monday 1030 financial reporting updates & issues · moody's aaa aa1, aa2, aa3 a1, a2 a3...

TRANSCRIPT

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

ZZ

Financial Reporting Updates & Issues Financial Reporting Updates & Issues

Mary Caswell

NAIC

© 2016 National Association of Insurance Commissioners

This presentation is pre-qualified for NAIC Designation Renewal Credits (DRCs). If you currently hold an NAIC APIR, PIR, or SPIR designation and are pursuing continuing education credit to maintain it, you may be awarded credits for your participation. To receive credit, you must be in attendance for the duration of the presentation.

Attention APIR, PIR, or SPIR Designees…

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

Learning Objectives

At the end of this presentation, you will be able to:

• Identify the 2016 adopted annual reporting changes.

• Identify the Notes to Financial Statement proposed changes and the related SSAPs.

• Describe the 2016 annual statement changes that have been exposed for comment.

© 2016 National Association of Insurance Commissioners

Mary Caswell

NAIC Data Quality Manager

– Manages Data Quality Unit

– Supports Blanks Working Group

– Supervises Staff Support for:

• Health Reform Solvency Impact Subgroup

• Investment Reporting Subgroup

– Joined NAIC in August 2000

– Contact email information: [email protected]

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

Adopted proposal – 2015-22BWG

• Supplemental Exhibits and Schedules Interrogatories– Filing the Communication of Internal Control

Related Matters Noted in Audit filing • Regulator only, non-public

• To be filed electronically with the NAIC.

© 2016 National Association of Insurance Commissioners

Adopted changes

• Schedule D, Part 1A, Section 1 and Schedule D, Part 1B, – Remove the reference to “non-rated”

2015-25BWG

• P&C blank and Health Property Supplement– Special code added to Schedule F, Part 3 and 5

• “2” = Reinsurance contracts ceding 75% or more direct premiums written• “3” = Counterparty reporting exception for asbestos and pollution

contracts under SSAP 62R – New supplemental schedule

• Details of reinsurers aggregated on Schedule F, Part 3 • Conforming modifications to existing Schedule F, Parts 3 & 5

– Disclosure as Note 23J (also data captured)• Reinsurance agreements qualifying for reinsurer aggregation

2015-26BWG

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

SUPPLEMENTAL SCHEDULE FOR REINSURANCE COUNTERPARTY REPORTING EXCEPTION –ASBESTOS AND POLLUTION CONTRACTS

Original Reinsurer Retroactive Reinsurer

Reinsurance Recoverables On Original Reinsurer Collateral

15 Reinsurance Recoverable on Paid Losses and Paid Loss Adjustment Expenses

23 24

1 2 3 4 5 6 7 8 9 10 11 12 13 14 16 Overdue 22 %Trust 17 18 19 20 21 More

Than

ID # NAIC

CocodeName of Reinsurer

Domiciliary Jurisdiction ID #

Name of Reinsurer Reported

Schedule F, Part 3

Paid Losses

Paid LAE

UnpdCase

Losses & LAE

IBNR Losses & LAE

Cols 7 + 8 + 9

+10 Totals

Funds Held

Ltrs of Credit

Funds and

Other Allowe

d Offset Items

AmtAppvd

as Other Offset Items Crrnt

1 to 29 Days

30 to 90

Days

91 to 120 Days

Over 120 Days

Total Overd

ue Cols. 17 + 18 + 19 + 20

Total Due Cols. 16 + 21

% Over-due Col.

21/Col. 22

90 Days Over-due Col.(19 +

20)/Col.22

9999999Totals

© 2016 National Association of Insurance Commissioners

Exposed proposal – 2016-01BWG

Schedule Y, Part 1A: – Add a column to identify SCAs where a SUB 1 or

SUB 2 NAIC filing is required.

– Add an electronic only column for LEI.

Schedule D, Part 6, Section 1: – Add a column to identify the nonadmitted amount.

– Separate Column 4 into two columns • NAIC Company Code• Id Number

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

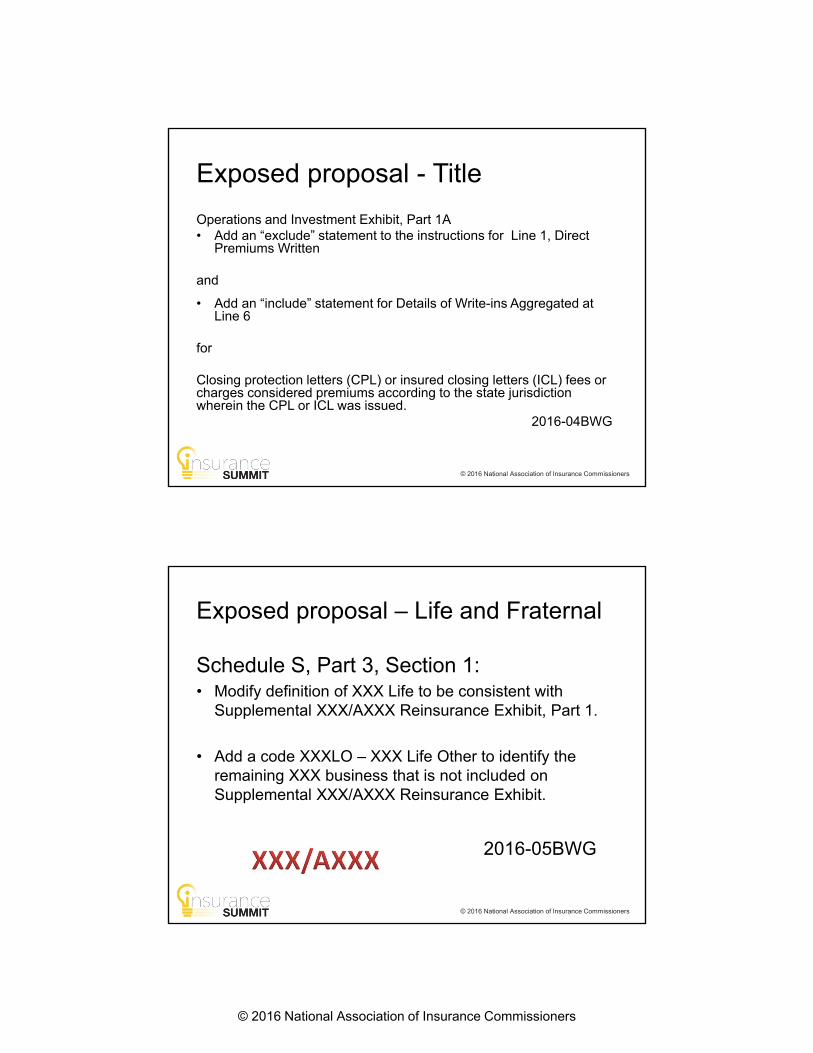

Exposed proposal – 2016-02BWG

• Incorporate previously adopted Schedule D, Part 1 guidance that included clarification for the description, issue, issuer and capital structure code columns.

• Combine Senior Subordinated Debt and Junior Subordinated debt codes into one code as “Subordinated Debt for the Capital Structure”

• Modify CUSIP and Description column instructions for Schedule D, Parts 2 - 6 for consistency with Schedule D, Part 1.

• Add the electronic columns for Issuer, Issue and ISIN across Schedule Ds for consistency.

© 2016 National Association of Insurance Commissioners

Exposed proposal – Title

Actuarial Opinion, item 6.d. Reserve Development:

• Add a new paragraph regarding the ratio of One-Year or Two-Year Known Claims Reserve Development.

2016-03BWG

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

Exposed proposal - Title

Operations and Investment Exhibit, Part 1A • Add an “exclude” statement to the instructions for Line 1, Direct

Premiums Written

and

• Add an “include” statement for Details of Write-ins Aggregated at Line 6

for

Closing protection letters (CPL) or insured closing letters (ICL) fees or charges considered premiums according to the state jurisdiction wherein the CPL or ICL was issued.

2016-04BWG

© 2016 National Association of Insurance Commissioners

Exposed proposal – Life and Fraternal

Schedule S, Part 3, Section 1:• Modify definition of XXX Life to be consistent with

Supplemental XXX/AXXX Reinsurance Exhibit, Part 1.

• Add a code XXXLO – XXX Life Other to identify the remaining XXX business that is not included on Supplemental XXX/AXXX Reinsurance Exhibit.

2016-05BWG

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

Exposed proposal

Investment Schedules – General: • Reduce the number of foreign codes from 12 to 4

and remove the foreign code matrix.2016-06BWG

Schedule D, Part 1: • Modify the instructions to provide clarification on

the Bond Characteristic Column.2016-07BWG

© 2016 National Association of Insurance Commissioners

2016-06BWG

“A” For Canadian securities issued in Canada and denominated in U.S.

dollars.

“B” For those securities that meet the definition of foreign provided in the

Supplement Investment Risk Interrogatories and pay in a currency OTHER

THAN U.S. dollars.

“C” For foreign securities issued in the U.S. and denominated in U.S. dollars.

“D” For those securities that meet the definition of a foreign as provided in

Supplement Investment Risk Interrogatories and denominated in U.S.

dollars (e.g., Yankee Bonds or Eurodollar bonds).

Leave blank for securities that do not meet the criteria for the use of “A”, “B”, “C” or “D.”

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

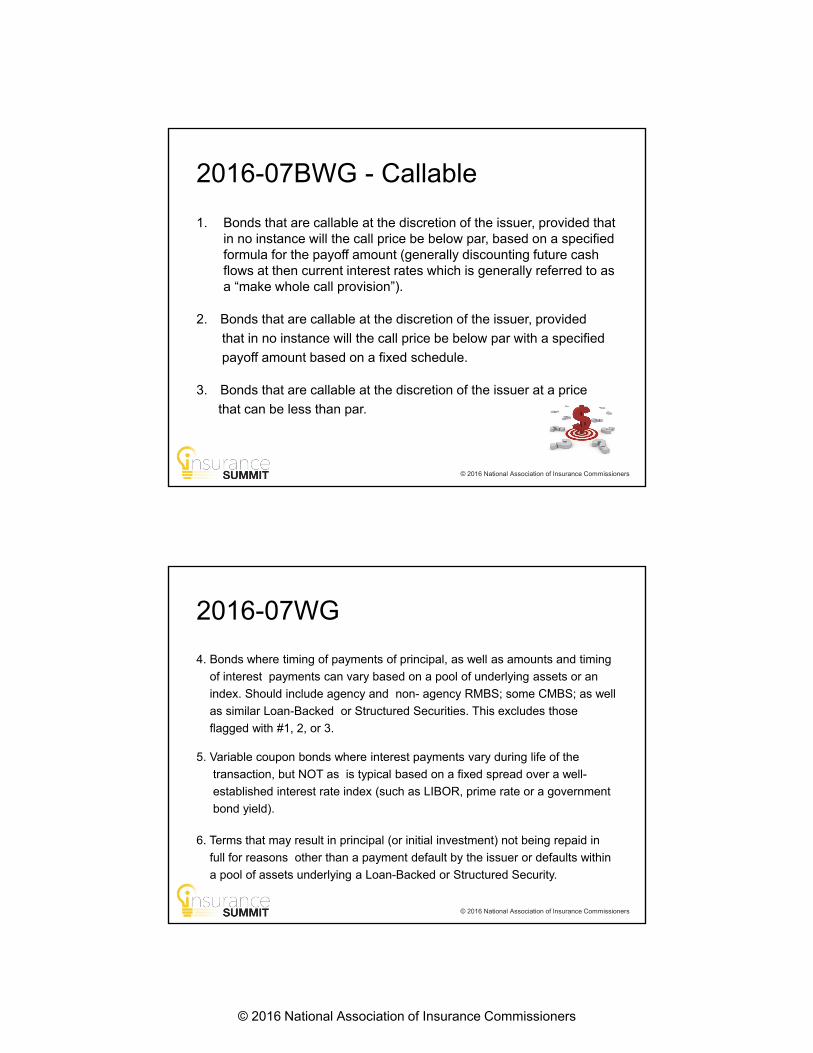

2016-07BWG - Callable

1. Bonds that are callable at the discretion of the issuer, provided that in no instance will the call price be below par, based on a specified formula for the payoff amount (generally discounting future cash flows at then current interest rates which is generally referred to as a “make whole call provision”).

2. Bonds that are callable at the discretion of the issuer, provided

that in no instance will the call price be below par with a specified

payoff amount based on a fixed schedule.

3. Bonds that are callable at the discretion of the issuer at a price

that can be less than par.

© 2016 National Association of Insurance Commissioners

2016-07WG

4. Bonds where timing of payments of principal, as well as amounts and timing

of interest payments can vary based on a pool of underlying assets or an

index. Should include agency and non- agency RMBS; some CMBS; as well

as similar Loan-Backed or Structured Securities. This excludes those

flagged with #1, 2, or 3.

5. Variable coupon bonds where interest payments vary during life of the

transaction, but NOT as is typical based on a fixed spread over a well-

established interest rate index (such as LIBOR, prime rate or a government

bond yield).

6. Terms that may result in principal (or initial investment) not being repaid in

full for reasons other than a payment default by the issuer or defaults within

a pool of assets underlying a Loan-Backed or Structured Security.

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

2016-07BWG

7. Bonds whose payments of principal and/or interest are denominated

in a currency other than the US dollar.

8. Bonds where issuer’s obligation to make payments is determined

by performance of a different credit other than that of the issuer,

which could be either affiliated or unaffiliated.

9. Mandatory convertible bonds. Bonds that are mandatorily convertible

into equity, or, at the option of issuer, convertible into equity, or

whose terms provide for payment in the form of equity instead of

cash.

10. Other types of options not otherwise reported in 1-9.

© 2016 National Association of Insurance Commissioners

Exposed proposal – P&C, Health Supplement

• Add an electronic only column to capture the secure code for reinsurers on Schedule F, Part 3, Part 5 and Part 6 Section 1.

2016-08BWG

1 2 3 4 5 6 7

Secure CodeFollowing is a listing of the valid secure codes.

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

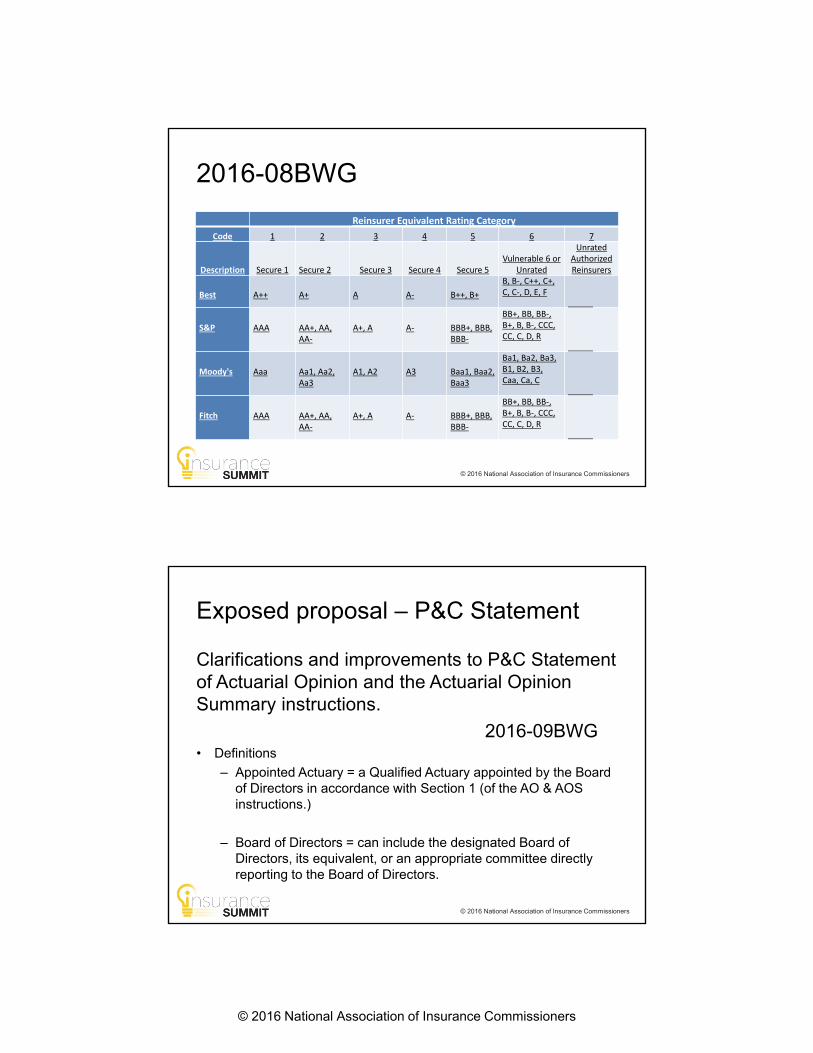

2016-08BWG

Reinsurer Equivalent Rating CategoryCode 1 2 3 4 5 6 7

Description Secure 1 Secure 2 Secure 3 Secure 4 Secure 5Vulnerable 6 or

Unrated

Unrated Authorized Reinsurers

Best A++ A+ A A- B++, B+B, B-, C++, C+, C, C-, D, E, F

S&P AAA AA+, AA, AA-

A+, A A- BBB+, BBB, BBB-

BB+, BB, BB-, B+, B, B-, CCC, CC, C, D, R

Moody's Aaa Aa1, Aa2, Aa3

A1, A2 A3 Baa1, Baa2, Baa3

Ba1, Ba2, Ba3, B1, B2, B3, Caa, Ca, C

Fitch AAA AA+, AA, AA-

A+, A A- BBB+, BBB, BBB-

BB+, BB, BB-, B+, B, B-, CCC, CC, C, D, R

© 2016 National Association of Insurance Commissioners

Exposed proposal – P&C Statement

Clarifications and improvements to P&C Statement of Actuarial Opinion and the Actuarial Opinion Summary instructions.

2016-09BWG• Definitions

– Appointed Actuary = a Qualified Actuary appointed by the Board of Directors in accordance with Section 1 (of the AO & AOS instructions.)

– Board of Directors = can include the designated Board of Directors, its equivalent, or an appropriate committee directly reporting to the Board of Directors.

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

2016-09BWG – P&C Statement

6. The Appointed Actuary must provide RELEVANT COMMENT paragraphs to address the following topics of regulatory importance.

A. Company-Specific Risk Factors

The Appointed Actuary should include an explanatory paragraph to describe the major factors, combination of factors or particular conditions underlying the risks and uncertainties the Appointed Actuary considers relevant. The explanatory paragraph should not include general, broad statements about risks and uncertainties due to economic changes, judicial decisions, regulatory actions, political or social forces, etc., nor is the Appointed Actuary required to include an exhaustive list of all potential sources of risks and uncertainties.

© 2016 National Association of Insurance Commissioners

Exposed proposal - P&C Statement

Property/Casualty Exhibit of Premiums and Losses and Insurance Expense Exhibit, Parts II and III:

• Add an new line “Line 2.5 - Private Flood” for writers of the private market coverage.

2016-10BWG

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

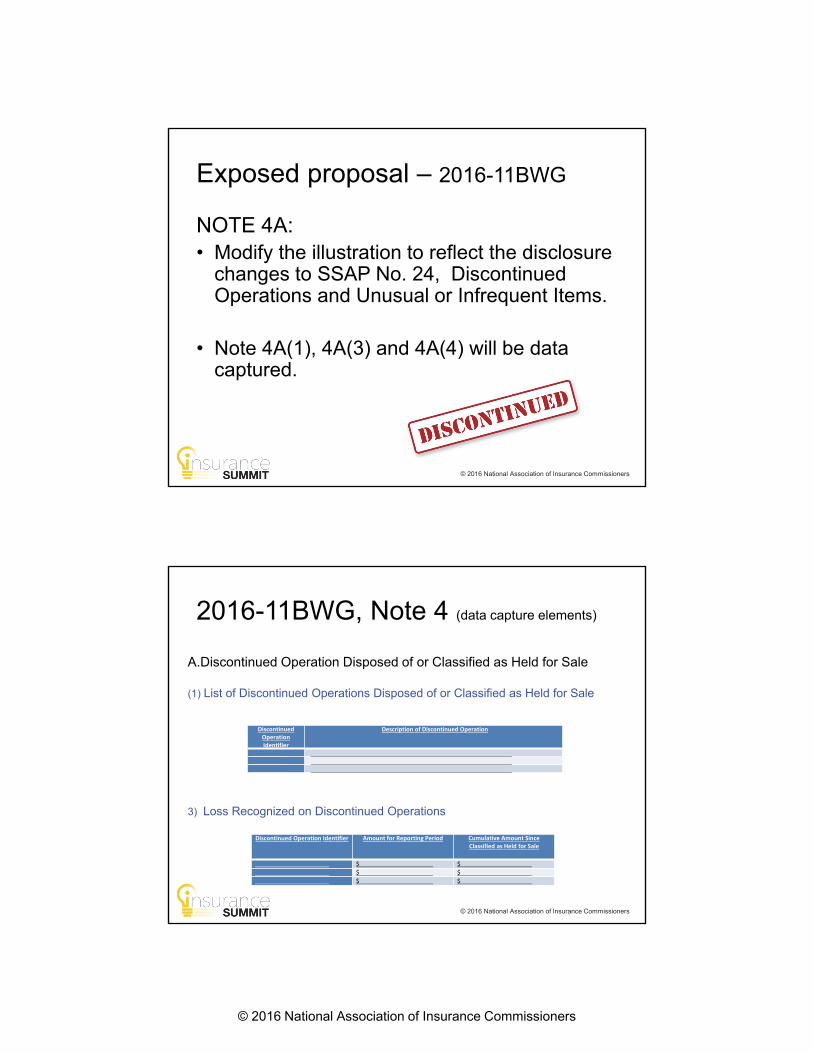

Exposed proposal – 2016-11BWG

NOTE 4A: • Modify the illustration to reflect the disclosure

changes to SSAP No. 24, Discontinued Operations and Unusual or Infrequent Items.

• Note 4A(1), 4A(3) and 4A(4) will be data captured.

© 2016 National Association of Insurance Commissioners

2016-11BWG, Note 4 (data capture elements)

Discontinued OperationIdentifier

Description of Discontinued Operation

Discontinued Operation Identifier Amount for Reporting Period Cumulative Amount Since Classified as Held for Sale

$ $$ $$ $

A.Discontinued Operation Disposed of or Classified as Held for Sale

(1) List of Discontinued Operations Disposed of or Classified as Held for Sale

3) Loss Recognized on Discontinued Operations

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

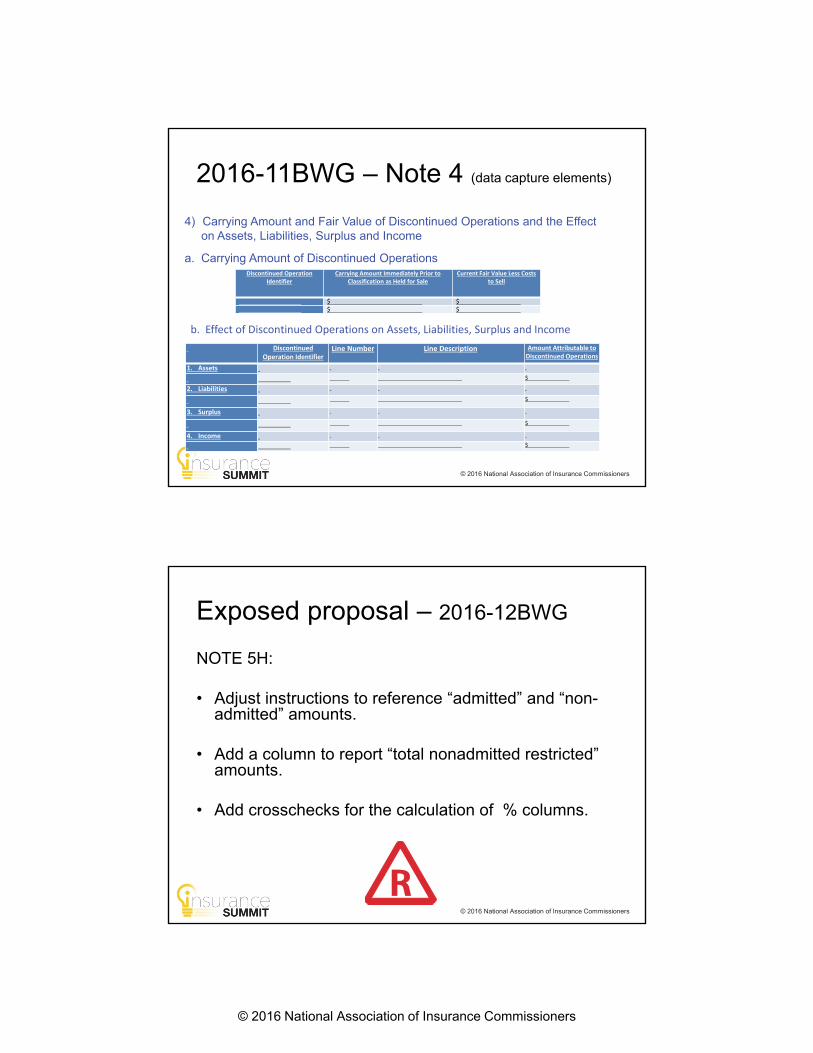

2016-11BWG – Note 4 (data capture elements)

Discontinued Operation Identifier

Carrying Amount Immediately Prior to Classification as Held for Sale

Current Fair Value Less Costs to Sell

$ $$ $

Discontinued Operation Identifier

Line Number Line Description Amount Attributable to Discontinued Operations

1. Assets$

2. Liabilities$

3. Surplus$

4. Income$

4) Carrying Amount and Fair Value of Discontinued Operations and the Effecton Assets, Liabilities, Surplus and Income

a. Carrying Amount of Discontinued Operations

b. Effect of Discontinued Operations on Assets, Liabilities, Surplus and Income

© 2016 National Association of Insurance Commissioners

Exposed proposal – 2016-12BWG

NOTE 5H:

• Adjust instructions to reference “admitted” and “non-admitted” amounts.

• Add a column to report “total nonadmitted restricted” amounts.

• Add crosschecks for the calculation of % columns.

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

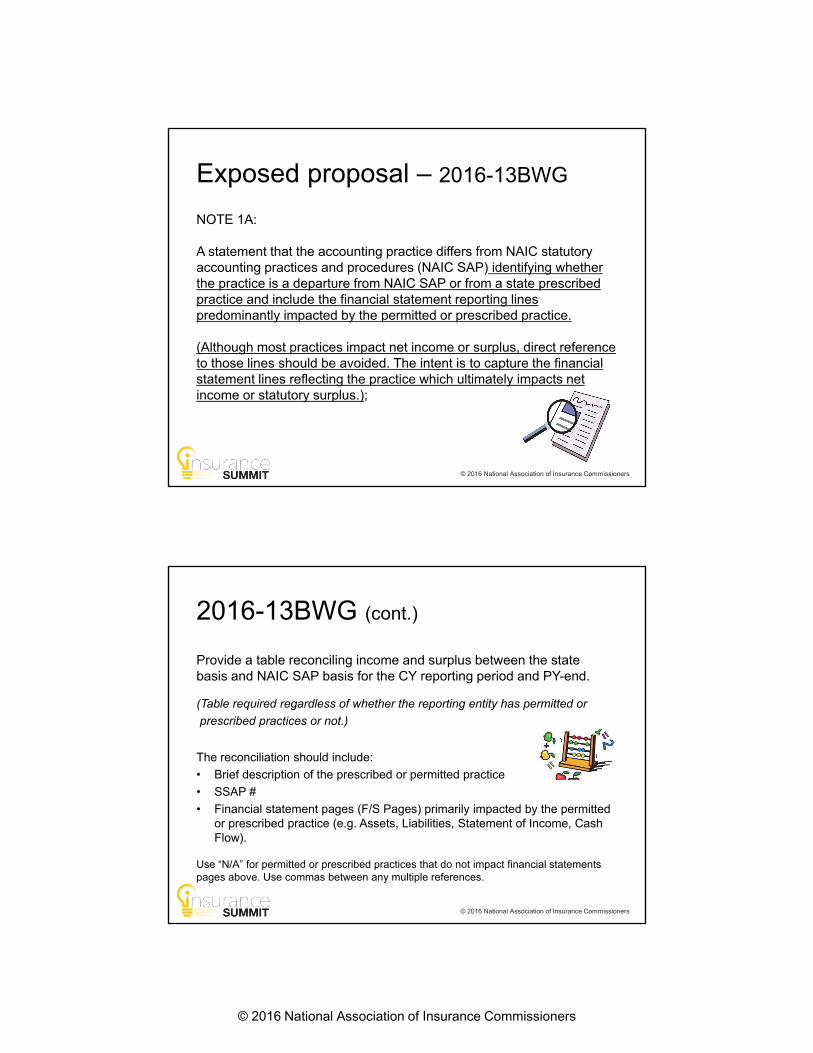

Exposed proposal – 2016-13BWG

NOTE 1A:

A statement that the accounting practice differs from NAIC statutory accounting practices and procedures (NAIC SAP) identifying whether the practice is a departure from NAIC SAP or from a state prescribed practice and include the financial statement reporting lines predominantly impacted by the permitted or prescribed practice.

(Although most practices impact net income or surplus, direct reference to those lines should be avoided. The intent is to capture the financial statement lines reflecting the practice which ultimately impacts net income or statutory surplus.);

© 2016 National Association of Insurance Commissioners

2016-13BWG (cont.)

Provide a table reconciling income and surplus between the state basis and NAIC SAP basis for the CY reporting period and PY-end.

(Table required regardless of whether the reporting entity has permitted or

prescribed practices or not.)

The reconciliation should include:

• Brief description of the prescribed or permitted practice

• SSAP #

• Financial statement pages (F/S Pages) primarily impacted by the permitted or prescribed practice (e.g. Assets, Liabilities, Statement of Income, Cash Flow).

Use “N/A” for permitted or prescribed practices that do not impact financial statements pages above. Use commas between any multiple references.

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

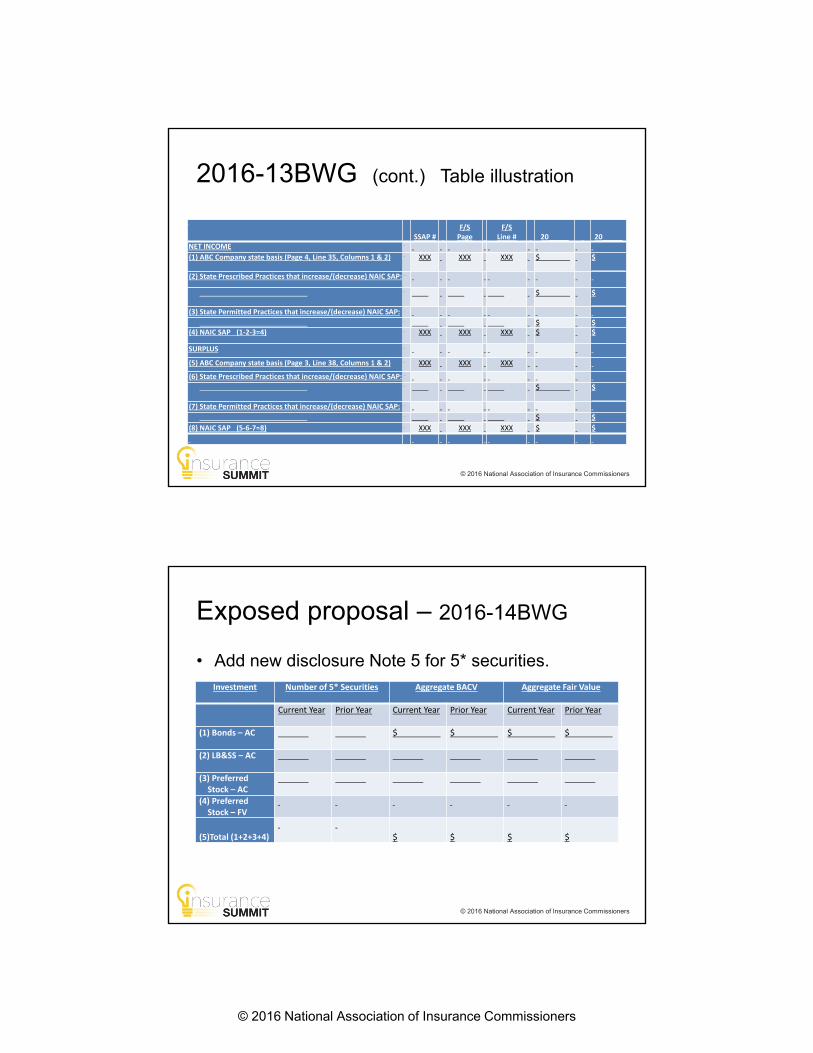

2016-13BWG (cont.) Table illustration

SSAP #F/S

PageF/S

Line # 20_____ 20_____NET INCOME(1) ABC Company state basis (Page 4, Line 35, Columns 1 & 2) XXX XXX XXX $ $

(2) State Prescribed Practices that increase/(decrease) NAIC SAP:

$ $

(3) State Permitted Practices that increase/(decrease) NAIC SAP:$ $

(4) NAIC SAP (1-2-3=4) XXX XXX XXX $ $

SURPLUS

(5) ABC Company state basis (Page 3, Line 38, Columns 1 & 2) XXX XXX XXX

(6) State Prescribed Practices that increase/(decrease) NAIC SAP:$ $

(7) State Permitted Practices that increase/(decrease) NAIC SAP:$ $

(8) NAIC SAP (5-6-7=8) XXX XXX XXX $ $

© 2016 National Association of Insurance Commissioners

Exposed proposal – 2016-14BWG

• Add new disclosure Note 5 for 5* securities. Investment Number of 5* Securities Aggregate BACV Aggregate Fair Value

Current Year Prior Year Current Year Prior Year Current Year Prior Year

(1) Bonds – AC $ $ $ $

(2) LB&SS – AC

(3) Preferred Stock – AC

(4) Preferred Stock – FV

(5)Total (1+2+3+4) $ $ $ $

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

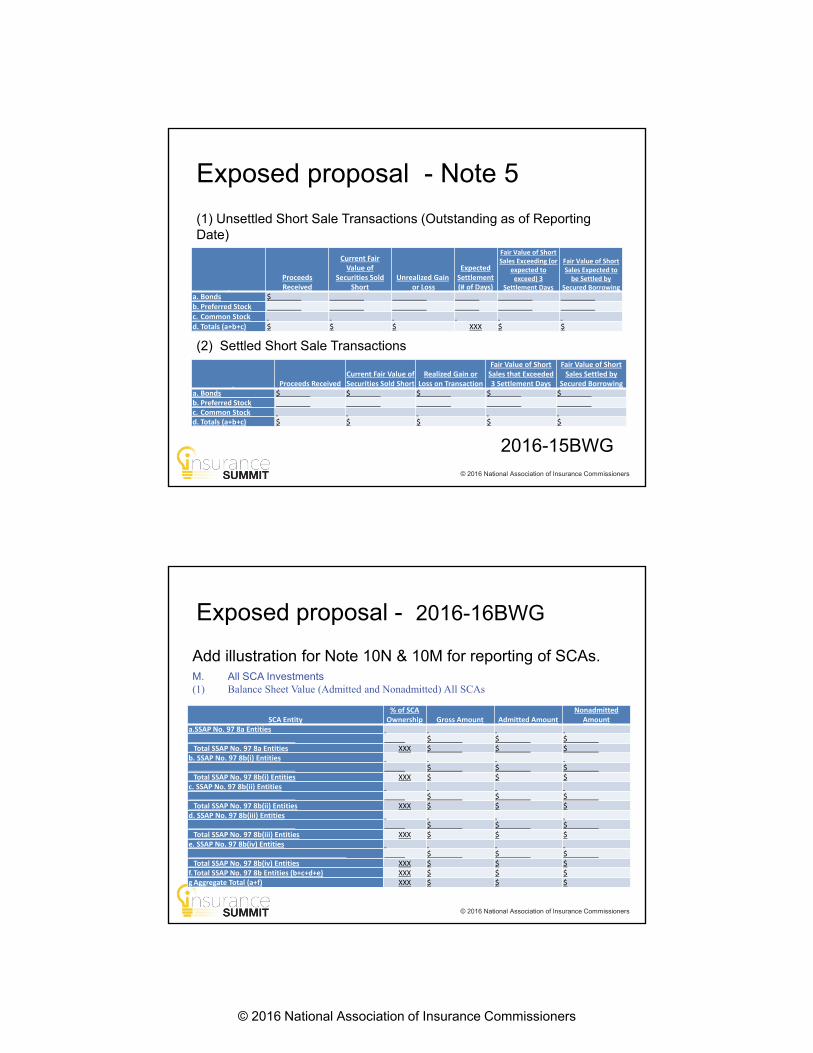

Exposed proposal - Note 5

(1) Unsettled Short Sale Transactions (Outstanding as of Reporting Date)

(2) Settled Short Sale Transactions

2016-15BWG

Proceeds Received

Current Fair Value of

Securities Sold Short

Unrealized Gainor Loss

Expected Settlement(# of Days)

Fair Value of Short Sales Exceeding (or

expected to exceed) 3

Settlement Days

Fair Value of Short Sales Expected to

be Settled by Secured Borrowing

a. Bonds $b. Preferred Stockc. Common Stockd. Totals (a+b+c) $ $ $ XXX $ $

Proceeds ReceivedCurrent Fair Value of Securities Sold Short

Realized Gain or Loss on Transaction

Fair Value of Short Sales that Exceeded 3 Settlement Days

Fair Value of Short Sales Settled by

Secured Borrowinga. Bonds $ $ $ $ $b. Preferred Stockc. Common Stockd. Totals (a+b+c) $ $ $ $ $

© 2016 National Association of Insurance Commissioners

Exposed proposal - 2016-16BWG

Add illustration for Note 10N & 10M for reporting of SCAs.

SCA Entity% of SCA

Ownership Gross Amount Admitted AmountNonadmitted

Amounta.SSAP No. 97 8a Entities

$ $ $Total SSAP No. 97 8a Entities XXX $ $ $

b. SSAP No. 97 8b(i) Entities$ $ $

Total SSAP No. 97 8b(i) Entities XXX $ $ $c. SSAP No. 97 8b(ii) Entities

$ $ $Total SSAP No. 97 8b(ii) Entities XXX $ $ $

d. SSAP No. 97 8b(iii) Entities$ $ $

Total SSAP No. 97 8b(iii) Entities XXX $ $ $e. SSAP No. 97 8b(iv) Entities

$ $ $Total SSAP No. 97 8b(iv) Entities XXX $ $ $

f.Total SSAP No. 97 8b Entities (b+c+d+e) XXX $ $ $g Aggregate Total (a+f) XXX $ $ $

M. All SCA Investments(1) Balance Sheet Value (Admitted and Nonadmitted) All SCAs

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

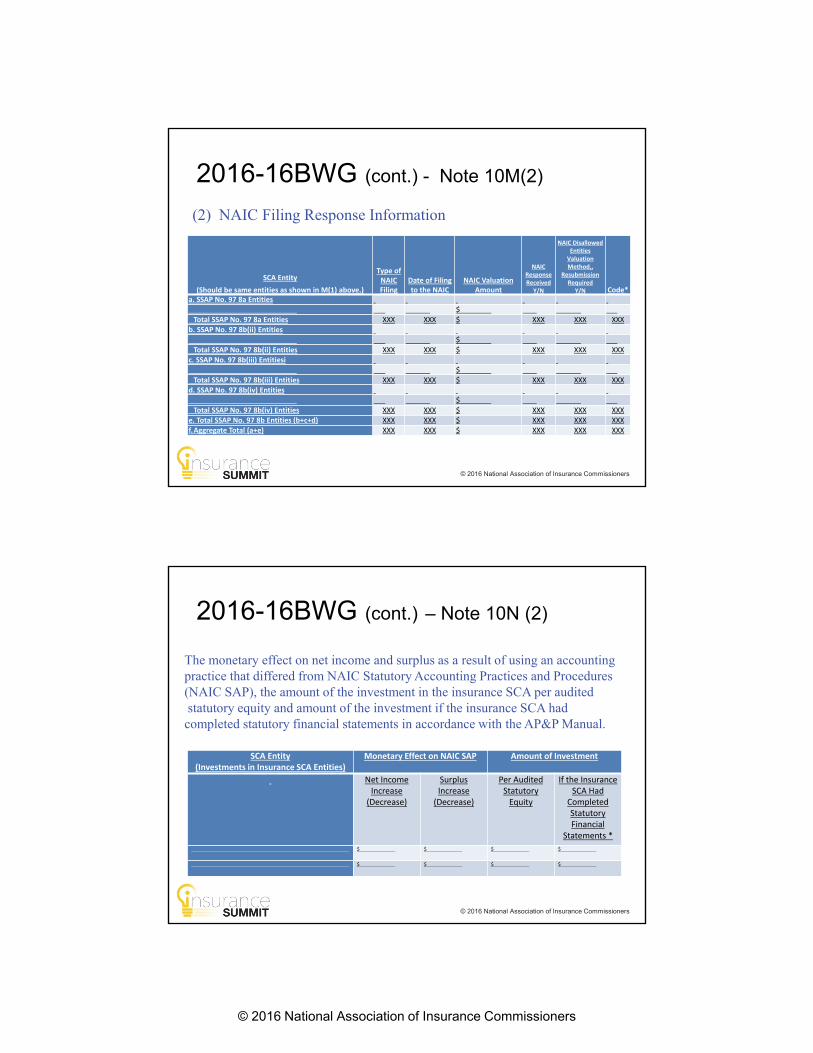

2016-16BWG (cont.) - Note 10M(2)

SCA Entity(Should be same entities as shown in M(1) above.)

Type of NAIC Filing

Date of Filing to the NAIC

NAIC Valuation Amount

NAIC Response Received

Y/N

NAIC Disallowed Entities

Valuation Method,,

Resubmission Required

Y/N Code*a. SSAP No. 97 8a Entities

$Total SSAP No. 97 8a Entities XXX XXX $ XXX XXX XXX

b. SSAP No. 97 8b(ii) Entities$

Total SSAP No. 97 8b(ii) Entities XXX XXX $ XXX XXX XXXc. SSAP No. 97 8b(iii) Entitiesi

$Total SSAP No. 97 8b(iii) Entities XXX XXX $ XXX XXX XXX

d. SSAP No. 97 8b(iv) Entities$

Total SSAP No. 97 8b(iv) Entities XXX XXX $ XXX XXX XXXe. Total SSAP No. 97 8b Entities (b+c+d) XXX XXX $ XXX XXX XXXf.Aggregate Total (a+e) XXX XXX $ XXX XXX XXX

(2) NAIC Filing Response Information

© 2016 National Association of Insurance Commissioners

2016-16BWG (cont.) – Note 10N (2)

SCA Entity(Investments in Insurance SCA Entities)

Monetary Effect on NAIC SAP Amount of Investment

Net Income Increase

(Decrease)

Surplus Increase

(Decrease)

Per Audited Statutory

Equity

If the Insurance SCA Had

Completed Statutory Financial

Statements *$ $ $ $

$ $ $ $

The monetary effect on net income and surplus as a result of using an accounting practice that differed from NAIC Statutory Accounting Practices and Procedures (NAIC SAP), the amount of the investment in the insurance SCA per auditedstatutory equity and amount of the investment if the insurance SCA had

completed statutory financial statements in accordance with the AP&P Manual.

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

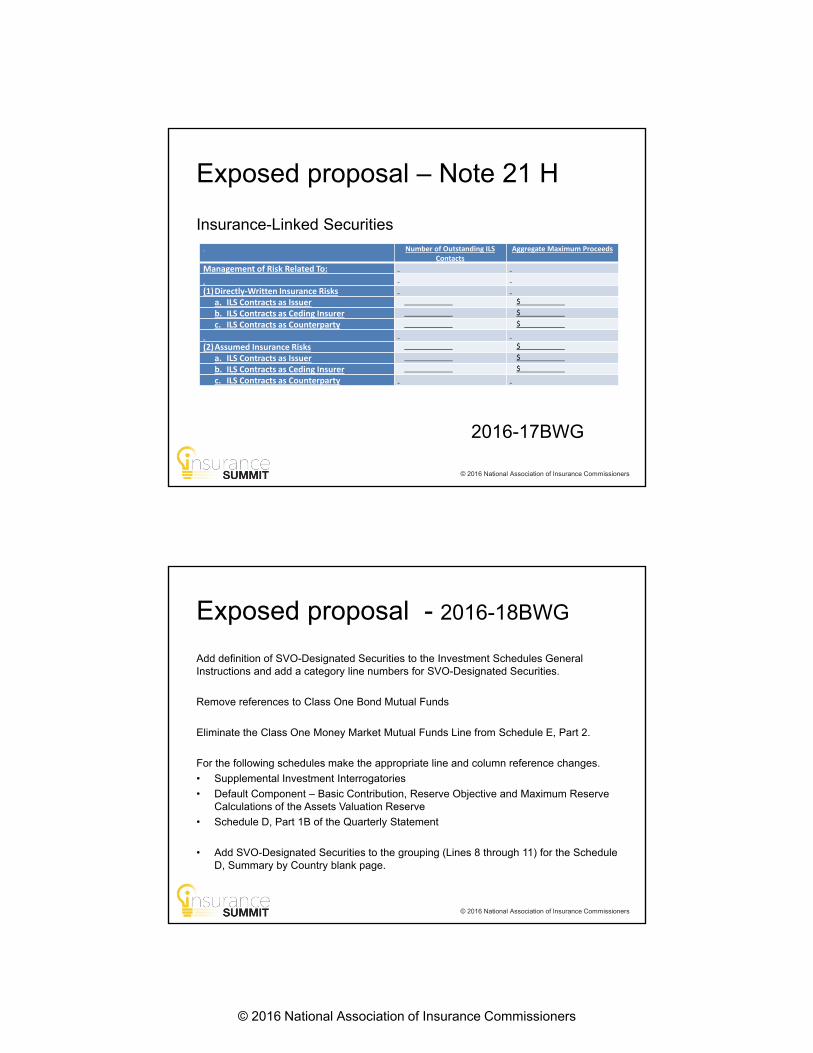

Exposed proposal – Note 21 H

Insurance-Linked Securities

2016-17BWG

Number of Outstanding ILS Contacts

Aggregate Maximum Proceeds

Management of Risk Related To:

(1)Directly-Written Insurance Risksa. ILS Contracts as Issuer $b. ILS Contracts as Ceding Insurer $c. ILS Contracts as Counterparty $

(2)Assumed Insurance Risks $a. ILS Contracts as Issuer $b. ILS Contracts as Ceding Insurer $c. ILS Contracts as Counterparty

© 2016 National Association of Insurance Commissioners

Exposed proposal - 2016-18BWG

Add definition of SVO-Designated Securities to the Investment Schedules General Instructions and add a category line numbers for SVO-Designated Securities.

Remove references to Class One Bond Mutual Funds

Eliminate the Class One Money Market Mutual Funds Line from Schedule E, Part 2.

For the following schedules make the appropriate line and column reference changes.

• Supplemental Investment Interrogatories

• Default Component – Basic Contribution, Reserve Objective and Maximum Reserve Calculations of the Assets Valuation Reserve

• Schedule D, Part 1B of the Quarterly Statement

• Add SVO-Designated Securities to the grouping (Lines 8 through 11) for the Schedule D, Summary by Country blank page.

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

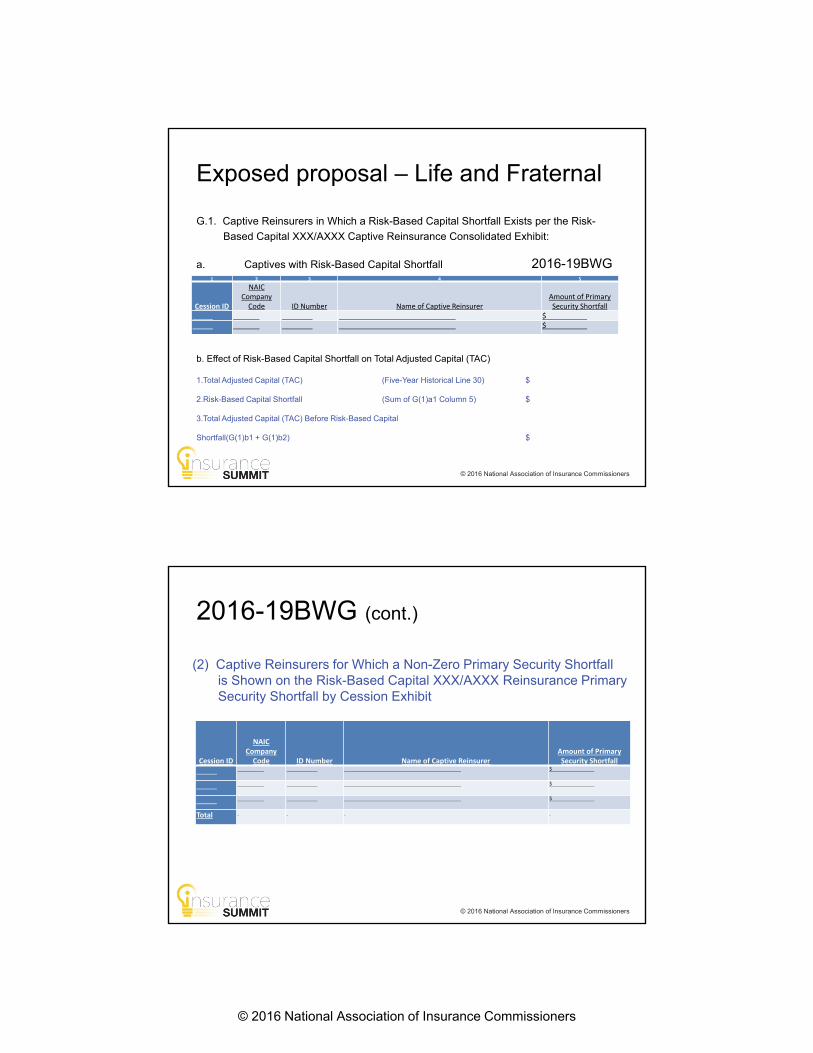

Exposed proposal – Life and Fraternal

G.1. Captive Reinsurers in Which a Risk-Based Capital Shortfall Exists per the Risk-

Based Capital XXX/AXXX Captive Reinsurance Consolidated Exhibit:

a. Captives with Risk-Based Capital Shortfall 2016-19BWG 1 2 3 4 5

Cession ID

NAIC Company

Code ID Number Name of Captive ReinsurerAmount of Primary Security Shortfall

$$

b. Effect of Risk-Based Capital Shortfall on Total Adjusted Capital (TAC)

1.Total Adjusted Capital (TAC) (Five-Year Historical Line 30) $

2.Risk-Based Capital Shortfall (Sum of G(1)a1 Column 5) $

3.Total Adjusted Capital (TAC) Before Risk-Based Capital

Shortfall(G(1)b1 + G(1)b2) $

© 2016 National Association of Insurance Commissioners

2016-19BWG (cont.)

Cession ID

NAIC Company

Code ID Number Name of Captive ReinsurerAmount of Primary Security Shortfall

$

$

$

Total

(2) Captive Reinsurers for Which a Non-Zero Primary Security Shortfall is Shown on the Risk-Based Capital XXX/AXXX Reinsurance PrimarySecurity Shortfall by Cession Exhibit

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

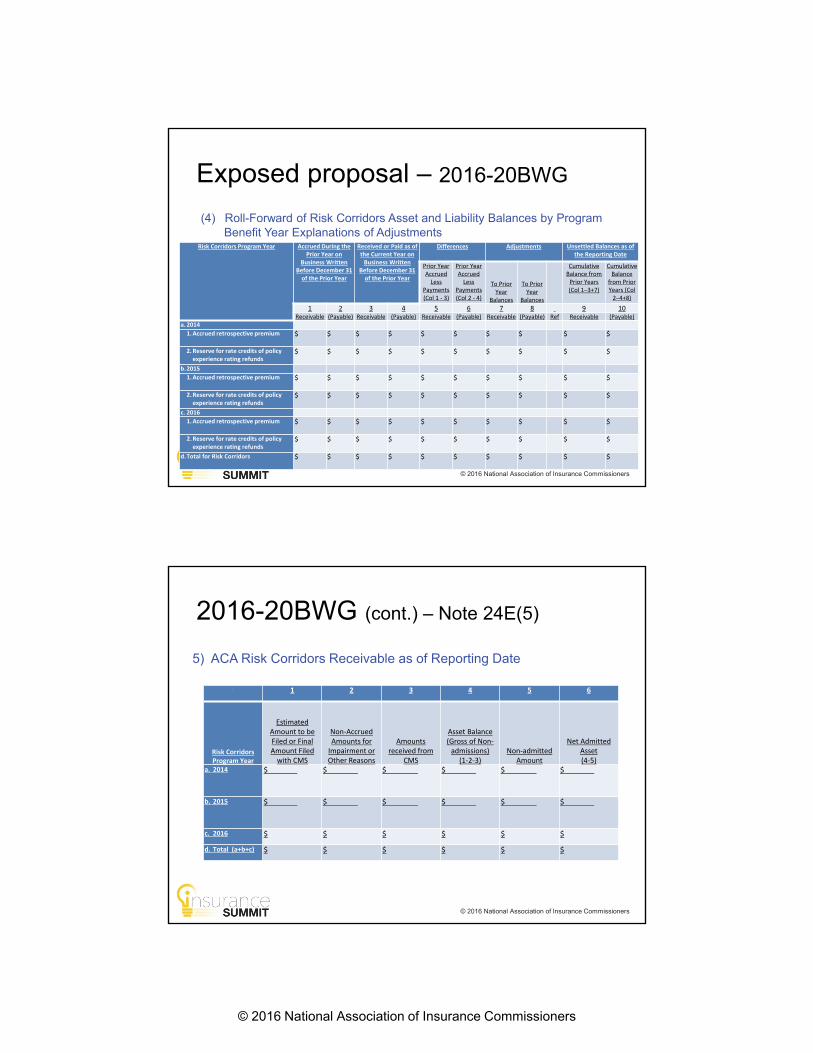

Exposed proposal – 2016-20BWG

Risk Corridors Program Year Accrued During the Prior Year on

Business Written Before December 31

of the Prior Year

Received or Paid as of the Current Year on

Business Written Before December 31

of the Prior Year

Differences Adjustments Unsettled Balances as of the Reporting Date

Prior Year Accrued

Less Payments (Col 1 - 3)

Prior Year Accrued

Less Payments (Col 2 - 4)

To Prior Year

Balances

To Prior Year

Balances

Cumulative Balance from

Prior Years (Col 1–3+7)

Cumulative Balance

from Prior Years (Col

2–4+8)

1 2 3 4 5 6 7 8 9 10Receivable (Payable) Receivable (Payable) Receivable (Payable) Receivable (Payable) Ref Receivable (Payable)

a. 20141. Accrued retrospective premium $ $ $ $ $ $ $ $ $ $

2. Reserve for rate credits of policy experience rating refunds

$ $ $ $ $ $ $ $ $ $

b.20151. Accrued retrospective premium $ $ $ $ $ $ $ $ $ $

2. Reserve for rate credits of policy experience rating refunds

$ $ $ $ $ $ $ $ $ $

c. 20161. Accrued retrospective premium $ $ $ $ $ $ $ $ $ $

2. Reserve for rate credits of policy experience rating refunds

$ $ $ $ $ $ $ $ $ $

d.Total for Risk Corridors $ $ $ $ $ $ $ $ $ $

(4) Roll-Forward of Risk Corridors Asset and Liability Balances by ProgramBenefit Year Explanations of Adjustments

© 2016 National Association of Insurance Commissioners

2016-20BWG (cont.) – Note 24E(5)

1 2 3 4 5 6

Risk Corridors Program Year

Estimated Amount to be Filed or Final Amount Filed

with CMS

Non-Accrued Amounts for

Impairment or Other Reasons

Amounts received from

CMS

Asset Balance (Gross of Non-

admissions) (1-2-3)

Non-admitted Amount

Net Admitted Asset(4-5)

a. 2014 $ $ $ $ $ $

b. 2015 $ $ $ $ $ $

c. 2016 $ $ $ $ $ $

d. Total (a+b+c) $ $ $ $ $ $

5) ACA Risk Corridors Receivable as of Reporting Date

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

Exposed proposal – 2016-21BWG

H – Restricted Assets:(4) Collateral Received and Reflected as Assets Within the Reporting Entity’s Financial Statements

1 2 3 4

Collateral AssetsBook/Adjusted Carrying Value Fair Value

% or Assets to Total Assets (Admitted

and Nonadmitted *% of Assets to Total Admitted Assets **

a. Cash $ $ % %b. Schedule D, Part 1 % %c. Schedule D, Part 2, Section 1 % %d. Schedule D, Part 2, Section 2 % %e. Schedule B % %f. Schedule A % %g. Schedule BA, Part 1 % %h. Schedule DL, Part 1 % %i. Other % %j. Total Collateral Assets

(a+b+c+d+e+f+g+h+i) $ $ % %

Amount% of Liability to Total

Liabilities *k. Recognized Obligation to Return Collateral Asset $ %

© 2016 National Association of Insurance Commissioners

Exposed proposal - 2016-22BWG

General Interrogatories (annual and quarterly)

28.05 Investment management – Identify all investment advisors, investment managers,broker/dealers, including individuals that have the authority to make investmentdecisions on behalf of the reporting entity. For assets that are managed internally byemployees of the reporting entity, note as such. [“…that have access to the investmentaccounts”; “…handle securities”]

1Name Firm or Individual

2Affiliation

28.051 For those firms/individuals listed in the table for Question 28.05, do any firms/individuals unaffiliated with the reporting entity (i.e. designated with a “U”) manage more than 10% of the reporting entity’s assets? Yes [ ] No [ ]

28.052 For firms/individuals unaffiliated with the reporting entity (i.e. designated with a “U”) listed in the table for Question 28.05, does the total assets under management aggregate to more than 50% of the reporting entity’s assets? Yes [ ] No [ ]

© 2016 National Association of Insurance Commissioners

© 2016 National Association of Insurance Commissioners

2016-22BWG (cont.)

28.06 For those firms or individuals listed in the table for

28.05 with an affiliation code of “A” (affiliated) or “U”

(unaffiliated), provide the information for the table

below.

1

Name Firm or Individual

2Central

RegistrationDepository

Number

3

Legal Entity Identifier (LEI)

3

Registered With

4Investment

Management Agreement (IMA) Filed

© 2016 National Association of Insurance Commissioners

Questions?