mr green & co ab -...

TRANSCRIPT

Mr Green & Co AB

Interim Report January-June 2017

Per Norman CEO & Simon Falk CFO

21 July 2017 conference call

2Q217 vs Q216

Revenues +36.3%

EBITDAmargin18.2%

Customerdeposits+34.4%

Strong financial development

3ALL TIME HIGH ACROSS ALL KEY FINANCIALS

Q217 Q216 Change H117 H116 Change

287.8 211.2 36.3% 563.9 429.7 31.2%

Revenue, MSEK

Q217 Q216 Change H117 H116 Change

52.4 12.0 337% 86.6 42.2 105%

EBITDA, MSEK

Q217 Q216 Change H117 H116 Change

35.5 -3.1 N.A. 55.0 13.7 302%

EBIT, MSEK

Q217 Q216 Change H117 H116 Change

0.90 -0.13 N.A. 1.43 0.55 159%

EPS, SEK

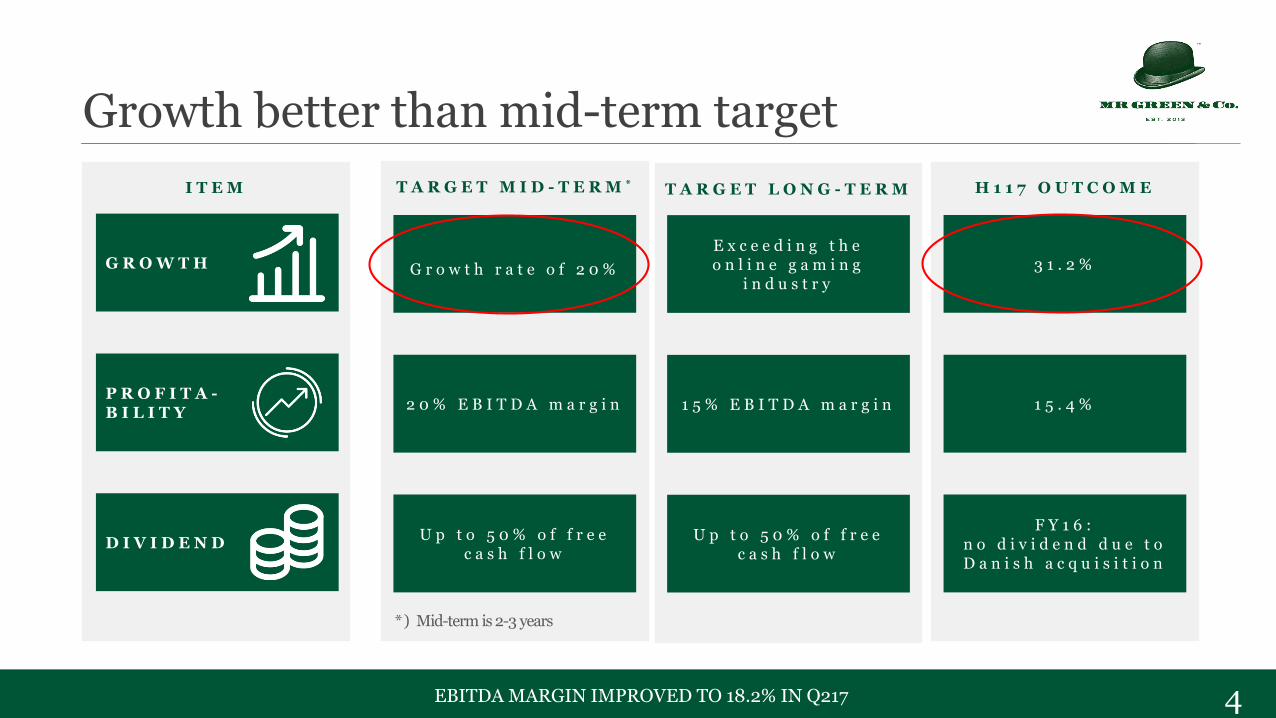

Growth better than mid-term target

4EBITDA MARGIN IMPROVED TO 18.2% IN Q217

T A R G E T L O N G - T E R MT A R G E T M I D - T E R M * H 1 1 7 O U T C O M EI T E M

G R O W T H

P R O F I T A -B I L I T Y

D I V I D E N D

G r o w t h r a t e o f 2 0 %

2 0 % E B I T D A m a r g i n

U p t o 5 0 % o f f r e e c a s h f l o w

3 1 . 2 %

1 5 . 4 %

F Y 1 6 :n o d i v i d e n d d u e t o D a n i s h a c q u i s i t i o n

E x c e e d i n g t h e o n l i n e g a m i n g

i n d u s t r y

1 5 % E B I T D A m a r g i n

U p t o 5 0 % o f f r e e c a s h f l o w

*) Mid-term is 2-3 years

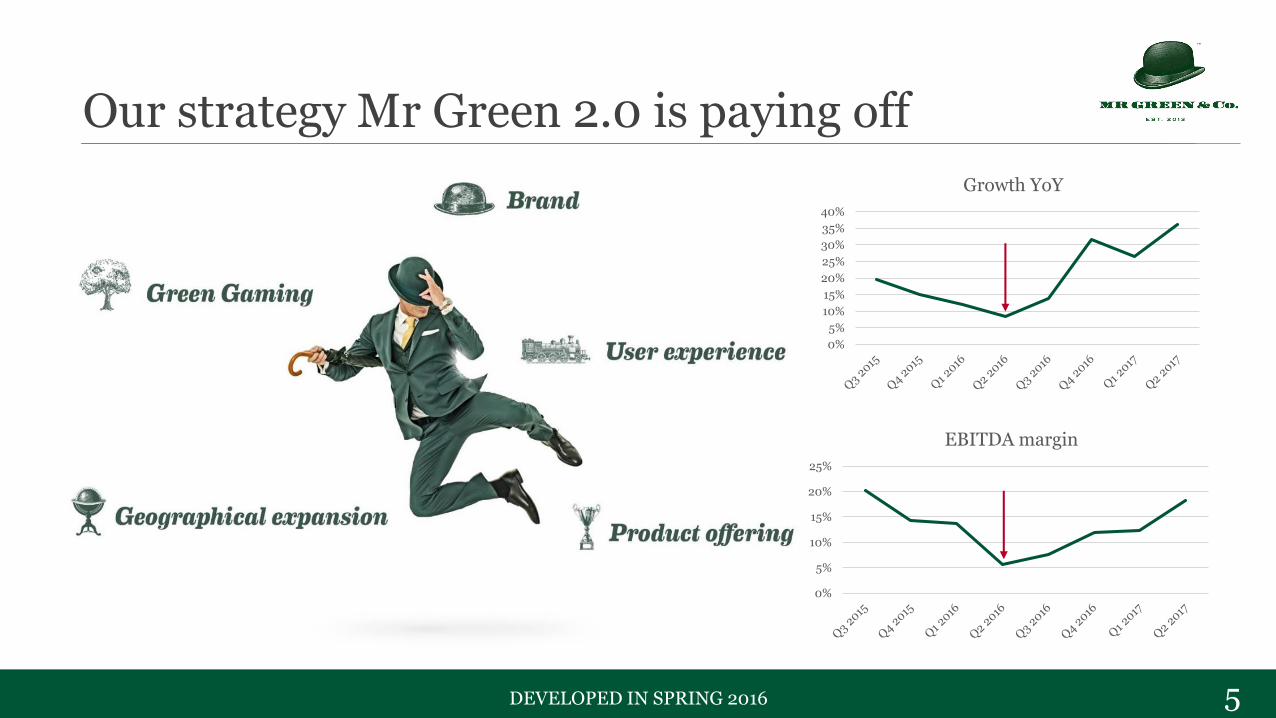

Our strategy Mr Green 2.0 is paying off

5DEVELOPED IN SPRING 2016

0%

5%

10%

15%

20%

25%

30%

35%

40%

Growth YoY

0%

5%

10%

15%

20%

25%

EBITDA margin

Sportsbook 2.0 New customer loyalty

program Launch Mr Green in

Denmark Number games –

bingo, keno, lotto across all markets

Continued geographic expansion organic and/or M&A driven

20172016 Q117

Our strategic actions

6CONTINOUS DEVELOPMENT OF DATA AND BI DRIVEN CUSTOMER COMMUNICATION TO PERSONALISE AND ENTERTAIN

Reel Thrill Tourna-ments launched

New subsidiary Wizard’s Hat Ltd

Acquisition of Dansk Underholdning

Initiated operations in Latin America

Enhanced digital marketing

New management teams in place

New technology platform

Data and BI-driven customer communication

Sportsbook 1.0 New live casino Listing on Nasdaq

Stockholm GRI reporting

Placement of new shares

Relaunch of casino site Garbo

Green Gaming predictive tool ready for launch

Completion of acquisition of Dansk Underholdning

Increased focus on the Nordics

Keno ready for launch

Q217

Mr Green’s new predictive Green Gaming tool

7

Developed in-house together with Sustainable

Interaction

Used together with Gamtest

Will identify risk behaviour on an individual

level

Offer self tests, breaks, self exclusion, cool down

games, self help (cognitive) etc.

To be launched in Q317

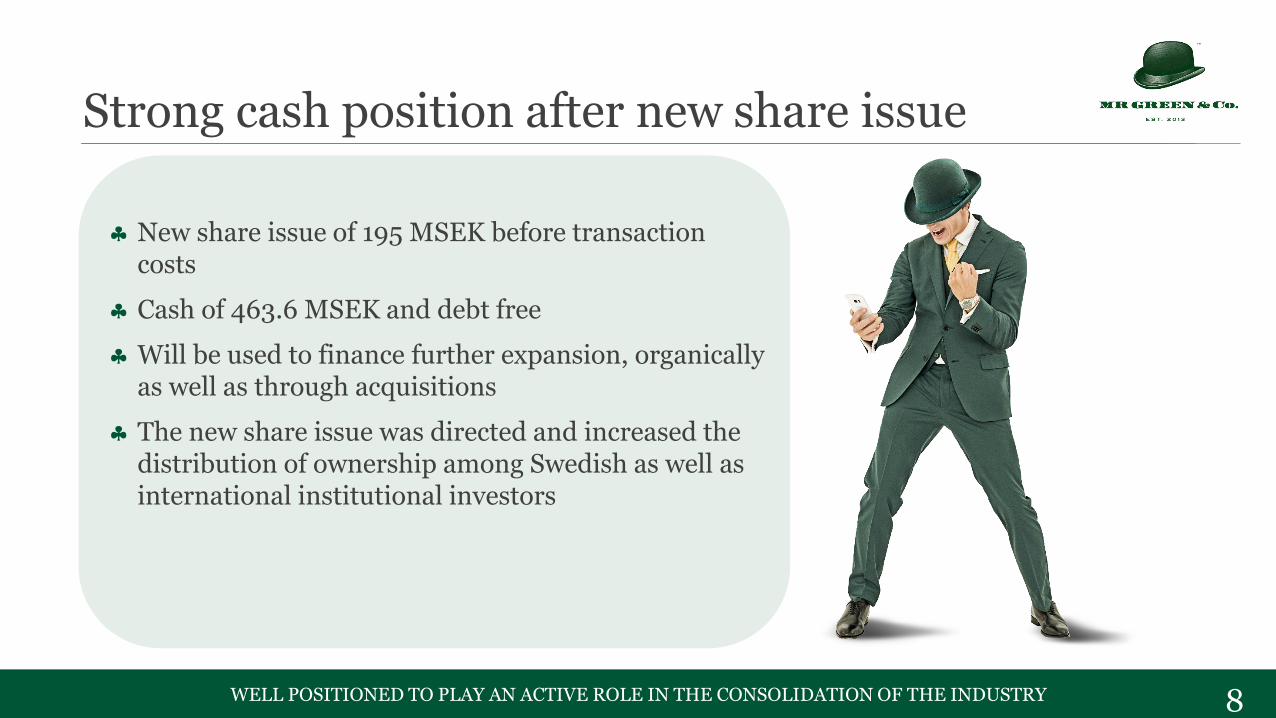

Strong cash position after new share issue

8WELL POSITIONED TO PLAY AN ACTIVE ROLE IN THE CONSOLIDATION OF THE INDUSTRY

New share issue of 195 MSEK before transaction costs

Cash of 463.6 MSEK and debt free

Will be used to finance further expansion, organically as well as through acquisitions

The new share issue was directed and increased the distribution of ownership among Swedish as well as international institutional investors

Financials

0%

10%

20%

30%

40%

50%

60%

0

100

200

300

400

500

600

700

800

900

1 000

Customer deposits, MSEK YoY growth, %

Record high number of customers

-10%

0%

10%

20%

30%

40%

50%

60%

0

20 000

40 000

60 000

80 000

100 000

120 000

140 000

Active customers YoY growth, %

NUMBER OF ACTIVE CUSTOMERS

116,674

10

Number of active customers

+25.8% from Q216

Customer deposits +34.4%

from Q216

CUSTOMER DEPOSITS

25.8%

808.6 MSEK

34.4%

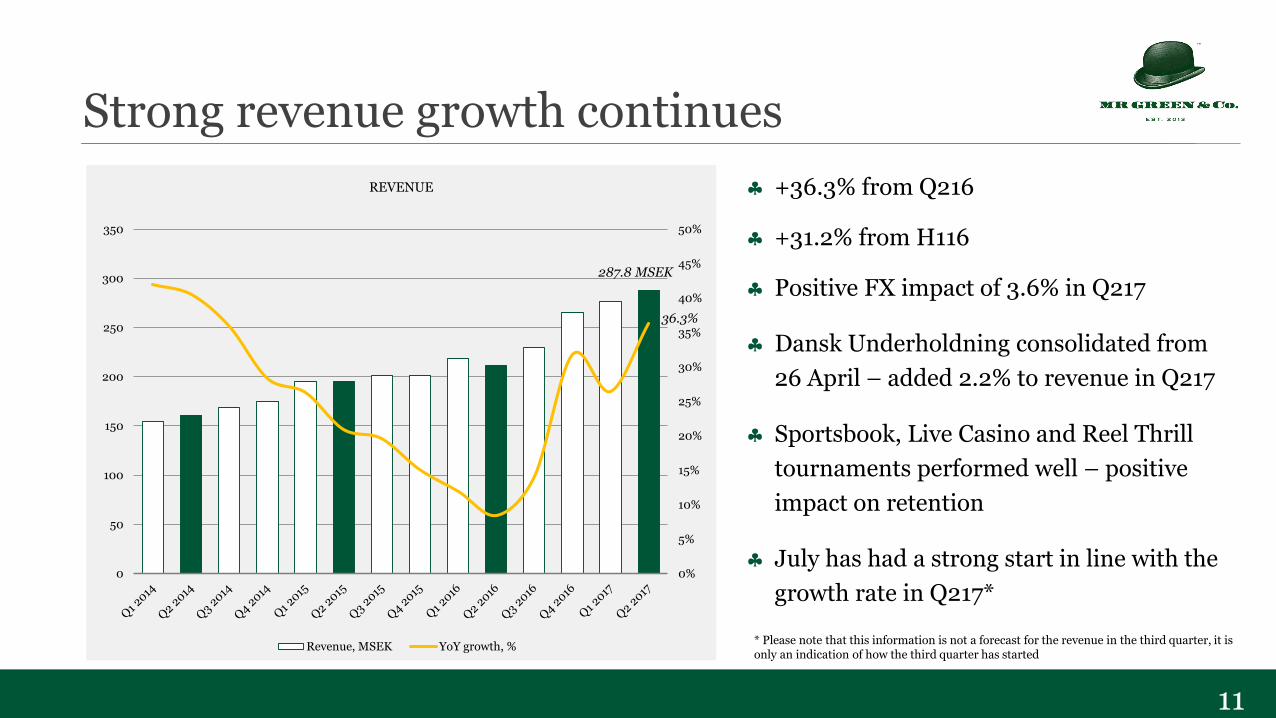

Strong revenue growth continues

11

REVENUE

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

50

100

150

200

250

300

350

Revenue, MSEK YoY growth, %

+36.3% from Q216

+31.2% from H116

Positive FX impact of 3.6% in Q217

Dansk Underholdning consolidated from

26 April – added 2.2% to revenue in Q217

Sportsbook, Live Casino and Reel Thrill

tournaments performed well – positive

impact on retention

July has had a strong start in line with the

growth rate in Q217*

287.8 MSEK

36.3%

* Please note that this information is not a forecast for the revenue in the third quarter, it is only an indication of how the third quarter has started

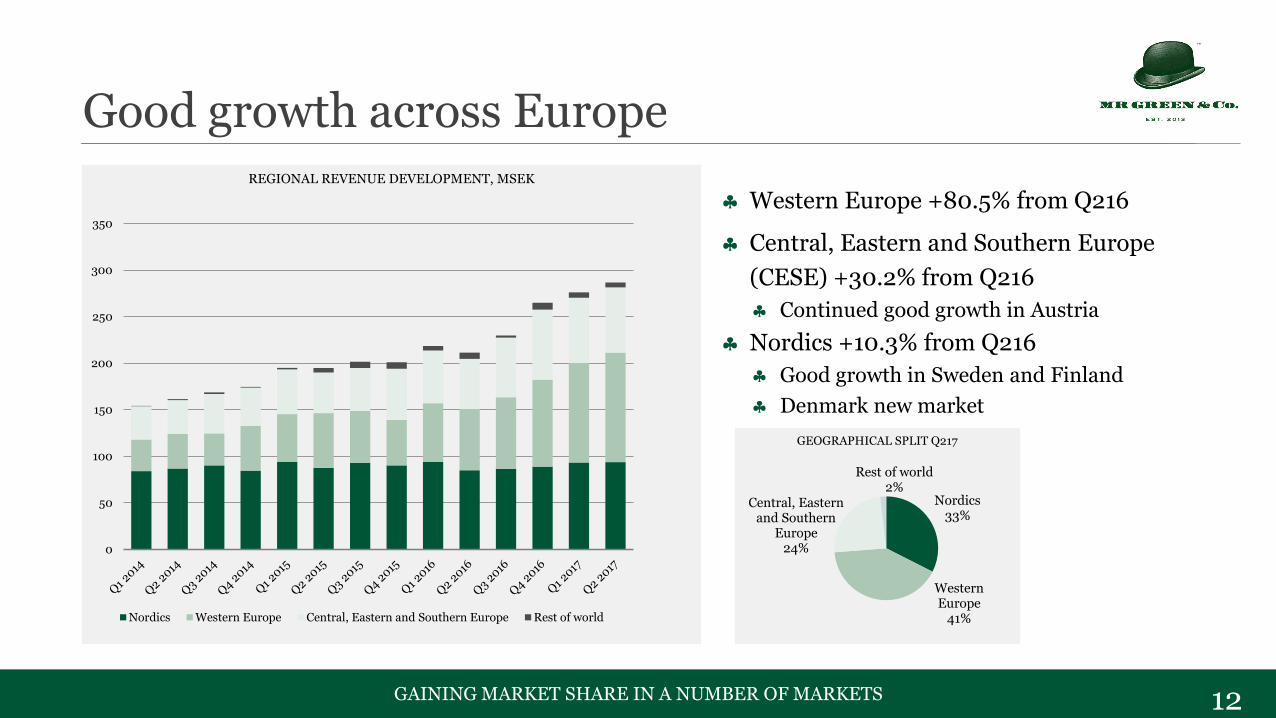

Good growth across Europe

12GAINING MARKET SHARE IN A NUMBER OF MARKETS

REGIONAL REVENUE DEVELOPMENT, MSEK

0

50

100

150

200

250

300

350

Nordics Western Europe Central, Eastern and Southern Europe Rest of world

Western Europe +80.5% from Q216

Central, Eastern and Southern Europe

(CESE) +30.2% from Q216

Continued good growth in Austria

Nordics +10.3% from Q216

Good growth in Sweden and Finland

Denmark new market

GEOGRAPHICAL SPLIT Q217

Nordics33%

Western Europe

41%

Central, Eastern and Southern

Europe24%

Rest of world2%

Decreased CoS and marketing ratios

13MARKETING RATIO EXPECTED TO INCREASE COMING QUARTERS DUE TO PRODUCT LAUNCHES

0%

10%

20%

30%

40%

0

20

40

60

80

100

120

CoS, MSEK CoS/revenue, % CoS excl betting duties/revenue, %

0%

10%

20%

30%

40%

50%

60%

0

20

40

60

80

100

120

Marketing cost, MSEK Marketing cost/revenue, %

COST OF SERVICES SOLD MARKETING COST

30.3%

87.3 MSEK

15.1%

32.1%

92.5 MSEK

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

0

5

10

15

20

25

30

35

40

Personnel cost, MSEK Personnel cost/revenue, %

35.2 MSEK

12.2%

Stable development in personnel cost

14OTHER OPEX IMPACTED BY IT COSTS RELATED TO HIGH PROJECT ACTIVITY

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

0

5

10

15

20

25

30

35

40

45

Other cost Other cost/Revenue

41.1 MSEK

14.3%

PERSONNEL COST OTHER OPEX

EBITDA

0,0%

5,0%

10,0%

15,0%

20,0%

25,0%

30,0%

0

10

20

30

40

50

60

EBITDA, MSEK EBITDA margin, %

18.2%

Strong improvement in EBITDA

15

EBITDA 52.4 MSEK and EBITDA

margin 18.2%

Improved profitability mainly due to

strong revenue growth and increased

marketing efficiency

Austrian self assessment a

precautionary measure

Negotiations were conducted at the

court of first instance in Austria

We do not expect the matter to be

resolved in the near future

Note: EBITDA before non-recurring items

52.4 MSEK

Betting duties 15.2%

Betting duties 4.0%

Summary

Key profitability drivers in Q217

17CLEAR STRATEGY TO REACH 20% EBITDA TARGET

New taxes in existing markets

Taxes from new markets

Tax sharing Lower rates in %

due to higher revenues

Taxed markets give access to more beneficial payment

Lower rates in % due to higher volumes

Improved conversion

Cost sharing related to betting duties

Improved retention Increased digital

media use Increased organic

traffic generation

Economy of scale

Continuous cost consciousness

EBITDA margin

EBITDA margin

Mid-term target

20%

Illustrative

Taxes Game suppliers

PaymentMarketing efficiency

OPEX

Much more to come

18AIMING TO BE A PLAYER IN THE INDUSTRY CONSOLIDATION

Launching:

Mr Green in DenmarkSportsbook 2.0

New customer loyalty programGreen Gaming predictive toolNumber games across Europe

♣ Good growth momentum

♣ Accelerating with new strategic initiatives

♣ Further raising our level of ambition

19

Q&A