morgan stanley global metals & mining...

TRANSCRIPT

Morgan Stanley Global Metals &

Mining Conference

November 2011

1

Disclaimer

•Forward-Looking Statements

This document may contain forward-looking information and statements about

ArcelorMittal and its subsidiaries. These statements include financial projections and estimates

and their underlying assumptions, statements regarding plans, objectives and expectations with

respect to future operations, products and services, and statements regarding future performance.

Forward-looking statements may be identified by the words “believe,” “expect,” “anticipate,”

“target” or similar expressions. Although ArcelorMittal‟s management believes that the

expectations reflected in such forward-looking statements are reasonable, investors and holders

of ArcelorMittal‟s securities are cautioned that forward-looking information and statements are

subject to numerous risks and uncertainties, many of which are difficult to predict and generally

beyond the control of ArcelorMittal, that could cause actual results and developments to differ

materially and adversely from those expressed in, or implied or projected by, the forward-looking

information and statements. These risks and uncertainties include those discussed or identified in

the filings with the Luxembourg Stock Market Authority for the Financial Markets (Commission de

Surveillance du Secteur Financier) and the United States Securities and Exchange Commission

(the “SEC”) made or to be made by ArcelorMittal, including ArcelorMittal‟s Annual Report on Form

20-F for the year ended December 31, 2010 filed with the SEC. ArcelorMittal undertakes no

obligation to publicly update its forward-looking statements, whether as a result of new

information, future events, or otherwise.

2

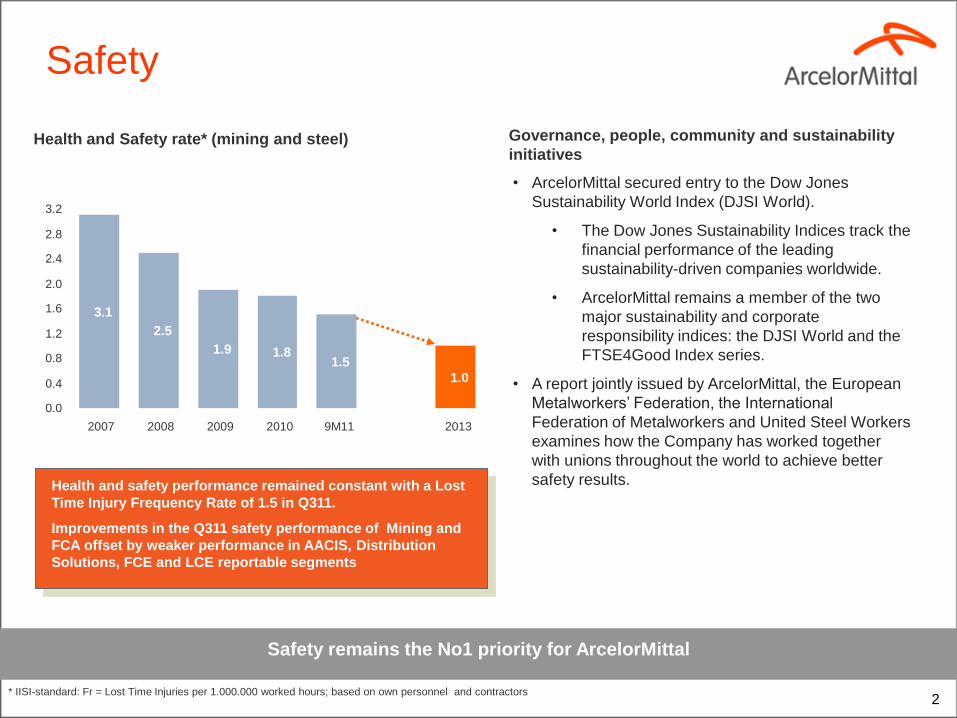

Safety

* IISI-standard: Fr = Lost Time Injuries per 1.000.000 worked hours; based on own personnel and contractors

Health and safety performance remained constant with a Lost

Time Injury Frequency Rate of 1.5 in Q311.

Improvements in the Q311 safety performance of Mining and

FCA offset by weaker performance in AACIS, Distribution

Solutions, FCE and LCE reportable segments

Safety remains the No1 priority for ArcelorMittal

Governance, people, community and sustainability

initiatives

• ArcelorMittal secured entry to the Dow Jones

Sustainability World Index (DJSI World).

• The Dow Jones Sustainability Indices track the

financial performance of the leading

sustainability-driven companies worldwide.

• ArcelorMittal remains a member of the two

major sustainability and corporate

responsibility indices: the DJSI World and the

FTSE4Good Index series.

• A report jointly issued by ArcelorMittal, the European

Metalworkers‟ Federation, the International

Federation of Metalworkers and United Steel Workers

examines how the Company has worked together

with unions throughout the world to achieve better

safety results.

Health and Safety rate* (mining and steel)

3.1

2.5

1.9 1.8 1.5

1.0

0.0

0.4

0.8

1.2

1.6

2.0

2.4

2.8

3.2

2007 2008 2009 2010 9M11 2013

3

Core strengths

• High quality core assets – Utilising 71% of our capacity ArcelorMittal delivered an average EBITDA/tonne of $114/t in 3Q‟11

– ~40% of “steel EBITDA” in 9M‟11 was generated from production outside Europe/North America

• Industry leading automotive steel franchise – 40% share of core markets

– Higher (and growing) market share in advanced high strength steels

• A world-class and growing mining business – 4.3bn tonnes of iron ore reserves with a further 11.3bn tonnes of resources

– Competitive on cost and quality; margins on “marketable tonnes” comparable with industry leaders

• Good track record of consistent management gains – $3.8bn achieved since 2008 and on track for $4.8bn by end 2012

– New $1bn Asset Optimisation Plan launched to generate sustainable EBITDA improvement

• A strong balance sheet – 5.1yr average maturity with no covenants on term debt*

– $11.3bn of liquidity** at September 30, 2011

* Covenant of 3.5x Net Debt/EBITDA applies only to available liquidity lines ($10.6bn of which $2.1bn drawn at September 30, 2011); ** Cash and cash equivalents and available drawing capacity under credit lines; Refer to

resource and reserve definitions as provided by in the September 2011 investor day materials

ArcelorMittal in a strong position to respond to evolving markets

4

1H

1H1H

2H

2H

2H

0

2000

4000

6000

8000

10000

12000

2009 2010 2011

EBITDA progression (US$mn)

14532162 2408

114/t

105/t

81/t

0

500

1000

1500

2000

2500

3000

3500

Q3'09 Q3'10 Q3'11

0

20

40

60

80

100

120

Snapshot: Profitability improving Y-o-Y

• 3Q‟11 EBITDA increased 11.4% y-o-y to $2.4 billion; 9M11 EBITDA $8.4bn, 25.9% higher than 9M10

• 3Q‟11 EBITDA/t of $114, 8.5% higher than 3Q‟10

• Own iron ore production 14.1Mt in 3Q‟11 and 39.0Mt in 9M11; on track for 10% growth this year

• Net debt at September 30, 2011 of $24.9 billion as compared to $25.0 billion at June 30, 2011

• Guidance: 2H‟11 EBITDA expected to be above 2H‟10

2H 2011 EBITDA expected to exceed the level of 2H 2010

Group EBITDA (US$mn)

5

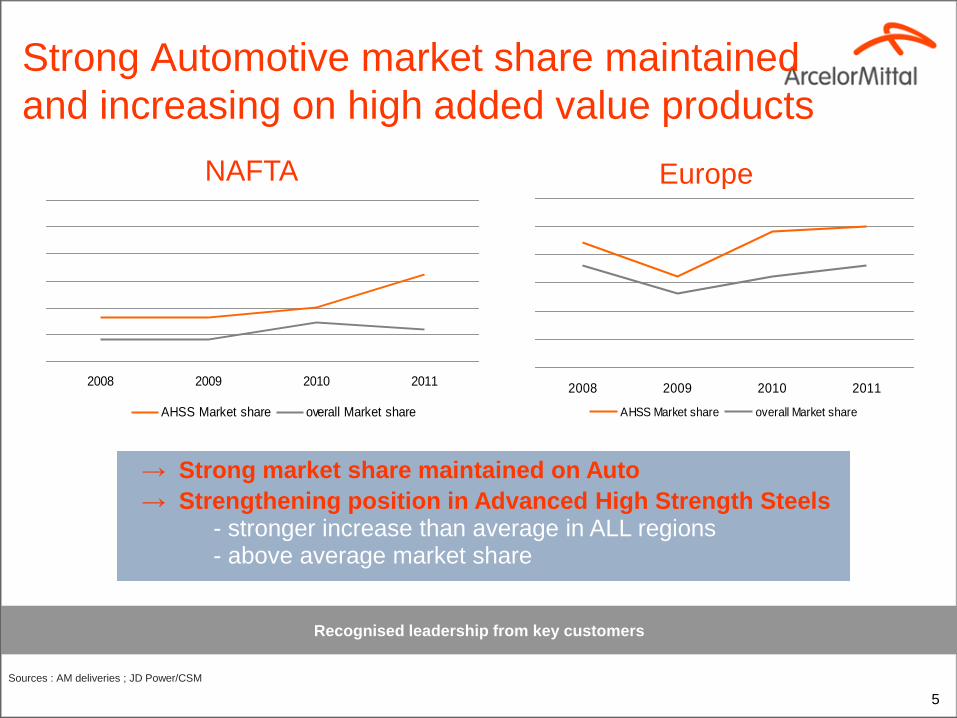

Strong Automotive market share maintained

and increasing on high added value products

→ Strong market share maintained on Auto

→ Strengthening position in Advanced High Strength Steels - stronger increase than average in ALL regions - above average market share

Sources : AM deliveries ; JD Power/CSM

NAFTA Europe

2008 2009 2010 2011

AHSS Market share overall Market share

2008 2009 2010 2011

AHSS Market share overall Market share

Recognised leadership from key customers

6

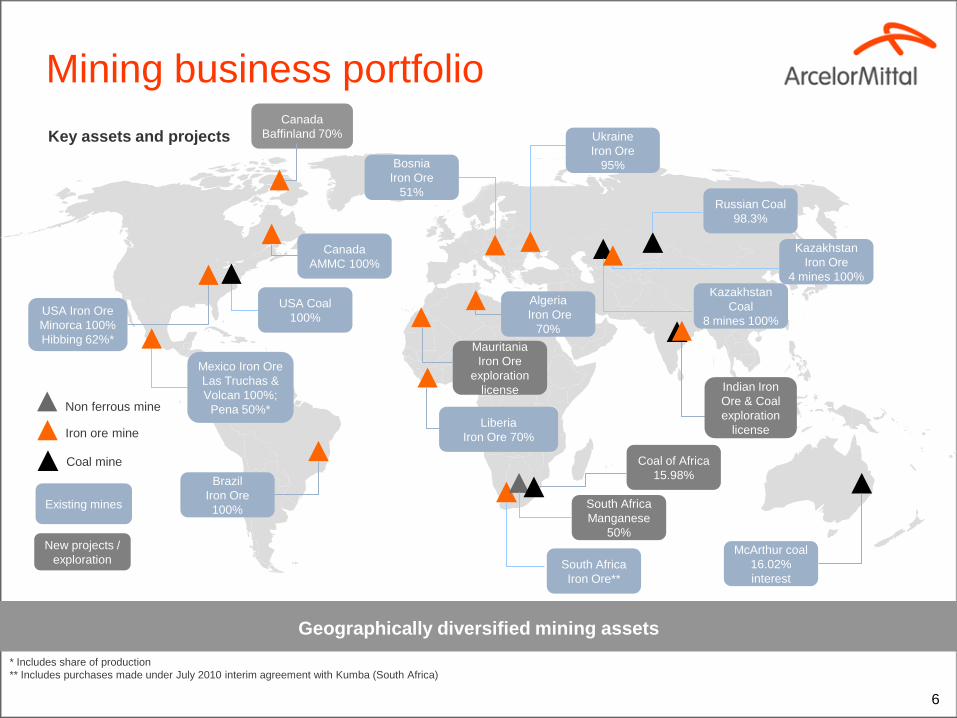

Geographically diversified mining assets

South Africa

Iron Ore**

* Includes share of production

** Includes purchases made under July 2010 interim agreement with Kumba (South Africa)

Mining business portfolio

Key assets and projects

USA Iron Ore

Minorca 100%

Hibbing 62%*

Mexico Iron Ore

Las Truchas &

Volcan 100%;

Pena 50%* Liberia

Iron Ore 70%

Algeria

Iron Ore

70%

Brazil

Iron Ore

100%

New projects /

exploration

Existing mines

Mauritania

Iron Ore

exploration

license

Canada

AMMC 100%

Bosnia

Iron Ore

51%

USA Coal

100%

South Africa

Manganese

50%

Indian Iron

Ore & Coal

exploration

license

Ukraine

Iron Ore

95%

Kazakhstan

Coal

8 mines 100%

Kazakhstan

Iron Ore

4 mines 100%

Russian Coal

98.3%

Iron ore mine

Non ferrous mine

Coal mine

McArthur coal

16.02%

interest

Coal of Africa

15.98%

Canada

Baffinland 70%

7

Type of product

Region

Proven & probable

reserves

Measured & indicated

resources

Inferred

resources

Mtonnes %Fe Mtonnes %Fe Mtonnes %Fe

Canada (AMMC) 2,350 29 3,442 30 1,025 28

Canada

(Baffinland) 375 65 41 66 444 65

USA 581 20 41 23 90 23

Central America 308 29 117 29 88 28

South America 134 58 321 38 130 37

West Africa 22 61 1,539 44 1,522 41

Eastern Europe 366 37 866 38 - -

Central Asia 120 41 1,629 40 30 51

TOTAL 4,255 33 7,997 36 3,329 39

Iron ore reserves and resources

2010 year-end estimates

The life of mine plans of operations and planned expansion projects

are 90% based on ore reserve estimates

Lumps

Fines

Pellet feed

Conc

• Tonnage and grade estimates are reported as „Run of Mine‟. Tonnage is reported on a wet metric basis. Where we own less than 100% of the operation, the estimates have not been adjusted to reflect our ownership interest.

• Mineral resource estimates are reported in addition to ore reserve estimates.

• The ore reserve and mineral resource estimates have been prepared under the supervision of ArcelorMittal qualified personnel . Detailed independent audits are conducted on a regular basis.

The terms "mineral resource", "measured mineral resource", "indicated mineral resource" and "inferred mineral resource" are defined in, and have been calculated in accordance with the guidelines set forth in,

Canadian National Instrument 43-101 (“NI 43-101”). NI 43-101 is a codified set of rules and guidelines for reporting and displaying information related to mineral properties owned by, or explored by, companies which

report results on stock exchanges within Canada, and is recognized by several other international stock exchanges and regulatory bodies. However, these terms are not defined terms under SEC Industry Guide 7 and

(absent an applicable exception) are not permitted to be used in reports and registration statements filed with the SEC. Investors are cautioned not to assume that any part or all of mineral deposits in these categories

will ever be converted into reserves. "Inferred mineral resources" have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all

or any part of an inferred mineral resource will ever be upgraded to a higher category.

8

0

10000

20000

30000

40000

50000

60000

70000

80000

90000

2010 2011F 2012 2013 2014 2015

Cost plus tonnage Marketable tonnage

97%

Growth

41%

Growth

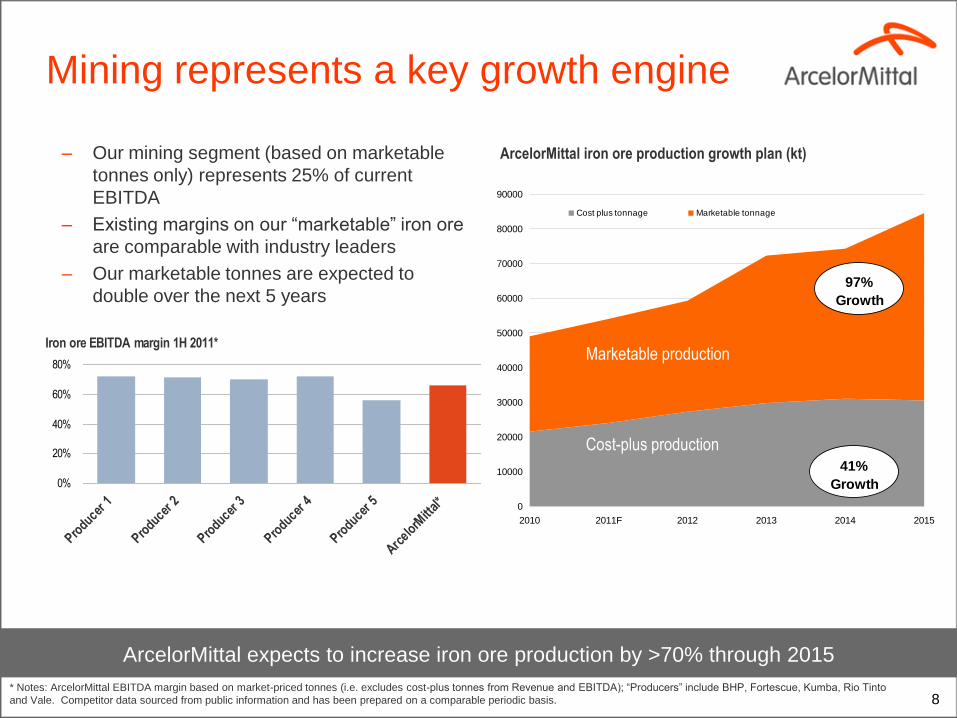

Mining represents a key growth engine

ArcelorMittal iron ore production growth plan (kt)

Marketable production

Cost-plus production

ArcelorMittal expects to increase iron ore production by >70% through 2015

Iron ore EBITDA margin 1H 2011*

0%

20%

40%

60%

80%

Producer

1

Producer

2

Producer

3

Producer

4

Producer

5

Arcelo

rMitt

al*

– Our mining segment (based on marketable

tonnes only) represents 25% of current

EBITDA

– Existing margins on our “marketable” iron ore

are comparable with industry leaders

– Our marketable tonnes are expected to

double over the next 5 years

* Notes: ArcelorMittal EBITDA margin based on market-priced tonnes (i.e. excludes cost-plus tonnes from Revenue and EBITDA); “Producers” include BHP, Fortescue, Kumba, Rio Tinto

and Vale. Competitor data sourced from public information and has been prepared on a comparable periodic basis.

9

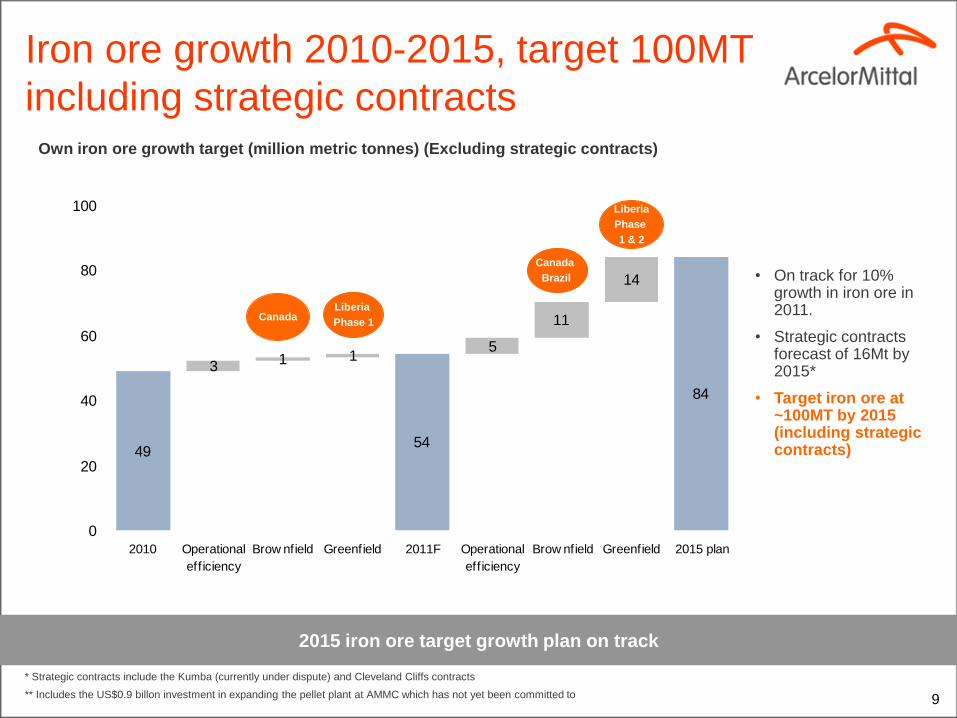

Iron ore growth 2010-2015, target 100MT

including strategic contracts

2015 iron ore target growth plan on track

Canada

Brazil

Liberia

Phase

1 & 2

Liberia

Phase 1

Own iron ore growth target (million metric tonnes) (Excluding strategic contracts)

Canada

• On track for 10% growth in iron ore in 2011.

• Strategic contracts forecast of 16Mt by 2015*

• Target iron ore at ~100MT by 2015 (including strategic contracts)

* Strategic contracts include the Kumba (currently under dispute) and Cleveland Cliffs contracts

** Includes the US$0.9 billon investment in expanding the pellet plant at AMMC which has not yet been committed to

49

3 1 1

54

5

11

14

84

0

20

40

60

80

100

2010 Operational

eff iciency

Brow nfield Greenfield 2011F Operational

eff iciency

Brow nfield Greenfield 2015 plan

10

1.9

4.0

$0bn

$1bn

$1bn

$2bn

$2bn

$3bn

$3bn

$4bn

$4bn

$5bn

2009 2012

2012 supported by management gains

• Management gains will contribute more to EBITDA than it did in

2009

Management gains will have a significantly higher contribution to EBITDA in 2012 than in 2009

*

* This assumes that we exit 2011 with management gains of $4bn and make no further progress in 2012; at end of 2Q‟11 $3.6bn had been achieved and end-

2012 target remains $4.8bn

Contribution of management gains to EBITDA (US$bn)

11

-

200

400

600

800

1,000

1,200

2011 2012 2013

2012 supported by Asset Optimisation

• Focus on “Core” assets will ensure lowest cost footprint

achieved and yield significant savings; target $1bn by end-2012

Asset Optimisation Plan will further support EBITDA in 2012

Expected Contribution of Asset Optimisation Plan to EBITDA (US$mn)

12

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2011 2012 2013 2014 2015 2016 Thereafter

RCF, 8%

Bonds, 64%

Other, 17%

Commercia l

paper, 6%

Convertible,

8%

0.0

2.0

4.0

6.0

8.0

10.0

12.0

2008 2009 2010 2011 2012 2013 Thereafter

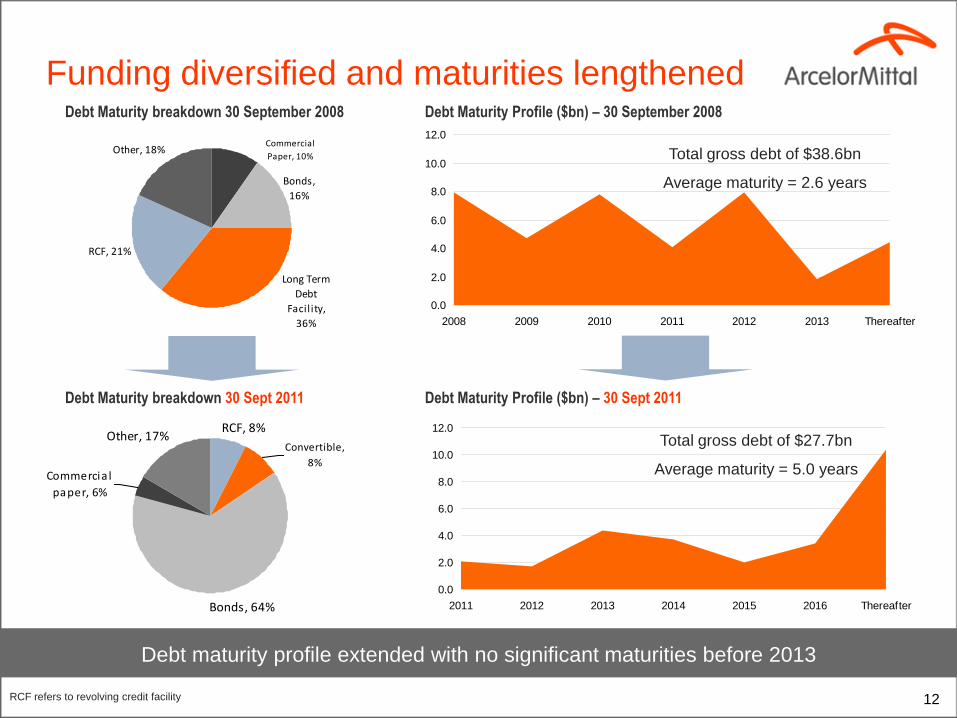

Funding diversified and maturities lengthened

Debt maturity profile extended with no significant maturities before 2013

Debt Maturity breakdown 30 Sept 2011 Debt Maturity Profile ($bn) – 30 Sept 2011

Debt Maturity Profile ($bn) – 30 September 2008 Debt Maturity breakdown 30 September 2008

RCF refers to revolving credit facility

Total gross debt of $38.6bn

Average maturity = 2.6 years

Total gross debt of $27.7bn

Average maturity = 5.0 years

RCF, 21%

Other, 18%

Long Term

Debt

Facility,

36%

Bonds,

16%

Commercial

Paper, 10%

13

• We have $11.3bn of liquidity at 30 Sept 2011

Liquidity is significant and diversified

Continued strong liquidity position and lengthening of debt maturities

8.5

1.1

1.02.8

Liquidity at 30/9/11 Debt due in 2011

Unused

credit line

Cash &

Equivalent

Short term & Others

11.3

Commercial paper

2.1

– We have no significant counterparty risk on our liquidity lines of $10.6bn

– Exposure is widely spread amongst 28 different banks with average exposure of ~$350mm

Liquidity lines:

– $4bn syndicated credit facility matures 06/05/15

– $6bn syndicated credit facility matures 18/03/16

– $0.6bn bilateral facility matures 30/06/13

14

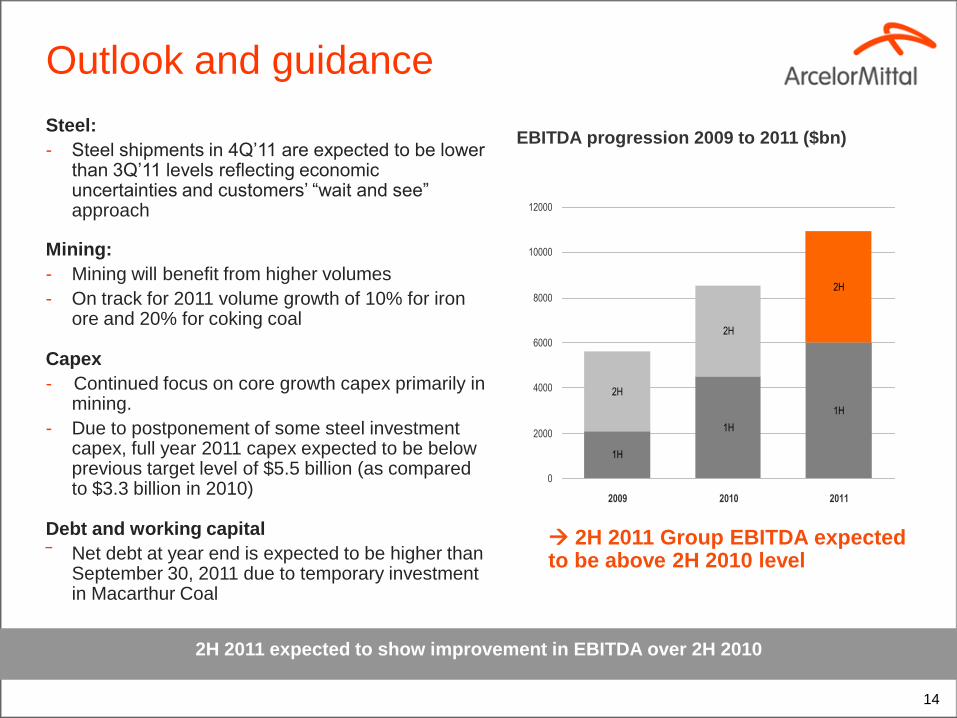

Outlook and guidance

2H 2011 expected to show improvement in EBITDA over 2H 2010

Steel:

- Steel shipments in 4Q‟11 are expected to be lower than 3Q‟11 levels reflecting economic uncertainties and customers‟ “wait and see” approach

Mining:

- Mining will benefit from higher volumes

- On track for 2011 volume growth of 10% for iron ore and 20% for coking coal

Capex

- Continued focus on core growth capex primarily in mining.

- Due to postponement of some steel investment capex, full year 2011 capex expected to be below previous target level of $5.5 billion (as compared to $3.3 billion in 2010)

Debt and working capital

‾ Net debt at year end is expected to be higher than September 30, 2011 due to temporary investment in Macarthur Coal

1H

1H

1H

2H

2H

2H

0

2000

4000

6000

8000

10000

12000

2009 2010 2011

2H 2011 Group EBITDA expected to be above 2H 2010 level

EBITDA progression 2009 to 2011 ($bn)

15

Appendix

16

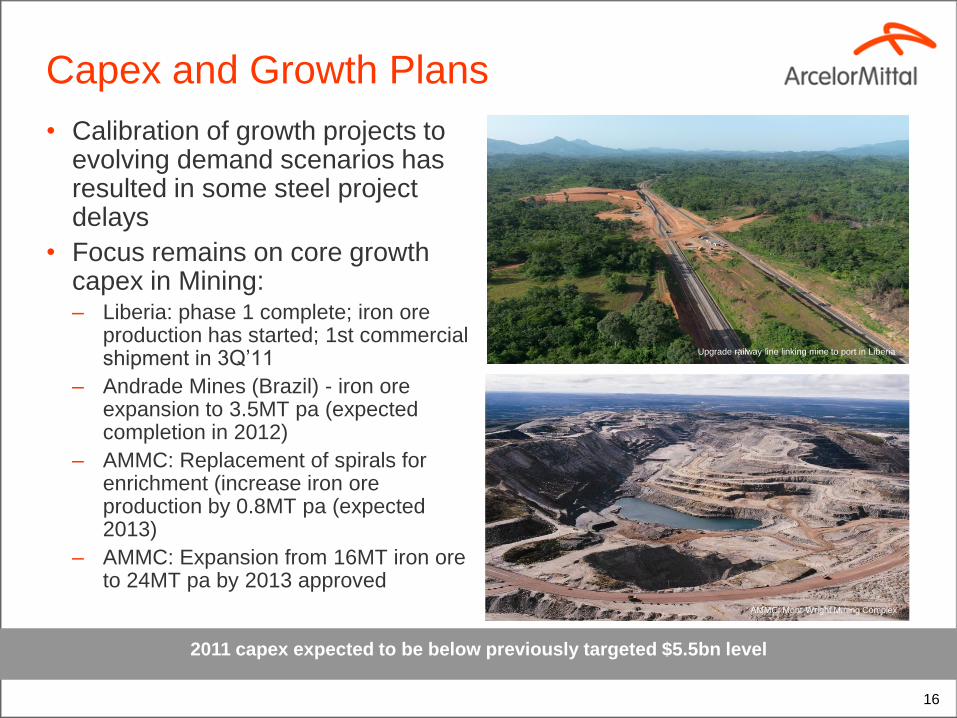

Capex and Growth Plans

• Calibration of growth projects to evolving demand scenarios has resulted in some steel project delays

• Focus remains on core growth capex in Mining: – Liberia: phase 1 complete; iron ore

production has started; 1st commercial shipment in 3Q‟11

– Andrade Mines (Brazil) - iron ore expansion to 3.5MT pa (expected completion in 2012)

– AMMC: Replacement of spirals for enrichment (increase iron ore production by 0.8MT pa (expected 2013)

– AMMC: Expansion from 16MT iron ore to 24MT pa by 2013 approved

2011 capex expected to be below previously targeted $5.5bn level

Upgrade railway line linking mine to port in Liberia

AMMC: Mont-Wright Mining Complex

0

5

10

15

20

25

30

35

2009 2010 2011F 2012F

0

1

2

3

4

5

6

7

Iron ore (LHScale) Coal (RHScale)

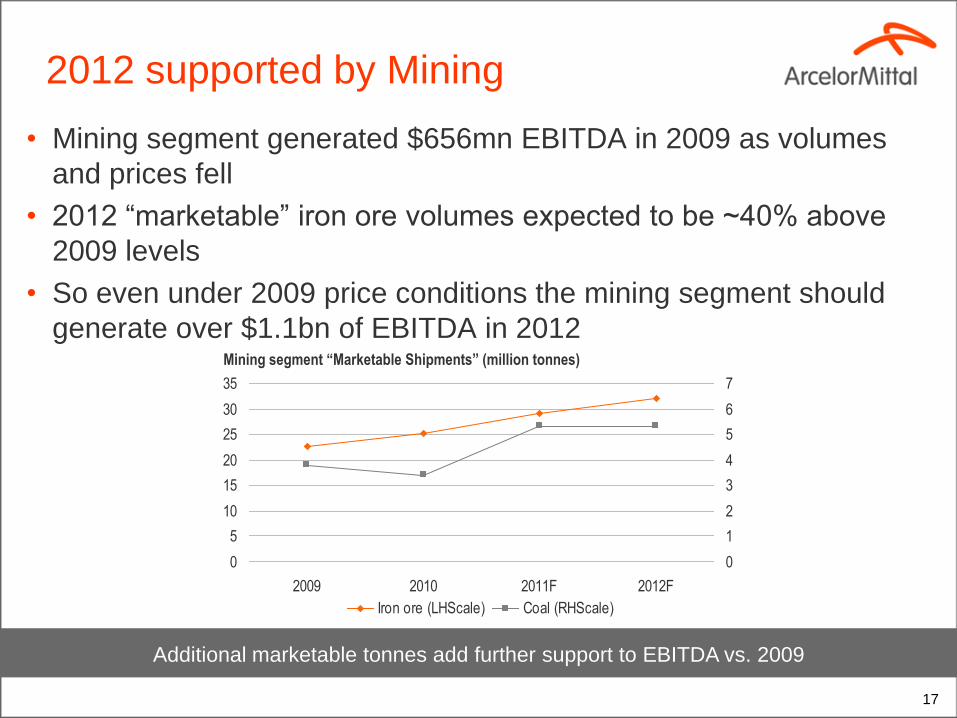

• Mining segment generated $656mn EBITDA in 2009 as volumes

and prices fell

• 2012 “marketable” iron ore volumes expected to be ~40% above

2009 levels

• So even under 2009 price conditions the mining segment should

generate over $1.1bn of EBITDA in 2012

2012 supported by Mining

Additional marketable tonnes add further support to EBITDA vs. 2009

17

Mining segment “Marketable Shipments” (million tonnes)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan 0

8

Mar

08

May 0

8

Jul 08

Sep 0

8

Nov 0

8

Jan-0

9

Mar-

09

May-0

9

Jul-09

Sep-0

9

Nov-0

9

Jan-1

0

Mar-

10

May-1

0

Jul-10

Sep-1

0

Nov-1

0

Jan-1

1

Mar-

11

May-1

1

Jul-11

0

2,000

4,000

6,000

8,000

10,000

12,000

US Service Centre Inventories (tonnes) Inventory/Shipments (MoS)

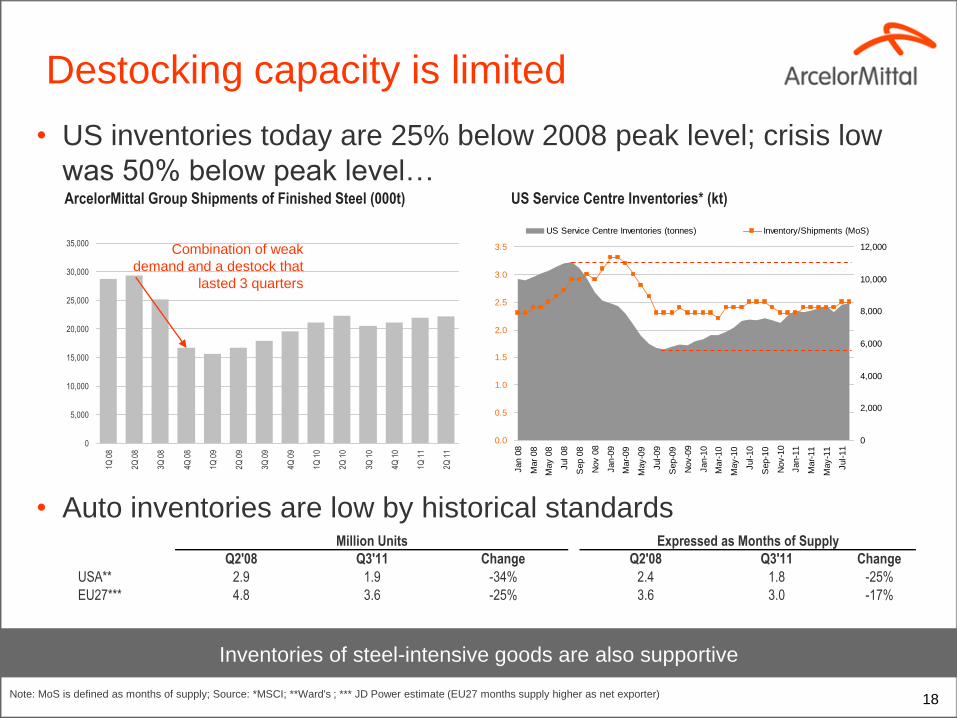

Destocking capacity is limited

• US inventories today are 25% below 2008 peak level; crisis low

was 50% below peak level…

• Auto inventories are low by historical standards

18

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

1Q 0

8

2Q 0

8

3Q 0

8

4Q 0

8

1Q 0

9

2Q 0

9

3Q 0

9

4Q 0

9

1Q 1

0

2Q 1

0

3Q 1

0

4Q 1

0

1Q 1

1

2Q 1

1

ArcelorMittal Group Shipments of Finished Steel (000t) US Service Centre Inventories* (kt)

Inventories of steel-intensive goods are also supportive

Combination of weak

demand and a destock that

lasted 3 quarters

Note: MoS is defined as months of supply; Source: *MSCI; **Ward's ; *** JD Power estimate (EU27 months supply higher as net exporter)

Million Units Expressed as Months of Supply

Q2'08 Q3'11 Change Q2'08 Q3'11 Change

USA** 2.9 1.9 -34% 2.4 1.8 -25%

EU27*** 4.8 3.6 -25% 3.6 3.0 -17%

19

Outlook for Steel

20

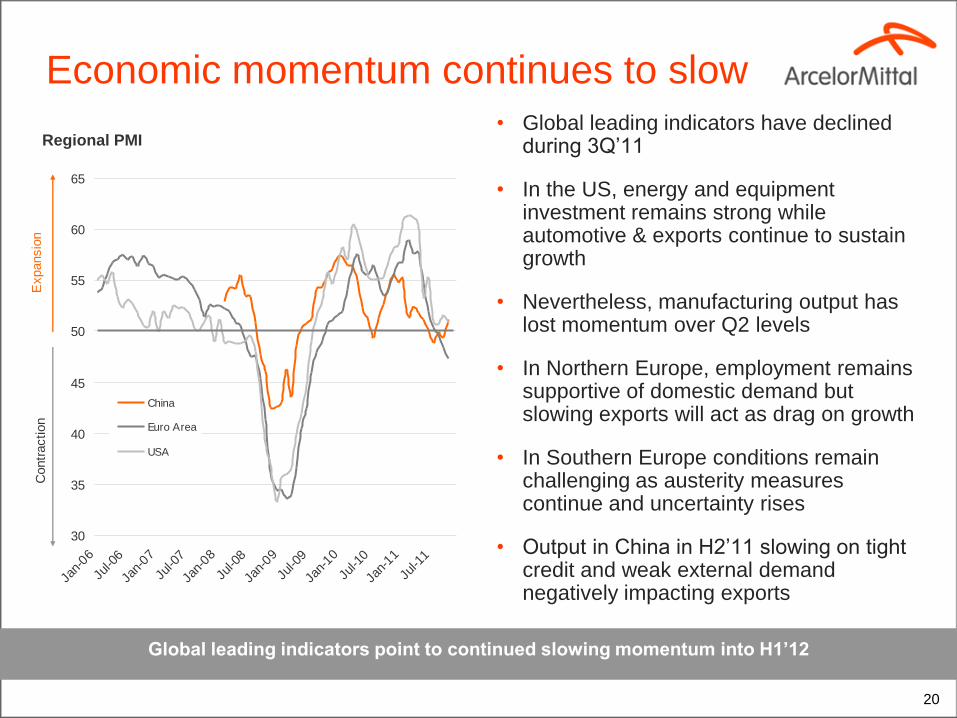

• Global leading indicators have declined during 3Q‟11

• In the US, energy and equipment investment remains strong while automotive & exports continue to sustain growth

• Nevertheless, manufacturing output has lost momentum over Q2 levels

• In Northern Europe, employment remains supportive of domestic demand but slowing exports will act as drag on growth

• In Southern Europe conditions remain challenging as austerity measures continue and uncertainty rises

• Output in China in H2‟11 slowing on tight credit and weak external demand negatively impacting exports

Regional PMI

Global leading indicators point to continued slowing momentum into H1’12

Economic momentum continues to slow

30

35

40

45

50

55

60

65

Jan-

06

Jul-0

6

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

China

Euro Area

USA

Expansio

nC

ontr

action

21

Developed world construction stable at low

levels

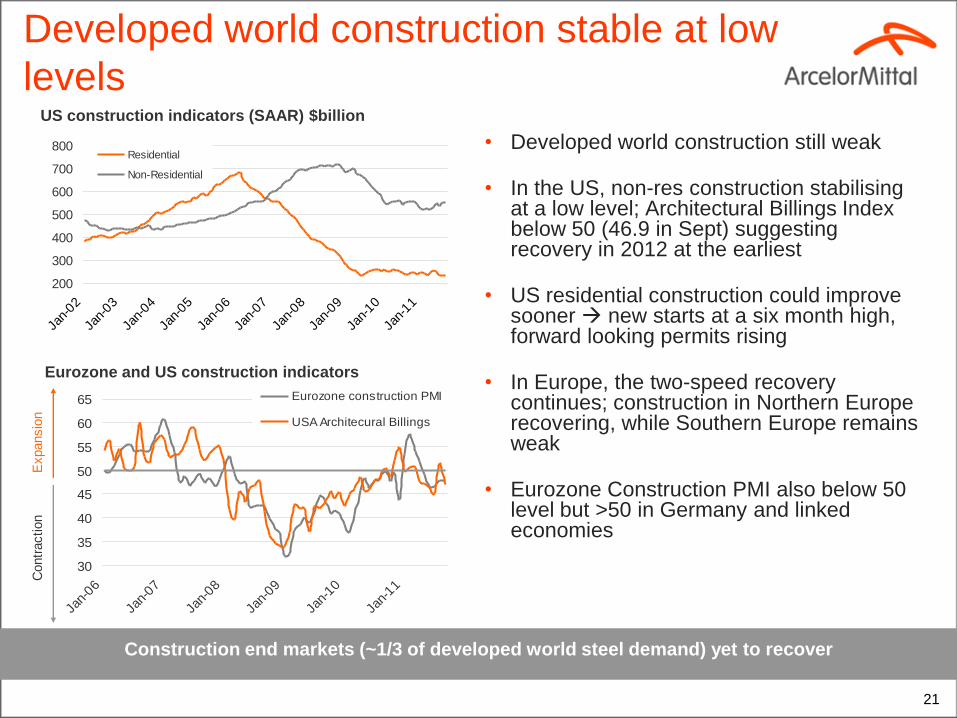

• Developed world construction still weak

• In the US, non-res construction stabilising at a low level; Architectural Billings Index below 50 (46.9 in Sept) suggesting recovery in 2012 at the earliest

• US residential construction could improve sooner new starts at a six month high, forward looking permits rising

• In Europe, the two-speed recovery continues; construction in Northern Europe recovering, while Southern Europe remains weak

• Eurozone Construction PMI also below 50 level but >50 in Germany and linked economies

Eurozone and US construction indicators

US construction indicators (SAAR) $billion

Construction end markets (~1/3 of developed world steel demand) yet to recover

Expansio

nC

ontr

action

30

35

40

45

50

55

60

65

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Eurozone construction PMI

USA Architecural Billings

Index

200

300

400

500

600

700

800

Jan-

02

Jan-

03

Jan-

04

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Residential

Non-Residential

22

Pace of growth in China slowing

• We expect a soft landing for the Chinese economy

• Construction remained strong in 1H‟11 but signs of slowing in 2H‟11

• Controls on private real estate market are having an impact; but any slowdown should be offset by increased public housing spend

• We expect a slowdown in steel production in the coming months, but we still expect ASC growth of over 8.5% in 2011

• Exports peaked at 4.8mmt in Mar‟11, and so far fallen -14.3% from these levels to 4.2mt in Sept‟11

• Overall 2011 net exports expected at 32mt vs 24.5mt in 2010

China ASC growth >8.5% in 2011

-0.5

0.5

1.5

2.5

3.5

4.5

5.5

6.5

Jan-0

6

Jul-0

6

Jan-0

7

Jul-0

7

Jan-0

8

Jul-0

8

Jan-0

9

Jul-0

9

Jan-1

0

Jul-1

0

Jan-1

1

Jul-1

1

70

90

110

130

150

170

190

210

230

250

270

290

310

330

Jan-

05

Jan-

06

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Floor Space under construction (12mma)

New ly Started Construction (SA, 3mma)

China Construction Indicator (Million Metre sq.)

Net Exports of Finished Steel (000t)

23

0

2000

4000

6000

8000

10000

12000

14000

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

2

2.2

2.4

2.6

2.8

3

3.2

3.4

3.6

USA (MSCI)

Months Supply

Destocking capacity is limited

Europe Service Centre Inventories (Mn MT)

Brazil Service Centre Inventories (Mn MT)

US Service Centre Total Steel Inventories (Mn MT)

China Inventories in 25 Major Cities (Mn MT)

Inventory levels are at normal levels in US and China, reducing in Brazil and have increased in Europe

1000

1200

1400

1600

1800

2000

2200

2400

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

1.6

1.8

2

2.2

2.4

2.6

2.8

3

3.2

3.4

3.6EU (EASSC)

Months Supply

2

4

6

8

10

12

14

16

18

20

Jan-

07

Apr-0

7

Jul-0

7

Oct-0

7

Jan-

08

Apr-0

8

Jul-0

8

Oct-0

8

Jan-

09

Apr-0

9

Jul-0

9

Oct-0

9

Jan-

10

Apr-1

0

Jul-1

0

Oct-1

0

Jan-

11

Apr-1

1

Jul-1

1

Oct-1

1

Flat Long

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

1.5

2

2.5

3

3.5

4

4.5Flat stocks at service centres

Months of supply

24

Slowing underlying demand and weaker

sentiment impacting on prices

Spot iron ore, coking coal and scrap price

(index IH 2008=100) Regional Steel price HRC ($/t)

Raw material prices have recently come under pressure

30

40

50

60

70

80

90

100

110

120

130

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Iron Ore

Coking Coal

Scrap

400

500

600

700

800

900

1000

1100

1200

1300

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

China domestic Shanghai

N.America FOB Midwest

N.Europe domestic ex-works

25

0

200

400

600

800

1000

1200

1400

2008 2009 2010 2011 2012

China EU27 NAFTA ROW

Global apparent steel consumption

6.5-7% 6.5-7%

6.5-7%

6.5-7%

China: +5% YoY

EU27: +6.1% YoY

RoW: +5.5% YoY

NAFTA: +5% YoY*

We expect global Apparent Steel Consumption growth of +7% in 2011 slowing to ~5%* in 2012

RoW: +4.6% YoY

NAFTA: +9% YoY

China: >8.5% YoY

EU27: +/- 1% YoY*

* Base case assumption is low single-digit growth in developed world apparent steel consumption (ASC); a consumer-sentiment driven technical recession in EU and US could lead to a low

single-digit decline in developed world ASC; a deeper Euro-debt crisis with negative YoY GDP growth could see low double-digit decline in developed world ASC

26

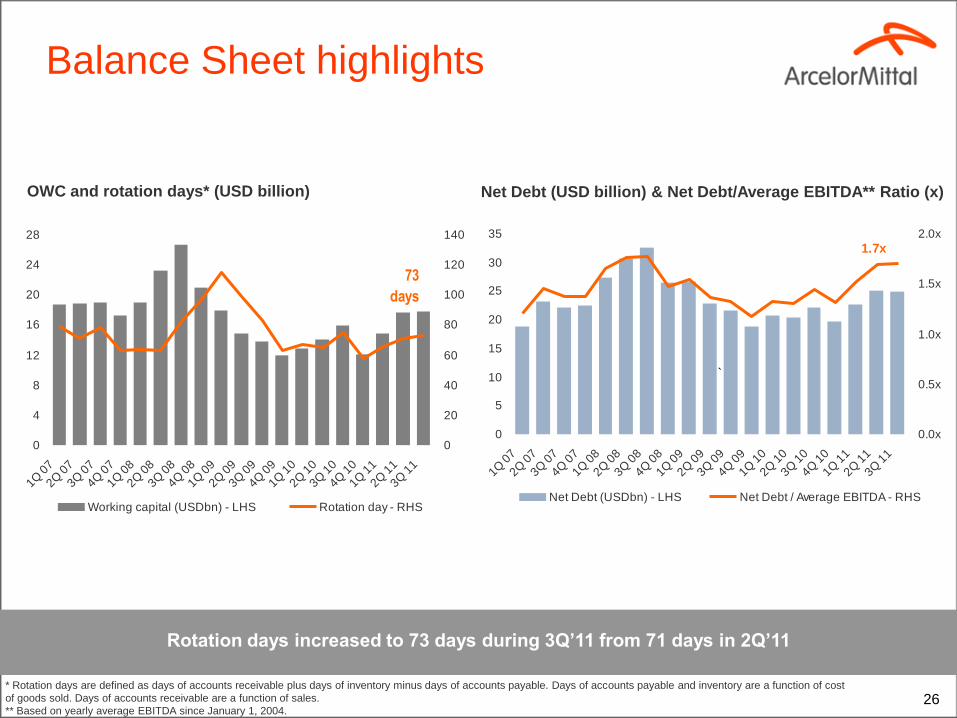

Balance Sheet highlights

OWC and rotation days* (USD billion) Net Debt (USD billion) & Net Debt/Average EBITDA** Ratio (x)

* Rotation days are defined as days of accounts receivable plus days of inventory minus days of accounts payable. Days of accounts payable and inventory are a function of cost

of goods sold. Days of accounts receivable are a function of sales.

** Based on yearly average EBITDA since January 1, 2004.

Rotation days increased to 73 days during 3Q’11 from 71 days in 2Q’11

0

5

10

15

20

25

30

35

1Q 0

7

2Q 0

7

3Q 0

7

4Q 0

7

1Q 0

8

2Q 0

8

3Q 0

8

4Q 0

8

1Q 0

9

2Q 0

9

3Q 0

9

4Q 0

9

1Q 1

0

2Q 1

0

3Q 1

0

4Q 1

0

1Q 1

1

2Q 1

1

3Q 1

1

0.0x

0.5x

1.0x

1.5x

2.0x

Net Debt (USDbn) - LHS Net Debt / Average EBITDA - RHS

1.7x

`

0

4

8

12

16

20

24

28

1Q 0

7

2Q 0

7

3Q 0

7

4Q 0

7

1Q 0

8

2Q 0

8

3Q 0

8

4Q 0

8

1Q 0

9

2Q 0

9

3Q 0

9

4Q 0

9

1Q 1

0

2Q 1

0

3Q 1

0

4Q 1

0

1Q 1

1

2Q 1

1

3Q 1

1

0

20

40

60

80

100

120

140

Working capital (USDbn) - LHS Rotation day - RHS

73

days

27

Net debt scenarios

• We expect to achieve net debt target of <$22.5bn by mid 2012

• Under these economic scenarios: we expect to achieve our net debt target by mid-2012

we retain significant headroom to the 3.5x net debt/LTM** EBITDA covenants on our liquidity lines

Net debt is expected to decline under these scenarios

The following financial metrics are for illustrative purposes only and should not be

construed as guidance

Economic Scenarios EBITDA Working Capital Net Debt ND/EBITDA

Low growth* Greater than 2011 Neutral <$22.5bn <2.0

Recession* Lower than 2011 but above crisis Release <$22.5bn >2.0 but <3.0

2009-type crisis 2009 Level + Delta Management Gains + Mining Growth Significant Release <$22.5bn <3.0

* Low-growth scenario suggests low single-digit growth in developed world apparent steel consumption (ASC); a consumer-sentiment driven technical recession could lead to a low single-digit

decline in developed world ASC; a deeper Euro-debt crisis with negative YoY GDP growth could see low double-digit decline in developed world ASC ** LTM refers to last twelve months

28

ArcelorMittal Mines Canada (AMMC):

expansion underway

• Expansion of our Mont Wright mine at AMMC and concentrate capacity to 24Mt pa due 2013 (from 16Mtpa post operational improvements) approved

• Expansion capitalising on existing infrastructure, product quality and experienced workforce

• Capex C$1.2bn for mine and concentrator plant expansion*

• Cash cost is circa US$35/tonne

• Advantageously located with easy access to European and US markets

Mining expansion plan (concentrate) Million mt

Canadian industrial location ArcelorMittal Mines Canada overview

* Total scheme investment of US$2.1 billion includes investment in expanding the pellet plant which has not yet been committed to

Bloom LakeBloom Lake

Strategic advantage from exclusive use of own rail and port facilities

14 15

1

9

5

10

15

20

25

2011F 2013

Brownfield expansion

Canada base

`

* AMMC 2013 brownfield expansion includes 1mt increase for spirals

29

14

15

0

4

8

12

16

2011F 2012 2015

`

• Phase 1: DSO complete

– 240km rail rehabilitation completed

– Upgrade of Buchanan port and material handling facilities completed

– First direct shipping ore (“DSO”) product shipped in September 2011

– Ramping up to 4mtpa in 2012

• Phase 2: 15mtpa concentrate from 2015

– Expansion to 15mtpa requires investment in a concentrator currently in the final stages of approval

Liberia progress

Liberia greenfield planned expansion (Million MT)

Industrial location of mine

All marketable tonnes

Guinea

Atlantic

Ocean

Liberia

Ivory Coast Yekepa

Buchanan

Sierra Leone

Railway link from Yekepa

to Buchanan (240km)

Liberia progress on track

Liberia greenfield progress

• Total project capex (Phase 1 and 2) US$2 billion

• Expected capex of US$0.7 billion by end of 2011

30

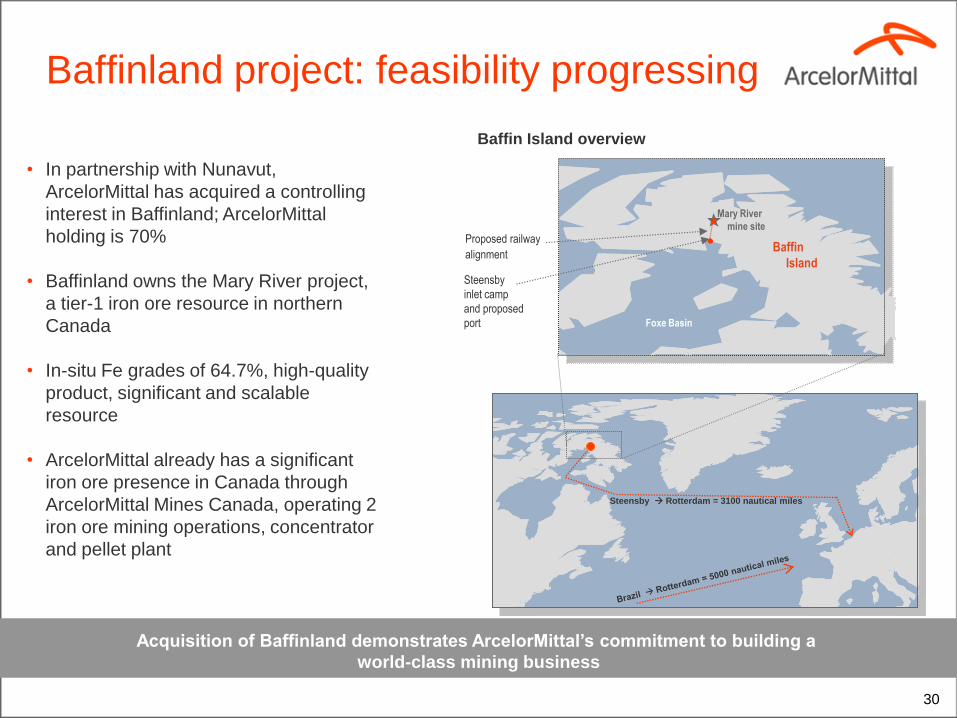

Baffinland project: feasibility progressing

Acquisition of Baffinland demonstrates ArcelorMittal’s commitment to building a

world-class mining business

• In partnership with Nunavut,

ArcelorMittal has acquired a controlling

interest in Baffinland; ArcelorMittal

holding is 70%

• Baffinland owns the Mary River project,

a tier-1 iron ore resource in northern

Canada

• In-situ Fe grades of 64.7%, high-quality

product, significant and scalable

resource

• ArcelorMittal already has a significant

iron ore presence in Canada through

ArcelorMittal Mines Canada, operating 2

iron ore mining operations, concentrator

and pellet plant

Baffin

Bay

Foxe Basin

Baffin

Island

Mary River

mine site

Proposed railway

alignment

Steensby

inlet camp

and proposed

port

Baffin Island overview

Steensby Rotterdam = 3100 nautical miles

31

70

80

90

100

110

120

130

140

150

160

2011F 2012 2013 2014 2015

70

80

90

100

110

120

130

140

150

160

Iron ore production Operating unit cost

Iron ore and coal production and opex

As production increases for iron ore and coal, operating costs are expected to fall

Iron ore production and operating unit cost

(Index base 100=2011)

Coal production and operating unit cost

(Index base 100=2011)

• Investments in AMMC and Liberia reduce the cost position of iron ore (excluding Baffinland)

• 2015 iron ore cash costs expected to be ~15% lower than 2011 (constant $ basis)

70

80

90

100

110

120

130

2011F 2012 2013 2014 2015

70

80

90

100

110

120

130

Coal production Operating unit cost

Index Index

Note: Operating unit costs shown are on a FOB basis

32

Tendering MCC shares to Peabody

• ArcelorMittal will sell its stake in Macarthur to Peabody

• Capital requirement was higher than anticipated for a non-

controlling investment

• ArcelorMittal believes it is more appropriate to focus capital

elsewhere in the business

• Cash out in 4Q‟11 of up to $1.2bn; this cash will return in

1Q‟12 along with a further $0.8bn proceeds for original

16.1% stake

• P&L loss but essentially cash neutral after dividend and

forex

ArcelorMittal is expected to receive $0.8bn for its existing 16.1% stake in Macarthur in Q1’12

33

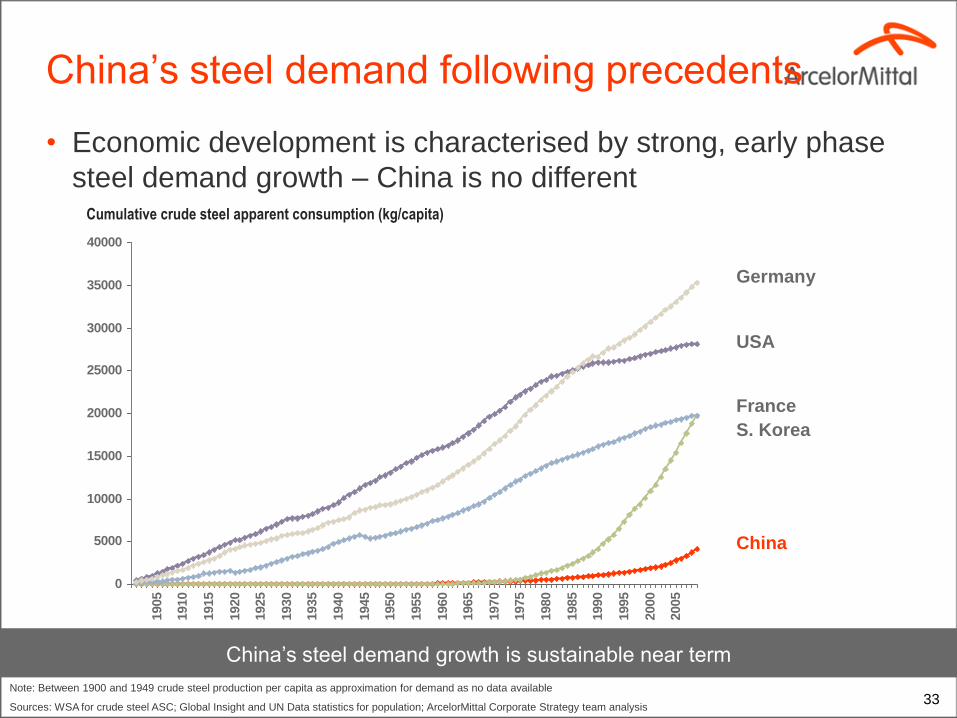

China‟s steel demand following precedents

• Economic development is characterised by strong, early phase

steel demand growth – China is no different

China‟s steel demand growth is sustainable near term

Note: Between 1900 and 1949 crude steel production per capita as approximation for demand as no data available

Sources: WSA for crude steel ASC; Global Insight and UN Data statistics for population; ArcelorMittal Corporate Strategy team analysis

0

5000

10000

15000

20000

25000

30000

35000

40000

1905

1910

1915

1920

1925

1930

1935

1940

1945

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

China

S. Korea

France

Germany

USA

Cumulative crude steel apparent consumption (kg/capita)

34 Sources: NBS, Mysteel, local governments‟ 12th 5-year plans, ArcelorMittal Corporate Strategy

0

100

200

300

400

500

600

700

800

900

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

East

North

South

Southwest

Northeast

Northwest

• China steel growth shifting from East/North to South/Southwest

China‟s steel demand growth is expected to be sustained

China steel demand growth will continue

Apparent steel consumption (million tonnes)

Demand projections

35 35

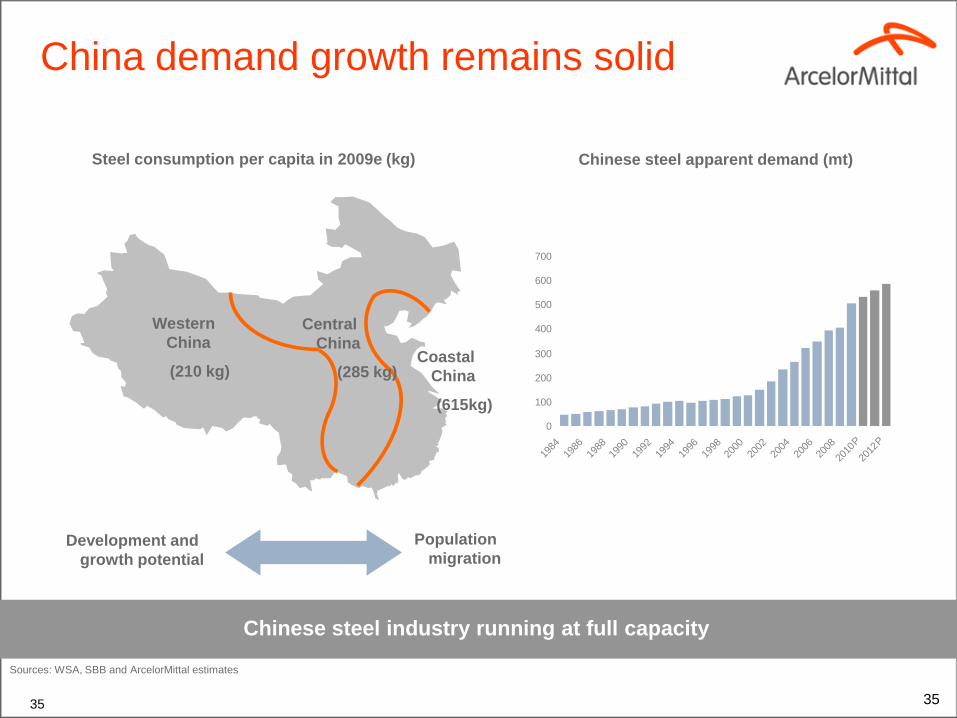

Chinese steel industry running at full capacity

Sources: WSA, SBB and ArcelorMittal estimates

Steel consumption per capita in 2009e (kg)

Western

China

(210 kg) Coastal

China

(615kg)

Central

China

(285 kg)

Development and

growth potential

Population

migration

Chinese steel apparent demand (mt)

China demand growth remains solid

0

100

200

300

400

500

600

700

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

P

2012

P

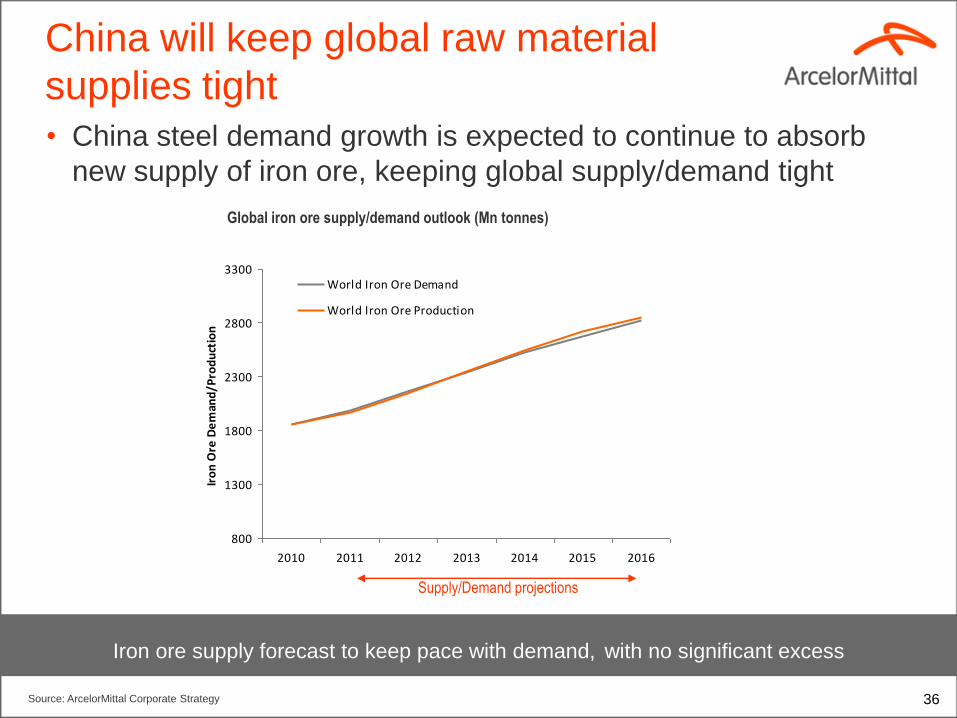

36 Source: ArcelorMittal Corporate Strategy

• China steel demand growth is expected to continue to absorb

new supply of iron ore, keeping global supply/demand tight

Iron ore supply forecast to keep pace with demand, with no significant excess

China will keep global raw material

supplies tight

Global iron ore supply/demand outlook (Mn tonnes)

800

1300

1800

2300

2800

3300

2010 2011 2012 2013 2014 2015 2016

Iro

n O

re D

em

and

/Pro

du

ctio

n

World Iron Ore Demand

World Iron Ore Production

Supply/Demand projections

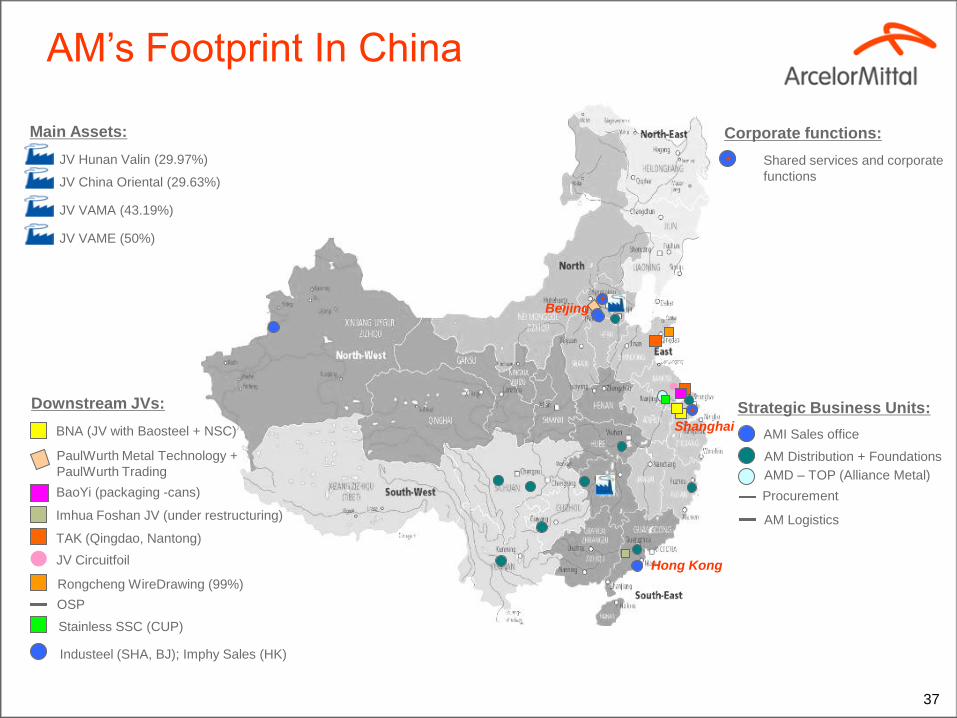

37

Beijing

Hong Kong

Shanghai

Main Assets:

JV Hunan Valin (29.97%)

JV China Oriental (29.63%)

JV VAMA (43.19%)

JV VAME (50%)

Corporate functions:

Strategic Business Units:

AMI Sales office

AMD – TOP (Alliance Metal)

PaulWurth Metal Technology +

PaulWurth Trading

Imhua Foshan JV (under restructuring)

BaoYi (packaging -cans)

TAK (Qingdao, Nantong)

OSP

BNA (JV with Baosteel + NSC)

Downstream JVs:

JV Circuitfoil

Rongcheng WireDrawing (99%)

Stainless SSC (CUP)

Industeel (SHA, BJ); Imphy Sales (HK)

AM Distribution + Foundations

Procurement

AM Logistics

AM‟s Footprint In China

Shared services and corporate

functions

38

102

450400

60

India Other

developing

world

China Developed

World*

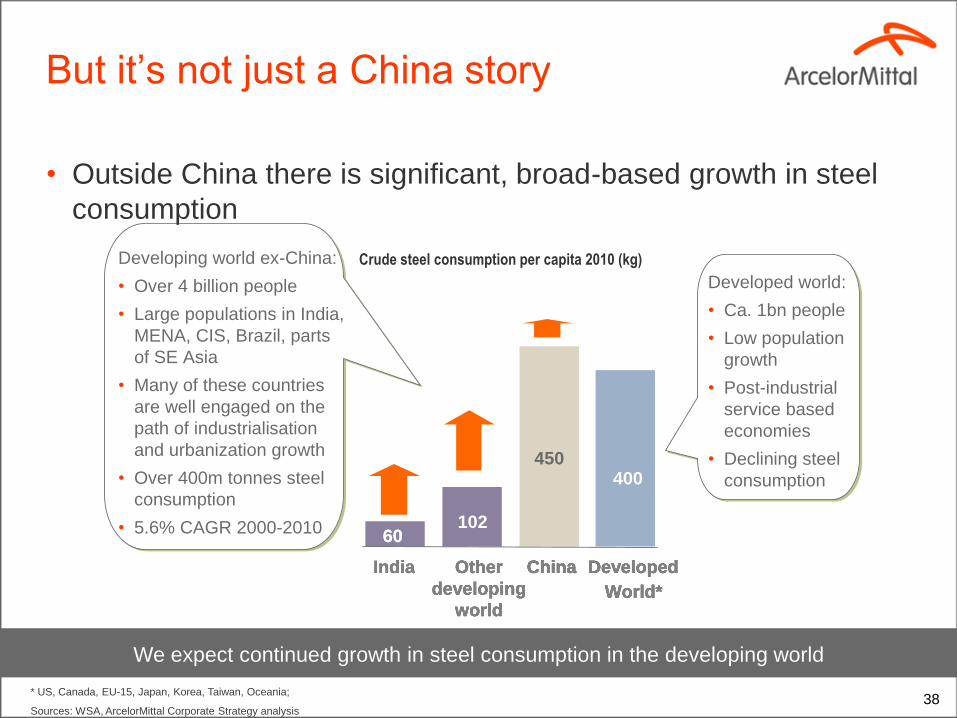

Developing world ex-China:

• Over 4 billion people

• Large populations in India,

MENA, CIS, Brazil, parts

of SE Asia

• Many of these countries

are well engaged on the

path of industrialisation

and urbanization growth

• Over 400m tonnes steel

consumption

• 5.6% CAGR 2000-2010

Developed world:

• Ca. 1bn people

• Low population

growth

• Post-industrial

service based

economies

• Declining steel

consumption

China Developed

World*

Other

developing

world

China Developed

World*

India Other

developing

world

China Developed

World*

60

India Other

developing

world

China Developed

World*

* US, Canada, EU-15, Japan, Korea, Taiwan, Oceania;

Sources: WSA, ArcelorMittal Corporate Strategy analysis

But it‟s not just a China story

• Outside China there is significant, broad-based growth in steel

consumption

Crude steel consumption per capita 2010 (kg)

We expect continued growth in steel consumption in the developing world

39

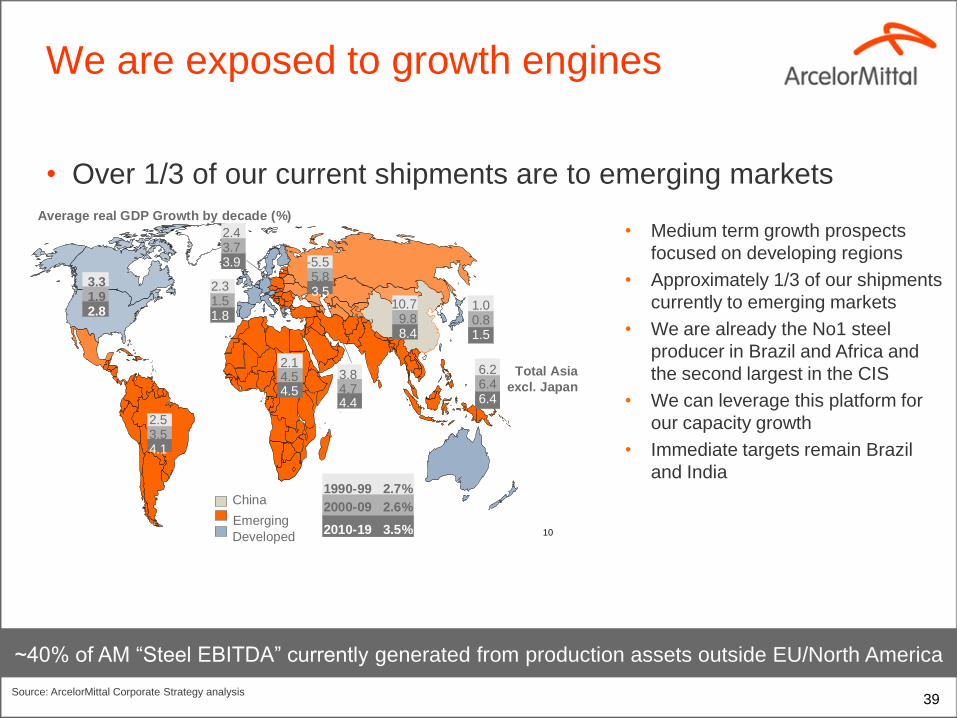

We are exposed to growth engines

• Over 1/3 of our current shipments are to emerging markets

10

Source: Global Insight

Average real GDP Growth by decade (%)

2.31.51.8

3.31.92.8 1.0

0.81.5

10.79.88.4

2.14.54.5

2.43.73.9 -5.5

5.83.5

3.84.74.4

6.26.46.4

2.53.54.1

Total Asia

excl. Japan

1990-99 2.7%

2000-09 2.6%

2010-19 3.5%

China

Emerging

Developed

Global medium term prospects centred on

growth in the developing regions

• Medium term growth prospects

focused on developing regions

• Approximately 1/3 of our shipments

currently to emerging markets

• We are already the No1 steel

producer in Brazil and Africa and

the second largest in the CIS

• We can leverage this platform for

our capacity growth

• Immediate targets remain Brazil

and India

~40% of AM “Steel EBITDA” currently generated from production assets outside EU/North America

Source: ArcelorMittal Corporate Strategy analysis

40

High capex will constrain supply growth

• Returns on greenfield steel capex are unattractive

Margins need to improve before new capacity is justified outside China

0

200

400

600

800

1000

1200

1400

Greenfield Brownfield

Typical capex per tonne for HRC (US$/t) – Capacity growth in developed

world constrained by

environmental considerations

– Beyond China, capacity growth in

developing world is not keeping

pace with demand growth

– Typical greenfield capacity would

require an EBITDA/t margin of

~$250/t to deliver a 15% post-

tax* return on investment

Source: ArcelorMittal Corporate Strategy analysis; *Note assumes a tax rate of 30%

41

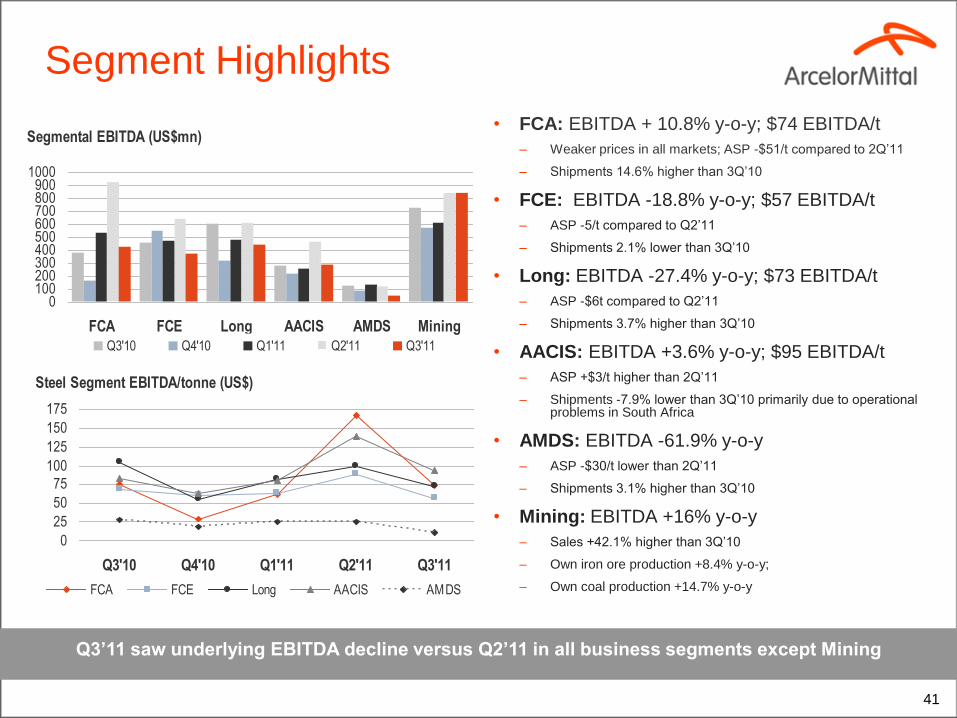

Segment Highlights

Q3’11 saw underlying EBITDA decline versus Q2’11 in all business segments except Mining

• FCA: EBITDA + 10.8% y-o-y; $74 EBITDA/t

– Weaker prices in all markets; ASP -$51/t compared to 2Q‟11

– Shipments 14.6% higher than 3Q‟10

• FCE: EBITDA -18.8% y-o-y; $57 EBITDA/t

– ASP -5/t compared to Q2‟11

– Shipments 2.1% lower than 3Q‟10

• Long: EBITDA -27.4% y-o-y; $73 EBITDA/t

– ASP -$6t compared to Q2‟11

– Shipments 3.7% higher than 3Q‟10

• AACIS: EBITDA +3.6% y-o-y; $95 EBITDA/t

– ASP +$3/t higher than 2Q‟11

– Shipments -7.9% lower than 3Q‟10 primarily due to operational problems in South Africa

• AMDS: EBITDA -61.9% y-o-y

– ASP -$30/t lower than 2Q‟11

– Shipments 3.1% higher than 3Q‟10

• Mining: EBITDA +16% y-o-y

– Sales +42.1% higher than 3Q‟10

– Own iron ore production +8.4% y-o-y;

– Own coal production +14.7% y-o-y

Segmental EBITDA (US$mn)

0100200300400500600700800900

1000

FCA FCE Long AACIS AMDS Mining

Q3'10 Q4'10 Q1'11 Q2'11 Q3'11

Steel Segment EBITDA/tonne (US$)

0

25

50

75

100

125

150

175

Q3'10 Q4'10 Q1'11 Q2'11 Q3'11

FCA FCE Long AACIS AMDS

42

Contacts

Daniel Fairclough – Global Head Investor Relations

+44 207 543 1105

Hetal Patel – UK/European Investor Relations

+44 207 543 1128

Valérie Mella – Investor Relations

+44 207 543 1156

Maureen Baker – Fixed Income/Debt Investor Relations

+33 1 71 92 10 26

Steve John – SRI Relations

+44 203 214 2854

Thomas A McCue – US Investor Relations

+312-899-3927

Lisa Fortuna – US Investor Relations

+312-899-3985