municipal secondary market disclosure … · 13033f mp 2 13033f mw 7 series b 130795uf2 13033f7r5...

TRANSCRIPT

MUNICIPAL SECONDARY MARKET DISCLOSURE

INFORMATION COVER SHEET This cover sheet should be sent with all submissions made to the Municipal Securities Rulemaking Board and Nationally Recognized Municipal Securities Information Repositories (NRMSIRS) pursuant to Securities and Exchange Commission rule 15c2-12 or any analogous state statute. Issuers’ and/or Other Obligated Person’s Names: California Health Facilities Financing Authority, California

Adventist Health System/West (CHFFA) California Statewide Communities Development Authority Adventist Health System/West (CSCDA) Multnomah County Hospital Facilities Authority

CUSIP Numbers:

Description of Material Event Notice/Financial Information (Check One): 1. Principal and interest payment delinquencies 2. Non-payment related defaults 3. Unscheduled draws on debt service reserves reflecting financial difficulties 4. Unscheduled draws on credit enhancements reflecting financial difficulties 5. Substitution of credit or liquidity providers, or their failure to perform 6. Adverse tax opinions or events affecting the tax-exempt status of the security 7. Modifications to rights of security holders 8. Bond calls 9. Defeasances 10. Release, substitution or sale of property securing repayment of the securities 11. Rating changes 12. Failure to provide annual financial information as required 13. Other material event notice 14. X Financial information (not to be filed with the MSRB): Please check all appropriate boxes

CAFR 1: a. X includes Annual Financial Information __does not include Annual Information b. Audited? Yes X No _

Operating Data Period Covered: 12 months ended December 31, 2011

I hereby represent that I am authorized by the Obligated Person to distribute this information publicly:

Signature:

Name: Rodney Wehtje Title: Vice President and Treasurer

Employer: Adventist Health System/West

Address: 2100 Douglas Blvd.

City, State, and Zip Code: Roseville, CA 95661

Voice Telephone Number: 916.781.4786

CHFFA AHS/W 2003 Series A CSCDA AHS/W 2007 CHFFA AHS/W 2009 Series C

13033F MN 7 13033F MV 9 Series A 130795US4 13033F7Q7 13033F7W4 13033F MP 2 13033F MW 7 Series B 130795UF2 13033F7R5 13033F7X2 13033F MQ 0 13033F MX 5 13033F7S3 13033F7Y0 13033F MR 8 13033F MY 3 CHFFA AHS/W 2009 13033F7T1 13033F7Z7 13033F MS 6 13033F MZ 0 Series A 13033LBE6 13033F7U8 13033F8A1 13033F MT 4 13033F NA 4 Series B 13033LBC0 13033F7V6 13033F8B9

CSCDA AHS/W 2005 Series A Multnomah County, OR 2009A

130911 U40 130911 V23 62551P BQ9 130911 U57 130911 V31 62551P BR7 130911 U65 130911 V49 62551P BS5 130911 U73 130911 U99 130911 U81

Adventist Health System/West Annual Report: December 31, 2011 Per Continuing Disclosure Certificates:

CHFFA 2003 Series A CSCDA 2005 Series A CSCDA 2007 Series A and B CHFFA 2009 Series A, B and C Multnomah County, OR HFA 2009 Series A

Certificate Reference Requirement Location Section 4(1) Audited combined financial statement Tab “AH 2011 Audit” Section 4(2) a. Debt Service Coverage and Capitalization Tab “Financial Ratios”

b. Summary Listing of Hospitals Tab “Operating/Utilization Statistics” c. Combined Summary of Revenues & Expenses Tab “AH 2011 Audit” Note that 6.4% of Revenues are from entities outside of the Obligated Group d. Combined Balance Sheet Tab “AH 2011 Audit” Note that 3.7% of Assets are from entities outside of the Obligated Group e. Payor Mix Tab “Operating/Utilization Statistics” f. Utilization Statistics Tab “Operating/Utilization Statistics” g. Operating Statistics Tab “Operating/Utilization Statistics”

Section 4(3) Combining financial statements Tab “AH 2011 Audit”

Audited Combined Financial Statements and Supplementary Information ADVENTIST HEALTH December 31, 2011 Audited Combined Financial Statements Report of Independent Auditors .................................................................................................................... 1 Combined Balance Sheets ............................................................................................................................. 2 Combined Statements of Operations and Changes in Net Assets.................................................................. 4 Combined Statements of Cash Flows ............................................................................................................ 6 Notes to Combined Financial Statements ...................................................................................................... 7 Supplementary Information Report of Independent Auditors on Supplementary Information ................................................................ 24 Combining Balance Sheet ........................................................................................................................... 25 Combining Statement of Operations and Changes in Net Assets ................................................................ 29

Ernst & Young LLP Sacramento Office 2901 Douglas Boulevard Suite 300 Roseville, California 95661

Tel: +1 916 218-1900 Fax: +1 916 218-1999 www.ey.com

A member firm of Ernst & Young Global Limited

-1-

REPORT OF INDEPENDENT AUDITORS The Board of Directors Adventist Health Roseville, California We have audited the accompanying combined balance sheets of Adventist Health (the “System”) as of December 31, 2011 and 2010, and the related combined statements of operations and changes in net assets, and cash flows for the years then ended. These financial statements are the responsibility of the System’s management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. We were not engaged to perform an audit of the System’s internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the System’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion. In our opinion, the financial statements referred to above present fairly, in all material respects, the combined financial position of Adventist Health at December 31, 2011 and 2010, and the combined results of its operations and changes in net assets, and its cash flows for the years then ended, in conformity with accounting principles generally accepted in the United States. As discussed in Note P to the combined financial statements, the System changed the presentation and classification of the provision for bad debts on the combined statements of operations and changes in net assets as a result of the adoption of Accounting Standards Update No. 2011-07, Presentation and Disclosure of Patient Service Revenue, Provision for Bad Debts, and the Allowance for Doubtful Accounts for Certain Health Care Entities. April 23, 2012

COMBINED BALANCE SHEETS(In thousands of dollars)

ADVENTIST HEALTH

December 312011 2010

ASSETS

CURRENT ASSETSCash and cash equivalents 250,119$ 227,514$ Marketable securities 45,393 19,898 Assets whose use is limited:

Board-designated 78 82 Held by trustees 22,472 21,079 Donor-restricted 56 56

Patient accounts receivable, net of allowance foruncollectible accounts of approximately $78,000 and$73,000 at December 31, 2011 and 2010, respectively 357,638 323,906

Receivables from third-party payors 7,957 33,026 Other receivables 27,280 39,388 Inventories 42,594 38,850 Prepaid expenses and other current assets 23,711 20,448

TOTAL CURRENT ASSETS 777,298 724,247

OTHER ASSETSNotes receivable 16,658 20,169 Marketable securities 472,564 473,978 Assets whose use is limited:

Board-designated 102,563 107,219 Held by trustees 231,242 144,992 Donor-restricted 20,429 19,225

Long-term investments 25,004 19,814 Deferred financing costs 7,373 7,464 Other long-term assets 38,905 20,508

TOTAL OTHER ASSETS 914,738 813,369

PROPERTY AND EQUIPMENT, net 1,397,999 1,324,761

TOTAL ASSETS 3,090,035$ 2,862,377$

-2-

December 312011 2010

LIABILITIES AND NET ASSETS

CURRENT LIABILITIESAccounts payable 86,885$ 90,008$ Accrued compensation and related payables 146,738 136,869 Accrued interest 11,404 11,594 Liabilities to third-party payors 58,151 88,767 Other current liabilities 40,772 40,553 Short-term financing 152 4,576 Current maturities of long-term debt 25,622 21,189

TOTAL CURRENT LIABILITIES 369,724 393,556

LONG-TERM DEBT, net of current maturities 1,048,825 936,173

OTHER NONCURRENT LIABILITIES 292,078 266,484 TOTAL LIABILITIES 1,710,627 1,596,213

NET ASSETSUnrestricted 1,322,034 1,212,589 Temporarily restricted 51,412 48,350 Permanently restricted 5,962 5,225

TOTAL NET ASSETS 1,379,408 1,266,164

TOTAL LIABILITIES AND NET ASSETS 3,090,035$ 2,862,377$

See notes to combined financial statements.

-3-

COMBINED STATEMENTS OF OPERATIONS AND CHANGES IN NET ASSETS(In thousands of dollars)

ADVENTIST HEALTH

Year Ended December 312011 2010

UNRESTRICTED REVENUES, GAINS, AND SUPPORTNet patient service revenue 2,598,941$ 2,497,128$ Less provision for bad debts 113,865 95,761

Net patient service revenue less provision for bad debts 2,485,076 2,401,367

Premium revenue 22,779 24,497 Other revenue 138,695 129,580 Net assets released from restrictions for operations 6,759 7,503

TOTAL UNRESTRICTED REVENUES,GAINS, AND SUPPORT 2,653,309 2,562,947

EXPENSESEmployee compensation 1,365,001 1,254,195 Professional fees 233,288 200,608 Supplies 395,525 372,874 Purchased services and other 407,658 435,982 Interest 35,747 32,092 Depreciation 118,760 103,808

TOTAL EXPENSES 2,555,979 2,399,559

EXCESS OF REVENUES OVER EXPENSESFROM CONTINUING OPERATIONS 97,330$ 163,388$

-4-

2011 2010

UNRESTRICTED NET ASSETSExcess of revenues over expenses from

continuing operations (from page 4) 97,330$ 163,388$ Change in net unrealized gains and losses

on other-than-trading securities 6,967 14,802 Donated property and equipment 688 461 Net assets released from restrictions for capital additions 6,069 7,703

INCREASE IN UNRESTRICTED NET ASSETSBEFORE DISCONTINUED OPERATIONS 111,054 186,354

Net (loss) gain from discontinued operations (1,609) 3,701 Loss on disposal - (790)

INCREASE IN UNRESTRICTED NET ASSETS 109,445 189,265

TEMPORARILY RESTRICTED NET ASSETSRestricted gifts and grants 15,770 14,304 Net realized and unrealized gains on investments 123 162 Change in value of split-interest agreements (3) 145 Net assets released from restrictions (12,828) (15,206)

INCREASE (DECREASE) IN TEMPORARILYRESTRICTED NET ASSETS 3,062 (595)

PERMANENTLY RESTRICTED NET ASSETSRestricted gifts and grants 10 126 Net realized and unrealized gains on investments 727 55 Other - (187)

INCREASE (DECREASE) IN PERMANENTLYRESTRICTED NET ASSETS 737 (6)

INCREASE IN NET ASSETS 113,244 188,664

NET ASSETS, BEGINNING OF YEAR 1,266,164 1,077,500

NET ASSETS, END OF YEAR 1,379,408$ 1,266,164$

Year Ended December 31

See notes to combined financial statements.

-5-

COMBINED STATEMENTS OF CASH FLOWS(In thousands of dollars)

ADVENTIST HEALTHYear Ended December 31

2011 2010

OPERATING ACTIVITIESChange in net assets 113,244$ 188,664$ Adjustments to reconcile increase in net assets to net cash

provided by operating activities of continuing operations:Loss (gain) from discontinued operations and on disposal 1,609 (2,911) Depreciation 118,760 103,808 Provision for bad debts 113,865 95,761 Provision for loss on notes receivable 5,375 5,423 Net gain on investments (23,713) (24,530) Net loss on sale of property and equipment 4,060 631 Increase in net patient accounts receivable (147,597) (118,793) Increase in other assets (14,552) (16,760) Decrease in net liabilities to third-party payors (5,569) (27,658) Increase (decrease) in other liabilities 31,163 (15,754) Other (402) (3,851)

NET CASH PROVIDED BY OPERATING ACTIVITIESOF CONTINUING OPERATIONS 196,243 184,030

INVESTING ACTIVITIESPurchases of property and equipment (193,605) (182,932) Proceeds from sale of property and equipment 313 59 Issuance of notes receivable (6,195) (21,559) Collections on notes receivable 5,793 2,366 Purchases of investments, net (90,238) (11,177)

NET CASH USED IN INVESTING ACTIVITIESOF CONTINUING OPERATIONS (283,932) (213,243)

FINANCING ACTIVITIESProceeds from issuance of short-term financing 15,820 23,823 Payments on short-term financing (20,245) (59,802) Proceeds from issuance of long-term debt 198,104 72,093 Payments on long-term debt (81,030) (69,611) Expenditures for deferred financing costs (478) -

NET CASH PROVIDED BY (USED IN) FINANCINGACTIVITIES OF CONTINUING OPERATIONS 112,171 (33,497)

CASH (USED IN) PROVIDED BY DISCONTINUED OPERATIONS (1,877) 45

INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS 22,605 (62,665)

CASH AND CASH EQUIVALENTS, BEGINNING OF YEAR 227,514 290,179

CASH AND CASH EQUIVALENTS, END OF YEAR 250,119$ 227,514$

See notes to combined financial statements.

-6-

NOTES TO COMBINED FINANCIAL STATEMENTS (In thousands of dollars) ADVENTIST HEALTH

-7-

NOTE A – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES Reporting Entity and Principles of Combination – Adventist Health System/West (Adventist Health or the “System”) is a California not-for-profit religious corporation that controls and operates hospitals and other health care facilities in the Western United States. Many of the hospitals now controlled and operated by Adventist Health were formerly operated by various conferences of the Seventh-day Adventist Church (the “Church”). The obligations and liabilities of Adventist Health and its hospitals and other health care facilities are neither obligations nor liabilities of the Church or any of its other affiliated organizations. The combined financial statements include the accounts of the following entities, which operate or previously operated under the business name of Adventist Health:

Adventist Health (Corporate Office) - Roseville, California Adventist Health Physicians Network - Roseville, California Adventist Medical Center - Hanford, California Adventist Medical Center - Portland, Oregon Adventist Medical Center - Reedley, California Castle Medical Center - Kailua, Hawaii Central Valley General Hospital - Hanford, California Feather River Hospital - Paradise, California Glendale Adventist Medical Center - Glendale, California Howard Memorial Hospital - Willits, California Paradise Valley Hospital - Roseville, California St. Helena Hospital Clear Lake - Clearlake, California St. Helena Hospital Napa Valley - St. Helena, California San Joaquin Community Hospital - Bakersfield, California Simi Valley Hospital - Simi Valley, California Sonora Regional Medical Center - Sonora, California South Coast Medical Center - Roseville, California Southern California Medical Foundation - Roseville, California Tillamook County General Hospital - Tillamook, Oregon Ukiah Valley Medical Center - Ukiah, California Walla Walla General Hospital - Walla Walla, Washington Western Health Resources - Roseville, California White Memorial Medical Center - Los Angeles, California

The entities that are included in the combined financial statements are organized as not-for-profit corporations under the laws of the state in which they operate and most are tax-exempt organizations under §501(c)(3) of the Internal Revenue Code. The Board of Directors (the “Board”) of Adventist Health and/or Adventist Health management constitutes the membership and/or serves as the legal board of the individual hospital corporations. All material inter-company transactions have been eliminated in combination.

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-8-

NOTE A – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued Cash and Cash Equivalents – Cash and cash equivalents consist primarily of unrestricted readily marketable securities with original maturities not in excess of three months when purchased and net deposits in demand accounts. Cash deposits are federally insured in limited amounts. Inventories – Inventories are stated at the lower of cost or market as determined on a first-in, first-out basis. Marketable Securities – Marketable securities, stated at fair market value, consist primarily of United States (US) government treasury and agency securities and corporate notes, which are readily marketable and are designated as other-than-trading. Investment income or loss (including interest, dividends, and realized gains and losses on investments) is included in the excess of revenues over expenses unless the income or loss is restricted by donor or law. Unrealized gains and losses, calculated using the specific identification method, are excluded from the excess of revenues over expenses. Securities with remaining maturity dates of one year or less as of the balance sheet date are classified as current. Assets Whose Use Is Limited – Certain System investments are limited as to use through Board resolution, provisions of contractual arrangements with third parties, terms of indentures, self-insurance trust arrangements, or donors who restrict the use of specific assets. The Board and certain hospital boards have resolved to fund the replacement and expansion of depreciable capital assets but may, at their discretion, use these funds for other purposes. Assets that are expected to be expended within one year are classified as current, including board-designated assets that are available and periodically borrowed for working capital needs. Split-interest Agreements – The System is the trustee and beneficiary of various split-interest agreements. The carrying amounts of the System’s split-interest assets are included with investments held by trustee and donor-restricted investments and include marketable securities and real estate. Trust assets are initially recognized at fair market value and subsequently reviewed for impairment on an annual basis. Assets under split-interest agreements were $25,060 and $24,083 at December 31, 2011 and 2010, respectively. Trust obligations are reported as liabilities at their discounted estimated present value using actuarially-determined life expectancy tables. Discount rates range between approximately 6% to 10%. Liabilities under split-interest agreements were $7,721 and $9,239 at December 31, 2011 and 2010, respectively. Deferred Financing Costs – Direct financing costs are deferred and amortized over the life of the financings using the effective-interest method. Property and Equipment – Property and equipment are reported on the basis of cost, except for donated items, which are recorded as an increase in unrestricted net assets based on fair market value at the date of the donation. During the period of construction, the System capitalizes expenditures that materially increase values, change capacities, extend useful lives, or interest costs net of earnings on invested bond proceeds. Management periodically evaluates the carrying amounts of long-lived assets for possible impairment. The System estimates that it will recover the carrying value of its long-lived assets from future operations; however, considering the regulatory environment, competition, and other factors affecting the industry, there is at least a reasonable possibility this estimate might change in the near term. The effect of any change could be material.

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-9-

NOTE A – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued Depreciation is computed using the straight-line method over the expected useful lives of the assets, which range from three to 40 years. Amortization of equipment under capital leases is included in the provision for depreciation. Bond Discounts/Premiums – Bonds payable are included in long-term debt, net of unamortized original issue discounts or premiums. Such discounts or premiums are amortized using a weighted-average method based on outstanding principal over the life of the bonds. Other Noncurrent Liabilities – Other noncurrent liabilities are comprised primarily of accruals for workers’ compensation claims, professional and general liability claims, deferred revenue, and long-term charitable gift annuity obligations. Net Assets – All resources not restricted by donors are included in unrestricted net assets. Resources temporarily restricted by donors for specific operating purposes, or for a period of time greater than one year, are reported as temporarily restricted net assets. When the restrictions have been met, the temporarily restricted net assets are reclassified to unrestricted net assets and reported in the combined statements of operations and changes in net assets under unrestricted revenues, gains, and support. Resources restricted by donors for additions to property and equipment are initially reported as temporarily restricted net assets and are transferred to unrestricted net assets when expended. Resources restricted by donors for nonexpendable endowments are reported as permanently restricted net assets. Investment income from restricted net assets is classified as either temporarily restricted or unrestricted based on the intent of the donor. Gifts of future interests are reported as temporarily restricted net assets. Gifts, grants, and bequests not restricted by donors are reported as other revenue. Net Patient Service Revenue – Net patient service revenue is recognized when services are provided and reported at the estimated net realizable amounts from patients, third-party payors, and others, including estimated retroactive adjustments under reimbursement agreements with third-party payors and the provision for bad debts. Retroactive adjustments are accrued on an estimated basis in the period the related services are rendered. Charity Care – The System provides care without charge or at amounts less than its established rates to patients who meet certain criteria under its charity care policy. In assessing a patient’s ability to pay, the System uses federal poverty income levels and evaluates the relationship between the charges and the patient’s income. The System did not materially change its charity care policy during 2011. The estimated cost of charity care was $57,145 and $49,744 in 2011 and 2010, respectively. The costs were determined by using a cost-to-charge ratio. Premium Revenue – The System has agreements with various Health Maintenance Organizations (HMOs) to provide medical services to subscribing participants. Under these agreements, the System receives monthly capitation payments based on the number of each HMO’s covered participants, regardless of the services actually performed by the System.

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-10-

NOTE A – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES – Continued Functional Expenses – Approximately 87% of total expenses reported in the accompanying combined financial statements relate to the provision of health care services in 2011 and 2010. The remaining expenses represent general and administrative support. Advertising – The System expenses advertising costs as incurred. Advertising expense, included in purchased services and other expenses, was $9,158 and $9,436 in 2011 and 2010, respectively. Excess of Revenues Over Expenses – The combined statements of operations and changes in net assets include excess of revenues over expenses from continuing operations as a performance indicator. Changes in unrestricted net assets that are excluded from excess of revenues over expenses from continuing operations include unrealized gains and losses on investments in other-than-trading securities, contributions of long-lived assets, use of restricted funds for capital additions, gains and losses from discontinued operations, and loss on disposal. Use of Estimates – The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires management to make estimates and assumptions that affect the reported amounts in the combined financial statements and the accompanying notes. Actual results could differ from these estimates. Reclassification – Certain 2010 amounts have been reclassified to conform to the 2011 presentation. NOTE B – FAIR VALUE OF FINANCIAL INSTRUMENTS The carrying value of all financial assets and liabilities approximates fair value except for self-insurance liabilities and long-term debt. The following methods and assumptions were used to estimate the fair value of each class of financial instruments: Other Noncurrent Liabilities – Self-insurance liabilities are based on actuarial estimates. It is not practical to estimate the fair value of the remaining liabilities due to the uncertainty of the timing of actual payments. Long-term Debt – The fair value of the System’s long-term debt, including current maturities, is estimated based on quoted market prices for the same or similar issues or on the current rates offered to the System for debt of the same remaining maturities. The carrying amount and fair value of long-term debt at December 31, 2011, was $1,074,447 and $1,083,984, respectively. At December 31, 2010, the carrying amount and fair value of long-term debt was $957,362 and $916,175, respectively.

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-11-

NOTE B – FAIR VALUE OF FINANCIAL INSTRUMENTS – Continued Financial Instruments – Fair value is the price that would be received upon sale of an asset in an orderly transaction between market participants at the measurement date and in the principal or most advantageous market for that asset. The fair value should be calculated based on assumptions that market participants would use in pricing the asset, not on assumptions specific to the entity. A fair value hierarchy for valuation inputs has been established to prioritize the valuation inputs into three levels based on the extent to which inputs used in measuring fair value are observable in the market. Each fair value measurement is reported in one of the three levels determined by the lowest level input considered significant to the fair value measurement in its entirety. These levels are defined as: Level 1: Quoted prices are available in active markets for identical assets as of the measurement date. Financial assets in Level 1 include US treasury securities, domestic and foreign equities, and exchange-traded mutual funds. Level 2: Pricing inputs are based on quoted prices for similar instruments in active markets, quoted prices for identical or similar instruments in markets that are not active, and model-based valuation techniques for which all significant assumptions are observable in the market or can be corroborated by observable market data for substantially the full term of the assets. Financial assets in this category generally include government agencies and municipal bonds, asset-backed securities, and corporate bonds. Level 3: Pricing inputs are generally unobservable for the assets and include situations where there is little, if any, market activity for the investment. The System had no investments in this level at December 31, 2011 and 2010.

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-12-

NOTE B – FAIR VALUE OF FINANCIAL INSTRUMENTS – Continued The fair value of the System’s financial assets, measured on a recurring basis at December 31, 2011, consists of the following:

The fair value of the System’s financial assets, measured on a recurring basis at December 31, 2010, consists of the following:

There were no significant transfers to or from Levels 1 or 2 during the years presented.

Quoted Pricesin Active

Markets for SignificantIdentical Observable Fair Value at

Instruments Inputs December 31(Level 1) (Level 2) 2011

Cash and cash equivalents 354,386$ -$ 354,386$ US government treasury obligations 21,217 - 21,217 US agency debentures - 93,719 93,719 US agency mortgage-backed securities - 106,356 106,356 Corporate debt securities - 404,498 404,498 Municipal bonds - 74,332 74,332 Equities 60,423 - 60,423

436,026$ 678,905$ 1,114,931$

Quoted Pricesin Active

Markets for SignificantIdentical Observable Fair Value at

Instruments Inputs December 31(Level 1) (Level 2) 2010

Cash and cash equivalents 248,734$ -$ 248,734$ US government treasury obligations 22,485 - 22,485 US agency debentures - 74,070 74,070 US agency mortgage-backed securities - 120,082 120,082 Corporate debt securities - 391,868 391,868 Municipal bonds - 67,528 67,528 Equities 61,753 - 61,753

332,972$ 653,548$ 986,520$

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-13-

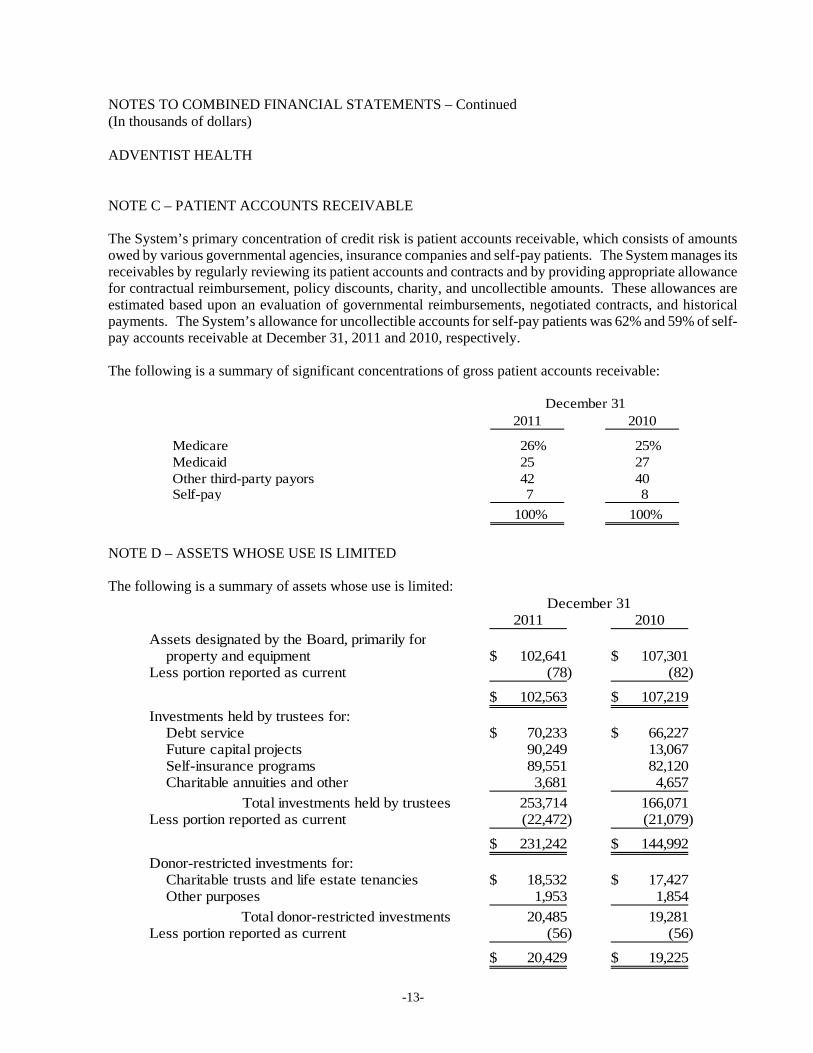

NOTE C – PATIENT ACCOUNTS RECEIVABLE The System’s primary concentration of credit risk is patient accounts receivable, which consists of amounts owed by various governmental agencies, insurance companies and self-pay patients. The System manages its receivables by regularly reviewing its patient accounts and contracts and by providing appropriate allowance for contractual reimbursement, policy discounts, charity, and uncollectible amounts. These allowances are estimated based upon an evaluation of governmental reimbursements, negotiated contracts, and historical payments. The System’s allowance for uncollectible accounts for self-pay patients was 62% and 59% of self-pay accounts receivable at December 31, 2011 and 2010, respectively. The following is a summary of significant concentrations of gross patient accounts receivable:

December 312011 2010

Medicare 26% 25%Medicaid 25 27Other third-party payors 42 40Self-pay 7 8

100% 100%

NOTE D – ASSETS WHOSE USE IS LIMITED The following is a summary of assets whose use is limited:

December 312011 2010

Assets designated by the Board, primarily forproperty and equipment 102,641$ 107,301$

Less portion reported as current (78) (82)

102,563$ 107,219$ Investments held by trustees for:

Debt service 70,233$ 66,227$ Future capital projects 90,249 13,067 Self-insurance programs 89,551 82,120 Charitable annuities and other 3,681 4,657

Total investments held by trustees 253,714 166,071 Less portion reported as current (22,472) (21,079)

231,242$ 144,992$ Donor-restricted investments for:

Charitable trusts and life estate tenancies 18,532$ 17,427$ Other purposes 1,953 1,854

Total donor-restricted investments 20,485 19,281 Less portion reported as current (56) (56)

20,429$ 19,225$

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-14-

December 312011 2010

Investments reported at fair value as determined by quoted market prices:

Trustee-held cash and cash equivalents 104,267$ 21,220$ US government treasury obligations 21,217 22,485 US agency debentures 93,719 74,070 US agency mortgage-backed securities 106,356 120,082 Corporate debt securities 404,498 391,868 Municipal bonds 74,332 67,528 Equities 60,423 61,753

864,812 759,006 Commercial real estate 30,078 28,188 Other investments 24,911 19,149

919,801$ 806,343$

NOTE E – INVESTMENTS The following is a summary of investments classified by major type, which are included in the balance sheet under marketable securities, assets whose use is limited, and investments: Net realized investment income, including capital gains, interest, and dividend income, is reported as a component of other revenue and includes the following:

For purposes of performance evaluation, management considers investment earnings on bond and self-insurance trustee-held funds to be components of operating income. These earnings are used to pay the operating expenses of interest and insurance.

Year Ended December 312011 2010

Investment earnings: Unrestricted and board-designated funds 25,784$ 29,314$ Trustee-held funds: Bonds 2,883 3,302 Self-insurance programs 6,368 1,672

35,035$ 34,288$

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-15-

NOTE E – INVESTMENTS – Continued Changes in net unrealized gains and losses on other-than-trading securities, reported at fair value, are separately disclosed in the combined statements of operations and changes in net assets. Unrealized gains and losses associated with these securities relate principally to market changes in interest rates for similar types of securities. Since the System has the intent and ability to hold these securities for the foreseeable future, and it is more likely than not that the System will not be required to sell the investments before their recovery, the declines are not reported as realized unless they are deemed to be other-than-temporary. In determining whether the losses are other-than-temporary, the System considers the length of time and extent to which the fair value has been less than cost or carrying value, the financial strength of the issuer, and the intent and ability of the System to retain the security for a period of time sufficient to allow for anticipated recovery or maturity. NOTE F – PROPERTY AND EQUIPMENT The following is a summary of property and equipment:

The System has commitments to complete certain construction in progress projects in the amount of $36,069 at December 31, 2011.

December 312011 2010

Land and improvements 130,454$ 120,277$ Buildings and improvements 1,610,421 1,502,275 Equipment 711,042 669,065

2,451,917 2,291,617Less accumulated depreciation (1,173,248) (1,078,153)

1,278,669 1,213,464 Construction in progress 119,330 111,297

1,397,999$ 1,324,761$

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-16-

NOTE F – PROPERTY AND EQUIPMENT – Continued The System is in the process of developing internal use software for clinical operations. Depreciation expense for the software totaled $9,056 and $8,275 in 2011 and 2010, respectively. Amounts capitalized are included in property and equipment as follows: NOTE G – LONG-TERM DEBT A Master Note under the Master Bond Indenture provides security for substantially all long-term debt. Under the terms of the Master Bond Indenture, substantially all System combined entities are jointly and severally obligated for the payments to be made under the Master Note. In addition, security is provided by a combination of bond insurance, funds held in trust of $70,233, standby bond purchase agreements of $58,327, and bank letters of credit aggregating to $152,042 at December 31, 2011. Bonds are not secured by any property of the System. The System is obligated under variable rate demand instruments, which are subject to certain market risks. The letters of credit, which the System intends to renew on a long-term basis, expire between 2013 and 2016 with the arrangements converting any unpaid amounts to term loans due between 2013 and 2016. The term loans would bear interest based on prime or the London Interbank Offered Rate (LIBOR). Long-term debt has been issued primarily on a tax-exempt basis. Certain lenders impose limitations on the issuance of new debt by the System and require it to maintain specified financial ratios. Interest paid, net of amounts capitalized, totaled $35,938 and $32,287 in 2011 and 2010, respectively. Interest capitalized totaled $5,076 and $9,686 in 2011 and 2010, respectively. The System recorded operating lease expense amounting to $44,441 and $39,073 in 2011 and 2010, respectively.

December 312011 2010

Equipment 112,847$ 104,291$ Less accumulated depreciation (46,440) (37,384)

66,407 66,907 Construction in progress 15,658 8,430

82,065$ 75,337$

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-17-

NOTE G – LONG-TERM DEBT – Continued The following is a summary of long-term debt and capital lease obligations:

Scheduled maturities of long-term debt, capital lease obligations, and minimum lease payments on noncancelable operating leases with initial terms in excess of one year are as follows for the year ended December 31, 2011:

Long-termDebt and Operating

Capital Leases Leases

2012 25,622$ 25,965$ 2013 25,672 18,367 2014 33,901 12,730 2015 19,274 9,150 2016 40,566 5,792 Thereafter 925,863 18,289

1,070,898$ 90,293$

December 312011 2010

Long-term bonds payable, with fixed ratescurrently ranging from 4.50% to 5.75%,payable in installments through 2040 639,675$ 650,615$

Long-term bonds payable, with rates that varywith market conditions, payable in installmentsthrough 2041 337,500 208,900

Long-term notes payable, with rates that varywith market conditions, payable in installments through 2025 92,318 91,042

Net unamortized original issue premium 3,549 4,085 1,073,042 954,642

Capital lease obligations 1,405 2,720 1,074,447 957,362

Less current maturities (25,622) (21,189)

1,048,825$ 936,173$

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-18-

NOTE H – RESTRICTED NET ASSETS Net assets are restricted for the following purposes:

NOTE I – PATIENT SERVICE REVENUE Patient service revenue after contractual allowances and discounts and before provisions for bad debts, by major payor sources, was as follows:

The System has agreements with third-party payors that provide for payments to the System at amounts different from its established rates. Payment arrangements include prospectively determined rates per discharge, reimbursed costs, discounted charges, fee schedules, and per diem payments. The health care industry is subject to complex laws and regulations of federal, state and local governments. Compliance with such laws and regulations can be subject to future government review and interpretation as well as regulatory actions unknown or unasserted at this time. These laws and regulations include, but are not necessarily limited to, matters such as licensure, accreditation, government health care program participation requirements, reimbursement laws and regulations, anti-kickback and anti-referral laws and false claims prohibitions, and in the case of tax-exempt hospitals, the requirements of tax-exemption. In recent years, government activity has increased with respect to investigations and allegations concerning possible violations of reimbursement, false claims, anti-kickback and anti-referral statutes and regulations by health care providers. The System also operates a Compliance Program, which reviews compliance with government health care program requirements and investigates allegations of non-compliance received from internal and external sources. From time to time findings may result in repayment of monies previously received from government payers and/or commercial payers, payment of penalties, and/or disclosure of such overpayments, including, but not limited to, disclosure to Centers for Medicare and Medicaid Services and its contracted agents, or the Office of Inspector General -

December 312011 2010

Temporarily restricted: Equipment and buildings 31,528$ 29,508$ Patient care, education, research, and other 13,429 12,766 Time-restricted trusts held for unrestricted purposes 6,455 6,076

51,412$ 48,350$

Permanently restricted - Endowments 5,962$ 5,225$

Year Ended December 312011 2010

Medicare 820,907$ 712,727$ Medicaid 440,660 500,821 Others 1,337,374 1,283,580

Net patient service revenue 2,598,941$ 2,497,128$

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-19-

NOTE I – PATIENT SERVICE REVENUE – Continued Department of Health and Human Services. As a result, there is at least a reasonable possibility that the recorded estimates may change by a material amount in the near term. Differences between original estimates and subsequent revisions, including final settlements, ongoing audits, and investigations, are recognized in the period in which the revisions are made. Subsequent revisions compared favorably to original estimates by approximately $45,187 and $18,600 for the years ended December 31, 2011 and 2010, respectively. The System recorded revenue from state programs for serving a disproportionate share of Medicaid and low-income patients in the amount of $37,471 and $45,852 in 2011 and 2010, respectively. During 2011, the state of California enacted a six-month quality assurance fee program whereby participating hospitals would pay fees to the state to obtain Medi-Cal reimbursement matched by federal funds. In December, 2011, the Centers for Medicare and Medicaid Services approved the fee program, which covered the period of January 1, 2011 through June 30, 2011. The fees paid to the state along with the federal matching funds are redistributed to California hospitals to fund certain Medi-Cal coverage expansions. In 2011, the System recorded $77,719 in patient service revenue and $35,765 in other expenses related to this program with a net income effect of $41,954. Of the total revenue recorded, $68,178 had been received as of December 31, 2011, and the remaining $9,541 is included in receivables from third-party payors. Expenses consist of $33,265 in quality assurance fees paid to the state and $2,500 in payments to the California Health Foundation Trust for redistribution to hospitals that would otherwise incur a net loss from the program. In September 2011, a 30-month quality assurance fee program was established for the period from July 1, 2011 through December 31, 2013. This program has not received final approval and no amounts have been recorded in the accompanying financial statements. During 2010, the state enacted a 21-month quality assurance fee program that covered the period of April 1, 2009 through December 31, 2010. In 2010, the System recorded $187,187 in patient service revenue and $107,424 in other expenses related to this program with a net income effect of $79,763. Of the total revenue recorded, $155,113 had been received as of December 31, 2010, and the remaining $32,074 was included in receivables from third-party payors. Expenses consisted of $98,566 in quality assurance fees paid to the state and $8,858 in payments to the California Health Foundation Trust for redistribution to hospitals that would otherwise incur a net loss from the program. In 2011 the System recorded another $5,441 in patient service revenue related to this program for amounts that were not approved and known until 2011.

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-20-

NOTE J – RETIREMENT PLAN Most of the System’s operating entities participate in a single defined contribution plan (the “Plan”). The Plan is exempt from the Employee Retirement Income Security Act of 1974. The Plan provides, among other things, that the employer will contribute 3% of wages plus additional amounts for employees earning more than the Social Security wage base capped by the IRS compensation limit for the Plan year. Additionally, the Plan provides that the employer will match 50% of the employee’s contributions up to 4% of the contributing employee’s wages. Substantially all full-time employees who are at least 18 years of age are eligible for coverage in the Plan. The cost to the System for the Plan is reported in the combined statements of operations in the amount of $33,773 and $32,881 for the years ended December 31, 2011 and 2010, respectively. NOTE K – SELF-INSURANCE LIABILITY PROGRAMS The System has established a separate self-insured revocable trust (the “System Trust”) that covers the System’s facilities for professional and general liability claims up to $7,500 per occurrence and $20,000 in aggregate. The System contracts with Adhealth, Limited (Adhealth), a Bermuda company, to provide excess coverage for professional and general liability claims that exceed the self-insured revocable trust limits. Adhealth provided excess coverage with aggregate and per claim limits of $107,500 for professional and general liability claims, and additional limits of $25,000 for general liability claims for the years ended December 31, 2011 and 2010. Adhealth has purchased reinsurance through commercial insurers for 100% of the excess limits of coverage. Claim liabilities (reserves) for future losses and related loss adjustment expenses for professional liability claims have been determined by an actuary at the present value of future claim payments using a 3% discount rate for program years 2011 and 2010. Such claim reserves are based on the best data available to the System; however, these estimates are subject to a significant degree of inherent variability. Accordingly, there is at least a reasonable possibility that a material change to the estimated reserves will occur in the near term. The System Trust’s accrued liability for professional and general liability claims is included in the combined balance sheets in the amount of $105,071 and $91,612 at December 31, 2011 and 2010, respectively. The System has a 50% ownership position in Adhealth at December 31, 2011 and 2010, and accounts for its investment using the equity method of accounting. The System provides funding to Adhealth based on Adhealth’s cost of acquiring commercial insurance. The funding contributions are reflected as an expense in the combined statements of operations and changes in net assets. The System maintains a self-insured workers’ compensation plan to pay for the cost of workers’ compensation claims. The System has entered into an excess insurance agreement with an insurance company to limit its losses on claims. The cost of workers’ compensation claims is accrued using actuarially determined estimates that are based on historical factors. Such claim reserves are based on the best data available to the System; however, these estimates are subject to a significant degree of inherent variability. Accordingly, there is at least a reasonable possibility that a material change to the estimated reserves will occur in the near term. Workers’ compensation claim liabilities have been determined by an actuary at the present value of future claim payments using a 3% discount rate for 2011 and 2010. The System’s accrued liability for workers’ compensation claims is recorded in the combined balance sheets in the amount of $64,481 and $44,223 at December 31, 2011 and 2010, respectively.

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-21-

NOTE L – RELATED-PARTY TRANSACTIONS The System had transactions with organizations that are considered related parties. The amounts receivable from related parties are reported in the accompanying combined financial statements as other receivables of $1,229 and $2,529 and notes receivable of $12,857 and $13,403 at December 31, 2011 and 2010, respectively. NOTE M – COMMITMENTS AND CONTINGENCIES Certain member organizations are involved in litigation arising in the ordinary course of business. In addition, the Department of Health and Human Services’ Office of the Inspector General is investigating whether certain member organizations have submitted false claims to the Medicare and Medicaid programs or have violated other laws. Submission of false claims or violation of other laws can result in substantial civil and/or criminal penalties and fines, including treble damages and/or possible debarment from future participation in such programs. The System is cooperating in these investigations. Although management does not believe these matters will have a material adverse effect on the System’s combined financial position, there can be no assurance that such will be the case. A member organization received a subpoena on November 17, 2011 in relation to a hospital initiative that was implemented in 2009 with the goal of improving patient access to inpatient care. The scope of the information requested is very broad, and applies in some cases to documents from 2008 to present. The government has not asserted any specific claims and the System is cooperating with this investigation. Adventist Health, Glendale Adventist Medical Center, Southern California Medical Foundation, and White Memorial Medical Center received a subpoena from the federal government on November 3, 2008 requesting documents and information pertaining to each entity’s compliance with the federal Anti-kickback law and “Stark” law. The scope of the information request is very broad, and applies in some cases to documents from 1994 to the present. The government has not asserted any specific claims and the System is cooperating with this investigation. The System extended lines of credit primarily to physicians totaling $4,331 and $3,855 at December 31, 2011 and 2010, respectively. There were $414 and $4,348 of purchase commitments at December 31, 2011 and 2010, respectively. The System has assessed its earthquake retrofit requirements for health care facilities under a state of California law that requires compliance with certain seismic standards. The necessary improvements have been included in the System’s capital planning process. Upon completion of the current construction projects in process, the System will have accomplished the major seismic-required capital projects identified. NOTE N – FEMA FINANCIAL GRANTS Several of the System’s hospitals are located in areas of frequent earthquake activity and have sustained damage from earthquakes in the past. Three System hospitals received $156,150 of grant funds from the Federal Emergency Management Agency (FEMA) for repair of damage and seismic structural upgrades and all of these funds were recorded in the accompanying financial statements in years prior to 2011. FEMA reserves

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-22-

NOTE N – FEMA FINANCIAL GRANTS – Continued the right to recover funds from the System for a period of eight years from completion of the final phase of construction if the facilities do not continue to be used by a tax-exempt organization for the provision of acute care patient services. FEMA grant funds received for capitalized expenditures are accounted for as an exchange transaction and are reported as deferred revenue. Deferred revenue of $115,563 and $121,455 at December 31, 2011 and 2010, respectively, is recorded as other noncurrent liabilities in the combined financial statements. After completion of a project, the related deferred revenue is amortized over the expected useful life of the asset and recorded as other revenue. Amortization of deferred revenue totaled $5,892 and $5,880 for the years ended December 31, 2011 and 2010, respectively. NOTE O – DERIVATIVE FINANCIAL INSTRUMENTS The System uses two variable-to-fixed interest rate swap agreements with a financial institution to manage interest rate risk on future variable interest payments. The agreements are based on notional principal amounts of $20,000 and $10,000 and commenced in August 2002 and expire in September 2012. Under the terms of the agreements, the System pays a fixed rate of 3.24% and receives a variable payment approximately equal to the interest rate on two of its long-term obligations. The interest rate differential was recognized as an increase to interest expense in the amount of $927 and $919 in 2011 and 2010, respectively. The aggregate fair market value of the swap, using Level 2 measurements, was a net payable of $678 and $1,510 at December 31, 2011 and 2010, respectively. NOTE P – NEW ACCOUNTING PRONOUNCEMENTS In July 2011, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2011-07, Presentation and Disclosure of Patient Service Revenue, Provision for Bad Debts, and the Allowance for Doubtful Accounts for Certain Health Care Entities, which amended Accounting Standards Codification (ASC) 954, Health Care Entities, to provide greater transparency regarding a health care entity’s net patient service revenue and the related allowance for doubtful accounts. ASU 2011-07 requires certain health care entities to classify the provision for patient bad debts as a deduction from revenue rather than an expense, and requires enhanced disclosures about patient service revenues and the policies for recognizing revenue and assessing bad debts. The System retrospectively early adopted ASU 2011-07, effective June 30, 2011. In May 2011, the FASB issued ASU No. 2011-04, Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs, which amended ASC 820, Fair Value Measurement to change the wording used to describe many of the requirements in U.S. GAAP for measuring fair value and for disclosing information about fair value measurements. Management is currently evaluating the potential impact of this guidance, which will be effective January 1, 2012, but does not expect it to have a material impact on the combined financial condition, results of operations, or cash flows.

NOTES TO COMBINED FINANCIAL STATEMENTS – Continued (In thousands of dollars) ADVENTIST HEALTH

-23-

NOTE P – NEW ACCOUNTING PRONOUNCEMENTS – Continued In August 2010, the FASB issued ASU No. 2010-24, Presentation of Insurance Claims and Related Insurance Recoveries, which amended ASC 954, Health Care Entities, to clarify that a health care entity should not net insurance recoveries against a related claim liability. Additionally, the amount of the claim liability should be determined without consideration of insurance recoveries. The System adopted ASU 2010-24 on January 1, 2011, and its adoption had the effect of increasing Other Long-Term Assets and Other Noncurrent Liabilities by $16,000 at December 31, 2011. Retrospective application is not required and was not applied to the comparative 2010 balance sheet. In August 2010, the FASB issued ASU No. 2010-23, Measuring Charity Care for Disclosures, which amends ASC 954, Health Care Entities, to require that cost be used as a measurement for charity care disclosure purposes and that cost can be identified as the direct and indirect costs of providing the charity care. It also requires disclosure of the method used to identify or determine such costs. The System adopted ASU 2010-23 effective January 1, 2011. In February 2010, the FASB issued ASU No. 2010-09, Subsequent Events: Amendments to Certain Recognition and Disclosure Requirements, which amended ASC 855, Subsequent Events, requiring the evaluation of subsequent events through the date that the financial statements are issued. The System adopted ASU 2010-09 effective January 1, 2010, and the adoption of this guidance did not have a material impact on the System’s combined financial statements. In January 2010, the FASB issued ASU No. 2010-06, Improving Disclosure About Fair Value Measurements, which amended ASC 820, Fair Value Measurement. ASU 2010-06 requires new disclosures and clarifies some existing disclosure requirements about fair value measurement as set forth in ASC Subtopic 820-10. The System adopted ASU 2010-06 effective January 1, 2010, and the adoption did not have a material impact on the combined financial statements. NOTE Q – SUBSEQUENT EVENTS On April 5, 2012, an industry-wide settlement agreement was finalized among the Department of Health and Human Services, the Centers for Medicare and Medicaid Services, and many providers including several System hospitals (the “Settlement”). The Settlement resulted in revised reimbursement due to a change in how Medicare's rural floor budget neutrality adjustment was calculated for federal fiscal years 1998 through 2011. As a result of this Settlement, the System recorded additional income of $18,252 in 2011. The System has evaluated subsequent events through the April 23, 2012 issuance date of the combined financial statements.

Ernst & Young LLP Sacramento Office 2901 Douglas Boulevard Suite 300 Roseville, California 95661

Tel: +1 916 218-1900 Fax: +1 916 218-1999 www.ey.com

A member firm of Ernst & Young Global Limited

-24-

REPORT OF INDEPENDENT AUDITORS ON SUPPLEMENTARY INFORMATION

Board of Directors Adventist Health Roseville, California We have audited the combined financial statements of Adventist Health as of and for the years ended December 31, 2011 and 2010, and have issued our report thereon dated April 23, 2012, which contained an unqualified opinion on those financial statements. Our audits were conducted for the purpose of forming an opinion on the combined financial statements as a whole. The accompanying combining financial statement schedules for Adventist Health are presented for purposes of additional analysis and are not a required part of the combined financial statements. Such information is the responsibility of management and was derived from and relates directly to the underlying accounting and other records used to prepare the financial statements. The information has been subjected to the auditing procedures applied in the audits of the combined financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the combined financial statements or to the combined financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States. In our opinion, the information is fairly stated in all material respects in relation to the combined financial statements as a whole. April 23, 2012

COMBINING BALANCE SHEET(In thousands of dollars)

ADVENTIST HEALTH

December 31, 2011Adventist Adventist Adventist Adventist Adventist Central Glendale

Adjustments Health Health Medical Medical Medical Castle Valley Feather AdventistCombined and Corporate Physicians Center Center Center Medical General River MedicalBalances Eliminations Office Network (Hanford) (Portland) (Reedley) Center Hospital Hospital Center

ASSETS

CURRENT ASSETSCash and cash equivalents 250,119$ (595,484)$ 176,699$ 2,728$ 1,226$ 91,198$ 2$ 48,505$ 52,849$ 1,112$ 44,145$ Marketable securities 45,393 44,560 - - - - - 409 - - 373 Assets whose use is limited:

Board-designated 78 (101,981) 1,120 - - 3,544 - 827 - 59 1,080 Held by trustees 22,472 (2,542) 12,942 - 854 1,200 - 682 523 689 1,874 Donor-restricted 56 - - - - - - - - - -

Patient accounts receivable, net ofallowance for uncollectible accounts 357,638 (10,504) - 2,054 29,277 40,095 2,748 16,305 8,658 22,494 55,423

Receivables from third-party payors 7,957 (21,606) - - 577 - 2,125 806 262 7,019 3,201 Other receivables 27,280 (9,488) 6,608 56 3,778 5,052 17 1,260 1,401 417 4,311 Intra-system financing receivables - (17,104) 16,883 - - - - 73 43 - 101 Inventories 42,594 - - - 3,529 3,339 360 1,909 174 3,144 6,883 Prepaid expenses and other current assets 23,711 - 4,726 - 2,108 2,176 1,974 1,516 123 1,141 2,480

TOTAL CURRENT ASSETS 777,298 (714,149) 218,978 4,838 41,349 146,604 7,226 72,292 64,033 36,075 119,871

OTHER ASSETS Intra-system financing receivables - (968,141) 814,077 - 11,937 6,249 - 54 4,000 15,670 22,692 Notes receivable 16,658 - 14,951 - 54 - - - - 13 - Marketable securities 472,564 450,919 20,027 - - - - - - - - Assets whose use is limited:

Board-designated 102,563 102,420 - - - - - - - 143 - Held by trustees 231,242 (1,856) 213,794 - 2,876 245 - 3,681 237 1,865 1,238 Donor-restricted 20,429 - - - - 8 - 7,065 - 945 231

Long-term investments 25,004 - 18,110 - 1,533 412 - 666 - - 1,019 Deferred financing costs 7,373 - 7,373 - - - - - - - - Other long-term assets 38,905 15,543 - - 698 1,572 3,697 542 3 - 2,134

TOTAL OTHER ASSETS 914,738 (401,115) 1,088,332 - 17,098 8,486 3,697 12,008 4,240 18,636 27,314

PROPERTY AND EQUIPMENT Land and improvements 130,454 - 6,568 - 6,273 18,662 - 12,784 2,350 12,484 7,173 Buildings and improvements 1,610,421 - 7,883 - 172,827 175,424 - 92,084 13,692 59,228 356,207 Equipment 711,042 - 146,266 - 46,356 78,756 5,272 32,974 6,305 27,086 66,058

2,451,917 - 160,717 - 225,456 272,842 5,272 137,842 22,347 98,798 429,438 Less accumulated depreciation (1,173,248) - (77,500) - (66,607) (149,970) - (81,416) (11,962) (56,847) (197,113)

1,278,669 - 83,217 - 158,849 122,872 5,272 56,426 10,385 41,951 232,325 Construction in progress 119,330 - 21,113 - 6,419 2,265 - 1,579 3,477 18,637 22,396

PROPERTY AND EQUIPMENT, net 1,397,999 - 104,330 - 165,268 125,137 5,272 58,005 13,862 60,588 254,721

TOTAL ASSETS 3,090,035$ (1,115,264)$ 1,411,640$ 4,838$ 223,715$ 280,227$ 16,195$ 142,305$ 82,135$ 115,299$ 401,906$

See accompanying auditors' report on supplementary information. -25-

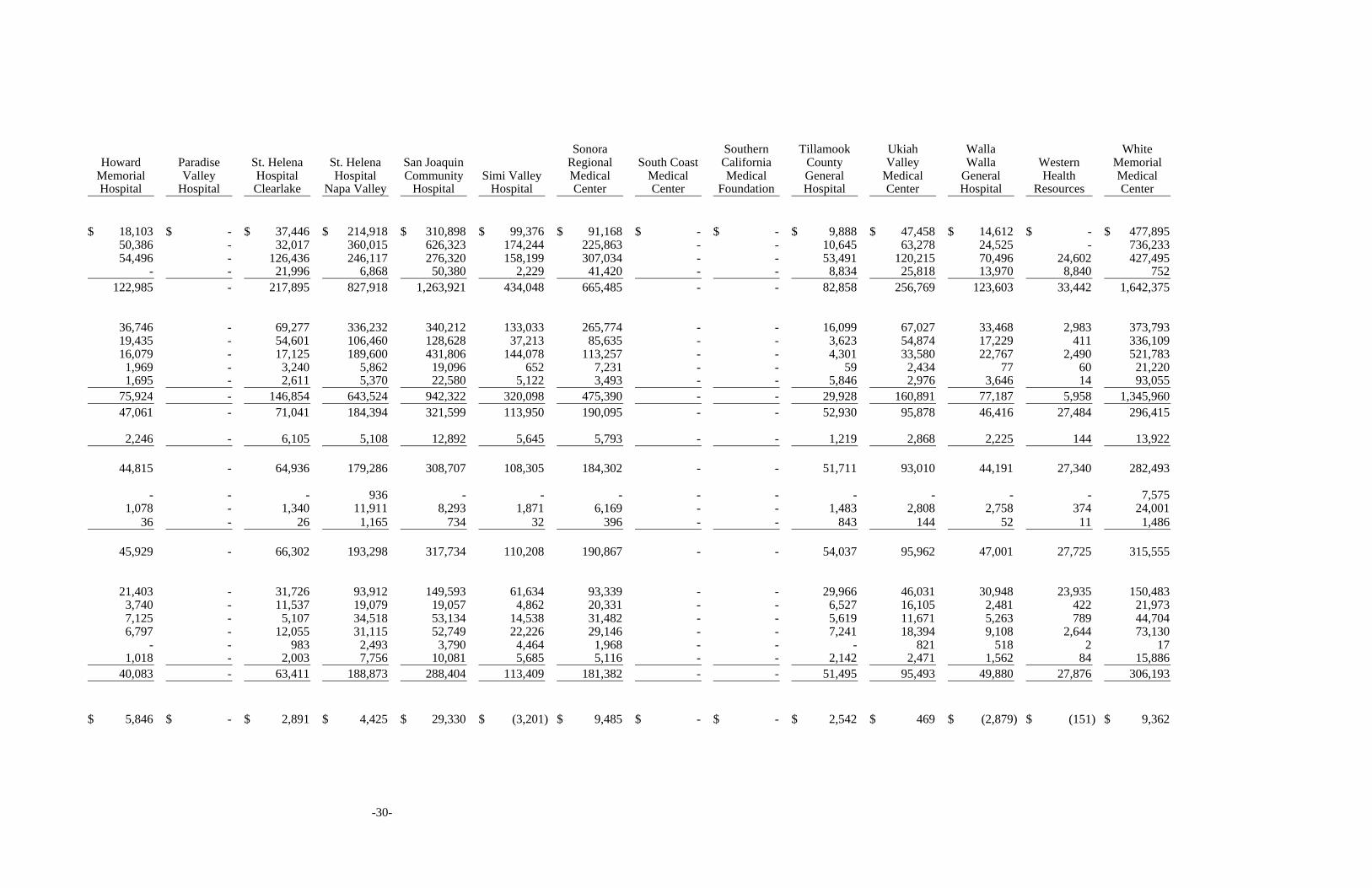

Sonora Southern Tillamook Ukiah Walla WhiteHoward Paradise St. Helena St. Helena San Joaquin Regional South Coast California County Valley Walla Western Memorial

Memorial Valley Hospital Hospital Community Simi Valley Medical Medical Medical General Medical General Health MedicalHospital Hospital Clearlake Napa Valley Hospital Hospital Center Center Foundation Hospital Center Hospital Resources Center

27,170$ 2,554$ 3,657$ 346$ 83,944$ 2,876$ 30,571$ -$ 1,120$ 23,504$ 11,775$ 278$ 1,945$ 237,399$ - - - - - - - - - - - - - 51

- - - - - - - - - - - - - 95,429 242 212 240 734 582 516 1,120 - 1 76 486 - 663 1,378

- - - 56 - - - - - - - - - -

5,267 - 5,806 30,680 41,647 15,051 22,311 - - 8,851 11,200 8,073 3,885 38,317 - 584 17 149 2,471 295 - - - 1,402 6,393 351 - 3,911

131 503 353 3,957 4,254 793 304 - - 455 1,104 543 43 1,428 - - - - - 4 - - - - - - - -

679 - 607 2,689 6,761 1,722 3,008 - - 769 1,931 1,149 - 3,941 158 - 143 1,263 397 1,497 1,461 53 - 737 394 92 109 1,163

33,647 3,853 10,823 39,874 140,056 22,754 58,775 53 1,121 35,794 33,283 10,486 6,645 383,017

- 12,570 7,907 17,822 6,528 46,716 797 - - - 989 - - 133 - - 200 610 - 330 - - - 481 14 5 - - - - - - - - - - - - - - - 1,618

- - - - - - - - - - - - - - 403 - 640 1,147 460 1,652 489 - - 283 1,432 - - 2,656

- - - 12,180 - - - - - - - - - - - - 630 - - 2,100 - - - - 500 - - 34 - - - - - - - - - - - - - - - - 586 2,472 8,749 676 395 - - - 173 - - 1,665

403 12,570 9,963 34,231 15,737 51,474 1,681 - - 764 3,108 5 - 6,106

16 - 9,663 16,510 6,675 8,048 8,640 - - 1,548 1,970 1,501 77 9,512 2,684 - 16,772 105,093 107,805 107,286 57,666 - - 20,251 24,690 24,648 216 265,965 9,625 - 10,292 50,915 53,860 29,747 32,792 - - 11,751 17,398 16,247 242 69,100

12,325 - 36,727 172,518 168,340 145,081 99,098 - - 33,550 44,058 42,396 535 344,577 (8,411) - (20,395) (93,070) (69,545) (56,549) (50,588) - - (24,876) (29,049) (29,912) (241) (149,197) 3,914 - 16,332 79,448 98,795 88,532 48,510 - - 8,674 15,009 12,484 294 195,380 5,050 - 4,951 5,559 6,476 12,087 1,146 - - 62 3,247 3,355 - 1,511 8,964 - 21,283 85,007 105,271 100,619 49,656 - - 8,736 18,256 15,839 294 196,891

43,014$ 16,423$ 42,069$ 159,112$ 261,064$ 174,847$ 110,112$ 53$ 1,121$ 45,294$ 54,647$ 26,330$ 6,939$ 586,014$

-26-

COMBINING BALANCE SHEET – Continued(In thousands of dollars)

ADVENTIST HEALTH

December 31, 2011Adventist Adventist Adventist Adventist Adventist Central Glendale

Adjustments Health Health Medical Medical Medical Castle Valley Feather AdventistCombined and Corporate Physicians Center Center Center Medical General River MedicalBalances Eliminations Office Network (Hanford) (Portland) (Reedley) Center Hospital Hospital Center

LIABILITIES AND NET ASSETS

CURRENT LIABILITIESBank checks outstanding, less cash on deposit -$ (6,578)$ -$ -$ 1,939$ -$ -$ -$ -$ 815$ -$ Accounts payable 86,885 (7,621) 8,996 3,583 5,997 5,579 1,566 3,350 2,836 5,638 14,324 Accrued compensation and related payables 146,738 (12,023) 45,765 - 8,238 11,634 753 6,647 2,983 7,017 13,760 Accrued interest 11,404 (1,447) 12,777 - - - - - - - - Liabilities to third-party payors 58,151 (21,606) - - 5,393 1,379 18 - 2,592 - 125 Other current liabilities 40,772 (15,233) 22,437 1,000 1,102 6,403 3 1,547 53 238 4,929 Short-term financing 152 (124,076) - - 42 - 2,939 - 404 548 - Current maturities of long-term debt 25,622 (17,385) 16,156 - 1,848 267 - 802 1,500 1,749 4,667

TOTAL CURRENT LIABILITIES 369,724 (205,969) 106,131 4,583 24,559 25,262 5,279 12,346 10,368 16,005 37,805

LONG-TERM DEBT, net of current maturities 1,048,825 (967,907) 1,122,579 - 148,092 67,022 11,932 2,484 70 75,067 182,230

OTHER NONCURRENT LIABILITIES 292,078 8,749 111,342 - 4,951 1,063 - 6,765 1,204 2,955 39,433 TOTAL LIABILITIES 1,710,627 (1,165,127) 1,340,052 4,583 177,602 93,347 17,211 21,595 11,642 94,027 259,468

NET ASSETS

Unrestricted 1,322,034 49,863 71,588 255 44,397 182,959 (1,016) 115,288 70,489 19,790 137,529 Temporarily restricted 51,412 - - - 1,716 1,418 - 4,776 4 1,482 4,628 Permanently restricted 5,962 - - - - 2,503 - 646 - - 281

TOTAL NET ASSETS 1,379,408 49,863 71,588 255 46,113 186,880 (1,016) 120,710 70,493 21,272 142,438

TOTAL LIABILITIES AND NET ASSETS 3,090,035$ (1,115,264)$ 1,411,640$ 4,838$ 223,715$ 280,227$ 16,195$ 142,305$ 82,135$ 115,299$ 401,906$

See accompanying auditors' report on supplementary information. -27-

Sonora Southern Tillamook Ukiah Walla WhiteHoward Paradise St. Helena St. Helena San Joaquin Regional South Coast California County Valley Walla Western Memorial

Memorial Valley Hospital Hospital Community Simi Valley Medical Medical Medical General Medical General Health MedicalHospital Hospital Clearlake Napa Valley Hospital Hospital Center Center Foundation Hospital Center Hospital Resources Center

-$ -$ -$ 2,202$ -$ 902$ -$ 38$ -$ -$ -$ 682$ -$ -$ 883 - 1,706 5,533 11,476 3,539 4,607 59 - 1,251 2,450 996 114 10,023

1,970 272 2,942 8,502 12,914 5,110 6,758 247 - 2,267 3,621 2,302 1,480 13,579 - - 12 29 - - - 29 - - - 4 - -

1,302 - 2,420 4,885 18,991 243 2,365 55 - - - 492 - 39,497 - 96 21 611 4,678 1,004 666 587 - - 29 138 3 10,460 - - - 17,456 - 64,156 - 22,724 - - - 15,959 - - - - 641 1,946 5,769 3,426 1,961 - - - 608 1,667 - -

4,155 368 7,742 41,164 53,828 78,380 16,357 23,739 - 3,518 6,708 22,240 1,597 73,559

- - 52,728 65,623 81,696 132,041 44,108 7,893 - - 17,020 6,147 - -

483 1,605 1,235 2,914 2,174 17,100 5,031 4,748 - 251 3,048 - 793 76,234 4,638 1,973 61,705 109,701 137,698 227,521 65,496 36,380 - 3,769 26,776 28,387 2,390 149,793

38,308 14,450 (20,807) 25,331 120,692 (55,070) 43,728 (36,327) 1,121 38,525 26,940 (2,767) 4,544 432,224 68 - 1,171 21,554 2,674 2,396 888 - - 3,000 925 710 5 3,997

- - - 2,526 - - - - - - 6 - - - 38,376 14,450 (19,636) 49,411 123,366 (52,674) 44,616 (36,327) 1,121 41,525 27,871 (2,057) 4,549 436,221

43,014$ 16,423$ 42,069$ 159,112$ 261,064$ 174,847$ 110,112$ 53$ 1,121$ 45,294$ 54,647$ 26,330$ 6,939$ 586,014$

-28-

COMBINING STATEMENT OF OPERATIONS AND CHANGES IN NET ASSETS (In thousands of dollars)

ADVENTIST HEALTH

Year Ended December 31, 2011Adventist Adventist Adventist Adventist Adventist Central Glendale

Adjustments Health Health Medical Medical Medical Castle Valley Feather AdventistCombined and Corporate Physicians Center Center Center Medical General River MedicalBalances Eliminations Office Network (Hanford) (Portland) (Reedley) Center Hospital Hospital Center

UNRESTRICTED REVENUES, GAINS, AND SUPPORTGross patient charges:

Inpatient daily hospital charges 2,187,424$ (25)$ -$ -$ 116,414$ 99,232$ 1,982$ 68,759$ 15,640$ 87,981$ 475,679$ Inpatient ancillary charges 4,128,130 (23) - - 259,026 206,243 2,288 116,080 16,364 315,920 908,703 Outpatient ancillary charges 3,652,454 (17) - - 491,230 269,101 5,515 111,460 15,058 416,082 479,124 Other patient charges 455,763 - - 34,675 2,824 73,264 1,374 31,647 75,093 40,969 14,810

Gross patient charges 10,423,771 (65) - 34,675 869,494 647,840 11,159 327,946 122,155 860,952 1,878,316

Less provisions for: Medicare contractual adjustments 3,124,403 (2) - 6,383 206,719 85,987 1,632 60,701 3,405 397,538 687,396 Medicaid contractual adjustments 1,514,625 - - 1,188 233,797 4,764 3,591 5,134 (10,197) 149,796 282,334 Other contractual adjustments 2,852,729 90,150 - 11,046 194,679 263,747 1,059 133,944 14,294 138,413 508,531 Administrative adjustments 86,077 - - - 589 6,375 7 3,734 173 10,445 2,854 Charity - Other 246,996 - - - 15,842 19,479 112 1,592 7,405 4,819 51,339

Total provisions 7,824,830 90,148 - 18,617 651,626 380,352 6,401 205,105 15,080 701,011 1,532,454 Net patient service revenue 2,598,941 (90,213) - 16,058 217,868 267,488 4,758 122,841 107,075 159,941 345,862

Less provision for bad debts 113,865 - - 402 13,081 21,352 692 3,067 780 6,241 10,083 Net patient service revenue less

provision for bad debts 2,485,076 (90,213) - 15,656 204,787 246,136 4,066 119,774 106,295 153,700 335,779

Premium revenue 22,779 - - 848 - 12,972 - - 448 - - Other revenue 138,695 (110,352) 123,297 9,690 3,864 13,691 11 10,898 2,261 10,387 12,862 Net assets released from restrictions for operations 6,759 - - - 98 576 - 56 17 441 646

TOTAL UNRESTRICTED REVENUES, GAINS, AND SUPPORT 2,653,309 (200,565) 123,297 26,194 208,749 273,375 4,077 130,728 109,021 164,528 349,287

EXPENSES

Employee compensation 1,365,001 (95,787) 74,057 7,205 115,563 156,546 2,744 69,151 43,821 86,477 172,254 Professional fees 233,288 (3) 8,977 12,406 17,583 12,574 1,545 5,833 19,839 12,525 15,895 Supplies 395,525 - 2,645 1,942 29,173 35,722 375 22,704 5,768 29,036 54,210 Purchased services and other 407,658 (101,409) 26,062 4,189 29,187 48,189 416 18,533 17,585 22,434 77,867 Interest 35,747 (3,366) 7,625 - 5,678 2,881 13 538 55 1,865 5,402 Depreciation 118,760 - 12,786 422 11,858 10,880 - 5,150 1,502 5,342 17,016

TOTAL EXPENSES 2,555,979 (200,565) 132,152 26,164 209,042 266,792 5,093 121,909 88,570 157,679 342,644

EXCESS (DEFICIENCY) OF REVENUES OVER EXPENSES FROM CONTINUING OPERATIONS 97,330$ -$ (8,855)$ 30$ (293)$ 6,583$ (1,016)$ 8,819$ 20,451$ 6,849$ 6,643$

See accompanying auditors' report on supplementary information. -29-

Sonora Southern Tillamook Ukiah Walla WhiteHoward Paradise St. Helena St. Helena San Joaquin Regional South Coast California County Valley Walla Western Memorial

Memorial Valley Hospital Hospital Community Simi Valley Medical Medical Medical General Medical General Health MedicalHospital Hospital Clearlake Napa Valley Hospital Hospital Center Center Foundation Hospital Center Hospital Resources Center

18,103$ -$ 37,446$ 214,918$ 310,898$ 99,376$ 91,168$ -$ -$ 9,888$ 47,458$ 14,612$ -$ 477,895$ 50,386 - 32,017 360,015 626,323 174,244 225,863 - - 10,645 63,278 24,525 - 736,233 54,496 - 126,436 246,117 276,320 158,199 307,034 - - 53,491 120,215 70,496 24,602 427,495

- - 21,996 6,868 50,380 2,229 41,420 - - 8,834 25,818 13,970 8,840 752 122,985 - 217,895 827,918 1,263,921 434,048 665,485 - - 82,858 256,769 123,603 33,442 1,642,375

36,746 - 69,277 336,232 340,212 133,033 265,774 - - 16,099 67,027 33,468 2,983 373,793 19,435 - 54,601 106,460 128,628 37,213 85,635 - - 3,623 54,874 17,229 411 336,109 16,079 - 17,125 189,600 431,806 144,078 113,257 - - 4,301 33,580 22,767 2,490 521,783 1,969 - 3,240 5,862 19,096 652 7,231 - - 59 2,434 77 60 21,220 1,695 - 2,611 5,370 22,580 5,122 3,493 - - 5,846 2,976 3,646 14 93,055

75,924 - 146,854 643,524 942,322 320,098 475,390 - - 29,928 160,891 77,187 5,958 1,345,960 47,061 - 71,041 184,394 321,599 113,950 190,095 - - 52,930 95,878 46,416 27,484 296,415

2,246 - 6,105 5,108 12,892 5,645 5,793 - - 1,219 2,868 2,225 144 13,922

44,815 - 64,936 179,286 308,707 108,305 184,302 - - 51,711 93,010 44,191 27,340 282,493

- - - 936 - - - - - - - - - 7,575 1,078 - 1,340 11,911 8,293 1,871 6,169 - - 1,483 2,808 2,758 374 24,001

36 - 26 1,165 734 32 396 - - 843 144 52 11 1,486

45,929 - 66,302 193,298 317,734 110,208 190,867 - - 54,037 95,962 47,001 27,725 315,555

21,403 - 31,726 93,912 149,593 61,634 93,339 - - 29,966 46,031 30,948 23,935 150,483 3,740 - 11,537 19,079 19,057 4,862 20,331 - - 6,527 16,105 2,481 422 21,973 7,125 - 5,107 34,518 53,134 14,538 31,482 - - 5,619 11,671 5,263 789 44,704 6,797 - 12,055 31,115 52,749 22,226 29,146 - - 7,241 18,394 9,108 2,644 73,130

- - 983 2,493 3,790 4,464 1,968 - - - 821 518 2 17 1,018 - 2,003 7,756 10,081 5,685 5,116 - - 2,142 2,471 1,562 84 15,886

40,083 - 63,411 188,873 288,404 113,409 181,382 - - 51,495 95,493 49,880 27,876 306,193

5,846$ -$ 2,891$ 4,425$ 29,330$ (3,201)$ 9,485$ -$ -$ 2,542$ 469$ (2,879)$ (151)$ 9,362$

-30-

COMBINING STATEMENT OF OPERATIONS AND CHANGES IN NET ASSETS – Continued (In thousands of dollars)

ADVENTIST HEALTH

Year Ended December 31, 2011Adventist Adventist Adventist Adventist Adventist Central Glendale

Adjustments Health Health Medical Medical Medical Castle Valley Feather AdventistCombined and Corporate Physicians Center Center Center Medical General River MedicalBalances Eliminations Office Network (Hanford) (Portland) (Reedley) Center Hospital Hospital Center

UNRESTRICTED NET ASSETSExcess (deficiency) of revenues over expenses

from continuing operations 97,330$ -$ (8,855)$ 30$ (293)$ 6,583$ (1,016)$ 8,819$ 20,451$ 6,849$ 6,643$ Change in net unrealized gains and losses

on other-than-trading securities 6,967 7,964 1 - - - - (30) - - - Donated property and equipment 688 - - - - - - 37 - - - Net assets released from restrictions for capital additions 6,069 - - - 1,309 4 - 787 25 15 466 Transfers from (to) related parties - - 10,568 - - - - - - - -

INCREASE (DECREASE) IN UNRESTRICTED NET ASSETS BEFORE DISCONTINUED OPERATIONS 111,054 7,964 1,714 30 1,016 6,587 (1,016) 9,613 20,476 6,864 7,109

Net loss from discontinued operations (1,609) - - - - - - - - - - INCREASE (DECREASE) IN

UNRESTRICTED NET ASSETS 109,445 7,964 1,714 30 1,016 6,587 (1,016) 9,613 20,476 6,864 7,109

TEMPORARILY RESTRICTED NET ASSETSRestricted gifts and grants 15,770 - - - 823 549 - 1,293 37 504 878 Net realized and unrealized gains on investments 123 - - - - 107 - 1 - - - Change in value of split-interest agreements (3) - - - - - - (6) - - - Net assets released from restrictions (12,828) - - - (1,407) (580) - (843) (42) (456) (1,112)

INCREASE (DECREASE) IN TEMPORARILY RESTRICTED NET ASSETS 3,062 - - - (584) 76 - 445 (5) 48 (234)

PERMANENTLY RESTRICTED NET ASSETSRestricted gifts and grants 10 - - - - 10 - - - - - Net realized and unrealized gains on investments 727 - - - - - - - - - 8

INCREASE IN PERMANENTLY RESTRICTED NET ASSETS 737 - - - - 10 - - - - 8

INCREASE (DECREASE) IN NET ASSETS 113,244 7,964 1,714 30 432 6,673 (1,016) 10,058 20,471 6,912 6,883

NET ASSETS, BEGINNING OF YEAR 1,266,164 41,899 69,874 225 45,681 180,207 - 110,652 50,022 14,360 135,555

NET ASSETS, END OF YEAR 1,379,408$ 49,863$ 71,588$ 255$ 46,113$ 186,880$ (1,016)$ 120,710$ 70,493$ 21,272$ 142,438$

See accompanying auditors' report on supplementary information. -31-

Sonora Southern Tillamook Ukiah Walla WhiteHoward Paradise St. Helena St. Helena San Joaquin Regional South Coast California County Valley Walla Western Memorial

Memorial Valley Hospital Hospital Community Simi Valley Medical Medical Medical General Medical General Health MedicalHospital Hospital Clearlake Napa Valley Hospital Hospital Center Center Foundation Hospital Center Hospital Resources Center

5,846$ -$ 2,891$ 4,425$ 29,330$ (3,201)$ 9,485$ -$ -$ 2,542$ 469$ (2,879)$ (151)$ 9,362$

- - - - - - - (968) - - - - - - - - - - - - 651 - - - - - - -

196 - 35 2,000 224 - - - - - - - - 1,008 4,432 - - - (15,000) - - - - - - - - -

10,474 - 2,926 6,425 14,554 (3,201) 10,136 (968) - 2,542 469 (2,879) (151) 10,370

- (220) - - - - - (1,335) (54) - - - - -

10,474 (220) 2,926 6,425 14,554 (3,201) 10,136 (2,303) (54) 2,542 469 (2,879) (151) 10,370

51 - 156 5,260 2,609 330 379 - - 124 422 216 - 2,139 - - - 14 - - - - - - 1 - - - - - - 3 - - - - - - - - - -

(232) - (61) (3,165) (958) (32) (396) - - (843) (144) (52) (11) (2,494)

(181) - 95 2,112 1,651 298 (17) - - (719) 279 164 (11) (355)

- - - - - - - - - - - - - - - - - 719 - - - - - - - - - -

- - - 719 - - - - - - - - - -

10,293 (220) 3,021 9,256 16,205 (2,903) 10,119 (2,303) (54) 1,823 748 (2,715) (162) 10,015

28,083 14,670 (22,657) 40,155 107,161 (49,771) 34,497 (34,024) 1,175 39,702 27,123 658 4,711 426,206

38,376$ 14,450$ (19,636)$ 49,411$ 123,366$ (52,674)$ 44,616$ (36,327)$ 1,121$ 41,525$ 27,871$ (2,057)$ 4,549$ 436,221$

-32-

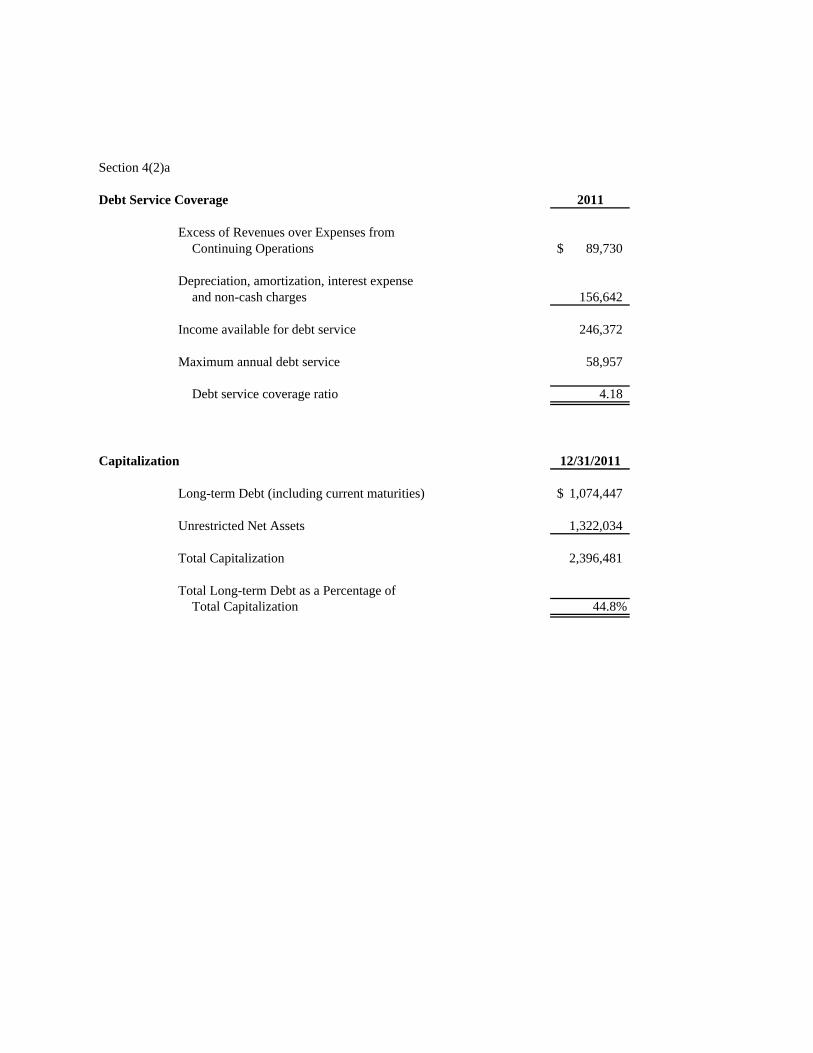

Section 4(2)a

Debt Service Coverage 2011

Excess of Revenues over Expenses fromContinuing Operations 89,730$

Depreciation, amortization, interest expenseand non-cash charges 156,642

Income available for debt service 246,372

Maximum annual debt service 58,957

Debt service coverage ratio 4.18

Capitalization 12/31/2011

Long-term Debt (including current maturities) 1,074,447$

Unrestricted Net Assets 1,322,034

Total Capitalization 2,396,481

Total Long-term Debt as a Percentage ofTotal Capitalization 44.8%

Section 4(2)(b). Below is a listing of the System's hospital facilities, grouped by state, and sortedwithin each state alphabetically.

Summary Listing of the System's Hospitals

Number of2011

at December Total RevenueObligated Group Hospital Name(1) Location 31, 2011 (in thousands)

Adventist Medical Center - Hanford Hanford, CA 199 $208,749

Central Valley General Hospital Hanford, CA 49 109,021

Feather River Hospital Paradise, CA 100 164,528

Glendale Adventist Medical Center Glendale, CA 457 349,287

St Helena Hospital Deer Park, CA 212 193,298

San Joaquin Community Hospital Bakersfield, CA 255 317,734

Sonora Regional Medical Center Sonora, CA 152 190,867

Simi Valley Hospital Simi Valley, CA 144 110,208

Ukiah Valley Medical Center Ukiah, CA 78 95,962