microsoft powerpoint june 27 07 final ppt - nordex · china india established markets emerging ......

TRANSCRIPT

Conference CallJune 27, 2007

Nordex AG

Page 2

Situation

• Major shareholders Goldman Sachs and CMP Capital Management Partners are investigating a possible sale of their shares in the company

• At this stage, it is not possible to ascertain whether and in what form a total or partial sale will take place

• Nordex has decided to use the increased visibility of the business to provide a long-term view on the stand-alone value of the company

• Nordex keeps its existing medium-term guidance of 50% top-line growth unchanged but provides more detail on strategy and business development

Page 3

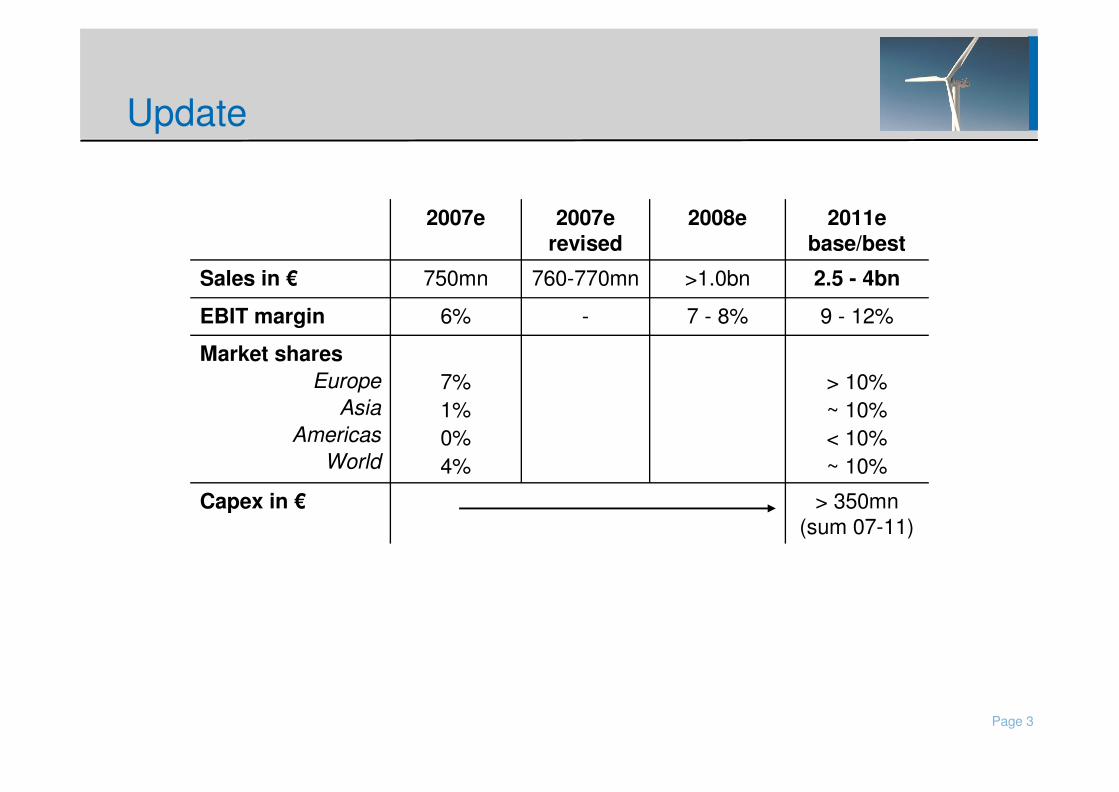

Update

7 - 8%

>1.0bn

2008e

> 10%~ 10%< 10%~ 10%

7%1%0%4%

Market sharesEurope

AsiaAmericas

World

> 350mn (sum 07-11)

Capex in €

9 - 12%-6%EBIT margin

2.5 - 4bn760-770mn750mnSales in €

2011e base/best

2007e revised

2007e

Page 4

Strategy to maintain above industry growth

1. Focus on selective growth markets

• Core European markets

• Infrastructure in China set for future growth

• Re-entry in North America

� Leverage strong track record

2. Drive local markets from within

• Own legal entities with local management in each volume market

• Implementation of value chain in each region

• Market-specific product development

3. Focus on MW class with highly attractive growth rates

4. Focus on long-standing relationship with utilities and IPPs

Page 5

Strong market outlook

2007e 2008e 2009e 2010e 2011e

Europe Americas Asia/Pacific RoW

BTM growth projection until 2011 by region New installations 2007-11

CAGR

Asia/Pacific: 29%

Americas: 24%

Europe: 16%

Thereof Offshore: 5%

18,800

21,980

25,730

28,835

33,500

CAGR: 17.4% Share

46%

2%

26%

26%

Source: BTM 2007

Page 6

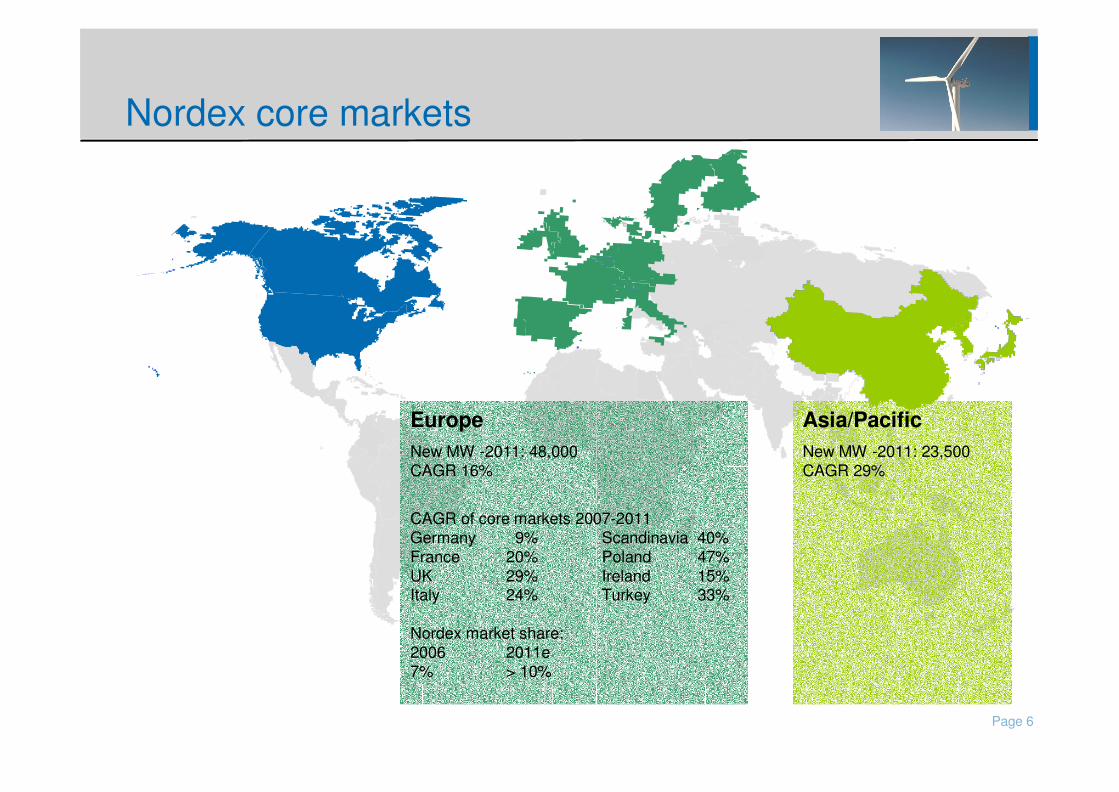

Nordex core markets

EuropeNew MW -2011: 48,000CAGR 16%

CAGR of core markets 2007-2011Germany 9% Scandinavia 40%France 20% Poland 47%UK 29% Ireland 15%Italy 24% Turkey 33%

Nordex market share:2006 2011e7% > 10%

Asia/PacificNew MW -2011: 23,500 CAGR 29%

� Local production and purchasing structures up and running

Nordex market share:2006 2011e1% ~ 10%

North AmericaNew MW -2011: 28,000 CAGR 24%

� Set-up of full operationstructures (incl. Production) by 2009

Nordex market share:2006 2011e0% < 10%

Source: MAKE, Nordex

Page 7

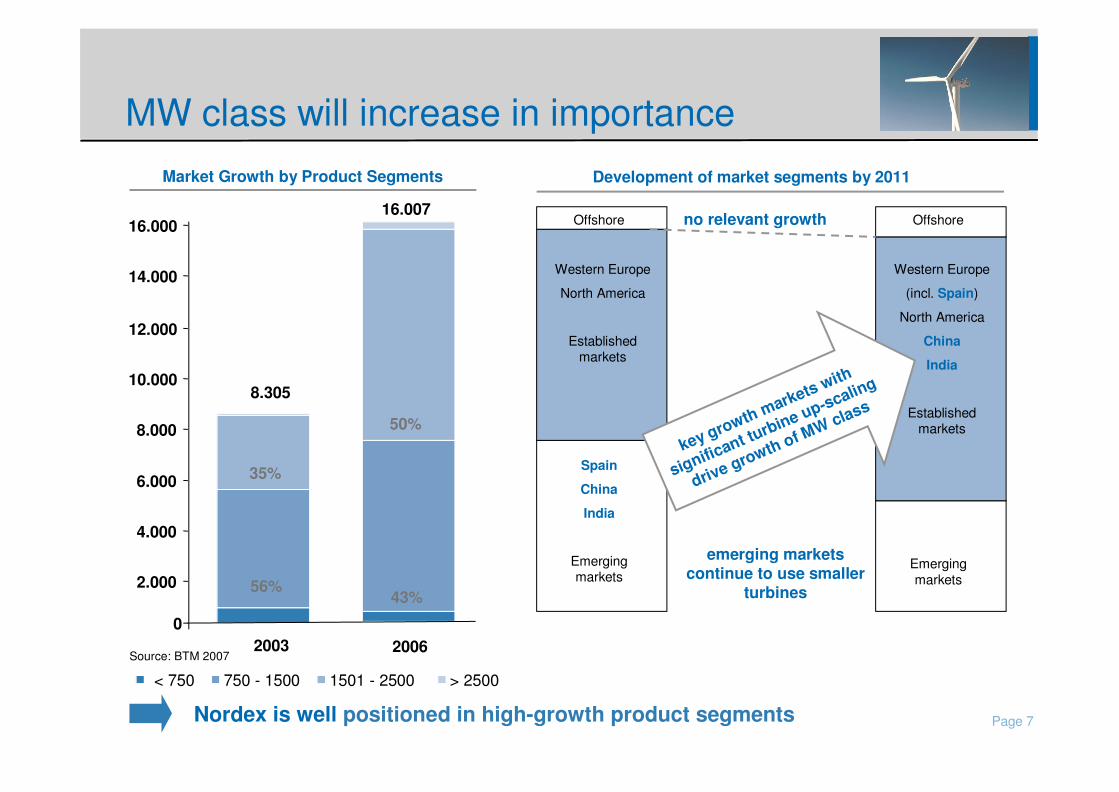

MW class will increase in importance

< 750 750 - 1500 1501 - 2500 > 2500

8.305

0

2.000

4.000

6.000

8.000

10.000

12.000

2003

16.007

2006

14.000

16.000

50%

43%

Market Growth by Product Segments

35%

56%

Nordex is well positioned in high-growth product segments

Source: BTM 2007

Development of market segments by 2011

Offshore

Western Europe

North America

Established markets

Spain

China

India

Emerging markets

Offshore

Western Europe

(incl. Spain)

North America

China

India

Established markets

Emerging markets

no relevant growth

emerging markets continue to use smaller

turbines

key growth markets with

significant turbine up-scaling

drive growth of MW class

Page 8

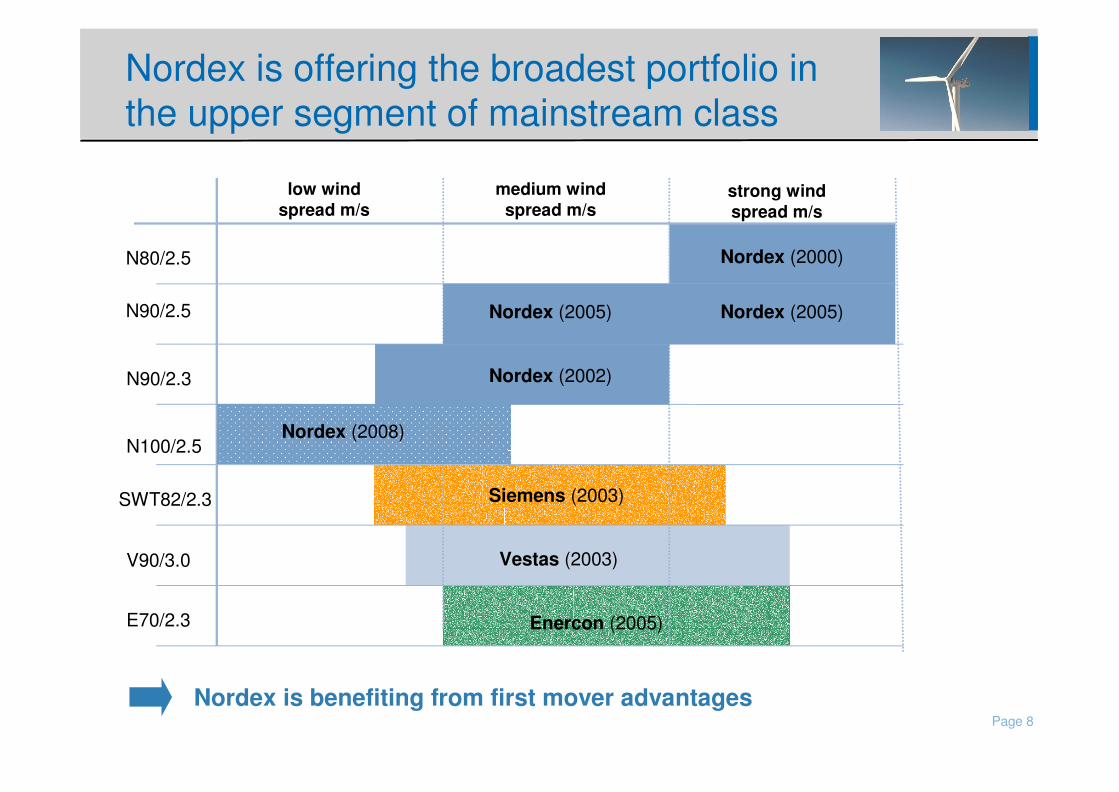

Nordex is offering the broadest portfolio in the upper segment of mainstream class

low windspread m/s

medium windspread m/s

N80/2.5

N90/2.5

Nordex (2000)

SWT82/2.3

V90/3.0

E70/2.3

N90/2.3

strong windspread m/s

N100/2.5

Nordex (2005)Nordex (2005)

Nordex (2002)

Nordex (2008)

Siemens (2003)

Vestas (2003)

Enercon (2005)

Nordex is benefiting from first mover advantages

Page 9

Leveraging established products –strong pipeline

2007 2008 2009 2010 2011 2012

N 60

S 70/77

N 80/90

N 100

N1XX

Product offering Europe

Main product Asia

Product offering Europe

Product offering U.S.

Product offering Europe/U.S. – completion of product range

Prototype

Product offering Asia/Europe Only delivery of single projects

Prototype U.S.

(Production only from Asia)

Prototype Maturity phase

Page 10

in € m

Reinvestments

New investments*

Germany

China

USA

Other Countries

Total CAPEX

Extension of production capacities to fulfil sales scenarios 2008 - 2011

2007e 2008e 2009e 2010e 2011e

Σ 70 Σ 100

Σ 50

Σ 80

Σ 50

Σ > 350

* blade + turbine production

Total capacity of 4,450 MW will secure mid-term growth path of 50% per year

Page 11

Financing Capabilities

1. Short-term financing of capex in place

• Nordex is fully booked until 2008

• Increased visibility due to order increase and change in customer structure

2. Strong positive cash flow expected in the medium term

• High amount of advanced payments

• Stable calculation of project margins

3. Significant improvement of EBIT margin

4. Decision between debt or equity financing in the long-term to be taken

Page 12

Improved visibility due to increase in orders

Order book (€ bn)

0.5

1.0

1.5

2.0

firm orders conditional orders

31/3/06 30/6/06 30/9/06 31/12/06 31/3/07 30/4/07

Book to bill ratio has rosen from 1.0 (Q1/05) to 2.4 (Q1/07)

Page 13

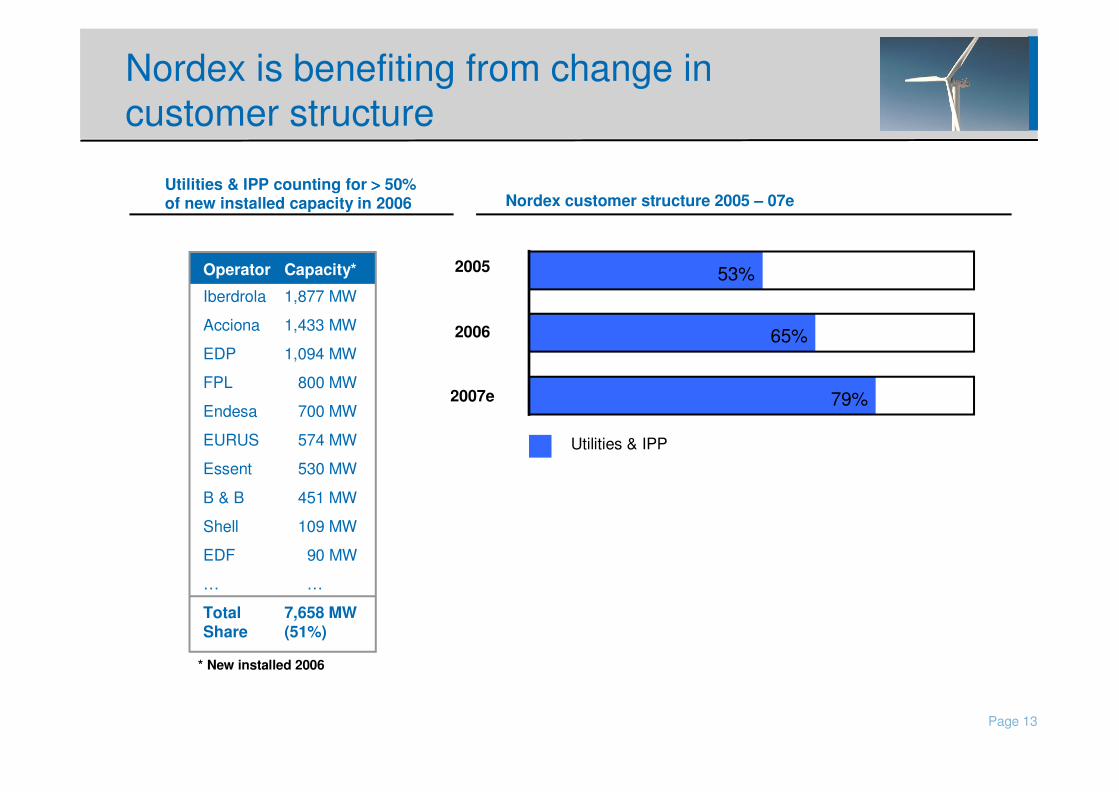

Nordex is benefiting from change in customer structure

Operator Capacity*

Iberdrola

Acciona

EDP

FPL

Endesa

EURUS

Essent

B & B

Shell

EDF

…

Total Share

1,877 MW

1,433 MW

1,094 MW

800 MW

700 MW

574 MW

530 MW

451 MW

109 MW

90 MW

…

7,658 MW(51%)

Nordex customer structure 2005 – 07eUtilities & IPP counting for >>>> 50% of new installed capacity in 2006

* New installed 2006

Utilities & IPP

2005

2006

2007e

65%

79%

53%

� Long standing relationship

� Financial stability

� Earnings visibility

Page 14

Main drivers of bottom-line growth

2007e 2008e 2011e

Target EBIT margin 6% 7-8% 9-12%

++ Higher utilisation of capacity

+ Price increase per MW due to shortages of WTG

- Expenditures into new markets

Page 15

Proven process stability under strong growth path of 50% per year

Example: contribution margin sales vs. final calculation

0.9%

2004

2005

2006

100% 98%

100% 100.9%

-2%

100% 100.8%0.8%

Tight processes and quality control

• Gate approval process (sales)

• Expected demand (supply)

• Production plan

• Project (start) calculation

• Internal handover (PM / service)

1-5/07 100% 101.2%1.2%

Page 16

Determinants of future Nordex growth path

1. Sustainable strong market growth for wind turbines

2. Products meeting market requirements

3. Availability of needed financial funds

4. Sufficient production capacities in place

5. Stability of business processes in Nordex

2005 -´07 2008 -´11

CAGR: 17% forecasted

2.0 – 3.0 MW expected to stay mainstream

Positive negotiations / talks (bonds, cash)

Extension of facilities prefaced

Close controlling systems in place

Page 17

• Order backlog secures top-line growth of 50% per year until 2008

• Nordex set out to generate € 4.0bn revenues and an EBIT-margin of 12% in 2011

• Long-term view on stand-alone value to facilitate investment decisions for equity investors and potential strategic buyers

Conclusion