n u i 4 • planning guide the accounting cycle...

TRANSCRIPT

CHAPTER 14 • PLANNING GUIDE

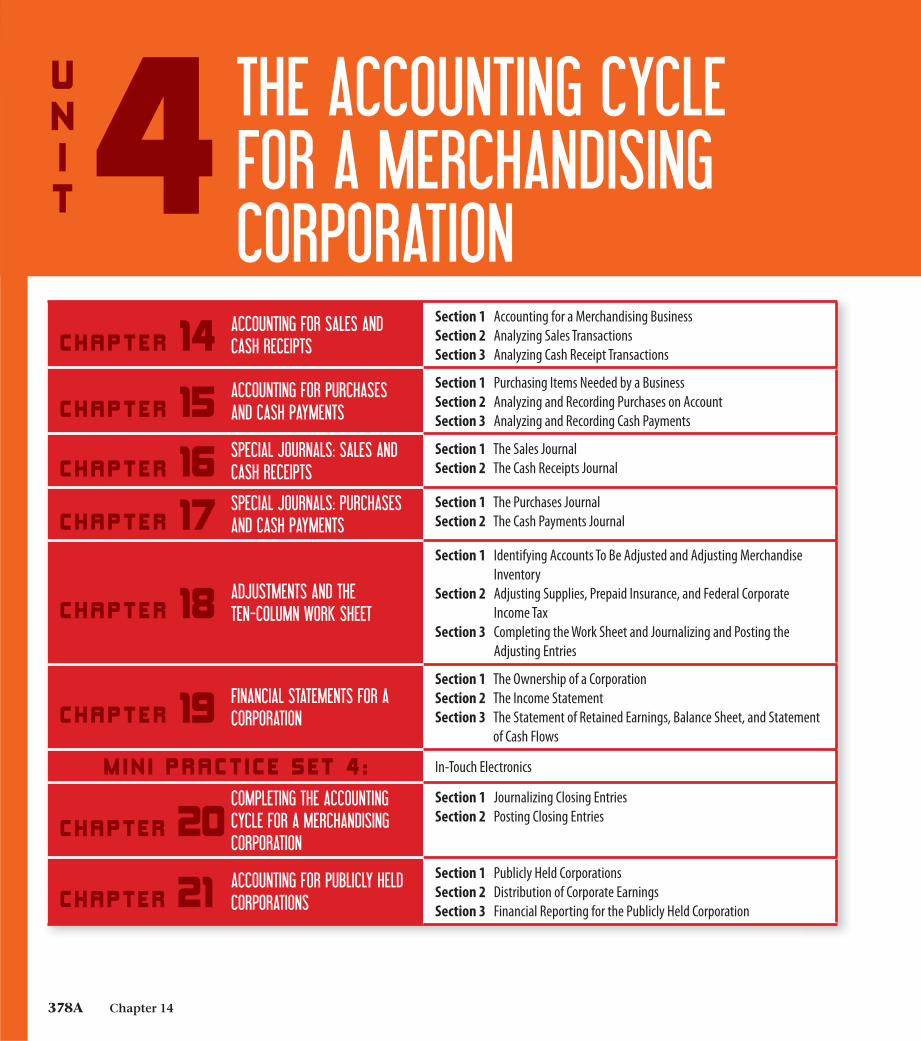

4UNIT

THE ACCOUNTING CYCLE FOR A MERCHANDISING CORPORATION

CHAPTER 14 ACCOUNTING FOR SALES AND CASH RECEIPTS

Section 1 Accounting for a Merchandising BusinessSection 2 Analyzing Sales TransactionsSection 3 Analyzing Cash Receipt Transactions

CHAPTER 15 ACCOUNTING FOR PURCHASES AND CASH PAYMENTS

Section 1 Purchasing Items Needed by a BusinessSection 2 Analyzing and Recording Purchases on AccountSection 3 Analyzing and Recording Cash Payments

CHAPTER 16 SPECIAL JOURNALS: SALES AND CASH RECEIPTS

Section 1 The Sales JournalSection 2 The Cash Receipts Journal

CHAPTER 17 SPECIAL JOURNALS: PURCHASES AND CASH PAYMENTS

Section 1 The Purchases JournalSection 2 The Cash Payments Journal

CHAPTER 18 ADJUSTMENTS AND THE TEN-COLUMN WORK SHEET

Section 1 Identifying Accounts To Be Adjusted and Adjusting Merchandise Inventory

Section 2 Adjusting Supplies, Prepaid Insurance, and Federal Corporate Income Tax

Section 3 Completing the Work Sheet and Journalizing and Posting the Adjusting Entries

CHAPTER 19 FINANCIAL STATEMENTS FOR A CORPORATION

Section 1 The Ownership of a CorporationSection 2 The Income StatementSection 3 The Statement of Retained Earnings, Balance Sheet, and Statement

of Cash Flows

M IN I PRACT I C E SET 4 : In-Touch Electronics

CHAPTER 20COMPLETING THE ACCOUNTING CYCLE FOR A MERCHANDISING CORPORATION

Section 1 Journalizing Closing EntriesSection 2 Posting Closing Entries

CHAPTER 21 ACCOUNTING FOR PUBLICLY HELD CORPORATIONS

Section 1 Publicly Held CorporationsSection 2 Distribution of Corporate EarningsSection 3 Financial Reporting for the Publicly Held Corporation

378A Chapter 14

378A_378B_U4_INT_895867.indd 378A 12/2/10 11:30 AM

READING GUIDEThe Essential Question, chapter objectives, and Main Idea are previewed here.

ACADEMIC STANDARDS

Academic Standards are integrated into each chapter.

Academic VocabularyAcademic Vocabulary throughout the text helps students learn words that they will see in their reading and on tests.

Review and Assessment Reading comprehension, Content and Academic Vocabulary, and academic integration activities provide opportunities to assess skills and apply content to academic situations.

PROBLEMSEnd-of-section and end-of-chapter problems give students the opportunity to complete comprehensive problems that integrate the accounting skills they have learned so far.

REAL WORLD Accounting Careers

Real accountants give information and advice about their experiences working in the accounting fi eld.

REAL WORLD Applications & Connections

These exercises give students practice completing activities that connect accounting to the real world of business. • Case Study• Career Wise• A Matter of Ethics• HOT Audit• 21st Century Skills• Spotlight on Personal Finance• Global Accounting

Common Mistakes Accuracy is key in accounting and this feature provides examples of the most common types of accounting mistakes.

Connect to HistoryCCoonnnneeccttt tttoo HHHiiissttoorryyrr

This feature describes important milestones in the history of accounting and business fi nance.

FOCUS ON THE PHOTO The units begin with a photo and a caption that asks students a question designed to help them start thinking about what they will read.

Keys to SuccessThese unit-opener features encourage students to think about the kinds of skills that will help them excel in the workplace.

MINI PRACTICE SETSThese problems give students practice in applying the accounting concepts they have learned over multiple chapters.

Academic Rigor Real-World Connections Unit Resources

UNIT COURSE MANAGER

Chapter 14 378B

378A_378B_U4_INT_895867.indd 378B 12/2/10 11:30 AM

4UNIT

THE ACCOUNTING CYCLE FOR A MERCHANDISING CORPORATION

378_379_U04_UO_893567.indd 378 8/31/10 7:31 PM

INTRODUCING UNIT 4

FOCUSLook BackIn Unit 3, students learned the basic accounting cycle, and how to use the general journal and general ledger.

Look AheadUnit 4 builds on prior learning by expanding the cycle to include using the special journals, subsidiary ledgers, and adjustments.

Chapter 14: Accounting for Sales and Cash Receipts

Chapter 15: Accounting for Purchases and Cash Payments

Chapter 16: Special Journals: Sales and Cash Receipts

Chapter 17: Special Journals: Purchases and Cash Payments

Chapter 18: Adjustments and the Ten-Column Work Sheet

Chapter 19: Financial Statements for a Corporation

Chapter 20: Completing the Accounting Cycle for a Merchandising Corporation

Chapter 21: Accounting for Publicly Held Corporations

TEACHUnit Launch ActivityHave students identify what a merchandising business does. Ask them to identify the differences and similarities that they think exist between it and a service business. Have them review the characteristics of sole proprietorships and corporations.

Beginning students might have a limited view of what skills they should develop in order to prepare for a career in accounting. In today’s workplace, they will need more than accounting and math skills. According to the Website careers-in-accounting.com, the scope of skills required for success in the field is becoming much broader. Skills now considered to be important include the following: people skills, sales skills, communication skills, analytical skills, ability to synthesize, creative ability, initiative, and computer skills. Students need to prepare themselves to meet the demands of this expanding view of an accountant’s job.

Trends in Accounting

378 Unit 4

378_379_U04_UO_895867.indd 378 11/24/10 4:08 PM

Speaking and Listening Present information, findings, and supporting evidence such that listeners can follow the line of reasoning and the organization, development, and style are appropriate to task, purpose, and audience.

glencoe.com Get podcasts, videos, and accounting forms.

mac

FOCUS ON THE PHOTOBecause you purchase most products, such as clothing, from merchandising corporations, learning about these companies can help you be a wise consumer. What are some large merchandising corporations and what popular items do they sell?

English Language ArtsSpeaking and Listening Using spoken language eff ectively will help you lead others in the workplace. Assume you are a representative of the merchandising corporation of your choice. Give a short presentation about the company, including such information as product line, current sales fi gures and number of stores. What image of the company are you trying to project? How might visual data help get across your message?

Keys to SuccessQ Why are good speaking and listening skills

essential to career advancement?

A A common trait among managers and leaders is the ability to eff ectively communicate with others. People in leadership positions often speak to small and large groups. Whether to inform or to inspire, strong public speakers present their remarks in a style appropriate to the topic, purpose, and audience. They demonstrate command of English and get across their information clearly and concisely, enhancing their presentation with visual displays of data.

<<< A LOOK BACKUnit 3 described the payroll system, including calculating and journalizing payroll for a sole proprietorship.

A LOOK AHEAD >>>In Unit 4, you will switch from sole proprietorships to learn how to complete the accounting cycle for a merchandising corporation.

379

378_379_U04_UO_893567.indd 379 9/1/10 2:00 PM

INTRODUCING UNIT 4

College and Career Readiness

English Language Arts As a follow-up activity, help students prepare an outline for a short presentation about the company, organizing outline topics by information such as product line, current sales fi gures, and number of stores. Ask students what they learned from the assignment and the follow-up activity.

Communicate Clearly The merchandising business in this photo is a clothing store. The employee in the photo is providing customer service over the phone. By using communication and collaboration skills effectively, this representative of the merchandising business can get across information clearly and concisely, enhancing and promoting present and future customer relations. Divide students into groups and ask them to choose one of their company outlines, and have them research that company further. Have groups present their information orally, making sure that every member contributes some information about the company.

FOCUS ON THE PHOTO Possible answer: Some corporations include: Target and Walmart, which sell a variety of products, from household items and electronics to gardening supplies and food; CVS stores, which operate pharmacies and also sell miscellaneous products; and Foot Locker, which sells shoes.

glencoe.com

For teaching suggestions and sample answers, go to glencoe.com and click on Teacher Center.

ASSESS/CLOSEHave students draw the accounting cycle for a merchandising business. At each stage, they should identify the transactions that occur, the accounting forms involved, and the activities performed.

Gifted Students Have students choose a corporation that is publicly traded that interests them. Have them track the value of the corporation’s stock over the period of time they study this unit

and read articles about it in the fi nancial media. Ask them at the end of the unit to suggest reasons for the stock’s increase, decrease, or stability.

Spatial Learning Have students make a visual presentation, demonstrating the operating cycle for a merchandising business, and show where the cycle differs for a service business.

Differentiated Instruction

Unit 4 379

378_379_U04_UO_895867.indd 379 11/24/10 4:08 PM

CHAPTER 14 • PLANNING GUIDE

SECTION RESOURCESSection College & Career Readiness Professional Development

SECTION 14.1 ACCOUNTING FOR A MERCHANDISING BUSINESS Reading Strategy, pp. 383, 384, 385

Critical Thinking, pp. 383, 384, 385 English Language Learners, p. 384Teacher to Teacher, p. 384

A wholesale sells to retailers, and a retailer sells to the fi nal users.

SECTION 14.2 ANALYZING SALES TRANSACTIONS Critical Thinking, pp. 387, 388, 389, 390,

392, 393, 394Reading Strategy, pp. 388, 390, 391, 392, 394Writing Support, pp. 389, 393Differentiated Instruction, pp. 387, 390Math Skill Practice, pp. 390, 391

Extended Skill Practice, pp. 389, 391, 392

In addition to using the general ledger, a business keeps a subsidiary ledger of individual customer accounts.

SECTION 14.3 ANALYZING CASH RECEIPT TRANSACTIONS Critical Thinking, pp. 397, 398, 399, 400,

401, 402, 403Reading Strategy, pp. 399, 402, 403Differentiated Instruction, p. 402Math Skill Practice, pp. 398, 399, 400, 401

Extended Skill Practice, pp. 399, 401Extending the Content, p. 400Connect to History, p. 403Case Study, p. 41421st Century Skills, p. 414Career Wise, p. 415Spotlight on Personal Finance, p. 415H.O.T. Audit, p. 415

Merchandising businesses receive cash from cash sales, payments on account, bankcard sales, and occasionally from other types of transactions.

PACING YOUR LESSONS

Chapter Introduction Section 1 Section 2 Section 3 Chapter Assessment

1 period 1 period 2 periods 2 periods 1 period

P

*This pacing guide is based on a traditional 36-week course. See pp. TM38–TM39 for complete pacing guide information.

380A Chapter 14

380A_380B_C14_INT_895867.indd 380A 12/2/10 10:56 AM

STANDARDS AND SKILLS • CHAPTER 14

STANDARDS-BASED LESSON PLANNational Standards for Business Education

StandardsI.A.4 Explain how accounting information is used to allocate resources in the business and personal decision-making process

IV.B.4 Determine the cost of inventory for merchandising and manufacturing businesses and apply appropriate valuation methods

IV.E.1 Describe the criteria used to determine revenue recognition

VI.A.2 Identify and apply appropriate information technology to the accounting system

PROFESSIONALDEVELOPMENT

Targeted professional development is correlated throughout Glencoe Accounting. The McGraw-Hill Professional Development Mini Clip Video Library provides teaching strategies to strengthen academic and learning skills. Log on to glencoe.com.

In this Chapter, you will fi nd these Mini Clips:• Reading: Strategic Readers, p. 385• ELL: Graphic Organizers, p. 388• Math: Introducing Multi-Step Equations, p. 390 • Reading: Vocabulary, p. 393 • Reading: Planning and Classroom Management, p. 397• Math: The Meaning of Equality, p. 402

*Highlighted blocks indicate areas covered in the chapter. Additional skills are also covered throughout the Teacher Edition.

Resources: Allocating Time Allocating Money Allocating Material and Facility Resources

Allocating Human Resources

Information:Acquiring and

Evaluating Information

Organizing and Maintaining Information

Interpreting and Communicating

Information

Using Computers to Process Information

Interpersonal Skills: Participating as a Member of a Team Teaching Others Serving Clients/

Customers Exercising Leadership Negotiating to Arrive at a Decision

Working With Cultural Diversity

Systems: Understanding Systems

Monitoring and Correcting Performance

Improving and Designing Systems

Technology: Selecting Technology Applying Technology to Task

Maintainingand Troubleshooting

Technology

21st Century Skills Correlations

*See pp. TM33–TM35 for detailed NBEA standards and correlations.

Chapter 14 380B

380A_380B_C14_INT_895867.indd 380B 12/3/10 8:31 AM

CORRELATIONS TO NATIONAL STANDARDS FOR BUSINESS EDUCATION

See p. TM33 for a detailed correlation chart.Standards: I.A.4, I.C.3, I.C.4, I.C.5, IV.B.1, IV.B.4, IV.E.1, VI.A.2

FOCUS

Dutch Valley Foods offers monthly specials to retailers to boost sales to retailers nationwide. The company distributes wholesale products, including well-known brands as well as organic, gluten-free, and novelty candy items, to retailers via its own fleet of trucks that travel to 27 states. To facilitate shipments to the remaining 23 states and Puerto Rico, Dutch Valley Foods uses the services of UPS.

Analyze Possible answer: Accept all reasonable answers. When Dutch Valley Foods sells to retailers, the general ledger accounts that are affected might include the Merchandise Inventory, Sales, Accounts Receivable, Accounts Payable, and Cash in Bank.

FOCUS ON THE PHOTO Visual LiteracyPossible answer: The product or service sold, amount of the sale, terms, amount of any tax, and the name/account of the buyer. Ask: What do you already know about sales and cash receipts regarding a merchandising business? Possible answer: Students might be familiar with sales and cash receipts transactions by working as a sales clerk for a merchandising business, or by selling tickets, candy, or magazines for a school fundraiser.

D h V ll F d ff hl

REAL-WORLD Business Connection

glencoe.com Get podcasts, videos, and accounting forms.

REAL-WORLD Business Connection

FOCUS ON THE PHOTOAs a wholesale merchandising business, Dutch Valley Foods depends on sales of its bulk items, such as nuts and dried fruit. Accurate tracking of such sales transactions helps this company decide what products to off er. What information from sales do you think should be recorded in the accounting records?

Dutch Valley FoodsNuts from supermarket bulk bins, jars of jam from a gift basket, maple syrup on a restaurant table. There is a chance some or even all of them moved through the warehouses of Pennsylvania-based distributor Dutch Valley Foods before reaching you. The company buys food and nonfood products from vendors that include such well-known brands as Hershey, Keebler and Smucker, and then sells them in bulk to the retail businesses that sell directly to you. Dutch Valley Foods is a wholesaler, a business that sells to retailers.

Connect to the BusinessRetailers buy merchandise from Dutch Valley Foods for resale to the public. Depending on sales policy, the retailer will accept payment in a variety of forms. Each form of payment aff ects a diff erent general ledger account.

AnalyzeWhen Dutch Valley Foods sells foods to retailers, what general ledger accounts do you think are aff ected?

BIG IDEAAs a consumer, you have

frequent contact with merchandising businesses.

ACCOUNTING FOR SALES AND CASH RECEIPTS

14CHAPTER

380_382_C14_CO_893567.indd 380 9/10/10 12:52 PM

INTRODUCING CHAPTER 14

BIG IDEA

Merchandising businesses, which include wholesalers and retailers, provide the products that consumers buy. Retailers include stores and markets where consumers shop.

380 Chapter 14

380_382_C14_CO_895867.indd 380 11/24/10 5:31 PM

TEACH Previewing the Main IdeasUse these questions and activities at the beginning of the sections to focus on the Main Ideas.

SECTION 14.1 ACCOUNTING FOR A MERCHANDISING BUSINESSAsk: What is a merchandising business? It is a business that buys goods from wholesalers and sells them to the final user or consumer. Tell students that a merchandising business is most often a retailer but can also be a wholesaler.

SECTION 14.2 ANALYZING SALES TRANSACTIONSAsk: Why do businesses need a general ledger? A general ledger maintains and organizes the accounts used for the preparation of financial statements. Tell students they will learn about an accounts receivable subsidiary ledger, which maintains all customer accounts resulting from the sale of merchandise on account.

SECTION 14.3 ANALYZING CASH RECEIPT TRANSACTIONSAsk: What is a cash receipt? It is money received by a business. Tell students that a merchandising business has several different sources of cash receipts.

381

380_382_C14_CO_893567.indd 381 9/8/10 12:22 PM

INTRODUCING CHAPTER 14

The interactive student text and working papers can be found on McGraw-Hill Connect.

Online Learning CenterGet activity and game ideas, reproducible forms, and links to additional accounting resources.

Glencoe Technology Solutions

glencoe.com

Chapter 14 381

380_382_C14_CO_895867.indd 381 11/24/10 5:32 PM

Before You ReadBefore You Read

READING GUIDE STANDARDS

CHAPTER 14

Chapter Objectives

Main IdeaA wholesaler sells to retailers, and a retailer sells to the fi nal users. In addition to using the general ledger, a business keeps a subsidiary ledger of individual customer accounts. Merchandising businesses receive cash from cash sales, payments on account, bankcard sales, and occasionally from other types of transactions.

The Essential Question How do merchandising businesses keep track of what is sold and how much money is collected?

Concepts

C1 Explain the difference between a service business and a merchandising business. (p. 383)

C2 Explain the difference between a retailer and a wholesaler. (p. 383)

Analysis

A1 Analyze transactions relating to the sale of merchandise. (p. 387)

Procedures

P1 Record sales and cash receipt transactions in a general journal. (p. 396)

STANDARDS

ACADEMIC

English Language ArtsNCTE 4 Use common written language to communicate effectively. (p. 406)

MathematicsNCTM Problem Solving Solve problems that arise in mathematics and in other contexts. (p. 406)

NCTE National Council of Teachers of EnglishNCTM National Council of Teachers of Mathematics

Common Core

Reading Read closely to determine what the text says explicitly and to make logical inferences from it; cite specific textual evidence when writing or speaking to support conclusions drawn from the text. (p. 406)

382 Chapter 14 Accounting for Sales and Cash Receipts

380_382_C14_CO_893567.indd 382 8/31/10 5:37 PM

INTRODUCING CHAPTER 14

FOCUS READING GUIDE

Before You ReadThe Essential Question The essential question encourages students to inquire about the underlying purpose of accounting. Use the essential question as a discussion starter, emphasizing to students that there are no right or wrong answers.

Main IdeaHave students give some examples of a retailer and a wholesaler. Then have students read the Main Idea in Before You Read. Ask: Why do consumers buy from retailers rather from wholesalers? primarily because of sales restrictions

Chapter Objectives Have students review the objectives to set expectations for what they’ll learn in Chapter 14.

Academic StandardsHelp students see cross-curricular connections whenever possible.

College and Career Readiness standards emphasize skills and concepts students will need beyond high school.

Connect to the Reading Guide Use the following questions to help students connect to the reading.1. What does the chapter title tell you?

Predict2. What do you already know about this

subject from personal experience? Activate Prior Knowledge

3. What have you learned about this in the earlier chapters? Make Connections

4. What gaps exist in your knowledge of this subject? Set a Purpose for Reading

Print• Chapter Study Guides and

Working Papers pp. 343–388• Fast File Chapter 14 ResourcesDigital Transparencies(TeacherWorks Plus)• Section 1: Transparencies 14-1 to

14-2

• Section 2: Transparencies 14-3 to 14-10

• Section 3: Transparencies 14-11 to 14-20

Technology• Presentation Plus! • TeacherWorks Plus

• Peachtree Accounting Software and Applications

• Using QuickBooks® with Glencoe Accounting

Online• McGraw-Hill Connect• Glencoe Accounting Online

Learning Center

CHAPTER 14 RESOURCES MANAGER

382 Chapter 14

380_382_C14_CO_895867.indd 382 11/24/10 5:32 PM

ACCOUNTING FOR A MERCHANDISING BUSINESS

SECTION 14.1

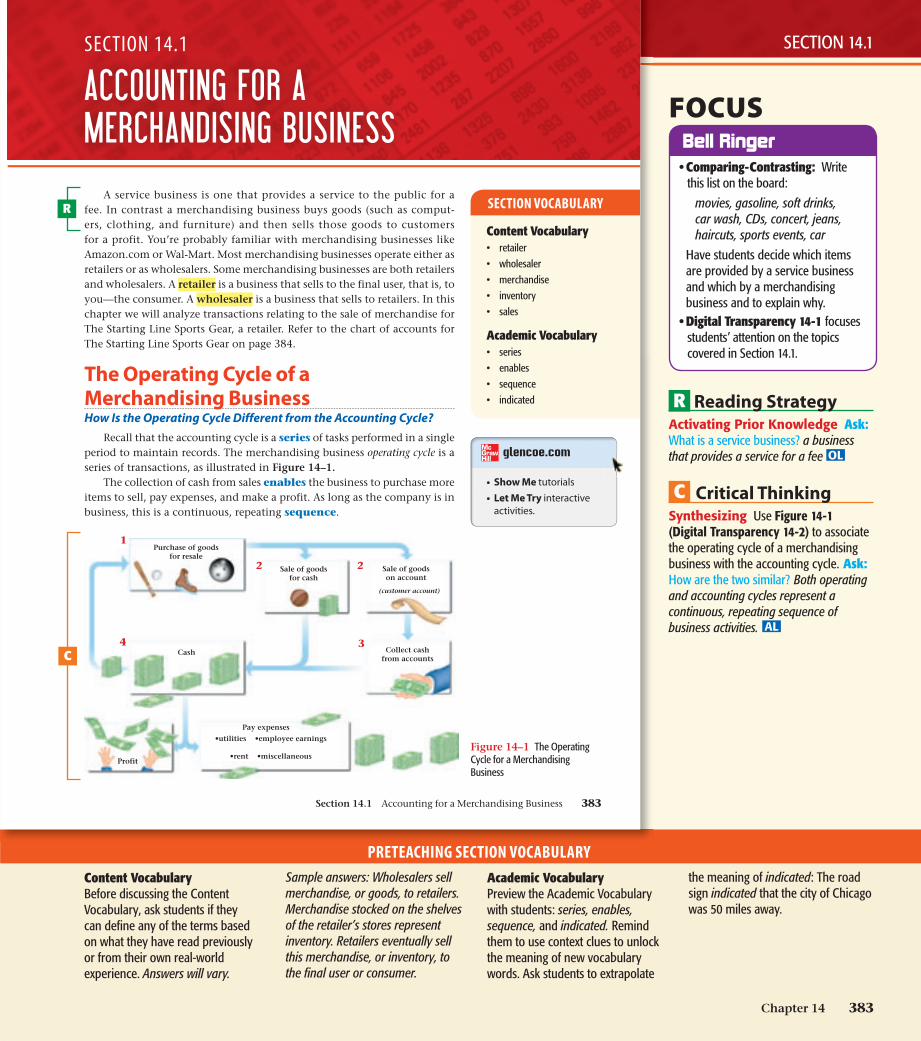

A service business is one that provides a service to the public for a fee. In contrast a merchandising business buys goods (such as comput-ers, clothing, and furniture) and then sells those goods to customers for a profit. You’re probably familiar with merchandising businesses like Amazon.com or Wal-Mart. Most merchandising businesses operate either as retailers or as wholesalers. Some merchandising businesses are both retailers and wholesalers. A retailer is a business that sells to the final user, that is, to you—the consumer. A wholesaler is a business that sells to retailers. In this chapter we will analyze transactions relating to the sale of merchandise for The Starting Line Sports Gear, a retailer. Refer to the chart of accounts for The Starting Line Sports Gear on page 384.

The Operating Cycle of a Merchandising BusinessHow Is the Operating Cycle Different from the Accounting Cycle?

Recall that the accounting cycle is a series of tasks performed in a single period to maintain records. The merchandising business operating cycle is a series of transactions, as illustrated in Figure 14–1.

The collection of cash from sales enables the business to purchase more items to sell, pay expenses, and make a profit. As long as the company is in business, this is a continuous, repeating sequence.

Purchase of goodsfor resale

Profit

Cash

Pay expenses

•utilities •employee earnings

•rent •miscellaneous

2 Sale of goodsfor cash

2

3

Sale of goodson account

(customer account)

Collect cashfrom accounts

1

4

SECTION VOCABULARY

Content Vocabulary• retailer

• wholesaler

• merchandise

• inventory

• sales

Academic Vocabulary• series

• enables

• sequence

• indicated

glencoe.com

• Show Me tutorials • Let Me Try interactive

activities.

Figure 14–1 The Operating Cycle for a Merchandising Business

Section 14.1 Accounting for a Merchandising Business 383

383-404_C14_SEC_893567.indd 383 8/31/10 5:23 PM

R

C

SECTION 14.1

FOCUSBell Ringer • Comparing-Contrasting: Write

this list on the board:

movies, gasoline, soft drinks, car wash, CDs, concert, jeans, haircuts, sports events, car

Have students decide which items are provided by a service business and which by a merchandising business and to explain why.

• Digital Transparency 14-1 focuses students’ attention on the topics covered in Section 14.1.

Bell Ringer

R Reading StrategyActivating Prior Knowledge Ask: What is a service business? a business that provides a service for a fee OL

C Critical ThinkingSynthesizing Use Figure 14-1 (Digital Transparency 14-2) to associate the operating cycle of a merchandising business with the accounting cycle. Ask: How are the two similar? Both operating and accounting cycles represent a continuous, repeating sequence of business activities. AL

PRETEACHING SECTION VOCABULARYContent VocabularyBefore discussing the Content Vocabulary, ask students if they can defi ne any of the terms based on what they have read previously or from their own real-world experience. Answers will vary.

Sample answers: Wholesalers sell merchandise, or goods, to retailers. Merchandise stocked on the shelves of the retailer’s stores represent inventory. Retailers eventually sell this merchandise, or inventory, to the fi nal user or consumer.

Academic VocabularyPreview the Academic Vocabulary with students: series, enables, sequence, and indicated. Remind them to use context clues to unlock the meaning of new vocabulary words. Ask students to extrapolate

the meaning of indicated: The road sign indicated that the city of Chicago was 50 miles away.

Chapter 14 383

383_404_C14_SEC_895867.indd 383 11/24/10 5:33 PM

TE RTEACHER

TEACHERTEACHER

TOTO Researching Jobs in Accounting Ask students to look in newspapers every day for a week and fi nd jobs available for accounting clerks, bookkeepers, payroll clerks, CPAs, and accountants. The students cut out classifi ed ads and highlight job requirements and the starting salaries. They make a collage of the ads and compare salaries with those for other available jobs.

Chris MendezBel Air High School, El Paso, Texas

AACCHH

ASSETS

101 Cash in Bank 130 Supplies105 Change Fund 135 Prepaid Insurance110 Petty Cash Fund 140 Delivery Equipment115 Accounts Receivable 142 Accumulated Depreciation—Delivery Equipment117 Allowance for Uncollectible Accounts 145 Office Equipment118 Notes Receivable 147 Accumulated Depreciation—Office Equipment120 Interest Receivable 150 Store Equipment125 Merchandise Inventory 152 Accumulated Depreciation—Store Equipment

LIABILITIES

201 Accounts Payable 212 Social Security Tax Payable202 Notes Payable 213 Medicare Tax Payable203 Discount on Notes Payable 214 Federal Unemployment Tax Payable204 Federal Corporate Income Tax Payable 215 State Unemployment Tax Payable205 Employees’ Federal Income Tax Payable 220 Sales Tax Payable211 Employees’ State Income Tax Payable

STOCKHOLDERS’ EQUITY

301 Capital Stock 310 Income Summary305 Retained Earnings REVENUE

401 Sales 410 Sales Returns and Allowances405 Sales Discounts 415 Interest Income

COST OF MERCHANDISE

501 Purchases 510 Purchases Discounts505 Transportation In 515 Purchases Returns and Allowances

EXPENSES

601 Advertising Expense 645 Loss/Gain on Disposal of Plant Assets605 Bankcard Fees Expense 650 Maintenance Expense610 Cash Short and Over 655 Miscellaneous Expense612 Delivery Expense 657 Payroll Tax Expense615 Depreciation Expense—Delivery Equipment 660 Rent Expense620 Depreciation Expense—Office Equipment 665 Salaries Expense625 Depreciation Expense—Store Equipment 670 Supplies Expense630 Federal Corporate Income Tax Expense 675 Uncollectible Accounts Expense635 Insurance Expense 680 Utilities Expense640 Interest Expense

CHART OF ACCOUNTS

....

....

....

....

....

....

....

....

....

CHA Champion Store SupplyCOM Computer SolutionsDAR Dara’s Delivery ServiceFAS FastLane AthleticsGEA Geary Office SupplyPRO Pro Runner WarehouseSLF Sports Link FootwearSNS Sports Nutrition Supply

Accounts Receivable Subsidiary Ledger Accounts Payable Subsidiary Ledger▼ ▼

BRE Break Point Sports ClubDIM Dimaio, JoeGAL Galvin, RobertKLE Klein, CaseyMON Montero, AnitaRAH Rahim, ShashiRAM Ramos, GabrielSOU South Branch High School Athletics SUL Sullivan, MeganTAM Tammy’s Fitness ClubWON Wong, KimYOU Young, Lara

384 Chapter 14 Accounting for Sales and Cash Receipts

383-404_C14_SEC_893567.indd 384 8/31/10 5:24 PM

R

C2

C1

SECTION 14.1

TEACHEnglish Language LearnersUnderstanding the vocabulary is critical to success in this course. Students whose primary language is not English might need extra support in order to keep up with the new vocabulary. Always demonstrate new processes and procedures. Provide visuals whenever possible. Keep these posted so that students can access them when necessary.

R Reading StrategyReading Accounting Forms Point out to students that The Starting Line’s general ledger accounts are organized by classifi cation and account number. Ask: What is different about the classifi cation of a corporate merchandising business chart of accounts? It includes two new categories: Stockholders’ Equity and Cost of Merchandise. OL

C1 Critical ThinkingComparing Ask: What is the difference between owner’s equity and stockholders’ equity? Owner’s equity represents the fi nancial claims of one individual in a sole proprietorship. Stockholders’ equity represents fi nancial claims of all corporate stockholders. AL

C2 Critical ThinkingMaking Inferences Ask: What are the two sources of revenue for The Starting Line? sales and interest income Ask: What do you think Account 405 is used for? to record the amount of discounts the company gives OL

384 Chapter 14

383_404_C14_SEC_895867.indd 384 11/24/10 5:34 PM

Accounts Used by a Merchandising BusinessWhat Accounts Does a Merchandising Business Use?

A merchandising business buys goods from a wholesaler or a manufacturing business and then sells these goods to its customers. Goods bought for resale are called merchandise. The items of merchandise the business has in stock are referred to as inventory.

Merchandise Inventory AccountThe inventory of a business is represented in the general ledger by the

asset account Merchandise Inventory. Increases to Merchandise Inventory are recorded as debits, and decreases are recorded as credits. The normal bal-ance of the Merchandise Inventory account is a debit. At the beginning of each period, the dollar amount of merchandise in stock is indicated by the debit balance in Merchandise Inventory.

During the operating cycle, the business sells merchandise that is in stock and purchases new items to replace the inventory sold. The sale of merchandise and the purchase of new merchandise are recorded in separate accounts.

Sales AccountWhen a retail merchandising business sells goods to a customer,

the amount of the merchandise sold is recorded in the Sales account. Sales is a revenue account. Increases to the Sales account are recorded as credits, and decreases are recorded as debits. The normal balance of the Sales account is a credit. Both cash sales and sales on account are recorded as credits to the Sales account.

Sales on account affect the Accounts Receivable account, and cash sales affect the Cash in Bank account.

Reading Check Define In your own words, define the content vocabulary terms retailer, wholesaler, merchandise, and inventory.

International Sales What Challenges Face a Company That Has International Sales?

When companies have sales transactions on an international level, many complexities arise. The obligations and rights of each party to the sale extend across borders and into different sets of legal requirements.

The United Nations Convention on Contracts for the International Sales of Goods (CISG) was created to provide guidelines and laws governing the international sale of goods. While “The Convention” does not cover sales of all goods, it governs most business-to-business transactions.

International sales also introduce the challenge of multiple currencies. Which currency will be used for the transaction? How will currency exchange rates affect revenue? These are just a few considerations that must be examined when conducting international sales.

Merchandise Inventory

Credit�

Decrease Side

Debit�

Increase SideNormal Balance

Sales

Credit�

Increase SideNormal Balance

Debit�

Decrease Side

Section 14.1 Accounting for a Merchandising Business 385

383-404_C14_SEC_893567.indd 385 8/31/10 5:24 PM

C

R1

R2

PROFESSIONALDEVELOPMENT

Reading: Strategic Readers Author Scott Paris discusses the characteristics of strategic readers.

SECTION 14.1

TEACHR1 Reading StrategyReading Accounting Forms Refer students to the Merchandise Inventory T account. Ask: What is its classifi cation? asset Ask: What is its balance and increase side, and its decrease side? Balance and increase side is debit; decrease side is credit. OL

R2 Reading StrategyReading Accounting Forms Refer students to the Sales T account. Ask: What is its classifi cation? revenue Ask: What is its balance and increase side, and its decrease side? Balance and increase side is credit; decrease side is debit. OL

C Critical ThinkingComparing Ask: What does the balance of the Merchandise Inventory account show? the amount of merchandise in stock available for sale at the beginning of the period Ask: What does the balance of the Sales account show? the amount of merchandise that has been sold OL

Reading CheckAccept all reasonable answers. Definitions: retailer—a business that sells to the final user, the consumer; wholesaler—business that sells to retailers; merchandise—goods bought for resale; inventory—items of merchandise the business has in stock to sell

Chapter 14 385

383_404_C14_SEC_895867.indd 385 11/24/10 5:36 PM

SECTION 14.1

ASSESSSECTION 14.1 ASSESSMENT RESOURCES Use these resources to assess mastery of section content.• Chapter Study Guides and Working

Papers (Problem 14-1)• Presentation Plus!

glencoe.com

Online Learning Center: Click on Student Center. Click on Self-Assessment Quizzes and select Chapter 14.

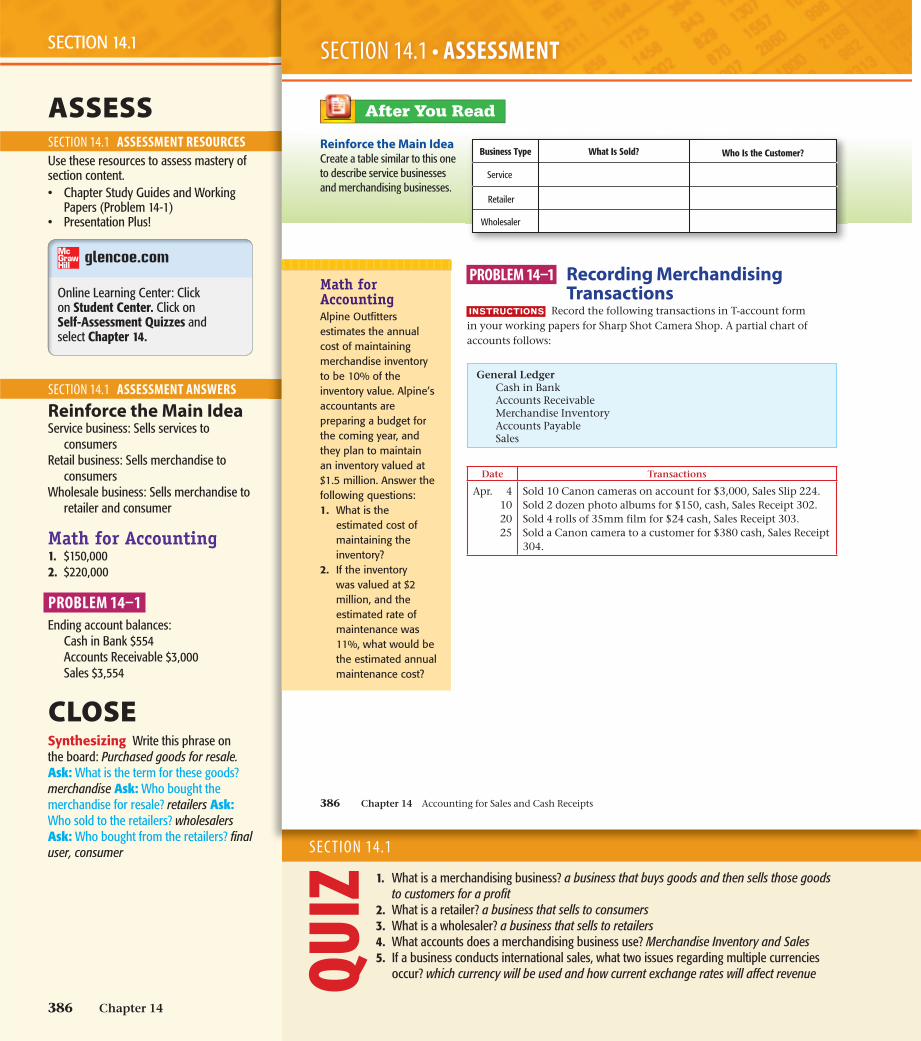

SECTION 14.1 ASSESSMENT ANSWERS

Reinforce the Main IdeaService business: Sells services to

consumersRetail business: Sells merchandise to

consumersWholesale business: Sells merchandise to

retailer and consumer

Math for Accounting1. $150,0002. $220,000

PROBLEM 14–1Ending account balances:

Cash in Bank $554Accounts Receivable $3,000Sales $3,554

CLOSESynthesizing Write this phrase on the board: Purchased goods for resale. Ask: What is the term for these goods? merchandise Ask: Who bought the merchandise for resale? retailers Ask: Who sold to the retailers? wholesalers Ask: Who bought from the retailers? fi nal user, consumer

Business Type What Is Sold? Who Is the Customer?

Service

Retailer

Wholesaler

After You Read

PROBLEM 14–1 Recording Merchandising Transactions

INSTRUCTIONS Record the following transactions in T-account form in your working papers for Sharp Shot Camera Shop. A partial chart of accounts follows:

General Ledger Cash in Bank Accounts Receivable Merchandise Inventory Accounts Payable Sales

Date Transactions

Apr. 4102025

Sold 10 Canon cameras on account for $3,000, Sales Slip 224.Sold 2 dozen photo albums for $150, cash, Sales Receipt 302.Sold 4 rolls of 35mm film for $24 cash, Sales Receipt 303.Sold a Canon camera to a customer for $380 cash, Sales Receipt 304.

Math for AccountingAlpine Outfitters estimates the annual cost of maintaining merchandise inventory to be 10% of the inventory value. Alpine’s accountants are preparing a budget for the coming year, and they plan to maintain an inventory valued at $1.5 million. Answer the following questions:1. What is the

estimated cost of maintaining the inventory?

2. If the inventory was valued at $2 million, and the estimated rate of maintenance was 11%, what would be the estimated annual maintenance cost?

Reinforce the Main IdeaCreate a table similar to this one to describe service businesses and merchandising businesses.

SECTION 14.1 • ASSESSMENT

386 Chapter 14 Accounting for Sales and Cash Receipts

383-404_C14_SEC_893567.indd 386 9/10/10 12:34 PM

SEC TION 14.1

QUIZ 1. What is a merchandising business? a business that buys goods and then sells those goods

to customers for a profi t 2. What is a retailer? a business that sells to consumers3. What is a wholesaler? a business that sells to retailers4. What accounts does a merchandising business use? Merchandise Inventory and Sales5. If a business conducts international sales, what two issues regarding multiple currencies

occur? which currency will be used and how current exchange rates will affect revenue

386 Chapter 14

383_404_C14_SEC_895867.indd 386 11/29/10 11:59 AM

PRETEACHING SECTION VOCABULARY

SECTION VOCABULARY

Content Vocabulary• sale on account

• charge customer

• credit cards

• sales slip

• sales tax

• credit terms

• accounts receivable subsidiary ledger

• subsidiary ledger

• controlling account

• sales return

• sales allowance

• credit memorandum

• contra account

Academic Vocabulary• proportion

• detect

In a merchandising business, the most frequent transaction is the sale of merchandise. Some businesses sell on a cash-only basis. Others sell only on credit. Most businesses handle both cash and credit sales.

Sales on AccountWhat Does a Sale on Account Involve?

The sale of merchandise that will be paid for at a later date is called asale on account, a charge sale, or a credit sale. The sale on account is made to a charge customer; this credit option is also called a charge account.

Store Credit Card SalesCharge customers use credit cards issued by a business such as Target

to make their purchases. A store credit card, imprinted with the customer’s name and account number, facilitates the sale on account.

Nonbank Credit Card SalesIn the next section, you will learn about bank credit cards. We consider

nonbank credit cards here because they are similar to a store credit card. A nonbank credit card is a credit card issued by corporations such as American Express and Discover. Nonbank credit card sales are considered a form of credit sales because payment is collected at a later date.

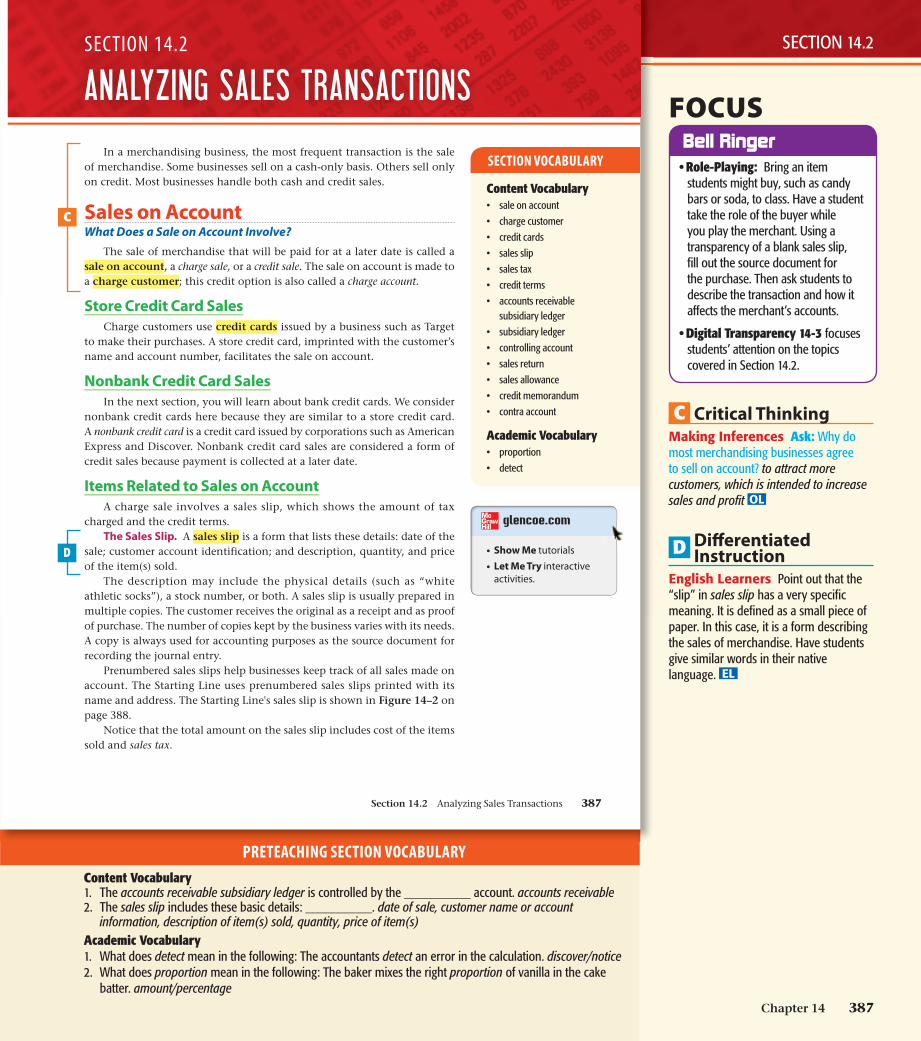

Items Related to Sales on AccountA charge sale involves a sales slip, which shows the amount of tax

charged and the credit terms.The Sales Slip. A sales slip is a form that lists these details: date of the

sale; customer account identification; and description, quantity, and price of the item(s) sold.

The description may include the physical details (such as “white athletic socks”), a stock number, or both. A sales slip is usually prepared in multiple copies. The customer receives the original as a receipt and as proof of purchase. The number of copies kept by the business varies with its needs. A copy is always used for accounting purposes as the source document for recording the journal entry.

Prenumbered sales slips help businesses keep track of all sales made on account. The Starting Line uses prenumbered sales slips printed with its name and address. The Starting Line's sales slip is shown in Figure 14–2 on page 388.

Notice that the total amount on the sales slip includes cost of the items sold and sales tax.

ANALYZING SALES TRANSACTIONS SECTION 14.2

glencoe.com

• Show Me tutorials • Let Me Try interactive

activities.

Section 14.2 Analyzing Sales Transactions 387

383-404_C14_SEC_893567.indd 387 8/31/10 5:25 PM

C

FOCUSBell Ringer • Role-Playing: Bring an item

students might buy, such as candy bars or soda, to class. Have a student take the role of the buyer while you play the merchant. Using a transparency of a blank sales slip, fi ll out the source document for the purchase. Then ask students to describe the transaction and how it affects the merchant’s accounts.

• Digital Transparency 14-3 focuses students’ attention on the topics covered in Section 14.2.

Bell Ringer

C Critical ThinkingMaking Inferences Ask: Why do most merchandising businesses agree to sell on account? to attract more customers, which is intended to increase sales and profi t OL

D Diff erentiated Instruction

English Learners Point out that the “slip” in sales slip has a very specifi c meaning. It is defi ned as a small piece of paper. In this case, it is a form describing the sales of merchandise. Have students give similar words in their native language. EL

SECTION 14.2

Content Vocabulary1. The accounts receivable subsidiary ledger is controlled by the __________ account. accounts receivable2. The sales slip includes these basic details: __________. date of sale, customer name or account

information, description of item(s) sold, quantity, price of item(s)Academic Vocabulary1. What does detect mean in the following: The accountants detect an error in the calculation. discover/notice2. What does proportion mean in the following: The baker mixes the right proportion of vanilla in the cake

batter. amount/percentage

D

Chapter 14 387

383_404_C14_SEC_895867.indd 387 11/24/10 7:41 PM

Sales Tax. Most states and some cities tax the retail sale of goods and services with a sales tax. Items subject to sales tax and sales tax rates vary from state to state. The sales tax rate is usually stated as a percentage of the sale, such as 5%. Sales tax rates are determined by the proper taxing authority.

The sales tax is paid by the customer and collected by the business. The business acts as the collection agent for the state or city government. (In the future we will refer only to the state government.) At the time of the sale, the business adds the sales tax to the total selling price of the goods. Periodically, the business sends the collected sales tax to the state. Until the state is paid, however, the sales tax collected from customers represents a liability of the business. The business keeps a record of the sales tax owed to the state in a liability account called Sales Tax Payable. For Sales Tax Payable, the increase and balance side is a credit and the decrease side is a debit.

To calculate the sales tax, multiply the merchandise subtotal by the sales tax rate (see Figure 14–2). Casey Klein bought $200 worth of merchandise. The sales tax rate is 6%. The sales clerk multiplied $200 by 6% (.06) to compute the $12 sales tax. The total transaction amount is $212.

Not all sales of retail merchandise are taxed. In most states, sales to tax-exempt organizations, such as schools, are not taxed. For example, South Branch High School purchased $1,500 worth of merchandise on account. Schools are tax exempt, so no sales tax is added to the amount of the sale.

Credit Terms. The sales slip in Figure 14–2 has space to indicate the credit terms of the sale. Credit terms state the time allowed for payment. The credit terms for the sale to Casey Klein are n/30. The “n” stands for

the net, or total, amount of the sale. The “30” stands for the number of days the customer has to pay for the merchandise. Casey Klein owes The Starting Line $212 (the net amount) by December 31 (30 days after December 1).

The Accounts Receivable Subsidiary LedgerWhat Is a Subsidiary Ledger?

Businesses with few charge customers usually include an Accounts Receivable account for each customer in the general ledger. A large business, however, with many charge customers sets up a separate ledger that contains an account for each charge customer. This ledger is called theaccounts receivable subsidiary ledger. A subsidiary ledger is a ledger, or book, that contains detailed data summarized to a controlling account in the general ledger. For example, the accounts receivable subsidiary ledger contains details of all the individuals and businesses that owe money to a company. Summary information about accounts receivable appears in the Accounts Receivable account in the general ledger. Accounts Receivable is acontrolling account because its balance equals the total of all account balances in the subsidiary ledger. The balance of Accounts Receivable thus serves as a control on the accuracy of the balances in the accounts receivable subsidiary ledger after all posting is complete.

DATE: NO.

SOLDTO

UNITPRICEDESCRIPTION

CASHCLERK CHARGE TERMS

QTY. AMOUNT

SUBTOTAL

SALES TAX

TOTALThank You!

Casey Klein3345 Spring Creek ParkwayPlano, Texas 75074

50December 1, 20--

n/30✓ B.E.

1

6

1

Pair Running Shoes

Pair Athletic Socks

Vinyl Jacket/Pants

$ 100.00

10.00

40.00

00$ 100

60 00

40 00

$ 200 00

12 00

$ 212 00

Figure 14–2 The Starting Line Sports Gear Sales Slip

Sales Tax Payable

Credit�

Increase SideNormal Balance

Debit�

Decrease Side

388 Chapter 14 Accounting for Sales and Cash Receipts

383-404_C14_SEC_893567.indd 388 9/10/10 12:35 PM

TEACHC1 Critical ThinkingConnecting to Financial Literacy Tell students that most cities and states impose a sales tax on consumer goods and services. Ask: What is the rate (percentage) of sales tax you are charged when you purchase clothes, CDs, or other items? Answers will vary from city to city, state to state. AL

C2 Critical ThinkingSeparating Parts Refer students to Figure 14-2 (Digital Transparency 14-4). Ask: Why is it necessary to separate the sales tax amount from the amount of merchandise sold? These are two separate elements affecting two different accounts. The business must send the sales taxes collected to the appropriate government agency. OL

R Reading StrategyReading Accounting Forms Ask: In Figure 14-2, how much merchandise was sold? $200 Ask: How much was the sales tax? $12 Ask: What was the total sale amount? $212 BL

SECTION 14.2C1

C2

R

PROFESSIONALDEVELOPMENT

ELL: Graphic Organizers Students use graphic organizers to distinguish between major and minor details.

388 Chapter 14

383_404_C14_SEC_895867.indd 388 11/24/10 5:37 PM

General LedgerAccounts Receivable—controlling account $10,000

Accounts Receivable Subsidiary LedgerIndividual Accounts Within Ledger:

Brown, Joshua $2,000Clark, Gillian 3,000Greene, Jason 1,000Perez, Sarita 4,000

Total $10,000

Controlling account balance equals total of accounts in subsidiary ledger.

Figure 14–3 shows the accounts receivable subsidiary ledger form used by The Starting Line. The subsidiary ledger account form has lines at the top for the name and address of the customer. In a manual accounting system, subsidiary ledger accounts are arranged in alphabetical order. They are not usually numbered. In a computerized system, however, each charge customer is assigned a specific account number.

Notice that the subsidiary ledger account form has only three amount columns. The Debit and Credit columns are used to record increases and decreases to the customer’s account. There is only one Balance column. Since Accounts Receivable is an asset account, the normal balance is a debit, so one balance amount is sufficient.

ADDRESS

NAME

CREDITDEBIT BALANCEDESCRIPTIONDATEPOST.REF.

Figure 14–3 Subsidiary Ledger Account Form

Reading Check Explain Why is Accounts Receivable a controlling account?

Recording Sales on AccountHow Are Sales on Account Recorded?

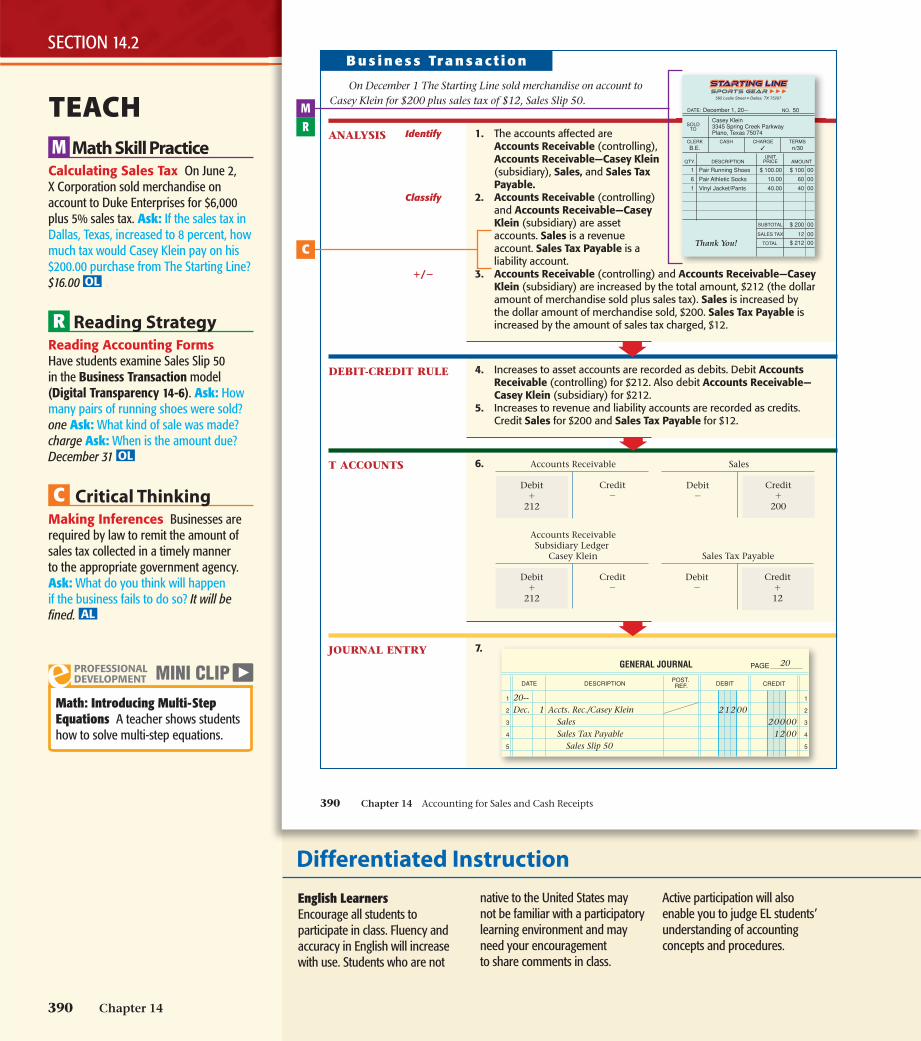

According to the revenue recognition principle, revenue for a sale on account is recognized and recorded at the time of the sale, when it is earned. Revenue must also be realizable, which means that it is expected to be converted to cash. Look at The Starting Line’s sale on account to Casey Klein in the next business transaction.

Notice that the debit in the general journal entry is to “Accounts Receivable/Casey Klein.” The slash indicates that two accounts are debited: Accounts Receivable (controlling) and Accounts Receivable—Casey Klein (subsidiary).

As mentioned earlier, when merchandise is sold to tax-exempt organizations, such as school districts, sales tax is not charged. An example of such a transaction and sales receipt follows on page 391.

Section 14.2 Analyzing Sales Transactions 389

383-404_C14_SEC_893567.indd 389 9/10/10 12:35 PM

SECTION 14.2

TEACHC1 Critical ThinkingComparing Have students compare the total of the Accounts Receivable (controlling) account in the general ledger shown with that in the accounts receivable subsidiary ledger. Ask: Do they agree? yes Ask: What does that prove? The total of the subsidiary ledger is the same as that of the Accounts Receivable (controlling) account. BL

W Writing SupportWriting Clearly Have students assume that the controlling and subsidiary ledger account totals were not in agreement. Ask: Write a memo to your manager identifying a possible cause of the difference. The cause is usually a computational or posting error in the subsidiary ledger or accounts receivable account. AL

C2 Critical ThinkingDifferentiating Refer students to Figure 14-3 (Digital Transparency 14-5). Ask: Why does a subsidiary ledger account form have only three amount columns, instead of the four columns in a general ledger account form? The customer’s account balance is always assumed to be a debit. AL

Reading CheckAccounts Receivable is a controlling account because its balance equals the total of all account balances in the subsidiary ledger.

Determining Sales Tax and Total Sales Use Demonstration Problem 14-2 in Chapter 14 Fast File for step-by-step practice determining sales tax and total sales. The problem also appears on the TeacherWorks Plus.

EXTENDED SKILL PRACTICE

C1

W

C2

Chapter 14 389

383_404_C14_SEC_895867.indd 389 11/24/10 5:37 PM

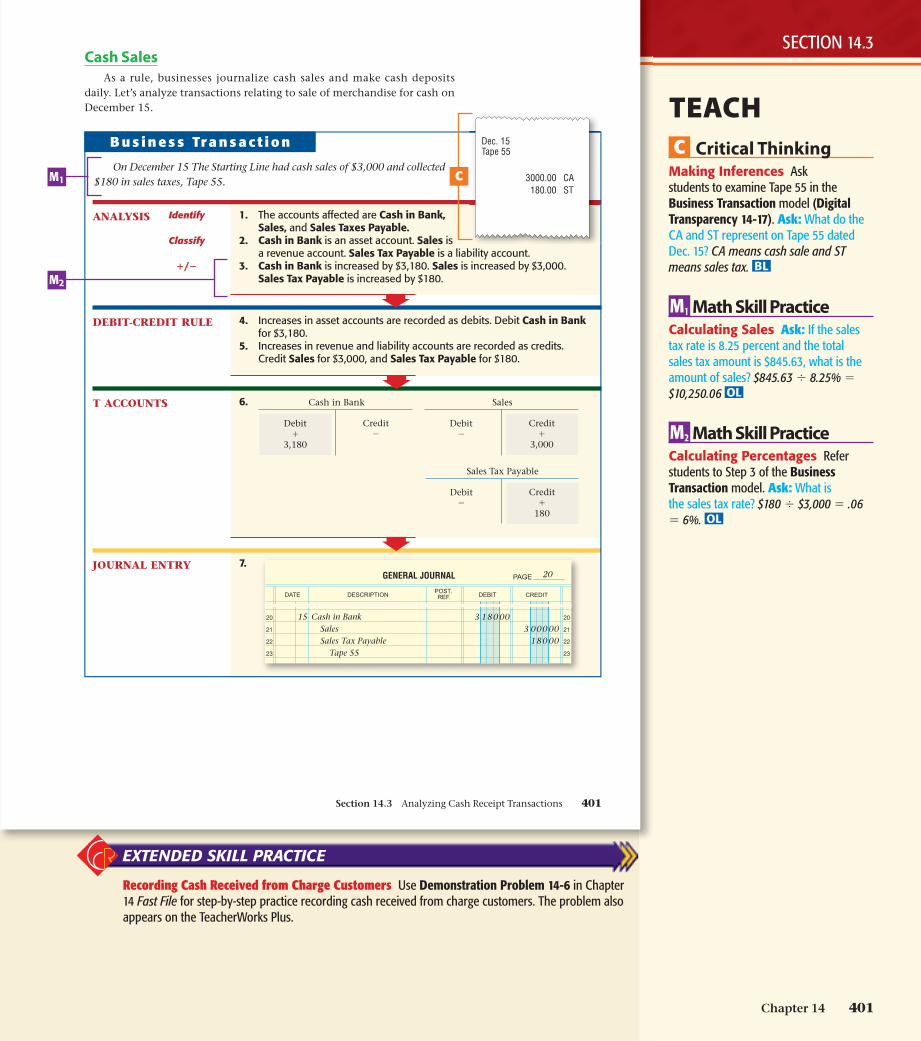

1. The accounts affected are Accounts Receivable (controlling), Accounts Receivable—Casey Klein (subsidiary), Sales, and Sales Tax Payable.

2. Accounts Receivable (controlling) and Accounts Receivable—Casey Klein (subsidiary) are asset accounts. Sales is a revenue account. Sales Tax Payable is a liability account.

3. Accounts Receivable (controlling) and Accounts Receivable—Casey Klein (subsidiary) are increased by the total amount, $212 (the dollar amount of merchandise sold plus sales tax). Sales is increased by the dollar amount of merchandise sold, $200. Sales Tax Payable is increased by the amount of sales tax charged, $12.

7.JOURNAL ENTRY

On December 1 The Starting Line sold merchandise on account to Casey Klein for $200 plus sales tax of $12, Sales Slip 50.

6.T ACCOUNTS

4. Increases to asset accounts are recorded as debits. Debit Accounts Receivable (controlling) for $212. Also debit Accounts Receivable—Casey Klein (subsidiary) for $212.

5. Increases to revenue and liability accounts are recorded as credits. Credit Sales for $200 and Sales Tax Payable for $12.

ANALYSIS Identify

Classify

�/�

DEBIT-CREDIT RULE

B u s i n e s s Tr a n s a c t i o n

Sales

Credit�

200

Debit�

Accounts ReceivableSubsidiary Ledger

Casey Klein

Credit�

Debit�

212

Sales Tax Payable

Credit�12

Debit�

Accounts Receivable

Credit�

Debit�

212

GENERAL JOURNAL PAGE

1

2

3

4

5

1

2

3

4

5

DEBIT CREDITDESCRIPTIONDATEPOST.REF.

20

20--Dec. Accts. Rec./Casey Klein

SalesSales Tax Payable

Sales Slip 50

1 212 00200 00

12 00

DATE: NO.

SOLDTO

UNITPRICEDESCRIPTION

CASHCLERK CHARGE TERMS

QTY. AMOUNT

SUBTOTAL

SALES TAX

TOTALThank You!

Casey Klein3345 Spring Creek ParkwayPlano, Texas 75074

50December 1, 20--

n/30✓ B.E.

1

6

1

Pair Running Shoes

Pair Athletic Socks

Vinyl Jacket/Pants

$ 100.00

10.00

40.00

00$ 100

60 00

40 00

$ 200 00

12 00

$ 212 00

390 Chapter 14 Accounting for Sales and Cash Receipts

383-404_C14_SEC_893567.indd 390 9/10/10 12:35 PM

TEACHM Math Skill PracticeCalculating Sales Tax On June 2, X Corporation sold merchandise on account to Duke Enterprises for $6,000 plus 5% sales tax. Ask: If the sales tax in Dallas, Texas, increased to 8 percent, how much tax would Casey Klein pay on his $200.00 purchase from The Starting Line? $16.00 OL

R Reading StrategyReading Accounting Forms Have students examine Sales Slip 50 in the Business Transaction model (Digital Transparency 14-6). Ask: How many pairs of running shoes were sold? one Ask: What kind of sale was made? charge Ask: When is the amount due? December 31 OL

C Critical ThinkingMaking Inferences Businesses are required by law to remit the amount of sales tax collected in a timely manner to the appropriate government agency. Ask: What do you think will happen if the business fails to do so? It will be fi ned. AL

SECTION 14.2

English Learners Encourage all students to participate in class. Fluency and accuracy in English will increase with use. Students who are not

native to the United States may not be familiar with a participatory learning environment and may need your encouragement to share comments in class.

Active participation will also enable you to judge EL students’ understanding of accounting concepts and procedures.

Differentiated Instruction

MR

C

PROFESSIONALDEVELOPMENT

Math: Introducing Multi-Step Equations A teacher shows students how to solve multi-step equations.

390 Chapter 14

383_404_C14_SEC_895867.indd 390 11/24/10 5:38 PM

JOURNAL ENTRY

On December 3 The Starting Line sold merchandise on account to South Branch High School Athletics for $1,500, Sales Slip 51.

B u s i n e s s Tr a n s a c t i o n

J

GENERAL JOURNAL PAGE

6

7

8

9

6

7

8

9

DEBIT CREDITDESCRIPTIONDATEPOST.REF.

20

Accts. Rec./So. Branch H.S.Sales

Sales Slip 51

3 1 500 001 500 00

DATE: NO.

SOLDTO

UNITPRICEDESCRIPTION

CASHCLERK CHARGE TERMS

QTY. AMOUNT

SUBTOTAL

SALES TAX

TOTALThank You!

South Branch High School Athletics1750 Rutgers Dr.Dallas, TX 75207

51December 3, 20--

2/10, n/30✓ B.E.

15

15

15

2

3

Baseball Uniforms

Baseball Caps

Baseball Mitts

Baseballs

Baseball Bats

$ 40.00

20.00

35.00

15.00

15.00

00$ 600

300 00

525 00

30 00

45 00

$ 1,500 00

0 00

$ 1,500 00

This transaction is analyzed and recorded in the same manner as the December 1 entry for Casey Klein except there is no sales tax. The Starting Line’s accountant debits Accounts Receivable/South Branch High SchoolAthletics for $1,500 and credits the Sales account for $1,500.

Sales Returns and AllowancesAll merchandising businesses expect that some customers will be

dissatisfied with their purchases. The reasons for dissatisfaction vary. An item may be damaged or defective. The color or size may be incorrect. Whatever the reason, merchants usually allow dissatisfied customers to return merchandise. Any merchandise returned for credit or a cash refund is called a sales return.

Sometimes a customer discovers that merchandise is damaged or defective but still usable. When this happens, the merchant may reduce the sales price for the damaged merchandise. A price reduction granted for damaged goods kept by the customer is called a sales allowance.

The Credit Memorandum. If the sales return or allowance occurs on a charge sale, the business usually prepares a credit memorandum. A credit memorandum lists the details of a sales return or allowance. The charge customer’s account is credited (decreased) for the amount of the return or allowance.

Figure 14–4 on page 392 shows a credit memorandum, or credit memo, used by The Starting Line. The credit memo was prepared when Gabriel Ramos returned merchandise that he bought on account on November 29. Note that the credit memo includes a description of the returned item, the reasons for the return, and the amount to be credited to Gabriel Ramos’ account.

The Starting Line's credit memo also includes spaces for the date and sales slip number of the original sale. Notice too that the total on the credit memo includes the sales tax charged on the original sale.

The same form is used if Gabriel Ramos is instead given a sales allowance. Of course, the amount credited to his account would be less. The credit granted for an allowance is the difference between the original sales price and the reduced price.

Section 14.2 Analyzing Sales Transactions 391

383-404_C14_SEC_893567.indd 391 9/10/10 12:36 PM

SECTION 14.2

TEACHR1 Reading StrategyReading Source Documents Refer students to Sales Slip 51 in the Business Transaction model (Digital Transparency 14-7). Ask: Explain the sales terms. 2% discount if paid within 10 days, net amount due in 30 days OL

M Math Skill PracticeCalculating Balances Have students review Sales Slip 51 in the Business Transaction model. Ask: What would the total sale amount be if 30 baseball uniforms had been purchased? $1,200 Ask: Why is no sales tax recorded on the sales slip? The high school is tax exempt. OL

R2 Reading StrategyRecalling Procedural Information Have students review the Journal Entry in the Business Transaction model. Ask: What does the diagonal line in the Posting Reference column indicate? The $1,500 amount is posted to the Accounts Receivable (controlling) account in the general ledger and to the Accounts Receivable—South Branch H.S. account in the accounts receivable subsidiary ledger. OL

Recording Sales on Account Use Demonstration Problem 14-3 in Chapter 14 Fast File for step-by-step practice recording sales on account. The problem also appears on the TeacherWorks Plus.

EXTENDED SKILL PRACTICE

R2

R1

M

Chapter 14 391

383_404_C14_SEC_895867.indd 391 11/24/10 5:39 PM

The Starting Line's credit memos are prenumbered and prepared in duplicate. The orig-inal is given to the customer. The copy is the business's source document used for the journal entry to record the transaction.

The Sales Returns and Allowances Account. Sales returns and allowances decrease the total revenue earned by a business. This decrease, how-ever, is not recorded in the Sales

account. Instead, a separate account called Sales Returns and Allowances is used. Sales Returns and Allowances summarizes the total returns and allow ances for damaged, defective, or otherwise unsatisfactory merchan dise. If the Sales Returns and Allowances account balance is large in proportion to the Sales account balance, there may be merchan dising problems. The Sales Returns and Allow ances account is carefully analyzed to detect any trouble.

The Sales Returns and Allowances account is a contra account. As a contra account, its balance decreases the balance of its related account. Sales Returns and Allowances is more specifically classified as a contra revenue account because it is related to a revenue account, Sales. Since the normal balance side of Sales is a credit, the normal balance side of Sales Returns and Allowances is a debit. This relationship is shown here:

Sales

Credit�

Increase SideNormal Balance

Debit�

Decrease Side

Sales Returns and Allowances

Credit�

Decrease Side

Debit�

Increase SideNormal Balance

Cash RefundsSometimes a merchant will give a customer a cash refund instead of a

credit. The Starting Line's store policy is to give a cash refund only if the original sale was a cash sale. For cash refunds the Cash in Bank account is credited instead of Accounts Receivable.

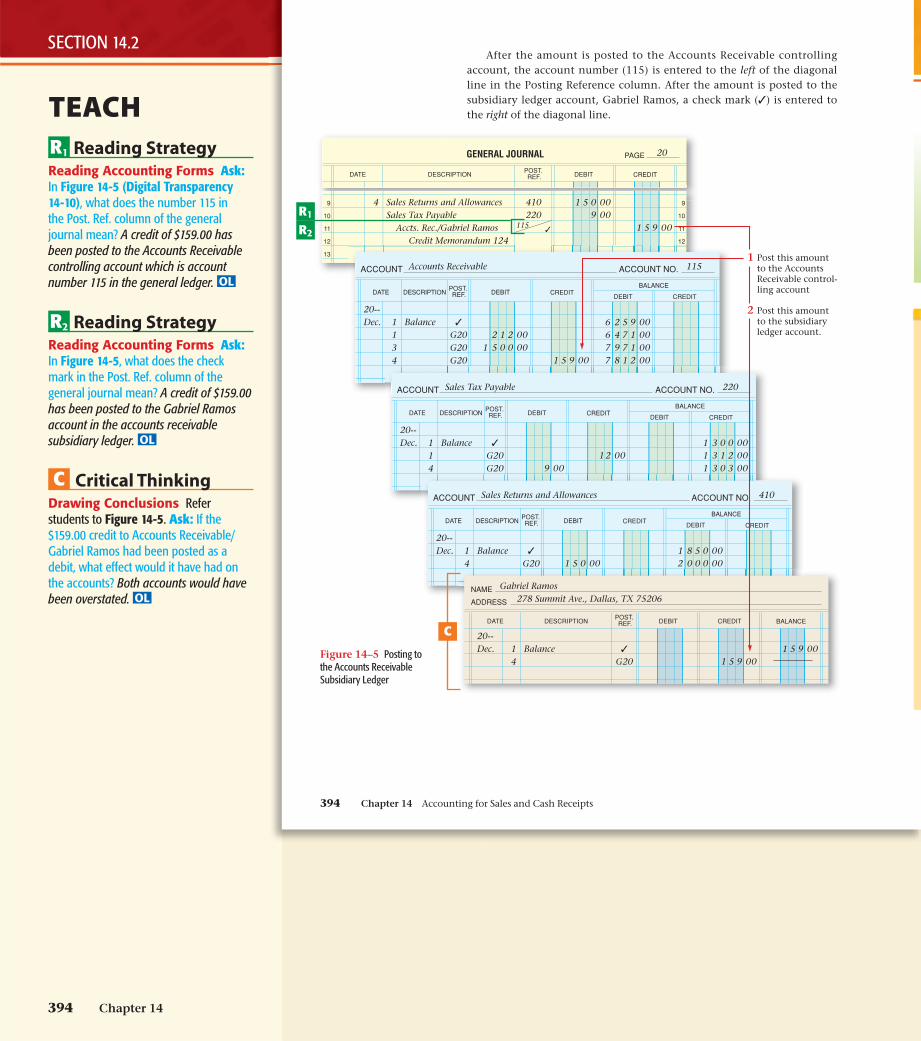

Posting to the Accounts Receivable Subsidiary LedgerHow Do You Post to the Accounts Receivable Subsidiary Ledger?

Refer to Figure 14–5. Look at the general journal entry. The credit is to Accts Rec./Gabriel Ramos. The slash indicates that both Accounts Receiv able (controlling) and Accounts Receivable—Gabriel Ramos (subsidiary) are credited. Notice that a diagonal line is entered in the Post. Ref. column. This diagonal line indicates that the amount, $159, is posted in two places: first to the Account Receivable controlling account in the general ledger and then to the Gabriel Ramos account in the accounts receivable subsidiary ledger.

Contra Accounts Since contra revenue accounts decrease the balance of the sales account, their balance and increase sides will be on the side opposite that of the sales account. To illustrate, draw a T account, label it Sales, and write in the balance, increase, and decrease sides. Draw another T account and label it Sales Returns and Allowances or Sales Discounts. Now write in the balance, increase, and decrease sides. Compare the two.

CommonMistakes

DATE:

NAME:

CUSTOMER SIGNATURE

CREDIT MEMORANDUM NO. 124

ADDRESS:

ORIGINALSALES DATE

ORIGINALSALES SLIP

APPROVAL

SUBTOTAL

SALESTAX

TOTAL

DESCRIPTIONQTY

REASON FOR RETURN

THE TOTAL SHOWN AT THERIGHT WILL BE CREDITEDTO YOUR ACCOUNT.

AMOUNT

MDSERET

Gabriel Ramos278 Summit AvenueDallas, TX 75206

December 4, 20--

Gabriel Ramos

$ 150 00

$ 150 00

9 00

$ 159 00

1 Athletic Suit

wrong color

Nov. 29, 20-- No. 35 J.R. ✕

Figure 14–4 Credit Memorandum

392 Chapter 14 Accounting for Sales and Cash Receipts

383-404_C14_SEC_893567.indd 392 9/10/10 12:36 PM

TEACHC1 Critical ThinkingSynthesizing Refer students to Figure 14-4 (Digital Transparency 14-8). Ask: Will Gabriel Ramos’s account be debited or credited? credited Ask: Will this memo result in an increase or decrease to the account? decrease OL

R Reading StrategyReading Accounting Forms Refer students to Figure 14-4. Ask: How much in merchandise is being returned? $150.00 Ask: For what reason? wrong color Ask: How much credit is being granted? $159.00 OL

C2 Critical ThinkingMaking Inferences Refer students to the Sales Returns and Allowances T account. Ask: What does the balance in the account represent? the amount of credit granted for returned or damaged merchandise Ask: Will credit granted increase or decrease the amount generated by sales? decrease OL

Common Mistakes Understanding the use of these terms in the context of accounting is critical. Discuss and demonstrate with examples until all students have a clear understanding.

SECTION 14.2

Recording Sales Returns and Allowances Use Demonstration Problem 14-4 in Chapter 14 Fast File for step-by-step practice recording sales returns and allowances. The problem also appears on the TeacherWorks Plus.

EXTENDED SKILL PRACTICE

C1

R

C2

392 Chapter 14

383_404_C14_SEC_895867.indd 392 11/24/10 5:41 PM

1. The accounts affected are Accounts Receivable (controlling), Accounts Receivable—Gabriel Ramos (subsidiary), Sales Returns and Allowances, and Sales Tax Payable.

2. Accounts Receivable (controlling) and Accounts Receivable—Gabriel Ramos (subsidiary) are asset accounts. Sales Returns and Allowances is a contra revenue account. Sales Tax Payable is a liability account.

3. Sales Returns and Allowances is increased by $150. Sales Tax Payable is decreased by $9. Accounts Receivable (controlling) and Accounts Receivable—Gabriel Ramos (subsidiary) are decreased by $159.

7.JOURNAL ENTRY

On December 4 The Starting Line issued Credit Memo randum 124 to Gabriel Ramos for the return of merchan dise purchased on account, $150 plus $9 sales tax.

6.T ACCOUNTS

4. Increases to a contra revenue account are recorded as debits. Debit Sales Returns and Allowances for $150. Decreases to liability accounts are recorded as debits. Debit Sales Tax Payable for $9.

5. Decreases to asset accounts are recorded as credits. Credit Accounts Receivable (controlling) for $159. Also credit Accounts Receivable—Gabriel Ramos (subsidiary) for $159.

ANALYSIS Identify

Classify

�/�

DEBIT-CREDIT RULE

B u s i n e s s Tr a n s a c t i o n

Sales Tax Payable

Credit�

Debit�9

Accounts Receivable

Credit�

159

Debit�

Sales Returns and Allowances

Credit�

Debit�

150

Accounts ReceivableSubsidiary Ledger

Gabriel Ramos

Credit�

159

Debit�

GENERAL JOURNAL PAGE

9

10

11

12

13

9

10

11

12

13

DEBIT CREDITDESCRIPTIONDATEPOST.REF.

20

Sales Returns and AllowancesSales Tax Payable

Accts. Rec./Gabriel RamosCredit Memorandum 124

4 150 009 00

159 00

DATE:

NAME:

CUSTOMER SIGNATURE

CREDIT MEMORANDUM NO. 124

ADDRESS:

ORIGINALSALES DATE

ORIGINALSALES SLIP

APPROVAL

SUBTOTAL

SALESTAX

TOTAL

DESCRIPTIONQTY

REASON FOR RETURN

THE TOTAL SHOWN AT THERIGHT WILL BE CREDITEDTO YOUR ACCOUNT.

AMOUNT

MDSERET

Gabriel Ramos278 Summit AvenueDallas, TX 75206

December 4, 20--

Gabriel Ramos

$ 150 00

$ 150 00

9 00

$ 159 00

1 Athletic Suit

wrong color

Nov. 29, 20-- No. 35 J.R. ✕

Section 14.2 Analyzing Sales Transactions 393

383-404_C14_SEC_893567.indd 393 9/10/10 12:36 PM

C1

C2

W

SECTION 14.2

TEACHW Writing SupportWriting Clearly Ask students to assume that their employer does not understand the need for the Sales Returns and Allowances account. Have students write a memo stating why it is needed. It is used to summarize returns and allowances and to identify possible merchandising problems if the amount seems to be high. AL

C1 Critical ThinkingApplying Procedures Refer students to the Business Transaction model (Digital Transparency 14-9). Ask: What is the source document for recording the entry in the transaction? Credit Memorandum 124 Ask: After the entry is recorded, what is done with the source document? It is fi led with other business records. OL

C2 Critical ThinkingMaking Inferences Ask: In the Business Transaction model, why is the contra revenue account debited? Revenue increases with a credit; therefore, when a sales return and allowance is given for merchandise returned, it must be recorded as a debit in the contra account, which reduces revenue. AL

PROFESSIONALDEVELOPMENT

Reading: Vocabulary Author Josefi na Tinajero describes the critical importance of academic language.

Chapter 14 393

383_404_C14_SEC_895867.indd 393 11/24/10 5:41 PM

After the amount is posted to the Accounts Receivable controlling account, the account number (115) is entered to the left of the diagonal line in the Posting Reference column. After the amount is posted to the subsidiary ledger account, Gabriel Ramos, a check mark (✓) is entered to the right of the diagonal line.

DEBIT CREDIT

BALANCEDEBIT CREDITDESCRIPTIONDATE

POST.REF.

ACCOUNT NO.ACCOUNT

20--Dec. Balance1

134

✓

G20G20G20

Accounts Receivable 115

DEBIT CREDIT

BALANCEDEBIT CREDITDESCRIPTIONDATE

POST.REF.

ACCOUNT NO.ACCOUNT

20--Dec. 1 3 0 0 00

1 3 1 2 001 3 0 3 009 00

1 2 00Balance1

14

✓

G20G20

Sales Tax Payable 220

2 1 2 001 5 0 0 00

DEBIT CREDIT

BALANCEDEBIT CREDITDESCRIPTIONDATE

POST.REF.

ACCOUNT NO.ACCOUNT

20--Dec. 1 8 5 0 00

2 0 0 0 001 5 0 00Balance1

4✓

G20

Sales Returns and Allowances 410

ADDRESS

NAME

CREDITDEBIT BALANCEDESCRIPTIONDATEPOST.REF.

20--Dec.

1 5 9 001 5 9 00Balance1

4✓

G20

Gabriel Ramos278 Summit Ave., Dallas, TX 75206

20

1 5 0 009 00

1 5 9 00

Sales Returns and AllowancesSales Tax Payable

Accts. Rec./Gabriel RamosCredit Memorandum 124

4 410220

115✓

GENERAL JOURNAL PAGE

9

10

11

12

13

9

10

11

12

DEBIT CREDITDESCRIPTIONDATEPOST.REF.

6 2 5 9 006 4 7 1 007 9 7 1 007 8 1 2 001 5 9 00

1 Post this amount to the Accounts Receivable control-ling account

2 Post this amount to the subsidiaryledger account.

Figure 14–5 Posting to the Accounts Receivable Subsidiary Ledger

394 Chapter 14 Accounting for Sales and Cash Receipts

383-404_C14_SEC_893567.indd 394 9/10/10 12:37 PM

R1

R2

C

TEACHR1 Reading StrategyReading Accounting Forms Ask: In Figure 14-5 (Digital Transparency 14-10), what does the number 115 in the Post. Ref. column of the general journal mean? A credit of $159.00 has been posted to the Accounts Receivable controlling account which is account number 115 in the general ledger. OL

R2 Reading StrategyReading Accounting Forms Ask: In Figure 14-5, what does the check mark in the Post. Ref. column of the general journal mean? A credit of $159.00 has been posted to the Gabriel Ramos account in the accounts receivable subsidiary ledger. OL

C Critical ThinkingDrawing Conclusions Refer students to Figure 14-5. Ask: If the $159.00 credit to Accounts Receivable/Gabriel Ramos had been posted as a debit, what effect would it have had on the accounts? Both accounts would have been overstated. OL

SECTION 14.2

394 Chapter 14

383_404_C14_SEC_895867.indd 394 11/24/10 5:41 PM

ASSESSSECTION 14.2 ASSESSMENT RESOURCES Use these resources to assess mastery of section content.• Chapter Study Guides and Working

Papers (Problem 14-2)• Presentation Plus!

glencoe.com

Online Learning Center: Click on Student Center. Click on Self-Assessment Quizzes and select Chapter 14.

SECTION 14.2 ASSESSMENT ANSWERS

Reinforce the Main IdeaTop box: sales slipMiddle box: recorded in journalBottom boxes: posted to subsidiary

ledger; posted to general ledger

Math for Accounting1. 5.2%2. 5.2% is favorable compared to the

industry average of 6.5%.

PROBLEM 14–2Sept. 1: Dr. Accts. Rec./James Palmer

$318; Cr. Sales $300 and Sales Tax Pay. $18; Sales Slip 101

Sept. 4: Dr. Accts. Rec./Anna Rodriguez $636; Cr. Sales $600 and Sales Tax Payable $36; Sales Slip 102

Sept. 7: Dr. Sales Ret. and Allow. $300 and Sales Tax Pay. $18; Cr. Accts. Rec./James Palmer $318; Credit Memo 15

Sept. 19: Dr. Sales Ret. and Allow. $40 and Sales Tax Pay. $2.40; Cr. Accts. Rec./Anna Rodriguez $42.40; Credit Memo 16

CLOSESynthesizing Write on the board a sales return and allowance transaction including sales tax. Ask: What accounts are debited and credited? debit: Sales Returns and Allowances and Sales Tax Payable; credit: Accounts Receivable/Customer

Sales Transactions

After You Read

SECTION 14.2 • ASSESSMENT

PROBLEM 14–2 Recording Sales on Account and Sales Returns and Allowances Transactions

INSTRUCTIONS In your working papers, record the following transactions of Alpine Ski Shop on page 2 of the general journal. Use the following accounts:

General Ledger Cash in Bank Sales Tax Payable Accounts Receivable Accounts Payable Merchandise Inventory Sales Sales Returns and Allowances

Accounts Receivable Subsidiary Ledger Palmer, James Rodriguez, Anna

Date Transactions

Sept. 1

4

7

19

Sold $300 in merchandise plus sales tax of $18 on account to James Palmer, Sales Slip 101. Sold $600 in merchandise plus $36 sales tax to Anna Rodriguez on account, Sales Slip 102.Issued Credit Memorandum 15 to James Palmer for the return of $300 in merchandise plus sales tax of $18.Anna Rodriguez telephoned the manager of Alpine Ski Shop and said that the zipper on her ski jacket is broken. The manager agreed to give her a $40 credit on her purchase, plus a $2.40 sales tax credit, Credit Memorandum 16.

Math for AccountingAssume the lighting fixture industry has $.065 in sales returns and allowances for every $1.00 in sales (in other words, an industry average of 6.5%). Last year Light House Gallery had sales of $900,000 and returns and allowances of $46,800. Answer the following questions:1. What was Light

House Gallery’s percentage of returns and allowances to sales?

2. Is the percentage favorable or unfavorable compared to the industry average?

Reinforce the Main Idea Create a flowchart like this one. Enter labels in the boxes and next to the arrows. Use these terms to create the labels: general ledger, journal, posted to, recorded in, sales slip, subsidiary ledger. Terms can be used more than once.

Section 14.2 Analyzing Sales Transactions 395

383-404_C14_SEC_893567.indd 395 9/10/10 12:37 PM

QUIZ 1. What is a sale on account? sale of merchandise paid for at a later date

2. Calculate the sales tax on sales of $1,214, at a sales tax rate 6.25%. $75.883. Explain sales terms “n/30.” Net amount is due in 30 days.4. What is an accounts receivable subsidiary ledger? an alphabetical listing of all charge

customer accounts5. What is the Sales Returns and Allowances account, and how is it used? It is a contra revenue

account used for recording credit granted for returned and/or damaged merchandise.

SEC TION 14.2

SECTION 14.2

Chapter 14 395

383_404_C14_SEC_895867.indd 395 11/24/10 7:46 PM

PRETEACHING SECTION VOCABULARY

SECTION VOCABULARY

Content Vocabulary• cash receipt

• cash sale

• cash discount

• sales discount

Each business must account for the cash it receives. In this section you will explore cash sales, charge sales, bank card sales, and cash discounts.

Cash TransactionsHow Does Cash Come into a Business?

A transaction in which money is received by a business is called a cash receipt. The three most common sources of cash for a merchandising business are payments for cash sales, charge sales, and bankcard sales. Cash is also received, though much less frequently, from other types of transac-tions. Let’s learn how to handle these four kinds of cash receipts.

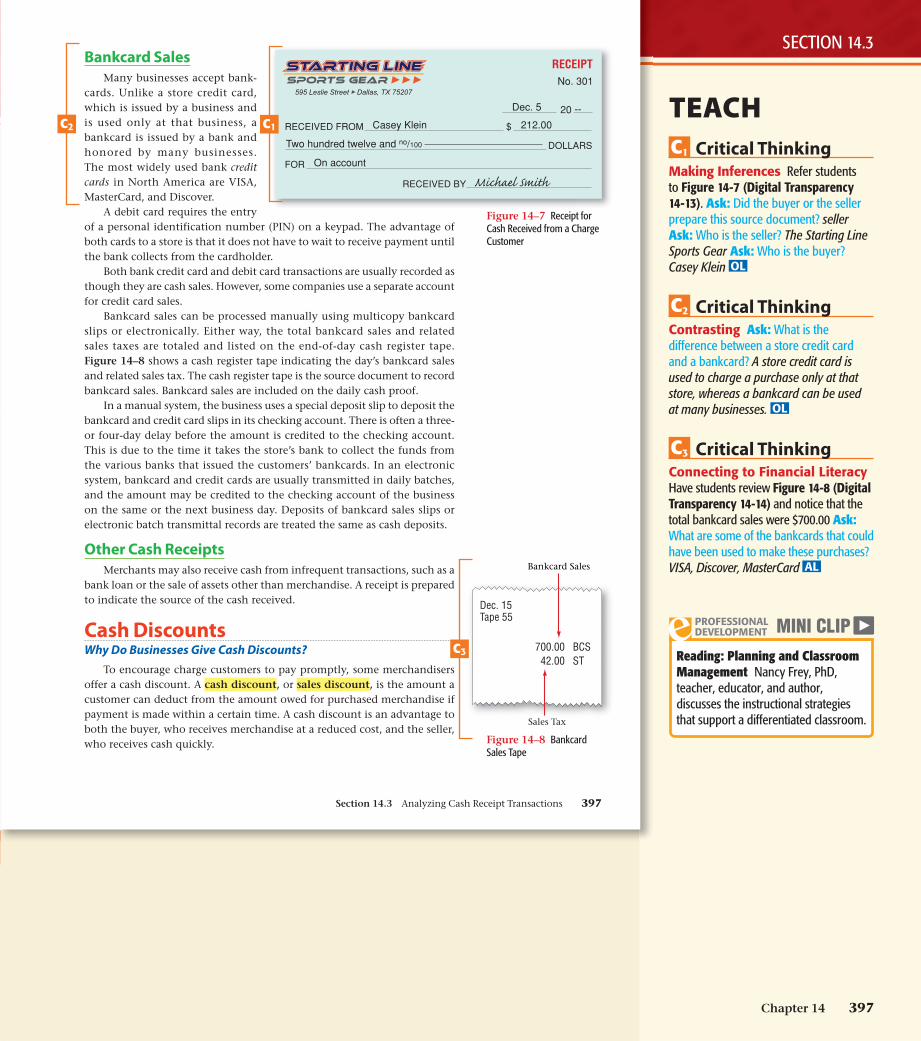

Cash SalesIn a cash sale transaction, the business receives full payment for the

merchandise sold at the time of the sale. The proof of sale and the source document generated by a cash sale transaction differ from those for a sale on account.

Most retailers use a cash register to record cash sales. Instead of using preprinted sales slips, cash sales are recorded on two rolls of paper tape inside the cash register. The details of a cash sale are printed on the two tapes at the same time. The portion of one tape that contains a record of the sale is torn off and given to the customer as a receipt. The other tape remains in the register.

A business totals and clears its cash register daily. The cash register tape lists the total cash sales and the total sales tax collected on these sales. The tape also shows the day’s total charge sales. A proof is usually prepared to show that the amount of cash in the cash register equals the amount of cash sales and sales tax recorded on the cash register tape. The proof and the tape are sent to the accounting clerk, who uses the tape like the one in Figure 14–6 as the source document for the journal entry to record the day’s cash sales.

Charge Customer PaymentsBusinesses record cash received on account from charge customers by

preparing receipts. A receipt, shown in Figure 14–7 on page 394, is a form that serves as a record of cash received. Receipts are prenumbered and may be prepared in multiple copies. The receipt is a source document for the journal entry.

Reading Check Recall What are the three most common sources of cash for a merchandising business?

ANALYZING CASH RECEIPT TRANSACTIONSSECTION 14.3

Figure 14–6Cash Register Tape

3000.00 CA180.00 ST

Dec. 15Tape

Cash Sales

Sales Tax

glencoe.com

• Show Me tutorials • Let Me Try interactive

activities.

396 Chapter 14 Accounting for Sales and Cash Receipts

383-404_C14_SEC_893567.indd 396 9/10/10 12:37 PM

C1

C2

FOCUSBell Ringer • Advising: Have students assume

that they are giving accounting advice to a business owner who does not think it is necessary to record sales on account in both accounts receivable and individual customer accounts. Have students explain why this method of recording sales and cash receipts benefi ts the business.

• Digital Transparency 14-11 focuses students’ attention on the topics covered in Section 14.3.

Bell Ringer

C1 Critical ThinkingMaking Inferences Ask: Why do you think most businesses record cash sales using a cash register rather than preprinted sales slips? Answers will vary but can include the speed of using cash register over preprinted slips, having cash register print totals and possibly update inventory data. OL

C2 Critical ThinkingMaking Inferences Refer students to Figure 14-6 (Digital Transparency 14-12). Ask: Is the amount shown on the tape the result of one individual cash sale, or does it refl ect the total cash sales for the day? total for the day OL

Reading Checkpayments from cash sales, charge sales, and bankcard sales

SECTION 14.3

Content Vocabulary1. In a brief paragraph, explain the difference between a cash discount and a sales discount. Answers will vary.

Be sure students note that both are basically the same transaction, but to the seller, it is a sales discount, but to a buyer, it is a cash discount. The discount is the amount that a customer can deduct from the amount owed for purchased merchandise if payment is made within a certain time.

2. Explain the meaning of a cash sale. Answers will vary. It is a transaction whereby a business receives full payment for merchandise sold at the time of the sale.