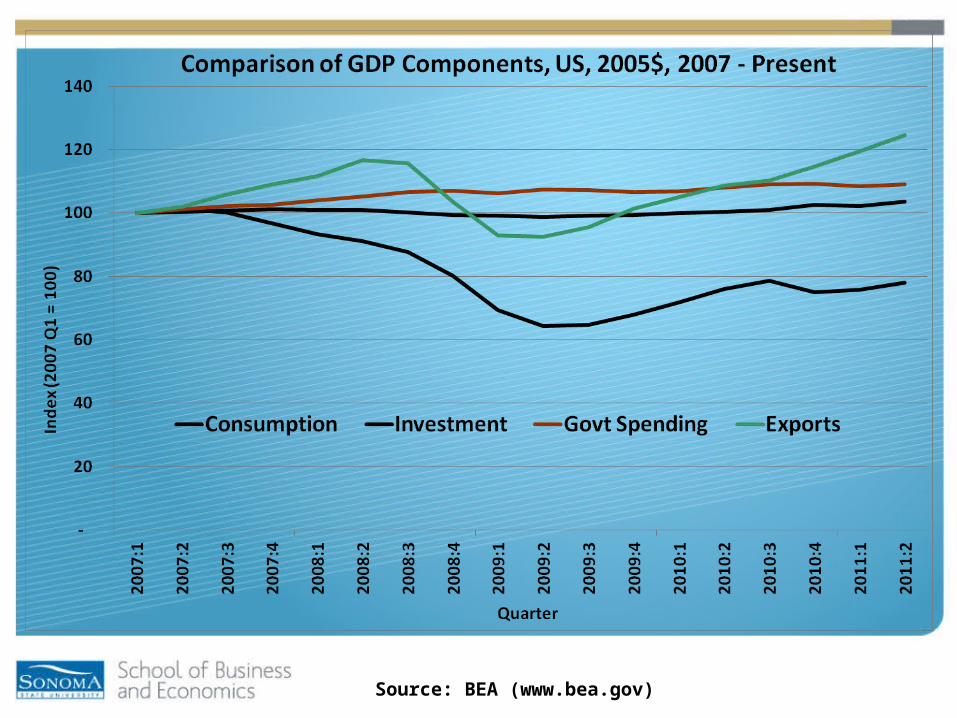

Source: BEA (www.bea.gov)

8Source: BEA (www.bea.gov)

9Source: BEA (www.bea.gov)

10

California• 2011-12 likely to be slightly better than 2010-11• Labor market still the big deal, and will remain in 2012• CA slowly bifurcating in terms of housing markets

– Interior valleys: Japanese-like recovery– Wine country: general economic recovery and conversion of

emerging world wealth to local housing/services demand• California’s recovery hinges on two major factors

– The expansion of the tech industry and it remaining here– How state government intends to fund itself

Source: BEA (www.bea.gov)

Source: BEA (www.bea.gov)

13

TechPulse Index, Index (Jan 2007 = 100), 1990-Oct 2011

Source: FED SF and Federal Reserve

Napa County and the Region• Napa has a place of economic strength in region

– Creating jobs in wake of recession– Tourism and wine to be the long term niche

• Need to continue to strengthen this niche– Northern and Southern Napa working in cohesion– Market to emerging world wealth: go to NVC for

Mandarin!• Competition is regional and growing

14

15

Employment, Seasonally Adjusted, 1990 – Aug 2011, Index 1990 = 100

Sources: EDD and CREA at SSU

Sources: BLS and CREA at SSU 16

New Unemployment Insurance Claims, Index (2002= 100)

17

Companies Gained and Lost, Napa County, 2006-11 and 2009-11

Sources: EDD and CREA at SSU

18

Jobs Gains and Losses, Napa County, 2006-11 and 2009-11

Sources: EDD and CREA at SSU

Local Housing Market Recovery: Keys• Job creation in technology industries• National economic recovery continuing• Recognition housing needs to follow general

economic recovery, and will not drive it• International audience for real estate welcomed

and marketed

19

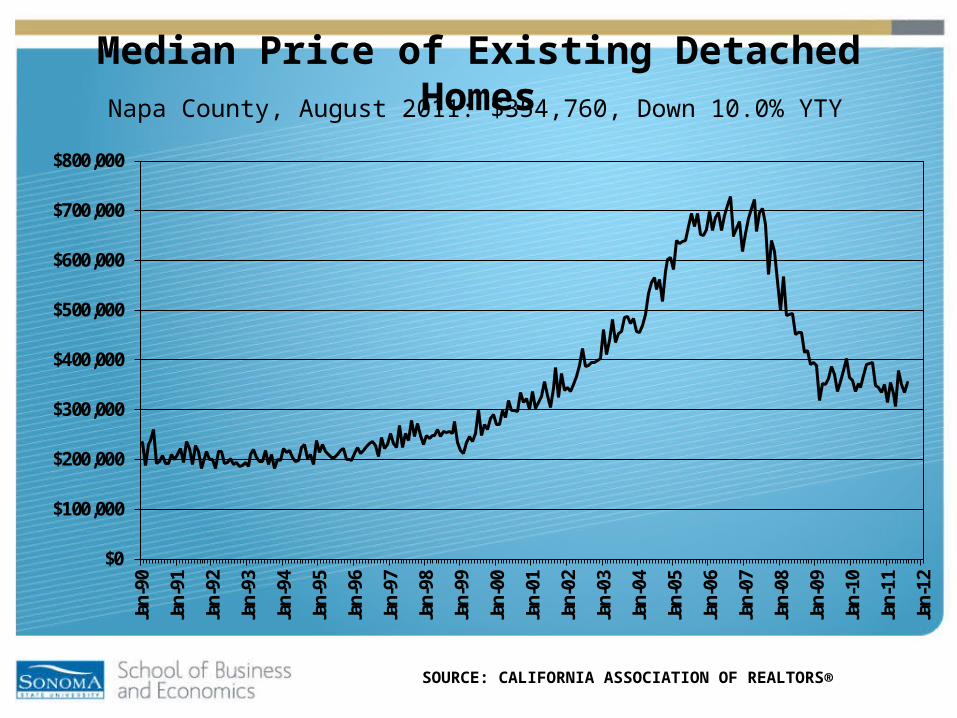

Median Price of Existing Detached HomesNapa County, August 2011: $354,760, Down 10.0% YTY

$0

$100,000

$200,000

$300,000

$400,000

$500,000

$600,000

$700,000

$800,000Ja

n-90

Jan-

91

Jan-

92

Jan-

93

Jan-

94

Jan-

95

Jan-

96

Jan-

97

Jan-

98

Jan-

99

Jan-

00

Jan-

01

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

SOURCE: CALIFORNIA ASSOCIATION OF REALTORS®

SOURCE: California Association of REALTORS®

County Aug-10 Jul-11 Aug-11Lake 74% 73% 64%Marin 29% 25% 28%Mendocino 52% 61% 48%Napa 39% 51% 48%Solano 67% 70% 71%Sonoma 41% 46% 42%CALIFORNIA 44% 43% 44%

Distressed Sales by County(Percent of Total Sales)

Where are we headed?• Recession-like activity through mid-2012 in

labor markets• Napa showing overt signs of recovery

– Maybe best in region• Recognize regional connections/economies• No signs of rapid recovery yet

– Economy to grow through 2012– Napa well poised for the long term

22