money moves: getting black women in the black

TRANSCRIPT

Money Moves : Gett ing B lack Women in the B lack

Nat iona l Coa l i t ion of 100 B lack Women, Inc .

P R E S E N T S

Money Moves: Getting Black Women in the Black

D E V E L O P E D B Y T H E

N a t i o n a l C o a l i t i o n o f 1 0 0 B l a c k W o m e n , I n c .N a t i o n a l E c o n o m i c E m p o w e r m e n t C o m m i t t e e

P R E S E N T E D B Y

Seretha S. Tinsley, National 1st Vice President,

National Coalition of 100 Black Women, Inc.

Belinda Walker, Chair –National Economic Empowerment Committee

Angela Collins-Lewis, Co-Chair –National Economic Empowerment Committee

National Coalition of 100 Black Women, Inc.1718 Peachtree Street, NW Suite 970

Atlanta, GA 30309(404) 390-3982

BEFORE WE

GET STARTED

04 03 02 01

G e t t i n g F a m i l i a r w i t h

Z o o m

U s i n g t h e C h a t F u n c t i o n

G i v i n g F e e d b a c k

& P o l l s

I n t e r a c t & PA R T I C I PAT E !

Before We Get Started…

Virginia W. Harris, MPA, CIA, CGFM

National President, National Coalition of 100 Black Women, Inc.

WELCOME &

INTRODUCTIONS

Angela Collins-Lewis

A member of the Queen City Metropolitan Chapter of NC100BW for seven years, Angela has consistently demonstrated her leadership abilities by successfully serving on The Board of Directors as the Chapter Chaplin since 2014.

Angela is the Co-Chair of the National Economic Empowerment Committee and serves the Queen City Metropolitan Chapter as Economic Empowerment Chair, a mentor for Building Bridges to Success, and contributor to the public policy, education, scholarship, fundraising, and civic engagement committees. Under her leadership, the chapter has earned 1st and 2nd place nationally for their stellar EE programming and building sustainable strategic partners.

Co-Chair, Economic Empowerment Committee

OUR

PRESENTERS

Belinda Walker

Belinda is a Servant Leader who has enjoyed a long track record in the community service arena! Currently, she serves as the NCBW-National Economic Empowerment Committee Chair (appointed 2019). In 2019, she completed her four-year tenure as the First Vice President of Programs for the National Coalition of 100 Black Women, Inc. – Metropolitan Atlanta Chapter.

Her additional roles in the NCBW-Metropolitan Atlanta Chapter have consisted of Second Vice President of Fund Development for four years, Health Committee Chair, Leadership Development Committee Co-Chair and several fundraising events leadership roles.

Chair, Economic Empowerment Committee

Tonight ’s Agenda

01 02 03 04

S i s t e r - N o m i c $ O v e r v i e w

W e a l t h P r o h i b i t o r s &

E c o n o m i c L a n d s c a p e

S i s t e r - N o m i c $ C u r r i c u l u m

N e x t S t e p s

IN THIS TRAINING PRESENTATION, WE’LL COVER:

PART I:S ister -Nomic$

OVERVIEW

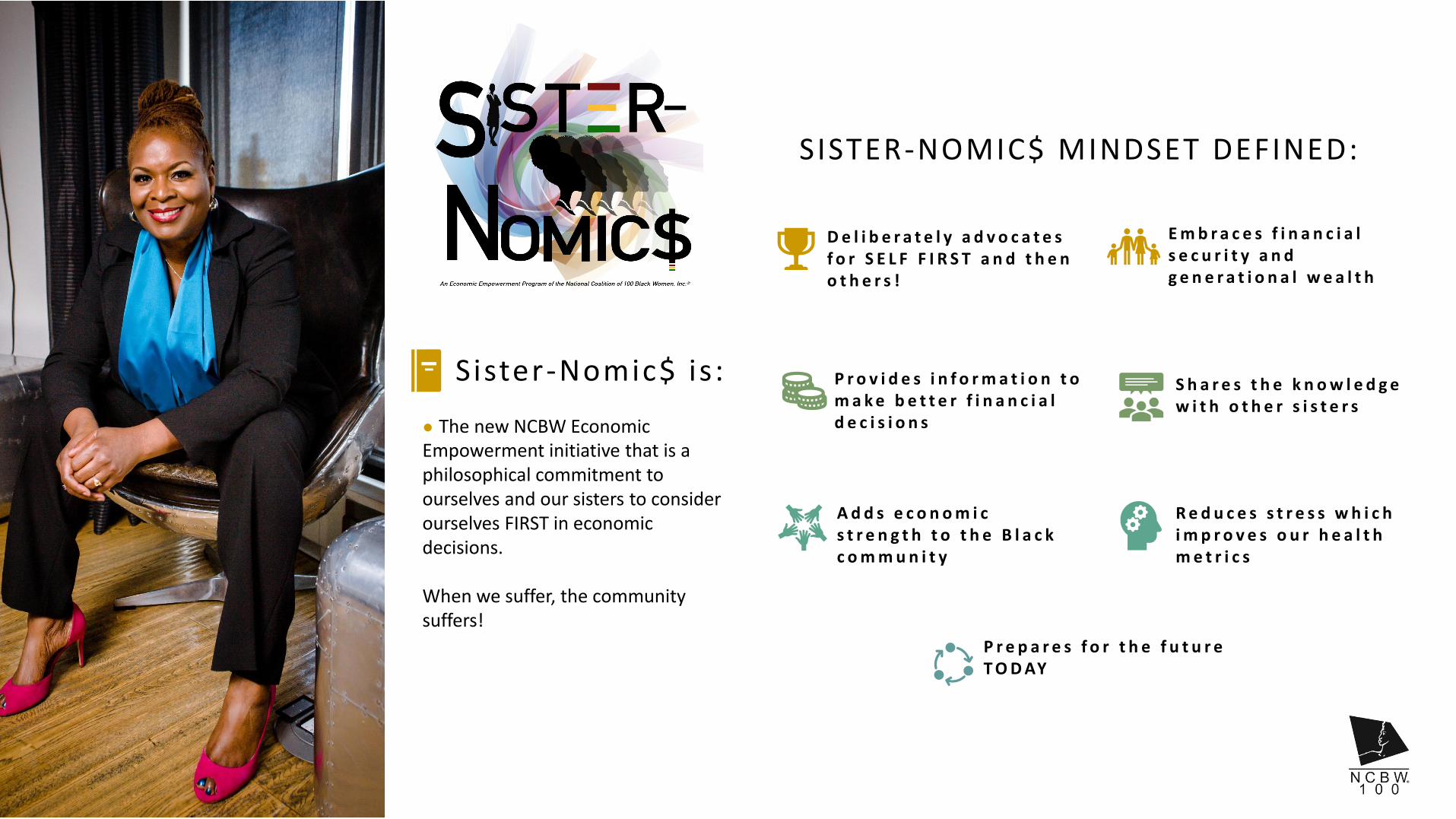

D e l i b e r a t e l y a d v o c a t e s f o r S E L F F I R S T a n d t h e n o t h e r s !

E m b r a c e s f i n a n c i a l s e c u r i t y a n d g e n e r a t i o n a l w e a l t h

P r e p a r e s f o r t h e f u t u r e T O D AY

P r o v i d e s i n f o r m a t i o n t o m a k e b e t t e r f i n a n c i a l d e c i s i o n s

S h a r e s t h e k n o w l e d g e w i t h o t h e r s i s t e r s

A d d s e c o n o m i c s t r e n g t h t o t h e B l a c k c o m m u n i t y

R e d u c e s s t r e s s w h i c h i m p r o v e s o u r h e a l t h m e t r i c s

SISTER-NOMIC$ MINDSET DEFINED:

Sister-Nomic$ is:

● The new NCBW Economic Empowerment initiative that is a philosophical commitment to ourselves and our sisters to consider ourselves FIRST in economic decisions.

When we suffer, the community suffers!

LOGO

Use official colors only in any representation of the Sister-Nomic$ logo.

TAGLINE

“The Sister-Nomic$ Economic sustainability framework –A National Coalition of 100 Black Women Inc. Economic Empowerment Initiative, based on Self-Preservation in all financial decisions.”

Sister-Nomic$ OverviewBranding & Marketing Requirements

The Sister-Nomic$ Economic sustainability framework – is based on Self-Preservation in all financial decisions.

S ister -Nomic$ Over v iew

Reduce debt and increase assets with each financial decision.

Embrace financial security and create generational wealth.

Contribute to the economic strength of the black community by supporting black institutions and businesses.

The Sister-Nomic$ Principles

Invest in both short term and long-term investments that will build her net worth.

Seek and share information with family and friends to facilitate informed financial decisions.

Patronize majority owned businesses that respect, support, and employ members of the black community and collaborate with its organizations.

Remain informed and engaged on political decisions that impact the wellbeing of the black community.

PART II:STRONG

BLACK WOMAN SYNDROME

SECTION 1:

DEFINITION & SUMMARY

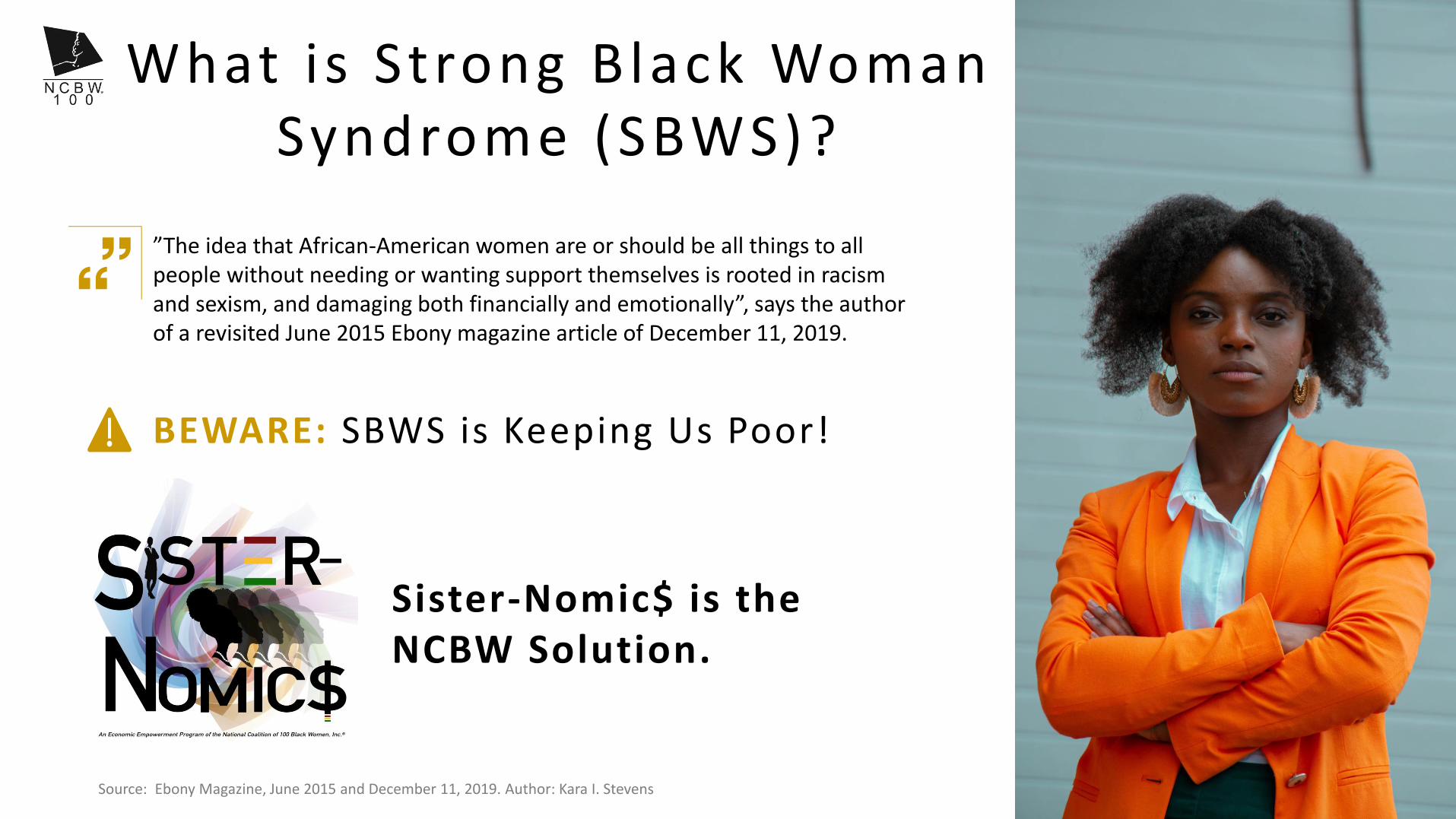

BEWARE: SBWS is Keeping Us Poor!

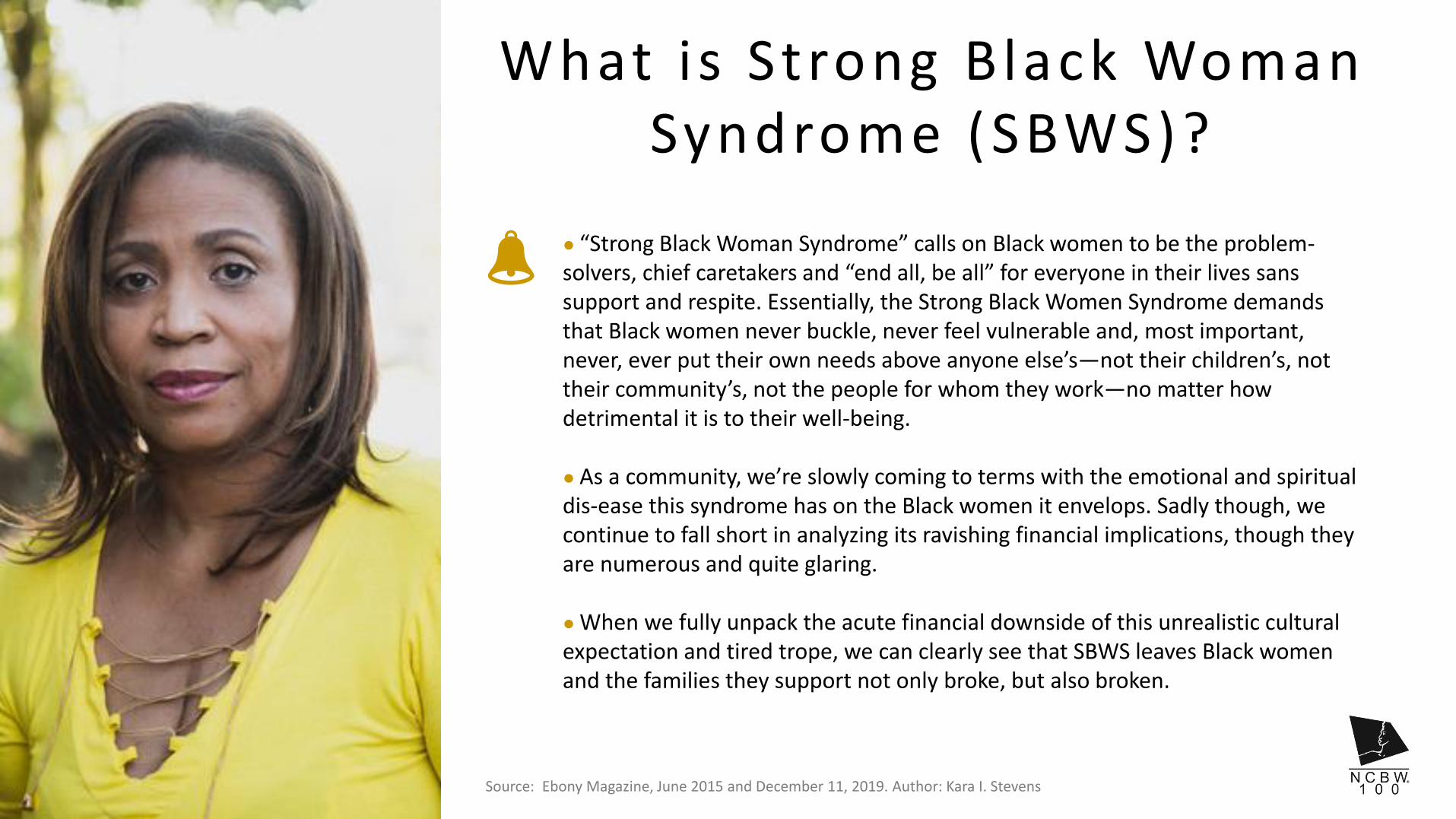

What is Strong Black Woman Syndrome (SBWS)?

”The idea that African-American women are or should be all things to all people without needing or wanting support themselves is rooted in racism and sexism, and damaging both financially and emotionally”, says the author of a revisited June 2015 Ebony magazine article of December 11, 2019.

Source: Ebony Magazine, June 2015 and December 11, 2019. Author: Kara I. Stevens

Sister-Nomic$ is the NCBW Solution.

What is Strong Black Woman Syndrome (SBWS)?

● “Strong Black Woman Syndrome” calls on Black women to be the problem-solvers, chief caretakers and “end all, be all” for everyone in their lives sans support and respite. Essentially, the Strong Black Women Syndrome demands that Black women never buckle, never feel vulnerable and, most important, never, ever put their own needs above anyone else’s—not their children’s, not their community’s, not the people for whom they work—no matter how detrimental it is to their well-being.

● As a community, we’re slowly coming to terms with the emotional and spiritual dis-ease this syndrome has on the Black women it envelops. Sadly though, we continue to fall short in analyzing its ravishing financial implications, though they are numerous and quite glaring.

● When we fully unpack the acute financial downside of this unrealistic cultural expectation and tired trope, we can clearly see that SBWS leaves Black women and the families they support not only broke, but also broken.

Source: Ebony Magazine, June 2015 and December 11, 2019. Author: Kara I. Stevens

SECTION 2:

4 WAYS SBWS KEEPS US POOR

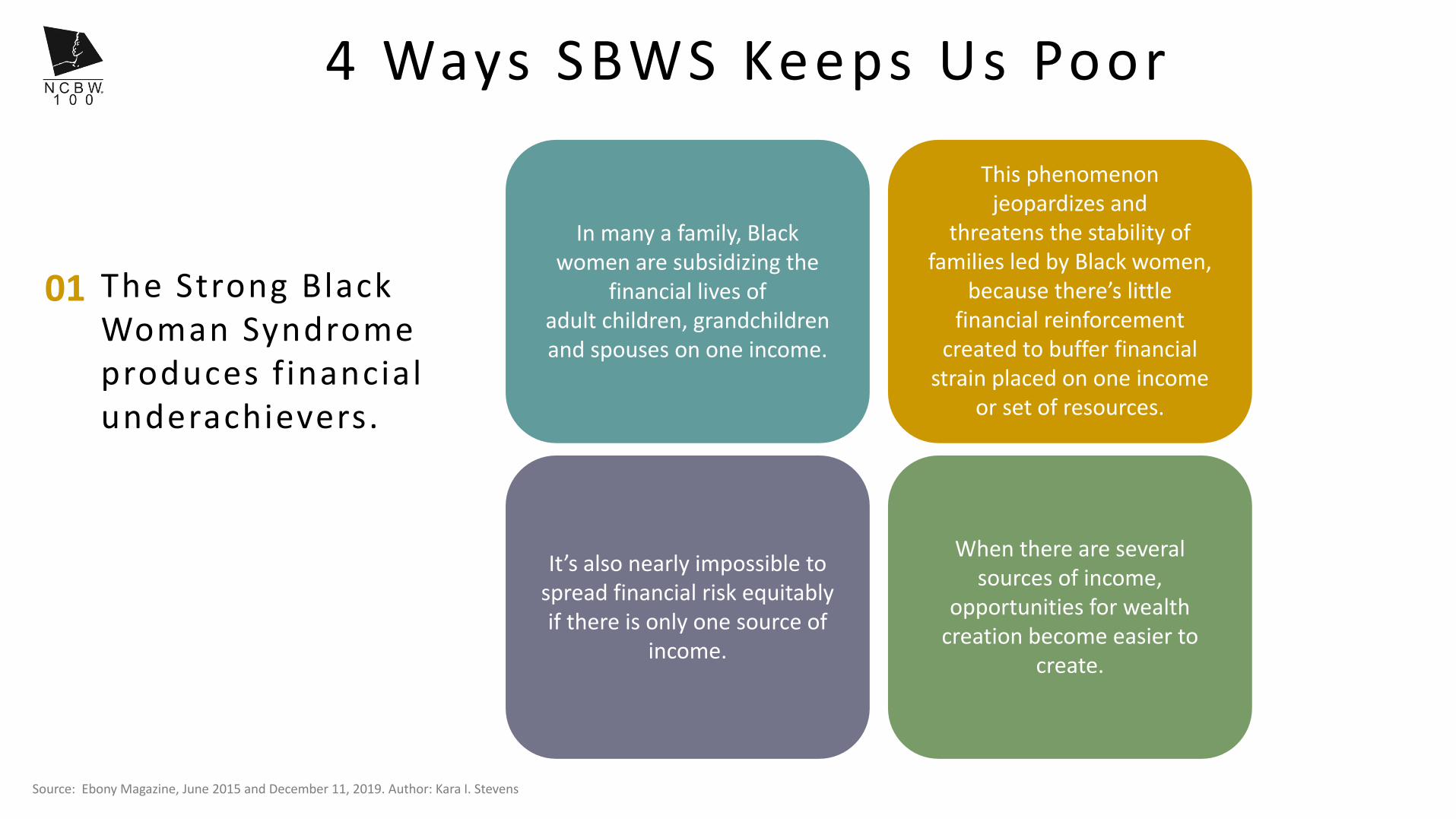

The Strong Black Woman Syndromeproduces f inancial underachievers.

4 Ways SBWS Keeps Us Poor

In many a family, Black women are subsidizing the

financial lives of adult children, grandchildren and spouses on one income.

This phenomenon jeopardizes and

threatens the stability of families led by Black women,

because there’s little financial reinforcement

created to buffer financial strain placed on one income

or set of resources.

01

It’s also nearly impossible to spread financial risk equitably if there is only one source of

income.

When there are several sources of income,

opportunities for wealth creation become easier to

create.

Source: Ebony Magazine, June 2015 and December 11, 2019. Author: Kara I. Stevens

The Strong Black Woman Syndromestif les business expansion.

4 Ways SBWS Keeps Us Poor ( c o n t ’d )

For Black women with this complex, there’s the distorted belief that they shouldn’t ask

for help.

02

She may consider asking for these types of support

because she considers it a sign of weakness or believes she can’t depend on anyone

but herself.

An aspiring entrepreneur suffering with the syndrome is often uncomfortable with asking for support, such as seed money, a referral, or

childcare support.

Source: Ebony Magazine, June 2015 and December 11, 2019. Author: Kara I. Stevens

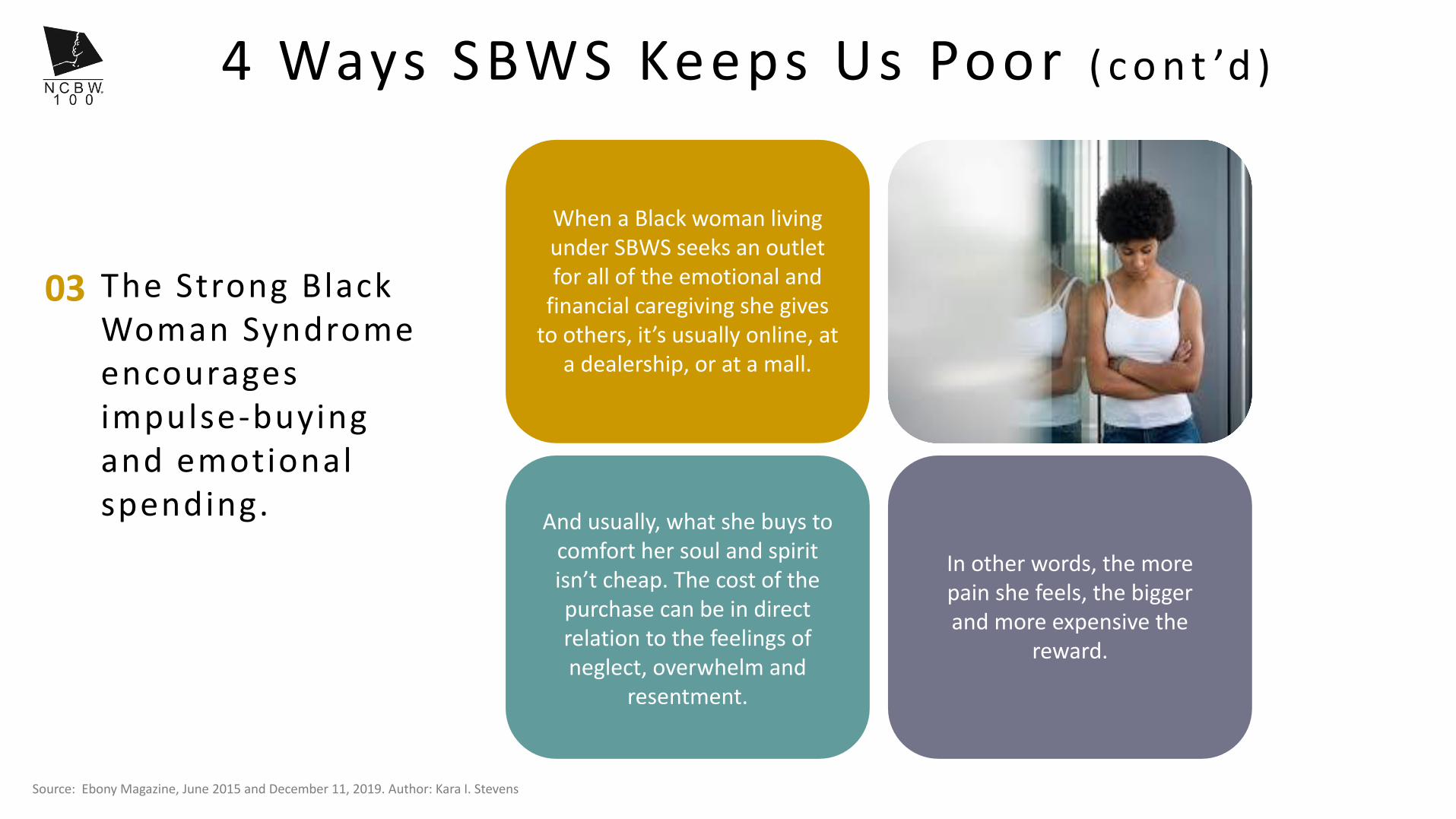

The Strong Black Woman Syndromeencourages impulse-buying and emotional spending.

4 Ways SBWS Keeps Us Poor ( c o n t ’d )

When a Black woman living under SBWS seeks an outlet for all of the emotional and

financial caregiving she gives to others, it’s usually online, at

a dealership, or at a mall.

03

And usually, what she buys to comfort her soul and spirit isn’t cheap. The cost of the purchase can be in direct relation to the feelings of neglect, overwhelm and

resentment.

In other words, the more pain she feels, the bigger and more expensive the

reward.

Source: Ebony Magazine, June 2015 and December 11, 2019. Author: Kara I. Stevens

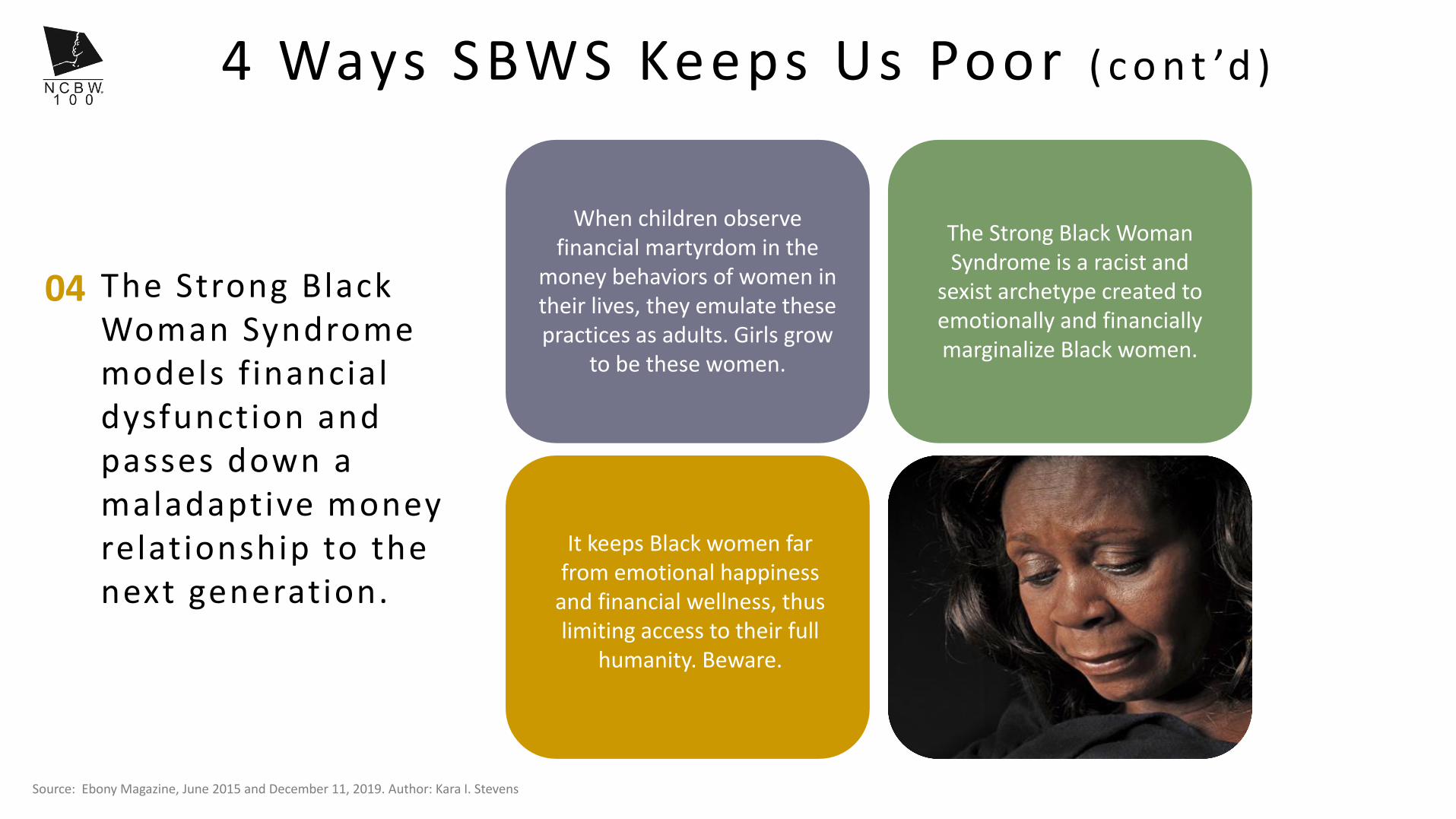

The Strong Black Woman Syndromemodels financial dysfunction and passes down a maladaptive money relationship to the next generation.

4 Ways SBWS Keeps Us Poor ( c o n t ’d )

When children observe financial martyrdom in the

money behaviors of women in their lives, they emulate these practices as adults. Girls grow

to be these women.

The Strong Black Woman Syndrome is a racist and

sexist archetype created to emotionally and financially marginalize Black women.

04

It keeps Black women far from emotional happiness

and financial wellness, thus limiting access to their full

humanity. Beware.

Source: Ebony Magazine, June 2015 and December 11, 2019. Author: Kara I. Stevens

PART III:BLACK WOMEN’S

ECONOMICLANDSCAPE

SECTION 1:

EXPLORING THEPAY GAP

● Black women ask for promotions and raises at about the same rates as white women, but they get worse results.

● Lower earnings for Black women means less money for their families, especially since more than 80% of Black mothers are the main breadwinners for their households.

● The gap is largest for Black women who have bachelor’s and advanced degrees.

● From age 16, Black girls are paid less than boys the same age—and the gap only grows from there.

Pay Gap Facts

Source: LeanIn.org :“The Black Women’s Pay

Gap by the Numbers”

B l a c k w o m e n a r e d o i n g t h e i r p a r t

T h e g a p h u r t s w o m e n a n d f a m i l i e s .

T h e p a y g a p a c t u a l l y w i d e n s f o r w o m e n a t h i g h e r

e d u c a t i o n l e v e l s .

T h e p a y g a p s t a r t s e a r l y

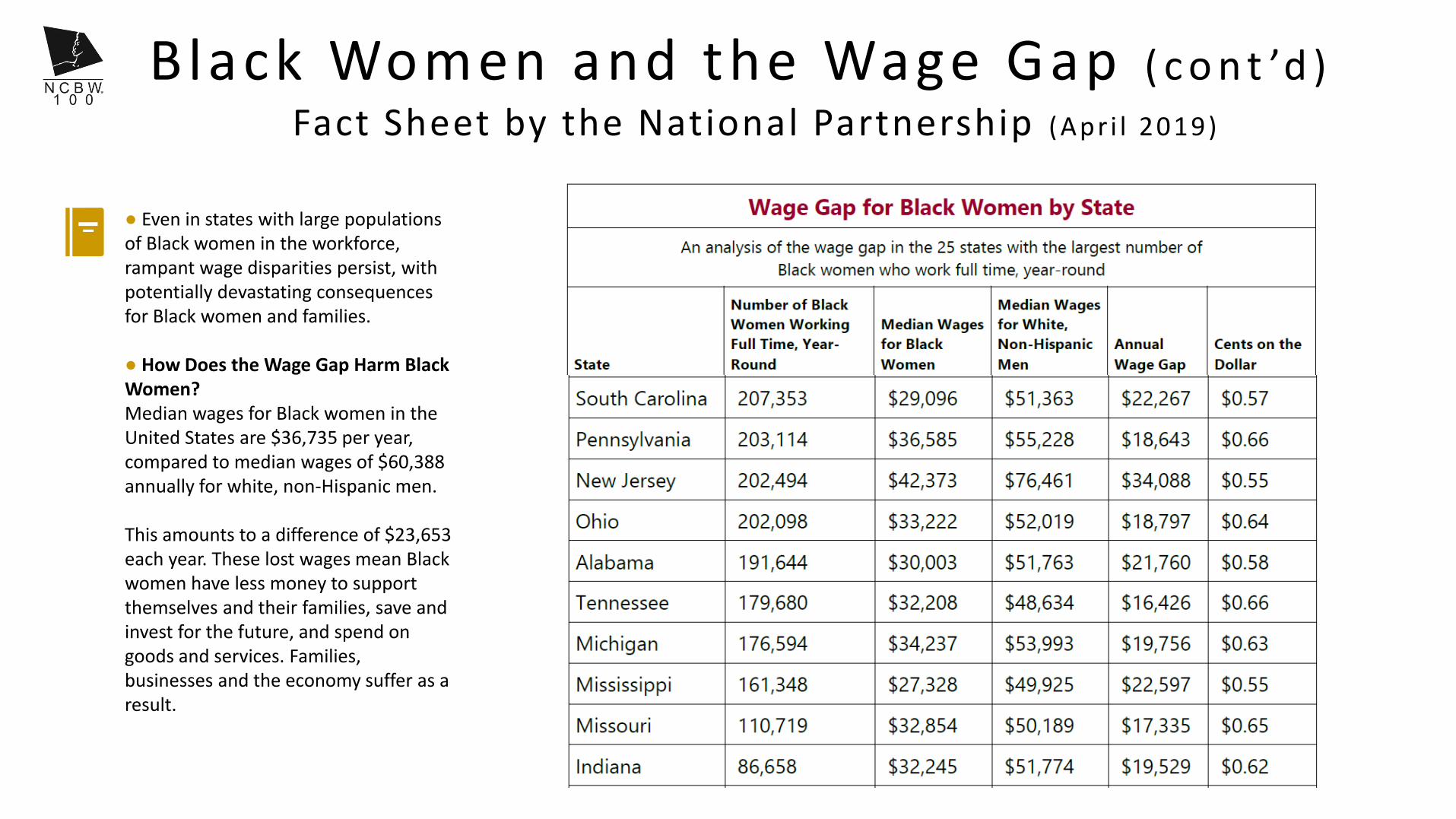

● Even in states with large populations of Black women in the workforce, rampant wage disparities persist, with potentially devastating consequences for Black women and families.

● How Does the Wage Gap Harm Black Women?Median wages for Black women in the United States are $36,735 per year, compared to median wages of $60,388 annually for white, non-Hispanic men.

This amounts to a difference of $23,653 each year. These lost wages mean Black women have less money to support themselves and their families, save and invest for the future, and spend on goods and services. Families, businesses and the economy suffer as a result.

Black Women and the Wage GapFact Sheet by the National Partnership (Apr i l 2019)

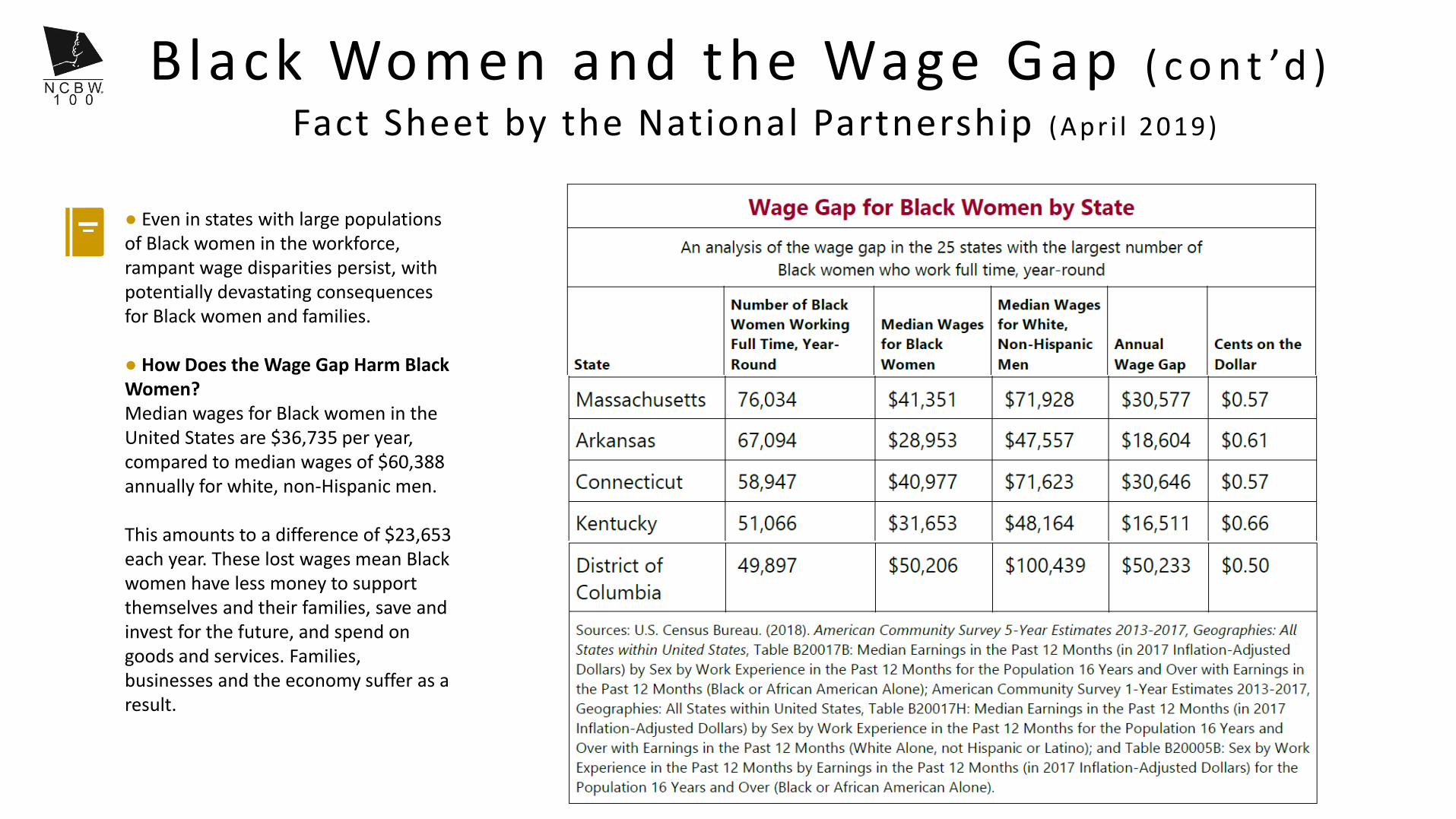

● Even in states with large populations of Black women in the workforce, rampant wage disparities persist, with potentially devastating consequences for Black women and families.

● How Does the Wage Gap Harm Black Women?Median wages for Black women in the United States are $36,735 per year, compared to median wages of $60,388 annually for white, non-Hispanic men.

This amounts to a difference of $23,653 each year. These lost wages mean Black women have less money to support themselves and their families, save and invest for the future, and spend on goods and services. Families, businesses and the economy suffer as a result.

Black Women and the Wage Gap ( c o n t ’d )

Fact Sheet by the National Partnership (Apr i l 2019)

● Even in states with large populations of Black women in the workforce, rampant wage disparities persist, with potentially devastating consequences for Black women and families.

● How Does the Wage Gap Harm Black Women?Median wages for Black women in the United States are $36,735 per year, compared to median wages of $60,388 annually for white, non-Hispanic men.

This amounts to a difference of $23,653 each year. These lost wages mean Black women have less money to support themselves and their families, save and invest for the future, and spend on goods and services. Families, businesses and the economy suffer as a result.

Black Women and the Wage Gap ( c o n t ’d )

Fact Sheet by the National Partnership (Apr i l 2019)

SECTION 2:

STRUGGLES FORENTREPRENEURS

The St rug g le for B lack Women Entrepreneurs

According to the Census Bureau, black-owned businesses increased from 1.9 million to 2.6 million between 2007 and 2012. That boom can be attributed to black women, who make up 59% of black-owned businesses.

The astounding rate at which black women are opening businesses was also quantified in a newly released study commissioned by American Express, titled The 2018 State of Women-Owned Business Report, which found that the number of firms owned by black women grew by a whopping 164% from 2007 to 2018. That’s more than three times the rate of all women-owned businesses, which increased by 58% within that time period.

The new report also found that poor treatment coupled with feeling undervalued at work and the lack of pay equity are catalysts that led women of color to start businesses at a greater rate.

Source: Black Enterprise Magazine, “The Struggle for Black Women Entrepreneurs Continues”

The Struggle for B lack Women Entrepreneurs

Another problem black female founders face is a lack of educational resources and mentors for their businesses. Frequently, black women “don’t know who to go to, where to go and what organizations are out there that can support them,” Dell Gines, the author of the Black Women Business StartUps report, told Forbes.

This is one reason why “you see a lot of clustering in very few industries with a low barrier to entry–service businesses such as hair salons, catering, child daycare centers and consulting.”

Source: Black Enterprise Magazine, “The Struggle for Black Women Entrepreneurs Continues”

(cont ’d)

SECTION 3:

NCBW ECONOMICEMPOWERMENT

SURVEY

Q2 What is your approximate household income?Results: 34.45% =$150,000+ , 10.92% =$100,000-$125,000, 26.89% =75,000-$99,999, %= $50,000-74,999, 6.72% =$25,000 - $49,999

Q3 What is your employment/employer type?Results: Corporate - 28.10%, Government – 23.14%, Retirees-20.66%, Non-profit-17.36%, Entrepreneurs /Self Employed – 10.74%, Unemployed – 0%

Q4 In relation to your personal knowledge of finances, where do you think you learned the most information?Results: Financial professional - 23.20%, Parents/Friends – 21.6%, School & Self-help – 15.20%, Other – 10.40%, Internet – 7.20%

Q5 Have you ordered a copy of your credit report in the past 12 months?Results: 72.80% Yes , 27.20% - No

Q6 How knowledgeable are you of the National Economic Empowerment’s “Sister-Nomic$ Program” and its principles?Results: 49.60% Very knowledgeable & can describe, 23.20% - Somewhat & read resolutions, 16% - Head about/ vaguely familiar, 11.20% - Not familiar with

Q7 What are your local community/service area’s greatest Economic/Financial disparities?Results: 30.40% -Homeownership/Affordable Housing, 21.60% - Lack of Financial literacy, 18.40% - Livable wage/Wage Inequality, 9.60% - Homelessness, 8.80%-Under-employment/Unemployment, 6.40 % - Consumer/Bad Credit, 4.80% Employment Readiness, 0% - Lack of Health Insurance

Q8 How does your chapter evaluate the impact of your programs and initiatives in your community (metrics)?Results: 50% - Pre/Post-Evaluations, 45.16% - Survey/Questionnaires, 35.48% - Increased Participant attendance, 29.03% Observations, 21.77% -Storytelling/Testimonials,6.45% Other

Q9 What tools/resources can your chapter most benefit from the National Economic Empowerment Committee, in facilitating the “Sister-Nomic$ Program” to your community?Results: 53.60%- Webinars, 53.60% - Program curriculum, 40.80 % Pamphlets, Marketing material, 33.60% Coaching, 40.80% PP presentation, 28.80% Templates, 3.2% - Other

Summarized Results : NCBW EE Survey

Q10 What Economic Empowerment program initiatives does your chapter currently have in place? (As it relates to the National focus areas: Livable wage/Employment opportunities, Affordable housing, Pay equity, African- American Women-owned businesses)?Results: 80.83% Financial literacy, 33.83% Youth Programs, 31.67% Entrepreneurship Program, 25.83% Affordable Housing/Homeownership, 12.50% Job Fair/Employment Readiness, 7.50% Other

Q11 Exploring ways for NCBW to bridge the economic gap with Black Women, can your chapter leverage community/corporate partners that would provide/donate facility space, to render the “Sister-Nomic$” Economic Empowerment Program to participants?Results: 85.25% - Yes, 14.75% = No

Q12 If you answered yes to the previous question, please indicate what type of partner location. (i.e. church facility, non-profit agency, government agency, school(s), etc.)?Results: Church, School, Non-profits, Library, etc.

Q13 Do you have a second stream of income from a hobby/side pursuit?Results: 47.20% - Yes, 52.80 % - No

Q14 Are you interested in starting your own business?Results: 51.20% = Yes, 48.50% = No

Q15 Are you a Business owner/Entrepreneur?Results: 36.29% = Yes, 63.71 % - No

Q16 Interested in NCBW Members-only National Business owner/Entrepreneur’s Directory?Results: 70.80% = Yes, 29.20% = No

Q17 Interested in NCBW National website (for a nominal fee)?Results: 55.75% = Yes, 44.35% = No

Summarized Results : NCBW EE Survey

PART IV:S ister -Nomic$CURRICULUM

SECTION 1:

OBJECTIVES

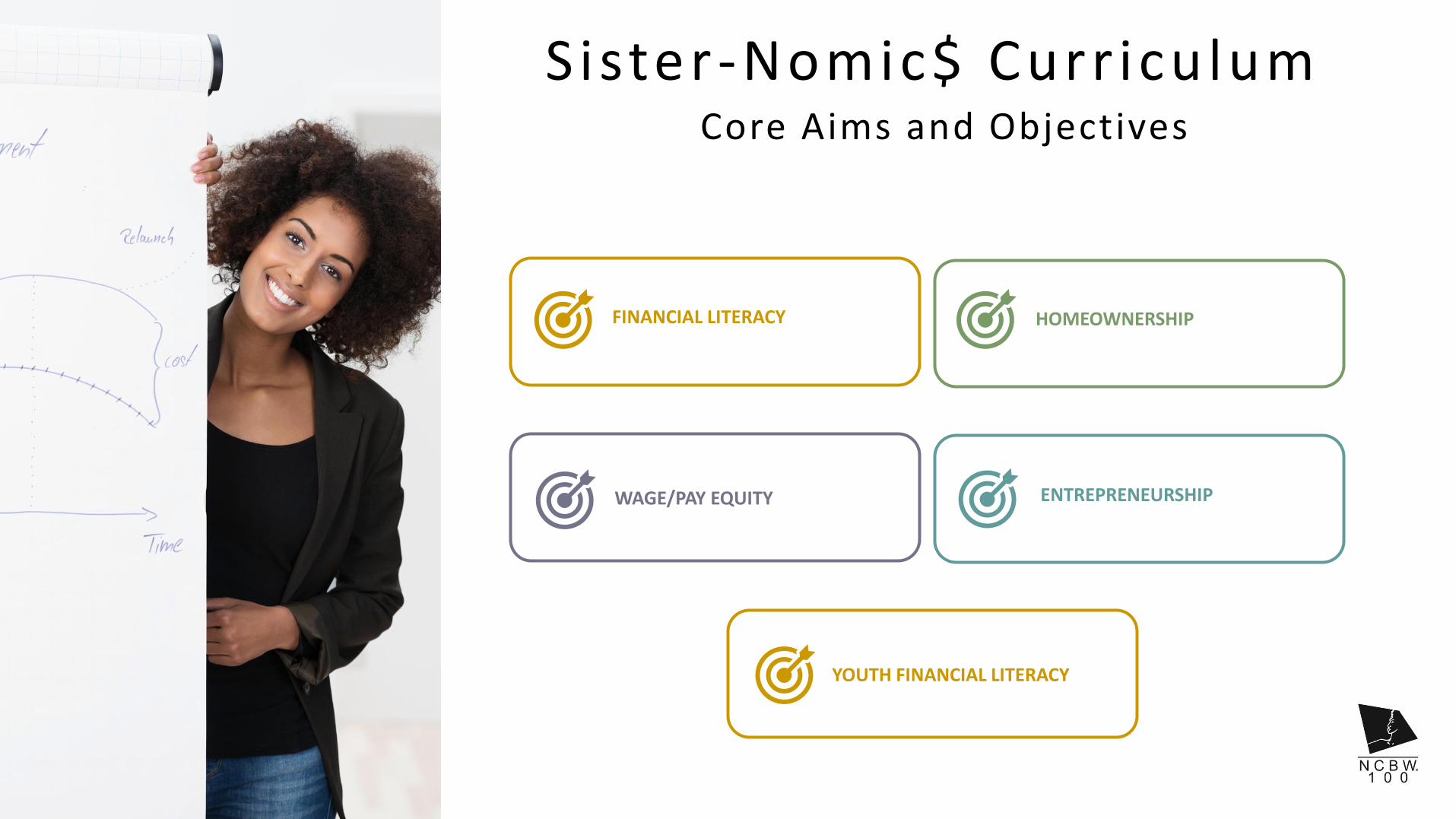

FINANCIAL LITERACY

Sister -Nomic$ Curr iculum Core Aims and Objectives

HOMEOWNERSHIP

WAGE/PAY EQUITY ENTREPRENEURSHIP

YOUTH FINANCIAL LITERACY

SECTION 2:

CURRICULUMMODULES

Sister-Nomic$ Curr iculum

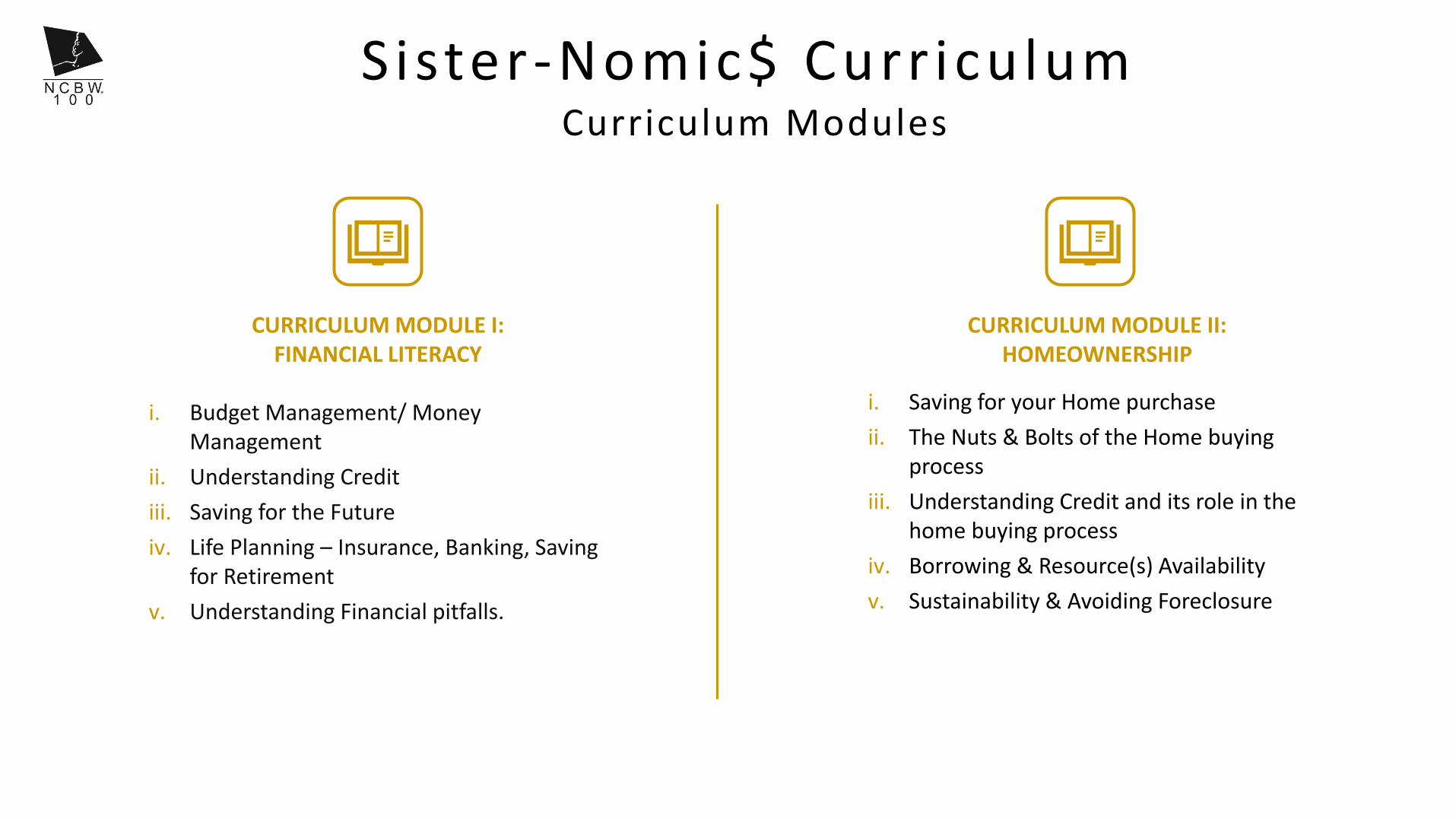

i. Budget Management/ Money Management

ii. Understanding Credit

iii. Saving for the Future

iv. Life Planning – Insurance, Banking, Saving for Retirement

v. Understanding Financial pitfalls.

CURRICULUM MODULE I: FINANCIAL LITERACY

CURRICULUM MODULE II: HOMEOWNERSHIP

i. Saving for your Home purchase

ii. The Nuts & Bolts of the Home buying process

iii. Understanding Credit and its role in the home buying process

iv. Borrowing & Resource(s) Availability

v. Sustainability & Avoiding Foreclosure

Curriculum Modules

Sister-Nomic$ Curr iculum

i. Individual Development Plan/ Continuous improvement/ education

ii. Strategic Planning – Recording your accomplishments and experiences from start to finish

iii. Knowing your worth in the Labor Market

iv. Interviewing preparation to Talk the Talk.

v. Wage Negotiation- Show Me the Money!

vi. Preparing Black girls for their careers at every age (middle, high school and college)

CURRICULUM MODULE III: WAGE/PAY EQUITY

CURRICULUM MODULE IV: ENTREPRENEURSHIP & SMALL BUSINESS OWNERSHIP

i. Roadmap from side Hustle to thriving business.

ii. Borrowing/Seed money

iii. Business planning – Scaling your business & profitability.

iv. Resiliency & Grit – Managing self-care & stress

v. Small Business Tools & Resources –SCORE, SBA, Business Incubators

vi. Effectively Networking to Net the Work!

vii. Business Mentors – Women-to-Women/ Gleaning from the Best!

Curriculum Modules (cont ’d)

Sister-Nomic$ Curr iculum

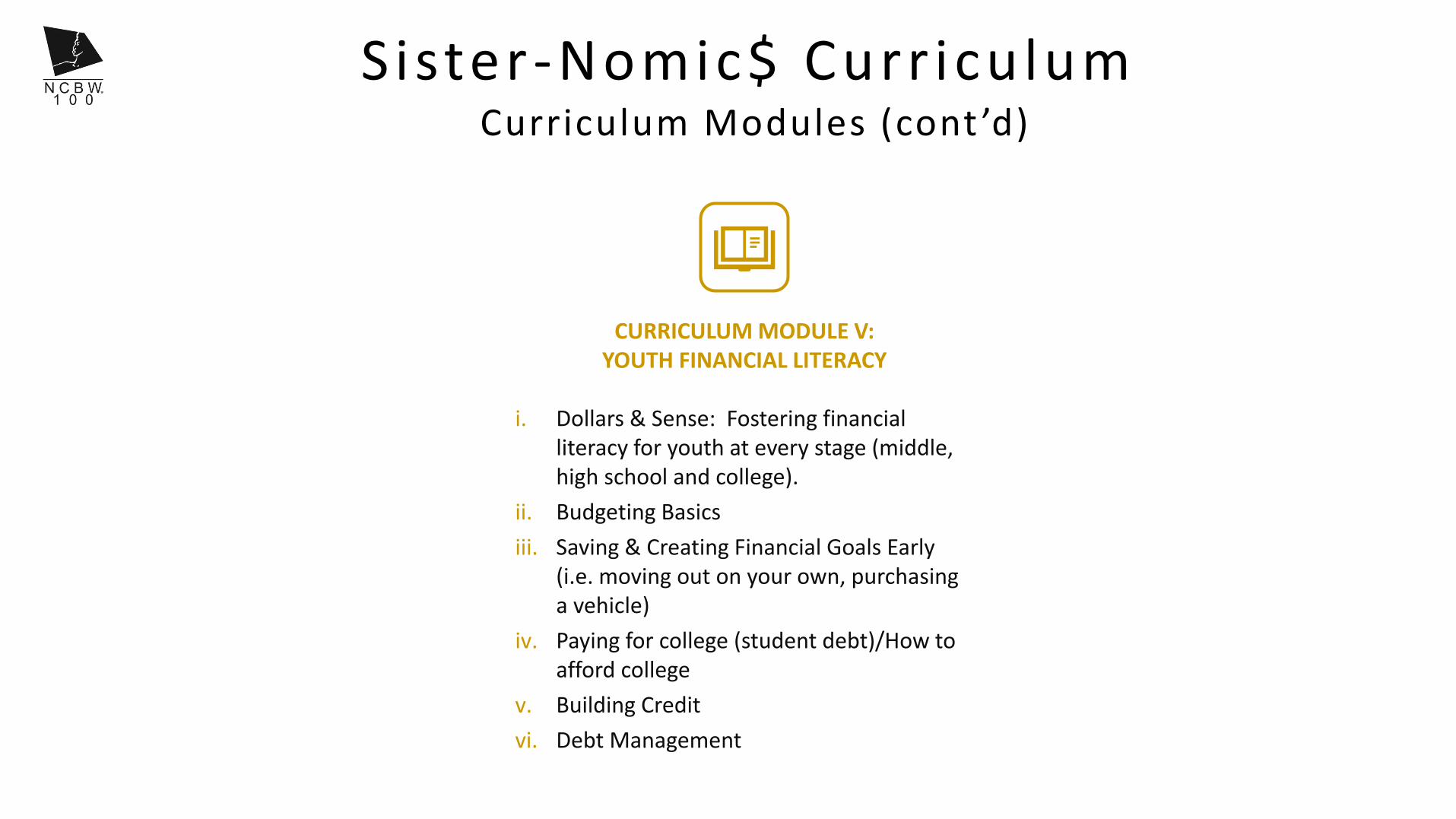

i. Dollars & Sense: Fostering financial literacy for youth at every stage (middle, high school and college).

ii. Budgeting Basics

iii. Saving & Creating Financial Goals Early (i.e. moving out on your own, purchasing a vehicle)

iv. Paying for college (student debt)/How to afford college

v. Building Credit

vi. Debt Management

CURRICULUM MODULE V: YOUTH FINANCIAL LITERACY

Curriculum Modules (cont ’d)

SECTION 3:

STANDARDS& REQUIREMENTS

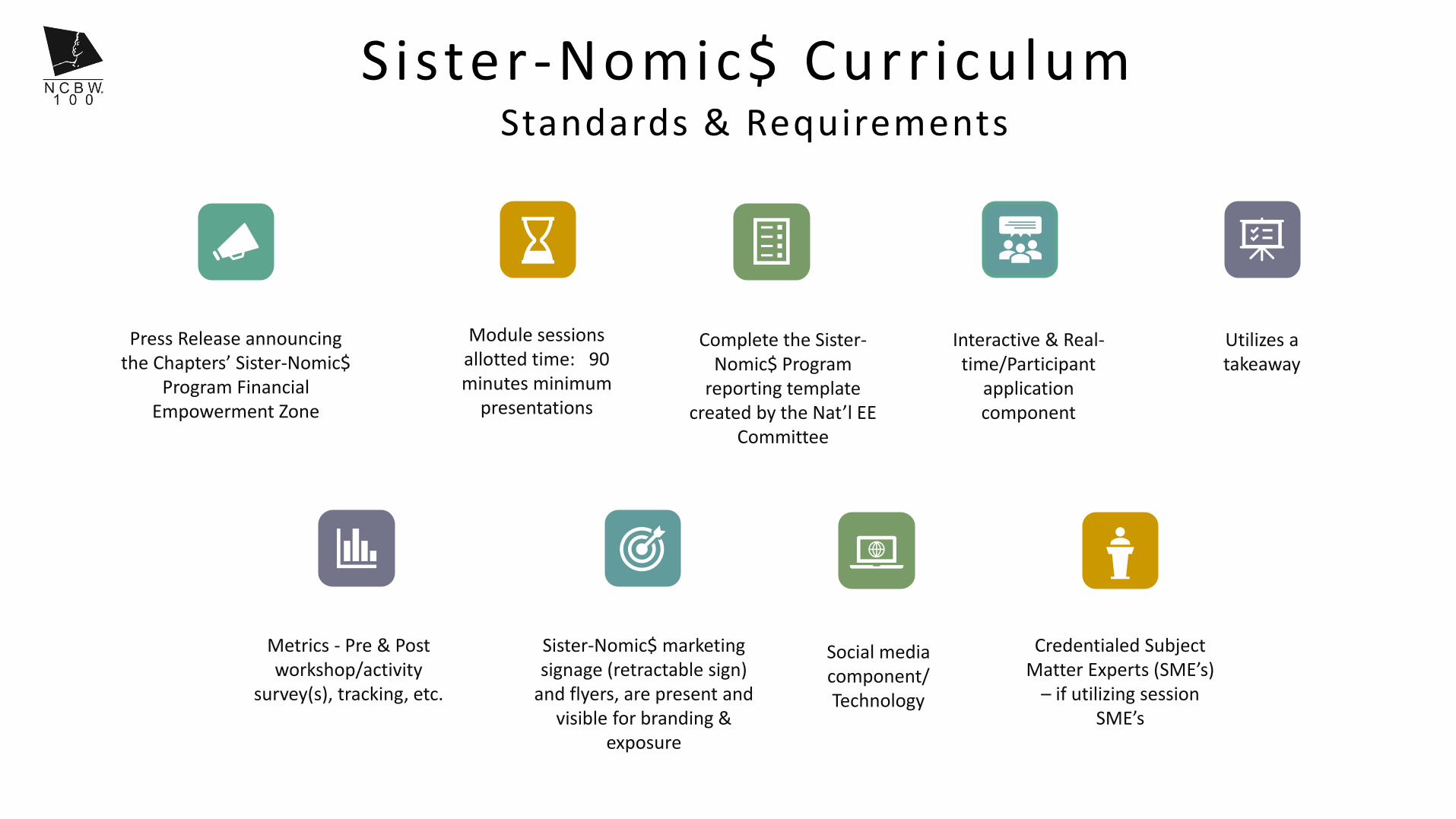

Module sessions allotted time: 90 minutes minimum

presentations

Complete the Sister-Nomic$ Program

reporting template created by the Nat’l EE

Committee

Interactive & Real-time/Participant

application component

Utilizes a takeaway

Sister-Nomic$ Curr iculum

Sister-Nomic$ marketing signage (retractable sign)

and flyers, are present and visible for branding &

exposure

Social media component/ Technology

Credentialed Subject Matter Experts (SME’s)

– if utilizing session SME’s

Metrics - Pre & Post workshop/activity

survey(s), tracking, etc.

Standards & Requirements

Press Release announcing the Chapters’ Sister-Nomic$

Program Financial Empowerment Zone

SECTION 4:

CURRICULUMDELIVERY

Report Format Guidelines

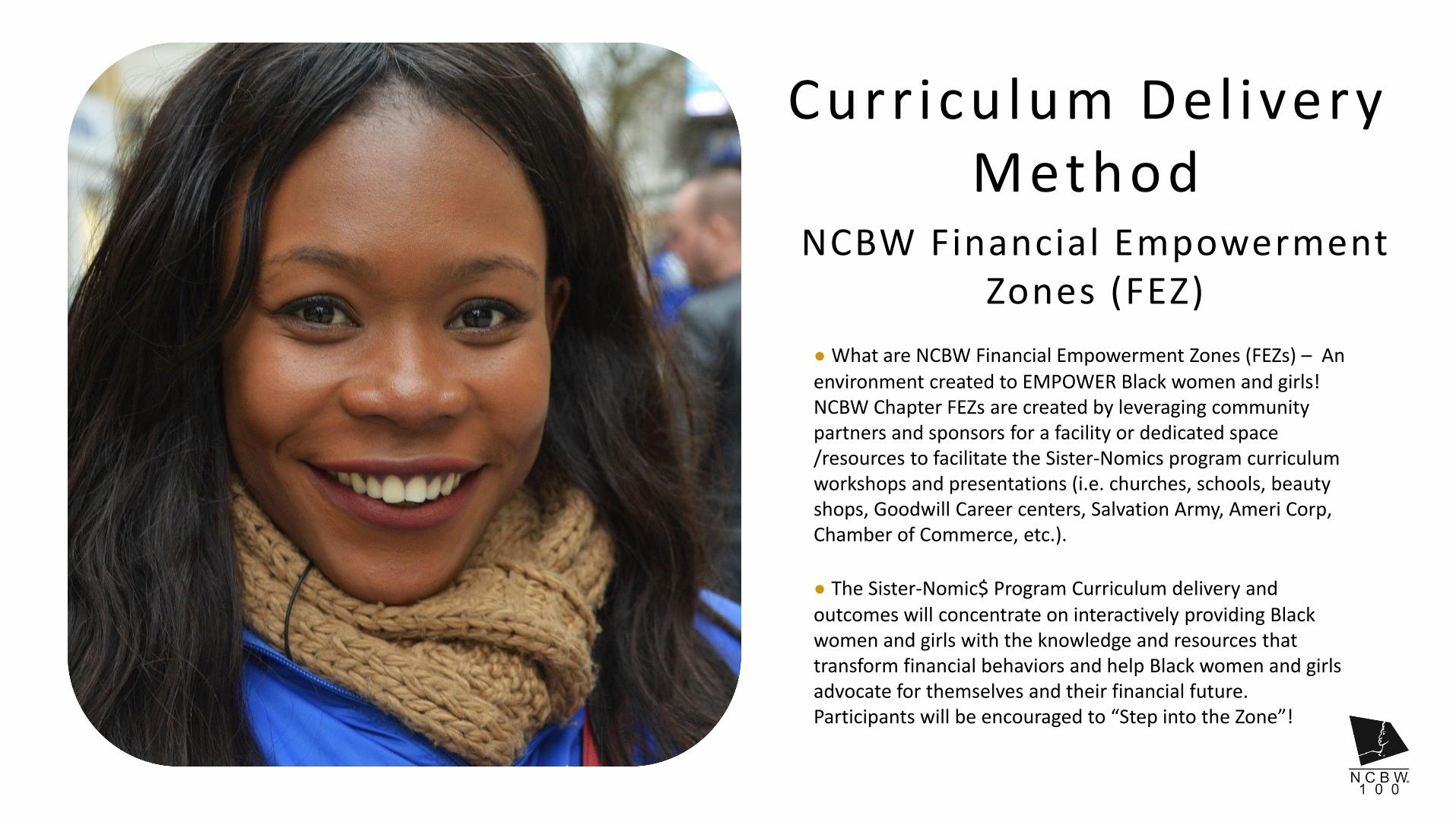

Curr iculum Del ivery Method

● What are NCBW Financial Empowerment Zones (FEZs) – An environment created to EMPOWER Black women and girls! NCBW Chapter FEZs are created by leveraging community partners and sponsors for a facility or dedicated space /resources to facilitate the Sister-Nomics program curriculum workshops and presentations (i.e. churches, schools, beauty shops, Goodwill Career centers, Salvation Army, Ameri Corp, Chamber of Commerce, etc.).

● The Sister-Nomic$ Program Curriculum delivery and outcomes will concentrate on interactively providing Black women and girls with the knowledge and resources that transform financial behaviors and help Black women and girls advocate for themselves and their financial future. Participants will be encouraged to “Step into the Zone”!

NCBW Financial Empowerment Zones (FEZ)

FEZ Partner Case Study #1: Church

Sister-Nomic$ F inancia l Empowerment Zones (FEZ)

The NCBW-Metro Money Chapter (MMC) is leveraging their relationship with The Helping Hands Church, who is eager to have their various Women's’ Groups and the local community to participant in the NCBW Sister-Nomic$ Program Initiative. The Helping Hands Church has agreed to provide the fellowship hall facility as meeting space, including tables, chairs and some limited a/v capacity. Additionally, the church has agreed to promote attendance to the Sister-Nomic$ program’s Financial Empowerment Zone, to their congregation and in their community bulletin.

The NCBW-MMC has agreed to announce the partnership and promote the NCBW Sister-Nomic$ Initiative to the community via a press release. The Chapter will facilitate the Financial Empowerment Zone every other Thursday night 7:00 pm - 8:30 pm, utilizing the subscribed Sister-Nomic$ Curriculum and program material. NCBW-MMC will ensure that the Sister-Nomic$ Financial Empowerment marketing signage (retractable sign) and flyers, are visible for branding purposes. NCBW-MMC will provide the Sister-Nomic$ study materials, speakers, facilitate workshops, subject matter experts and host interactive sessions to participants.

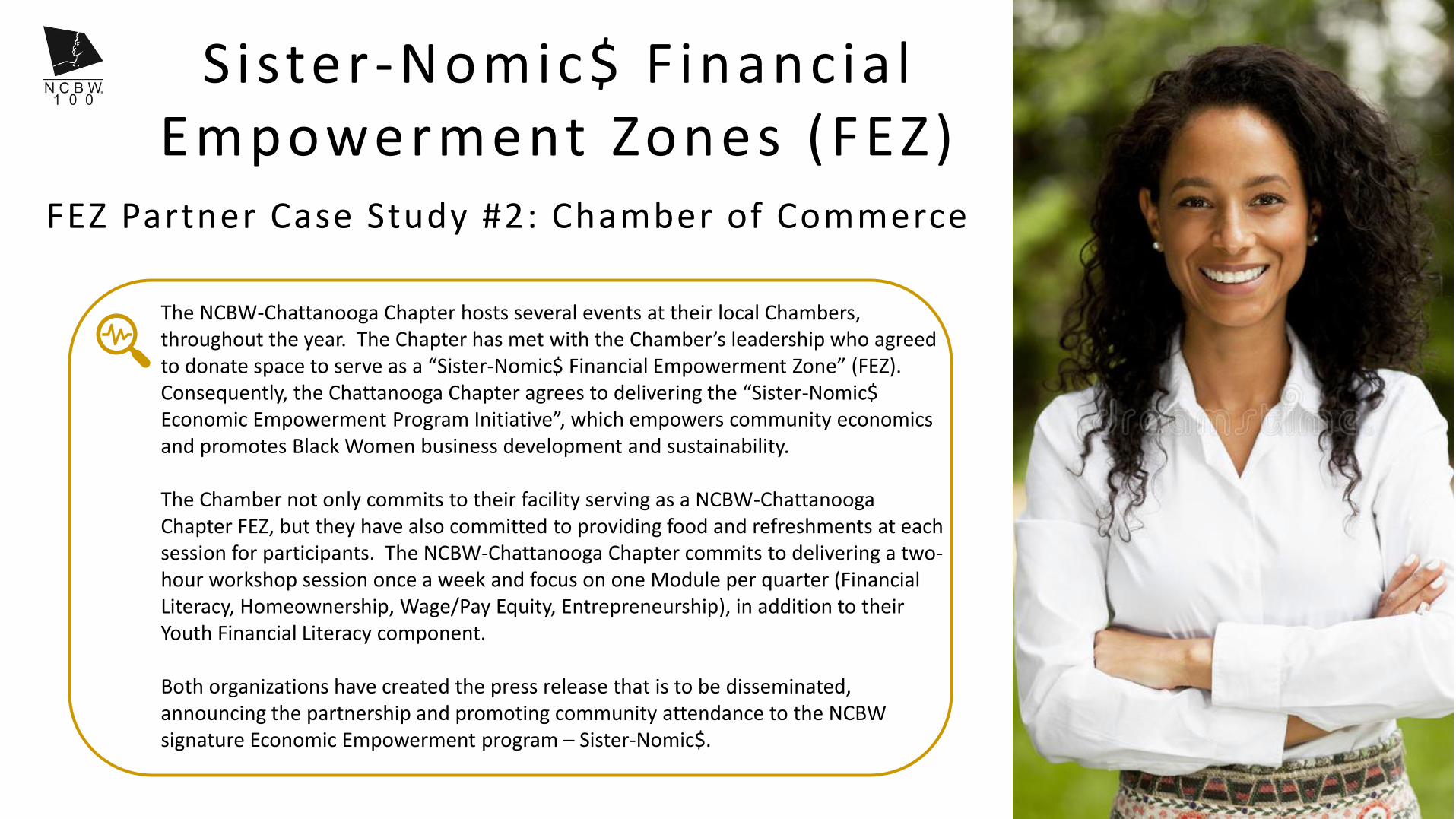

FEZ Partner Case Study #2: Chamber of Commerce

Sister-Nomic$ F inancia l Empowerment Zones (FEZ)

The NCBW-Chattanooga Chapter hosts several events at their local Chambers, throughout the year. The Chapter has met with the Chamber’s leadership who agreed to donate space to serve as a “Sister-Nomic$ Financial Empowerment Zone” (FEZ). Consequently, the Chattanooga Chapter agrees to delivering the “Sister-Nomic$ Economic Empowerment Program Initiative”, which empowers community economics and promotes Black Women business development and sustainability.

The Chamber not only commits to their facility serving as a NCBW-Chattanooga Chapter FEZ, but they have also committed to providing food and refreshments at each session for participants. The NCBW-Chattanooga Chapter commits to delivering a two-hour workshop session once a week and focus on one Module per quarter (Financial Literacy, Homeownership, Wage/Pay Equity, Entrepreneurship), in addition to their Youth Financial Literacy component.

Both organizations have created the press release that is to be disseminated, announcing the partnership and promoting community attendance to the NCBW signature Economic Empowerment program – Sister-Nomic$.

PART V:HOMEOWNERSHIP

SECTION 1:

OVERVIEW

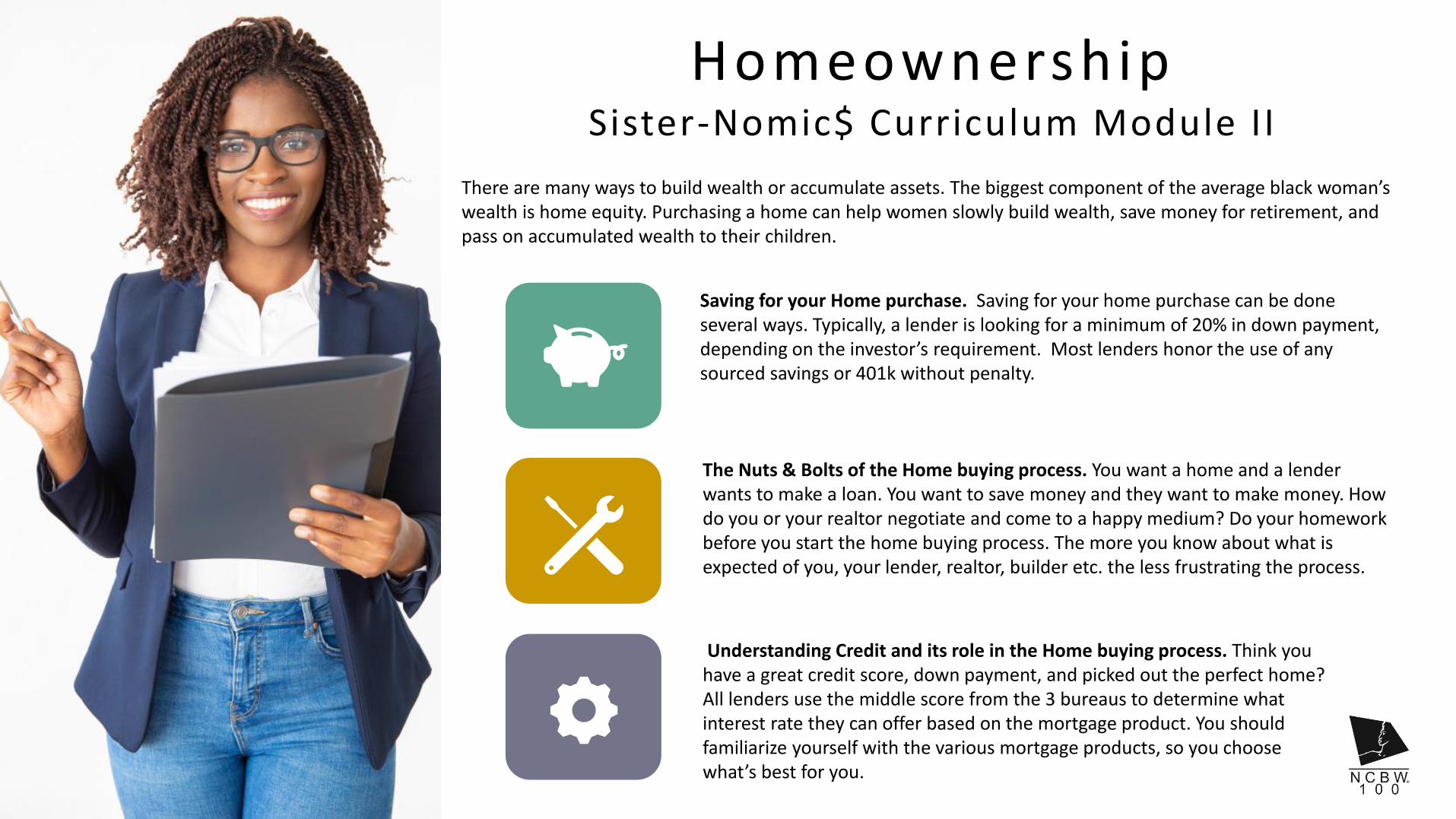

HomeownershipSister-Nomic$ Curriculum Module II

Saving for your Home purchase. Saving for your home purchase can be done several ways. Typically, a lender is looking for a minimum of 20% in down payment, depending on the investor’s requirement. Most lenders honor the use of any sourced savings or 401k without penalty.

The Nuts & Bolts of the Home buying process. You want a home and a lender wants to make a loan. You want to save money and they want to make money. How do you or your realtor negotiate and come to a happy medium? Do your homework before you start the home buying process. The more you know about what is expected of you, your lender, realtor, builder etc. the less frustrating the process.

Understanding Credit and its role in the Home buying process. Think you have a great credit score, down payment, and picked out the perfect home? All lenders use the middle score from the 3 bureaus to determine what interest rate they can offer based on the mortgage product. You should familiarize yourself with the various mortgage products, so you choose what’s best for you.

There are many ways to build wealth or accumulate assets. The biggest component of the average black woman’s wealth is home equity. Purchasing a home can help women slowly build wealth, save money for retirement, and pass on accumulated wealth to their children.

Report Format Guidelines

Homeownersh ip

● As we all know, a mortgage is a large financial commitment usually over a lot of years. In fact, the interest you pay over the course of a 30-year mortgage nearly doubles what you borrow! Outside of wanting your very own home, typically a home is a great investment as usually you build equity as pay it off.

● There are several ways to build equity in your home. The larger your down payment, the less you owe on the mortgage you just signed up for. If the loan amount is lower than the purchase price, you have immediate equity.

● If you want to purchase a home, but do not have enough money saved to pay for a large down payment and closing costs, a down payment assistance program might just be what you need to make the dream of home ownership a reality.

● Down payment assistance programs are Government and City sponsored programs that are available to help home buyers with their down payment and closing costs for the home purchase.

Borrowing & Resource(s) Availability

Contact your lender as soon as you realize that

you have a problem.

Open and respond to all mail from your

lender.

Know your mortgage rights.

Understand foreclosure

prevention options.

Homeownership

Prioritize your spending.

Use your assets. Avoid foreclosure prevention companies.

Don’t lose your house to foreclosure recovery

scams!

Contact Us.

Sustainability & Avoiding Foreclosure

Don’t ignore the problem.

If you are unable to make your mortgage payment:

SECTION 2:

WELLS FARGOPROGRAMS

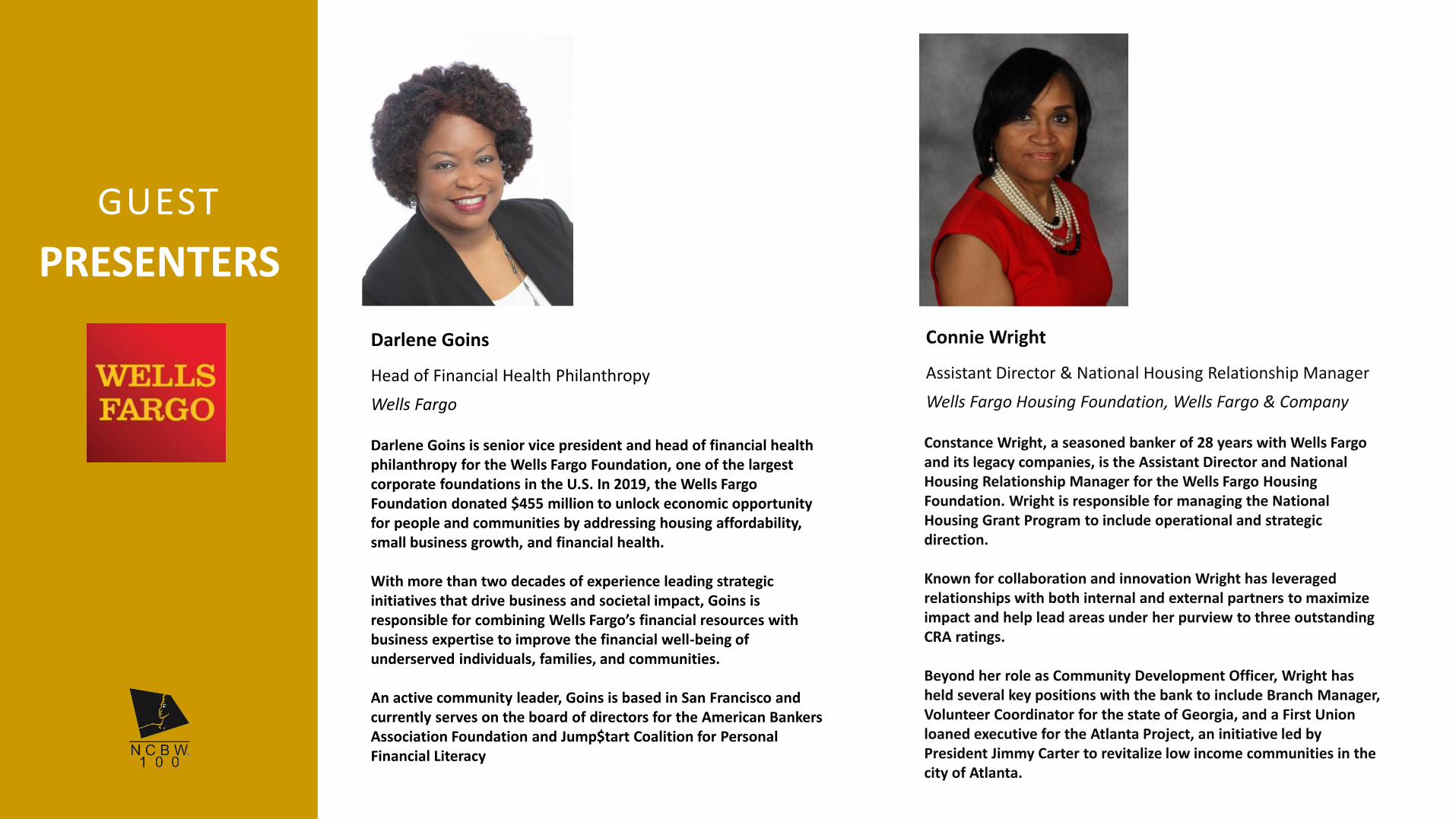

Connie Wright

Constance Wright, a seasoned banker of 28 years with Wells Fargo and its legacy companies, is the Assistant Director and National Housing Relationship Manager for the Wells Fargo Housing Foundation. Wright is responsible for managing the National Housing Grant Program to include operational and strategic direction.

Known for collaboration and innovation Wright has leveraged relationships with both internal and external partners to maximize impact and help lead areas under her purview to three outstanding CRA ratings.

Beyond her role as Community Development Officer, Wright has held several key positions with the bank to include Branch Manager, Volunteer Coordinator for the state of Georgia, and a First Union loaned executive for the Atlanta Project, an initiative led by President Jimmy Carter to revitalize low income communities in the city of Atlanta.

Assistant Director & National Housing Relationship Manager

GUEST

PRESENTERS

Darlene Goins

Darlene Goins is senior vice president and head of financial health philanthropy for the Wells Fargo Foundation, one of the largest corporate foundations in the U.S. In 2019, the Wells Fargo Foundation donated $455 million to unlock economic opportunity for people and communities by addressing housing affordability, small business growth, and financial health.

With more than two decades of experience leading strategic initiatives that drive business and societal impact, Goins is responsible for combining Wells Fargo’s financial resources with business expertise to improve the financial well-being of underserved individuals, families, and communities.

An active community leader, Goins is based in San Francisco and currently serves on the board of directors for the American Bankers Association Foundation and Jump$tart Coalition for Personal Financial Literacy

Head of Financial Health Philanthropy

Wells Fargo Housing Foundation, Wells Fargo & CompanyWells Fargo

PART VI:NEXT STEPS& SUMMARY

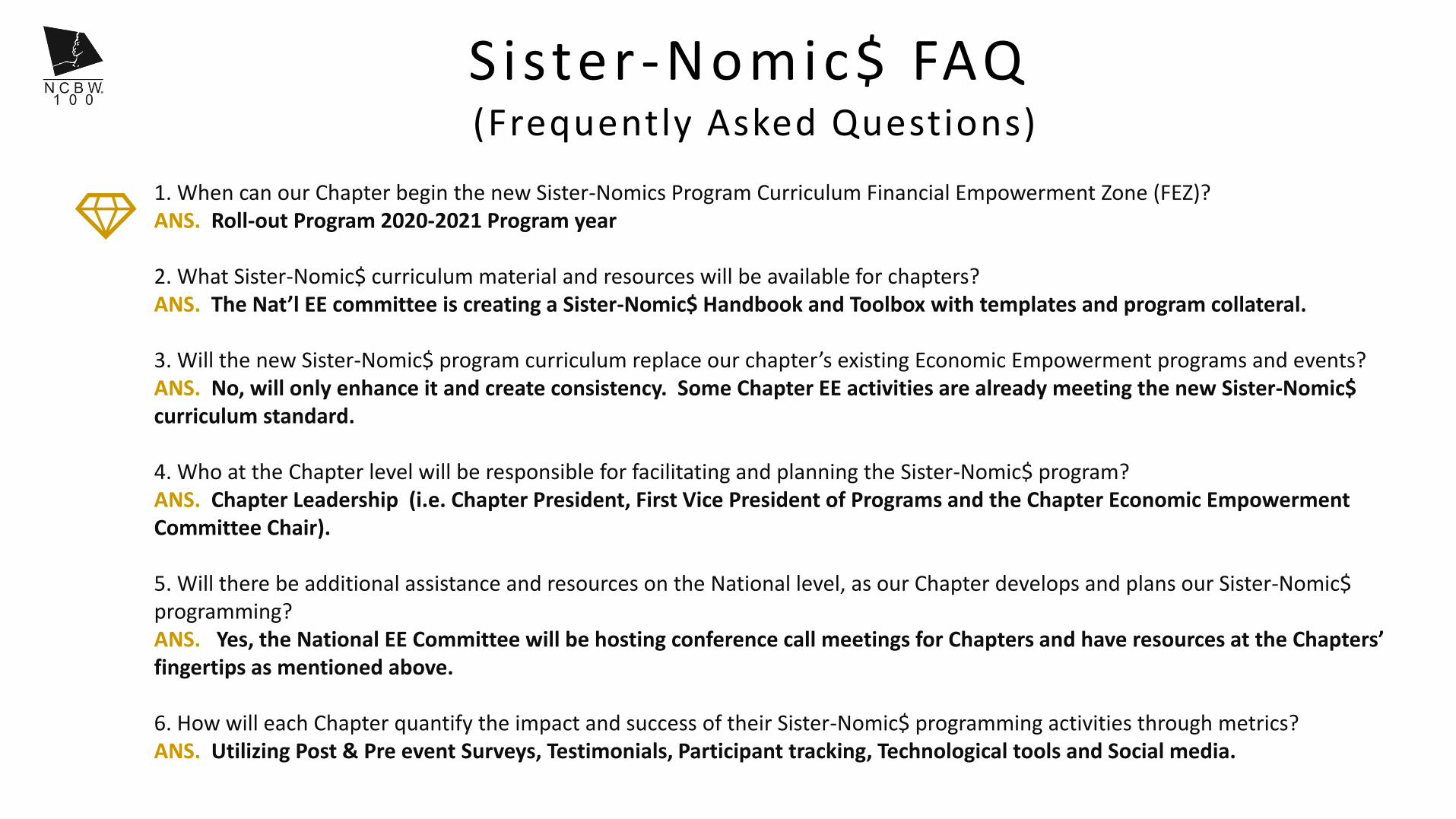

1. When can our Chapter begin the new Sister-Nomics Program Curriculum Financial Empowerment Zone (FEZ)?ANS. Roll-out Program 2020-2021 Program year

2. What Sister-Nomic$ curriculum material and resources will be available for chapters?ANS. The Nat’l EE committee is creating a Sister-Nomic$ Handbook and Toolbox with templates and program collateral.

3. Will the new Sister-Nomic$ program curriculum replace our chapter’s existing Economic Empowerment programs and events?ANS. No, will only enhance it and create consistency. Some Chapter EE activities are already meeting the new Sister-Nomic$ curriculum standard.

4. Who at the Chapter level will be responsible for facilitating and planning the Sister-Nomic$ program?ANS. Chapter Leadership (i.e. Chapter President, First Vice President of Programs and the Chapter Economic Empowerment Committee Chair).

5. Will there be additional assistance and resources on the National level, as our Chapter develops and plans our Sister-Nomic$ programming?ANS. Yes, the National EE Committee will be hosting conference call meetings for Chapters and have resources at the Chapters’ fingertips as mentioned above.

6. How will each Chapter quantify the impact and success of their Sister-Nomic$ programming activities through metrics?ANS. Utilizing Post & Pre event Surveys, Testimonials, Participant tracking, Technological tools and Social media.

Sister-Nomic$ FAQ(Frequently Asked Questions)

Complete the Sister-Nomic$ Toolbox to consist of: Sample MOU, Sample Press Release; Program Templates

Hosting Chapter EE Webinars, conference calls and Chat sessions

Sister-Nomics program handbook

Creating the NCBW Members-Only Entrepreneurs & Small Business Directory

Next Steps:National Economic Empowerment Committee

CONCLUSION:

BRINGING IT ALL TOGETHER

Summary Overview

• Embrace, enact, and encourage the Sister-Nomic$ philosophy and principles in your lives, chapters, and community

Sister-Nomic$ is the Solutions

• Understand the negative financial and emotional impacts of SBWS and resist/reject the trope

SBWS is Keeping Us Poor!

• Familiarize yourself with the Sister-Nomic$ curriculum, standards & requirements, and delivery methods

Curriculum

Q & A

THANK YOU FOR JOINING

Money Moves : Gett ing B lack Women in the B lack