momentum - senate group presentation

TRANSCRIPT

1 Momentum Trust

Business interests & Estate Administration

A selection of “war stories” to illustrate the importance of financial planning for businesses

Jeffrey Wiseman 5 November 2015

2

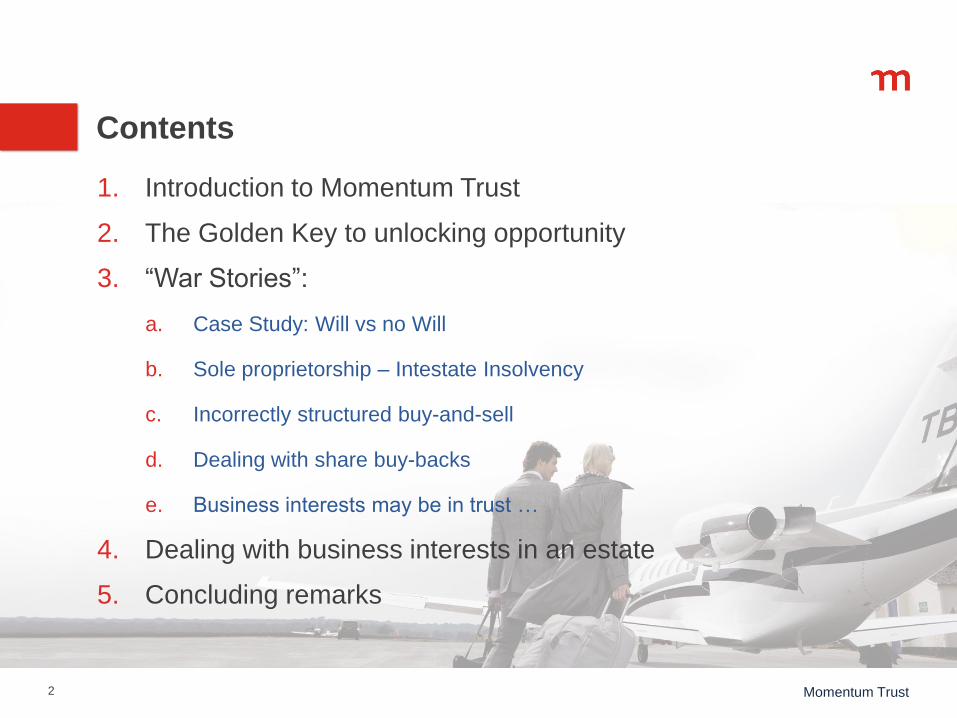

Contents

Momentum Trust

1. Introduction to Momentum Trust

2. The Golden Key to unlocking opportunity

3. “War Stories”:

a. Case Study: Will vs no Will

b. Sole proprietorship – Intestate Insolvency

c. Incorrectly structured buy-and-sell

d. Dealing with share buy-backs

e. Business interests may be in trust …

4. Dealing with business interests in an estate

5. Concluding remarks

3 Momentum Trust

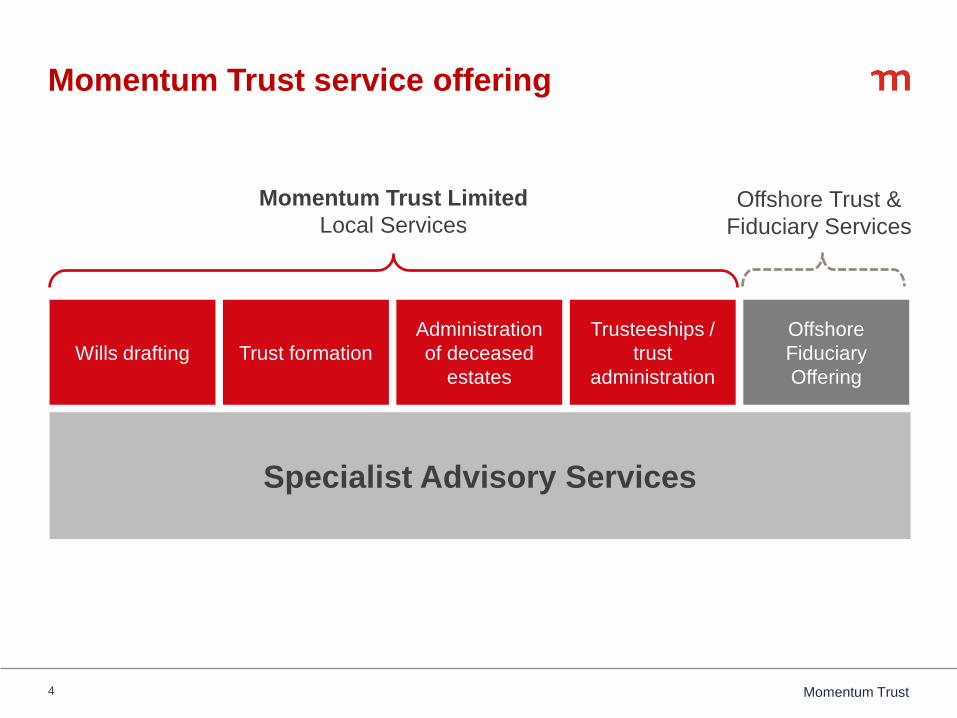

Momentum Trust service offering

4 Momentum Trust

Momentum Trust service offering

Specialist Advisory Services

Wills drafting Trust formation

Administration

of deceased

estates

Trusteeships /

trust

administration

Offshore

Fiduciary

Offering

Momentum Trust Limited

Local Services Offshore Trust &

Fiduciary Services

5 Momentum Trust

The Golden Key to unlocking Opportunity

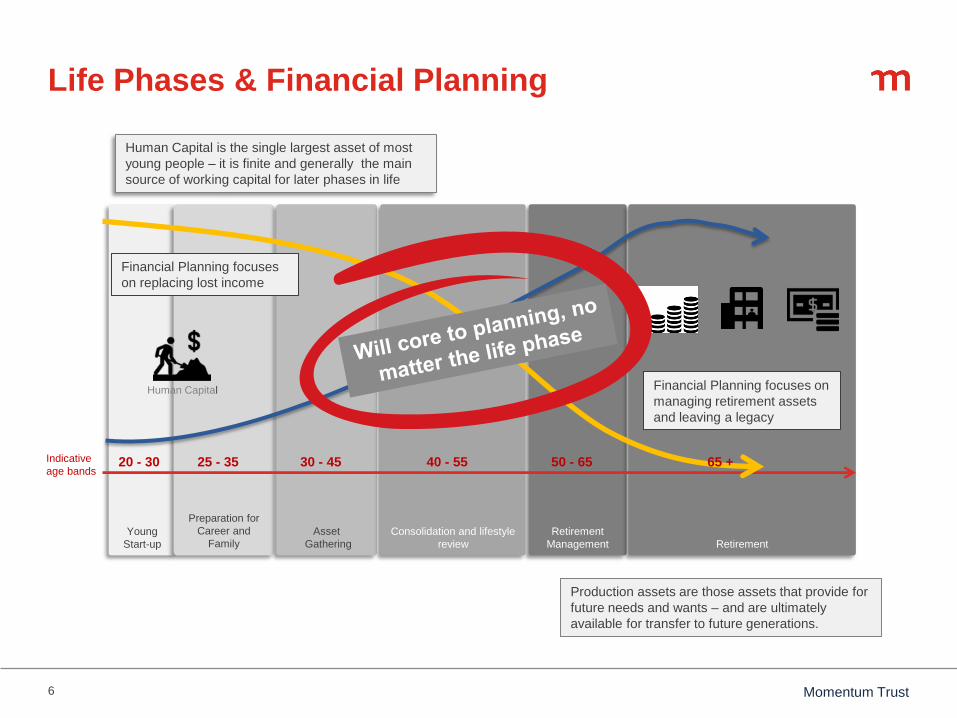

6 Momentum Trust

Retirement

Management

Life Phases & Financial Planning

Young

Start-up

Preparation for

Career and

Family Asset

Gathering

Consolidation and lifestyle

review Retirement

20 - 30 40 - 55 30 - 45 25 - 35 50 - 65 Indicative

age bands

Human Capital is the single largest asset of most

young people – it is finite and generally the main

source of working capital for later phases in life

65 +

Human Capital

Production assets are those assets that provide for

future needs and wants – and are ultimately

available for transfer to future generations.

Financial Planning focuses

on replacing lost income

Financial Planning focuses on

managing retirement assets

and leaving a legacy

7 Momentum Trust

Understanding your client’s wishes most important

8 Momentum Trust

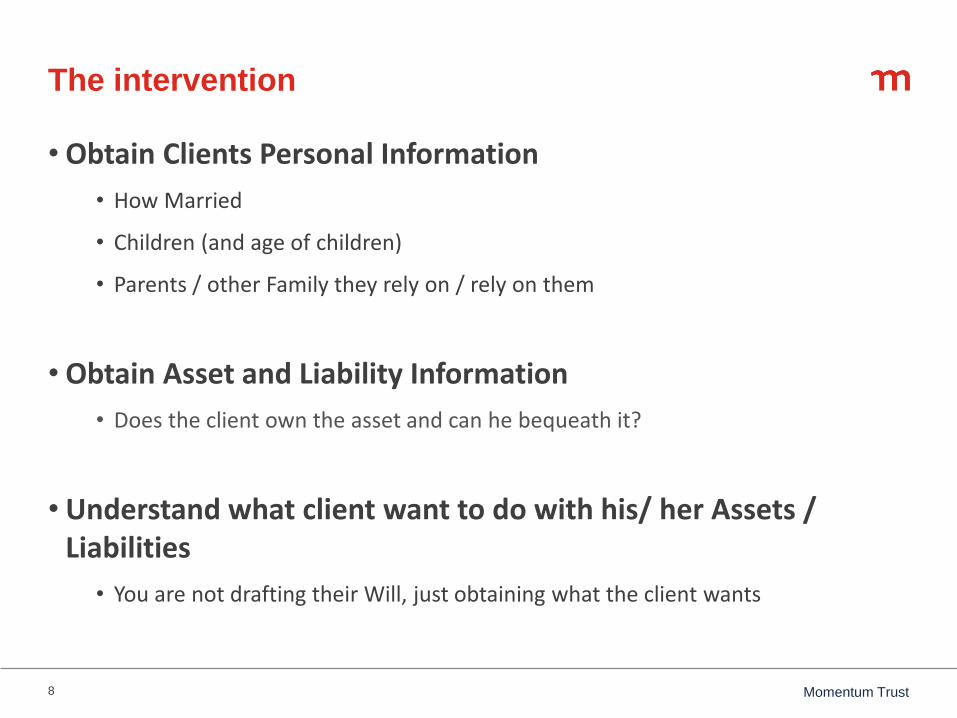

The intervention

• Obtain Clients Personal Information

• How Married

• Children (and age of children)

• Parents / other Family they rely on / rely on them

• Obtain Asset and Liability Information

• Does the client own the asset and can he bequeath it?

• Understand what client want to do with his/ her Assets / Liabilities

• You are not drafting their Will, just obtaining what the client wants

9 Momentum Trust

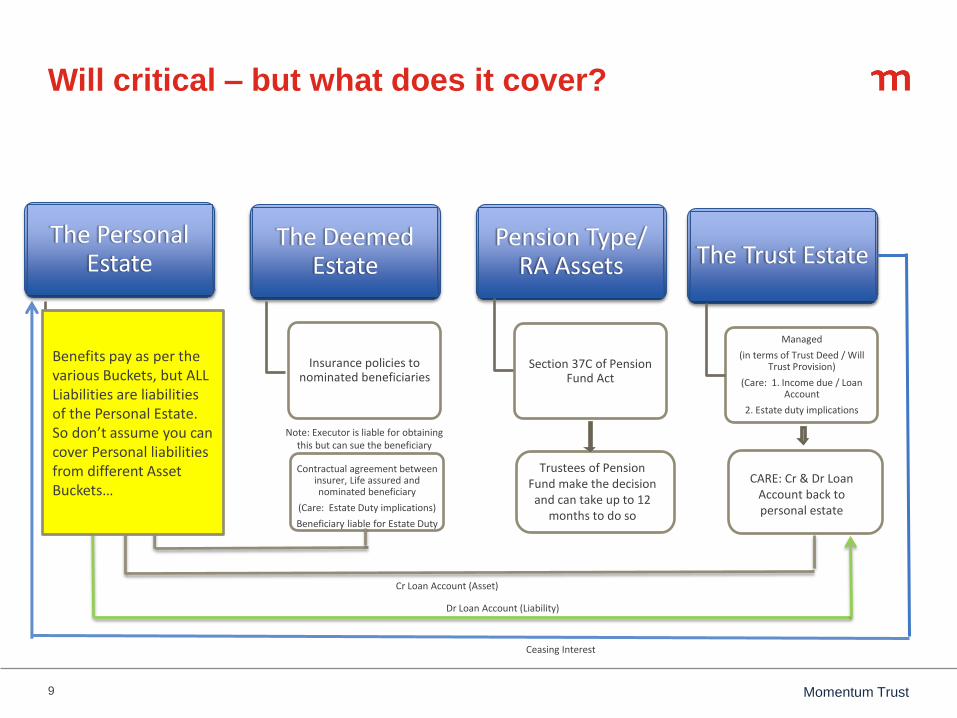

The Personal Estate

- House

- Business interests

- Vehicles etc.

- Bank accounts

- Investments

(local and offshore)

Disposed of under Will

CARE: Marital & Maintenance Claims

The Deemed Estate

Insurance policies to nominated beneficiaries

Contractual agreement between insurer, Life assured and nominated beneficiary

(Care: Estate Duty implications)

Beneficiary liable for Estate Duty

Note: Executor is liable for obtaining this but can sue the beneficiary

Pension Type/ RA Assets

Section 37C of Pension Fund Act

Trustees of Pension Fund make the decision and can take up to 12

months to do so

The Trust Estate

Managed

(in terms of Trust Deed / Will Trust Provision)

(Care: 1. Income due / Loan Account

2. Estate duty implications

CARE: Cr & Dr Loan Account back to personal estate

Cr Loan Account (Asset)

Ceasing Interest

Dr Loan Account (Liability)

Benefits pay as per the various Buckets, but ALL Liabilities are liabilities of the Personal Estate. So don’t assume you can cover Personal liabilities from different Asset Buckets…

Will critical – but what does it cover?

10 Momentum Trust

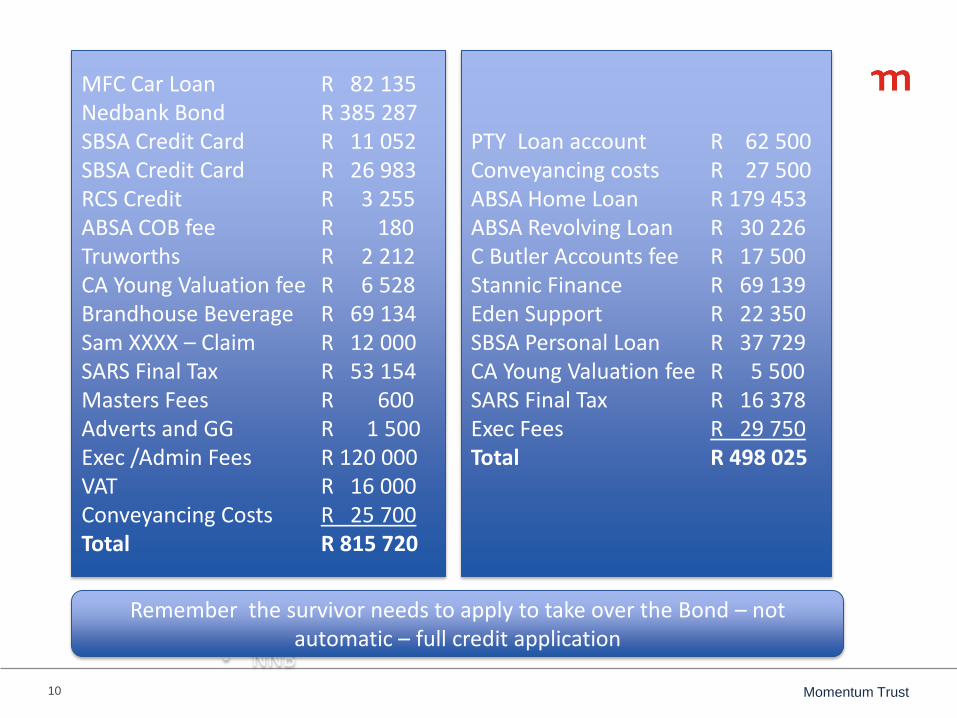

MFC Car Loan R 82 135 Nedbank Bond R 385 287 SBSA Credit Card R 11 052 SBSA Credit Card R 26 983 RCS Credit R 3 255 ABSA COB fee R 180 Truworths R 2 212 CA Young Valuation fee R 6 528 Brandhouse Beverage R 69 134 Sam XXXX – Claim R 12 000 SARS Final Tax R 53 154 Masters Fees R 600 Adverts and GG R 1 500 Exec /Admin Fees R 120 000 VAT R 16 000 Conveyancing Costs R 25 700 Total R 815 720

• NNB

PTY Loan account R 62 500 Conveyancing costs R 27 500 ABSA Home Loan R 179 453 ABSA Revolving Loan R 30 226 C Butler Accounts fee R 17 500 Stannic Finance R 69 139 Eden Support R 22 350 SBSA Personal Loan R 37 729 CA Young Valuation fee R 5 500 SARS Final Tax R 16 378 Exec Fees R 29 750 Total R 498 025

Remember the survivor needs to apply to take over the Bond – not automatic – full credit application

11 Momentum Trust

The cash shortfall

• Single most frustrating element of an Executors work.

• Often policies are paid outside the estate but the people receiving the benefits simply won’t pay into the estate (for a number of reasons).

• Cash Shortfalls probably account for 70% of delays in estate administration.

Comments: General costs to be settled;

- Final medical accounts;

- Bank overdrafts / credit card without credit life insurance;

- Bonds on houses the spouse can’t afford to take-over (if not settled by life cover);

- Property transfer costs;

- Costs to obtain rates clearance certificate (4 months paid in advance);

- Masters Fees and 2 x newspaper and Government gazette adverts;

- Executors remuneration (see notes and slide on Executors Fees).

12 Momentum Trust

Liquidity issues to address …

The Cash Shortfall: • Review all Polices to see that they do what they are meant to do!

o Funeral Cover o Credit Life o Policies payable to the estate o Deemed Policies

To Spouse – Care: Insolvency and in community of property Buy and Sell – Care Key Man – Care Share Buy Back – Care Contingent Liability - Care Policy paid to Non Resident Family member – Care Additional Estate duty derived from above

• Short term Insurance & Medical Aid • Investment performance of Assets to Financial Plan • Wider Family links

13 Momentum Trust

“9 to 12 months in a perfect world” NOTE: 1. The process is sequential – each step needs to be concluded before the next step can start (of course we do prepare and process

simultaneously what we can) 2. Applies to all Estates 3. Like the 6 step financial planning process

Cancel bond of security.

The Estate Administration Process

14 Momentum Trust

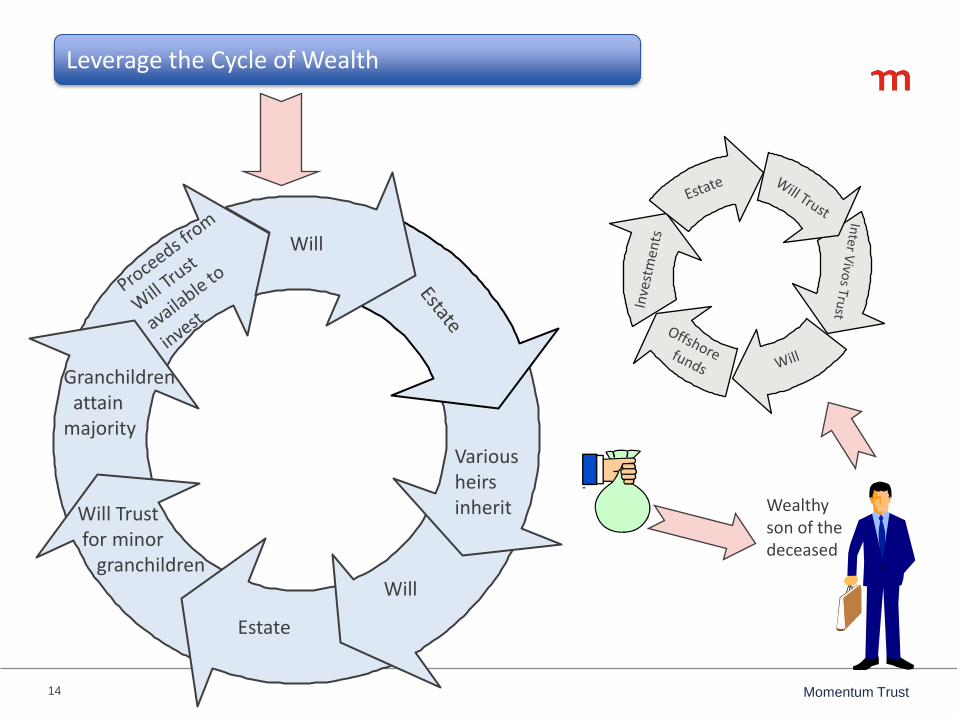

Leverage the Cycle of Wealth

Will

Various heirs inherit

Will

Estate

Will Trust for minor granchildren

Granchildren attain majority

Wealthy son of the deceased

15 Momentum Trust

Case Study: Will vs No Will

16 Momentum Trust

Freedom of Testation: fact or fiction

• BUT:

- Married ICOP (only your half-share);

- Married OCOP ANC with accrual – accrual claim;

- You are married ANC and leave nothing to spouse - maintenance claim in terms of Maintenance of surviving Spouses Act;

- Care: Competing Maintenance claims from spouse/ minor children;

- Section 37 C of the Pension Fund Act – Board of Trustees make decision;

- There is a Buy and Sell Agreement in place over the business;

- You only have a limited interest in the property / investments;

- Section 38 take-over;

- Redistribution agreement between Heirs : may result in specific assets accruing differently to the Will, in lieu of cash or assets.

“You can bequeath whatever you want to whomever you wish” ... as long as not “Contra Bonos Mores”

17 Momentum Trust

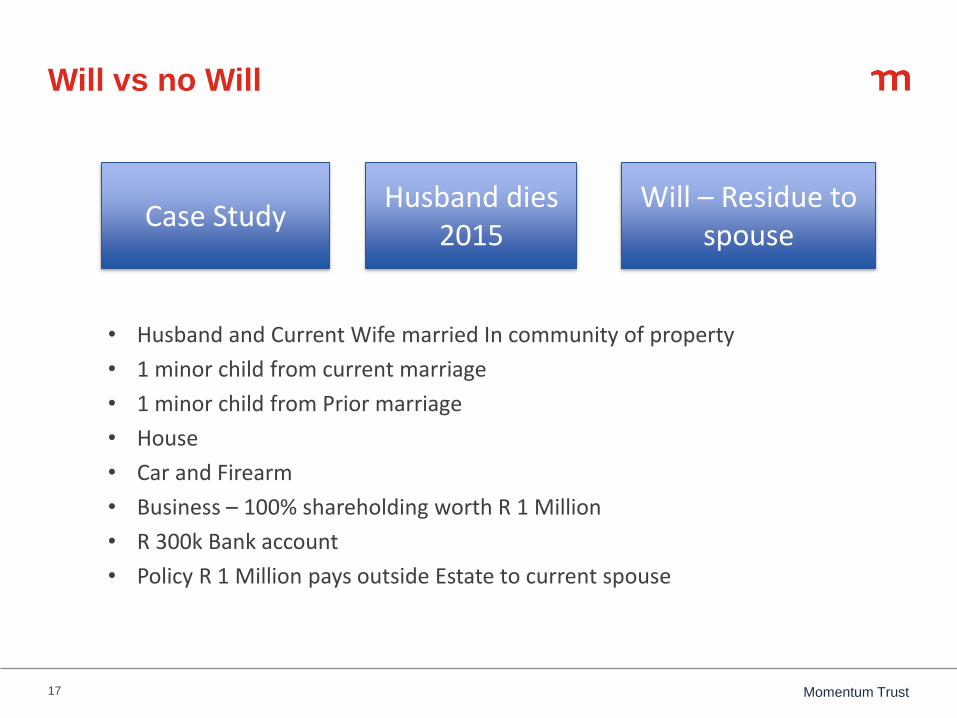

Will vs no Will

• Husband and Current Wife married In community of property

• 1 minor child from current marriage

• 1 minor child from Prior marriage

• House

• Car and Firearm

• Business – 100% shareholding worth R 1 Million

• R 300k Bank account

• Policy R 1 Million pays outside Estate to current spouse

Case Study Husband dies

2015 Will – Residue to

spouse

18 Momentum Trust

Will – Residue to spouse

• House – spouse inherits

• Car and Firearm – spouse inherits

• Business – Spouse inherits

• R 300k (Less costs) – spouse inherits

• Policy to nominated Beneficiary – spouse Inherits

No concerns other than probable Maintenance Claim in respect of the minor child

19 Momentum Trust

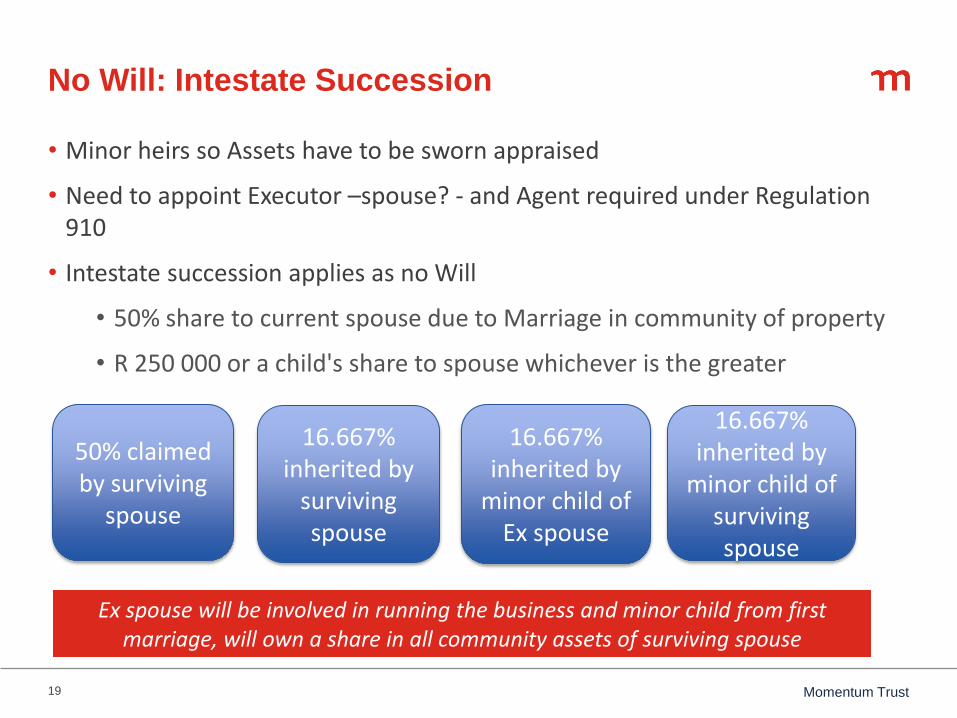

No Will: Intestate Succession

• Minor heirs so Assets have to be sworn appraised

• Need to appoint Executor –spouse? - and Agent required under Regulation 910

• Intestate succession applies as no Will

• 50% share to current spouse due to Marriage in community of property

• R 250 000 or a child's share to spouse whichever is the greater

16.667%

inherited by surviving spouse

50% claimed by surviving

spouse

16.667% inherited by

minor child of Ex spouse

16.667% inherited by

minor child of surviving spouse

Ex spouse will be involved in running the business and minor child from first marriage, will own a share in all community assets of surviving spouse

20 Momentum Trust

“War Story”: Intestate Insolvency

21 Momentum Trust

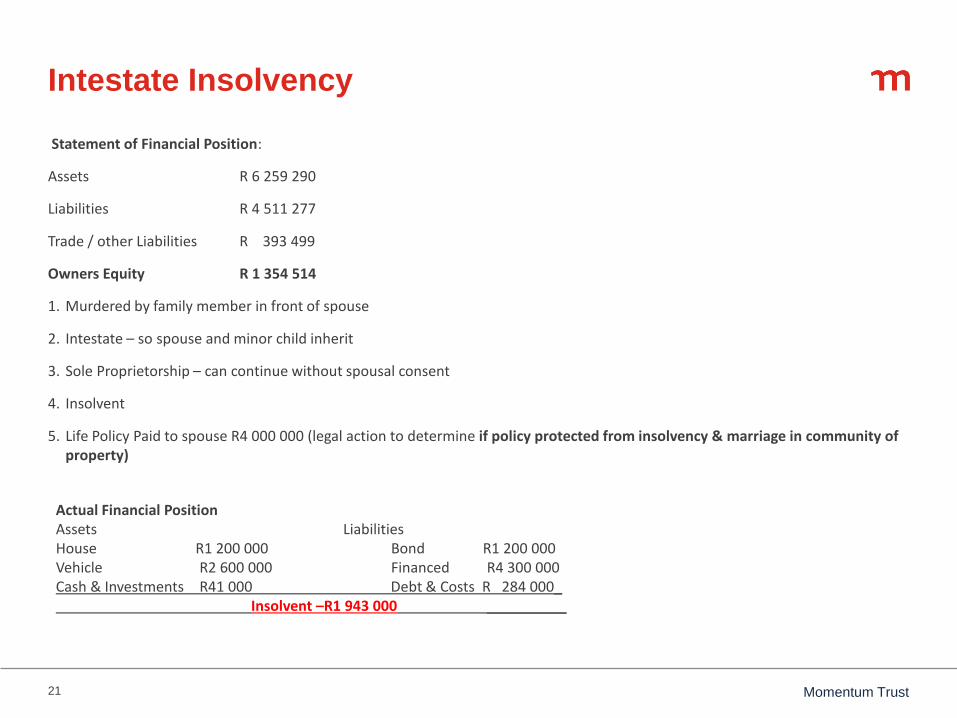

Intestate Insolvency

Statement of Financial Position:

Assets R 6 259 290

Liabilities R 4 511 277

Trade / other Liabilities R 393 499

Owners Equity R 1 354 514

1. Murdered by family member in front of spouse

2. Intestate – so spouse and minor child inherit

3. Sole Proprietorship – can continue without spousal consent

4. Insolvent

5. Life Policy Paid to spouse R4 000 000 (legal action to determine if policy protected from insolvency & marriage in community of property)

Actual Financial Position Assets Liabilities House R1 200 000 Bond R1 200 000 Vehicle R2 600 000 Financed R4 300 000 Cash & Investments R41 000 Debt & Costs R 284 000_ Insolvent –R1 943 000 __________

22 Momentum Trust

“War Stories”: Incorrectly structured buy-and-sell

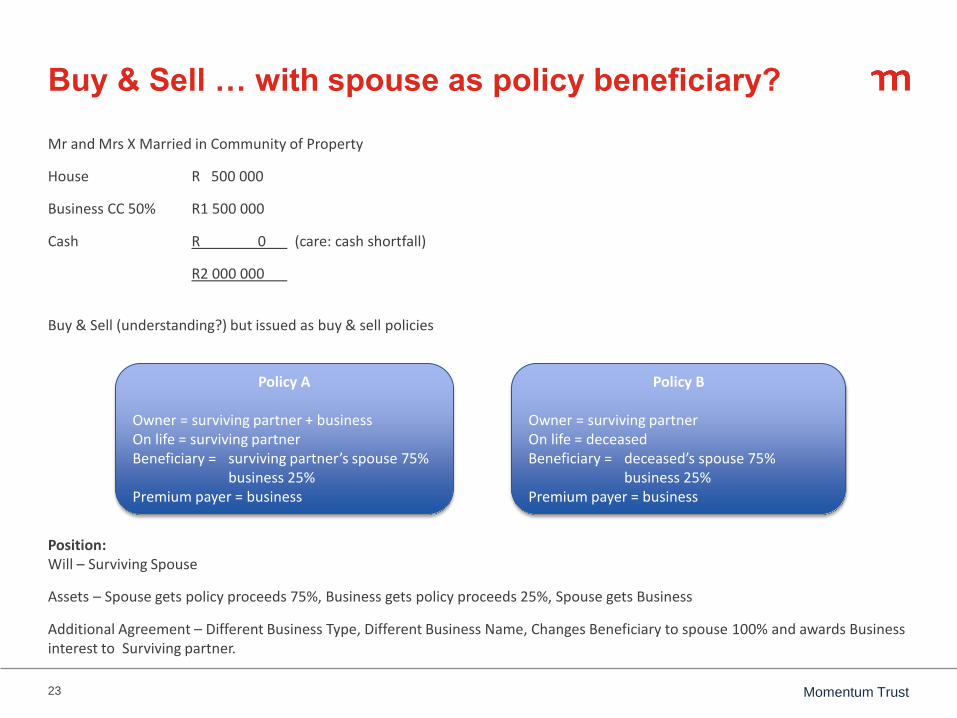

23 Momentum Trust

Buy & Sell … with spouse as policy beneficiary?

Mr and Mrs X Married in Community of Property

House R 500 000

Business CC 50% R1 500 000

Cash R 0 (care: cash shortfall)

R2 000 000

Buy & Sell (understanding?) but issued as buy & sell policies

Position: Will – Surviving Spouse

Assets – Spouse gets policy proceeds 75%, Business gets policy proceeds 25%, Spouse gets Business

Additional Agreement – Different Business Type, Different Business Name, Changes Beneficiary to spouse 100% and awards Business interest to Surviving partner.

Policy B

Owner = surviving partner On life = deceased Beneficiary = deceased’s spouse 75% business 25% Premium payer = business

Policy A

Owner = surviving partner + business On life = surviving partner Beneficiary = surviving partner’s spouse 75% business 25% Premium payer = business

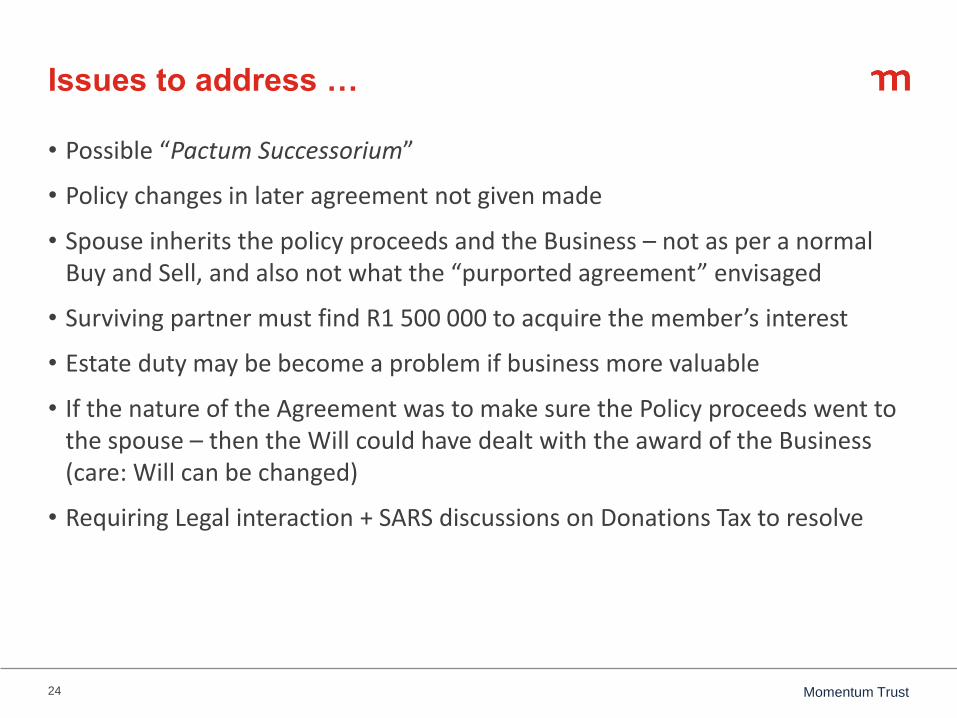

24 Momentum Trust

Issues to address …

• Possible “Pactum Successorium”

• Policy changes in later agreement not given made

• Spouse inherits the policy proceeds and the Business – not as per a normal Buy and Sell, and also not what the “purported agreement” envisaged

• Surviving partner must find R1 500 000 to acquire the member’s interest

• Estate duty may be become a problem if business more valuable

• If the nature of the Agreement was to make sure the Policy proceeds went to the spouse – then the Will could have dealt with the award of the Business (care: Will can be changed)

• Requiring Legal interaction + SARS discussions on Donations Tax to resolve

25 Momentum Trust

“War Stories”: Dealing with share buy-backs

26 Momentum Trust

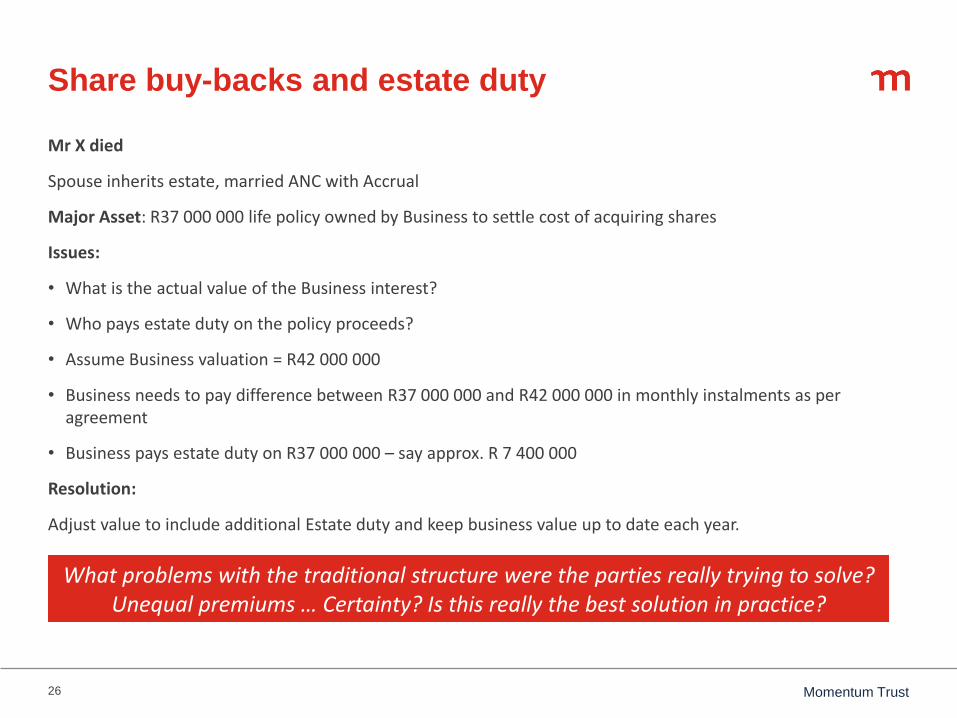

Share buy-backs and estate duty

Mr X died

Spouse inherits estate, married ANC with Accrual

Major Asset: R37 000 000 life policy owned by Business to settle cost of acquiring shares

Issues:

• What is the actual value of the Business interest?

• Who pays estate duty on the policy proceeds?

• Assume Business valuation = R42 000 000

• Business needs to pay difference between R37 000 000 and R42 000 000 in monthly instalments as per agreement

• Business pays estate duty on R37 000 000 – say approx. R 7 400 000

Resolution:

Adjust value to include additional Estate duty and keep business value up to date each year.

What problems with the traditional structure were the parties really trying to solve?

Unequal premiums … Certainty? Is this really the best solution in practice?

27 Momentum Trust

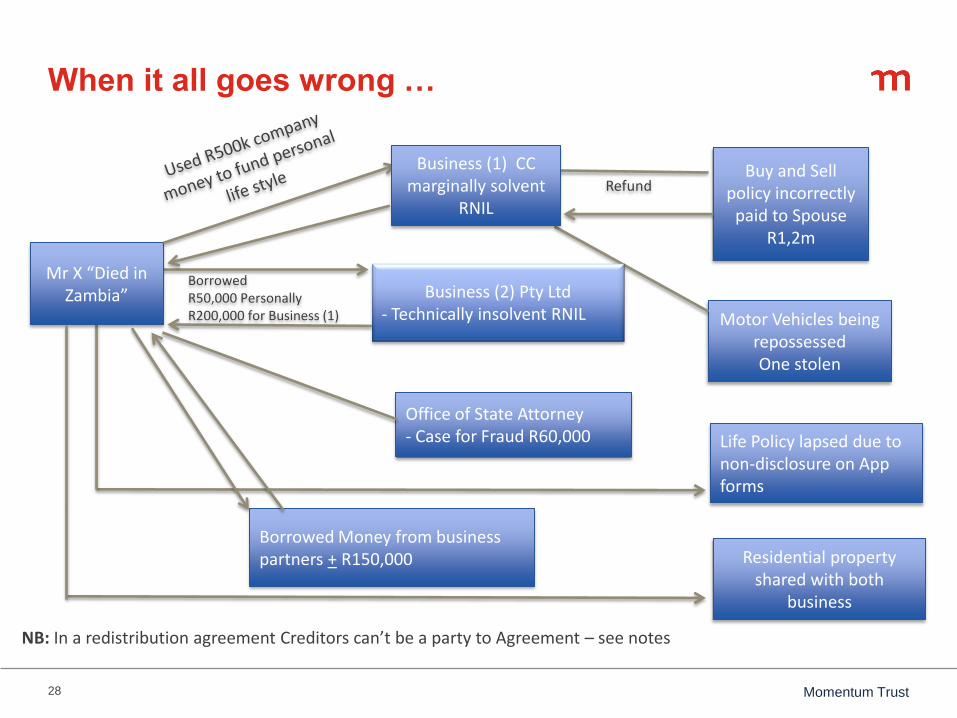

“War Stories”: Make sure you know your client!

28 Momentum Trust

Buy and Sell policy incorrectly

paid to Spouse R1,2m

Refund

Motor Vehicles being repossessed One stolen

Borrowed R50,000 Personally R200,000 for Business (1)

Business (2) Pty Ltd - Technically insolvent RNIL

Office of State Attorney - Case for Fraud R60,000

Borrowed Money from business partners + R150,000

Life Policy lapsed due to non-disclosure on App forms

Mr X “Died in Zambia”

Business (1) CC marginally solvent

RNIL

NB: In a redistribution agreement Creditors can’t be a party to Agreement – see notes

Residential property shared with both

business

When it all goes wrong …

29 Momentum Trust

“War Story”: Business interests may be in Trust …

30 Momentum Trust

The xxxx Family Trust

Engineering Business R28m Div 50% Share

Funded Spouses Assets - 5 houses + R10m “School Teacher”

Personal SA Estate - 2 x Bank A/C - 2 x Trailers

(R9,8M Loan) Declare post death dividend R10,25m

Offshore Assets

13 Properties + R25m

(including Hotel)

Estate + R4m Pension + R2m Life

Pension/Deemed

HSBC & Isle of Man SBSA R4m

- 2 x Bank accounts - 2 x Trailers = + R200k

The simple may become complicated …

31 Momentum Trust

Dealing with business interests in an estate

32 Momentum Trust

Dealing with business interests in an estate

• Financial planning the key to success:

• Often the difference between an estate that is easily administered and one that

is not

• The value of the business without the key individual

• The effect of suretyships on the estate

• Understand the reality of third parties becoming involved

• Know your client and about his affairs!

• An executor steps into the shoes of the deceased:

• Vehicle rental business

• Tenderpreneur in the construction industry

• Farmer with rare game

• Licences – Pharmacy, medical practice, etc.

33 Momentum Trust

Dealing with business interests in an estate

• Management agreements

• Banking relationships (insurance, risk of loss, etc.)

• Dealing with contractors

• Family often values the money generated by the business than the

business itself

• Trustees don’t want to run businesses!

• Suretyships often misunderstood and can be devastating to an estate:

• Residue

• Time delays

34 Momentum Trust

Concluding remarks

35 Momentum Trust

Concluding remarks

1. Never underestimate the importance of proper financial planning in

making sure that your client’s will is executable and easy to

administer

2. Encourage clients to consider their business running without them

and to make sure that appropriate arrangements are in place

3. The choice of executor, particularly where clients have business

interests is critical – decisions often have to be made at the level that

the deceased would have made them and a failure in this regard can

be very expensive

36 Momentum Trust

Thank you

Questions?

37 Momentum Trust

Disclaimer

Please note that the content of this presentation and the presentation itself does not constitute advice of any nature whatsoever and

should not be construed as such. It is always recommended that proper professional consultation should be sought, taking into

account your unique personal situation, to enable you to optimally use your trust. Please contact Momentum Fiduciary Services and

professional advice in this regard can be provided to you by us.