monitoring the monitor: distracted institutional investors ... · monitoring the monitor:...

TRANSCRIPT

Monitoring the Monitor: Distracted Institutional Investors and

Board Governance*

Claire Yang Liu

UNSW Business School

UNSW Australia

Angie Low

Nanyang Business School

Nanyang Technological University

Ron Masulis

UNSW Business School

UNSW Australia

Le Zhang

UNSW Business School

UNSW Australia

This Version: May 18, 2017

* We thank Chang-Mo Kang, E. Han Kim, Bo Li, Mark Humphrey-Jenner, Ji Yeol Jimmy Oh,

Paul Karehnke, Peter Pham, David Reeb, Rik Sen, Elvira Sojli, Buvaneshwaran Venugopal, Wing

Wah Tham, and Robert Tumarkin, as well as conference participants from the FIRN Annual Conference,

Conference on Asia-Pacific Financial Markets, Australasian Finance and Banking Conference, and seminar

participants at Georgia Institute of Technology and UNSW Australia for helpful comments.

Monitoring the Monitor: Distracted Institutional Investors and Board Governance

Abstract

While boards are crucial to shareholder wealth, the literature often overlooks how

continuous shareholder oversight can improve director incentives. Using exogenous

industry shocks in investors’ portfolio firms, we find that institutional investor distraction

weakens board oversight. Distracted institutions are less likely to use their votes to

discipline ineffective independent directors, and directors with poor voting outcomes are

less likely to turnover. As a result, directors have less monitoring incentives with

independent directors missing more meetings and boards holding fewer meetings. Board

structures are also compromised with the appointment of more ineffective independent

directors and lead. to worse governance outcomes such as greater earnings management,

higher excess CEO pay, and lower firm valuation. Our findings suggest that continuous

institutional investor attention represents an important determinant of board monitoring

incentives.

Keywords: Board of directors, Shareholder activism, Institutional investors, Board

monitoring, Shareholder voting, Corporate governance.

JEL classification: G23, G34.

1

1. Introduction

Large shareholders and the board of directors are two key corporate governance

mechanisms. Due to the legal and regulatory limits on the power of large shareholders in the

United States,1 the board of directors is generally considered to have a critical role in corporate

governance. The board serves as “gatekeeper” of all shareholder proposals to amend the charter

and also as the “approver” of almost all major corporate decisions. The board is also charged

with monitoring management, hiring and firing of CEOs, and setting executive compensation.

While the board is a powerful governance mechanism for monitoring managers,

director monitoring incentives do not appear to be particularly strong. This raises important

questions on how reliable are boards of directors in representing shareholder interests. What

motivates directors to monitor? Who monitors the board monitors? To address these questions,

we examine whether institutional investor monitoring on a regular basis improves board

incentives to exert greater effort in monitoring and motivating senior management.

Several recent studies report evidence that institutional investors in general improve

corporate decision making and thus, firm value.2 The existing literature tends to emphasize

shareholder actions during extreme events, e.g. proxy contests and lawsuits. However, those

actions are likely to serve as a weapon of last resort. Given the significant powers boards have

over major corporate decisions, it is more effective and less costly for shareholders to take

precautionary actions to monitor the board on a regular basis. Our study helps to further our

current understanding of director monitoring incentives, and how institutional investors

improve firm performance by continually monitoring the board.

1 In the U.S. shareholders cannot directly initiate business transactions or charter amendments, nor modify those

proposed by directors. In contrast, shareholders in the U.K., Japan, and France can force these decisions if the

proposals receive a majority vote (Hansmann and Kraakman, 2001). 2 For instance, Doidge, Dyck, Mahmudi and Virani (2015); Appel, Gormley and Keim (2016); Kempf, Manconi

and Spalt (2016); and Li, Liu, and Wu (2016).

2

Prior studies that go “behind-the-scenes” generally report evidence that institutional

investors actively intervene by engaging management and directors in active discussions.3 Less

is understood about whether such interventions result in improved director incentives and board

monitoring effectiveness. A board of directors is the only representative that shareholders have

in the firm who can make or approve major corporate decisions. Thus, the incentives of boards

to act in shareholder interests are very important in minimizing shareholder-manager agency

problems. Yet, it is unclear, whether the labour market for directors sufficiently punishes

poorly-performing directors (Fahlenbrach, Low, and Stulz, 2016).4 Furthermore, independent

directors generally have weak financial incentives to actively monitor a firm’s management on

a consistent basis (Yermack, 2004). Moreover, the existing governance literature documents

that certain types of directors are ineffective monitors. For example, independent directors who

are more socially dependent on the CEO, busy directors, non-domestic directors, co-opted

directors and possibly old directors tend to be less effective monitors.5 In the absence of

effective board monitoring, institutional investors can be exposed to severe agency problems

and experience significant losses. Thus, monitoring boards to ensure they perform their

fiduciary duties should be a critical channel through which outside investors seek to maximize

their returns on investments.

Several studies have argued that institutional investors may not actively intervene to

improve firm governance due to the classical free-rider problem as discussed in Grossman and

Hart (1980) and Shleifer and Vishny (1986). Furthermore, the threat of exit makes active

intervention less important as the potential stock price declines that result from exit may be a

3 See e.g. Becht et al. (2010); Carleton, Nelson, and Weisbach (1998); McCahery, Sautner, and Starks (2016). 4 Past literature on the directorial labor market impact of poor monitoring by directors mostly focuses on extreme

events such as earnings restatements (Srinivasan, 2005), financial fraud lawsuits (Fich and Shivdasani, 2007),

bankruptcies (Gilson, 1990), and option backdating (Ertimur, Ferri, and Maber, 2012). 5 See for example, Chidambaran, Kedia and Prabhala (2011), Coles, Daniel, and Naveen (2014), Falato,

Kadyrzhanova, and Lel (2014), Fich and Shivdasani (2006), Fracassi and Tate (2012), Hwang and Kim (2009)

(2012), Masulis and Mobbs (2014), and Nguyen (2012).

3

sufficient threat to motivate managers to work hard (Kahn and Winton, 1998; Maug, 1998).

Even if institutional investors actively intervene to change firm policies, it is unclear whether

shareholder monitoring and board monitoring are close substitutes for mitigating manager-

shareholder agency conflicts. Institutional shareholders can directly monitor management and

thus, obtain direct influence over major corporate decisions, which negates the need to

otherwise intervene in board governance. Also, activist institutional investors can join the

boards to directly effect changes (Gow, Shin, and Srinivasan, 2014) without the need to

influence monitoring by other board members. Thus, it is unclear whether institutions actively

intervene to affect board governance.

We construct an exogenous measure of institutional shareholder monitoring to test

whether institutional monitoring affects board monitoring incentives. Following Kempf,

Manconi, and Spalt (2016), we address such endogeneity concerns by utilizing exogenous

variations in institutional shareholder attention, caused by unrelated industry shocks to other

portfolio firms held by the institutional investors. We use these shocks to capture reductions in

the level of institutional shareholder monitoring. The following example illustrates how such

an exogenous shock to outside monitoring of the board can occur. Suppose a mutual fund

investor has two large stockholdings belonging to two unrelated industries, for example a bank

and a pharmaceutical firm. When the pharmaceutical industry is experiencing a large return

shock, the mutual fund manager needs to allocate more time and effort to monitor the

pharmaceutical firm. Assuming the attention and effort of a fund manager is in limited supply,

we expect the bank to receive less attention. Hence, this shock reduces a mutual fund manager’s

monitoring intensity of the bank.6 To the extent that these industry-level shocks to a fund’s

6 In a similar manner, Kacperczyk, Van Nieuwerburgh, and Veldkamp (2016) model how mutual fund managers,

due to their finite mental capacity, optimally choose to allocate their limited attention to different information

depending on the business cycle. Consistent with the idea of limited resources on the part of institutional investors,

in their survey of institutional investors, McCahery, Sautner, and Starks (2016) find that limited resources

(personnel) and “too many firms in our portfolio” rank as important impediments to shareholder activism.

4

portfolio firms are unrelated to the focal firm’s fundamentals, this measure captures the

exogenous variation in institutional investor monitoring intensity that is orthogonal to the focal

firm’s fundamentals.

Generalizing on the above example, we aggregate industry shocks using the weights of

the shocked industries in an institutional shareholder’s portfolio, to construct an investor-level

measure of exogenous distractions experienced by each institutional shareholder towards a

given firm in a given quarter. Next, we construct a focal firm-level investor distraction measure

by summing the distraction levels of all of its institutional investors. Kempf, Maconi, and Spalt

(2016) convincingly show that this distraction measure is negatively related to the amount of

attention institutional investors spend on monitoring a firm’s activities such as participating in

conference calls and initiating governance-related proposals.

To investigate whether investor distraction affects director incentives to monitor, we

first examine the voting behavior of institutional investors in director elections. Shareholder

voting in director elections represents one primary mechanism for institutional shareholders to

exert influence over a firm’s board and ultimately over its corporate decisions. While directors

rarely fail to be re-elected, except in proxy fights, experiencing disciplinary votes can be

embarrassing to a director and adversely affect her reputation and likelihood of being

renominated in the future (Aggarwal, Dahiya, and Prabhala, 2015). Therefore, shareholder

voting may motivate independent directors to act in shareholder interests due to these adverse

reputational impacts.

Using an investor-level measure of mutual fund distraction, we find that mutual funds

are less likely to discipline directors with negative votes when they are distracted.

Economically, a one standard deviation rise in a mutual fund investor’s distraction level is

associated with a fall in the likelihood that the investor withholds or votes against an

independent director candidate in the annual shareholder meeting by 3.3%. This effect is

5

stronger for problematic director candidates, defined as those who are busy directors, directors

socially linked to the CEO, and foreign directors.7 Such directors are shown in prior studies to

be ineffective monitors.

Next, we examine how the distraction by multiple institutional investors of a firm

affects director voting outcomes. We find that independent directors in general receive

significantly fewer disciplinary votes from institutional shareholders when these investors are

distracted. Economically, one standard deviation increase in investor distraction reduces the

likelihood of an independent director receiving poor vote results by almost 5%. Consistent with

our fund vote results, this effect is stronger for problematic director candidates. In addition, the

sensitivity of director departure to poor election vote results is also significantly lower when

institutional shareholders are distracted, consistent with weaker disciplinary effects of

shareholder votes.

Taken together, the voting results indicate that independent directors, especially

problematic ones, are significantly less likely to be disciplined by voting outcomes when

institutional shareholders are distracted. Next, we examine whether weakened board oversight

by institutional shareholders affects director monitoring incentives. We find that independent

directors miss more board meetings and boards hold fewer meetings when institutional

shareholders are distracted. For example, we find that one standard deviation rise in

institutional investor distractions is associated with an almost 16% rise in the likelihood of poor

director meeting attendance. Furthermore, institutional investor distraction leads to more

problematic independent directors on the board, due to the increased likelihood of a new

7 Endogeneity issues such as unobserved heterogeneity across mutual funds, directors, and firms are unlikely to

be driving our results. As our dataset comprises of the voting outcomes of each mutual fund for individual director

elections for each firm and each year, we exploit within-investor differences in monitoring intensity across their

different portfolio firms for each year by controlling for fund-year fixed effects. We also exploit within-election

proposal differences in monitoring intensity across the mutual funds voting on each election proposal by including

individual director election proposal fixed effects, which essentially accounts for time-varying director and firm

characteristics.

6

problematic director being appointed to the board and retention of existing problematic

directors. These findings suggest that the institutional investor monitoring has important

implications for director monitoring incentives and efforts.

Finally, we examine how the reduction in board monitoring efforts and incentives due

to investor distraction affects several governance outcomes. Firms with distracted investors

exhibit significantly greater earnings management, grant their CEOs higher compensation, but

with less performance-based incentives, and generally have lower equity valuation.

Importantly, the negative impact of investor distraction on these governance outcomes are

amplified in firms where problematic directors sit on key committees or where board

monitoring efforts are compromised. Taken together, our results suggest that institutional

shareholder distraction leads to significantly poorer board monitoring quality and

effectiveness.

Our study contributes to the literature on corporate governance in several ways. First,

we extend our understanding of what motivates independent directors to do their job well and

monitor management carefully. While it is well known that boards make important corporate

decisions which have economically large impacts on shareholder value, director incentives to

monitor managers are not well-understood. It is unclear why directors with limited financial

incentives are willing to exert sufficient effort to closely monitor managers (Yermack, 2004).

Fama and Jensen (1983) argue that director reputational concerns provide a strong motivation,

and recent studies show that reputational concerns affect director incentives to perform their

roles as effective monitors.8 We advance our understanding of director incentives by showing

that institutional investor oversight of boards significantly improves director incentives to exert

efforts in monitoring the senior management.

8 For instance, Jiang, Wan, and Zhao (2016); Masulis and Mobbs (2014); Levitt and Malenko (2016).

7

Second, our study furthers our understanding of how institutional investors intervene

to improve board governance and firm value. Existing studies that examine shareholder

interventions in corporate governance emphasize the actions of shareholder activists during

extreme events, including the use of proxy contests and law suits.9 However, evidence on

shareholder actions to improve board functioning on a regular basis is surprisingly scarce.10

We help fill this gap in the existing literature, and show that institutional investors use their

disciplinary votes to monitor and discipline directors on a regular basis. Our study also differs

substantially from Kempf, Manconi, and Spalt (2016) who show that firms are more likely to

undertake diversifying acquisitions and grant their CEOs opportunistically-timed equity grants

when institutional investors are distracted. Given that acquisitions and CEO pay are within the

board’s decision domain, we show that the underlying mechanism through which distracted

shareholders can impact firm policies is through board monitoring and consultations. In

particular, our study highlights the important role that institutional investors play in monitoring

the board. We show that reduced institutional investor monitoring leads to poorer board

effectiveness, in part due to independent directors reducing their own monitoring efforts in

response to reduced voting pressure, and in part due to poorly chosen board appointments.

Our study is also related to the literature that explores how corporate governance

mechanisms interact with each other. Existing evidence is mixed as to how governance

mechanisms interact (Agrawal and Knoeber, 1996; Cremers and Nair, 2005; Gillan, Hartzell,

and Starks, 2011), and it remains unclear whether the monitoring roles of the board and

9 See e.g., Brav et al. (2008) on hedge fund activism, Del Guercio and Hawkins (1999) on the impact of

shareholder proposals put forward by public pension funds, Doidge et al. (2016) on the activities of Canadian

Coalition for Good Governance, a formal collective action organization of institutional investors, Del Guercio,

Seery, and Woidtke (2008) on vote-no campaigns, Gillian and Starks (2000) on detailed analysis of shareholder

proposal voting outcomes. See also Gillian and Starks (2007), Denes, Karpoff, and McWilliams (2016) for

comprehensive reviews on shareholder activism. 10 Outside shareholders can submit Rule 14a-8 shareholder proposals relating to board independence and other

board issues but they are often ineffective in eliciting change (Gillian and Starks, 2007; Denes, Karpoff, and

McWilliams, 2016). Activist shareholders can also organize “just vote no” campaigns to withhold votes from

directors but Del Guercio, Seery, and Woidtke (2008) show that such campaigns often target at large, poorly

performing firms and are typically sponsored by public pension funds.

8

institutional shareholders are complements or substitutes. We contribute to this literature by

showing that the monitoring function of corporate boards, a key internal governance

mechanism, depends crucially on the effectiveness of institutional shareholder monitoring of

directors, which acts as a complementary governance mechanism.

Lastly, we contribute to the literature that examines the impact of institutional investor

monitoring on firm policies and governance outcomes. Monitoring by institutional investors is

found to have a positive impact on a firm’s governance indices, CEO compensation, mergers

and acquisitions profitability, firm risk-taking, and earnings management 11 However,

endogeneity makes it difficult to assess the causal dimension of these effects. For example,

Chung and Zhang (2011) conclude that the positive association between institutional

ownership and good governance structure is driven by institutional investors gravitating

towards firms with good governance so as to minimize their own monitoring costs. Recent

studies have used the annual reconstitution of the Russell 1000 and 2000 indexes as an

exogenous shock to examine how changes in passive institutional ownership affect firm

governance and policies.12 Our study differs from theirs in that we focus on how institutional

shareholder monitoring intensity affects board governance as a crucial internal governance

mechanism. Additionally, we examine a wide range of institutional investor classes, not just

passive index investors.

11 Examples include: Hartzell and Starks (2003), Aggarwal et al. (2011), Chen, Harford, and Li (2007), Cornett,

Marcus, Tehranian (2008), Aghion, Van Reenen, and Zingales (2013), and Kim and Lu (2011). 12 Appel, Gormley, and Keim (2016) find that an increase in passive institutional ownership increases board

independence while Schmidt and Fahlenbrach (2016) find no change in board independence and appointments of

independent directors are met with worse announcement returns when passive institutional ownership increases.

9

2. Variable Construction, Data, and Descriptive Statistics

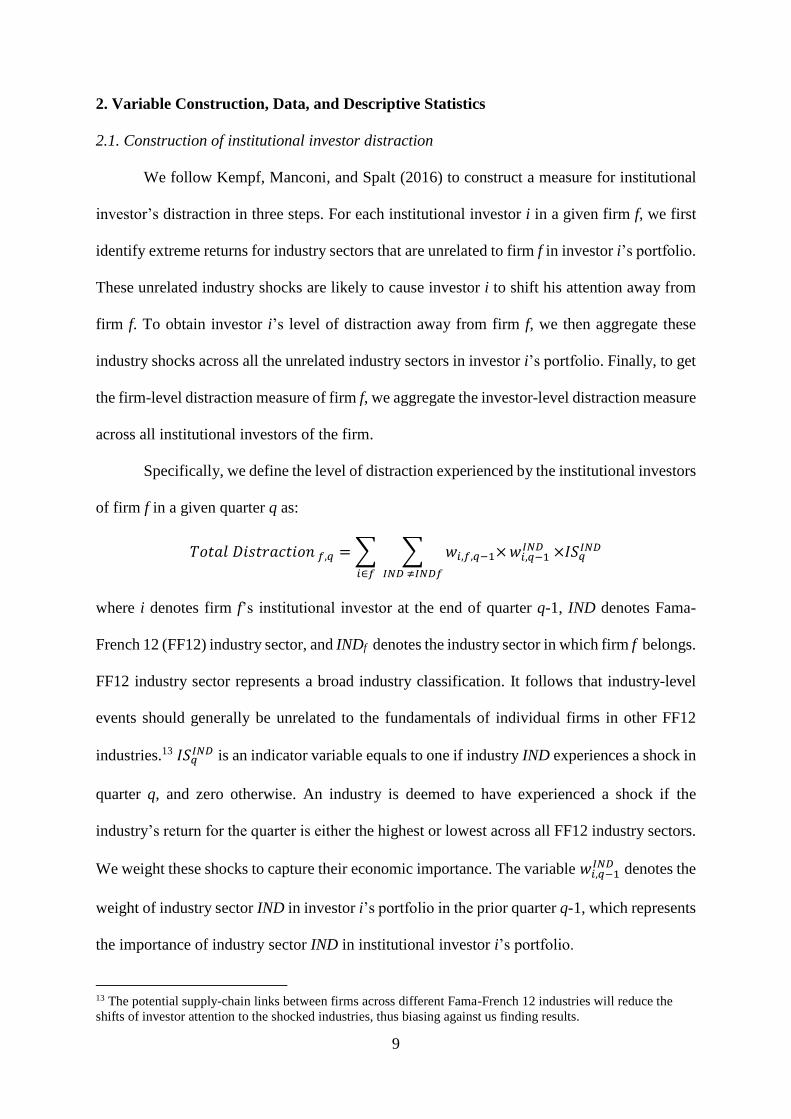

2.1. Construction of institutional investor distraction

We follow Kempf, Manconi, and Spalt (2016) to construct a measure for institutional

investor’s distraction in three steps. For each institutional investor i in a given firm f, we first

identify extreme returns for industry sectors that are unrelated to firm f in investor i’s portfolio.

These unrelated industry shocks are likely to cause investor i to shift his attention away from

firm f. To obtain investor i’s level of distraction away from firm f, we then aggregate these

industry shocks across all the unrelated industry sectors in investor i’s portfolio. Finally, to get

the firm-level distraction measure of firm f, we aggregate the investor-level distraction measure

across all institutional investors of the firm.

Specifically, we define the level of distraction experienced by the institutional investors

of firm f in a given quarter q as:

𝑇𝑜𝑡𝑎𝑙 𝐷𝑖𝑠𝑡𝑟𝑎𝑐𝑡𝑖𝑜𝑛 𝑓,𝑞 = ∑ ∑ 𝑤𝑖,𝑓,𝑞−1×

𝐼𝑁𝐷 ≠𝐼𝑁𝐷𝑓𝑖∈𝑓

𝑤𝑖,𝑞−1𝐼𝑁𝐷

×𝐼𝑆𝑞

𝐼𝑁𝐷

where i denotes firm f’s institutional investor at the end of quarter q-1, IND denotes Fama-

French 12 (FF12) industry sector, and INDf denotes the industry sector in which firm f belongs.

FF12 industry sector represents a broad industry classification. It follows that industry-level

events should generally be unrelated to the fundamentals of individual firms in other FF12

industries.13 𝐼𝑆𝑞𝐼𝑁𝐷 is an indicator variable equals to one if industry IND experiences a shock in

quarter q, and zero otherwise. An industry is deemed to have experienced a shock if the

industry’s return for the quarter is either the highest or lowest across all FF12 industry sectors.

We weight these shocks to capture their economic importance. The variable 𝑤𝑖,𝑞−1𝐼𝑁𝐷 denotes the

weight of industry sector IND in investor i’s portfolio in the prior quarter q-1, which represents

the importance of industry sector IND in institutional investor i’s portfolio.

13 The potential supply-chain links between firms across different Fama-French 12 industries will reduce the

shifts of investor attention to the shocked industries, thus biasing against us finding results.

10

The sum of the products of 𝑤𝑖,𝑞−1𝐼𝑁𝐷 and 𝐼𝑆𝑞

𝐼𝑁𝐷 across all industries unrelated to firm f,

capture investor i’s level of distraction away from firm f, when events occur in unrelated

industries of investor i’s portfolio. To aggregate across institutional investors of a firm, we

weight the level of distraction of each investor i in firm f by 𝑤𝑖,𝑓,𝑞−1 which measures the

importance of investor i in firm f in the prior quarter, q-1. Intuitively, investor i have more

weight if 1) firm f has more weight in i’s portfolio and 2) investor i owns a larger fraction of

firm f’s shares. Following Kempf et al. (2016), we compute 𝑤𝑖,𝑓,𝑞−1 as:

𝑤𝑖,𝑓,𝑞−1 = 𝑄𝑃𝐹𝑤𝑒𝑖𝑔ℎ𝑡𝑖,𝑓,𝑞−1 + 𝑄𝑃𝑒𝑟𝑐𝑂𝑤𝑛𝑖,𝑓,𝑞−1

∑ (𝑄𝑃𝐹𝑤𝑒𝑖𝑔ℎ𝑡𝑖,𝑓,𝑞−1 + 𝑄𝑃𝑒𝑟𝑐𝑂𝑤𝑛𝑖,𝑓,𝑞−1)𝑖∈𝐹,𝑞−1

where 𝑃𝐹𝑤𝑒𝑖𝑔ℎ𝑡𝑖,𝑓,𝑞−1 is the weight of the market value of firm f in investor i’s portfolio, and

𝑃𝑒𝑟𝑐𝑂𝑤𝑛𝑖,𝑓,𝑞−1 is investor i’s percentage ownership in firm f. The former measures how much

time the investor is likely to spend in analysing firm f, and the latter measures how much

influence investor i can have in the firm.

We sort all stocks held by investor i into quintiles by 𝑃𝐹𝑤𝑒𝑖𝑔ℎ𝑡𝑖,𝑓,𝑞−1 and all investors

of firm f into quintiles by 𝑃𝑒𝑟𝑐𝑂𝑤𝑛𝑖,𝑓,𝑞−1. 𝑄𝑃𝐹𝑤𝑒𝑖𝑔ℎ𝑡𝑖,𝑓,𝑞−1 and 𝑄𝑃𝑒𝑟𝑐𝑂𝑤𝑛𝑖,𝑓,𝑞−1 takes a

value from 1 to 5 depending on which quintile 𝑃𝐹𝑤𝑒𝑖𝑔ℎ𝑡𝑖,𝑓,𝑞−1 and 𝑃𝑒𝑟𝑐𝑂𝑤𝑛𝑖,𝑓,𝑞−1 ,

respectively, falls in. The weights 𝑤𝑖,𝑓,𝑞−1 sum to 1 for each firm f after scaling by the

denominator. It follows that higher values of Total Distraction indicates that the institutional

shareholders in firm f are more distracted by attention-grabbing returns from unrelated industry

sectors, and therefore their overall monitoring intensity of firm f’s’ board is reduced.

As we have stockholding data and voting data by each individual mutual fund, in

addition to our main firm-level distraction measure, we can also calculate an investor-level

distraction measure for each fund using a similar approach as above so as to examine how fund-

level distractions affect their voting behaviour.

11

2.2. Validity of the distraction measure

There are two important advantages of measuring institutional investor distractions in

this way. First, to the extent that the return shocks are in unrelated industries, this measure

captures exogenous variation in institutional shareholder monitoring, since the return shocks

from other FF12 industries are unlikely to be driven by the focal firm’s fundamentals. This

helps to alleviate reverse causality issues and issues relating to omitted variables, which might

affect both institutional investor monitoring levels and firm behaviour. Second, the investor-

level distraction measure differs across the firms held by each investor due to the way it is

constructed. Thus, we are able to compare the within-investor difference in levels of

distractions towards each firm held in the investor’s portfolio, essentially taking into account

the selection issues whereby certain institutions select into firms with specific features due to

their preferences.

We further evaluate whether return shocks in unrelated industries can cause permanent

changes in the focal firm’s board governance and performance. We first check the length of

the extreme industry-level returns, and find that each industry return shock on average only last

for 1.25 quarters and the maximum length of continuous return shocks is only 2 quarters. These

short-lived industry-level return shocks are likely to be random events, and unlikely to cause

institutional investors to significantly rebalance their portfolios. Consistent with our

expectation, Kempf, Manconi, and Spalt (2016) find that the focal firm is unlikely to experience

a large change in its portfolio weight in the institution’s portfolio when the institutional investor

is distracted by events elsewhere. Therefore, unrelated industry shocks are unlikely to drive

changes in the focal firm’s board governance through changes in the stockholdings of the

distracted institutional investor.

Nevertheless, non-shocked industries can continuously experience lowered

institutional investor monitoring intensities for relatively longer periods, as investors

12

continuously shift their attention to different shocked industries over time. Suppose a mutual

fund investor has 4 stocks in unrelated industries, for example a bank, a pharmaceutical firm,

a food retailer, and a manufacturing firm. Suppose the pharmaceutical industry experiences a

large return shock in quarter 1, the food retailer experiences a large return shock in quarter 2,

and the manufacturing industry experiences a large return shock in quarter 3. As the mutual

fund manager continuously shifts her attention to different industries other than the financial

services industry, the bank is being “overlooked” during this period. In untablulated analysis,

we find that this distraction period on average lasts for 7 quarters. Thus, looser investor

monitoring due to distractions can lead to significant changes in the focal firm’s board

governance and its long-run operating performance.

2.3. Data and sample formation

Our main sample comes from linking several well-known databases. We start with firm-

years in the RiskMetrics director database, which contains information on board structure and

director characteristics. We obtain information on institutional investor shareholdings from the

Thomson-Reuters Institutional Holdings (13F) database to construct the investor distraction

measure. We then merge the director and institutional holding data with firm accounting and

stock returns data from Compustat and CRSP, respectively. We drop firm-years with missing

information for our distraction measure, board structure, or key financial and stock return

variables. We also exclude the heavily regulated finance and utility industries. Further, we

exclude firms with dual-class share structures and closely-held firms where insiders or directors

as a group hold more than 50% of shares, because institutional shareholders are unlikely to

have much influence on the corporate governance of these firms.14 We focus on independent

14 These exclusions reduce the initial sample size by about 10% and leads to a cleaner sample for the purpose of

our analysis.

13

directors in this study because they are the primary board monitors.15 Our final sample consists

of 121,205 independent director-firm-years from 15,575 firm-year observations for the period

1996 to 2013. However, the sample size may vary across tests due to availability of control

variables and dependent variables.

To examine board characteristics and composition, we require CEO-director social ties

information from BoardEx. Although BoardEx has data from 2000, it becomes better populated

only from 2003 and onwards. Therefore, for most of our tests involving board structure, we

start the sample period from 2003 and end in 2013 resulting in 7,663 firm-year observations.

To examine voting outcomes, we also obtain shareholder voting data from ISS Voting

Analytics for the period 2003 to 2012. We merge ISS Voting Analytics with RiskMetrics

director data using company and director names, and further merged this data with CEO-

director social ties information from BoardEx. After requiring non-missing voting data and

social ties data, we end up with 30,310 individual director elections. We call this sample the

director votes sample. In these elections, we observe 21,127 distinct mutual fund-years and

2,081,611 votes.

2.4. Descriptive statistics

Table 1 provides summary statistics for our key variables. Detailed descriptions of all

of the variables can be found in Appendix A. We winsorize all the continuous dependent and

control variables at 1% and 99%. Panel A summarizes the means, medians, 25th and 75th

percentiles, and the standard deviation of the institutional investor distraction measures. For

our fund-level distraction measure, the mean and median mutual fund distraction levels in our

15 We follow the director classification in Riskmetrics. Independent directors are outside directors that have no

family or economic ties to management or the firm they monitor other than that through their directorship.

RiskMetrics primarily relies on the NYSE and Nasdaq listing rules to classify independent directors, and identifies

independent directors based on proxy statements and disclosures of related transactions. Examples of non-

independence using the RiskMetrics definition include but are not limited to: former employees of the firm or

subsidiaries, major shareholders, customers, suppliers, and family members of executives.

14

sample are both 0.14, with a standard deviation of 0.06. The mean and median firm-level

distraction measure, Total Distraction, is 0.17 and 0.16 respectively, while the 25th percentile

and 75th percentile values are 0.13 and 0.21, respectively. By construction, Total Distraction

has a minimum value of 0.05. The distribution of our distraction measure across firms is in line

with Kempf, Manconi, and Spalt (2016).

Panel B reports summary statistics for director election outcomes and director

characteristics for our director voting sample with data on voting outcomes and social ties.

Among the 30,310 independent director election votes, on average 5% were “No” votes, i.e.,

defined as “against” or “withheld” votes. Across all director elections, the median director

election sees only 2% of the votes being cast as “No” votes and only 5% cast as negative votes

at the 75th percentile. Therefore, negative votes are rare. At the maximum, 74% of the votes

were negative votes. We also find that only 11% of directors receive a poor voting outcome,

which we define as elections where a director receives more than 10% of “No” votes.

Furthermore, 6% of the ISS director election recommendations are negative. These proposal-

level statistics are similar to those in Cai, Garner, and Walkling (2009).

Almost 25% of the independent directors in the director voting sample are considered

problematic which we define as an independent director who is busy, socially connected to the

CEO, and/or foreign based. A busy director is one who holds 3 or more directorships in total

during the year (Fich and Shivdasani, 2006). Directors who attend the same educational

institutions and/or the same non-business organization as the CEO are deemed to be socially

connected to the CEO.16 A foreign director is one who primarily works for a non-U.S. employer

16 Although BoardEx uses a unique identifier for each of the educational institutions in the database, the same

educational institution may appear under different identifiers (e.g. Harvard University and Harvard Business

School). To remedy this problem, we manually match the names of the educational institutions and create new

identifiers that uniquely identify each educational institution. For shared social ties at non-business organizations,

we include connections at charities, social clubs, and armed forces, and exclude those compulsory professional

and industrial organizations where social interaction is unlikely due to the compulsory nature of membership in

the organizations (e.g. American Bar Association).

15

or last worked for a foreign company if already retired (Masulis, Wang, and Xie, 2012). Among

the problematic directors, 18% are busy directors, 13% are socially dependent directors, and

3% are foreign directors. About 16% of directors leave the board and are not renominated by

the board in the subsequent director elections. We use data from Voting Analytics to determine

whether a particular director is being renominated by the board or not.

In Panel C, we report the director characteristics for our full sample of director-firm-

year observations from 1996 to 2013. We find that only 1% of the independent directors in our

sample have attendance problems defined as missing 25% or more of board meetings.

Independent directors have an average of 1.6 total directorships, while the median number of

directorships is 1. In addition, the average director is 63 years old with board tenure averaging

11 years. Moreover, independent directors generally have weak firm financial incentives with

a director’s mean (median) equity stake in the firm representing only 0.07% (0.02%) of

outstanding shares.

We report board characteristics for the subsample of firm-years with information from

BoardEx. On average 21% of the independent directors on the board are considered

problematic. About 10% of new director appointments and 66% renominations are problematic.

We also look at the distribution of problematic directors on the major committees. On average

about 21% to 22% of the audit, compensation, and nomination committee members are

problematic.

In Panel E, we report descriptive statistics for firm characteristics at the firm-year level.

Boards on average hold 8 meetings per year. The average board has 9 members, out of whom

71% are classified as independent. CEOs own about 2.5% of shares outstanding. Finally, about

60% of the firm-years have a staggered board in our sample.

16

3. Shareholder Distraction and Voting

3.1. Investor-level mutual fund distraction and fund votes

In this section, we examine voting behavior of institutional investors in director

elections as one critical channel of investor monitoring of director quality and performance,

and a disciplinary mechanism for poorly-performing directors. Although the vast majority of

director elections are uncontested and the rejection of a standing director is extremely rare,

Aggarwal, Dahiya, and Prabhala (2015) show poor vote results have disciplinary effects in

themselves. Directors with weak voting support tend to depart from the board and even if they

remain on the board, they get demoted to less important board positions. These poorly-

performing directors also suffer from significant reputational losses in the directorial labor

market in that they gain fewer additional board appointments and lose more of their other board

seats than other independent directors.

We first look at investor-level distraction and their individual voting behavior in Table

2 Panel A. Since 2003, mutual funds are required to publicly disclose their voting behavior

through N-PX filings with the Securities and Exchange Commission (SEC). Therefore, our

analysis of mutual fund voting starts in 2003.17 We focus on actively-managed equity funds as

such funds are most likely to gain from active intervention. We provide more details about the

formation of our voting sample in Appendix B. For each director election proposal, depending

on whether it is under plurality or majority voting, mutual funds can vote “For,” “Against,” or

withhold their vote.18 According to Cai, Garner, and Walkling (2009), shareholders can express

their dissatisfaction by withholding votes, thus “Withhold” is functionally equivalent to

“Against.” Therefore, we classify “Withhold” as well as “Against” votes as “No” or negative

votes. Our dependent variable in Panel A is Oppose Director, which is an indicator variable

17 In the earlier years, Voting Analytics only covers the largest fund families. 18 We include director elections involving plurality voting and majority voting. Under plurality voting,

shareholders can vote “For” or withhold their votes while in majority voting, shareholders can vote “For” or vote

“Against” a director (Ertimur, Ferri, and Oesch, 2015).

17

that equals one if the mutual fund cast a negative vote for a particular director in a given annual

election and is zero otherwise. We find that Oppose Director is equal to one in 6% of cases.

Due to their relative rarity, negative votes by mutual funds should have strong disciplinary

effects on independent directors.

The key independent variable in Table 2 Panel A is Mutual Fund Distraction, which is

the level of distraction experienced by the voting mutual fund in the past four quarters

immediately preceding the voting date. We report linear probability model (LPM) estimates

with two sets of fixed effects and with clustering of standard errors at the fund level. The first

set of fixed effects is interacted fund and year fixed effects, which allows us to compare the

vote outcomes at firms where the voting mutual fund is more distracted against vote outcomes

at firms where the same fund is less distracted during the same year. The second set of fixed

effects are director election proposal fixed effects, which allow us to control for the

characteristics of each election proposal, including time-varying director characteristics and

time-varying firm characteristics including performance. For instance, the ISS

recommendation for the director candidate and shareholder activist events like “just vote no”

campaigns are taken into account using director election proposal fixed effects.

In Model (1) of Panel A, we find that the coefficient on Mutual Fund Distraction is

-0.033 and statistically significant at the 5% level, suggesting that when mutual funds are

distracted, they are less likely to oppose management recommendations in independent director

elections. Economically, a one standard deviation increase (decrease) in institutional investor

distractions reduces the chance that the investor votes against (for) an independent director

candidate in the election by 3.3% (0.033*0.06/6%), adjusted for the unconditional probability

of voting against an election proposal (6%).

We then examine whether problematic directors in particular are less likely to be

disciplined when institutional investors are distracted. We identify three types of independent

18

directors whose monitoring incentives are likely to be compromised. The first type of

problematic director is an independent director who is socially connected to the CEO. Socially

connected directors tend to be friendlier to management and thus, are ineffective monitors

(Hwang and Kim 2009, 2012; Chidambaran, Kedia, and Prabhala, 2011; Fracassi and Tate,

2012; Nguyen, 2012). For example, studies show that CEO-director ties lead to a decline in

CEO turnover-performance sensitivity, and CEOs in such firms also extract more private

benefits, which significantly reduce firm values. The second type of problematic director is an

independent director who is excessively busy due to sitting on multiple boards. Busy directors,

defined as those with 3 or more total directorships during the year, are likely to be

overcommitted and tend to be less effective monitors (Fich and Shivdasani, 2006; Falato,

Kadyrzhanova, and Lel, 2014; Masulis and Mobbs, 2014). The third type of problematic

director is a foreign independent director whose primary employer is a non-US company.

Masulis, Wang and Xie (2012) find that foreign directors are less effective board monitors, and

they tend to miss more board meetings, accept greater earnings management, higher CEO pay,

leading to poor firm performance.

In Models (2) and (3), we split the independent director sample into problematic and

non-problematic candidates. We find that most of the significant effects we found earlier come

from the subsample of problematic director candidates in Model (2), and we observe no

significant effects for non-problematic director candidates in Model (3). Given that most

investors tend to support the director election proposals in general, non-problematic directors

are likely to receive support regardless of whether the investor is distracted. Therefore, we do

not observe a significant impact of mutual fund distraction on voting outcomes for the non-

problematic directors. However, problematic directors often receive less support in general as

vigilant investors vote against these underperforming directors. Yet, when investors are

distracted they tend to ignore the underperformance of these problematic directors and support

19

them in the elections. These findings suggest that directors, especially problematic directors,

are less likely to be disciplined during general elections when mutual fund investors are

distracted.19

Mutual funds within the same fund families may have similar voting patterns. To

account for voting patterns by fund families, we aggregate the mutual fund distraction and

voting behavior at fund family level and report the results in Panel B. The dependent variable

in Panel B is the average of Oppose Director across all funds in the same family, and the key

independent variable is Mean Mutual Fund Distraction, the average distraction of all the funds

in the same family. We use interacted fund family, year fixed effects and election proposal

fixed effects, and standard errors are clustered by fund family. After accounting for the similar

voting patterns within the same mutual fund families, we find similar and consistent evidence

that mutual fund investors are less likely to vote against directors, especially problematic ones,

when they are distracted.

In untabulated tests, we exclude family firms where institutional investors are likely to

have more limited influence and we find that the link between mutual fund distraction and their

voting pattern is stronger. We also use a larger sample where we include both actively-managed

and passively-managed funds. We find that the results are weaker, but remain qualitatively

similar. Additionally, using Bushee’s classification of institution types, we find a stronger

distraction effect for mutual funds that are affiliated to institutions who are more likely to

monitor, such as investment companies, independent investment advisors, and public pension

funds.

19 Another possible measure of ineffective directors is to use ISS recommendations. However, ISS

recommendations have important limitations. For example, ISS have been accused of making “blanket

recommendations” that are uniform recommendations for or against certain types of directors or firm

characteristics. Furthermore, using ISS recommendations to measure ineffective directors would require the

additional assumption that investors are active voters and do not rely on ISS recommendations when they are not

distracted. But this assumption is unlikely to be valid as Iliev and Lowry (2014) find that mutual fund investors

vary greatly on their reliance on ISS recommendations with a substantial portion of funds relying solely on ISS

recommendations.

20

3.2. Firm-level investor distraction and director election results

In Table 3, we examine the impact of distractions by a firm’s institutional investors on

director election outcomes at the firm-level. Our dependent variable is the Fraction of "No"

Votes for a Director and the key independent variable is Total Distraction, defined as the

average distraction of the firm’s institutional investors over the past 4 quarters immediately

before the meeting date. In Models (1) and (2), we examine the impact of investor distraction

on director election outcomes for all independent directors. In Models (3) to (6), we compare

the impact of investor distraction for the election outcomes of problematic versus non-

problematic independent directors. We report LPM estimates and include firm and year fixed

effects in all models as well as director fixed effects in the even-numbered models. We further

control for director and firm characteristics that are likely to affect the director voting results,

and the average fraction of “No” votes for all the independent directors in the firm standing for

election during the year. In all these regressions, we cluster standard errors at the director level.

In Models (1) and (2), we find that the coefficient on Total Distraction is negative and

statistically significant, suggesting that there are fewer “No” votes for director elections when

a firm’s institutional investors are distracted.20 Economically, a one standard deviation increase

in institutional investor distractions increases the negative votes received by a director by 1.7%

to 2.8% (0.014*0.06/5% or 0.023*0.06/5%). For control variables, we find that director

election results are influenced by Average Director “No” Votes, indicating that shareholders’

overall satisfaction with the board members significantly affects individual director election

outcomes. Also, we find that the coefficients on Negative ISS and Poor Meeting Attendance

are positive and significant, which is consistent with the Cai, Garner, and Walking (2009) who

20 Model 2 has fewer observations than Model 1 because directors who only appear once in elections are dropped

in Model 2 with director fixed effects.

21

find that ISS recommendations and director attendance are important determinants of director

voting results.

In Models (3) to (6), we find that the coefficient on investor distraction is statistically

significant for the subsample of problematic independent directors, while it is insignificant for

the subsample of non-problematic directors. The economic magnitude are also much bigger for

the problematic directors. These findings suggest that the effect of investor distraction on

director election outcomes is more pronounced for problematic independent directors, who are

more likely to face negative shareholder assessments.

We then repeat the above analysis using an alternative measure of director disciplinary

vote, Poor Vote Result, as the dependent variable in Panel B. Poor Vote Result is an indicator

variable equals to one if the percent of “No” votes received by a director exceeds 10% of total

votes cast, and zero otherwise.21 We obtain similar results as in Panel A. Economically, a one

standard deviation increase in total distraction leads to a 4.3% or a 4.9% (0.089*0.06/11% or

0.079*0.06/11%) decrease in the likelihood that the independent director receives a poor

election result, after we adjust for the unconditional probability of poor vote result (11%).

Again, the results are concentrated among the sample of problematic directors.

Overall, our findings support the view that directors generally face less pressure to

perform in director elections when institutional investors are distracted, and this effect is more

pronounced for more problematic directors who would have otherwise face more dissent when

investors are more vigilant.

21 The choice of cutoffs is arbitrary. We find similar results using the 30% cutoff as in Aggarwal, Dahiya, and

Prabhala (2015).

22

3.3. Sensitivity of director departures to vote results

Aggarwal, Dahiya, and Prabhala (2015) find that directors are more likely to depart

after they face a more negative shareholder reception in director elections and therefore, annual

elections serve as a potentially important disciplining mechanism for directors. We conjecture

that this disciplinary effect will be weakened when outside institutional investors are distracted.

In Table 4, we examine the impact of shareholder distraction on the sensitivity of director

departures to election results. Our dependent variable is Director Departure, an indicator

variable equals to one if the director is not renominated by the board in the subsequent elections

and zero otherwise.22 We construct this variable by following each director from one election

to the next in Voting Analytics and checking whether the management proposals include

putting up the director for election.23 The focal variables in our analysis are the interaction

terms between Total Distraction and weak vote outcomes, which we measure using Fraction

“No” Votes for a Director and Poor Vote Result Indicator. We only include directors who are

aged 70 and below to exclude departures due to mandatory retirements (Fahlenbrach, Low, and

Stulz, 2016). Since we require vote resultdata for this test, our sample is restricted to directors

who stand up for re-elections at the end of their terms. Thus, our sample is unlikely to include

director departures due to health problems and deaths. We estimate LPMs with either firm and

year fixed effects or director, firm, and year fixed effects. We cluster standard errors at the

director level.

Table 4 Panel A presents the results. Consistent with Aggarwal, Dahiya, and Prabhala

(2015), we find in all models that directors who receive less shareholder support during

elections are less likely to be subsequently renominated. Consistent with our conjecture, we

22 Our results are robust to using a departure indicator using RiskMetrics Director data instead, i.e., we follow

each director from one year to the next in the RiskMetrics Directors database and define a departure as having

occurred if the director is no longer on the board in the subsequent years. 23 We lost some observations because we need to check 2 or 3 subsequent years to see whether the director is

renominated in firms with staggered boards.

23

find that the disciplinary effect of these vote outcomes is attenuated when institutional investors

are distracted. In particular, we find that the coefficients on the interaction terms between Total

Distraction and Fraction of “No” Votes for a Director and Poor Voting Result are negative

and statistically significant in all the columns, suggesting that investor distraction weakens the

sensitivity of director departures to poor election outcomes. In an untabulated analysis, we

interact investor distraction with Poor Meeting Attendance. We find a significant negative

coefficient on the interaction term between Total Distraction and Poor Meeting Attendance,

indicating that directors with poor attendance records are less likely to be replaced when

institutional investors are distracted.

In Panel B of Table 4, we find that the distraction effect on the sensitivity of

independent director departures to weak election outcomes is statistically and economically

stronger in the subsample of problematic directors compared to the non-problematic directors.

This finding is consistent with previous results, which shows that the problematic directors are

less likely to be disciplined when outside investors are distracted.

4. Shareholder Distraction and Board Activities

So far, we have shown that directors are less likely to be disciplined by shareholder

voting when institutional investors are distracted. This should have an impact on their

incentives to diligently monitor management. Therefore, in this section, we examine the impact

of institutional investor distraction on changes in board activities. We measure board activity

by director attendance at board meetings, the frequency of board meetings, composition of

board monitors, and appointments of new problematic directors. Our conjecture is that when

outside institutional investors are distracted and exert less monitoring pressure on the board,

the board reduces their own monitoring efforts by missing more meetings, holding less board

meetings in general, and appointing problematic monitors to the board.

24

4.1. Independent director meeting attendance

We first examine whether institutional investor distraction increases the likelihood of

directors missing board meetings. Attendance records can serve as an important indicator of

the monitoring intensity of outside directors for at least two reasons. First, it is an observable

measure of director performance, which allows us to investigate whether directors behave

differently when one or more major shareholders are distracted. Second, attending board

meetings is a direct way for directors to obtain the information necessary to carry out their

duties and exert influence over firm managers. To the extent that institutional investor

monitoring intensities decline when they shift attention away from the firm, we would expect

to find that directors miss more board meetings.

Table 5 reports results from LPMs where our dependent variable, Poor Meeting

Attendance, is an indicator variable that equals to one if a director has poor board meeting

attendance defined as missing more than 25% of board meetings over the past fiscal year, and

zero otherwise. The key explanatory variable in the regressions is Total Distraction, which

measures the distraction level of the firm’s institutional investors over the past 4 quarters

immediately before the annual meeting date. The control variables used are based on Masulis

and Mobbs (2014). To account for time invariant firm and director characteristics, we include

models with firm fixed effects and models with both director and firm fixed effects. We include

a pre-SOX indicator in place of year fixed effects, to take into account the fact that boards tend

to be more vigilant in the post-SOX era and thus are less likely to miss board meetings. The

pre-SOX indicator is set equal to one for fiscal years 2002 and before, and zero otherwise.

Standard errors are robust and clustered at the director level.24

24 In untabulated test, we include meeting fee and director retainers as additional control variables (the information

on these variables is only available in the period prior to 2006). We also use alternative regression specifications

such as the logit and probit models with industry and year fixed effects. Our results remain unchanged.

25

Our results are reported in Panel A of Table 5. In Models (1) and (2), we find that the

coefficient on Total Distraction is positive and statistically significant, suggesting that

independent directors miss more board meetings when institutional shareholders become

distracted. Economically, a one standard deviation increase in the distraction level leads to a

12% (0.020*0.06/1%) increase in the probability that the director exhibits attendance problems,

after adjusting for the unconditional probability of poor attendance records (1% in our sample).

Among the control variables, the pre-sox indicator is statistically significant at 1% in all

specifications. This result confirms the common belief that the passage of SOX increases

director accountability to shareholders and several studies report that boards tend to be more

vigilant after SOX (e.g., Masulis and Mobbs, 2014). We also find that directors holding a

greater number of directorships tend to miss more board meetings while older directors miss

fewer meetings. This latter result could reflect a selection effect. These findings are in line with

previous studies such as Adams and Ferreira (2009) and Masulis and Mobbs (2014).

To the extent that directors on multiple boards selectively distribute their efforts more

towards larger and more prestigious firms due to reputational concerns (Masulis and Mobbs,

2014), we would expect that directors may not uniformly miss board meetings across all the

boards they sit on when they are not monitored intensively by outside investors. In particular,

we should see a stronger effect of investor distraction on director attendance problems among

smaller firms. In Models (3) and (4), we test this conjecture and include an interaction term

between Total Distraction and firm size. We find that the coefficient on the interaction term is

negative and significant, suggesting that the impact of shareholder distraction on director

frequency of missing meetings is more pronounced in smaller firms.

In Panel B of Table 5, we compare the impact of investor distraction for the attendance

records of problematic versus non-problematic independent directors. For this test, we restrict

the sample period to years 2000 to 2013 when the data on CEO-director social ties is available

26

from BoardEx. The results continue to hold if we start the sample from 2003 when the data is

better populated in BoardEx. The coefficients on total distraction in the subsample of

problematic independent directors are statistically significant in Models (1) and (2), but not

significant in the subsample of non-problematic directors that are reported in Models (3) and

(4). This result indicates that the effect of total distraction is stronger for the subsample of

problematic directors. The poorer attendance performance of problematic directors can be

explained by our findings in Tables 2 to 4 where we find that problematic directors face

significantly weaker disciplinary votes when institutional investors are distracted.25

Overall, we find strong evidence that directors are less attentive when institutional

investors become distracted, particularly in smaller firms where director reputational concerns

are weaker and for problematic directors who face significantly less monitoring when outside

investors are distracted.

4.2. Board meeting frequencies

We next examine how board meeting frequencies are related to institutional shareholder

distractions. Previous studies (Lipton and Lorsch, 1992; Conger et al., 1998; Vafeas 1999)

suggest that board meeting frequency is an important measure of board activity and directors

perform their monitoring duties more diligently if they meet more frequently. As Execucomp

stop reporting board meeting frequency numbers in 2006, we use the MSCI GMI Ratings

database to extend our meeting frequency data for the period from 2007 and onwards. We

perform OLS regressions using the natural logarithm of number of board meetings as the

dependent variable in Models (1) and (2) and include firm and year fixed effects. We also show

25 In an untabulated analysis, we further assess whether poorer attendance by problematic directors is purely driven

by busy directors. We split the busy director sample into busy directors who are also socially connected directors,

and busy, but non-socially connected directors. We find a stronger distraction-poor attendance link among busy

directors that are also socially connected directors. This finding indicates that both busy and social dependent

directors are driving the poorer attendance record of problematic directors.

27

results with industry and year fixed effects using Poisson count models where the dependent

variable is the unlogged number of board meetings. Standard errors are clustered at the firm

level for both types of models.

Our results are reported in Table 6. In Model (1), we find that the coefficient on Total

Distraction is negative and statistically significant, indicating that boards hold fewer meetings

when they are less monitored by outside investors. Vafeas (1999) finds that boards hold more

meetings if the firm is underperforming. Therefore, in Model (2), we examine the sensitivity

of board meeting frequencies to poor firm performance when outside investors are distracted

by including an indicator variable, Poor Tobin’s Q, and its interaction term with Total

Distraction. We find that the coefficient on the interaction term is negative and significant,

indicating that boards are less diligent in trying to improve firm performance when outside

investors are distracted. We find similar results in Models (3) and (4) when we use the Poisson

count model. The number of observations is slightly larger in Models (3) and (4) than in Models

(1) and (2). This is because firms that only appear once in our sample are dropped due to the

firm fixed effects used in Models (1) and (2).

In an untabulated analysis, we use an alternative dependent variable, Fewer Board

Meetings, which is an indicator variable equals to one if the number of board meetings during

the year is less than the number of meetings last year and zero otherwise. We find that investor

distraction significantly increases the likelihood of firms having fewer meetings than before.

4.3. Board composition, new appointments, and renominations of directors

In this subsection, we examine the board composition and appointment of problematic

directors following a change in the level of shareholder attention. Board composition is a key

determinant of board monitoring quality. By appointing effective monitors to the board,

shareholders can be better represented in major corporate decisions, which can ultimately

28

improve firm performance and value. Table 7 reports the regression estimates for the period

2003-2013.26 In Models (1) and (2), we examine the impact of shareholder distraction on board

composition where our dependent variable is Proportion Problematic Directors, which is the

ratio of number of problematic directors to the number of independent directors.

In Model (1), we find that the coefficient on shareholder distraction is positive and

significant, suggesting that firms are more likely to have problematic directors on the board

when the institutional investors are distracted. Given that we control for firm fixed effects, the

coefficients can be interpreted as within-firm changes in board composition. Economically, a

one standard deviation increase in total distraction leads to 1.8% (0.066*0.06/0.21) increase in

the proportion of problematic directors. Previously, we have found that problematic directors

are most likely to benefit from decreased monitoring from distracted institutional investors.

Therefore, in Model (2), we include an interaction term between Total Distraction and the

proportion of problematic independent directors on the nominating committee, Proportion PID

on Nomination Committee. We find that the coefficient on the interaction is positive and

significant, suggesting that the impact of institutional investor distraction on board composition

is more pronounced when there are problematic directors on the nomination committee.

In Models (3) - (6), we further test whether the changes in board composition are driven

by the new appointments or the renominations of problematic directors. The dependent variable

in Models (3) & (4) is New Problematic Director Appointment, an indicator variable equals to

one if the firm has newly appointed at least one problematic independent director during the

year and zero otherwise. The dependent variable in Models (5) & (6) is Renomination of

Problematic Director, an indicator equals to one if the firm has renominated problematic

26 The identification of problematic independent directors requires social ties information from BoardEx that is

available from 2000 and onwards. However, BoardEx significantly increased its coverage in 2003. Furthermore,

the existence of ineffective independent directors on boards and key committees is more relevant after SOX, when

firms are required to have independent boards and 100% independent directors on key committees. Therefore, we

start from Year 2003 for these set of tests.

29

directors and zero otherwise. We estimate LPMs with firm and year fixed effects. The

coefficient on Total Distraction is positive and significant at 5% level in Model (3).

Economically, a one standard deviation increase in total distraction increases the likelihood of

appointing a new problematic director by 13.4% (0.224*0.06/0.10). Furthermore, the impact

of shareholder distraction on appointments of problematic directors is stronger among firms

with more problematic committee members as shown in Model (4). In Models (5) and (6), we

find consistent but weaker evidence for the renomination of problematic directors. Thus the

changes in the board composition is primarily driven by the new appointments of problematic

directors.

In an untabulated analysis, we repeat our analysis in Table 7 and find that distraction

effect is stronger among firms with more CEO power as measured by CEO-chairman duality.

These results are consistent with our conjecture that CEOs and boards take the opportunity

when outside shareholders are distracted to appoint and retain ineffective directors. We also

find that when investors become more distracted, the proportion of problematic directors on

the major monitoring committees (compensation, audit and nomination committees)

significantly increases.

Overall, we find evidence that investor distraction adversely affects board composition,

especially when the nomination committee includes problematic monitors. More specifically,

directors with lower monitoring intensities are more likely to be appointed and renominated to

the board when institutional investors shift their attention away from the firm.

5. Shareholder Distraction and Board Monitoring Effectiveness

So far, we have shown that independent directors, especially problematic directors are

less likely to be disciplined by shareholder votes when institutional investors are distracted.

This leads to boards holding fewer meetings and board members missing more meetings.

30

Boards also appoint and renominate more problematic directors who are less effective

monitors, leading to worse board structures. The decrease in monitoring effectiveness of the

board when shareholders are distracted should manifest itself in the governance outcomes that

fall within the domain of board monitoring activities. In this section, we examine how earnings

management, CEO compensation, and firm valuation are affected by reduced board monitoring

efforts caused by investor distraction. These governance outcomes are often used in the prior

literature to assess board effectiveness.

5.1. Investor distraction and earnings management

We examine the impact of investor distraction on earnings management in Table 8. To

measure earnings management, we follow Dechow, Sloan, and Sweeney (1995) and calculate

a firm’s discretionary accruals.27 We estimate OLS regressions where our dependent variable

is the level of discretionary accruals. We include year fixed effects and firm fixed effects to

control for the time-invariant unobservable firm characteristics that could affect a firm’s

earnings reporting policy. Standard errors are clustered by firm. We find that the coefficient of

Total Distraction is positive and statistically significant, suggesting that firms are able to

pursue more earnings management when institutional investors are distracted.

In Model (2), we interact Total Distraction with the proportion of problematic

independent directors on the audit committee, Proportion PID on Audit Committee, since a

firm’s financial reports are primarily approved by members of this board committee. We find

that the coefficient on the interaction term is positive and significant, suggesting that the impact

of shareholder distraction on earnings management is more pronounced when there are more

27 Using the modified Jones model, discretionary accruals is defined as total accruals minus the predicted value

of total accruals. The predicted value of total accruals is from regressing total accruals on the inverse of total

assets, the difference between change of sales and change of accounts receivable scaled by total assets, and PPE

scaled by total assets. The regression coefficients are estimated cross-sectionally every year for each two-digit

SIC industry.

31

problematic independent directors sitting on the audit committee. In an untabulated test, we

replace the dependent variable with a positive accruals indicator, which equals to one if the

discretionary accruals is positive and zero otherwise. We find similar results.

5.2. Investor distraction and CEO pay

Following Cai, Garner, and Walkling (2009), we define unexplained CEO

compensation as the residual from a regression where the dependent variable is the natural

logarithm of the total CEO compensation and the explanatory variables include log(assets),

ROA, total firm risk, and interacted industry and year fixed effects. The second aspect of CEO

pay we examine is pay-for-performance sensitivity, which is calculated as the CEO's wealth

change from their portfolio of stock and options for a 1% change in firm stock price (Core and

Guay, 2002). In our regressions, we include year fixed effects and firm fixed effects. Standard

errors are clustered by firm.

Table 9 presents the results. In Model (1) where we examine unexplained CEO pay, we

find that the coefficient of institutional investor distraction is positive and statistically

significant at the 1% level, suggesting that CEO pay is higher when a firm’s institutional

shareholders are distracted. Economically, one standard deviation increase in investor

distraction is predicted to increase the likelihood of high excess CEO pay by 4.8%

(0.37*0.06/0.46), after we adjust for the unconditional probability of high CEO pay (46%). We

argue that due to investor distraction, boards have less monitoring incentives and this in turn

leads to lapses in governance. To establish this, we examine whether the impact of investor

distraction on excess pay is stronger when boards monitor less. In Model (2), we interact total

investor distraction with the proportion of problematic independent directors on the

compensation committee since CEO compensation is initially determined by this committee.

We find that the coefficient on this interaction term is positive and significant, indicating that

32

the effect of shareholder distraction on high CEO pay is more pronounced if there are more

problematic independent directors sitting on the compensation committee.

In Model (3) where we examine the CEO pay-for-performance sensitivity, we find that

the coefficient on total investor distraction is negative and significant at the 10% level,

indicating that when investors are distracted, CEOs are less motivated to perform. In Model

(4), we interact Total Distraction with the proportion of problematic directors on the

compensation committee. Although the coefficient on the interaction is in the right direction,

it is insignificant. Kempf, Manconi, and Spalt (2016) find that investor distraction leads to

increases in opportunistically-timed stock options, which have the effect of increasing pay-for-

performance sensitivity instead. Therefore, our weaker results for CEO pay-for-performance

sensitivity can be explained by low CEO pay-for-performance sensitivity and

opportunistically-timed stock options being substitute mechanisms for CEOs to extract private

benefits

In an untabulated test, we also control for the existence of Say-on-Pay proposals. This

information is from Voting Analytics and is available for the period 2003-2012. Our high CEO

pay result remains significant after controlling for Say-on-Pay proposals, but our CEO pay-for-

performance sensitivity results are weaker.

5.3. Investor distraction, reduction in board monitoring efforts and equity evaluation

In Table 10, we use Tobin’s Q as an overall indicator of firm valuation. In Model (1),

we find that the coefficient of Total Distraction is significantly negative, suggesting that firm

equity value is lower when shareholders are distracted. The economic magnitude is also large.

A one standard deviation increase in investor distraction reduces firm value by 6.7%

(2.31*0.06/2.06), relative to the average Tobin’s Q in the sample. This result complements

those of Kempf, Manconi, and Spalt (2016) who find that firms with distracted investors tend

33

to have lower stock return performance. We argue that the underperformance by such firms is

partly caused by reduced board monitoring incentives when investors are distracted.

To identify the exact channel through which shareholder distraction could have an

impact on governance outcomes, we use three proxies to measure board monitoring efforts/

incentives. We have shown that investor distraction on average leads to directors missing more

board meetings therefore, the first measure we use is an indicator variable that equals one if at

least one of the independent directors has a poor meeting attendance record during the fiscal

year, and zero otherwise. Our second variable also measures board monitoring efforts and is

the number of board meetings held during the year. We have also shown that investor

distraction leads to less frequent board meetings, therefore, we want to understand whether the