million ton deficit –fact or...

TRANSCRIPT

Page 1

MILLION TON DEFICIT – FACT OR FICTION?CMAA – MIAMI March 13,2015Pamela Thornton

Oliver Tritton

March 15

Disclaimer

• Source of data: Armajaro, unless otherwise stated. The fund(s) mentioned herein are exempted companies incorporated with limited liability in the Cayman Islands as an open-ended

investment company. The Fund is an unregulated collective investment scheme for the purposes of the Financial Services and Markets Act 2000 of the United Kingdom (the “Act”). The

promotion of the Fund and the distribution of this document in the United Kingdom is accordingly restricted by law. Shares in the fund are not available for sale in any state or

jurisdiction in which such sale would be prohibited. Please note, the fund has not been registered, nor will be registered, under the U.S. Investment Company Act of 1940, as amended,

or the Securities Act of 1933, as amended, and may not be sold directly or indirectly in the U.S. or to a US person.

• The information and opinions contained in this document are for background purposes only and do not purport to be full or complete. No reliance may be placed for any purpose on the

information or opinions contained in this document or their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or

completeness of the information or opinions contained in this document by Armajaro Asset Management LLP or its members or employees and no liability is accepted by such persons

for the accuracy or completeness of any such information or opinions. The contents including details of any research, investment strategies and any bespoke financial products are

confidential to the person to whom it is delivered and should not be copied, distributed, or disclosed, in whole or in part, to any other person without our prior consent. Past

performance is not indicative of future performance.

• This document does not constitute or form part of any offer to issue or sell, or any solicitation of any offer to subscribe or purchase, any Shares nor shall it or the fact of its distribution

form the basis of, or be relied on in connection with, any contract therefore. Recipients of this document who intend to apply for Shares following publication of the prospectus by the

Fund are reminded that any such application may be made solely on the basis of the information and opinions contained in the prospectus which may be different from the information

and opinions contained in this document.

• In the United Kingdom this document is issued and approved by Armajaro Asset Management LLP (authorised and regulated by the Financial Services Authority and registered with the

U.S. Securities and Exchange Commission (SEC) as an investment adviser under the Investment Advisers Act of 1940), 16 Charles Street, London, W1J 5DS. The fund is not regulated

under the Financial Services and Markets Act 2000 (the Act) and consequently no protection is provided by the UK regulatory system. Similarly, benefits available under the UK Financial

Services Compensation Scheme do not apply. This document is only intended for distribution to persons permitted to receive it by Section 238 of the Act and is intended for distribution

to Professional Clients

• The views expressed are those of the manager at the time of publication and are subject to change.

Page 2

All data as at 30 March 2012 unless otherwise stated.

March 15

SUMMARY

• Background to the 2020 projection

• Existing state of cocoa macro research

• Demand Prognosis

• Supply Developments

• Conclusion

Page 3March 15

Page 4

2020 S&D Picture – Headlines in November 2014

* ICCO statement 21st November 2014March 15

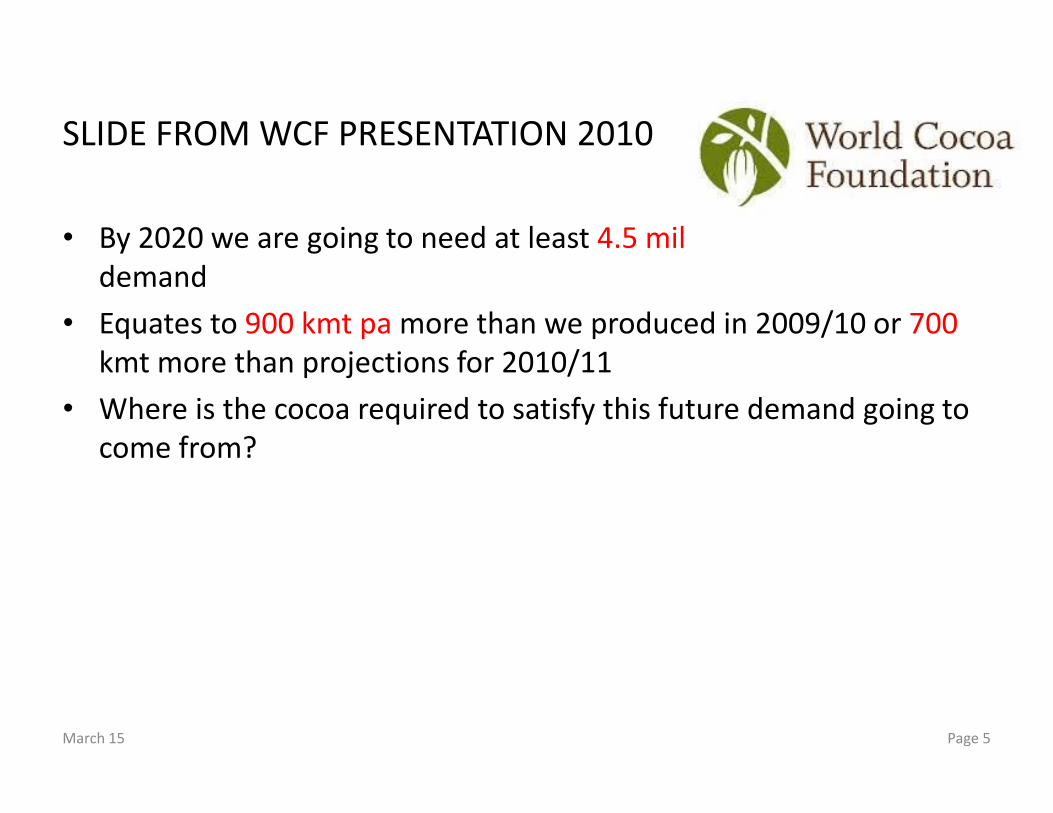

SLIDE FROM WCF PRESENTATION 2010

• By 2020 we are going to need at least 4.5 mil tons pa to satisfy

demand

• Equates to 900 kmt pa more than we produced in 2009/10 or 700

kmt more than projections for 2010/11

• Where is the cocoa required to satisfy this future demand going to

come from?

Page 5March 15

Global Macro Cocoa Resources

• Definition – research directed to estimating the size and trend of global cocoa production, demand and stocks and by extension, price

• Key producers lack the financial resources to conduct an inventory of the area under cocoa , planting density, age profile of trees etc

• No major governmental organization like FAO has done so because not considered a “strategic” food

• ICCO produce the best production /stocks info in the public domain but this is essentially backward-looking research. No pod counting. Have to accept numbers provided by members.

• The cocoa industry now spends millions on sustainability conferences and programs ,has mapped the cocoa genome etc yet has spent little on conducting an inventory of global cocoa resources from which to derive a baseline for any forward planning.

• Only 11 companies conduct their own field forecasting exercises. TOTAL trade and industry spending on original raw research likely to be between $15 - 20 M/pa.

Page 6March 15

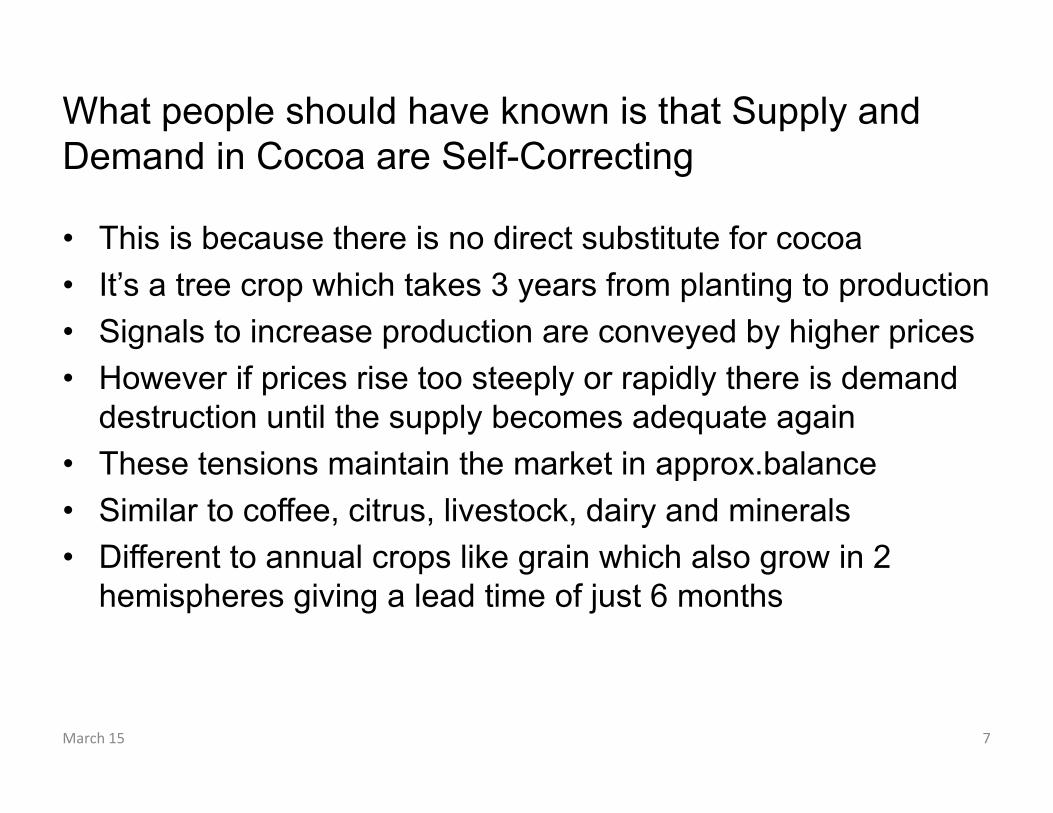

What people should have known is that Supply and

Demand in Cocoa are Self-Correcting

• This is because there is no direct substitute for cocoa

• It’s a tree crop which takes 3 years from planting to production

• Signals to increase production are conveyed by higher prices

• However if prices rise too steeply or rapidly there is demand

destruction until the supply becomes adequate again

• These tensions maintain the market in approx.balance

• Similar to coffee, citrus, livestock, dairy and minerals

• Different to annual crops like grain which also grow in 2

hemispheres giving a lead time of just 6 months

March 15 7

• Demand Picture in 2020

Page 8

Demand

March 15

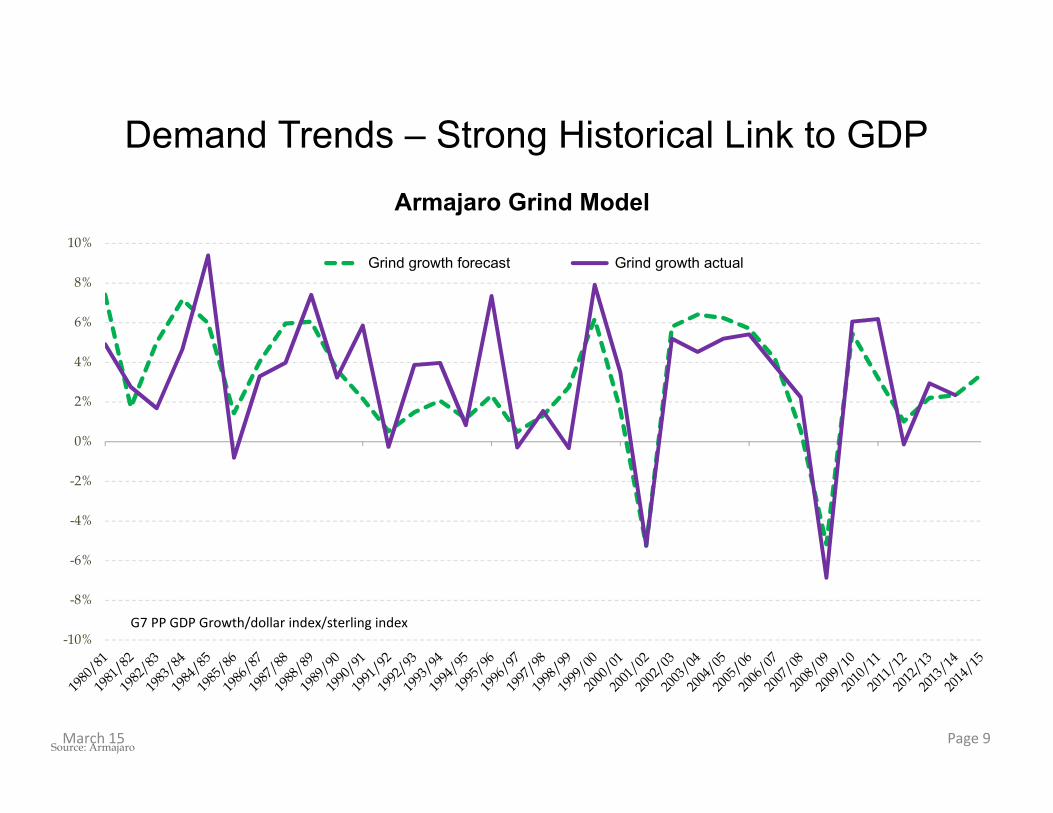

Demand Trends – Strong Historical Link to GDP

Page 9

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

Armajaro Grind Model

Grind growth forecast Grind growth actual

G7 PP GDP Growth/dollar index/sterling index

Source: Armajaro March 15

Demand Trends – Strong Link to Macro Factors

Page 10

60

65

70

75

80

85

90

3400

3500

3600

3700

3800

3900

4000

4100

4200

2005 2006 2007 2008 2009 2010 2011 2012 2013

Cocoa Grind Vs US New Car Sales

Cocoa Grind New Car Sales

40

42

44

46

48

50

52

54

56

58

60

3400

3500

3600

3700

3800

3900

4000

4100

4200

2005 2006 2007 2008 2009 2010 2011 2012 2013

Cocoa Grind VS Chicago PMI Index

Cocoa Grind PMI Index

2,000

2,500

3,000

3,500

4,000

4,500

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Billions

Grind Vs Global GDP

Grindings Global GDP (Constant 2000 US$)

• Well-established demand trends have

maintained their relationships over decades

Source: Armajaro/World Bank/IMF March 15

Annual Growth in Grind per annum

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

Page 11Source: Armajaro

March 15

Processing Margins

Page 12

-£400

-£300

-£200

-£100

£0

£100

£200

£300

£400

Hamburg pressing Nigeria pressing Ghana mid pressing Ghana main pressing CDI pressing

Source: Armajaro DataMarch 15

Demand in 2020

Page 13

[VALUE]

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

000s Tonnes

Global Grind – Linear Trend Approx 2% p.a.

Dot-com bubble/subprime

mortgage crisis

Global financial crisis

= Forecast

Source: ArmajaroMarch 15

Apparent Consumption in 2020

Page 14

[VALUE]

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

96/9797/9898/9999/0000/0101/0202/0303/0404/0505/0606/0707/0808/0909/1010/1111/1212/1313/1414/1515/1616/1717/1818/1919/20

000’s Tonnes

Developed Developing

Source: ICCO/ArmajaroMarch 15

• Supply Outlook

Page 15

PRODUCTION

March 15

Summary of Demand

• Instead of linear analysis of global demand – to project further forward it is

necessary to split developed and developing country trends.

• Developed countries consumption has grown at an average rate of 1.6% over the

last 20 years.

• Developing countries have been growing faster, at 4.3%.

• Developing economies will consume 35% of production in 2020

• Grind forecasted to rise by 940 kmt between 2010 and 2020 to 4582kmt.

• Using different trends for developed and developing countries, consumption is

projected to rise by just over 1mmt to 4609kmt in the 19/20 season.

Page 16March 15

Global Cocoa Production 1984-2015

Page 17

1000

1500

2000

2500

3000

3500

4000

4500

000’s tonnes

Global Production

Linear (Global Production)

Previous High/Ceiling?

4320k tonnes

Source: ArmajaroMarch 15

• Cocoa production has continued to follow an upward trend of approximately

2% a year

• Strongest global crop on record was in 2010/11, at 4,320k tonnes

• Increased production primarily due to new plantings in CDI and Ecuador

• Can cocoa production continue to expand at this rate? Is the previous high a

short-term ceiling?

Page 18March 15

Production Trends by Continent

Page 19

0

500

1000

1500

2000

2500

3000

3500

4000

000’s tonnes

Africa South & Central America Asia

= ForecastMarch 15

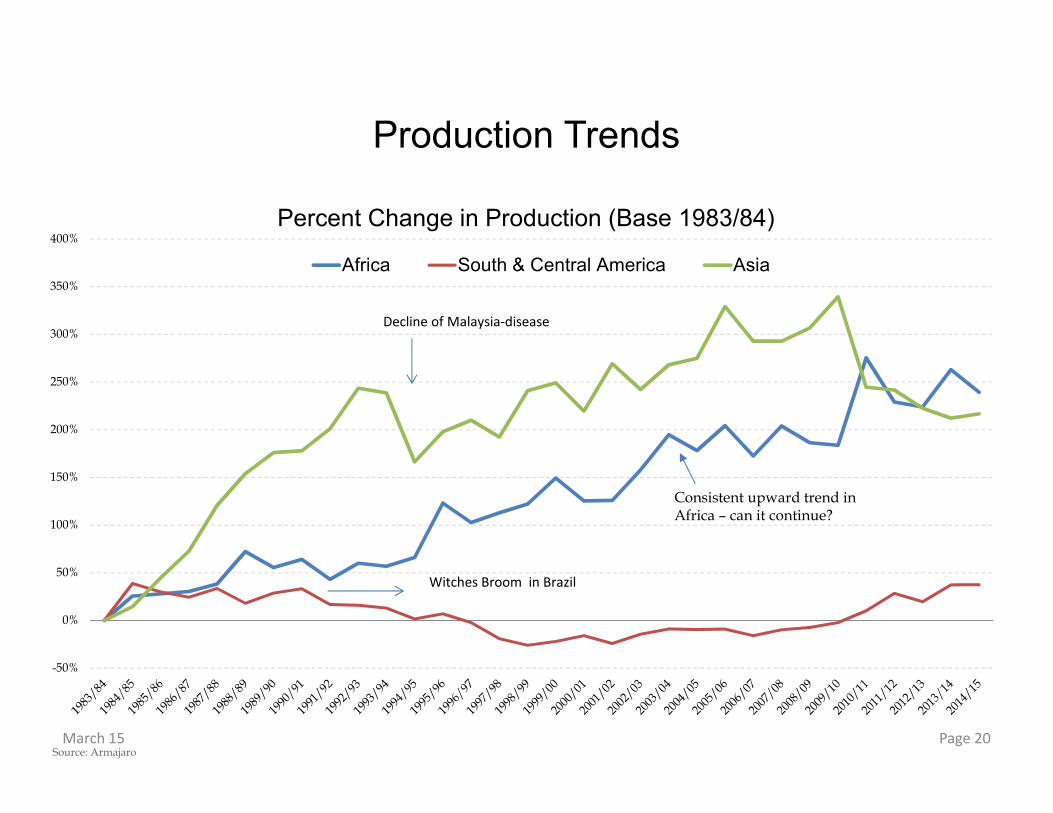

Production Trends

Page 20

Consistent upward trend in Africa – can it continue?

-50%

0%

50%

100%

150%

200%

250%

300%

350%

400%

Percent Change in Production (Base 1983/84)

Africa South & Central America Asia

Decline of Malaysia-disease

Witches Broom in Brazil

Source: ArmajaroMarch 15

Production Trends – Major Origins

Page 21

0

200

400

600

800

1000

1200

1400

1600

1800

2000

000’s tonnes

Ghana Côte d'Ivoire Brazil Ecuador Indonesia

Source: ArmajaroMarch 15

Futures Prices – Performance Since March 2010

Page 22

-50%

-30%

-10%

10%

30%

50%

70%

90%

110%

130%

150%Palm Oil Rubber Orange Juice Rice Cotton Cocoa

Only cocoa has higher

futures prices in Jan 2015

compared to 5 years ago

but marginal

Source: ReutersMarch 15

Page 23

Farm gate Prices

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Oct06

Jan07

Apr07

Jul07

Oct07

Jan08

Apr08

Jul08

Oct08

Jan09

Apr09

Jul09

Oct09

Jan10

Apr10

Jul10

Oct10

Jan11

Apr11

Jul11

Oct11

Jan12

Apr12

Jul12

Oct12

Jan13

Apr13

Jul13

Oct13

Jan14

Apr14

Jul14

Oct14

USD/Tonne

C. D'IVOIRE GHANA BRAZIL INDONESIA ECUADOR

March 15

• 1. Indonesia

Page 24March 15

• Indonesia remains 3rd largest cocoa producer, but trend is downwards as farmers move into palm oil and rubber

• Farmers have grappled with diseases and aging trees

• Small plot size

• Production has dropped for 6 consecutive years

• Farmers have the ability to modernize their farms

• Prices are good and closely track the world market

• But competing economy activities are the risk to cocoa

25March 15

Indonesia – Structural Downtrend or Temporary?

Page 26

0

1

2

3

4

5

6

7

1980 1985 1990 1995 2000 2005 2010

Millions Acres

Acreage

Cocoa, beans Oil, palm fruit Rubber

0

5000

10000

15000

20000

25000

30000

35000

40000

1980 1985 1990 1995 2000 2005 2010

000’s tonnes

Palm Oil Production

0

100

200

300

400

500

600

1980 1985 1990 1995 2000 2005 2010

000’s tonnes

Cocoa Production

Source: Armajaro Data/ World Bank

0.9

1.0

1.0

1.1

1.1

1.2

1.2

1990 1995 2000 2005 2010

Mil

lio

n S

q.

Km

Rainforest Area

March 15

Oil Palm

Page 27

Expansion of acreage in Indonesia

• Oil palm needs a rainforest climate – high

humidity and temperatures – therefore a lot of

plantations are established at the expense of

rainforests.

• Major importers include India, China and the

EU.

• Fundamentals are good, with demand

forecasted to increase as many developed

economies shift away from the use of trans-

fasts to healthier alternatives.

• Strong demand also coming from biofuel and

energy sectors

Source: GreenPalmMarch 15

Income Comparison

Page 28

700

720

740

760

780

800

820

840

Cocoa Coffee Rubber Oil Palm

US$ per hectare per year

Net Income Potential for Different Smallholder Crops

3-5 years 4-6 years 10+ years 3-7 yearsLag between

planting and

positive cash

flow

Sources: Indonesia, A business case for sustainable coffee productionMarch 15

• 2. South America

Page 29March 15

Brazil

• Diseases account for losses of more than 30% of the potential crop each year.

• Brazil suffered an outbreak of witches broom in the mid 90s

• Actively using CCN51 and equivalents and seeking more disease resistant/tolerant

planting material

Page 30

0

50

100

150

200

250

300

350

400

450

00

0’s

to

nn

es

Brazil Annual Production

Never recovered from witches

broom outbreak

Source: Armajaro March 15

0

50

100

150

200

250

300

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

000's tonnes

Brazil Ecuador Peru

Page 31

Production Trends – Ecuador overtakes Brazil

Source: Armajaro March 15

Ecuador and Peru

Page 32

• Compared to West Africa production

is small

• Despite this, the region likely to be

key for the future of cocoa production

by being the “model”

• Advanced techniques

• Could change the face of the cocoa

industry away from small-scale

farmers to large-scale, technological

production

• We forecast combined production will

exceed 400k mt by 2020.

2,465

300

0

500

1000

1500

2000

2500

3000

2014/15

000’s tonnes

Production in 2014/15

Peru & Ecuador

Ivory & Ghana

Source: Armajaro March 15

Why Ecuador?

• Use of CCN51 has revolutionized the cultivation of cocoa

• Yields of 2-2.5 mt /ha the “norm” for large scale plantations

• But not just for big farms

• Small holders can get 1mt quite handily

• Disease tolerant – rebounds much faster than Nacional

• Dedication and enthusiasm of farmers has persisted

• Ecuador has now created a “high tech farming cluster” with

cocoa a key part

• Propagation of good planting material

March 15 33

• Multiple and experimental irrigation systems

• Sophisticated use of chemicals/fertilizers

• Innovative planting patterns to permit mechanization

• Continuous development of post-harvest practices to improve

flavour profile

34March 15

• Ecuador farmers have done this for themselves DESPITE their government

• Government discouraged use of CCN51

• Their continued promotion of low yielding Nacional effectively commits farmers to poverty

• No evidence that large scale industry is prepared to pay an equalizing price for Nacional

• Chocolate industry have been complicit – complaining about flavour while they should have been finding ways to use CCN beans

• Nacional and CCN now effectively trading at “par”

• Production would have been far higher if they had got on board sooner

35March 15

• 3. West Africa

Page 36March 15

Production Trends – Ghana & Côte d'Ivoire

Page 37

-600

-400

-200

0

200

400

600

800

1000

1200

35%

40%

45%

50%

55%

60%

65%

(Ghan

a & Côte d'Ivoire) –Rest of W

orld Crop

% of World Crop

Combined production from Ghana

& Ivory overtook the rest of the

world in 1995/96. This trend has

increased ever since.

60% of total crop threshold

Source: Armajaro March 15

Land Competition between Crops 1980-2013

Page 38

0.0

0.5

1.0

1.5

2.0

2.5

1980 1985 1990 1995 2000 2005 2010

Million A

cres

Ghana

Cocoa beans Maize Oil palm fruit Rice, paddy

Source: FAO Stat

0

0.5

1

1.5

2

2.5

3

1980 1985 1990 1995 2000 2005 2010Million A

cres

Côte d'Ivoire

Cocoa beans Coffee, green Maize

Oil palm fruit Rice Natural rubber

• No indication of significant land loss to other crops

• Farmers traditionally grow different crops to diversify income sources

• Familiarity of cocoa and fixed prices provide incentives compared to competing crops

• Whilst yields are stable/marginally increased over the years, production rises have been due to new plantings.

March 15

Production Trends – Ghana/Côte d'Ivoire

Page 39

0

200

400

600

800

1000

1200

1400

1600

1800

2000

000’s mts

Ghana Côte d'Ivoire

Market fears CI was in a

topping out phase

Structural downtrend or

temporary blip?

Source: Armajaro

Dotted Line = Since last conference

= forecast

March 15

Reasons Behind Big Crops of 2010-11

• 2010/11 combined CDI/Ghana crops remain the record

• Optimal weather – abundant rainfall and crucially temps 2-3 degrees above

normal (correlation in trend in both countries)

CDI

• Post-election political struggles boosted prices

• Super efficient harvesting in CDI – might be the last harvest?

• Farmers stayed on the farm to keep a low profile

• Converted everything to cash in case they had to leave

GHANA

• Ghana farmers just given a big price increase

Page 40March 15

CDI Situation Since 10/11

• Main driver of strong output is expansion of acreage in CDI

• Northern Burkinabe origin farmers feel more secure since election and more

willing to expand farms

• Increased plantings esp in NW and N – normally new land but sometimes

as a result of declining productivity of old farms

• Economics more attractive

• Introduction of fixed price for season enables farmers to plan ahead

• Sustained upward trend in price for 3 seasons

• Enforcement of fixed price has boosted farmer income esp for mid crop

• Increased use of fertilization on farms

• CCC have improved roads/access to markets

Page 41March 15

Consequences/Issues Facing CDI

• Spread of CSSV

• Lack of high quality, high yielding planting material to

rejuvenate farms

• Farms getting bigger causing increased demand for labour –

much of it coming from families in north lured by potential of

having own farm - potential child labour issues

• Movement to cities by younger people

• Deforestation accelerated – rainforest destroyed

42March 15

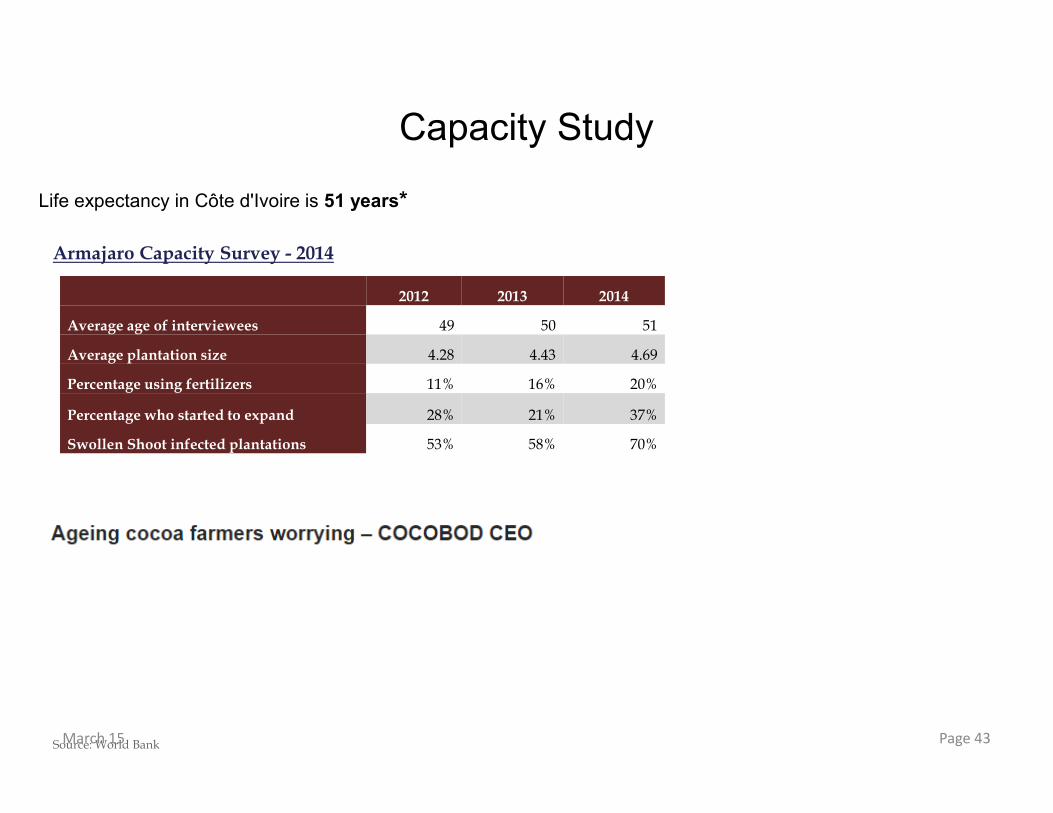

Capacity Study

Page 43

Life expectancy in Côte d'Ivoire is 51 years*

Source: World Bank

2012 2013 2014

Average age of interviewees 49 50 51

Average plantation size 4.28 4.43 4.69

Percentage using fertilizers 11% 16% 20%

Percentage who started to expand 28% 21% 37%

Swollen Shoot infected plantations 53% 58% 70%

Armajaro Capacity Survey - 2014

March 15

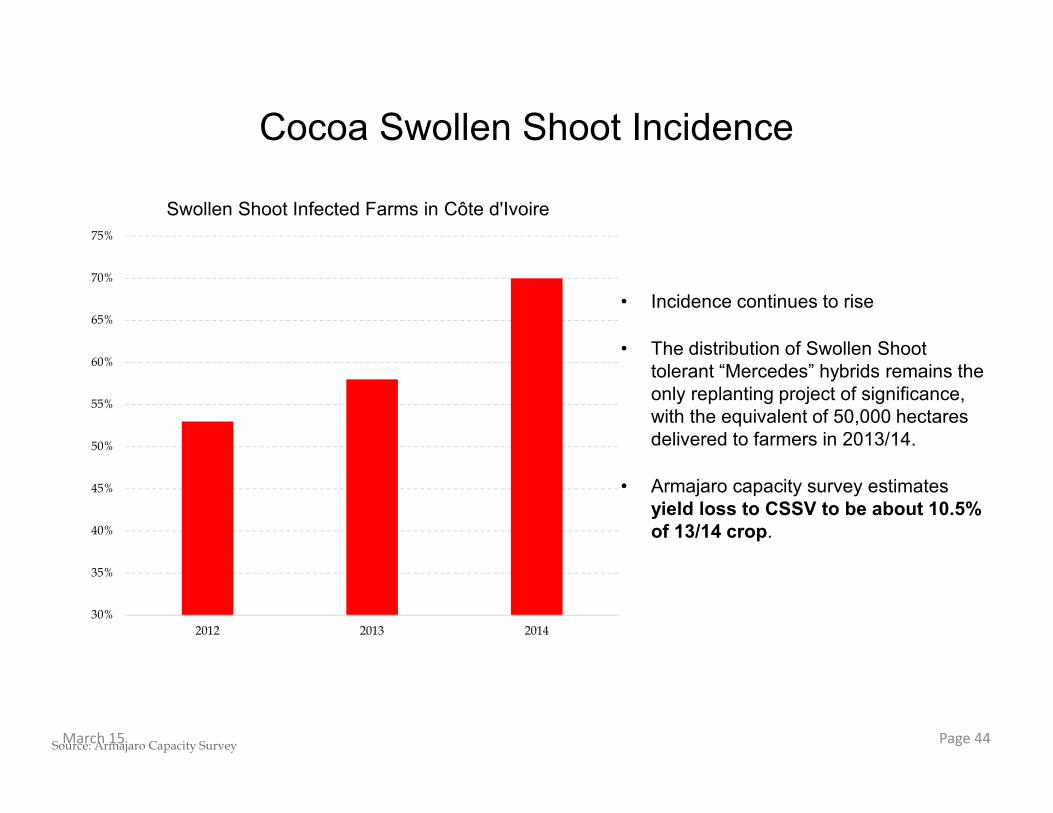

Cocoa Swollen Shoot Incidence

Page 44

30%

35%

40%

45%

50%

55%

60%

65%

70%

75%

2012 2013 2014

Swollen Shoot Infected Farms in Côte d'Ivoire

Source: Armajaro Capacity Survey

• Incidence continues to rise

• The distribution of Swollen Shoot

tolerant “Mercedes” hybrids remains the

only replanting project of significance,

with the equivalent of 50,000 hectares

delivered to farmers in 2013/14.

• Armajaro capacity survey estimates

yield loss to CSSV to be about 10.5% of 13/14 crop.

March 15

Page 45March 15

46March 15

Côte d'Ivoire – Employment in Agriculture

Page 47

10%

20%

30%

40%

50%

60%

70%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Population (Millions)

Source: IMF

% of Total Employment)

March 15

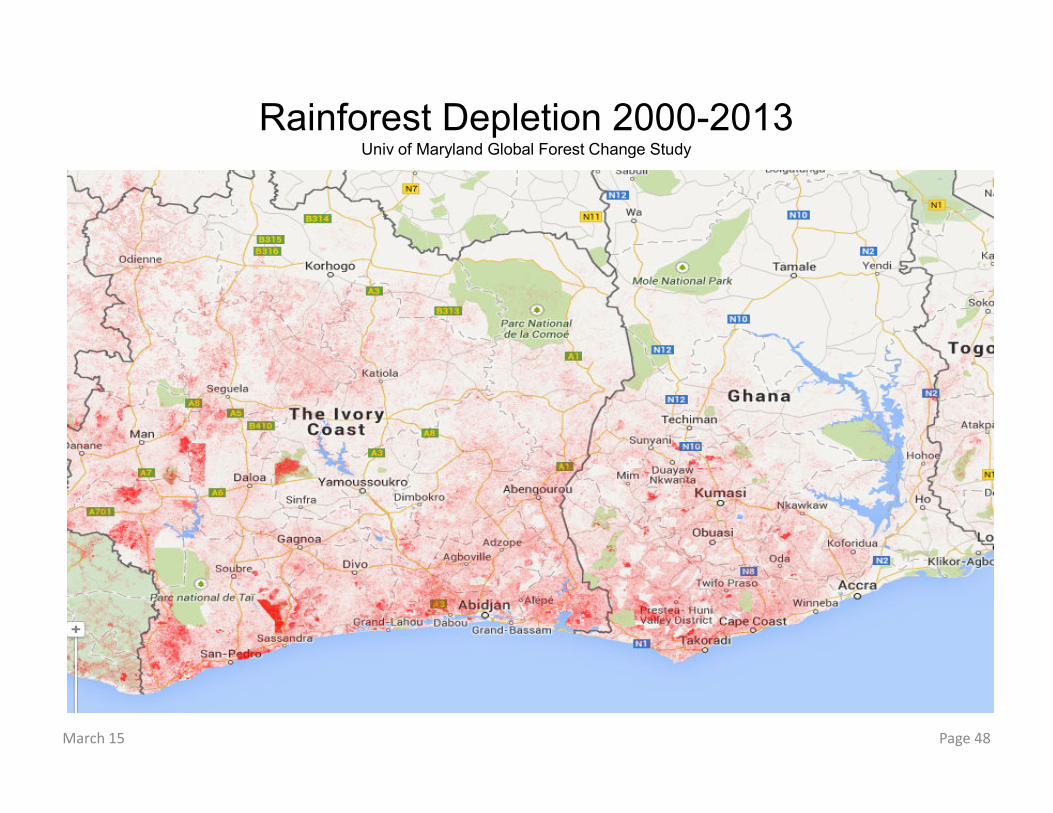

Rainforest Depletion 2000-2013Univ of Maryland Global Forest Change Study

Page 48March 15

Page 49March 15

Ghana Situation Since 10/11

• Farmer price stalled as government spending caused budget deficit

• CMC cut back on fertilizer and mass spraying programs

• Oil economy

• Rural migration esp of young

• Alternative land use (see previous) opportunities esp in gold mining

Page 50March 15

Ghana Problem - Crop 2014/15

• Unexpected collapse in crop for 14/15

• But not seen in our pod counts

• 13/14 crop boosted by reduction in normal end season hoarding

• Knock-on effect of weaker start to 14/15

• No weather issues-good rains, harmattan only hit in late Dec/early Jan

• No abnormal disease issues

• Fertilizer distribution was delayed but impact should be expressed in pod

load/survival

• Likely drop from c950 kmt to 700/750

• An unprecedented drop of 24%

• One-off or structural change?

• How so sudden?

Page 51March 15

Page 52

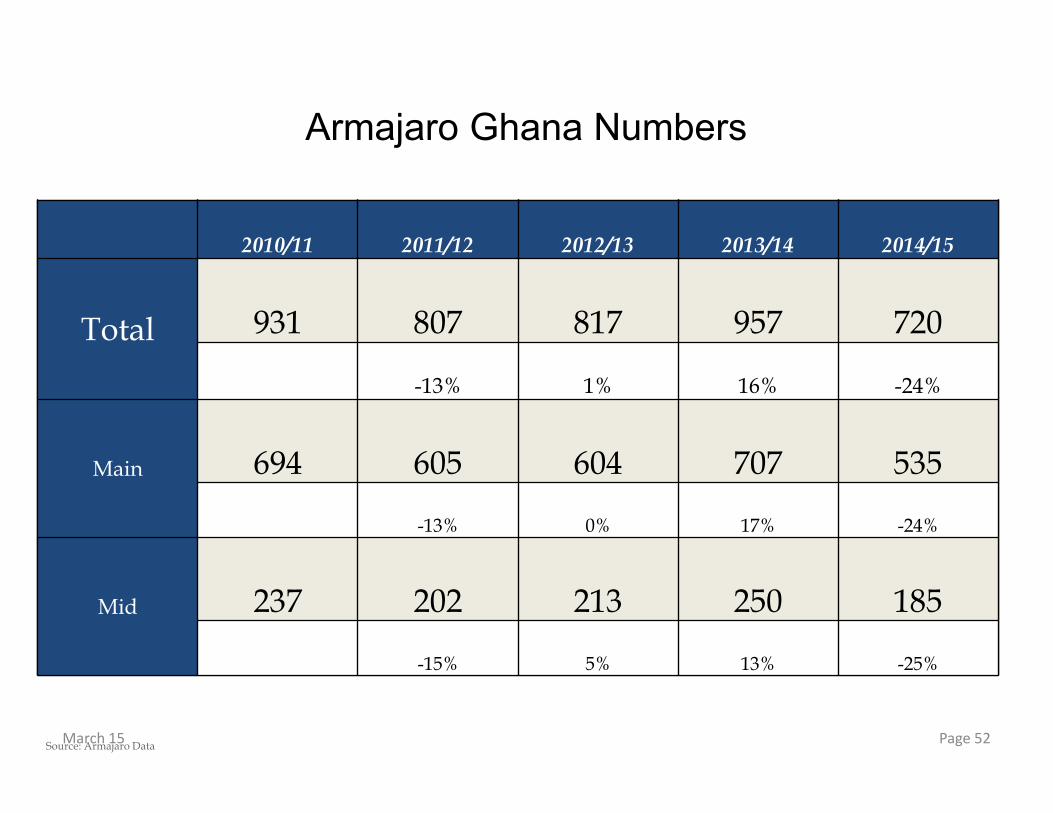

Armajaro Ghana Numbers

2010/11 2011/12 2012/13 2013/14 2014/15

Total 931 807 817 957 720

-13% 1% 16% -24%

Main 694 605 604 707 535

-13% 0% 17% -24%

Mid 237 202 213 250 185

-15% 5% 13% -25%

Source: Armajaro DataMarch 15

Nigeria Cocoa & Oil Production

Page 53

0

500

1000

1500

2000

2500

3000

50

100

150

200

250

300

350

m. B

arrels

000's tonnes

Cocoa Oil

Source: Armajaro/Energy Information AdministrationMarch 15

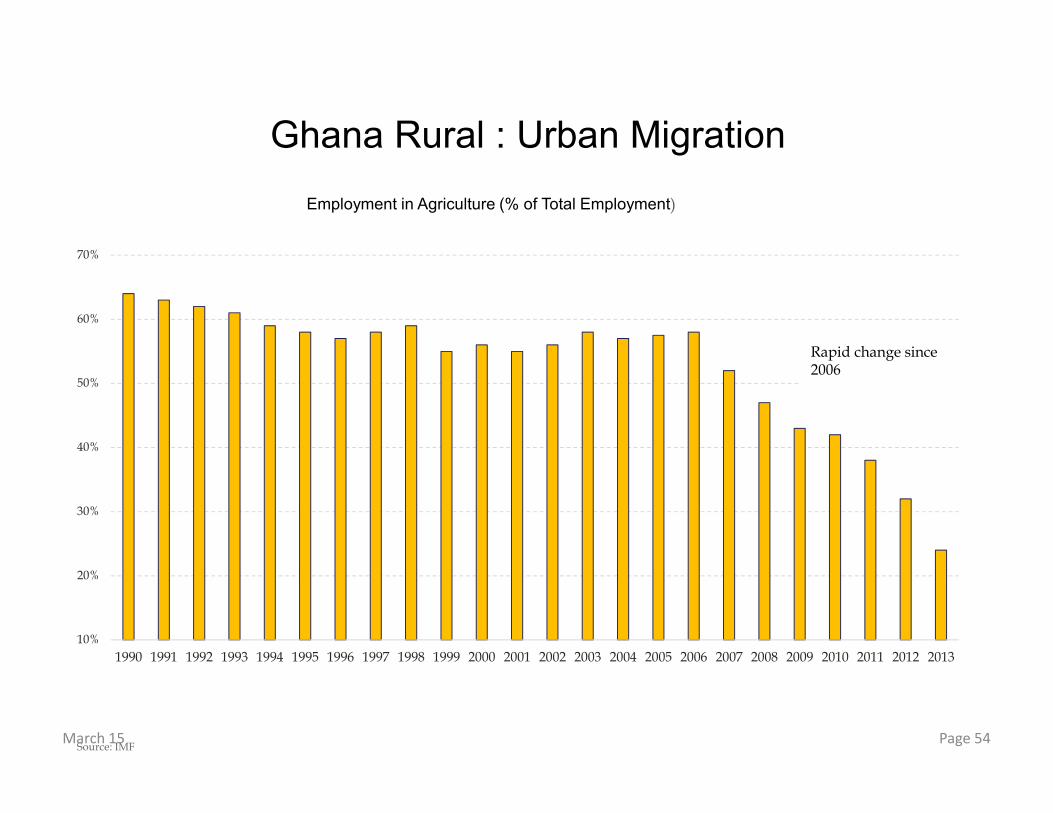

Ghana Rural : Urban Migration

Page 54

10%

20%

30%

40%

50%

60%

70%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Employment in Agriculture (% of Total Employment)

Source: IMF

Rapid change since 2006

March 15

-

20,000

40,000

60,000

80,000

100,000

120,000

140,000

Cocoa Farmer* Minimum Salary Operations Manager Project Manager Professor Fuel Handler

GHC/Year

Average Annual Salary in Ghana (GHC/year)

Page 55

Urban Migration – Why the move?

*Assumptions: 5 hectares with yield of 400kg/ha.

Note: Purely income from cocoa. most farmers will gain income from other crops

March 15

Gold – Photo from Trek September 2014

Page 56March 15

Page 57

Infrared Imagery: Near Bogoso

Source: Cranfield UniversityMarch 15

Google Earth – Near Bogoso in Western Region

Before: 2011

Page 58Source: Armajaro

Distance = 7km

March 15

Page 59

Google Earth – After: 2014

Source: ArmajaroMarch 15

Page 60

24th April 2013 - Eastern Region, close to Armajaro sites in Jejeti and Asafo

Gold – Google Earth Images: BEFORE

Source: Google EarthMarch 15

Page 61

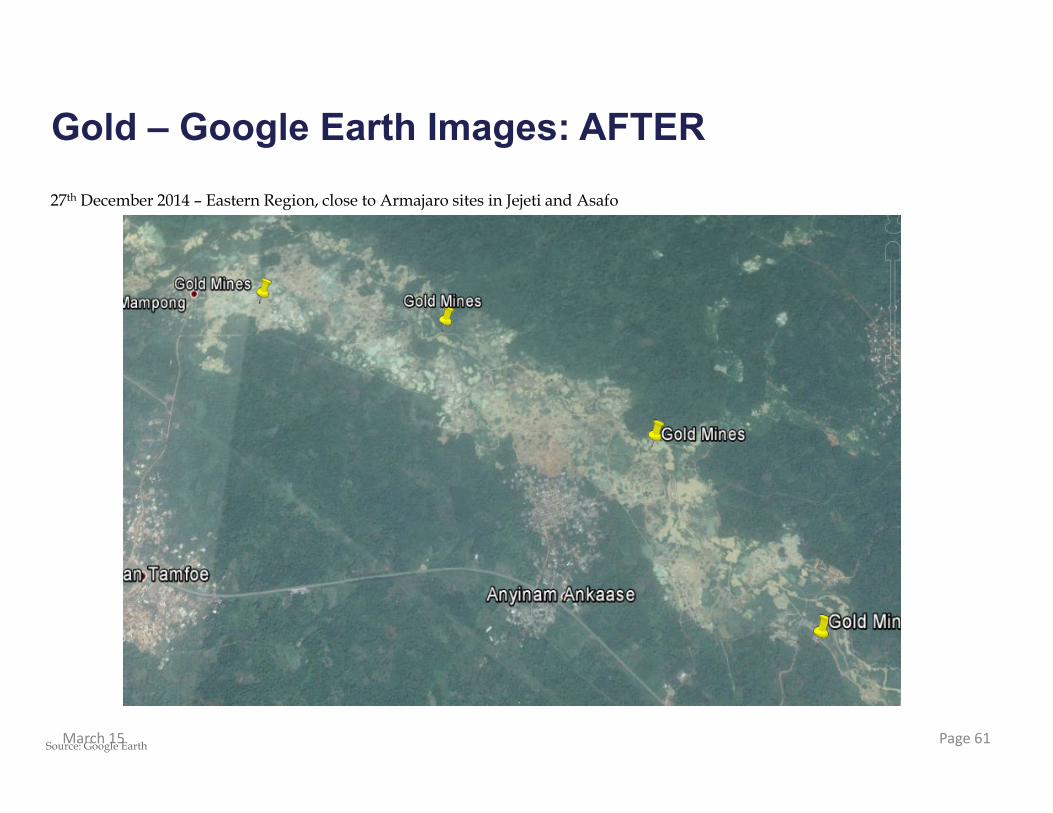

27th December 2014 – Eastern Region, close to Armajaro sites in Jejeti and Asafo

Gold – Google Earth Images: AFTER

Source: Google EarthMarch 15

Page 62

A closer look at the damage

Source: Google EarthMarch 15

Page 63

Gold – Google Earth Images: BEFORE

1st January 2012

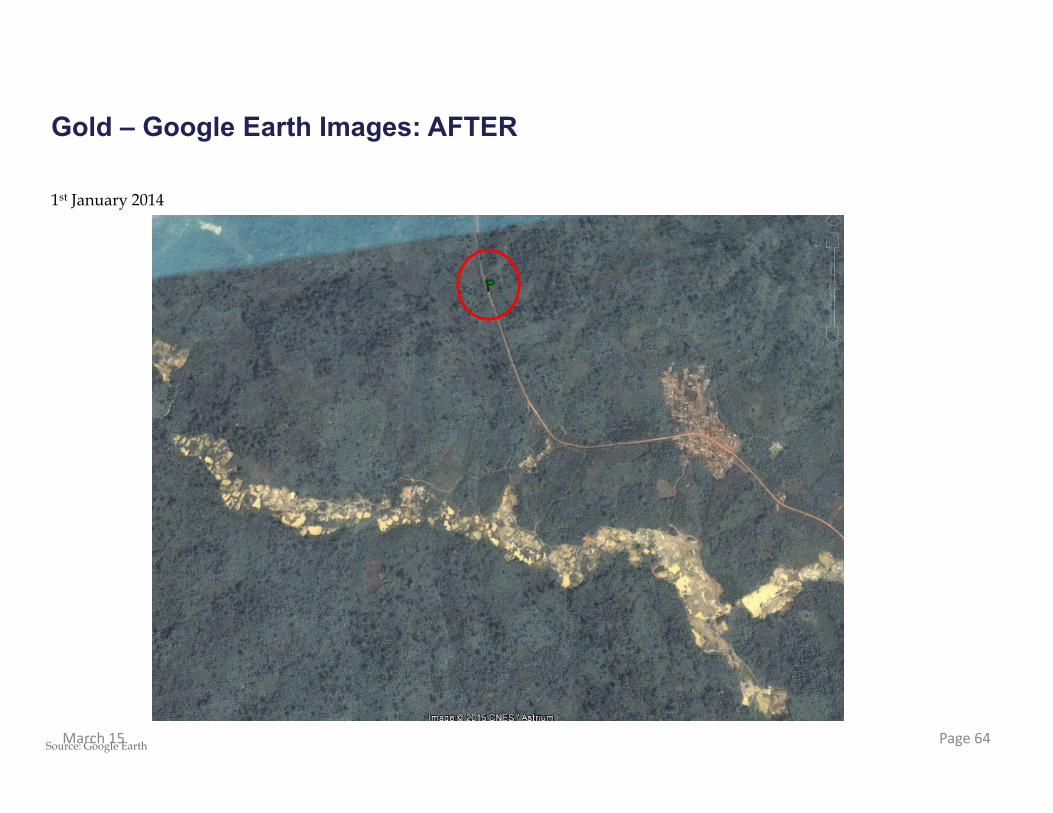

Armajaro Crop Survey Site: Near Kotokuom

Source: Google EarthMarch 15

Page 64

1st January 2014

Gold – Google Earth Images: AFTER

Source: Google EarthMarch 15

Page 65

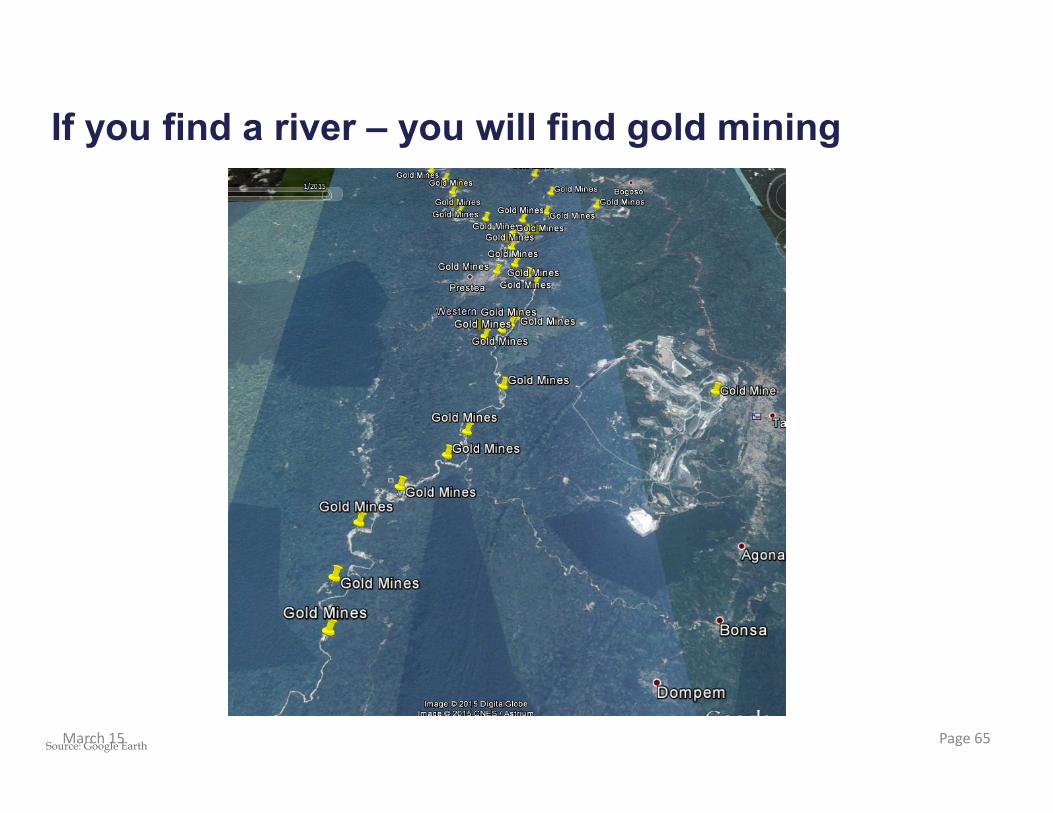

If you find a river – you will find gold mining

Source: Google EarthMarch 15

Page 66

Gold: Competition or Complement?

Intercropping agricultural crops is common and helps diversify farmer income

However, Gold is a different proposition and threatens production in new way

• Toxic chemicals (cyanide and mercury) destroy the soil

• Water pollution

• Cocoa land used for gold mining

• Farmers abandoning farms to mine gold

• Farmers selling their farms to mining firms

• Farmers unable to get workers required during harvest season as they

can earn more in mines

March 15

A number of academic studies have taken place on the impact of gold mining on agriculture.

Key findings are:

1. Hilson & Garthford study in 2014 – gold generates benefits for some individual farmers (via

income), these benefits are outweighed by aggregate costs of small-scale mining activities in

terms of collective loss of agricultural lands and water pollution

2. Aragon & Rud 2013 – Gold mining in Ghana reduces agricultural output in nearby farms by

40%.

3. In the case of Ghana, there is substantial evidence, ranging from anecdotal to scientic, that

gold mining is associated with high levels of pollution and loss of agricultural livelihoods

(Human Rights Clinic, 2010; Akabzaa, 2009; Aryeetey et al., 2007; Hilson and Yakovleva, 2007)

Page 67

Gold: Academic Studies

March 15

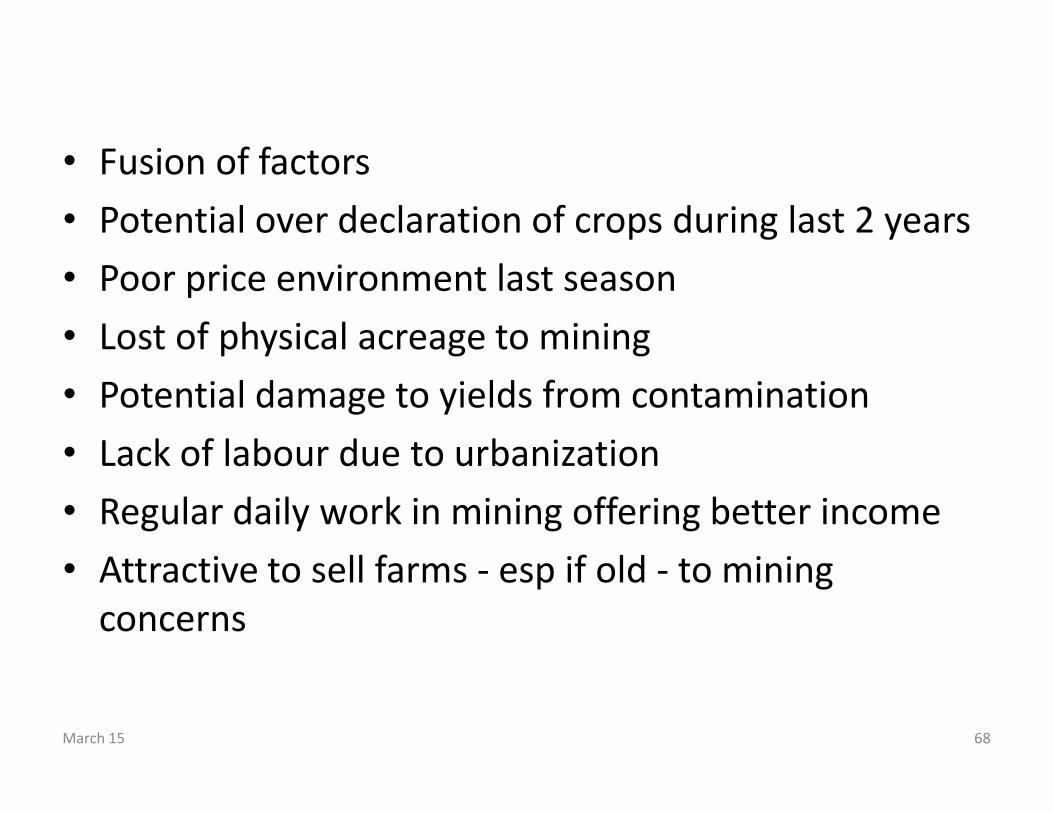

• Fusion of factors

• Potential over declaration of crops during last 2 years

• Poor price environment last season

• Lost of physical acreage to mining

• Potential damage to yields from contamination

• Lack of labour due to urbanization

• Regular daily work in mining offering better income

• Attractive to sell farms - esp if old - to mining

concerns

March 15 68

Will it last?

• Unclear on causes but confident current crop is sharply lower

• Observed transfer of land to mining

• Not reversible

• Rivers polluted

• Soil contaminated

• Demographics of farmers suggest rebound unlikely and trend

might continue

• Loss of growth potential from the most reliable supplier

March 15 69

• Conclusion

Page 70March 15

Page 71

S&D Balance

Source: Armajaro Data

-400

-200

0

200

400

600

800

1,000

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

Balance Production Grindings

March 15

Page 72

S&D Potential Picture in 2020

2500

3000

3500

4000

4500

5000

000s tonnes

Production Grindings

Source: Armajaro DataMarch 15

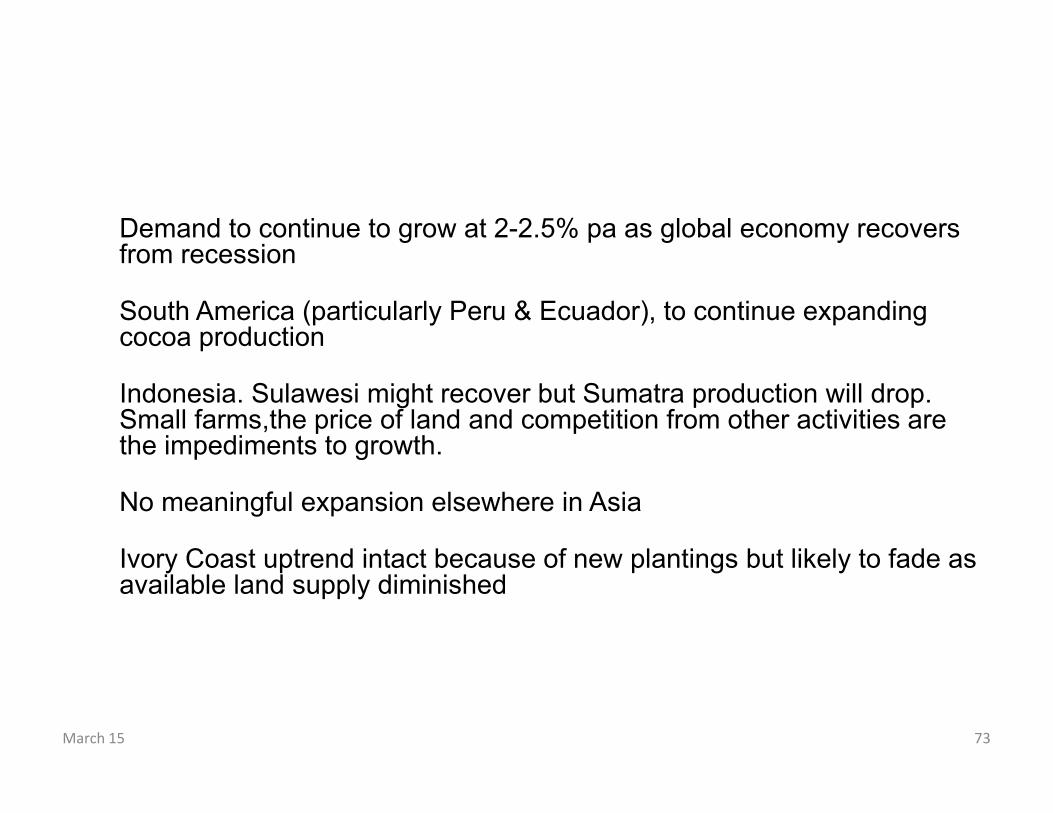

Demand to continue to grow at 2-2.5% pa as global economy recovers from recession

South America (particularly Peru & Ecuador), to continue expanding cocoa production

Indonesia. Sulawesi might recover but Sumatra production will drop. Small farms,the price of land and competition from other activities are the impediments to growth.

No meaningful expansion elsewhere in Asia

Ivory Coast uptrend intact because of new plantings but likely to fade as available land supply diminished

March 15 73

• Ghana a huge question mark.The upward trend looks over.

• Old, decaying farms in W.Africa should be taken out of production and

converted to other land use so that attention can be given to raising

yields/income on younger, existing farms

• Industry made poor decisions , notably ignoring Ecuador , and is paying

the price with little progress in W.Africa and a lost opportunity to diversify

the geographical production base

• Higher prices are required to encourage production and attract younger

farmers

March 15 74

Page 75Source: Armajaro

S&D Balance

2012/13 % +/- 2013/14 % +/- 2014/15 % +/-

NET PRODUCTION 3,853 -3% 4,245 10% 4,051 -5%

GRINDINGS 4,051 3% 4,150 2% 4,108 -1%

Surplus / Deficit -198 95 -57

BALANCE

Global Balance 2012/13-2014/15

March 15 76

-198

95

-57

-250

-200

-150

-100

-50

0

50

100

150

2012/13 2013/14 2014/15

000's tonnes

Short-term Factors

• Immediate political risks high in Nigeria and potentially rising

in Cote d’Ivoire

• Weather has been benign for several years but some risk

ahead eg El Nino especially for Ecuador

• Unanswered questions about Ghana’s futures

• Demand growth rebound in 15/16 after a poor year

• Deficit this year and next a high probability

March 15 77

WCF PRESENTATION 2010

• Cocoa is a unique product

• It requires harvesting by hand

• Requires multi-stage post-harvest handling

• Approx 25000 pods have to be cut open to produce 1 metric ton of

beans

• We have been spoiled as consumers benefitting from the efforts

of desperately poor people who lack alternatives

• This pool of African farmers is not enough to meet the needs of

world demand going forward

78March 15

Page 79Source: Armajaro

Weather

Page 80March 15

THANK YOU

81March 15

Appendix

82March 15

Gold: Case Study

• Artisanal and small-scale mining has emerged in communities endowed with natural

resources as a lucrative activity due to its income-generating potential

• The situation changed due to the influx of Chinese from 2006, bring expensive machinery

with them. Following a government crackdown on these illegal mines in 2012, many of the

Chinese were deported. The Ghanaians rapidly took over these mines, using the machinery

and expertise left behind

• Start-up costs are negligible (as machinery was left), and reward is instant due to daily

income

Page 83March 15

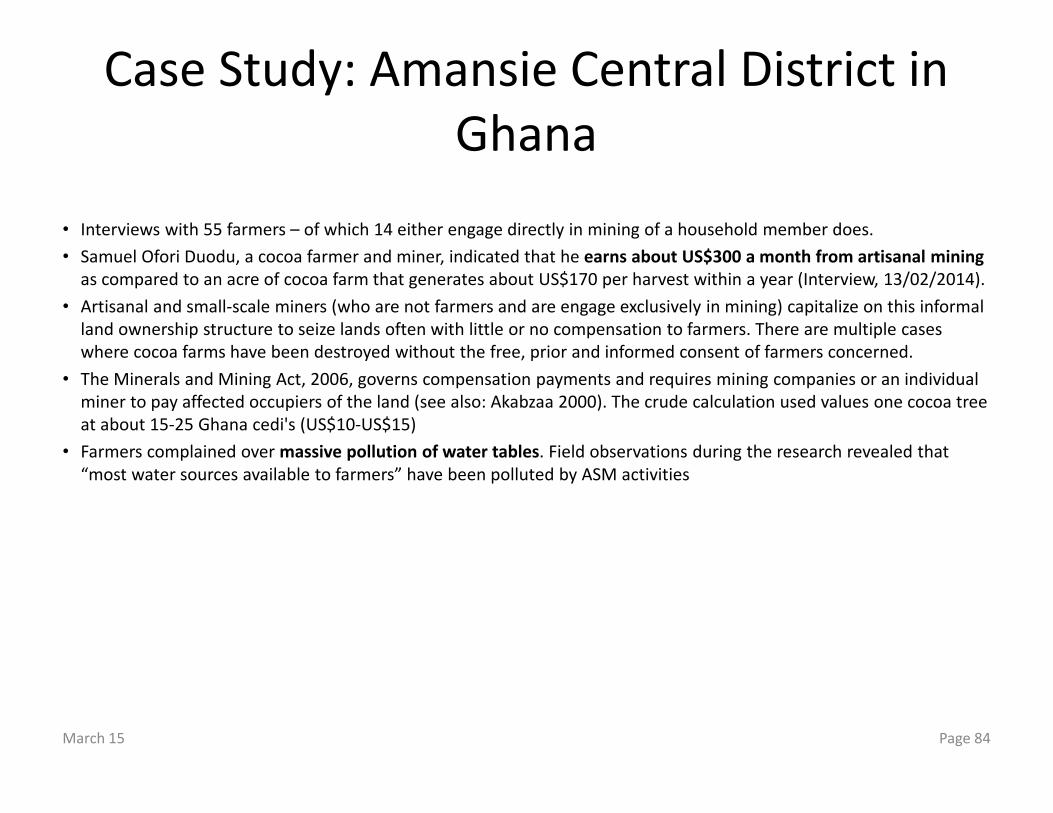

Case Study: Amansie Central District in

Ghana

• Interviews with 55 farmers – of which 14 either engage directly in mining of a household member does.

• Samuel Ofori Duodu, a cocoa farmer and miner, indicated that he earns about US$300 a month from artisanal mining

as compared to an acre of cocoa farm that generates about US$170 per harvest within a year (Interview, 13/02/2014).

• Artisanal and small-scale miners (who are not farmers and are engage exclusively in mining) capitalize on this informal

land ownership structure to seize lands often with little or no compensation to farmers. There are multiple cases

where cocoa farms have been destroyed without the free, prior and informed consent of farmers concerned.

• The Minerals and Mining Act, 2006, governs compensation payments and requires mining companies or an individual

miner to pay affected occupiers of the land (see also: Akabzaa 2000). The crude calculation used values one cocoa tree

at about 15-25 Ghana cedi's (US$10-US$15)

• Farmers complained over massive pollution of water tables. Field observations during the research revealed that

“most water sources available to farmers” have been polluted by ASM activities

Page 84March 15