module 8: private mortgage insurance unit 1: what is pmi ... · understand basic pmi underwriting...

TRANSCRIPT

Module 8: Private Mortgage Insurance

Unit 1: What is PMI? Basics and Qualification

MOD8-1_1PMI.CFM (5 MIN)

UNIT 1 LEARNING OBJECTIVES

In this unit, you’ll learn to:

identify the uses and function of private mortgage insurance (PMI);

understand basic PMI underwriting standards;

understand the current interplay between PMI underwriting and Fannie Mae / Freddie Mac standards;

and

determine the required PMI requirements based on Fannie Mae / Freddie Mac guidelines.

PMI COVERAGE, AND BPMI VS. PMI

Mortgage insurance is insurance, including any mortgage guaranty insurance, against the nonpayment of, or

default in, an individual mortgage or loan involved in a residential mortgage transaction. Private mortgage

insurance (PMI) means mortgage insurance other than mortgage insurance made available under the National

Housing Act (i.e., mortgage insurance on Federal Housing Administration-insured loans) or Title V of the

Housing Act of 1949 (i.e., mortgage insurance on U.S. Department of Agriculture loans to farmers). [12 United

States Code §4901(8), (13)]

PMI indemnifies a lender for financial loss on a conventional loan secured by an interest in real estate when a

borrower defaults.

The lender’s recoverable losses include principal on the debt, any deficiency in the value of the secured

property and foreclosure costs. Recoverable losses do not include losses due to flood, earthquake or fire

damage, which are separately insurable.

Also, PMI is not mortgage life insurance, it is default insurance. Mortgage life insurance pays off the insured

loan in the event a borrower dies, becomes disabled or loses their health or income.

Private mortgage insurers, while comparable, are unrelated to government-created insurance agencies, such

as the Federal Housing Administration (FHA) and the U.S. Department of Veterans Affairs (VA), which also

insure or guarantee loans made to qualified borrowers. Loans insured by the FHA or guaranteed by the VA

have their own guidelines and are not subject to laws controlling PMI.

The borrower usually pays the PMI premiums, not the lender, although the lender is the insured and holder of

the policy. This type of PMI is called borrower-paid PMI (BPMI).

Premium rates are set as a percentage of the loan balance, are calculated in the same manner as interest, and

are paid monthly by the borrower with the principal and interest payments.

Some lenders and PMI carriers offer lender-paid mortgage insurance (LPMI) programs. If issued by the PMI

carrier, the lender will pay the PMI premium (in a lump sum or on a monthly basis) and in turn charge the

borrower a higher interest rate on their principal payments.

A lender that offers LPMI must make an LPMI-specific disclosure prior to approval of a borrower’s loan

application.

This disclosure must include:

a statement that LPMI cannot be cancelled, while BPMI may be cancelled or automatically terminated;

a statement that LPMI usually results in a higher interest rate on the loan;

a statement that LPMI terminates only upon a refinance or payoff of the loan;

a ten-year generic analysis of the costs and benefits of both BPMI and LPMI; and

a statement that LPMI may be federally tax deductible. [12 USC §4905(c)(1)]

Editor’s note — The discussion of PMI which follows assumes BPMI, unless otherwise noted.

Comprehension check

You must answer this question before you may proceed to the next page.

___________ are covered by private mortgage insurance.

VA-guaranteed loans

FHA-insured loans

Conventional loans

All of the above.

QUALIFYING FOR PMI IN FOUR FACTORS

Consider a prospective homebuyer who wants to purchase a detached single family residence (SFR) to occupy

as their principal residence. The terms for payment of the price will be a 10% down payment from funds held

by the buyer/borrower.

The balance of the price will be funded by a conventional fixed-rate mortgage (FRM) which will not exceed the

conventional loan limit of $417,000. Rebates received by the borrower, whether funded directly or indirectly

by the seller from the proceeds of the sale or by the broker from the seller-paid broker fees, will not exceed

3% of the price paid for the property.

However, the loan will fund 90% of the property’s value, a loan-to-value ratio (LTV) which exceeds the 80%

LTV generally considered free from risk of loss should the borrower default. To shift that risk of loss to others,

the lender requires PMI. The lender’s alternative would be to retain the risk and attempt to cover it with an

increase in the rate of interest when the loan amount exceeds 75% to 80% of the property’s value.

A mortgage lender may require any borrower to qualify and pay the premium for PMI as a condition for

making a loan.

Lenders originating loans for borrowers seeking to purchase owner-occupied residential real estate, and

whose down payment is less than 20% of the purchase price will insist the loan be insured by PMI to cover the

risk of loss on a default by the borrower. This requirement is set by the investors who will eventually purchase

the loan. With conventional loans, the investor who sets the minimum guidelines is either Fannie Mae or

Freddie Mac. [Fannie Mae Selling Guide B7-1-01; Freddie Mac Single-Family Seller/Servicer Guide 27.1]

Thus, a mortgage loan originator involved in arranging or negotiating the new conventional financing with an

LTV exceeding 80%, will retain control of the transaction’s destiny and avoid surprises based on their

knowledge of four sets of considerations used by issuers of PMI:

the borrower’s profile;

the property purchased;

loan terms and conditions; and

the loan processing package.

Editor’s note — The guidelines discussed in the ensuing pages are the general minimum set standards of the

three largest PMI providers for PMI on a loan for a primary residence, and do not represent any one insurer’s

guidelines for approval. The full underwriting guidelines of the three largest PMI providers are listed and linked

below.

Related reading:

Underwriting criteria by PMI provider as of mid-2016

MGIC Underwriting Guidelines

Radian Underwriting Guidelines

Genworth Financial Underwriting Guidelines

(IMPORTANT: These links take you outside of the course. You will not receive credit for time spent reading

material outside of this course.)

MOD8-1_2LEVERAGED.CFM (3 MIN)

THE LEVERAGED BORROWER’S PROFILE AND THE PMI CREDIT CHECK

The lender making a conventional loan to fund the purchase of a principal residence when the loan will exceed

80% LTV will require the borrower to meet the qualifications for PMI coverage, not just the lender’s

qualification requirements.

Thus, PMI qualification requirements become the lender’s minimum requirements for making the loan when

default insurance is required.

A borrower required to qualify for PMI before a lender will fund a loan undergoes an in-depth risk analysis

based on the PMI carrier’s eligibility requirements. Generally, to qualify for PMI, the borrower must:

be a natural person, not a corporation, partnership or limited liability company (with limited exception

for inter vivos revocable trusts since they are not entities); and

take title as the vested owner of the property.

Genworth offers special programs for non-natural persons seeking PMI coverage. [Genworth Underwriting

Manual Section 5.1]

The lender, when qualifying the borrower for a loan to be covered by PMI, relies on the more restrictive PMI

insurer’s requirements regarding the borrower’s:

liquid assets after closing;

debt-to-asset ratio;

debt-to-income ratio; and

regard for financial obligations.

Lenders often turn down applications for loans due to the borrower’s inability to qualify for PMI. At a

minimum, the borrower will be required to submit documents for review by the PMI insurer.

The borrower’s credit rating and disposable income must clearly support their ability to make the monthly

payments on the low down payment loan.

As of the Second Quarter of 2016, the major PMI providers require a borrower to meet the following

minimum standards for a borrower purchasing a single family primary residence:

a minimum credit score of 620 (out of 850) with at least three trade lines supporting the credit score

for a minimum of 12 months;

a total debt-to-income ratio of no more than 41-50%, depending on credit and whether underwriting

authority is delegated;

two months’ PITI payments in cash reserves on closing;

employment full time during the past two years, a current pay stub, written verification by employer

(VOE form), and telephone confirmation of employment at closing, unless self-employed;

if self-employed, financial statements for two prior years and year-to-date, IRS tax returns;

legal residence in the United States;

limit to two loans under PMI coverage in name of borrower;

no bankruptcy within two to seven years;

current on existing mortgage or rental payments with no 30-day late payments on mortgage or rental

payments within the last year;

no short sale within four to seven years;

no foreclosure or deed-in-lieu within five to seven years; and

any existing judgment or lien must be satisfied.

These qualifications are relaxed if the loan submitted has had automated underwriting approval from Freddie

Mac’s Loan Prospector (LP) or Fannie Mae’s Desktop Underwriter (DU) engines.

Additionally, as Fannie Mae and Freddie Mac still do the lion’s share of the industry’s securitization, most

loans subject to PMI will be required to adhere to the ability-to-repay rules. The ability-to-repay rules were

discussed in a prior module.

Comprehension check

You must answer this question before you may proceed to the next page.

A loan-to-value ratio of ___________ triggers private mortgage insurance on a conventional loan.

80%

more than 80%

20%

less than 20%

Type of property

Generally, PMI providers will cover:

single family residences;

two-unit properties;

co-operatives; and

manufactured housing.

Genworth does insure 3-4 unit properties, up to a maximum loan amount of $625,500.

For a property to qualify for PMI coverage, the property must meet the following standards:

property may be used a principal residence, second home, or investment;

vesting of title to the property to be in the name of the individual(s) purchasing the property; and

cash reserves of amount equal to not less than three months of assessments.

All three of the large insurers now welcome investor business, although with attendant changes in restrictions.

MOD8-1_3PMICOVERAGE.CFM (4 MIN)

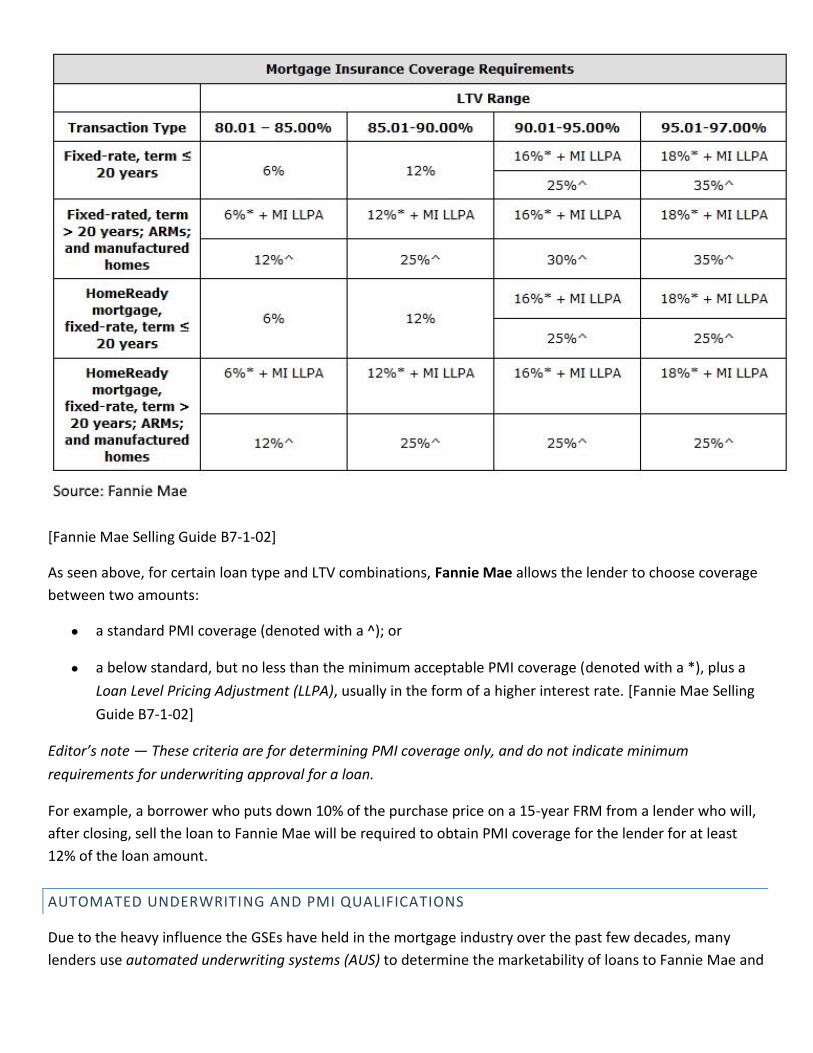

PMI COVERAGE REQUIRED

For a loan to qualify for PMI, the most permissive guidelines allow:

funding of a purchase-assist or rate and term refinance by a borrower;

a maximum loan amount of $417,000;

a maximum 97% LTV;

a maximum 30-year amortization schedule; and

FRMs or fully-amortizing ARMs.

The PMI providers do allow for cash-out refinances, however the LTV limits and credit score requirements are

accordingly adjusted to reflect the higher risk of default.

PMI insures a percentage of a loan amount. In turn, the loan amount represents a percentage of the

property’s value, called the LTV.

Loans insured by PMI are covered for losses on a percentage of the loan amounts. These percentages are

effectively set by LTV and property guidelines issued by investors. The two main investors are still the

government-sponsored entities, Freddie Mac and Fannie Mae.

Freddie Mac PMI Coverage Requirements

[Freddie Mac Single-Family Seller/Servicer Guide Chapter 4701.1]Freddie Mac also allows custom and reduced

PMI coverage for certain qualified borrowers. Additionally, special rules apply for calculating the LTV used to

determine PMI coverage when the PMI is financed into the principal of the loan. [Freddie Mac Single-Family

Seller/Servicer Guide Chapter 4701.1]

For example, a borrower who puts down 15% of the purchase price on a 30-year FRM from a lender who will,

after closing, sell the loan to Freddie Mac will be required to obtain standard PMI coverage for the lender for

at least 12% of the loan amount.

Comprehension check

You must answer this question before you may proceed to the next page.

The _____________ the loan-to-value ratio, the ____________ the PMI coverage required.

lower; greater

greater; greater

greater; lower

Fannie Mae PMI Coverage Requirements

[Fannie Mae Selling Guide B7-1-02]

As seen above, for certain loan type and LTV combinations, Fannie Mae allows the lender to choose coverage

between two amounts:

a standard PMI coverage (denoted with a ^); or

a below standard, but no less than the minimum acceptable PMI coverage (denoted with a *), plus a

Loan Level Pricing Adjustment (LLPA), usually in the form of a higher interest rate. [Fannie Mae Selling

Guide B7-1-02]

Editor’s note — These criteria are for determining PMI coverage only, and do not indicate minimum

requirements for underwriting approval for a loan.

For example, a borrower who puts down 10% of the purchase price on a 15-year FRM from a lender who will,

after closing, sell the loan to Fannie Mae will be required to obtain PMI coverage for the lender for at least

12% of the loan amount.

AUTOMATED UNDERWRITING AND PMI QUALIFICATIONS

Due to the heavy influence the GSEs have held in the mortgage industry over the past few decades, many

lenders use automated underwriting systems (AUS) to determine the marketability of loans to Fannie Mae and

Freddie Mac. Fannie Mae’s AUS is called Desktop Underwriter (DU); Freddie Mac’s is called Loan Prospector

(LP).

Lender underwriters verify the information on the loan application is in line with submitted credit and

property information. Application and credit data is then entered into an AUS for a decision, based on each

GSE’s underwriting guidelines.

PMI providers have likewise adapted their qualification standards to suit AUS decisions. While not entirely

supplanting the manual underwriting and verification duties of the lender or the PMI provider, AUS decisions

streamline the process and are sometimes considered in tandem with existing PMI provider guidelines. The

level of interactivity with AUS decisions varies by PMI provider, but PMI providers generally accept GSE AUS

decisions, subject to additional PMI provider underwriting requirements, called overlays.

For example, Radian’s One Underwrite program qualifies a PMI applicant’s DTI ratios based on whether they

were deemed Eligible by DU, rather than reviewing DTI ratios independently. The Eligible decision is subject to

five Radian underwriting overlays confirming minimum credit score requirements, property type and

minimum borrower contribution.

LOAN PACKAGING FOR PMI DOCUMENT EFFICIENCY

Full documentation in the loan packaging process is fundamental to a lender controlling their risk of loss on

each loan they originate.

Fundamentals of mortgage lending call for full documentation, analysis of credit and income, and a review of

the completed package by the lender who will end up actually owning the loan and taking the risk.

A knowledgeable mortgage loan originator should be able to pre-determine the likelihood of closing a loan by

conducting their own review of a borrower’s credit score and source of funds. Only then are they ready to

commence the search for suitable loan product and lender (taking into consideration the PMI guidelines of the

lender’s preferred PMI provider) on behalf of a borrower.

At a minimum, the application to the PMI provider must include:

a copy of the loan application;

a credit report current within 90 days and covering a minimum of two years; and

an appraisal of the real estate to be purchased.

However, the PMI provider may also require additional documentation to verify the loan transaction fulfills

the insurer’s underwriting requirements, including:

verification of occupancy status;

a copy of the signed purchase agreement/sales contract;

verification of funds for closing;

verification of the borrower’s salary/wages, including overtime and second jobs; and

verification of employment.

Unit 2: Defaults and Cancellations

MOD8-2_1DEFAULTS.CFM (4 MIN)

UNIT 2 LEARNING OBJECTIVES

This unit will teach the student to:

identify the PMI provider’s responsibilities in the case of a borrower’s default;

determine minimum cancellation requirements and timelines for PMI under the Homeowners

Protection Act (HPA) of 1998; and

understand the penalties for a failure to adhere to the HPA.

DEFAULTING BORROWER AND PMI RECOURSE

Most private mortgage insurance (PMI) contracts do not authorize the carrier to seek indemnity from the

borrower for claims made on the policy by the lender — unlike Federal Housing Administration (FHA) or

Department of Veterans Affairs (VA) insurance programs which place borrowers at a risk of loss for a greater

amount than their down payment.

However, if the loan is recourse, the lender’s right to seek a deficiency judgment may be assigned to the PMI

carrier.

Most insured loans are purchase-money loans made to borrowers looking to acquire their principal residence.

Purchase money loans are nonrecourse obligations, with recovery on the loan limited to the value of the real

estate. [26 Code of Federal Regulations §1.1001-2]

In the case of fraud on recourse or nonrecourse loans, the PMI carrier is not barred by anti-deficiency statutes

and will be able to enforce collection of their losses against the borrower for misrepresentations, such as a

misrepresentation of the property value.

Consider a lender whose loan is secured by a first trust deed on a personal residence in default.

The lender forecloses on the property by a trustee’s sale and acquires the property by bidding the dollar

amount of its current fair market value (FMV). The lender then submits its claim to the insurer, including

documents showing the price bid at the trustee’s sale and a recent appraisal of the property.

If the owner of the property is in default, and the insured lender is willing to work out a short sale, the PMI

carrier must be notified immediately of the impending short payoff. PMI will not cover loan discounts on short

sales unless the owner is in default.

Additionally, PMI policies contain a physical damage exclusion which generally excludes the following damages

from coverage:

toxic contamination;

earthquakes;

floods; or

civil unrest.

Comprehension check

You must answer this question before you may proceed to the next page.

Purchase money loans are _____________, with recovery on the loan limited to the value of the real estate.

nonrecourse

recourse

THE RIGHT TO CANCEL UNDER THE HOMEOWNERS PROTECTION ACT OF 1998

Prior to July 29, 1999, homeowners experienced noted difficulty in cancelling borrower-paid PMI (BPMI),

either as a result of convoluted lender cancellation policies or blatant lender refusal to cancel PMI upon

request.

The Homeowners Protection Act of 1998 (HPA) established uniform PMI cancellation policies for home loans,

and went into effect for all loans closed on or after July 29, 1999. [12 United States Code §§4901-4910]

IN THE NEWS

In August of 2015, the CFPB issued a guidance bulletin on HPA guidelines, citing “substantial industry

confusion over PMI cancellation and termination requirements” and continuing violations of the HPA. [August

4, 2015 CFPB Press Release, “CFPB Provides Guidance About Private Mortgage Insurance Cancellation and

Termination.”]

SCOPE OF THE HPA

The scope of the HPA is limited to PMI issued on loans for the purchase, construction or refinance of a

principal residence. Thus, PMI for loans secured by second homes is not covered under the HPA.

However, both Fannie Mae and Freddie Mac have adopted the HPA requirements for loans secured by second

homes, effectively extending the disclosure and cancellation requirements to second homes— at least for

those loans purchased by the two GSEs.

Note also that lender-paid mortgage insurance (LPMI) cannot be cancelled or terminated, and is not subject to

any of the cancellation/termination or disclosure requirements discussed below, except where specifically

indicated. [12 USC §4905(b)]

For home loans closed on or after July 29, 1999

Under the HPA, when the borrower qualifies for PMI and a policy is issued, the lender must notify the

borrower of the borrower’s right to cancel the PMI:

at the time of closing; and

each year thereafter. [12 USC §4903]

The notice of right to cancel PMI delivered at the time of closing must include:

a written amortization schedule;

notification of the borrower’s right to cancel PMI at the 80% LTV mark based on either:

o the written amortization schedule; or

o actual payments;

(if an ARM) notification that the lender/servicer will notify the borrower of the cancellation date;

the date and conditions for automatic PMI termination; and

exemptions to the right to cancel PMI on high-risk loans, and whether those exemptions apply to the

borrower’s loan. [12 USC §4903(a)(1)]

The annual notice of right to cancel PMI must include:

the borrower’s right to and the conditions for a request for cancellation of the PMI;

the borrower’s right to and the conditions for automatic termination of the PMI; and

the contact address and phone number of the loan servicer the borrower may contact for questions

about cancelling the PMI.

For home loans closed before July 29, 1999

The requirements of the HPA were not retroactive under federal law. Thus, for any loans closed before the

effective date of July 29, 1999, the right to cancel is determined by controlling state law or investor guidelines.

An annual notice must still be provided to the borrower, and must include:

a disclosure stating the borrower may be able to request a cancellation of PMI, depending on state law

or investor guidelines; and

the contact address and phone number of the loan servicer the borrower may contact for questions

about cancelling the PMI. [12 USC §4903(b)]

If the borrower and the lender agree to a loan modification, the cancellation and termination dates must be

recalculated to reflect the modified terms of the loan. [12 USC §4902(d)]

MOD8-2_2BPMI.CFM (4 MIN)

BUYER-REQUESTED CANCELLATION OF PMI

Under federal law, PMI can be:

cancelled upon borrower request [12 USC §4902(a)];

automatically terminated by the termination date [12 USC §4902(b)]; or

automatically terminated by the final termination date. [12 USC §4902(c)]

A borrower may cancel PMI if they:

submit a written request to the server to initiate the cancellation of PMI;

have not had a 60-day late on their mortgage in the 24 months prior to the later of:

o the date the LTV reaches 80%; or

o the date of the borrower’s request for cancellation;

have not had a 30-day late on their mortgage in the 12 months prior to the later of:

o the date the LTV reaches 80%; or

o the date of the borrower’s request for cancellation;

are current on their mortgage payments; and

provide evidence to the lender that:

o the property securing the loan has not declined in value; and

o the property is not encumbered by any subordinate liens. [12 USC §4901(4); 12 USC §4902(a)]

If a servicer determines the borrower has not met the above requirements for PMI cancellation, the servicer

must provide written notice of the reason why the cancellation request is being denied. This notice must

include the results of any appraisal relied on in making the decision. [12 USC §4904(b)(1)]

TERMINATION OF PMI AND THE LPMI ELIMINATION NOTICE

If the borrower does not meet the criteria for requesting cancellation of PMI, PMI will automatically

terminate on the automatic termination date. The automatic termination date is:

if the borrower is current on their mortgage payments, the date the LTV reaches 78%, based on the

initial amortization schedule (or the current amortization schedule, if the loan is an ARM) [12 USC

§§4901(18), 4902(b)(1)]; or

if the borrower is not current on their mortgage payments when the LTV reaches 78%, the first day of

the first month after the date the borrower becomes current on their mortgage payment.[12 USC

§4902(b)(2)]

If PMI is not otherwise cancelled or terminated and the borrower is current on their mortgage payments, PMI

must be terminated on the first day of the month following the midpoint of the amortization schedule, called

the final termination date. [12 USC §4902(c)]

If PMI is not otherwise cancelled and the borrower is not current on their mortgage payments, PMI must be

terminated when the borrower become current on their mortgage payments. [12 USC §4902(b)]

Within 30 days of what would have been the automatic termination date on the same loan with BPMI, the

loan servicer of a loan with LPMI must provide a written notice informing the borrower that they may wish to

review their options for eliminating LPMI, e.g., a refinance. [12 USC §4905(c)(2)]

Comprehension check

You must answer this question before you may proceed to the next page.

__________ may be cancelled upon borrower request.

BPMI

LPMI

Both of the above.

Neither of the above.

EXCEPTIONS FOR HIGH-RISK LOANS

A high-risk loan is either:

a loan with a conforming loan amount determined to be a high risk by Fannie Mae or Freddie Mac; or

a loan with a non-conforming loan amount determined to be a high risk by the originating lender. [12

USC §4902(g)(1)]

Conforming high-risk loans cannot be cancelled by borrower request or terminated automatically. Instead,

PMI is terminated on the first day of the month following the midpoint of amortization schedule, provided the

borrower is current on their mortgage payments, called the final termination date. [12 USC §4902(c)]

If the borrower is not current, PMI must be terminated when the borrower become current on their mortgage

payments. [12 USC §4902(c)]

Neither Fannie Mae nor Freddie Mac have actually defined or given the criteria for a high-risk loan, however

they have federal statutory authority to do so. [12 USC §4902(g)(1)(A)]

Non-conforming high-risk loans cannot be cancelled by borrower request, but must be automatically

terminated once the LTV reaches 77%, based on the initial amortization schedule (or the current amortization

schedule, if the loan is an ARM). [12 USC §4902(g)(1)(B)]

As with conforming loans, if PMI is not terminated automatically, it must be terminated on the first day of the

month following the midpoint of amortization schedule, provided the borrower is current on their mortgage

payments. [12 USC §4902(c)]

MOD8-2_3DEADLINES.CFM (3 MIN)

DEADLINES FOR PAYMENTS AND RETURN OF PREMIUMS AND REQUIRED NOTICE OF

CANCELLATION OR TERMINATION

A lender cannot require payments for PMI premiums more than 30 days after:

the later of:

o the date the lender receives the borrower’s request for cancellation; or

o the date the borrower provides to the lender evidence the borrower has met all borrower-

requested cancellation requirements;

the automatic termination date; or

the final termination date. [12 USC §4902(e)]

The lender and servicer must return all unearned PMI premiums to the borrower within 45 days after the

cancellation or termination of PMI. [12 USC §4902(f)(1)]

Within 30 days of cancellation or termination of PMI, the loan servicer must notify the borrower in writing

that PMI has been terminated and no other PMI payments will be due. [12 USC §4904(a)]

The notice must be given to the borrower within 30 days of:

the later of:

o the date the lender receives the borrower’s request for cancellation; or

o the date the borrower provides to the lender evidence the borrower has met all borrower-

requested cancellation requirements [12 USC §4904(b)(2)(A)]; or

the automatic termination date. [12 USC §4904(b)(2)(B)]

VIOLATION OF THE HPA

Any servicer, lender or PMI provider that violates the HPA is subject to civil penalties.

If a violation of the HPA is confirmed in an action brought about by an individual borrower, the violating

servicer, lender or PMI provider is liable for:

actual money loss, plus interest set by the court;

statutory damages of up to $2,000; and

court and attorney fees.

If a violation of the HPA is confirmed in a class action and the violating servicer, lender or PMI provider is

federally regulated, it is liable for:

the lesser of:

o $500,000; or

o 1% of the liable party’s gross revenues; and

court and attorney fees.

If a violation of the HPA is confirmed in a class action and the violating servicer, lender or PMI provider is NOT

federally regulated, it is liable for:

actual money loss, plus interest set by the court;

statutory damages of up to $1,000 per class member, up to the lesser of:

o $500,000; or

o 1% of the liable party’s gross revenues; and

court and attorney fees. [12 USC §4907(a)]

A borrower must bring about an action based on a violation of the HPA within two years of discovering the

violation. [12 USC §4907(b)]

Comprehension check

You must answer this question before you may proceed to the next page.

The lender and servicer has __________ after the cancellation or termination of PMI to return all unearned

PMI premiums to the borrower.

60 days

75 days

90 days

45 days

FEDERAL LAW PREEMPTION

State laws regarding PMI existed in California, Colorado, Connecticut, Maryland, Massachusetts, Minnesota,

Missouri and New York prior to the enactment of the HPA in July 29, 1998.

These state laws and any amendments to these state laws made before July 29, 2000 were allowed to control

as long as they provided more borrower protection than the HPA. Specifically, these state laws were allowed

to control insofar as they:

provided earlier termination of PMI than the HPA;

required more information be disclosed to the borrower than the HPA; or

required more frequent or earlier disclosure than is required under the HPA. [12 USC §4908(a)(2)]

The HPA also supersedes any conflicting provisions in servicing agreements between servicers and investors

(including Fannie Mae and Freddie Mac). [12 USC §4908(b)]

Unit 3: PMI, MIP or neither?

MOD8-3_1RECENT.CFM (3 MIN)

UNIT 3 LEARNING OBJECTIVES

This unit will teach the student to:

compare and contrast the FHA’s mortgage insurance premium (MIP) with PMI and a 20% down

payment to quickly determine a borrower’s best option; and

review PMI pricing options, based on borrower creditworthiness.

RECENT HISTORY: FHA AND MIP DURING THE PMI EMBARGO

In contrast to private mortgage insurance (PMI) on conventional loans, the Federal Housing Administration

(FHA)’s mortgage insurance premium (MIP) insures lenders against loss due to the foreclosure of an FHA-

insured loan.

From the mortgage meltdown late in 2007 to early in 2010, PMI providers decamped from distressed areas,

leaving any borrowers in those areas with less than a 20% down payment with no other options but to go with

an FHA-insured loan. As a result, FHA loans began to take an increasing share of the mortgage market, even in

notoriously expensive states such as California.

PMI providers have returned to business areas as usual in recent years.

THE COST OF MIP

Recall from the first unit that borrower-paid private mortgage insurance (BPMI) is paid monthly along with

their monthly mortgage principal and interest payments.

Editor’s note — PMI will be used interchangeably with BPMI for the comparisons in this unit.

In contrast, a borrower pays MIP in two ways:

as an up-front fee, set by a percentage of the base loan amount, and paid at the closing of the loan;

and

as an annual premium, set by a percentage of the loan balance, paid monthly. [HUD Handbook

4000.1(II)(A)(2)(e)]

The costs of both kinds of MIP vary depending on loan purpose, term, base loan amount and loan-to-value

(LTV) ratio.

Comprehension check

You must answer this question before you may proceed to the next page.

_________ include(s) both an up-front premium and annual premiums.

Private mortgage insurance

FHA mortgage insurance premiums

Both of the above.

Neither of the above.

Up-Front MIP

Annual MIP

Editor’s note — These updated annual MIP amounts do not impact streamline refinance transactions endorsed

on or before May 31, 2009.

In early 2013, the FHA increased annual MIP rates, and extended the payment period for MIP.

Consider a 30-year fixed-rate mortgage (FRM) for a base loan amount of $250,000. The loan will be used to

purchase a single family residence (SFR) with 3.5% down payment by the borrower. The borrower is quoted a

3.75% interest rate.

Based on the FHA MIP requirements, the up-front MIP for this borrower is 1.75%. The annual MIP is 0.85%.

Thus, the borrower will be paying a 3.75% interest rate + 0.85% annual MIP for a total of 5.10% of the loan

amount — for the duration of the loan. Additionally, they would have paid 1.75% of the loan amount, or

$4,375 in up-front MIP.

Editor’s note — Up-front MIP may be financed into the loan. That option was covered in a previous module. For

purposes of comparing MIP with PMI, we will assume the up-front MIP was paid by the borrower on loan

closing.

MOD8-3_2PMIQUAL.CFM (5 MIN)

FANNIE MAE AND FREDD IE MAC’S 3% DOWN PAYMENT PROGRAMS

Freddie Mac will accept 3% down payments under their new Home Possible Advantage program for

mortgages closing on or after March 23, 2015.

To qualify for a Freddie Mac mortgage with a 3% down payment, a homebuyer needs to:

use the mortgage to fund the purchase or a no-cash refinance; occupy the property securing the mortgage as their primary residence; own no interest in any other residential property as of the note date, eliminating homeowners who

want to finance the purchase of a home before they have sold their current home; have an annual income no greater than the area’s median income (different rules apply for high cost or

underserved areas — a look-up tool for area income limits is available here); purchase or refinance a one-unit, non-manufactured home (condos are allowed); and have a maximum back-end debt-to-income (DTI) ratio of 43% (there is no front-end DTI limit).

First-time homebuyers must first fulfill education requirements, which can be met through:

an internet-based homeownership education program developed by a mortgage default insurance company; or

a homeownership education program which meets the standards set by the National Industry for Homeownership Education and Counseling.

Further, the mortgage needs to be:

a first trust deed lien; conventional (no government-insured mortgages); fully amortizing; a fixed rate loan with a term no longer than 30 years; and within the maximum loan-to-value (LTV) ratio of 97%.

The mortgage insurance coverage level on a mortgage with a down payment greater or equal to 3% and less

than 5% is 18%. These mortgages are not eligible for custom or reduced mortgage insurance.

Fannie Mae now also allows down payments as low as 3%. This is offered through either:

their My Community Mortgage (MCM) program for first-time homebuyers, for those who meet Freddie Mac’s annual income and DTI ratio limitations; or

standard purchase transactions for all other first-time homebuyers who exceed median incomes.

Freddie Mac and Fannie Mae’s rules conform on most points. However, Fannie Mae’s program differs in that:

homebuyers taking out non-MCM mortgages do not have to fulfill education requirements; homebuyers may not have owned a residence during the last three years; and limited cash-out refinances are allowed for non-MCM mortgages.

Fannie Mae and Freddie Mac will allow homebuyers taking out these low down payment mortgages to use

down payment gifts, as long as the property is a single unit. This may bring out the builders, as prior to 2008 it

was common for builders to indirectly gift the full required down payment on Federal Housing Administration

(FHA) and later conventional mortgages (through help of a third party “facilitator”). These Nehemiah loans as

they were sometimes structured, were all the result of 1990s deregulation.

However, Fannie Mae qualifies 2-4 unit and manufactured homes as long as homebuyers make a minimum 3%

contribution which cannot be covered by gift funds.

Fannie and Freddie claim these mortgages will cost the homebuyer slightly less than FHA-insured mortgages.

This is due to the slightly lesser cost of private mortgage insurance (PMI) compared to the FHA’s mortgage

insurance premiums (MIPs).

If the homebuyer and the property meet the program qualifications, the homebuyer may qualify to put down

as little as 3%. However, just because Fannie and Freddie are willing to purchase this low down payment type

of mortgage doesn’t mean lenders will be willing to originate them.

Prior to this change, Fannie and Freddie required a minimum 5% down payment mortgage. This minimum

contribution was already low, in light of annual home price fluctuations, especially during this volatile

recovery.

With such low down payments, new homebuyers have less skin in the game. Thus, if home prices dropped,

say, more than 3% in a year (actually most likely in the first few months of 2015), homebuyers would suddenly

have a negative equity asset on their hands. This negative equity condition has recently proven to be an

incentive to default on mortgage payments.

Lenders tend to be more conservative than Fannie and Freddie, citing the fear of buy backs when

underwriting errors exist and the homebuyer defaults. This fear is particularly warranted when programs —

such as these — introduce a greater risk of default and impose additional underwriting requirements.

Therefore, expect lenders to be very cautious when it comes to offering 3% down payment mortgages of the

conventional type.

Remember, lenders still receive 0.25% risk-free interest on bank reserves from the Federal Reserve (the Fed).

Thus, they have less impetus to lend, evidenced by the exponential increase in excess bank reserves (excess

reserves at the Fed have risen 1,300 times their amount in 2008 as of October 2014).

If lenders do decide to take on the additional risk, these low down payment programs might open the door to

homeownership for many ready and willing first-time homebuyers years before they otherwise would have

been able to buy.

If these programs are a success, they’ll certainly help our failing housing recovery end more quickly. We’ll see

what lenders choose to do with them; once again, the ball is in their court.

PMI QUALIFICATIONS COMPARED

Consider the same borrower shopping for a loan: a 30-year fixed-rate mortgage (FRM) with a loan amount of

$250,000. The loan will be used to purchase a single family residence (SFR). The borrower has a credit score of

680.

The first thing to consider is that since Fannie Mae and Freddie Mac are nearly exclusively shouldering the

investment of conventional conforming loan products, their underwriting guidelines will control lender

decisions.

That being the case, Freddie Mac’s maximum allowable LTV on 30-year FRM for the purchase of an SFR is 97%,

under the new Home Possible program. [Freddie Mac Single-Family Seller/Servicer Guide A34]

The PMI Coverage Requirements from the first unit indicate that Freddie Mac will require 18% PMI coverage

for 30-Year FRM with an LTV greater than 90%.

COMPARING COSTS OF MORTGAGE INSURANCE

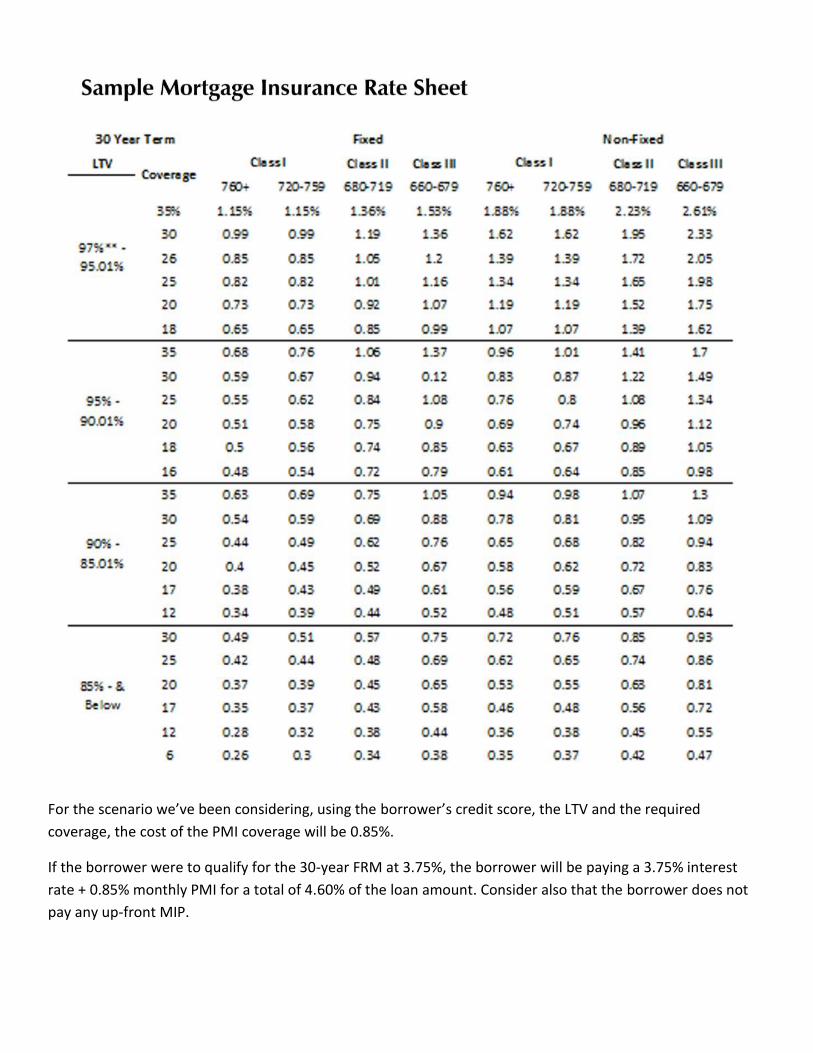

To determine the PMI premium which will be charged to the borrower, consult the underwriting guidelines

and rates published by the PMI providers.

For the scenario we’ve been considering, using the borrower’s credit score, the LTV and the required

coverage, the cost of the PMI coverage will be 0.85%.

If the borrower were to qualify for the 30-year FRM at 3.75%, the borrower will be paying a 3.75% interest

rate + 0.85% monthly PMI for a total of 4.60% of the loan amount. Consider also that the borrower does not

pay any up-front MIP.

With an FHA-insured mortgage, the borrower pays a 1.75% up-front MIP required of an FHA-insured loan. The

1.75% up-front MIP is a fee, comparable to points paid on loan origination, and does not directly benefit the

borrower. In addition to the up-front MIP, the borrower also pays an annual MIP, which is also 0.85% in the

current scenario.

Additionally, the PMI will cancel at the borrower’s request at 80% LTV, or automatically at 78% LTV. Under the

new FHA guidelines, this borrower’s MIP would last for the duration of the loan.

Thus, all other factors being equal, a borrower qualified for both a conventional loan with PMI and an FHA-

insured mortgage maximizes their purchasing power if they choose a conventional loan with PMI.

Related reading:

PMI Rates by PMI Provider

MGIC BPMI Rates

Radian BPMI Rates

Genworth BPMI Rates

(IMPORTANT: These links take you outside of the course. You will not receive credit for time spent reading

material outside of this course.)

Comprehension check

You must answer this question before you may proceed to the next page.

On a loan with an LTV above 90%, which type of mortgage insurance would be cancellable first?

FHA MIP.

BPMI.

LPMI.

COMPARING CREDIT REQUIREMENTS AND DEBT-TO-INCOME REQUIREMENTS

Of course, the costs alone are not the only deciding factors. The choice between a PMI-insured conventional

loan and an MIP-insured FHA loan hinges mainly on three factors:

the borrower’s credit;

the borrower’s debt; and

the LTV.

A conventional loan requiring PMI under Freddie Mac guidelines, requires a minimum credit score of 620.

[Freddie Mac Single-Family Seller/Servicer Guide Exhibit 25; Fannie Mae 2015 Selling Guide B3-5.1-01]

In contrast, the minimum credit score required for maximum FHA-insured financing (up to 97% LTV) is only

580. Borrowers with credit scores between 500 and 579 may be eligible for up to 90% LTV financing. [HUD

Handbook 4000.1(II)(A)(2)(b)(i)]

Editor’s note — In practice, very few borrowers with 580 credit scores receive FHA-insured financing. Lenders

can (and do) impose their own stricter requirements when making loans. According to the July 2015 Ellie Mae

Origination Insight report, the average credit score for closed FHA purchases and refinances was around 680.

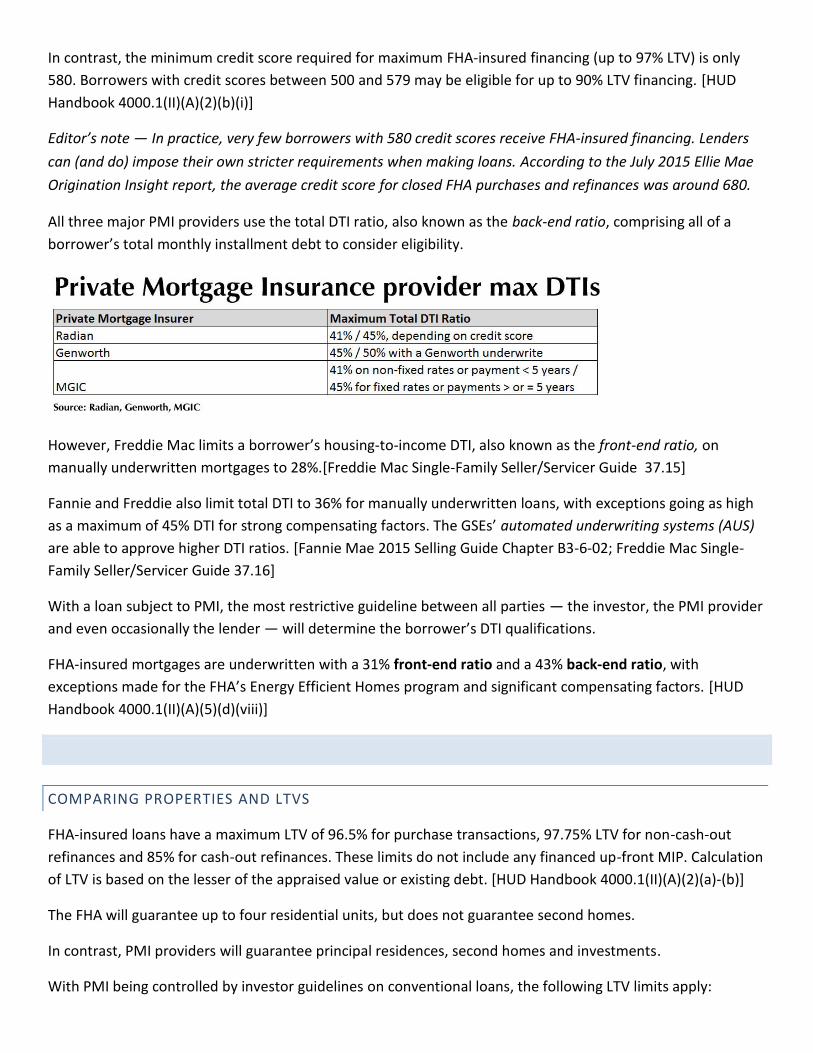

All three major PMI providers use the total DTI ratio, also known as the back-end ratio, comprising all of a

borrower’s total monthly installment debt to consider eligibility.

However, Freddie Mac limits a borrower’s housing-to-income DTI, also known as the front-end ratio, on

manually underwritten mortgages to 28%.[Freddie Mac Single-Family Seller/Servicer Guide 37.15]

Fannie and Freddie also limit total DTI to 36% for manually underwritten loans, with exceptions going as high

as a maximum of 45% DTI for strong compensating factors. The GSEs’ automated underwriting systems (AUS)

are able to approve higher DTI ratios. [Fannie Mae 2015 Selling Guide Chapter B3-6-02; Freddie Mac Single-

Family Seller/Servicer Guide 37.16]

With a loan subject to PMI, the most restrictive guideline between all parties — the investor, the PMI provider

and even occasionally the lender — will determine the borrower’s DTI qualifications.

FHA-insured mortgages are underwritten with a 31% front-end ratio and a 43% back-end ratio, with

exceptions made for the FHA’s Energy Efficient Homes program and significant compensating factors. [HUD

Handbook 4000.1(II)(A)(5)(d)(viii)]

MOD8-3_3COMPARING.CFM (3 MIN)

COMPARING PROPERTIES AND LTVS

FHA-insured loans have a maximum LTV of 96.5% for purchase transactions, 97.75% LTV for non-cash-out

refinances and 85% for cash-out refinances. These limits do not include any financed up-front MIP. Calculation

of LTV is based on the lesser of the appraised value or existing debt. [HUD Handbook 4000.1(II)(A)(2)(a)-(b)]

The FHA will guarantee up to four residential units, but does not guarantee second homes.

In contrast, PMI providers will guarantee principal residences, second homes and investments.

With PMI being controlled by investor guidelines on conventional loans, the following LTV limits apply:

On owner-occupied properties, Freddie Mac limits one-unit purchases and no-cash-out refinances to 97% for

one-unit, and 80% for two-unit. Cash out refinances are limited to 80% and 75%, respectively.

On second homes, Freddie Mac limits purchases and no-cash-out refinances to 85%, and cash-out refinances

to 75%. Higher LTVs may apply for refinances of loans currently owned or securitized by Freddie Mac. [Freddie

Mac Single-Family Seller/Servicer Guide 23.4]

On owner-occupied properties financed by fixed rate mortgages, Fannie Mae limits one-unit purchases and

no-cash-out refinances to 97% for one-unit, and 80% for two-unit. Cash out refinances are limited to 85% and

75%, respectively.

On second homes financed by fixed rate mortgages, Fannie Mae limits purchases and no-cash-out refinances

to 90%, and cash-out refinances to 75%. Higher LTVs may apply for loans underwritten by DU.

Fannie Mae’s maximum LTV limits are reduced for adjustable rate mortgage loans. [Fannie Mae Eligibility

Matrix, June 30, 2015]

Comprehension check

You must answer this question before you may proceed to the next page.

Which type of mortgage insurance will cover second homes?

FHA MIP.

PMI.

Both of the above.

Neither of the above.

THE ALTERNATIVE: A 20% SOLUTION

As the FHA continues to price itself out of the market to recoup the losses incurred while it shouldered the

nation’s appetite for homeownership, it won’t be long before PMIs will increase rates to meet that

competition. All this action on mortgage insurance will adversely affect the pricing of housing until borrowers,

as a group, take the time to accumulate savings for the industry preferred down payment of 20% and not be

deprived of the purchasing power delivered by qualifying for a conventional loan, with or without mortgage

insurance.

Often, lenders and PMI providers do not fully appreciate it is the amount of the down payment that primarily

controls the risk of default. However, forcing all borrowers to put down 20% of the purchase price of the

property would eliminate mortgage default insurance premiums and decrease the market demand for loans,

and is thus against the best interests of PMI providers and mortgage lenders.

MOD8-3_4RECURRING.CFM (3 MIN)

RECURRING LOAN COSTS WITH MIP/PMI

This chart tracks the total percentage rate paid on principal for default insurance paid by borrowers who make

a down payment of less than 20% of the price they pay for a home, including premiums and interest due on

30-year and 15-year FRMs.

The chart includes both:

the FHA’s MIP; and

PMI.

PMI rates listed on the chart are the average rates offered by PMI providers MGIC, and Genworth Mortgage

Insurance Co. The PMI rates are for 25% loss coverage on a conforming FRM originated at an LTV of 90.01%-

95% on appraised value, secured by the single-family residence (SFR) occupied as the primary residence of a

borrower with an average credit score of 700.

The borrower who has the financial ability to make a 20% down payment comes out ahead of the borrower

whose insufficient down payment requires default insurance for the lender. Without 20% down, they are

forced to pay the annual PMI fee, which is regressively based on the entire loan amount due. This adverse

leveraging turns a MIP/PMI premium of 1% of the mortgage balance into a charge of 6-16% on the additional

funds needed to increase a down payment to 20%.

Though the additional savings paid upfront to increase the down payment and avoid the insurance premium

does not earn interest in a bank account, this opportunity cost for moving funds to avoid PMI insurance is well

worth it. The borrower with a 20% down payment avoids the entire amount of the premium, which is based

on the loan principal (and not on the additional down payment amount). Thus, while the borrower may gain

some interest earnings by holding onto their cash savings, the costs of holding onto the cash are greater than

a savings account will pay.

For instance, consider the borrower who purchases a property priced at $300,000 with a 5% down payment

($15,000). To fund the remainder of the purchase price, they opt for a 30-year FRM with mortgage insurance.

With a down payment of less than 20%, they must provide and pay the premiums for PMI, an additional

annual cost equal to 0.89% of the loan balance. They have savings or access to funds for another $45,000

which could be used to bring the down payment to the 20% mark and avoid PMI and the premiums.

Applying this leveraging situation to our $285,000 95% financing, the PMI premium charge payable for the first

year will be roughly $2,537. This premium is entirely avoided if $45,000 is withdrawn from savings and used to

increase the down payment to 20% of the price. The $45,000 is only earning 1% in a bank account, $450

annually, which will be forgone on use of the savings to increase the down payment amount.

Thus, the additional $45,000 used to increase the down payment to avoid PMI premiums earns $2,537 the

first year; an 5.64% annual rate of return, five times more than earnings on the savings withdrawn to raise the

down payment to 20%.

Each year following will realize slightly lesser amounts “saved” until the loan principal is reduced or the home

increases in value to an LTV of 78%, or five years pass and the mortgage insurance is no longer required.

In conclusion, borrowers who can make a 20% down payment need to be advised of the option available to

them, if not directly encouraged by their agents to make the payment. A down payment large enough to avoid

mortgage insurance coverage enables borrowers to reduce their monthly recurring costs of homeownership

while MIP/PMI is in place. The result: a higher rate of return than would otherwise be received on the amount

of the borrower’s savings when used to make the greater down payment and avoid the MIP/PMI.

Unit 4: PMI in the market

MOD8_CS1.CFM (3 MIN)

HOW MORTGAGE INSURERS FARED IN THE GREAT RECESSION

It’s no surprise that the private mortgage insurance (PMI) providers had a rough time in the wake of the

housing crash. With hundreds of thousands of homeowners defaulting on mortgages insured by PMI

providers, the expected happened: PMI providers were unable to keep their mandatory reserves in check, and

some were forced to stop issuing policies.

However, in the recovery which followed, PMI providers have gradually recovered market share and their own

solvency.

PMI IS BACK FROM THE DEAD

In the first quarter of 2012, MGIC reported its seventh-straight quarterly loss, totaling nearly $20 million.

In February of 2012, PMI provider MGIC announced it had gotten waivers from Fannie Mae to continue writing

mortgage insurance policies.

MGIC suffered repeated losses covering mortgage lender risks of loss on foreclosure, inching closer to joining

the ill-fated group of other beleaguered private mortgage insurers, including Radian Group, Inc., PMI Group,

Inc., and Triad Guaranty Inc. PMI and Triad Guaranty Inc. were ordered to stop writing policies, but MGIC

plans to continue business.

The ratio of borrowers reinstating loan payments to those remaining in default has grown more disparate,

from a 95-to-100 ratio in 2010, to an 87-to-100 ratio as of November 2011. While MGIC reported a fourth

quarter net loss of $135.3 million compared to last year’s $186.7 million loss, policy sales have also decreased

2.8 percent and the rate of borrower default continues to drain the company’s resources.

However, MGIC’s balance sheet has improved substantially during the recovery, thanks in no small part to a

spate of FHA MIP rate increases in recent years. As the number of PMI loans increases, the premiums for both

FHA and MGIC policies are rising.

The preventative prescription for this kind of blow to MGIC and other mortgage insurers has always been

borrower skin in the game (and being able to charge profitable premiums in competition with FHA also helps).

A borrower will be much less likely to dump onto mortgage insurance companies the sizable obligation of

paying lenders hundreds-of-thousands of dollars if the borrower has already invested a substantial sum of

money in the property by fronting a 20% down payment.

This 20% indicates the borrower has a real motivation to pay a proper price for a property and then stay with

their chosen property and do all they can to maintain possession of it. 20% is a cushion against price drops

(though this time around down payments and equities even at 50% did not prevent total destruction of the

equity in some instances).

And in early 2013, for the first time since 2010, the private mortgage insurance (PMI) company MGIC

reported quarterly profits.

In the second quarter (Q2) of 2013, MGIC reported:

$196 million in mortgage claims costs; and $12 million in profit.

Compare this to Q2 2012, when MGIC reported:

$551 million in mortgage claims costs; and $274 million in losses.

This outcome seemed virtually impossible one year ago, when MGIC was still suffering under a seemingly

unrelenting barrage of homeowner defaults.

But two key changes in the mortgage market have impacted MGIC’s balance sheet since then:

homeowner defaults decreased — in California the rate was 53% lower in Q2 2013 than in Q2 2012; and

the Federal Housing Administration (FHA) raised their mortgage insurance premiums (MIP) and extended their MIP requirement through the life of the loan.

Considering today’s rising interest rates, the FHA’s increased MIP does little to ingratiate home buyers with

their product. As the disparity in rates between MIP and PMI premiums grows, so does the number of

homebuyers choosing PMI firms like MGIC rather than an FHA-insured loan.

MGIC and other PMI companies can raise a hallelujah — it looks like they may stick around after all and

prosper with the private sector. Home buyers will reap the benefits of this unlikely survival through increased

competition between PMI and FHA MIP rates.

When private insurance providers are left to compete and hash out their differences without government

programs outbidding them, borrowers win.

MINIMUM REQUIREMENTS FOR PMI PROVIDERS

In mid-2014, the Federal Housing Finance Agency, the government entity in charge of Fannie Mae and Freddie

Mac, solicited comment on setting minimum requirements for private mortgage insurance companies to meet

in order to insure loans sellable to Fannie Mae or Freddie Mac.

Beginning December 31, 2015, private mortgage insurers have been required to meet a minimum net worth of

$400 million, to avoid a repeat of the multiple PMI provider failures which occurred after the mortgage

meltdown.

Additionally, each PMI provider is required to have liquid assets exceeding their “minimum required assets”,

which is a figure calculated based on the PMI provider’s exposure.

RECOVERED MARKETS

Since the fallout of the financial crisis, the PMI providers have rebounded. In the second quarter (Q2) of 2016,

all three major PMI providers showed growing or steady net income quarter-over-quarter, with new PMI

policies issued growing year over year from:

$11.9 billion in Q2 of 2015 to $12.9 billion in Q2 of 2016 for Radian [Press Release: Radian Announces

Second Quarter 2016 Financial Results];

$11.6 billion in Q2 of 2015 to $12.6 billion in Q2 of 2016 for MGIC [Press Release: MGIC Investment

Corporation Reports Second Quarter 2016 Results]; and

$8.2 billion in Q2 of 2015 to $11.4 billion in Q2 of 2016 for Genworth. [Press Release: Genworth

Financial Announces Second Quarter 2016 Results]

MOD8_CS2.CFM (3 MIN)

PMI AS THE ALTERNATIVE TO GOVERNMENT-SPONSORED ENTERPRISE CONTROL

Think privatization, or just supporting private enterprise over government enterprise — in this case MGIC

versus government-sponsored enterprises (GSEs) and the Federal Housing Administration (FHA).

The PMI industry is the only alternative to the FHA-provided mortgage insurance premium (MIP) for low-down

payment sales. Presently, mortgage lenders rely on private mortgage insurers to issue coverage since the FHA

only covers a minority (a number which is fortunately dropping) of mortgage originations.

PMI providers’ financial difficulties pose difficulties for getting the government out of the mortgage guarantee

business, an industry abused for three decades to artificially stimulate the economy via housing.

Although low down payment borrowers qualifying for PMI are offered various advantages (such as lower

premium rates) over borrowers covered by the FHA’s MIP, nothing creates a more stable real estate market

than skin in the game. In the long run, borrowers meeting the standard 20% down payment have a higher

stake in homeownership.

More sales volume and fees will be earned in the future with stable 20% down borrowers today. But this is a

tough sell to large media brokers with large branch office operations that need sales today to survive.

Still, government has a stake in private insurers staying in the game.

However, most lenders entirely overlook the fact that Fannie Mae and Freddie Mac are not the only guarantor

of home loans wrestling for a piece of the secondary market: PMI providers have long limited a mortgage

lender’s risk of lending to homeowners.

PMI providers may not have the capacity to insure mortgages at the premium rates lenders hope for, but then

neither did Fannie Mae or Freddie Mac.

As borrowers and lenders alike have learned, abstractedly parceling out more and more mortgages to extend

lending companies beyond their practical limits inevitably results in a backlash. It’s a matter of financial

gravity. Perhaps a private safety net for loans in the secondary mortgage market to cover defaults on riskier

mortgages will cause lenders to be more concerned with conducting business within their means.

The alternative at this point is the perpetuating of ever shakier mortgage investments as was increasingly

allowed by government and designed by Wall Street Bankers during the past 30 years – particularly those last

few leading up to the crash.

We will see how fast the conventional lenders return and whether they played a role in the return of PMI.

These events will become historically important. They are the seedlings which grow into excess mortgage

money, more relaxed conditions and an eventual, and unsustainable, run up in prices. But give it three or four

years to kick in, even if regulations place limits on the risks they all can take without endangering society and

its institutions again.

FUTURE RISKS FOR THE PMI MARKET

In its Q2 2016 results statement, MGIC referenced several risk factors which may impact its future business

prospects. [Press Release: MGIC Investment Corporation Reports Second Quarter 2016 Results]

Some of the risk factors referenced are common to the entire PMI industry, including:

the loss of market share due to competitors’ aggressive pricing;

increased use of alternatives to private mortgage insurance; and

a changes imposed on or by Fannie Mae and Freddie Mac, the government-sponsored enterprises

(GSEs).

Competitive forces

MGIC reported a high level of competition among PMI providers for new insurance business, and expects the

competition to intensify in the future. Recent strategies employed by MGIC and its competitors include:

rate reductions on BPMI premiums;

a wider range of premiums based on the risk posed by the PMI applicant, which is commonly referred

to as black-box pricing; and

discounted rates on LPMI.

The emphasis on risk-based pricing means PMI providers are pricing lower-FICO-score mortgage less favorably

than their high-FICO score counterparts. However, MGIC indicates that as competition rises, there is a chance

that they may lose business by tightening or adhering to their existing underwriting standards.

Since the majority of PMI providers write policies for loans sold to the GSEs, they cannot lower their standards

below the qualified mortgage standards followed by the GSEs. However, if mortgage volume declines, the

pressure to maintain profits by gaining market share will likely involve some form of loosening standards by

PMI providers in the future.

PMI alternatives

As discussed previously in this module, several alternatives to PMI exist, including:

government-insured or -guaranteed mortgages;

mortgages self-insured by lenders holding the mortgage in their portfolios; and

lenders structuring mortgages to avoid the need for PMI, e.g., with 80-10-10, 80-15-5 or 80-20

mortgages.

MGIC reports that the FHA’s share of low down payment residential mortgages subject to some form of

mortgage insurance is at an estimated 41% in Q1 2016, up from 40.2% in 2015 and 33.9% in 2014. While this is

showing a slight upward trend, MGIC provides some context: FHA’s share was estimated to be at a low of

15.5% in 2006 during the Millennium Boom, and at a high of 70.8% in 2009 while the mortgage market was

struggling to recover from the financial crisis.

The likelihood of a resurgence in FHA dominance is low. FHA took steps to pull back from market with

increased mortgage insurance premiums (MIPs) and premium duration several years ago.

The U.S. Department of Veterans Affairs (VA) is estimated to have a 26.3% share in low down payment

residential mortgages subject to mortgage insurance, as of Q1 2016. This share is up from 2015 when it was

24.7% and 2014 when it was 25.4%. While there are more mortgage applicants who qualify for VA-guaranteed

mortgages than in the past, the bar to eligibility will effectively limit VA-guaranteed mortgages from becoming

too big a PMI competitor.

GSE changes

The government conservatorship of Fannie Mae and Freddie Mac was initially intended to be temporary. Once

the economy stabilized, the Federal Housing Finance Agency (FHFA) was to phase out the mortgage market’s

dependency on the federal government via Fannie Mae and Freddie Mac. However, the crisis came and went,

and the GSEs remain as crucial to the mortgage market as ever. Change is possible, but MGIC indicates it is

difficult to anticipate when or even if a change in the status of the GSEs would impact PMI.

Likewise, if the GSEs were to impose stricter private mortgage insurer eligibility (net worth) requirements,

each PMI provider doing business with the GSEs would likely see a decrease in returns, as more of their assets

would have to be held in reserve. This would likely have the impact of raising premiums, or simply fewer new

PMI policies approved. The effect on the mortgage market would be a decrease in the number of low down

payment mortgages available, or an increase in government-sponsored mortgage financing.

No drastic changes are anticipated in the future, but the GSEs update the factors calculating the minimum

eligibility requirements ever two years, and has the authority to make changes to the factors at any time.