monthly state of the market report - spp.org msom report 201003.pdf · spp market monitoring unit...

TRANSCRIPT

Monthly State of the Market

Report

March 2010

published April 15, 2010

produced by SPP Market Monitoring Unit

Copyright © 2009 by Southwest Power Pool, Inc. All rights reserved.

SPP Market Monitoring Unit

Monthly State of the Market Report 2 March 2010

Table of Contents

Executive Summary .............................................................................................................................................. 3

Figures .................................................................................................................................................................... 4

Figure 1 – SPP EIS Price Contour Map ................................................................................................... 4

Figure 2 – Congestion by Shadow Price Impact – March 2010 ............................................................... 5

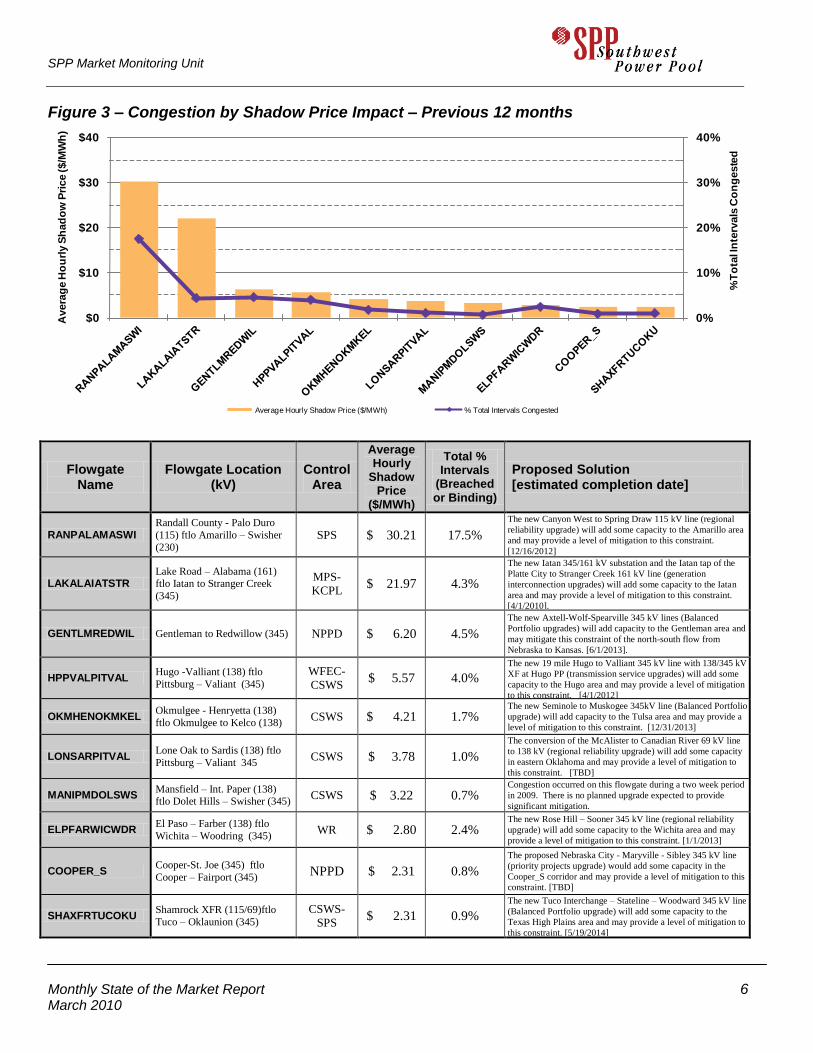

Figure 3 – Congestion by Shadow Price Impact – Previous 12 months .................................................. 6

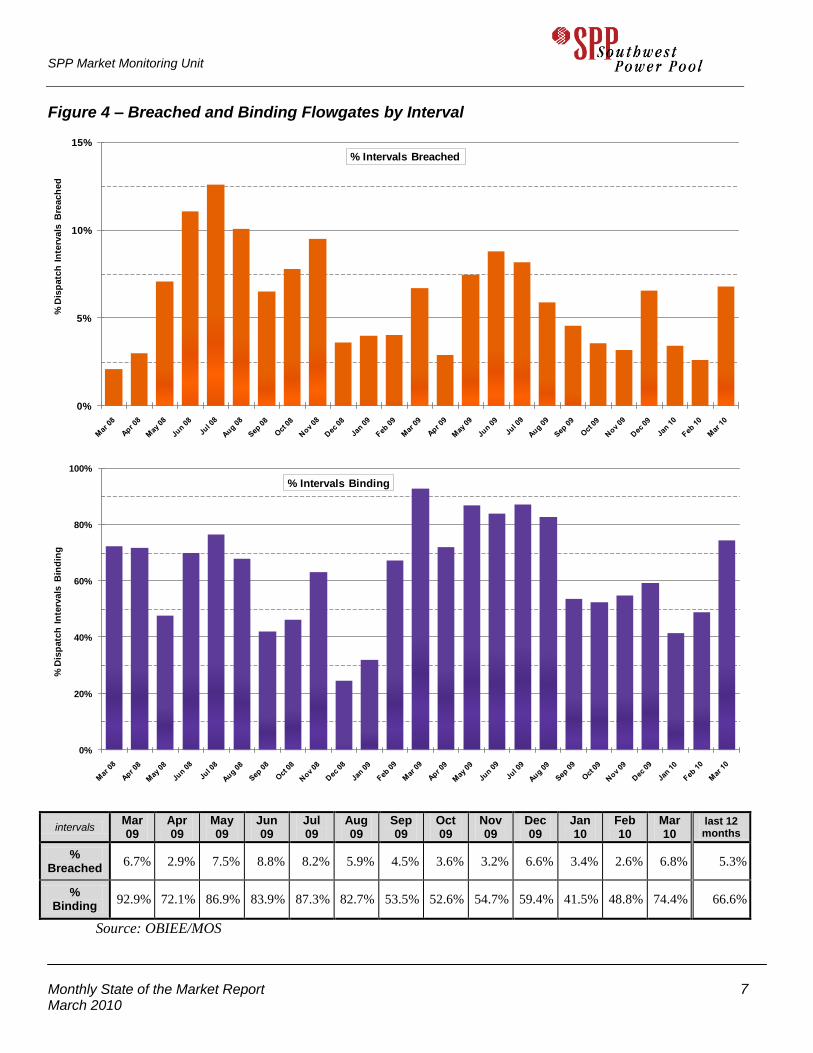

Figure 4 – Breached and Binding Flowgates by Interval ......................................................................... 7

Figure 5 – LIP / Gas Cost Comparison .................................................................................................... 8

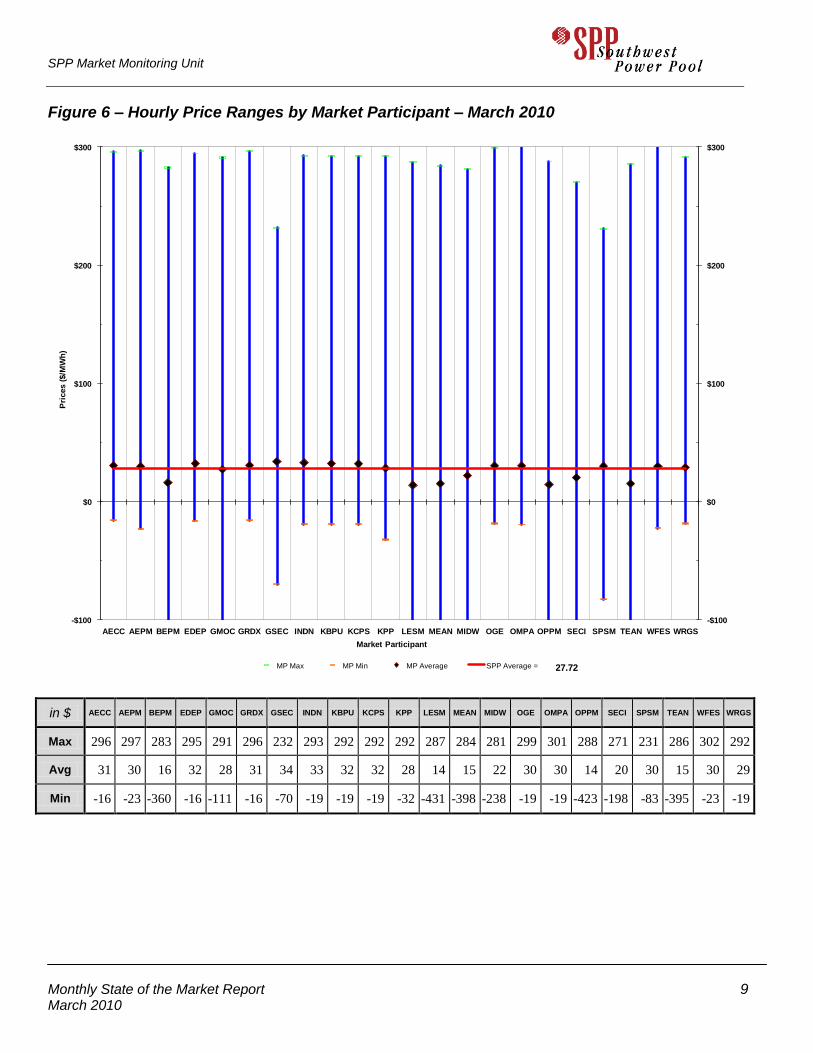

Figure 6 – Hourly Price Ranges by Market Participant – March 2010 .................................................... 9

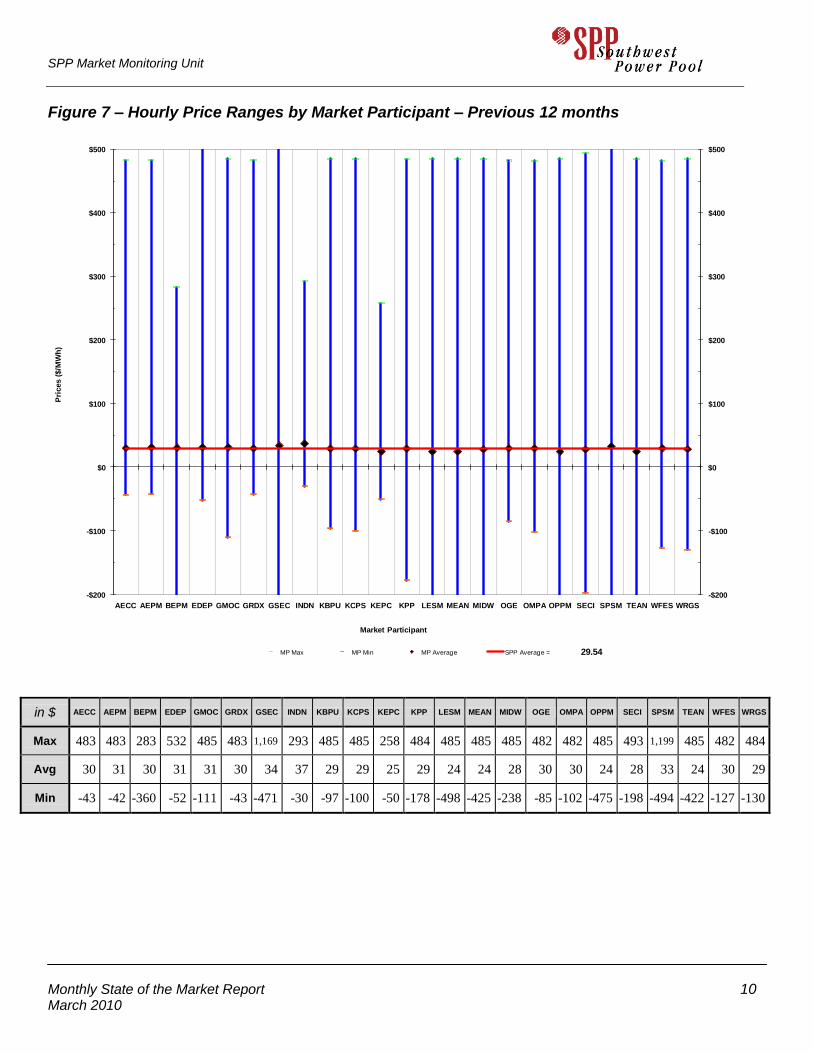

Figure 7 – Hourly Price Ranges by Market Participant – Previous 12 months ..................................... 10

Figure 8 – Regional Monthly Prices ...................................................................................................... 11

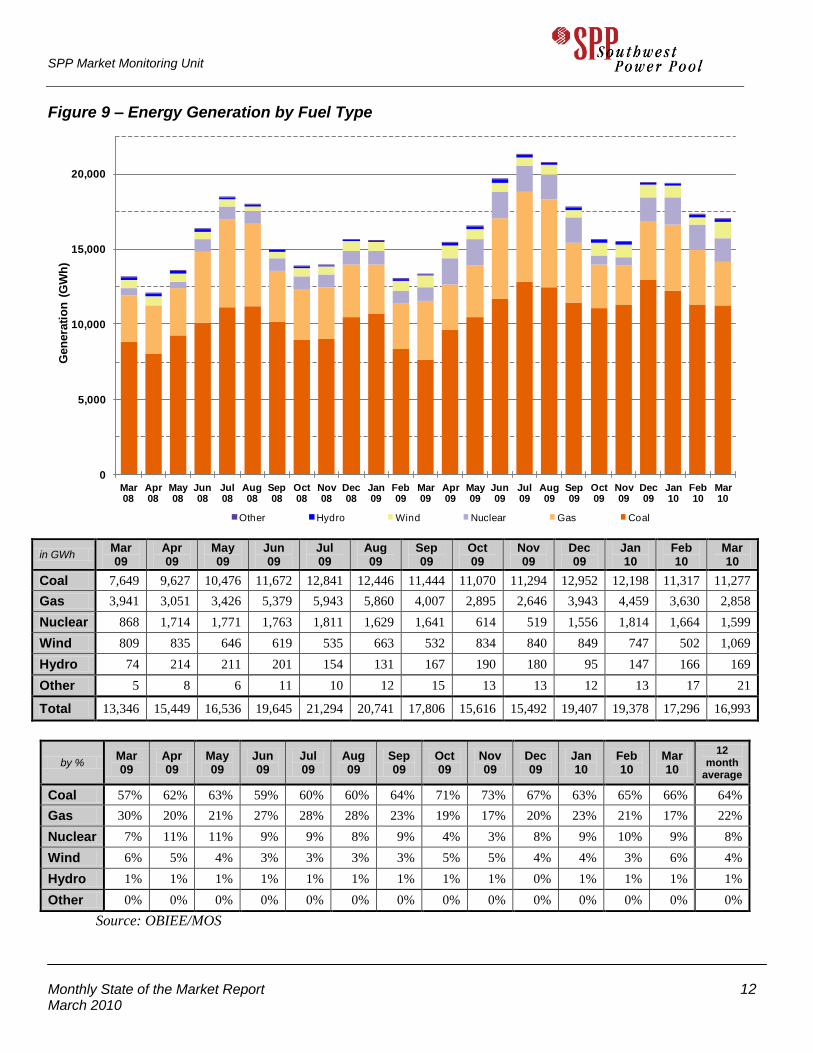

Figure 9 – Energy Generation by Fuel Type .......................................................................................... 12

Figure 10 – Wind Generation & Capacity ............................................................................................. 13

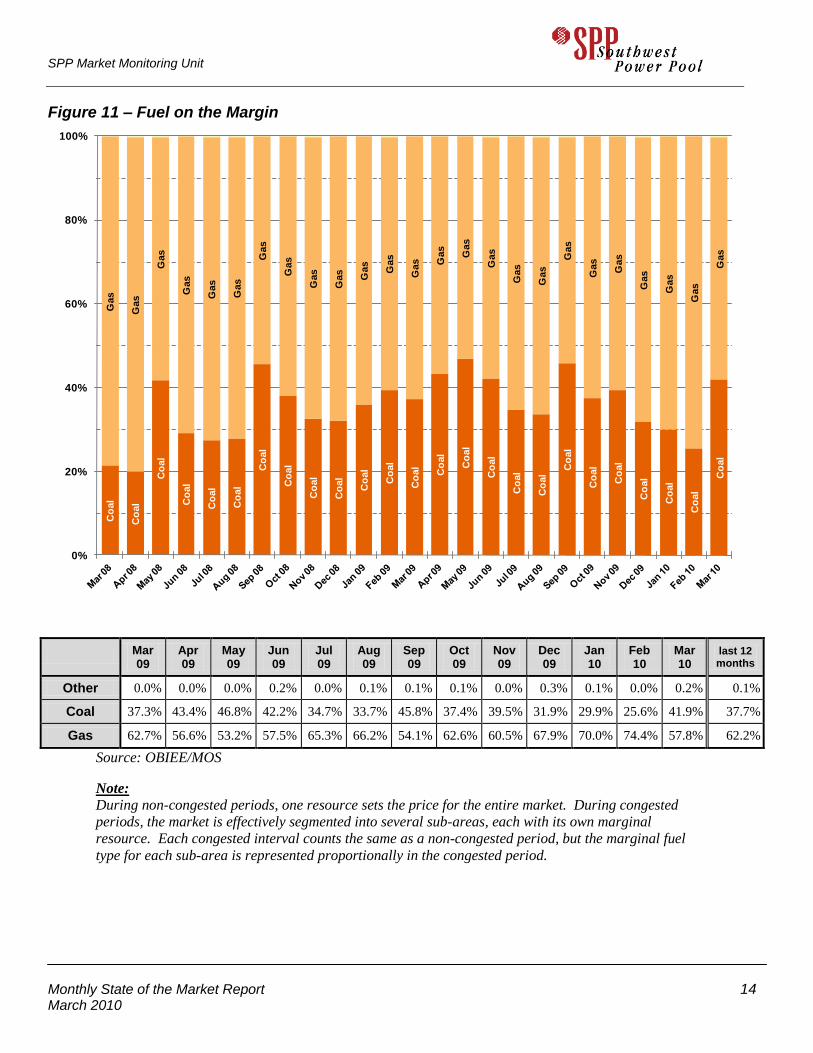

Figure 11 – Fuel on the Margin .............................................................................................................. 14

Figure 12 – EIS Settlements - GWh ....................................................................................................... 15

Figure 13 – EIS Settlements - $ ............................................................................................................. 16

Figure 14 – Depth of Energy Market for Resources Only – by Status .................................................. 17

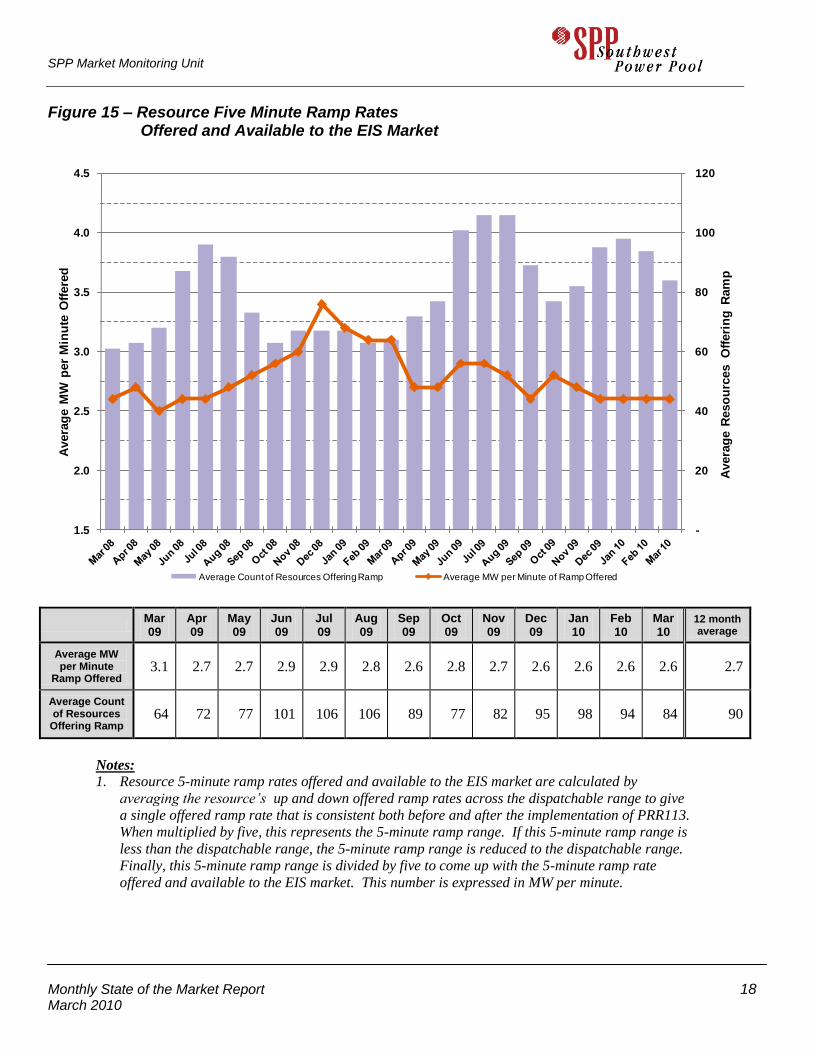

Figure 15 – Resource Five Minute Ramp Rates .................................................................................... 18

Figure 16 – Monthly Summary of Market Ramp Rate Deficiency ........................................................ 19

Figure 17 – Dispatchable Range ............................................................................................................ 20

Figure 18 – Transmission Owner Revenue ............................................................................................ 21

Figure 19 – Average Transmission Reservations and Schedules ........................................................... 22

Figure 20 – RNU Components ............................................................................................................... 23

Disclaimer

The data and analysis in this report are provided for informational purposes only and shall not be considered or relied upon as market advice or market settlement data. The Southwest Power Pool Market Monitoring Unit (SPP MMU) makes no representation or warranties of any kind, express or implied, with respect to the accuracy or adequacy of the information contained herein. The SPP MMU shall have no liability to recipients of this information or third parties for the consequences arising from errors or discrepancies in this information, or for any claim, loss or damage of any kind or nature whatsoever arising out of or in connection with (i) the deficiency or inadequacy of this information for any purpose, whether or not known or disclosed to the authors, (ii) any error or discrepancy in this information, (iii) the use of this information, or (iv) a loss of business or other consequential loss or damage whether or not resulting from any of the foregoing

SPP Market Monitoring Unit

Monthly State of the Market Report 3 March 2010

Executive Summary

Prices in the Southwest Power Pool (SPP) Energy Imbalance Services (EIS) market averaged

$27.72/MWh for March 2010, a decrease of $12.84 (32%) in the last month. As observed previously,

SPP EIS prices follow closely with spot gas prices. Figure 5 shows this correlation quite vividly, showing

the EIS price of electricity with the price of spot gas at the Panhandle hub. This month’s EIS price is

comparable to the $27.38 price one year ago in March 2009. SPP prices follow similar trends in MISO

and ERCOT as shown in Figure 8.

Although the average price was low in March 2010, several market participants experienced extremely

high price volatility. Almost all market participants experienced a highest hourly price between $280-

$300. However, a handful of participants experienced a lowest hourly price of around -$300. Although

total price volatility for SPP was 60% (Figure 8), those market participants with the largest spread in their

high and low prices saw their price volatility for March exceed 300%.

Congestion increased somewhat in March as shown in the average shadow price of our top two flowgates

in Figure 2. This congestion can be seen as price separation in the Texas panhandle and in northwestern

Missouri in Figure 1. Congestion tends to limit the general flow of electricity from north to south.

March saw an all-time high in wind production. This is evident in the sharp increase shown in Figure 10.

March and April are the traditional windy months, but March 2010 represents a 32% increase in wind

production from March 2009, a period when wind capacity increased by only 21%. This increase in wind

production tends to displace production from gas, accounting for a greater amount of coal on the margin

as seen in Figure 11.

Participation in the EIS market is reflected in three metrics (resource status, available ramp and

dispatchable range), seen in Figures 14, 15, and 17. Figure 14 shows that the percentage of energy

produced under market dispatch is at 76%, just below the 12-month average of 77%. Resource ramp rate

is 2.6 MW per minute on Figure 15, just below the 12-month average of 2.7 MW per minute. The

dispatchable range is at 42.17% on Figure 17, just shy of the all-time low, which was set last month. The

low level of offered dispatchable range is the most troubling trend identified in the current set of market

metrics.

SPP Market Monitoring Unit

Monthly State of the Market Report 4 March 2010

Figures

Figure 1 – SPP EIS Price Contour Map

March 2010

500 kV

345 kV

230 kV

161 kV

138 kV

115 kV

69 kV

12 Month EIS Price Contour Map

500 kV

345 kV

230 kV

161 kV

138 kV

115 kV

69 kV

SPP Market Monitoring Unit

Monthly State of the Market Report 5 March 2010

Figure 2 – Congestion by Shadow Price Impact – March 2010

0%

20%

40%

60%

80%

$0

$20

$40

$60

$80

%T

ota

l In

terv

als

Co

ng

este

d

Avera

ge H

ou

rly S

had

ow

Pri

ce

($/M

Wh

)

Average Hourly Shadow Price ($/MWh) % Total Intervals Congested

Flowgate Name Flowgate Location

(kV) Control

Area

Average Hourly

Shadow Price

($/MWh)

Total % Intervals

(Breached or Binding)

Detailed Description

TEMP01_15940 Osage Switch - Canyon East

(115) ftlo Bushland - Deaf

Smith (230) SPS $ 76.45 39.6%

First flowgate to run into North – South flow in

Panhandle of Texas. EAST of 345 kV from SECI..

Max Gen. = 7000, Max Load = 5300 MW.

RANPALAMASWI Randall County - Palo Duro (115) ftlo Amarillo –

Swisher (230) SPS $ 75.95 30.2%

First flowgate to run into North – South flow in Panhandle of Texas. WEST of 345 kV from SECI..

Max Gen. = 7000, Max Load = 5300 MW.

TEMP25_16260 Lake Road – Alabama (161)

ftlo St. Joe - Hawthorn (345)

MPS-

KCPL $ 38.79 7.0%

External impacts mainly from MISO quickly load up

flowgates TEMP_25, LAKALAIATSTR,

SJHALKNAIASC, and COOPER_S causing multiple

violations of SPP flowgates. The SPP Market was unable to absorb the increase of external impacts

quickly enough. Relief came from MISO Market, SPP

Market, and non-firm curtailments. High positive LIPs around LAKALAIATSTR at the same time high

negative LIPs around COOPER_S.

LAKALAIATSTR Lake Road – Alabama (161)

ftlo Iatan to Stranger Creek (345)

MPS-

KCPL $ 30.05 7.0%

SJHALKNAIASC St. Joe – Hawthorn(345)

Lake Road Nashua(161) ftlo

Iatan – Stranger Creek (345)

MPS-

KCPL $ 16.48 7.5%

TEMP26_16045 Neosho – Columbus (161) ftlo Neosho – Delaware

(345) CSWS $ 13.70 7.3%

Decreases in generation in southwest Missouri cause loading in this line. Congestion was mostly confined to

a two day period at the end of March.

COOPER_S Cooper-St. Joe (345) ftlo Cooper – Fairport (345)

NPPD $ 12.32 3.6% See explanation for TEMP25_16260, LAKALAIATSTR and SJHALKNAIASC above.

TEMP24_16244 Circ - Reno (115) ftlo

Empec - Wich (345)

MIDW-

SECI $ 9.54 5.0%

High wind generation in West Kansas. About 1000 MW

wind coming from SECI along with generation outage. Unable to provide for counter flow.

SHAXFRTUCOKU Shamrock XFR (115/69)ftlo Tuco – Oklaunion (345)

CSWS-

SPS $ 7.69 2.5%

Higher loading due to transformer outage nearby. Low

voltages in the Shamrock area if Tuco – Oklaunion 345

kV is lost.

TEMP20_16147 Neosho – Columbus (161) ftlo Neosho – Oneta (345)

CSWS $ 5.29 3.0% See TEMP26_16045.

SPP Market Monitoring Unit

Monthly State of the Market Report 6 March 2010

Figure 3 – Congestion by Shadow Price Impact – Previous 12 months

0%

10%

20%

30%

40%

$0

$10

$20

$30

$40

%T

ota

l In

terv

als

Co

ng

este

d

Avera

ge H

ou

rly S

had

ow

Pri

ce ($/M

Wh

)

Average Hourly Shadow Price ($/MWh) % Total Intervals Congested

Flowgate Name

Flowgate Location (kV)

Control Area

Average Hourly

Shadow Price

($/MWh)

Total % Intervals

(Breached or Binding)

Proposed Solution [estimated completion date]

RANPALAMASWI Randall County - Palo Duro

(115) ftlo Amarillo – Swisher

(230) SPS $ 30.21 17.5%

The new Canyon West to Spring Draw 115 kV line (regional

reliability upgrade) will add some capacity to the Amarillo area

and may provide a level of mitigation to this constraint.

[12/16/2012]

LAKALAIATSTR Lake Road – Alabama (161)

ftlo Iatan to Stranger Creek

(345)

MPS-

KCPL $ 21.97 4.3%

The new Iatan 345/161 kV substation and the Iatan tap of the

Platte City to Stranger Creek 161 kV line (generation

interconnection upgrades) will add some capacity to the Iatan

area and may provide a level of mitigation to this constraint.

[4/1/2010].

GENTLMREDWIL Gentleman to Redwillow (345) NPPD $ 6.20 4.5%

The new Axtell-Wolf-Spearville 345 kV lines (Balanced

Portfolio upgrades) will add capacity to the Gentleman area and

may mitigate this constraint of the north-south flow from

Nebraska to Kansas. [6/1/2013].

HPPVALPITVAL Hugo -Valliant (138) ftlo

Pittsburg – Valiant (345)

WFEC-

CSWS $ 5.57 4.0%

The new 19 mile Hugo to Valliant 345 kV line with 138/345 kV

XF at Hugo PP (transmission service upgrades) will add some

capacity to the Hugo area and may provide a level of mitigation

to this constraint. [4/1/2012]

OKMHENOKMKEL Okmulgee - Henryetta (138)

ftlo Okmulgee to Kelco (138) CSWS $ 4.21 1.7%

The new Seminole to Muskogee 345kV line (Balanced Portfolio

upgrade) will add capacity to the Tulsa area and may provide a

level of mitigation to this constraint. [12/31/2013]

LONSARPITVAL Lone Oak to Sardis (138) ftlo

Pittsburg – Valiant 345 CSWS $ 3.78 1.0%

The conversion of the McAlister to Canadian River 69 kV line

to 138 kV (regional reliability upgrade) will add some capacity

in eastern Oklahoma and may provide a level of mitigation to

this constraint. [TBD]

MANIPMDOLSWS Mansfield – Int. Paper (138) ftlo Dolet Hills – Swisher (345)

CSWS $ 3.22 0.7% Congestion occurred on this flowgate during a two week period

in 2009. There is no planned upgrade expected to provide

significant mitigation.

ELPFARWICWDR El Paso – Farber (138) ftlo

Wichita – Woodring (345) WR $ 2.80 2.4%

The new Rose Hill – Sooner 345 kV line (regional reliability

upgrade) will add some capacity to the Wichita area and may

provide a level of mitigation to this constraint. [1/1/2013]

COOPER_S Cooper-St. Joe (345) ftlo

Cooper – Fairport (345) NPPD $ 2.31 0.8%

The proposed Nebraska City - Maryville - Sibley 345 kV line

(priority projects upgrade) would add some capacity in the

Cooper_S corridor and may provide a level of mitigation to this

constraint. [TBD]

SHAXFRTUCOKU Shamrock XFR (115/69)ftlo

Tuco – Oklaunion (345)

CSWS-

SPS $ 2.31 0.9%

The new Tuco Interchange – Stateline – Woodward 345 kV line

(Balanced Portfolio upgrade) will add some capacity to the

Texas High Plains area and may provide a level of mitigation to

this constraint. [5/19/2014]

SPP Market Monitoring Unit

Monthly State of the Market Report 7 March 2010

Figure 4 – Breached and Binding Flowgates by Interval

0%

5%

10%

15%

% D

isp

atc

h I

nte

rvals

Bre

ach

ed

% Intervals Breached

0%

20%

40%

60%

80%

100%

% D

isp

atc

h I

nte

rvals

Bin

din

g

% Intervals Binding

intervals Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

last 12 months

% Breached

6.7% 2.9% 7.5% 8.8% 8.2% 5.9% 4.5% 3.6% 3.2% 6.6% 3.4% 2.6% 6.8% 5.3%

% Binding

92.9% 72.1% 86.9% 83.9% 87.3% 82.7% 53.5% 52.6% 54.7% 59.4% 41.5% 48.8% 74.4% 66.6%

Source: OBIEE/MOS

SPP Market Monitoring Unit

Monthly State of the Market Report 8 March 2010

Figure 5 – LIP / Gas Cost Comparison

$20

$30

$40

$50

$60

$70

$80

$2

$4

$6

$8

$10

$12

$14

Ele

ctr

icit

y P

rice (

LIP

)

Gas C

ost

Gas (Panhandle) Electricity (LIP)

Mar 09

Apr 09

May09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

12 month

average

Electricity (LIP)

[$/MWh] 27.38 22.21 23.67 25.83 27.77 25.73 23.27 29.91 28.29 37.86 42.18 40.56 27.72 29.54

Gas Panhandle [$/MMBtu]

2.60 2.72 3.05 2.82 3.07 2.96 2.88 3.99 3.48 5.21 5.72 5.22 4.17 3.77

SPP Market Monitoring Unit

Monthly State of the Market Report 9 March 2010

Figure 6 – Hourly Price Ranges by Market Participant – March 2010

27.72

-$100

$0

$100

$200

$300

AECC AEPM BEPM EDEP GMOC GRDX GSEC INDN KBPU KCPS KPP LESM MEAN MIDW OGE OMPA OPPM SECI SPSM TEAN WFES WRGS

-$100

$0

$100

$200

$300

Pri

ces (

$/M

Wh

)

Market Participant

MP Max MP Min MP Average SPP Average =

in $ AECC AEPM BEPM EDEP GMOC GRDX GSEC INDN KBPU KCPS KPP LESM MEAN MIDW OGE OMPA OPPM SECI SPSM TEAN WFES WRGS

Max 296 297 283 295 291 296 232 293 292 292 292 287 284 281 299 301 288 271 231 286 302 292

Avg 31 30 16 32 28 31 34 33 32 32 28 14 15 22 30 30 14 20 30 15 30 29

Min -16 -23 -360 -16 -111 -16 -70 -19 -19 -19 -32 -431 -398 -238 -19 -19 -423 -198 -83 -395 -23 -19

SPP Market Monitoring Unit

Monthly State of the Market Report 10 March 2010

Figure 7 – Hourly Price Ranges by Market Participant – Previous 12 months

29.54

-$200

-$100

$0

$100

$200

$300

$400

$500

AECC AEPM BEPM EDEP GMOC GRDX GSEC INDN KBPU KCPS KEPC KPP LESM MEAN MIDW OGE OMPA OPPM SECI SPSM TEAN WFES WRGS

-$200

-$100

$0

$100

$200

$300

$400

$500

Pri

ces (

$/M

Wh

)

Market Participant

MP Max MP Min MP Average SPP Average =

in $ AECC AEPM BEPM EDEP GMOC GRDX GSEC INDN KBPU KCPS KEPC KPP LESM MEAN MIDW OGE OMPA OPPM SECI SPSM TEAN WFES WRGS

Max 483 483 283 532 485 483 1,169 293 485 485 258 484 485 485 485 482 482 485 493 1,199 485 482 484

Avg 30 31 30 31 31 30 34 37 29 29 25 29 24 24 28 30 30 24 28 33 24 30 29

Min -43 -42 -360 -52 -111 -43 -471 -30 -97 -100 -50 -178 -498 -425 -238 -85 -102 -475 -198 -494 -422 -127 -130

SPP Market Monitoring Unit

Monthly State of the Market Report 11 March 2010

Figure 8 – Regional Monthly Prices

$0

$20

$40

Mar 09 Apr 09 May 09 Jun 09 Jul 09 Aug 09 Sep 09 Oct 09 Nov 09 Dec 09 Jan 10 Feb 10 Mar 10

$/M

Wh

SPP MISO ERCOT

Region Average

Price Maximum

Price Minimum

Price Volatility

Average On-Peak

Price

Average Off-Peak

Price

SPP $ 27.72 $ 285.85 $ -65.54 60% $ 33.09 $ 23.40

MISO $ 28.53 $ 135.86 $ -42.76 48% $ 33.25 $ 23.90

ERCOT $ 29.83 $ 457.13 $ -13.36 124% $ 29.25 $ 30.40

Note: This table is a “rough comparison” because of inherent differences in the structure of the three markets and also because of the differences in how prices for SPP, MISO, and ERCOT are calculated. For SPP, load weighted averages are used, while the data from MISO and ERCOT are not load weighted. Volatility is measured by the Coefficient of Variation, which is the standard deviation across all hours divided by the average of all hours.

0%

50%

100%

150%

200%

250%

Mar 09 Apr 09 May 09 Jun 09 Jul 09 Aug 09 Sep 09 Oct 09 Nov 09 Dec 09 Jan 10 Feb 10 Mar 10

Regional Price Volatility

SPP Volatility

MISO Volatility

ERCOT Volatility

SPP Market Monitoring Unit

Monthly State of the Market Report 12 March 2010

Figure 9 – Energy Generation by Fuel Type

0

5,000

10,000

15,000

20,000

Mar 08

Apr 08

May 08

Jun 08

Jul 08

Aug 08

Sep 08

Oct 08

Nov 08

Dec 08

Jan 09

Feb 09

Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

Gen

era

tio

n (

GW

h)

Other Hydro Wind Nuclear Gas Coal

in GWh Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

Coal 7,649 9,627 10,476 11,672 12,841 12,446 11,444 11,070 11,294 12,952 12,198 11,317 11,277

Gas 3,941 3,051 3,426 5,379 5,943 5,860 4,007 2,895 2,646 3,943 4,459 3,630 2,858

Nuclear 868 1,714 1,771 1,763 1,811 1,629 1,641 614 519 1,556 1,814 1,664 1,599

Wind 809 835 646 619 535 663 532 834 840 849 747 502 1,069

Hydro 74 214 211 201 154 131 167 190 180 95 147 166 169

Other 5 8 6 11 10 12 15 13 13 12 13 17 21

Total 13,346 15,449 16,536 19,645 21,294 20,741 17,806 15,616 15,492 19,407 19,378 17,296 16,993

by % Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

12 month

average

Coal 57% 62% 63% 59% 60% 60% 64% 71% 73% 67% 63% 65% 66% 64%

Gas 30% 20% 21% 27% 28% 28% 23% 19% 17% 20% 23% 21% 17% 22%

Nuclear 7% 11% 11% 9% 9% 8% 9% 4% 3% 8% 9% 10% 9% 8%

Wind 6% 5% 4% 3% 3% 3% 3% 5% 5% 4% 4% 3% 6% 4%

Hydro 1% 1% 1% 1% 1% 1% 1% 1% 1% 0% 1% 1% 1% 1%

Other 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

Source: OBIEE/MOS

SPP Market Monitoring Unit

Monthly State of the Market Report 13 March 2010

Figure 10 – Wind Generation & Capacity

0

500

1,000

1,500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Win

d G

en

era

tio

n (

GW

h)

Win

d C

ap

acit

y (M

W)

Wind Capacity (MW) Wind Generation (GWh)

Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

Capacity (MW)

2,743 2,917 2,933 2,939 2,939 3,040 3,103 3,202 3,202 3,313 3,313 3,313 3,313

Generation (GWh)

809 835 646 619 535 663 532 834 840 849 747 502 1,069

Capacity Factor

40% 40% 30% 29% 24% 29% 24% 35% 36% 34% 30% 23% 43%

# of Resources

38 42 45 46 46 47 48 49 49 51 51 51 51

Source: OBIEE/MOS

SPP Market Monitoring Unit

Monthly State of the Market Report 14 March 2010

Figure 11 – Fuel on the Margin C

oal

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Co

al

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas G

as

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas

Gas

0%

20%

40%

60%

80%

100%

Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

last 12 months

Other 0.0% 0.0% 0.0% 0.2% 0.0% 0.1% 0.1% 0.1% 0.0% 0.3% 0.1% 0.0% 0.2% 0.1%

Coal 37.3% 43.4% 46.8% 42.2% 34.7% 33.7% 45.8% 37.4% 39.5% 31.9% 29.9% 25.6% 41.9% 37.7%

Gas 62.7% 56.6% 53.2% 57.5% 65.3% 66.2% 54.1% 62.6% 60.5% 67.9% 70.0% 74.4% 57.8% 62.2%

Source: OBIEE/MOS

Note:

During non-congested periods, one resource sets the price for the entire market. During congested

periods, the market is effectively segmented into several sub-areas, each with its own marginal

resource. Each congested interval counts the same as a non-congested period, but the marginal fuel

type for each sub-area is represented proportionally in the congested period.

SPP Market Monitoring Unit

Monthly State of the Market Report 15 March 2010

Figure 12 – EIS Settlements - GWh

0%

5%

10%

15%

20%

0

10,000

20,000

30,000

40,000

EIS

Tra

nsacti

on

s a

s %

of

To

tal

GW

h

Scheduled Transactions (GWh) Load EI GWh Resource EI GWh % EIS Transactions

in GWh Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

Resource EI 2,396 3,204 3,327 3,691 3,293 2,875 2,541 2,333 2,483 2,840 2,805 2,159 2,565

Load EI 588 888 1,245 1,491 1,056 630 526 476 546 642 623 532 551

Scheduled Transaction

23,548 25,892 27,646 33,451 37,608 37,726 31,407 28,392 27,970 35,158 35,469 31,864 30,644

Total Energy 26,533 29,983 32,217 38,633 41,956 41,232 34,474 31,201 31,000 38,641 38,896 34,555 33,760

by % Mar 09

Apr 09

May09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov09

Dec 09

Jan 10

Feb 10

Mar 10

Last 12 Months

Resource EI 9.0% 10.7% 10.3% 9.6% 7.8% 7.0% 7.4% 7.5% 8.0% 7.3% 7.2% 6.2% 7.6% 8.0%

Load EI 2.2% 3.0% 3.9% 3.9% 2.5% 1.5% 1.5% 1.5% 1.8% 1.7% 1.6% 1.5% 1.6% 2.2%

Scheduled Transactions

88.8% 86.4% 85.8% 86.6% 89.6% 91.5% 91.1% 91.0% 90.2% 91.0% 91.2% 92.2% 90.8% 89.8%

Totals may not equal 100% due to rounding.

SPP Market Monitoring Unit

Monthly State of the Market Report 16 March 2010

Figure 13 – EIS Settlements - $

$0

$100

$200

$300

Mil

lio

ns

Resource EI Load EI

in million $ Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

12 Month Average

Resource EI 64 71 81 100 92 74 59 69 70 107 122 87 76 84

Load EI 17 20 32 41 31 17 13 15 16 26 28 23 17 23

Total EI 80 92 112 141 122 92 72 84 85 133 150 111 93 107

SPP Market Monitoring Unit

Monthly State of the Market Report 17 March 2010

Figure 14 – Depth of Energy Market for Resources Only – by Status

-

5,000

10,000

15,000

20,000

GW

h P

rod

ucti

on

Other Manual (other) Manual (intermittent) Nuclear Self-Dispatch Market Dispatch

in GWh Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

Market Dispatch

10,554 11,230 12,233 15,300 16,721 15,789 13,393 12,576 12,733 15,490 15,139 13,699 13,020

Self-Dispatch 580 648 851 719 984 1,636 1,173 741 534 470 407 336 399

Nuclear 875 1,720 1,769 1,764 1,817 1,633 1,639 614 514 1,561 1,832 1,675 1,614

Manual (intermittent)

854 926 684 697 615 705 587 894 922 898 833 573 1,175

Manual (other) 544 1,013 1,060 1,235 1,245 1,030 1,077 863 811 1,052 1,369 1,119 974

Other (6) (18) (13) 2 (6) 0 (12) (11) (6) 4 (2) (7) (9)

TOTAL 13,400 15,518 16,584 19,717 21,375 20,794 17,857 15,677 15,549 19,475 19,578 17,395 17,174

by % of total

Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

Last 12 Months

Market Dispatch 79% 72% 74% 78% 78% 76% 75% 80% 82% 80% 77% 79% 76% 77%

Self-Dispatch 4% 4% 5% 4% 5% 8% 7% 5% 3% 2% 2% 2% 2% 4%

Nuclear 7% 11% 11% 9% 9% 8% 9% 4% 3% 8% 9% 10% 9% 8%

Manual (intermittent) 6% 6% 4% 4% 3% 3% 3% 6% 6% 5% 4% 3% 7% 4%

Manual (other) 4% 7% 6% 6% 6% 5% 6% 6% 5% 5% 7% 6% 6% 6%

Other 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% 0%

Note: May not total to 100% due to rounding. Source: MOS

SPP Market Monitoring Unit

Monthly State of the Market Report 18 March 2010

Figure 15 – Resource Five Minute Ramp Rates

Offered and Available to the EIS Market

-

20

40

60

80

100

120

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Avera

ge R

eso

urc

es O

fferi

ng

Ram

p

Avera

ge M

W p

er

Min

ute

Off

ere

d

Average Count of Resources Offering Ramp Average MW per Minute of Ramp Offered

Mar 09

Apr 09

May09

Jun 09

Jul 09

Aug09

Sep09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

12 month average

Average MW per Minute

Ramp Offered 3.1 2.7 2.7 2.9 2.9 2.8 2.6 2.8 2.7 2.6 2.6 2.6 2.6 2.7

Average Count of Resources

Offering Ramp 64 72 77 101 106 106 89 77 82 95 98 94 84 90

Notes:

1. Resource 5-minute ramp rates offered and available to the EIS market are calculated by

averaging the resource’s up and down offered ramp rates across the dispatchable range to give

a single offered ramp rate that is consistent both before and after the implementation of PRR113.

When multiplied by five, this represents the 5-minute ramp range. If this 5-minute ramp range is

less than the dispatchable range, the 5-minute ramp range is reduced to the dispatchable range.

Finally, this 5-minute ramp range is divided by five to come up with the 5-minute ramp rate

offered and available to the EIS market. This number is expressed in MW per minute.

SPP Market Monitoring Unit

Monthly State of the Market Report 19 March 2010

Figure 16 – Monthly Summary of Market Ramp Rate Deficiency

-

40

80

120

160

200

240

280

320

360

-

20

40

60

80

MW

Ram

p A

vail

ab

le p

er

Min

ute

Ram

p D

efi

cie

ncy I

nte

rvals

UP Ramp Deficiency Intervals DOWN Ramp Deficiency Intervals Total MW Ramp Available per Minute

Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

12 month average

UP Ramp Deficiency Intervals

28 16 9 10 3 7 12 37 43 35 25 22 11 19

DOWN Ramp Deficiency Intervals

4 22 80 32 0 5 4 0 5 0 0 0 3 13

Total Ramp Deficiency Intervals

32 38 89 42 3 12 16 37 48 35 25 22 14 32

% of Total Market

Dispatch Intervals

0.4% 0.5% 1.0% 0.5% 0.0% 0.1% 0.1% 0.4% 0.5% 0.4% 0.3% 0.3% 0.1% 0.4%

MW Ramp Available per

Minute 198 195 208 293 307 300 231 216 221 247 255 244 218 244

SPP Market Monitoring Unit

Monthly State of the Market Report 20 March 2010

Figure 17 – Dispatchable Range

42%

46%

50%

Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

last 12 mo

Average 48.2% 44.9% 46.6% 46.8% 47.0% 46.4% 45.0% 42.8% 43.3% 43.5% 42.9% 42.3% 42.7% 44.5%

AdjMax = Resource Plan Max, adjusted for ancillary service.

AdjMin = Resource Plan Min, adjusted for ancillary service.

Dispatchable Range = (AdjMax – AdjMin) / AdjMax for a particular resource.

For example:

Resource A: AdjMax = 200, AdjMin = 100; (200 – 100) / 200 = 50% Range

Resource B: AdjMax = 200, AdjMin = 180; (200 – 180) / 200 = 10% Range

SPP Market Monitoring Unit

Monthly State of the Market Report 21 March 2010

Figure 18 – Transmission Owner Revenue

$0

$10

$20

$30

$40

$50

Mil

lio

ns

in millions $ JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

2008 32.1 34.6 33.1 33.0 32.9 32.1 32.6 33.8 37.7 34.7 35.0 36.3

2009 35.7 34.2 33.4 43.8 41.0 43.1 43.4 43.7 42.7 41.3 40.0 43.5

2010 44.7 43.9 46.6

SPP Market Monitoring Unit

Monthly State of the Market Report 22 March 2010

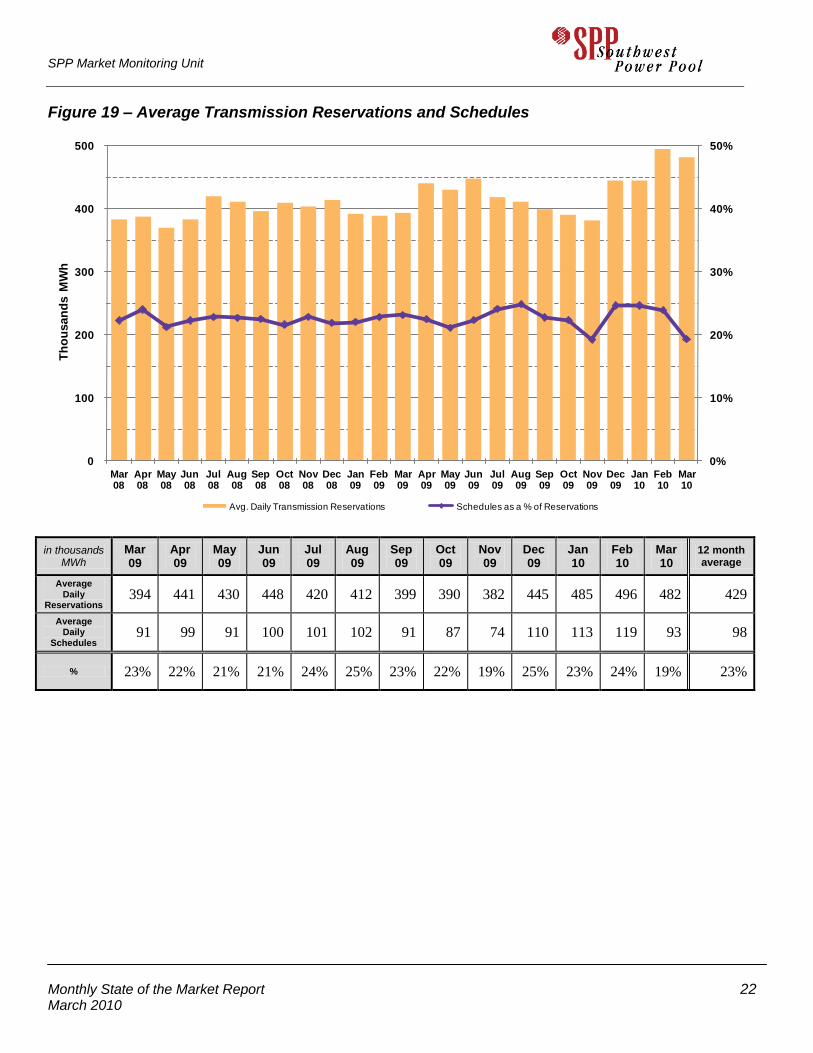

Figure 19 – Average Transmission Reservations and Schedules

0%

10%

20%

30%

40%

50%

0

100

200

300

400

500

Mar 08

Apr 08

May 08

Jun 08

Jul 08

Aug 08

Sep 08

Oct 08

Nov 08

Dec 08

Jan 09

Feb 09

Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

Th

ou

san

ds M

Wh

Avg. Daily Transmission Reservations Schedules as a % of Reservations

in thousands MWh

Mar 09

Apr 09

May09

Jun 09

Jul 09

Aug09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

12 month average

Average Daily

Reservations 394 441 430 448 420 412 399 390 382 445 485 496 482 429

Average Daily

Schedules 91 99 91 100 101 102 91 87 74 110 113 119 93 98

% 23% 22% 21% 21% 24% 25% 23% 22% 19% 25% 23% 24% 19% 23%

SPP Market Monitoring Unit

Monthly State of the Market Report 23 March 2010

Figure 20 – RNU Components

-$6

-$4

-$2

$0

$2

$4

Mil

lio

ns

SP LOSS UDC U/S O/S EIS Total RNU

$ (thousands) Mar 09

Apr 09

May 09

Jun 09

Jul 09

Aug 09

Sep 09

Oct 09

Nov 09

Dec 09

Jan 10

Feb 10

Mar 10

EIS 3,574 188 2,036 1,816 1,336 760 1,051 2,737 -245 -923 -1,166 1,347 589

O/S -139 -80 -147 -1,183 -164 -89 -71 -95 -99 -101 -45 -26 -96

U/S -645 -155 -886 -540 -259 -51 -41 -31 -177 -257 -91 -52 -78

UDC -79 -40 -61 -135 -134 -84 -64 -71 -56 -136 -138 -81 -35

SP Loss -33 0 -15 -21 -28 1 -7 -8 -2 -17 -5 -6 -3

Total RNU 2,678 -87 928 -63 752 538 869 2,531 -579 -1,434 -1,444 1,181 377

EIS (Energy Imbalance Charge/Credit) – All energy deviations between actual generation or load and schedules are settled as (EIS).

O/S (Over-Scheduling Charge) - During any hour, if Locational Imbalance Prices diverge and a Market Participant’s Load imbalance is more than 4% (but at least 2 MW) at an applicable Settlement Location in that hour, that MP may be subject to an Over-Scheduling Charge.

U/S (Under-Scheduling Charge) - During any hour, if Locational Imbalance Prices diverge and a Market Participant’s Load imbalance is more than 4% (but at least 2 MW) at an applicable Settlement Location in that hour, that MP may be subject to an Under-Scheduling Charge.

UDC (Uninstructed Resource Deviation) – the difference between the dispatch instructions and the actual performance of a Resource.

SP Loss - Self-Provided Losses