money coach program 2016-2017 group coach workbook · job i’m interested in _____ (examples of...

TRANSCRIPT

Money Coach Program 2016-2017

Group Coach Workbook

Program Manager: Stephaine Crosley [email protected]

414-273-8101 www.makeadifferencewisconsin.org

1

My Money Coach Students

Name Email Cell Interests

2

2016-2017 Money Coach Calendar

Sep Oct Nov

Dec Jan Feb

Mar Apr May

10th : Celebration Event

3

Session (90 minutes) Session Structure and Agenda Materials Needed

Session One

1. Welcome and coach introduction2. Complete Student Pre-Survey2. Review Student Agreement3. Collect signed docs( student agreement, consent form, credit union/bank docs)4. Review structure of session5. Coaches conduct 10-12 minute one-on-ones with each of their 6 students6. Group coach helps students work on their College and Career Readiness Roadmap7. Homework assignment reviewed. (Expense tracking)

Materials:1. Student Workbooks2. Coach Workbooks2. Student Profile (Pre-Survey)3. Student Interview Questions4. Consent Forms5. Credit Union/Bank Forms6. Name Tents

Session Two-Eight Structure

Get access to computers for every session. Students need to actively work on their budgeting as well as monitoring their bank account using online banking. Building an activity where students are creating a realistic budget for the path they will choose after graduation.

Kickoff

Begin with a 5 minute check-in question or activity.♦ Get students active early♦ Gauge how they are feeling♦ Have some fun♦ Create your own check-in questions or activities or choose from the list provided

1. Check-in Questions

Agenda

♦ How one-on-ones will be handled today♦ Primary learning activity ♦ Homework and housekeeping♦ Money Moment: Share or ask students to share a positive money moment

Coach/Student One-on-Ones

♦ Coaches should conduct these every session. (10-12 minutes per student) ♦The key areas of focus are: 1. Getting to know what is important in their life personally. 2. Continuously review their College and Career Readiness Roadmap. 3. Review their expense tracking and budget worksheet. 4. Reviewing their savings account balance and transaction activity.♦ Session 4 and 7: Complete student progress report.

1. Coach Tool: Student Check-in Report2. College and Career Readiness Roadmap3. Expense Tracking Worksheet4. Budget4. Savings Account Review: report from financial institution to be provided. (Have student pull up account online or mobile if appropriate.) 5. Student Progress Report

Group Coach: Lesson/Activity

♦ Group Coach begins financial education lesson. Lesson topics may be a continuation of the lesson from the previous session or new depending on the readiness of students.

Session 2

Money Sense: Customized "Check It Out":1. Field Trip to bank or credit union to open a savings and checking account, enroll in online and mobile banking, and deposit a check.2. Discussion of opening and managing a bank account and avoiding check cashing stores.

1. Outline of Check it Out topics to cover.2. Checking account simulation activity3. Prezi4. Name Tents

Session 3

Continue "banking" lesson from session 2 if necessary, then move to: Money Sense: Customized "Bank Your Future"1. Review select concepts from Bank Your Future.2. Complete "Young Adult Budgeting Activity".3. Introduce Money Coach Budget and have student's begin developing their individual budget they will update each month.

1. Outline of Bank Your Future topics to cover.2. Young Adult Budgeting activity (hard copy and electronic version)3. Prezi4. Expense Tracking Worksheet5. Budget

Session 4

Continue "Bank Your Future" lesson from session 3 if necessary, then move to: Money Sense: Customized "To Your Credit" lesson.1. Review select concepts from To Your Credit.2. Complete the loan officer activity.3. One-on-one coaches complete student progress reports.

1. Outline of To Your Credit topics to cover.2. Loan Officer activity3. Prezi4. Student Progress Report

Session 5Continue "To Your Credit" lesson from session 4 if necessary, then move to: 1. Tax Lesson

1. Tax Activity

Session 6 Money Path (will be lead by a trained volunteer and assisted by group coach) 1. Money Path student workbook

Session 7

1. Budgeting for post graduation. Students create a realistic budget for the path they will choose after graduation. 2. Students identify topics for discussion at final session.3. One-on-one coaches complete student progress reports.

1. Young adult budget handouts2. Student Progress Report

Session 8

1. All coaches facilitate open discussion of topics identified in previous month. Get students ready to go out and live independently.2. Coaches provide students with an uplifting send off message!3. Coaches remind students of May 10th event and details

1. List of items students want to discuss2. Student Account Balance Report

Money Coach Event May 10, 2017. Celebration Event (Messmer High School)

Money Coach Session Structure

Session 1 College and Career Readiness Roadmap

In session one, you and the one – on – one coaches will be meeting the students for the first time.

Building rapport is key to engaging and reaching your new Money Coach students. Hold a brief planning discussion with your fellow coaches ahead of this session and work on how you want to collaborate to deliver your introductions.

The Money Coach Program Manager will kick off the first session by welcoming everyone, completing a brief overview of the program and facilitating any housekeeping items. This will take approximately 10 minutes and then the session will be turned over to the coaches.

Coach Instructions

1. Please incorporate the following into the introduction.

• All coaches should take a few minutes to introduce themselves. Be sure to share a little about yourself personally and professionally, and why you are a money coach.

• Have a little fun with a check in question or activity. • Have students introduce themselves and what they are looking forward to learning more about

so they develop strong financial skills and habits.

2. Introduce the College and Career Readiness Roadmap. Be sure to explain to students what it is and why we are having them complete it. Here are a few talking points.

• Understanding what path you have chosen or are considering choosing after high school will allow coaches to better customize their coaching for each student.

• Building savings habits are critical. We are asking each of you to save at least $200 of your Money Coach Scholarship to help pay for a college or career expense you will have in the future.

• What do you want your coach to help you with to get ready for your college or career path?

3. The group coach should ask all students to complete the roadmap. The one – on – one coaches should begin meeting individually with each of their students.

The group coach should work the room and check – in with students as they are completing their roadmap. The goal is to have them completed prior to leaving this session.

PREP NOTES

5

Session 1 College and Career Readiness Roadmap

A. Amount I will save by the end of the program. ($200

minimum) B. How I will save. C. Amount I need to save per

month for 8 months.

$____________

Scholarship: On my own: (job, allowance, money from parent)

$________

Total Savings Goal ÷ 8 months = $________ per month

Student Name: High School:

Grade: Money Coach Participant: New Returning

College: Continue my education by attending college Type of school: 2 year 4 year Career: Enter the workforce full time Job I’m interested in ___________________

(Examples of items or expenses specific to your college or career path might include the following: a laptop to help with school work, book fees, dorm/apartment necessities, new clothes or supplies for a job, a security deposit for apartment, etc.)

My goal is to save for… _______________________________________________________

___________________________________________________________________________

STEP 1: Choose your path after high school.

STEP 2: Set a goal of saving at least $200 of your scholarship money to help you buy something or cover expenses related to your college or career path.

College AND Career READINESS ROADMAP

$_______

6

Session 1 College and Career Readiness Roadmap

Navigating the college process o Choosing a school o Applying o Paying for tuition, school books, supplies o Managing my student life

Notes ____________________________________________________________________

__________________________________________________________________________

Living independently (at school, home with family, or in an apartment or flat) o Finding housing o Understanding a rental lease o Creating a budget o Being responsible with paying bills, caring for my place, grocery shopping, safety, etc.

Notes ____________________________________________________________________

__________________________________________________________________________

Getting a part time job during high school o Job search o Writing a resume o Applying and making a good first impression o Interviewing o Getting ready for my first day

Notes ____________________________________________________________________

__________________________________________________________________________

Getting a full time job after high school graduation o Assessing my skills and where I would like to improve o Exploring opportunities: What do I want to do? o Acquiring initial employment while I pursue my employment goal in an industry I am interested in o Writing a resume o Applying and making a good first impression o Interviewing o Getting ready for my first day

Notes ____________________________________________________________________

__________________________________________________________________________

Other ___________________________________________________________________

__________________________________________________________________________

STEP 3: To help me prepare for my college or career path, I would like my coach to help me with the following:

7

Banking Bank and/or Credit Union representatives will be joining us at the Money Coach site for this session. The Money Coach Program Manager will facilitate this lesson. The agenda for this session is:

• Strength and safety of banks and credit unions

• Role of a personal banker/customer service representative

• Checking and savings accounts: What are they and how do they work?

• Terms of the account(s) students are opening

• How to deposit and withdraw funds from accounts

• Enroll in online banking and begin to learn how to use this as a tool for managing their account

• Learn about mobile banking

Depending on the financial institution participating in this session, students may meet one – on – one with bankers to open their account(s). In some situations, the accounts will have been opened prior to the session.

The role of all coaches will be to assist students with enrolling in and utilizing online banking and answering questions.

Depending on time availability, short one – on – one sessions may occur between students and their one – on – one coach.

NOTE: You will continue the “Banking” discussion in the next session. Close this session with a message to have students use their account, spend time learning more about online banking and bring questions to the next session.

Be sure to review the agenda and activities for the next session. (See next page.)

PREP NOTES

8

Banking Follow – Up Discussion and Activities after students have used their account for 30 days:

1. Group Discussion

• Ask students to describe how they have used their accounts.

• Ask students if they have used online and/or mobile banking and to describe how they are using those

tools.

• Open up the floor for student questions

2. Online Banking Activity

• Have students sign in to their online banking account.

• Ask students to complete the following:

o Review account balance

o Review account activity

o Review how to transfer money from checking to savings (some students may only have a savings

account but they should review the functionality of transferring funds.

• Have students enroll in mobile banking if they want to have that tool available.

3. Complete the following segments of Make A Difference – Wisconsin’s ‘Check It Out’, Money Sense Lesson.

• Use the instructor notes for this lesson as your guide. (Separate workbook) Complete the following

segments of the lesson.

o Check Cashing Stores: pgs. 14-17

o Monitoring Transactions: pgs. 32-37

o Feel free to discuss other concepts from the lesson as needed based on student knowledge

level and questions they are asking about banking.

• You can review our online training curriculum module ahead of facilitating this lesson too. Just click on the link below to listen to a short (< 10 mins.) audio walk through of the lesson to get a feel for how to cover the material.

https://www.makeadifferencewisconsin.org/topic/check-it-out/ • Focus on getting students actively involved in the lesson. No lecture! Ask them what they know

about the topics before filling in knowledge gaps.

9

Banking • Access the link below to open the Prezi presentation for the ‘Check It Out’ lesson.

http://prezi.com/olkksjj_jxfs/?utm_campaign=share&utm_medium=copy

(You may also access the Prezi on www.makeadifferencewisconsin.org website. Log in to the “volunteer section to access the Prezi on the opening page or in the Resource Library.). The presentation will open in a small window (shown below), maximize this window by clicking the rectangle in the lower right corner.

Once the presentation window is maximized to “Fullscreen” use the Navigation Arrows > to move forward and back from slide to slide. Use the Navigation Slide Bar Dot when advancing more than one slide. You may also move from slide to slide using the left and right arrows on a computer keyboard.

PREP NOTES

Window Maximize

Navigation Arrows Navigation Slide Bar Dot

10

This Page Intentionally Left Blank

11

Budgeting Budgeting is a critical financial skill we want all students to master. Student learning objectives are

• Describe the components of a budget and the importance of maintaining one • Identify important expense and saving categories most young adults will need to plan for • Explain how to track expenses • Complete a budgeting activity

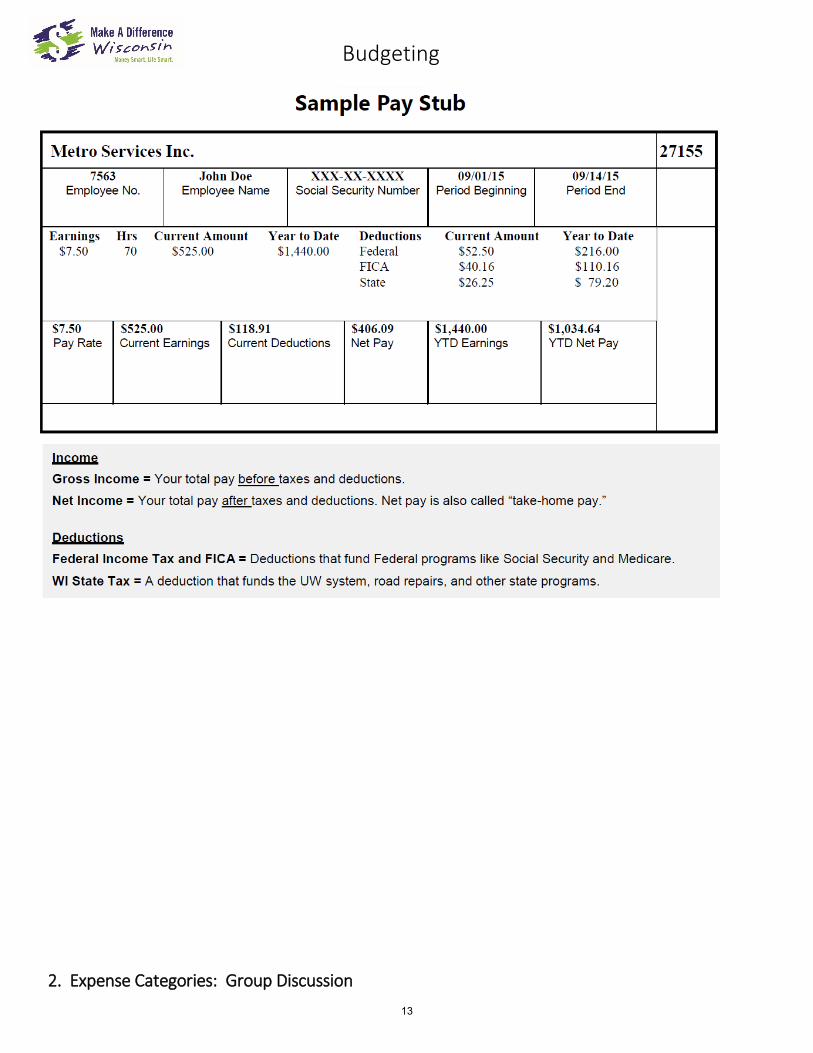

Complete the following with your group of money coach students. 1. Sample Pay Stub Activity

Distribute “Sample Pay Stub” Handout Discussion • Does anyone have a job? Where do you work? What’s on your paystub? • Ask students to identify John’s… • Hourly wage • Hours worked this pay period • Gross Pay • Net Pay

• Ask: What is automatically deducted from John’s paycheck? • Ask: What is FICA? (Federal Insurance Contributions Act)

o FICA has two parts: o Social Security: Intended to provide you with part of your retirement income. o Medicare: Provides you with health insurance when you turn age 65.

Key Points • A percentage of your income is taken out to cover FICA taxes.

• Federal and state taxes vary depending on your income and increase as your taxable income increases.

• Concerns related to long-range financing of Social Security: • Size of baby boom generation collecting benefits vs. size of the current workforce. A

smaller group of people is funding a larger group. • Increases in life expectancy. People are collecting benefits for a longer period of time.

• Long-term saving is required to reach retirement goals.

Stories, Examples & Notes

Transition: Now let’s have you identify different expense categories.

Social Security taxes Employer and employee 6.2% on wages up to $118,500 Medicare taxes Employer and employee 1.45% on all wages earned

For every $100 you earn, $7.65 goes to the federal government for FICA taxes.

12

Budgeting

2. Expense Categories: Group Discussion

13

Budgeting

Discussion (Ask for a student volunteer to be your scribe and write down student answers on the white board or chalk board.)

• What is a fixed expense and what is a variable expense? Ask students to give an example.

• Ask students to identify the types of expense categories most young adults will encounter once they are working full time and living independently.

• Fill in the gaps of expenses they may not have considered.

Key Points

Fixed and Variable Expenses

Expenses may be fixed or variable. A fixed expense is a recurring expense of approximately the same amount each period (month). These types of expenses are easy to budget for because they need to be paid each month. Examples include,

• mortgage or rent payments • automobile payments • insurance premiums • utility bills • cell phone, cable, internet bills

An expense is variable when you have control over when and how much you spend. Variable expenses generally do not recur each period or their amounts are very different from month to month. Variable expenses include,

• entertainment • dining out • groceries • vacation costs • purchases of clothing and household items

These expenses are variable because you have a choice regarding:

• IF you want to incur the expense, and/or • HOW MUCH you want to spend on the expense.

14

Budgeting

3. Needs vs. Wants Discussion

• Ask students to define the difference between a “need” and a “want”.

• Ask students to give examples.

Key Points

Needs vs. Wants

Regardless of whether your expense is fixed or variable, it can be categorized as either a need or a want. • The most basic definition of a need is that it is something you need in order to survive.

Examples of the most basic needs are food, shelter and clothing. Most of us have many other needs in our lives also. Examples might be o transportation o books for college o computer o furniture o sporting equipment o cell phone

• However, what type of item you choose to spend money on in any of these categories makes a big difference in our budget. You probably can get by just fine with a decent pair of jeans that cost less than $50 rather than a pair that cost $150. You probably even have a choice between lower cost used books rather than new for college.

• A want is something you really wish you had, but you can still go through your day-to-day

activities without it. For example, if you are furnishing your apartment or home you may want to purchase a high end leather sectional coach and the newest 60 inch Ultra HD TV.

In reality, you likely only need a comfortable new or used couch that cost a fraction of the leather sectional you want and you can probably get by with your current TV or a less expensive choice. Making these choices will help you save more for other short and long term needs.

15

Budgeting

• Spending money on wants is okay as long as you can afford them and understand the tradeoff of spending more than you need. Ask yourself if you could use the money for a more important need or goal that you have in your life. Strike a balance between needs and wants by setting spending and saving priorities.

Category Need Want

Groceries Chicken and ground beef Steak

Rent Clean, modest 1-bedroom

High-rise overlooking the lake

Dining Out Great sandwich and side

Lobster, appetizers, salad, desert

Car Used New

TV 40-inch HD flat screen with sound bar and Netflix

60-inch ultra HD with custom, full surround-sound and premium cable channels

First Home to Own 3-bedroom, 2-bath with garage and yard

4-bedroom, 3-bath, 3-car garage, entertainment room

Furniture Couch priced under $1000

Leather sectional at $4000

Stories, Examples & Notes

Transition: Now let’s have you identify different expense categories.

16

Budgeting 4. Savings Needs and Goals

Discussion

• Challenge students to think about all of their potential savings needs as young adults.

• Now ask students to identify potential savings goals/categories. Explain the importance of saving money on a regular basis to provide for the financial goals you want to obtain.

• Ask students what they would do if they need car repairs and didn’t have an emergency fund in place. Where would they get the money?

Key Points Review how to set and achieve a goal based on a establishing a savings plan!

Short-Term Goals (1–3 years) • Emergency fund: handle unexpected expenses or loss of income (keep 3–6 months of expenses saved).

• Near-term planned expenses: pay for known, upcoming purchases for college, home, car, vacation, gifts, etc.

o Example: Build an emergency fund Savings goal: $1800

Months to save: 12/mo.

Monthly savings required: $150

Intermediate-Term Goals (4–10 years) • Down payment to buy a car in 5 years. (Save for a portion of the cost so you can minimize your loan payment.)

• Down payment on a home in 10 years. (If possible, set a goal of saving 20% of the down payment to avoid paying private mortgage insurance. Otherwise, shoot for 10 %.)

o Example: Save for the down payment on a $150,000 home you plan to purchase in 10 years

Savings goal: $20,000

Years to save: 10

Monthly savings required to reach goal: $166

Stories, Examples & Notes

Transition: Now let’s have you identify different expense categories.

17

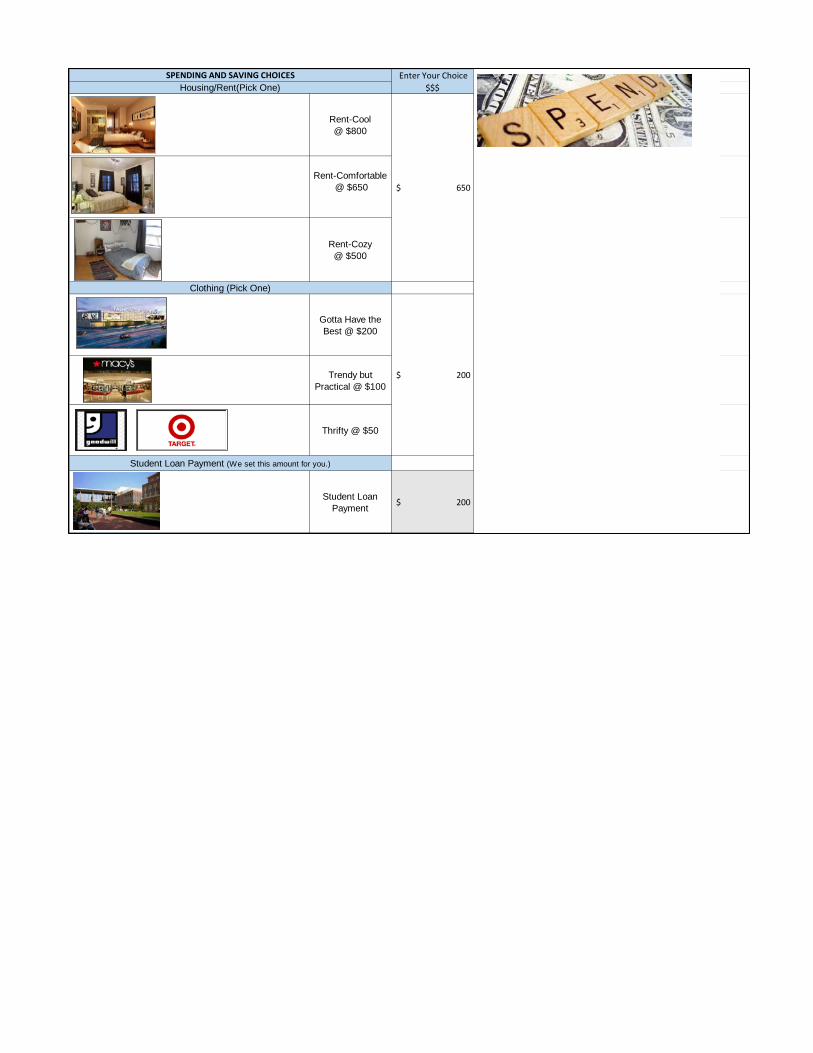

Budgeting 5. Complete the Young Adult Budgeting Activity

• Handout the activity worksheets if students will complete manually or have students open the excel document if they will complete it electronically. Students should type the following URL to access the document electronically.

makeadifferencewisconsin.org/for-students/

• Pull up the document on your computer and projector. • Review the instructions and give an example of how to choose and enter your choice for a spending

category. If students are using the excel version be sure to show them how to enter a spending or saving choice by clicking in the box and tying the dollar amount followed by hitting enter.

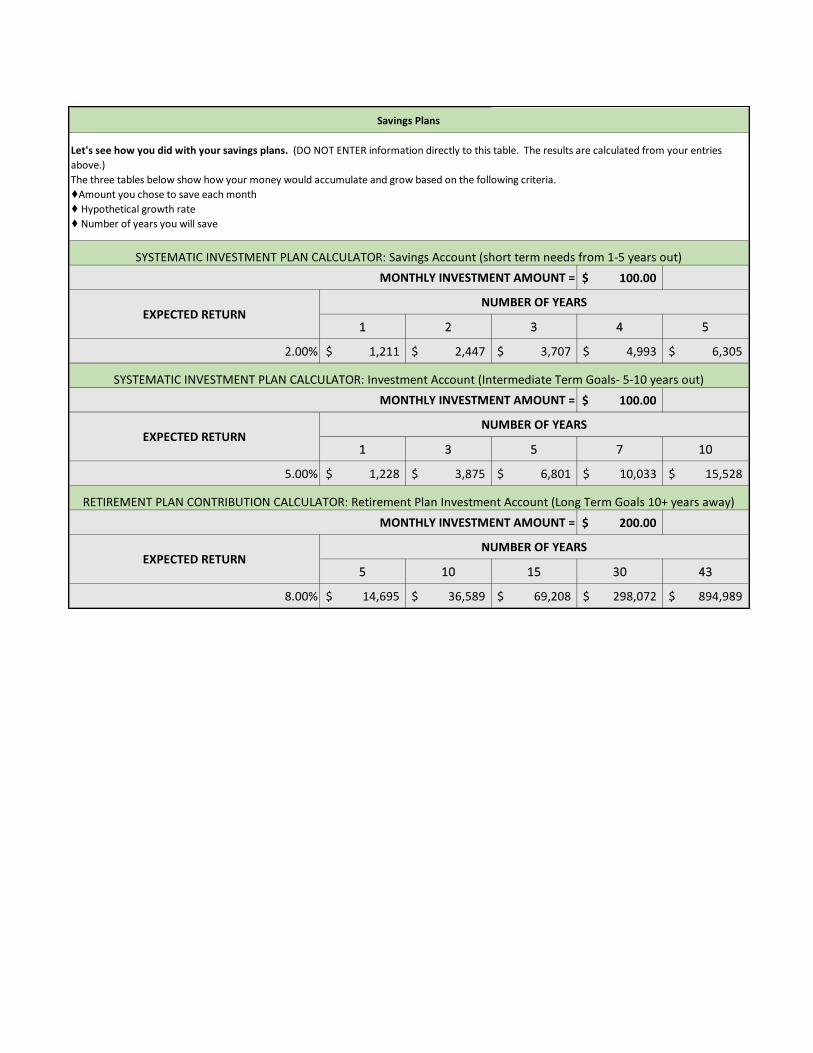

• Review the Budget format: o Income and taxes o Fixed and Variable Expense o Savings o Budget Surplus or Deficit( the goal is to have this number be close to zero)

• Savings Plans o At the end of the worksheet is a table listing savings plans. If students are using the excel version

of the budget worksheet, their savings totals will be automatically populated. If students are completing the worksheet manually, you can provide them with the answers by simply entering various dollar amounts on your electronic version and the students can write down their totals.

o Be sure to summarize the importance of Establishing short, intermediate and long – term goals and that saving regularly is the

only way to set aside money for future financial needs and goals The power of time, starting early and compounding for intermediate and long – term

goals

PREP NOTES

18

3,333$

Everybody pays this 6.20% amount to the government out of every paycheck. It is used to fund current and future social

security benefits.

FICA @ 6.20% of Income $ (207)

Everybody pays this 1.45% amount to the government out of every paycheck. Medicare is the federal health insurance program for people who are 65 or older.

Medicare @ 1.45% of Income $ (48)

This is the amount withheld from each paycheck and sent to the Internal Revenue Service. The amount you pay depends on your taxable income.

Federal Tax Withholding $ (269)

This is the amount withheld from each paycheck and sent to the state you live in. The amount you pay is based on your taxable income. Some states don't have a state tax. The tax for states that do ranges from approximately 3% - 13 % of your taxable income.

State Tax Withholding $ (104)

$2,705

Monthly Income and Taxes

Taxes (We calculated these for you. Be sure to review them for understanding.)

Gross Income (This is how much you get paid.)

Net Pay-Direct Deposit

Creating a budget that helps you plan your spending and saving wisely will put you on a path to financial success. It is the key to reaching your short and long term financial goals. Complete the budget simulation activity below to take a pracitce run. Where requested, enter a spending or savings amount. You have a list to choose from in many categories. Make the choice that closest matches your money personality. Once complete, determine if you have a suplus or deficit. Revise your budget until your budget is balanced ($0 surplus or deficit). Be sure you are saving money for the future to!

Budget Activity for a Young Adult

You earn $40,000 annually from your career which is $3333 monthly.

You pay Uncle Sam and the U.S. Governement taxes each paycheck.

Rent-Cool @ $800

Rent-Comfortable @ $650

Rent-Cozy @ $500

Gotta Have the Best @ $200

Trendy but Practical @ $100

Thrifty @ $50

Student Loan Payment $ 200

SPENDING AND SAVING CHOICES

Clothing (Pick One)

Enter Your Choice $$$

Student Loan Payment (We set this amount for you.)

Housing/Rent(Pick One)

$ 650

$ 200

You Name It! I'm Doing It! @

$300

Weekend Fun @ $200

Finding Cheap Fun @$100

Gas (Heat) $ 50

Electricity $ 35 Cable (Pick One)♦ Don't want it @

$0♦ Basic Cable @

$40♦ Preferred Cable

@ $80

$ 80

Internet (If you want it enter $40) $ 40

Cell Phone(Pick One)

♦ major carrier @ 60/mo.

Or♦ bargain carrier

20/mo.

$ 60

Savings Account (Short Term

Needs)Enter $50 - $200

$ 100

Investment Account

(Intermediate Needs for 5-10

Year Goals)Enter $50 - $200

$ 100

I'm not too worried about this at my

age.$0.00 per month

I guess I should start saving a little

for retirement.$100 per month

I'd like to get a jump on this and

start early.$200 per month

Entertainment (Pick One)

$ 300

Utilites are important services. Some you have to have and others, like cable, you get to choose if and what level of service

you want.

Utilities

Savings (Enter Your Amounts)

You can paint a picture of what retirement looks like for yourself. ♦What lifestyle do you desire?♦What activities will you engage in?♦How will you be active with your community?♦Do you want to do any part-time work?

No matter what lifestyle you choose, you will be responsible for paying yourself an income. You will likely receive some social security, but not not nearly enough to meet all of your needs.

Bottom line, you need to save money and invest it wisely so you have a nest egg built up for retirement.

$ 200

Choose one of the three choices to the right.

Groceries + Go out for lunch and Take

Out for dinner 3x/Week @ $400

Groceries -Home cooking + bring my

lunch to work @ $275

Groceries - Bargain Hunter

and bring my lunch to work @ $200

New Sports Car @ $500/mo.

New mid size Car @ $300/mo.

Used Low Miles @ $225/mo.

Used High Miles @ $175/mo.

Bus and Bike @ 75/mo.

This is the amount I pay each month to have health insurance coverage.

Insurance Premium $ 125

I'm young and healthy so this should be a reasonable expense.

Perscriptions and Over The Counter

Meds $ 15

Personal Care $ 25

Medical/Healthcare (We set these amounts for you.)

$ 275

Food (Pick One)

Transportation (Gas, Maintenance, Loan Payment, Insurance) (Pick One)

$ 225

Vacation - Local Plans

Plenty to do around here at no

cost.

Vacation - 1 trip @ $1200/yr.

Save $100 per month

$ 100

Vacation - 1 trip @ $2400/yr.

Save $200 per month

Books, Games, Home Items

Enter an amount. A good estimate is

$20 - $40 per month

Gifts $ 20

Gym Membership (Full Service)

@60/mo.) $ 60

Gym Membership (Basic Service)

@10/mo.)

Gym MembershipDon't Need One!Exercise on My

Own

Donations(church, community

services, charities)

Other - Hobbies $ 20

Other - PetsFood, vet, toys

$ 2,880

(175)

Total Expenses and Savings

Miscellaneous (Enter Your Amount)

Vacation (Pick One)

Monthly Surplus or Shortfall♦ If the number is positive Congratulations. You can use the surplus to increase

your savings goals.♦ If the number is negative it simply means you need to revisit the choices you

made and revise your spending.

$ 100.00

1 2 3 4 5

2.00% 1,211$ 2,447$ 3,707$ 4,993$ 6,305$

$ 100.00

1 3 5 7 10

5.00% 1,228$ 3,875$ 6,801$ 10,033$ 15,528$

$ 200.00

5 10 15 30 43

8.00% 14,695$ 36,589$ 69,208$ 298,072$ 894,989$

EXPECTED RETURNNUMBER OF YEARS

EXPECTED RETURNNUMBER OF YEARS

RETIREMENT PLAN CONTRIBUTION CALCULATOR: Retirement Plan Investment Account (Long Term Goals 10+ years away)MONTHLY INVESTMENT AMOUNT =

SYSTEMATIC INVESTMENT PLAN CALCULATOR: Investment Account (Intermediate Term Goals- 5-10 years out)MONTHLY INVESTMENT AMOUNT =

MONTHLY INVESTMENT AMOUNT =

EXPECTED RETURNNUMBER OF YEARS

SYSTEMATIC INVESTMENT PLAN CALCULATOR: Savings Account (short term needs from 1-5 years out)

Let's see how you did with your savings plans. (DO NOT ENTER information directly to this table. The results are calculated from your entries above.)The three tables below show how your money would accumulate and grow based on the following criteria.♦Amount you chose to save each month♦ Hypothetical growth rate♦ Number of years you will save

Savings Plans

This Page Intentionally Left Blank

19

Credit

Complete the following segments of Make A Difference – Wisconsin’s ‘To Your Credit’, Money Sense

Lesson.

• Use the instructor notes for this lesson as your guide. (Separate workbook) Complete the following

segments of the lesson.

o Credit Cards: pgs. 6-19

o Credit Report and Credit Score: pgs. 20-33

o Loan Officer Activity: pgs. 32-33

o Feel free to discuss other concepts from the lesson as needed based on student

knowledge level and questions they are asking about credit.

• Access the link below to open the Prezi presentation for the ‘To Your Credit’ lesson.

http://prezi.com/y5p3ep1c3dy-/?utm_campaign=share&utm_medium=copy

(You may also access the Prezi on www.makeadifferencewisconsin.org website. Log in to the “volunteer section to access the Prezi on the opening page or in the Resource Library.).

The presentation will open in a small window (shown below), maximize this window by clicking the rectangle in the lower right corner.

Once the presentation window is maximized to “Fullscreen” use the Navigation Arrows > to move forward and back from slide to slide. Use the Navigation Slide Bar Dot when advancing more than one slide.

You may also move from slide to slide using the left and right arrows on a computer keyboard.

Window Maximize

Navigation Arrows Navigation Slide Bar Dot

26

Credit

• Student handouts will be provided to you ahead of your Money Coach session.

• You can review our online training curriculum module ahead of facilitating this lesson too. Just click on the link below to listen to a short (< 10 mins.) audio walk through of the lesson to get a feel for how to cover the material. https://www.makeadifferencewisconsin.org/topic/to-your-credit/

• Focus on getting students actively involved in the lesson. No lecture! Ask them what they know about the topics before filling in knowledge gaps.

• Be sure to save time for the loan officer activity.

PREP NOTES

27

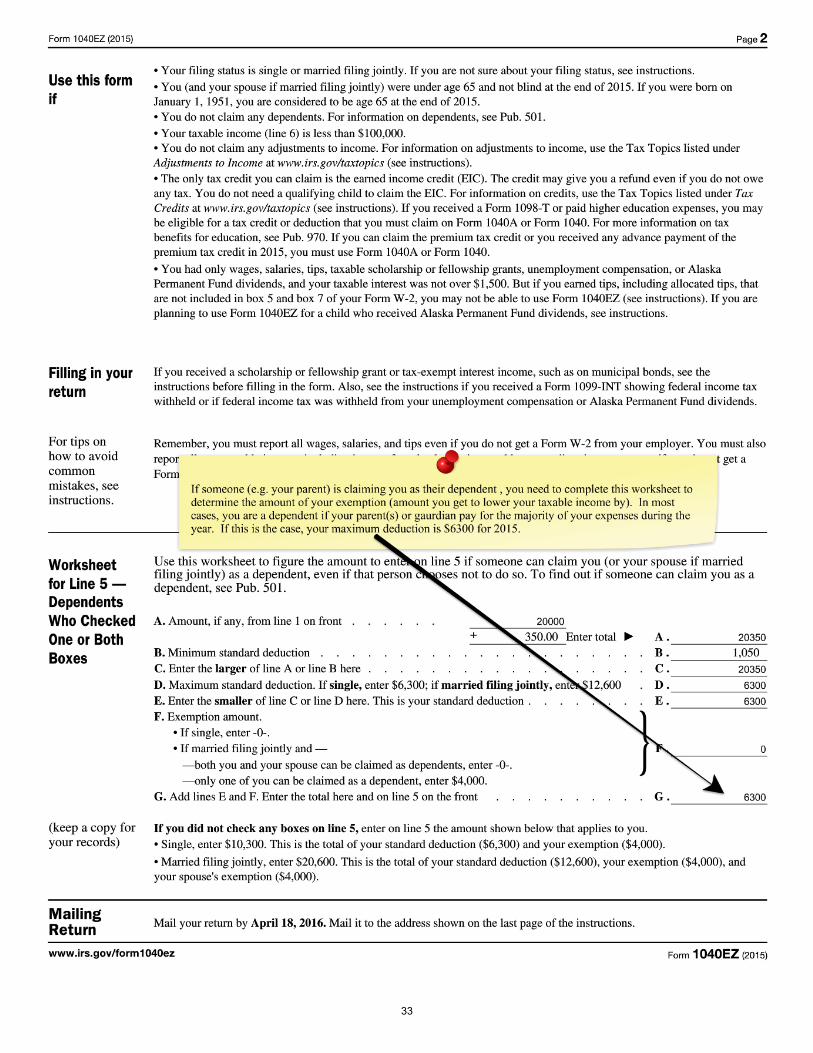

Tax Simulation Activity

Complete the following tax simulation activity: (Be sure to bring these documents up on the projector to help illustrate the lesson.) 1. Handout the sample W-2. Review the sample W-2, focusing primarily on the fields with data. Your goal is to keep this simple and build student confidence on completing their own tax return. 2. Review the Anatomy of a Tax Return. Review the various components and call out boxes in a logical order from top to bottom. Be sure to involve students in the discussion and ask students about their experience completing a tax return Also, some students may have tax withholding but have never filed a return to see if they would get a refund. Most, if not all, would get a refund because their income is below the standard deduction of $6300 (2015). 3. Handout the blank 1040 EZ and have them use the sample W-2 provided earlier to complete the tax form. Walk the room as they are working on their return and provide assistance as needed. Upon completion, ask students to provide the answers field by field and confirm all students have the form completed accurately. Show the answer version of the 1040 EZ to verify the answers. 4. Hold a Q&A session as needed.

PREP NOTES

28

22222a Employee’s social security number

OMB No. 1545-0008

b Employer identification number (EIN)

c Employer’s name, address, and ZIP code

d Control number

e Employee’s first name and initial Last name Suff.

f Employee’s address and ZIP code

1 Wages, tips, other compensation 2 Federal income tax withheld

3 Social security wages 4 Social security tax withheld

5 Medicare wages and tips 6 Medicare tax withheld

7 Social security tips 8 Allocated tips

9 10 Dependent care benefits

11 Nonqualified plans 12a Co d e

12bCo d e

12cCo d e

12dCo d e

13 Statutory employee

Retirement plan

Third-party sick pay

14 Other

15 State Employer’s state ID number 16 State wages, tips, etc. 17 State income tax 18 Local wages, tips, etc. 19 Local income tax 20 Locality name

Form W-2 Wage and Tax Statement 2015

Department of the Treasury—Internal Revenue Service

Copy 1—For State, City, or Local Tax Department

Jane L. Sample

123 Oak StreetBlack River Falls, WI 55555

34000

34000

34000

2108

493

120034000

Action Outdoors100 Big Buck LaneBlack River Falls, WI 55555

2800

123-45-6789

29

Instructions for Employee (Also see Notice to Employee, on the back of Copy B.)Box 1. Enter this amount on the wages line of your tax return. Box 2. Enter this amount on the federal income tax withheld line of your tax return.

Box 5. You may be required to report this amount on Form 8959, Additional Medicare Tax. See the Form 1040 instructions to determine if you are required to complete Form 8959.Box 6. This amount includes the 1.45% Medicare Tax withheld on all Medicare wages and tips shown in Box 5, as well as the 0.9% Additional Medicare Tax on any of those Medicare wages and tips above $200,000.Box 8. This amount is not included in boxes 1, 3, 5, or 7. For information on how to report tips on your tax return, see your Form 1040 instructions.

You must file Form 4137, Social Security and Medicare Tax on Unreported Tip Income, with your income tax return to report at least the allocated tip amount unless you can prove that you received a smaller amount. If you have records that show the actual amount of tips you received, report that amount even if it is more or less than the allocated tips. On Form 4137 you will calculate the social security and Medicare tax owed on the allocated tips shown on your Form(s) W-2 that you must report as income and on other tips you did not report to your employer. By filing Form 4137, your social security tips will be credited to your social security record (used to figure your benefits).Box 10. This amount includes the total dependent care benefits that your employer paid to you or incurred on your behalf (including amounts from a section 125 (cafeteria) plan). Any amount over $5,000 is also included in box 1. Complete Form 2441, Child and Dependent Care Expenses, to compute any taxable and nontaxable amounts.

Box 11. This amount is (a) reported in box 1 if it is a distribution made to you from a nonqualified deferred compensation or nongovernmental section 457(b) plan or (b) included in box 3 and/or 5 if it is a prior year deferral under a nonqualified or section 457(b) plan that became taxable for social security and Medicare taxes this year because there is no longer a substantial risk of forfeiture of your right to the deferred amount. This box should not be used if you had a deferral and a distribution in the same calendar year. If you made a deferral and received a distribution in the same calendar year, and you are or will be age 62 by the end of the calendar year, your employer should file Form SSA-131, Employer Report of Special Wage Payments, with the Social Security Administration and give you a copy.

Box 12. The following list explains the codes shown in box 12. You may need this information to complete your tax return. Elective deferrals (codes D, E, F, and S) and designated Roth contributions (codes AA, BB, and EE) under all plans are generally limited to a total of $18,000 ($12,500 if you only have SIMPLE plans; $21,000 for section 403(b) plans if you qualify for the 15-year rule explained in Pub. 571). Deferrals under code G are limited to $18,000. Deferrals under code H are limited to $7,000. However, if you were at least age 50 in 2015, your employer may have allowed an additional deferral of up to $6,000 ($3,000 for section 401(k)(11) and 408(p) SIMPLE plans). This additional deferral amount is not subject to the overall limit on elective deferrals. For code G, the limit on elective deferrals may be higher for the last 3 years before you reach retirement age. Contact your plan administrator for more information. Amounts in excess of the overall elective deferral limit must be included in income. See the “Wages, Salaries, Tips, etc.” line instructions for Form 1040.Note. If a year follows code D through H, S, Y, AA, BB, or EE, you made a make-up pension contribution for a prior year(s) when you were in military service. To figure whether you made excess deferrals, consider these amounts for the year shown, not the current year. If no year is shown, the contributions are for the current year.

A—Uncollected social security or RRTA tax on tips. Include this tax on Form 1040. See “Other Taxes” in the Form 1040 instructions.

B—Uncollected Medicare tax on tips. Include this tax on Form 1040. See “Other Taxes” in the Form 1040 instructions.

C—Taxable cost of group-term life insurance over $50,000 (included in boxes 1, 3 (up to social security wage base), and 5)

D—Elective deferrals to a section 401(k) cash or deferred arrangement. Also includes deferrals under a SIMPLE retirement account that is part of a section 401(k) arrangement.

E—Elective deferrals under a section 403(b) salary reduction agreement

(continued on back of Copy 2)

30

Instructions for Employee (continued from back of Copy C)

F—Elective deferrals under a section 408(k)(6) salary reduction SEP

G—Elective deferrals and employer contributions (including nonelective deferrals) to a section 457(b) deferred compensation plan

H—Elective deferrals to a section 501(c)(18)(D) tax-exempt organization plan. See “Adjusted Gross Income” in the Form 1040 instructions for how to deduct.

J—Nontaxable sick pay (information only, not included in boxes 1, 3, or 5)

K—20% excise tax on excess golden parachute payments. See “Other Taxes” in the Form 1040 instructions.

L—Substantiated employee business expense reimbursements (nontaxable)

M—Uncollected social security or RRTA tax on taxable cost of group-term life insurance over $50,000 (former employees only). See “Other Taxes” in the Form 1040 instructions.

N—Uncollected Medicare tax on taxable cost of group-term life insurance over $50,000 (former employees only). See “Other Taxes” in the Form 1040 instructions.

P—Excludable moving expense reimbursements paid directly to employee (not included in boxes 1, 3, or 5)

Q—Nontaxable combat pay. See the instructions for Form 1040 or Form 1040A for details on reporting this amount.

R—Employer contributions to your Archer MSA. Report on Form 8853, Archer MSAs and Long-Term Care Insurance Contracts.

S—Employee salary reduction contributions under a section 408(p) SIMPLE plan (not included in box 1)

T—Adoption benefits (not included in box 1). Complete Form 8839, Qualified Adoption Expenses, to compute any taxable and nontaxable amounts.

V—Income from exercise of nonstatutory stock option(s) (included in boxes 1, 3 (up to social security wage base), and 5). See Pub. 525 and instructions for Schedule D (Form 1040) for reporting requirements.

W—Employer contributions (including amounts the employee elected to contribute using a section 125 (cafeteria) plan) to your health savings account. Report on Form 8889, Health Savings Accounts (HSAs).

Y—Deferrals under a section 409A nonqualified deferred compensation plan

Z—Income under a nonqualified deferred compensation plan that fails to satisfy section 409A. This amount is also included in box 1. It is subject to an additional 20% tax plus interest. See “Other Taxes” in the Form 1040 instructions.

AA—Designated Roth contributions under a section 401(k) plan

BB—Designated Roth contributions under a section 403(b) plan

DD—Cost of employer-sponsored health coverage. The amount reported with Code DD is not taxable.

EE—Designated Roth contributions under a governmental section 457(b) plan. This amount does not apply to contributions under a tax-exempt organization section 457(b) plan.

Box 13. If the “Retirement plan” box is checked, special limits may apply to the amount of traditional IRA contributions you may deduct. See Pub. 590, Individual Retirement Arrangements (IRAs).

Box 14. Employers may use this box to report information such as state disability insurance taxes withheld, union dues, uniform payments, health insurance premiums deducted, nontaxable income, educational assistance payments, or a member of the clergy's parsonage allowance and utilities. Railroad employers use this box to report railroad retirement (RRTA) compensation, Tier 1 tax, Tier 2 tax, Medicare tax and Additional Medicare Tax. Include tips reported by the employee to the employer in railroad retirement (RRTA) compensation.

Note. Keep Copy C of Form W-2 for at least 3 years after the due date for filing your income tax return. However, to help protect your social security benefits, keep Copy C until you begin receiving social security benefits, just in case there is a question about your work record and/or earnings in a particular year.

31

32

33

34

35

This Page Intentionally Left Blank

36

♦ This lesson will be lead by an experienced Money Path volunteer.

♦ Coaches will assist students with the activities.

Money Path

37

Money Path is a lesson focused on teaching high school students financialplanning principles necessary for making a successful transition to living financially independent. The lesson is delivered by an experienced business professional from the community in a highly interactive manner.

Money Path

Lesson AgendaFormat: technology-based, activity-driven,

hands-on, decision-focused

A Financial Planning Lesson for Teens

-James RummageWhitnall High School educator

“I’m going to model my

teaching around the concepts

in this lesson for my personal finance class.”

Choose Your Path: Go to college or start career?

Personal Profile: Take on financial life of a 23 year-old

Goal Setting Activity: Set financial goals from young adult through retirement

Budget Activity: It’s a matter of choice. Spend less to save more?

Financial Plan Simulation (software program): Students revise plans to improve likelihood of reaching goals

Financial Planning Checklist for Young Adults1. Retirement plan contributions2. Budgeting & saving3. Short, intermediate & long term goals4. Credit score5. Life insurance

38

“We need to know this!”

“I would recommend this to anyone who wants to be

successful.”

What high school students have to say about Money Path....

Financial Plan Simulation( software dashboard )

“It helped me better understand how money impacts me and that it’s best to plan

early.”

39

Independently Living Budgeting For My First Year Of College Or Career

Activity

• Students should be prepared to manage their finances independently as they transition to their college or career path.

• Handout the appropriate budget to students based on the path they have chosen after high school graduation. We have created two versions; one for a college bound student and one for a career/workforce bound student.

• Review the budget format and have students begin building their budget for real for the next step in their life.

• For students going to college, have them use the known sources of income/money to finance school. If these dollars are not finalized have them complete the expense side of the budget. This will help them determine what they need in scholarships, grants and student loans.

• Assist students by walking around the room and observing, answering and asking questions.

• Ask 1-2 students to share what they came up with for their budget.

40

This Page Intentionally Left Blank

41

Independently Living Budgeting For My First Year Of College Or Career

Enter Monthly Amounts Projected Monthly Monthly Monthly

WagesGiftsGrants and ScholarshipsStudent LoansOtherTOTAL Income

Monthly Savings

School ExpensesTuitionFeesBooksSuppliesTOTAL School expenses

Mortgage/RentWater billEnergy bill (gas and electric)Homeowners or renters insuranceInternet and CableOtherTOTAL Lodging & utilities

GrocieriesDining OutSnacks, Soda, etc.EntertainmentMovies Music Downloads/DVDs/Video GamesWeekend Fun, Events, Concerts, HobbiesTickets to sporting eventsPersonal ExpensesPersonal productsCell PhoneLoan Payments Clothing/Shoes/ShoppingSalon ServicesOther

Gas/Car maintenance/InsurancePublic TransportationTOTAL ExpensesTOTAL BUDGETIncome-Saving -Total Expenses= (surplus/deficit)

Money Coach: Budget Worksheet for College StudentName:

Food

Transportation

INCOME

EXPENSES

SAVINGS: PAY YOURSELF FIRST!

Housing and Utilities

42

Independently Living Budgeting For My First Year Of College Or Career

Enter Monthly Amounts Projected Monthly Monthly Monthly

WagesGiftsOtherTOTAL Income

Monthly Savings

Mortgage/RentWater billEnergy bill (gas and electric)Homeowners or renters insuranceInternet and CableOtherTOTAL Lodging & utilities

GrocieriesDining OutSnacks, Soda, etc.EntertainmentMovies Music Downloads/DVDs/Video GamesWeekend Fun, Events, Concerts, HobbiesTickets to sporting eventsPersonal ExpensesPersonal productsHealth/Dental/Vision Insurance PremiumsMedical and Perscription ExpenseCell PhoneLoan Payments (car, student)Clothing/Shoes/ShoppingSalon ServicesOther

Gas/Car maintenance/InsurancePublic TransportationTOTAL ExpensesTOTAL BUDGETIncome-Saving -Total Expenses= (surplus/deficit)

Money Coach: Budget Worksheet for Young Adult Starting CareerName:

Food

Transportation

INCOME

EXPENSES

SAVINGS: PAY YOURSELF FIRST!

Housing and Utilities

43

Make A Difference – Wisconsin empowers teenagers with financial literacy educational resources and real-world lessons. Our engaging volunteers, dynamic schools and generous supporters share a vision of stronger communities built by an investment in “money smart” teens.

Make A Difference – Wisconsin 710 N. Plankinton Ave. Milwaukee, WI 53226

414-273-8101 www.makeadifferencewisconsin.org

44