milestone events - bannerman resources limited · this presentation should be read in conjunction...

TRANSCRIPT

Milestone Events

Completion of Etango Uranium Project DFS &

Agreement with Namibian State-owned Mining Company

April 2012

Technical Disclosures and

Forward-Looking Disclaimers

This presentation should be read in conjunction with the release by Bannerman Resources Limited dated 10 April 2012 and entitled “Bannerman Reports Positive

DFS Results and Milestone Agreement with Namibian State-Owned Mining Company”.

Certain disclosures in this presentation, including management's assessment of Bannerman Resources Ltd’s plans and projects, constitute forward-looking

statements that are subject to numerous risks, uncertainties and other factors relating to Bannerman’s operation as a mineral development company that may cause

future results to differ materially from those expressed or implied in such forward-looking statements. The following are important factors that could cause the

Company's actual results to differ materially from those expressed or implied by such forward looking statements: fluctuations in uranium prices and currency

exchange rates; uncertainties relating to interpretation of drill results and the geology, continuity and grade of mineral deposits; uncertainty of estimates of capital and

operating costs, recovery rates, production estimates and estimated economic return; general market conditions; the uncertainty of future profitability; and the

uncertainty of access to additional capital. Full descriptions of these risks can be found in the Company’s various statutory reports, including its Annual Information

Form available on the SEDAR website, sedar.com. Readers are cautioned not to place undue reliance on forward-looking statements. Bannerman Resources Ltd

expressly disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise.

Mineral resources that are not ore reserves do not have demonstrated economic viability.

The information in this presentation that relates to the exploration results of the projects owned by Bannerman is based on information compiled by Mr Martinus

Prinsloo, Exploration Superintendent of Bannerman. Mr Prinsloo is a Member and a Chartered Professional of the Australasian Institute of Mining and Metallurgy, a

Recognised Professional Organisation by the Australasian Joint Ore Reserves Committee, who has sufficient experience relevant to the style of mineralisation and

types of deposits under consideration and to the activity which is being undertaken to qualify as a Competent Person as defined in the 2004 Edition of the

“Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves” and as a Qualified Person for purposes of National Instrument

43-101 of the Canadian Securities Administrators. Mr Prinsloo consents to the inclusion in this presentation of the matters based on his information in the form and

context in which it appears.

The information in this presentation relating to the Mineral Resources of the Etango Project is based on a resource estimate compiled or reviewed by Mr Brian Wolfe,

a full time employee of Coffey Mining Pty Ltd. Mr Wolfe is a Member of the Australian Institute of Geoscientists and has sufficient experience relevant to the style of

mineralisation and types of deposits under consideration and to the activity which is being undertaken to qualify as a Competent Person as defined in the 2004 Edition

of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”, and is an independent consultant to Bannerman and a

Qualified Person as defined by Canadian National Instrument 43-101. Mr Wolfe consents, and provides corporate consent for Coffey Mining Pty Ltd, to the inclusion

in this presentation of the matters based on his information in the form and context in which it appears.

The information in this presentation relating to the Ore Reserves of the Etango Project is based on information compiled or reviewed by Mr Harry Warries, a full time

employee of Coffey Mining Pty Ltd. Mr Warries is a Fellow of The Australasian Institute of Mining and Metallurgy and has sufficient experience relevant to the style of

mineralisation and types of deposits under consideration and to the activity which is being undertaken to qualify as a Competent Person as defined in the 2004 Edition

of the “Australasian Code for Reporting of Exploration Results, Mineral Resources and Ore Reserves”, and is an independent consultant to Bannerman and a

Qualified Person as defined by Canadian National Instrument 43-101. Mr Warries consents, and provides corporate consent for Coffey Mining Pty Ltd, to the

inclusion in this presentation of the matters based on his information in the form and context in which it appears.

2

Contents

3 Resource definition (core) drilling at the Etango site.

1. Latest Developments

2. Next Steps

3. Investment Rationale

4. Etango Uranium Project DFS

5. Upside Opportunities

6. Appendices

Etango Uranium Project Definitive Feasibility Study (DFS)

Completed on time and within budget.

Demonstrates Etango to be a viable global top 10 pure uranium project.

80% conversion of M&I Resources to Ore Reserves (119Mlbs U3O8) for minimum 16 year mine life.

Facilitates further engagement with potential development partners.

Partnership with Namibian state-owned Epangelo Mining Company:

Conditional binding Term Sheet signed for purchase of an initial 5% interest and an additional

5% option (arising upon a mine development decision) in the Etango Project, both at market value.

Initial 5% transaction delivers approx A$3.9 million cash for Bannerman.

Epangelo to fund its share of future Etango Project expenditure on agreed terms.

Continues to build positive relationship with the Namibian Government and enhances the Etango

Project for potential development partners.

Latest Developments

4

1. Latest Developments

Next Steps

5

Completion of environmental public consultation process.

Completion of Etango DFS.

Signing of a partner agreement with Epangelo.

Commencement of resource expansion drilling programs to add new resources and extend

Etango’s modelled mine life beyond 20 years.

Lodgement of the DFS, environmental assessments and management plans with relevant

regulatory authorities in Namibia in support of an Environmental Clearance and the

existing mining licence application.

Results from resource expansion drilling programs.

Continued engagement with potential development partners, with the DFS in hand.

2. Next Steps

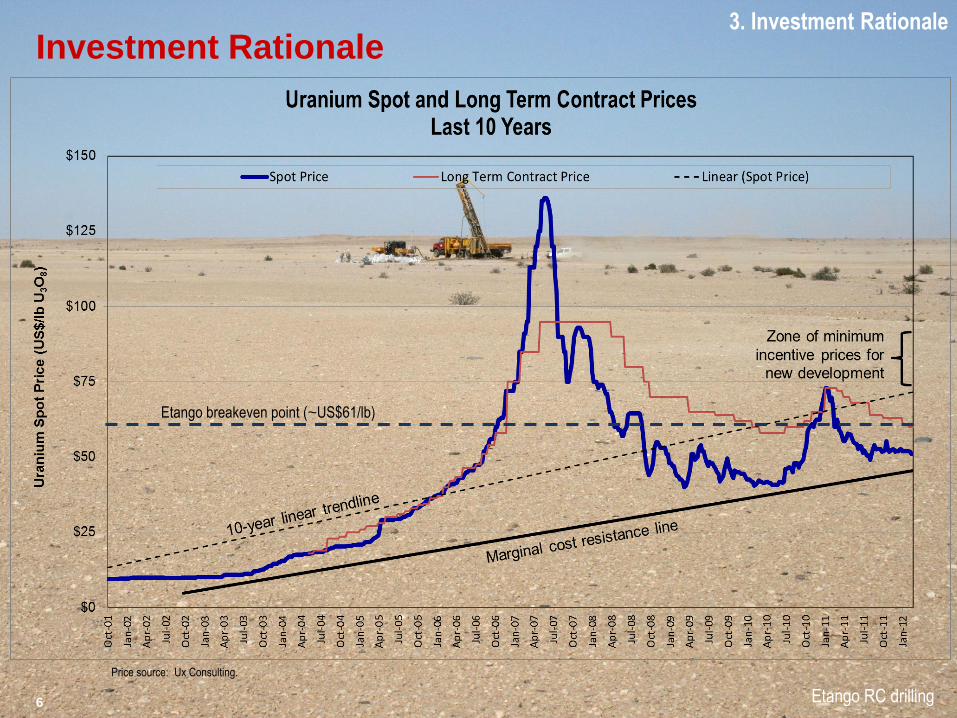

Price source: Ux Consulting.

Investment Rationale

Etango RC drilling 6

Etango breakeven point (~US$61/lb)

3. Investment Rationale

New Reactor Build Outlook: Countries previously living in energy poverty are rapidly expanding

7

Source: WNA April 2011

0

20

40

60

80

100

120

140

160

180

200

Canada UnitedKingdom

SouthKorea

Ukraine France Japan India Russia USA China

Proposed

Planned

Under Construction

Operating Reactors

443 reactors operating,

61 under construction,

495 planned and proposed.

China has stated its intention to

increase from 40 GWe today to

80 GWe by 2020*.

India has recently reiterated its plan to

increase nuclear capacity 14-fold to

63 GWe by 2032.

*Source: The National Energy Administration of China,

and various broker and press reports.

# reactors

3. Investment Rationale

Etango at a Glance Scale, Simplicity, Substance

8

Scale +16 year mine life, 119Mlbs U3O8 P&P Ore Reserves.

Significant production 6-9 Mlbs U3O8 per year.

Low technical risks Conventional mining, metallurgy and processing.

Premier location 35 year history of mining in Namibia, existing infrastructure.

Advanced project One of the few large scale uranium projects with a DFS.

Committed to production Proven team with +US$30bn development experience.

3. Investment Rationale

Global Top 10 Uranium Project

9

0

50

100

150

200

250

300

350

246

134 119

53

McC

arth

ur

Riv

er

Cam

eco

/Are

va

JORC/43-101 Ore Reserves (Mlbs U3O8) of pure uranium projects H

usa

b

Ext

ract

/CG

NP

C

Cig

ar L

ake

Cam

eco

/Are

va

Ran

ger

/Jab

iluka

E

RA

Inka

i C

amec

o/K

azat

om

pro

m

Lan

ger

Hei

nri

ch

Pal

adin

Rö

ssin

g

Rio

Tin

to

Eta

ng

o

Ban

ner

man

Val

enci

a F

ors

ys

Do

rno

d

AR

MZ

Inka

i So

uth

U

ran

ium

On

e

335 320

209

135 119

61

34

Source: Bannerman & Versant Partners, March 2012

Reflects 100% of projects.

3. Investment Rationale

10

High Investment Leverage to the Uranium Price

3. Investment Rationale

Positioned for investment re-rating…

11

Source: Various broker research, Bannerman, April 2012

US$0.90

US$1.40

US$0.85

US$4.00

US$5.20

-

US$1.00

US$2.00

US$3.00

US$4.00

US$5.00

US$6.00

Listed uranium companies - Enterprise values (US$)

per attributable U3O8 resource pound

Exploration Pre-Feasibility Feasibility Developer Producer

Bannerman

US$0.35/lb

3. Investment Rationale

3. Etango Uranium Project

4. Etango Uranium Project DFS Global top 10 undeveloped uranium project

Resource definition (RC) drilling at the Etango site. 12

Definitive Feasibility Study

13

Over 30 man years of technical effort over a 4 year period.

Over US$50 million invested in resource drilling, testwork and feasibility engineering.

Globally renowned independent technical experts – AMEC, Coffey Mining and Bateman.

Comprehensive implementation plan for engineering, procurement, construction and commissioning.

4. Etango Uranium Project DFS

14

DFS Highlights

Mine life Minimum 16 years with defined extension opportunities

Mining & processing Conventional open pit mining; three-stage crushing; heap leaching, SX

Waste/ore strip ratio 3.3 : 1

Plant throughput 20 million tonnes of ore per year

Production (annual) 7-9 Mlbs U3O8 per year in first five years, thereafter 6-8 Mlbs U3O8/year

Production (life of mine) 104 Mlbs U3O8 with defined extension opportunities

Pre-production capital cost US$870 million

Sustaining capital Funded from operating cashflow - US$381 over the life of mine

Operating cost US$41/lb in years 1-5; US$46/lb U3O8 over the life of mine

Operating margin 32% for years 1-5 at current LT contract price of US$60/lb U3O8

46% for years 1-5 at base case price of US$75/lb U3O8

Payback (post-production) 6 years

Breakeven uranium price US$61/lb U3O8

4. Etango Uranium Project DFS

Etango Project Mineral Resource and

Ore Reserve Estimates

15

Notes:

1. Figures may not add due to rounding.

2. Bannerman holds an 80% interest in the Etango Project through its Namibian subsidiary. All details reported are for 100% of the Project.

3. Mineral Resources are reported at a cut-off grade of 100ppm U3O8 and are inclusive of Ore Reserves.

4. Ordinary Kriged Resource estimate based upon 3m cut composites; bulk density of 2.64t/m3; and panel dimensions of 25mNS by 25mEW by 10mRL.

5. The Ore Reserve was estimated with a modelled mining loss of 2.6% of metal, mining dilution of 4.9% of the total ore tonnes, a cut-off grade of 70ppm

U3O8, a processing recovery of 84.5%, a metal price of US$75/lb U3O8 and the DFS cost estimates.

6. Mineral Resources which are not Ore Reserves do not have demonstrated economic viability.

Category Tonnes

(Mt)

Grade

(ppm U3O8)

Contained U3O8

(Mlbs)

Measured 62.7 205 28.3

Indicated 273.5 200 120.4

Measured & Indicated Resource 336.2 201 148.8

Inferred (Etango) 45.7 202 20.3

Inferred (Ondjamba & Hyena) 118.7 166 43.6

Proved and Probable Ore Reserve 279.6 194 119.3

80%

conversion

4. Etango Uranium Project DFS

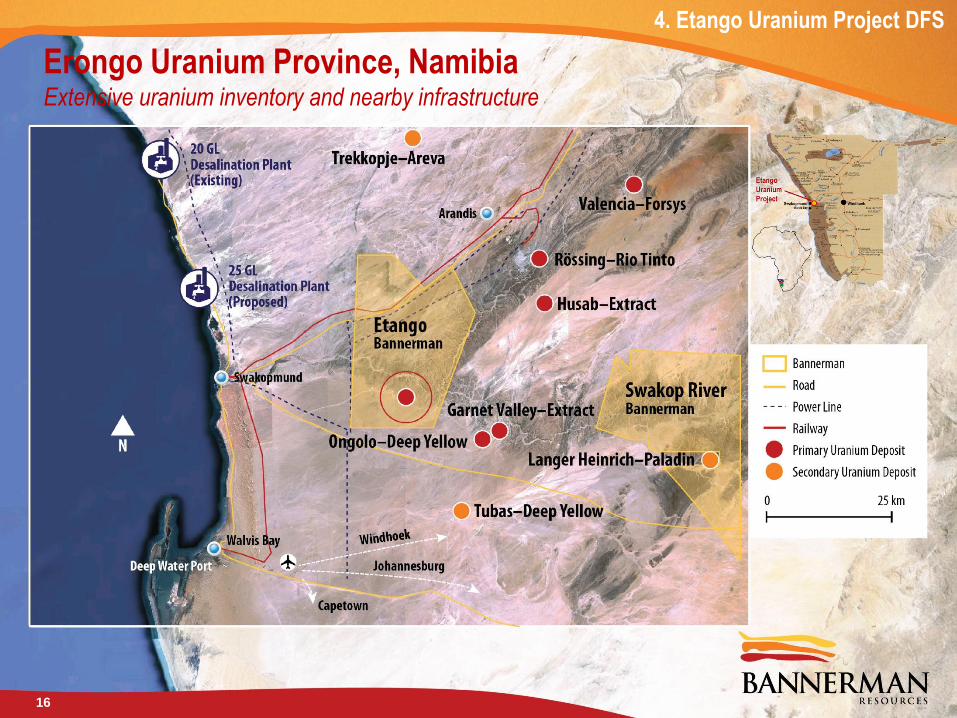

Erongo Uranium Province, Namibia Extensive uranium inventory and nearby infrastructure

16

4. Etango Uranium Project DFS

Erongo Region Trading hub of Namibia

17

4. Etango Uranium Project DFS

Key Features

18

Consistent mineralisation in broad

zones, from surface.

Shallow deposit enables fast ramp-

up as 70% of the mineralisation is

within 200 metres of surface.

~90% of mineralisation within the

visual alaskite (granite) host rock

unit.

Waste/ore ratio of 3.3 to 1.

Rapid leaching.

Etango Site Layout

4. Etango Uranium Project DFS

19

Simple Open Pit Mining Operation

YEAR 16

6km

1.2 billion

tonnes (ore and

waste) mined

over 16 years

Years 1-5 mining fleet:

• 32 haul trucks

• 15 drills

• 6 excavators

• 6 graders

• 6 bulldozers

1km

4. Etango Uranium Project DFS

Conventional Process Flowsheet…

20

4. Etango Uranium Project DFS

21

Conventional On-Off Heap Leach Operation

4. Etango Uranium Project DFS

22

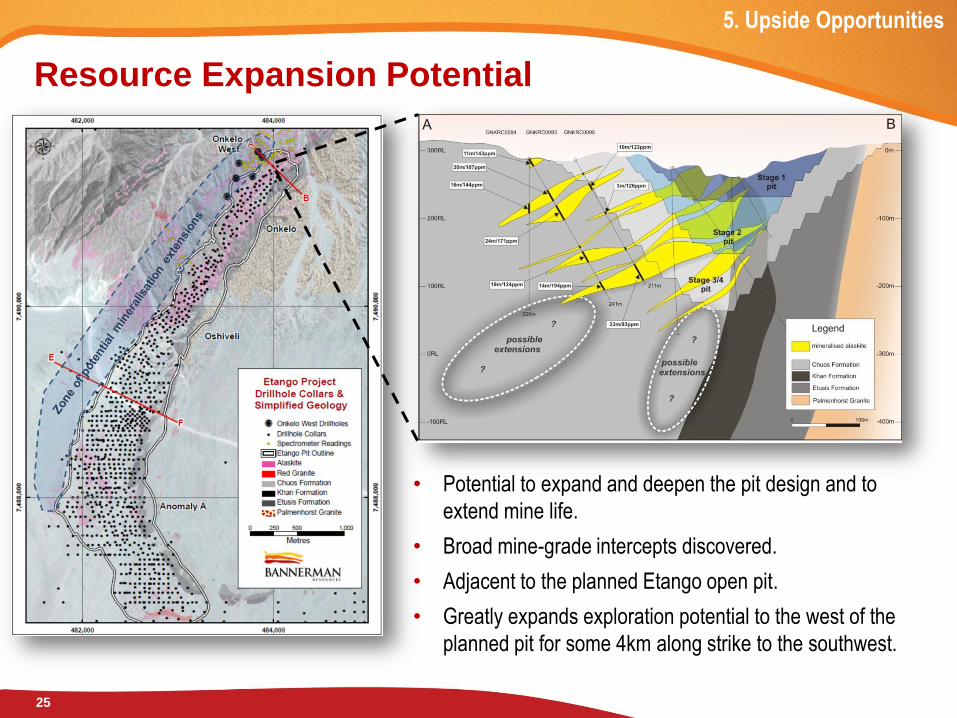

5. Upside Opportunities

Etango RC drilling

Increased Resource Utilisation

23

Ondjamba Deposit

(Inferred resource)

Hyena Deposit

(Inferred resource)

Etango Deposit

Open at depth

Resource zones

outside pit design

1km

5. Upside Opportunities

Total U3O8 Mineral Resource comprises 149Mlbs M&I and 64Mlbs Inferred

Resource Expansion Drilling Programs

24

5. Upside Opportunities

5km

N

Etango Project Area

Existing Etango resource (149Mlbs M&I

and 64Mlbs Inferred)

Etango Deeps Target (red)

Etango West Target (blue)

Etango South Target (green)

Ondjamba/Hyena Already drilled (yellow)

Additional target (green)

Ompo Already drilled (yellow)

Additional target (green)

First stage

drilling just

commenced.

Resource Expansion Potential

25

• Potential to expand and deepen the pit design and to

extend mine life.

• Broad mine-grade intercepts discovered.

• Adjacent to the planned Etango open pit.

• Greatly expands exploration potential to the west of the

planned pit for some 4km along strike to the southwest.

5. Upside Opportunities

26

In Summary Bannerman well positioned to take advantage of expected higher uranium prices

DFS completed.

Partnership agreement with Epangelo (subject to due diligence and

financing).

Commencement of resource expansion drilling program.

Lodgment of updated environmental studies and management plans

in June 2012 quarter in support of Mining Licence application.

Stepping up engagement with potential development partners.

www.bannermanresources.com Scale, Simplicity, Substance

Corporate Snapshot As at April 5, 2012

Share price A$0.205

Shares - currently on issue 297 M

Shares - fully diluted (for options, rights, existing convertible note & contingent issues) 337 M

Market capitalisation (undiluted) A$61M / US$63M

Average daily traded volume in last 12 months ~1.4M shares/day

Cash on hand (as at December 31, 2011) A$12.3 million

Project ownership: 80% of the Etango Uranium Project, Namibia.

Institutional ownership ~31%

Board/management ~13%

North America

Australia

Europe

Namibia

Asia

Shareholder distribution

28

APPENDIX

Historical Share Price Demonstrates Leverage

29

APPENDIX

Epangelo Agreement – Key Terms

30

Documentation Binding Term Sheet signed between Bannerman, Epangelo, Bannerman’s 80% Namibian subsidiary

Bannerman Mining Resources (Namibia) (Pty) Ltd (BMRN) and the private 20% shareholder of BMRN.

Interest to be

acquired

Epangelo can purchase 5% of BMRN by acquiring interests from the existing BMRN shareholders for the

look-through value calculated at a share price of A$0.225 per Bannerman share. This equates to sales

proceeds for Bannerman of approximately A$3.9 million. The post-acquisition shareholdings in BMRN are

Bannerman (76%), Epangelo (5%) and the existing private shareholder (19%).

Conditions Conditional on a four month period for completion of Epangelo due diligence, sourcing of acquisition finance,

full-form documentation and receipt of regulatory approvals (as required).

Funding Epangelo to fund its share of Project expenditure or dilute in accordance with agreed mechanism:

• Funding for the period up to a mine development decision to come either from third parties or via a loan from

Bannerman on commercial terms (interest at LIBOR+6%, secured over Epangelo’s shares in BMRN and

repayable from future mine dividends); and

• After a mine development decision, if Epangelo does not contribute its share of cash calls, it shall dilute

ultimately to nil in accordance with an agreed “dilution and sale” formula.

Option Epangelo has a one-off option to acquire an additional 5% in BMRN upon a mine development decision for a

2.5% discount to the look-through market value at that time.

BMRN Board

representation

Epangelo shall shortly appoint one representative to the BMRN Board. Epangelo’s representative will resign

from the Board should the acquisition not be completed within the four month period.

Pre-emptive rights Pre-emptive rights exist in favour of non-selling BMRN shareholders.

Epangelo capacity

building

Bannerman will assist in building Epangelo’s management and technical capacity through secondments of

Epangelo personnel to the Etango Project team and through education and training initiatives.

APPENDIX

31

Benefits for Namibia Significant new employment opportunities and royalty/taxation revenues

APPENDIX

• Employment opportunities - Creation of 800-1,500 new jobs during construction, and an average of 1,000 new

jobs during operations. The majority of employees are expected to be recruited in Namibia.

• Education and training for Namibians working in the operation, with the annual training and education budget

incorporated in the DFS capital and operating cost estimates.

• Economic “multiplier effect” of mine and employee expenditure in the local communities and in Namibia

generally. Economic modelling by independent experts has indicated that the mine operating phase will create a

further ~1,500 indirect jobs in the local communities.

• Mineral royalties to the Namibian Government equal to 3% of net revenues, equating to approximately

US$14-20 million (N$100-150 million) per year at a base case uranium price of US$75/lb U3O8.

• Company taxes of over US$0.5 billion (N$4 billion) over the life-of-mine at a base case uranium price of

US$75/lb U3O8.

• Employee PAYE taxes of at least US$8 million (N$60 million) per year over the life-of-mine.

• Other taxes including import duties.

• Expansion of Bannerman’s existing reputable corporate social responsibility program which focusses on

education and tourism related activities at regional and national levels.

Etango – DFS Pre-Production Capital Costs

32

APPENDIX

DFS Pre-Production Capital Cost Estimate (April 2012) US$

million

Mining – fleet, establishment & pre-stripping 127

Process plant 354

Site infrastructure 91

External infrastructure (power, water, rail, road and port) 47

EPCM costs 72

Accuracy provision 54

First fills and spares 29

Owner’s costs (personnel, housing, training, insurance etc) 40

Other (camp facilities, mobilisation and demobilisation and

temporary services)

56

Total pre-production capital expenditure 870

33

APPENDIX

DFS Cash Operating Cost Estimate (April 2012) First 5

Years

Life-of-

Mine

Mining:

- US$/tonne mined

- US$/tonne ore

1.72

7.87

1.97

8.55

Processing (US$/tonne ore):

Consumables, labour, maintenance & other 3.37 3.41

Sulphuric acid 1.78 1.79

Power 1.29 1.31

Water 0.64 0.65

7.08 7.15

General & administration ( US$/tonne ore): 1.26 1.23

Total cash operating costs (US$/tonne ore) 16.21 16.93

Total cash operating costs (US$/lb U3O8 produced) 40.85 45.71

Etango – DFS Cash Operating Costs

34

Proven Track Record

Dec 2011

APPENDIX

Straightforward

Metallurgy

35

Uranium recoveries greater than

90% have been consistently

achieved in short leach cycle

times;

Low in acid-consuming

carbonates.

Little, if no, oxidant required.

Good geotechnical stability and

high permeability promotes heap

leaching.

Granitic – “sand &

gravel” like, with no clay Close-up image of the base of a

7 metre column test

APPENDIX

36

Bannerman in Namibia

Bannerman personnel at the Biodiversity Street Parade, Swakopmund

APPENDIX

37

Early Learner Assistance Program in local schools

Pioneered cooperation with

tourism bodies including the

Coastal Tourism Association of Namibia

Radiation safety initiatives,

including the first Radiation Management Plan

Environmental rehabilitation of all drill sites

Making a Real Difference

Assistance with the creation, growth and training of local businesses

Support of the Erongo Development Foundation

Co-sponsor of the annual

Hospitality Association of Namibia conference

Training and

education initiatives

APPENDIX