midlothian isd · builders start 114 and close 100 new homes in the district during the 2nd quarter...

TRANSCRIPT

Midlothian ISD

District Housing

Activity Report 2Q 2016

Solutions Through Demographics

DFW: STARTS, CLOSINGS & LOT DELIVERIES

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

55,000

60,000

20

03 2 3 4

20

04 2 3 4

20

05 2 3 4

20

06 2 3 4

20

07 2 3 4

20

08 2 3 4

20

09 2 3 4

20

10 2 3 4

20

11 2 3 4

20

12 2 3 4

20

13 2 3 4

20

14 2 3 4

20

15 2 3 4

20

16 2

An

nu

al R

ate

Starts Closings Lot Deliveries

Year-Over-Year Change

Annual Starts +13.7%

Annual Closings +18.0%

Annual Starts: 29,492

Annual Closings: 26,631

Current Cycle

2

3

HOUSING GROWTH DRIVERS: TEXAS ECONOMY

-500,000

-400,000

-300,000

-200,000

-100,000

0

100,000

200,000

300,000

400,000

500,000

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 15 16

Annual Texas Employment GrowthJob growth

June, 2015 – June, 2016

United States

– +2.522 million +1.77%

Texas

– +172,600 +1.45%

# of Jobs Created in Past 5 Years

– DFW 516,300

– Houston 367,800

– Austin 192,400

– San Antonio 136,100

Annual Job Growth in Major Texas Markets (June, 2016)

– DFW +114,100

– Austin +38,400

– San Antonio +23,40

– Houston +5,200

Source: TWC – CES (Not Seasonally

Adjusted)

6/2015 - 6/2016+172,600 net new jobs

+1.45% growth rate12,035,500 employed

4

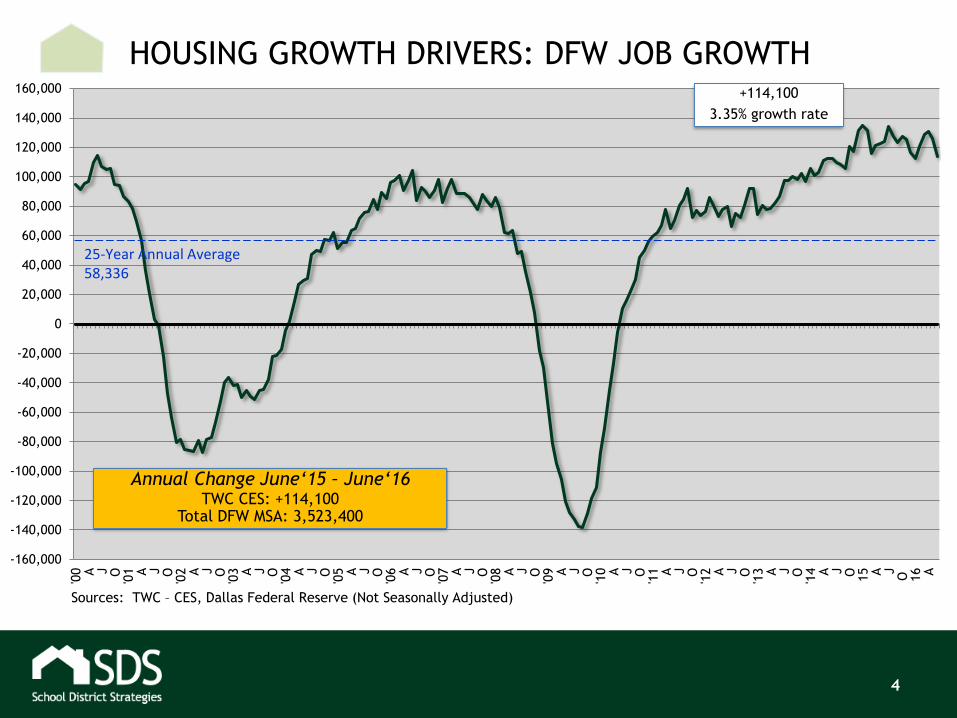

HOUSING GROWTH DRIVERS: DFW JOB GROWTH

-160,000

-140,000

-120,000

-100,000

-80,000

-60,000

-40,000

-20,000

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000'0

0 A J O'0

1 A J O'0

2 A J O'0

3 A J O'0

4 A J O'0

5 A J O'0

6 A J O'0

7 A J O'0

8 A J O'0

9 A J O'1

0 A J O'1

1 A J O'1

2 A J O'1

3 A J O'1

4 A J O 15 A J

O 16 A

Sources: TWC – CES, Dallas Federal Reserve (Not Seasonally Adjusted)

Annual Change June‘15 – June‘16TWC CES: +114,100

Total DFW MSA: 3,523,400

+114,100

3.35% growth rate

25-Year Annual Average58,336

5

HOUSING GROWTH DRIVERS: LOW MORTGAGE RATES

3

3.5

4

4.5

5

5.5

6

6.5

7

2008

2009

2010

2011

2012

2013

2014

2015

2016

Source: Freddie Mac

July 21, 2016

30YR : 3.45%

15YR : 2.75%

1YR ARM : 2.78%

30-Yr Fixed Rate Outlook

Mortgage Bankers

AssociationConforming Rates: 7/14/16 Forecast

3Q16 3.6%

4Q16 3.8%

1Q17 4.0%

2Q17 4.1%

30-Yr Conforming Rates (Freddie Mac)

30-Yr rate has been under 4% for

most of the current housing cycle

6

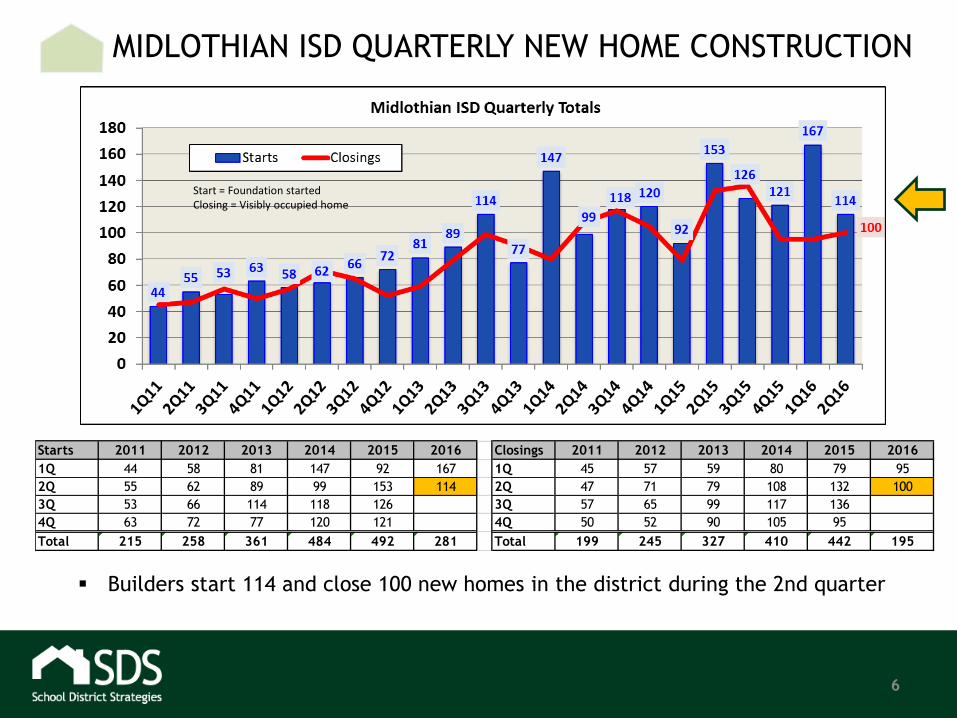

MIDLOTHIAN ISD QUARTERLY NEW HOME CONSTRUCTION

Start = Foundation started Closing = Visibly occupied home

Builders start 114 and close 100 new homes in the district during the 2nd quarter

Starts 2011 2012 2013 2014 2015 2016 Closings 2011 2012 2013 2014 2015 2016

1Q 44 58 81 147 92 167 1Q 45 57 59 80 79 95

2Q 55 62 89 99 153 114 2Q 47 71 79 108 132 100

3Q 53 66 114 118 126 3Q 57 65 99 117 136

4Q 63 72 77 120 121 4Q 50 52 90 105 95

Total 215 258 361 484 492 281 Total 199 245 327 410 442 195

7

MIDLOTHIAN ISD ANNUAL NEW HOME CONSTRUCTION

& LOT DELIVERIES

Annual Starts: 528

Annual Closings: 426

Year-Over-Year Change

Annual Starts +9.3%

Annual Closings -1.6%

Builders start construction on 528 new homes in the district over the past 12 months

New home closings fall back to 426 annual units (-1.6% Y-o-Y)

Developers deliver 715 new single-family lots in MISD over the past year

Start = Foundation started Closing = Visibly occupied home

Rank District

Total Starts

3Q15-2Q16

Total Closings

3Q15-2Q16

ESC

Region

1 Frisco 2,570 2,600 10

2 Denton 2,146 1,858 11

3 Prosper 2,489 1,835 10

4 Northwest 1,366 1,243 11

5 Lewisville 1,310 1,197 11

6 Little Elm 1,016 1,077 11

7 Keller 806 942 11

8 Eagle Mtn.-Saginaw 858 941 11

9 Rockwall 951 741 10

10 Crowley 851 719 11

11 Mansfield 759 668 11

12 McKinney 842 643 10

13 Wylie 724 597 10

14 Dallas 717 562 10

15 Forney 574 500 10

16 Allen 551 492 10

17 Burleson 452 491 11

18 Plano 483 464 10

19 H.E.B. 432 455 11

20 Midlothian 528 426 10

8

DFW DISTRICT RANKINGS

BY NEW HOME CLOSINGS 3Q15-2Q16

• Midlothian ISD

ranked 17th in total

new home starts and

20th in total closings

over the past year

compared to the

other 81 DFW school

districts

9

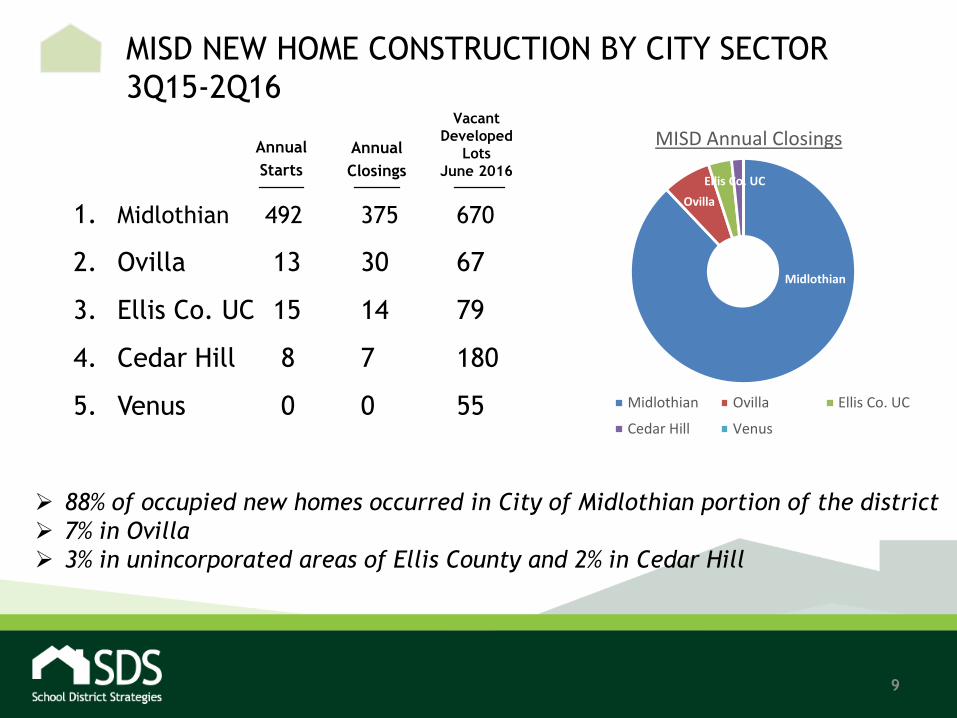

MISD NEW HOME CONSTRUCTION BY CITY SECTOR

3Q15-2Q16

1. Midlothian 492 375 670

2. Ovilla 13 30 67

3. Ellis Co. UC 15 14 79

4. Cedar Hill 8 7 180

5. Venus 0 0 55

Annual

Starts

Annual

Closings

Vacant

Developed

Lots

June 2016

88% of occupied new homes occurred in City of Midlothian portion of the district

7% in Ovilla

3% in unincorporated areas of Ellis County and 2% in Cedar Hill

Midlothian

Ovilla

Ellis Co. UC

MISD Annual Closings

Midlothian Ovilla Ellis Co. UC

Cedar Hill Venus

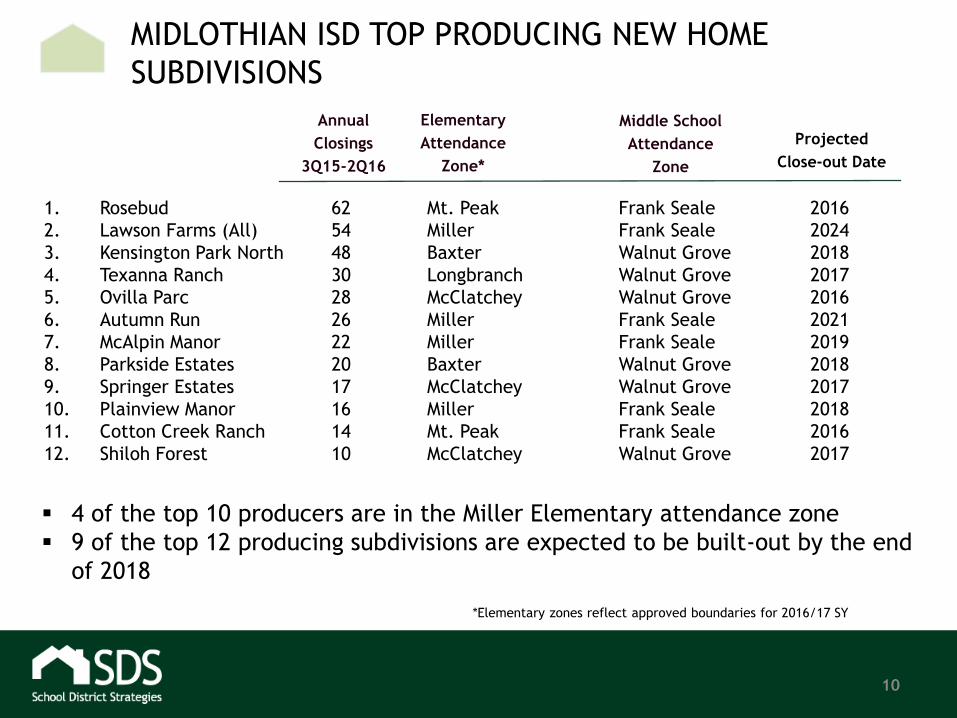

1. Rosebud 62 Mt. Peak Frank Seale 2016

2. Lawson Farms (All) 54 Miller Frank Seale 2024

3. Kensington Park North 48 Baxter Walnut Grove 2018

4. Texanna Ranch 30 Longbranch Walnut Grove 2017

5. Ovilla Parc 28 McClatchey Walnut Grove 2016

6. Autumn Run 26 Miller Frank Seale 2021

7. McAlpin Manor 22 Miller Frank Seale 2019

8. Parkside Estates 20 Baxter Walnut Grove 2018

9. Springer Estates 17 McClatchey Walnut Grove 2017

10. Plainview Manor 16 Miller Frank Seale 2018

11. Cotton Creek Ranch 14 Mt. Peak Frank Seale 2016

12. Shiloh Forest 10 McClatchey Walnut Grove 2017

10

MIDLOTHIAN ISD TOP PRODUCING NEW HOME

SUBDIVISIONS

Annual

Closings

3Q15-2Q16

Elementary

Attendance

Zone*

Middle School

Attendance

Zone

Projected

Close-out Date

4 of the top 10 producers are in the Miller Elementary attendance zone

9 of the top 12 producing subdivisions are expected to be built-out by the end

of 2018

*Elementary zones reflect approved boundaries for 2016/17 SY

11

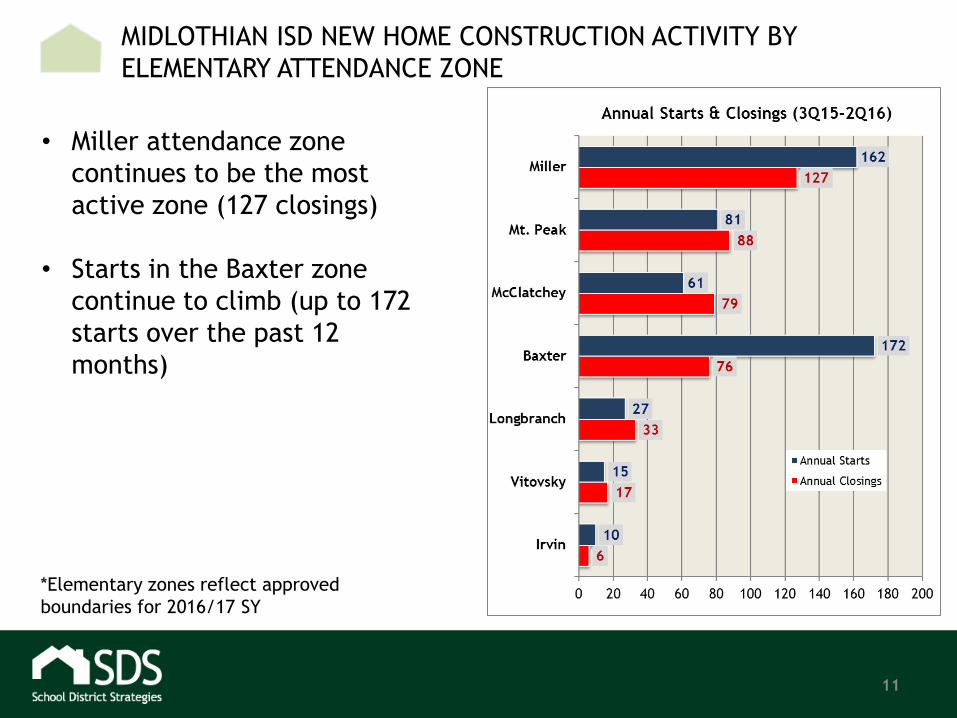

MIDLOTHIAN ISD NEW HOME CONSTRUCTION ACTIVITY BY

ELEMENTARY ATTENDANCE ZONE

• Miller attendance zone

continues to be the most

active zone (127 closings)

• Starts in the Baxter zone

continue to climb (up to 172

starts over the past 12

months)

*Elementary zones reflect approved

boundaries for 2016/17 SY

12

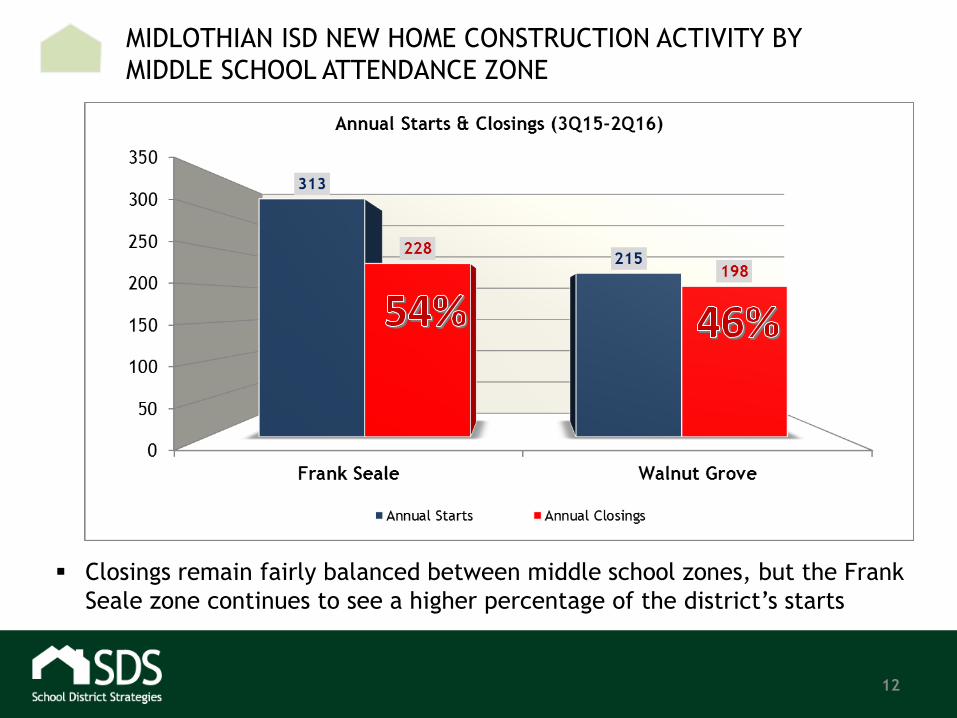

MIDLOTHIAN ISD NEW HOME CONSTRUCTION ACTIVITY BY

MIDDLE SCHOOL ATTENDANCE ZONE

Closings remain fairly balanced between middle school zones, but the Frank

Seale zone continues to see a higher percentage of the district’s starts

13

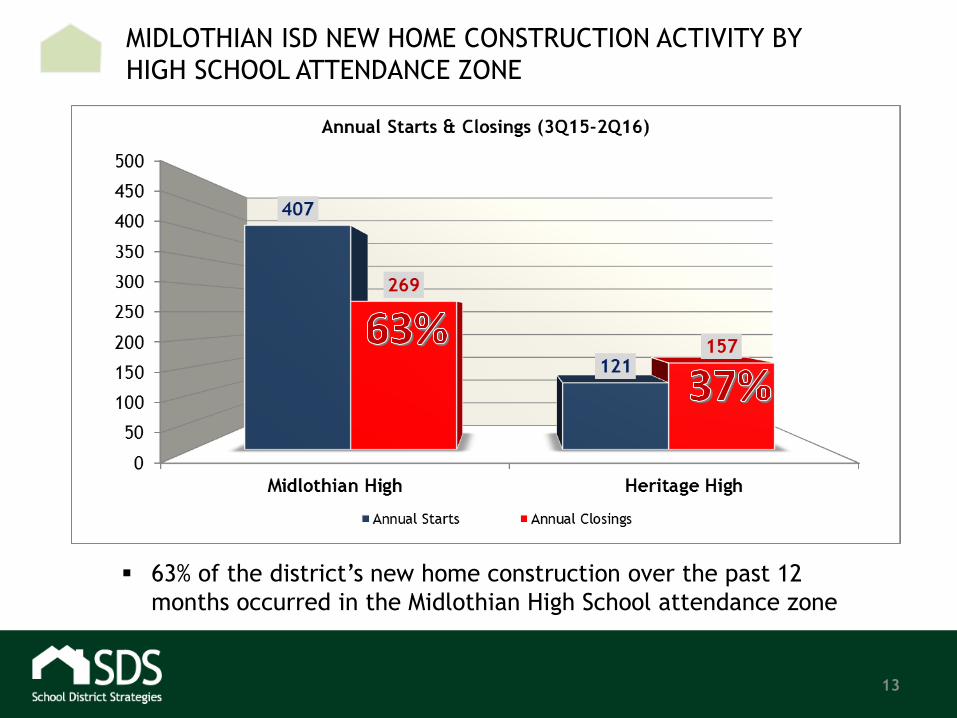

MIDLOTHIAN ISD NEW HOME CONSTRUCTION ACTIVITY BY

HIGH SCHOOL ATTENDANCE ZONE

63% of the district’s new home construction over the past 12

months occurred in the Midlothian High School attendance zone

14

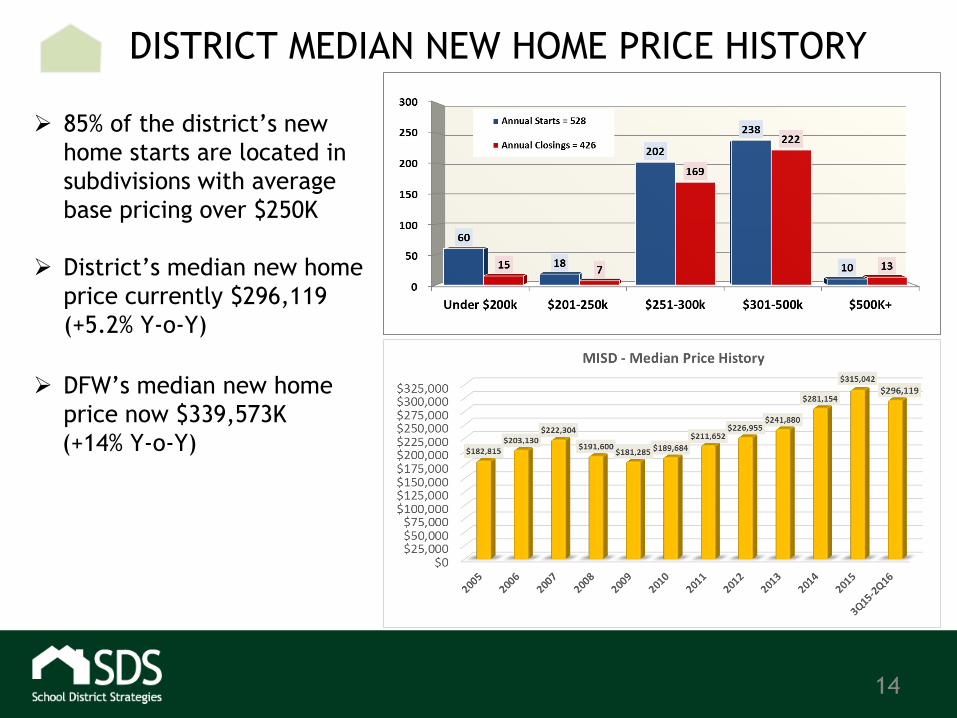

DISTRICT MEDIAN NEW HOME PRICE HISTORY

85% of the district’s new

home starts are located in

subdivisions with average

base pricing over $250K

District’s median new home

price currently $296,119

(+5.2% Y-o-Y)

DFW’s median new home

price now $339,573K

(+14% Y-o-Y)

15

MIDLOTHIAN ISD RESIDENTIAL DEVELOPMENT

1,218 future single-family residential lots currently under

development in MISD (New record for 12-month period)

© School District Strategies

16

MIDLOTHIAN ISD RESIDENTIAL DEVELOPMENT

118 new lots delivered in 2Q16 Bryson Manor Ph. 1 – 59 lots (McClatchey/Walnut Grove/Heritage)

Dove Creek Ph.1A – 59 lots (Mt. Peak/Seale/MHS)

1,051 total vacant developed lots on the ground in the district as June 2016

1,218 Future Lots Under Development Skyview – 120 duplexes (Irvin)

Summit at Lake Ridge Ph. 22-B – 33 lots (Vitovsky)

Kensington Park North Ph. 2 – 81 lots (Baxter)

Jordan Run Ph. 3 – 27 lots (Mt. Peak)

Autumn Run Ph. 2 – 53 lots (Miller)

Hawkins Meadow Ph.1 – 123 lots (Miller)

Hillstone Estates Ph.1 – 78 lots (Miller)

Lawson Farms Ph. 2A – 314 lots (Miller)

Enclave at Lawson Farms – 60 lots (Miller)

Four Trees – 138 lots (McClatchey)

Bryson Springs Ph.1 – 36 lots (McClatchey)

Horizon Estates – 81 lots (Longbranch)

Bob White Estates – 74 lots (Longbranch)

52% (628 lots) are under development in the Miller Elementary zone

*Blue = New or updated in 2Q16

Note: In July, lot development started at Thomas Trail Estates (89 lots in Mt. Peak) and Mockingbird Lane Addition (73 lots in McClatchey)

Baxter ES Zone:

The Grove South – 176 lots

Townhome tract Z11-2015-48

(rezoning denied by City)

Irvin ES Zone:

Pandera Point Apartments – 199 units

Longbranch ES Zone:

Diamond J Ranch (+/- 2,700 lots)

Heritage Crossing – 272 lots

Hayes Crossing – 338 lots (plat denied

by City)

Legacy Estates – 116, 1-acre lots

Shady Valley Estates – 91 lots

Spring Creek Estates – 104 lots

Clifton Place – 21 lots

Miller ES Zone:

Tract Z14-2015-65 – 50 lots

17

MISD PROPOSED RESIDENTIAL PROJECTS

McClatchey ES Zone:

Mockingbird Lane Addition (76, 1-acre

lots)

Stonewood Lake Estates – 143 lots

Wilson Crossing – 86 lots (W. of La Rinconada)

Mt. Peak ES Zone:

Thomas Trail Estates - 89 lots

La Paz Ranch – 128 lots

Vitovsky ES Zone:

Windsor Hills (Ellis Co. FWSD No. 2)

Lakeview Hills

Greenway Trails (Walton) - 669 lots

Prairie Ridge - 1,286 lots

Highland Meadows – 747 lots

Cottonwood Creek - 325 lots

Cashmere Ranch Apartments

28.8 acre tract south of Overlook Est.

*Blue = New or updated in 2Q16

18

Aerial Photos

June 30, 2016

19

NSH 360 Toll Road

Mansfield ISD

Midlothian ISD

20

NKensington Park North

21

NFour Trees

22

NParkside Estates

Mockingbird Estates

Baxter Elem.

23

NWindermere Estates

Kensington Park

Mockingbird Estates

24

NMaple Ridge Townhomes

Proposed Rezoning for Townhomes

Timber Oaks Apts.

N. 14th St.

25

NSkyview

Future Pandera Point

ApartmentsRidgeview Estates

26

NHawkins Meadow / Midlothian

Towne Crossing Retail

Lawson Farms

Hawkins Meadow

Future Kroger

SH 287

27

NAutumn Run

Lawson Farms

Ph. 2

Hawkins MeadowFuture Kroger

28

NLawson Farms (North Side)

FutureCity Park

Hawkins Meadow

29

NLawson Farms (South Side)

FutureCity Park

30

NHillstone Estates

31

N

Dove Creek

McAlpin Rd

Future Coventry Crossing Ph. 2

32

NCoventry Crossing

Hill Crest Addition

33

NMcAlpin Manor

34

MIDLOTHIAN ISD RESIDENTIAL LOT INVENTORY BY ELEM. ZONE

ATTENDANCE ZONE* ANNUAL STARTS3Q15-2Q16

DEVELOPED LOTS

REMAINING(VDL)

FUTURE & PRELIM

PLANNED SINGLE FAMILY

LOTS

PLANNED FUTURE

APARTMENT UNITS

BAXTER 172 261 413 0

IRVIN 10 21 485 199

LONGBRANCH 27 16 3,834 0

McCLATCHEY 61 189 665 0

MILLER 162 186 1,085 0

MT. PEAK 81 138 801 0

VITOVSKY 15 240 12,034 95

TOTAL 528 1,051 19,317 294

*Elementary

zones reflect

approved

attendance

zones for

2016/17 SY

35

MIDLOTHIAN ISD RESIDENTIAL LOT INVENTORY BY

MIDDLE AND HIGH SCHOOL ZONE

ATTENDANCE ZONE ANNUAL STARTS3Q15-2Q16

DEVELOPED LOTSREMAINING

(VDL)

FUTURE & PRELIM PLANNED

SINGLE FAMILY LOTS

PLANNED FUTURE APARTMENT UNITS

FRANK SEALE 313 582 5,684 199

WALNUT GROVE 215 469 13,633 95

TOTAL 528 1,051 19,317 294

ATTENDANCE ZONE ANNUAL STARTS3Q15-2Q16

DEVELOPED LOTSREMAINING

(VDL)

FUTURE & PRELIM PLANNED

SINGLE FAMILY LOTS

PLANNED FUTURE APARTMENT UNITS

MIDLOTHIAN HS 407 820 14,667 294

HERITAGE HS 121 231 4,650 0

TOTAL 528 1,051 19,317 294

36

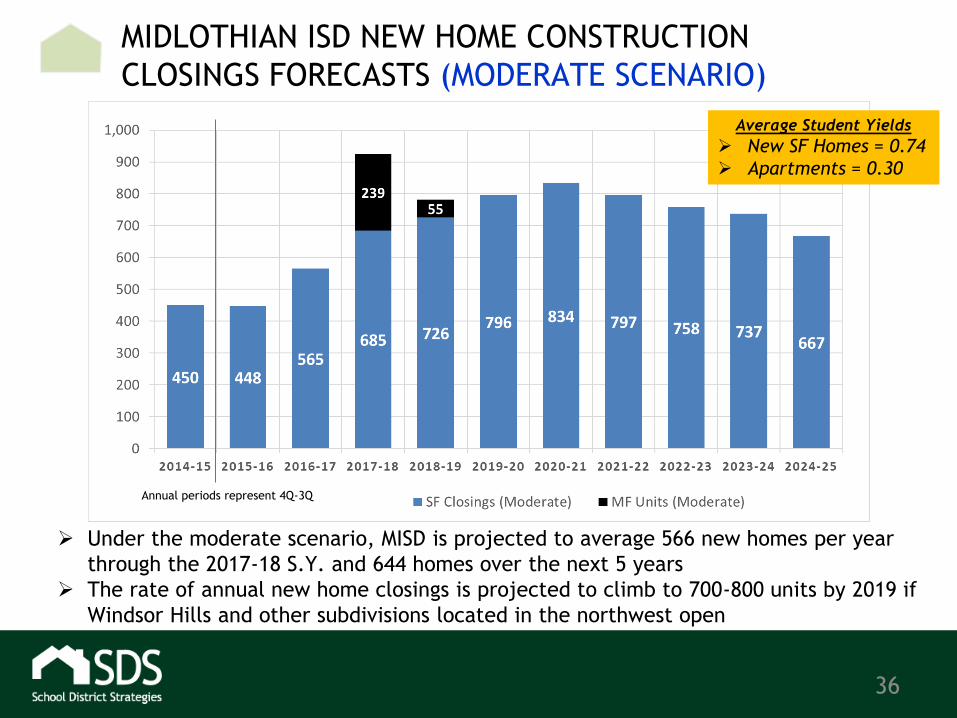

MIDLOTHIAN ISD NEW HOME CONSTRUCTION

CLOSINGS FORECASTS (MODERATE SCENARIO)

Under the moderate scenario, MISD is projected to average 566 new homes per year

through the 2017-18 S.Y. and 644 homes over the next 5 years

The rate of annual new home closings is projected to climb to 700-800 units by 2019 if

Windsor Hills and other subdivisions located in the northwest open

Annual periods represent 4Q-3Q

Average Student Yields

New SF Homes = 0.74

Apartments = 0.30

37

MIDLOTHIAN ISD NEW HOME CONSTRUCTION

CLOSINGS FORECAST (HIGH SCENARIO)

Under the high growth scenario, new home closings in the district would average

639 per year over the next 3 years and then climb to 900 homes per year by 2020

(averaging 744 per year over the next 5 years)

Annual periods represent 4Q-3Q

Average Student Yields

New SF Homes = 0.74

Apartments = 0.30

38

MIDLOTHIAN ISD PRE-OWNED HOME SALES

• 166 resales in the district during the 2nd quarter of 2016

• 615 total resales over the past 12 months (+14% year-over-year)

• 3Q15-2Q16 Median resale price = $225,000 (+13.7% Y-o-Y)

Source: NTREIS – SF detached, non-builder sales only

39

MIDLOTHIAN ISD PRE-OWNED HOME SALES 3Q15-2Q16

Source: NTREIS – SF detached, non-builder sales only 7/1/2015-6/30/2016

40

Projected

Historical

Moderate Projected Enrollment Growth

3 Year = +1,3015 Year = +2,390

10 Year = +5,066

Low =2.7%Avg. AnnualGrowth

41

MISD FACILITY CAPACITY TIMELINE 2Q 2016 (MODERATE)

Current

2015/16 2016/17 2017/18 2018/19 2019/20 2020/21 2021/22 2022/23 2023/24 2024/25 2025/26

Baxter Elementary Campus Capacity = 750

Total Enrollment 647 602 654 706 729 752 771 784 797 809 822

Capacity Utilization 86% 80% 87% 94% 97% 100% 103% 105% 106% 108% 110%

Space Remaining 103 148 96 44 21 -2 -21 -34 -47 -59 -72

Irvin Elementary Campus Capacity = 400

Total Enrollment 365 360 367 412 420 428 437 441 444 447 450

Capacity Utilization 91% 90% 92% 103% 105% 107% 109% 110% 111% 112% 112%

Space Remaining 35 40 33 -12 -20 -28 -37 -41 -44 -47 -50

Longbranch Elementary Campus Capacity = 750

Total Enrollment 730 544 548 561 581 613 645 679 712 746 777

Capacity Utilization 97% 73% 73% 75% 78% 82% 86% 90% 95% 100% 104%

Space Remaining 20 206 202 189 169 137 105 71 38 4 -27

Miller Elementary Campus Capacity = 750

Total Enrollment 585 547 602 671 744 807 866 919 962 990 1,002

Capacity Utilization 78% 73% 80% 89% 99% 108% 115% 123% 128% 132% 134%

Space Remaining 165 203 148 79 6 -57 -116 -169 -212 -240 -252

Mt. Peak Elementary Campus Capacity = 750

Total Enrollment 786 668 695 727 762 806 851 888 918 943 965

Capacity Utilization 105% 89% 93% 97% 102% 107% 113% 118% 122% 126% 129%

Space Remaining -36 82 55 23 -12 -56 -101 -138 -168 -193 -215Vitovsky Elementary Campus Capacity = 750

Total Enrollment 635 635 648 673 702 748 814 900 1,001 1,119 1,244

Capacity Utilization 85% 85% 86% 90% 94% 100% 109% 120% 134% 149% 166%

Space Remaining 115 115 102 77 48 2 -64 -150 -251 -369 -494

McClatchey Elementary Campus Capacity = 750

Total Enrollment n/a 502 533 573 618 665 707 738 759 777 785

Capacity Utilization 67% 71% 76% 82% 89% 94% 98% 101% 104% 105%

Space Remaining 248 217 177 132 85 43 12 -9 -27 -35

Elementary Totals Total Elementary Capacity = 4,900

Total Enrollment 3,748 3,858 4,047 4,323 4,557 4,819 5,090 5,348 5,593 5,831 6,045

Capacity Utilization 76% 79% 83% 88% 93% 98% 104% 109% 114% 119% 123%

Space Remaining 1,152 1,042 853 577 343 81 -190 -448 -693 -931 -1,145

Midlothian ISD - Campus

Projections (Moderate

Scenario)

Projected Fall Enrollment

42

MISD FACILITY CAPACITY TIMELINE 2Q 2016 (MODERATE)

Current

2015/16 2016/17 2017/18 2018/19 2019/20 2020/21 2021/22 2022/23 2023/24 2024/25 2025/26

Midlothian ISD - Campus

Projections (Moderate

Scenario)

Projected Fall Enrollment

Frank Seale Middle Campus Capacity = 1,200

Total Enrollment 968 1,007 1,057 1,136 1,194 1,258 1,334 1,405 1,470 1,531 1,586

Capacity Utilization 81% 84% 88% 95% 99% 105% 111% 117% 122% 128% 132%

Space Remaining 232 193 143 64 6 -58 -134 -205 -270 -331 -386

Walnut Grove Middle Campus Capacity = 1,200

Total Enrollment 1,017 1,003 1,043 1,099 1,158 1,224 1,289 1,349 1,409 1,469 1,524

Capacity Utilization 85% 84% 87% 92% 96% 102% 107% 112% 117% 122% 127%

Space Remaining 183 197 157 101 42 -24 -89 -149 -209 -269 -324

Middle School Totals Total Middle School Capacity = 2,400

Total Enrollment 1,985 2,010 2,100 2,235 2,351 2,482 2,623 2,754 2,879 3,000 3,109

Capacity Utilization 83% 84% 87% 93% 98% 103% 109% 115% 120% 125% 130%

Space Remaining 415 390 300 165 49 -82 -223 -354 -479 -600 -709

Heritage High Campus Capacity = 1,000

Total Enrollment 567 801 834 880 935 999 1,059 1,115 1,164 1,209 1,246

Capacity Utilization 57% 80% 83% 88% 93% 100% 106% 112% 116% 121% 125%

Space Remaining 433 199 166 120 65 1 -59 -115 -164 -209 -246

Midlothian High Campus Capacity = 2,500

Total Enrollment 1,847 1,803 1,888 2,011 2,116 2,237 2,362 2,483 2,598 2,710 2,812

Capacity Utilization 74% 72% 76% 80% 85% 89% 94% 99% 104% 108% 112%

Space Remaining 653 697 612 489 384 263 138 17 -98 -210 -312

High School Totals Total High School Capacity = 3,500

Total Enrollment 2,414 2,604 2,721 2,890 3,051 3,236 3,421 3,598 3,762 3,919 4,059

Capacity Utilization 69% 74% 78% 83% 87% 92% 98% 103% 107% 112% 116%

Space Remaining 1,086 896 779 610 449 264 79 -98 -262 -419 -559

District Totals (PK-12) Total District Capacity = 10,800

Total Enrollment 8,147 8,472 8,869 9,448 9,959 10,537 11,134 11,700 12,235 12,750 13,213

Capacity Utilization 75% 78% 82% 87% 92% 98% 103% 108% 113% 118% 122%

Space Remaining 2,653 2,328 1,931 1,352 841 263 -334 -900 -1,435 -1,950 -2,413

43

Copyright 2016 School District Strategies.

Disclaimer - Although School District Strategies (SDS) has used commercially reasonable efforts to obtain information from sources in a manner that

SDS believes to be reliable, we do not guarantee its accuracy and such information may be incomplete, condensed or interpolated. Information

presented in this report represents our estimates as of the date of the publication and is subject to change without notice. This report is not

intended as a recommendation or endorsement for any action taken by others. In no event will School District Strategies be liable for direct,

indirect, incidental or consequential lost profits, lost savings, damages or other liabilities resulting from any information provided herein.

16980 Dallas Parkway

Suite 101

Dallas, Texas 75248

www.schooldistrictstrategies.com