ministry of education 2: adjustments in the accounts unit 3: partnership unit 4: purchase of...

TRANSCRIPT

Republic of Namibia

MINISTRY OF EDUCATION

NAMIBIA SENIOR SECONDARY CERTIFICATE (NSSC)

2010

DEVELOPED IN COLLABORATION WITH UNIVERSITY OF CAMBRIDGE INTERNATIONAL EXAMINATIONS

ACCOUNTING SYLLABUS

HIGHER LEVEL

SYLLABUS CODE: 8335

GRADES 11 - 12

Republic of Namibia

MINISTRY OF EDUCATION

NAMIBIA SENIOR SECONDARY CERTIFICATE (NSSC)

ACCOUNTING SYLLABUS

HIGHER LEVEL

This syllabus replaces previous NSSC syllabuses and will be implemented in

2010 in Grade 11

Ministry of Education National Institute for Educational Development (NIED) Private Bag 2034 Okahandja Namibia © Copyright NIED, Ministry of Education, 2009 Accounting Syllabus Higher Level Grades 11 - 12 ISBN: 99916-69-19-1 Printed by NIED Publication date: 2009

TABLE OF CONTENTS 1. Introduction .................................................................................................................................... 1

2. Rationale ........................................................................................................................................ 1

3. Aims ............................................................................................................................................... 1

4. Learning Content ............................................................................................................................ 2

5. Assessment Objectives ................................................................................................................. 23

6. Scheme Of Assessment ................................................................................................................ 24

7. Specification Grid ........................................................................................................................ 25

8. Grade Descriptions ....................................................................................................................... 26

9. Glossary ........................................................................................................................................ 28

ANNEXE A International Standards Terminology ............................................................................. i

NSSCH Accounting Syllabus, NIED 2009 1

1. INTRODUCTION

The Namibia Senior Secondary Certificate (NSSC) for Accounting: Higher Level is designed as a two year course for examination after completion of the Junior Secondary Certificate. The syllabus is designed to meet the requirements of the Curriculum Guide for Formal Senior Secondary Education for Namibia and has been approved by the National Examination, Assessment and Certification Board (NEACB).

The Namibia National Curriculum Guidelines:

• Recognise that learning involves developing values and attitudes as well as knowledge and skills;

• Promote self-awareness and an understanding of the attitudes, values and beliefs of others in a multilingual and a multicultural society;

• Encourage respect for human rights and freedom of speech; • Provide insight and understanding of crucial “global” issues in a rapidly changing world

which affect quality of life: the AIDS pandemic, global warming, environmental degradation, maldistribution of wealth, expanding and increasing conflicts, the technological explosion and increased connectivity;

• Recognise that as information in its various forms becomes more accessible, learners need to develop higher cognitive skills of analysis, interpretation and evaluation to use information effectively;

• Seek to challenge and to motivate learners to reach their full potential and to contribute positively to the environment, economy and society.

Thus the Namibia National Curriculum Guidelines provide opportunities for developing essential, key skills across the various fields of study. Such skills cannot be developed in isolation and they may differ from context to context according to the field of study.

Accounting contributes directly to the development of the 8 skills marked*:

• Communication skills* • Numeracy* • Information skills* • Problem-solving skills* • Self-management and Competitive skills* • Social and Co-operative skills* • Physical skills • Work and study skills* • Critical and creative thinking skills*

2. RATIONALE

In Accounting learners understand and master mathematical skills, knowledge, concepts and processes, in order to investigate and interpret numerical relationships and patterns. It helps learners develop conciseness and logical and analytical thinking and apply these skills to other areas of learning and real life.

3. AIMS

The aims of the syllabus are the same for all learners. They are set out below and describe the educational purposes of a course in Accounting. They are not listed in order of priority.

The aims are to enable learners to:

• develop an understanding of the principles of accounting; • examine the role of accounting as an information system, enabling students to prepare and

evaluate accounting statements, systems and reports; • provide a means of developing a critical and analytical approach to quantitative problems,

and the numerate skills required for accounting;

NSSCH Accounting Syllabus, NIED 2009 2

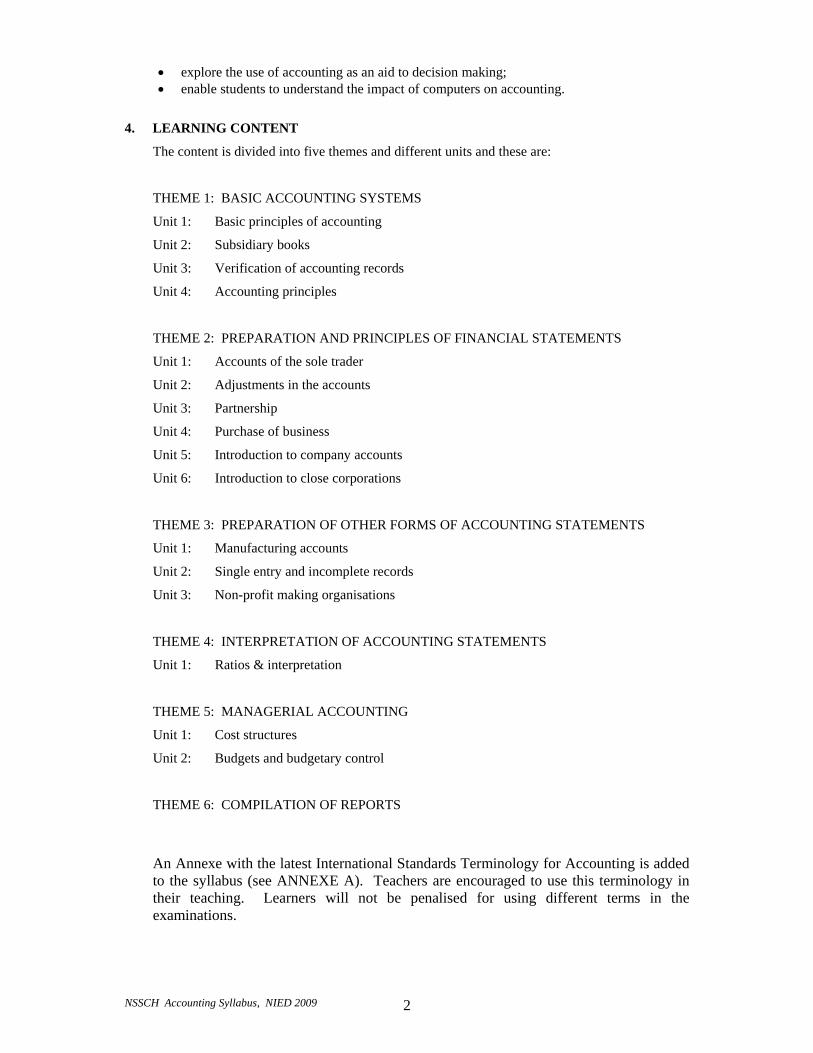

• explore the use of accounting as an aid to decision making; • enable students to understand the impact of computers on accounting.

4. LEARNING CONTENT

The content is divided into five themes and different units and these are:

THEME 1: BASIC ACCOUNTING SYSTEMS

Unit 1: Basic principles of accounting

Unit 2: Subsidiary books

Unit 3: Verification of accounting records

Unit 4: Accounting principles

THEME 2: PREPARATION AND PRINCIPLES OF FINANCIAL STATEMENTS

Unit 1: Accounts of the sole trader

Unit 2: Adjustments in the accounts

Unit 3: Partnership

Unit 4: Purchase of business

Unit 5: Introduction to company accounts

Unit 6: Introduction to close corporations

THEME 3: PREPARATION OF OTHER FORMS OF ACCOUNTING STATEMENTS

Unit 1: Manufacturing accounts

Unit 2: Single entry and incomplete records

Unit 3: Non-profit making organisations

THEME 4: INTERPRETATION OF ACCOUNTING STATEMENTS

Unit 1: Ratios & interpretation

THEME 5: MANAGERIAL ACCOUNTING

Unit 1: Cost structures

Unit 2: Budgets and budgetary control

THEME 6: COMPILATION OF REPORTS

An Annexe with the latest International Standards Terminology for Accounting is added to the syllabus (see ANNEXE A). Teachers are encouraged to use this terminology in their teaching. Learners will not be penalised for using different terms in the examinations.

NSSCH Accounting Syllabus, NIED 2009 3

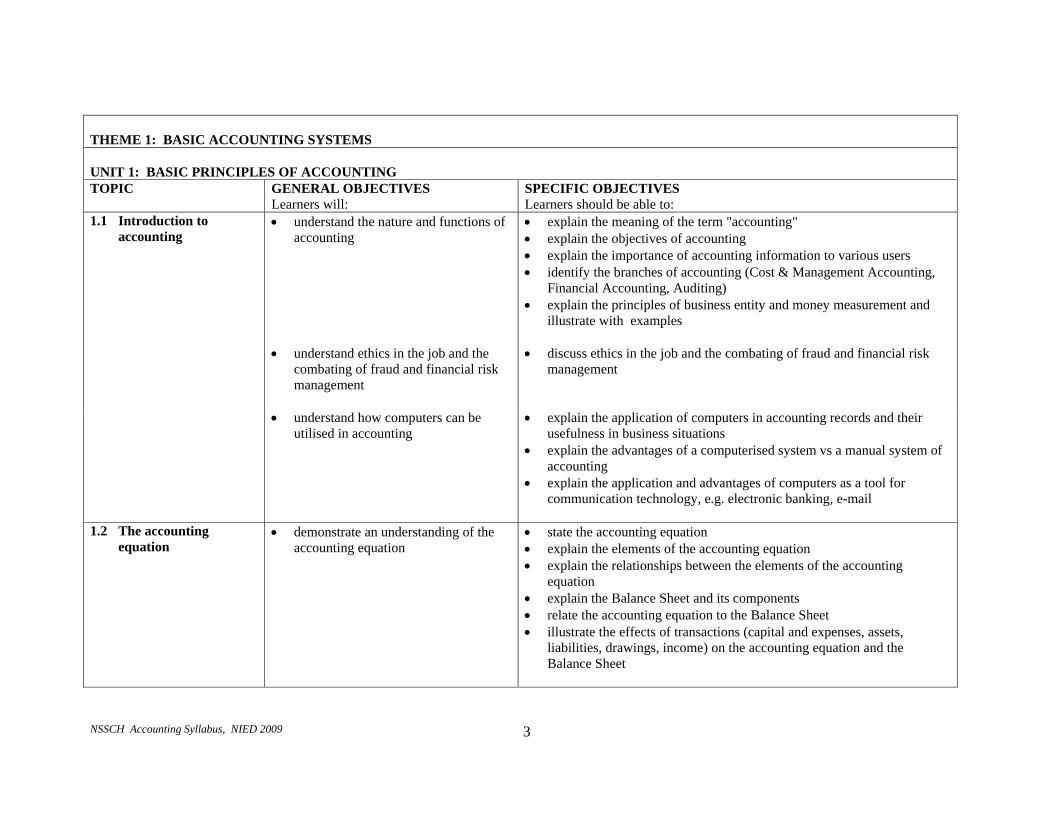

THEME 1: BASIC ACCOUNTING SYSTEMS UNIT 1: BASIC PRINCIPLES OF ACCOUNTING TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

1.1 Introduction to accounting

• understand the nature and functions of accounting

• explain the meaning of the term "accounting" • explain the objectives of accounting • explain the importance of accounting information to various users • identify the branches of accounting (Cost & Management Accounting,

Financial Accounting, Auditing) • explain the principles of business entity and money measurement and

illustrate with examples

• understand ethics in the job and the combating of fraud and financial risk management

• discuss ethics in the job and the combating of fraud and financial risk management

• understand how computers can be utilised in accounting

• explain the application of computers in accounting records and their usefulness in business situations

• explain the advantages of a computerised system vs a manual system of accounting

• explain the application and advantages of computers as a tool for communication technology, e.g. electronic banking, e-mail

1.2 The accounting

equation • demonstrate an understanding of the

accounting equation • state the accounting equation • explain the elements of the accounting equation • explain the relationships between the elements of the accounting

equation • explain the Balance Sheet and its components • relate the accounting equation to the Balance Sheet • illustrate the effects of transactions (capital and expenses, assets,

liabilities, drawings, income) on the accounting equation and the Balance Sheet

NSSCH Accounting Syllabus, NIED 2009 4

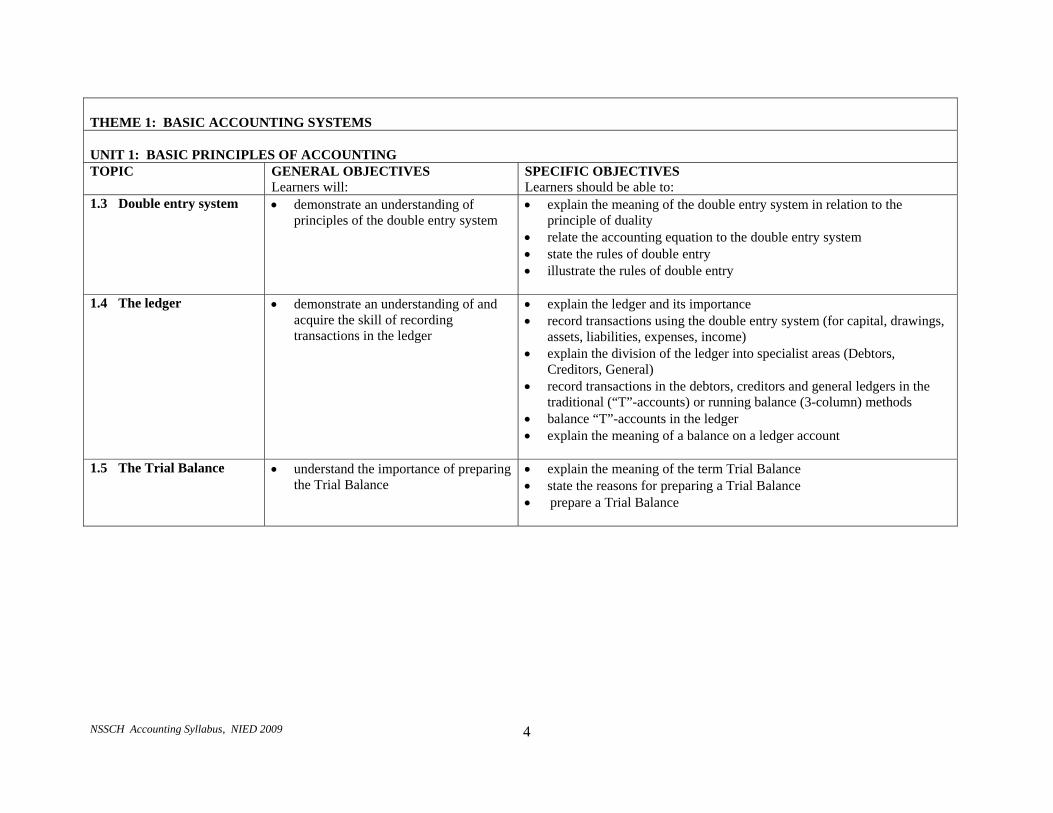

THEME 1: BASIC ACCOUNTING SYSTEMS UNIT 1: BASIC PRINCIPLES OF ACCOUNTING TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

1.3 Double entry system

• demonstrate an understanding of principles of the double entry system

• explain the meaning of the double entry system in relation to the principle of duality

• relate the accounting equation to the double entry system • state the rules of double entry • illustrate the rules of double entry

1.4 The ledger

• demonstrate an understanding of and acquire the skill of recording transactions in the ledger

• explain the ledger and its importance • record transactions using the double entry system (for capital, drawings,

assets, liabilities, expenses, income) • explain the division of the ledger into specialist areas (Debtors,

Creditors, General) • record transactions in the debtors, creditors and general ledgers in the

traditional (“T”-accounts) or running balance (3-column) methods • balance “T”-accounts in the ledger • explain the meaning of a balance on a ledger account

1.5 The Trial Balance • understand the importance of preparing the Trial Balance

• explain the meaning of the term Trial Balance • state the reasons for preparing a Trial Balance • prepare a Trial Balance

NSSCH Accounting Syllabus, NIED 2009 5

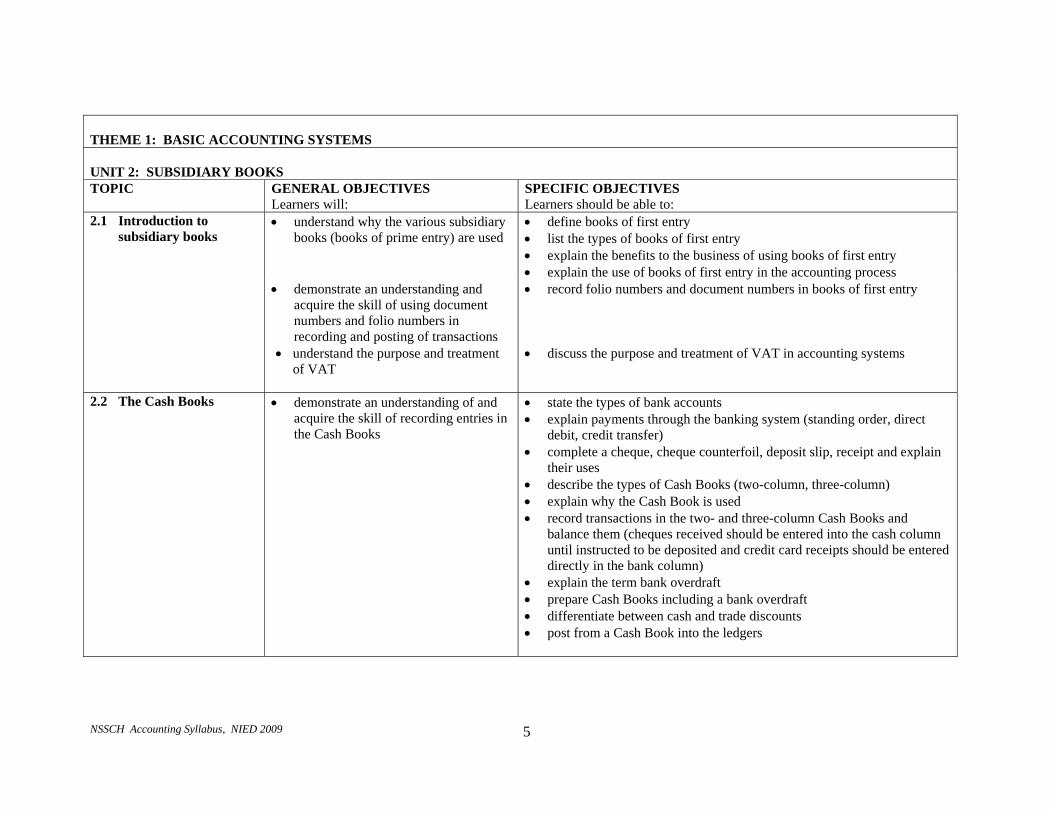

THEME 1: BASIC ACCOUNTING SYSTEMS UNIT 2: SUBSIDIARY BOOKS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

2.1 Introduction to subsidiary books

• understand why the various subsidiary books (books of prime entry) are used

• define books of first entry • list the types of books of first entry • explain the benefits to the business of using books of first entry • explain the use of books of first entry in the accounting process

• demonstrate an understanding and acquire the skill of using document numbers and folio numbers in recording and posting of transactions

• record folio numbers and document numbers in books of first entry

• understand the purpose and treatment of VAT

• discuss the purpose and treatment of VAT in accounting systems

2.2 The Cash Books

• demonstrate an understanding of and acquire the skill of recording entries in the Cash Books

• state the types of bank accounts • explain payments through the banking system (standing order, direct

debit, credit transfer) • complete a cheque, cheque counterfoil, deposit slip, receipt and explain

their uses • describe the types of Cash Books (two-column, three-column) • explain why the Cash Book is used • record transactions in the two- and three-column Cash Books and

balance them (cheques received should be entered into the cash column until instructed to be deposited and credit card receipts should be entered directly in the bank column)

• explain the term bank overdraft • prepare Cash Books including a bank overdraft • differentiate between cash and trade discounts • post from a Cash Book into the ledgers

NSSCH Accounting Syllabus, NIED 2009 6

THEME 1: BASIC ACCOUNTING SYSTEMS UNIT 2: SUBSIDIARY BOOKS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

2.3 Petty Cash Book • demonstrate an understanding of and acquiring the skill of recording entries in the Petty Cash Book

• complete a petty cash voucher and explain its uses • explain why a Petty Cash Book is used • record transactions in the Petty Cash Book using the imprest system and

balance it • post from the Petty Cash Book into the ledgers

2.4 Debtors Journal

• understand the documentation procedures in credit sales

• state the need for credit control • explain the contents of and complete a sales invoice • explain the terms relating to sales on an invoice (including trade

discount, E&OE, cash discount, carriage inwards, carriage outwards)

• demonstrate an understanding of and acquire the skill of recording entries in the Debtors Journal

• explain why the Debtors Journal is used • prepare the Debtors Journal from details extracted from a sales invoice • post from the Debtors Journal to the Debtors Ledger and the General

Ledger

2.5 Creditors Journal • understand the documentation procedures in credit purchases

• explain the importance of checking invoices against delivery notes and purchase orders

• explain the contents of and complete a purchases invoice

• demonstrate an understanding of and acquire the skill of recording entries in the Creditors Journal

• explain why the Creditors Journal is used • prepare the Creditors Journal from details extracted from purchases

invoice • post from the Creditors Journal to the Creditors Ledger and General

Ledger

NSSCH Accounting Syllabus, NIED 2009 7

THEME 1: BASIC ACCOUNTING SYSTEMS UNIT 2: SUBSIDIARY BOOKS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

2.6 Returns Journals • understand the documentation procedures in returns of goods/merchandise

• explain the contents of and complete credit and debit notes • differentiate between a debit note and a credit note

• demonstrate an understanding of and acquire the skill of recording returns inwards and outwards in the Returns Journals

• explain returns inwards and outwards • explain the reasons for returns • explain why the Returns Journals are used • prepare the Debtors Returns and Creditors Returns Journals from details

extracted from credit notes • post from the Debtors Returns and Creditors Returns Journals to the

appropriate ledgers

2.7 General Journal

• demonstrate an understanding of and acquire the skill of recording journal entries

• explain the importance of the General Journal • state the uses of the General Journal • prepare journal entries, including those to record:

- opening entries - bad debts - drawings of stock - donation of goods - interest charged on overdue accounts: interest received and interest

paid - purchase of fixed assets on credit - correction of errors - purchase of consumables on credit - discount allowed cancelled on dishonoured - cheques

• post from the General Journal into the ledgers

2.8 Other business documents

• demonstrate an understanding of the use of a Statement of Account

• explain the use and content of and complete a Statement of Account

NSSCH Accounting Syllabus, NIED 2009 8

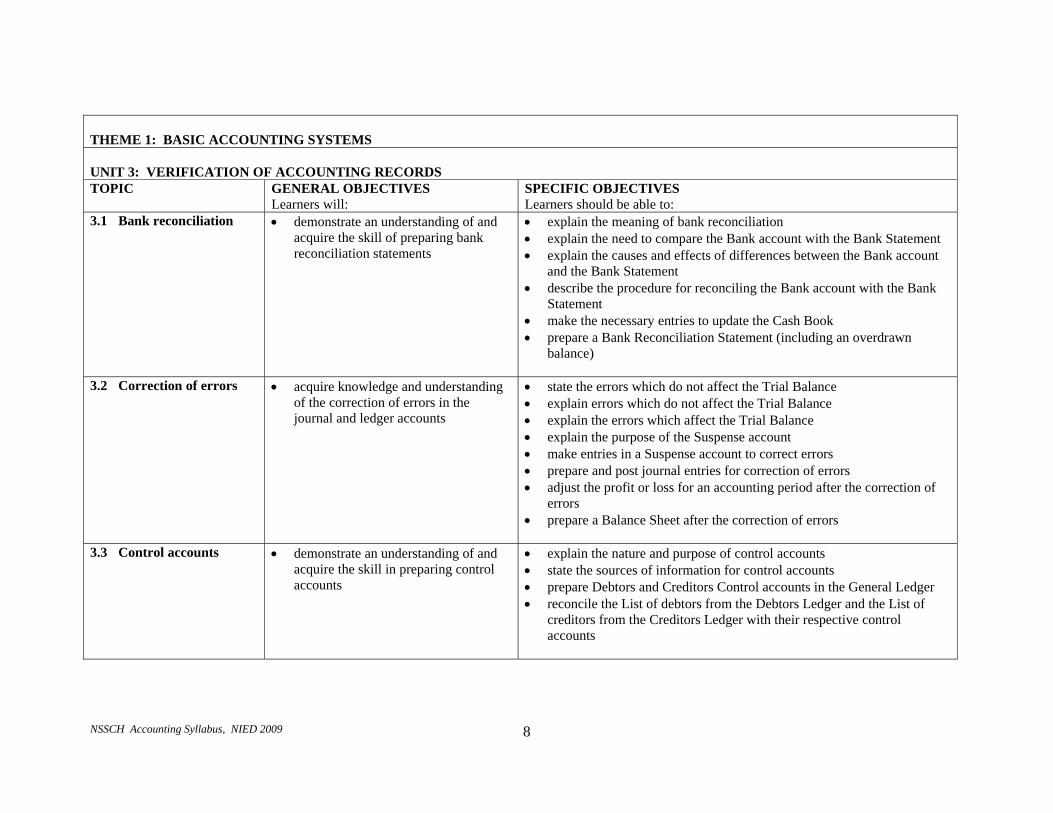

THEME 1: BASIC ACCOUNTING SYSTEMS UNIT 3: VERIFICATION OF ACCOUNTING RECORDS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

3.1 Bank reconciliation

• demonstrate an understanding of and acquire the skill of preparing bank reconciliation statements

• explain the meaning of bank reconciliation • explain the need to compare the Bank account with the Bank Statement • explain the causes and effects of differences between the Bank account

and the Bank Statement • describe the procedure for reconciling the Bank account with the Bank

Statement • make the necessary entries to update the Cash Book • prepare a Bank Reconciliation Statement (including an overdrawn

balance)

3.2 Correction of errors

• acquire knowledge and understanding of the correction of errors in the journal and ledger accounts

• state the errors which do not affect the Trial Balance • explain errors which do not affect the Trial Balance • explain the errors which affect the Trial Balance • explain the purpose of the Suspense account • make entries in a Suspense account to correct errors • prepare and post journal entries for correction of errors • adjust the profit or loss for an accounting period after the correction of

errors • prepare a Balance Sheet after the correction of errors

3.3 Control accounts • demonstrate an understanding of and acquire the skill in preparing control accounts

• explain the nature and purpose of control accounts • state the sources of information for control accounts • prepare Debtors and Creditors Control accounts in the General Ledger • reconcile the List of debtors from the Debtors Ledger and the List of

creditors from the Creditors Ledger with their respective control accounts

NSSCH Accounting Syllabus, NIED 2009 9

THEME 1: BASIC ACCOUNTING SYSTEMS UNIT 4: ACCOUNTING PRINCIPLES TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

4.1 Accounting principles • appreciate the importance and show understanding of the main principles underlying the preparation of accounting statements

• identify the accounting principles (cost, money measurement, business entity, dual aspect, realisation, going-concern, consistency, prudence, accrual/matching, substance over form, materiality)

• explain and illustrate each of the accounting principles • explain the difference between capital and revenue receipt, capital and

revenue expenditure

NSSCH Accounting Syllabus, NIED 2009 10

THEME 2: PREPARATION AND PRINCIPLES OF FINANCIAL STATEMENTS UNIT 1: ACCOUNTS OF THE SOLE TRADER TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

1.1 Final accounts and financial statements

• demonstrate an understanding of how to prepare Trading and Profit and Loss Accounts of a trading business

• explain the position of a sole trader in relation to profit • state the purpose of preparing the Trading and Profit and Loss Accounts • differentiate between gross profit and net profit • close off the nominal accounts affecting the Trading and Profit and Loss

Accounts • explain how the closing stock is valued (lower of cost or net realisable

value) • determine the cost of goods sold and the gross profit in the Trading

Account • draw up Trading and Profit and Loss Accounts in a horizontal/vertical

format

• demonstrate an understanding of how to prepare Income Statements of a sole trader

• draw up an Income Statement from a Trial Balance to calculate gross profit and net profit

• demonstrate an understanding of how to prepare Departmental Trading and Profit and Loss Accounts of a trading business

• prepare simple columnar Trading and Profit and Loss Accounts when dealing with a business with departments

• demonstrate an understanding of how to prepare Balance Sheets of a sole trader

• explain the purpose of and define the term Balance Sheet • identify the components of the Balance Sheet • prepare a Balance Sheet of a sole trader in a horizontal/vertical format

(current assets to be listed in order of liquidity)

NSSCH Accounting Syllabus, NIED 2009 11

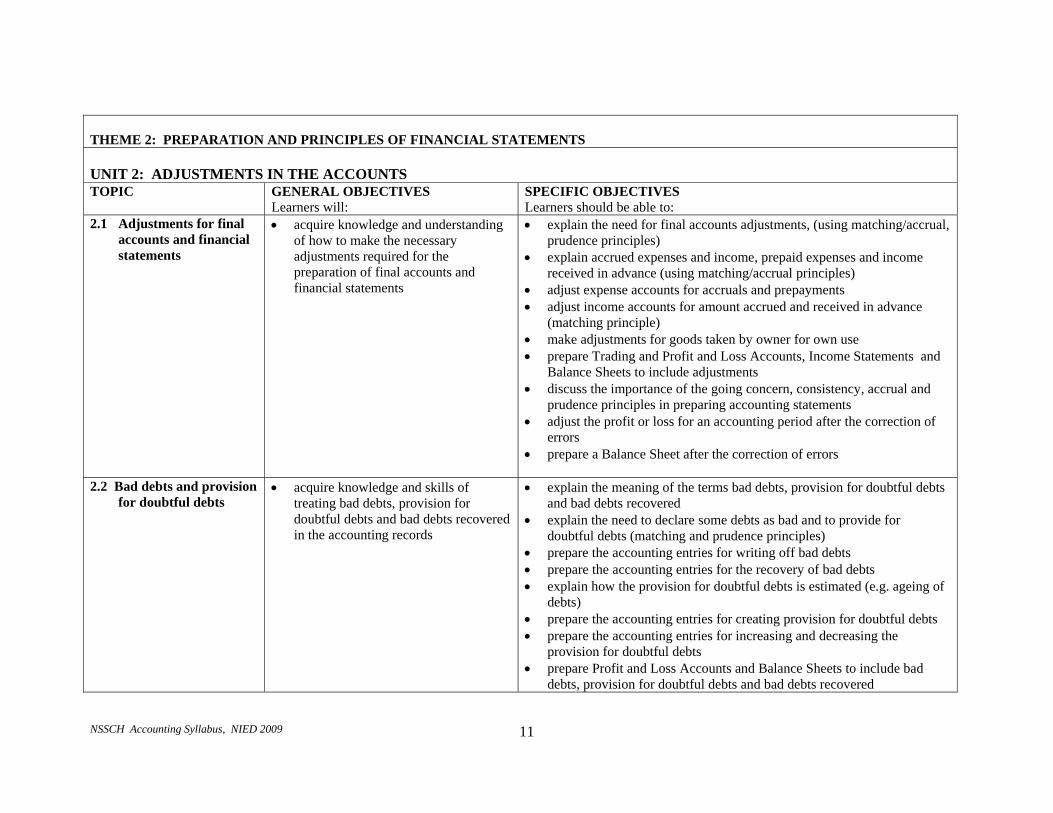

THEME 2: PREPARATION AND PRINCIPLES OF FINANCIAL STATEMENTS UNIT 2: ADJUSTMENTS IN THE ACCOUNTS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

2.1 Adjustments for final accounts and financial statements

• acquire knowledge and understanding of how to make the necessary adjustments required for the preparation of final accounts and financial statements

• explain the need for final accounts adjustments, (using matching/accrual, prudence principles)

• explain accrued expenses and income, prepaid expenses and income received in advance (using matching/accrual principles)

• adjust expense accounts for accruals and prepayments • adjust income accounts for amount accrued and received in advance

(matching principle) • make adjustments for goods taken by owner for own use • prepare Trading and Profit and Loss Accounts, Income Statements and

Balance Sheets to include adjustments • discuss the importance of the going concern, consistency, accrual and

prudence principles in preparing accounting statements • adjust the profit or loss for an accounting period after the correction of

errors • prepare a Balance Sheet after the correction of errors

2.2 Bad debts and provision for doubtful debts

• acquire knowledge and skills of treating bad debts, provision for doubtful debts and bad debts recovered in the accounting records

• explain the meaning of the terms bad debts, provision for doubtful debts and bad debts recovered

• explain the need to declare some debts as bad and to provide for doubtful debts (matching and prudence principles)

• prepare the accounting entries for writing off bad debts • prepare the accounting entries for the recovery of bad debts • explain how the provision for doubtful debts is estimated (e.g. ageing of

debts) • prepare the accounting entries for creating provision for doubtful debts • prepare the accounting entries for increasing and decreasing the

provision for doubtful debts • prepare Profit and Loss Accounts and Balance Sheets to include bad

debts, provision for doubtful debts and bad debts recovered

NSSCH Accounting Syllabus, NIED 2009 12

THEME 2: PREPARATION AND PRINCIPLES OF FINANCIAL STATEMENTS UNIT 2: ADJUSTMENTS IN THE ACCOUNTS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

2.3 Depreciation of fixed assets

• demonstrate an understanding of the nature and calculation of depreciation

• explain the meaning of depreciation and provision for depreciation and its effect on fixed assets (prudence and matching principles)

• explain the causes of depreciation • explain the reasons for depreciation • explain the methods of depreciation (straight line, reducing balance,

revaluation) • calculate depreciation using the above methods taking into account

assets bought or disposed during the year and/or at year end • state the advantages and disadvantages of each of the above methods of

depreciation

• acquire knowledge and understanding of the accounting treatment of depreciation

• record depreciation of fixed assets in the ledger using the Depreciation (expense) and Provision for Depreciation account

• prepare Trading and Profit and Loss Accounts to include depreciation of fixed assets

• record the disposal of fixed assets in the asset account, Provision for Depreciation account and the Disposal account

NSSCH Accounting Syllabus, NIED 2009 13

THEME 2: PREPARATION AND PRINCIPLES OF FINANCIAL STATEMENTS UNIT 3: PARTNERSHIP TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

3.1 Nature of partnership

• understand the nature of partnership

• explain the meaning of the term partnership • explain the features of partnership agreement • explain the position of the partnership when there is no partnership deed

3.2 Accounting for partnership

• demonstrate an understanding of and acquire the skill to prepare the accounts of partnerships

• record entries on the dissolution of a

partnership

• explain the differences between the accounting records of a sole trader and those of a partnership business

• explain the importance of the Appropriation Account • show the treatment of the division of the balance of profit or loss,

interest on capital, interest on drawings, partners’ salaries and interest on partners’ loans in the accounts

• make the other adjustments as detailed in Theme 2, Unit 2; • prepare the following accounts of a partnership:

- Trading Account - Profit and Loss Account - Profit and Loss Appropriation Account (horizontal/vertical)

• differentiate between fixed and fluctuating capital accounts • explain the importance of the current account of partners • prepare the capital and current accounts of partners in the ledger • prepare the partnership Balance Sheet (horizontal/vertical) • explain the meaning of the term goodwill • prepare the accounting entries for goodwill on admission of a new

partner • record the entries (including journal entries) which arise from the

dissolution of a partnership (excluding piecemeal dissolution)

NSSCH Accounting Syllabus, NIED 2009 14

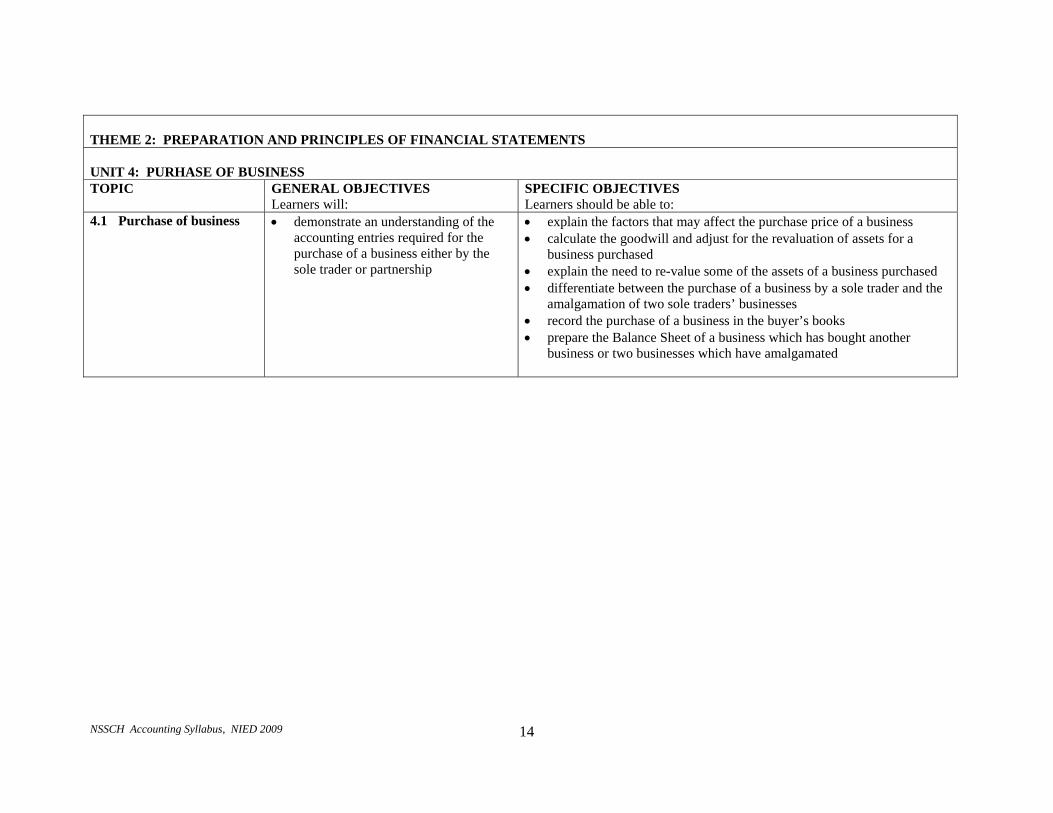

THEME 2: PREPARATION AND PRINCIPLES OF FINANCIAL STATEMENTS UNIT 4: PURHASE OF BUSINESS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

4.1 Purchase of business • demonstrate an understanding of the accounting entries required for the purchase of a business either by the sole trader or partnership

• explain the factors that may affect the purchase price of a business • calculate the goodwill and adjust for the revaluation of assets for a

business purchased • explain the need to re-value some of the assets of a business purchased • differentiate between the purchase of a business by a sole trader and the

amalgamation of two sole traders’ businesses • record the purchase of a business in the buyer’s books • prepare the Balance Sheet of a business which has bought another

business or two businesses which have amalgamated

NSSCH Accounting Syllabus, NIED 2009 15

THEME 2: PREPARATION AND PRINCIPLES OF FINANCIAL STATEMENTS UNIT 5: INTRODUCTION TO COMPANY ACCOUNTS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

5.1 Nature of limited liability companies

• know and understand the capital structure of limited liability companies

• explain the meaning of the term "limited liability company" • explain shares (nominal and market value) and debentures • explain the difference between ordinary shares and preference shares

(including non-cumulative, cumulative, participating, redeemable preference shares)

• explain the difference between authorised and issued share capital of a limited company

• explain the difference between capital and revenue reserves • explain the difference between reserves and provisions

5.2 Accounting for limited liability companies

• demonstrate an understanding of and acquire the skill of preparing accounting entries for the issue of shares

• record the entries (including journal entries) which arise from the issue of shares at par or at a premium

• demonstrate an understanding of and acquire the skill of preparing simple accounts of limited liability companies

• explain the differences between the final accounts of a sole trader or partnership business and those of a limited liability company

• explain the composition of the final accounts of a limited liability company

• explain the importance of the Appropriation Account • explain the meaning of the terms "interim dividend" and "final dividend" • calculate and record interim and final dividends

• demonstrate an understanding of and acquire the skill of preparing simple accounts of limited liability companies

• explain capital reserves, general reserves, special reserves, revaluation reserves and retained profit

• prepare a simple Trading and Profit and Loss and Appropriation Account of a limited company

• explain and calculate the shareholders’ funds • prepare a simple Balance Sheet with notes of a limited liability company

NSSCH Accounting Syllabus, NIED 2009 16

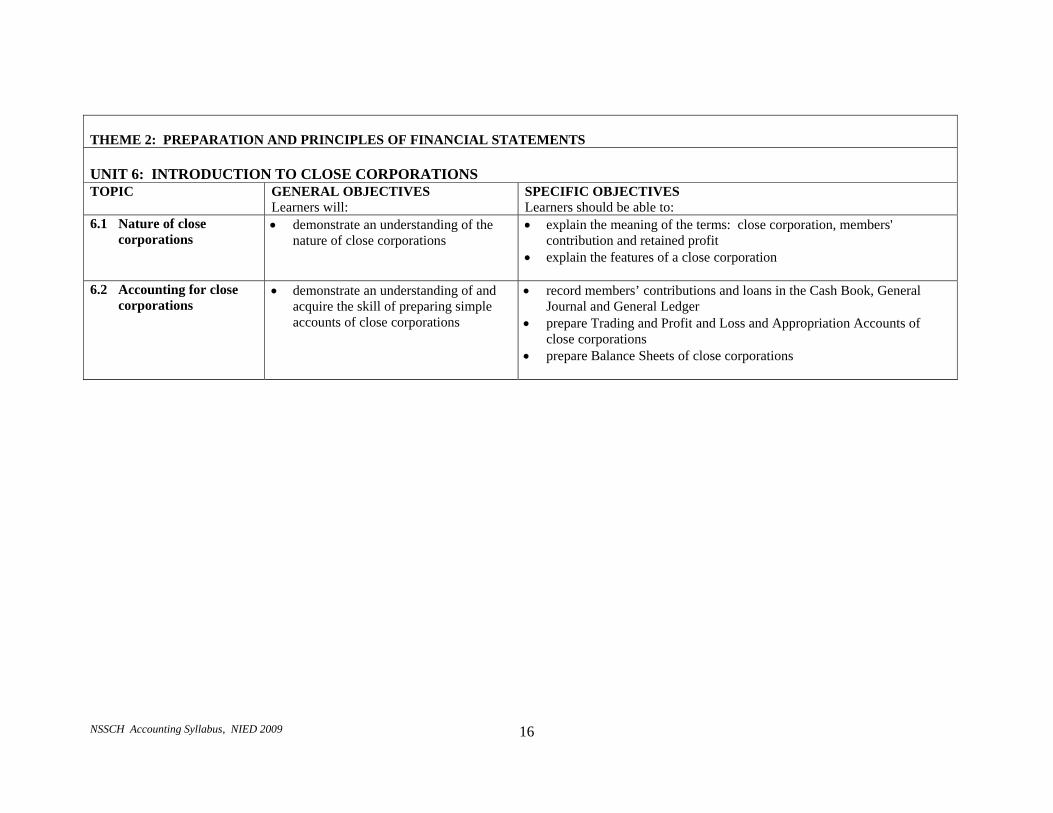

THEME 2: PREPARATION AND PRINCIPLES OF FINANCIAL STATEMENTS UNIT 6: INTRODUCTION TO CLOSE CORPORATIONS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

6.1 Nature of close corporations

• demonstrate an understanding of the nature of close corporations

• explain the meaning of the terms: close corporation, members' contribution and retained profit

• explain the features of a close corporation

6.2 Accounting for close corporations

• demonstrate an understanding of and acquire the skill of preparing simple accounts of close corporations

• record members’ contributions and loans in the Cash Book, General Journal and General Ledger

• prepare Trading and Profit and Loss and Appropriation Accounts of close corporations

• prepare Balance Sheets of close corporations

NSSCH Accounting Syllabus, NIED 2009 17

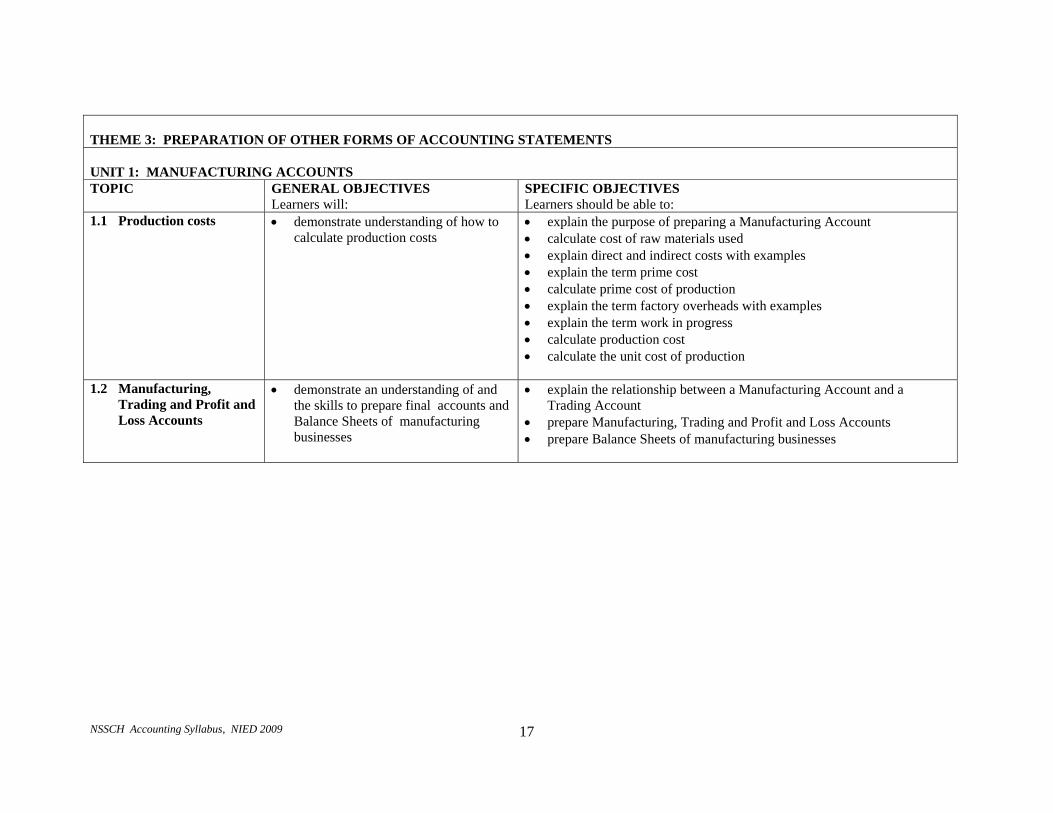

THEME 3: PREPARATION OF OTHER FORMS OF ACCOUNTING STATEMENTS UNIT 1: MANUFACTURING ACCOUNTS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

1.1 Production costs

• demonstrate understanding of how to calculate production costs

• explain the purpose of preparing a Manufacturing Account • calculate cost of raw materials used • explain direct and indirect costs with examples • explain the term prime cost • calculate prime cost of production • explain the term factory overheads with examples • explain the term work in progress • calculate production cost • calculate the unit cost of production

1.2 Manufacturing, Trading and Profit and Loss Accounts

• demonstrate an understanding of and the skills to prepare final accounts and Balance Sheets of manufacturing businesses

• explain the relationship between a Manufacturing Account and a Trading Account

• prepare Manufacturing, Trading and Profit and Loss Accounts • prepare Balance Sheets of manufacturing businesses

NSSCH Accounting Syllabus, NIED 2009 18

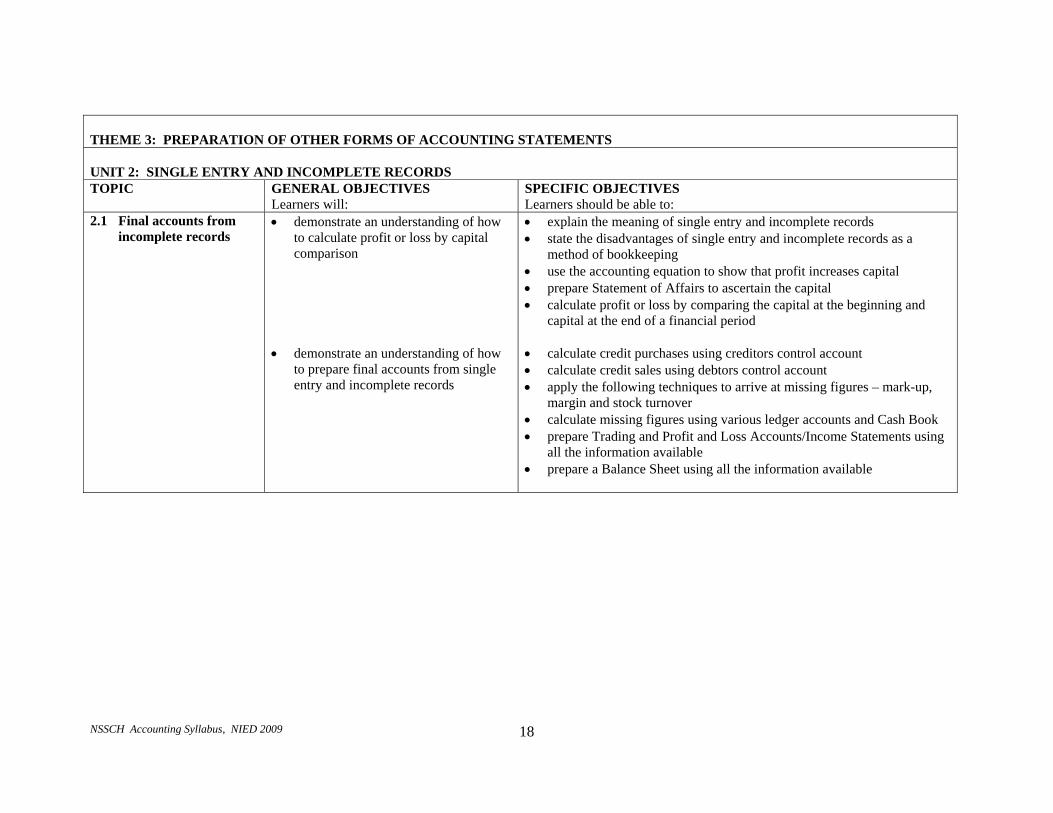

THEME 3: PREPARATION OF OTHER FORMS OF ACCOUNTING STATEMENTS UNIT 2: SINGLE ENTRY AND INCOMPLETE RECORDS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

2.1 Final accounts from incomplete records

• demonstrate an understanding of how to calculate profit or loss by capital comparison

• explain the meaning of single entry and incomplete records • state the disadvantages of single entry and incomplete records as a

method of bookkeeping • use the accounting equation to show that profit increases capital • prepare Statement of Affairs to ascertain the capital • calculate profit or loss by comparing the capital at the beginning and

capital at the end of a financial period

• demonstrate an understanding of how to prepare final accounts from single entry and incomplete records

• calculate credit purchases using creditors control account • calculate credit sales using debtors control account • apply the following techniques to arrive at missing figures – mark-up,

margin and stock turnover • calculate missing figures using various ledger accounts and Cash Book • prepare Trading and Profit and Loss Accounts/Income Statements using

all the information available • prepare a Balance Sheet using all the information available

NSSCH Accounting Syllabus, NIED 2009 19

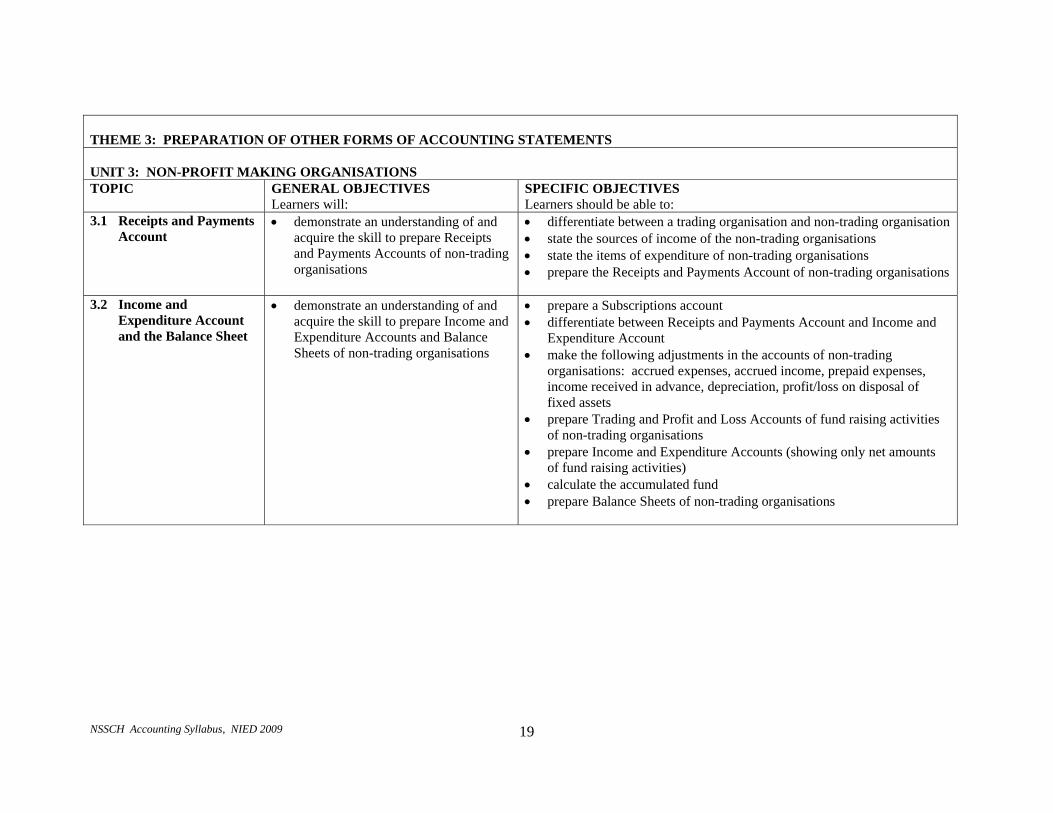

THEME 3: PREPARATION OF OTHER FORMS OF ACCOUNTING STATEMENTS UNIT 3: NON-PROFIT MAKING ORGANISATIONS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

3.1 Receipts and Payments Account

• demonstrate an understanding of and acquire the skill to prepare Receipts and Payments Accounts of non-trading organisations

• differentiate between a trading organisation and non-trading organisation • state the sources of income of the non-trading organisations • state the items of expenditure of non-trading organisations • prepare the Receipts and Payments Account of non-trading organisations

3.2 Income and Expenditure Account and the Balance Sheet

• demonstrate an understanding of and acquire the skill to prepare Income and Expenditure Accounts and Balance Sheets of non-trading organisations

• prepare a Subscriptions account • differentiate between Receipts and Payments Account and Income and

Expenditure Account • make the following adjustments in the accounts of non-trading

organisations: accrued expenses, accrued income, prepaid expenses, income received in advance, depreciation, profit/loss on disposal of fixed assets

• prepare Trading and Profit and Loss Accounts of fund raising activities of non-trading organisations

• prepare Income and Expenditure Accounts (showing only net amounts of fund raising activities)

• calculate the accumulated fund • prepare Balance Sheets of non-trading organisations

NSSCH Accounting Syllabus, NIED 2009 20

THEME 4: INTERPRETATION OF ACCOUNTING STATEMENTS UNIT 1: RATIOS AND INTERPRETATION TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

1.1 Ratios

• know the calculation of accounting ratios and their uses for sole traders, partnerships and limited companies and close corporations

• explain the meaning of the term accounting ratios • classify accounting ratios into profitability, liquidity, efficiency and

investment ratios • define liquidity ratios • calculate liquidity ratios (current, quick) • explain the uses of liquidity ratios • define efficiency ratios • calculate efficiency ratios (rate of stock turn, collection period for

debtors, payment period for creditors) • explain the uses of efficiency ratios • define profitability ratios • calculate profitability ratios (percentage of gross profit and net profit to

sales, net profit as a percentage of capital employed) • explain the uses of profitability ratios • calculate the working capital and the effects of transactions on it • make suggestions and recommendations for improving profitability and

working capital • define investment ratios • calculate investment ratios (earnings per share, price/earnings) • explain the uses of the investment ratios

1.2 Interpretation and evaluation of final accounts

• understand the importance of accounting ratios for the interpretation and evaluation of business performance

• discuss the importance of accounting ratios to owner(s)/manager(s), trade creditors, lenders, employees and potential investors

• compare accounting ratios over time and for different businesses to advise management

• discuss the limitations of accounting ratios

• demonstrate an understanding of and acquire the skill of preparing simple cash flow statements

• prepare simple cash flow statements

NSSCH Accounting Syllabus, NIED 2009 21

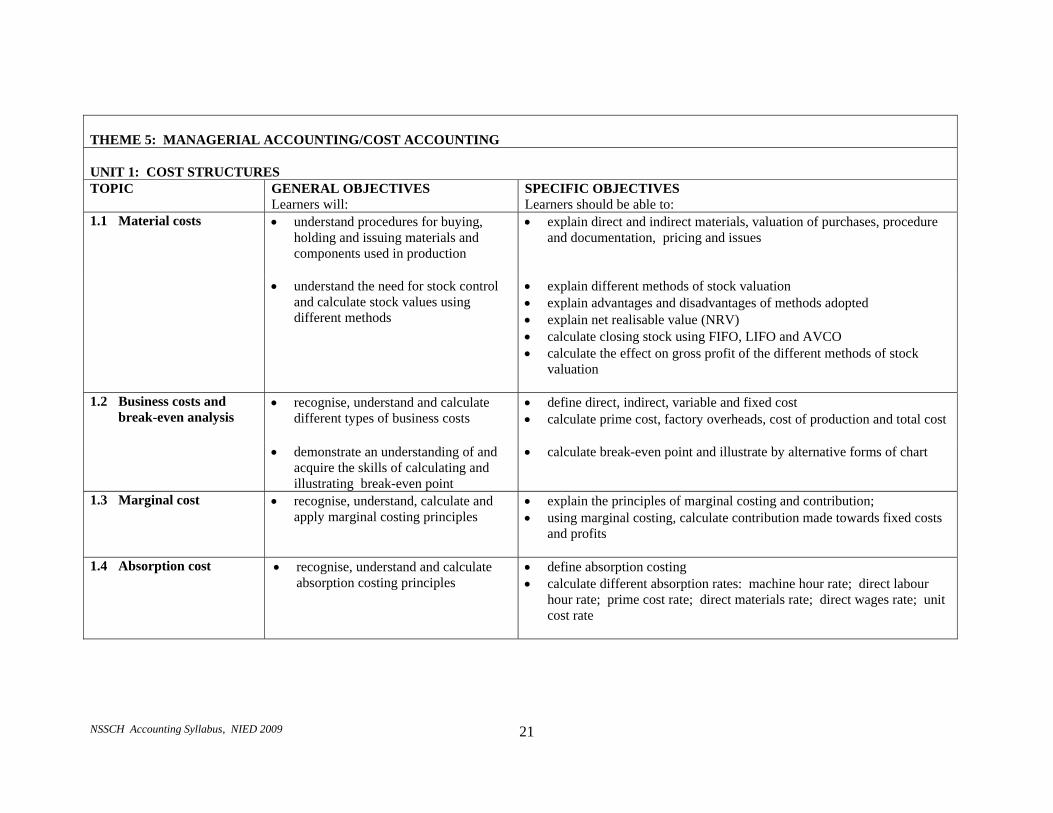

THEME 5: MANAGERIAL ACCOUNTING/COST ACCOUNTING UNIT 1: COST STRUCTURES TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

1.1 Material costs

• understand procedures for buying, holding and issuing materials and components used in production

• explain direct and indirect materials, valuation of purchases, procedure and documentation, pricing and issues

• understand the need for stock control and calculate stock values using different methods

• explain different methods of stock valuation • explain advantages and disadvantages of methods adopted • explain net realisable value (NRV) • calculate closing stock using FIFO, LIFO and AVCO • calculate the effect on gross profit of the different methods of stock

valuation

1.2 Business costs and break-even analysis

• recognise, understand and calculate different types of business costs

• define direct, indirect, variable and fixed cost • calculate prime cost, factory overheads, cost of production and total cost

• demonstrate an understanding of and acquire the skills of calculating and illustrating break-even point

• calculate break-even point and illustrate by alternative forms of chart

1.3 Marginal cost

• recognise, understand, calculate and apply marginal costing principles

• explain the principles of marginal costing and contribution; • using marginal costing, calculate contribution made towards fixed costs

and profits

1.4 Absorption cost • recognise, understand and calculate absorption costing principles

• define absorption costing • calculate different absorption rates: machine hour rate; direct labour

hour rate; prime cost rate; direct materials rate; direct wages rate; unit cost rate

NSSCH Accounting Syllabus, NIED 2009 22

THEME 5: MANAGERIAL ACCOUNTING UNIT 2: BUDGETS AND BUDGETARY CONTROL TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

2.1 Budgets • demonstrate an understanding of the uses of budgets and budgetary control and acquire the skill to prepare simple budgets

• prepare simple cash budgets and production budgets • explain the control function of budgets • advise management on appropriate courses of action

THEME 6: COMPILATION OF REPORTS TOPIC GENERAL OBJECTIVES

Learners will: SPECIFIC OBJECTIVES Learners should be able to:

Reports • compile reports using relevant data • aid management in decision-making by reporting on and analysing data (including managerial costing procedures, ratios, methods of depreciation)

NSSCH Accounting Syllabus, NIED 2009 23

5. ASSESSMENT OBJECTIVES

The four assessment objectives in Accounting are:

A Knowledge with understanding B Application C Analysis and Evaluation D Judgement and Decision Making A description of each assessment objective follows:

A KNOWLEDGE WITH UNDERSTANDING

Learners should be able to:

1. demonstrate knowledge and understanding of facts, terms, principles and techniques appropriate to the syllabus;

2. demonstrate understanding of knowledge through numeracy, literacy, presentation and interpretation;

(Questions assessing these objectives will often begin with words such as: define, list, outline, write up, record, calculate, compute, prepare, draw up, explain.)

B APPLICATION

Learners should be able to:

1. apply knowledge and information to a variety of accounting situations appropriate to their level of attainment;

2. recognise, select and organise relevant data in order to identify needs of business in written, numerical and diagrammatic form;

3. present information in an appropriate accounting format;

(Questions assessing these skills will often begin with words such as: compare, assess, consider, write up, record, calculate, prepare, draw up, discuss, etc.)

C ANALYSIS AND EVALUATION

Learners should be able to:

1. interpret, analyse and evaluate accounting information, and draw reasoned conclusions;

2. display an understanding of the role and the limitations of accounting information as a basis for decision making.

(Questions assessing these skills may begin with words such as: evaluate, analyse, organise, compare, discuss, examine, etc.)

D JUDGEMENT AND DECISION MAKING

Learners should be able to:

1. present reasoned explanations, understand implications and communicate in an accurate and logical manner;

2. make reasoned judgements and present appropriate recommendations and formulate valid conclusions.

(Questions assessing these objectives will often begin with words or phrases such as: suggest, advise, comment on, present, interpret, calculate, prepare, etc.)

NSSCH Accounting Syllabus, NIED 2009 24

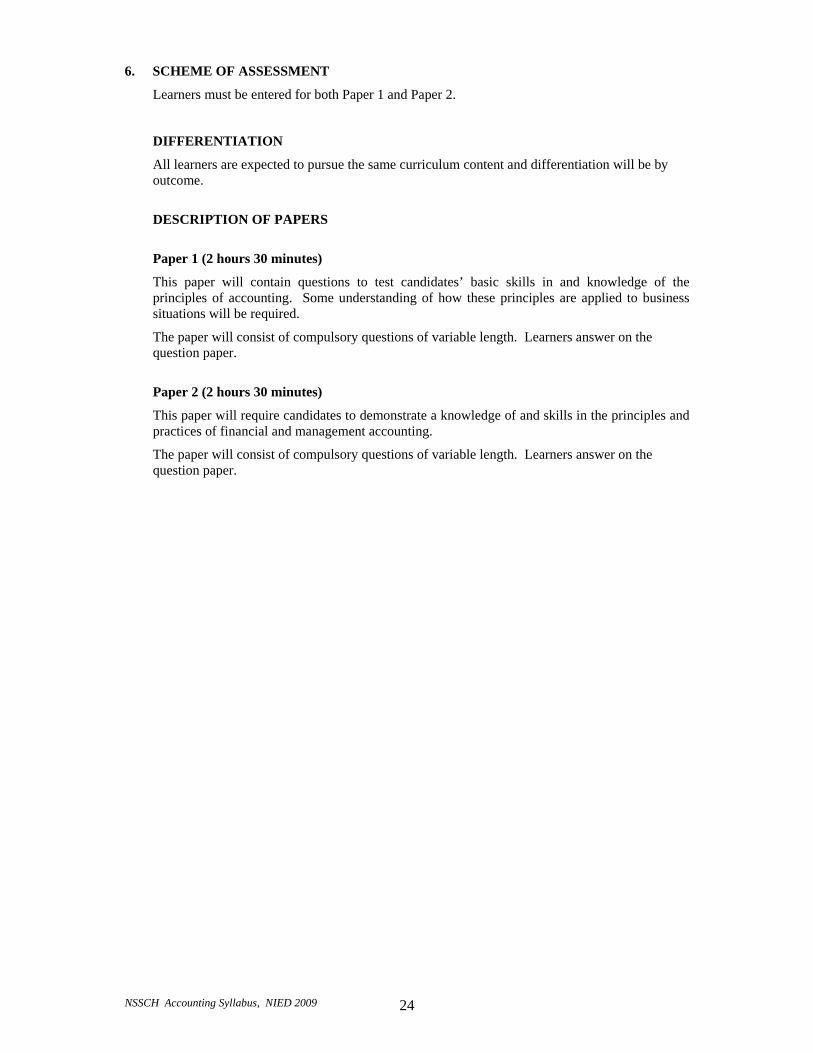

6. SCHEME OF ASSESSMENT

Learners must be entered for both Paper 1 and Paper 2.

DIFFERENTIATION

All learners are expected to pursue the same curriculum content and differentiation will be by outcome.

DESCRIPTION OF PAPERS

Paper 1 (2 hours 30 minutes)

This paper will contain questions to test candidates’ basic skills in and knowledge of the principles of accounting. Some understanding of how these principles are applied to business situations will be required.

The paper will consist of compulsory questions of variable length. Learners answer on the question paper.

Paper 2 (2 hours 30 minutes)

This paper will require candidates to demonstrate a knowledge of and skills in the principles and practices of financial and management accounting.

The paper will consist of compulsory questions of variable length. Learners answer on the question paper.

NSSCH Accounting Syllabus, NIED 2009 25

7. SPECIFICATION GRID

The relationship between the assessment objectives and components of the schemes of assessment.

Assessment Objectives Paper 1 - Marks Paper 2 - Marks Weighting of Assessment Objectives

A Knowledge with Understanding 40 35 25 %

B Application 60 60 40 %

C Analysis and Evaluation 35 35 23.3 %

D Judgement and Decision Making 15 20 11,7 %

Total marks 150 150 100 %

Weighting 50 % 50 %

The marks given to test the assessment objectives give an indication of their relative importance in each paper.

NSSCH Accounting Syllabus, NIED 2009 26

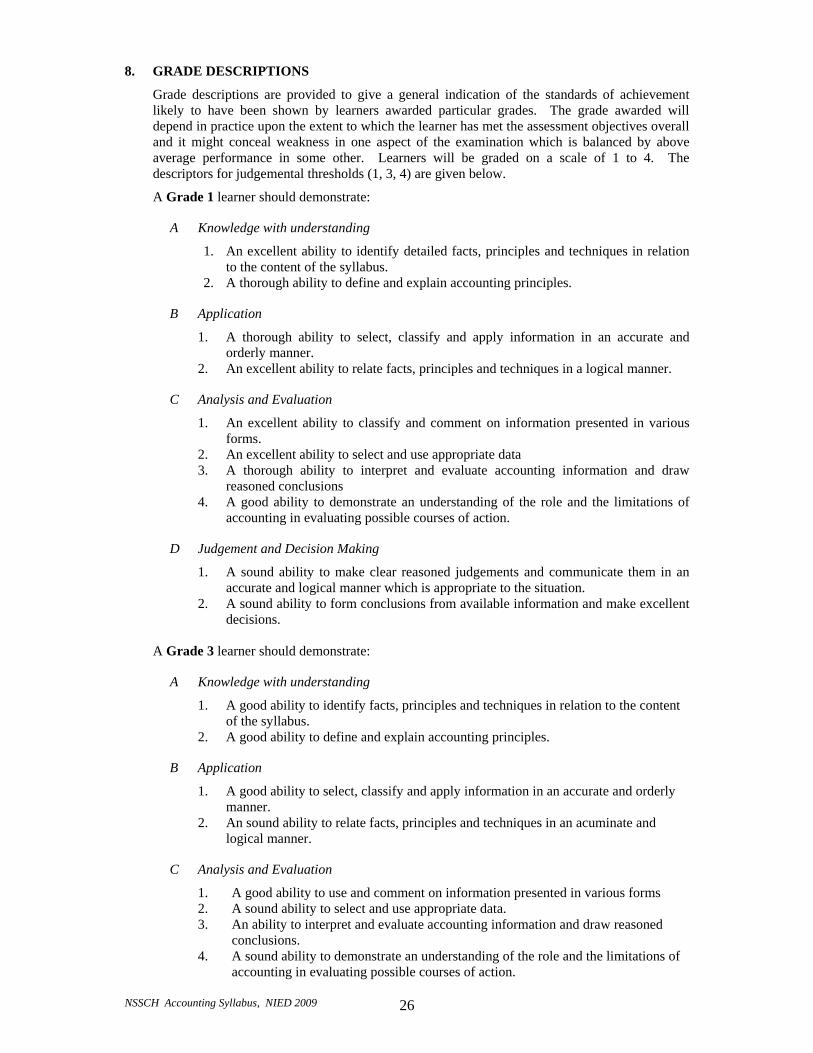

8. GRADE DESCRIPTIONS

Grade descriptions are provided to give a general indication of the standards of achievement likely to have been shown by learners awarded particular grades. The grade awarded will depend in practice upon the extent to which the learner has met the assessment objectives overall and it might conceal weakness in one aspect of the examination which is balanced by above average performance in some other. Learners will be graded on a scale of 1 to 4. The descriptors for judgemental thresholds (1, 3, 4) are given below.

A Grade 1 learner should demonstrate:

A Knowledge with understanding

1. An excellent ability to identify detailed facts, principles and techniques in relation to the content of the syllabus.

2. A thorough ability to define and explain accounting principles.

B Application

1. A thorough ability to select, classify and apply information in an accurate and orderly manner.

2. An excellent ability to relate facts, principles and techniques in a logical manner.

C Analysis and Evaluation

1. An excellent ability to classify and comment on information presented in various forms.

2. An excellent ability to select and use appropriate data 3. A thorough ability to interpret and evaluate accounting information and draw

reasoned conclusions 4. A good ability to demonstrate an understanding of the role and the limitations of

accounting in evaluating possible courses of action.

D Judgement and Decision Making

1. A sound ability to make clear reasoned judgements and communicate them in an accurate and logical manner which is appropriate to the situation.

2. A sound ability to form conclusions from available information and make excellent decisions.

A Grade 3 learner should demonstrate:

A Knowledge with understanding

1. A good ability to identify facts, principles and techniques in relation to the content of the syllabus.

2. A good ability to define and explain accounting principles.

B Application

1. A good ability to select, classify and apply information in an accurate and orderly manner.

2. An sound ability to relate facts, principles and techniques in an acuminate and logical manner.

C Analysis and Evaluation

1. A good ability to use and comment on information presented in various forms 2. A sound ability to select and use appropriate data. 3. An ability to interpret and evaluate accounting information and draw reasoned

conclusions. 4. A sound ability to demonstrate an understanding of the role and the limitations of

accounting in evaluating possible courses of action.

NSSCH Accounting Syllabus, NIED 2009 27

D Judgement and Decision Making

1. An ability to make reasoned judgements. 2. An ability to form conclusions from available information and make appropriate

decisions. A Grade 4 learner should demonstrate:

A Knowledge with Understanding

1. An ability to recall and use facts, principles and techniques in relation to the content of the syllabus.

2. A familiarity with definitions of accounting principles.

B Application

1. An ability to select, classify and apply information in an orderly manner. 2. An ability to relate facts, principles and techniques to some situations.

C Analysis and Evaluation

1. An ability to classify and present data in a simple way and some ability to select relevant information from a set of data.

2. An ability to select and use appropriate data. 3. An ability to gather information relating to a particular topic, present it in an

ordered manner and draw some basic conclusions.

D Judgement and Decision Making

1 An ability to understand implications and make recommendations.

NSSCH Accounting Syllabus, NIED 2009 28

9. GLOSSARY

Business entity The business and its owner are separate business entities and therefore their affairs should be treated apart from each other

Accounting equation An equation used in accounting that states that in a business, Assets = Owner’s equity + Liabilities

Trial balance A list of all the balances in the General Ledger as well as cash and bank balances from the Cash Book and the petty cash balance from the Petty Cash Book

Bank overdraft The balance owed to the bank, because more money was spent than was available in a current bank account

Imprest system The system according to which the petty cash float is restored each month by a payment of cash exactly equal to the total spent

Returns inwards Goods sold on credit to a customer and returned for some reason to be refunded for (Sales returns)

Returns outwards Goods bought on credit from a supplier and returned for some reason to be refunded for (Purchases returns)

Dishonoured cheque: A cheque which is found to be worth nothing as the bank on which it is drawn refuses to pay it.

Bank reconciliation To reconcile the bank balance according to the Bank Statement with the bank balance of the Cash Book

Dual aspect Accounting deals with two aspects of a business: Double-entry bookkeeping (giving and receiving)

Realisation Profits (gains) can only be shown when it is actually been earned. Revenue (income) is only realized when the legal title to the goods passes from the seller to the buyer

Going-concern A business is seen as a going concern if it is to continue for the foreseeable future

Prudence Profits should not be overstated (allowed for foreseeable losses) and fixed assets should not be over-valued

Accrual/matching Profit is the difference between the revenue and the expenses incurred in generating that revenue, within a certain period. Take accruals and prepayments into account

Substance over form Where the legal form and real substance of a transaction differs, accounting should show the transaction according to its real substance, i.e. how the transaction affects the economic situation of the business

Materiality Something should only be included in the financial statements if it would be of interest to the stakeholders

Gross profit The difference between sales revenue and the cost of goods sold where revenue exceeds the cost of goods sold

Net profit The difference between sales revenue plus other income and cost of goods sold plus other expenses, where revenue plus other income exceeds cost of goods sold plus other expenses

NSSCH Accounting Syllabus, NIED 2009 29

(Sales – Cost of sales + other income – expenses)

Liquidity The ability of a business relating to its cash position (how quickly assets can be turned into cash), to pay its liabilities when due

Bad debts The actual amount that a business will not be able to collect from debtors, which is written off

Doubtful debts Estimated amount which are not bad debts yet, but are likely to become bad debts

Depreciation Decrease in value of fixed assets over time

Partnership A business with two or more owners working together to make a profit

Prime cost The total cost of direct raw material and direct labour spent on a product in the manufacturing process

Factory overhead Those factory costs which are associated with the manufacturing process but not directly identifiable as a part of the cost of the finished product

Work in progress Products where the production process has begun but has not been completed on the date on which the accounting records are closed

Single entry Where a transaction is recorded on either the debit or the credit side, instead of both

Mark-up The percentage added on to the cost price, which represents the gross profit

Margin The percentage of the selling price that represents the gross profit

Stock-turnover The number of times that the stock of a business is replaced during an accounting period

Close corporation Form of business for smaller businesses; a less complex and more easily administered legal entity

Contribution by members Members of a close corporation obtain a member’s interest if a contribution of one or more of the following is made: cash, property, services rendered

Financing requirements Close corporation must meet certain solvency and liquidity requirements when certain payments are made

Founding statement Document prepared with a specific content for registration by the Registrar

Loans to members Loans to members may be made only if the prior consent in writing of all members are requirement has been met

Retained income Net income not distributed to members in a specific year; will become available in a following financial year for distribution

Statement of net investments Statement supplying the aggregate balances and changes in respect of members’ contributions, retained income, loans to members and loans from members

NSSCH Accounting Syllabus, NIED 2009 30

Articles of association Document containing regulations for internal matters and management of a particular company

Audit fees Amount paid to company’s auditors

Authorised share capital Total capital amount with which the company has been registered, as mentioned in the memorandum of association

Broker Person who buys and sells shares on behalf of a third party

Capital reserves Share premium + Capital redemption Reserve + Revaluation Reserve

Cash flow statement Statement showing the source and application of all financial sources during an accounting period

Certificate of incorporation Certificate issued by Registrar of Companies to public company, granting the right to commence business.

Company Legally constituted society of people with common capital and a legal, common objective, usually to make a profit

Directors’ fees Amount paid to directors of a company

Dividends Compensation received by shareholders for capital invested in a company; declared only from income available for appropriation

External users Users of a company’s financial statements; persons not directly concerned with management of the company

Income tax Amount paid by persons and legal entities on their net earnings to Receiver of Revenue

Interim dividends Dividends declared and paid from income by directors of company during an accounting period

Internal users Users of a company’s financial statements; people normally employed by the firm and responsible for its management

Issued share capital Part of authorised share capital already issued

Legal entity Competent body regarded as a person in legal matters, with contractual capacity

Memorandum of association Document stating the main objective of a company, the general nature of the business, the name of the company and details on the amount of share capital with which the company is to be registered

Nominal share capital See Authorised share capital

Nominal value Value allocated to a share when issued

Ordinary shares Shares entitling the shareholder to a share in the distributable income of the company in the form of a dividend after preference dividend are paid

Par value See Nominal value

Preference shares Shares entitling the shareholder to a fixed dividend, providing that sufficient income is available and that the dividend is declared in accordance with the articles of association

NSSCH Accounting Syllabus, NIED 2009 31

Private company Company of which the minimum number of shareholders is one and the maximum number of shareholders is fifty, the public being prohibited from buying shares in a private company

Prospectus Invitation to the public to buy shares in a particular company

Provisional income tax Income tax to be calculated by companies on their estimated income every six months and paid to the Receiver of Revenue; these amounts being taken into account by the Receiver of Revenue when the company’s assessment is calculated

Public company Company of which the minimum number of members is seven and the maximum number of members is limited to the number of shares issued, the public being invited to buy shares by means of a prospectus

Register of dividends Book in which details on dividend paid and/or due to individual shareholders are written up

Register of members List kept by a company of all its shareholders

Registered share capital See Authorised share capital

Reserve share capital See Unissued share capital

Retained income Share of a company’s income which is not appropriated; also known as unappropriated income

Revenue Reserves Retain profit

Share capital Capital of a company

Share certificate Certificate containing full details of shares owned by holder of certificate

Shareholders People who own shares in a company

Share premium Amount received because the issuing price is higher than the par value of a share; part of shareholders’ equity

Shares Units into which the capital of a company is divided (shares are negotiable)

Special reserves Capital reserves + revenue reserves for a specific project

Stock exchange Place where shares are traded

Taxable income Amount on which the income tax payable by a company is calculated

Tax assessment Document sent to companies by Receiver of Revenue indicating amount due to the company or due by the company in respect of income tax

Tax return Document completed by companies and sent to the Receiver of Revenue giving full details of net income made by the company during an accounting period

Unissued share capital Difference between authorised and issued share capital

NSSCH Accounting Syllabus, NIED 2009 i

ANNEXE A INTERNATIONAL STANDARDS TERMINOLOGY The following list has been collated to help Centres prepare for the introduction of international standards to CIE accounting syllabuses. It is anticipated that standards which are well known, and are relevant to the level of study, will be brought into question papers, mark schemes and associated documents. Centres are encouraged to apply the new terminology to their teaching and learning materials so that candidates sitting for examination will be aware of the terms. Candidates will not be penalised for using different terms.

International usage Current CIE/UK usage Balance sheet Balance sheet Bank (and other) loans/ Interest bearing loans and borrowing

Loans repayable after 12 months

Bank overdrafts and loans/ Interest bearing loans and borrowing

Loans repayable within 12 months

Capital or Equity/Shareholders’ Equity Capital Cash (and cash equivalents) Bank and cash Cost of sales Cost of goods sold Current assets Current assets Current liabilities Current liabilities/

Creditors: amounts due within 12 months Finance costs Interest payable Finance Income/Investment revenues Interest receivable Financial Statements Final accounts Gross profit Gross profit Income statement Trading and profit and loss account Intangible assets Goodwill etc. Inventory/Inventories (of raw materials and finished goods)

Stock

Investment property Investments Non-current assets Fixed assets Non-current liabilities Long term liabilities/

Creditors: amounts falling due after more than one year

Other operating expenses Sundry expenses (administration and distribution)

Other operating income Sundry income Other payables Accruals Other receivables Prepayments Plant and equipment Plant and equipmentProfit (before tax) for the year Net Profit Property Land and buildings Raw materials Ordinary goods purchased

Purchases

Revenue Sales Share capital Share capital Trade payables Creditors Trade receivables Debtors Work in progress Work in progress

The National Institute for Educational Development P/Bag 2034 Okahandja NAMIBIA Telephone: +64 62 509000 Facsimile: + 64 62 509073 E-mail: [email protected] Website: http://www.nied.edu.na © NIED 2009