modelling the effects of banking sector reforms on bank...

TRANSCRIPT

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

924

www.globalbizresearch.com

Modeling the Effects of Banking Sector Reforms on Bank

Management Practices in Nigeria

Adolphus J. Toby,

Department of Banking and Finance,

Rivers State University of Science and Technology,

Rivers State, Nigeria.

E-mail: [email protected]

Daerego S. Thompson,

Department of Banking and Finance,

Rivers State University of Science and Technology,

Rivers State, Nigeria.

___________________________________________________________________________________

Abstract

This study models the effects of banking sector reforms on bank management practices in

Nigeria. Comparable data for the pre-reform period (1960-1985) and the post-reform period

(1986-2008) were generated from the Central Bank of Nigeria (CBN) Statistical Bulletin and

analyzed with descriptive and inferential statistical tools. The explanatory power of the

specified multiple regression models is robust since the average Variance Inflation Factors

(VIFs) and tolerance values confirm the non-existence of multicollinearity among the

independent variables (IVs). The descriptive statistics show steeply rising lending rates and

widening bank margins in the post-reform period. Critical bank management variables like

bank liquidity ratio (BLR) and loan-to-deposit ratio (LTDR) fell outside prudential limits,

portraying continuing compliance lapses in the post-reform period. Moreover, the liquidity

and funding capabilities of banks did not improve significantly with falling savings rates and

cash reserve ratio (CRR). In the pre-reform period, the banks adopted conservative lending

policies as the prime lending rate (PLR) became more significant in determining their

liquidity and funding profiles. In the post-reform period, bank management was aggressive in

their lending policies as the loan-to-deposit ratio was more significantly sensitive to changes

in the maximum lending rate (MLR). Both prudential and policy incentives made banks to

expand funding to all sectors irrespective of their risk class. Marginal increases in the

treasury certificate rate (TCR) and minimum rediscount rate (MRR) brought about a

significant reduction in the cash reserve ratio (CRR), hence facilitating banking

intermediation. Current reforms should, however, moderate rising lending rates, promote

prudential compliance and ensure sound financial management of the banks. Complementary

monetary policy reforms should aim at minimizing rent-seeking behaviour, moral hazards

and consequential systemic failure.

_____________________________________________________________________

Keywords: Modelling, Banking Reforms, Bank Management, Bank Performance

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

925

www.globalbizresearch.com

1. Introduction

The banking sector as an important sector in the financial services industry needs to be

reformed from time to time in order to enhance its competitiveness and capacity to play the

fundamental role of financing investment. Reforms in the banking sector are necessary to

ensure the safety of depositors‟ funds and deepen the financial system to engender growth of

the economy (Somaye, 2008; Okpara, 2011). The widespread reforms that characterized the

Nigerian banking industry in recent times are aimed at addressing weak corporate

governance, risk management, operational inefficiencies and undercapitalization for the

purpose of complying with international best practices.

The Nigerian banking industry has evolved in seven stages since its inception in 1891.

The first stage (1891-1951) was the free banking era, characterized by unregulated banking

practices and hence massive bank failures. The second phase (1952-1959) started with the

enactment of the Banking Ordinance (1952) which provided for a clear definition of banking

business, prescription of minimum capital requirements for the expatriate and indigenous

banks, maintenance of a reserve fund, adequate liquidity and banking supervision. The third

stage (1959-1985) came with the commencement of the Central Bank of Nigeria (CBN) in

June 1959. The CBN Act of 1958 incorporated all the requirements in the 1952 Ordinance

and introduced mandatory liquidity ratio in the banking business.

The fourth stage of banking sector reforms (1986-1992) was liberalization of the banking

industry that hitherto was dominated by Government-controlled banks. During this period the

banking sector suffered deep financial distress which necessitated another round of reforms

designed to manage the distress. The fifth phase (1999-2002) saw the return of liberalization,

accompanied by the adoption of distress solution programmes. The era also saw the

introduction of universal banking which empowered the banks to operate in all aspects of

retail banking and non-banking financial markets (Balogun, 2007a). The sixth phase (2004-

2008) was described as the consolidation period which focused on strengthening the financial

system through banking mergers and acquisitions, foreign exchange market stabilization,

interest rate restructuring and the pursuit of stabilization as against structural adjustment

policies for monetary and inflationary controls (Soludo, 2005).

The seventh stage also called the post-consolidation period (2008-2011) witnessed an

interplay between the adverse effects of the 207-2009 Global Financial Crisis and heavy risk-

concentrations in the previously consolidated banks. The CBN developed a blueprint for

reforming the Nigerian banking industry built around four pillars (a) enhancing the quality of

banks, (b) establishing financial stability, (c) enabling healthy financial sector evolution and

(d) ensuring the financial sector contributes to the real economy. There was also greater

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

926

www.globalbizresearch.com

emphasis on requisite disclosure, transparency and risk-based supervision (RBS) to restore

sanity in the banking system.

In 2010, the CBN introduced the new banking model aimed at withdrawing the

permission given to banks to engage in non-traditional banking activities. A bank will not be

allowed to own subsidiaries, and may also be restricted in certain geographical markets

(Mike, 2010). This will ensure that a bank concentrates and specializes in the core banking

business rather become the so-called financial supermarkets witnessed under the erstwhile

Universal Banking Programme.

Under the new model, a bank will become either commercial or merchant. A merchant

bank is required to have a minimum paid-up share capital of N15billion. A commercial bank

may be one of the three types – regional, national and international with minimum paid-p

capital requirements of N10billion, N25billion and N50billion respectively. The model also

provides for specialized banks which include primary mortgage institutions (PMIs), discount

houses, development banks, micro-finance banks (MFBs), and non-interest banks which may

be either regional or national.

A holding company model is an essential part of the new licensing structure. The primary

activity of a holding company will be to provide banking and other financial or non-financial

services depending on its regulatory authorization through its subsidiaries within the area

specified in its operating license. The assets of the holding company constitute essentially

investments in subsidiaries, which are represented by the sum of share capital and reserves on

the liability side of the balance sheet.

However, recent works on the effects of banking reforms in Nigeria have shown mixed

results. Somoye (2008) has argued extensively with empirical data that the consolidation of

the Nigerian banking industry in 2006 did not improve the overall performance of the banks

and contributed marginally to the growth of the real sector. Ubirimie (2008) using a panel

data comprising 1,153 observations of 138 Nigerian banks over the 1980-2007 period and

industry-level indices over the same period has argued that the recent banking reforms did not

significantly improve bank profitability and stability.

Azeez and Oke (2012) have equally found that banking reforms have not adequately and

positively impacted the Nigerian economy. Oputu (2010) has, however, noted that the policy

responses to the banking crisis in Nigeria emphasized the need for structural reforms in the

financial and corporate sectors, in addition to the implementation of appropriate

macroeconomic policies. Sanusi (2012) has argued that the Central Bank of Nigeria (CBN)

undertook various banking reforms to enable the banking system play its actual role of

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

927

www.globalbizresearch.com

intermediation, strengthen its growth potentials, and establish its global presence in the

international financial markets.

It is documented in Curtie (2003) that the introduction of new ownership structures,

market mechanisms and financing techniques under policies of liberalization and privatization

are not necessarily solutions without providing for changes in economic, societal and legal

infrastructure. Uppah (2011) has shown empirically that in India foreign and non-private

sector banks are much better in performance when compared to nationalized banks in the

post-banking sector reforms period. The works of Boateng and Huang (2010) have shown

that the liberalization of the Chinese banking business to foreign banks in 2003 has an

encouraging effect on the banking sector, although the evidence is not statistically significant.

At macroeconomic level, higher per capita GDP and lower unemployment have been

significantly related to better bank performance.

The major research questions, therefore, are (1) what is the effect of variations in bank

rates on bank liquidity management in Nigeria before and after the banking reforms? (2)

what is the nature of the relationship between selected central bank rates and the cash reserve

requirements before and after banking reforms? and (3) what is the effect of bank rates on

bank funding management before and after banking reforms?

In this study we test three major null hypotheses:

H01: There is no significant relationship between bank rates and bank liquidity ratio in the pre

and post reform periods.

H02: There is no significant relationship between CBN rates and cash reserve requirements in

the pre-and post-reform periods.

H03: There is no significant relationship between bank rates and loan-to-deposit ratio in the

pre-and post reform periods.

The next part of the paper review relevant literature in the contexts of Nigerian banking

reforms, the experience of other countries and the nexus between banking sector reforms and

bank performance. This is followed by the data sources, methodology and model

specification, and then results and discussion. The paper ends with summary, conclusion and

recommendations.

2. Review of Relevant Literature

The works of Balogun (2007a) review the perspectives of banking reforms in Nigeria in

five eras: pre-SAP (1970-85), the post-SAP (1986-93), the reforms Lethargy (1993-1998),

pre-Soludo (1999-2004), and Post-Soludo (2005-2006). Using both descriptive and

econometric methods, the study found that each phase of reforms culminated in improved

incentives, that policy reforms resulted in increased capitalization and exchange rate

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

928

www.globalbizresearch.com

devaluation. Interest rate restructuring and abolition of credit rationing had positive effects

on real sector credit. The empirical results confirm that eras of pursuits of market reforms

were characterized by improved incentives without necessarily increasing the credit purvey to

the real sector. Also while growth was stifled in the eras of control, the reforms era was

associated with rise in inflationary measures. Among the pitfalls of reforms identified by the

study are faulty premise and wrong sequencing of reforms and a host of conflicts emanating

from the adoption of theoretical models for reforms and above all, frequent reversals and/or

non-sustainability of reforms. The study notes the need to bolster reforms through the

deliberate adoption of policies that would ensure convergence of domestic and international

rates of return on financial market investments.

In another study, Balogun (2007b) focuses specifically on the Soludo‟s banking sector

reforms. A review of the theoretical qualifications to the Soludo‟s reform shows that in

thoughts, it is rooted in the classical traditions of Say‟s Law, acts monetarist, but expects a

Keynesian outcome that money can stimulate expansion in aggregate domestic product. In

conclusion, the study noted the need to adopt an interest rate operating procedure for

monetary policy in addition to moving the economy consciously towards the „law of one

market and one price‟ for the domestic and foreign money markets.

Earlier studies on the effects of banking sector deregulation in Nigeria found that initially

deregulation seems to enhance profits and profitability at the expense of bank liquidity and

capital adequacy (Toby, 1994). Medium-term strategy emphasized new patterns of portfolio

behaviour with greater emphasis on bank liquidity than on bank profitability. The challenges

of financial deregulation in Nigeria between 1986 and 1992 occasioned a consequential shift

in banks‟ assets and liabilities, an increasing proportion of rate-sensitive components of assets

and liabilities, and growing interest elasticity of balance sheet items (Toby, 1993). The bank

distress that followed the post-liberalization period, and the resolution measures are aptly

documented extensively in Toby (1999, 2002, 2005). Empirical results have, however, raised

the question of whether or not capital adequacy requirement affects banks‟ asset quality, and

hence limit risk concentrations in the Nigerian banking industry. The works of Toby (2005)

argue that well-capitalized banks reveal poor asset quality characteristics, while

undercapitalized banks display better asset quality in their loan portfolio.

More recent studies have revealed that the minimum liquidity ratio (MLR) was irrelevant

in controlling industry non-performing loans (npls) portfolio prior to banking consolidation in

2006 (see Toby, 2007). The cash reserve ratio (CRR) was found to be a more effective tool in

controlling the level of npls in the industry as a whole and the distressed banks in particular.

An extensive survey of X-efficiencies and scale economies in banking in the pre and post

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

929

www.globalbizresearch.com

reform periods raises a caution against the wholesome implementation of deregulation and

consolidation in developing banking systems (Toby, 2006. It is also shown that the adoption

of loose monetary policy regimes in the post-consolidation era (2006-2011) provided further

constraints on banks‟ balance sheets as banks still relied more on purchased funds to meet

liquidity and lending requirements (Toby, 2010). Toby (2011) also found that the pursuit of

consolidation and risk-based supervision (RBS) moderated npls without a corresponding

impact on liquidity and lending growth.

In terms of policy thrust the banking sector reforms are expected “to build and foster a

competitive and healthy financial system to support development and to avoid systemic

distress” (Soludo, 2007). The traditional view in general is that banking sector reforms is

encapsulated in institutional, monetary and exchange rates restructuring, and can be analyzed

via the body of their transmission mechanisms (Balogun, 2007a). The literature notes four

major channels between instruments of monetary policy and its ultimate targets (inflation

control and growth in real output). These are (i) direct interest rate effects, which affect

investment and consumption decisions, (ii) indirect effect via other asset prices, such as

prices of bonds, equities and real estate, which will influence spending through balance sheet

and cash flow effects, (iii) exchange rate effects, which will change relative prices of

domestic and foreign goals, influencing net imports, and also the value of currency

denominated assets, with resulting balance sheet effects, and (iv) credit availability effects,

which may include credit rationing if there are binding ceilings on interest rates.

It is argued that the Central Bank of Nigeria (CBN) initiates financial sector reforms to

enhance competition, reduce distortion in investment decisions, and evolve a sound and more

efficient financial system (CBN, 2011). The reforms which focused on structural changes,

monetary policy, interest rate administration and foreign exchange management, encompass

both financial market liberalization and institutional building in the financial sector.

The works of Toby (2006) show that the liquidity management practices of Nigerian

banks were at variance with monetary policy targets both in times of “intense” deregulation

and “guided” deregulation. The evidence confirms that a reduction in the cash reserve

requirement necessitated an increase in average bank liquidity and a paradoxical decline in

aggregate credit to the economy. The study also shows that interest rates moderated in times

of “guided” deregulation with commercial banks playing a dominant role in the Certificate of

Deposit (CD) and Commercial Paper (CP) markets.

In the post-global crisis era (2007-2009), the emphasis was on loose monetary policy

direction in the medium-term (Toby, 2010). However, Mora (2010) found that the bank-

centred nature of the crisis made it harder than in the past for banks to attract deposit and

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

930

www.globalbizresearch.com

provide liquidity to borrowers shut out of securities markets. Saxegaard (2006) examines the

pattern of excess liquidity in Sub-Saharan Africa and its consequences for the effectiveness of

monetary policy. The study suggests that excess liquidity weakens the monetary transmission

and thus the ability of monetary authorities to influence the demand conditions in the

economy.

Ziorklui (2001) has argued that many developing countries embarked on financial sector

reforms to remove the vestiges of financial market repression in order to promote financial

market efficiency and savings mobilization. Ziorklui reviews in-depth with policy

implications, Ghana‟s financial sector reform, the Financial Institutions Sector Adjustment

Programme (FINSAP) to address the endemic problems of Ghana‟s financial sector. The

efficiency of financial markets in promoting financial deepening and savings mobilization of

financial resources is widely recognized in the literature (McKinnon, 1973; Shaw, 1973).

McKinnon postulates that an increase in holding financial assets (financial deepening) by the

public promotes savings mobilization which leads to higher levels of savings, investment,

production, growth and poverty alleviation. However, financial market intervention by

governments in developing countries constrains the potential of financial markets in

mobilizing savings for growth and development.

The major objectives of financial sector reforms in developing economies include market

liberalization for the promotion of more efficient resource allocation, expansion of savings

mobilization base, promotion of investment and growth through market-based interest rates

(Omoruyi, 1991). It is argued that the reform of the banking sector is imperative to enable it

play a key role in primary and trading risks and implementing monetary and fiscal policies

(Balogun, 2007a). In this vein, banking reforms are expected to address the issues which

mitigate the efficiency of the banking sector such as “shallow depths of the capital market,

dependence of financial sector on public sector and foreign exchange trading as sources of

funding, apparent lack of harmony between fiscal and monetary policies and above all, poor

loans repayments performance as well as bad debts” (Ojo, 2005; Nnanna, 2005).

Many studies have reviewed the impact of the post-reform period on the performance of

banking institutions in India. Ahluwalia (2002) has argued that the deregulation of the Indian

banking industry has some positive outcomes such as a fall in the share of non-performing

loans, increased entry of new private sector banks, branch expansion or financial widening as

well as deepening, and the achievement of the minimum capital adequacy ratio by 90 per cent

of domestic banks. More et al (2006) have shown strong evidence that the sharp increase in

growth post 1994 was bank credit-led. There is, however, the general perception that public

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

931

www.globalbizresearch.com

sector involvement in the banking sector blunts incentives to effectively respond to market-

based reforms (Bhattacharya and Patel, 2003; Kumbhakar and Subrata, 2003).

Price-setting behaviour may be endogenous not just to market structure, but also to size

and deregulation. Interest rate deregulation may lead to an increase in bank funding costs and

a fall in bank profitability. This could be countered through an increase in the number and

price of services offered by banks (Humphey and Pulley, 1997) a strategy that is easier for

larger banks to effect. This is consistent with a fall in spreads for large banks with high non-

interest expenditure and incomes.

Kumbhakar et al (2001) study whether and how deregulation, assumed to generate

increased competition, affected the profitability of Spanish savings banks between 1986 and

1995. Their panel study uses a flexible variable profit function and incorporates time-varying

technical efficiency, high rates of technical progress and increasing trend growth in

productivity.

Liberalization of volume and interest rates has been observed to raise profitability in the

banking sectors of Norway (Berg, et al, 1992) and Turkey (Zaim, 1995). Berger and

Humphrey (1997) have noted that the effects of deregulation may depend on industry

conditions prior to reform and on the type of measures implemented. There is also empirical

evidence that shows a decline in cost productivity immediately after deregulation (Berger and

Mester, 2003; Humphrey and Pulley, 1997), though improved output and quality of output

led to higher profit productivity (Berger and Mester, 2003). A number of studies for US

banks suggest that liberalization of deposit rates has little or no effect (Bauer, et al, 1993);

Hughes et al (1996) and Jayaratne and Strahau (1998) find that geographical expansion has

affected profitability in the U.S.

2.1 Nexus between Banking Sector Reform and Bank Performance

Brissimis et al (2008) examine the relationship between banking sector reform and bank

performance-measured in terms of efficiency, total factor productivity growth and net interest

margin-accounting for the effects through competition and bank risk-taking. The results

indicate that both banking sector reform and competition exert a positive impact on bank

efficiency, while the effect of reform on total factor productivity growth is significant only

towards the end of the reform process. Brissimis et al also found that the effect of capital and

credit risk on bank performance is in most cases negative, while it seems that higher liquid

assets reduce the efficiency and productivity of banks.

Three interrelated determinants of bank performance are extensively reviewed in the

literature and these include the financial reform process, the degree of competition and the

risk-taking behaviour of banks (Brissimis et al, 2008). The leading works of Keeley (1990)

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

932

www.globalbizresearch.com

argue that the deregulation of the US banking sector in the 1970s and 1980s increased

competition and led to a reduction in monopoly rents and thus, through worsened

performance, to a higher equilibrium risk of failure. The Keeley‟s paradigm has provoked a

number of studies examining the relationship between deregulation, bank risk-taking and

competition, yielding rather conflicting results (Matutes and Vives, 2000; Bolt and Tieman,

2004; Allen and Gale, 2004). One group concludes that deregulation boosts efficiency

through operational savings, thus leading to a surge in productivity growth (Kumbhakar et al,

2001; Isik and Hassan, 2003). The alternate group found that deregulation has a negative

effect on the performance of banks, as it stimulates a decline in productive efficiency and/or

total factor productivity growth (Griefell-Tatje and Lowell, 1996; Whealock and Wilson,

1999).

In the econometric contributions of Simar and Wilson (2007) and Khan and Lewbal

(2007), bank performance, measured in terms of productive efficiency (PE) and total factor

productivity (TFP) growth, is derived via nonparametric techniques and then the scores

obtained are linked to reform, competition and bank risk-taking. In this context, Brissimis et

al (2008) have specified the following empirical model to study the relationship between the

performance, reform, competition and risk-taking in banking.

(1) Pit = 1 + 1refc + 2i + 3xit + 4mt + it

where the performance P of bank i at time t is written as a function of a time-dependent

banking-sector reform variable, reft, an index of banking industry market power, ; a vector

of bank-level variables representing credit, liquidity and capital risk, x; variables that capture

the macroeconomic conditions common to all baks, m; and the error term, . The

methodology suggested by Uchida and Tsutsui (2005) has been widely used to measure the

evolution of competitive conditions over time in the banking system. The model jointly

estimates a system of three equations that correspond to a translog cost function, to a revenue

equation obtained form the profit maximization problem of banks and to an inverse loan

demand function:

InCit = bo + b1 Inqit + ½ b2 (Indit)2 + b3 Indit + ½ b4 (Indit)

2 + b5Inwit + ½ b6 (Inwit)

2 + b7 (Inqit)

(Inwit) + b8 (Inqit) (Indit) + b9 (Indit) (Inwit) + ecit

(2) Rit = c Rit + rit qit + Cit (b1+b2 Inqit + b7 Inwit + b8 Indit + Cit qit (b3+b4 Indit + b8

Inqit + b9 Inwit)

Ht dit

+ esit

In Pit = go – (1/t) Inqit + gi Ingdpgt + g2 Iniri + eit

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

933

www.globalbizresearch.com

Where C is the total cost of bank I at time t, q is bank output, ds are deposit, w is bank

output other than deposits, R is bank revenue, r is the interest rate on deposits, p is the price of

bank output and e is the error term. Variables with bars are defined as deviations from their

cross-sectional means in each time period, so as to remove their trends. The variable gdpg

and ir are exogenous variables that affect demand. The degree of competition in each year is

given by, which represents the well-known conjectural variations elasticity of total industry

output with respect to the output of the ith bank.

3. Data Sources, Methodology and Model Specification

The data for this study were generated from the Central Bank of Nigeria (CBN) Statistical

Bulletin and NDIC Annual Reports for the period 1960-2008. The pre-reform period (1960-

1985) was distinguished from the post-reform period (1986-2008). Both dependent and

independent variables were identified. The major dependent variables are bank liquidity ratio

(BLR), cash reserve ratio (CRR) and loan-to-deposit ratio (LTDR). The independent

variables include both bank and VBN rates. The bank rates in this study are savings rate

(SR), prime lending rate (PLR) and maximum lending rate (MLR). The CBN rates are

minimum re-discount rate (MRR), treasury bills rate (TBR) and treasury certificates rate

(TCR).

The first level of analysis involves the calculation of simple averages and standard

deviations for critical bank management and performance indicators in the pre- and post

reform periods, with some highlights on the liberalization and consolidation periods in

selected intervening years. The liberalization period is 1986-92, while the early years of

consolidation are from 2006 to 2008. The second level of analysis involves the specification

of the multiple regression models for inferential purposes to test the research hypotheses.

3.1 Model specification

The multiple regression models specified and tested in this study are given in equations 3-5:

(3) BLR = + 1SR + 2PLR + 3 MLR + i

(4) CRR = + 1MRR+ 2TBR + 3 TCR + i

(5) LTDR = + 1SR + 2TBR + 3 TCR + i

For our given set of data, the values of the alpha () and beta () coefficients can be

determined mathematically to minimize the sum of squared deviations between predicted

dependent variable and the actual dependent variable scores. In this study we employed the

Software Package for Social Sciences (SPSS) to estimate the relevant variables and

parameters in the specified equations. The package provided us with multiple correlation

coefficient (R), t-test, F-ratio and coefficient of determination (R2). Our null hypothesis will

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

934

www.globalbizresearch.com

be accepted if the t-statistic falls within the relevant critical values, otherwise it will be

rejected. The model is significant if the F-ratio falls outside the critical region, otherwise it is

not significant.

Within the framework of the classical linear regression model (CLRM), the specified

multiple regressions models assume the absence of multicollinearity. Multicollinearity means

that within the set of independent variables (IVs) some of the IVs are nearly or totally

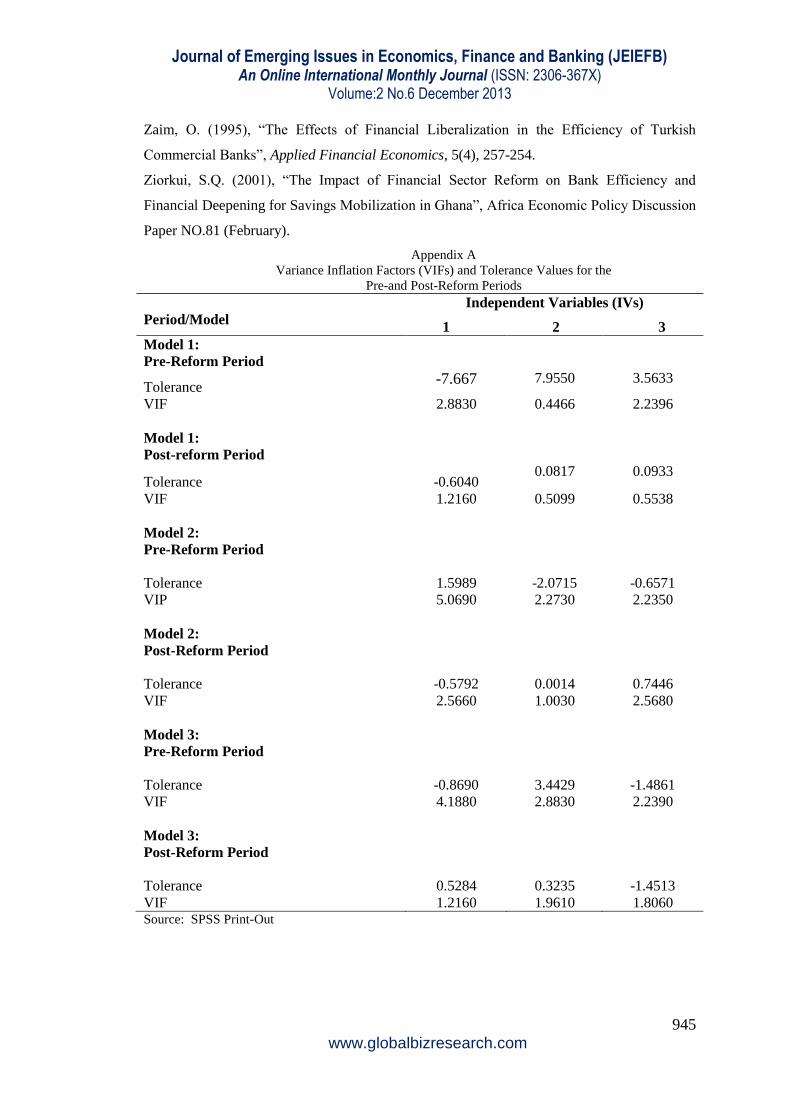

predicted by the other IVs. In this study, we estimated the condition index, variance inflation

factors (VIFs) and tolerance values.

As noted in the literature, if the condition index (CI) is between 10 and 30, there is

moderate to strong multicollinearity and if it exceeds 30, there is moderate to severe

multicollinearity (Belsley et al, 1980). As a rule of thumb, if the Variance Inflation Factor

(VIF) of a variable exceed 10 (this will happen if R2 exceeds 0.90), that variable is said to be

highly collinear (Kleinbaum, et al, 1988). The tolerance values should not be close to zero.

4. Results and Discussion

4.1 Collinearity Diagnostics

The tests of multicollinearity are found in Appendixes A and B. On the average the

Variance Inflation Factors (VIFs) have values of less than 10. Moreover, the tolerance values

are not close to zero in most of the cases. A rule of thumb is to label as large these condition

indices in the range of 30 or larger. We find that this condition is not met for any of the IVs.

Although in some cases we could find large proportions of variance (0.50 or more), they did

not correspond to large condition indices (30 or more). The absence of multicollinearity

among the IVs means that the explanatory powers of our models are robust.

4.2 Descriptive Statistical Analysis

The data in Table 1 show selected monetary policy and bank management indicators in

the pre and post-reform periods. The results also show the average changes in these

indicators in the liberalization and consolidation periods. The average savings rate increased

from 8.0% in the pre-form period to 9.41% in the post-reform period. Average savings rate

peaked at 11.09% in the liberalization period, and began a downward trend after the banking

consolidation which commenced January 1, 2006. In 2011, average savings rate dropped to

an all-time low of between 2.00-2.5%.

While average savings rate began a downward trend between the liberalization period and

the post-consolidation era, the prime lending rate has witnessed a pronounced rising trend

from 20.54% in the liberalization period to 34.43% in the consolidation period. Generally,

the average prime lending rate rose steeply from 9.95% in the pre-reform period to 23.77% in

the post-reform period. The same upward trend is noticed in the average maximum lending

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

935

www.globalbizresearch.com

rate from 11.6% in the pre-reform period to 27.41% in the post-reform period. The average

MLR rose from 23.34% in the liberalization period to 38.41% in the consolidation period.

The average bank margin increased from 3.6% in the pre-reform period to 14.19% in the post-

reform period.

The bank liquidity ratio (BLR) declined from 52.76% in the pre-reform period to 49.30%

in the post-reform period, showing glaring deviations from the stipulated minimum liquidity

ratio of 35-4-%. The consolidation era recorded an average bank liquidity ratio (BLR) of

47.50% still above the repeated prudential target. The average cash reserve ratio (CRR)

declined from 8.61% in the pre-reform period to 6.10% in the post-reform era. The average

CRR dropped to 2.54% in the consolidation period. The loan-to-deposit ratio (LTDR)

declined from 74.37% in the pre-reform period to 66.82% in the post-reform period.

However, LTDR peaked at 83.9% on the average in the early years in the early years of the

consolidation period, showing another prudential breach above the regularly maximum of

80.0%. Specifically, prudential compliance improved marginally from 27.76% in the pre-

reform period to 22.55% in the post-reform period. However, prudential breaches were more

evident in the early years of banking consolidation (29.83%). Prudential compliance is

measured by the difference between actual and prescribed financial ratios as published by the

Central Bank of Nigeria. The wider the gap, the lower the level of compliance.

The standard deviation () shows that the bank liquidity ratio (BLR) was more variable in

the pre-reform period ( = 7.8152) than it is in the post-reform period ( = 5.0642). The cash

reserve ratio (CRR) also showed greater variability in the pre-reform period (( = 2.5623)

than in the post-reform period ( = 1.7498). However, the loan-to-deposit ratio was more

variable in the post-reform period ( = 6.5880) than in the pre-reform period.

Table 1: Average Monetary Policy and Bank Management Indicators (Pre and Post Reform Eras)

S/N Bank Performance Indicator Pre-Reform

Period

Liberalization

Period

Consolidation

Period

Post-Reform

Period

1 Savings Rate (SR) 8.00 11.09 7.04 9.41

2 Prime Lending Rate (PLR) 9.95 20.54 34.43 23.77

3 Maximum Lending Rate (MLR) 11.6 23.34 38.41 27.27

4 Bank Margin (%) 3.6 8.12 31.37 14.19

5 Bank Liquidity Ratio (BLR) 54.26 44.98 47.5 49.30

6 Cash Reserve Ratio (CRR) 8.61 6.02 3.54 6.10

7 Loan-to-Deposit Ratio (LTDR) 74.37 65.88 83.92 66.82

8 Prudential Compliance (PCR) 27.76 19.98 29.83 22,55

S.D. () for pre-reform period: BLR (7.8152), CRR (2.5623) & LTDR (3.3498)

S.D. () for post-reform period: BLR (5.0642), CRR (1.7498) & LTDR (6.5889)

Sources: Author‟s Calculations based on the CBN Statistical Bulletin (1960-2008)

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

936

www.globalbizresearch.com

4.3 Inferential Results

The inferential results in Table 2 (Model 1) reveal the beta and correlation coefficients,

including the relevant t-test statistics in the pre-reform period. Changes in average savings

rate provided a negative sensitivity to changes in bank liquidity ratio (BLR). The beta

coefficient of -0.7608 shows that as the savings rate rises by 100%, we should expect the

bank liquidity ratio to fall by 76.08% and vice-versa. The association between SR and BLR

is extremely weak both in terms of overall correlation and partial correlation coefficient.

However, the negative beta coefficient is significant at the 5% level since the computed t-test

of -1.8940 falls outside the H0 acceptance region of 0.0714.

A beta coefficient of 0.5603 shows that as the prime lending rate (PLR) rises by 100%,

we should expect the computed t-test of 1.681 falls outside the acceptance region of 0.1068.

The beta coefficient of 0.2931 shows that as the maximum lending rate (MLR) rises by 100%,

the banks‟ liquidity ratio (BLR) rises by just 29.31%. In this case the beta coefficient is still

significant at the 5% since the t-test of 0.9980 falls outside the H0 acceptance region of

0.3291.

Table 2: Effects of Banking Reforms on Selected Bank Management Ratios in the Pre-Reform Period

Model/Variables Beta

Coefficient

SE Beta

Corr. Part.

Corr.

t-test

Sig.t (5%)

Model 1 (DV* BLR)

SR -0.7608 0.4016 -0.0901 -0.3718 -1.8940 0.0714

PLR 0.5603 0.3332 0.1192 0.3300 1.6510 0.1068

MLR 0.2931 0.2937 0.0591 0.1959 0.9980 0.3291

Model 2 (DV**CRR)

TCR 0.2940 0.4452 -0.2531 0.1006 0.6610 0.5158

TBR -0.4516 0.8902 -0.3506 -0.1802 -0.5070 0.6170

MRR -0.1642 0.9111 -0.3416 -0.3562 0.1800 0.8587

Model 3 (DV***LTDR)

SR -0.1001 0.0209 -0.0489 -0.2340 0.8173

PLR 0.2815 0.1158 0.1658 0.7930 0.4364

MLR -0.1431 0.05679 -0.0956 -0.4570 0.6520

SR: Saving Rate PLR: Prime Lending Rate MLR: Maximum Lending Rate TCR: Treasury

Certificate Rate TBR: Treasury Bills Rate MRR: Maximum Rediscount Rate DV: Dependent

Variable

Source: SPSS Print-Out

The Table 2 (Model 2) results show the relationship between CBN rates and the cash

reserve ratio in the pre-reform period. The beta of 0.2940 shows that as the treasury

certificate rate (TCR) rises by 100%, we should expect the cash reserve ratio (CRR) to rise by

29.40%. This relationship is significant at the 5% level since the t-test of 0.6610 falls outside

the H0 acceptance region of 0.5158. The treasury bill rate (TBR) is not significantly related to

the CRR at the 5% level since the computed t-test of -0.5070 falls within the H0 acceptance

region of 0.6170. The MRR is not significantly related to the CRR.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

937

www.globalbizresearch.com

The nature of the relationship between bank rates and loan-to-deposit ratio (LTDR) in the

pre-reform period is summarized in Table 2 (Model 3). The beta coefficient (-0.1001) for

saving rate (SR) and LTDR is not significant at the 5% level since the computed t-test of -

0.2340 falls within the critical region of 0.8173. The maximum lending rate (MLR) is

insignificantly related to the LTDR at the 5% level since the computed t-test of -0.4570 falls

within the acceptance region 0.6520. However, with a beta-coefficient of 0.2815, we find

that a 100% increase in the prime lending rate (PLR) results to a 28.15% increase in LTDR

and vice-versa. The beta coefficient is significant since the calculated t-test of 0.7930 falls

outside the critical region of 0.4364.

In the post-reform period, savings rate continues with a negative beta coefficient of -

0.6610

Table 3 (Model 1). This indicates that as savings rate rises by 100%, we should expect

the bank liquidity ratio to fall by 66.1%. The beta coefficient is significant at the 5% level

since the computed t-test of -3.3030 falls outside the H0 acceptance region of.0.0037. In the

case of the prime lending rate (PLR), a beta coefficient of 0.0908 shows that a 100% increase

in the PLR brings about an insignificant increase of 9.08% in bank liquidity ratio (BLR) at the

5% level. Similarly a beta coefficient of 0.0996 shows that a 100% rise in maximum lending

rate (MLR) produces an insignificant rise in bank liquidity ratio of 9.96% at the 5% level.

The t-test of 0.4090 falls within the H0 acceptance region of 0.6874.

The relationship between CBN rates and cash reserve ratio (CRR) in the post-reform

period is shown in Table 3 (Model 2). The selected CBN rates show beta coefficients of -

0.6570 (TCR), 0.1042 (TBR) and 0.7989 (MRR). As the treasury certificate rate (TCR)

increases by 100%, we should expect the cash reserve ratio (CRR) to fall by 65.70% and vice-

versa. This inverse relationship between TCR and CRR is significant at the 5% level since

the computed t-test of 0.6610 falls outside the region of . The Treasury bill rate (TBR) is not

significantly related to the cash reserve ratio (CRR) at the 5% level since the t-test of 0.5270

falls within the H0 acceptance region of 0.6046.

As the minimum rediscount rate (MRR) increases by 100%, we should expect the cash

reserve ratio (CRR) to rise by 79.89%. This positive relationship is significant at the 5% level

since the computed t-test of 2.5230 falls outside the critical region of 0.0207.

The significant determinants of the LTDR in the post-reform period are summarized in

Table 3 (Model 3). The savings rate is not significantly related to the LTDR at the 5% level

since the computed t-test of 0.1490 falls within the H0 acceptance region of +0.8833.

However, both PLR and MLR are significantly related to LTDR at the 5% level of

significance since the computed t-test falls outside the critical H0 acceptance region. The PLR

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

938

www.globalbizresearch.com

is negatively sensitive to LTDR, with a correlation coefficient of -0.3472. With a correlation

coefficient of 0.6475, we find a significantly positive association between MLR and LTDR,

and this is significant at the 5% level.

Table 3: Effects of Banking Reforms on Selected Bank Management Ratios in the Post-Reform Period

Model/Variables Beta

Coefficient

SE Beta

Corr.

Part.

Corr.

t-test

Sig.t (5%)

Model 1 (DV* BLR)

SR -0.6610 0.2001 -0.5910 -0.5993 -3.3030 0.0037

PLR 0.0908 0.2541 -0.1190 0.0648 0.3570 0.7249

MLR 0.0996 0.2438 -0.0526 0.0741 0.4090 0.6874

Model 2 (DV**CRR)

TCR -0.6570 0.3165 -0.0377 -0.4101 -2.0750 0.0518

TBR 0.1042 0.1979 0.0920 0.10406 0.5270 0.6046

MRR 0.7989 0.3167 0.2801 2.5230 2.5230 0.0207

Model 3 (DV***LTDR)

SR 0.0284 0.1906 -0.1543 0.0257 0.1489 0.8833

PLR 0.1408 0.2420 -0.3472 1.0056 0.5820 0.5675

MLR -0.7503 0.2323 0.6473 -0.5583 -3.2300 0.0440

SR: Saving Rate PLR: Prime Lending Rate MLR: Maximum Lending Rate TCR: Treasury

Certificate Rate TBR: Treasury Bills Rate MRR: Maximum Rediscount Rate DV: Dependent

Variable

Source: SPSS Print-Out

The model summaries are found in Table 4. The coefficient of determination (R2)

increased significantly from 0.1526 in the pre-reform period to 0.3746 in the post-reform

period. The explanatory power of the selected bank rates (SR, PLR and MLR) improved

significantly with the introduction of several banking reforms. Specifically, a 100% change

in the Deposit Money Banks‟ rates brought about a 15.26% change in the bank liquidity ratio

(BLR) in the pre-reform period. However, the same change in the bank rates brought about a

37.46% variation in the BLR in the post-reform period.

The CBN rates affected the cash reserve ratio (CRR) more significantly in the post-

reform period than the pre-reform period. R2 increased from 0.1400 in the pre-reform period

to 0.2581 in the post-reform period. The variation in the LTDR was not significant with a

significant change in the bank rates in pre-reform period. With a coefficient of determination

(R2) of 0.0378, the computed F-ratio of 0.2880 fell within the critical region of 0.8340.

However, in the post reform period, a 100% change in the bank rates brought a 43.24%

variation in the LTDR.

Table 4: Effects of Banking Reforms on Bank Management Practices:Model Summaries

Model Summary Pre-Reform Post-Reform

Model 1 with BLR*

MultR 0.3907 0.6120

R2 0.1526 0.3746

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

939

www.globalbizresearch.com

Adj. R2 0.0371 0.2758

F-Ratio 1.3210 3.7930

Sig. F 0.2930 0.0280

Model 2 with CRR**

MultR 0.3742 0.5081

R2 0.1400 0.2581

Adj. R2 0.0227 0.1410

F-Ratio 1.1940 2.2040

Sig. F 0.3350 0.1210

Model 3 with LTDR***

MultR 0.1944 0.6575

R2 0.0378 0.4324

Adj. R2 -0.0934 0.3427

F-Ratio 0.2880 4.8240

Sig. F 0.8340 0.0120

* Model 1: BLR = + 1 SR +2 PLR + 3 MLR + i

** Model 2: CRR = + 1 MRR +2 TBR + 3 TCR+ i

*** Model 3: LTDR = + 1 SR +2 PLR + 3 MLR + i

5. Summary, Conclusion and Recommendations

Based on description statistics, major lending rates (PLR & MLR) showed an upward

trend from the pre-reform period to the post-reform period. The average bank margin

increased form 3.6% in the pre-reform period to 14.19% in the post-reform period. The

average bank liquidity ratio (BLR) exceeded the prudential limits in the pre- and post-reform

periods, although the prudential breach was more pronounced in the pre-reform period. The

loan-to-deposit ratio (LTDR) peaked at 83.92% in the early years of the consolidation period,

showing another prudential breach above the regulatory maximum of 80.0%.

The bank rates significantly affected the bank liquidity ratio (BLR) in the pre-reform

period. In the post-reform period, the savings rate affected the BLR significantly, but

negatively at the 5% level. Both the prime lending rate (PLR) and the maximum lending rate

(MLR) were insignificant in determining variations in the BLR in the post-reform period.

The treasury certificate rate (TCR) was significantly related to the cash reserve ratio (CRR) in

the pre-reform period. However, the treasury bill rate (TBR) and the minimum rediscount

rate (MRR) were not significantly related to CRR. In the post reform period, both TCR and

MRR were significantly related to CRR.

In the pre-reform period, the prime lending rate (PLR) was more significantly related to

the loan-to-deposit ratio (LTDR). However, in the post-reform period paid, the maximum

lending rate (MLR) was more significantly related to LTDR. The explanatory powers of the

bank rates in determining the bank liquidity ratio (BLR) and the loan-to-deposit ratio (LTDR)

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

940

www.globalbizresearch.com

were more significant in the post-reform period than in the pre-reform period. The variation

in the bank rates did not lead to any significant variation in the LTDR in the pre-reform

period. The CBN rates affected the cash reserve ratio (CRR) more significantly in the post-

reform period than the pre-reform period.

Recent banking reforms have failed to curb the rising cost of funds in Nigeria. Although

savings mobilization has been emphasized, most banks have boosted their liquidity ratios

based on sources other than savings. The level of prudential compliance has not improved

drastically. Both bank liquidity ratio (BLR) and loan-to-deposit ratios have always exceeded

their prudential limits, particularly in times of intense reforms. However, bank management

has always recorded significantly rising margins and profitability, even in the face of

increasing compliance lapses.

Under regimes of increasing treasury certificate rates (TCR) and minimum rediscount rate

(MRR) we should expect the cash reserve ratio to fall, thereby enabling banks to create more

credit. The significant beta coefficients in the post reform period are indicative of progressive

central banking activities aimed at boosting the real sector.

Most bankers were more conservative in lending during the pre-reform period as the

prime lending rate (PLR) manifested a significant beta relationship with the loan-to-deposit

ratio (LTDR). The preferred borrowers dominated their loans portfolio apparently because of

their tolerable risk class. In the post-reform period, bank management became more

aggressive in lending irrespective of the risk class. The beta coefficient of the maximum

lending rate (MLR) is significantly correlated to LTDR, and could explain the rising risk

concentrations in the post-reform period, particularly after the liberalization of the banking

industry. The multiplicity of specialized and CBN-guaranteed facilities to SMEs and

agriculture did not curb bankers‟ risk appetite in boosting their risk assets portfolio.

Extensive monetary policy reforms could have resulted in the more significant

explanatory powers of both bank and CBN rates in determining bank management practices.

The cumulative effect of bank rates on bank liquidity ratio and the loan-to-deposit ratio could

portray the pursuit of aggressive monetary policy regimes in the post-regime period. Bank

management, however, remained insensitive to prudential standards. The current risk-based

supervisory framework should be sustained with emphasis on Basel III and IFRS compliance

issues. Monetary policy reforms should aim at minimizing rent-seeking behaviour, moral

hazards and consequential systemic failure. The monetary policy rate (MPR) should narrow

bank margins while minimizing the risk of insolvency. Current reforms should moderate

rising lending rates, keep liquidity and funding within prudential limits, and enhance sound

financial management of the banks.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

941

www.globalbizresearch.com

References

Ahluwalia, M.S. (2002), “Economic Reforms in India Since 1991: Has Gradualism

Worked?”, Journal of Economic Perspectives, 16(3), 11-28.

Allen, F. and Gale, D. (2004), Competition and Financial Stability”, Journal of Money, Credit

and Banking, 36(4), 453-480.

Azeez, B. A. and Oke, M.O. (2012), “A Time-Series Analysis on the Effect of Banking

Reforms on Nigeria‟s Economic Growth”, International Journal of Economic Research, 3(4),

26-37.

Balogun, E.D. (2007a), “A Review of Soludo‟s Perspective of Banking Sector Reforms in

Nigeria”, MPRA, http://mpra.uso uni-muechen.de/3803/Accessed 2/6/2009.

Balogun, E.D. (2007b), “Banking Sector Reforms and the Nigerian Economy: Performance,

Pitfalls and Future Policy Options” Munich Personal RePPc Archive (MPRA),

http://mpra.uni-ucnchen.de/3804/Accessed 2/6/2009.

Bauer, P.W. Berger, A.N. and Humphrey D.B. (1993), “Efficiency and Productivity Growth

in U.S Banking”

In The Measurement of Productive Efficiency: Techniques and Applications, edited by H.O.

Fried, C.A. Lovell and S.S. Schmidt, pp.386-413. Oxford: Oxford Univ. Press.

Belsey, D.A. Kuh, E. and Wetsch, R.E. (1980), Regression Diagnostics: Identifying

Influential Data and Sources of Collinearity, John Wiley & Sons, New York.

Berger, S.A., Forsound, F.R. and Jansen, E.S. (1992), “Malmquist Indices of Productivity

Growth During the Deregulation of Norwegian Banking, 1980-89”, Scandinavian Journal of

Economics, 94(2), 211-228.

Berger, A.N. And Humphrey, D.S. (1992), “Measurement and Efficiency Issues in

Commercial Banking”. In Output Measurement in the Service Sectors, Studies in Income and

Wealth, 56, edited by Z. Grilichers, 249-279. Chicago: The University of Chicago Press for

National Bureau of Economic Research.

Berger, A. N. and Mester, I.J. (2003), Explaining the Dramatic Changes in Performance of

U.S. Banks: Technological Change, Deregulation, and Dynamic Changes in Competition,”

Journal of Financial Intermediation, 12(2), 57-95.

Bhattacharya, S. and Patel, U. (2003), “Reform Strategies in India”, Conference on India’s

and China’s Experience with Reforms and Growth, 2013.

Boateng, A. and Huang, W. (2012), “Banking Sector Reforms and Commercial Bank

Performance in China,”Available at SSRN:http://ssrn.com/abstracts=1663680. Accessed

23/8/2011.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

942

www.globalbizresearch.com

Bolt, W. and Tienan, A.F. (2004), “Bank Competition, Risk and Regulation,” Scandinavian

Journal of Economics, 106(1), 783-804.

Brissimis, S.N., Delis, M.D. and Papanikolaou, N.I. (2008), “Exploring the Nexus between

Banking Sector Reform and Performance: Evidence from Newly Acceded EU Countries”,

Bank of Greece Working Paper, No.78, 1-38.

Central Bank of Nigeria (2011), Monetary Policy, Available at

http://www.cenbank.org/Monetary Policy/Reforms.asp Accessed 10/10/2011.

Currie, C. (2003), “The Need for a New Theory of Economic Reform”, University of

Technology, Sydney School of Finance and Economics Working Paper No.131, 1-14, Also

available at http://www.business,uts.edu.au/finance/Accessed 1/10/2011.

Grifell-Tatje, E., and Lovell, C.A.K. (1996), “Deregulation and Productivity Decline: The

Case of Spanish Savings Banks”, European Economic Review, 40(2), 1281-1303.

Hughes, J.P., Joseph, P.W. Mester, L.J. and Moon, C. (1996), “Efficient Banking under

Interstate Branching,” Journal of Money, Credit and Banking, 28(4), 1045-1071.

Humphrey, D.B. and Pulley, L.B. (1997), “Banks‟ Responses to Deregulation: Profits,

Technology, and Efficiency”, Journal of Money, Credit and Banking, 29(1), 73-93.

Isik. I. and Hassan, M.K. (2003), “Financial Deregulation and Total Factor Productivity

Change: An Empirical Study of Turkish Commercial Banks”, Journal of Banking and

Finance, 27(2), 1455-1485.

Jayaratne, J. and Strahan, P.E. (1998), “Entry Restrictions, Industry Evolution, and

Efficiency: Evidence from Commercial Banking”, Journal of Law and Economics, 41(1),

239-273.

Kelley, M.C. (1990), “Deposit Insurance, Risk, and Market Power in Banking”, American

Economic Review, 80(2), 1183-1200.

Khen, S. Lewbel, A. (2007), “Weighted and two-stage Least Squares Estimation of

Semiparametric Truncated Regression Models”, Econometric Theory, 23(4), 309-347.

Kleinbaum, D.G. Kupper, L.L. and Muller, K.E. (1988), Applied Regression Analysis and

Other Multivariate Methods PWS – Kent, Boston, Mass.

Kumbhakar. S.C. Lozaro-Fivas, A. Lovell, C.A.K.; Hassan, I. (2001), “The Effects of

Deregulation on the Performance of Financial Institutions: The Case of Spanish Savings

Banks”, Journal of Money, Credit and Banking, 33(3), 101-120.

Kumbhakar, S.C. and Subrata S. (2003), “Deregulation, Ownership, and Productivity Growth

in the Banking Industry: Evidence form India”, Journal of Money, Credit and Banking, 35(3),

403-24.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

943

www.globalbizresearch.com

McKinnon, R.I. (1973), Money and Capital in Economic Development, the Brooklings

Institution, Washington D.C.

Mike, A.U, (2010), “New Banking Model in Nigeria: Opportunities and Challenges”, Zenith

Economic Quarterly, 1(3), 29-38.

Mor, N. Chandrasekar, R. and Wahi, D. (2006), “Banking Sector Reform in India”, IMF Staff

Papers.

Mora, N. (2010), “Can Banks Provide Liquidity in a financial Crisis?”, Federal Reserve Bank

Kansas City Economic Review, 95(1), 31-68.

Matutes, C. and Vives, X. (2000), “Imperfect Competition, Risk Target and Regulation in

Banking,” European Economic Review, 44(2), 1-34.

Nnanna, O.J. (2005), “Central Banking and Financial Sector Management in Nigeria: An

Insider View” in Nigeria” (Essays in Honour of Professor Obasanmi Olakankpo), pp. 99-120.

Ojo, J.A.T. (2005), “Central Banking and Financial Sector Management in Nigeria: An

Insider View,” in Fakiyesi, O.O. & S.O. Akano (Eds.), Issues in Money, Finance and

Economic Management in Nigeria (Essays in Honour of Professor Obasanmi Olakankpo),

pp.35-98.

Okpara, G.C. (2011), “Bank Reforms and the Performance of the Nigerian Banking Sector:

An Empirical Analysis”, International Journal of Current Research, 2(1), 142-153.

Omoruyi, S.E. (1991), “The Financial Sector in Africa: Overview and Reforms in Economic

Adjustment Programmes”, Central Bank of Nigeria Economic and Financial Review, 29(2),

110-124

Oputu, E.N. (2010), “Banking Sector Reforms and the Industrial Sector: The Bank of Industry

Experience”, CBN Economic and Financial Review, 48(4), 67-76.

Sanusi, L.S. (2012), (2010), “Banking Sector Reform and Its Impact on the Nigerian

Economy”, Lecture Delivered at the University of Warwick‟s Economic Summit, 17th

February.

Saxegaad, M. (2006), “Excess Liquidity and the Effectiveness of Monetary Policy: Evidence

from sub-Saharan Africa”, International Monetary Fund Working Paper No.06/115, 1-32.

Shaw, E.S. (1973), Financial Deepening in Economic Development, New York, Oxford

University Press.

Simar, L. and Wilson, P.W. (2007), “Estimation and Inference in Two-Stage, Semi-

Parametric Models of Production Processes”, Journal of Econometrics, 136(2), 31-64.

Soludo, C.C. (2005), “Recent Reforms in the Nigerian Banking Industry: Issues and

Prospects”, Paper delivered at the 2004 End of Year Party organized by the Clearing House

Committee.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

944

www.globalbizresearch.com

Soludo, C.C. (2007) “Macroeconomic, Monetary and Financial Sector Developments in

Nigeria”, CBN Website www.cenbank.org.Accessed 24/9/2010.

Somoye, R. O. (2008), “The Performance of Commercial Banks in Post Consolidation Period

in Nigeria: an Empirical Review”, European Journal of Economics, Finance and

Administrative Sciences, 14(1), 62-72.

Toby, A.J. (1993), “Bank Survival Strategies in a Volatile Economic Environment: The

Nigerian Experience,” People’s Bank Economic Review, 19(2 & 3), 71-76.

Toby, A.J. (1994), “Deregulation, Competitive Pressure and New Patterns of Bank Behaviour

in Nigeria,” The Indian Journal of Economics, 75(297), 151-166.

Toby, A.J. (1999), “Analysis of the Financial Performance of Public Enterprise Banks”, First

Bank Economic Review, 7(5), 36-61.

Toby, A.J. (2002), “Ratio-Discriminant Model and Prediction of Bank Distress in Nigeria,”

Journal of Business Research, 1(2), 242-290.

Toby, A.J. (2005), “Capital Adequacy Regulation and Bank Asset Quality: The Nigerian

Empirical Evidence”, African Journal of Finance and Management, 13(2), 8-20.

Toby, A.J. (2006a), “Methodological Approach to the Study of X-Efficiencies and Scale

Economies in Banking: Are Smaller Bank More Efficient than Larger Banks?” Journal of

Financial Management and Analysis, 19(2), 85-96.

Toby, A.J. (2006b), “Monetary Policy Targets and Bank Liquidity Management Practices in

Nigeria: An Inter-temporal Analysis”, The Indian Journal of Economics, 86(No.243), 459-

472.

Toby, A.J. (2007), “Camel Analysis, Prudential Regulation and Banking System Soundness

in Nigeria”, ICFAI Journal of Bank Management, 6(3), 43-60.

Toby, A.J. (2010), “Global Financial Crisis and Bank Management Practices in Nigeria:

Survey Findings”, Journal of Financial and Analysis, 23(2), 27-51.

Toby, A.J. (2011), Inter-temporal Modelling of Financial Fragility and Performance of

Nigerian Banking Institutions”, International Journal of Management Sciences, 3(5), 78-90.

Ubirimie, T.U. (2005), “Determinants of Bank Profitability: Industry-Level Evidence for

Nigeria”, Available at SSRN:http://ssm.com/abstract=1120232. Accessed 17/4/2009.

Uchida, H. and Tsutsui, Y. (2005), “Has Competition in the Japanese Banking Sector

Improved?”, Journal of Banking and Finance, 29(3), 419-439.

Uppah, R.K. (2011), “Banking Sector Reforms: Policy Implications and Fresh Outlook,”

Information Management and Business Review, 2(2), 55-64.

Whealock, D.C. and Wilson, P.W. (1999), “Technical Progress, Inefficiency and Productivity

Change in US Banking, 1984-1993,” Journal of Money, Credit and Banking, 31(4), 213-234.

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

945

www.globalbizresearch.com

Zaim, O. (1995), “The Effects of Financial Liberalization in the Efficiency of Turkish

Commercial Banks”, Applied Financial Economics, 5(4), 257-254.

Ziorkui, S.Q. (2001), “The Impact of Financial Sector Reform on Bank Efficiency and

Financial Deepening for Savings Mobilization in Ghana”, Africa Economic Policy Discussion

Paper NO.81 (February).

Appendix A

Variance Inflation Factors (VIFs) and Tolerance Values for the

Pre-and Post-Reform Periods

Period/Model

Independent Variables (IVs)

1 2 3

Model 1:

Pre-Reform Period

Tolerance -7.667 7.9550 3.5633

VIF 2.8830 0.4466 2.2396

Model 1:

Post-reform Period

Tolerance

-0.6040 0.0817 0.0933

VIF 1.2160 0.5099 0.5538

Model 2:

Pre-Reform Period

Tolerance 1.5989 -2.0715 -0.6571

VIP 5.0690 2.2730 2.2350

Model 2:

Post-Reform Period

Tolerance -0.5792 0.0014 0.7446

VIF 2.5660 1.0030 2.5680

Model 3:

Pre-Reform Period

Tolerance -0.8690 3.4429 -1.4861

VIF 4.1880 2.8830 2.2390

Model 3:

Post-Reform Period

Tolerance 0.5284 0.3235 -1.4513

VIF 1.2160 1.9610 1.8060 Source: SPSS Print-Out

Journal of Emerging Issues in Economics, Finance and Banking (JEIEFB) An Online International Monthly Journal (ISSN: 2306-367X)

Volume:2 No.6 December 2013

946

www.globalbizresearch.com

Appendix B

Condition Indices for the Pre-and Post-Reform Periods

Model/Period

Eigenval

Cond.

Index

Variance

Proportions

1 2 3

Model 1:

Pre-Reform Period

1 3.89493 1.000 0.00081 0.00234 0.00076 0.00086

2 0.08671 6.702 0.04686 0.28198 0.00068 0.00364

3 0.01269 17.519 0.00572 0.00211 0.42480 0.55271

4 0.00566 26.221 0.94661 0.71357 0.57376 0.44279

Model 1:

Post-Reform Period

1 3.79188 1.000 0.00265 0.001226 0.00160 0.00182

2 0.16696 4.766 0.02800 0.92345 0.00689 0.01177

3 0.02578 12.129 0.95081 0.03794 0.10301 0.27303

4 0.01538 15.703 0.01854 0.02635 0.88899 0.71337

Model 2:

Pre-Reform Period

1 3.92862 1.000 0.00361 0.00027 0.00028 0.00076

2 0.06025 8.075 0.68535 0.00953 0.01086 0.00103

3 0.00885 21.074 0.311012 0.04146 0.06201 0.99218

4 0.00229 41.464 0.00002 0.94875 0.92684 0.00552

Model 2:

Post-Reform Period

1 3.03646 1.000 0.00567 0.00234 0.01272 0.00281

2 0.91214 1.825 0.00060 0.00038 0.97744 0.00047

3 0.03794 8.946 0.93974 0.05309 0.00945 0.17594

4 0.01345 15.024 0.05399 0.94418 0.00038 0.82079

Model 3:

Pre-Reform Period

1 3.89493 1.000 0.00081 0.00234 0.00076 0.00086

2 0.08671 6.702 0.04686 0.28198 0.00068 0.00364

3 0.01269 17.519 0.0572 0.00211 0.42480 0.55271

4 0.00566 26.221 0.94661 0.71357 0.57376 0.44279

Model 3:

Post-Reform Period

1 3.93580 1.000 0.00031 0.00468 0.00017 0.00015

2 0.05950 8.133 0.00782 0.96516 0.00299 0.00318

3 0.00327 12.684 0.93919 0.2140 0.219600 0.06792

4 0.00143 15.481 0.05268 0.00876 0.7774 0.92876

Source: SPSS Print-Out