middle market m&a: update and key areas of due...

TRANSCRIPT

April 26, 2016

Middle Market M&A: Update and Key Areas of

Due Diligence

1

Terry Jackson is a Vice President in the BMO Capital Markets Mergers & Acquisitions Group. Terry

has advised on numerous M&A and financing transactions across a broad range of sectors within

the business services, consumer and retail, energy, financial services, real estate, and technology

industries.

Prior to joining BMO Capital Markets, Terry was a Vice President in the Investment Banking

Division of Raymond James where he advised on M&A, public offering and private placement

transactions across several different industries. Prior to joining the Investment Banking Division of

Raymond James, Terry served in the role of Assistant to the Chairman where he executed

corporate strategy initiatives and evaluated corporate development opportunities on behalf of the

executive management team of Raymond James. Previously, he was a Senior Associate in the

Duff & Phelps’ Valuation Services practice where he was involved in numerous advisory

assignments in the e-commerce, Internet, networking, software, telecom and transaction

processing sectors. Terry began his career in the tax services practice of PricewaterhouseCoopers.

Terry received his MBA in finance with honors from the Wharton School at the University of

Pennsylvania and his Bachelor of Science in accounting and a Master of Accountancy from

Brigham Young University, where he graduated magna cum laude and with distinction, respectively.

Terry is also a CFA charterholder and a licensed CPA in California.

Speaker Biography

Terry Jackson, CFA

Vice President, Mergers & Acquisitions

BMO Capital Markets

+1-312-461-2716

2

MIDDLE MARKET M&A UPDATE

Section 1: Middle Market M&A Update

Section 1 Middle Market M&A Update

Section 2 Middle Market M&A 101

Section 3 Middle Market M&A Key Areas of Due Diligence

Appendix A - C

3 Source: FactSet

1. Includes all announced transactions.

2. Includes all announced transactions with target disclosed values between US$200MM - US$5,000MM.

MIDDLE MARKET M&A UPDATE

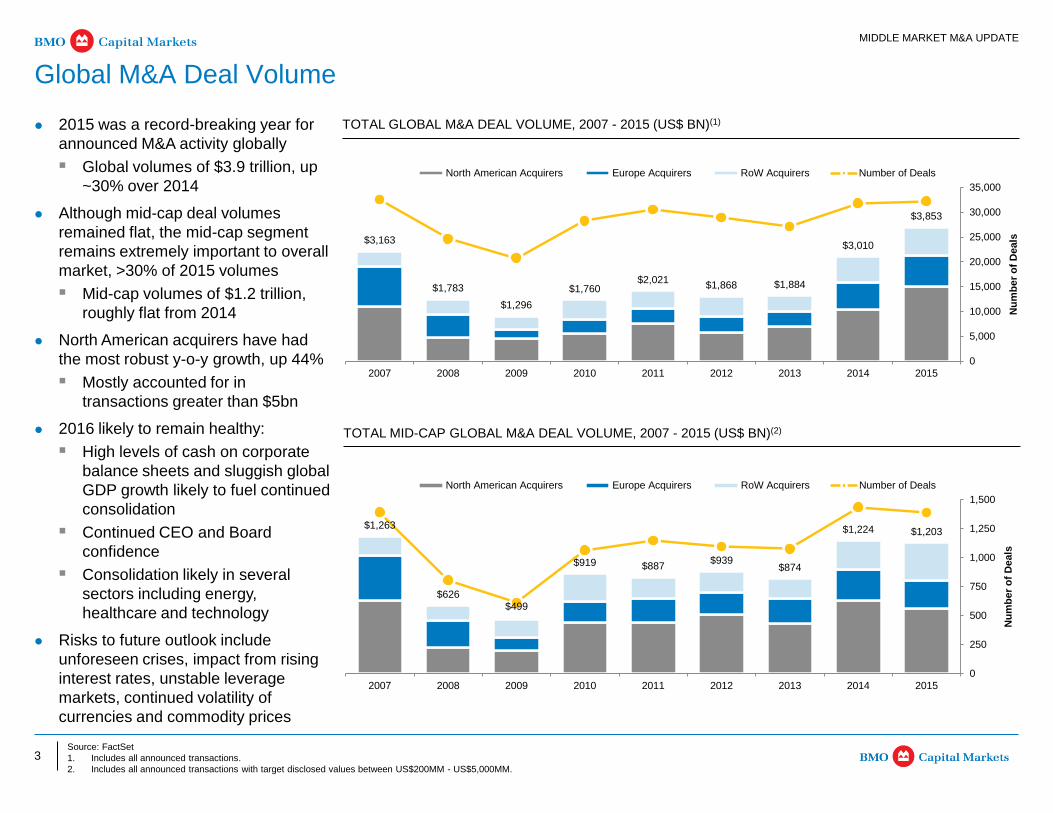

Global M&A Deal Volume

2015 was a record-breaking year for

announced M&A activity globally

Global volumes of $3.9 trillion, up

~30% over 2014

Although mid-cap deal volumes

remained flat, the mid-cap segment

remains extremely important to overall

market, >30% of 2015 volumes

Mid-cap volumes of $1.2 trillion,

roughly flat from 2014

North American acquirers have had

the most robust y-o-y growth, up 44%

Mostly accounted for in

transactions greater than $5bn

2016 likely to remain healthy:

High levels of cash on corporate

balance sheets and sluggish global

GDP growth likely to fuel continued

consolidation

Continued CEO and Board

confidence

Consolidation likely in several

sectors including energy,

healthcare and technology

Risks to future outlook include

unforeseen crises, impact from rising

interest rates, unstable leverage

markets, continued volatility of

currencies and commodity prices

TOTAL GLOBAL M&A DEAL VOLUME, 2007 - 2015 (US$ BN)(1)

TOTAL MID-CAP GLOBAL M&A DEAL VOLUME, 2007 - 2015 (US$ BN)(2)

$1,263

$626$499

$919 $887$939

$874

$1,224 $1,203

0

250

500

750

1,000

1,250

1,500

2007 2008 2009 2010 2011 2012 2013 2014 2015

Nu

mb

er

of

Deals

North American Acquirers Europe Acquirers RoW Acquirers Number of Deals

$3,163

$1,783

$1,296

$1,760$2,021

$1,868 $1,884

$3,010

$3,853

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2007 2008 2009 2010 2011 2012 2013 2014 2015

Nu

mb

er

of

Deals

North American Acquirers Europe Acquirers RoW Acquirers Number of Deals

4

19.9%

16.4%

13.1%9.6%

12.7%

11.4%

5.5%

11.4%

Business Services & Media

Industrial

Energy & Power

FIG

Food & Consumer

Healthcare

Real Estate

Tech

Source: FactSet

1. Includes all completed transactions with U.S. targets or acquirors involved and target disclosed values greater than $1 million.

2. Includes all completed transactions with a U.S. acquiror and target disclosed values between US$200MM - US$5,000MM.

MIDDLE MARKET M&A UPDATE

U.S. M&A Market Snapshot

15.9%

20.1%

12.9%9.6%

9.2%

12.3%

7.6%

12.4%

U.S. MID-CAP M&A VOLUME COMPOSITION BY SECTOR, 2014 AND 2015(2)

Broad-based deal growth across all

sectors

Relatively consistent deal volume

composition over the last few years

Top three sectors in terms of total

deal volume were Industrial,

Business Services & Media and

Energy & Power

2014 2015

TOTAL U.S. M&A DEAL VOLUME, 2007 - 2015 (US$ BN)(1)

$1,617

$1,225

$819$975$929

$778$602

$1,083

$1,694

201520142013201220112010200920082007

United States Cross-border: U.S. Acquiror Cross-border: Non-U.S. Acquiror 2015 completed deal volume

approaching near peak levels

U.S. completed deal volume of

$1.6 trillion, up 32% over 2014

Significant increase in cross-border

activity

Total cross-border volume of

$557 billion, up 152% from 2014

Highest transaction volume of

foreign acquirors for U.S.

targets, with $327 billion in

volume, up 179% from 2014

5

8.0x

10.0x

12.0x

14.0x

16.0x

18.0x

20.0x

Ja

n-0

7A

pr-

07

Ju

l-0

7O

ct-

07

De

c-0

7M

ar-

08

Ju

n-0

8S

ep-0

8D

ec-0

8M

ar-

09

Ju

n-0

9S

ep-0

9D

ec-0

9M

ar-

10

Ju

n-1

0S

ep-1

0D

ec-1

0M

ar-

11

Jun-1

1S

ep-1

1D

ec-1

1M

ar-

12

Ju

n-1

2S

ep-1

2D

ec-1

2M

ar-

13

Ju

n-1

3S

ep-1

3D

ec-1

3M

ar-

14

Ju

n-1

4S

ep-1

4D

ec-1

4M

ar-

15

Ju

n-1

5S

ep-1

5D

ec-1

5

S&P 500 LTM P/E Multiple

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Jan-0

7A

pr-

07

Ju

l-0

7O

ct-

07

De

c-0

7M

ar-

08

Ju

n-0

8S

ep-0

8D

ec-0

8M

ar-

09

Jun-0

9S

ep-0

9D

ec-0

9M

ar-

10

Ju

n-1

0S

ep-1

0D

ec-1

0M

ar-

11

Ju

n-1

1S

ep-1

1D

ec-1

1M

ar-

12

Ju

n-1

2S

ep-1

2D

ec-1

2M

ar-

13

Ju

n-1

3S

ep-1

3D

ec-1

3M

ar-

14

Jun-1

4S

ep-1

4D

ec-1

4M

ar-

15

Ju

n-1

5S

ep-1

5D

ec-1

5

US Benchmark Bond - 10 Year LIBOR - USD 3 month

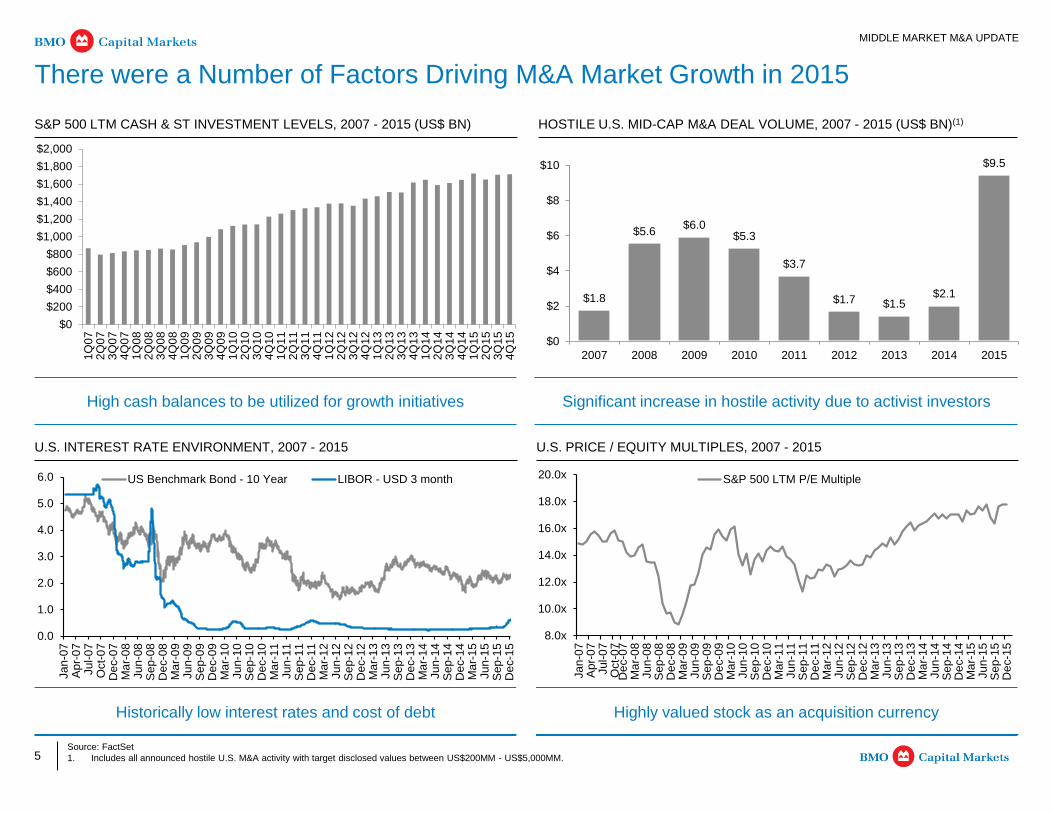

Significant increase in hostile activity due to activist investors High cash balances to be utilized for growth initiatives

U.S. INTEREST RATE ENVIRONMENT, 2007 - 2015 U.S. PRICE / EQUITY MULTIPLES, 2007 - 2015

Highly valued stock as an acquisition currency Historically low interest rates and cost of debt

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

4Q

15

3Q

15

2Q

15

1Q

15

4Q

14

3Q

14

2Q

14

1Q

14

4Q

13

3Q

13

2Q

13

1Q

13

4Q

12

3Q

12

2Q

12

1Q

12

4Q

11

3Q

11

2Q

11

1Q

11

4Q

10

3Q

10

2Q

10

1Q

10

4Q

09

3Q

09

2Q

09

1Q

09

4Q

08

3Q

08

2Q

08

1Q

08

4Q

07

3Q

07

2Q

07

1Q

07

MIDDLE MARKET M&A UPDATE

There were a Number of Factors Driving M&A Market Growth in 2015

Source: FactSet

1. Includes all announced hostile U.S. M&A activity with target disclosed values between US$200MM - US$5,000MM.

S&P 500 LTM CASH & ST INVESTMENT LEVELS, 2007 - 2015 (US$ BN) HOSTILE U.S. MID-CAP M&A DEAL VOLUME, 2007 - 2015 (US$ BN)(1)

$1.8

$5.6$6.0

$5.3

$3.7

$1.7 $1.5$2.1

$9.5

$0

$2

$4

$6

$8

$10

2007 2008 2009 2010 2011 2012 2013 2014 2015

6

6.0x

7.0x

8.0x

9.0x

10.0x

11.0x

12.0x

13.0x

14.0x

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2014 2015

Financial Buyer Strategic Buyer

$425.7

$539.4

$508.8

$501.2

$470.3

$473.9

$498.7

$530.4

$533.2

$543.4

$400.0

$450.0

$500.0

$550.0

$600.0

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

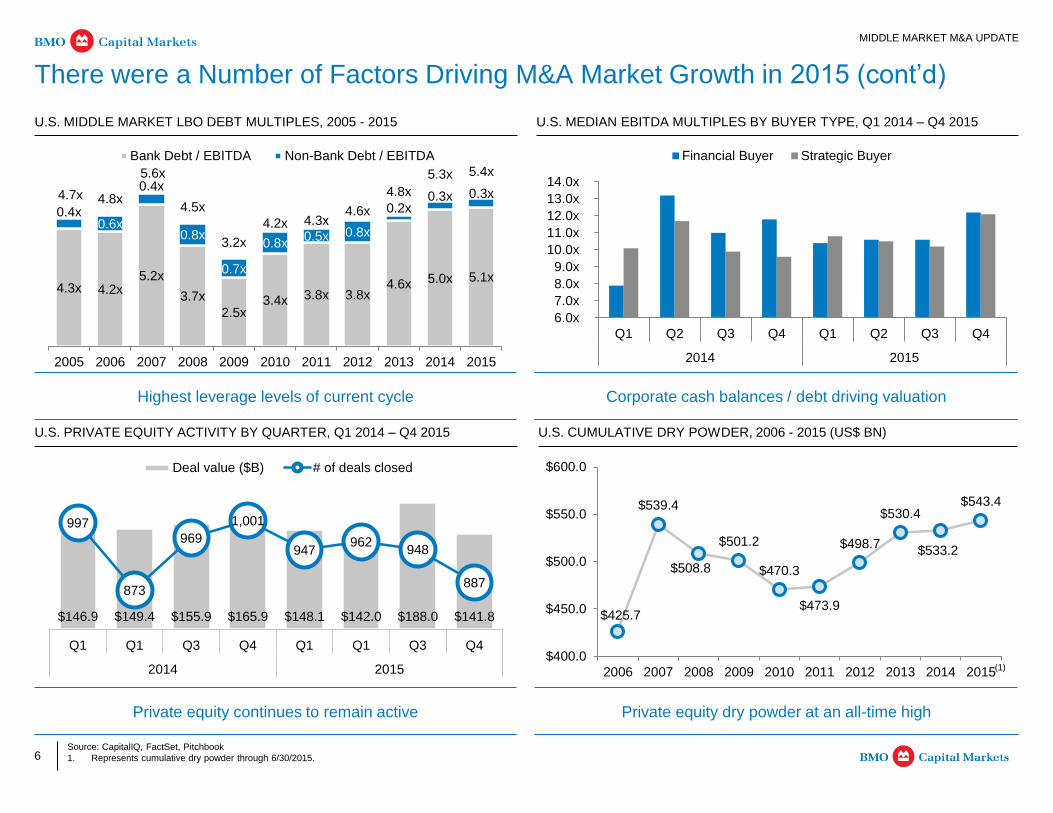

$146.9 $149.4 $155.9 $165.9 $148.1 $142.0 $188.0 $141.8

997

873

969

1,001

947962

948

887

Q1 Q1 Q3 Q4 Q1 Q1 Q3 Q4

2014 2015

Deal value ($B) # of deals closed

MIDDLE MARKET M&A UPDATE

There were a Number of Factors Driving M&A Market Growth in 2015 (cont’d)

Source: CapitalIQ, FactSet, Pitchbook

1. Represents cumulative dry powder through 6/30/2015.

U.S. PRIVATE EQUITY ACTIVITY BY QUARTER, Q1 2014 – Q4 2015 U.S. CUMULATIVE DRY POWDER, 2006 - 2015 (US$ BN)

(1)

Private equity dry powder at an all-time high Private equity continues to remain active

4.3x 4.2x5.2x

3.7x

2.5x3.4x 3.8x 3.8x

4.6x 5.0x 5.1x

0.4x0.6x

0.4x

0.8x

0.7x

0.8x0.5x 0.8x

0.2x0.3x 0.3x4.7x 4.8x

5.6x

4.5x

3.2x

4.2x 4.3x4.6x

4.8x

5.3x 5.4x

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Bank Debt / EBITDA Non-Bank Debt / EBITDA

U.S. MIDDLE MARKET LBO DEBT MULTIPLES, 2005 - 2015 U.S. MEDIAN EBITDA MULTIPLES BY BUYER TYPE, Q1 2014 – Q4 2015

Corporate cash balances / debt driving valuation Highest leverage levels of current cycle

7 Source: Capital IQ, FactSet, SDC

Note: As of April 15, 2016 unless otherwise noted.

1. Includes U.S. targets, acquirers or sellers involved in transactions with disclosed value ranges of $200 - $5,000 million.

2. Includes U.S. targets, acquirers or sellers involved in transactions with disclosed values greater than $1 million.

3. LTM majority transactions with disclosed value ranges of $200 - $5,000 million through April 8, 2016; $ in billions.

MIDDLE MARKET M&A UPDATE

M&A Middle Market Trends – Activity

13 WEEK MOMENTUM (ANNOUNCED BASIS) VS. PRIOR PERIOD(1)

YTD M&A ACTIVITY LTM ANNOUNCED ($ BASIS)(3)

Bus. Svcs. & Media

9.1%

Industrials15.1%

Real Estate14.0%FIG

9.8%

Food & Consumer

10.8%

Energy & Power11.9%

Healthcare10.6%

Tech18.8%

$67.8

$89.5

$57.99

$96.5

$62.7

$69.0

$75.9

$120.5

Total M&A activity has decreased year-

over-year, both in terms of volume and

number of deals

Deals have decreased far less in

terms of size than number, implying

larger transaction sizes

Sponsor and overall activity have

decreased similarly

Middle market M&A activity has also

decreased year-over-year both in terms

of volume and number of deals

$14.5

$17.9 $17.2

$11.0 $9.2

$5.3 $3.4

$6.6

$21.9

$18.8 $19.0

$12.6 $13.7

$4.4

$10.5

$6.4 $5.4 $7.8

$11.1

$8.0

$36.2

$9.0 $7.4

$10.7

$13.8

$9.7

-$3.0

$2.0

$7.0

$12.0

$17.0

$22.0

$27.0

$32.0

$37.0

LY1/30 LY 2/6 LY2/13 LY2/20 LY2/27 LY 3/5 LY3/12 LY3/19 LY3/26 LY 4/2 LY 4/9 LY4/16 LY4/22

Ag

gre

gate

Valu

e (

$ i

n b

illi

on

s)

CY Non Sponsors CY Sponsors LY Non Sponsors LY Sponsors

19 16 No. of Deals: 15 7 9 23 17 10 10 12 12 15 11 14 18 12 22 14 10 16 15 22 8 13 20 19

Mid-Cap M&A Activity (1)

# $

YTD Stats All Sponsor All Sponsor

2016 208 95 $159.9 $71.2

2015 238 105 $203.9 $78.6

% Δ (13%) (10%) (22%) (9%)

All M&A Activity (2)

# $

YTD Stats All Sponsor All Sponsor

2016 649 190 $329.2 $97.8

2015 1,048 311 $525.4 $197.1

% Δ (38%) (39%) (37%) (50%)

8

MIDDLE MARKET M&A UPDATE

Middle Market M&A Trends – Relevant Topics

Once an esoteric insurance product, now a commonplace feature in M&A deals

Enhanced post-closing deal protection for buyers and clean exits for sellers

Distinguishes bids in an auction by requiring minimal or no survival of R&W in purchase agreement

General market observations:

$30mm coverage costs 3.5-4.0% ($1.0-1.2mm) with policy deductible of 1.5% of purchase price for zero recourse

to seller (some seller recourse may be 5-10% cheaper)

– Costs are typically split 50/50 between buyer and seller

Policies are typically for three years for general R&W and up to six years for fundamental reps, including tax

AIG, Ambridge Partners, and Concorde Specialty Risk are more comfortable with zero recourse deals

Ace, Allied, and Hartford less inclined on no indemnity deals or may require 2.0% policy deductible

Generally, insurance companies won’t begin their underwriting work until buyer is exclusive and will want to

review SPA, schedules

Policy negotiation and underwriting generally takes seven to ten business days

Carve-out policies are also becoming commonplace (i.e. environmental)

Reps & Warranties (R&W)

Insurance

Marginal benefit to sanctioning a QoE report by seller unless add-backs represent a substantial portion of adjusted

EBITDA and will distract buyers

Desired goal can be accomplished with staple financing indication

In almost all situations, buyers will want to complete their own QoE report

Third party consulting reports supporting growth strategy offers best return on investment

Seller has ability to influence and drive conclusions; conflicts consulting firm with working with potential buyers

Potential to hire consulting firm following management presentations where all buyers sign-off on scope of

engagement and receive report; winning party ultimately pays for report

Seller Diligence Reports / Quality of

Earnings (QoE)

9

MIDDLE MARKET M&A 101

Section 2: Middle Market M&A 101

Section 1 Middle Market M&A Update

Section 2 Middle Market M&A 101

Section 3 Middle Market M&A Key Areas of Due Diligence

Appendix A - C

10

“Buyside” Motivation “Sellside” Motivation

Strategic fit / synergies

Portfolio / geographic diversification

Consolidator in a fragmented marketplace

Market leader / platform opportunity

Defensive focus: “eat or be eaten”

Opportunistic valuation

Acquisition of technology

Private equity investment horizon

Seeking new strategic direction / growth capital

Succession issues

Opportunistic valuation

Shareholder dissent

Operational underperformance

1+1 > 2

MIDDLE MARKET M&A 101

What Motivates Companies to Transact?

M&A situations may be driven by a variety of circumstances

11

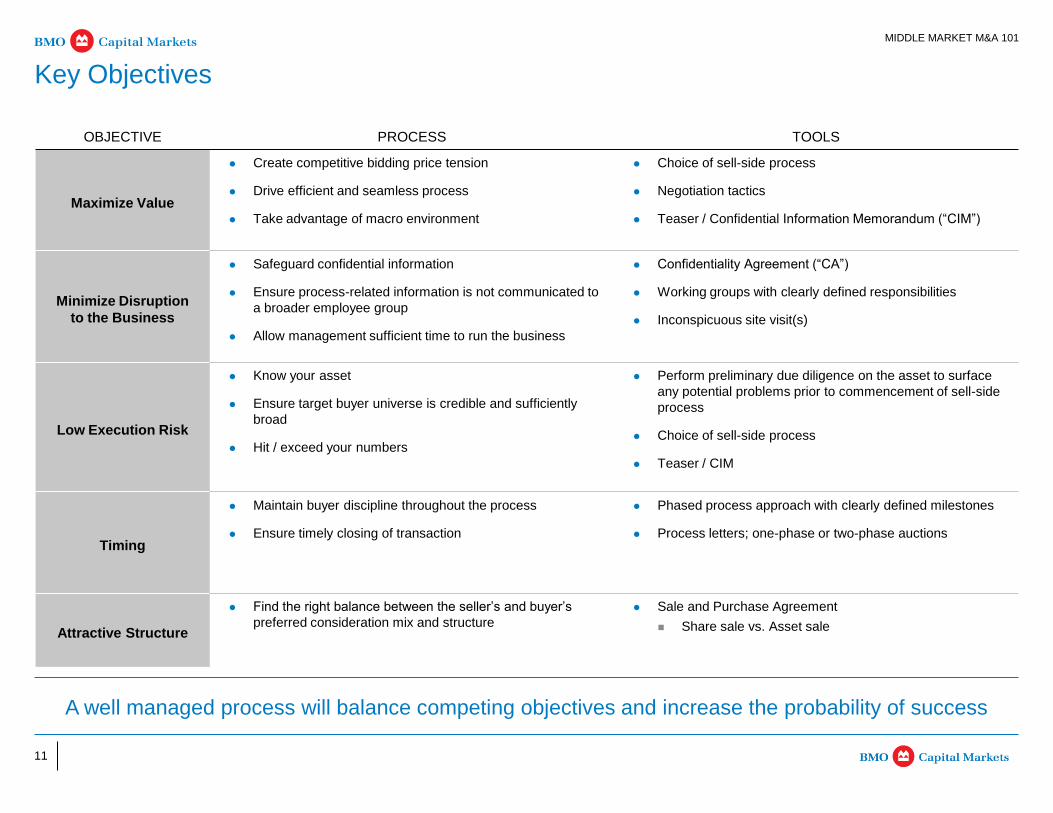

MIDDLE MARKET M&A 101

Key Objectives

A well managed process will balance competing objectives and increase the probability of success

OBJECTIVE PROCESS TOOLS

Maximize Value

Create competitive bidding price tension

Drive efficient and seamless process

Take advantage of macro environment

Choice of sell-side process

Negotiation tactics

Teaser / Confidential Information Memorandum (“CIM”)

Minimize Disruption

to the Business

Safeguard confidential information

Ensure process-related information is not communicated to

a broader employee group

Allow management sufficient time to run the business

Confidentiality Agreement (“CA”)

Working groups with clearly defined responsibilities

Inconspicuous site visit(s)

Low Execution Risk

Know your asset

Ensure target buyer universe is credible and sufficiently

broad

Hit / exceed your numbers

Perform preliminary due diligence on the asset to surface

any potential problems prior to commencement of sell-side

process

Choice of sell-side process

Teaser / CIM

Timing

Maintain buyer discipline throughout the process

Ensure timely closing of transaction

Phased process approach with clearly defined milestones

Process letters; one-phase or two-phase auctions

Attractive Structure

Find the right balance between the seller’s and buyer’s

preferred consideration mix and structure

Sale and Purchase Agreement

Share sale vs. Asset sale

12

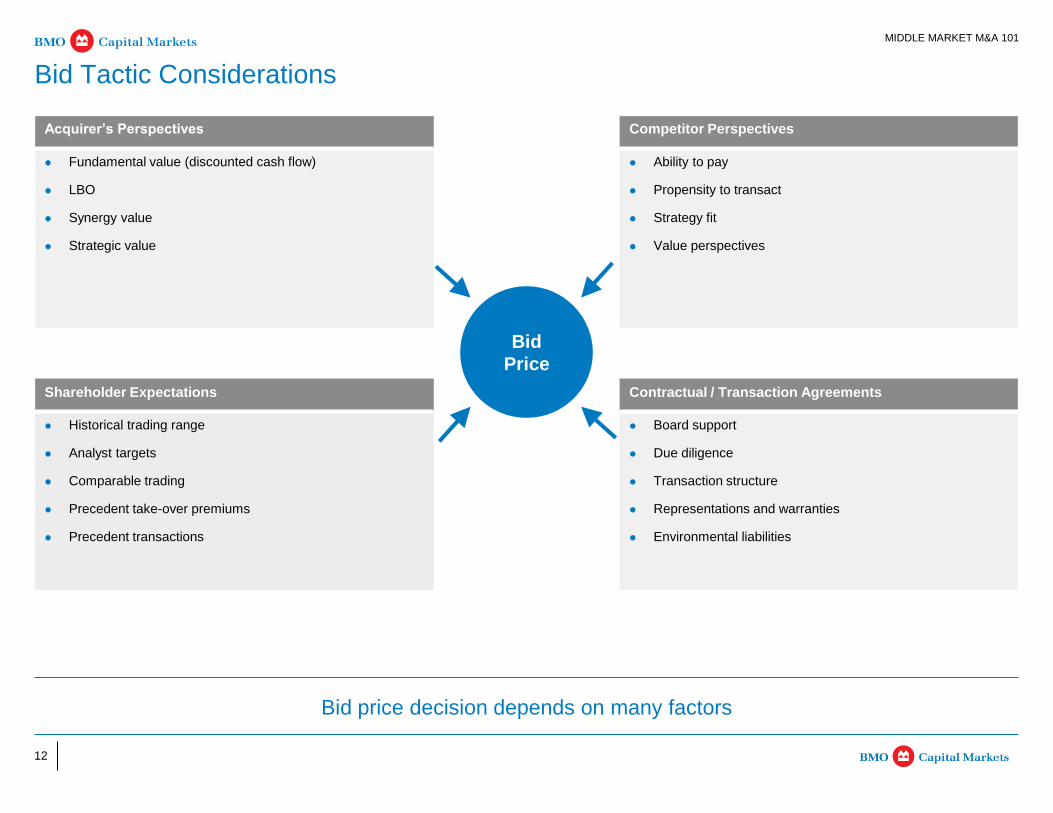

MIDDLE MARKET M&A 101

Bid Tactic Considerations

Bid price decision depends on many factors

Bid

Price

Acquirer’s Perspectives Competitor Perspectives

Fundamental value (discounted cash flow)

LBO

Synergy value

Strategic value

Ability to pay

Propensity to transact

Strategy fit

Value perspectives

Shareholder Expectations Contractual / Transaction Agreements

Historical trading range

Analyst targets

Comparable trading

Precedent take-over premiums

Precedent transactions

Board support

Due diligence

Transaction structure

Representations and warranties

Environmental liabilities

13

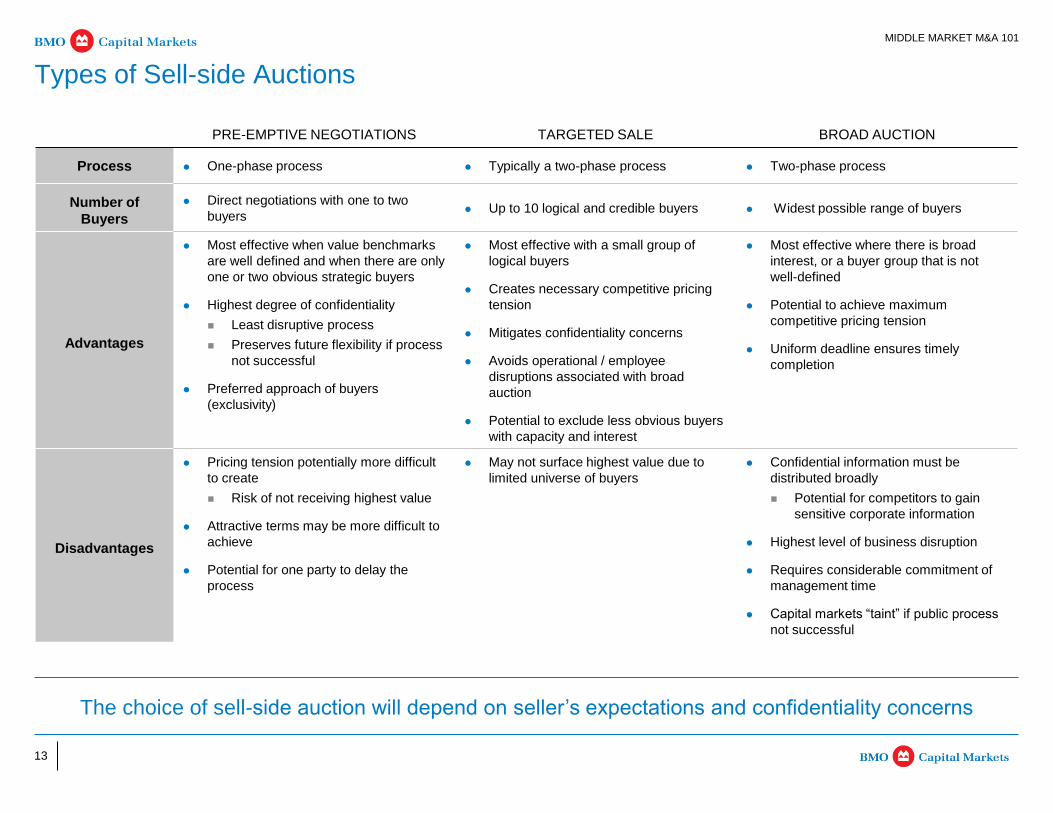

MIDDLE MARKET M&A 101

Types of Sell-side Auctions

The choice of sell-side auction will depend on seller’s expectations and confidentiality concerns

PRE-EMPTIVE NEGOTIATIONS TARGETED SALE BROAD AUCTION

Process One-phase process Typically a two-phase process Two-phase process

Number of

Buyers

Direct negotiations with one to two

buyers Up to 10 logical and credible buyers Widest possible range of buyers

Advantages

Most effective when value benchmarks

are well defined and when there are only

one or two obvious strategic buyers

Highest degree of confidentiality

Least disruptive process

Preserves future flexibility if process

not successful

Preferred approach of buyers

(exclusivity)

Most effective with a small group of

logical buyers

Creates necessary competitive pricing

tension

Mitigates confidentiality concerns

Avoids operational / employee

disruptions associated with broad

auction

Potential to exclude less obvious buyers

with capacity and interest

Most effective where there is broad

interest, or a buyer group that is not

well-defined

Potential to achieve maximum

competitive pricing tension

Uniform deadline ensures timely

completion

Disadvantages

Pricing tension potentially more difficult

to create

Risk of not receiving highest value

Attractive terms may be more difficult to

achieve

Potential for one party to delay the

process

May not surface highest value due to

limited universe of buyers

Confidential information must be

distributed broadly

Potential for competitors to gain

sensitive corporate information

Highest level of business disruption

Requires considerable commitment of

management time

Capital markets “taint” if public process

not successful

14

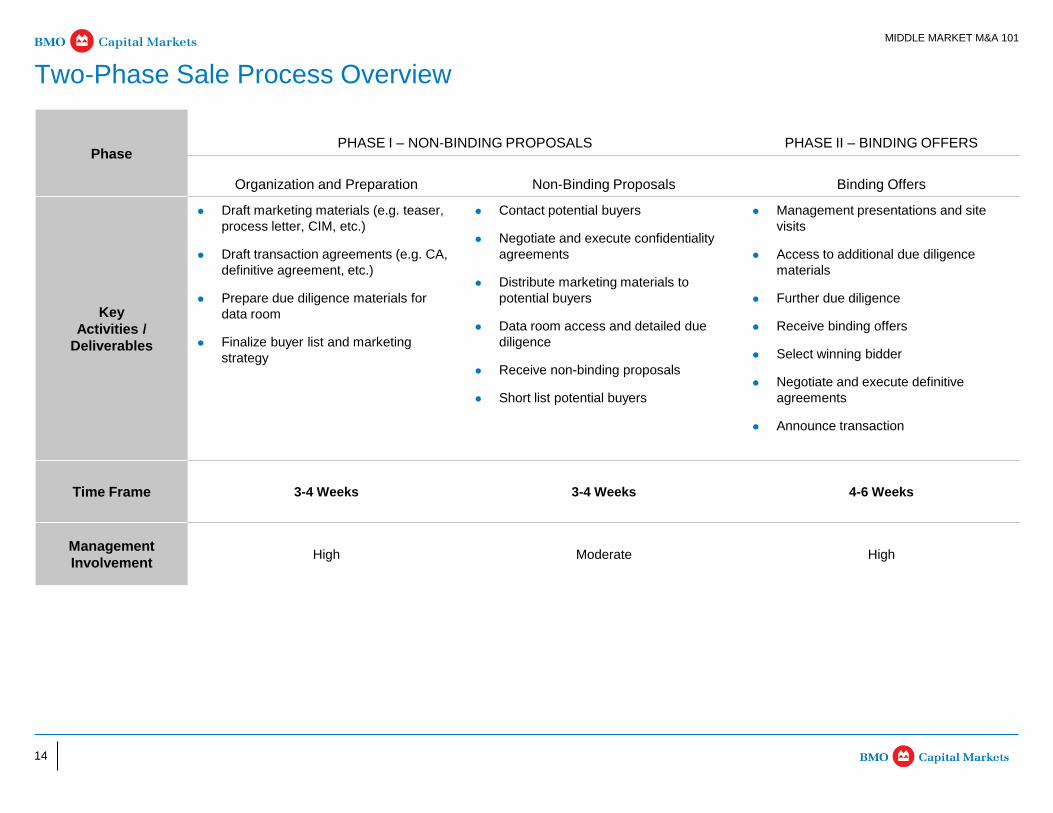

MIDDLE MARKET M&A 101

Two-Phase Sale Process Overview

Phase PHASE I – NON-BINDING PROPOSALS PHASE II – BINDING OFFERS

Organization and Preparation Non-Binding Proposals Binding Offers

Key

Activities /

Deliverables

Draft marketing materials (e.g. teaser,

process letter, CIM, etc.)

Draft transaction agreements (e.g. CA,

definitive agreement, etc.)

Prepare due diligence materials for

data room

Finalize buyer list and marketing

strategy

Contact potential buyers

Negotiate and execute confidentiality

agreements

Distribute marketing materials to

potential buyers

Data room access and detailed due

diligence

Receive non-binding proposals

Short list potential buyers

Management presentations and site

visits

Access to additional due diligence

materials

Further due diligence

Receive binding offers

Select winning bidder

Negotiate and execute definitive

agreements

Announce transaction

Time Frame 3-4 Weeks 3-4 Weeks 4-6 Weeks

Management

Involvement High Moderate High

15

MIDDLE MARKET M&A 101

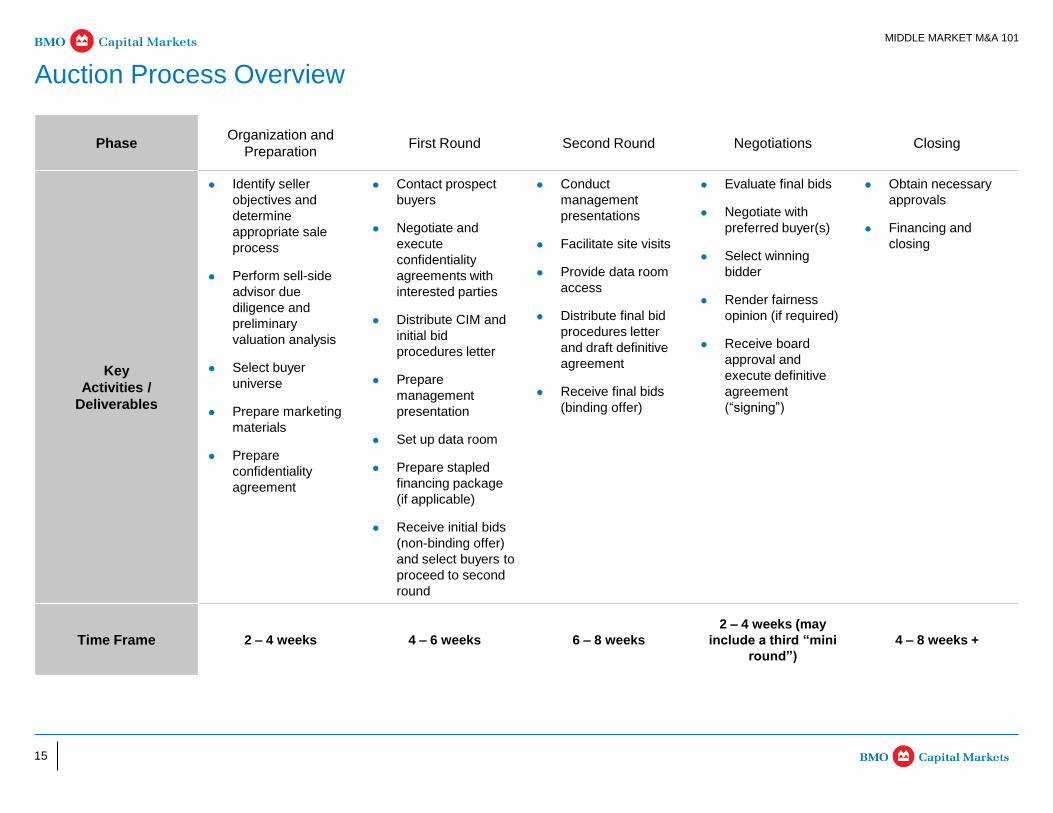

Auction Process Overview

Phase Organization and

Preparation First Round Second Round Negotiations Closing

Key

Activities /

Deliverables

Identify seller

objectives and

determine

appropriate sale

process

Perform sell-side

advisor due

diligence and

preliminary

valuation analysis

Select buyer

universe

Prepare marketing

materials

Prepare

confidentiality

agreement

Contact prospect

buyers

Negotiate and

execute

confidentiality

agreements with

interested parties

Distribute CIM and

initial bid

procedures letter

Prepare

management

presentation

Set up data room

Prepare stapled

financing package

(if applicable)

Receive initial bids

(non-binding offer)

and select buyers to

proceed to second

round

Conduct

management

presentations

Facilitate site visits

Provide data room

access

Distribute final bid

procedures letter

and draft definitive

agreement

Receive final bids

(binding offer)

Evaluate final bids

Negotiate with

preferred buyer(s)

Select winning

bidder

Render fairness

opinion (if required)

Receive board

approval and

execute definitive

agreement

(“signing”)

Obtain necessary

approvals

Financing and

closing

Time Frame 2 – 4 weeks 4 – 6 weeks 6 – 8 weeks

2 – 4 weeks (may

include a third “mini

round”)

4 – 8 weeks +

16

MIDDLE MARKET M&A 101

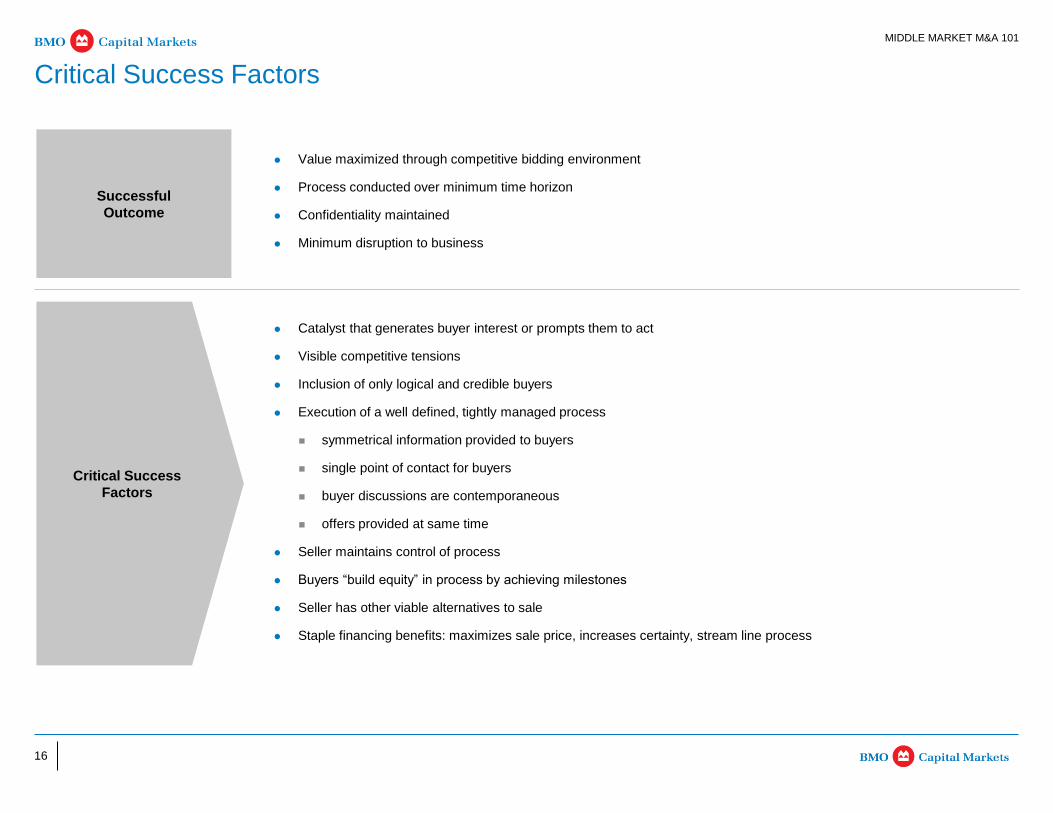

Critical Success Factors

Value maximized through competitive bidding environment

Process conducted over minimum time horizon

Confidentiality maintained

Minimum disruption to business

Successful

Outcome

Critical Success

Factors

Catalyst that generates buyer interest or prompts them to act

Visible competitive tensions

Inclusion of only logical and credible buyers

Execution of a well defined, tightly managed process

symmetrical information provided to buyers

single point of contact for buyers

buyer discussions are contemporaneous

offers provided at same time

Seller maintains control of process

Buyers “build equity” in process by achieving milestones

Seller has other viable alternatives to sale

Staple financing benefits: maximizes sale price, increases certainty, stream line process

17

MIDDLE MARKET M&A KEY AREAS OF DUE DILIGENCE

Section 3: Middle Market M&A Key Areas of Due Diligence

Section 1 Middle Market M&A Update

Section 2 Middle Market M&A 101

Section 3 Middle Market M&A Key Areas of Due Diligence

Appendix A - C

18

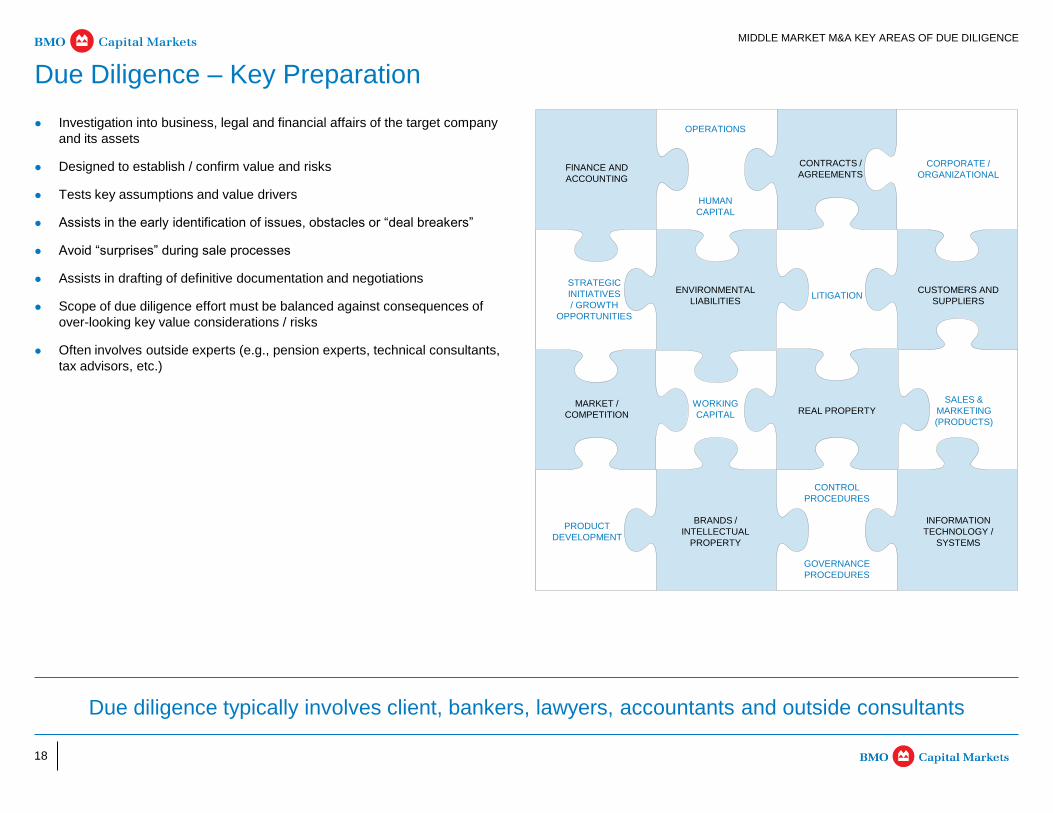

Investigation into business, legal and financial affairs of the target company

and its assets

Designed to establish / confirm value and risks

Tests key assumptions and value drivers

Assists in the early identification of issues, obstacles or “deal breakers”

Avoid “surprises” during sale processes

Assists in drafting of definitive documentation and negotiations

Scope of due diligence effort must be balanced against consequences of

over-looking key value considerations / risks

Often involves outside experts (e.g., pension experts, technical consultants,

tax advisors, etc.)

MIDDLE MARKET M&A KEY AREAS OF DUE DILIGENCE

Due Diligence – Key Preparation

Due diligence typically involves client, bankers, lawyers, accountants and outside consultants

FINANCE AND

ACCOUNTING

OPERATIONS

CONTRACTS /

AGREEMENTS

SALES &

MARKETING

(PRODUCTS)

STRATEGIC

INITIATIVES

/ GROWTH

OPPORTUNITIES

ENVIRONMENTAL

LIABILITIES LITIGATION

CUSTOMERS AND

SUPPLIERS

MARKET /

COMPETITION

WORKING

CAPITAL REAL PROPERTY

CORPORATE /

ORGANIZATIONAL

PRODUCT

DEVELOPMENT

BRANDS /

INTELLECTUAL

PROPERTY

CONTROL

PROCEDURES

INFORMATION

TECHNOLOGY /

SYSTEMS

HUMAN

CAPITAL

GOVERNANCE

PROCEDURES

19

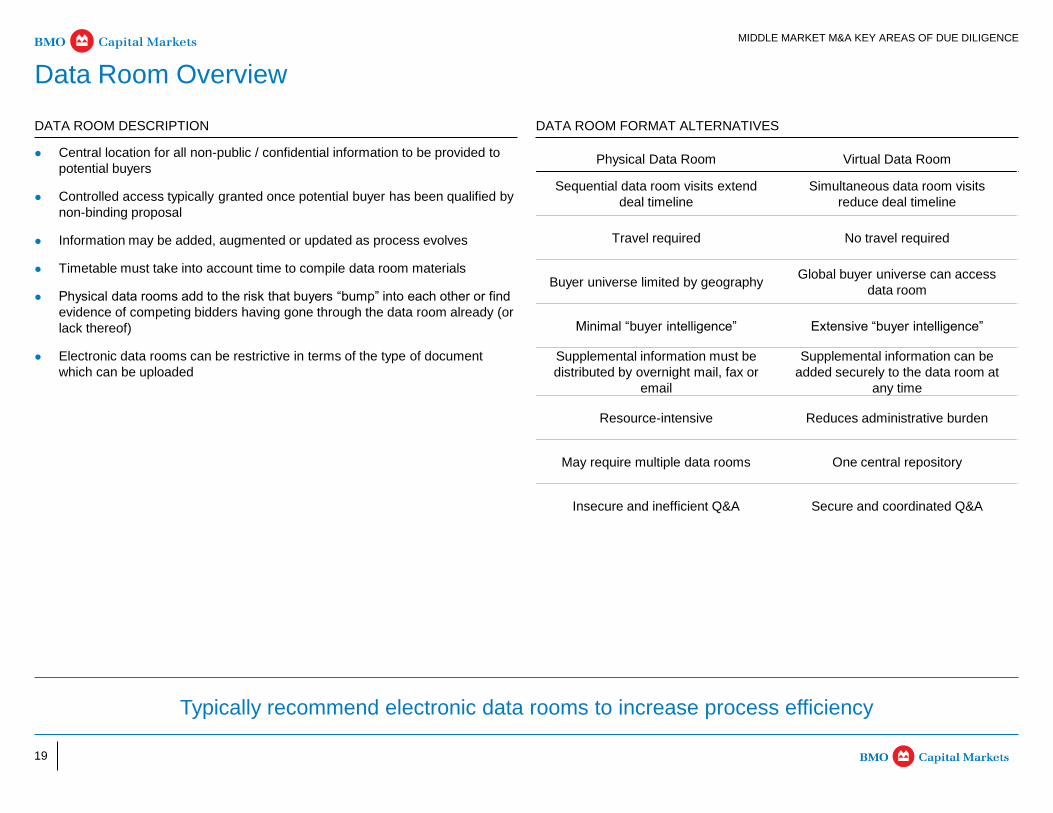

Central location for all non-public / confidential information to be provided to

potential buyers

Controlled access typically granted once potential buyer has been qualified by

non-binding proposal

Information may be added, augmented or updated as process evolves

Timetable must take into account time to compile data room materials

Physical data rooms add to the risk that buyers “bump” into each other or find

evidence of competing bidders having gone through the data room already (or

lack thereof)

Electronic data rooms can be restrictive in terms of the type of document

which can be uploaded

MIDDLE MARKET M&A KEY AREAS OF DUE DILIGENCE

Data Room Overview

Typically recommend electronic data rooms to increase process efficiency

DATA ROOM DESCRIPTION

Physical Data Room Virtual Data Room

Sequential data room visits extend

deal timeline

Simultaneous data room visits

reduce deal timeline

Travel required No travel required

Buyer universe limited by geography Global buyer universe can access

data room

Minimal “buyer intelligence” Extensive “buyer intelligence”

Supplemental information must be

distributed by overnight mail, fax or

Supplemental information can be

added securely to the data room at

any time

Resource-intensive Reduces administrative burden

May require multiple data rooms One central repository

Insecure and inefficient Q&A Secure and coordinated Q&A

DATA ROOM FORMAT ALTERNATIVES

20

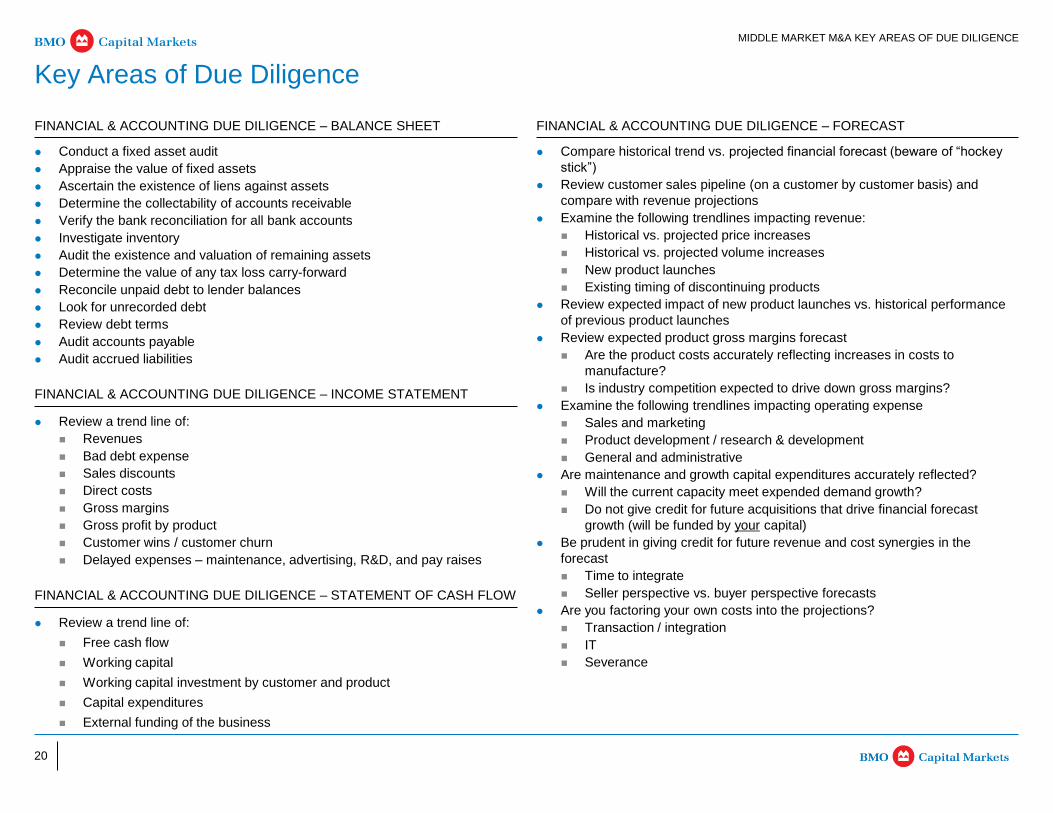

Compare historical trend vs. projected financial forecast (beware of “hockey

stick”)

Review customer sales pipeline (on a customer by customer basis) and

compare with revenue projections

Examine the following trendlines impacting revenue:

Historical vs. projected price increases

Historical vs. projected volume increases

New product launches

Existing timing of discontinuing products

Review expected impact of new product launches vs. historical performance

of previous product launches

Review expected product gross margins forecast

Are the product costs accurately reflecting increases in costs to

manufacture?

Is industry competition expected to drive down gross margins?

Examine the following trendlines impacting operating expense

Sales and marketing

Product development / research & development

General and administrative

Are maintenance and growth capital expenditures accurately reflected?

Will the current capacity meet expended demand growth?

Do not give credit for future acquisitions that drive financial forecast

growth (will be funded by your capital)

Be prudent in giving credit for future revenue and cost synergies in the

forecast

Time to integrate

Seller perspective vs. buyer perspective forecasts

Are you factoring your own costs into the projections?

Transaction / integration

IT

Severance

FINANCIAL & ACCOUNTING DUE DILIGENCE – BALANCE SHEET FINANCIAL & ACCOUNTING DUE DILIGENCE – FORECAST

MIDDLE MARKET M&A KEY AREAS OF DUE DILIGENCE

Key Areas of Due Diligence

Conduct a fixed asset audit

Appraise the value of fixed assets

Ascertain the existence of liens against assets

Determine the collectability of accounts receivable

Verify the bank reconciliation for all bank accounts

Investigate inventory

Audit the existence and valuation of remaining assets

Determine the value of any tax loss carry-forward

Reconcile unpaid debt to lender balances

Look for unrecorded debt

Review debt terms

Audit accounts payable

Audit accrued liabilities

FINANCIAL & ACCOUNTING DUE DILIGENCE – INCOME STATEMENT

Review a trend line of:

Revenues

Bad debt expense

Sales discounts

Direct costs

Gross margins

Gross profit by product

Customer wins / customer churn

Delayed expenses – maintenance, advertising, R&D, and pay raises

FINANCIAL & ACCOUNTING DUE DILIGENCE – STATEMENT OF CASH FLOW

Review a trend line of:

Free cash flow

Working capital

Working capital investment by customer and product

Capital expenditures

External funding of the business

21

MIDDLE MARKET M&A KEY AREAS OF DUE DILIGENCE

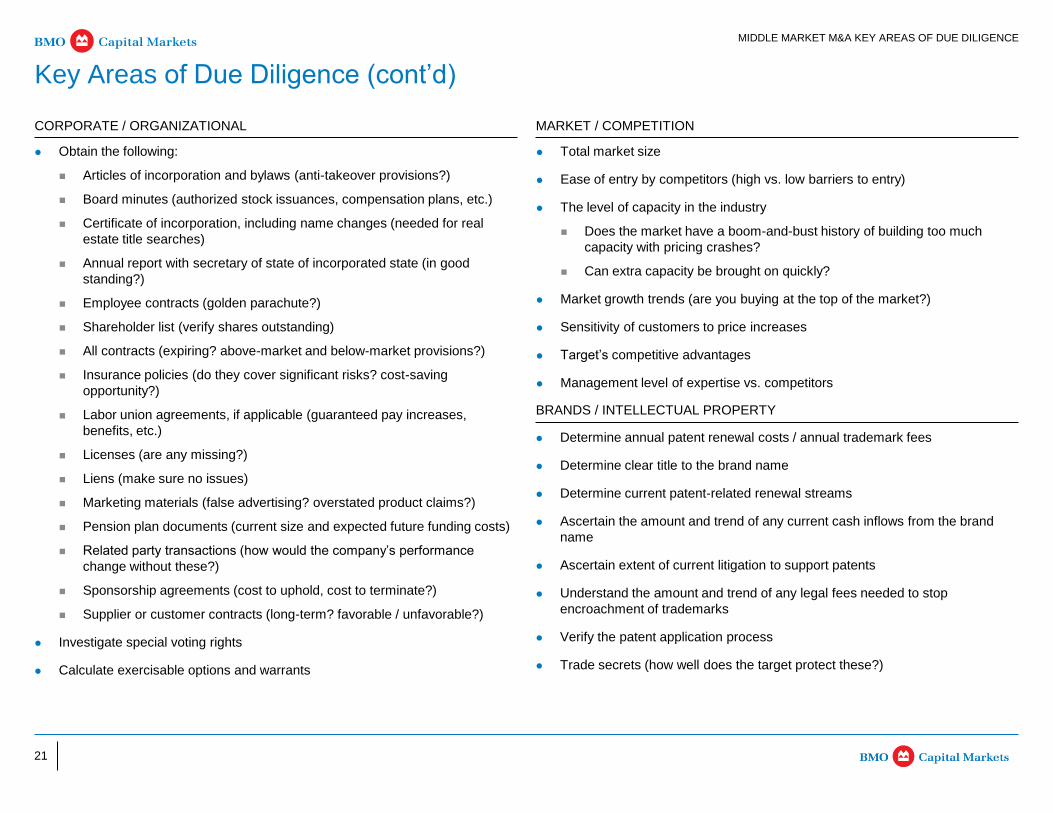

Obtain the following:

Articles of incorporation and bylaws (anti-takeover provisions?)

Board minutes (authorized stock issuances, compensation plans, etc.)

Certificate of incorporation, including name changes (needed for real

estate title searches)

Annual report with secretary of state of incorporated state (in good

standing?)

Employee contracts (golden parachute?)

Shareholder list (verify shares outstanding)

All contracts (expiring? above-market and below-market provisions?)

Insurance policies (do they cover significant risks? cost-saving

opportunity?)

Labor union agreements, if applicable (guaranteed pay increases,

benefits, etc.)

Licenses (are any missing?)

Liens (make sure no issues)

Marketing materials (false advertising? overstated product claims?)

Pension plan documents (current size and expected future funding costs)

Related party transactions (how would the company’s performance

change without these?)

Sponsorship agreements (cost to uphold, cost to terminate?)

Supplier or customer contracts (long-term? favorable / unfavorable?)

Investigate special voting rights

Calculate exercisable options and warrants

Key Areas of Due Diligence (cont’d)

CORPORATE / ORGANIZATIONAL MARKET / COMPETITION

Total market size

Ease of entry by competitors (high vs. low barriers to entry)

The level of capacity in the industry

Does the market have a boom-and-bust history of building too much

capacity with pricing crashes?

Can extra capacity be brought on quickly?

Market growth trends (are you buying at the top of the market?)

Sensitivity of customers to price increases

Target’s competitive advantages

Management level of expertise vs. competitors

BRANDS / INTELLECTUAL PROPERTY

Determine annual patent renewal costs / annual trademark fees

Determine clear title to the brand name

Determine current patent-related renewal streams

Ascertain the amount and trend of any current cash inflows from the brand

name

Ascertain extent of current litigation to support patents

Understand the amount and trend of any legal fees needed to stop

encroachment of trademarks

Verify the patent application process

Trade secrets (how well does the target protect these?)

22

MIDDLE MARKET M&A KEY AREAS OF DUE DILIGENCE

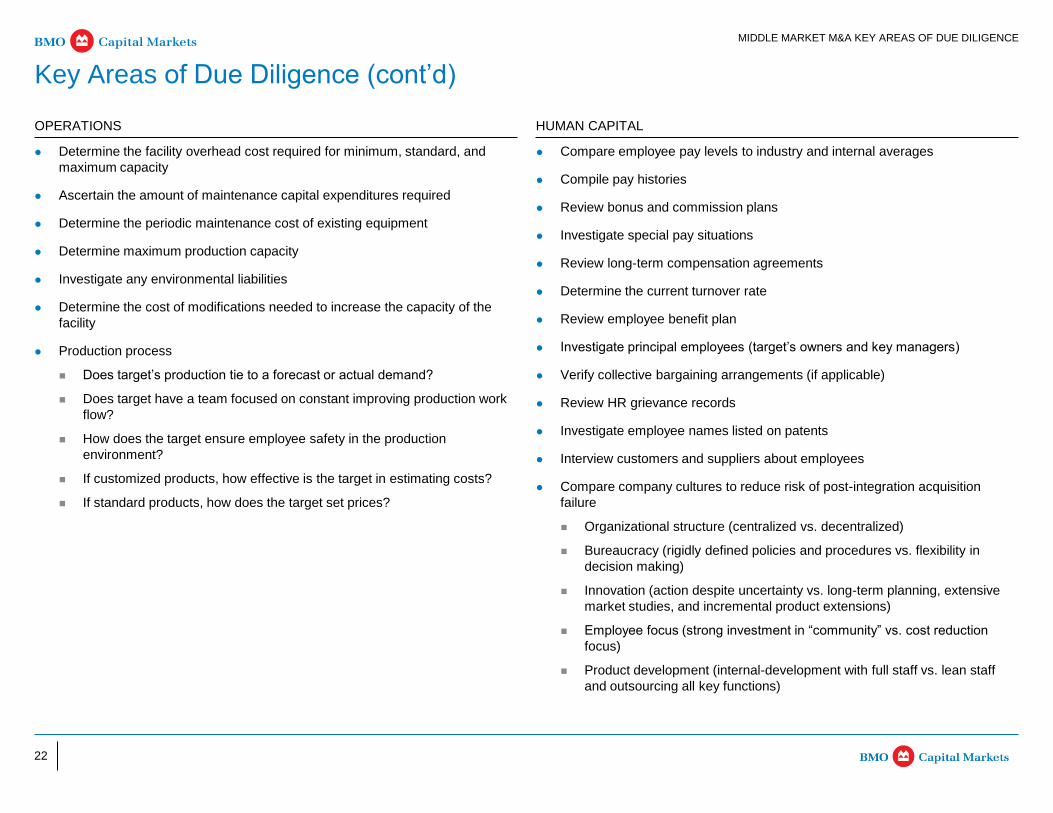

Determine the facility overhead cost required for minimum, standard, and

maximum capacity

Ascertain the amount of maintenance capital expenditures required

Determine the periodic maintenance cost of existing equipment

Determine maximum production capacity

Investigate any environmental liabilities

Determine the cost of modifications needed to increase the capacity of the

facility

Production process

Does target’s production tie to a forecast or actual demand?

Does target have a team focused on constant improving production work

flow?

How does the target ensure employee safety in the production

environment?

If customized products, how effective is the target in estimating costs?

If standard products, how does the target set prices?

Key Areas of Due Diligence (cont’d)

OPERATIONS HUMAN CAPITAL

Compare employee pay levels to industry and internal averages

Compile pay histories

Review bonus and commission plans

Investigate special pay situations

Review long-term compensation agreements

Determine the current turnover rate

Review employee benefit plan

Investigate principal employees (target’s owners and key managers)

Verify collective bargaining arrangements (if applicable)

Review HR grievance records

Investigate employee names listed on patents

Interview customers and suppliers about employees

Compare company cultures to reduce risk of post-integration acquisition

failure

Organizational structure (centralized vs. decentralized)

Bureaucracy (rigidly defined policies and procedures vs. flexibility in

decision making)

Innovation (action despite uncertainty vs. long-term planning, extensive

market studies, and incremental product extensions)

Employee focus (strong investment in “community” vs. cost reduction

focus)

Product development (internal-development with full staff vs. lean staff

and outsourcing all key functions)

23

MIDDLE MARKET M&A KEY AREAS OF DUE DILIGENCE

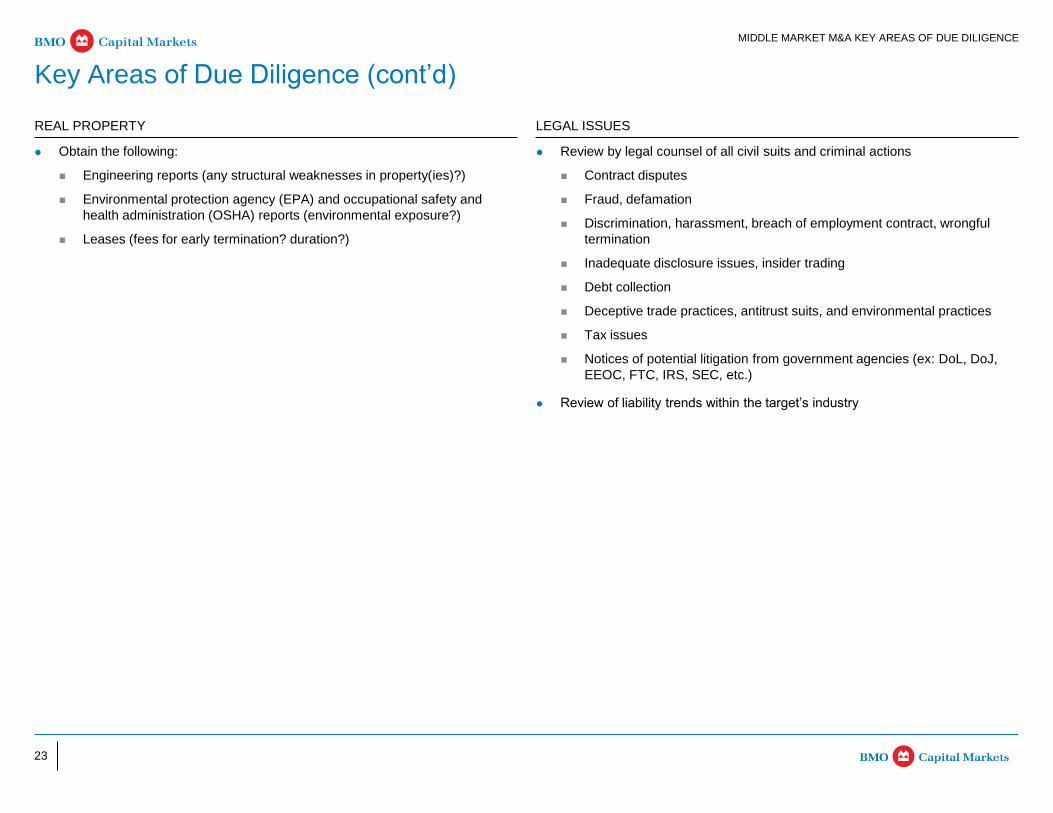

Obtain the following:

Engineering reports (any structural weaknesses in property(ies)?)

Environmental protection agency (EPA) and occupational safety and

health administration (OSHA) reports (environmental exposure?)

Leases (fees for early termination? duration?)

Key Areas of Due Diligence (cont’d)

REAL PROPERTY LEGAL ISSUES

Review by legal counsel of all civil suits and criminal actions

Contract disputes

Fraud, defamation

Discrimination, harassment, breach of employment contract, wrongful

termination

Inadequate disclosure issues, insider trading

Debt collection

Deceptive trade practices, antitrust suits, and environmental practices

Tax issues

Notices of potential litigation from government agencies (ex: DoL, DoJ,

EEOC, FTC, IRS, SEC, etc.)

Review of liability trends within the target’s industry

24

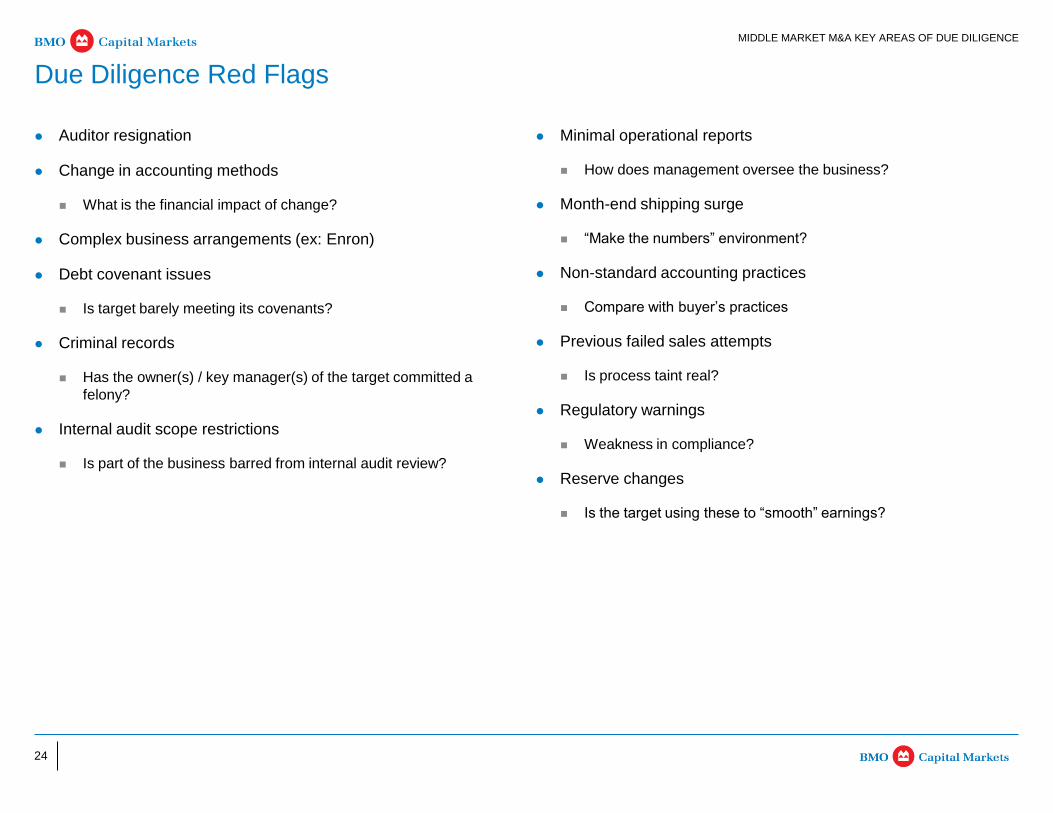

Auditor resignation

Change in accounting methods

What is the financial impact of change?

Complex business arrangements (ex: Enron)

Debt covenant issues

Is target barely meeting its covenants?

Criminal records

Has the owner(s) / key manager(s) of the target committed a

felony?

Internal audit scope restrictions

Is part of the business barred from internal audit review?

Minimal operational reports

How does management oversee the business?

Month-end shipping surge

“Make the numbers” environment?

Non-standard accounting practices

Compare with buyer’s practices

Previous failed sales attempts

Is process taint real?

Regulatory warnings

Weakness in compliance?

Reserve changes

Is the target using these to “smooth” earnings?

MIDDLE MARKET M&A KEY AREAS OF DUE DILIGENCE

Due Diligence Red Flags

25

APPENDIX A: KEY M&A MATERIALS

Appendix A: Key M&A Materials

Section 1 Middle Market M&A Update

Section 2 Middle Market M&A 101

Section 3 Middle Market M&A Key Areas of Due Diligence

Appendix A - C

26

Governs use of and protects target’s confidential information

Key provisions include:

Scope (definition of confidential information)

Permitted use

Permitted disclosure

Non-disclosure of negotiations

Return or destruction of information

Standstill (public companies)

Non-solicit of employees

Limitations on contact

Term of agreement

Outlines process and timetable for potential buyers

Often use two separate process letters (one for non-binding proposal

phase and one for binding offer phase)

Highlights target’s objectives with respect to transaction

Outlines required / requested content for non-binding proposals or binding

offers, as the case may be

Provides potential buyers with a single point of contact for all questions /

queries

Governs behavior (morally not legally) of the parties during the process

No unauthorized contact

Targets maintains right to alter or terminate process as it deems

appropriate

Target makes no representations or warranties

APPENDIX A: KEY M&A MATERIALS

Go-to-Market Materials – CA / Process Letter

CA and process letter are used to control the process and the activities of buyers

CONFIDENTIALITY AGREEMENT PROCESS LETTER

27

1. Executive Summary

2. Investment Considerations

3. Industry Overview

Segment Overview

Market Share and Position

Competition

4. Company Overview

History

Strategy

Products and Services

Customers and Suppliers

Management and Employees

5. Operations Overview

Manufacturing

Distribution

Sales and Marketing

Information Systems

Legal and Environmental

6. Financial Information

Historical Financial Results and MD&A

Projected Financial Results and MD&A

Appendix

Audited Financial Statements

Recent Press Releases

Product Brochures

CIM is drafted, in large part, by investment bankers with input from

management based on:

Public filings, company brochures, confidential information (limited), etc.

Written in “third person, plain text” style

Word document

Concepts should be crisp, concise and sales oriented – opportunity to

highlight “upside”

Management presentation condenses key messages of CIM into 1-hour

“highlight reel”

Presentation rehearsals to refine management presentation delivery critical

Presenters often need coaching

APPENDIX A: KEY M&A MATERIALS

Go-to-Market Materials – CIM / Management Presentation

CIM and management presentation are key ‘sales documents’

ILLUSTRATIVE TABLE OF CONTENTS PROCESS DESCRIPTION

28

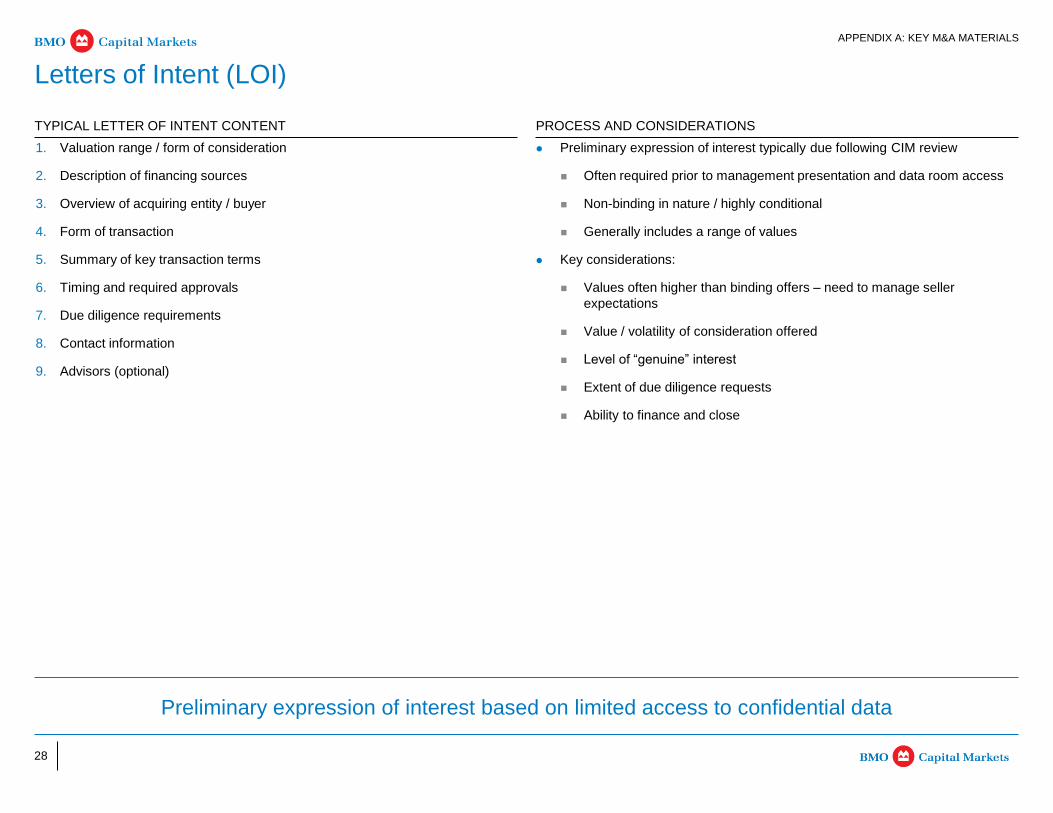

1. Valuation range / form of consideration

2. Description of financing sources

3. Overview of acquiring entity / buyer

4. Form of transaction

5. Summary of key transaction terms

6. Timing and required approvals

7. Due diligence requirements

8. Contact information

9. Advisors (optional)

Preliminary expression of interest typically due following CIM review

Often required prior to management presentation and data room access

Non-binding in nature / highly conditional

Generally includes a range of values

Key considerations:

Values often higher than binding offers – need to manage seller

expectations

Value / volatility of consideration offered

Level of “genuine” interest

Extent of due diligence requests

Ability to finance and close

APPENDIX A: KEY M&A MATERIALS

Letters of Intent (LOI)

Preliminary expression of interest based on limited access to confidential data

TYPICAL LETTER OF INTENT CONTENT PROCESS AND CONSIDERATIONS

29

APPENDIX A: KEY M&A MATERIALS

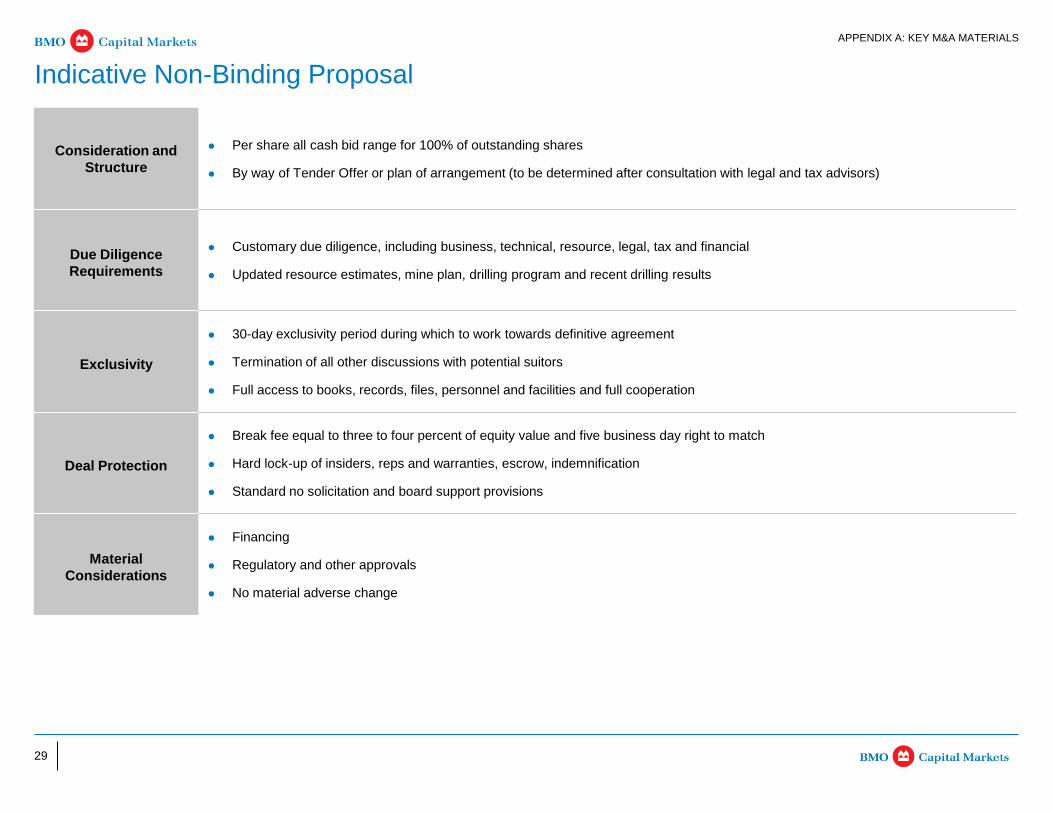

Indicative Non-Binding Proposal

Consideration and

Structure

Per share all cash bid range for 100% of outstanding shares

By way of Tender Offer or plan of arrangement (to be determined after consultation with legal and tax advisors)

Due Diligence

Requirements

Customary due diligence, including business, technical, resource, legal, tax and financial

Updated resource estimates, mine plan, drilling program and recent drilling results

Exclusivity

30-day exclusivity period during which to work towards definitive agreement

Termination of all other discussions with potential suitors

Full access to books, records, files, personnel and facilities and full cooperation

Deal Protection

Break fee equal to three to four percent of equity value and five business day right to match

Hard lock-up of insiders, reps and warranties, escrow, indemnification

Standard no solicitation and board support provisions

Material

Considerations

Financing

Regulatory and other approvals

No material adverse change

30

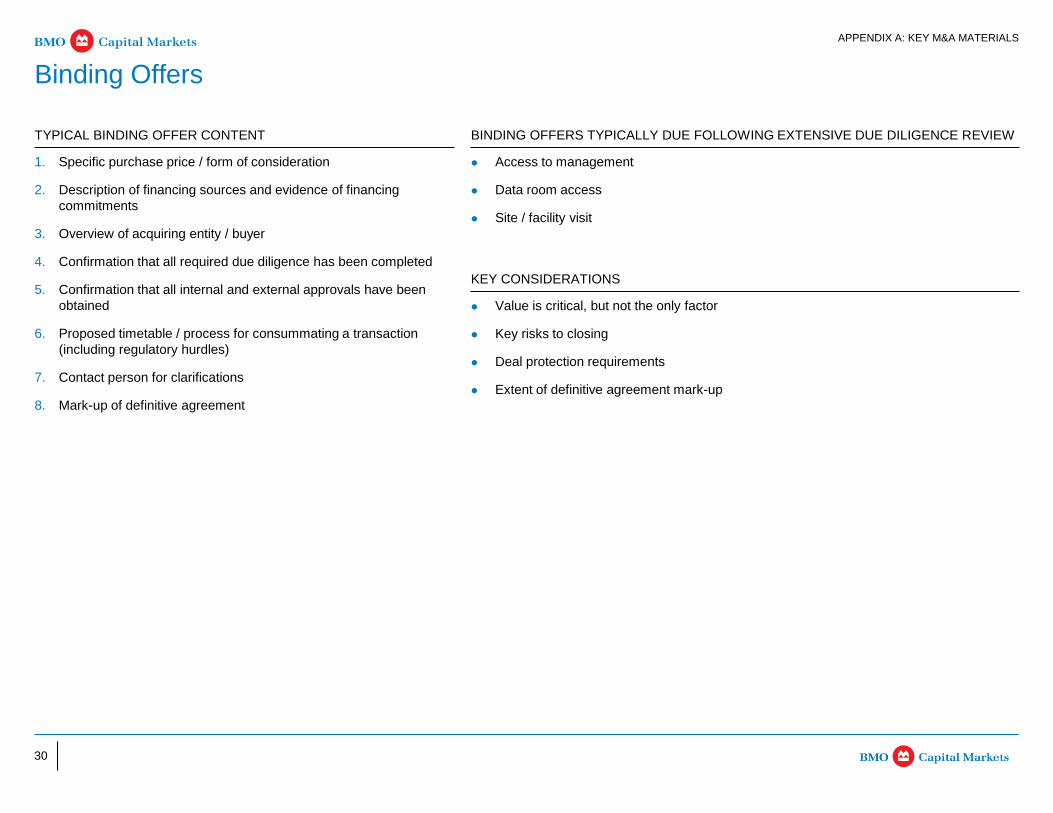

1. Specific purchase price / form of consideration

2. Description of financing sources and evidence of financing

commitments

3. Overview of acquiring entity / buyer

4. Confirmation that all required due diligence has been completed

5. Confirmation that all internal and external approvals have been

obtained

6. Proposed timetable / process for consummating a transaction

(including regulatory hurdles)

7. Contact person for clarifications

8. Mark-up of definitive agreement

Access to management

Data room access

Site / facility visit

APPENDIX A: KEY M&A MATERIALS

Binding Offers

TYPICAL BINDING OFFER CONTENT BINDING OFFERS TYPICALLY DUE FOLLOWING EXTENSIVE DUE DILIGENCE REVIEW

Value is critical, but not the only factor

Key risks to closing

Deal protection requirements

Extent of definitive agreement mark-up

KEY CONSIDERATIONS

31

APPENDIX B: SAMPLE DUE DILIGENCE LIST

Appendix B: Sample Due Diligence List

Section 1 Middle Market M&A Update

Section 2 Middle Market M&A 101

Section 3 Middle Market M&A Key Areas of Due Diligence

Appendix A - C

32

Corporate / ownership structure

List of all directors, officer and managers

List of material subsidiaries and affiliates

Board / investor presentations

Corporate brochures and other marketing materials

Copies of all prior valuations and appraisals

Independent industry reports or studies by outside consultants

Minute books for all investor, board and committee meetings

Current list of investors

Schedule of fully diluted shares / partnership units outstanding (including

expiration and exercise price of all options and warrants)

Shareholder / partnership agreement(s)

Audited financial statements for last five years (including copies of all audit

letters)

Quarterly financial statements for last three years

Five-year business plan (including detailed management forecast / budget)

Capital spending plan (identifying minimum sustaining and other capital

expenditures with associated benefits)

Fixed asset schedule (including historical capital spending and depreciation)

Intangible asset schedule

Historical working capital schedule (including monthly break-down of working

capital for last three years)

Monthly financial reporting package for last five years

Detailed cost of sales breakdown

Details regarding all contingent liabilities

Summary of current federal and state tax position (including current tax basis

and net operating loss carry forwards)

Income tax returns for company and all material subsidiaries for last three

years

Accounting policies manual

Historical sales breakdown by top 10 customers for last five years

Historical pricing by product / service

APPENDIX B: SAMPLE DUE DILIGENCE LIST

Sample Due Diligence Check List

GENERAL FINANCIAL

33

Photographs and facility descriptions

Site maps / surveys

Layouts and configurations

Capacity utilization

Copies of all titles

List of all charges and liens

Copies of all lease agreements and amendments

Description of recent capital improvements

List of major suppliers

Copies of all material supplier contracts

Overview of information technology systems

Software and hardware licensing agreements

IT service agreements

Description of sales and marketing plan / strategy

Physical site tours

Legal agreements (including letters of credit

outstanding)

Closing books for all financings and material

transactions

Insurance policies, coverage and claims history

Summary of existing, pending or threatened

litigation, arbitration or investigations

Copies of all regulatory opinions

Licenses, permits, consents and authorizations

required to operate

Any correspondence with regulatory bodies

Copies of all non-disclosure / non-compete

agreements

Copies of all trademarks, trademark applications,

copyrights and registrations

Copies of all other material contracts

APPENDIX B: SAMPLE DUE DILIGENCE LIST

Sample Due Diligence Check List (cont’d)

FACILITIES / OPERATIONAL HUMAN RESOURCES LEGAL AND OTHER

Organizational chart showing reporting lines

Curriculum vitae for all senior management

personnel and executive officers

Copies of all employment contracts

Summary of employees (including location,

average length of employment, average age and

functional area)

Human resources manuals and brochures

Description of compensation framework and

bonus plans

Description of benefits and pension plans

Description of profit sharing plans

Form of outside consultant service agreement

34

APPENDIX C: DISCLAIMER

Appendix C: Disclaimer

Section 1 Middle Market M&A Update

Section 2 Middle Market M&A 101

Section 3 Middle Market M&A Key Areas of Due Diligence

Appendix A - C

35

APPENDIX C: DISCLAIMER

These materials are confidential and proprietary to, and may not be reproduced, disseminated or referred to, in whole or in part without the prior consent of BMO Capital

Markets (“BMO”). These materials have been prepared exclusively for the BMO client or potential client to which such materials are delivered and may not be used for

any purpose other than as authorized in writing by BMO. BMO assumes no responsibility for verification of the information in these materials, and no representation or

warranty is made as to the accuracy or completeness of such information. BMO assumes no obligation to correct or update these materials. These materials do not

contain all information that may be required to evaluate, and do not constitute a recommendation with respect to, any transaction or matter. Any recipient of these

materials should conduct its own independent analysis of the matters referred to herein.

BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A. (member FDIC),

Bank of Montreal Ireland p.l.c., and Bank of Montreal (China) Co. Ltd and the institutional broker dealer businesses of BMO Capital Markets Corp. (Member SIPC) and

BMO Capital Markets GKST Inc. (Member SIPC) in the U.S., BMO Nesbitt Burns Inc. (Member Canadian Investor Protection Fund) in Canada and Asia, BMO Capital

Markets Limited (authorized and regulated by the Financial Conduct Authority) in Europe and Australia and BMO Advisors Private Limited in India. “BMO Capital

Markets” is a trademark of Bank of Montreal, used under license. "BMO (M-Bar roundel symbol)" is a registered trademark of Bank of Montreal, used under license.

BMO does not provide tax or legal advice. Any discussion of tax matters in these materials (i) is not intended to be used, and cannot be used or relied upon, for the

purposes of avoiding any tax penalties and (ii) may have been written in connection with the “promotion or marketing” of the transaction or matter described herein.

Accordingly, the recipient should seek advice based on its particular circumstances from an independent tax advisor.

Disclaimer

All values in this document are in US$ unless otherwise specified