moving pakistan forward -...

TRANSCRIPT

ANNUAL REPORT 2013

MovingPakistanForward

02 Profile

03 Mission Statement

04 Executive Committee 2013

05 Executive Committee 2014

06 Past Presidents

07 List of Members

08 Members’ Contributions to Pakistan’s Economy

09 Executive Committee’s Report

10 Highlights of the year

19 Programs & Events Photo Gallery

33 Reports of Sub-Committees

34 Finance & Taxation

36 HR & CSR

38 Industry & Trade

39 IPR & Legal

40 Media, PR & Programs

42 Pharmaceutical & Agricultural Chemicals

44 Membership & Admin

45 North Members

46 Security

48 US Relations

50 ABC Representation Annexures

54 ABC Suggestions For The Federal Budget 2013-14 “A”

66 Summary of the ABC Suggestions for the Trade Policy 2013-14 “B”

69 Financial Statements

96 Appreciation

Contents

The American Business Council of PakistanF-30, Block 7, KDA Scheme # 5, Kehkashan, Clifton, Karachi, Pakistan. G.P.O. Box 1322

T: (92-21) 35877351-52, 35877390 F: (92-21) 35877391 E-mail: [email protected]

Website: www.abcpk.org.pk

ProfileThe American Business Council of Pakistan (ABC) was formed in 1984 and has completed 30 years of service to Pakistan, playing a major role in bridging investments from the United States.

The ABC is one of the largest investors group in Pakistan – currently, we have 65 members and most of them are Fortune 500 companies. They operate in various sectors i.e. healthcare, financial services, information technology, chemicals & fertilizers, energy, FMCG, food & beverage, oil & gas and others. ABC members have cumulative revenues of US$ 4.0 billion and an investment of over US$ 770 million. Our members contribute a sizable amount to the national exchequer every year as direct and indirect taxes – last year they contributed Rs. 87 billion. The ABC members also employ over 42,000 people directly who support 170,000 dependents and indirectly employ nearly one million people with agents, distributors, contractors, etc.

The Council is managed by an Executive Committee that is elected every year by its members and meets monthly to review various aspects of its ongoing initiatives. Depending on the economic cycle the initiatives may vary from year to year. Sub-Committees are formed, which meet regularly, to ensure that adequate focus is given to important issues affecting majority of Council membership.

The ABC is an effective channel for dialogue with the Government of Pakistan. Regular suggestions and input for improvement are provided to the relevant bodies like ministries, regulatory and tax authorities, etc., throughout the year. The focus of the Executive Committee is to ensure that the ABC’s suggestions are incorporated in the annual Federal Budget and Trade Policy. The Council also facilitates direct interaction with the Federal and Provincial governments through its guest speakers’ program, seminars and events all of which are aimed at sustaining an ongoing dialogue.

The ABC is affiliated with the Federation of Pakistan Chambers of Commerce & Industry (FPCCI) and is a member of the U.S. Chamber of Commerce (USCC), Washington D.C., and Asia-Pacific Council of American Chambers of Commerce (APCAC). ABC also has a close working relationship with the U.S.-Pakistan Business Council, Washington which is a component of the USCC.

Key ABC’s Objectives are:

• To raise the profile of the ABC so as to ensure it is seen not only as a progressive body but also results in the greater participation and engagement of members.

• Increase the inclusivity of the North-Based membership • Play an active role and engage with Govt. bodies, including IPOP, FBR, BoI and relevant Govt.

Ministries. • Lobby the Govt. on taxation issues effecting ABC member Companies • Address the issues posed by the power sector and engage with the Govt. to try and find solutions • Seek ways of working around the law & order and security threats effecting the smooth running of

business in Pakistan • To recognize the contribution of ABC members towards their commitment to continuously upgrade

processes, systems, products and services, and create value for their employees, existing and potential customers and the local communities they operate in.

02

Mission Statement

To Protect and promote the interests of U.S.

Investors in Pakistan; to encourage and

stimulate new investments; to introduce

and inculcate best practices; To strive to

establish a level playing field in the country

in order to promote the development of

commerce between the USA and

Pakistan.

03

ANNUAL REPORT 2013

Mr. Mohammad Iqbal ShekhaniChief Executive OfficerJohan (Pvt.) Ltd. (Culligan)

Mr. Saad Amanullah KhanChief Executive OfficerGillette Pakistan Ltd.

Mr. Tasleemuddin Ahmed BatlayDirectorColgate-Palmolive (Pakistan) Ltd.

Mr. Akram Wali MohammadChief ExecutiveGerry’s International (Pvt.) Ltd. (FedEx)

Mr. Irshad Ali KassimChairmanKaram Ceramics Limited

Mr. Arshad Saeed HusainManaging DirectorAbbott Laboratories Pakistan (Pvt.) Ltd.

Executive Committee 2013

PRESIDENTMr. Farrokh K. CaptainChairman & Managing DirectorCaptain-PQ Chemical Industries (Pvt.) Ltd.

Mr. Tauqir AhmedChief ExecutiveDuPont Pakistan Operations (Pvt.) Ltd.

Mr. Nadeem Arshad ElahiManaging Director & Country HeadTRG (Pvt.) Ltd.

Mr. Ahmed Jamal MirManaging Director& CEOPrestige Communications (Pvt.) Ltd. (GREY)

Ms. Zehra NaqviChief ExecutiveACE InsuranceLimited

Mr. Muhammad Navid QaziCountry General ManagerCisco Systems Pakistan (Pvt.) Ltd.

Mr. Faisal Hamid SabzwariCountry ManagerProcter & Gamble Pakistan (Pvt.) Ltd.

VICE PRESIDENTMr. Osman Asghar KhanChief Executive OfficerEMC Information Systems (Pvt.) Ltd.

MEMBERS

SUB-COMMITTEE CHAIRMENSECRETARY GENERAL

Ms. Aisha Kirmani

04

AUDITORSKPMG Taseer Hadi & Company

BANKERSCitibank, N.A.

Tax AdvisorsPlus Consultants

Executive Committee 2014

Dr. Farid KhanManaging DirectorPfizer Pakistan Ltd.

Mr. Tasleemuddin Ahmed BatlayDirectorColgate-Palmolive (Pakistan) Ltd.

Mr. Arshad Saeed HusainManaging DirectorAbbott Laboratories (Pakistan) Ltd.

Mr. Amin Mohammad KhowajaExecutive Director & General ManagerJ.P. Morgan Pakistan (Pvt.) Ltd.

MEMBERS

Mr. Faisal Hamid SabzwariCountry ManagerProcter & Gamble Pakistan (Pvt.) Ltd.

Mr. Nadeem LodhiManaging Director & Citi Country OfficerCitibank, N.A.

Mr. Ahmed Jamal MirManaging Director& CEOPrestige Communications (Pvt.) Ltd. (GREY)

Ms. Zehra NaqviChief ExecutiveACE Insurance Limited

VICE PRESIDENTMr. Akram Wali MohammadGroup Managing DirectorGerry’s International (Pvt.) Ltd. (FedEx)

SENIOR VICE PRESIDENTMr. Tauqir AhmedChief ExecutiveDuPont Pakistan Operations(Pvt.) Ltd.

PRESIDENTMr. Saad Amanullah KhanChief Executive OfficerGillette Pakistan Ltd.

05

Ms. Aisha Kirmani

SECRETARY GENERAL

AUDITORSKPMG Taseer Hadi & Company

BANKERSCitibank, N.A.

Tax AdvisorsPlus Consultants

Mr. Aamir M. MirzaPakistan Country Lead Monsanto Pakistan (Pvt.) Ltd.

SUB COMMITTEE CHAIRMAN

ANNUAL REPORT 2013

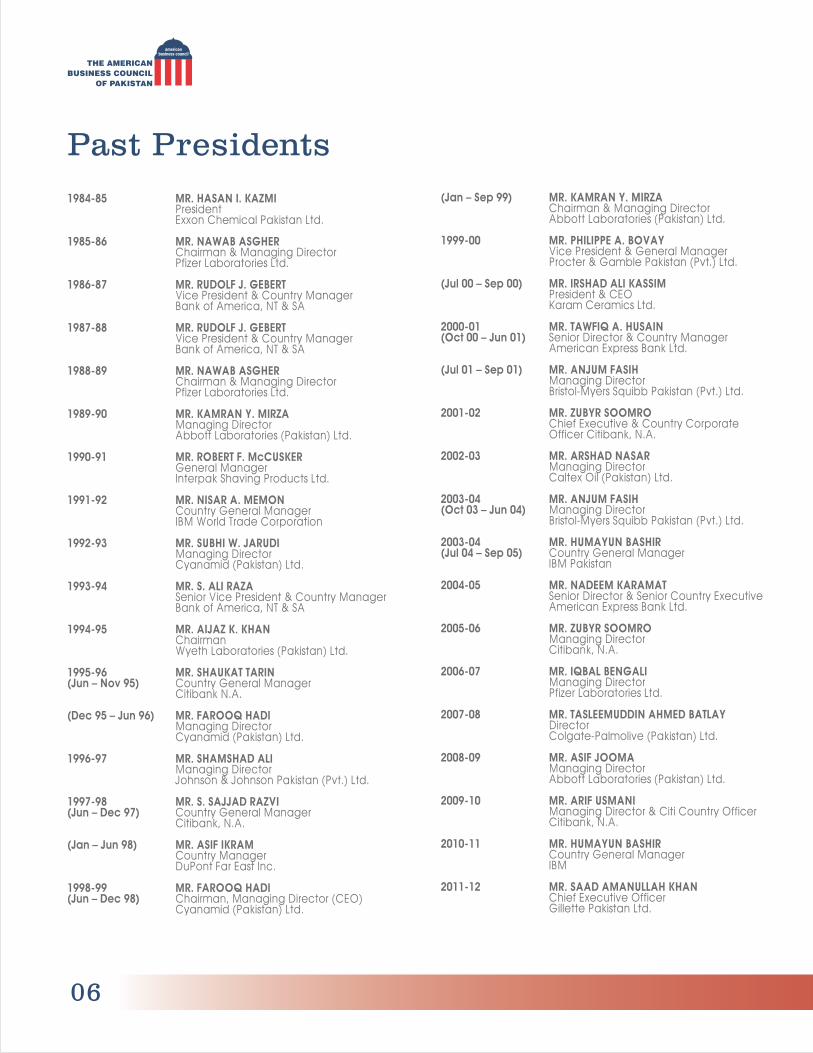

Past Presidents1984-85 MR. HASAN I. KAZMI President Exxon Chemical Pakistan Ltd. 1985-86 MR. NAWAB ASGHER Chairman & Managing Director Pfizer Laboratories Ltd. 1986-87 MR. RUDOLF J. GEBERT Vice President & Country Manager Bank of America, NT & SA 1987-88 MR. RUDOLF J. GEBERT Vice President & Country Manager Bank of America, NT & SA 1988-89 MR. NAWAB ASGHER Chairman & Managing Director Pfizer Laboratories Ltd. 1989-90 MR. KAMRAN Y. MIRZA Managing Director Abbott Laboratories (Pakistan) Ltd. 1990-91 MR. ROBERT F. McCUSKER General Manager Interpak Shaving Products Ltd. 1991-92 MR. NISAR A. MEMON Country General Manager IBM World Trade Corporation 1992-93 MR. SUBHI W. JARUDI Managing Director Cyanamid (Pakistan) Ltd. 1993-94 MR. S. ALI RAZA Senior Vice President & Country Manager Bank of America, NT & SA 1994-95 MR. AIJAZ K. KHAN Chairman Wyeth Laboratories (Pakistan) Ltd. 1995-96 MR. SHAUKAT TARIN(Jun – Nov 95) Country General Manager Citibank N.A.

(Dec 95 – Jun 96) MR. FAROOQ HADI Managing Director Cyanamid (Pakistan) Ltd. 1996-97 MR. SHAMSHAD ALI Managing Director Johnson & Johnson Pakistan (Pvt.) Ltd. 1997-98 MR. S. SAJJAD RAZVI(Jun – Dec 97) Country General Manager Citibank, N.A. (Jan – Jun 98) MR. ASIF IKRAM Country Manager DuPont Far East Inc.

1998-99 MR. FAROOQ HADI(Jun – Dec 98) Chairman, Managing Director (CEO) Cyanamid (Pakistan) Ltd.

(Jan – Sep 99) MR. KAMRAN Y. MIRZA Chairman & Managing Director Abbott Laboratories (Pakistan) Ltd. 1999-00 MR. PHILIPPE A. BOVAY Vice President & General Manager Procter & Gamble Pakistan (Pvt.) Ltd. (Jul 00 – Sep 00) MR. IRSHAD ALI KASSIM President & CEO Karam Ceramics Ltd. 2000-01 MR. TAWFIQ A. HUSAIN(Oct 00 – Jun 01) Senior Director & Country Manager American Express Bank Ltd. (Jul 01 – Sep 01) MR. ANJUM FASIH Managing Director Bristol-Myers Squibb Pakistan (Pvt.) Ltd. 2001-02 MR. ZUBYR SOOMRO Chief Executive & Country Corporate Officer Citibank, N.A. 2002-03 MR. ARSHAD NASAR Managing Director Caltex Oil (Pakistan) Ltd.

2003-04 MR. ANJUM FASIH(Oct 03 – Jun 04) Managing Director Bristol-Myers Squibb Pakistan (Pvt.) Ltd. 2003-04 MR. HUMAYUN BASHIR(Jul 04 – Sep 05) Country General Manager IBM Pakistan 2004-05 MR. NADEEM KARAMAT Senior Director & Senior Country Executive American Express Bank Ltd. 2005-06 MR. ZUBYR SOOMRO Managing Director Citibank, N.A. 2006-07 MR. IQBAL BENGALI Managing Director Pfizer Laboratories Ltd. 2007-08 MR. TASLEEMUDDIN AHMED BATLAY Director Colgate-Palmolive (Pakistan) Ltd. 2008-09 MR. ASIF JOOMA Managing Director Abbott Laboratories (Pakistan) Ltd. 2009-10 MR. ARIF USMANI Managing Director & Citi Country Officer Citibank, N.A. 2010-11 MR. HUMAYUN BASHIR Country General Manager IBM 2011-12 MR. SAAD AMANULLAH KHAN Chief Executive Officer Gillette Pakistan Ltd.

06

List of ABC MembersCORPORATE MEMBERS

1. Abbott Laboratories (Pakistan) Ltd.2. ACE Insurance Limited3. ACNielsen Pakistan (Pvt.) Ltd.4. American Life Insurance Company (Pakistan) Limited5. Becton Dickinson Pakistan (Pvt.) Ltd.6. Captain-PQ Chemical Industries (Pvt.) Ltd.7. Chevron Pakistan Ltd.8. Cisco Systems Pakistan (Pvt.) Ltd.9. Citibank, N.A.10. Coca-Cola Beverages Pakistan Ltd.11. Colgate-Palmolive (Pakistan) Ltd.12. Continental Biscuits Ltd.13. Crescent Bahuman Limited14. Cresox (Pvt.) Limited15. DuPont Pakistan Operations (Pvt.) Ltd.16. Eli Lilly Pakistan (Pvt.) Ltd.17. El Paso Technology Pakistan (Pvt.) Ltd.18. EMC Information Systems (Pvt.) Ltd.19. F.C.I. International (Pvt.) Ltd.20. FMC United (Pvt.) Ltd.21. Gerry’s International (Pvt.) Ltd. (FedEx)22. Gillette Pakistan Limited23. IBM24. Intel Pakistan Corporation25. International Franchises (Pvt.) Ltd. (Dunkin Donuts)26. International Learning Center (Pvt.) Ltd. (Berlitz)27. Johan (Pvt.) Ltd. (Culligan)28. Johnson & Johnson Pakistan (Pvt.) Ltd.29. J.P. Morgan Pakistan (Pvt.) Limited30. Karam Ceramics Limited31. LMK Resources Pakistan (Pvt.) Ltd.32. Levi Strauss Pakistan (Pvt.) Limited33. MCR (Pvt.) Ltd. (Pizza Hut)34. Microsoft Corporation Pakistan Liaison Office35. Monsanto Pakistan (Pvt.) Ltd.36. Muller & Phipps Pakistan (Pvt.) Ltd.37. NCR Corporation38. New Hampshire Insurance Company

39. OBS Pakistan (Pvt.) Ltd.40. Ogilvy & Mather Pakistan (Pvt.) Ltd.41. Optimus Ltd. (Hertz)42. Oracle Corporation43. Pepsi-Cola International (Pvt.) Ltd.44. Pfizer Pakistan Ltd.45. Philip Morris (Pakistan) ltd.46. Prestige Communications (Pvt.) Ltd. (GREY)47. Primatics Financial (Pvt.) Ltd.48. Procter & Gamble Pakistan (Pvt.) Ltd.49. Rafhan Maize Products Co. Ltd.50. Riaz Bottlers (Pvt.) Ltd. (PepsiCo)51. Sakonent (SMC-Pvt.) Ltd.52. S.C. Johnson & Son of Pakistan (Pvt.) Ltd.53. Sheraton Middle East Management Corporation54. Singer Pakistan Limited55. Siza Foods (Pvt.) Ltd. (McDonald’s)56. Teradata Global Consulting Pakistan (Pvt.) Ltd.57. Teradata Pakistan (Pvt.) Ltd.58. The Coca-Cola Export Corporation59. TRG (Pvt.) Ltd.60. 3M Pakistan (Pvt.) Ltd.61. Unisys Pakistan (Pvt.) Limited62. Universal Logistics Services (Pvt.) Ltd. (UPS)63. Visa Worldwide Singapore Pte. Limited64. Vision Network Television Ltd. (CNBC)65. WPP Marketing Communications (Pvt.) Ltd. (JWT)

ASSOCIATE MEMBER

1. Sun Consulting (Pvt.) Ltd.

MEMBERSHIP BY CATEGORY

Industrial Undertakings 17Trading 06Financial Institutions 06Others 37Quoted at Karachi Stock Exchange 11

07

ANNUAL REPORT 2013

08

Member Companies' Contribution To Pakistan’s Economy*The ABC Financial Survey 2013 indicates that our member companies make a significant contribution to Pakistan’s economy, as follows:

Investment and Revenue Update

The ABC members have cumulative revenues of US$ 4.0 billion with an investment of over US$ 770 million.

Contribution to National Exchequer

The ABC members contribute a sizable amount to the national exchequer every year as direct and indirect taxes – last year the contribution was Rs. 87 billion.

Exports

The ABC members’ exported goods worth Rs. 13 billion during 2013.

Human Resources

The ABC member companies employed over 42,000 persons directly, who support 170,000 dependents and indirectly employ nearly one million people with their agents, distributors, suppliers, contractors, etc.

*The numbers quoted represent 66% of ABC Members

Executive Committee Report 2012-13

OVERVIEW During 2013 The American Business Council of

Pakistan (ABC) remained active in its efforts to promote, support, and advocate for its members. The business climate was difficult with the year opening on an unsteady note as a general sense of uncertainty prevailed in the run up to the Federal Elections in May 2013 and security remaining an on-going area of concern. Despite the challenging operating environment, ABC members maintained a growth trajectory and remained committed to doing business responsibly in Pakistan.

The Executive Committee maintained an

inclusive stance, seeking regular input from members and respective Sub-Committees on various matters including the Federal Budget, Trade Policy, Human Resources and Security. Representatives of the ABC met with heads of numerous government departments and concerned functionaries of the government, including the Prime Minister, Federal Minister for Finance, Chairman BoI, Federal Secretary Commerce & Chairman Federal Board of Revenue. During these meetings policy recommendations in support of an economic climate conducive to growth, development of human capital and foreign investment were put forth.

The United States (U.S.) is one of Pakistan’s most important export markets and the ABC members are a major source of investment in Pakistan. In an effort to facilitate U.S. investment, business travel to the U.S. and dialog with visitors on behalf of its members, the ABC Executive Committee worked closely with agencies of the American Government. A strong working relationship was maintained with the U.S. Embassy in Islamabad and U.S. Consulate in Karachi.

The participation of every member company

is greatly appreciated and essential to the ABC’s success as well as for the cultivation of the fundamentals of a strong business climate that can support and drive a vibrant economy. While the ABC will continue to provide a platform for its members to network and share ideas through regular events and conferences, for the year ahead we look towards our members for their active involvement to further ABC’s mission whilst making it an effective tool to represent and leverage U.S. enterprises in Pakistan.

09

ANNUAL REPORT 2013

Highlights of the Year

1. ABC SUGGESTIONS TO THE FEDERAL GOVERNMENT

(a) Suggestions for the Federal Budget 2013-14

The American Business Council greatly appreciated the Government’s consultative efforts to involve all chambers and business forums in the budget preparation process. The Council submitted its proposals relating to tax and procedural issues (Annexure “A”) to the Federal Board of Revenue, Ministry of Commerce and the Board of Investment in May 2013.

(b) Suggestions for the Trade Policy 2013-14

The American Business Council suggestions for Trade Policy (Import/Export) 2013-14 were submitted to the Ministry of Commerce, Federal Board of Revenue and the Board of Investment in May 2013.

MEETINGS

• Executive Committee meeting with USAID Regional Director - January 11th, 2013

The Executive Committee met outgoing Regional Director USAID, Mr. Ed Birgells and his successor Mr. Leon Waskin at the ABC Secretariat in Karachi. The Executive Committee thanked Mr. Ed Birgells for his contributions and support and wished Mr. Leon Waskin success in his new role. The role of the private sector in USAID development initiatives was discussed. The possibility of USAID partnering with the Corporate Social Responsibility (CSR) departments of the ABC member companies to facilitate an exchange of information on the work being carried out by various NGOs was also discussed.

• Executive Committee meeting with the U.S. Consul General - January 17th, 2013

On invitation of the United States Consul General (USCG) in Karachi Mr. Michael Dodman, the newly elected ABC Executive Committee members attended a lunch meeting at USCG’s residence in Karachi.

Mr. Farrokh K. Captain, President of ABC briefed the Consul General on ABC’s plan for the upcoming year and reiterated the ABC’s commitment to raise its profile. Mr. Michael Dodman welcomed the incoming

ABC Executive Committee and expressed his appreciation for the initiatives being undertaken by ABC members in Pakistan.

• ABC lunch meeting with the American Journalists - January 22nd, 2013

The delegation from the International Center for Journalists met the ABC members over lunch in Karachi. The purpose of this visit was to develop a long-term partnership between news organizations and content creators. Intended to provide media professionals with an opportunity to gain insight into the culture and traditions of Pakistan, this initiative is likely to contribute towards a better understanding of Pakistan by the American audience.

• ABC Executive Committee’s visit to the U.S. Embassy - February 25th, 2013

ABC Executive Committee members led by the President of ABC, Mr. Farrokh K. Captain met the U.S. Ambassador H.E. Richard Olson; Robert Ewing, Economic Counselor; Jim Fluker, Commercial Counselor; Daniel Goodspeed, Consular Section Official; John Eustace, Regional Security Official; Justin Diaz and other Economic Section and U.S. Commercial Service Officials at the U.S. Embassy in Islamabad.

10

Highlights of the Year• ABC President & Executive Director’s meeting

with Federal Minister for Finance & Chairman, BoI - February 25th, 2013

Mr. Farrokh K. Captain, ABC President and Ms. Raheen Mani, Executive Director met with Senator Saleem H. Mandviwalla, Federal Minister for Finance & Chairman, Board of Investment (BoI) on 25th February at his office in Islamabad. During the meeting the President ABC requested the ABC’s representation on government Advisory Councils of Commerce & Finance, the Chairman BoI graciously agreed to endorse the ABC’s request for active representation on the Advisory Councils of the Ministries of Commerce & Finance.

• ABC President & Executive Director meet with Chairman, Federal Board of Revenue – February 26th, 2013

Mr. Farrokh K. Captain, President of ABC and Ms. Raheen Mani, Executive Director met

Mr. Ali Arshad Hakeem, Chairman Federal Board of Revenue (FBR) in Islamabad. The ABC President stressed on the importance of having a transparent taxation system. The Chairman FBR lauded the ABC members for their contribution towards national exchequer and assured the President that ABC’s taxation proposals and policy recommendations will be taken into consideration. The Chairman FBR expressed his willingness to address ABC members as a Guest Speaker.

• ABC President & Executive Director meet Secretary Commerce - February 26th, 2013

Mr. Farrokh K. Captain, President ABC and Ms. Raheen Mani, Executive Director met

Mr. Munir Qureshi, Secretary Commerce in

Islamabad. The President of ABC used this opportunity to brief the Secretary Commerce on proposed amendments to ABC’s Articles of Association. The Secretary Commerce assured the ABC President that he would request the Director General Trade Organization to extend his support on the matter.

• Executive Director’s meeting with the U.S. Visa Section Chief - March 1st, 2013

On behalf of ABC Executive Committee, Ms. Raheen Mani, Executive Director met with Ms. Kelly Kopcial, U.S. Visa Section Chief at the U.S. Consulate in Karachi. The U.S. Visa Section Chief informed the Executive Director that various options were being considered to facilitate ABC business travelers.

• President of ABC’s dinner for members - March 11th, 2013

President of ABC invited members for dinner at his residence in Karachi.

• President of ABC & Executive Director’s meeting with the U.S. Consul General -

March 12th, 2013

Mr. Michael Dodman, U.S. Consul General visited the ABC Secretariat in Karachi and met with Mr. Farrokh K. Captain, President ABC and Ms. Raheen Mani, Executive Director. Matters of mutual interest were discussed in the meeting.

• ABC Members meet over lunch with Pakistan Ambassador to the U.S. - March 14th, 2013

A luncheon meeting with H.E. Sherry Rehman, Pakistan Ambassador to the U.S. was held in Karachi for the ABC members.

11

ANNUAL REPORT 2013

Highlights of the Year The Ambassador underscored the need for

the United States and Pakistani government to take their bilateral relationship to new heights by focusing on trade and investment. She further added that there was great potential for increased cooperation between the two countries in a broad spectrum of areas. The meeting was well attended and received good feedback from members.

• Executive Committee meeting with the U.S. - Pakistan Business Council (USPBC)

Chairman and Executive Director - April 24th, 2013

The Executive Committee met over lunch with Mr. Miles Young, Chairman of the U.S.-Pakistan Business Council (USPBC) and Ms. Esperanza Gomez Jelalian, Executive Director, U.S.-Pakistan Business Council & Director, South Asia, U.S. Chamber of Commerce in Karachi. During the meeting, the USPBC Chairman praised the success of the Government of Pakistan in reforming and deregulating the country’s economy. The ABC Executive Committee agreed on the need for mutual cooperation on issues related to advancing U.S.-Pakistan bilateral business and investment opportunities in order to attract and facilitate prospective U.S. companies looking to setup business in Pakistan.

• Executive Committee meeting with the U.S. Economic Counselor and the Consul General - May 25th, 2013

The Executive Committee met Mr. Robert Ewing, U.S. Economic Counselor and Mr. Michael Dodman, Consul General at the ABC office in Karachi. The U.S. Economic Counselor stressed on the importance of business and investment in shifting the ties of

the two countries from conventional assistance towards a more business oriented one. The Economic Counselor was of the view that Pakistan’s emerging market and population of more than 190 million consumers holds great opportunities for American companies.

• U.S. Ambassador calls on Executive Committee - June 28th , 2013

U.S. Ambassador to Pakistan, H.E. Richard Olson paid a courtesy call to members of the Executive Committee in the ABC Secretariat in Karachi. The discussion predominantly centered on the security and energy issues faced by ABC members. The Executive Committee requested the U.S. Embassy to convey these concerns to high level representatives of the Pakistani government.

• Executive Committee meeting with the USAID Mission Director - July 9th, 2013

The ABC Executive Committee met with Gregory Gottlieb, USAID Mission Director at the ABC office in Karachi. The Mission Director shared that the primary focus of the U.S. civilian assistance program is to develop a stable, secure and tolerant Pakistan with a vibrant economy. USAID has focused its program over the last few years on five areas essential to Pakistan’s stability and long-term development that are reflective of Pakistani priorities; energy, economic growth, stabilization, education and health.

• Executive Committee meets President of the Overseas Private Investment Corporation, U.S. Ambassador and U.S. Consul General - July 18th, 2013

The Executive Committee members met with

12

Highlights of the Year Ms. Elizabeth Littlefield, CEO and President of

the Overseas Private Investment Corporation (OPIC), U.S. Ambassador Richard Olson, Consul General in Karachi Michael Dodman and other U.S. government officials at the ABC office in Karachi.

The ABC members shared their view on the overall investment climate of Pakistan, economic outlook for the year ahead and presented new opportunities for U.S. investors to partner with Pakistani businesses. Recognizing how critical the energy sector is to Pakistan’s long-term economic growth, OPIC will pay close attention to how it can best support investors willing to address this challenge. Ms. Littlefield expressed her gratitude to the Executive Committee for their contribution towards a fruitful discussion.

OPIC has invested in 123 projects in Pakistan since its formation in 1971. Its current Pakistan portfolio includes 14 active projects worth nearly $300 million in key industries including energy, health care, financial services for small and medium sized enterprises, and telecommunications. OPIC is the U.S. Government’s development finance institution. It mobilizes private capital to help solve critical development challenges, providing investors with financing, guarantees, political risk insurance, and support for private equity investment funds.

• Executive Committee and Security Sub-Committee members engage with Citizens-Police Liaison Committee (CPLC) - July 25th, 2013

Members of the ABC Executive Committee and Security Sub-Committee met with Mr. Ahmed Chinoy, Chief of Citizens-Police Liaison Committee (CPLC) and his team on

their visit to the ABC Secretariat. The Executive Committee, on behalf of the Council, presented Mr. Ahmed Chinoy with a humble contribution of Rs. 250,000 for CPLC. Mr. Chinoy briefed members on CPLC’s role in monitoring and combating crime.

• President of ABC meets with Finance Minister – August 28th, 2013

The President of ABC was present in a meeting Federal Finance Minister Senator Ishaq Dar held with various members of the business community including Chief Executives of leading institutions, corporate leaders, and representatives of exchange companies, at the State Bank of Pakistan in Karachi. Attendees cited their concerns on government borrowing from the banking system and the stringent conditions tied with borrowing from International Monetary Fund (IMF). The Federal Minister assured participants that seeking financial assistance from IMF would in fact prevent Pakistan from defaulting on its debt obligations and would ultimately help strengthen the currency.

• President of ABC’s meeting with Pakistan’s Prime Minister – September 3rd, 2013

Mr. Farrokh K. Captain, President of ABC met Prime Minister Nawaz Sharif at the Governor House in Karachi. Amongst various issues discussed, the ABC President also voiced his concerns on the law and order situation of Karachi to the Prime Minister. The Prime Minister assured participants that his Government was committed to restoring law and order and bringing normalcy back to the country’s economic hub which was of foremost importance to his team.

13

ANNUAL REPORT 2013

Highlights of the Year• Executive Committee meets the U.S. Senior

Commercial Officer – September 25th, 2013

Mr. David McNeil, U.S. Senior Commercial Officer (Commercial Counselor) visited the ABC office in Karachi and met the Executive Committee members as a courtesy call. Various matters of mutual interest were discussed during the meeting.

OTHER ACTIVITIES:

The ABC Member Internship Program in Collaboration with the U.S. Mission

The U.S. Mission in Pakistan and the ABC worked together to provide internship opportunities to Pakistani alumni of U.S. Government Funded Exchange Programs within member companies. The internships were fully funded by participating ABC companies in line with their internal policies. The U.S. Mission in Pakistan administers more than 30 academic and professional exchange programs funded by the U.S. government. These programs send more than 1,000 Pakistanis to the United States each year for periods ranging from three weeks to over a year. Participants reflect Pakistan’s rich diversity; approximately 50% are female, many come from disadvantaged and minority communities, and they represent a full range of academic and professional backgrounds. Many are in their final year or have just completed their studies, and some are mid-career professionals.

The ABC Participates in U.S. Embassy Global UGrad Reunion

The U.S. Embassy invited members of the ABC to participate in a panel discussion on internship opportunities available within their organizations at the second annual reunion for alumni of the

Global Undergraduate (UGrad) exchange program, on December 14th in Islamabad. The ABC Participants included Mr. Muhammad Navid Qazi from Cisco Systems Pakistan and Mr. Rahim Lalani from TRG.

The audience included nearly 300 alumni who have undertaken a semester of study in the United States. The Global UGrad program in Pakistan is the largest in the world. Since 2010, U.S. Embassy Islamabad has sent nearly 700 Pakistani university students to the United States for one semester of study at a U.S. university.

U.S. Visa Facilitation for ABC Member Company Employees

The ABC announced the launch of a U.S. visa facilitation scheme for its members on December 17th. The scheme requires AMEX to create a special visa appointment category for full-time employees of the American Business Council Member Companies anywhere in Pakistan who are going to U.S. on a temporary basis for business purposes, or to perform work as permitted by the appropriate nonimmigrant work visa. There will be 10 interview appointments per interview day reserved for the ABC member employees (adjusted if demand increases). With there otherwise often being some weeks wait time for a visa appointment, this facility will provide members with the flexibility to schedule a visa appointment at their earliest convenience. Over the course of the year the Executive Committee of The American Business Council of Pakistan (ABC) has worked to further strengthen its relationship with the U.S. Mission in Pakistan. Going forward, the ABC will continue to work with the U.S. Mission to provide facilities for its members.

14

Highlights of the Year

CEO Roundtable Meetings

1st CEO Roundtable Meeting - February 6th, 2013

Held on February 6th 2013 the 1st CEO Roundtable Meeting was well attended by members of the ABC. Participants shared feedback on how business had fared in 2012, plans for 2013 and the opportunities and challenges present in each of their respective areas of business. The CEO Roundtable meeting allowed ABC members to network, exchange ideas and identify common areas of concern facing American businesses in Pakistan.

Dr. Amjad Waheed, CFA & CEO, NBP Fullerton Asset Management Ltd. (NAFA) was invited as Guest Speaker. Dr. Amjad Waheed spoke of how many developing countries including Pakistan face a saving investment gap and of the crucial role played by FDI in facilitating economic growth by filling this gap. FDI allows the transfer of technology, uplifts competition in the domestic input market, contributes to human capital development and profits created by FDI contribute to corporate tax revenues in the host country.

2nd CEO Roundtable Meeting - July 1st, 2013

The 2nd CEO Roundtable meeting was held on July 1st. The ABC members discussed the implications of the Federal Budget FY13-14 on the overall economy. Mr. Syed Shabbar Zaidi, Partner A.F. Ferguson and Co., and Mr. Muhammad Hidayatullah of M. Hidayatullah & Co., Chartered Accountants were invited to brief the audience on the impact of the Federal Budget on the economy. The Federal Budget included considerable changes in both expenditure and

taxation plans, as well as ambitious targets that will have a momentous effect on the external sector of the economy. The ABC members expressed their concern on rising external debt and rapidly shrinking foreign exchange reserves. The members were of the view that depleting foreign reserves will exert downward pressure on the currency and cause debt servicing costs to balloon.

3rd CEO Roundtable Meeting - July 8th, 2013

The 3rd CEO Roundtable meeting was held on July 8th, 2013 in Karachi with Dr. Ishrat Husain, former Governor, State Bank of Pakistan and presently Dean and Director of the Institute of Business Administration (IBA), Karachi, attending as Guest Speaker. Dr. Husain talked about the various social and economic challenges faced by Pakistan. His knowledge and experience provided invaluable insight to the ABC members.

4th CEO Roundtable Meeting – September 2nd, 2013

The 4th CEO Roundtable Meeting was held on September 2nd in Karachi. The ABC member company CEOs shared updates on overall business performance, investment plans for 2014 in their respective sectors of the economy and the challenges being faced by their businesses, with each other. Participants had an opportunity to assess how the economic climate was affecting various businesses, identify common issues being faced by American companies in Pakistan and develop strategies to contest these issues in a united manner.

15

ANNUAL REPORT 2013

Highlights of the YearCHANGE AT ABC SECRETARIAT

Ms. Raaheen Mani resigned in June 2013 and was replaced by Ms. Aisha Kirmani as the ABC Secretary General in November 2013.

MEMBERSHIP

(i) Enrolment of New Members:

Teradata Pakistan (Pvt.) Ltd. June 7, 2013F.C.I. International (Pvt.) Ltd. August 23, 2013Ogilvy & Mather Pakistan (Pvt.) Ltd. August 23, 2013Primatics Financial (Pvt.) Ltd. August 23, 2013International Learning Center (Pvt.) Ltd. (Berlitz) August 23, 2013Sakonent (SMC Pvt.) Ltd. December 31, 2013

(ii) Cessation of Old Member:

AT&T Global Network Services International Inc.

MEETINGS OF THE EXECUTIVE COMMITTEE

The Executive Committee convened and participated in 32 meetings and events during the period. It constituted of 10 Sub-Committees, defined their Terms of Reference and gave policy directions from time to time.

On behalf of the Executive Committee,

Farrokh K. CaptainPresident

Karachi

16

ACE Insurance Limited6th Floor, N.I.C. Building,Abbasi Shaheed Road,Off. Sharah-e-Faisal,Karachi - Pakistan.

Tel: 111-789-789Fax: (92-21) 35683935www.acelimited.com

Programs& EventsPhoto Gallery

ANNUAL REPORT 2013

Programs & Events Photo Gallery

The ABC CEO Roundtable – July 8, 2013, Karachi

20

(From right) Mr. Osman Asghar Khan, Vice President ABC, Mr. AminM. Khowaja, General Manager, J.P. Morgan Pakistan, Mr. Tauqir Ahmed, Member Executive Committee and a guest

(From left) Mr. Osman Asghar Khan, Vice President ABC, Dr. Ishrat Husain, Dean & Director, IBA, Mr. Farrokh K. Captain, President ABC and Mr. Michael Dodman, US Consul General, Karachi

Programs & Events Photo Gallery

The ABC CEO Roundtable – July 8, 2013, Karachi

21

ANNUAL REPORT 2013

(Center) Mr. Saad Amanullah Khan, Chairman, Finance Sub-Committee addressing members of the audience. (Left) Mr. Nadeem Elahi, Member Executive Committee

(Center) Mr. Nadeem Lodhi, Managing Director & CCO, Citibank N.A.(1st from left) Mr. S. Iqbal Ghazi, CEO, Sun Consulting and (3rd) Mr. Tauqir Ahmed, Member Executive Committee

Programs & Events Photo Gallery

Friends of CPLC – ABC donation for the year 2013 to the CPLC – July 25, 2013, Karachi

22

(From right) Mr. Tauqir Ahmed, Member ExCom & Chairman Security Sub-Committee (2nd) Mr. Jamil A. Mughal, Director Marketing, Siza Foods (3rd) Mr. Ghulam Abbas, Security Consultant, IBM and other guests at the meeting

(From left) Mr. Shabeeh Ikram, General Manager, Johnson & Johnson (3rd) Mr. Kamal Ahmed, Director Finance, ACE Insurance (4th) Mr. Tasleemuddin Ahmed Batlay, Chairman, IPR & Legal Sub-Committee (5th) Mr. M. Iqbal Shekhani, Member Executive Committee and guests at the meeting

(4th from left) Mr. Ahmed Chinoy, Chief CPLC (2nd) Mr. Tauqir Ahmed, Chairman, Security Sub-Committee (3rd) Mr. Saad Amanullah Khan, Chairman, Finance Sub-Committee (5th) Mr. M. Iqbal Shekhani, Member Executive Committee

Programs & Events Photo Gallery

The ABC meeting with the U.S. Journalists – January 22, 2013, Karachi

(2nd from left) Mr. Farrokh K. Captain, President ABC (1st) Mr. Mujib Khan, Country Manager, New Hampshire Insurance (3rd) U.S. Journalist and (4th) Mr. Nadeem Elahi, Member Executive Committee

The ABC President with U.S. Journalist delegation and ABC members

23

ANNUAL REPORT 2013

(1st from right) Mr. Irshad Kassim and (2nd) Mr. Ahmed Jamal Mir, Members of the Executive Committee with guests

Programs & Events Photo Gallery

ExCom meets CEO & President of the Overseas Private Investment Corporation (OPIC), U.S. Ambassador and U.S. Consul General - July 18th, 2013, Karachi

24

(2nd from left) Mr. Farrokh K. Captain, President ABC (1st) Mr. M. Iqbal Shekhani (3rd) Ms. Zehra Naqvi and (4th) Mr. Irshad Kassim, Members of the Executive Committee

(1st from right) Mr. Irshad Ali Kassim, Member Executive Committee (2nd) Ms. Elizabeth Littlefield, CEO and President OPIC, (3rd) Mr. Farrokh K. Captain, President ABC, (4th) Ms. Anu Prattipati, Political and Economic Chief, (5th) H.E. Richard Olson, U.S. Ambassador to Pakistan

25

Programs & Events Photo Gallery

ExCom meeting with the USAID Country Director - July 9th, 2013, Karachi

ANNUAL REPORT 2013

(1st from left) Mr. Nadeem Elahi (2nd) Mr. Ahmed Jamal Mir and (3rd) Mr. M. Iqbal Shekhani, Members of the Executive Committee

(2nd from right) Mr. Farrokh Captain, President ABC with (3rd) Mr. Gregory Gottlieb, USAID Country Director and Members of the Executive Committee

Programs & Events Photo Gallery

ExCom meeting with the U.S. Ambassador – June 28, 2013, Karachi

26

(1st from left) Mr. Osman Khan, Vice President ABC (2nd) Mr. Farrokh Captain, President ABC (3rd) Mr. Tasleem Batlay (4th) Ms. Zehra Naqvi and (5th) Mr. Tauqir Ahmed, Members of the Executive Committee

(2nd From left) Mr. Michael Dodman, U.S. Consul General (3rd) H.E. Richard Olson, U.S. Ambassador to Pakistan (4th) Mr. Arshad Saeed Husain, Chairman Pharma Sub-Committee and (5th) Mr. Ahmed Jamal Mir, Member Executive Committee

H.E. Richard Olson, U.S. Ambassador to Pakistan with the ABC President, Executive Committee members and guests from the U.S. Consulate

Programs & Events Photo Gallery

ExCom meeting with U.S. Commercial Counselor – September 25, 2013, Karachi

27

ANNUAL REPORT 2013

(1st from left) Mr. Malik Muhammad Attiq, U.S. Commercial Specialist, (2nd) Mr. David McNeil, U.S. Commercial Counselor with the ABC President and other members of the Executive Committee

Programs & Events Photo Gallery

ExCom meeting with the USAID Regional Director–January 11th,

2013, Karachi

28

(1st from left) Mr. Saad Amanullah Khan, Chairman, Finance Sub-Committee (2nd) Mr. Irshad Kassim and (3rd) Mr. M. Iqbal Shekhani, Executive Committee members

The ABC President and Executive Committee members with Mr. Ed Birgells, USAID Regional Director (5th from left) and other USAID staff

Programs & Events Photo Gallery

The ABC CEO Roundtable – July 1, 2013, Karachi

29

ANNUAL REPORT 2013

Mr. Farrokh K. Captain, President ABC greeting Mr. Muhammad Hidayatullah of M. Hidayatullah & Co., Chartered Accountants, Guest Speaker at the CEO Roundtable

The Guest Speaker, Mr. Muhammad Hidayatullah briefing members on the impact of the Federal Budget to the economy

(5th from left) Mr. Farrokh Captain, President ABC, presenting a memento to Mr. Muhammad Hidayatullah. From left (1st) Mr. Irshad Kassim (2nd) Mr. Ahmed Jamal Mir, Executive Committee members (3rd) Mr. Shabbar Zaidi, Partner, A.F. Ferguson & Co., (6th) Mr. Osman Khan, Vice President ABC and (7th) Mr. M. Iqbal Shekhani, ExCom member

Programs & Events Photo Gallery

U.S.-Pakistan Business Council (USPBC) Chairman and Executive Director meet the ABC - April 24th, 2013, Karachi

30

(1st from left) Mr. Miles Young, Chairman, U.S.-Pakistan Business Council (USPBC), (2nd) Mr. Farrokh Captain, President ABC and (3rd) Ms. Esperanza Gomez Jelalian, Executive Director, U.S.-Pakistan Business Council & Director, South Asia, U.S. Chamberof Commerce

From right (1st) Mr. Miles Young, Chairman, U.S.-Pakistan Business Council (USPBC), (2nd) Mr. Saad Amanullah Khan, Chairman, Finance Sub-Committee (3rd) Mr. Farrokh Captain, President ABC (4th) Ms. Esperanza Gomez Jelalian, Executive Director, U.S.-Pakistan Business Council (USPBC), (5th) Mr. M. Iqbal Shekhani and (6th) Mr. Ahmed Jamal Mir, Executive Committee members

The ABC Executive Committee members with Mr. Miles Young, Chairman, U.S.-Pakistan Business Council (USPBC), Ms. Esperanza Gomez Jelalian, Executive Director, U.S.-Pakistan Business Council and other guests

Reports ofSub-Committees

Report of Finance & Taxation Sub-Committee

MEMBERS

Mr. S. Anis AhmedAbbott Laboratories (Pakistan) Ltd.

Mr. Hassan Ali New Hampshire Insurance Company

Mr. Hashim Sadiq AliAmerican Life Insurance Company (Pakistan) Ltd. Mr. Muhammad Arsalan BatlaOBS Pakistan (Pvt.) Ltd.

Mr. Humza ChaudhriACE Insurance Ltd.

Mr. Imran FarooquiProcter & Gamble Pakistan (Pvt.) Ltd.

Mr. Zafar HasanSIZA Foods (Pvt.) Ltd. (McDonald's)

Mr. Kashif Imtiaz KhanIBM

Mr. Munaf LakdaMuller & Phipps Pakistan (Pvt.) Ltd.

Mr. Syed Zeeshan MobinOBS Pakistan (Pvt.) Ltd.

Mr. Omer MuradWPP Marketing Communications (Pvt.) Ltd (JWT)

Mr. Javed MurtazaMonsanto Pakistan (Pvt.) Ltd.

Mr. Atif Izhar SiddiquiEli Lilly Pakistan (Pvt.) Ltd.

Mr. Syed WajeehuddinPfizer Pakistan Ltd.

Mr. Adamjee YakoobCitibank, N.A.

Mr. Ali Akbar ZaidyJohnson & Johnson Pakistan (Pvt.) Ltd.

TERMS OF REFERENCE

1. Study major Government policy directives on various matters relating to Finance and Taxation concerning members of the ABC and the American business community at large.2. Identify and develop positions on major issues relating to Finance and Taxation.3. Develop the ABC proposals for the Federal Budget.4. Ensure a level playing field for member companies by lobbying for the removal of discriminatory rules and regulations.5. Oversee financial matters of the ABC.

CHAIRMAN

Mr. Saad Amanullah KhanChief Executive OfficerGillette Pakistan Limited

34

THE ACTIVITIES OF THE SUB-COMMITTEE ARE SUMMARIZED BELOW:

1. The Chairman of the Finance Sub-Committee invited Mr. Syed Shabbar Zaidi, Partner, A.F. Ferguson and Co., at the ABC Secretariat on March 29th 2013 to seek input for the budget proposals of for ABC.2. The Chairman conducted a periodic review of the ABC budget and advised the Secretariat on placement of reserves.3. The Sub-Committee sought input from the ABC members to prepare an all inclusive proposal for the Federal Budget 2013-14. The ABC submitted 8 taxation related proposals impacting U.S. companies operating in Pakistan and on the procedural front, there were 6 proposals to help streamline processes & improve taxation collection systems. These proposals are aimed at positively impacting the operations of US companies in Pakistan. The procedural suggestions are designed to

help streamline and improve tax collection and appeal processes. The comprehensive document was submitted to the Federal Government in March 2013. The Sub- Committee reiterated its commitment to supporting the development of a robust, understandable and transparent taxation environment. 4. A summary of the Federal Budget Recommendations is available in the annexures.

As Chairman of the Sub-Committee, I wish to thank all members of the Sub-Committee and the ABC Secretariat for their support and cooperation during the year.

35

ANNUAL REPORT 2013

MEMBERS

Mr. Wasif Waseem AshrafCrescent Bahuman Limited

Mr. Atif AftabOracle Corporation

Mr. Jarri Masood3M (Pvt.) Ltd

Mr. Danish Bin InbsatCitibank N.A.

Ms. Farhana FahadSinger Pakistan Limited

Ms. Habiba WarindIBM

Ms. Aqsa YahyaSheraton Karachi Hotel

Mr. Zeshan Taj KhanPfizer Pakistan Ltd.

Ms. Sanam Kohati FaizCitibank N.A.

Ms. Claudia ManuelProcter & Gamble (Pvt.) Ltd

Dr. M. Saeed ShekhaniOBS Pakistan (Pvt) Ltd.

TERMS OF REFERENCE:

1. To provide support to the ABC staff and define their reporting lines, benefits and increments.2. Study contemporary trends, practices and policies relating to Human Resource Management and Industrial Relations impacting members.3. Identify and develop position on major issues and make. recommendations to the Executive Committee for representation to the Government as and when needed.4. Serve as a forum for consultation and exchange of information with members and serve the community on matters relating to Human Resource Management and Industrial Relations.5. Creating partnerships with suitable philanthropic organizations that positively impact the ABC and the perception of US companies operating in Pakistan, with a clear established method of achieving these goals.6. Identify areas of need for both long term partnerships and during emergency relief efforts.7. Facilitate meetings between the ABC member ship and deserving philanthropic organizations to encourage greater interaction, awareness and support.8. Regularly communicate and highlight CSR achievements of the ABC and its member companies.9. Reflect the philosophy of our members and their commitment to being good corporate citizens.

Report of HR & CSR Sub-Committee

CHAIRMAN

Ms. Zehra NaqviChief Executive ACE Insurance Limited

36

THE ACTIVITIES OF THE SUB-COMMITTEE ARE SUMMARIZED BELOW:

• The Chairperson of the HR Sub-Committee implemented a merit based increment system for the ABC Secretariat.• The Chairperson conducted a number of interviews to shortlist suitable candidates for the Secretary General position. • The Chairperson worked with the Executive Committee to ensure a competency based

recruitment process was applied to fill the Secretary General position. This included the development of a comprehensive job description for the position in question. • The Chairperson worked closely with the ABC President to develop a comprehensive employment contract with competitive compensation & benefits for the Secretary General position.

Thank you to all the Sub-Committee members and the ABC Secretariat for their support & contribution.

37

ANNUAL REPORT 2013

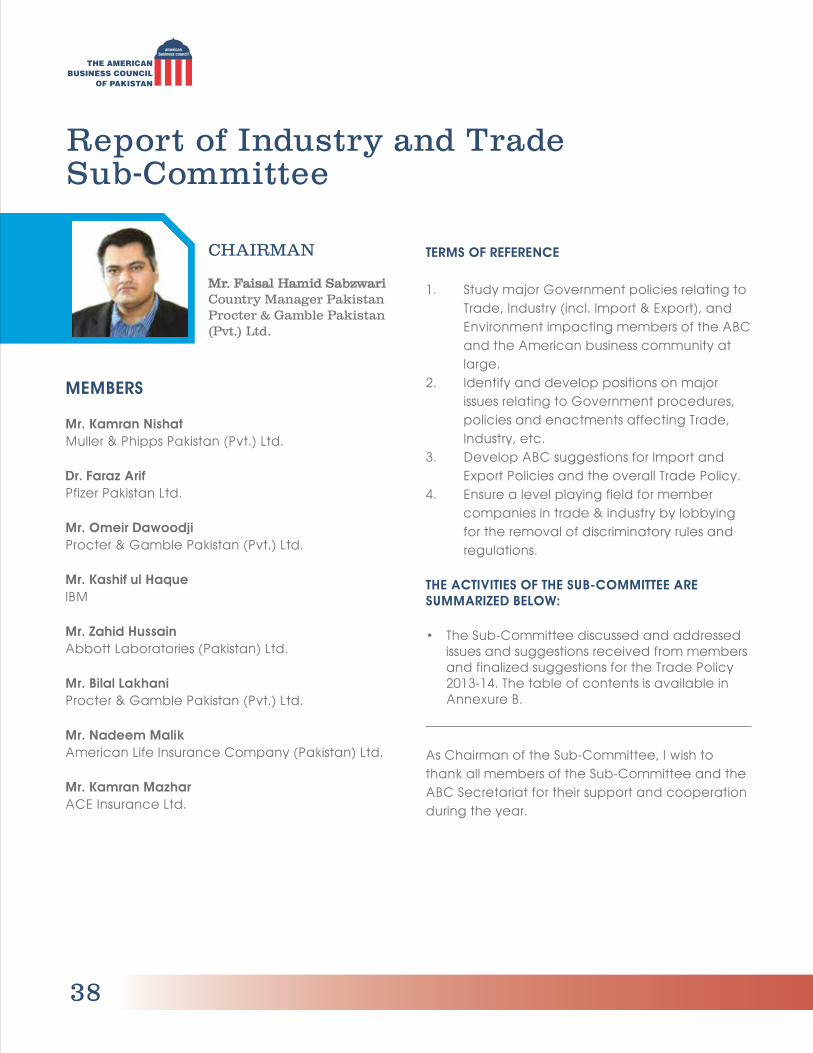

CHAIRMAN

Mr. Faisal Hamid SabzwariCountry Manager PakistanProcter & Gamble Pakistan (Pvt.) Ltd.

Report of Industry and Trade Sub-Committee

MEMBERS

Mr. Kamran NishatMuller & Phipps Pakistan (Pvt.) Ltd.

Dr. Faraz ArifPfizer Pakistan Ltd.

Mr. Omeir DawoodjiProcter & Gamble Pakistan (Pvt.) Ltd.

Mr. Kashif ul HaqueIBM

Mr. Zahid HussainAbbott Laboratories (Pakistan) Ltd.

Mr. Bilal LakhaniProcter & Gamble Pakistan (Pvt.) Ltd.

Mr. Nadeem MalikAmerican Life Insurance Company (Pakistan) Ltd.

Mr. Kamran MazharACE Insurance Ltd.

TERMS OF REFERENCE

1. Study major Government policies relating to Trade, Industry (incl. Import & Export), and Environment impacting members of the ABC and the American business community at large.

2. Identify and develop positions on major issues relating to Government procedures, policies and enactments affecting Trade, Industry, etc.

3. Develop ABC suggestions for Import and Export Policies and the overall Trade Policy.

4. Ensure a level playing field for member companies in trade & industry by lobbying for the removal of discriminatory rules and regulations.

THE ACTIVITIES OF THE SUB-COMMITTEE ARE SUMMARIZED BELOW:

• The Sub-Committee discussed and addressed issues and suggestions received from members and finalized suggestions for the Trade Policy 2013-14. The table of contents is available in Annexure B.

As Chairman of the Sub-Committee, I wish to thank all members of the Sub-Committee and the ABC Secretariat for their support and cooperation during the year.

38

Report of IPR & Legal Sub-Committee

MEMBERS

Mr. Fayyaz AhmedEli Lilly Pakistan (Pvt.) Ltd.

Mr. Muhammad KamranACNielsen Pakistan (Pvt.) Ltd.

Ms. Aiza KhawajaIBM

Mr. Bilal LakhaniProcter & Gamble Pakistan (Pvt.) Ltd.

Mr. Shaharyar NashatPfizer Pakistan Ltd.

Mr. Yasar NoorOracle Corporation

Mr. Raza Mustafa SaeediJohnson & Johnson Pakistan (Pvt.) Ltd.

Mr. Hashim SadiqAmerican Life Insurance Co. (Pak.) Ltd.

Mr. Jawaid SiddiquiDuPont Pakistan Operations (Pvt.) Ltd.

TERMS OF REFERENCE:

1. Identify key IPR issues impacting ABC members and work on programs and actions intended to influence legislation relating to IPR in both Pakistan and the U.S.2. Ensure a level playing field for member companies relating to IPR.3. Create a liaison with the government offices and establish a platform for the ABC and its members and to special focus on IPO to get back our seat on the IPO Policy Board.4. Advise on matters having legal implications or relating to the ABC.

THE ACTIVITIES OF THE SUB-COMMITTEE ARE SUMMARIZED BELOW:

• The Sub-Committee engaged with members to submit the ABC’s feedback on the working paper prepared by IPO-P for Pakistan’s accession to Patent Corporation Treaty (PCT).• The Sub-Committee lobbied for restoration of the ABC seat on IPO Policy Board. • The Chairman of the IPR and Legal Sub- Committee worked with the ABC Legal Advisors Orr, Dignam & Company to ensure that the changes made to the ABC Articles of Association were in compliance with the Trade Organizations Act 2013.

CHAIRMAN

Mr. Tasleemuddin Ahmed BatlayDirectorColgate-Palmolive (Pakistan) Ltd.

CO-CHAIRMAN

Mr. Akram Wali MohammadGerry’s International (Pvt.) Ltd.

Thank you to all the Sub-Committee members and the ABC Secretariat for their support & contribution.

39

ANNUAL REPORT 2013

CO-CHAIRMAN

Mr. Ahmed Jamal MirPrestige Communications (Pvt.) Ltd. (GREY)

MEMBERS

Mr. Nadeem ElahiTRG (Pvt.) Ltd.

Mr. Adeel ShahidCitibank, N.A.

Mr. Ahmer Ashraf Pfizer Pakistan Ltd.

Mr. Omeir DawoodjiProcter & Gamble Pakistan (Pvt.) Ltd.

Mr. Iqbal ShekhaniJohan (Pvt.) Ltd. (Culligan)

Mr. Akif Zia Malik New Hampshire Insurance Company

TERMS OF REFERENCE

1. Positively project the ABC to all stakeholders through events and special activities.

2. Ensure highlighting various ABC activities through different modes of media and provide support to the ABC in producing a quarterly newsletter.

3. Create awareness of ABC key issues.4. Propose a plan to invite high profile guest

speakers to address the ABC members on current issues or subjects of general business interest.

5. Propose a plan for the ABC Economic Summit and recommend high profile speakers and invitees for the event. Work with ABC Secretary General to plan and manage the event.

THE ACTIVITIES OF THE SUB-COMMITTEE ARE SUMMARIZED BELOW:

• The Sub-Committee worked with the ABC Secretariat to ensure the ABC CSR report was widely circulated and shared with all relevant stakeholders.

• It was actively engaged with members to develop content for publication of the ABC newsletter.

• The Sub-Committee worked with the Secretariat to resume the circulation of the monthly e-brief. The monthly update aims at creating awareness amongst members on ABC activities and initiatives.

• The Sub-Committee organized a number of CEO Roundtable briefings for members. These briefings provided members with an opportunity to network and learn about the opportunities and challenges being faced by businesses operating in various sectors of the economy.

• 1st CEO Roundtable Meeting - February 6th, 2013 – Member company representatives reviewed business performance over 2012 and

Report of Media, PR & Programs Sub-Committee

CHAIRMAN

Mr. Osman Asghar KhanCountry ManagerEMC Information Systems (Pvt.) Ltd.

40

41

plans for 2013. Dr. Amjad Waheed, CFA & CEO, NBP Fullerton Asset Management Ltd. (NAFA) was invited as Guest Speaker. Dr. Amjad Waheed provided members with an in-depth analysis of the economic challenges facing the nation.

• 2nd CEO Roundtable Meeting - July 1st, 2013 - Participants discussed the implications of the Federal Budget FY13-14 on the overall economy. Mr. Syed Shabbar Zaidi, Partner A.F. Ferguson and Co., and Mr. Muhammad Hidayatullah of M. Hidayatullah & Co., Chartered Accountants were invited to brief the audience on the impact of the Federal Budget on the economy.

• 3rd CEO Roundtable Meeting - July 8th, 2013 - Dr. Ishrat Husain, Former Governor, SBP and Dean and Director of IBA attended as a Guest Speaker. Dr. Husain spoke of the various social and economic challenges faced by Pakistan. His knowledge and experience provided invaluable insight to attendees.

• 4th CEO Roundtable Meeting – September 2nd, 2013 – Business managers shared an update on how the economic climate was affecting their respective businesses, identified common issues being faced by American companies in Pakistan and developed strategies to contest these issues in a united manner.

Unfortunately, due to a personal emergency the Economic Summit was postponed and then subsequently cancelled. The roundtables were all sponsored by the two co-chairs. Thank you to all the Sub-Committee members and the ABC Secretariat for their support & contribution.

ANNUAL REPORT 2013

MEMBERS

Mr. Muhammad AsimMonsanto Pakistan (Pvt.) Ltd.

Dr. Iftikhar Ahmed JafriPfizer Pakistan Ltd.

Mr. Atif KamalDuPont Pakistan Operations (Pvt.) Ltd.

Dr. Muhammad Saeed ShekhaniOBS Pakistan (Pvt.) Ltd.

Dr. Salman LodiJohnson & Johnson Pakistan (Pvt.) Ltd.

TERMS OF REFERENCE

1. Co-ordinate with members in all matters relating to the Pharmaceutical & Agricultural Chemicals industry to identify & develop positions on major issues pertaining to this sector.2. Ensure a level playing field for member companies in this sector by lobbying for the removal of discriminatory rules and regulations.

THE ACTIVITIES OF THE SUB-COMMITTEE ARE SUMMARIZED BELOW:

• The Sub-Committee worked with the Pharma Bureau to lobby the GoP and regulatory authorities for improving the functioning of the Drug Regulatory Authority, issuance of pending registrations, grant of an interim price adjust ment and on the development of a transparent pricing policy. • The Sub-Committee provided the U.S. Mission with timely information and input on Pharma related matters.• It effectively used the ABC platform to ensure that the U.S. Mission was kept abreast of issues affecting the Pharmaceutical Industry and actively supported the ABC Pharma companies.• Members of the Sub-Committee worked with the Pharma Bureau to develop new product pricing mechanisms. • The Sub-Committee worked towards ensuring a level playing field in the Agrochemicals and Seeds industry (registration of crop protection products and seeds, etc.).• It provided input to the IPR Sub-Committee on

CHAIRMAN

Mr. Arshad Saeed HusainManaging DirectorAbbott Laboratories (Pakistan) Ltd.

CO-CHAIRMAN

Mr. Kamran NishatMuller & Phipps Pakistan (Pvt.) Ltd.

Report of Pharmaceutical & Agricultural Chemicals Sub-Committee

42

IPR issues (Smuggled and Counterfeit products) faced by the Pharma and Agro industry.• The Chairman of the Sub-Committee worked with the ABC President to submit a formal request to Prime Minister Mian Muhammad

Nawaz Sharif for reconsideration on the reversal of SRO 1002. The SRO would have provided an interim relief of 1.25% on medicine prices that have been frozen for the last 13 years.

Thank you to all the Sub-Committee members and the ABC Secretariat for their support & contribution.

43

ANNUAL REPORT 2013

MEMBERS

Mr. Osman Asghar KhanEMC Information Systems (Pvt.) Ltd.

Mr. Ahmed Jamal MirPrestige Communications (Pvt.) Ltd. (Grey)

TERMS OF REFERENCE:

1. To oversee and review the membership criteria for the ABC2. Pursue a membership drive to seek new members for the ABC

THE ACTIVITIES OF THE SUB-COMMITTEE ARE SUMMARIZED BELOW:

• During the year a comprehensive exercise was undertaken to encourage new members to join the Council.• The Sub-Committee’s membership drive resulted in six new members being enrolled over the course of the year.• The Sub-Committee provided inputs into the changes required in the Membership section of the ABC’s Articles of Association.• After incorporating the necessary input from the ABC’s legal advisors, the findings and input of the Sub-Committee were approved at the AGM.

Report of Membership & Admin Sub-Committee

CHAIRMAN

Mr. Irshad Ali KassimChairmanKaram Ceramics Limited

Thank you to all the Sub-Committee members and the ABC Secretariat for their support & contribution.

44

TERMS OF REFERENCE

1. To facilitate the presence of ABC in the North region.

2. To have close interaction with the ABC members located in North.

3. To have close liaison with the Government functionaries for resolution of all ABC issues.

THE ACTIVITIES OF THE SUB-COMMITTEE ARE SUMMARIZED BELOW:

• The Chairman of the North Members Sub-Committee participated and made valuable contributions to the ABC Executive Committee trip to Islamabad on February 25th, 2013 where they met the U.S. Ambassador Richard Olson; Robert Ewing, Economic Counselor; Jim Fluker, Commercial Counselor; Daniel Goodspeed, Consular Section Official; John Eustace, Regional Security Official; Justin Diaz and other Economic Section and U.S. Commercial Service Officials at the U.S. Embassy.

• The Chairman of North Sub-Committee participated in various forums such as Federal Government’s Trade Policy chaired by Federal Minister of Commerce and Secretary Commerce where he presented ABC’s recommendations for the Trade Policy.

CHAIRMAN

Mr. Navid QaziCountry General ManagerCisco Systems Pakistan (Pvt.) Ltd.

Thank you to all the Sub-Committee members and the ABC Secretariat for their support & contribution.

Report of North Members Sub-Committee

45

ANNUAL REPORT 2013

MEMBERS

Mr. Ghulam AbbasIBM

Mr. Syed AdnanTRG (Pvt.) Ltd.

Mr. Kamal AhmedACE Insurance Ltd.

Mr. Tauqeer AhmedNew Hampshire Insurance Company

Col. (R) Pervez AkhtarChevron Pakistan Ltd.

Mr. Irfan AmirAmerican Life Insurance Company(Pakistan) Ltd.

Mr. Rashid EjaziACNielsen Pakistan (Pvt.) Ltd.

Brig. (R) Farrukh Saeed Sheraton Karachi Hotel

Mr. Faisal GhayasSinger Pakistan Ltd.

Mr. Mohammad Rashid-ul-HassanOBS Pakistan (Pvt.) Ltd.

Mr. Imdad KhanLMK Resources Pakistan (Pvt.) Ltd.

Mr. Jamil MughalSIZA Foods (Pvt.) Ltd. (McDonald's)

Mr. Rehan QureshiEMC Information Systems (Pvt.) Ltd.

Mr. Usman QureshiDuPont Pakistan Operations (Pvt.) Ltd.

Col. (R) Chaudhry Muhammad SabahuddinCitibank, N.A.

Col. (R) Filraz SiddiquiPfizer Pakistan Ltd.

Report of Security Sub-Committee

CHAIRMAN

Mr. Tauqir AhmedChief ExecutiveDuPont Pakistan Operations Pvt.) Ltd.

46

TERMS OF REFERENCE

1. To create a forum via which ABC companies are able to access effective information and contact the appropriate resources when the need arises.2. To maintain a database of actual incidents experienced by ABC member companies that can be taken up in meetings with the government or relevant people.3. To identify and maintain contacts within the Govt., Rangers, Police, CPLC and Army, to be shared with all members.4. To share information on security threats, advisory notes and best practices regarding safety measures amongst the Sub-Committee and larger membership as required via SMS.5. To remind all members to regularly update their security plans and strategies.

THE ACTIVITIES OF THE SUB-COMMITTEE ARE SUMMARIZED BELOW:

1. The Chairman worked with the Sub-Committee to map out security issues and put in place a cohesive way of working together by building up a reliable communication system.2. The Sub-Committee worked with Mr. Norbert Almeida, Head of Security at P&G, to include interested ABC Security Heads to the Security Alert SMS system. This facility allowed the ABC Security Heads to benefit from an increased flow of information and security advisories.

3. The Sub-Committee maintained contact with the rangers and police. 4. The Sub-Committee provided financial support to the CPLC by requesting donations from member companies and invited Mr. Ahmed Chinoy, Chief of Citizens-Police Liaison Committee (CPLC) and his team to meet with the ABC Executive Committee.5. The Sub-Committee provided the ABC Membership with the facility of using the expertise of the Sub-Committee as an advisory panel on security issues.

SUPPORT TO MEMBERS:

• Members’ specific issues were actively dealt with through coordination with the Police and CPLC for early resolution.• Law & order incidents within the business community were regularly shared with members along with proposed precautionary measures.

COORDINATION WITH US EMBASSY / CONSULATE:

The Sub-Committee had close interaction with U.S. Embassy and the Consulate. The U.S. Consulate in Karachi and Embassy in Islamabad issues periodic warnings / advisory information to U.S. citizens and American companies in Pakistan. These warden messages, which include precautionary measures, were immediately forwarded by email to ABC members.

Thank you to all the Sub-Committee members and the ABC Secretariat for their support & contribution.

47

ANNUAL REPORT 2013

MEMBERS

Mr. Tauqir AhmedDuPont Pakistan Operations (Pvt.) Ltd.

Mr. Faisal SabzwariProcter & Gamble Pakistan (Pvt.) Ltd.

Mr. Osman Asghar KhanEMC Information Systems (Pvt.) Ltd.

Mr. Ahmed Jamal Mir Prestige Communications (Pvt.) Ltd. (Grey)

The U.S. Relations Sub-Committee is headed by Mr. Farrokh K. Captain. The Subcommittee does not seek membership from outside the Executive Committee. It functions as a small task force as and when the President needs to call on it.

TERMS OF REFERENCE

1. The ABC to play a key role in defining and influencing U.S. policy, practices and procedures towards Pakistan.2. Maintain an active relationship with key stake holders representing the U.S. in Pakistan.3. Define the key messages of the ABC, to be shared and aligned with the U.S. at every opportunity.

THE ACTIVITIES OF THE SUB-COMMITTEE ARE SUMMARIZED BELOW:

• There was ongoing discussion with the U.S. Embassy and Consulate with the outcome being a much stronger relationship with the U.S. Mission. These interactions included two meeting with H.E. Richard G. Olson, U.S. Ambassador to Pakistan and several meetings with U.S. Consul General Michael Dodman.• The Sub-Committee met with H.E. Richard G. Olson, U.S. Ambassador to Pakistan on February 25th 2013 in Islamabad, along with other members of the Executive Committee.• H.E. Richard G. Olson, U.S. Ambassador to Pakistan paid a courtesy call to meet members of the Executive Committee at the ABC Secretariat on June 28th, 2013. • The Sub-Committee strategized on establishing an active role for Pakistan corporate sector in the formulation of U.S. economic policy towards Pakistan.• The Sub-Committee continued to explore ways and means to promote U.S.-Pakistan relations at the non-officials level. Changing perceptions both in Pakistan and the USA are the focal point of this thinking and it is important to continuously work on this front. The ABC visa facilitation program came after several years of interaction with U.S. Consular officials.• The Sub-Committee maintained dialogue with the U.S. Consul General Michael Dodman and Consular Chief Mark McGovern over the course of the year to successfully implement a U.S. visa facilitation scheme for the ABC member company employees. The scheme requires AMEX to create a special visa appointment category for full-time employees of the American Business Council Member

Report of US Relations Sub-Committee

CHAIRMAN

Mr. Farrokh K. CaptainChairman & Managing DirectorCaptain-PQ Chemical Industries (Pvt.) Ltd.

48

Companies anywhere in Pakistan who are going to the U.S. on temporary travel for business purposes, or to perform work as permitted by the appropriate nonimmigrant work visa. There will be 10 interview appointments per interview day reserved for the ABC member employees (adjusted if demand increases). With their

otherwise often being some weeks wait time for a visa appointment, this facility will provide members with the flexibility to schedule a visa appointment at their early convenience.

Thank you to all the Sub-Committee members and the ABC Secretariat for their support & contribution.

49

ANNUAL REPORT 2013

ABC was represented on the following Councils/Committees:

1. ADVISORY COUNCIL OF THE MINISTRY OF FINANCE President ABC

2. ADVISORY COUNCIL OF THE MINISTRY OF COMMERCE President ABC

3. PROVINCIAL COMMITTEE ON INVESTMENT (SINDH) President ABC

4. FEDERATION OF PAKISTAN CHAMBERS OF COMMERCE & INDUSTRY (FPCCI)

a) EXECUTIVE COMMITTEE Mr. Tasleemuddin Ahmed Batlay Director Colgate-Palmolive Pakistan Ltd.

b) GENERAL BODY Corporate Class Mr. Saad Amanullah Khan Chief Executive Officer Gillette Pakistan Ltd.

Associate Class Mr. Tasleemuddin Ahmed Batlay Director Colgate-Palmolive Pakistan Ltd.

ABC Representation

50

ABC Suggestions for the Federal Budget 2013-14

ANNUAL REPORT 2013

EXECUTIVE SUMMARY

Attached are the proposals for the upcoming Federal Budget 2013/2014 which comprise of 8 taxation related proposals and 6 procedural improvement/modification proposals. All these proposals will positively impact the ability for U.S. companies to operate efficiently in Pakistan. The procedural suggestions are designed to help streamline and improve tax collection and appeal processes.

The ABC vision remains to have a robust, understandable and transparent taxation environment which includes:

• EVERY EARNING MEMBER OF SOCIETY SHOULD BE PAYING TAXES:

• We have one of the lowest “Tax to GDP” ratios in the world, at less than 9%.

• Major sectors of the economy are not appropriately taxed, such as agriculture, real estate & the stock market.

• Industry, which makes up 20% of the GDP, is disproportionately taxed.

• Currently less than 2% of the population pays personal taxes.

• HAVE A SIMPLE TAXATION STRUCTURE:

• Taxes should be easy to levy and easy to file

for tax payers. • The focus should be on only 3 sources of

taxation, i.e. 1. General Sale Tax (GST); 2. Customs Duty; 3. Corporate and Personal Income Tax.

• SHOULD BE COMPETITIVE VIS-À-VIS OTHER COUNTRIES:

• Make Pakistan attractive for foreign investment by making its taxation competitive.

• This in turn will help reverse the unfortunate brain drain taking place.

Saad Amanullah KhanChairman Finance &

Taxation Sub-Committee

ABC Suggestions for Federal Budget 2013-14 ANNEXURE - A

54

ABC Suggestions for Federal Budget 2013-14TAXATION PROPOSAL INDEX 1. HIGH CORPORATE TAXES

1A) Expansion of the Tax Net 1B) High Corporate Income Tax 1C) Rationalize Minimum Turnover Tax

for all Companies 1D) Simplify Advance Taxes for

Manufacturer 1E) High Rate of Advance Income Tax at

Import Stage 1F) Section 153A Tax under Garb of

Documentation 1G) Inter Corporate Dividend

2. PRESUMPTIVE TAX REGIME (PTR)

3. EXPANSION OF GENERAL SALES TAX (GST)

3A i) Suspension without notification 3A ii) Blacklisted Suppliers 3B) Withholding of Sales Tax

4. EXCISE DUTY

4 A) Elimination of FED on Soft Drinks 4B) Refund of FED (Excess Input less

output) is not allowed

5. PERSONAL INCOME TAX 5A) Tax Relief for lower Salaried Class 5 B) Implementation of a “Tax Payer Card”

5C) Elimination of Cap on exemption of Interest on House Loans

5 D) Tax on Employers’ Contribution to Recognized Provident Fund

5 E) Withholding tax on Banking Transactions

5F) Small Payments for Prize and Winnings 5G) Introducing Rebates for Salaried

Individuals and other individuals i) Tax Credit on Education Expenses ii) Tax Rebate on Medical Expenses iii) Increased range of Tax Slabs (Salaries)

5 H) Anomaly in tax slabs for salaried individuals

6. BANKING SECTOR

6A) Disallowance of Unrealized Loss on Foreign Exchange Contracts, Foreign Currency Options and Interest Rate Derivative Contracts

6 B) Disallowance of Bad Debts

7. SALES TAX 7 A) Pharmaceutical Sector i) Pharmaceutical Inputs ii) Import of In-Vitro Diagnostic

Equipment iii) Import of Amber Glass Bottles Type-III

8. CREATING VIBRANCY IN THE IT SECTOR

8 A) Incentivize IT Export of Services 8 B) Preferential Tax Regime for IT Sector 8 C) Value Addition Tax for Importers

55

ANNUAL REPORT 2013

5 E) Withholding tax on Banking Transactions

5F) Small Payments for Prize and Winnings 5G) Introducing Rebates for Salaried

Individuals and other individuals i) Tax Credit on Education Expenses ii) Tax Rebate on Medical Expenses iii) Increased range of Tax Slabs (Salaries)

5 H) Anomaly in tax slabs for salaried individuals

6. BANKING SECTOR

6A) Disallowance of Unrealized Loss on Foreign Exchange Contracts, Foreign Currency Options and Interest Rate Derivative Contracts

6 B) Disallowance of Bad Debts

7. SALES TAX 7 A) Pharmaceutical Sector i) Pharmaceutical Inputs ii) Import of In-Vitro Diagnostic

Equipment iii) Import of Amber Glass Bottles Type-III

8. CREATING VIBRANCY IN THE IT SECTOR

8 A) Incentivize IT Export of Services 8 B) Preferential Tax Regime for IT Sector 8 C) Value Addition Tax for Importers

PROCEDURAL PROPOSAL INDEX

1. GENERAL SALES TAX RELATED 1A) Section 8B of the Sales Tax Act 1990

should be abolished/amended 1B) Section 48 of the Sales Tax Act, 1990 1C) Sales Tax Withholding Agents &

Withholding Rules 2007

2. AMENDMENT OF ASSESSMENT – SECTION 122

3. APPEAL PROCESS – SECTION

124/127/129/131/132

4. STREAMLINING IDEAS FOR COLLECTION OF TAXES

4A) Streamline Collection of General Sales Tax 4B) Streamlining Collection of Withholding

Taxes 4C) Payments to Non Resident Persons

under Section 152 of the ITO, 2001 4D) Unwarranted Notices Received u/s 176 of the ITO 2001

4E) Tax Challaan Verification

5. CORPORATE TAX RELATED 5A) Long Outstanding Refund

6. UNWARRANTED NOTICES RECEIVED FROM TAX AUTHORITIES

56

1. HIGH CORPORATE TAXES

1 A) Expansion of the Tax Net

All sectors including Agriculture and Retail and Wholesale need to be brought under the tax net and proportionally taxed.a) All individuals and commercial businesses

should be taxed irrespective of their exemption status.b) Tax evaders need to identified and taxed.

Some ideas on identifying evaders are:a. Better coordination between SECP and FBR:

This will result in detecting companies which are although registered with SECP but are not registered with FRB and thus are not under the tax net.

b. International Travel, Utility an Communication Bills: Individuals and companies making payments for their utility bills (electricity, gas, water), communication bills (cell phones, PTCL) and for internationally travel (business or pleasure) need to be checked whether they are in the tax net. If spending is above a certain level then these entities made to pay taxes.

c. Foreign Remittances Taxed: Foreign transfers not related to royalty, dividends or business services need to be tracked and taxed. Under subsection 4 of section 111 of the Income Tax Ordinance 2001, Foreign Remittances through banking channels are not questioned or taxed. Modified this sub-section to the extent that a minimum tax can be levied.

d. Bank Account Information: It should be made mandatory for Banks and Financial Institutions to share with FBR all banks deposits, loans and investments made so that FBR may probe the source of such amounts deposited/invested.

e. Investments in Mutual Funds Pension Funds: Source of investment in Mutual Funds/Pension Funds for Tax Credit should be documented.

f. Dealers of Precious Metals: It should be made mandatory for all dealers of precious metal (gold etc.) to file or maintain records including name, NTN/CNIC, complete mailing address etc of all buyers of such metal and submit such details to FBR on quarterly basis.

1 B) High Corporate Income Tax

In order to remain internationally competitive, Pakistan needs to reduce its corporate tax rate to a maximum of 30% in line with regional standards.

1 C) Rationalize Minimum Turnover Tax for all Companies

It is recommended that to create a level playing field to the new entrants in the market the minimum tax should be reduced to 0.2% in the first 3 Tax Years of the company. For existing companies who have made investments exceeding US$ 0.5 Million, the same should be applicable for the year of additional investment to encourage investment in existing facilities. On net we recommend this facility should be valid for 10 years after the investment is made.

1 D) Simplify Advance Tax for Manufacturers

1. It is recommended that preferably the law be changed to the one, which was in force before the 2006 Finance Act amendment whereby a company was required to pay advance tax equal to one fourth of the tax liability finalized for the latest tax year or at least the benchmark of 90% should be reduced to 80%, as it has been historically.

Taxation Proposals for Federal Budget 2013-14

57

ANNUAL REPORT 2013

2. Manufacturers should be given exemption from withholding taxes u/s 153 and u/s 148. They should only be required to pay advance tax u/s 147. This way the manufacturers will pay the same amount of advance tax but through a much simpler way. Reduce complexity at both ends, i.e. payer and government.

1 E) High Rate of Advance Income Tax at Import Stage

It is suggested that tax at source be reduced to 1% for manufactures. Further the commissioner should be empowered to issue exemption certificate.

1 F) Section 153 A Tax Under Garb of Documentation

Section 153A should not be reinstated as it has proved in the past to create more complexity and does not deliver benefits towards the documentation of the economy. We remain committed to seeking practical methods and solutions towards the documentation of the economy.

1 G) Inter Corporate Dividend

Tax on dividend to the corporate entities should be exempt from this withholding tax.

2. PRESUMPTIVE TAX REGIME (PTR)

It is proposed that Presumptive Tax Regime (PTR) should be eliminated. This can be done in phases with the objective fully document the existing economy, as well as to encourage foreign companies to enter into Pakistan’s market.

a) Initially FBR should allow adjustment of first

three years of tax losses against their full and final tax liability as assessed under PTR.b) Gradually incentivize companies, as it is

currently doing, to move to a Normal Tax Regime (NTR). One suggestion is to make NTR rates more attractive verses PTR and modify the law accordingly.

c) Manufacturers/importers assessed under NTR, meeting with a certain preset criteria, should be given the option to merge their manufacturing and trading profits for the purpose of their final tax calculations. Preset criteria will limit possible abuse & only those companies should be allowed to opt who meet the minimum criteria on investment in fixed assets, or company turnover.

d) In addition companies falling under PTR and making losses should not be subject to WWF levy.

3. EXPANSION OF GENERAL SALES TAX (GST)

To expand the tax net, attracting entities register for GST is critical. Some ideas for creating incentives and dispelling fear for potential entities to enter the GST net are:

Expansion and Communication:

1. The GST rate should be reduced to be comparable levels versus other Asian markets which will encourage registration. A general economic model is that if GST exceeds 10%, people start engaging in widespread tax evading activity.

2. The GST process should be simplified to enable medium and small sized trader's to understand the ‘concept; easily. The documentation requirements should be reduced to avoid unnecessary work.

Taxation Proposals for Federal Budget 2013-14

58

3. Special team using 3rd party qualified companies should be brought on-board and who will work with businesses to help them understand and file for GST. This is in line with FBR work towards enhancing cooperation and helping in expanding the GST net.

4. The Government should run media and awareness programs to publicize these incentives and to explain the easy user friendly filing and collection system.

Incentives to Attract Registration:

1. No sales tax audits should be carried out for newly registered small traders during the first 5 years of an entity’s registration. Only exception will be if the entity claims any refunds, in that case for verifications.

2. Small traders, having limited turnover, may be allowed to file a sales tax return once every 6 months. This will make the compliance easy for small traders.