mobile money in microfinance - education network … · mobile money in microfinance oikocredit’s...

TRANSCRIPT

Mobile Money in Microfinance Oikocredit’s Response to Challenges in the MF Sector

Ulrike Chini

ISB Summer School 2016, Tallinn

… empowering People worldwide

Oikocredit’s Vision

• Is a worldwide cooperative society

• Founded in 1975, thus 40 years of experience

• Seeks “A global, just society in which resources are

shared sustainably and all people are empowered with

the choices they need to create a life of dignity.”

• Seeks to contribute to the building of this global, just society

by challenging all to invest responsibly.

Facts & figures

• 809 partners in 69 countries

• 544 microfinance partners (of total number of partners)

• € 900.2 million invested in loans and equity

• € 497.8 million approved

• € 419.0 million disbursed

• 46 million clients reached by Oikocredit’s MF partners

• regional offices in 33 countries

At 31 December 2015

Funding to partners in 69 countries

800 partners Over 80 % women

Funding by sector At 31 December 2015

€ 900.2 million portfolio

TOP MF countries:

India, Cambodia, Bolivia,

Paraguay, Ecuador, Peru

90 Fair Trade partners

*including microfinance, SME finance and leasing

Coffee, Cacoa, Nuts, Quinoa, Spices…

Oikocredit Finances Fair Trade

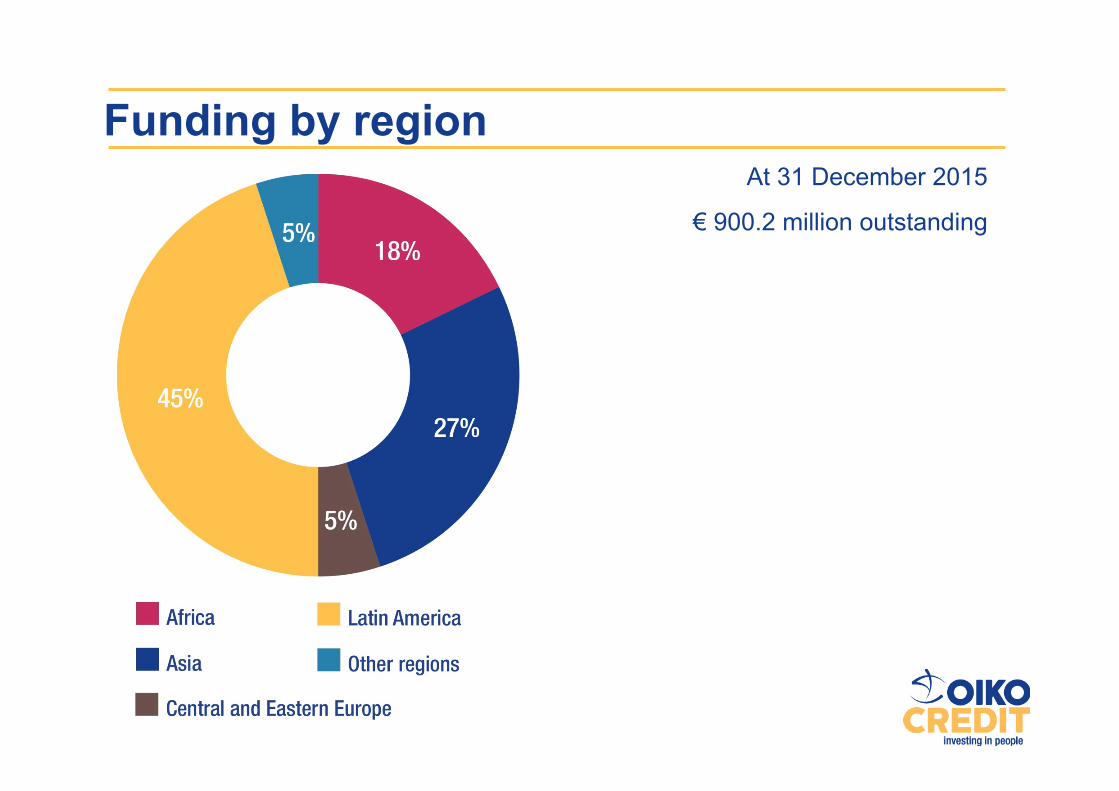

Funding by region At 31 December 2015

€ 900.2 million outstanding

Oikocredit’s Focus on…

• Social Performance

• Capacity Building

• 86 % female clients (MFIs)

• 51 % rural clients

• Social mission of partners

• Renewable Energy,

Agriculture, Africa

Challenges in the MF Sector

• Concentration of foreign funds on a few large MFI

• Need to maintain focus on social mission

• Strong need for training, capacity building, tracking of social

performance data

• Regulation

• Digitalization

• High costs

FinTechs are attacking incumbents on every possible vertical

Wells Fargo is the world’s largest bank by market cap. Currently there is a FinTech for every single element of their business, while they themselves partner with Apple Pay.

What is FinTech? • FinTech (short for Financial Technology) is a collective term for a diverse

set of companies, technologies and business models

• Around for decades, sector attention is increasing since dozens of startups

quickly reached valuations of $1+ billion in recent years. Think PayPal (Elon

Musk + Peter Thiel), Square, LendingClub, Adyen, TransferWise, etc.

• As of early 2016, 5,000+ sizeable FinTech startups around various themes

and dozens of emerging FinTech hubs

FinTech – main finance sector disruptor • “Disintermediation” is arguably FinTech’s most powerful weapon – cutting out

the financial middle man

• Increased Internet access and smartphone adoption are two of the most important drivers of the FinTech rise, globally

• Bankers & insurers themselves think consumer banking & payments are most at risk from FinTech, but they might be missing the point...

Mobile Money

Digital money transfers open up opportunities for new kinds of

financial services, such as

Agriculture

Health Energy

Asset

Education

Savings

Oikocredit Finances…

• MUSONI, Kenya, established 2009, MFI providing financial

services through mobile payments, works with M-Pesa,

Safaricom mobile payment platform.

• BBOXX, Kenya, set up 2010, off-grid solar power. BBOXX

provides home kits, via a three year purchase agreement, to

be paid monthly via mobile.

• AMK, Cambodia, MFI, making use of mobile banking agents,

committed to enhance welfare of – rural – clients through tailor

made products.

Oikocredit Finances…

• WIZZIT, South Africa, established in 2004, develops mobile

banking software and supports installation, implementation

and product development. The mobile banking software

(Everest) is currently used in various African countries as well

as in Eastern Europe and Central America.

Banking services include money transfers or pre-paid

electricity and air-time purchases via the mobile phone.

Financial Service Providers

• Microfinance Institutions (MFI)

• Telecommunications Companies like Safaricom: offers their

mobile banking platform M-Pesa, set up by Safaricom &

Vodafone. Available in many African countries, in India. High

transaction costs, up to 60 % /a. Profit in 2014: 27 % of total

amount of money transfers*.

M-Shwari, saving & borrowing, avg loan 2014 = $ 10, 7,5 %

interest rate/mo. (Safaricom & CBA)

* Wikipedia

Challenges of Mobile Money

• Faster services, lower costs (?), easy access (also

in remote areas), financial inclusion…

• But what about:

Regulation, data protection, security of IT

systems, transparency, financial literacy, social

services, relationships.

• ???

Thank you! www.oikocredit.coop

Disclaimer

This document was produced by Ulrike Chini, Oikocredit, Ecumenical Development Cooperative Society U.A. with the greatest of care and to the best of her knowledge and belief at the time of writing. The opinions expressed in this document are hers at the time of writing and are subject to change at any time without notice. Oikocredit International provides no guarantee with regard to its content and completeness and does not accept any liability for losses which might arise from making use of this information.

This document is provided for information purposes only and is for the exclusive use of the recipient. It does not constitute an offer or a recommendation to buy or sell financial instruments or banking services and does not release the recipient from exercising his/her own judgment. The recipient is in particular recommended to check that the information provided is in line with his /her own circumstances with regard to any legal, regulator, tax or other consequences, if necessary with the help of a professional advisor.

This document may not be reproduced either in part or in full without the written permission of Oikocredit International. It is expressly not intended for persons who, due to their nationality or place of residence, are not permitted access to such information under local law.

Every investment involves risk, especially with regard to fluctuations in value and return. It should be noted that historical returns and financial market scenarios are no guarantee of future performance. Investments in foreign currencies involve the additional risk that the foreign currency might lose value against the investor‘s reference currency.

Oikocredit International is a cooperative society with limited liability (coöperatieve vereniging met uitgesloten aansprakelijkheid) under the laws of the Kingdom of the Netherlands.