module 30 retirement planning. menu the need for retirement planning tax deferral and retirement...

TRANSCRIPT

Module 30Retirement Planning

Menu

The need for retirement planning

Tax deferral and retirement planning

Qualification of pension plans

Other retirement savings vehicles

Types of retirement vehicles

Payouts from retirement plans

Penalties for excess distributions and accumulations

Tax and other planning

The Need for Retirement Planning

Key Learning ObjectivesKey Learning Objectives IntroductionIntroduction Accumulations needed for retirementAccumulations needed for retirement

Tax Deferral and Retirement Planning

Key Learning Objectives Introduction to tax deferrals Before- and after-tax savings comparison Cost of deferral to the government Tax deferral vehicles Pension plans

Qualification of Pension Plans and other Retirement Vehicles

Key Learning ObjectivesKey Learning Objectives Exclusive benefit §401(a)(2)Exclusive benefit §401(a)(2) Nondiscrimination §401(a)(5)Nondiscrimination §401(a)(5) Participation §401(a)(3)Participation §401(a)(3) Coverage §410(b)Coverage §410(b) Vesting §401(a)(7)Vesting §401(a)(7) Distribution §401(a)(9)Distribution §401(a)(9)

Types of Plans

Key Learning Objectives (1) Defined contribution plans Defined benefit plans Combined defined benefit and contribution

plans Excess contributions Keogh (self-employed pension) plans

Defined Contribution PlansContribution is defined by specified formulaContribution is defined by specified formula

Maximum amount lesser ofMaximum amount lesser of

25% of the employee's compensation 25% of the employee's compensation

or or

$30,000 (2000), indexed for inflation$30,000 (2000), indexed for inflation Once contribution is given to the pension Once contribution is given to the pension

trustees, employer has no further financial trustees, employer has no further financial responsibility responsibility

Risk falls on the employeeRisk falls on the employee

Defined Benefit PlansBenefit is defined by specific formulaBenefit is defined by specific formula

Maximum benefit is smallest ofMaximum benefit is smallest of

* $10,000, * $10,000,

* 100% of the participant’s average * 100% of the participant’s average compensation for 3 highest paid compensation for 3 highest paid

years, ORyears, OR

* $135,000 (2000), inflation adjusted* $135,000 (2000), inflation adjusted Risk associated with investing the plan’s Risk associated with investing the plan’s

assets falls on employer not the employeeassets falls on employer not the employee

Excess Contribution

Contributions to a plan in excess of the Contributions to a plan in excess of the limits are not deductible to the employerlimits are not deductible to the employer

Trigger a 10% excise tax on the employerTrigger a 10% excise tax on the employer Excess funds can be Excess funds can be

returned to employerreturned to employer retained in plan and retained in plan and

used in future yearsused in future years

Keogh (Self-Employed Pension) Plans

No significant difference from other pension plansNo significant difference from other pension plans Net income from self-employment is substituted for Net income from self-employment is substituted for

compensationcompensation Gross income from self-employment reduced byGross income from self-employment reduced by

All normal deductions of earning that All normal deductions of earning that incomeincome

Half of the person’s self-employment taxHalf of the person’s self-employment tax The amount contributed on that person’s The amount contributed on that person’s

behalf to the Keogh planbehalf to the Keogh plan

Other Types of Plans

Key Learning Objectives (2)Key Learning Objectives (2) CODA--CODA-- Cash or deferred arrangement

§401(k)§401(k)

Tax deferred annuity §403(b) §403(b)

IRA -- IRA -- Individual retirement account §408(a)§408(a)

Cash or Deferred ArrangementsCODA--§401(k)

Allow employees to elect to defer part of their Allow employees to elect to defer part of their compensationcompensation

Vest immediatelyVest immediately Income earned by contributions tax deferredIncome earned by contributions tax deferred Tax is deferred until money is paid out of the Tax is deferred until money is paid out of the

planplan Elective deferrals may not exceed $10,500 Elective deferrals may not exceed $10,500

(2000)(2000)

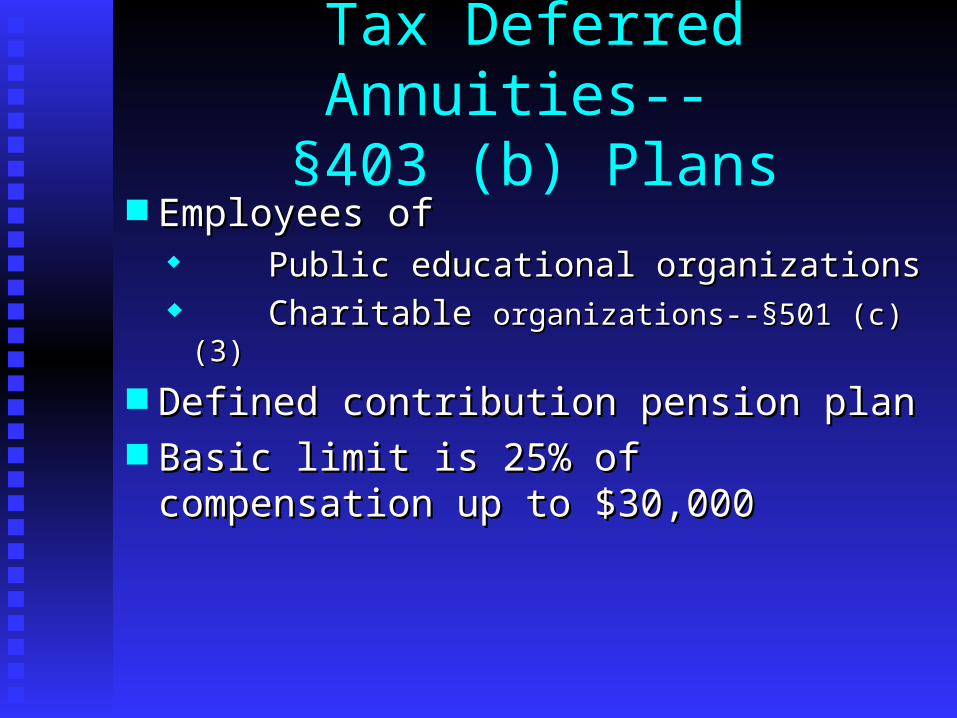

Tax Deferred Annuities-- §403 (b) Plans

Employees ofEmployees of Public educational organizationsPublic educational organizations Charitable Charitable organizations--§501 (c)(3)organizations--§501 (c)(3)

Defined contribution pension planDefined contribution pension plan Basic limit is 25% of compensation up Basic limit is 25% of compensation up

to $30,000 to $30,000

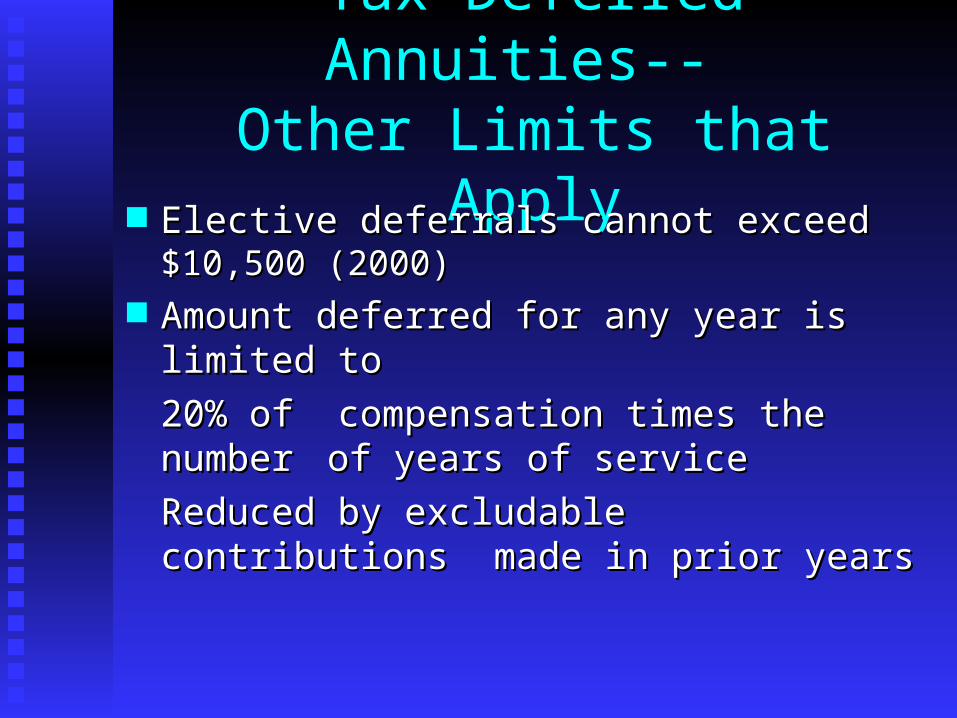

Tax Deferred Annuities-- Other Limits that Apply

Elective deferrals cannot exceed Elective deferrals cannot exceed $10,500 $10,500 (2000)(2000)

Amount deferred for any year is limited to Amount deferred for any year is limited to

20% of compensation times the 20% of compensation times the number number of years of serviceof years of service

Reduced by excludable contributions Reduced by excludable contributions made in prior yearsmade in prior years

Individual Retirement Accounts IRA--§408 (1)

Every individual with earned income is Every individual with earned income is entitled to contribute to an IRAentitled to contribute to an IRA not everyone is entitled to deduct contributionnot everyone is entitled to deduct contribution

Earnings in an IRA accrue without being Earnings in an IRA accrue without being subject to taxsubject to tax Even if contribution is not deductibleEven if contribution is not deductible

Individual Retirement Accounts IRA--§408 (1)

Maximum annual contribution is lesser ofMaximum annual contribution is lesser of the individual’s earned income orthe individual’s earned income or $2,000$2,000

Married couple--each may contribute Married couple--each may contribute $2,000 even if only one had income$2,000 even if only one had income

Individual Retirement Accounts Deductible Contribution?

May be deductible in computing AGIMay be deductible in computing AGI Deduction is limited if Deduction is limited if

Covered by qualified pension Covered by qualified pension plan ANDplan AND

AGI > base amountsAGI > base amounts determined by determined by

filing statusfiling status

The Roth IRATax now, proceeds tax free

The contribution is taxable Withdrawals (and earnings) are not taxed Must be identified as Roth IRAs when

made Maximum contribution to ALL IRAs

limited to $2,000 per taxpayer All IRA contributions must be grouped in

considering the limit

The Roth IRAFurther Limits on Contribution

The allowable contribution is reduced when the taxpayer’s AGI exceeds For single taxpayer -- $95,000. For married, filing jointly -- $150,000. For married, filing separately -- $0.

The allowable contribution is phased out proportionately over the next $15,000 of AGI

Types of Plans

Key Learning Objectives (3)Key Learning Objectives (3) SEP --SEP -- Simplified employee pension

plan §408(k)§408(k)

SIMPLE -- SIMPLE -- Savings Incentive Match Plan for Employees §408(p)§408(p)

Simplified Employee Pension Plan SEP--408(k)

Avoids the trouble and expense of setting up and maintaining a pension trust

Contribution is made to an IRA established by/or for the individual employee

Simplified Employee Pension Plan SEP--408(k)

Maximum contribution is limited to the lesser of

15 percent of compensation

or

$30,000

Simplified Employee Pension Plan SEP--408(k)

The employee can still contribute $2,000 to this or other IRAs, $4,000 if spousal IRA

BBut deductibility of this contribution may be affected by the SEP Can’t deduct a contribution to an IRA if Can’t deduct a contribution to an IRA if

covered by pension plancovered by pension plan

Savings Incentive Match Plan for Employees--SIMPLE--§408(p)

Company must have <100 employeesCompany must have <100 employees No other qualified plans allowedNo other qualified plans allowed No non-discrimination testsNo non-discrimination tests No top-heavy rulesNo top-heavy rules 100% vesting of employer 100% vesting of employer

contributionscontributions

Savings Incentive Match Plan for Employees--SIMPLE--§408(p)

Employee eligible ifEmployee eligible if

Compensation > $5,000Compensation > $5,000

In any two previous yearsIn any two previous years Employee can defer lessor ofEmployee can defer lessor of

$6,000 $6,000 or or 25% of compensation25% of compensation

Can adopt either IRA or 401(k) structureCan adopt either IRA or 401(k) structure

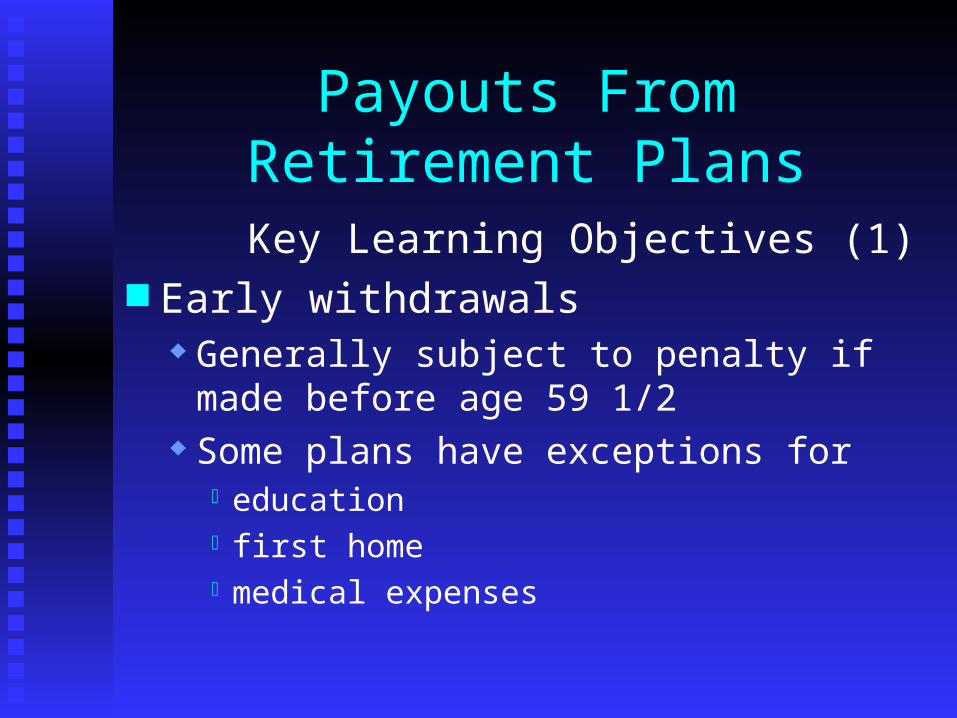

Payouts From Retirement Plans

Key Learning Objectives (1) Early withdrawals

Generally subject to penalty if made before age 59 1/2

Some plans have exceptions for education first homemedical expenses

Payouts From Retirement Plans

Key Learning Objectives (1) Rollover distributions

reinvested within 60 days to IRA New employer plan Keogh if self employed

Normal payouts from tax deferred vehicles taxed as ordinary income (unless ROTH)

Payouts from Retirement Plans

Key Learning Objectives (2)Key Learning Objectives (2) Lump-sum distributions

May be able to pay tax over 5 years Minimum required distributions

Must be made by age 701/2 (except ROTH) Penalty for not taking the required minimum

distribution

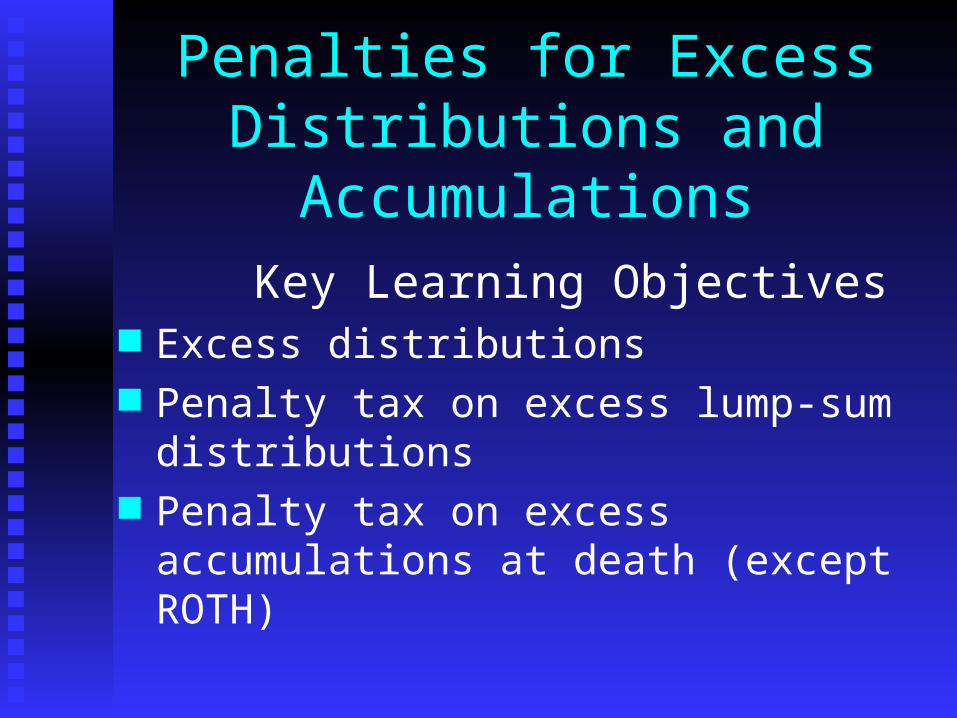

Penalties for Excess Distributions and Accumulations

Key Learning Objectives Excess distributions Penalty tax on excess lump-sum

distributions Penalty tax on excess accumulations at

death (except ROTH)

Tax and Other Planning

Key Learning ObjectivesKey Learning Objectives Using IRA as savings accountUsing IRA as savings account IRA savings benefit worksheetIRA savings benefit worksheet Should the tax on excess distributions Should the tax on excess distributions

or accumulations be avoided?or accumulations be avoided?