moberg pharma ab -...

TRANSCRIPT

0

Corporate presentationAktiespararna Trollhättan, April 20th 2016Anna Ljung, CFO

Moberg Pharma ABPROVIDING UNIQUE PRODUCTS IN UNDERSERVED NICHES

1

Disclaimer

1

Statements included herein that are not historical facts are forward-looking statements. Such forward-looking statements involve a number of risks and uncertainties and are subject to change at any time. In the event such risks or uncertainties materialize, Moberg Pharma’s results could be materially affected. The risks and uncertainties include, but are not limited to, risks associated with the inherent uncertainty of pharmaceutical research and product development, manufacturing and commercialization, the impact of competitive products, patents, legal challenges, government regulation and approval, Moberg Pharma’s ability to secure new products for commercialization and/or development and other risks and uncertainties detailed from time to time in Moberg Pharma’s interim or annual reports, prospectuses or press releases.

2

2

Net Sales grew to 286 MSEK (full year 2015)- U.S. OTC Sales operations- Products sold in 40+ countries- 35 employees in Sthlm and NJ

Focus in OTC/Dermatology/Topicals- Leading U.S. OTC SKU in Nail Fungus- Superior PII data for MOB015

Market Cap ~750 MSEK (OMX:MOB)

Moberg PharmaPROVIDING UNIQUE PRODUCTS IN UNDERSERVED NICHES

3

3

Strategic elements

Growth strategy- Organic growth- M&A/Innovation engine

Build value through combiningBrand/IP Equity

Outlook

Profitable growth, targeting a long-term EBITDA margin of at least 25%

Moberg PharmaPROVIDING UNIQUE PRODUCTS IN UNDERSERVED NICHES

2015 – Continued growth and doubling of profit

5

5

Q415 net sales grew by 7% to MSEK 54

Year-on-year, 2015 net sales grew by 43% (21% at fixed exchange rates) and EBITDA improved by 83%

Asian launch driving growth in distributor sales

Innovation engine progress – Bupi Ph II results, Colep, Cadila, reg meetings

SEK 300 million raised in the Nordic bond market to finance growth and acquisitions

Divestment of three non-core brands enable increased focus on strategic assets

Highlights from Q415 and Q116 to date

6

Net Sales, MSEK

Growth in 2015 improved EBITDA with 83%

6

286 (+43%)

200

EBITDA, MSEK EBITDA Commercial Operations, MSEK

2015 12m2014 12m

NOTE: EBITDA Commercial Operations does not include R&D and Business Development expenses for future products outside existing brands

25

46 (+83%)

13% 16% 22% 24%

68 (+58%)

43

7

23 consecutive quarters of Sales growth

Product Sales, TTM, MSEK

7

0

50

100

150

200

250

300

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Q22015

Q32015

Q42015

8

P&L - Sales growth and doubling of profit

8

1) Research and development expenses – existing product portfolio includes R&D expenses for new product variants under existing brands, regulatory work and quality.2) Research and development expenses - future products includes R&D expenses for new product candidates, for example MOB-015.

Due to the rounding component, totals may not tally.

P&L Summary (MSEK)Q4 2015 Q4 2014 FY 2015 FY 2014

Revenue 54 44 286 200Gross profit 37 32 214 151% 68% 72% 75% 75%

SG & A ‐26 ‐25 ‐142 ‐106R&D ‐ existing product portfolio1) ‐2 ‐1 ‐6 ‐7Other operating income/operating expenses 0 4 4 6EBITDA Commercial Operations 9 9 68 43% 16% 21% 24% 22%

R&D & BD ‐ future products2) ‐5 ‐6 ‐22 ‐18EBITDA 4 4 46 25% 8% 8% 16% 13%

Depreciation/amortization ‐3 ‐2 ‐11 ‐8Operating profit (EBIT) 1 1 35 17

9

Other21%

Nalox/ Kerasal Nail

55%

Kerasal11%

JointFlex13%

RoW15%

Europe 11%

Americas 74%

Sales via distributors

28%

Direct OTC Sales 72%

Majority of revenue from direct OTC sales – Launches in Asia drives RoW product sales

9

Channels Products Geography

Distribution of revenue, January – December 2015

10

Solid cash position and positive cash flow

10

Full-year 2015 Full-year 2014

Operative cash flow +31 MSEK +16 MSEK

Cash position 45 MSEK 62 MSEK

Not including:

Bond issue of 300 MSEK closed in January 2016Bond structure also allows tap issues of additional 300 MSEK

Divestment of three non-core brands for 10 MUSD closed in April 2016

Progress in Commercial Operations

12

12

Strategic brands

Kerasal® - Foot careEmtrix®

Balmex® - Diaper rash

Domeboro® - Derma/Skin irritation

Mature brands – Divested April 1, 2016

Jointflex® - External analgesic

Vanquish® - Internal analgesic

Fergon® - Iron supplement

Focus on strategic brands

13

Kerasal Nail - the OTC market leader in the U.S.

13

No 1 with 22% market share in Q4 20151)

Key claim “visible difference in 2 weeks”. Product supported by 4 clinical studies

Available at >30 000 points of sale

1)Retail sales of nail fungus products excluding private label in Multioutlet Stores over the last 52 weeksending December 27, 2015 as reported by SymphonyIRI

14

Scalable infrastructure for marketing U.S OTC brandsRetailers/WholesalersSales Force

Contract Manufacturers

Logistics

Sales and marketing/Brand Management

14

Note: Largest retailers and whole-salers only, not an all inclusive list.

15

Acquired from Chattem (Sanofi) for $3.9 million (MSEK 33.3)– Sales trending above $4 million annually– Deal financed with existing funds

Strong heritage in baby diaper rash with broad distribution in major chains:

Closed Balmex acquisition April 24, 2015

15

16

Distributor Sales well positioned for further growth

Note: Four largest distributors only, not an all inclusive list.bv

16

Sales in >40 markets

Growth in Europe (+7%)- Emtrix® rights in six EU markets taken back

Asian launches progresses well and rapid growth of sales

- 6 markets launched - Ongoing preparations in other

Large growth potential

17

TV commercial in Malaysia – aired from Nov/Dec 2014

17

18

Launches in Asia a key growth driver

18

MalaysiaLaunch Q4 2014, already market leader

Hong KongExcellent start of sales and reorders

SingaporeLaunch started, to be ramped up

ChinaRegional launch started in May 2015

IndonesiaLaunch and TV started Aug 2015

PhilippinesLaunch started Nov 2015

Other marketsLaunch preparations ongoing

Innovation Engine

20

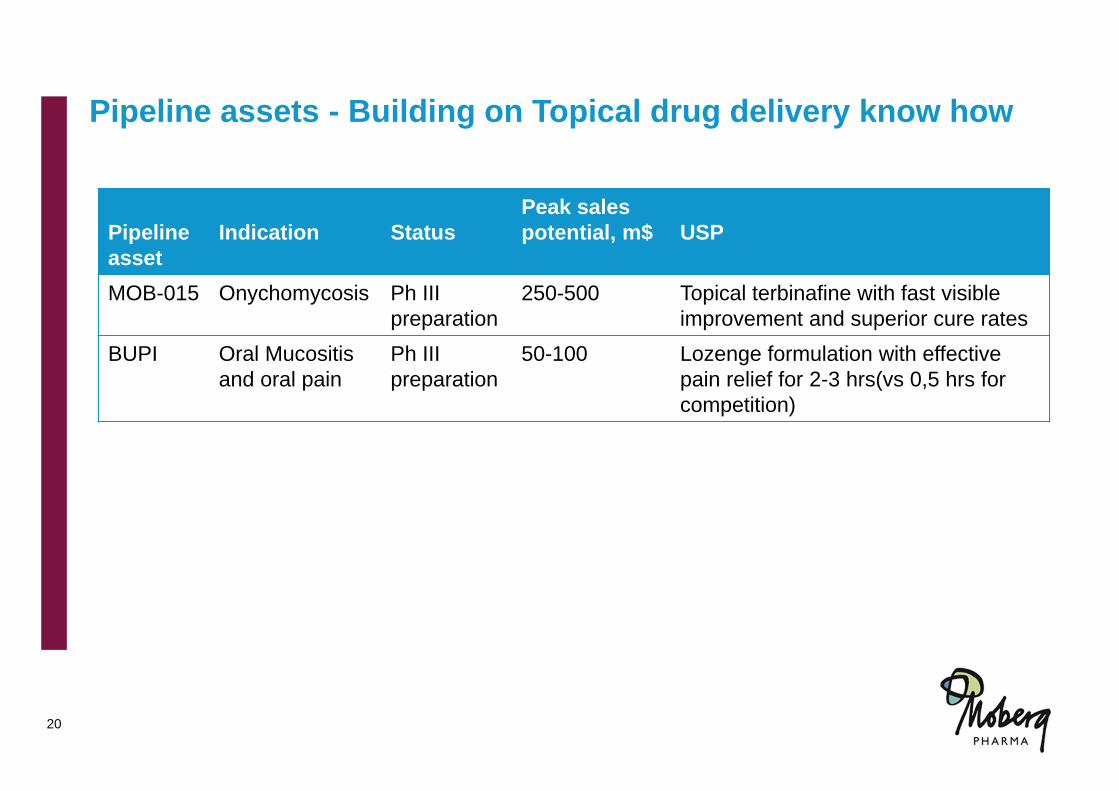

Pipeline assets - Building on Topical drug delivery know how

Pipeline asset

Indication StatusPeak sales potential, m$ USP

MOB-015 Onychomycosis Ph III preparation

250-500 Topical terbinafine with fast visible improvement and superior cure rates

BUPI Oral Mucositisand oral pain

Ph III preparation

50-100 Lozenge formulation with effective pain relief for 2-3 hrs(vs 0,5 hrs for competition)

20

21

MOB-015 – USPs and Strategy

21

USPs Targets a superior profile, in mild to moderate onychomycosisbased on phase II data and experience from the OTC product(>600 patients in clinical trials and >10 million units sold to date):

Superior cure rates – Mycological and ClinicalShorter treatment time – potentially 6 monthsFirst visible improvement within 2-4 weeks

Strategy Prepare Phase III to start in 2016Objective to maintain control of asset in key territories through phase III

1

2

3

22

BUPI targets to provide additional and prolonged pain relief

22

Product & Indication BUPI (bupivacaine lozenge) for oral pain relief (mouth and throat) 1st indication: Oral Mucositis in cancer patients. Large unmet need Other indications: Burning Mouth Syndrome, Sjögren’s syndrome, Upper

gastrointestinal endoscopy. Long-term also OTC potential.Value and Next steps Peak Sales potential $50-100m, whereof the OM indication is $20-25m Positive topline Phase II data

23

Innovation Engine

23

Organic growth Current products growing, adding new markets Line extensions adding incremental growth

- Focus on strategic brands 5 patent families enable additional products

- MOB-015, K-Nail+ patents granted

4ACQUISITIONS LAST 40 MONTHS

4PATENTS APPROVED 2015

Acquisitions/inlicensing Brands - Focus on US OTC market Pipeline assets enabling new products

Completed Acquisitions Alterna LLC, Nov 2012, $26m (2.3x Sales) Bayer brands, Dec 2013, $4.8m (1.6x Sales) Bupizenge, April 2014, dev. project,$1m Balmex, April 2015, $3.9m (<1x Net Sales)

24

24

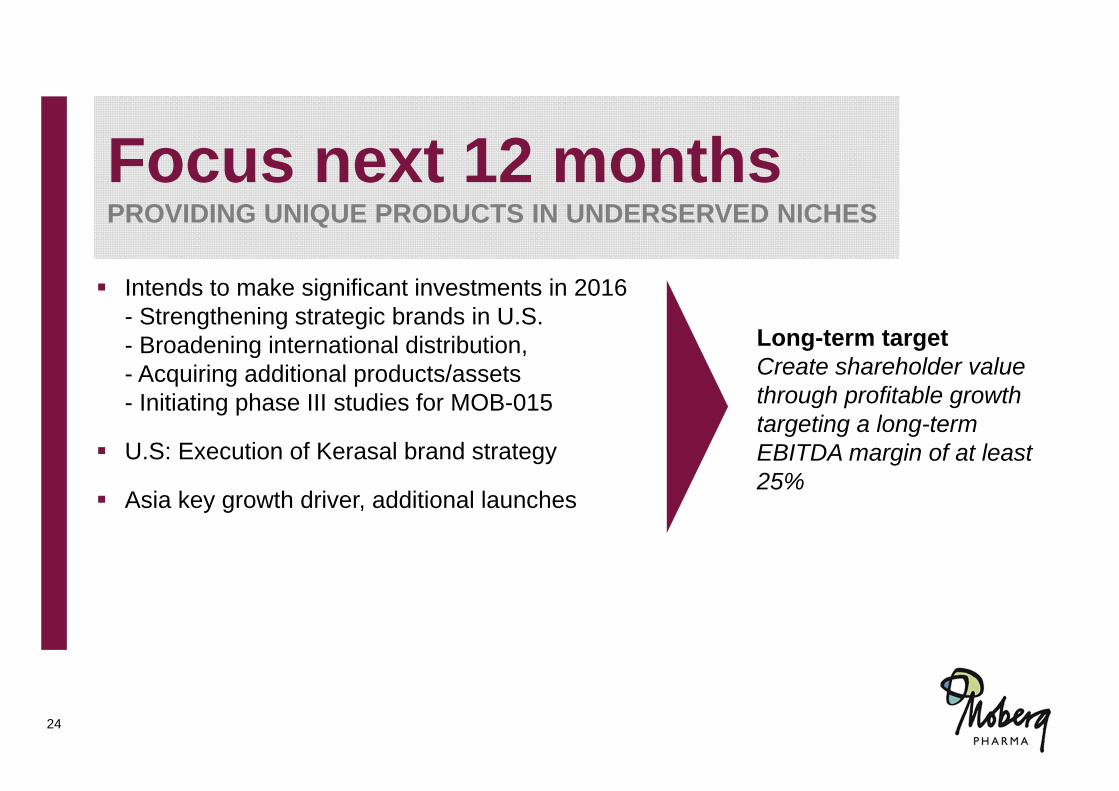

Focus next 12 monthsPROVIDING UNIQUE PRODUCTS IN UNDERSERVED NICHES

Intends to make significant investments in 2016- Strengthening strategic brands in U.S. - Broadening international distribution, - Acquiring additional products/assets - Initiating phase III studies for MOB-015

U.S: Execution of Kerasal brand strategy

Asia key growth driver, additional launches

Long-term targetCreate shareholder value through profitable growth targeting a long-term EBITDA margin of at least 25%

25

25

Commercial niche strategy enables a growing and profitable base business

Pipeline with large potential and at reasonable risk- Proven molecules limit development risk, cost and TTM

Acquisition strategy with substantial value potential- 4 acquisitions in last 40 months- Team, systems and infrastructure in place to enable scale-up- Capacity to finance deals

Strong Team with track record

Why invest in Moberg Pharma

26

26

Q&A