momentum strategies: evidence from the pacific … strategies: evidence from the pacific ... lilian...

TRANSCRIPT

Momentum Strategies: Evidence from the Pacific BasinStock Markets

Allaudeen Hameed* and Kusnadi Yuanto

Department of Finance and Accounting, Faculty of Business Administration,National University of Singapore, 10 Kent Ridge Crescent,Singapore 119260

First Draft: June 1999This version: August 1999

Abstract

We find some evidence of medium-term return continuation in our sample of six

Asian stock markets. An unrestricted momentum investment strategy does not yield

significant momentum returns due to the high volatility of returns in these emerging

markets. However, a country neutral strategy that fully invests in all countries over

the period 1981-1994 generates a statistically significant excess return of 0.37 percent

per month over a six-month holding period, before transaction costs. Further analyses

show that the momentum returns of more than 1 percent per month is observed when

applied to less diversified portfolios consisting of firms with small market

capitalization or high volume of trade, suggesting that price momentum is related to

firm specific factors.

Keywords: Medium-term return continuation; Asian stock markets; Momentum

investment strategy; Price predictability

* Corresponding author. Tel: 65-8743034; e-mail: [email protected].

We thank Narasimhan Jegadeesh, Grant McQueen, Lilian Ng and Geert Rouwerhorst for helpfulcomments. Allaudeen Hameed and Kusnadi Yuanto acknowledges the financial support from the NUSAcademic Research Grant and NUS Research Scholarship respectively. All errors are ours.

1

1. Introduction

A recent stream of research papers has documented the existence of momentum

effect in stock returns: stocks that outperformed (under-performed) the average stock

return in the past few months tend to perform better (worse) than the average stock

over the subsequent few months. Using the post-1940 data for stocks traded on the

New York Stock Exchange and the American Stock Exchange, Jegadeesh and Titman

(1993) report that a zero-cost momentum strategy of buying past winners and selling

past losers generates an average of 1 percent per month. Similar evidence is reported

by Rouwenhorst (1998) for stocks traded on European markets.

While the evidence of momentum in stock prices over the medium term of 3 to 12

months is well accepted for the developed markets in the US and Europe, the

interpretation of the evidence has been mixed. Barberis, Shliefer and Vishny (1998),

Daniel, Hirshleifer and Subrahmanyam (1998) and Hong and Stein (1999) present

theoretical (behavioral) models of investor behavior suggesting that price momentum

is consistent with investors having imperfect information. The slow price reactions

arise from revisions in investor expectations based on past prices and in response to

new information. Chan, Jegadeesh and Lakonishok (1996) argue that under-reaction

of stock prices to information contained in past stock returns and past company

earnings give rise to price momentum.

An alternative explanation for the momentum profits is that differential risks and

risk premia are associated with the winner and loser portfolios so that the momentum

profits reflect compensation for investing in a risky portfolio. Fama and French

(1996) examine if their three-factor asset pricing model can explain momentum

profits reported by Jegadeesh and Titman (1993) and find their model is inadequate.

Conrad and Kaul (1998) show that the momentum strategy’s average profits reflect

2

the result of buying (on average) high mean return securities and selling (on average)

low mean return securities. If the differences in the unconditional mean returns are

attributable to variation in expected returns, then, the momentum profits are due to

cross-sectional differences in risk. Moskowitz and Grindblatt (1999) suggest that the

profitability of the momentum strategy is explained by momentum in industry factors,

and possibly indicate industry-related risk as the source of the profits.

An important drawback of the studies that examine the U.S. data for explanations

of the trends and predictable patterns is that they may suffer from data-snooping

biases as noted by Lo and MacKinlay (1990) and Foster, Smith and Whaley (1996).

Financial researchers have observed and treated for momentum with the same data,

hence making it difficult to obtain independent evidence.

In this paper, we offer “out-of-sample” evidence on the robustness of momentum

trading strategies, by examining stock returns in a group of emerging, Asia Pacific

stock markets. While substantial work has been done using data from developed

markets, very little is known about the predictability of returns in the emerging

markets. If momentum profits are due to the slow reaction of prices to information

contained in past returns, we ought to find similar evidence in other markets. We

know from prior research that emerging markets are characterized by low correlation

with other emerging markets and with developed markets (see Harvey (1995)).

Consequently, evidence from emerging markets is particularly interesting as it

provides a validation test on a sample that is not highly correlated with the data in

previous papers.

An exception to the dearth of evidence on medium-term predictability using

individual securities in emerging markets is a recent paper by Rouwenhorst (1999),

who finds some evidence of momentum profit in emerging markets. He reports a

3

statistically significant average monthly return of 0.39 percent for the momentum

strategy of buying past-six month winners and selling past losers. The average return

is much smaller than the average of 1 percent per month reported in Jegadeesh and

Titman (1993) and Rouwenhorst (1998) for developed markets. In addition,

Rouwenhorst (1999) finds significant momentum profits in only 6 out of the 20

emerging markets in his sample.1 Trading in emerging markets is associated with high

transaction costs (such as brokerage commissions and bid-ask spreads) and low

liquidity in some of the listed securities. Given the high trading costs, the existing

evidence does not indicate the economic significance of the momentum returns in

these markets. Our paper attempts to shed additional light on the presence and nature

of momentum returns in emerging markets. Specifically, we also examine the effect

of firm size and trading volume on return predictability.

We implement the momentum trading strategies on securities traded on six Asian

markets: Hong Kong, Malaysia, Singapore, South Korea, Taiwan and Thailand. We

find momentum in prices evident in the smallest firms and the firms with high

volume. For example, the momentum strategy that invests in the smallest 30 percent

of firms across the six markets generates an average profit of 1.21 percent per month

over a six-month holding period. The average profit is 1.12 percent month if the

strategy is implemented on only the top 30 percent of all firms in terms of trading

volume (turnover). While these are the significant strategies, the more general,

unrestricted momentum strategies of buying winners and selling losers yield

insignificant returns across various holding periods. Following Jegadeesh and Titman

1 Rouwenhorst (1999) argues that it is difficult to detect momentum in individual countries because of

the highly volatile nature of emerging market returns. The statistical significance increases when one

4

(1993) and Rouwenhorst (1998), we examine 16 unrestricted momentum strategies

that involve ranking securities based on their J-month performance (J=3,6,9 and 12)

and evaluating the returns over the next K-months (K=3,6,9 and 12). None of the 16

strategies produce significant momentum returns.2 We also implement restricted

strategies to obtain better-diversified portfolios. Of these strategies, only the country

neutral strategy produces a statistically significant return of 0.37 percent, which is

consistent with the 0.39 percent monthly returns reported in Rouwenhorst (1999).

Our results can be summarized as follows. First, an unrestricted momentum

trading strategy fails to show significant price momentum in emerging markets

(although a lower variance of the traded portfolio returns is achieved by forming

portfolios that are diversified across countries). Second, we find that firm

characteristics such as size and trading volume influence return predictability: returns

on small firms and high turnover stocks seem to exhibit some medium-term

momentum. Our results characterize the medium-term price predictability

phenomenon and its relation to firm characteristics in emerging markets.

The rest of the paper is organized as follows: Section II describes the sample

while Section III documents the returns on momentum trading strategies. Section IV

analyses the momentum profits across all sample countries, size and turnover sorted

groupings and investigates the influence of calendar effects. Section V concludes the

paper.

considers a diversified portfolio of many markets due to the low pair-wise correlation between these

markets.

2 These results are robust to skipping a month after ranking and defining winners and losers based on

the top/bottom 10 percent and 30 percent of the securities. Our findings are also unaffected by the

decision to exclude the extreme 5 percent of returns each period.

5

2. Data

The sample consists of monthly stock returns on over 1000 individual securities

traded on six Asian markets over the period 1979-1994. The data is taken from the

PACAP database, compiled by the University of Rhode Island. The countries

included in the analysis are: Hong Kong (201 firms), Malaysia (244 firms), Singapore

(103 firms), South Korea (309 firms), Taiwan (92 firms) and Thailand (59 firms). For

each security, we obtained the monthly price, returns, size, trading volume, and

number of days traded in a month. We used all the emerging market data available

from PACAP, except Indonesia for which the data series starts in 1990. Month-end

exchange rate information is taken from the PACAP to convert the local currency

returns to US dollar returns.

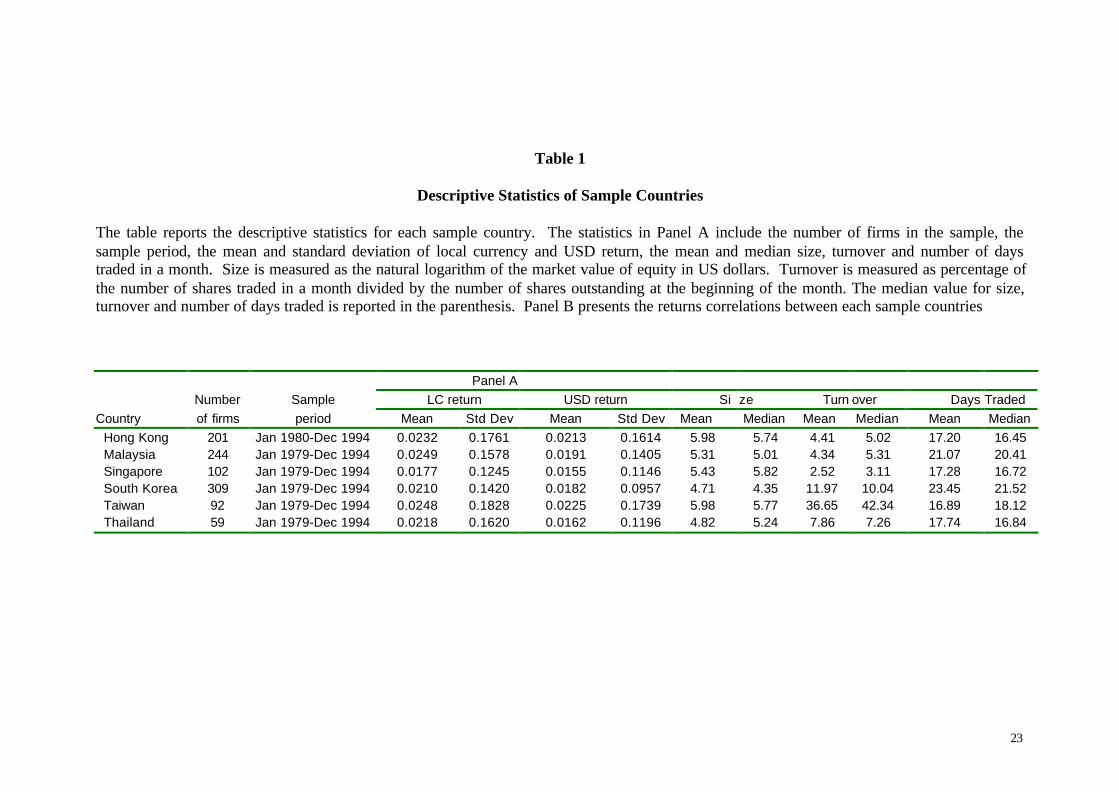

Table 1 Panel A summarizes the descriptive statistics for all the sample countries.

For local currency return, the average mean return across the six Asian countries is

about 2.2 percent per month. The mean and standard deviation of returns are slightly

smaller for returns in U.S. dollars but continue to be high relative to most developed

markets.3 The highest average U.S. dollar return of 2.25 percent is reported for

Taiwan, while the lowest average return is 1.55 percent in Singapore. The high

volatility of emerging market returns are reflected in monthly standard deviations that

are about 10 percent or more for the six countries. Similar characteristics are reported

by Bekaert and Harvey (1997).

The subsequent columns give the statistics for the mean firm size, turnover and

number of days traded in a month. Firm size is measured as the natural logarithm of

the market value of equity for the sample firms (in US dollars) included in each

3 The higher value for local currency return than the US dollar return indicates a slight negative

correlation between the local currency return and exchange rate changes.

6

country. The mean firm size is highest in Taiwan and Hong Kong (5.98) and lowest

in South Korea (4.71).

Two measures of trading activity are reported in the last few columns of Table 1

(Panel A). Turnover is measured as percentage of the number of shares traded in a

month divided by the number of shares outstanding, which is implicitly an equally-

weighted measure of turnover. The mean share turnover shows a large cross-sectional

variation across the emerging Asian markets. The maximum turnover is 37 percent in

Taiwan, which is almost 15 times the average turnover of 2.5 percent in Singapore.

The last statistic is the number of days traded in a month, which is similar across all

countries, with an average of about 19 trading days per month.

Table 1 Panel B reports the return correlation coefficient between each sample

countries. With the exception of Singapore and Malaysia, the market exhibits a low

level of correlation in stock returns across these markets. The high correlation of 81

percent between returns in Singapore and Malaysia is due to the historical stock

market linkages between the countries and the high level of trading by (local)

investors across both markets. The correlation between other pairs of countries ranges

between 7 percent and 44 percent. South Korea appears to have the lowest correlation

with all other countries.

3. Momentum trading strategy

Our momentum trading strategy is similar to that used in Jegadeesh and Titman

(1993) and Rouwenhorst (1998). The relative strength portfolios are constructed as

follows: at the end of each month, all stocks from the six sample countries are ranked

in ascending orders based on their past J-months return (J=3, 6, 9, and 12). They are

then assigned to one of the ten relative strength decile portfolios (1 represents the

7

“Loser” portfolio or the one with lowest past performance and 10 represents the

“Winner” portfolio or the one with the highest past performance). These portfolios

are equally weighted at formation and then held for K subsequent months (K=3, 6, 9

and 12). This gives us 16 combinations of J and K months, and hence, 16 momentum

strategies.

To check for robustness of our results to our definition on winners and losers, we

also assign the stocks into three portfolios (instead of ten) based on past J month

performance: the top 30 percent of firms are classified as winners while the bottom 30

percent are the losers. This alternative measure of momentum places less emphasis on

the tail-end of the distribution (which may be important given the high volatility in

emerging markets). A similar measure is used in Moskowitz (1997), Rouwenhorst

(1999) and Hong, Lim and Stein (1999).

Since only monthly returns are available, while the holding period exceeds 1

month, an overlap in the holding period returns is created. As a result, K-composite

portfolios are formed, each of which are initiated one month apart. In each month,

1/K of the holdings are revised and the rest are carried over from the previous month.

As an example: towards the end of month t, the J=3, K=3 portfolio of Winners consist

of three parts: a position carried over from the investment at the end of month t-3 in

the top 10 percent of firms with highest past three-months performance as of t-3, and

two similar positions resulting from similar investment in month t-2 and t-1

respectively. At the end of month t, the first position is liquidated and replaced with

an investment in the stocks with highest past three-month performance as of time t.

Table 2 presents the monthly average returns of the strategies implemented on all

stocks in all sample countries from 1981 to 1994, where winners and losers are

8

defined as the top and bottom ten percent of past returns. 4 The table shows that, for

the six month interval (J=6, K=6), an equally-weighted portfolio formed from stocks

in the bottom decile of past six-month performance (Loser portfolio) earns 1.91

percent, while the corresponding Winner portfolio earns 2.44 percent. A zero-cost

relative strength portfolio consisting of buying the past winner and selling the past

loser (Winner-Loser) gives a positive, but statistically insignificant, excess return of

0.53 percent per month. The highest average return of 0.79 percent per month (or 9.48

percent per year) is obtained for a 12 month holding period (K=12), formed by

ranking the stocks on past 6 and 9 months performance (J=6 and 9). However, none of

the strategies yield statistically significant returns at conventional significant levels.

The portfolios in Table 2 are formed at the end of the ranking period. The end-of

month prices used in the ranking period may be either the bid or ask price. The

month-end closing price of a loser security at the end of ranking period is likely to be

the bid price while the closing price of the winner security is likely to be the ask price.

The loser and winner security are likely to experience return reversal in the holding

period – leading to a reduction in momentum returns. To alleviate the bid-ask effects

on momentum returns, if any, we delay the implementation of the buying and selling

decision by one month. Our unreported results show that across all investment

strategies, delaying the portfolio holding period by one month does not affect the

results. The inability to detect significant momentum profits is not due to reversals in

prices over the shorter term.

Another possible reason why price continuation in returns in Table 2 is not

observed is that our results may be influenced by return outliers as represented by the

4 Note that two years are lost due to the J=12, K=12 strategy, which requires 12 months of performance

ranking and another 12 months of portfolio holding.

9

extreme deciles. Extreme performers in the ranking period may reduce the signal-to-

noise properties of the returns. To account for the outlier effect, we rank the stock

returns into three portfolios: the top and bottom 30 percent is classified as winners and

losers respectively. This alternative classification allows for a broader-based measure

and is less affected by extreme returns. A similar measure is used in Rouwenhorst

(1999) and Hong, Lim and Stein (1999). The results confirm our finding that the

momentum returns in our sample are not statistically significant.5 Hence, the

momentum portfolio results reported in this paper are not affected by the method used

to form the portfolios. 6

Compared to the results by Jegadeesh and Titman (1993) and Rouwenhorst

(1998), the magnitude and statistical significance of momentum profits in Asian stock

markets are considerably less than those earned in either US or Europe. The bid-ask

bounce effect, return outliers, and portfolio formation methods are not likely to be

source of the difference in findings.

To closely examine the pattern of medium term price movements in the Asian

markets, the remainder of the paper will concentrate on a particular momentum

strategy: one that is formed on the basis of lagged 6-month return and held for the

next 6 months using decile portfolios. A similar six-month strategy is examined in

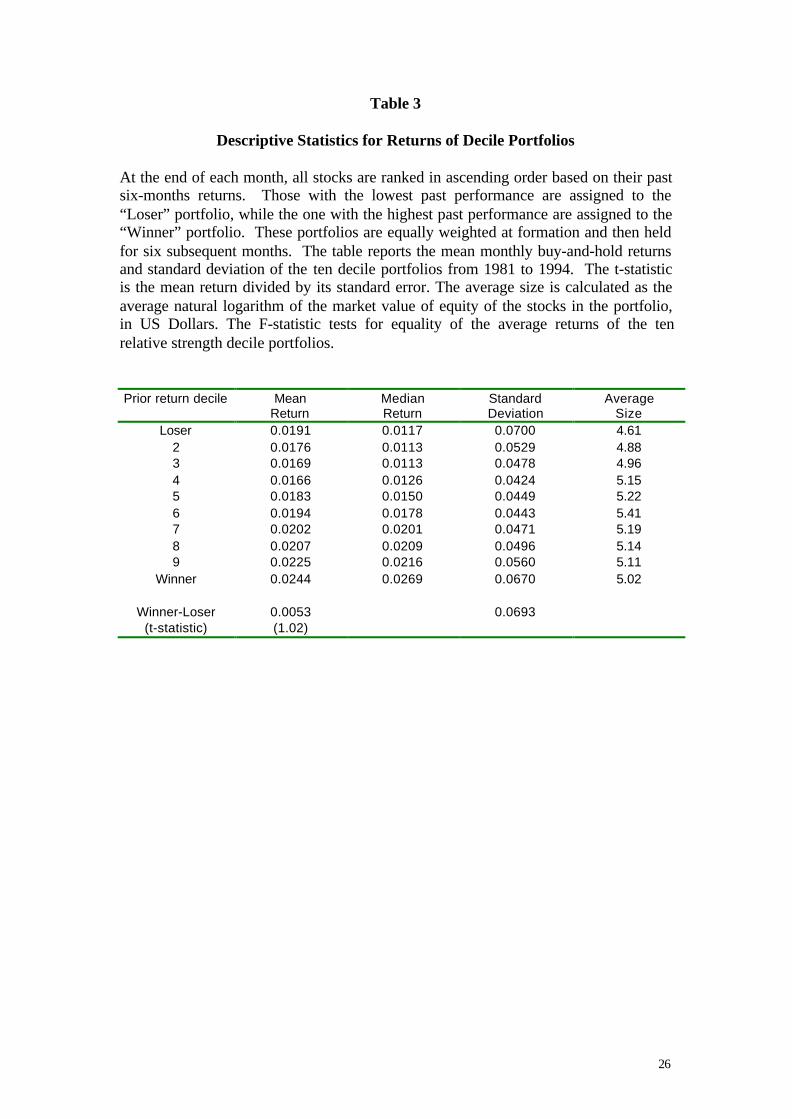

Jegadeesh and Titman (1993), Rouwenhorst (1988, 1999) and others. Table 3 reports

5 The average returns to buying the top 30 percent of stocks and shorting the bottom 30 percent of

stocks are generally similar to that reported for the decile portfolios and none of the 16 strategies yield

significant momentum returns. The results are qualitatively unchanged if we implement the momentum

strategy with a one-month lag.

6 We have also excluded the extreme 5 percent of the ranking period returns in the formation of winner

and loser portfolios. The results are qualitatively unaffected by these extreme observations for both the

decile portfolio and the top/bottom 30 percent portfolio return measures.

10

a high mean return in the extreme deciles with the smallest return recorded for the

middle deciles. In contrast to the results for the U.S. and European markets, we do not

observe a positive relation between past performance and subsequent average returns.

As noted by Rouwenhorst (1999), the standard deviation of returns are large;

even for the combined portfolio of winner-loser, the standard deviation of returns is

6.9 percent. The correlation between the winner and loser portfolios is a high 49.0

percent. Hence, the unrestricted relative strength strategy may not be well diversified

and the high volatility of returns may make it difficult to detect statistical significance.

The winner and loser portfolios may predominantly take positions on securities from a

specific country, making the portfolio ill-diversified. The next section will examine

the effect of forming portfolios that are diversified across countries. We also examine

if other firm specific variables like size and volume play a contributory role in price

momentum.

4. Momentum Strategies and Country, Size and Turnover Effects

The previous section discusses the relative strength strategy that combines stocks

from all the sample countries without any requirement to ensure diversification of the

portfolio across countries. This raises two concerns. Firstly, since the winner and loser

portfolio classification procedure assigns larger weight to a set of firms which are the

extreme past performers; these firms may be highly volatile, small and thinly traded.

Our previous results do not relate price momentum to any of these firm

characteristics. Secondly, the firms may not be diversified across the countries – most

firms may come from a country with the highest variation in returns. To control for

these two problems, we form an international (or regional) portfolio that invests

11

across several markets and consider a momentum strategy that is fully invested in all

six countries in the sample.

4.1 Country-Neutral Relative Strength Strategies

Return continuation in international stock returns may be due to two potential

sources: country momentum and firm-specific momentum. Persistence in country

specific performance may tilt the winner and loser portfolio weights to countries with

strong and weak performance respectively. If stocks in Malaysia (Taiwan) are

experiencing a boom (bear) market, their returns will be greater (lower) compared to

the returns of stocks from the other markets. Hence, the resulting Winner (Loser)

portfolio will be concentrated in Malaysian (Taiwanese) stocks. Clearly, this strategy

is associated with a portfolio that is poorly diversified across countries. Evidence of

country momentum is presented in Assness, Liew and Stevens (1996) and Chan,

Hameed and Tong (1998). Our results so far suggest that country momentum may be

difficult to detect in view of the high volatility in these emerging markets. Firm

specific momentum in performance, however, is likely to be more discernible in a

portfolio that is geographically well diversified.

Country-neutral relative strength portfolios are formed by ranking stocks in

ascending orders based on their past six-months performance relative only to stocks

from the same market. The top 10 percent of stocks with highest past six-months

performance from each country are assigned to the Winner portfolio and the bottom

10 percent to the Loser portfolio. These portfolios are then held for the subsequent

six-months. The resulting decile portfolios have equal country weights and are,

hence, country-neutral. Table 4 presents the mean return and corresponding t-statistic

for the country-neutral relative strength portfolio, as well as for individual countries.

12

The standard deviation of the momentum returns shows a large drop from 0.7 percent

to 0.2 percent, indicating a strong diversification effect. After accounting for country

composition, the mean return of the zero-cost portfolio is statistically significant at

0.37 percent per month. Hence, equal-weighting the sample countries has the effect of

reducing the volatility of the relative strength strategy and a better risk control for the

portfolio.

The same table also reports the excess returns to the Winner-Loser portfolios by

individual countries. The average excess returns figure is positive for each of the six

sample countries, with the highest in Taiwan (0.6 percent) and lowest in Malaysia

(0.19 percent). However, all the excess returns are not significantly different from

zero and as expected, their standard deviations are more than twice that of the

country-neutral momentum strategy. This suggests that a large portion of the risks of

the unrestricted momentum strategy is attributed to country-specific factors, which

can be diversified internationally. Our results are consistent with Rouwenhorst (1998)

who finds that the momentum returns in the European stocks are unlikely to be due to

country-specific momentum but are more likely to be attributable to under-reaction to

firm specific shocks. Our findings also reinforce the results in Rouwenhorst (1999)

concerning the difficulty in finding significant price momentum in individual

emerging stock markets.7

7 On examining sub-period results, we fail to find significant momentum returns in later years, 1989-

1994. This further reduces the significance of country-neutral momentum returns, to the extent that the

strategy may not be feasible in the early years due to restrictions on foreign investments in many

emerging countries (e.g. S. Korea and Taiwan). While market segmentation may explain some of the

observed results, we have to be cautious in interpretation as the tests based on a shorter sample may

lack power to reject the null.

13

4.2 Size and Relative Strength Strategies

The previous section discussed the effect of equally weighting each country in the

implementation of the relative strength strategy. However, as with the unrestricted

relative strength strategy, the country-neutral results do not account for size factors.

Size-based groupings are constructed by first ranking all the stocks according to size

as measured by market value of equity in U.S. dollars. The stocks containing the

smallest 30 percent, medium 40 percent and the largest 30 percent are assigned into

small, medium and large size groupings (denoted as S1, S2 and S3 respectively).

Within each size groupings, the stocks are sorted into ten deciles based on their past

six-months performance and are held for subsequent six months (J=6, K=6). The

Loser portfolio consists of ten percent of stocks with the lowest past six-months

performance, while the Winner portfolio consists of ten percent of stocks with the

highest past six-months performance, within each size grouping. From Table 5, it can

be seen that the positive relation between past return and future performance is

strongest in the small firms: the relative strength strategy of buying winner (decile

P10) and selling past losers (decile P1) yields a significant excess return (Winner-

Loser) of 1.21 percent. The other two size groupings (medium and large size firms) do

not produce significant momentum profits. 8 Hence, price momentum seems to be

concentrated in the small firms.

Our result is consistent with Hong et al (1999), who also find that the momentum

effect is the strongest in the very smallest stock and it declines sharply as market

capitalization increases. Their results are driven by the hypothesis that firm-specific

information, especially negative information, diffuses only gradually across the

14

investing public. If momentum comes from gradual information flow, then there

should be more momentum in those stocks for which information gets out more

slowly, ie: small stocks.

While significant relative strength excess return associated with small firms is

reported, this unrestricted strategy may be due to taking excessive portfolio positions

in a few countries. If the international portfolio strategy aims to be diversified, the

relative strength strategy must not huge country positions. To examine whether the

small firm price momentum holds across markets, we consider a size/country neutral

strategy.

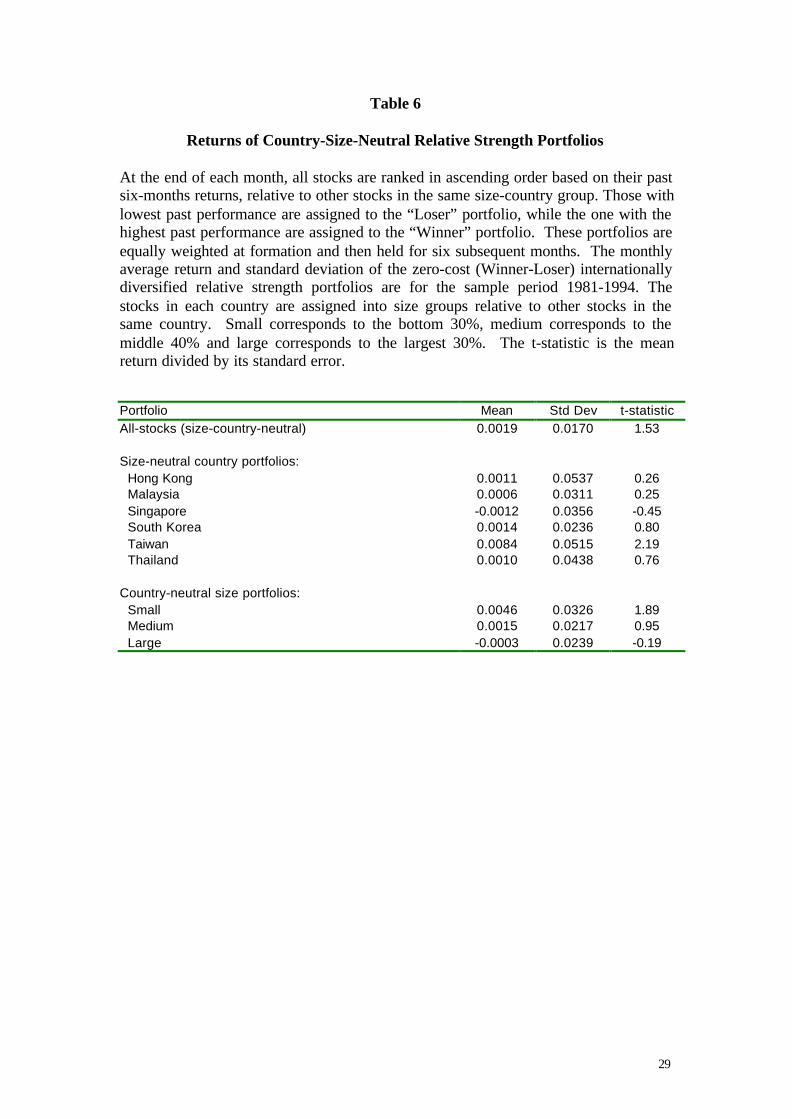

The size-country-neutral portfolios are constructed by first ranking all the stocks

in the six countries into three size-groups: small (lowest 30 percent), medium (middle

40 percent) and large (highest 30 percent). This produces 18 size-country groups.

Stocks in each of the 18 groups are further ranked according to their past six-months

performance. The Loser portfolio consists of ten percent of stocks with the lowest

past six-months performance from each size-country group, while the Winner

portfolio consists of ten percent of stocks with the highest past six-months

performance from each size-country group. Table 6 shows that the average zero-cost

portfolio return to the strategy that is country and size neutral is insignificant at 0.19

percent and the profits reported for the portfolio of small firms in these markets

decreases from 1.21 percent to 0.46 percent. The relative strength portfolio strategy

for the small firms become weaker when we restrict the portfolio weights to be

country-neutral, showing significance only at a 10 percent level. The excess returns

8 As a robustness check, we also computed the proportion of excess returns that are positive. We reach

similar conclusion: the proportion of positive returns on the Winner-Loser portfolio for the three size

groupings S1, S2, and S3 and combined grouping, ALL are 61%, 54%, 57%, and 56%, respectively.

15

on medium and large firms continue to be insignificant, although we also see a

reduced volatility of returns. For completeness, we also report the excess returns for

each country, after controlling for the size effect. The size-neutral strategy shows

significant excess returns for only one of the six countries (Taiwan). We suggest that

return continuation in the emerging markets are not pervasive and may be driven by

firm specific characteristics like firm size.

4.3 Turnover and Relative Strength Strategies

Several recent papers indicate that trading volume (turnover) is of particular

interest to investors and may influence the behavior of return momentum. Lee and

Swaminathan (1998) show that trading volume (turnover) predicts both the magnitude

and persistence of future price momentum. For the U.S. data, a substantial increase in

momentum profits is found for high turnover stocks. They suggest that turnover may

serve as indicator of the level of investor interest in a stock. For example, the low

turnover losers is likely to be at the bottom of its “life cycle” and that a price reversal

is likely, while a high volume loser may have plenty of negative price momentum.

Similar findings are reported in Chan, Hameed and Tong (1998) who show that the

momentum profits are higher for the portfolio of countries with higher lagged trading

volume than portfolio of countries with lower lagged trading volume. These papers

suggest that higher trading volume accentuate the return continuation effect.

We examine the role of stock turnover on price momentum in our sample

countries. We do this by constructing turnover sorted relative strength portfolios,

where turnover is defined as the ratio of monthly trading volume divided by number

of shares outstanding. The stocks in the sample are first ranked into three turnover-

groups: low (lowest 30 percent), medium (middle 40 percent) and high (highest 30

16

percent), denoted as T1, T2 and T3 respectively. For each turnover group, we define

winner and loser stocks based on their past six-months performance. The Loser

portfolio consists of ten percent of stocks with the lowest past six-months

performance from each turnover group, while the Winner portfolio consists of ten

percent of stocks with the highest past six-months performance from each turnover

group. Panel A of Table 7 shows the return on zero-cost relative strength portfolio

strategy applied to each of the three turnover groups. Of the three turnover groups,

only the largest turnover group registers a significant return of 1.12 percent. The

medium and low turnover stocks yield insignificant excess returns of –0.12 percent

and 0.52 percent respectively. Our finding of significant price momentum in high

turnover stocks is consistent with that reported by Chan, Hameed and Tong (1998)

and Lee and Swaminathan (1998). The fact that share turnover plays a similar

complimentary role in predicting stock returns in emerging markets is interesting to

note.9

One possible explanation for the finding of a stronger momentum effect for the

stocks in the higher turnover group might be that highly traded stocks tend to increase

the tendency of investors' herding behaviour. These investors might overweight the

past patterns and become overconfident about the future price of such stocks and

exaggerate the mispricings. Odean (1998) proposes that overconfident traders result in

market underreaction to the information by rational traders and the subsequent

momentum in stock prices in high volume stocks.

9 We also found a monotonic increase in average returns as we move from past losers to past winners in

the high turnover group. Similar results are obtained when we compute excess returns in terms of

proportion of returns that are positive. The proportion of positive excess returns for the low, medium

and high turnover relative strength portfolios are 55%, 53% and 62% respectively.

17

The strategy of investing in high turnover stocks is not likely to be diversified

across the countries in the sample as indicated by the large standard deviation of the

excess returns. To check if the return continuation effect for the high turnover stocks

comes from betting excessively on selected countries, we construct turnover-country-

neutral portfolios. We do this by first ranking all the stocks in each of the six

countries into three turnover-groups: low (lowest 30 percent), medium (middle 40

percent) and high (highest 30 percent). In each of the 18 turnover-country groups,

stocks are further ranked according to the past six-month performance. The Loser

portfolio consists of ten percent of stocks with the lowest past six-months

performance from each turnover-country group, while the Winner portfolio consists

of ten percent of stocks with the highest past six-months performance from each

turnover- country groups. Table 7 Panel B shows the effect of equally-weighting each

country within each turnover group (country-neutral portfolios). The highest turnover

group continues to show higher profits than the lower turnover groups. The average

profits and the corresponding standard deviations are much lower. While forming

country-neutral portfolio help to achieve lower volatility through diversification, it

also reduces the significance of the price momentum – the return to the Winner-Loser

portfolio for the highest turnover group reduces to 0.29 percent and is statistically

insignificant. Hence, the evidence suggests that the return continuation effect in the

high turnover securities does not hold across all countries. For the sake of

completeness, we also report the turnover-neutral relative strength returns for each

country. Of the six countries, only Malaysia shows a statistically significant profit of

0.56 percent. Overall average profits to the 18 turnover-country neutral portfolios are

also insignificant at 0.11 percent.

18

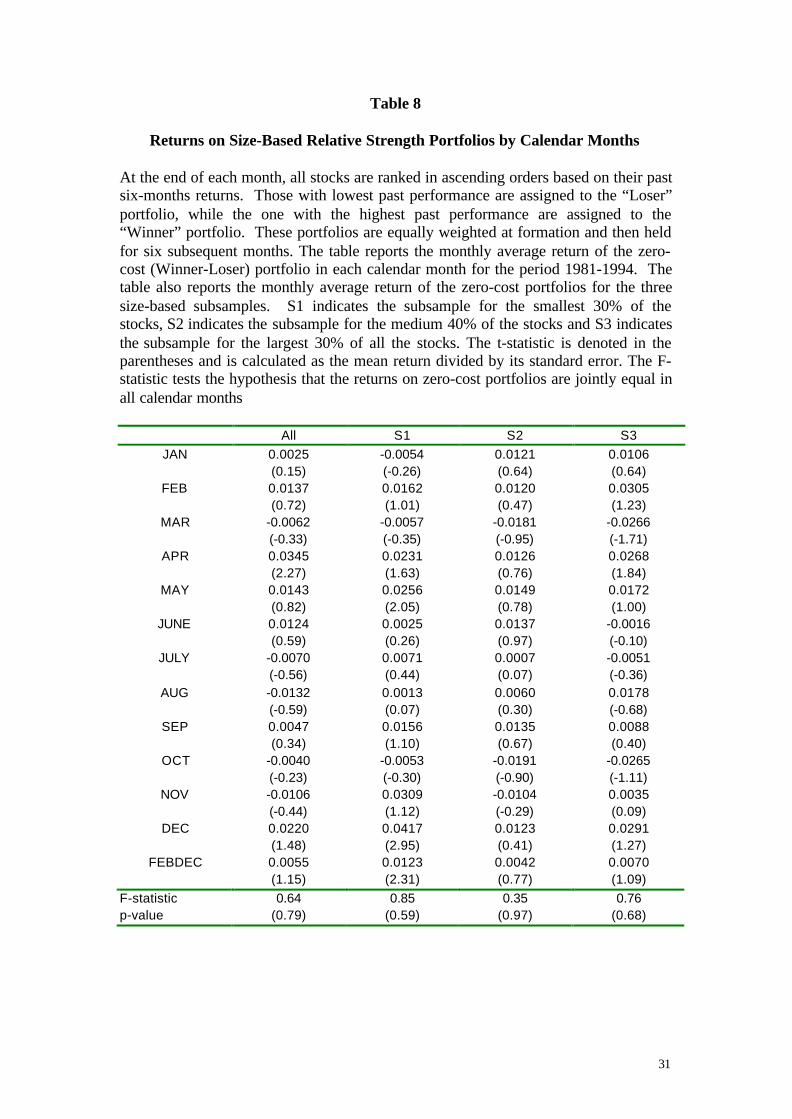

4.4 Seasonal Patterns in Relative Strength Portfolio Returns

In this section, we examine whether returns on the relative strength portfolios are

influenced by seasonal behavior in stock returns. For example, Jegadeesh and Titman

(1993) find that their relative strength portfolio returns are reduced by the price

reversals in January. Table 8 reports the breakdown of the momentum profits in each

calendar month for the size sorted sub-samples. The January effect does not exist for

the overall sample, since the average return in January is a positive 0.25 percent. 10

The average return is highest in the month of April (3.45 percent) and lowest in

August (-1.32 percent). In the size-sorted sub-samples, the patterns for the medium

and large firm samples are relatively similar to that found in the overall sample. For

the small firm sample, a slight negative (but insignificant) return in January (-0.54

percent), and a strong momentum in December (4.17 percent excess return) are

reported. Overall, the low overall relative strength excess return reported for our data

is not due to a seasonal behavior (price reversals) in any particular month. Similar

conclusion holds for the turnover-sorted portfolios, though they are not reported

here.11

5. Conclusion

This paper studies the return continuation effect in a sample of six emerging Asian

stock markets for the period 1981-1994. A regionally diversified portfolio across

these six markets consisting of long positions on past winners and short positions on

10 The proportion of positive returns in January is 60 percent, which is high, compared to the 24 percent

found by Jegadeesh and Titman (1993) for the US sample.

11 Results for turnover-sorted portfolios and on the alternative return measures (proportion of positive

returns) are available upon request.

19

past losers yields an average positive return of 0.37 percent per month over a six-

month holding period. However, the returns on the zero cost portfolio of Winner-

Loser become insignificant when we examine the post-liberalization period (1989-

1994) and when the portfolio is controlled for size or turnover effects. Interestingly,

we find significant momentum profits when the zero-cost portfolio takes on large

positions on firms that are small or are heavily traded. While past return by itself does

not predict future return, the interaction of past trading volume and past returns seem

to be related to future returns, suggesting an informational role of volume.

The lack of unrestricted price momentum indicate that either price momentum is

not pervasive across all markets or that momentum may not be detectable (low signal-

to-noise ratio) in emerging markets unless price information is used jointly with other

firm characteristics like trading volume.

20

References

Assness, Clifford, John Liew and Ross Stevens, 1996, Parallels between the cross-

sectional predictability of stock returns and country returns, working paper,

Goldman Sachs Asset Management.

Barberis, Nicolas, Andrei Shleifer, and Robert Vishny, 1998, A model of investor

sentiment, Journal of Financial Economics 49, 307-343.

Bekaert, Geert, and Campbell R. Harvey (1997), Emerging equity market volatility,

Journal of Financial Economis 43, 29-77.

Bossaerts, P. and P. Hiliion, 1998, Implementing statistical criteria to select return

forecasting models: What do we learn?, Review of Financial Studies

(forthcoming).

Chan Kalok, A. Hameed, and W. Tong, 1998, Profitability of momentum strategies in

the international equity markets, Working Paper.

Chan, Louis K.C., N. Jegadeesh, and J. Lakonishok, 1996, Momentum strategies,

Journal of Finance 51, 1681-1713.

Conrad, J., and G. Kaul, 1998, An anatomy of trading strategies, Review of Financial

Studies 11, 489-519.

Cooper, Michael, Roberto Gutierrrez and William Marcum, 1999, Finding

predictability in stock returns without the benefit of hindsight, Working paper,

Purdue University.

Daniel, Kent, David Hirshleifer and Avanidhar Subrahmanyam, 1998, Investor

psychology and security market under- and over reactions, Journal of Finance 53,

1893-1885.

Fama, Eugene F., and Kenneth R. French, 1996, Multifactor explanations of asset

pricing anomalies, Journal of Finance 51, 55-84.

21

Fama, Eugene F., 1998, Market efficiency, long-term returns, and behavioral finance,

Journal of Financial Economics 49, 283-306.

Foster, Doug, Tom Smith and Robert Whaley, 1997, Assessing goodness-of-fit of

asset pricing models: The distribution of the maximal R2, Journal of Finance 52,

591-607.

Harvey, Campbell R., 1995, Predictable risk and return in emerging markets, Review

of Financial Studies

Hong, Harrison and Jeremy Stein, 1999, A unified theory of underreaction,

momentum trading and overreaction in asset markets, forthcoming in Journal of

Finance (December 1999).

Hong, Harrison, Terence Lim, and Jeremy Stein, 1999, Bad news travels slowly: size,

analyst coverage, and the profitability of momentum strategies, forthcoming in

Journal of Finance.

Jegadeesh, N. and S. Titman, 1993, Returns to buying winners and selling losers:

Implications for stock market efficiency, Journal of Finance 48, 65-91.

Lee, Charles and Bhaskaran Swaminathan, 1998, Price momentum and trading

volume, Working paper, Cornell University.

Lo, A. and Mac Kinlay, 1990, Data snooping biases in tests of financial asset pricing

models, Review of Financial Studies 3, 431-467.

Moskowitz, Tobias J. and M. Grindblatt, Do industries explain momentum,

forthcoming in Journal of Finance (August 1999).

Odean, Terence, 1998, Volume, volatility, price, profit when all traders are above

average, Journal of Finance 53, 1887-1934.

Pesaran, M and A. Timmermann, 1995, Predictability of stock returns: Robustness

and economic significance, Journal of Finance 50, 1201-1228.

22

Richards, Anthony J., 1996, Winner-loser reversals in national stock market indices:

Can they be explained?, Journal of Finance 52, 2129-2144.

Rouwenhorst, K. Geert, 1998, International momentum strategies, ,Journal of Finance

53, 267-284.

Rouwenhorst, K. Geert, 1999, Local return factors and turnover in emerging markets,

forthcoming in Journal of Finance (August 1999).

23

Table 1

Descriptive Statistics of Sample Countries

The table reports the descriptive statistics for each sample country. The statistics in Panel A include the number of firms in the sample, thesample period, the mean and standard deviation of local currency and USD return, the mean and median size, turnover and number of daystraded in a month. Size is measured as the natural logarithm of the market value of equity in US dollars. Turnover is measured as percentage ofthe number of shares traded in a month divided by the number of shares outstanding at the beginning of the month. The median value for size,turnover and number of days traded is reported in the parenthesis. Panel B presents the returns correlations between each sample countries

Panel ANumber Sample LC return USD return Si ze Turn over Days Traded

Country of firms period Mean Std Dev Mean Std Dev Mean Median Mean Median Mean Median Hong Kong 201 Jan 1980-Dec 1994 0.0232 0.1761 0.0213 0.1614 5.98 5.74 4.41 5.02 17.20 16.45 Malaysia 244 Jan 1979-Dec 1994 0.0249 0.1578 0.0191 0.1405 5.31 5.01 4.34 5.31 21.07 20.41 Singapore 102 Jan 1979-Dec 1994 0.0177 0.1245 0.0155 0.1146 5.43 5.82 2.52 3.11 17.28 16.72 South Korea 309 Jan 1979-Dec 1994 0.0210 0.1420 0.0182 0.0957 4.71 4.35 11.97 10.04 23.45 21.52 Taiwan 92 Jan 1979-Dec 1994 0.0248 0.1828 0.0225 0.1739 5.98 5.77 36.65 42.34 16.89 18.12 Thailand 59 Jan 1979-Dec 1994 0.0218 0.1620 0.0162 0.1196 4.82 5.24 7.86 7.26 17.74 16.84

24

Panel BHong Kong Malaysia Singapore South Korea Taiwan Thailand

Hong Kong 1.00Malaysia 0.37 1.00

Singapore 0.41 0.81 1.00South Korea 0.11 0.07 0.10 1.00

Taiwan 0.27 0.22 0.21 0.08 1.00Thailand 0.44 0.38 0.40 0.07 0.35 1.00

25

Table 2

Returns of Relative Strength Decile Portfolios in Asian Stock Markets

At the end of each month, all stocks from six emerging Asian markets are ranked inascending order based on their past J-months returns into ten relative strength decileportfolios. Those with the lowest past performance (bottom 10 percent) are assignedto the “Loser” portfolio, while the one with the highest past performance (top 10percent) are assigned to the “Winner” portfolio. These portfolios are equally weightedat formation and then held for K subsequent months. The table reports the meanmonthly returns on these portfolios from 1981 to 1994. The t-statistic is the meanreturn divided by its standard error.

Ranking Period Holding Period (K)(J) Portfolio 3 6 9 123 Winner 0.0231 0.0217 0.0234 0.0221

Loser 0.0216 0.0205 0.0186 0.0154Winner-Loser 0.0014 0.0013 0.0047 0.0067(t-statistic) (0.28) (0.29) (1.34) (1.75)

6 Winner 0.0229 0.0244 0.0243 0.0227Loser 0.0213 0.0191 0.0185 0.0147Winner-Loser 0.0016 0.0053 0.0058 0.0079(t-statistic) (0.27) (1.02) (1.31) (1.64)

9 Winner 0.0248 0.0249 0.0236 0.0228Loser 0.0178 0.0187 0.0189 0.0149Winner-Loser 0.0070 0.0062 0.0047 0.0079(t-statistic) (1.18) (1.18) (1.01) (1.44)

12 Winner 0.0249 0.0235 0.0223 0.0225Loser 0.0197 0.0204 0.0204 0.0165Winner-Loser 0.0052 0.0031 0.0019 0.0060(t-statistic) (0.88) (0.57) (0.38) (0.99)

26

Table 3

Descriptive Statistics for Returns of Decile Portfolios

At the end of each month, all stocks are ranked in ascending order based on their pastsix-months returns. Those with the lowest past performance are assigned to the“Loser” portfolio, while the one with the highest past performance are assigned to the“Winner” portfolio. These portfolios are equally weighted at formation and then heldfor six subsequent months. The table reports the mean monthly buy-and-hold returnsand standard deviation of the ten decile portfolios from 1981 to 1994. The t-statisticis the mean return divided by its standard error. The average size is calculated as theaverage natural logarithm of the market value of equity of the stocks in the portfolio,in US Dollars. The F-statistic tests for equality of the average returns of the tenrelative strength decile portfolios.

Prior return decile MeanReturn

MedianReturn

StandardDeviation

AverageSize

Loser 0.0191 0.0117 0.0700 4.612 0.0176 0.0113 0.0529 4.883 0.0169 0.0113 0.0478 4.964 0.0166 0.0126 0.0424 5.155 0.0183 0.0150 0.0449 5.226 0.0194 0.0178 0.0443 5.417 0.0202 0.0201 0.0471 5.198 0.0207 0.0209 0.0496 5.149 0.0225 0.0216 0.0560 5.11

Winner 0.0244 0.0269 0.0670 5.02

Winner-Loser 0.0053 0.0693(t-statistic) (1.02)

27

Table 4

Returns of Country-Neutral Relative Strength Portfolios

At the end of each month, all stocks are ranked in ascending order based on their pastsix-months returns, relative to other stocks in the same country. Those with lowestpast performance are assigned to the “Loser” portfolio, while the one with the highestpast performance are assigned to the “Winner” portfolio. These portfolios are equallyweighted at formation and then held for six subsequent months. The monthly averagereturn and standard deviation of the zero-cost (Winner-Loser) internationallydiversified relative strength portfolios are for the sample period 1981-1994. The t-statistic is the mean return divided by its standard error.

Portfolio Mean Std Dev t-statisticAll stocks (country-neutral) 0.0037 0.0216 2.30By country: Hong Kong 0.0021 0.0412 0.65 Malaysia 0.0019 0.0443 0.58 Singapore 0.0051 0.0458 1.50 South Korea 0.0041 0.0482 1.15 Taiwan 0.0061 0.0750 1.09 Thailand 0.0022 0.0460 0.72

28

Table 5

Returns on Size-Based Relative Strength Decile Portfolios

At the end of each month, all stocks are ranked in ascending orders based on their pastsix-months returns. Those with lowest past return performance are assigned to P1,while the stocks with the next past-return performance deciles P2 and so on. Theseportfolios are equally weighted at formation and then held for 6 subsequent months.The table reports the monthly average return of the ten decile portfolios as well as thezero-cost (P10-P1) portfolio for the period 1981-1994. The table also reports themonthly average return of the portfolios for the three size-based subsamples. S1indicates the subsample for the smallest 30% of the stocks, S2 indicates the subsamplefor the medium 40% of the stocks and S3 indicates the subsample for the largest 30%of all the stocks. The t-statistic is denoted in the parentheses and is calculated as themean return divided by its standard error.

All S1 S2 S3P1 0.0191 0.0071 0.0179 0.0174

(3.66) (1.28) (3.11) (2.66)P2 0.0176 0.0123 0.0163 0.0158

(4.47) (3.15) (4.34) (3.53)P3 0.0169 0.0127 0.0161 0.0150

(4.75) (3.43) (4.31) (3.64)P4 0.0166 0.0108 0.0178 0.0176

(5.25) (3.37) (5.12) (4.47)P5 0.0183 0.0190 0.0201 0.0198

(5.48) (3.33) (4.15) (4.59)P6 0.0194 0.0142 0.0188 0.0225

(5.86) (4.12) (4.78) (3.77)P7 0.0202 0.0161 0.0210 0.0200

(5.74) (3.86) (4.19) (4.48)P8 0.0207 0.0215 0.0192 0.0230

(5.61) (3.51) (4.82) (4.90)P9 0.0225 0.0216 0.0186 0.0243

(5.39) (4.56) (4.42) (4.82)P10 0.0244 0.0192 0.0222 0.0242

(4.88) (4.06) (4.13) (4.21)P10-P1 0.0053 0.0121 0.0043 0.0068

(1.02) (2.48) (0.070) (1.07)

29

Table 6

Returns of Country-Size-Neutral Relative Strength Portfolios

At the end of each month, all stocks are ranked in ascending order based on their pastsix-months returns, relative to other stocks in the same size-country group. Those withlowest past performance are assigned to the “Loser” portfolio, while the one with thehighest past performance are assigned to the “Winner” portfolio. These portfolios areequally weighted at formation and then held for six subsequent months. The monthlyaverage return and standard deviation of the zero-cost (Winner-Loser) internationallydiversified relative strength portfolios are for the sample period 1981-1994. Thestocks in each country are assigned into size groups relative to other stocks in thesame country. Small corresponds to the bottom 30%, medium corresponds to themiddle 40% and large corresponds to the largest 30%. The t-statistic is the meanreturn divided by its standard error.

Portfolio Mean Std Dev t-statisticAll-stocks (size-country-neutral) 0.0019 0.0170 1.53

Size-neutral country portfolios: Hong Kong 0.0011 0.0537 0.26 Malaysia 0.0006 0.0311 0.25 Singapore -0.0012 0.0356 -0.45 South Korea 0.0014 0.0236 0.80 Taiwan 0.0084 0.0515 2.19 Thailand 0.0010 0.0438 0.76

Country-neutral size portfolios: Small 0.0046 0.0326 1.89 Medium 0.0015 0.0217 0.95 Large -0.0003 0.0239 -0.19

30

Table 7

Returns of Turnover-Neutral and Country-Turnover-Neutral Relative StrengthPortfolios

At the end of each month, all stocks are ranked in ascending order based on their pastsix-months returns, relative to turnover group (Panel A) and turnover-country group(Panel B). Small corresponds to the bottom 30%, medium corresponds to the middle40% and large corresponds to the largest 30%. Those with lowest past performanceare assigned to the “Loser” portfolio, while the one with the highest past performanceare assigned to the “Winner” portfolio. These portfolios are equally weighted atformation and then held for six subsequent months. Each panel reports the monthlyaverage return and standard deviation of the zero-cost (Winner-Loser) internationallydiversified relative strength portfolios for the sample period 1981-1994. The t-statisticis the mean return divided by its standard error.

Portfolio Mean Std Dev t-statistic Panel A: Turnover-Neutral Momentum StrategiesAll-stocks (turnover-neutral) 0.0050 0.0514 1.23

By turnover-group: Smallest 0.0052 0.0505 1.28 Medium -0.0012 0.0570 -0.27 Largest 0.0112 0.0660 2.12 Panel B: Turnover-Country-Neutral Momentum StrategiesAll-stocks (turnover-country-neutral) 0.0011 0.0181 0.82

Turnover-neutral country portfolios: Hong Kong 0.0018 0.0647 0.35 Malaysia 0.0056 0.0221 3.38 Singapore 0.0008 0.0291 0.39 South Korea 0.0026 0.0200 1.78 Taiwan 0.0018 0.0457 0.53 Thailand -0.0047 0.0561 -1.13

Country-neutral turnover portfolios: Small 0.0006 0.0294 0.28 Medium 0.0004 0.0195 0.29 Large 0.0029 0.0316 1.25

31

Table 8

Returns on Size-Based Relative Strength Portfolios by Calendar Months

At the end of each month, all stocks are ranked in ascending orders based on their pastsix-months returns. Those with lowest past performance are assigned to the “Loser”portfolio, while the one with the highest past performance are assigned to the“Winner” portfolio. These portfolios are equally weighted at formation and then heldfor six subsequent months. The table reports the monthly average return of the zero-cost (Winner-Loser) portfolio in each calendar month for the period 1981-1994. Thetable also reports the monthly average return of the zero-cost portfolios for the threesize-based subsamples. S1 indicates the subsample for the smallest 30% of thestocks, S2 indicates the subsample for the medium 40% of the stocks and S3 indicatesthe subsample for the largest 30% of all the stocks. The t-statistic is denoted in theparentheses and is calculated as the mean return divided by its standard error. The F-statistic tests the hypothesis that the returns on zero-cost portfolios are jointly equal inall calendar months

All S1 S2 S3JAN 0.0025 -0.0054 0.0121 0.0106

(0.15) (-0.26) (0.64) (0.64)FEB 0.0137 0.0162 0.0120 0.0305

(0.72) (1.01) (0.47) (1.23)MAR -0.0062 -0.0057 -0.0181 -0.0266

(-0.33) (-0.35) (-0.95) (-1.71)APR 0.0345 0.0231 0.0126 0.0268

(2.27) (1.63) (0.76) (1.84)MAY 0.0143 0.0256 0.0149 0.0172

(0.82) (2.05) (0.78) (1.00)JUNE 0.0124 0.0025 0.0137 -0.0016

(0.59) (0.26) (0.97) (-0.10)JULY -0.0070 0.0071 0.0007 -0.0051

(-0.56) (0.44) (0.07) (-0.36)AUG -0.0132 0.0013 0.0060 0.0178

(-0.59) (0.07) (0.30) (-0.68)SEP 0.0047 0.0156 0.0135 0.0088

(0.34) (1.10) (0.67) (0.40)OCT -0.0040 -0.0053 -0.0191 -0.0265

(-0.23) (-0.30) (-0.90) (-1.11)NOV -0.0106 0.0309 -0.0104 0.0035

(-0.44) (1.12) (-0.29) (0.09)DEC 0.0220 0.0417 0.0123 0.0291

(1.48) (2.95) (0.41) (1.27)FEBDEC 0.0055 0.0123 0.0042 0.0070

(1.15) (2.31) (0.77) (1.09)F-statistic 0.64 0.85 0.35 0.76p-value (0.79) (0.59) (0.97) (0.68)