nab charitable giving index · nab charitable giving index ... relative to incomes, however, the...

TRANSCRIPT

1

NAB Charitable Giving IndexIndepth report – 12 months to February 2015

n Giving to charity grew by just 2% over the year to February 2015, down from 10% at the same time last year. Growth slowed in most age groups (except 65+), in all regions and there was significant divergence in the rate of charitable giving growth across charity categories (Chart 1).

The slowdown in giving mirrors some key findings from our Consumer Anxiety Reports which shows that Australians are responding to heightened stress by cutting back spending on “non essentials”, including charitable donations (Chart 2). Slower growth in charitable donations has also occurred against a backdrop of below trend economic growth and rising unemployment.

Despite these challenges, the average donation size for all charities increased by $2 over the past year to $336 per donor, with nearly all charity sectors experiencing an increase in average donation size.

For this update, we have undertaken a review of charity categorisations (Table 1) to improve how charities are represented in the publication. This has resulted in some changes, with around 50% of the “Other” category re-allocated to a new “Charitable Lotteries” category. Despite this change, Humanitarian Services charities continue to attract by far the biggest (albeit declining) share of all charity donations (35%).

Finally, we continue to see a very strong relationship between average dollar giving and average incomes with the affluent suburbs of Middle Park (3206), Bellevue Hill (2023) and Hunters Hill (2110) leading the country for generosity. Relative to incomes, however, the suburbs of Castlemaine (3450), Sturt (5047) and Fitzroy North (3068) lead the way for charity.

- Alan Oster, Group Chief Economist, NAB

n The NAB Charitable Giving Index provides a clear window into people’s contribution to charities – playing an important role in helping the not-for-profit sector realise the giving potential in Australia.

The Index is also a powerful indicator of how people are giving to their charities. Mobile apps and web-based charities are changing the landscape and revolutionising the way people donate. With more seamless channels for donation, and a much stronger desire to give digitally, it’s important for charities to understand this shift in behaviour.

We’re committed to continuing to support the not-for-profit sector play a vital role in helping our communities prosper and this includes providing real insights into giving trends. I look forward to sharing further insights in our next release, due in six months.

- Rebecca Kotow, Head of Community Engagement, NAB

Table 1. Charity categories

Categories Examples of charities included

Animals & Environment

RSPCA; WWF Australia; Australian Conservation Foundation

Cancer Cancer Council Donations; The Movember Group; Peter MacCullum Cancer Centre

Community Service & Children/Family

The Salvation Army; St Vincent de Paul; The Smith Family; Brotherhood of St Laurence

Health & Disability

Diabetes Australia; Fred Hollows Foundation; Vision Australia; Guide Dogs Australia

Humanitarian Services World Vision; Oxfam; Red Cross

Medical Research & Services

Heart Research Institute; Royal Flying Doctor Service

Charitable Lotteries*

Boystown Lottery; Mater Prize Home; RSL Art Union

Other** Everyday Hero, Go Fundraise, mycause.com.au

*Charitable Lotteries has been extracted from the “Other” charities and will now feature as a standalone category. **Other includes charity aggregators and other charities that do not fit into any of the categories above.

Chart 1: Growth in NAB Charitable Giving Index (percentage change, year-on-year)

12

10

8

6

4

2

02013 2014 20152012

Chart 2: Overall changes in spending behaviour (net balance)

GroceriesSavings, investments, superChildrenUse of creditHome improvementsTravelPersonal goodsCharitable donationsEating outMajor household itemsEntertainment

Spending less

Spending morePaying o� debt

UtilitiesMedical expences

Transport

-40 -20-30 -10 0 10Source: NAB Consumer Anxiety Report Q1 2015

2

Average annual donation per donor for all charities in the year to February 2015

over the past year

$336 $2Average annual donation size

Average annual donation per donor by age

$431$414$373

$306

$223

$141

1.8% 2.9%

Growth in metropolitan areas Growth in regional areas

Growth by location (February yoy)

10%

2%

Growth in charitable giving % change (annual)

Top postcodes for charitable giving by state(average donated per person)

0.36%Castlemaine 3450

Largest percentage of taxable income donated

February 2014

February 2015

At a glance

Annual change in giving by category (%)

Cancer

Community Services &

Children/FamilyHealth & Disability

Humanitarian Services

Charitable Lotteries*

Medical Research &

Services Other**Animals &

Environment

Feb 2015 Feb 2014

1.6

6.7

-6.2

13.9

-1.8

4.71.3

7.5

-1.1

8.811.6

21.0

7.7

-0.7

23.1

28.3

0 50 1000% 5% 0% 5%

0 50 100

*Charitable Lotteries has been extracted from the “Other” charities and will now feature as a standalone category. **Other includes charity aggregators and other charities that do not �t into any of the categories above.

VICMiddle Park

3206$316

QLDYeronga

4104$189

TASSouth Hobart

7004$142

SAMyrtle Bank

5064$214

WACottesloe

6011$248

NSWBellevue Hill

2023$268

ACTDeakin2600$227

NTFannie Bay

820$103

15-24 25-34 35-44 45-54 55-64 65+

Total average donation size per donor increases with age

NAB Charitable Giving Index

3

Indepth report

Growth in charitable giving has slowed sharply as consumers allocate less of their household spending to “non essentials”, including charitable donations.Giving to charity grew by just 2% over the year to February 2015, down from 10% at the same time last year (Table 2). This slowdown mirrors recent findings from NAB’s Consumer Anxiety Report which shows Australian consumers are responding to heightened anxiety by cutting back their spending on “non essentials”, including charitable donations (Chart 2).

Slower growth in charitable donations during this period has also occurred against a backdrop of below trend economic growth and rising unemployment, with the number of unemployed persons growing by almost 52,000 over the year to February 2015.

Charitable giving is slowing across all age groups (bar 65+) and in all regions. Growth in charitable giving is trending down across most age groups, except those aged 65+ (Chart 3).

The biggest slowdown was in the 45-54 age group, where growth slowed to 0.4% (8.9% one year earlier). Interestingly, NAB research also shows that middle-aged Australians are reporting the highest levels of consumer anxiety, especially in relation to their cost of living, which may help to explain the pull back in charitable giving over the past year.

Growth was however weakest in the 25 to 34 age group (-0.4%) and grew by just 0.8% among 15-24 year olds. During the year under review, younger Australians have faced growing employment challenges, with youth unemployment climbing to 13.7% from 12.5% a year earlier (more than double the national average). In response, NAB research reveals one area where younger Australians have also cut back is on charitable donations as growing concern over their job security underpins heightened consumer anxiety.

Table 2. Key Charitable Giving Statistics

Index (annual average) % change (annual)

Feb-14 Jan-15 Feb-15 Feb-14 Jan-15 Feb-15

NAB Charitable Giving Index 136.3 138.8 139.1 10.0 2.5 2.0

Animals & Environment 120.9 123.0 122.9 6.7 2.2 1.6

Cancer 291.0 273.1 273.0 13.9 -4.9 -6.2

Community Services & Children/Family 175.8 173.3 172.7 4.7 -1.0 -1.8

Health & Disability 205.2 206.3 207.9 7.5 2.9 1.3

Humanitarian Services 92.8 91.7 91.8 8.8 -1.2 -1.1

Charitable Lotteries 136.5 151.4 152.3 21.0 12.0 11.6

Medical Research & Services 175.2 187.8 188.7 -0.7 7.1 7.7

Other 458.4 561.8 564.1 28.3 23.4 23.1

All data is non-seasonally-adjusted (nsa). Data is produced by Quantium and includes donations via credit card, direct debit, BPAY and EFTPOS. Direct transfers into charity bank accounts are not captured (e.g. bequests and cheque donations may not be captured). Nearly 600 charity brands are included in this analysis.

15-24 years 25-34 years 35-44 years

45-54 years 55-64 years 65+ years

Chart 3: Growth in Charitable Giving Index by age group (percentage change, year-on-year)

18

15

12

9

6

3

0

-32012 2013 2014 2015

12

10

8

6

4

2

0

Metropolitan Regional

Chart 4: Growth in Charitable Giving Indexby region (percentage change, year-on-year)

2012 2013 2014 2015

4

In contrast, giving by those aged 65+ began turning up in late-2014 and grew by 6.7% over the year to February 2015 but was still down from almost 12% at the same time last year.

Similarly, in terms of location charitable giving growth has slowed in both metropolitan and regional locations (Chart 4). However, charitable giving in regional areas (2.9%) continues to outpace that in metropolitan areas (1.8%), which is also consistent with overall consumer spending patterns in Australia.

Humanitarian Services charities continue to attract the biggest (albeit falling), market share of all donations.For this update, NAB has undertaken a thorough review of charity categorisations to improve how charities are represented in the publication, this has resulted in some changes.

The biggest impact of this re-classification is in the “Other” charity category. Approximately 50% of this category has been re-allocated to a new category for “Charitable Lotteries”. For the remaining categories and at an overall level, the impact of re-classification has been small.

Despite this re-classification, Humanitarian Services charities continue to attract by far the biggest (albeit declining) share of all charity donations (35%) (Chart 5).

Health & Disability charities received the next biggest share (13%), with Charitable Lotteries (11%) and Community Service & Children/Family (11%) charities the next biggest.

In contrast, Medical Research & Services (6%) and “Other” charities receive the smallest market shares, followed by Animals & Environment (8%) and Cancer (9%).

NAB Charitable Giving Index

Chart 5: Market share of total charity donations (12 months to February)

Med

ical

Res

earc

h&

Ser

vice

s

Oth

er

Canc

er

Hea

lth &

Dis

abili

ty

Hum

anita

rian

Serv

ices

Com

mun

ity S

ervi

ce&

Chi

ldre

n/Fa

mily

Ani

mal

s &

Envi

ronm

ent

Char

itabl

e Lo

tter

ies

40

30

20

10

0

Feb-13 Feb-14Feb-12 Feb-15

Chart 7: Market share of total charity donations by metro/regional (12 months to February 2015)

Hum

anita

rian

Serv

ices

Oth

er

Canc

er

Char

itabl

e Lo

tter

ies

Med

ical

Res

earc

h&

Ser

vice

s

Com

mun

ity S

ervi

ce&

Chi

ldre

n/Fa

mily

Ani

mal

s &

Envi

ronm

ent

Hea

lth &

Dis

abili

ty

40

30

20

10

0

Metropolitan Regional

35%

33%

13%

14%

6% 7%

12%

9%9% 10%

8% 7% 10% 16

%

7% 6%

Chart 6: Market share of total charity donations by age band (12 months to February 2015)

Hum

anita

rian

Serv

ices

Oth

er

Canc

er

Med

ical

Res

earc

h&

Ser

vice

s

Com

mun

ity S

ervi

ce&

Chi

ldre

n/Fa

mily

Ani

mal

s &

Envi

ronm

ent

Hea

lth &

Dis

abili

ty

40

30

20

10

0

15-24 25-34 35-44 45-54 55-64 65+

Char

itabl

e Lo

tter

ies

“The Humanitarian Services category makes up more than one third of all charity donations, but the share of the market has been declining while Charitable Lotteries and Other are gaining share.”Tony Davis, Quantium

5

Humanitarian Services charities enjoy the biggest share of donations across all age groups and regions.Humanitarian Services dominate market share of charitable giving in all age groups ranging from 29% (65+) to 38% (25 to 34 year olds) (Chart 6). In contrast, Medical Research & Services charities received the lowest share of donations from all age groups, except the over 65s, who allocated the smallest share of their total donations to “Other” charities.

Interestingly, younger Australians (aged between 15 to 34) tended to allocate a bigger share of their total giving to Humanitarian Services, Animal & Environment and Cancer charities, whereas older Australians gave more to Health & Disability, Community Service & Children/ Family charities (especially over 65s) and to Charitable Lotteries (55 to 64 year olds).

Humanitarian Services also account for the lion’s share of giving in both metropolitan and regional areas, capturing 35% and 33% of the charity market respectively (Chart 7). Within regional locations, Charitable Lotteries had the second highest market share at 16%, followed by Health & Disability (14%), Cancer (10%), Community Services (9%) and Animals & Environment (7%).

In metropolitan areas, Health & Disability (13%) enjoyed the second biggest market share, followed by Community Services & Children/Family (12%), Charitable Lotteries (10%), Cancer (9%) and Animals & Environment (8%). Medical Research & Services charities had the smallest market share (6%).

Charitable giving to “Other” charities is growing exceptionally quickly but giving to Cancer, Community Service & Children/Family and Humanitarian Services charities is contracting.We are seeing some significant divergence in the rate of charitable giving growth across charity categories (Chart 8).

“Other” charities are experiencing the fastest rate of growth (23.1%), and has been outperforming all other segments of the charity sector since late 2013. Solid growth was also seen in Charitable Lotteries (11.6%).

An upturn in giving to Medical Research & Services that began in late-2014 is also continuing, with growth rising to 7.7% over the year to February 2015.

In contrast, giving to Cancer fell 6.2%, well below the 13.9% increase seen over the year to February 2014. Giving to Community Service & Children/Family (-1.8%) and Humanitarian Services (-1.1%) is also contracting.

Chart 8: Growth in NAB Charitable Giving Index by category (percentage change, year-on-year)

40

30

20

10

0

-10

Cancer

Medical Research & Services

Humanitarian Services

Animals & Environment

Charitable Lotteries

Community Service & Children/Family

Health & Disability

Other Total

2012 2013 2014 2015

Chart 9A: Growth by category by age (year to February)

50

40

30

20

10

0

-10

-20

12 months to February 2015 12 months to February 2014

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

Animals Cancer CS & Family MedicalResearch

Chart 9B: Growth by category by age (year to February)

50

40

30

20

10

0

-10

-20

12 months to February 2015 12 months to February 2014

OtherHumanitarian LotteriesHealth &Disability

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

Indepth report

6

Medical Research & Services was the only charity category to experience faster growth across all age groups.Medical Research & Services were the only charity category to experience faster growth across all age groups (especially in the 25-34 and 65+ age groups) (Chart 9A and 9B). In contrast, giving slowed across all age groups in Cancer, Humanitarian Services, Health & Disability and Charitable Lotteries (although giving in this group is still growing at double-digit rates across all age groups).

Interestingly, older Australians aged 65+ (a demographic that also consistently reports among lowest levels of consumer anxiety) were the only group to report positive growth in giving across all charity categories.

Medical Research & Services was the only charity category to experience faster growth in both metro and regional areas.Growth in giving to Medical Research & Services charities was faster than in the previous year in both metropolitan and regional areas (Chart 10A and 10B).

Growth also accelerated in metropolitan areas for Health & Disability and for Community Service & Children/Family charities in regional areas.

All other charities experienced slower (or negative) growth in both metropolitan and regional areas. Particularly large falls were seen in giving to Cancer (especially in metropolitan areas where giving slowed from 14.2% over the year to February 2014 to -8.2% in the year to February 2015).

Average annual donations are greatest for Humanitarian Services and smallest for “Other”, Cancer and Medical Research charities.Over the year to February 2015, the average annual charity donation per donor increased marginally to $336, from $334 in February 2014 (Chart 11).

All categories experienced an increase in average donation size, except Medical Research & Services charities where the average donation fell from $158 to $156.

Humanitarian Services continue to receive the biggest average annual donation, growing 4.4% to $431. Community Services & Children/Family ($247), Animals & Environment ($213) and Charitable Lotteries ($212) were the next biggest.

NAB Charitable Giving Index

Chart 10A: Growth by category by region – metropolitan (year to February)

Med

ical

Res

earc

h&

Ser

vice

s

Oth

er

Canc

er

Hea

lth &

Dis

abili

ty

Hum

anita

rian

Serv

ices

Com

mun

ity S

ervi

ce&

Chi

ldre

n/Fa

mily

Ani

mal

s &

Envi

ronm

ent

Char

itabl

e Lo

tter

ies

50

40

30

20

10

0

-10

12 months to February 2015 12 months to February 2014

Chart 10B: Growth by category by region – regional (year to February)

Med

ical

Res

earc

h&

Ser

vice

s

Oth

er

Canc

er

Hea

lth &

Dis

abili

ty

Hum

anita

rian

Serv

ices

Com

mun

ity S

ervi

ce&

Chi

ldre

n/Fa

mily

Ani

mal

s &

Envi

ronm

ent

Char

itabl

e Lo

tter

ies

50

40

30

20

10

0

-10

12 months to February 2015 12 months to February 2014

12 mths to Feb 201512 mths to Feb 201412 mths to Feb 2013

Chart 11: Average annual donation per donor($A)

Med

ical

Res

earc

h&

Ser

vice

s

Oth

er

Canc

er

Tota

l

Hea

lth &

Dis

abili

ty

Hum

anita

rian

Serv

ices

Com

mun

ity S

ervi

ce&

Chi

ldre

n/Fa

mily

Ani

mal

s &

Envi

ronm

ent

Char

itabl

e Lo

tter

ies

500

400

300

200

100

0

7

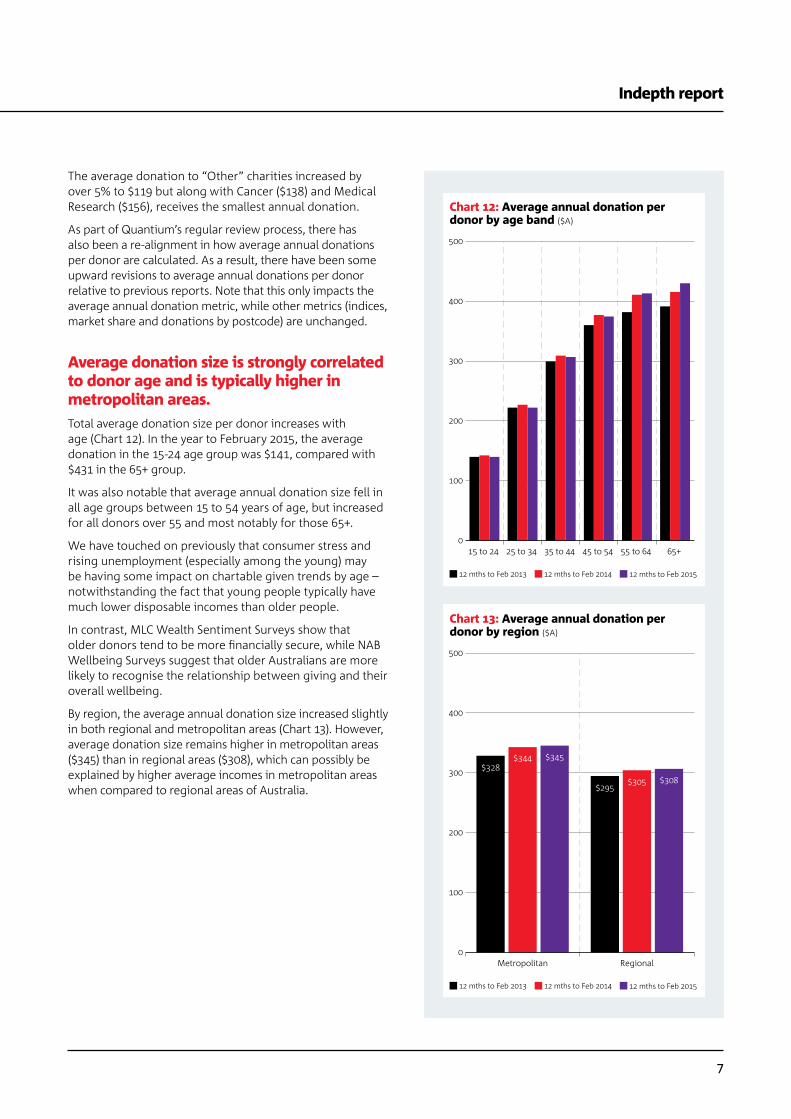

The average donation to “Other” charities increased by over 5% to $119 but along with Cancer ($138) and Medical Research ($156), receives the smallest annual donation.

As part of Quantium’s regular review process, there has also been a re-alignment in how average annual donations per donor are calculated. As a result, there have been some upward revisions to average annual donations per donor relative to previous reports. Note that this only impacts the average annual donation metric, while other metrics (indices, market share and donations by postcode) are unchanged.

Average donation size is strongly correlated to donor age and is typically higher in metropolitan areas. Total average donation size per donor increases with age (Chart 12). In the year to February 2015, the average donation in the 15-24 age group was $141, compared with $431 in the 65+ group.

It was also notable that average annual donation size fell in all age groups between 15 to 54 years of age, but increased for all donors over 55 and most notably for those 65+.

We have touched on previously that consumer stress and rising unemployment (especially among the young) may be having some impact on chartable given trends by age – notwithstanding the fact that young people typically have much lower disposable incomes than older people.

In contrast, MLC Wealth Sentiment Surveys show that older donors tend to be more financially secure, while NAB Wellbeing Surveys suggest that older Australians are more likely to recognise the relationship between giving and their overall wellbeing.

By region, the average annual donation size increased slightly in both regional and metropolitan areas (Chart 13). However, average donation size remains higher in metropolitan areas ($345) than in regional areas ($308), which can possibly be explained by higher average incomes in metropolitan areas when compared to regional areas of Australia.

Indepth report

Chart 12: Average annual donation per donor by age band ($A)

500

400

300

200

100

015 to 24 25 to 34 35 to 44 45 to 54 55 to 64 65+

12 mths to Feb 201512 mths to Feb 201412 mths to Feb 2013

Chart 13: Average annual donation perdonor by region ($A)

500

400

300

200

100

0Metropolitan Regional

12 mths to Feb 201512 mths to Feb 201412 mths to Feb 2013

$328$344 $345

$295$305 $308

8

NAB Charitable Giving Index

Australians over the age of 55 typically donate more to all charities, while the youngest Australians donate the least.Australian’s aged 55 to 64 are the biggest donors to Animals & Environment ($241), Cancer ($162), Charitable Lotteries ($239) and Humanitarian Services ($521) charities (Chart 14A and 14B). Those aged 65+ are the biggest donors to Community Service & Children/Family ($297), Health & Disability ($193) and “Other” ($163) charities, while the 45-54 age group are the biggest donors to Medical Research & Services ($174).

It is notable that average annual donations increased in all age groups for Animals & Environment, Cancer, Charitable Lotteries and Humanitarian Services charities.

In contrast, average donations to Community Service & Children/Family fell in the 15 to 24, 25 to 34 and 55 to 64 age groups. It also declined in the 15 to 24 age group in Health & Disability charities, the 15 to 24, 35 to 34, 45 to 54 and 55 to 64 age groups in Medical Research & Services and in the 45 to 54 age group in “Other” charities.

Average donation size increases in all charity sectors in both metropolitan and regional areas except for Medical Research & Services charities.The average annual donation per donor increased in all charity categories in both metropolitan and regional areas, except Medical Research & Services charities (Chart 15A and 15B).

On average, Humanitarian Services charities continue to attract the largest donation in both metropolitan ($438) and regional ($407) locations, with average donations to Humanitarian Services also growing 4.4% and 4.3% respectively.

Average donations in metropolitan areas were higher for Animals & Environment ($219), Community Service & Children/Family ($260), Health & Disability ($164), Medical Research & Services ($158) and “Other” ($121) charities than in regional areas.

In contrast, the average donation to Cancer ($139) and Charitable Lotteries ($219) was bigger in regional areas.

In growth terms, the biggest increase in donation size was seen in regional donations to “Other” charities which grew 8.3% (but off a smaller base) and Charitable Lotteries (6.1%). In metropolitan areas, the biggest growth also occurred in Charitable Lotteries (5%) and “Other” (4.5%) charities, but fell most for Medical Research & Services (-1.9%).

Chart 14A: Average annual donationper donor by age ($A)

550

500

450

400

350

300

250

200

150

100

50

0

12 months to February 2014 12 months to February 2015

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

Animals Cancer Lotteries CS & Children/Family

Chart 14B: Average annual donationper donor by age ($A)

550

500

450

400

350

300

250

200

150

100

50

0

12 months to February 2014 12 months to February 2015

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65+

Health &Disability

Humanitarian MedicalResearch

Other

9

Charitable Giving by Postcode

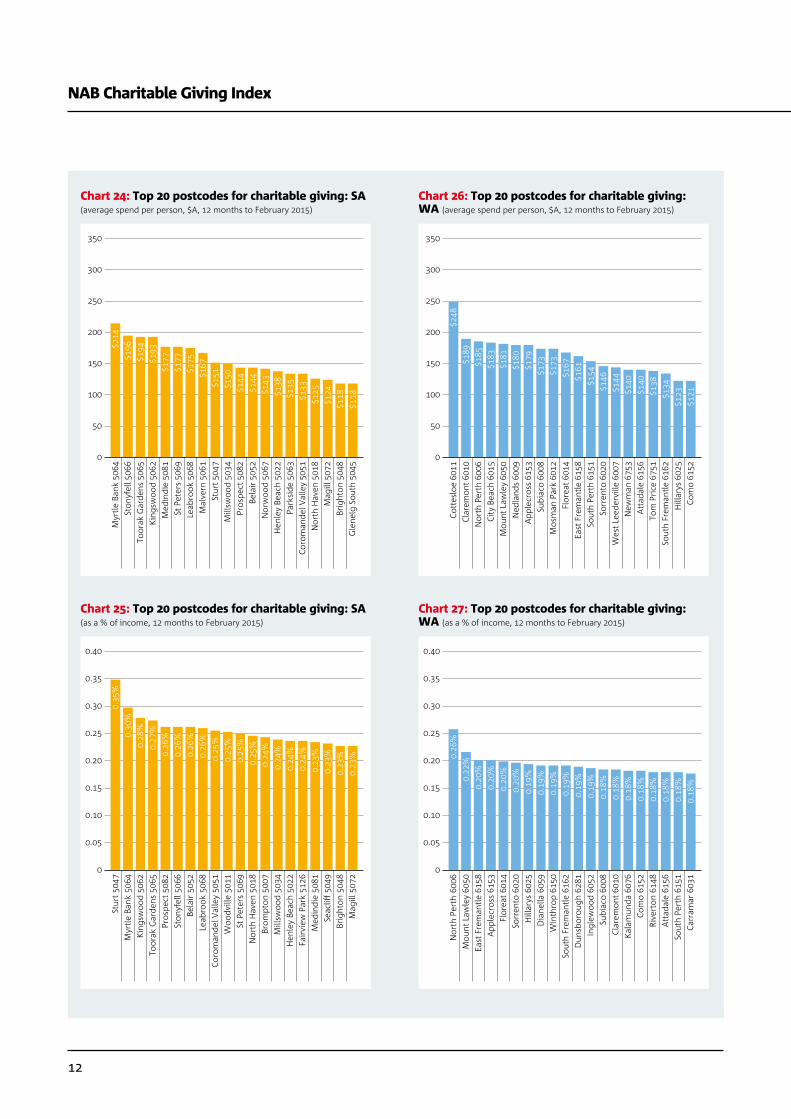

The average donation across all Australian postcodes was $88 per person. Middle Park (3206) in Victoria led the way, with an average donation of $316. As a share of income, Castlemaine (3450) also in Victoria was the most generous, donating 0.36%.The average donation per person across all Australian postcodes was $88 over the year to February 2015.

Among the top 20 suburbs for charitable giving nationally, the average donation was $226 per person (refer to Chart 16 to 33 for the top 20 postcodes in Australia and each state).

Middle Park (3206) in Victoria was the most generous suburb, donating on average $316 per person, or more than 3½ times the national average and around 18% more than in the next most generous suburb of Bellevue Hill NSW (2023) at $268, 20% more than third placed Hunters Hill NSW (2110) at $263 and almost 60% higher than the 20th highest suburb of Hawthorn East Victoria (3123) at $198.

We continue to see a very strong relationship between average dollar giving and average incomes. The average income in the top 20 postcodes was around $107,000, according to data from the Australian Tax Office or more than twice the national average.

Although donors from high income postcodes tend to donate more in dollar terms, they do not donate the most relative to their incomes.

Among the top 20 suburbs for charitable giving nationally as a percentage of their incomes, the average donation was 0.30% per person (compared with an average donation of 0.22% in the top 20 postcodes for dollar giving). Moreover, the average income in this group was just $59,000, around half the average of the top 20 suburbs for dollar giving.

By this measure, Castlemaine (3450) in Victoria was the most generous, donating 0.36% of their annual incomes to charity, followed by Sturt SA (5047) with 0.35%, Fitzroy North Victoria (3068) with 0.32%, Coolangatta QLD (4225) with 0.31%, Maleny QLD (4552) with 0.31%, Croydon NSW (2132) with 0.31% and Hamilton South NSW (2303) with 0.31%.

Middle Park (3206) Victoria, Fitzroy North (3068) Victoria and Myrtle Bank (5064) South Australia are the only suburbs to feature in the top 20 postcodes for charitable giving by dollar amount and as a percentage of their income. n

Indepth report

Chart 15A: Average annual donation per donor: metropolitan ($A)

450

400

350

300

250

200

150

100

50

0

Med

ical

Res

earc

h&

Ser

vice

s

Oth

er

Canc

er

Hea

lth &

Dis

abili

ty

Hum

anita

rian

Serv

ices

Com

mun

ity S

ervi

ce&

Chi

ldre

n/Fa

mily

Ani

mal

s &

Envi

ronm

ent

Char

itabl

e Lo

tter

ies

12 mths to Feb 201512 mths to Feb 201412 mths to Feb 2013

Chart 15B: Average annual donation per donor: regional ($A)

450

400

350

300

250

200

150

100

50

0

Med

ical

Res

earc

h&

Ser

vice

s

Oth

er

Canc

er

Hea

lth &

Dis

abili

ty

Hum

anita

rian

serv

ices

Com

mun

ity S

ervi

ce&

Chi

ldre

n/Fa

mily

Ani

mal

s &

Envi

ronm

ent

Char

itabl

e Lo

tter

ies

12 mths to Feb 201512 mths to Feb 201412 mths to Feb 2013

10

NAB Charitable Giving Index

*excluding postcodes with fewer than 5,000 residents

Chart 16: Top 20 postcodes for charitable giving: Australia (average spend per person, $A, 12 months to February 2015)

350

300

250

200

150

100

50

0

$316

$2

68

$263

$2

48

$245

$2

40

$227

$2

25

$219

$2

19

$215

$2

14

$209

$2

09

$208

$2

05

$202

$1

99

$199

$1

98

Mid

dle

Park

320

6Be

llevu

e H

ill 2

023

Hun

ters

Hill

211

0Co

ttes

loe

6011

Woo

llahr

a 20

25M

osm

an 2

088

Dea

kin

2600

Balm

ain

2041

Vau

clus

e 20

30A

rmad

ale

3143

Fitz

roy

Nor

th 3

068

Myr

tle B

ank

5064

Brig

hton

318

6To

orak

314

2G

ri�

th 2

603

Gor

don

2072

Padd

ingt

on 2

021

Killa

ra 2

071

Seaf

orth

209

2H

awth

orn

East

312

3

Chart 18: Top 20 postcodes for charitable giving: NSW (average spend per person, $A, 12 months to February 2015)

350

300

250

200

150

100

50

0Be

llevu

e H

ill 2

023

Hun

ters

Hill

211

0W

oolla

hra

2025

Mos

man

208

8Ba

lmai

n 20

41V

aucl

use

2030

Gor

don

2072

Padd

ingt

on 2

021

Killa

ra 2

071

Seaf

orth

209

2Li

nd�e

ld 2

070

Rose

ville

206

9Br

onte

202

4Cr

emor

ne 2

090

Pete

rsha

m 2

049

Dar

ling

Poin

t 202

7Ca

stle

crag

206

8H

amilt

on S

outh

230

3W

ahro

onga

207

6Tu

rram

urra

207

4

$268

$2

63

$245

$2

40

$225

$2

19

$205

$2

02

$199

$1

99

$197

$1

95

$194

$1

93

$186

$1

81

$181

$1

78

$175

$1

70

Chart 17: Top 20 postcodes for charitable giving: Australia (as a % of income, 12 months to February 2015)

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0

Cast

lem

aine

345

0St

urt 5

047

Fitz

roy

Nor

th 3

068

Cool

anga

tta

4225

Mal

eny

4552

Croy

don

2132

Ham

ilton

Sou

th 2

303

Blax

land

277

4M

yrtle

Ban

k 50

64H

owra

h 70

18Pe

ters

ham

204

9Br

unsw

ick

East

305

7M

arri

ckvi

lle 2

204

Mac

leod

308

5M

iddl

e Pa

rk 3

206

O’C

onno

r 26

02Ki

ngsw

ood

5062

Alp

hing

ton

3078

Blac

kbur

n 31

30To

orak

Gar

dens

506

5

0.36

%

0.35

%

0.32

%

0.31

%

0.31

%

0.31

%

0.31

%

0.30

%

0.30

%

0.30

%

0.29

%

0.29

%

0.29

%

0.29

%

0.28

%

0.28

%

0.28

%

0.28

%

0.28

%

0.27

%

Chart 19: Top 20 postcodes for charitable giving: NSW (as a % of income, 12 months to February 2015)

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0

Croy

don

2132

Ham

ilton

Sou

th 2

303

Blax

land

277

4Pe

ters

ham

204

9M

arri

ckvi

lle 2

204

New

Lam

bton

230

5A

lsto

nvill

e 24

77W

oy W

oy B

ay 2

256

Kato

omba

278

0G

oone

llaba

h 24

80G

ordo

n 20

72Ki

rraw

ee 2

232

Berr

y 25

35El

eeba

na 2

282

Spri

ngw

ood

2777

Stan

mor

e 20

48Su

mm

er H

ill 2

130

Mos

s V

ale

2577

Gle

be 2

037

Thor

nlei

gh 2

120

0.31

%

0.31

%

0.30

%

0.29

%

0.29

%

0.27

%

0.26

%

0.26

%

0.25

%

0.25

%

0.25

%

0.25

%

0.24

%

0.24

%

0.24

%

0.24

%

0.24

%

0.24

%

0.23

%

0.23

%

11

Indepth report

Chart 20: Top 20 postcodes for charitable giving: Victoria (average spend per person, $A, 12 months to February 2015)

350

300

250

200

150

100

50

0

Mid

dle

Park

320

6A

rmad

ale

3143

Fitz

roy

Nor

th 3

068

Brig

hton

318

6To

orak

314

2H

awth

orn

East

312

3M

alve

rn 3

144

Kew

310

1Ca

nter

bury

312

6Ca

mbe

rwel

l 312

4M

elbo

urne

300

4A

lphi

ngto

n 30

78Su

rrey

Hill

s 31

27Ba

lwyn

310

3A

shbu

rton

314

7N

orth

cote

307

0G

len

Iris

314

6Br

unsw

ick

East

305

7Sa

ndri

ngha

m 3

191

Mac

leod

308

5

$316

$2

19

$215

$2

09

$209

$1

98

$197

$1

96

$193

$1

87

$183

$1

82

$178

$1

63

$162

$1

58

$156

$1

56

$156

$1

53

Chart 22: Top 20 postcodes for charitable giving: Queensland (average spend per person, $A, 12 months to February 2015)

350

300

250

200

150

100

50

0Ye

rong

a 41

04Ch

apel

Hill

406

9A

shgr

ove

4060

Sher

woo

d 40

75Ba

rdon

406

5Pa

ddin

gton

406

4M

ooro

oka

4105

Haw

thor

ne 4

171

Wel

lingt

on P

oint

416

0Co

olan

gatt

a 42

25Sa

mfo

rd V

alle

y 45

20Th

e G

ap 4

061

Thor

nlan

ds 4

164

New

Far

m 4

005

Mal

eny

4552

Indo

oroo

pilly

406

8Co

orpa

roo

4151

Asc

ot 4

007

Clev

elan

d 41

63Ta

rrag

indi

412

1

$189

$1

75

$156

$1

46

$142

$1

41

$137

$1

36

$134

$1

34

$133

$1

32

$129

$1

25

$124

$1

24

$123

$1

20

$119

$1

18

Chart 21: Top 20 postcodes for charitable giving: Victoria (as a % of income, 12 months to February 2015)

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0

Cast

lem

aine

300

0Fi

tzro

y N

orth

300

4Br

unsw

ick

East

300

6M

acle

od 3

008

Mid

dle

Park

301

1A

lphi

ngto

n 30

12Bl

ackb

urn

3013

Brun

swic

k 30

15A

shbu

rton

301

6N

orth

cote

301

8M

ontm

oren

cy 3

019

Burw

ood

3020

Burw

ood

East

302

1Es

send

on 3

023

Surr

ey H

ills

3024

Haw

thor

n Ea

st 3

025

Wat

soni

a N

orth

302

8Co

burg

302

9N

orth

Mel

bour

ne 3

030

Box

Hill

Sou

th 3

031

0.36

%

0.32

%

0.29

%

0.29

%

0.28

%

0.28

%

0.28

%

0.27

%

0.27

%

0.27

%

0.26

%

0.25

%

0.25

%

0.24

%

0.24

%

0.24

%

0.24

%

0.24

%

0.23

%

0.23

%

Chart 23: Top 20 postcodes for charitable giving: Queensland (as a % of income, 12 months to February 2015)

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0

Cool

anga

tta

4225

Mal

eny

4552

Yero

nga

4104

Moo

rook

a 41

05Pa

lmw

oods

455

5Th

ornl

ands

416

4W

ellin

gton

Poi

nt 4

160

Dur

ack

4077

Sher

woo

d 40

75Ch

apel

Hill

406

9Co

oroy

456

3Bu

deri

m 4

556

Ash

grov

e 40

60Ta

mbo

rine

Mou

ntai

n 42

72D

oona

n 45

62Pe

trie

450

2Cl

onta

rf 4

019

Beer

wah

451

9Th

e G

ap 4

061

Ash

mor

e 42

14

0.31

%

0.31

%

0.27

%

0.25

%

0.25

%

0.24

%

0.23

%

0.23

%

0.23

%

0.22

%

0.22

%

0.21

%

0.21

%

0.21

%

0.21

%

0.21

%

0.21

%

0.21

%

0.21

%

0.20

%

12

NAB Charitable Giving Index

Chart 24: Top 20 postcodes for charitable giving: SA (average spend per person, $A, 12 months to February 2015)

350

300

250

200

150

100

50

0

Myr

tle B

ank

5064

Ston

yfel

l 506

6To

orak

Gar

dens

506

5Ki

ngsw

ood

5062

Med

indi

e 50

81St

Pet

ers

5069

Leab

rook

506

8M

alve

rn 5

061

Stur

t 504

7M

illsw

ood

5034

Pros

pect

508

2Be

lair

505

2N

orw

ood

5067

Hen

ley

Beac

h 50

22Pa

rksi

de 5

063

Coro

man

del V

alle

y 50

51N

orth

Hav

en 5

018

Mag

ill 5

072

Brig

hton

504

8G

lene

lg S

outh

504

5

$214

$1

96

$194

$1

93

$177

$1

77

$175

$1

67

$151

$1

50

$144

$1

44

$143

$1

38

$135

$1

33

$125

$1

24

$118

$1

18

Chart 26: Top 20 postcodes for charitable giving:WA (average spend per person, $A, 12 months to February 2015)

350

300

250

200

150

100

50

0Co

ttes

loe

6011

Clar

emon

t 601

0N

orth

Per

th 6

006

City

Bea

ch 6

015

Mou

nt L

awle

y 60

50N

edla

nds

6009

App

lecr

oss

6153

Subi

aco

6008

Mos

man

Par

k 60

12Fl

orea

t 601

4Ea

st F

rem

antle

615

8So

uth

Pert

h 61

51So

rren

to 6

020

Wes

t Lee

derv

ille

6007

New

man

675

3A

ttad

ale

6156

Tom

Pri

ce 6

751

Sout

h Fr

eman

tle 6

162

Hill

arys

602

5Co

mo

6152

$248

$1

89

$185

$1

83

$181

$1

80

$179

$1

73

$173

$1

67

$161

$1

54

$146

$1

44

$140

$1

40

$138

$1

34

$123

$1

21

Chart 25: Top 20 postcodes for charitable giving: SA(as a % of income, 12 months to February 2015)

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0

Stur

t 504

7M

yrtle

Ban

k 50

64Ki

ngsw

ood

5062

Toor

ak G

arde

ns 5

065

Pros

pect

508

2St

onyf

ell 5

066

Bela

ir 5

052

Leab

rook

506

8Co

rom

ande

l Val

ley

5051

Woo

dvill

e 50

11St

Pet

ers

5069

Nor

th H

aven

501

8Br

ompt

on 5

007

Mill

swoo

d 50

34H

enle

y Be

ach

5022

Fair

view

Par

k 51

26M

edin

die

5081

Seac

li� 5

049

Brig

hton

504

8M

agill

507

2

0.35

%

0.30

%

0.28

%

0.27

%

0.26

%

0.26

%

0.26

%

0.26

%

0.25

%

0.25

%

0.25

%

0.25

%

0.24

%

0.24

%

0.24

%

0.24

%

0.23

%

0.23

%

0.23

%

0.23

%

Chart 27: Top 20 postcodes for charitable giving: WA (as a % of income, 12 months to February 2015)

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0

Nor

th P

erth

600

6M

ount

Law

ley

6050

East

Fre

man

tle 6

158

App

lecr

oss

6153

Flor

eat 6

014

Sorr

ento

602

0H

illar

ys 6

025

Dia

nella

605

9W

inth

rop

6150

Sout

h Fr

eman

tle 6

162

Dun

sbor

ough

628

1In

glew

ood

6052

Subi

aco

6008

Clar

emon

t 601

0Ka

lam

unda

607

6Co

mo

6152

Rive

rton

614

8A

ttad

ale

6156

Sout

h Pe

rth

6151

Carr

amar

603

1

0.26

%

0.22

%

0.20

%

0.20

%

0.20

%

0.20

%

0.19

%

0.19

%

0.19

%

0.19

%

0.19

%

0.19

%

0.18

%

0.18

%

0.18

%

0.18

%

0.18

%

0.18

%

0.18

%

0.18

%

13

Indepth report

Chart 28: Top 20 postcodes for charitable giving:Tasmania (average spend per person, $A, 12 months to February 2015)

350

300

250

200

150

100

50

0

Sout

h H

obar

t 700

4H

owra

h 70

18Sa

ndy

Bay

7005

Wes

t Hob

art 7

000

Mar

gate

705

4Bl

ackm

ans

Bay

7052

Lind

isfa

rne

7015

King

ston

705

0N

ew T

own

7008

Rane

lagh

710

9La

unce

ston

725

0U

lver

ston

e 73

15W

ynya

rd 7

325

Wes

t Moo

nah

7009

Clar

emon

t 701

1D

evon

port

731

0So

uth

Laun

cest

on 7

249

Latr

obe

7307

Mon

tello

732

0Sm

ithto

n 73

30

$142

$1

39

$133

$1

08

$104

$1

02

$102

$1

01

$96

$86

$77

$70

$70

$68

$63

$60

$59

$57

$53

$45

Chart 30: Top 20 postcodes for charitable giving:ACT (average spend per person, $A, 12 months to February 2015)

350

300

250

200

150

100

50

0D

eaki

n 26

00G

ri�

th 2

603

Hug

hes

2605

O’C

onno

r 26

02Fa

rrer

260

7Ch

apm

an 2

611

Haw

ker

2614

Nar

rabu

ndah

260

4Ca

mpb

ell 2

612

Kam

bah

2902

Mon

ash

2904

Mac

greg

or 2

615

Kale

en 2

617

Lyon

s 26

06W

anni

assa

290

3N

icho

lls 2

913

Har

riso

n 29

14G

ordo

n 29

06Ca

lwel

l 290

5Ci

ty 2

601

$227

$208

$179

$178

$170

$168

$154

$152

$143

$132

$126

$115

$114

$111

$106

$91

$88

$81

$78

$57

Chart 29: Top 20 postcodes for charitable giving: Tasmania (as a % of income, 12 months to February 2015)

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0

How

rah

7018

Sout

h H

obar

t 700

4Ki

ngst

on 7

050

Sand

y Ba

y 70

05Li

ndis

farn

e 70

15M

arga

te 7

054

Rane

lagh

710

9Bl

ackm

ans

Bay

7052

Wes

t Hob

art 7

000

New

Tow

n 70

08U

lver

ston

e 73

15W

ynya

rd 7

325

Laun

cest

on 7

250

Wes

t Moo

nah

7009

Clar

emon

t 701

1D

evon

port

731

0So

uth

Laun

cest

on 7

249

Latr

obe

7307

Mon

tello

732

0Sm

ithto

n 73

30

0.30

%

0.26

%

0.22

%

0.22

%

0.22

%

0.22

%

0.22

%

0.22

%

0.21

%

0.20

%

0.17

%

0.16

%

0.16

%

0.16

%

0.15

%

0.14

%

0.14

%

0.13

%

0.12

%

0.11

%

Chart 31: Top 20 postcodes for charitable giving: ACT (as a % of income, 12 months to February 2015)

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0

O’C

onno

r 26

02Ch

apm

an 2

611

Dea

kin

2600

Farr

er 2

607

Haw

ker

2614

Hug

hes

2605

Kam

bah

2902

Cam

pbel

l 261

2G

ri�

th 2

603

Mac

greg

or 2

615

Mon

ash

2904

Nar

rabu

ndah

260

4Ka

leen

261

7W

anni

assa

290

3Ly

ons

2606

Nic

holls

291

3G

ordo

n 29

06H

arri

son

2914

Calw

ell 2

905

City

260

1

0.28

%0.

27%

0.27

%0.

26%

0.26

%0.

25%

0.23

%0.

22%

0.22

%0.

21%

0.20

%0.

20%

0.20

%0.

18%

0.18

%0.

15%

0.14

%0.

14%

0.14

%0.

10%

14

NAB Charitable Giving Index

Chart 32: Top 9 postcodes for charitable giving:NT (average spend per person, $A, 12 months to February 2015)

350

300

250

200

150

100

50

0

Fann

ie B

ay 8

20

Lean

yer

812

Nig

htcl

i� 8

10

Gill

en 8

70

Kath

erin

e 85

0

Dur

ack

830

Rose

bery

832

Hum

pty

Doo

836

Bees

Cre

ek 8

22

$103

$95

$89

$80

$72

$71

$64

$58

$38

Chart 33: Top 9 postcodes for charitable giving: NT (as a % of income, 12 months to February 2015)

0.40

0.35

0.30

0.25

0.20

0.15

0.10

0.05

0

Lean

yer

812

Nig

htcl

i� 8

10

Fann

ie B

ay 8

20

Gill

en 8

70

Kath

erin

e 85

0

Dur

ack

830

Rose

bery

832

Bees

Cre

ek 8

22

Hum

pty

Doo

836

0.17

%

0.16

%

0.15

%

0.15

%

0.14

%

0.13

%

0.11

%

0.10

%

0.10

%

About Quantium

Quantium is Australia’s leading data analytics and marketing strategy firm. Quantium has worked with NAB for more than 6 years, assessing de-identified transaction data to derive insights, trends and shopping habits of different customer groups. The resulting analysis forms Market Blueprint and is used by NAB and other businesses to drive innovation and business performance through customer, distribution and marketing strategies. www.quantium.com.au

Changes to the dataQuantium implements ongoing data improvements to Market Blueprint to better capture donation spend in their analysis. As the priority for the NAB Charitable Giving Index is to provide an accurate representation of the Australian donation landscape, Quantium is required to recalculate historical results at each release using the revised data.

For this update, NAB and Quantium have undertaken a thorough review of individual charity categorisations with the aim of improving how charities are represented in the publication. The main impact of this re-classification is the separation of charitable lotteries from “Other” into a standalone category. Medical Research has also been affected due to the reclassification of two major charities - Mater Prize Home (moved to Charitable Lotteries) and Fred Hollows Foundation (moved to Health & Disability). At an overall level and for the remaining categories, the impact of re-classification has been small.

Further to this, data improvements have been made to individual charities as at every release. At this release, improvements in data associated with Australian Red Cross have been made. Humanitarian Services and the overall index have been affected in particular.

As part of Quantium’s regular review process, there has also been a re-alignment in how average annual donations per donor are calculated. As a result, there have been some upward revisions to average annual donations per donor relative to previous reports. Note that this only impacts the average annual donation metric, while other metrics (indices, market share and donations by postcode) are unchanged.

15

Indepth report

Important notice.DISCLAIMER: While care has been taken in preparing this material, National Australia Bank Limited (ABN 12 004 044 937) does not warrant or represent that the information, recommendations, opinions or conclusions contained in this document (“Information”) are accurate, reliable, complete or current. The Information has been prepared for dissemination to professional investors for information purposes only and any statements as to past performance do not represent future performance. The Information does not purport to contain all matters relevant to any particular investment or financial instrument and all statements as to future matters are not guaranteed to be accurate. In all cases, anyone proposing to rely on or use the Information should independently verify and check the accuracy, completeness, reliability and suitability of the Information and should obtain independent and specific advice from appropriate professionals or experts.

To the extent permissible by law, the National shall not be liable for any errors, omissions, defects or misrepresentations in the Information or for any loss or damage suffered by persons who use or rely on such Information (including by reasons of negligence, negligent misstatement or otherwise). If any law prohibits the exclusion of such liability, the National limits its liability to the re-supply of the Information, provided that such limitation is permitted by law and is fair and reasonable. The National, its affiliates and employees may hold a position or act as a price maker in the financial instruments of any issuer discussed within this document or act as an underwriter, placement agent, adviser or lender to such issuer.

UK DISCLAIMER: If this document is distributed in the United Kingdom, such distribution is by National Australia Bank Limited, 88 Wood Street, London EC2V 7QQ. Registered in England BR1924. Head Office: 800 Bourke Street, Docklands, Victoria, 3008. Incorporated with limited liability in the State of Victoria, Australia. In the United Kingdom NAB is subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority.

U.S DISCLAIMER: If this document is distributed in the United States, such distribution is by nabSecurities, LLC. This document is not intended as an offer or solicitation for the purchase or sale of any securities, financial instrument or product or to provide financial services. It is not the intention of nabSecurities to create legal relations on the basis of information provided herein.

NEW ZEALAND DISCLAIMER: This publication has been provided for general information only. Although every effort has been made to ensure this publication is accurate the contents should not be relied upon or used as a basis for entering into any products described in this publication. To the extent that any information or recommendations in this publication constitute financial advice, they do not take into account any person’s particular financial situation or goals. Bank of New Zealand strongly recommends readers seek independent legal/financial advice prior to acting in relation to any of the matters discussed in this publication. Neither Bank of New Zealand nor any person involved in this publication accepts any liability for any loss or damage whatsoever may directly or indirectly result from any advice, opinion, information, representation or omission, whether negligent or otherwise, contained in this publication. National Australia Bank Limited is not a registered bank in New Zealand.

JAPAN DISCLAIMER: National Australia Bank Ltd. has no license of securities-related business in Japan. Therefore, this document is only for your information purpose and is not intended as an offer or solicitation for the purchase or sale of the securities described herein or for any other action.

© 2015 National Australia Bank Limited ABN 12 004 044 937 AFSL and Australian Credit Licence 230686 A116163-0515

To discuss this report in more detail, please speak with your NAB Relationship Manager, email [email protected], or contact:

Alan OsterGroup Chief Economist National Australia Bank+61 (0) 3 8634 2927 [email protected]

Tony Davis Director Quantium +61 (0) 2 9292 6400 [email protected]