my oral village

TRANSCRIPT

© My Oral Village, Inc. 2016

What We DoMy Oral Village (MOVE) is a not-for-profit firm that adapts retail financial

services to the needs of illiterate users.

We have three service offerings, drawing on deep specialization.

1.Digital OIM design2.Savings group OIM design 3.Research on oral market segment

© My Oral Village, Inc. 2016

‘Orality’ refers to the cultures and behaviors of people in communities where most cannot read or write. The culture of ‘mass literacy’ is the foundation of modern finance, accounting, newspapers, and even paper money. It is at an early or still-evolving stage in most of the world’s poor villages.

For purposes of financial inclusion, this makes the oral village a distinct market segment with distinct needs.

Why ‘My Oral Village’?

Swiss split tallies (right). Split tallies were used as loan records until the 19th century in much of Europe.

© My Oral Village, Inc. 2016

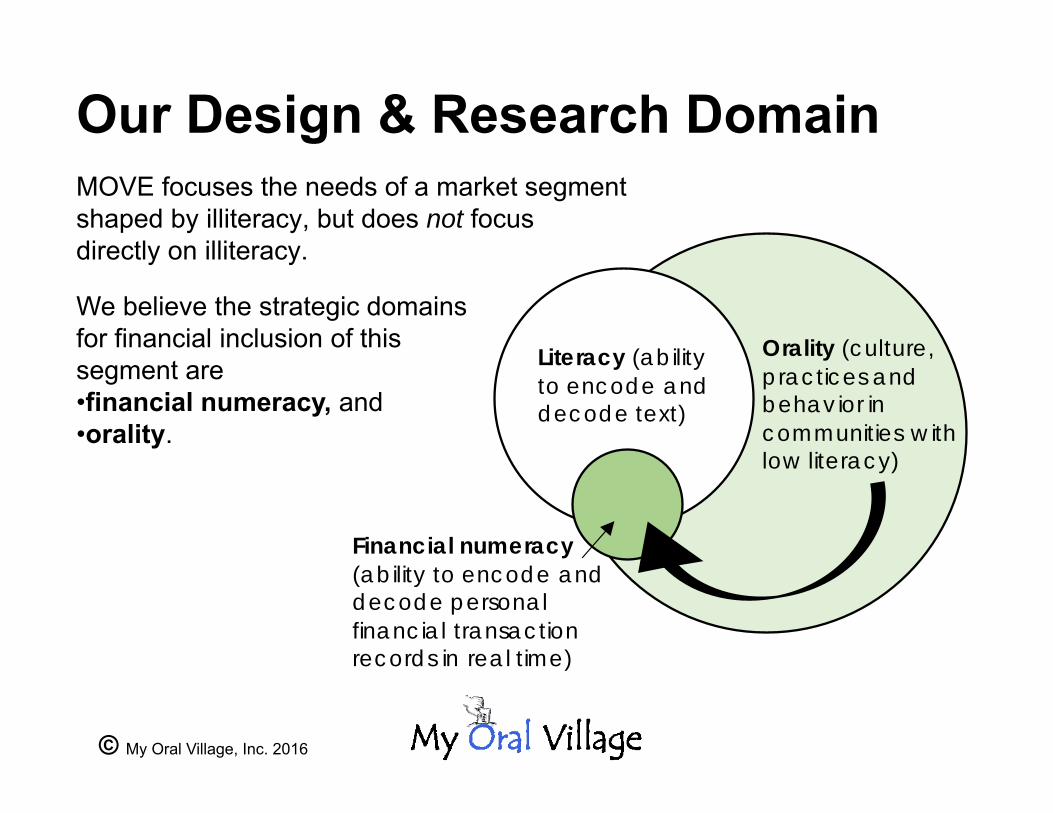

Our Design & Research Domain

We believe the strategic domains for financial inclusion of this segment are •financial numeracy, and •orality.

MOVE focuses the needs of a market segmentshaped by illiteracy, but does not focusdirectly on illiteracy.

Orality (culture,practices and behavior in communities with low literacy)

Literacy (ability to encode and decode text)

Financial numeracy (ability to encode and decode personal financial transaction records in real time)

© My Oral Village, Inc. 2016

Oral Information Management (OIM)Oral culture is predominantly pre-literate. To manage information, oral individuals use tools that do not depend on text or personal literacy. As the local economy monetizes these tools evolve and adapt, often ingeniously, but literacy may lag far behind.

MOVE builds on global best practices on oral information management (OIM) and supplements them with science to optimize opportunities for oral individuals to adapt faster and more effectively. Our bedrock principles include:

OIM Design Principles• Client-side product and service usability• Real-time transactional transparency for users

• Optimize voluntary client-side learning of strategic skills

• Efficient integration to financial/retail existing systems

• Optimize ‘win/win’ solutions (supplier-client)

© My Oral Village, Inc. 2016

The Painful Decline of Illiteracy

Source: UNESCO, May 2013

0

250

500

750

1,000

1985-94 1995-2004 2005-14 Projection, 2015

Illiterate adults, world (millions)1990-2015

All Male Female Linear (All)

female=

64.2%

Based on national census data about 750 million adults are illiterate, down from 910 million 25 years ago. Nearly two-thirds are women. Based on direct national

testing, UNESCO believes the true number is closer to 1 billion today.

© My Oral Village, Inc. 2016

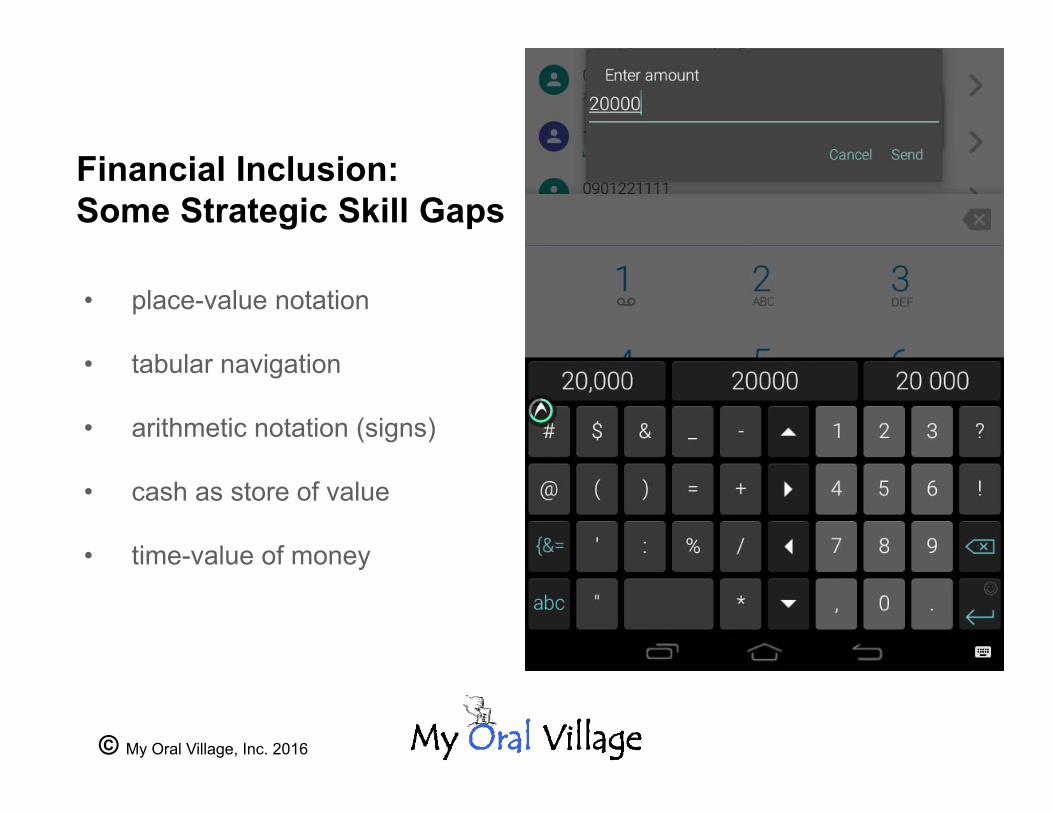

• place-value notation

• tabular navigation

• arithmetic notation (signs)

• cash as store of value

• time-value of money

Financial Inclusion: Some Strategic Skill Gaps

© My Oral Village, Inc. 2016

OIM Digital

© My Oral Village, Inc. 2016

Digital app designOral usability diagnostics, digital transactions Market research on oral segment: • financial numeracy• financial behavior and practices• digital capabilities

Practitioner training curriculum • building the business case• oral segment characteristics• product development/design

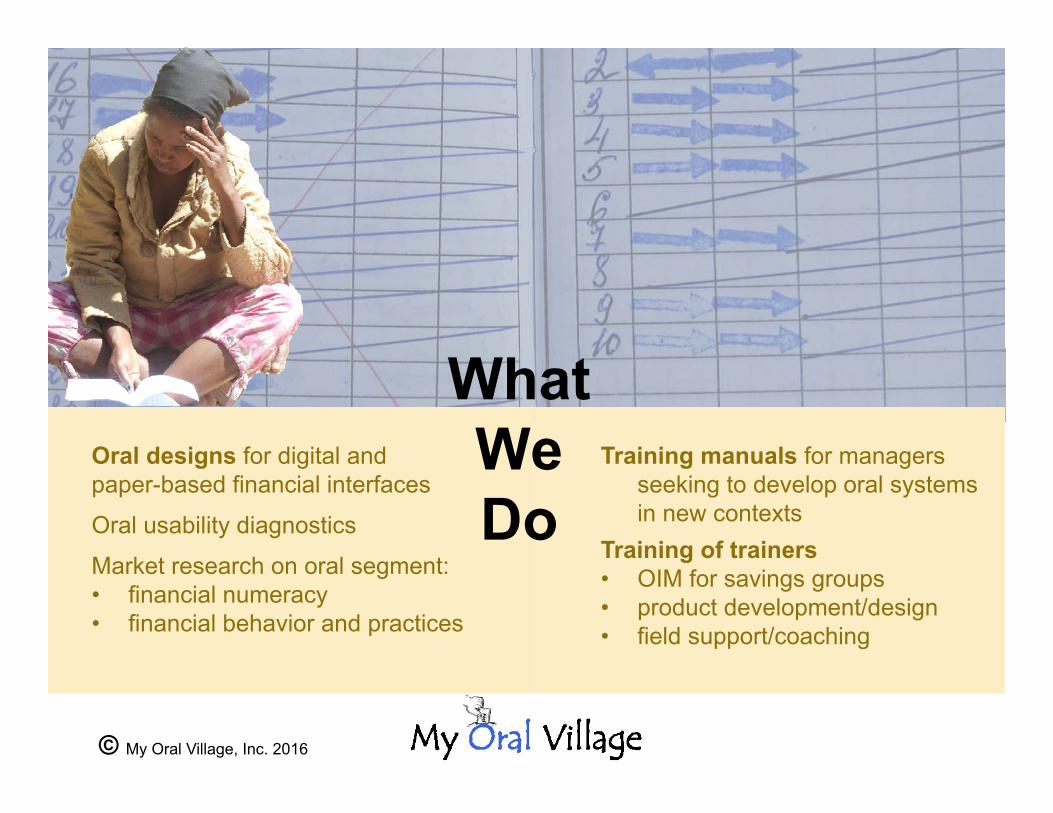

What We Do

© My Oral Village, Inc. 2016

Introducing Zebo 1.0 (Tanza version)Suite of 9 financial numeracy games, native to Android/Aakash tablet. They lever:• direct motivations to learn skills that support transactional competence, and • group-based mutual support norms and rules that can build competencies.

May need adaptation to different contexts. Designed for use by groups, especially those involved in financial transactions (e.g. joint-liability groups, savings groups, funeral societies, etc).

© My Oral Village, Inc. 2016

Mobile payment systems have been very successful, with nearly half a billion accounts opened in the past decade, mostly in Africa and Asia. However, nearly two-thirds of these accounts lie unused, and there is evidence that illiteracy is an important barrier to more widespread adoption.

Mobile Payments

OIM Mobile Payment AppIn field research, My Oral Village has established that a large majority of illiterate individuals cannot decode place-value (e.g. the meaning of the ‘6’ in 306,800), which is generally taught in late primary school. It is not possibly to safely transfer funds in existing mobile payment apps without this knowledge.

My Oral Village is designing and testing a mobile payment app that can be safely and confidently used by individuals who cannot decode place value.

© My Oral Village, Inc. 2016

OIM Savings Group

© My Oral Village, Inc. 2016

Training manuals for managers seeking to develop oral systems in new contexts

Training of trainers • OIM for savings groups• product development/design• field support/coaching

Oral designs for digital and paper-based financial interfacesOral usability diagnostics Market research on oral segment: • financial numeracy• financial behavior and practices

What We Do

© My Oral Village, Inc. 2016

My Oral Village has developed a complete OIM solution for savings groups, including:

• passbook design with navigation support, place value guide, and calculator page;

• time-limited ‘savings plan’ product that builds cash management skills; and

• share-out process design that is faster, more transparent and participatory than prevailing practice.

‘Counting team’ checks member passbooks during savings group share-out process.

My Oral Village can develop a full system and train your staff so they can expand/revise it in future.

Local model-based variations in member skills and practices, group goals (e.g. linkage) will affect results.

© My Oral Village, Inc. 2016

Oral Information Management Tools: Lighting the Path to Financial Inclusion (2014). This introduction to OIM offers examples from Cambodia, Bangladesh and Solomon Islands. It outlines core principles for OIM design, and reviews the theory behind the practice.

Governing the Oral Institution (2009). Drawing on pioneering studies of orality by Walter J. Ong, and work by Ronald Coase and Oliver Williamson on transaction costs, this paper lays out a theoretical framework and practical tools for overcoming the institutional failure of rural financial markets.

Oral Financial Numeracy: A Hypothesis and Exploratory Test (2016). Study of financial numeracy among 80 illiterate villagers in Tanzania and Cambodia. Physical cash, or a recognizable proxy, greatly eases counting and calculating for the oral segment. Supplies could use this to increase customer trust.

Publications

© My Oral Village, Inc. 2016

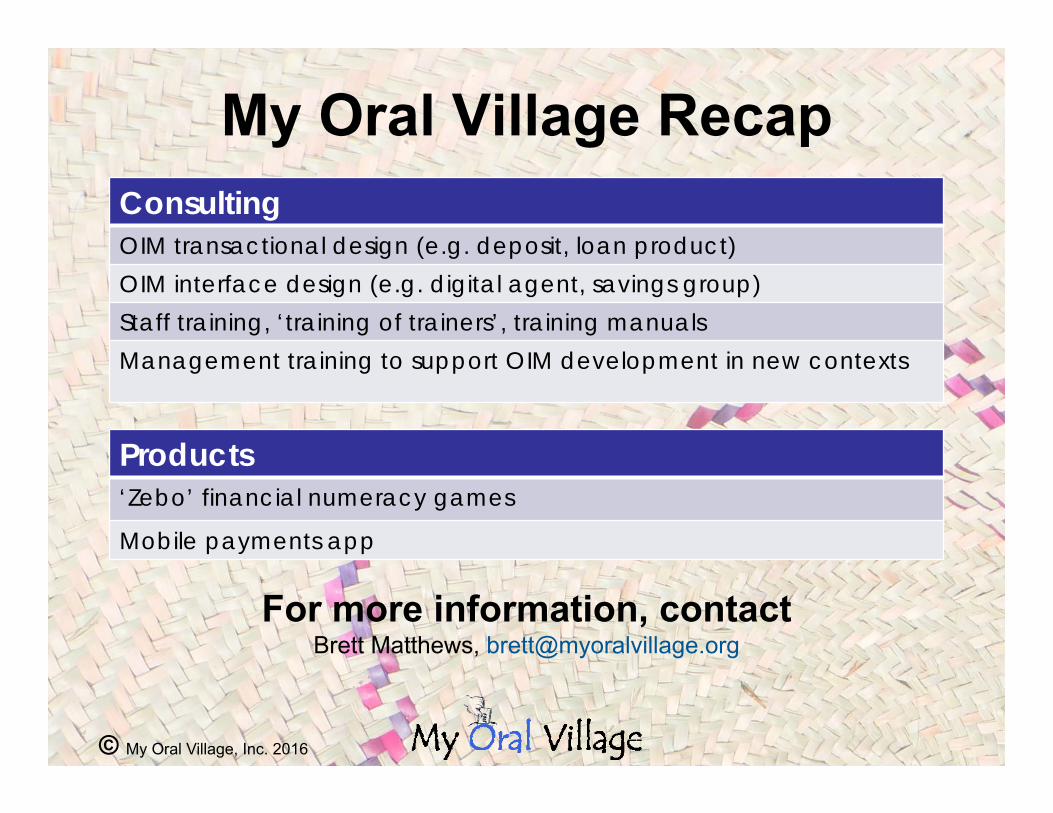

My Oral Village RecapConsultingOIM transactional design (e.g. deposit, loan product)OIM interface design (e.g. digital agent, savings group)Staff training, ‘training of trainers’, training manualsManagement training to support OIM development in new contexts

For more information, contact Brett Matthews, [email protected]

Products‘Zebo’ financial numeracy games

Mobile payments app

© My Oral Village, Inc. 2016

Brett MatthewsExecutive Director and Lead Designer24 years in financial services: 16 in microfinance and eight in a Canadian financial institution.

Special consultant to CGAP on oral financial inclusion.Delivered key presentation at CGAP sector consultation on smartphones in Washington, DC in Ap. 2016.

Other clients include UNCDF, DAI, FSDT, Oxford Policy Management, Central Bank of Solomon Islands and MicroSave.

Brett’s signature traits include strong focus on understanding the customer and developing solutions that lower transaction costs for suppliers and poor people. The digital revolution has created many opportunities, for those able to overcome limiting assumptions about illiteracy.

© My Oral Village, Inc. 2016

President Heather BroughtonTreasurer Cecilia LukoDirector David Myhre

Executive Director Brett MatthewsChief Marketing Officer Margaret Hazlewood

Contact: [email protected]