mortgage insurance product shf’s white paper december 2006

TRANSCRIPT

Mortgage Insurance ProductSHF’s White Paper

December 2006

CONTENTS

2

I. PORTFOLIO

II. LOAN ORIGINATION

III. LOAN BEHAVIOR

IV. PREPAYMENT

V. BEHAVIOR SCORE

INTRODUCTION

3

• This document as intended to provided consolidated information on SHF´s guaranteed portfolio, and is aimed to any analysts interested in learning the main characteristics of the mortgage pool insured by SHF

• It contains portfolio and prepayment information as of December of 2006 and behavior information as of November of 2006

• The final chapter of this document has a more thorough description and analysis of the behavior score used in SHF to measure portfolio credit quality

SHF not – Securitized Portfolio vs Securitized Portfolio

4

Not securitized Number of

Loans% Number of

LoansLoans

Balance% Loans Balance

UDISProfivi 193,918 80.65% 62,815 85.95%Prosavi 27,817 11.57% 2,688 3.68%

PESOSProfivi 18,722 7.79% 7,580 10.37%Total 240,457 73,084

Guaranteed PortfolioPortfolio Statistics

Not securitized

Number of Loans % Number of LoansLoans

Balance% Loans Balance

UDISProfivi 36,752 97.12% 22,793 98.79%Prosavi 266 0.70% 20 0.08%

PESOSProfivi 823 2.17% 260 1.13%Total 37,841 23,072

Portfolio Statistics

Securitized Loans

PORTFOLIO: Loan Characteristics

5

Securitizated Not securitized

Total 1.82 1.84Profivi 1.82 1.9

Prosavi 1.7 1.39

Total 144.04 86.24Profivi 144.58 88.79

Prosavi 68.06 68.35

Total 0.85 0.81Profivi 0.85 0.84

Prosavi 0.48 0.58

Total 285,699 285,108Profivi 287,230 313,134

Prosavi 69,692 88,982

Total 26.31 25.85Profivi 26.28 25.62

Prosavi 30 27.37

Average Loan Spread

Average Years to Maturity of Loan at Origination **

Average Administration Fee *

Average Loan to Value at Origination

Average Initial Loan *

* In pesos** Months

Portfolio Concentration By Region

6

Securitized Loans

Guaranteed Portfolio

Nuevo León 11.60% 18.42 480.73 FormalJalisco 10.65% 20.28 480.78 Formal

Baja California 10.51% 24.46 480.65 FormalMéxico 8.15% 21.92 483.85 Formal

Quintana Roo 6.53% 21.93 477.09 FormalTamaulipas 5.20% 24.02 480.04 FormalChihuahua 4.81% 24.93 484.16 Formal

Sonora 4.48% 22.57 482.98 FormalSinaloa 4.01% 21.77 482.77 Formal

21.82 481.27 Formal

Employment

Guaranteed Portfolio Concentration

State % Concentration Mean Age Mean Score

Sector

Baja California 15.62% 51 466.49 FormalMéxico 14.13% 49.71 468.44 Formal

Distrito Federal 11.10% 54.51 467.17 FormalJalisco 9.00% 47.62 468.57 Formal

Nuevo León 8.54% 46.99 468.01 FormalQuintana Roo 6.42% 48.38 466.23 Formal

Chihuahua 5.40% 52.75 468.87 FormalTamaulipas 4.26% 48.54 466.68 Formal

Puebla 4.25% 48.99 469 Formal45.13 468.19 Formal

EmploymentState % Concentration Mean Age Mean Score

Sector

Securizated Portfolio Concentration

Not Securitized Portfolio

CONTENTS

7

I. PORTFOLIO

II. LOAN ORIGINATION

III. LOAN BEHAVIOR

IV. PREPAYMENT

V. BEHAVIOR SCORE

Portfolio Distribution By Activity of the Individual

8

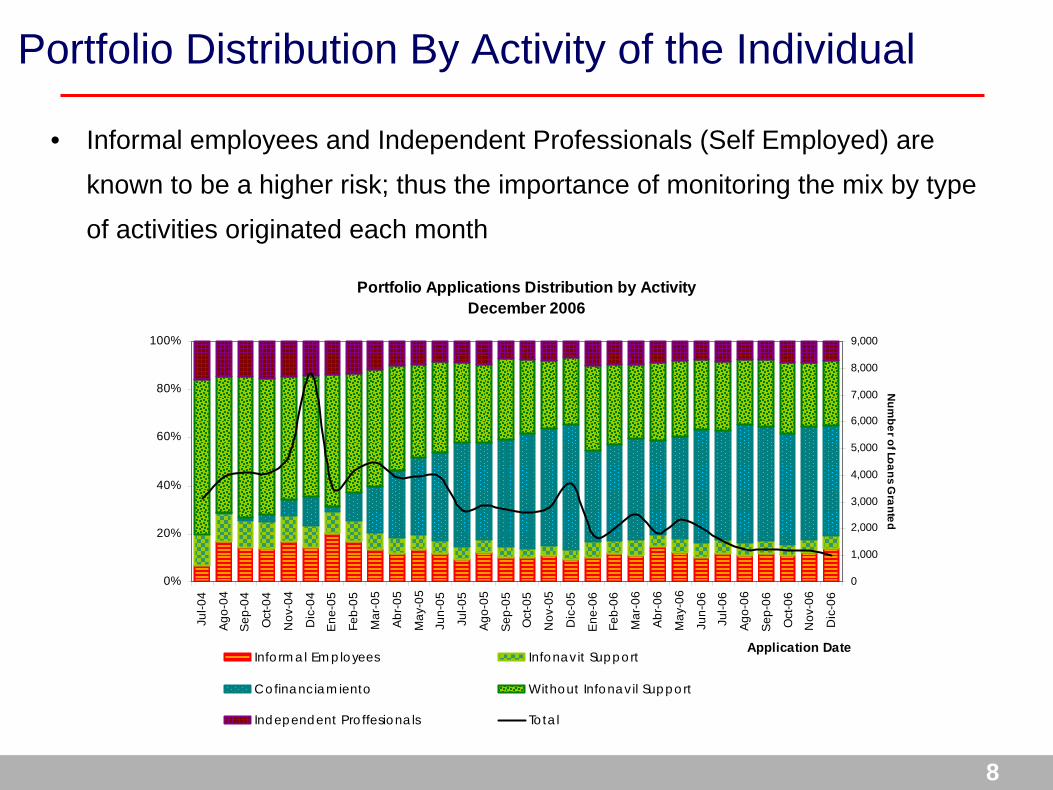

• Informal employees and Independent Professionals (Self Employed) are

known to be a higher risk; thus the importance of monitoring the mix by type

of activities originated each month

Portfolio Applications Distribution by ActivityDecember 2006

0%

20%

40%

60%

80%

100%

Jul-0

4

Ago

-04

Sep

-04

Oct

-04

Nov

-04

Dic

-04

Ene

-05

Feb-

05

Mar

-05

Abr

-05

May

-05

Jun-

05

Jul-0

5

Ago

-05

Sep

-05

Oct

-05

Nov

-05

Dic

-05

Ene

-06

Feb-

06

Mar

-06

Abr

-06

May

-06

Jun-

06

Jul-0

6

Ago

-06

Sep

-06

Oct

-06

Nov

-06

Dic

-06

Application Date

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Num

ber of Loans Granted

Informal Employees Infonavit Support

Cofinanciamiento Without Infonavil Support

Independent Proffesionals Total

Credit Score Distribution

9

I

Application Score Distribution December 2006

459 480 500 520

0

1,000

2,000

3,000

4,000

5,000

424

431

436

441

446

451

456

461

466

471

476

481

486

491

496

501

506

511

516

521

Application Score

• At December 2006 most of the

guaranteed loans by SHF had

credit score between 459 and

500 points (the odds of having

bad behavior doubles every

20 points)

• Some guarantees were

originated with a credit score

below cut-off point (459), and

this is due to some

alternatives the individual has

in order to remediate a low

credit score (for example:

entering into a savings

program, lowering the LTV )

Application Distribution by Bucket Score

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

- 458 459 - 480 481 - 500 501 - 520 521 - +

Bucket Scorre

Loans below cutoff point and guaranteed

10

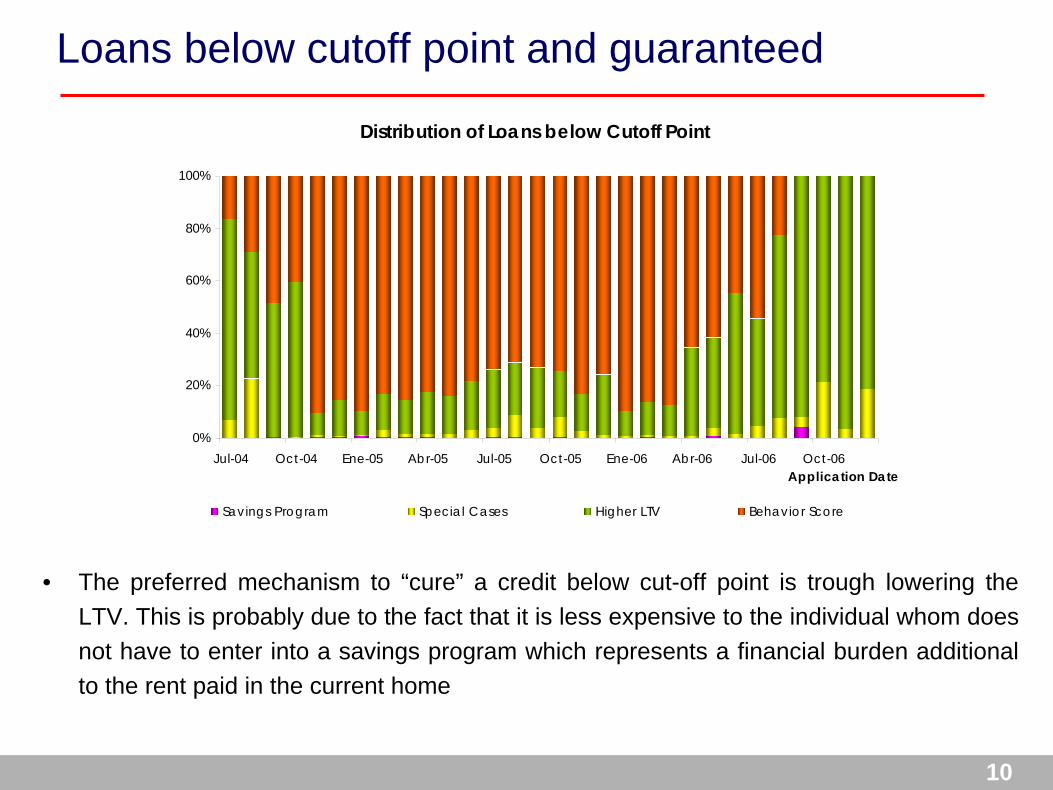

Distribution of Loans below Cutoff Point

0%

20%

40%

60%

80%

100%

Jul-04 Oct-04 Ene-05 Abr-05 Jul-05 Oct-05 Ene-06 Abr-06 Jul-06 Oct-06Application Date

Savings Program Special Cases Higher LTV Behavior Score

• The preferred mechanism to “cure” a credit below cut-off point is trough lowering the LTV. This is probably due to the fact that it is less expensive to the individual whom does not have to enter into a savings program which represents a financial burden additional to the rent paid in the current home

CONTENTS

11

I. PORTFOLIO

II. LOAN ORIGINATION

III. LOAN BEHAVIOR

IV. PREPAYMENT

V. BEHAVIOR SCORE

Portfolio Distribution by Number of Months Past Due

12

• The distribution of number of months past due is stabilizing as the age of the portfolio also becomes stable

Months Past Due June 06 July 06 August 06 September 06 October 06 November 06

0 73.04% 73.50% 74.28% 72.73% 64.09% 76.58%1 15.05% 14.61% 13.89% 14.63% 21.39% 9.41%2 4.49% 4.14% 3.82% 4.42% 5.81% 5.20%3 3.97% 4.18% 4.30% 4.23% 4.54% 4.49%4 0.50% 0.54% 0.54% 0.63% 0.64% 0.70%5 0.24% 0.27% 0.27% 0.35% 0.40% 0.34%

6+ 2.71% 2.76% 2.89% 3.01% 3.13% 3.27%

Transition Matrix of Current and Past Due Loans

13

• The Portfolio Transition Matrix has a tendency to maintain loans in the 0-3 months past due zone; however it is complicated for loans that reach 6+ payments due to recover in the short term

• The following is a monthly transition averaged form the 10th observed monthly transition matrices of 2006 (up to the Oct-Nov Transition)

K 0 1 2 3 4 5 6 +0 91.42 8.29 0.25 0.03 0.01 0.00 0.011 35.41 51.09 12.96 0.49 0.02 0.01 0.022 12.50 18.05 43.92 24.65 0.73 0.04 0.113 5.41 4.11 9.48 71.10 8.96 0.68 0.254 4.44 2.69 6.54 13.06 32.84 36.99 3.445 3.95 1.40 1.43 6.43 5.01 19.92 61.87

6 + 1.45 0.32 0.28 0.95 0.35 0.49 96.16

Transition Matrix of Current and Past Due Loansk + 1

Jan - Nov2006

Probability of Default – Analysis by vintages

14

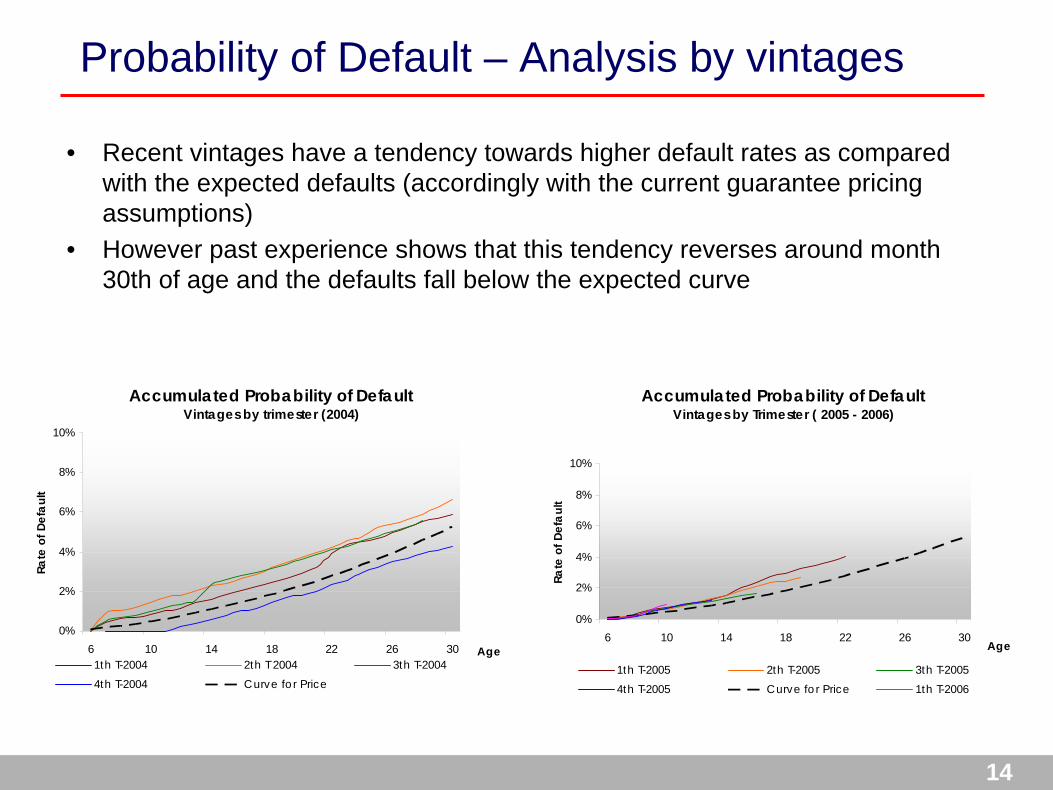

• Recent vintages have a tendency towards higher default rates as compared with the expected defaults (accordingly with the current guarantee pricing assumptions)

• However past experience shows that this tendency reverses around month 30th of age and the defaults fall below the expected curve

Accumulated Probability of DefaultVintages by trimester (2004)

0%

2%

4%

6%

8%

10%

6 10 14 18 22 26 30 Age

Rate

of D

efau

lt

1th T-2004 2th T 2004 3th T-20044th T-2004 Curve for Price

Accumulated Probability of DefaultVintages by Trimester ( 2005 - 2006)

0%

2%

4%

6%

8%

10%

6 10 14 18 22 26 30Age

Rate

of D

efau

lt

1th T-2005 2th T-2005 3th T-20054th T-2005 Curve for Price 1th T-2006

CONTENTS

15

I. PORTFOLIO

II. LOAN ORIGINATION

III. LOAN BEHAVIOR

IV. PREPAYMENT

V. BEHAVIOR SCORE

PREPAYMENT: General Statistics (UDIs)

16

The prepayment pattern tends to stabilize after month 30.

The spikes at the earlier vintages tend to be smoothed as further data pointsare registered.

GLOBAL PREPAYMENT RATE( UDI -DENOMINATED LOANS)

(08/1999 - 11/2006)

0.00%

0.15%

0.30%

0.45%

0.60%

0.75%

1 6 11 16 21 26 31 36 41 46 51 56 61 66 71 76 81 86

Age (Months)

Prep

aym

ent R

ate

CURTAILMENT PREPAYMENT RATE CPR = 2.37%

TOTAL PREPAYMENT RATE CPR = 4.46%

GLOBAL PREPAYMENTE RATE CPR = 6.71%

PREPAYMENT: General Statistics (PESOS)

17

The prepayment pattern tends to stabilize after month 30.

The spikes at the earlier vintages tend to be smoothed as further data pointsare registered.

GLOBAL PREPAYMENT RATE(PESOS- DENOMINATE LOANS)

(08/1999 - 11/2006)

0.00%

0.30%

0.60%

0.90%

1.20%

1.50%

1.80%

1 4 7 10 13 16 19 22 25 28 31 34 37

Age (Months)

Prep

aym

ent R

ate

CURTAILMENT PREPAYMENT RATE CPR = 2.36%

TOTAL PREPAYMENT RATE CPR = 3.87%

GLOBAL PREPAYMENT RATE CPR = 6.40%

CONTENTS

18

I. PORTFOLIO

II. LOAN ORIGINATION

III. LOAN BEHAVIOR

IV. PREPAYMENT

V. BEHAVIOR SCORE

Definition of the Behavior Score

19

• The Behavior Score is developed to evaluate the risk of debtors based in

their past behavior.

• The past experience is organized into a form which is amenable to

analysis. The most significant factors or variables which predict

behaviour are then determined.

• A numerical measure (an odds quote) is then developed (based on the

relevant factors) which allows a new applicant to be identified as a good

or poor risk

“Odds” Concepts and definitions

20

Once a score is calculated, it can be converted to odds. Odds represent the number of loans that will remain good for each account that will become bad. The odds - score relationship for these scorecards can be represented mathematically as follows:

ODDS = 20 x 2((SCORE - 500)/20)

For the sample account above, the odds would be calculated as shown:

ODDS = 20 x 2((480- 500)/20)

Therefore, ODDS = 10.

This means that for every 11 accounts that have a score of 480, we expect, based on past observation, that 10 accounts will perform satisfactorily for each account performing unsatisfactorily in the 12 months subsequent to scoring.

Description of Data

21

• The analysis of Behavior Score presented in this chapter is based on SHF’s warranty portfolio.

• The period of time considered goes form Jan-05 up to Oct-06, on a monthly frequency.

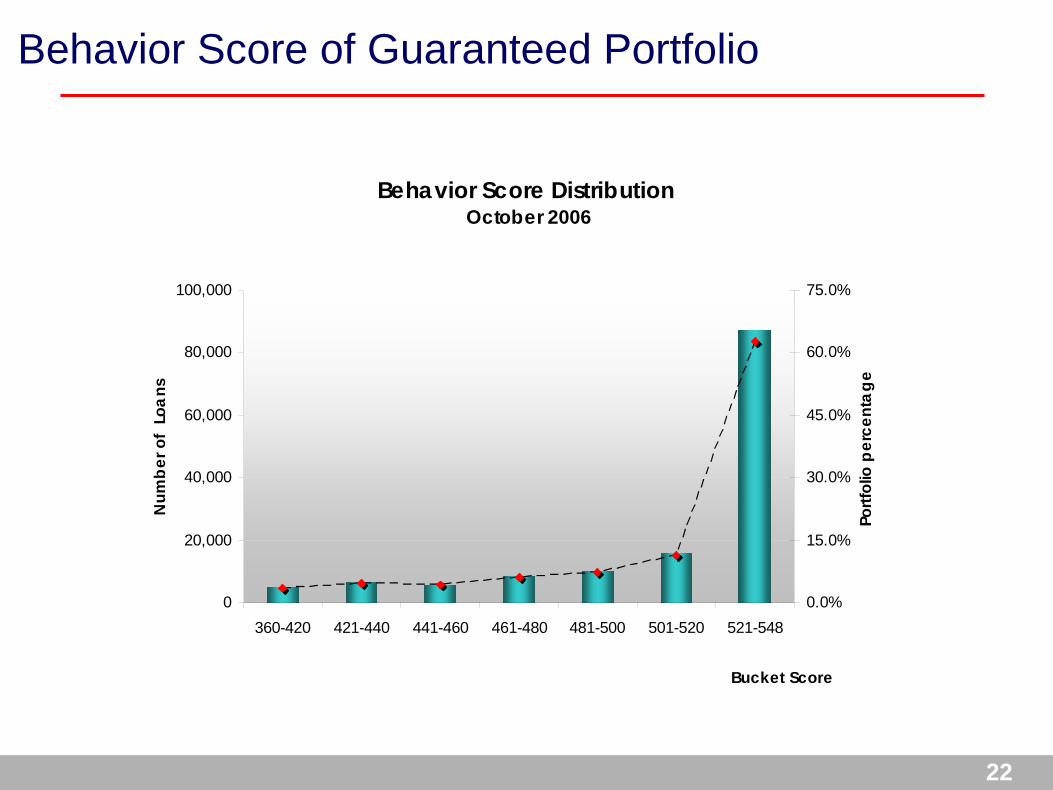

• The principal features of SHF’s Behavior Score are:Score Range between 360 and 548 (higher score, higher quality). The cut-off point was set equal to 503.Six months of data are needed to score a loanOnly applies to loans with less than four past due payments and at least six months of age.Odds double every 20 points

Behavior Score of Guaranteed Portfolio

22

Behavior Score Distribution October 2006

0

20,000

40,000

60,000

80,000

100,000

360-420 421-440 441-460 461-480 481-500 501-520 521-548

Bucket Score

Num

ber o

f Lo

ans

0.0%

15.0%

30.0%

45.0%

60.0%

75.0%

Portf

olio

per

cent

age

23

Behavior Score Transition Matrix: October 2006 –October 2005

• The Transition Matrix was constructed as an average of the monthly changes of loans along the score tranches.

• As expected, the main diagonal concentrates the maximum probability of transition, and the upper triangle of the matrix also shows large probabilities.

• These characteristics of the Behavior Score Transition Matrix imply a guaranteed portfolio with considerable stability along time, and a relatively good perspective to migrate to higher score tranches.

AverageTransition Matrix (%)Tranches of Score

360-400 401-420 421-440 441-460 461-480 481-500 501-520 521-548 Total

360-400 50.2 31.9 11.2 4.8 1.4 0.4 0.0 0.0 100401-420 7.5 40.6 28.3 14.1 6.3 3.0 0.2 0.0 100421-440 6.5 19.0 40.9 16.7 11.2 4.1 1.5 0.0 100441-460 1.9 8.3 13.8 34.0 23.8 12.2 5.7 0.5 100461-480 0.7 3.8 6.6 16.2 45.9 18.6 7.4 0.9 100481-500 0.0 0.3 1.0 3.5 20.5 45.6 22.6 6.3 100501-520 0.0 0.0 0.1 0.5 2.4 13.8 55.1 28.0 100521-548 0.0 0.0 0.0 0.0 0.0 0.4 7.9 91.6 100

Trach

es o

f Sco

re

Average Behavior Score by Loan to Value: Monthly

24

Behavior Score Evolution by Loan to Value

485

490

495

500

505

510

515

520

525

530

Jan-05

Mar-05

May-05

Jul-0

5

Sep-05

Nov-05

Jan-06

Mar-06

May-06

Jul-0

6

Sep-06

Month

Ave

rage

Sco

re

0-70% 70-85% 85-90% 90-100% Cut-off Point

• For LTV higher than 85%, the Behavior score is low, indeed below the cut-off point, because of the considerable risk of a loan with this feature.

25

Average Behavior Score by Loan to Value: October 2006

Average Behavior Score by Loan to Value October 06

400

420

440

460

480

500

520

540

560

0-70% 70-85% 85-90% 90-100%LTV

Ave

rage

Sco

re

0

10,000

20,000

30,000

40,000

50,000

60,000

Num

ber o

f Loa

ns

Mean Number of Loans

• Along the LTV tranches, the average behavior score remains relatively stable, although, the dispersion rises for the tranches of LTV higher than 85%.

Average Behavior Score by Creditor Activity: Monthly

26

Behavior Score Evolution by Activity

480

485

490

495

500

505

510

515

520

525

Jan-05

Mar-05

May-05

Jul-0

5Se

p-05Nov-0

5

Jan-06

Mar-06

May-06

Jul-0

6Se

p-06 Month

Ave

rage

Sco

re

Formal InformalInd. Professional Cut-off Point

• The Formal Sector, as debtor activity, has higher levels of Average Behavior Score.

• Clearly, debtors with formal jobs could face their liabilities in a better way than debtors with a non-formal job.

27

Average Behavior Score by Debtor Activity: October 2006

Behavior Score Evolution by Activity October 06

400

420

440

460

480

500

520

540

560

Formal Informal Ind. Professional

Activity

Ave

rage

Sco

re

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Num

ber o

f Loa

ns

Mean Number of Loans

• The number debtors with loans in the non-formal sector is considerably small, relatively to those in the formal sector.

28

Average Behavior Score by Asset Manager Rating: Monthly

Behavior Score Evolution by Assets Manager

480

490

500

510

520

530

540

Jan-05

Mar-05

May-05

Jul-0

5Se

p-05Nov-0

5

Jan-06

Mar-06

May-06

Jul-0

6Se

p-06

Month

Ave

rage

Sco

re

Average Over Average Cut-off Point

• The Asset Manager rating is granted by rating agencies to evaluate the ability and expertise to originate, collect and manage mortgages

29

Average Behavior Score by Asset Manager Rating: October 2006

Behavior Score Evolution by Assets Manager October 06

400

420

440

460

480

500

520

540

560

Average Over Average

Assets Manager

Ave

rage

Sco

re

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

Num

ber o

f Loa

ns

Mean Loans

• As expected, the Over-Average group of SOFOLes has a higher average score, considerably less dispersion and a large number of loans than the Average group.

30

Average Behavior Score by Age of Loans: October 2006

• Behavior Score is dependent on the age of the portfolio

Behavior Score Distribution by Age

503

508

513

518

523

528

533

538

7 12 17 22 27 32 37 42 47 52 57 62 67 72Months

Ave

rage

Sco

re

Cut-off point

Average Score by State: October 2006

31

• Northern States tend to have lower behavior scores

Nevertheless, in all states,

the Average Behavior

Score is above the cut-off

point. (503 pts.)

Nuevo León 29.93 Formal 504.61 9.27%Durango 35.61 Formal 510.21 1.43%Chiapas 35.86 Formal 510.95 2.80%Sonora 34.43 Formal 511.26 4.42%

Guanajuato 33.15 Formal 512.67 3.48%Sinaloa 30.73 Formal 512.75 3.28%

Baja California 38.49 Formal 513.49 11.71%Tamaulipas 34.07 Formal 514.27 4.27%

Guerrero 35.69 Formal 514.31 0.54%Estado de México 38.78 Formal 514.88 9.73%

Average of theCountry 35.26 Formal 515.71

Average Age in Months Employment Average Score Concentration (by

Number of Loans)State