mobile banking – the way forward mar 11, 2009 abrar a. mir evp, business development &...

TRANSCRIPT

Mobile Banking – The way Forward

Mar 11, 2009

Abrar A. MirEVP, Business Development & Strategic [email protected]

AgendaAgenda

• Mobile Banking definition

• Mobile Banking and interfaces

• Pros & Cons of interfaces

• Current models –Pakistan and Globally

• Evolution of Banking channels

• The Way Forward– Market Opportunity

– Mobile as extension of multichannel strategy

– Convergence of technology and financial services

– Future Business Models

– Mobile banking beyond being extension of internet banking

– Security Dilemma

• Key Take Aways

What is Mobile BankingWhat is Mobile Banking

Mobile Banking is the use of mobile-phone based interfaces to provide account information and transactions opportunities to

customers of financial InstitutionsThese interfaces could include any or all of the following:

1. SMS2. WAP3. Downloadable Application - J2ME4. Embedded application – STK5. USSD6. Proximity Payments

1. NFC2. RFID

Mobile Banking and Branchless Banking are not the same

Pros & cons of various InterfacesPros & cons of various InterfacesINTERFACES

Browser /WAP Inexpensive entry Emulation of the

online experience Appeal to mobile

professionals

Network speed Multiple process

steps for log-in

SMS/MMS

Speed to market Broad customer reach Gen Y/appeal Frictionless

customer interaction

Unsuitability forhigh-value apps

Unsuitability fortransactions due to lack of security

J2 ME High-value apps Rich user experience Security Bank retention of

display control

Download can beclumsy

Who owns customer service?

J2ME Compatibility not widespread

USSD Menu based services Rich user experience Security Available on every handse

Telecom operator dependent

STK Application has to be downloaded; SMS based; Encrypted;

Usability an issue?New feature additions in application require updates on every SIM

Multi interface Delivery will remain a minimum necessity to get access to broad range of target markets

Current models –Pakistan and GloballyCurrent models –Pakistan and Globally

• Various models are out there in the market that include:– M-Pesa– WIZZIT– ABSA– MTN Banking– G cash– SARAF Mobile– UBL ORION

A proliferation of technology and business models has been adopted, with no clear winner in terms of technology or business models as yet. Regulatory environment is also still evolving

There is "nothing more difficult to carry out, nor more doubtful of success, nor more dangerous to handle, than to initiate a new order of things" (Machiavelli)

Mobile Banking as an extension of Bank’s multichannel delivery strategyMobile Banking as an extension of Bank’s multichannel delivery strategy

CUSTOMERCUSTOMER

BranchBranch

Interactive TVInteractive TV

PC Banking PC Banking (Internet)(Internet)

Call CenterCall Center

ATM/ KiosksATM/ Kiosks

Mobile/ TelephonyMobile/ TelephonyPC Banking PC Banking

(Private Network)(Private Network)

Postal ChannelPostal Channel

Cost, Efficiency and Convenience key drivers for evolution of various

delivery channelsWill it just be another channel?

ORWill it transform the way banking is done and result in Transforming the business models both for the bank and it’s customers?

Channels getting more high tech and high touch

The Way forwardThe Way forward

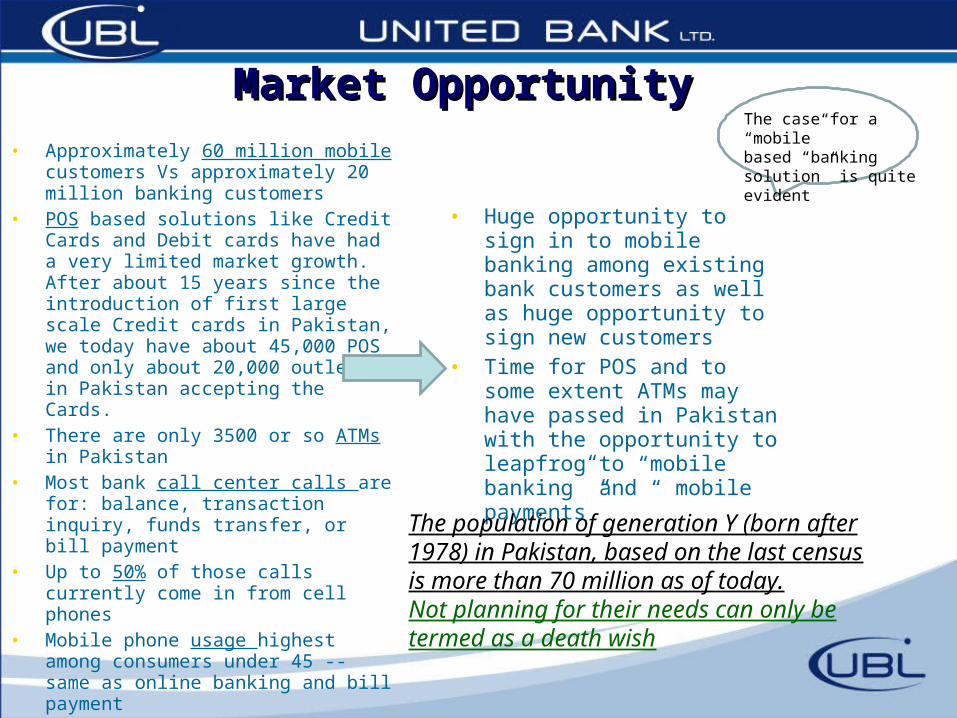

Market OpportunityMarket Opportunity• Approximately 60 million mobile

customers Vs approximately 20 million banking customers

• POS based solutions like Credit Cards and Debit cards have had a very limited market growth. After about 15 years since the introduction of first large scale Credit cards in Pakistan, we today have about 45,000 POS and only about 20,000 outlets in Pakistan accepting the Cards.

• There are only 3500 or so ATMs in Pakistan

• Most bank call center calls are for: balance, transaction inquiry, funds transfer, or bill payment

• Up to 50% of those calls currently come in from cell phones

• Mobile phone usage highest among consumers under 45 -- same as online banking and bill payment

The case for a “mobile”based “banking solution” is quite evident

• Huge opportunity to sign in to mobile banking among existing bank customers as well as huge opportunity to sign new customers

• Time for POS and to some extent ATMs may have passed in Pakistan with the opportunity to leapfrog to “mobile banking” and “ mobile payments”

The population of generation Y (born after 1978) in Pakistan, based on the last census is more than 70 million as of today.Not planning for their needs can only be termed as a death wish

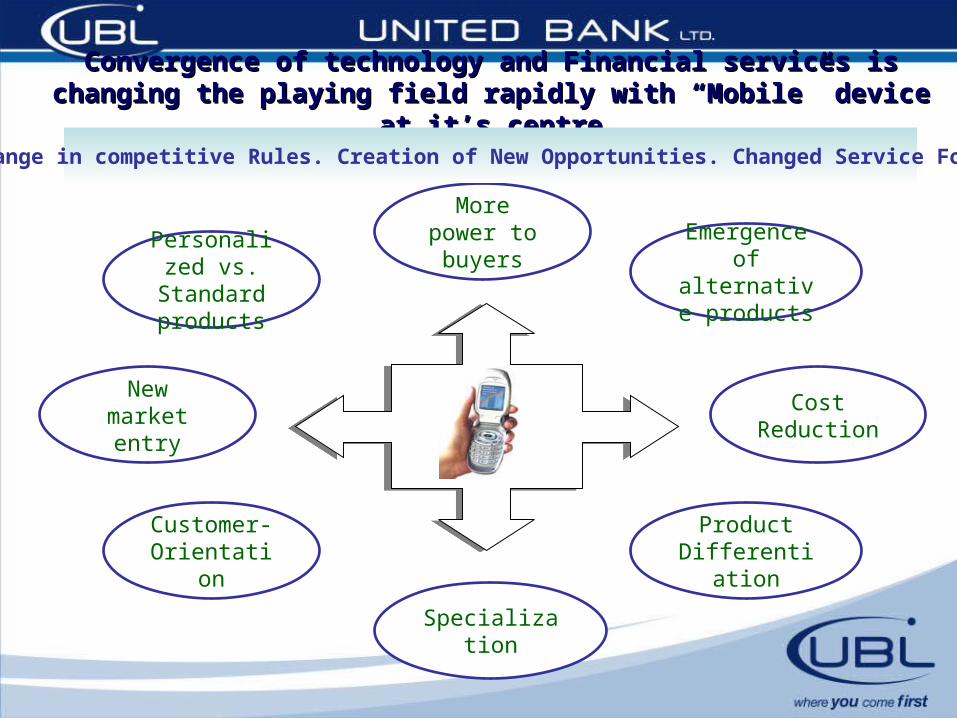

Convergence of technology and Financial services is changing the Convergence of technology and Financial services is changing the playing field rapidly with “Mobile” device at it’s centreplaying field rapidly with “Mobile” device at it’s centre

Emergence of alternative products

Personalized vs. Standard

products

More power to buyers

Cost Reduction

New market entry

Product Differentiation

Specialization

Customer-Orientation

Change in competitive Rules. Creation of New Opportunities. Changed Service Focus.

Convergence advantagesConvergence advantages

• Lower research cost– Time– Expense

• Greater convenience• Lower transaction costs• Broader communication,

from one to many• Real-time access• Transparent to user• Wider reach/access• 24 hours/day, 7 days/week• Accurate and efficient

• Lower research cost– Time– Expense

• Greater convenience• Lower transaction costs• Broader communication,

from one to many• Real-time access• Transparent to user• Wider reach/access• 24 hours/day, 7 days/week• Accurate and efficient

Technology is opening

up new markets, creating

new models of doing business

and reinventing the value

chain

Technology is opening

up new markets, creating

new models of doing business

and reinventing the value

chain

• Increased customer satisfaction

• Increased retention • Improved lead

generation• Increased market

share• Increased wallet share• Expanded sales &

marketing channels• Increased customer

knowledge

• Increased customer satisfaction

• Increased retention • Improved lead

generation• Increased market

share• Increased wallet share• Expanded sales &

marketing channels• Increased customer

knowledge

It is about the SERVICES and not the technology.Converging technologies are just the enabler that is

facilitating “service convergence”

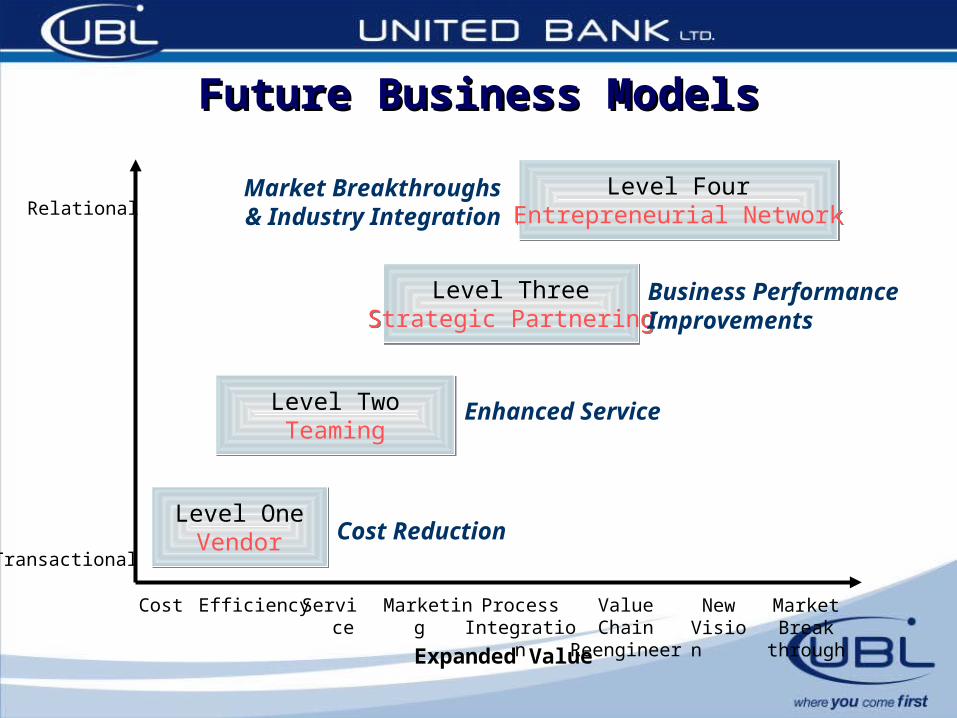

Future Business ModelsFuture Business Models

Relational

Cost Efficiency Service Marketing ProcessIntegration

Value ChainReengineer

NewVision

MarketBreak

throughExpanded Value

Transactional

Level OneVendor

Level OneVendor

Level TwoTeaming

Level TwoTeaming

Level ThreeStrategic Partnering

Level ThreeStrategic Partnering

Level FourEntrepreneurial Network

Level FourEntrepreneurial Network

Cost Reduction

Enhanced Service

Business Performance Improvements

Market Breakthroughs & Industry Integration

21st Century Business model Enablers21st Century Business model Enablers

Alliances

Business optimization

Electronic communities

Flat organizational structure

Global branding

Innovation/experimentation

Service excellence

Virtual customer intimacy

Development of strategic alliances to meet customer demands by utilising the core competencies of other providers

Use of the Internet and mobile as a revenue generator and as a low cost distribution channel

Design of value added content and functionality for strengthening relationships

Development of a flat / flexible structure with skill sets focused on innovation and delivery

Common look and feel across global markets

Experimentation with emerging technologies for continuous improvement

Development of world class customer service over all available channels

Collection and intelligent analyses of customer data for forecasting customer needs

Mobile banking will drive value beyond its Mobile banking will drive value beyond its early role as an extension of Internet banking / alternate early role as an extension of Internet banking / alternate

channel for deliverychannel for delivery

2007 2008 2009 2010 2011 2012

Ado

ptio

n

BillPay

FundsTransfer

BalanceInquiries

LocationFinder

CommercialCash Mgmt.

Familiarization Convergence Differentiation

Mobile POSPayments

StopPayment

CheckReorder

M-Statements

PersonalSecurity

ActionableAlerts

Account Opening

The security dilemma, a balancing actThe security dilemma, a balancing act• Security becomes more important as we move toward mobile payments and an ever increasing number of users

– Regulation – Compliance– Anti-money laundering– Identity theft– Access control

• First line of defense is to educate the user. The greatest root cause of external breaches continues to be the human factor

• The desire for greater functionality must constantly be supplemented with stronger security measures to offset the risks of each new capability.

• These security measures must be highly nimble; they must be quickly deployed and evolve over time to anticipate and adapt to new threats and emerging risks, as well as satisfy a new generation of customers who want more-personal and customized experiences that match their lifestyles.

• A security strategy is essentially a road map for mitigating risks while complying with legal, statutory, contractual and internally developed requirements.

• Some of the basic components include defining control objectives, identifying and assessing approaches to meet those objectives, selecting controls, establishing metrics and benchmarks, testing and implementation, and performing ongoing maintenance.

• The ultimate goal is to increase customer confidence across online channels and reduce losses due to fraud and identity theft across the enterprise.

Tough Security

vs

Customer Experience

KEY TAKE AWAYSKEY TAKE AWAYS THE BUSINESS CASE IS CLEARTHE BUSINESS CASE IS CLEAR

• The second act of mobile banking shows longevity as consumer need, network maturity, device sophistication, and advanced technology enablers coalesce into a business case.

• Mobile banking is emerging as an indispensible business asset to retain customers and reach new segments

• The Key success driver will be the “Customer value proposition” whereas most of the current m-payment solutions are driven from “supply side”

• Waiting to act turns banks into prey for nontraditional players that pose a short-term threat of disintermediation, but in the long run the banks will thrive.

• Consumers will pay for the convenience and urgency factors of mobile financial services, and banks should be looking at opportunities to monetize premium services.

• The banks will become “Money managers” for customers as the distinction between Mobile as a “distribution channel” vs. a” payment solution” will gradually disappear.

• Different “business models” will evolve based on different market needs and regulatory environment• “Interoperability” will always remain the key for the phenomenon to gain wide and quick adaption