mortgage professional australia magazine issue 13.03

DESCRIPTION

The magazine for mortgage professionals in Australia.TRANSCRIPT

MPAMAGAZINE.COM.AUISSUE 13.3

NON-BANKS ON TRIALWHY NON-BANKS AND

MORTGAGE MANAGERS AREN’T OUT FOR THE COUNT

BUSINESS PARTNERSHIPSWHAT HAPPENS WHEN THE

LOVE DIES?

TAKING ON THE BIG FOURME BANK CEO JAMIE MCPHEE

ARGUES THE CASE FOR THE NON-MAJORS

YO NGGU S

CONTENTS / ISSUE 13.03

2 | MPAMAGAZINE.COM.AU

31 | Young Guns Meet the young talent that’s taking the Australian mortgage broking industry by storm

COVER STORY

WEEKLY INVESTIGATIONS

NOW ONLINE: Are you valued by your brokerage?

Build better business

relationships: 3 vital tips

» mpamagazine.com.au

2446Non-banks on trial Non-bank lenders and mortgage managers argue their case

Head to head ME Bank CEO Jamie

McPhee talks to MPA about breaking

the big four dominance

CONTENTS / ISSUE 13.03

4 | MPAMAGAZINE.COM.AU

NEWS & VIEWS8 | Round-upThe latest market intelligence from the world of property, economics and mortgages

12 | On lineThe best from MPA Online and Australian Broker Online

14 | News Analysis What do mortgage enquiry and approval figures tell us about state-by-state mortgage demand?

SMART BUSINESS18 | Business partnerships: What happens when the love dies? How to avoid things turning sour when partnerships come to an end

28 | Mission impossible 9 tips for dealing with demanding clients

59 | Three keys to business planning Make this year your most successful to date

PROFILES44 | MPA Top 10 broker Jeremy Fisher on his drive for exceptional service

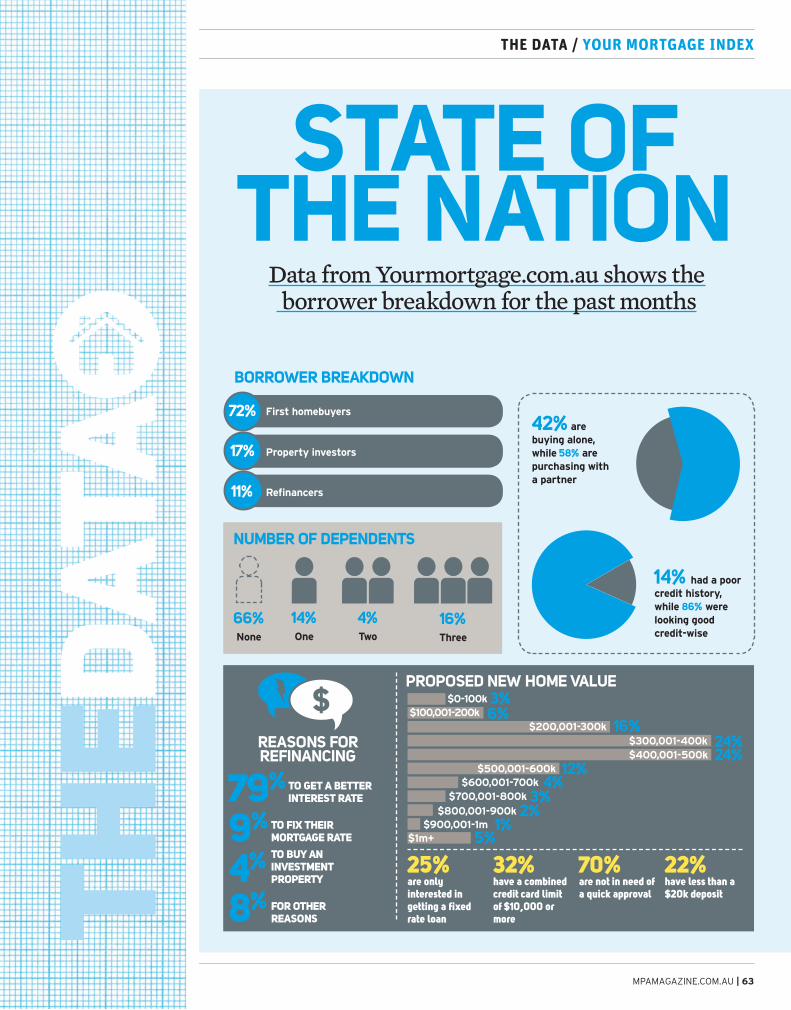

STATS63 | Your Mortgage Index The latest mortgage hunter trends from our sister website

LIFESTYLE62 | A day in the life of … James Veigli, Broker Profits Vault

64 | My favourite things ... Andrew Russell, Mortgage Choice

52

18

64

28

18

6 | MPAMAGAZINE.COM.AU

CONTENTS / EDITOR’S LETTER

There’s no doubt that mortgage brokers are facing some significant challenges in the current economic climate. Credit growth is slow and new regulations are coming in thick and fast.

It’s refreshing, therefore, to speak to those brokers who are new to the industry and gauge the genuine level of enthusiasm for the profession that is being exhibited at its grass roots. The 16 bright young

brokers that we’re profiling in MPA’s annual Young Guns feature (page 31) exemplify the passion and work ethic that’s required to make a go of mortgage broking in 2013. As you will see, their approach to getting the job done is truly inspirational.

Judging by recent industry figures, the mortgage market may be blowing either hot or cold depending on your location, and the big four’s slice of the pie is expanding (News Analysis, page 14), but the non-bank lenders and mortgage managers still believe they have plenty to offer brokers and their clients – despite the adverse publicity caused by the Provident Capital and Banksia collapses (page 46).

And it’s not just the non-banks that are arguing their case. ME Bank CEO Jamie McPhee certainly thinks that there’s room for the smaller bank lenders to work with brokers to increase their share of the mortgage market (page 24).

Whatever direction the mortgage market is heading, if our Young Guns are anything to go by, it looks as if the future of the broker channel is in safe hands.

Robin Christie, editor, MPA

FRESH TALENT

Contact the editor:[email protected]

CONNECT

Printed on paper produced from 100% sustainable forestry, grown and managed specifically for the paper pulp industry

COPY & FEATURESEDITOR Robin ChristieCONTRIBUTORS Bob Neill, David Fotheringham, Cindy Tonkin, Sue ViskovicPRODUCTION EDITORS Carolin Wun, Moira Daniels

ART & PRODUCTIONART DIRECTOR Jonathan PhillipsSENIOR DESIGNER Rebecca Downing

SALES & MARKETINGNATIONAL SALES MANAGER Rajan KhatakACCOUNT MANAGER Simon KerslakeMARKETING EXECUTIVE Anna KeaneTRAFFIC MANAGER Abby Cayanan

CORPORATECHIEF EXECUTIVE OFFICER Mike ShipleyMANAGING DIRECTOR Claire PreenCHIEF OPERATING OFFICER George WalmsleyMANAGING DIRECTOR – BUSINESS MEDIA Justin KennedyASSOCIATE PUBLISHER Rajan KhatakCHIEF INFORMATION OFFICER Colin ChanHUMAN RESOURCES MANAGER Julia Bookallil

Editorial enquiriesRobin Christie tel: +61 2 8437 4787 [email protected]

Advertising enquiriesSales ManagerRajan Khatak tel: +61 2 8437 [email protected] ManagerSimon Kerslake tel: +61 2 8437 [email protected]

Subscriptionstel: +61 2 8437 4731 • fax: +61 2 9439 [email protected]

Key Media keymedia.com.auKey Media Pty Ltd, Regional head office, Level 10, 1–9 Chandos St, St Leonards, NSW 2065, Australiatel: +61 2 8437 4700 fax: +61 2 9439 4599Offices in Singapore, Auckland, Torontompamagazine.com.au

Copyright is reserved throughout. No part of this publication can be reproduced in whole or part without the express permission of the editor. Contributions are invited, but copies of work should be kept, as MPA magazine can accept no responsibility for loss

NEWS / ROUND-UP

BROKERNEWS.COM.AU | 7

8 | MPAMAGAZINE.COM.AU

NEWS / ROUND-UP

Fraud a ‘continuing’ trend in broking: ASICFraudsters cost Australia a whopping $372.7m last year alone, and ASIC says the issue is a serious one within the mortgage broking industry.

ASIC spokesperson, Daniel Wright, said the organisation is seeing a ‘continuing’ trend of fraud within the mortgage broking industry and says it is the category of misconduct involving brokers that is, in fact, most regularly reported to ASIC.

“ASIC is particularly concerned with instances where persons have engaged in fraud or other misconduct relating to information provided in loan applications. Since the commencement of the NCCP, ASIC has banned six persons from engaging in credit activities for such conduct and has 18 other current investigations. ASIC has also secured criminal charges against one finance broker under the responsible lending provisions of the NCCP.”

But MFAA CEO Phil Naylor argued that fraud remains a relative rarity in the mortgage broking industry, accounting for less than a handful of finance industry cases.

“From MFAA’s experience, lending fraud occurs but based on our expulsions – three last year – it is clearly not a major issue for brokers. All lenders, aggregators and good brokers have systems and checks and balances to mitigate against fraud.”

Yet, a report released by KPMG – in the very same week that ASIC clamped down on two rogue brokers – brings the issue to a head.

Finance, perhaps unsurprisingly, boasts the highest fraud rate of any industry in Australia, according to KPMG’s 2013 Survey of Fraud, Bribery and Corruption in Australia and New Zealand. The report found that the financial services industry accounted for 86% of all fraud in Australia and New Zealand in 2012. Twenty-five per cent of fraudsters came from outside the company they victimised.

Do you see the web as a growing source of competition for home loan hunters? Think again, says MFAA CEO Phil Naylor. He believes that the internet is nothing more than a tool when it comes to borrowers seeking a home loan – and that online portals pose little risk to the broking industry.

While Naylor acknowledges that the internet is a vital tool for home buyers, he’s not convinced that flashy bank websites pose a major threat.

“While the internet is one of the most important sources of information for home buyers when researching potential property purchases, the best locations and their finance options, face-to-face contacted with an MFAA broker is central to completing a deal,” he said.

Naylor said the MFAA’s own research shows 81% of potential borrowers planning to buy a house within the next 12 months are using the internet as their ‘primary’ source of information – but that this is a preliminary step taken before contacting a mortgage broker.

“There is no risk the industry risks fading away as we are now providing more than 40% of home loans in the market and are growing as a crucial financial services sector. While technology is obviously important as a first step in potential borrowers searching for a loan, it is the broker who can secure the loan for the customer through face to face contact, which is more important than ever before.”

He added that the industry and its representatives are spending ‘record sums’ of money online in order to help brokers connect with their potential customers.

INTERNET NO THREAT TO BROKERS: MFAA

ONLINEFRAUD

42.7% The percentage of Australians that indicated that they are living debt free Source: December 2012 St.George-Melbourne Institute Household Financial Conditions Report

STATS

10 | MPAMAGAZINE.COM.AU

NEWS / ROUND-UP

Spread the news, residential property is still a solid choice for investors. This is the assessment of AMP Capital chief economist Shane Oliver. He has added, however, that residential property still places second to the share market in predicted medium-term (five-year) returns.

He argued that, for the past five years, bonds and cash have been ‘the place to be’ and that, while yields on bank deposits have been single digit, they’ve still been higher than returns from both shares and residential property.

Now, said Oliver, things have changed – signalling good news for those working in the property market.

“Going forward, shares and to a lesser degree property, are likely to be a better option for investors – depending, of course, on their risk tolerance – as global recovery supports growth assets and low yields hamper the returns from bonds and cash,” he said, adding that residential property and shares already offer higher yields than cash and bonds – and will benefit as economic growth improves.

“House and apartment yields are running around 3.7% and 4.8% respectively, which are well up from their lows last decade. With mortgage rates well off their highs and likely to fall further, the residential property market appears to have bottomed out after falling since mid-2010, with a mild cyclical recovery likely over the next 12 months.”

However, Oliver warned that short-term gains are likely to be restricted to around 5-7% as buyers remain cautious about taking on excessive debt, particularly as job insecurity remains high.

“More broadly, capital growth in residential real estate is likely to be constrained over the next 5–10 years by still very high property prices. This suggests a cyclical rebound in prices over the next year should be seen as part of a broad range-bound market for property prices in real terms as the market continues to work off the excesses that built up over the property boom of the mid-1990s [which] continued into last decade.”

He explained that, while good quality properties in sought after locations will no doubt do well, medium term back drop for property returns is likely to remain constrained – though still better than cash and bonds.

“There are two risks for property. The main downside risk is that China has a hard landing with the hit to export earnings, resulting in higher unemployment, forced sales and hence lower house prices,” he said. “The other risk is on the upside – a concern that the old housing bubble is reignited by the latest collapse in mortgage rates… This seems unlikely though, given Australians have developed a more cautious approach to debt since the GFC.”

Watch out, ASIC commissioner Peter Kell has stated that the regulator will crack down on brokers this year.

“ASIC conducted a study at the end of 2011 on how brokers were travelling in terms of complying with the new legislation and we found that, generally, there was a pretty good understanding of the new legislation – but there were some areas where we thought there needed to be an improvement,” he told Broker TV.

For example, Kell said brokers need to understand that they have responsibilities when it comes to establishing the customer’s ability to

repay or deal with the credit that’s being offered. “They can’t just rely on, for example, the lenders. So, while we are seeing generally good compliance, it’s very important for brokers to understand that their responsibilities in this area are also quite important to get across. They can’t sort of ‘outsource’ those to others.”

Kell said there are three areas ASIC will be focusing on in the mortgage broking space this year: fraudulent material provided on loan applications; advertising; and disclosure. He added that any claims of ASIC taking a ‘light touch’ approach are unwarranted.

REGULATION

ASIC VOWS 2013 BROKER CRACKDOWN

Housing investment back in fashion

INVESTMENT

83.65% The percentage of new home loan approvals that were variable rate in January – a six-month high Source: Mortgage Choice

STATS

INFOGRAPHIC

NAB Capital City House Price Forecasts (%)*

2013 2014

* percentage changes represent through the year growth ratesSource: NAB Residential Property Servey Dec 2012

0

1

2

3

4

5

Syd

ney

Mel

bour

ne

Bri

sban

e

Ade

laid

e

Per

th

Ave

rage

2.1

3.7

0.4

2.01.7

3.5

2.0

0.1

3.5

5.0

1.4

3.1

MPAMAGAZINE.COM.AU | 11

NEWS / PRODUCT ROUND-UP

PRODUCT NEWSYour bite-sized guide to the industry’s newest products and initiativesWho: BankwestWhat: Two new home loans: Double Deal Home Loan and Regular Saver Home Loan

Who: Australian First Mortgage (AFM)What: Second funding line in respect to lending to SMSFs

They say: “This new product is exciting as the higher LVR was in much demand” – AFM founding director Iain Forbes

We say: Higher LVR SMSF products are a welcome addition to the market.

KEY FEATURES: • 80% LVR on AFM’s new

Secure Option Full Doc residential product

• P&I repayments to 30 years• Interest-only repayments to

10 years• Maximum loan amount of

$500,000

Key specs – Double Deal:• Discount of 1.01% pa off the SVR for two years• No on-going fees• Minimum loan amount of $20,000• 95% LVR (where applicable)• Exclusive introduction application fee of

$295 (limited time offer)• 100% offset facility with a monthly fee of $15

Key specs – Regular Saver:• Basic variable product• Replaces the Lite Home Loan• Applicable for transfers from existing

Bankwest home loans (unlike Double Deal)

• Exclusive introduction application fee of $295 (limited time offer)

• 100% offset facility with a monthly fee of $15

They say: “I can confidently say that Bankwest is ready and is thrilled to give our customers more value for money whilst providing our brokers with a greater choice in this ultra-competitive market” – Bankwest head of specialist banking, Ian Rakhit

We say: The Double Deal’s introductory discount should turn heads.

NEWS / MULTIMEDIA

12 | MPAMAGAZINE.COM.AU

ON LINEThe latest highlights from MPA Online and Australian Broker Online

It’s that time of the year again. Fitch Ratings has published its signature postcode delinquency report, providing a fascinating insight into those areas where the mortgage delinquency rates are well above the national average. Are you operating in a high-risk area?

In terms of overall mortgage values, the country’s delinquency hot spot was Nelson Bay, NSW, which reached a 30-plus day arrears rate of 6.6% in September 2012. This was an improvement on its March 2012 rate of 7.8%, but wasn’t enough of a drop to take it off the top spot.

“Nelson Bay has been the worst performing postcode in Australia since this report was first published in November 2007,” said the agency in its write up.

“If these foreclosed properties were to be sold and the 90-plus day arrears cured, Nelson Bay arrears would improve significantly.

“Other postcodes, such as Surfers Paradise (Qld), Pacific Paradise (Qld), Waterford (Qld), Greenacre (NSW), Rooty Hill (NSW), and Green Valley (NSW), remain among the worst performing by mortgage value.”

When it came to those areas with the worst delinquency rates by number of mortgages in arrears, Tasmania’s Montrose was the worst performer – with 32 borrowers out of 1,000 in delinquency.

“Surfers Paradise (Qld), Eagle Vale (NSW), Cessnock (NSW), Waterford (Qld), Nelson Bay (NSW), Crestmead/Marsden (Qld), Green Valley (NSW), Eagle Vale (NSW), Macquarie Fields (NSW), and Helensvale (Qld) remained among the worst performing postcodes by number of mortgages in arrears, with 18–29 delinquent borrowers out of 1,000,” said the report.

In motionThe latest from Broker News and MPA TV

ASIC TO CRACK DOWN ON MORTGAGE INDUSTRYCommissioner Peter Kell talks about ASIC’s plans for the coming months.

MARKETING GURU’S TOP TIPSThe most effective ways to maximise your marketing strategy.

HOW TO CREATE THE PERFECT PARTNERSHIPWhat’s the best way to establish a referral relationship?

To find out more on all of these stories, as well as latest business strategy advice, special reports, profiles, news, views and analysis, visit mpamagazine.com.au

SAY WHAT? THE BIGGEST QUOTES FROM THE MONTH

“It’s a bit like boiling a frog inhot water; you don’t notice thechange because it happens sosteadily”– Intelligent Finance managing director Justin Doobov on Sydney being labelled the third most expensive city in the world

“I think it’s a matter of – if you do get a client – service the hell out of them”– Daniel O’Brien of PFS Financial Serviceson why individual service trumpsfocusing on any one market sector

“We’re still nMB, we’re notbecoming a sub-set of Aussie.We’re here for brokers whowant to develop a businessunder their own brand”– nMB managing director Gerald Foley on being bought by Aussie Home Loans last July

AUSTRALIA’S MORTGAGE DELINQUENCY HOT SPOTS REVEALED

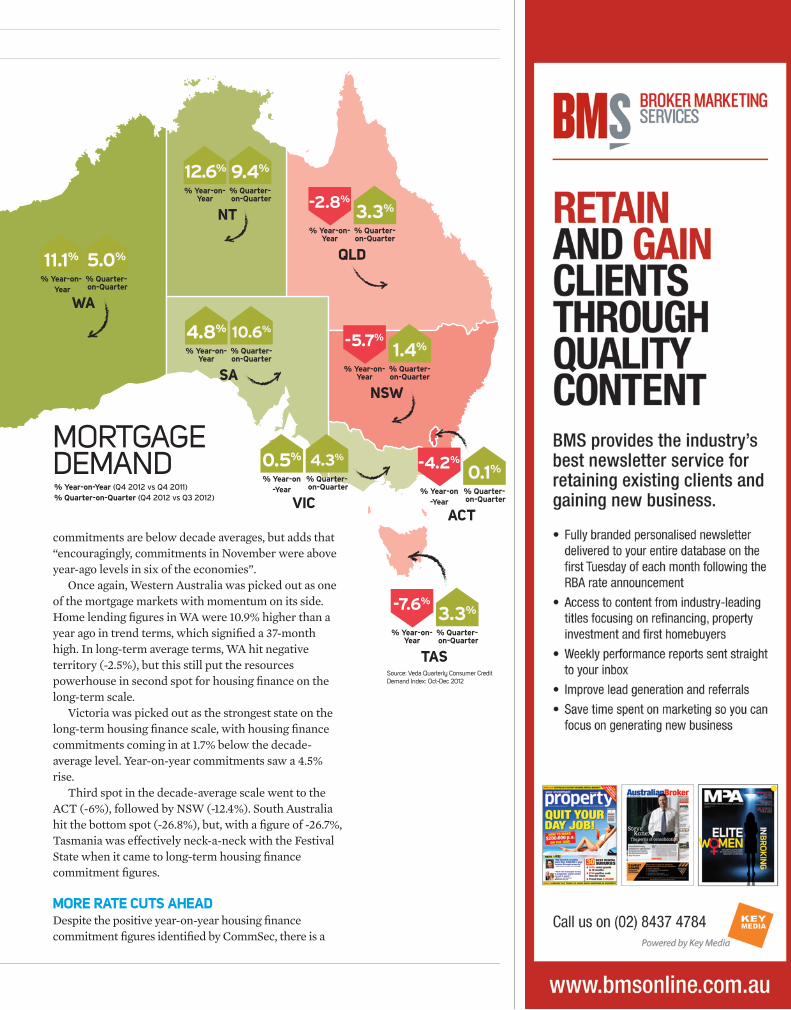

NEWS ANALYSIS / MORTGAGE DEMAND

14 | MPAMAGAZINE.COM.AU

HAVESMortgage enquiry and approval figures suggestthat, despite RBA rate cuts, Australia’s two-speedeconomy continues to be the overriding factordetermining the state-by state demand for home loans

Some interesting statistics have been released in recent times regarding the state of Australia’s mortgage market. Veda’s Quarterly Consumer Credit Demand Index for the final quarter of

2012, for example, indicates that mortgage enquiries remained flat – decreasing by 0.7% nationwide over the course of the year – but that the state-by-state situation tells a varied story.

Judging by the Index’s figures, brokers in the Northern Territory and Western Australia may well have seen an increase in clients walking through their doors – with mortgage enquiries picking up by 12.6% and 11.1% respectively in these resource boom states.

South Australia, too, saw an increase in mortgage enquiries towards the back end of 2012 (4.8%), while home loan enquiries in Victoria remained largely flat (0.5%).

At the bottom end of the scale, Veda’s figures suggest that brokers in Tasmania will have struggled to attract new business. Enquiries here fell by 7.6% between October and December 2012. New South Wales also saw a significant dip in home loan enquiries (-5.7%), while Queensland’s enquiry figures were also in negative territory (-2.8%).

SUBDUED OUTLOOK

HAVE-NOTS&

So what can brokers take from the Index’s latest results? According to Veda, mortgage enquiries are a good indicator of homebuyer demand and housing turnover, with movements in mortgage enquiries tending to lead movements in house prices by around six to nine months.

“Housing markets have, in the majority, been weak since late 2010,” said Angus Luffman, Veda’s general manager of consumer risk.

“There is little evidence in the latest Veda data that the RBA rate cuts are having much effect in reigniting housing turnover, with the level of mortgage applications staying flat since halting a two-year decline in the March 2012 quarter.”

“This generally soft mortgage applicant demand suggests that house price growth will be relatively subdued for at least the first half of 2013.”

REASONS FOR OPTIMISMCommSec’s latest State of the States report, however, provides more heart-warming reading for the broker community. Rather than looking at enquiry activity, the report looks at settled loans in the form of ABS housing finance commitment data.

Its author, CommSec chief economist Craig James, does concede that nationwide trend housing finance

MPAMAGAZINE.COM.AU| 15

commitments are below decade averages, but adds that “encouragingly, commitments in November were above year-ago levels in six of the economies”.

Once again, Western Australia was picked out as one of the mortgage markets with momentum on its side. Home lending figures in WA were 10.9% higher than a year ago in trend terms, which signified a 37-month high. In long-term average terms, WA hit negative territory (-2.5%), but this still put the resources powerhouse in second spot for housing finance on the long-term scale.

Victoria was picked out as the strongest state on the long-term housing finance scale, with housing finance commitments coming in at 1.7% below the decade-average level. Year-on-year commitments saw a 4.5% rise.

Third spot in the decade-average scale went to the ACT (-6%), followed by NSW (-12.4%). South Australia hit the bottom spot (-26.8%), but, with a figure of -26.7%, Tasmania was effectively neck-a-neck with the Festival State when it came to long-term housing finance commitment figures.

MORE RATE CUTS AHEADDespite the positive year-on-year housing finance commitment figures identified by CommSec, there is a

Source: Veda Quarterly Consumer Credit Demand Index: Oct-Dec 2012

MORTGAGE DEMAND% Year-on-Year (Q4 2012 vs Q4 2011)% Quarter-on-Quarter (Q4 2012 vs Q3 2012)

11.1% 5.0%

% Year-on- Year

% Quarter- on-Quarter

WA

12.6% 9.4%

% Year-on- Year

% Quarter- on-Quarter

NT-2.8%

3.3%

% Year-on- Year

% Quarter- on-Quarter

QLD

-5.7%

1.4%

% Year-on- Year

% Quarter- on-Quarter

NSW

4.8% 10.6%

% Year-on- Year

% Quarter- on-Quarter

SA

-4.2%

0.1%

% Year-on -Year

% Quarter- on-Quarter

ACT

0.5% 4.3%

% Year-on -Year

% Quarter- on-Quarter

VIC

-7.6%

3.3%

% Year-on- Year

% Quarter- on-Quarter

TAS

NEWS ANALYSIS / MORTGAGE DEMAND

16 | MPAMAGAZINE.COM.AU

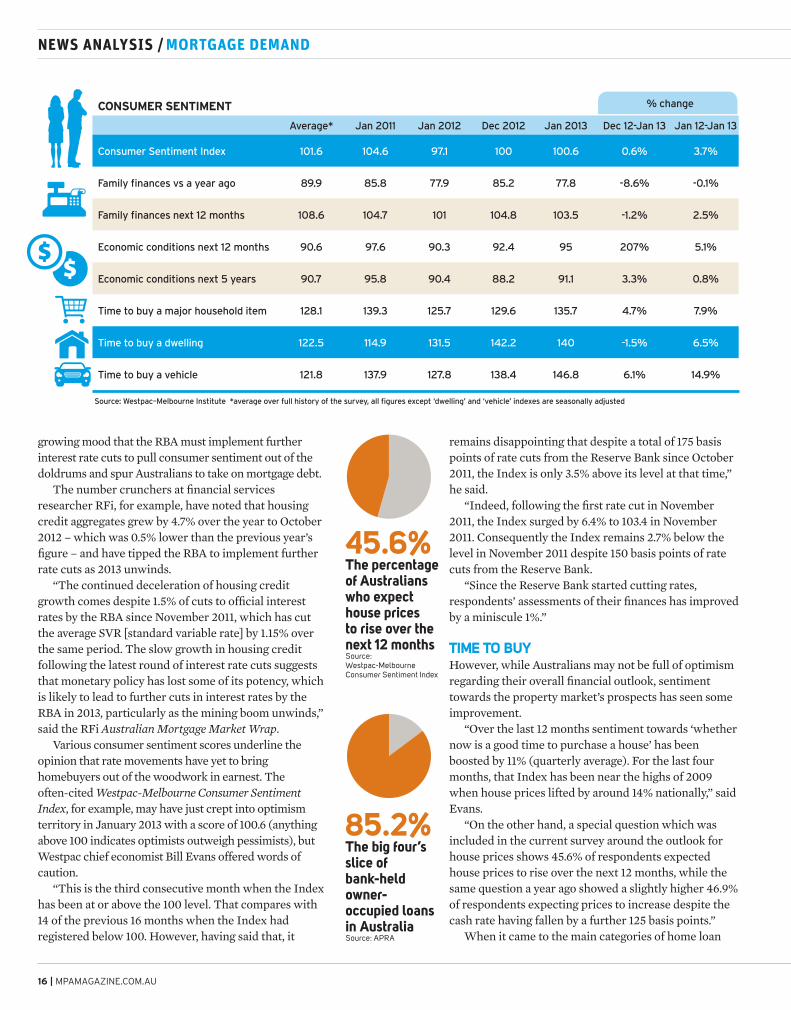

growing mood that the RBA must implement further interest rate cuts to pull consumer sentiment out of the doldrums and spur Australians to take on mortgage debt.

The number crunchers at financial services researcher RFi, for example, have noted that housing credit aggregates grew by 4.7% over the year to October 2012 – which was 0.5% lower than the previous year’s figure – and have tipped the RBA to implement further rate cuts as 2013 unwinds.

“The continued deceleration of housing credit growth comes despite 1.5% of cuts to official interest rates by the RBA since November 2011, which has cut the average SVR [standard variable rate] by 1.15% over the same period. The slow growth in housing credit following the latest round of interest rate cuts suggests that monetary policy has lost some of its potency, which is likely to lead to further cuts in interest rates by the RBA in 2013, particularly as the mining boom unwinds,” said the RFi Australian Mortgage Market Wrap.

Various consumer sentiment scores underline the opinion that rate movements have yet to bring homebuyers out of the woodwork in earnest. The often-cited Westpac-Melbourne Consumer Sentiment Index, for example, may have just crept into optimism territory in January 2013 with a score of 100.6 (anything above 100 indicates optimists outweigh pessimists), but Westpac chief economist Bill Evans offered words of caution.

“This is the third consecutive month when the Index has been at or above the 100 level. That compares with 14 of the previous 16 months when the Index had registered below 100. However, having said that, it

remains disappointing that despite a total of 175 basis points of rate cuts from the Reserve Bank since October 2011, the Index is only 3.5% above its level at that time,” he said.

“Indeed, following the first rate cut in November 2011, the Index surged by 6.4% to 103.4 in November 2011. Consequently the Index remains 2.7% below the level in November 2011 despite 150 basis points of rate cuts from the Reserve Bank.

“Since the Reserve Bank started cutting rates, respondents’ assessments of their finances has improved by a miniscule 1%.”

TIME TO BUYHowever, while Australians may not be full of optimism regarding their overall financial outlook, sentiment towards the property market’s prospects has seen some improvement.

“Over the last 12 months sentiment towards ‘whether now is a good time to purchase a house’ has been boosted by 11% (quarterly average). For the last four months, that Index has been near the highs of 2009 when house prices lifted by around 14% nationally,” said Evans.

“On the other hand, a special question which was included in the current survey around the outlook for house prices shows 45.6% of respondents expected house prices to rise over the next 12 months, while the same question a year ago showed a slightly higher 46.9% of respondents expecting prices to increase despite the cash rate having fallen by a further 125 basis points.”

When it came to the main categories of home loan

CONSUMER SENTIMENT

Average* Jan 2011 Jan 2012 Dec 2012 Jan 2013 Dec 12-Jan 13 Jan 12-Jan 13

Consumer Sentiment Index 101.6 104.6 97.1 100 100.6 0.6% 3.7%

Family finances vs a year ago 89.9 85.8 77.9 85.2 77.8 -8.6% -0.1%

Family finances next 12 months 108.6 104.7 101 104.8 103.5 -1.2% 2.5%

Economic conditions next 12 months 90.6 97.6 90.3 92.4 95 207% 5.1%

Economic conditions next 5 years 90.7 95.8 90.4 88.2 91.1 3.3% 0.8%

Time to buy a major household item 128.1 139.3 125.7 129.6 135.7 4.7% 7.9%

Time to buy a dwelling 122.5 114.9 131.5 142.2 140 -1.5% 6.5%

Time to buy a vehicle 121.8 137.9 127.8 138.4 146.8 6.1% 14.9%

Source: Westpac–Melbourne Institute *average over full history of the survey, all figures except ‘dwelling’ and ‘vehicle’ indexes are seasonally adjusted

45.6% The percentage of Australians who expect house prices to rise over the next 12 months Source: Westpac-Melbourne Consumer Sentiment Index

85.2% The big four’s slice of bank-held owner-occupied loans in Australia Source: APRA

% change

MPAMAGAZINE.COM.AU| 17

applicant, Evans noted that upgraders and investors are responding to the lower rates in “a broadly comparable fashion to 2009”, while first homebuyers have remained reluctant to dip their toes in the property market.

“This is certainly partly due to less generous government subsidies, but may also be impacted by weaker overall confidence around finances and job prospects,” he said.

Support for this theory comes from ING DIRECT’s latest Financial Wellbeing Index, which found that 39% of Gen Y respondents – who might otherwise have been looking to enter the property market for the first time – are instead focusing on saving. Amongst all respondents who intend to save this year, 51% intend to build a spare buffer of cash, while 16% were worried about job security.

The Index also found that the Australian appetite for housing debt remains subdued, with 49% of respondents paying down their mortgage ahead of time and 28% of respondents being mortgage free.

BIG FOUR DOMINATION RAMPS UPWhen it comes to those Australians who do have a desire to take on mortgage debt, one telling figure

highlighted by RFi was APRA’s assessment of the big four’s growing market share.

Within the ‘bank-held owner-occupied loans’ category, for example, the combined market share of the majors increased from 80.3% to 85.2%.

The RFi report does note, however, that the sudden increase “was largely due to APRA’s reclassification of Bankwest as a division of CBA, which officially went into effect on 1 October 2012”.

“As a result of the reclassification, CBA’s share of the owner-occupied home loans market grew from 23.5% in September to 28.4% in October 2012, while ANZ, NAB and Westpac’s penetration of the market remained steady,” said the report. “There was a lack of bank-held owner-occupied loans market share movement among the other lenders and the mutual banks.”

Overall, the banks took a 93.9% slice of owner-occupied lending commitments – a 1.3% increase on the previous month’s figure.

The reclassification of Bankwest also saw the big four cement its grip on the ‘bank-held investment property lending’ category, with APRA’s figures showing the major banks’ share of this segment of the market rising from 82.8% to 85.6%.

-0.7% The decrease in mortgage enquiries over the year to the December 2012 quarter Source: Veda Quarterly Consumer Credit Demand Index

18 | MPAMAGAZINE.COM.AU

Separation is a part of life, but the process can easilyturn sour when business is involved. Seaview Consulting

directors Bob Neill and David Fotheringham explainhow you can ensure a smooth transition – and avoid

decimating your practice’s value – when you and yourbusiness partner decide to go your separate ways

BUSINESS PARTNERSHIPS:

What happens when the

LOVE

FEATURE / BUSINESS PARTNERSHIPS

DIES

Reflecting on 2012, one of the things that surprised and disappointed was the number of business relationships that fractured and descended into protracted disputation during

the course of the year.We have witnessed a significant increase in the

number of partners or shareholders deciding that, whilst they may want to continue in business, they did not wish to do so with their current business partners.

This year’s New Year’s resolution should be for practice owners to revisit their documentation, particularly those aspects which cover exit provisions, to ensure it remains relevant and provides a clear process on how to conduct a smooth exit under varying circumstances.

Separation is a part of life, and for many it is the right decision, and an effective resolution allows all concerned to rule a line and move on.

However, when the dissolution does not go smoothly it becomes an expensive exercise that drains finances and emotion in equal doses. The consequences of protracted unresolved business relationships have far-reaching effects.

Firstly, there is the cost of each party engaging legal representation, which inevitably adds an adversarial flavour to the process and quickly extinguishes any goodwill that existed between the protagonists. Both parties are constantly assured they have a strong position and the desire to ‘win’ overtakes common sense.

Secondly, there is the loss of commercial value as the distraction from business that occurs whilst the battle rages and eats away at the principals’ time, energy, profits, and sustainability of the enterprise. The result can be that by the time agreement has been reached as to how much of the pie each is to get, it becomes irrelevant as the pie no longer has any substance.

Thirdly, the process of dispute takes a significant emotional toll on the participants, particularly where they have conducted business together and been brought close by the joint endeavours. The loss of trust and respect manifests itself in a bitter, unforgiving scenario.

Fourthly, when matters go to court, a ‘no holds barred’ approach is deployed and people’s dirty linen can be aired in the most public of forums. Personal issues are often viewed as impediments to a

professional’s ability to discharge his or her obligations to partners and colleagues.

Such human failings can destroy partnerships just like marital break-ups often lead to home lending foreclosures. Without some confidentiality agreement for protection this can quickly spiral out of control with information of a personal and sensitive nature aired in public.

However, without doubt the major cause for dissolutions escalating into significant disputes can be sourced back to poor or absent documentation around the agreed exit terms for the stakeholders. This inattention is quite astonishing amongst professional advisers, such as mortgage brokers, who would be scathing in their criticism of their clients if they paid as little attention to critical business issues under their watch.

A documented agreement should provide a road map on how to part ways with a minimum of disquiet and in a manner that maximises the value for all parties in an equitable way. The process should be flexible and reflective of the reasons for separation, include timeframes required for settlement and the process used to determine a separation value.

The difficulty is that no single document can predict the nature or reason for a request to separate. However, this does not prevent a business from documenting the framework in a manner that can enable the effective and smooth management of the separation request.

The strength of any relationship can be measured in the ease with which the parties can discuss and resolve differences in opinions or views in a manner that enables the relationship to grow and be rewarding.

The inability to have open dialogue is an early indication of potential future breakdown and should

“Separation is a part of life, and for many it is the right

decision” – BOB NEILL

DIES

FEATURE / BUSINESS PARTNERSHIPS

20 | MPAMAGAZINE.COM.AU

FEATURE / BUSINESS PARTNERSHIPS

also be a prompt for the partners to reflect on what documentation exists to enable an orderly exit should a separation be necessary.

The intent of the exit document is to provide a clear, balanced and fair process to facilitate an exit, while taking into consideration the circumstances of the separation and the ability for the business to operate going forward. It should also ensure that any acquiring party receives an appropriate value for the assets they purchase.

In some circumstances the separation may be managed by an agreed allocation of the revenue source – eg, commissions – with each party electing to manage the allocated clients in a manner suitable for them.

This becomes more difficult when the equity ownership is split to parties primarily performing different functions in the business – ie, one to a sales and advisory function and another to a back-end operational and administrative function. In these circumstances it is difficult to segment a client base by allocating the revenue source, and as such an appropriate exit document needs to address funding mechanisms and payment terms upfront.

JEALOUS CREATURESIt is beneficial to reflect on human nature. More often than not it is the accumulation of little things that destroys a relationship. It is rare for one isolated action to destroy a relationship.

Humans are often very jealous creatures, and if an individual perceives another individual is getting too many non-reciprocal benefits then tensions will surely surface. Ensuring your business has a mechanism and outlet to raise such concerns will prevent the snowball effect that may lead to a destruction of value and the end of a previously rewarding relationship.

If such a mechanism is absent, or should the need to separate arise, it is essential that a business such as a mortgage brokerage has a clearly documented process. When business partnership relationships turn sour and separation is the only solution, such a process can provide the mechanism that prevents the destruction of the firm’s assets and long-term financial viability.

The triggers for separation fall into two categories – insurable or uninsurable events. Insurable events are usually well thought through but difficulties can still arise if:• procedural aspects around the management of the

claims and remittance process do not exist• valuation methodologies are not well documented• payment timeframes are not clear and linked to

receipts from insurersFurthermore, additional documentation is required to address matters outside the insurance process, including procedures around the settlement of debts, the release of security or guarantees and other external factors that may impact the business.

The capital gains tax (CGT) taxation treatment around insurance policies is complex. Avoiding the taxation office taxing a significant share of any proceeds is essential, so confirmation of arrangements around buy-sell agreements need to be correctly structured.

Non-insurable events include the following examples of the varying reasons behind the desire for people to separate:• desire to move to greener pastures• retirement• staleness• a partner not hitting contractual key

performance indicators (KPIs)• acrimony• loss of trust• a sudden departure due to family or health

reasons• alleged theft or fraud• relocation interstate or overseas• financial stress or external demands (if equity

used as security)

The causes of separation

FEATURE / BUSINESS PARTNERSHIPS

22 | MPAMAGAZINE.COM.AU

THE SOLUTIONPrinciples to documenting an exit will depend on the manner in which the relationship is structured – ie, a partnership, equity in a company, units in a unit trust, or units in a hybrid unit trust.

Exit arrangements should be documented in a partnership agreement, a shareholders agreement, or a unit holder’s agreement. All partners should be bound by the agreement to ensure that the objectives of all parties are addressed in an equitable and agreed manner. Here are the key principles to bear in mind:

1 Due to the complexities associated with personal tax, employment termination payments (ETPs), CGT concessions, personal finances and interests of

the extended family in the outcome, construction of an exit arrangement should include and be conducted in a collaborative environment with a legal adviser, an accountant and another external independent financial adviser or specialist adviser.

2 Avoid trying to document all specific reasons for someone wanting to exit. Documentation should be based on generic reasons for an exit request

such as personal circumstance, performance, financial stress, unplanned events, health, loss of trust, moving to another business or retirement.

3 The treatment for insurable events should be managed separately to uninsurable events.

4 Attention to health-related absenteeism or reduced performance should be specifically addressed around times, KPIs and independent

assessment. You are more likely to be faced with an issue around performance triggered by health than death.

5 The procedure around the engagement with and transfer of clients including a methodology for value recognition is required. For disputed

clients, a process that involves an independent person contacting the client and confirming their preferred relationship in an orderly and agreed manner is also required.

6 Remuneration arrangements up to the point of departure need to be addressed including whether any adjustment is required for

underperformance to expectations or whether there are entitlements to contractual incentives including profit share. Transition/handover support obligations should also be documented.

7 The treatment of any balance sheet items must be documented, such as repayment of loans or loan accounts, personal use assets,

secured finance or guarantee arrangements in place and any ongoing responsibility for liabilities for historical work performed.

8 If an equity owner isn’t performing, the agreement should contain a mechanism that affords the non-performer notice of failure to

achieve specific and documented KPIs. The agreement should require that the non-performer be independently appraised of the KPI that has not been met and there should be reasonable time given to correct any underperformance. Failing to attain the KPIs will instigate exit procedures without any consequences.

9 It is essential the document includes a logical and compulsory dispute resolution process that includes the use of mediation with the ‘bolt on’ of

confidentiality clauses so as to avoid the disclosure of private and confidential matters in a public forum such as the courts.

10 Keep it simple: include calculations and make them easily measurable and referable to common assessable data, and use

illustrative calculations to aid in the interpretation should a disagreement occur.

BROKERNEWS.COM.AU | 23

FEATURE / CONSOLIDATION

BROKERNEWS.COM.AU | 23 BROKERNEWS.COM.AU | 23

HEAD TO HEAD / JAMIE MCPHEE

24 | MPAMAGAZINE.COM.AU

TAKING ON THE BIG FOUR

MPAMAGAZINE.COM.AU | 25

MPA: What are the biggest challenges that the mortgage industry faces at the moment?Jamie McPhee: The major banks have 83% of mortgage share. Such a large concentration of the mortgage industry with major banks means that competition is reduced, and a lack of competition over the longer term is never a positive outcome for customers. Pleasingly, however, non-major banks like ME Bank are starting to generate greater awareness of their highly competitive offers with customers and there are signs customers are starting to take notice and are starting to make the switch.

MPA: Are there any areas of the country, or sectors of the market (eg, first homebuyers), that

Sixteen months sinceME Bank embraced thebroker channel, its CEOJamie McPhee tells MPAwhy he believes that it’smore important than everfor brokers to educatecustomers about non-majoralternatives and help breakthe big four dominance

are experiencing strong demand for mortgages at the moment?JM: If anything, first homebuyers as a sector might actually be going backwards due to changes to the incentives provided by some state governments. Interestingly, ME Bank continues to see relatively strong demand for its first home savers account, with demand increasing by 85% during the last financial year. Customers respond when banks step in to help people buy a first home. We have also noticed an increase in fixed rate activity in recent months, based largely on the low fixed rates currently being offered. ME Bank is experiencing above-system demand for fixed rates – over 20% of total new home loans.

MPA: How do you think the current environment of falling interest rates will affect the mortgage market over the coming year?JM: Over time, falling interest rates will drive a greater demand for residential property. The other key driver is consumer confidence rebounding, which will be driven by people feeling more confident about job security. In addition, lower rates improve the affordability for first homebuyers. It’s worth noting that as the RBA cuts interest rates, deposit rates also fall, including term deposits. While some banks like ME Bank continue to offer term deposit rates at a position well above the cash rate – much higher than they are traditionally priced – some investors may start to look towards investment properties, giving a further boost to the housing market. We are starting to see a modest rise in house prices which is a positive sign of recovery, and is likely to stimulate further market growth into the future.

HEAD TO HEAD / JAMIE MCPHEE

26 | MPAMAGAZINE.COM.AU

MPA: Are there any other trends that you expect to see in the mortgage market over 2013?JM: As non-majors like ME Bank continue to raise awareness of their better offerings across service, fees, rates and flexibility, we would hope to see a continued movement away from the big four and a steady increase in competition.

MPA: How do you rate ME Bank’s relationship with mortgage brokers, and can it be improved? JM: ME Bank made a very positive entrance into the mortgage broking market in November 2011. Within a year we’d established great working relationships with 11 aggregators, and more than 2,500 brokers are now accredited to sell ME Bank home loans. We have

“We would hope to see a continued movement away from the big four and a steady increase in competition” – JAMIE MCPHEE

received much positive feedback, particularly on ME Bank’s position in ensuring all our customers receive fairer treatment. Our brokers are also our customers and we take our commitment to them seriously. It’s why brokers are given equal access to our BDMs and credit teams. We will continue to work with brokers to understand the difference their clients will experience with ME Bank.

MPA: What is ME Bank’s key value proposition when it comes to the mortgage broker channel? JM: As mentioned, ME Bank is the genuinely fairer banking alternative and our promise to our customers is to provide straightforward, transparent and low cost products combined with great service. For brokers, this means equal access to BDMs and credit teams regardless of volumes, and to uniformly provide quick decision times. For example, we offer the same low rate even for smaller loans. Another example is we’ve offered a lower standard variable rate than the majors ever since we became a bank in 2001.

MPA: What will take for the mortgage market dominance of the big four banks to be eroded? JM: Educating customers that non-major banks like ME Bank are a genuine banking alternative. We hold the same level of security but provide a fairer banking experience. ME Bank believes that mortgage brokers play an important role in educating customers about banking alternatives like ME Bank. Their clients go to them as they are looking for a trusted adviser who has their best interests at heart, so we see the brokers we work with as very important to helping get the word out to Australians that they don’t need to put up with the major banks. There are much better options – a genuinely fairer banking option – and they should vote with their feet.

28 | MPAMAGAZINE.COM.AU

MOTIVATION / IMPOSSIBLE CLIENTS

Cindy Tonkin is the author of ‘The Australian Consultant’s Guide – setting up your consultancy business profitably and painlessly’ and ‘Consulting Mastery: being good is not enough’. She is Australia’s office politics expert. Find out more at politicalacumen.com.au

someone else to explain. This may work because the other person changes ‘channel’ (from words to pictures, as I just suggested). Or it could be their ‘convincer’.

06|They may have to meet it more than once

Research on convincers (how people decide) shows that we all need to hear, see, experience or read things a certain number of times or over a

Sometimes your client wants the impossible:they want to pay you less; they want everythingdelivered yesterday; they want to do a deal outsidethe ordinary… Here are some essential tips to helpyou out when your clients make impossible demands

01|Make sure you are clear Firstly, make sure you are

clear: It can’t be done that quickly, at that price, the deal isn’t within guidelines. Say it out loud. Not with a lukewarm ‘yes’, but a cold hard ‘no’.

02|Is it impossible or a new product?

And before we go any further, be certain that what they want really is impossible. All progress is indebted to the unreasonable person: what they want could in fact be your new product.

03|Write it down But if not, to be doubly clear,

write it down. If you have a procedure, make a client version of it, so they can read it in black and white: what’s possible and what’s not.

04|Try a different channel Next option: try changing

sensory channels. Some people believe things they see, others what they hear, what they read or what they experience. You’ve tried sound and the written word. So draw a diagram. Walk them through it.

05|Try a different person If that doesn’t work, get

period before we believe it is true – until we are convinced. Every person has a different channel and a different number. I had a client once who needed to hear something for three months to make a decision. She talked about working with me for three months before making the appointment. She followed up on my quote three months later. My dad’s different: he needs to experience something once before

Mission impossible9 tips for dealing with demanding clients

MPAMAGAZINE.COM.AU | 29

NEWS / ROUND-UP

deciding. He proposed to my mother on their first date. He bought houses he saw once. He took a holiday on the spur of the moment. So your client may just need to hear, see, read or experience why what they are asking is impossible a few more times to know it’s not possible. If your convincer is short, and your client’s convincer is long, then maybe it’s just about a little patience.

07|Last resort: refer them to a colleague

There is also the nuclear option: don’t provide to them. Refer their business to a colleague.

08|Check out your processes

Finally, if your clients consistently ask for the impossible, check how you are

“There is also the nuclear option: don’t provide to them. Refer their business to a colleague”

marketing to attract this kind of request. Look at your customer information, website, customer welcome packs, everything you give to clients. Make them so clear that you’ll cut out some of the impossibles. A chain of pharmacies found the most impossible customers were those waiting to pick up prescriptions. They created a poster showing the 26 steps that the pharmacist went through to ensure a prescription didn’t accidentally kill someone. Customer impossibility evaporated.

09|Look after yourself In the end, the more fit,

healthy and happy you are, the more easily you can convert impossible clients into happy, referring clients. So look after you!

MPAMAGAZINE.COM.AU| 31

SPECIAL REPORT / YOUNG GUNS

Meet the young talentthat’s taking the Australian mortgagebroking industry by storm

AUSTRALIA’S BROKING STARS OF THE FUTURE

With all the stories of doom and gloom that have engulfed the Australian

financial services and property markets in recent years, you’d be forgiven for wondering why bright young things would be drawn to a career in mortgage broking. Listen to the doomsayers and you’ll hear about mass redundancies in the finance sector and cautious homebuyers sitting on their hands waiting for the property bubble to burst.

It’s both inspiring and refreshing, therefore, to speak to the numerous ambitious young brokers who have made great

strides in their fledgling careers, and show no signs of turning back. This year’s MPA Young Guns report features a bright crop of promising new entrants to the industry who are attacking the profession with vigour.

So how did we select these young stars? Candidates had to be no older than 35, have been broking for no more than two years and can’t have featured in last year’s Young Guns report – only fresh faces need apply. Judging by the calibre of new brokers that feature in this year’s rundown, the future of mortgage broking looks to be very bright indeed.

YO NGGU S

SPECIAL REPORT / YOUNG GUNS

32 | MPAMAGAZINE.COM.AU

NAME: FAB MASTRO COMPANY: MORTGAGE CHOICE LOCATION: MELBOURNE, VIC

Twenty-seven-year-old Fab Mastro has taken an interesting route into the world of mortgage broking. Before becoming a loans consultant at Mortgage Choice in Melbourne, he worked in the sporting and recreational industry with the YMCA, as well as some other sporting organisations. Recently, however, he decided that it was time to seek pastures new and move out into fresh territory with his career, and it turned out that mortgage broking was the perfect fit. Evidence that moving into the mortgage space was the right move for Fab comes in the form of his impressive settlement figures. During

the 2012 calendar year he settled $37.5m of home loans. Not bad for a mortgage broking freshman.

“Getting into the industry was a combination of factors,” he explains. “Having the right contacts, getting involved in an opportunity that was going to provide the right support base – which I definitely have – always enjoying the interaction with clients and having a love of property. After buying my first property and going through the process, I saw an opportunity to become involved in a way that suited both my lifestyle and my hunger for career progression. I

now work the hours I want to, can operate from a remote location if need be and am building not just a loan book, but hopefully clients for life. This has proven extremely rewarding, and it’s something I hope to do into the future.”

When questioned about what he has learnt about broking so far, he notes that the single thing clients are crying out for is great service.

“Some brokers talk about it and don’t deliver; others don’t talk enough about how they do deliver. It is a fine line, but at the end of the day it’s only achieved by putting in the effort and having an amazing support team behind you. If a client becomes a ‘raving fan’ of the service you provide, this is what then builds your business.”

Career-wise Mastro would like to further entrench himself in the finance and property industries, and would ultimately like to be able to employ others. To continue learning is also another key goal. “I suppose the day I stop learning in this industry is the day I move on!” he says. “I’m always looking for ways to improve the way I operate and gather different ideas of doing things, whether it is by trying to better my skills, learning new information by attending industry events or PD days – or simply improving my management techniques.

“The industry is in an interesting period right now. With the change in credit legislation and the overall slowing of credit growth, some would expect brokers to either leave the industry or begin the transition away from it. I really see it as an opportunity to change the way brokers operate and offer a more comprehensive service, both in what we initially provide to the client and the ongoing contact we have with them throughout the journey. I certainly have some ideas around this, but that may be an idea for another time!”

Young Guns enriching our futureThe ideas and talent recognised in this year’s MPA Young Guns feature are the ones that will grow and enrich our industry into the future. They may even change the way you are doing business.

The MPA Young Guns feature highlights a select few of the industry’s most outstanding young mortgage brokers. They have been nominated by their Aggregator and have been acknowledged for their customer service, outstanding performance and business growth.

The future of our industry depends upon professional, young operators who are focused on building successful businesses by delivering excellent customer service. This feature highlights those who are doing it right and it shows they are all driven to help their customers to get the best home loan to suit their needs.

Commonwealth Bank is committed to the mortgage broking industry and encourages all brokers to be professional in every way; to adopt on-going education and ethical behaviour.

If you want to see the best of now – look to the winners at industry Awards such as the Australian Mortgage Awards and the MFAA Excellence Awards. If you want to see the best of tomorrow, look to this special on Young Guns in the industry.

The MPA Young Guns feature has been recognising young talent since 2010. If your name isn’t in here yet, don’t give up trying.Kathy CummingsExecutive General Manager, Third Party and Mobile Banking

SPECIAL REPORT / YOUNG GUNS

MPAMAGAZINE.COM.AU| 33

NAME: KARLI MARTIN COMPANY: MORTGAGE CHOICE LOCATION: BRISBANE, QLD

One of the youngest brokers in this year’s Young Guns, 22-year-old Karli Martin has made great strides in her short career in the world of mortgage broking. Starting out as an admin assistant at Mortgage Choice in inner North Brisbane in July 2011, Martin showed great potential from the get-go, and within six months was offered the opportunity to move into a loans consultant role – which she grabbed with both hands.

“After seeing the professionalism of the brokers around me, I immediately jumped at the offer,” she explains. “I completed all the required qualifications and began writing loans in February 2012.” She went on to settle $23.2m worth of loans last year, showing that she’s taken to the job like a fish to water.

In terms of short-term goals, Martin aims to advance her mortgage broking skills and continue to increase her volume of clients and applications, which will in turn see her settlement numbers increase. “In the long term, my goal is to continue working for Mortgage Choice in Brisbane and to make the most of any opportunities that may emerge,” she adds.

“I only see positive things for the industry. There has been consistent growth in our local franchise business. I envisage this to be replicated industry wide and I don’t anticipate any change. Lenders are more competitive than ever trying to gain market share, and this combined with the drive of clients to compare loans to save money, means brokers are the best solution to assist them.”

So what’s the secret to her successful entry into the mortgage broking market? Martin puts it all down to having great mentors. “I’m very fortunate to be in an office surrounded by successful mortgage brokers. The things that I have learnt from them are invaluable [such as] understanding that the customer is the most important aspect to being successful, as is building strong business relationships. I’m a very competitive person who is always aiming to improve and develop, professionally. I believe this determination is important in any successful broker.”

NAME: CALLUM KERR COMPANY: AUSSIE LOCATION: GREENSBOROUGH, VIC

Thirty-five-year-old Callum Kerr originally started out in real estate, but the close ties with mortgage brokers that he forged while working in the UK saw him move into the broking field back in Australia.

“I was an estate agent in the UK for four years, as well as two years in Australia. In the UK we had a mortgage broker working in the office, and our sales targets were actually aligned to how many referrals go to the mortgage broker. So we needed to have a fairly good understanding of mortgages, how they worked and how much people could borrow. So that interested me.”

His mother is also a finance professional, having worked in banking all her life. She owns half of an Aussie franchise, and Kerr decided to move into the family business.

When asked whether the kind of in-house referral arrangement that he experienced between brokers and real estate agents in the UK would work in Australia, he noted that this may not work for all customers.

“We’ve got a lot of key referral partners, and a lot of them are estate agents. The difference here is when they’re working in the office it’s almost too in-house. [Client’s may think] ‘I don’t want the estate agent knowing how much I can borrow’,” he says.

“With the people we deal with in the first conversation we say we’re completely independent to these guys. ‘Whatever you say to me is 100% confidential’.”

Kerr echoes the sentiments of many of our Young Guns in stating that success is all about service: “You’re selling the person, not the product. For example, my real estate background helps me immensely. A lot of people don’t know how to make an offer, and I give them a bit of help with that as well.” All of which helped him to settle $35.8m in the past 12 months.

34 | MPAMAGAZINE.COM.AU

NAME: MATTHEW FORD COMPANY: FINESTREAM GROUP LOCATION: UNLEY, SA

Finestream Group managing director Matthew Ford may only be 23 years old, but he already has a fine head for business. And in the case of his team at Finestream Group, business is all about concentrating on what they do well – and marketing themselves in that area.

“We have always predominately been focused in the asset finance field, specialising in motor vehicles and plant and equipment finance,” he explains. “Increasing demand from our customers has led to the recent formation of a mortgage broking service. However, to avoid taking on more work than I could handle, and potentially jeopardising our existing level of service or reputation, I sought out and employed the best candidates I could find to manage the home loan business; young, mostly ex-bank workers with a strong motivation to carve out their own section of the industry, and enthusiasm and knowledge to provide the highest level of customer service.”

Referrals, too, are central to Ford’s ethos, and he has built up a solid network of referral partners. He also encourages his team

NAME: JOSH GILBERT COMPANY: LOAN MARKET LOCATION: ST KILDA, VIC

Twenty-nine-year-old Josh Gilbert exemplifies the work ethic demonstrated by our Young Guns. When asked what he’s learnt about becoming a successful mortgage broker in his short career, his answer is simple: “You are ultimately rewarded for how hard you work.”

“I think to be a successful broker you have to be good at building rapport with your clients and have good time management,” he adds, “[as well as] a desire to continually learn and most of all the motivation to drive your business.”

It’s this independent entrepreneurial streak, and a desire to meet the customer’s

needs, that drove Josh to move out of the confines of being a credit union lending consultant and into the broking space.

“I have seen first hand how restrictive working with one financial institution with a strict lending policy can be. It was frustrating declining customer applications back at my old job when I knew they could obtain finance at a bank just around the corner. I wanted to be that person that could offer solutions and not turn people away,” he explains.

“I want to continually develop my knowledge and skills of lending into more forms of complex lending solutions, eventually building a team around me that will allow me to focus more on seeking out new business as well as continually maintaining my existing database.”

He sees a bright future for the mortgage broking profession, where clients trust their brokers enough to ask them to recommend anything from financial planners and accountants to builders and buyer’s agents.

“This client mentality of not only seeing the mortgage broker for borrowing solutions but also as their one-stop shop for other services closely related to their industry can be attributed to two things,” he says.

“Since the legislation ban on exit fees, competition within the industry has grown. This on the basis of stronger industry body requirements (diploma) as well as ASIC continual overview of the NCCP Act. This will

ensure brokers are suitably qualified and help build credibility of brokers.

“With the continual increase in competing for leads growing over time, brokers are building strong relationships with as many closely associated industry partners as possible. This presents much needed cross-sell opportunities. All of whom can provide valuable services for our clients.”

These grand visions are all certainly a far cry from his post-high school vocation – shovelling rocks and sand in the scorching summer heat all day as a labourer.

SPECIAL REPORT / YOUNG GUNS

“It wasn’t that long ago that I didn’t even know what a broker was. I did know, however, that I didn’t want to be an accountant”– MATTHEW FORD, FINESTREAM GROUP

to actively ask clients for referrals, which means service has to be top-notch.

“We want them to walk away wanting to use us again, and to encourage their friends and family to do the same,” he says. “Being based in Adelaide, reputation is everything. Everybody knows everybody and you only get one shot to prove yourself to your clients and potential referral partners. We have worked very hard to build up our reputation in the field of asset and equipment finance in Adelaide. How you are perceived by the market is very important; we constantly work towards being known as the best in our field.”

Ford took a big risk in entering the mortgage broking market, as that meant ditching his job with a big four accounting firm, but a personal experience persuaded him to make the move. He knew he wanted to work with money and went into accounting to gain exposure to a cross section of different businesses before deciding on his next move.

“I did not enjoy it at all,” he explains. “Joining the firm was one of the best things that I will ever do because it taught me very quickly (and thank God right at the beginning of my career) what I did not like. I knew that I didn’t want to be an accountant, I knew that I didn’t want to be a very small wheel in a very large machine, and I knew that I didn’t want a desk job tucked away from the world referring to clients as surnames only rather than ever actually meeting them in person.” But a chance encounter would change all that.

“While working for a large accounting firm I purchased a house with the help of a mortgage broker who was referred to me by my real estate agent at the time. With a common interest in cars and business, we became friends and not long after that I quit the accounting firm and started working as a trainee mortgage broker in his company. After completion of my studies I was presented with the opportunity to purchase the business in its entirety. At this stage it was a small book of mortgage and asset finance clients based predominately in Adelaide,” he says.

“It wasn’t that long ago that I didn’t even know what a mortgage broker was. I did know, however, that I didn’t want to be an accountant – the career path that I had so promptly chosen out of high school. I always knew that I wanted to have my own business. I remember when I was about 12 or 13 I would think up elaborate business ideas complete with business names, and business plans, and present them to my father who to this day is my greatest business mentor.”

Having set about establishing Finestream’s

reputation, Ford took client feedback on board and decided to do things differently. Complaints about the duplication of paperwork that was required when dealing with various different finance professionals led him to test the one-stop-shop idea – incorporating broking, accounting, business advice and financial planning under one roof.

“The response I received was astronomical, with clients explaining how much easier this would make dealing with the financial requirements of life. Through this, Finestream Group was formed,” he says. “With each business unit supporting the next, and all the while focused on a framework of exceptional customer service, the business has grown organically and exponentially. We have beaten a down market by adjusting our business to be so dynamic that every Australian is now a potential client.”

MPAMAGAZINE.COM.AU| 35

NAME: BRUCE PODGERCOMPANY: AUSSIELOCATION: SOMERVILLE, VIC

Thirty-year-old Bruce Podger has been in the mortgage broking game since August 2011, and has got off to a flying start – settling $24m in loans in his first year. His was an unconventional route into the industry, having previously run his own café business, but the lure of flexible hours and being able to help people achieve their home ownership goals led him to take up a mortgage broking role with Aussie.

When asked about his career goals, Bruce is ambitious and to the point: “To have a loan

38 | MPAMAGAZINE.COM.AU

NAME: JUSTIN VELLA COMPANY: BERKELEY CAPITAL PARTNERS LOCATION: MELBOURNE, VIC

Twenty-five-year-old Justin Vella has some phenomenal figures to back up his claim to being one of Australia’s Young Guns. Over the past 12 months he has settled approximately $65.5m in loans – $59.5m in the commercial sector, and $6m in

residential transactions. He’s one of a new breed of mortgage broker who has entered the industry straight from university with a finance qualification (Bachelor of Business, Banking and Finance) already under his belt. In fact, Vella couldn’t even wait for graduation to get his foot in the door, joining Berkeley Capital Partners’ Work Integrated Learning program while still an undergraduate.

“The position was part-time and it gave me an opportunity to understand and get a feel for the industry first-hand while allowing me to complete my degree,” he explains. “Upon completion, I worked towards the necessary minimum requirements to become accredited. I have been trained via an accelerated training program under principal Brett Hartwig,

supported by my other colleagues, in both the commercial and residential sectors.”

He has since worked on a wide range of transactions, including residential and commercial property purchases and developments, cash-flow lending, trade finance, foreign exchange, equipment finance and refinances varying in complexity and size.

“Berkeley Capital Partners has provided me with the opportunity and exposure to complex commercial and property transactions allowing me to develop my skills and excel in the industry. As debt arrangers and advisors, with $500m-plus under management, I always felt Berkeley Capital Partners would give me great exposure to the finance industry. Our client base is broad and has a variety of high net worth corporate, commercial and small business relationships held within various industries,” he says.

NAME: ASHLEIGH WIGHT COMPANY: DIVERSIFI LOCATION: NORTH PERTH, WA

Diversifi’s Ashleigh Wight attained her Australian Credit Licence and became an MFAA broker at the age of 23, and within four months had already found herself in fourth place on Choice Aggregation Services’ monthly list of mortgage brokers who had attained the highest number of individual loan approvals.

“I then jumped to second position in WA the following month and simultaneously was awarded a Bronze Award for settling over $2m of loans. December 2012 saw another monumental month, with me settling over $4m of loans,” she says. “My milestone months of September and October 2012 also saw Diversifi achieve record numbers of group loan approvals, totalling over $36m.”

All up, eight months down the line, Wight had $14m of unconditionally approved loans to her name, and settlements that were just shy of the $10.3m mark. At the same time, she was announced as one of the five finalists in Australia for the MFAA’s Achievement Award for brokers who have less than four years’ experience in the mortgage

book of $100m by the end of my third year as a broker”. That gives him until August 2014 to hit his target.

In terms of the profession’s future, Bruce is optimistic that meeting the needs of busy customers will continue to be the mortgage broker’s domain. “I see the industry growing as competition in the market grows. Customers are getting busier and busier in the world these days. Having a broker one-stop shop makes the time involved in researching different home loans a lot simpler and easier for customers,” he says. “Being a successful broker in my opinion is about customer service. If you look after your customers they will refer you to others.”

MPAMAGAZINE.COM.AU| 39

SPECIAL REPORT / YOUNG GUNS

industry. Still just 24 years old, her enthusiasm is palpable.

“The honour in being named a finalist is truly a feeling that has been indescribable! I love what I do, but there has been a lot of hard work involved, with wonderful support from my principals, so I can honestly say that this accolade is a true testament of my commitment to a successful career. For Diversifi, me being named a finalist has instilled their belief there is a place for me to contribute to the industry and represent our brand in a reputable light,” says Wight.

When it comes to maintaining her reputation, Wight believes that service, patience and understanding are key.

“Clients want a broker who has patience and is willing to hold their hand through the loan process. This makes the world of difference between an exceptional experience with a mortgage broker and a below average experience. Returning phone calls and emails within two hours goes a long way when clients recall the service they received from you,” she says.

In terms of her future goals, Wight plans to establish her own Diversifi franchise within the next four to five years. And with her “love what you do, and you’ll never have to work another day in your life” philosophy, she has every chance of achieving that goal.

In the future she sees technology and internet continuing to evolve, and customers becoming more and more educated on financial alternatives and loan products – as well as realising the importance of using a mortgage broker for gaining unbiased advice.

“With access to lender comparisons, clients can make a more informed decision when choosing which lender to proceed with. With the support of the MFAA, the mortgage industry has seen rapid growth and has become a force to be reckoned with, as more and more consumers are using mortgage brokers, instead of approaching the banks direct,” she says.

NAME: CATALINA MILLA COMPANY: LOAN MARKET LOCATION: MELBOURNE, VIC

Thirty-three-year-old Loan Market broker Catalina Milla regularly settles $2.5m per month, making her a solid performer in the Melbourne market.

She picked up the idea of taking on broking herself through her work as office manager and PA to a broker. This is where she cut her teeth learning to structure and prepare loans “as well as how to problem solve and work together with the lenders to achieve results”.

While she has few complaints about her pre-broking career, which provided ample opportunity for teamwork and on-the-job education, there was something missing in Catalina’s eyes.

“The ability to evolve and expand in my career was limited,” she explains. “I had worked very hard for years and found when I became a parent I would have to change careers or begin within another industry. Becoming a mortgage broker allowed me to become mobile and work wherever I am – and take control of my business growth and potential through the amount of effort and hard work I am able to put in.”

Judging from her ethos of keeping in touch with clients regularly, and “knocking their socks off with service”, the amount of effort and hard work she’s able to put in is considerable. “Always place yourself in your client’s position and then structure their loan accordingly,” she says. “There is less need for maintenance in the long run, and it personalises your service to them by really trying to understand how your client wants their loan to function.”

In line with many of our Young Guns, Catalina sees the mortgage industry becoming more regulated in future, but views this as an opportunity for brokers to carve out a niche market in providing the unique capability to offer comparative solutions to clients “rather than limiting the clients’ options to only one lender’s products”.

And in this future she sees herself expanding her business to create a team of loan writers that can provide exceptional service “and an avenue for specialised lending and solution-based lending”.

“Clients want a broker who has patience and is willing to hold their hand through the process” - ASHLEIGH WIGHT, DIVERSIFI

40 | MPAMAGAZINE.COM.AU

NAME: HAYDEN DEMPSEY COMPANY: PREMIUM PORTFOLIO FINANCE LOCATION: PERTH, WA

Twenty-nine-year-old Hayden Dempsey may be new to the broking industry, but in his short time as a broker he has already become the owner of his own practice – Premium Portfolio Finance (PPF). He began his formal training as an accountant and cultivated his talent for sales through roles at the Police and Nurses Credit Society and then as a banker at NAB. At NAB, Dempsey was selected to be part of the National Mobile Bankers Advisory Board and, on average, wrote $50m per year – exceeding $20m in some quarters. He was recognised as one of the top 10 mobile bankers for NAB in Australia.

“The structure of your week is pre-booked due to the high level of demand. Targets are set from $35m up to $55m per year, depending on how long you have been working for the organisation. The considerable workload makes it increasingly difficult to build rapport as your focus has to be on the new mortgage clients only, and there is a fragile balance between service and productivity. That balance makes it difficult to maintain ongoing satisfaction within the role,” he explains, adding that the high-pressure environment also had its plusses.

“The best experiences were the

NAME: MATTHEW EGAN COMPANY: MULCAHY & CO LOCATION: BALLARAT, VIC

Twenty-eight-year-old Matthew Egan is going great guns for one so new to the mortgage broking industry. He already settles approximately $3.25m-worth of loans each month, which equates to annual settlement figures of just under $40m. He puts his success down to forming strong relationships with clients from a range of different backgrounds and

professions – which helps to diversify his client base.“These include residential, commercial business

owners, investors, self-employed, self-managed super fund lending, and farming primary producers,” he explains. “The diverse nature of my client base means my referrals will come from more than one source, which is vital to my success as a broker.”

He moved into broking to seek a new challenge and step out of his comfort zone. He was working as a lending manager for one of the majors at the time, but decided that he needed to move on to progress his career.

“Taking the biggest risk in my life and leaving my secure surroundings has been the best decision I have ever made in order to progress my career, knowledge and client network,” he says. “My career goals are to maintain strong trustworthy relationships with my clients, which will ultimately lead to longevity in an industry that can be difficult to succeed in.”

As well as getting the basics right – maintaining your level of training and product knowledge and having honest conversations with your clients to earn their trust – always being prepared to challenge yourself is a quality that Egan sees as vital to success.