my masters thesis

TRANSCRIPT

i

SHAREHOLDER WEALTH EFFECTS OF DIVIDEND POLICY

CHANGES IN AN EMERGING STOCK MARKET (THE CASE OF

PAKISTAN)

by

Muhammad Waqas

A thesis submitted in partial fulfillment of the requirements for

the degree of

M.Com (Accounting & Finance)

University of Central Punjab

2004-2006

Approved by ___________________________________________________ Thesis Co-ordinator: Mr. Syed Amir Ali Shah

__________________________________________________

__________________________________________________

__________________________________________________

Principal _______________________________________________________

Date __________________________________________________________

TABLE OF CONTENTS

Title Page No.

I Abstract…………………….…………………………………………….i

II Acknowledgement ……………………………………………………….ii

III List of Abbreviations……………………………………………………..iii

1. Introduction……………………………………………………………..1

1.1 Dividend………………………………………………………….1

1.2 Cash……………………………………………………………....1

1.3 Stock……………………………………………………………...2

1.4 Dividend Policy…………………………………………………..2

1.5 Karachi Stock Exchange………………………………………....2-5

1.6 The Badla or Traditional Carry Forward System…………………5

1.7 The Pakistan Experience………………………………………....5-8

1.8 Growth and Progress……………………………………………..9

2. Literature Review……………………………………………………….10-31

3. Hypothesis and Data Methodology……………………………………..32-36

4. Data Analysis……………………………………………………………37

4.1 Presentation and Discussion on Results…………………………..37-38

ii

5. Conclusion……………………………………………………………....39

Appendices

Appendix 1 Announcement History and Share Prices…………………41-44

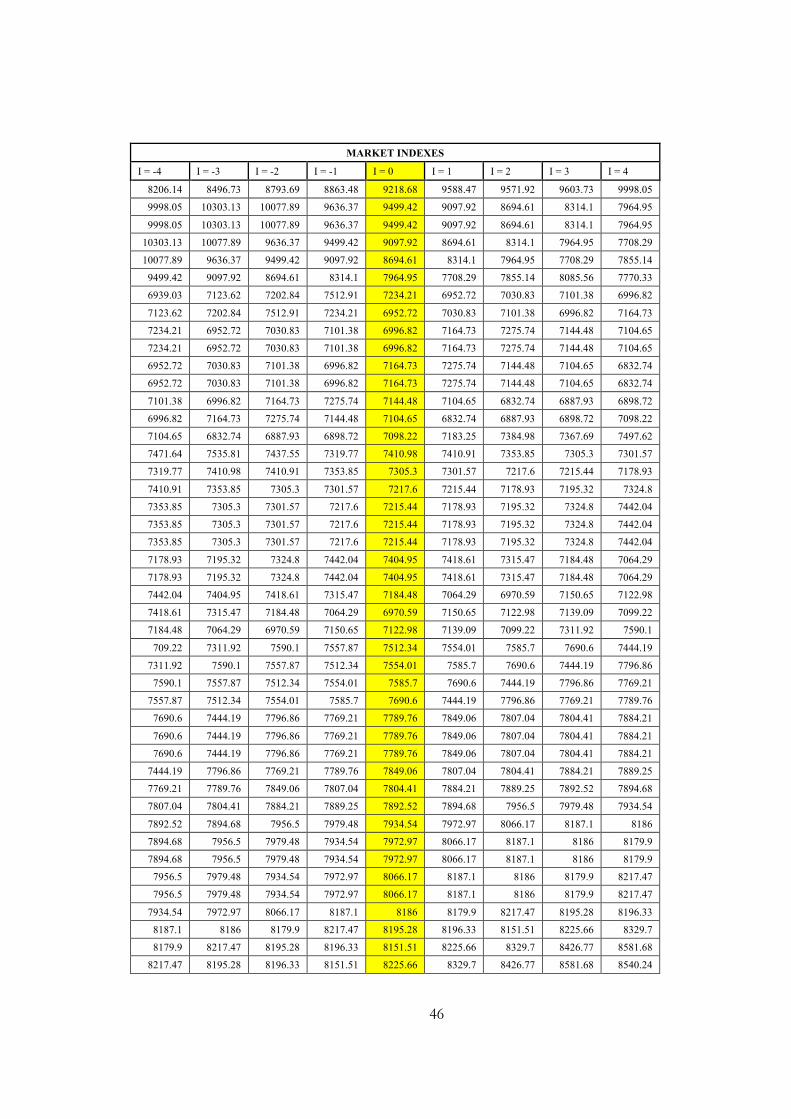

Appendix 2 Market Indexes…………………………………………..45-48

Appendix 3 Returns of Market……………………………………..…49-52

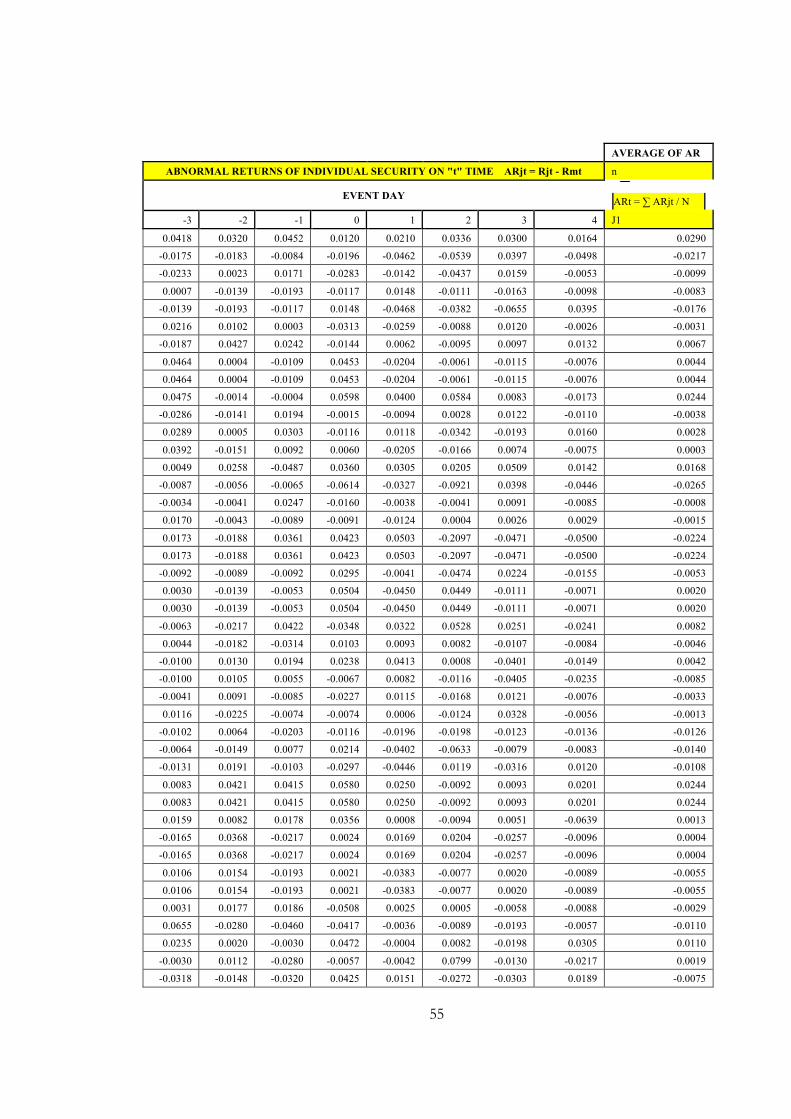

Appendix 4 Abnormal Returns of Individual Security………………..53-56

Bibliography…………………………………………………………….57-60

i

UNIVERSITY OF THE CENTRAL PUNJAB

ABSTRACT

SHAREHOLDER WEALTH EFFECTS OF DIVIDEND

POLICY CHANGES IN AN EMERGING STOCK MARKET

(THE CASE OF PAKISTAN)

by Muhammad Waqas

Thesis Co-coordinator: Mr. Syed Amir Ali Shah Department of Finance

This dissertation examines the stock market reaction to announcements of

cash dividend increases and bonus issues (stock dividends) in the

emerging stock market of Karachi Stock Exchange. Both events elicit

significantly negative abnormal returns, in line with evidence from

developed stock markets. This study contends that special characteristics

of the Karachi stock market delimit applicability of most traditional

explanations for cash and stock dividends in favor of an information-

signaling explanation. The empirical results are generally in agreement

with these contentions.

ii

ACKNOWLEDGMENTS

All praises to Almighty Allah who is “THE CREATOR” of whole of the

universe and admires to our Holy Prophet Muhammad (Peace Be upon

Him) who taught us every thing of this life and the life thereafter.

Now it is our responsibility to convey the “WORDING OF SUCCESS” to

whole of the Ummah. As it was indicated in the last Address of our Holy

Prophet (Peace Be upon Him). And the graves of “FELLOW BEINGS” are

the proof of the completion of this responsibility.

And I am also thankful to my respected Facilitator and Thesis Co-ordinator

Mr. Syed Amir Ali Shah. He delivered knowledge to us in such a way that

it would help me through out my practical life.

1

C h a p t e r 1

INTRODUCTION

1.1 Dividend

Dividends are payments made by a company to its shareholders. When a

company earns a profit, that money can be put to two uses. It can either be re-

invested in the business (called retained earnings) or it can be paid to the

shareholders of the company as a dividend. Many companies retain a portion

of their earnings and pay the remainder to their shareholders. Publicly-traded

companies usually pay dividends on a fixed schedule, commonly annually,

semi-annually or quarterly however, they may declare a dividend at any time.

Dividends are usually paid in cash. Sometimes dividends instead take the

form of shares in the company (either newly-created shares or existing shares

bought in the market). Exceptionally, dividends might take the form of shares

in other companies or other assets.

The profits of a company can either be reinvested in the business or paid to its

shareholders as a dividend. The frequency of these varies by country. In the

United States dividends of publicly-traded companies are usually declared

quarterly by the board of directors. In some other countries dividends are paid

biannually, as an interim dividend shortly after the company announces its

interim results and a final dividend typically following its annual general

meeting. In other countries, the board of directors will propose the payment of

a dividend to shareholders at the annual meeting who will then vote on the

proposal.

1.2 Cash

Cash and dividends (most common) are those paid out in form of real cash.

Such dividends are a form of investment income and are usually taxable to the

recipient in the year they are paid. This is the most common method of

sharing corporate profits with the shareholders of the company.

2

1.3 Stock

Stock or scrip dividends are those paid out in form of additional stock shares

of the issuing corporation, or other corporation (e.g., its subsidiary

corporation). They are usually issued in proportion to shares owned (e.g., for

every 100 shares of stock owned, 5% stock dividend will yield 5 extra

shares). This is very similar to a stock split in that it increases the total

number of shares while lowering the price of each share and does not change

the market capitalization or the total value of the shares held.

1.4 Dividend Policy

Once a company makes a profit, they must decide on what to do with those

profits. They could continue to retain the profits within the company, or they

could pay out the profits to the owners of the firm in the form of dividends.

Once the company decides on whether to pay dividends, they may establish a

somewhat permanent dividend policy, which may in turn impact on investors

and perceptions of the company in the financial markets. What they decide

depends on the situation of the company now and in the future. It also

depends on the preferences of investors and potential investors.

In the United States, a decision regarding the amount and frequency of

dividends is solely at the discretion of the board of directors. Shareholders are

explicitly forbidden from introducing shareholder resolutions involving

specific amounts of dividends. Where a company makes a loss during a year,

it may opt to continue paying dividends from the retained earnings from

previous years or to suspend the dividend. Where a company receives a non-

recurring gain, e.g. from the sale of some assets, and has no plans to reinvest

the proceeds, the money is often returned to shareholders in the form of a

special dividend.

1.5 Karachi Stock Exchange (KSE)

Karachi Stock Exchange (KSE), established in 1947, is the oldest and the

most active of the three stock exchanges in Pakistan, and currently lists 662

companies with a total market capitalization of about $52 billion. The

KSE100 represents major blue chips companies and is fairly good

3

representative of the market. Besides the KSE there are two regional stock

exchanges in Lahore and Islamabad. The other two exchanges are however

relatively inactive. For example, during July 2005-March 2006 period the

average daily turnover at the KSE was 462.4 million share, while at LSE

and ISE it was 65.4 and 1.7 million shares, representing 12% and 3% of the

total market activity respectively.

Similar to other emerging markets, KSE has a limited role in raising new

capital; e.g., there were only five new listings in the market in 2005. Despite

the small size of the market, it experiences a high turnover and high price

volatility. From the plot of the KSE100 index over the five year period

2001-2005, we can see that the market experienced significant fluctuations

over shorter time intervals. Finally, a skewed size distribution of stocks

traded is observed for the KSE, i.e., skewed in terms of size, trading

patterns, volume of brokers’ trading and weighted value of stocks in the

index. This is particularly true for top 20 stocks accounting for 85% of the

overall turnover.

Here I have provides salient features of Bombay Stock Exchange (BSE) and

KSE for comparison. The KSE is relatively a much smaller market compared

to the BSE, both in terms of the listed companies as well as market

capitalization. Reflecting its smaller size the KSE represents only 0.7% of the

total capitalization of the emerging markets, compared to BSE’s 7.9%share. It

is interesting to note the sharp contrast between Pakistan’s capitalization ratio

(which is low) and relatively high turnover ratio. This characteristic probably

reflects noise trading and speculative element in the market. The spectacular

rise in the KSE of 410% over the 2001-05 periods is remarkable, though

260% appreciation of the BSE also stands in sharp contrast with the

performance elsewhere in the world. The appreciation in the KSE100 index

and BSE30 index was 534% and 137% respectively for the same period. The

Pakistani stock market appreciation was four times higher than the Indian

market despite a higher rate of growth in the Indian GDP for the same period.

This also shows that the PE ratio and Price to Book value of Pakistani

4

companies included in the S&P/IFC Global Index is nearly 2/3, and the

dividends yield nearly half of that of the Indian companies. These statistics

suggest that the cost of capital for the Indian companies would be much lower

than for the Pakistani companies. Another important difference is the higher

degree of correlation of the BSE (0.69) with the S&P Composite Index,

compared with correlation coefficient of 0.32 in case of KSE, which reflects a

higher degree of integration of the BSE with the international capital markets.

Besides, the differences between the two markets in size, activity and other

characteristics noted above, there are two aspects of these markets which may

have a direct bearing on the regulatory response and its effectiveness in

dealing with market manipulation and volatility. First is the difference in the

industry structure and competition among the stock exchanges. As already

noted above, in case of India, NSE has emerged as the leading stock exchange

in the country, with 45% market share, thus eliminating BSE’s monopolistic

position that it had enjoyed ever since its inception. NSE along with 22 other

active regional exchanges creates a more competitive environment. In

Pakistan, KSE is still the dominant player with 85% share of the trading

activity.

Secondly, there seems to be a significant difference between the regulatory

enforcement and effectiveness of public policy. Nageswaran and Krithivasan

(2006), for example, claim that only Singapore, Hong Kong and India are

effective in enforcement among Asian countries. According to data compiled

by Goyal (2004), SEBI had taken up 657 cases for investigation in the period

1992-2003, and had completed 424 cases. 250 prosecutions were launched

against collective investment schemes over 2001-03. During the same year

there were 257 actions taken against brokers and others out of which there

were 42 suspensions. SEBI’s record in redressing grievances also appears to

be effective; the redress rate is about 95%. In contrast, according to a survey

conducted by La Porta et al. (2006) Pakistan scores rather low on the indices

of (i) orders to issuers, distributors and accountants (ii) criminal sanctions and

(iii) public enforcement which capture the extent to which a public regulator

5

exercises investigative power and its ability to impose penalties. Pakistan’s

score on these three indices is 0.17, 0.08 and 0.58, compared to India’s 0.67,

0.83 and 0.67 respectively. Khwaja and Mian (2005) remark with respect to

Pakistan that, “Thus, it is not surprising that to date there has hardly been any

case in which a broker was prosecuted for improper activity.”

1.6 The Badla or Traditional Carry Forward System

An old and traditional informal institution common to both India and Pakistan

is that of Badla, meaning something in return. It is a local term for a forward

trading facility, and essentially is a repo transaction carried out in a separate

after-hours market where the borrower who takes the badla from a badla

broker, carries forward his security exposure from the current settlement

period to the next one, by sale of his position in the present period and its

repurchase in the subsequent settlement period at a predetermined price

differential. In the event of a purchase, the investor may want to carry forward

the transaction to the next settlement cycle and for doing so, he has to

compensate the seller who sold it with an intention of getting cash.

1.7 The Pakistan Experience

The KSE experienced a steady bull run as reflected in both the KSE 100

index and trading volumes, starting just after the last stock market crisis in

May 2002, which accelerated towards the end of 2004. The KSE 100 saw an

unprecedented rise of 65%, from 6,218 on December 31, 2004 to 10,303 on

March 15, 2005, along with an increase in the value traded from around

$300-400 million to $1-2 billion per day. The market turned negative in the

second half of March, 2005 and index dropped to as low as 6,939 on April

12, 2005, a decline of 32.7 percent from its peak. The sharp rise in the index

could not be explained by any change in the fundamentals. The following

precipitous fall is also somewhat of a puzzle. Such a meteoric rise in index

and a subsequent crash is indicative of a classical speculative bubble in the

equity market.

Badla has been blamed as one of the reasons for the March 2005 crisis.

Pakistan’s influential financial newspaper Business Recorder stated that

6

there were two problems. First, badla financing was only open to a small

number of market players, which also includes financial institutions, as

opposed to share trading. Second, badla financing was provided by short-

term investors and the hot money can disappear overnight. During 2004-05,

KSE investors were willing to borrow at exorbitant Badla rates (which were

capped at 18% in KSE but rose in the uncapped Lahore Stock Exchange to

over 100%) because the accelerated rise in stock prices made even

expensive borrowing feasible. The COT (badla) financing ranged from 33%

to 45% of investment at KSE throughout 2004. The higher demand for badla

investment pushed the average badla rates from 9.4 % in 2003, to 11.4% in

2004, ranging from 12 to 19 percent, even though market interest rates

remained stable at a relatively low level through most of 2004.

The growing availability of badla financing brokers and institutions added to

the buying frenzy, though some of the major badla providers were

simultaneously selling in the futures market. In other words, “there was a

strong nexus between lenders and brokers/investors who could influence

market sentiment to their own advantage” (Task Force Report, 2005). The

chairman of SECP stated on July 16, 2005 that badla was the root cause of

almost all previous crises at the bourses, and was to be rooted out, and that

the badla and margin financing could not co-exist.

After the March 2005 crisis, a task force was set up by the Chairman of

Securities and Exchange Commission of Pakistan (SECP) to identify the

causes for the situation arising at the country’s three stock exchanges in

March 2005 and to propose measures for strengthening and consolidating the

regulatory regime, particularly with a view to enabling emergency

intervention, preventing systematic risk and promoting market stability. The

task force completed its report in July 2005 identifying a few areas that

contributed to the instability in the stock prices. The Task Force

recommended that there was a need for structural reforms and steps were

needed to protect public interest by ensuring that the financial might that has

been accumulated by the stock brokerage and badla financing institutions

7

should be effectively checked and brought to a reasonable size to ensure that

they are unable to manipulate the market.

Besides badla financing, other factors which contributed to this bull-run

included, increased liquidity due to higher foreign remittances, a regime of

low interest rates, IPO’s of public sector enterprises marked for divestment

and floatation of more mutual funds. During this period, especially since mid

October, 2004, there was an unusual build-up in the media about the

prospects of a rise in the KSE index. Statements from government officials

linked the rise in the KSE index to good economic management, indicated

that the market was destined to rise further, and announcement of the

impending accelerated program for the privatization of prominent and

profitable public sector corporations fuelled the bullish sentiment. Conduct of

corporate officials contributed to the market speculation; for example, rumors

of new oil and gas discoveries which would raise stock value manifold went

un-refuted or clarified by the management. There were also allegations of

“wash trades” and “pump and dump” plays by brokers.

The main thrust of the Pakistani regulators was to replace badla with formal

financing arrangements. The State Bank of Pakistan (SBP) in collaboration

with SECP, came out with rules governing margin financing issued to stock

brokers by banks. The SBP rules specified the conditions of extending such

loans to stock market brokers with proper risk management and internal

controls. It has also specified the minimum margin requirement of 30 percent

and reminded banks of the per party limit, in case of such lending to brokers.

The SECP intended to completely eliminate the carryover market (the badla

market) by the end of December 2004. Initially, the plan was to replace

margin financing with badla in 2003 but slow progress by the regulators has

resulted in the delay.

Regarding the replacement of badla financing the regulatory bodies were seen

as vacillating. For example, we quote a newspaper op-ed, Badla is back. “But

firmness doesn’t appear to be the strong point of the Securities and Exchange

Commission of Pakistan. … What went wrong? Or, rather, how heavy was

8

the pressure from vested interests? Were the members of the Karachi Stock

Exchange so powerful that they managed to force the regulator to work in

their interest? The SECP has not only proved to be a weak regulator but also

exposed itself to the criticism that it acts first and thinks later”.

There were other factors which lessened the effectiveness of the regulators’

actions. First, the composition of the Task Force was not without conflicts of

interest as its members also were on the Policy Board investigating matters

which should have been the subject matter of the Board itself when

formulating capital markets policies. Second, the mostly held view is that the

March debacle was due to excessive institutional selling and the withdrawal

of Badla financing simultaneously from the market. In the past, SECP had

been criticized for allowing the brokerage houses to own commercial and

investment banks which provided them additional resources to enter into

Badla financing and use it to manipulate market. Third, the Task Force, a

creation of SECP, could not look into the question of inadequate surveillance

and weak implementation by SECP.

The Task Force also did not look into the role of KSE management, in

possibly precipitating the withdrawal of the badla facility by calling upon the

various brokers and institutions to reconfirm that they would be able to honor

their obligations in the future contracts, and sending alarming signals to

market players. As there were four SECP nominated directors on the KSE

board, there is a possibility of conflict of interest. However, while the KSE

does receive some oversight from the SECP, it is predominantly broker-

managed, i.e., a majority of the exchange’s board of directors including the

chairman is brokers. The Task force also did not investigate the allegation of

market manipulation by certain mutual funds through withdrawing the badla

financing and to take advantage of the pursuing crash.

1.8 GROWTH AND PROGRESS

9

Today KSE has emerged as the key institution of the capital formation in

Pakistan with:

• Listed companies 654, securities listed on the exchange 694:

ordinary share 654, Preference shares 15 and debt securities

(TFC's) 25.

• Listed capital Rs.516,938.51 million (US$ 8,516.29 million).

• Market capitalization Rs.3,077,401.41 million (US$ 50,698.54

million).

• Average daily turnover 168.87 million shares with average daily

trade value Rs. 20,194.29 million (US$ 332.69 million).

• Membership strength at 200.

• Corporate Members are 158 out of which 9 are public listed

companies.

• Active Members are 163.

• Fully automated trading system with T+3 settlement cycle.

• Deliveries through central depository company.

• National Clearing and Settlement System in place.

10

C h a p t e r 2

LITERATURE REVIEW

Dividend policy remains a source of controversy despite years of theoretical

and empirical research, including one aspect of dividend policy: the linkage

between dividend policy and stock price risk (Allen and Rachim, 1996).

Paying large dividends reduces risk and thus influence stock price (Gordon,

1963) and is a proxy for the future earnings (Baskin, 1989). A number of

theoretical mechanisms have been suggested that cause dividend yield and

payout ratios to vary inversely with common stock volatility. These are

duration effect, rate of return effect, arbitrage pricing effect and information

effect. Duration effect implies that high dividend yield provides more near

term cash flow. If dividend policy is stable high dividend stocks will have a

shorter duration. Gordon Growth Model can be used to predict that high-

dividend will be less sensitive to fluctuations in discount rates and thus ought

to display lower price volatility.

Agency cost argument, as developed by Jensen and Meckling (1976)

proposed that dividend payments reduce costs and increase cash flow, that is

payment of dividends motivates managers to disgorge cash rather than

investing at below the cost of capital or wasting it on organizational

inefficiencies (Rozeff, 1982 and Easterbrook 1984). Some authors have

stressed the importance of information content of dividend (Asquith and

Mullin, 1983; Born, Moser and officer 1983). Miller and Rock (1985)

suggested that dividend announcements provide the missing pieces of

information about the firm and allows the market to estimate the firm’s

current earnings. Investors may have greater confidence that reported

earnings reflect economic profits when announcements are accompanied by

ample dividends. If investors are more certain in their opinions, they may

11

react less to questionable sources of information and their expectation of

value may be insulated from irrational influence.

Rate of return effect, as discussed by Gordon (1963), is that a firm with low

payout and low dividend yield may tend to be valued more in terms of future

investment opportunities (Donaldson, 1961). Consequently, its stock price

may be more sensitive to changing estimates of rates of return over distant

time periods. Thus expanding firms although may have lower payout ratio

and dividend yield, exhibit price stability. This may be because dividend

yields and payout ratio serves as proxies for the amount of projected growth

opportunities. If forecasts of profits from growth opportunities are less

reliable than forecasts of returns on assets in place, firms with low payout and

low dividend yield may have greater price volatility. According to duration

effect and arbitrage effect, the dividend yield and not the payout ratio is the

relevant measure. The rate of return effect implies that both dividend yield

and payout ratio matters. Dividend policy may serve as a proxy for growth

and investment opportunities. Both the duration effect and the rate of return

effect assume differentials in the timing of the underlying cash flow of the

business. If the relationship between risk and dividend policy remains after

controlling for growth, this would suggest evidence of either the arbitrage or

information effect.

Empirical studies have examined cross-sectional variation in dividend payout

ratios and CAPM beta coefficients. Beaver et. al. (1970) estimated CAPM

betas for 307 US firms and obtained significant correlation between beta and

dividend payout. Rozeff (1982) found a high correlation between value line

CAPM and betas and dividend payout for 1000 US firms. Fama (1991) and

Fama and French (1992) focus on dividends and other cash flow variables

such as accounting earnings, investment, industrial production etc to explain

stock returns. Baskin (1989) takes a slightly different approach and examines

the influence of dividend policy on stock price volatility, as opposed to

12

returns. The difficulty in any empirical work examining the linkage between

dividend policy and stock volatility or returns lies in the setting up of

adequate controls for the other factors. For example, the accounting system

generates information on several relationships that are considered by many to

be measures of risk. Baskin (1989) suggests the use of the following control

variables in testing the significance of the relationship between dividend yield

and price volatility: operating earnings, size of the firm, level of debt

financing, payout ratio and level of growth. These variables have a clear

impact on stock returns but also impact on dividend yield.

Karachi Stock Exchange (KSE) is an important emerging market of the

region among the developing countries. KSE is termed as high-risk high

return market where investors seek high-risk premium (Nishat, 1999). Few

studies have attempted to analyze the long run behavior of the market and

related issues (Nishat, 1991, 1992 1995, 1999, 2001; Nishat and Bilgrami,

1994) but no work has been done to explore role of dividend yield and payout

ratio in affecting the share prices. It is also important to study its role in the

Pakistani context after the introduction of reforms during 1990s, which

emphasized more towards openness to foreign investor, and competition,

which led to, increased volatility in the market (Nishat, 1999) and has reduced

the responsiveness of share price volatility to fundamental factors (Irfan and

Nishat. 2003). Reforms in Pakistan in general and specific to dividend policy

are; tax sealing on cash dividend, exemption of right and bonus shares from

tax, pattern shifting from cash to share dividend and government policy of

easing restrictions on transfer of market profits etc. The objective of this study

is to find the role of dividend policy measures i.e. dividend yield and payout

ratio on share price changes in the long run. It also attempts to assess the

pattern of relationship during pre reform (1981-1990) and reform (1991-2000)

periods.

13

A significant stream of prior research in the United States has empirically

documented that unexpected increases (decreases) in regular cash dividends

generally elicit a significantly positive (negative) stock market reaction (see,

for example, Fama et al. [1969] and Petit [1972]). Moreover, this finding

persists even after controlling for contemporaneous earnings announcements

(Aharony and Swary [1980]). In the same vein, Asquith and Mullins [1983]

find that, like dividend increases, dividend initiations have a significant

positive impact on shareholder wealth. Much subsequent research has focused

on explaining the dividend-increase induced positive stock market reaction.

The predominant explanation, by far, has been the information-signaling

hypothesis. Since managers have information that outside investors do not

have, dividend policy is a costly-to-replicate vehicle for conveying positive

private information to market participants. In line with these arguments,

signaling models by Bhattacharya [1979] and Miller and Rock [1985], among

others, find that dividend increases convey information about the firm's

current and future cash flows. In addition to supportive event-study results,

empirical studies by Ofer and Siegel [1987] and Healy and Palepu [1988]

examine changes in dividend policy in relation to future earnings and related

analysts forecasts, also consistent with the information-signaling hypothesis.

Bernartzi, Michaely, and

Thaler (1997) find that earnings are less likely to drop after a dividend

increase; however, they do not find that dividend increases are followed by

unexpected earnings increases. Their evidence is only weakly consistent with

an information-signaling hypothesis. DeAngelo, DeAngelo and Skinner

(1992) find that a loss is a necessary but not a sufficient condition for a

dividend cut, and that dividend cuts improve the ability of current earnings to

predict future earnings. Moreover, DeAngelo, DeAngelo, and Skinner (1992),

Bernartzi, Michaely, and Thaler (1997), and Jensen and Johnson (1995)

document that dividend cuts are followed by earnings increases, consistent

with dividend cuts marking the end of a firm’s financial decline and the

beginning of its restructuring. In sum, the empirical evidence by prior

14

research on the signaling value of dividend changes has been mixed. An

alternative explanation for changes in corporate dividend policy stems from

agency theory. Jensen (1986) suggests that managers, motivated by

compensation and human capital considerations, have incentives to over

invest free cash flows even in the absence of profitable growth opportunities

(the free cash flow hypothesis). Dividend payout policy in this case becomes

a vehicle for monitoring the managers' potential to misuse excess funds. Thus,

the observed positive stock market reaction following dividend increases is

consistent, in addition to information-signaling, with a reduction in agency

costs.

Lang and Litzenberger [1989] attempt to disentangle between signaling and

agency explanations by separating firms that are presumably over investing

(with q ratios less than one) from all other value-maximizing firms. They find

higher abnormal returns for over investing firms for which the agency-related

benefits of a dividend payout increase are higher compared to value-

maximizing firms. Consistent with the free cash flow hypothesis, the market

reaction to dividend increases by value-maximizing firms, albeit positive, is

significantly lower than the market reaction for over investors. By contrast,

Denis, Denis, and Sarin [1994], after controlling for dividend yield, find no

support for the free cash flow hypothesis for a large sample of dividend

changes. Furthermore, Yoon and Starks (1995) do not detect the release of

new information about managers’ investment policies following a change in

dividend policy. They find a positive relation between dividend policy

changes and capital expenditure changes, interpreting their evidence as being

supportive of an information-signaling over a free cash flow explanation of

dividend policy. Also consistent with the free cash flow hypothesis,

DeAngelo and DeAngelo [2000] find evidence that the market penalized

Times Mirror for intending to poorly reinvest free cash flow and applauded

later dividend redistributions of that cash flow. Finally, in a major

international study, La Porta et al. [2000] find that dividends are paid because

minority shareholders pressure corporate insiders to disgorge cash. Additional

15

studies on the relevance of the free cash flow hypothesis for alternative

payout methods such as share repurchase and special dividends have provided

mixed results (e.g., Howe, He, and Kao [1992], Vafeas [1997], and Nohel and

Tarhan [1998]). Despite mixed overall evidence on the free cash flow

hypothesis, most researchers attribute the conflicting results to imperfect

empirical constructs rather than theoretical flaws. A third explanation is the

tax hypothesis. Given the differential tax treatment between dividend income

and capital gains, dividend policy changes also have tax implications that are

reflected in stock market prices. In the United States, capital gains have

historically been taxed more favorably than dividends. In Cyprus capital gains

on stock investments have not been taxed at all while dividends received

(beyond an exempt amount) are taxed at an individual’s personal income tax

rate. Therefore, capital gains would be preferable to most individual investors

and dividend increases should elicit a negative stock price reaction.1 the

observed positive stock market reaction of dividend increases for U.S. firms

appears to be inconsistent with the unfavorable tax treatment of dividend

income. Conceivably, any negative tax effect may be dominated by stronger

positive signaling and/or free cash flow effects. Examination of the market

reaction to dividend changes in an emerging market such as Cyprus can be a

fruitful empirical exercise in that the relative import of alternative

explanations of dividend policy may likely differ compared to a developed

market. First, a clear implication of the standard free cash flow hypothesis as

advanced by Jensen [1986] is the separation of ownership and control since

wider ownership dispersion intensifies the conflict of interests between

managers and shareholders. This conflict of interests generally motivates

higher dividend payouts to limit the managerial tendency to misuse

shareholder funds. In Cyprus firms are, for the most part, closely held, with

ownership concentrated in the form of large equity blocks in the hands of

management and family members. This may suggest that managers in Cyprus

have a disincentive to misuse funds through over investing since the relative

benefit of managing a larger firm is likely to be outweighed by the direct cost

16

of over investing on the managers' substantial personal holdings in the firm.

The point is, as ownership becomes more concentrated, the likelihood of over

investment is reduced. Further, firm sizes are quite small in Cyprus so that the

managerial "hubris" effect of inflating firm size is likely negligible.

However, in many of these family businesses there may be conflict of

interests between the larger and the smaller shareholders. The problem may

be more pronounced in many emerging markets when lack of transparency,

both at the company level and in the stock market, allows alternative forms of

exploitation of the smaller shareholders by the larger shareholders and

management (see Holderness and Sheehan [1988]). Since monitoring is

difficult in such cases, it may be substituted by higher dividends that may

serve to mitigate this form of exploitation. Thus, although over investing free

cash flow in the Cyprus market is likely to be limited due to concentrated

corporate ownership structures, other forms of exploitation of smaller

shareholders by larger shareholders and management may partly justify

dividend increases, in addition to information signaling reasons. That is, small

stockholders purchasing equity against large block holders expect to suffer a

certain degree of exploitation. An unexpected increase in cash dividends

reduces the market’s assessment of future exploitation by large block holders,

causing an upward revision in the stock price.

In this study Rongrong Zhang [2005] examines the effects of firm and

country-level corporate governance mechanisms on dividend and cash

holding policies and their joint impact on firm value. He found that at the

firm-level, the excess control held by the largest owner is negatively related to

dividend payment; positively related to cash holdings and negatively related

to Tobin’s Q(The ratio of the stock market value of a firm to the price of the

firm’s capital assets); furthermore, he found positive valuation effects of

dividends and cash holdings. However, these effects depend on the ownership

structure of the firm. Dividend payments have incremental positive valuation

effect for firms with entrenched owners while cash holdings have negative

valuation effect for this type of firms. Considering the endogenous nature of

17

firm policies, he found that firms operating in countries with poor investor

protections make low dividend payments, have high cash holdings, and have

low firm value, supporting the findings of La Porta, Lopez-de-Silanes,

Shleifer, and Vishny (2000a, 2002) and Dittmar et al. (2003). In addition, he

explained that investor protection mitigates the adverse effect of excess

control by forcing controlling shareholders to eject cash. High cash holding is

beneficial only if outside investor’s rights are well protected.

According to the dividend signaling, dividend change announcements activate

share returns because they convey information about management’s

assessment on firms’ future prospects. The evidence gives no support for a

positive relation between dividend change announcements and the market

reaction for French firms, and only a weak support for the Portuguese and the

UK firms(see Elisabete Vieira). The global results do not give support to the

assumption that dividend change announcements are positively related with

future earnings changes.

The role of expected cash flow volatility as a determinant of dividend policy

both theoretically and empirically was explored. It was exposed that, given

the existence of a stock-price penalty associated with dividend cuts, managers

rationally pay out lower levels of dividends when future cash flows are less

certain (see Michael Bradley). He confirmed that payout ratios are lower for

firms with higher expected cash flow volatility as measured by leverage, size

and property level diversification. Findings were reliable with information-

based explanations of dividend policy but not with agency cost theories.

The cross-sectional stock returns behavior on the A-share market of the

Shanghai Stock Exchange (SSE), which is segmented from world’s other

equity markets was explored. We estimate the effects of beta, firm size, book-

to-market equity ratio and a variable unique to the Chinese stock markets, the

proportion of firm’s floating (tradable) equity over total equity on SSE stocks

over the period 1993–2002. We find that smaller firms and value stocks

perform better (see Kie Ann Wong [2006]). Systematic risk is negatively

18

significant in down markets. The proportion of floating equity has no direct

effect on stock returns.

Jamshed Y.Uppal has attempt to analyzed episodes of market manipulation

and volatility and the ensuing regulatory intervention in two emerging South

Asian markets, India and Pakistan. These episodes conform well to the

Kane’s theoretical framework of regulatory dialectics representing the

interaction of financial and regulatory innovation. He observed a common

pattern of avoidance-reregulation-avoidance, triggered by changes in the

market and technological environment. Markets adapt to such changes in the

form of innovation, avoidance and circumvention of regulation. The resulting

conflict calls for a re-regulation response, which, however, is followed by

another round of avoidance.

Spin-off announcements affect bondholders in two possible ways.

Bondholders may profit from the increase in the total firm value that is caused

by a spin-off. On the other hand, they may also suffer from a wealth transfer

from bondholders to shareholders, because they lose part of the coinsurance

effect that occurs in diversified firms. This problem is studied by analyzing

daily stock and bond abnormal returns around spin-off announcements. Over

a three-day event window, they found statistically significant abnormal

returns of 3.07 percent for shareholders and 0.11 percent for holders of

straight bonds (see Chris Veld and Yulia Veld ). Both stock and bond

abnormal returns are higher for firms with lower interest and dividend

payouts. Stock abnormal returns are also higher for firms with higher pre-

spin-off leverage. Overall, we find that the firm value increase compensates

for the wealth transfer effect and that bondholders’ wealth is not reduced as a

result of spin-off.

Prof. Varadraj B. Bapat explains corporate bond market is an important

segment of financial market in terms of funds raised as well as potential for

future growth though is lightly researched. One of the two propositions on

impact of dividend changes is signaling hypothesis (Bhattacharya, 1979)

which suggests a positive effect on bond prices, on an announcement of

19

dividend increase; whereas the other one is wealth transfer hypothesis

(Handjinicolaou and Kalay, 1984) which proposes a negative impact on bond

prices due to extortion of wealth from bond holders. By studying the impact

of dividend policy decisions on Indian corporate bond prices, the paper

examines these hypotheses and contributes to the literature on payout policy.

Dividend increase and decrease announcements of 5% or more during a

period of 5 years from year 1997-98 to 2001-02 have been identified and

abnormal returns for bonds and stocks are computed. The analysis shows that

abnormal bond and stock returns are positive and are statistically significant

in the event-month in case of dividend increase. Prof. Varadraj B. Bapat

concluded that signaling hypothesis is found to hold in Indian corporate bond

market.

Wolfgang Bessler (1999) In an environment of asymmetric information,

banks face information externalities due to their role as intermediaries of

information. In particular, bank insiders will possess private information from

monitoring loan customers. Accordingly, outsiders may interpret changes in a

bank's financial policy as signals about the quality of its loan portfolio and to

the extent that the assets (loans) of different banks are viewed as similar, they

will interpret such signals as pertaining to non-announcing banks as well

leading to contagion effects. We test for the presence of contagion effects in

stock returns associated with announcements of dividend cuts by money-

center banks. We find that dividend cuts induce negative abnormal returns in

the stocks of non-announcing money-center banks and to a lesser extent in the

stocks of large regional banks. The observed contagion effects appear

consistent with informed rather than contagious panic behavior because these

effects are systematically related to risks that are common to all affected

banks.

Melanie Cao in this paper studies the valuation and incentive effects of non-

traded stocks and stock options in a continuous-time, intertemporal,

consumption-investment framework. In addition to the market portfolio and

the risk free asset, we introduce an industry index into the agent’s portfolio

20

choice set. This industry index is assumed to be highly correlated with the

stock to partly undo the trading restrictions. We find that the industry index

can help align the employee’s private valuation of the stock and options with

that of the market’s. Although the private valuation is still below the market’s,

it is higher than that when the index is not available. When the partial

correlation between the stock and the index is perfect, the impact of the

trading restriction can be completely nullified and the employee’s private

valuation of the stock and options coincides with the market’s. The

introduction of the hedging index also enriches the implications concerning

incentives and risk taking behavior.

Guglielmo Maria Caporale 2003 in her paper uses the tests of Robinson

(1994a) to analyze the degree of dependence in the intertemporal structure of

daily stock returns (defined as the first difference of the logarithm of stock

prices, where the series being considered is the S&P500 index). These tests

have several distinguishing features compared with other procedures for

testing unit (or fractional) roots. In particular, they have a standard null limit

distribution and they are the most efficient ones when carried out against the

appropriate alternatives. In addition, they allow one to incorporate the

Bloomfield (1973) exponential spectral model for the underlying I (0)

disturbances. The full sample, which comprises 17,000 observations, is first

divided in 10 subsamples of 1700 observations each. These are then grouped

two by two, and five by five; finally, the whole sample is considered. The

results indicate that the degree of dependence remains relatively constant over

time, with the order of integration of stock returns fluctuating slightly above

or below zero. On the whole, there is very little evidence of fractional

integration, despite the length of the series. Therefore, it appears that the

standard practice of taking first differences when modeling stock returns

might be adequate.

Andreas Oehler 2002 prior research documents that many investors

disproportionately hold on to losing stocks while selling stocks which have

gained in value. This systematic behavior is labeled the “disposition effect”.

21

The phenomenon can be explained by prospect theory’s idea that subjects

value gains and losses relative to a reference point like the purchase price, and

that they are risk-seeking in the domain of possible losses and risk-averse

when a certain gain is obtainable. Our experiments were designed to test

whether individual- level disposition effects attenuate or survive in a dynamic

market setting. We analyze a series of 36 stock markets with 490 subjects.

The majority of our investors demonstrate a strong preference for realizing

winners (paper gains) rather than losers (paper losses). We adopt different

reference points and compare the behavioral patterns across three main

trading mechanisms, i.e. rules of price formation. The disposition effect is

greatly reduced only within high pressure mechanisms like a dealer market

when the last price is assumed as a reference point which is a more market

driven (external) benchmark. If disposition investors use the purchase price as

a reference point which is a more mental-accounting driven (internal)

benchmark they die hard in all market settings. Interestingly, our markets do

not collapse or become illiquid by disposition investors’ reluctance to trade. A

main reason for this is the coexistence of two or more groups of investors, e.g.

momentum traders and disposition investors.

Samy Ben Naceur 2003 study the dividend policy of 48 firms listed on the

Tunisian Stock Exchange during 1996-2002 periods. The study tests whether

managers of Tunisian listed firms smooth their dividends or not. Beside, the

study outlines the main determinants that may drive the dividend policy of

Tunisian quoted firms. To answer the first question, we use Lintner’s model

in a dynamic setting. The results clearly demonstrate that Tunisian firms rely

on both current earnings and past dividends to fix their dividend payment.

However, the study shows that dividends tend to be more sensitive to current

earnings than prior dividends. To find out the determinants of dividend

policy, dynamic panel regressions have been performed. First, profitable

firms with more stable earnings can afford larger free cash flows and thus,

pay larger dividends. Furthermore, they distribute larger dividends whenever

they are growing fast. However, neither the ownership concentration nor the

22

financial leverage seems to have any impact on dividend policy in Tunisia.

Besides, the liquidity of stock market and size negatively impacts the

dividend payment. The results are somewhat robust to different specifications.

Samy Ben Naceur 2003 since few decades, a wide theoretical debate is

concerned with the fundamental relationship between financial development

and economic growth. An efficient financial system leads to a sustainable

economic growth. In this study, we are interested especially with stock

markets as a main component of the financial system according to the

increasing role of financial markets in economies. So, their evolution plays an

important role in economic growth. We shed some light on the

macroeconomic determinants which must have an important influence on

stock markets development. It is recognized that real or financial variables

such as real income, saving rate, credit to private sector, M3, value traded,

turnover, etc. could have a significant impact on market capitalization. The

empirical study is conducted using an unbalanced panel data from twelve

MENA region countries. Econometric issues are based on estimation of some

fixed and random effects specifications. With such specifications in mind,

peculiarities of MENA region countries are detected as well as

differentiations among them. Thus, differences in market capitalization are

explained. The empirical expected results must reinforce the idea which

suggests the important role of economic development in promoting stock

market development. Explaining power of variables such as real income,

saving rate, inflation, financial intermediary development and stock market

liquidity is confirmed. Banks and stock markets seem to be complements

instead of substitutes.

Samy Ben Naceur 2005 since few decades, a wide theoretical debate is

concerned with the fundamental relationship between financial development

and economic growth as well as the separate impact of banks on growth and

financial markets on growth. Recent studies shed some light on the

simultaneous effect of banks and financial development on growth. The

empirical study is conducted using an unbalanced panel data from ten MENA

23

region countries. Econometric issues will be based on estimation of a

dynamic panel model with GMM estimators. Thus, peculiarities of MENA

region countries will be detected. The empirical results reinforce the idea of

no significant relationship between banking and stock market development,

and growth. The association between stock markets and growth is even

negative after controlling for bank development. This lack of relationship

must be linked either to underdeveloped financial systems in the MENA

region that hamper economic growth or to unstable growth rates in the region

that affect the quality of the association between finance and growth.

Moreover, in most transition economies the stock markets are very thin. This

may lead to excessively volatile share prices. According to Singh (1997),

stock price volatility may seriously hamper economic development.

Putu Anom Mahadwartha’s examines the relationship of financial policy

(dividend and leverage) influenced managerial ownership. Managerial

ownership as dependent variable regressed with dividend and leverage policy

that already separate the effect of agents and insiders wealth. Logit Model is

use to examine the relationship because managerial ownership proxy by

dummy variable. Hosmer-Lemeshow and Andrews Goodness-Of-Fit test used

to conclude the model fitted. Result showed a significant relationship that

financial policy influenced probability firm engages in managerial ownership

program. Dividend policy is a substitute for managerial ownership. The lower

dividend level will increase the probability of the firm engage in managerial

ownership program and still maintain the effectiveness of reducing agency

cost of equity. The lower leverage level will increase the probability of the

firm engage in managerial ownership program to multiply the effect of

reduced agency cost of debt with the reduction in agency cost of equity.

The paper is expansion from Mahadwartha (2002b) that is use Logit model to

test the predictability power of leverage policy and dividend policy to

managerial ownership policy. Leverage and dividend variable used already

divided the interest of inside shareholders and outside shareholders. The paper

also uses a modification on managerial ownership variable with lead one year

24

after (t+1), an addition of control variable (current assets) to increase

predictability model. The research period is from 1993 until 2001. The

research argues that leverage policy and dividend policy have higher effect on

managerial ownership in t+1 than t. The result shows consistency regarding

predictability power of leverage policy and dividend policy to managerial

ownership. Also shows that the predictability power is higher than

Mahadwartha (2002b). The relationship between leverage and dividend to

managerial ownership is negative with higher magnitude than Mahadwartha

(2002b). The results consistent with Agency Theory prediction, that there is

substitution between policies in bonding and monitoring mechanism to

control agency conflict.

The paper analyzes the relationship between managerial ownership with

leverage policy and dividend policy (balancing model of agency theory) and

interdependency of dividend and leverage (contracting model of agency

theory). The research also test collateral and growth hypothesis. Leverage and

dividend policy variables used in this study are already excluded outside

shareholders interest. Results show that managerial ownership as self bonding

and self monitoring in controlling agency conflict concern on the balancing

model of agency cost. Agency theory variables (dividend and leverage)

partially explain interdependency between leverage and dividend policies.

Relationships between dividend influenced leverage significantly explained

by contracting model of dividend but relationship between leverage

influenced dividend fail explained by balancing model of agency cost. The

results also support collateral and perquisites hypotheses. In general agency

costs that occurred in Indonesia are agency costs of debt.

Jeffrey Eugene Nisbett 2003 in this study has attempted to look at the

dividend policies of six public companies in St Kitts and Nevis guided by the

finance literature produced by Lintner, Lease, Glen and others. Our study has

shown that the St Kitts and Nevis companies display dividend payout ratios

which are not as low as those reported by Glen et al [3] for emerging markets

but which are not as high as those which Lease et al [14] reported in respect

25

of firms in the United States. Payout rates for St Kitts and Nevis public

companies averaged 52.88 per cent. This, it is felt, is due to two significant

factors which are perhaps interrelated. In the first place, during most of the

period studied, there was no market for trading shares until the ECSE was

established in 2001. Secondly, and somewhat related to the first factor, there

is the preference by companies to use retained earnings as a source of finance,

consistent with the theories of corporate finance that suggest that firms tend to

utilize the cheapest sources of finance first.

It has also been noted that the dividend versus earnings patterns for the

companies show greater variability in earnings. This is consistent with the

trends in other markets as has been observed in the finance literature on

emerging markets by Glen et al. and in developed markets by Lease et al.

Kai Li in this paper examines how informational asymmetries affect firms’

dividend policies. We find that, controlling for other factors that determine

dividend policy, firms more subject to information asymmetry are less likely

to pay, to initiate, or to increase dividends, and pay a lower amount of

dividends. We show that our main inferences are not driven by the sample

used in our study and remain the same after accounting for the changing

composition of payout over the sample period, the increasing importance of

institutional shareholdings, and the catering incentives. We conclude that our

evidence does not support the signaling view of dividends, but is strongly

consistent with the pecking order view of dividends.

In this paper, Deniz lgan 2004 develop a model involving both

corporatenance and market microstructure elements to analyze the impact of

shareholder need for liquidity on the rm™s decision to pay dividends.

Shareholders face a trade-o¤ between expected returns and adverse selection

costs. In equilibrium, some rms pays dividends and has lower growth

prospects but a more liquid market. Other rms option is to have a better

growth outlook by keeping the free cash-flow in order to invest if an

opportunity presents itself. The decision to pay dividends depends directly on

26

how much importance the rm™s manager attaches to

shareholders™objectives and on the liquidity of dividend paying –rms. We

then test the implications of our model closely following Fama & French

(2001), with the exception that we add measures for liquidity and shareholder

power to the list of explanatory variables as suggested by our theory. Firms

are more likely to pay dividends if they have more liquid stocks and if their

shareholders enjoy more power.

H. Kent Baker 2005 reports the results of a 2004 survey from managers of

dividend-paying Norwegian firms listed on the Oslo Stock Exchange about

their views on dividend policy. Specifically, we identify the most important

factors in making dividend policy decisions and managers’ views about

various dividend-related issues. The most important determinants of a firm’s

dividend policy are the level of current and expected future earnings, stability

of earnings, current degree of financial leverage, and liquidity constraints. No

significant correlation exists between the overall rankings of factors

influencing dividend policy between Norwegian and U.S. managers.

Norwegian managers express mixed views about whether a firm’s dividend

policy affects firm value. Respondents point to the possible role of dividend

policy as a signaling mechanism. No support exists for the tax-preference

explanation for paying dividends.

An empirical research has been made about managers of firms that

consistently pay cash dividends to determine their views about dividend

policy, the relationship between dividend policy and value, and four common

explanations for paying dividends. The evidence shows that managers stress

the importance of maintaining dividend continuity and widely agree that

changes in dividends affect firm value. Managers give the strongest Support

to a signaling explanation for paying dividends, weak to little support for the

tax-preference and agency cost explanations, and no support to the bird-in-

the-hand explanation (see H.Kent Baker [2002]). This study provides

evidence about how managers view dividend life cycles and residual dividend

policy.

27

Jennifer L. Blouin 2003 the Jobs and Growth Tax Relief Reconciliation Act

of 2003 reduces the maximum statutory tax rate on dividends from 38.1

percent to 15 percent. The purpose of this paper is to analyze dividend

distributions in the quarter immediately following passage of the Act to assess

the extent to which companies increased their dividend payments in response

to the lower tax rate. We find an overall increase in dividend payments

following enactment. In addition, we find that a firm’s dividend increases are

positively correlated with the percentage of its shares held by individuals.

However, the association only exists only for non-financial firms and is

concentrated among a few firms that made large, special dividends.

Alon Bray 2004 surveys 384 financial executives and conduct in depth

interviews with an additional 23 to determine the factors that drive dividend

and share repurchase decisions. Our findings indicate that maintaining the

dividend level is on par with investment decisions, while repurchases are

made out of the residual cash flow after investment spending. Perceived

stability of future earnings still affects dividend policy as in Lintner (1956).

However, fifty years later, we find that the link between dividends and

earnings has weakened. Many managers now favor repurchases because they

are viewed as being more flexible than dividends and can be used in an

attempt to time the equity market or to increase EPS. Executives believe that

institutions are indifferent between dividends and repurchases and that payout

policies have little impact on their investor clientele. In general, management

views provide little support for agency, signaling, and clientele hypotheses of

payout policy. Tax considerations play a secondary role.

Using data on corporate profits forecasts from the Survey of Professional

Forecasters, Sean D. Campbell 2005 decompose real stock returns into a

fundamental news component and a return news component and analyze the

effects of the Great Moderation on each. Empirically, the response of each

component of real stock returns to the Great Moderation has been quite

different. The volatility of fundamental news shocks has declined by 50%

since the onset of the Great Moderation, suggesting a strong link between

28

underlying fundamentals and the broader macro economy. Alternatively, the

volatility of return news shocks has remained stable over the Great

Moderation period. Since the bulk of stock market volatility is attributable to

return shocks, the Great Moderation has not had a significant effect on stock

return volatility. These empirical findings are shown to be consistent with

Campbell and Cochrane’s (1999) habit formation asset pricing model. In the

face of a large decline in consumption volatility, the volatility of fundamental

news shocks declines while the volatility of return shocks stagnates.

Ultimately, the effect of a Great Moderation in consumption volatility on

overall stock return volatility in the habit formation model is slight.

Michael Bradley 1998 explores the role of expected cash flow volatility as a

determinant of dividend policy both theoretically and empirically. Our simple

one period model demonstrates that, given the existence of a stock-price

penalty associated with dividend cuts, managers rationally pay out lower

levels of dividends when future cash flows are less certain. The empirical

results use a sample of REITS from 1985-1992 and confirm that payout ratios

are lower for firms with higher expected cash flow volatility as measured by

leverage, size and property level diversification. These results are consistent

with information-based explanations of dividend policy but not with agency

cost theories.

Larry R. Gorman investigate whether the changes in profitability and risk for

firms that resume dividend payments are more like the changes observed

around dividend initiations or dividend increases. We find that firms that

resume paying dividends are in the midst of a long-term trend of positive

stock price performance. The return on assets of firms that resume paying

cash dividends increases leading up to the event and for one to two years

thereafter. We also find a significant and apparently permanent reduction in

stock return volatility following the resumption of regular cash dividends. Our

results indicate that the changes in profitability and risk around dividend

resumption are most similar to those observed around dividend initiation.

29

In this paper Edith S. Hotchkiss 2003 provides new evidence the existence of

dividend clienteles. Our approach is to directly examine individual

institutional shareholders’ preferences for dividend paying stocks based on

the characteristics of stocks held in their portfolio. Many institutions follow

persistent investment styles, maintaining relatively high or low dividend yield

portfolios over time. Higher dividend yield firms tend to attract “high yield”

investors, which we define as institutions that hold portfolios of higher

dividend yield stocks. Stock price reactions to announcements of dividend

increases are related to characteristics of the institutions holding the stock and

are generally consistent with predictions of the clientele hypothesis. We also

observe significant changes in characteristics of institutions holding the stock

around dividend changes; dividend increases (decreases) are associated with

increased (decreased) holdings by institutions that appear to prefer dividends

based on their prior portfolio choices. Finally, we examine the trading

behavior of individual institutions and find that institutions that prefer

dividends have a significantly greater probability of increasing (decreasing)

their holdings in response to a dividend increase (decrease). However, we find

little evidence to support the idea that it is the tax status of the investor that

drives clientele behavior.

J. Bradfor De Long 1993 studies “excess volatility” in long-run British stock

prices over the period from 1870–1990. We find that the British stock market

does exhibit “excess volatility” if the pre-WWI period is included in the

sample. British price/dividend ratios before World War I were low relative to

those of other nations or to post-WWI Britain, suggesting that pre-war

investors were extraordinarily suspicious of those equities quoted on the

market. This fear of equities may have caused the British stock market to

perform poorly as a social capital allocation mechanism before World War I,

and may have played a role in British industrial decline.

Shamila Jayasuriya 2002 uses an asymmetric GARCH methodology to

examine the effect of stock market liberalization on stock return volatility for

fifteen emerging markets for the period December 1984 – March 2000. We

30

construct a long period of liberalization that captures all identified market

openings for each emerging market, and study the change in volatility both in

and after the liberalization period. We find that volatility may decrease,

increase, or remain unchanged due to liberalization. In addition, countries that

experienced higher post- liberalization volatility can be differentiated by

market characteristic s such as lower market transparency, lower investor

protection, and higher market exit restrictions.

Martin D. D. Evans 2005 in this paper examines the extent to which swings in

stock prices can be related to variations in the discounted value of expected

future dividends when investors face uncertainty about their future behavior. I

develop an econometric model that accounts for the instability of U.S.

dividend growth and discount rates during the past 120 years. Estimates of the

model reveal that changing forecasts of future dividend growth account for

more than 90% of the predictable variations in dividend-prices. The estimates

also imply that instability in the dividend and discount rate processes

contribute significantly to the predictability of long-horizon stock returns.

Data on corporate announcements of Chinese firms over 1991-2003 allow us

to examine the preference for and determinants of cash and stock dividends.

The results indicate that Chinese public investors prefer stock dividends over

cash dividends, while cash dividends are preferred by large non-tradable

shareholders, but not by public investors generally Louis T. W. Cheng 2006.

Stock dividends, which do not require explicit cash outflow from the firm, are

positively related to higher earnings and higher return on assets, supporting

the signaling hypothesis of dividend policy. Our results provide strong

evidence for the hypothesis that stock and cash dividends are substitutes. In

an imperfect market, these results have some implications for government

regulation of financial markets.

Michael Bremman 1997 the determination of stock prices and equilibrium

expected rates of return in a general equilibrium setting is still imperfectly

understood. In particular, as Grossman and Shiller (1981) and others have

argued, stock returns appear to be too volatile given the smooth process for

31

dividends and consumption growth. Mehra and Prescott (1985) claim that this

smoothness in consumption and dividend growth gives rise to an “equity

premium paradox” since it makes it impossible to explain the equity risk

premium with a risk aversion parameter of less than an implausible 35. This

paper reconciles the apparent smoothness of aggregate dividends and the

volatility of observed stock prices by developing a model of stock prices in a

dynamic general equilibrium setting in which learning is important.

Dividends, which are one component of the aggregate consumption

endowment, are assumed to follow a stochastic process with a mean-reverting

drift that is not directly observable by the representative agent but must be

estimated from the realized growth rates of dividends and aggregate

consumption. The stock price-dividend ratio is shown to depend on the

current estimate of the dividend growth rate as well as on the level of un-

certainty about the true growth rate. This non observability of the growth rate

of dividends introduces an element of learning into the stock valuation

process which is shown to increase the volatility of the stock price and

therefore reduce the level of risk aversion required to explain the equity

premium. The model is calibrated to the observed joint dividend and

consumption process for the US, and is shown to yield an interest rate and

stock price process that conform closely to the stylized facts for US capital

markets.

32

C h a p t e r 3

HYPOTHESIS AND DATA METHODOLOGY

Hypothesis

H1: There is a positive and significant abnormal return at the announcement of

a dividend.

H2: There is a negative and significant abnormal return at the announcement

of a dividend.

Data and Methodology

Event announcement dates for both cash and stock dividends (bonus issues)

were collected from web site of Karachi Stock Exchange which managed the

stock market officially during the period when daily stock returns were

available. Firms that were listed in the stock exchange during this period had

to officially inform the management of their dividend payouts both in cash

and in stock. The date of that communication constituted the event date. In

general, that date coincided with a board of directors’ meeting since the

decision presupposed approval by the board.

Cash dividend payouts are usually announced semi-annually by the larger

public firms and annually by the smaller firms in the Karachi Stock Exchange

(few quarterly dividend announcements were observed during the sample

period). Other types of announcements coinciding with confounding dividend

announcements were very rare during the sample period. For example, the

takeover of a public firm, stock split and share repurchases. These are

restricted by the regulatory bodies. Infrequently, dividend announcements

were accompanied by real-time earnings announcements. However, no

separate record of these announcements was kept and given the fairly limited

number of usable observations in my analysis I have decide on not to discard

any observations on the basis of other contemporary new releases. In any

case, the statistical significance of the market reaction to the events under

consideration is similar using both the parametric and non-parametric tests,

33

providing reasonable assurance that the documented market reactions are not

the result of a few outliers that are potentially confounded by coincident

earnings announcements.

A total of 161 announcements by 37 different firms took place during the

period under study. Of these, a large number of cash dividends represented an

increase over prior period cash dividends and comprise the dividends sample

employed period. Further announcements of stock dividend by different firms

took place in the sample period and comprise the stock dividend samples.

It should be noted that all firs in the Karachi Stock Exchange have highly

concentrated ownership structures. As discussed earlier, few top firms out of

100 index listed at the Karachi Stock Exchange over the sample period are

included in samples of dividends (37 firms out of 100 indexes). Therefore,

our sample firm’s ownership structure is substitutes well by the wider

ownership characteristics of the population. KSE regulations mandate that a

single ownership interest may not own more than 70% of the voting class of

securities of any public firm. Further, the four largest shareholders

collectively may not own more than 75% of the shares, ensuring that at least

25% of the voting stock is dispersed among the public. Importantly, in all

firms that are traded in the KSE the four largest investors own at least 50% or

more of the outstanding stock; that percentage routinely fluctuates between

65% and 75%. This suggests very little cross-sectional variation in ownership

concentration in the KSE. Unfortunately, such uniformity forbids us from

performing any meaningful statistical tests using differences in ownership

structure to differentiate between alternative explanations for dividend

changes across firms.

For completion of this study I used an electronic database with daily stock

returns of all firms traded in the Karachi Stock Exchange during the period

developed by one of the author. Given the lack of liquidity for the period

examined, in certain days no trading took place for some of the stocks. In

such cases I assumed that the closing price was the mid-point between the

bids and ask prices for that day. The shareholder wealth effect for the

34

dividend announcements was determined using standard event-study

methodology based on the single-factor market model (using risk adjusted

returns), as well as the market-adjusted model (assuming a beta of 1 for all

firms). Specifically, the assessment of announcement-related abnormal

returns follows standard event-study methods (e.g., Dennis and McConnell,

(1986) and was carried out as follows. First, each firm’s returns were assumed

to follow the single-factor market model,