microéconomie de la finance -...

TRANSCRIPT

Chapitre 47e édition

La théorie Moyenne-Variance du choix de portefeuille

2

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Part 4. Mean-Variance Portfolio Theory

3

4.1 Measuring Risk and Return

4.2 Asset Allocation with 2 Risky Assets

4.3 Introducing a Risk Free Asset and the Tobin’s Separation Theorem

4.4 Asset Allocation with N risky Assets

4.5 Portfolio Diversification

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Preamble:

Mean/Variance Analysis Assumptions

4

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Mean-variance is simpler

5

• Early researchers in finance, such as Markowitz and Sharpe, used just the mean and the variance of the return rate of an asset to describe it.

• Characterizing the prospects of a gamble with its mean and variance is often easier than using an NM utility function, so it is popular.

• But is it compatible with VNM theory?

• The answer is yes … approximately … under some conditions.

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Mean-variance assumptions

6

• Investors maximise expected utility of end-of-perio d wealth

• Can be shown that above implies maximise a function of expected portfolio returns and portfolio variance p roviding

- Either utility is quadratic, or

- Portfolio returns are normally distributed (and utility is concave),

- Consider only small risks (then approximately true)

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Mean-variance: quadratic utility

7

Suppose utility is quadratic, U(y) = ay–by2,

with some conditions on a and b

Expected utility is then

2

2

[ ( )] ( ) ( )

( ) ( ) V ar( ) .

E U y aE y bE y

aE y b E y y

= −

= − +

Thus, expected utility is a function of:

the mean: E(y),

and the variance: Var(y)

BUT not intuitive Utility function : increasing ARA

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Mean-variance: joint normals

8

• Suppose all lotteries in the domain have normally distributed prized. (They need not be independent of each other).

• Any combination of such lotteries will also be normally distributed.

• The normal distribution is completely described by its first two moments.

• Therefore, the distribution of any combination of lotteries is also completely described by just the mean and the variance.

• As a result, expected utility can be expressed as a function of just these two numbers as well.

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Mean-variance: small risks

9

• The most relevant justification for mean-variance is probably the case of small risks.

• If we consider only small risks, we may use a second order Taylor approximation of the NM utility function.

• A second order Taylor approximation of a concave function is a quadratic function with a negative coefficient on the quadratic term.

• In other words, any risk-averse NM utility function can locally be approximated with a quadratic function.

• But the expectation of a quadratic utility function can be evaluated with the mean and variance. Thus, to evaluate small risks, mean and variance are enough.

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

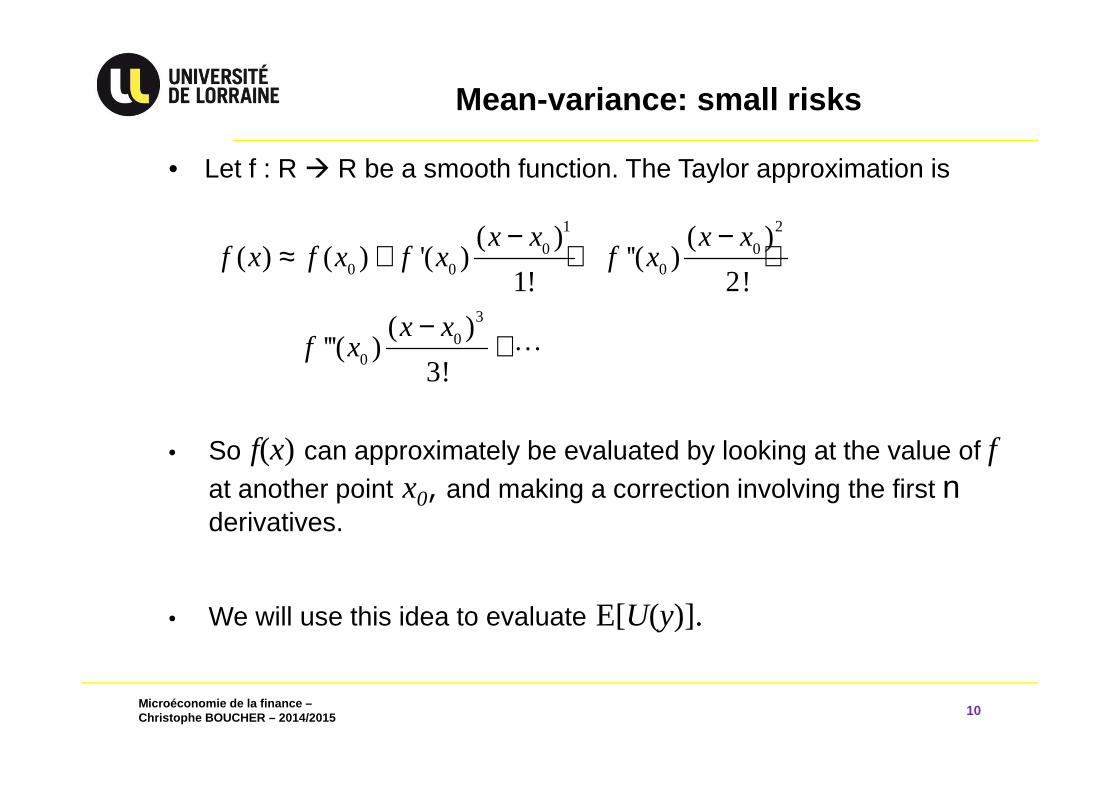

Mean-variance: small risks

10

• Let f : R R be a smooth function. The Taylor approximation is

• So f(x) can approximately be evaluated by looking at the value of fat another point x0, and making a correction involving the first nderivatives.

• We will use this idea to evaluate E[U(y)].

1 2

0 00 0 0

3

00

( ) ( )( ) ( ) '( ) ''( )

1! 2!

( )'''( )

3!

x x x xf x f x f x f x

x xf x

− −≈ + + +

−+⋯

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Mean-variance: small risks

11

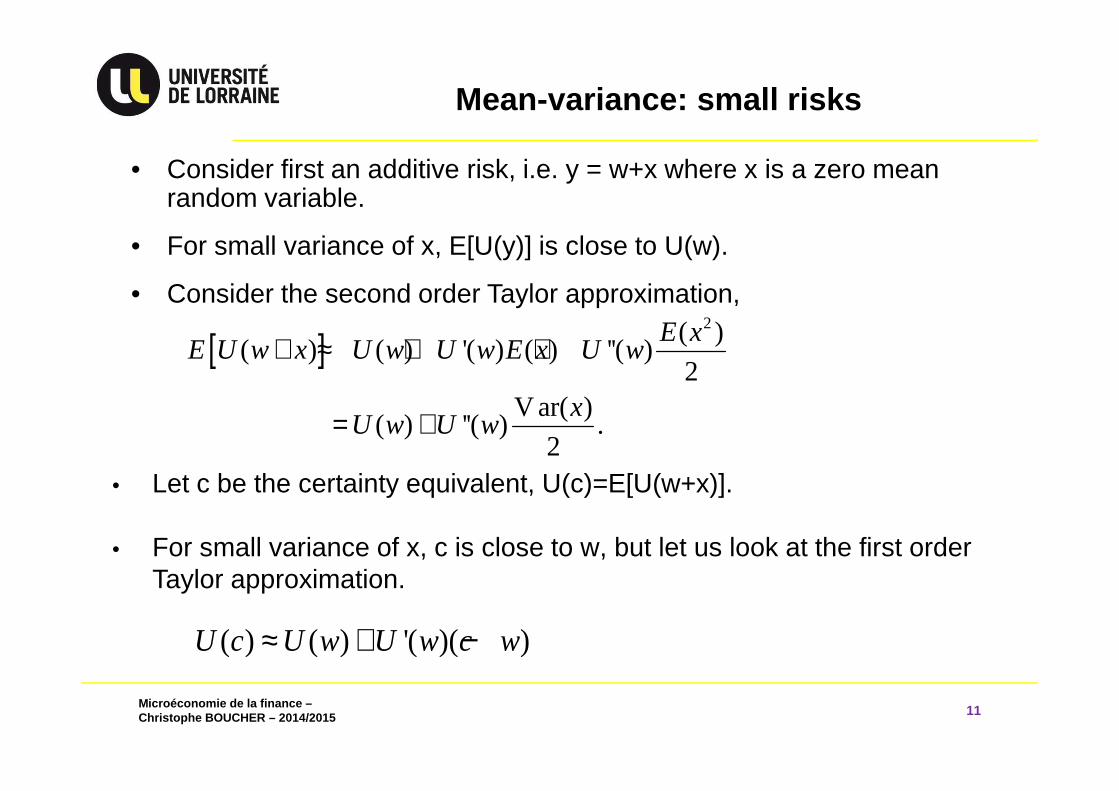

• Consider first an additive risk, i.e. y = w+x where x is a zero mean random variable.

• For small variance of x, E[U(y)] is close to U(w).

• Consider the second order Taylor approximation,

• Let c be the certainty equivalent, U(c)=E[U(w+x)].

• For small variance of x, c is close to w, but let us look at the first order Taylor approximation.

[ ]2( )

( ) ( ) '( ) ( ) ''( )2

V ar( )( ) ''( ) .

2

E xE U w x U w U w E x U w

xU w U w

+ ≈ + +

= +

( ) ( ) '( )( )U c U w U w c w≈ + −

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Mean-variance: small risks

12

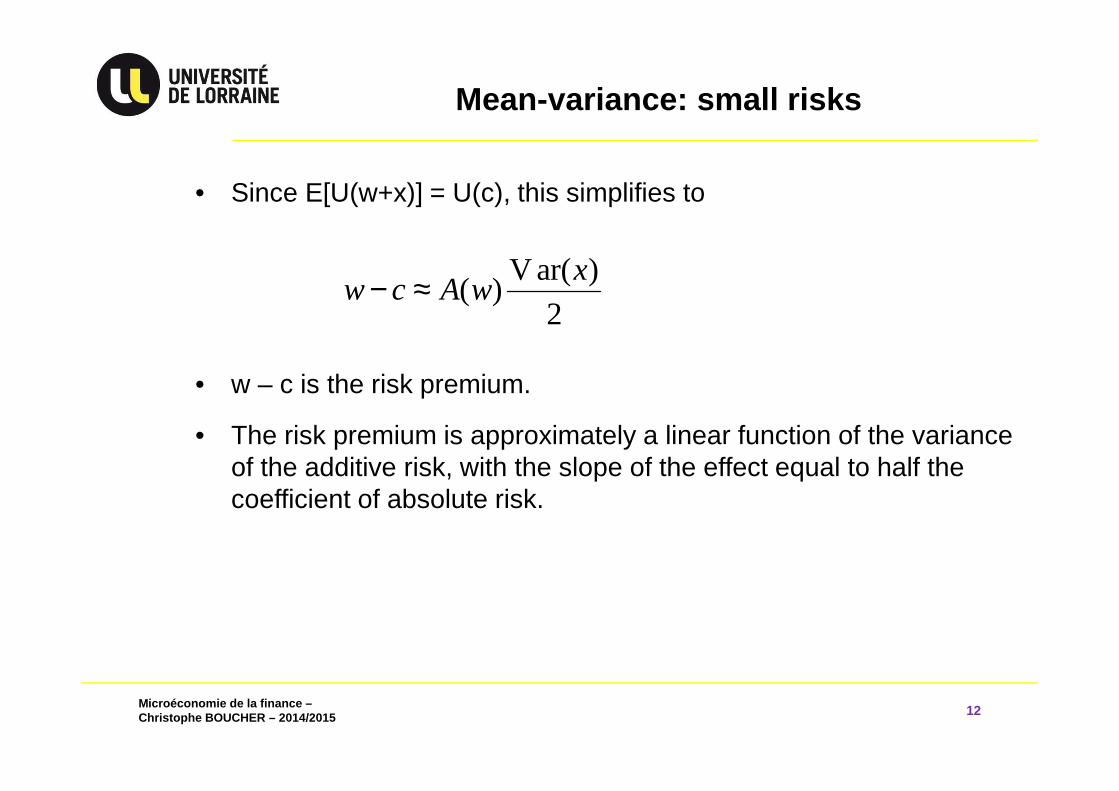

• Since E[U(w+x)] = U(c), this simplifies to

• w – c is the risk premium.

• The risk premium is approximately a linear function of the variance of the additive risk, with the slope of the effect equal to half the coefficient of absolute risk.

V ar( )( )

2

xw c A w− ≈

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

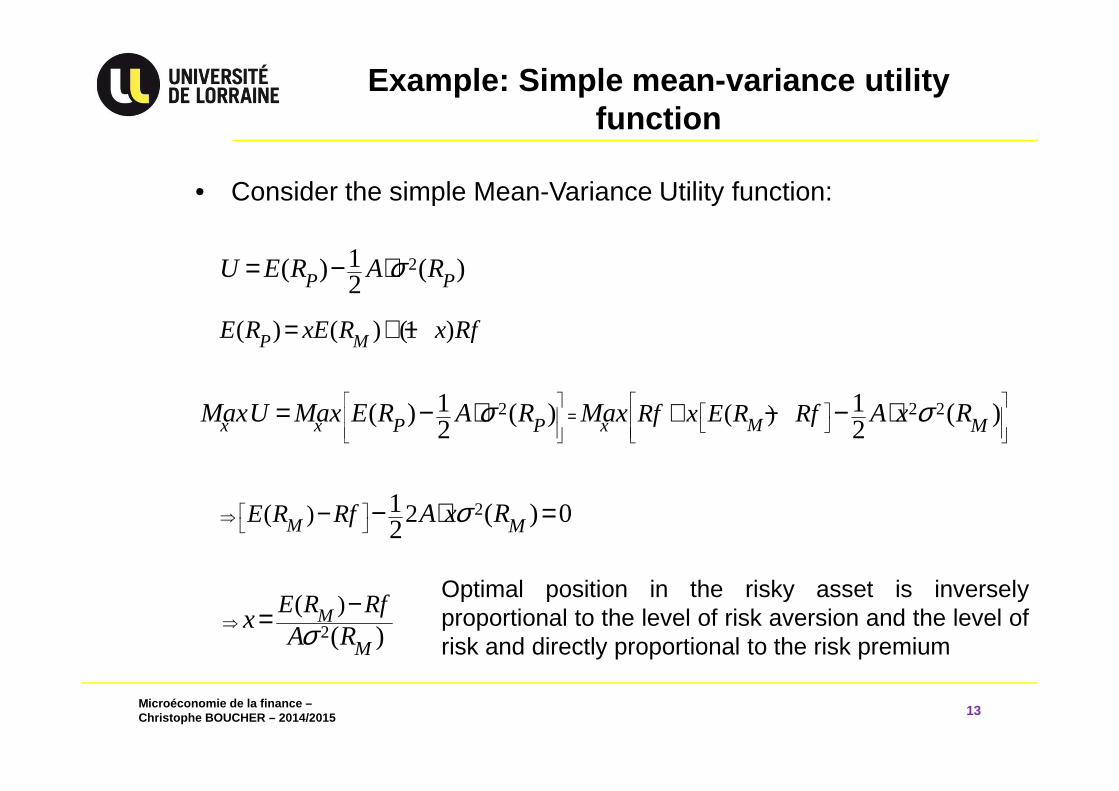

Example: Simple mean-variance utility function

13

• Consider the simple Mean-Variance Utility function:

21( ) ( )2P PU E R A Rσ= − ⋅

2 2 2)(1 1( ) ( ) ( )2 2Mx x xP P MRf x E R RfMaxU Max E R A R Max A x Rσ σ

=

+ −= − ⋅ − ⋅

( ) ( ) (1 )P ME R xE R x Rf= + −

2)( 21 ( ) 02M ME R Rf A x Rσ ⇒

− − ⋅ =

2

)(( )

M

M

E R Rfx

A Rσ⇒−=

Optimal position in the risky asset is inverselyproportional to the level of risk aversion and the level ofrisk and directly proportional to the risk premium

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

4.1 Measuring Risk and Return

14

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

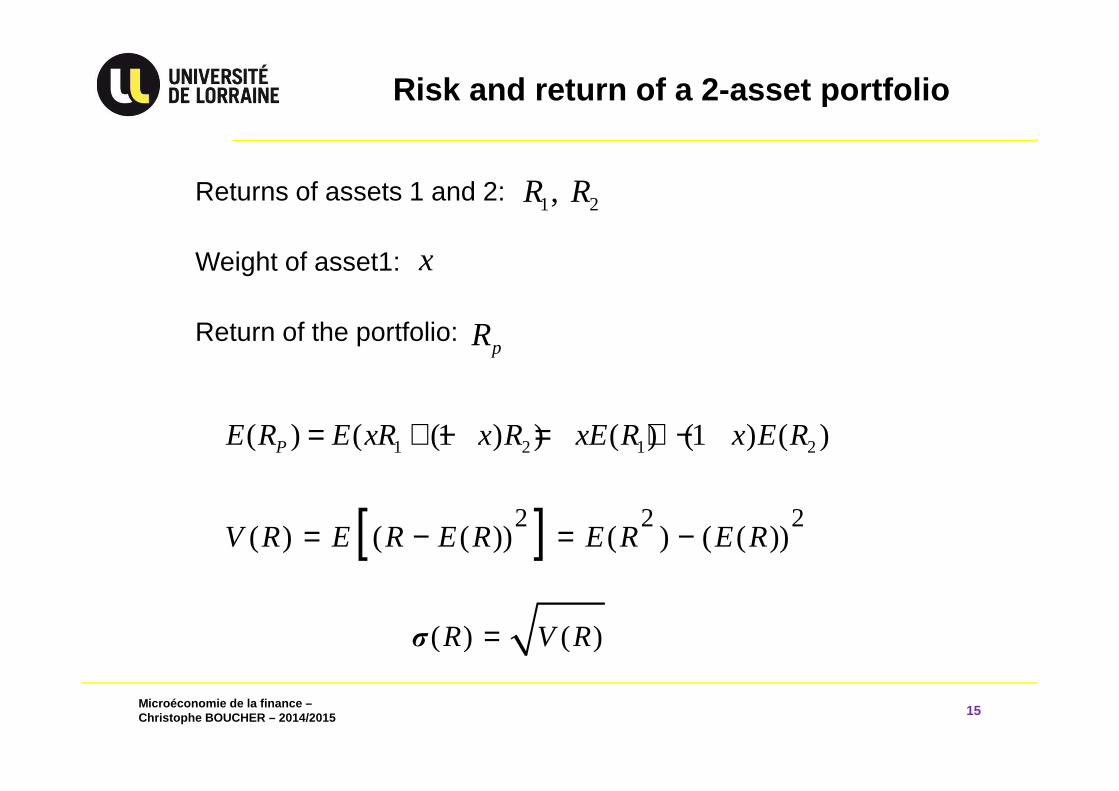

Returns of assets 1 and 2:

Weight of asset1:

Return of the portfolio:

Risk and return of a 2-asset portfolio

15

1 2, R R

x

pR

1 2 1 2( ) ( (1 ) ) ( ) (1 ) ( )PE R E xR x R xE R x E R= + − = + −

[ ]2 2 2( ) ( ( )) ( ) ( ( ))V R E R E R E R E R= − = −

( ) ( )R V Rσ =

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Risk and return of a 2-asset portfolio

16

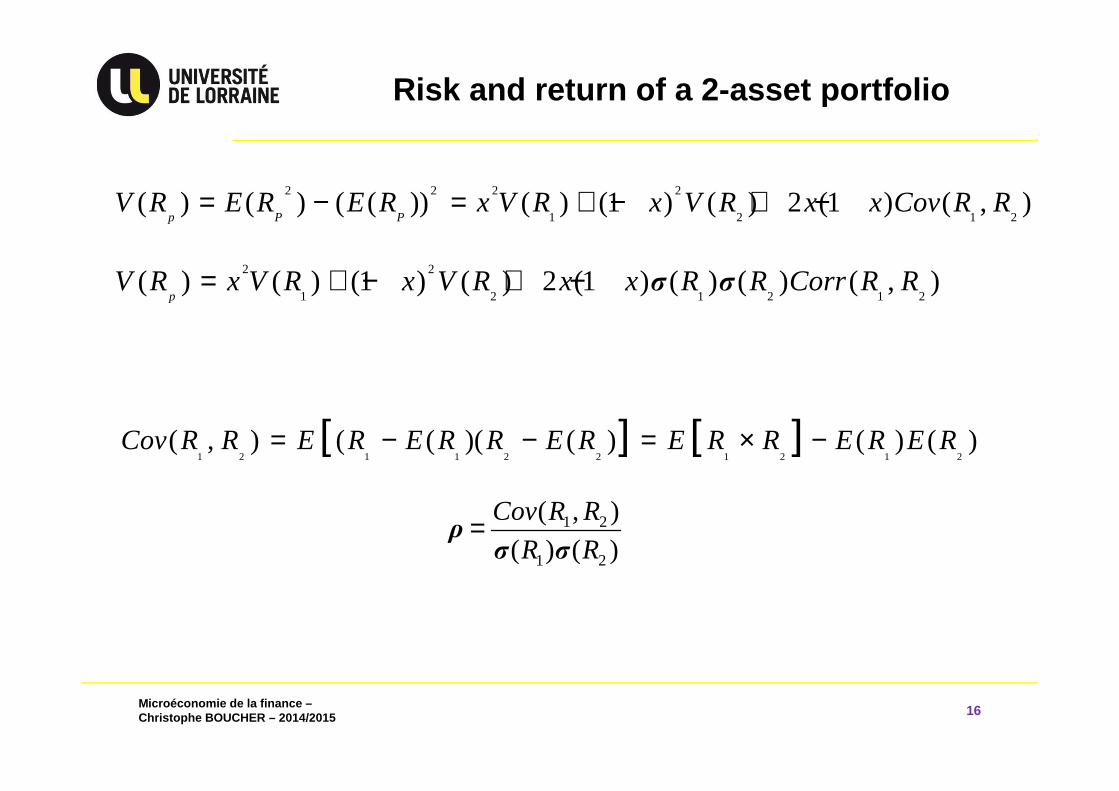

2 2 2 2

1 2 1 2( ) ( ) ( ( )) ( ) (1 ) ( ) 2 (1 ) ( , )

p P PV R E R E R x V R x V R x x Cov R R= − = + − + −

2 2

1 2 1 2 1 2( ) ( ) (1 ) ( ) 2 (1 ) ( ) ( ) ( , )

pV R x V R x V R x x R R Corr R Rσ σ= + − + −

[ ] [ ]1 2 1 1 2 2 1 2 1 2

( , ) ( ( )( ( ) ( ) ( )Cov R R E R E R R E R E R R E R E R= − − = × −

1 2

1 2

( , )

( ) ( )

Cov R R

R R=ρσ σ

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

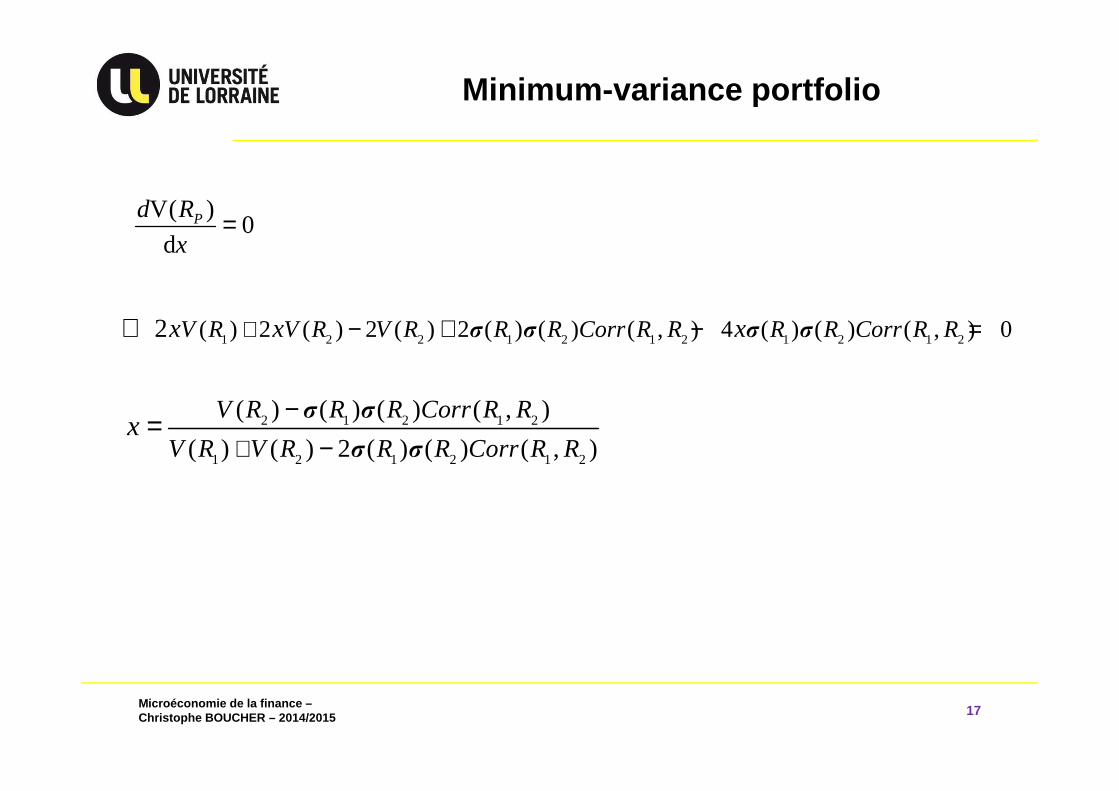

Minimum -variance portfolio

17

V( )0

dPd R

x=

1 2 2 1 2 1 2 1 2 1 2( ) 2 ( ) 2 ( ) 2 ( ) ( ) ( , ) 4 ( ) ( ) ( , ) 02 V R V R V R R R Corr R R R R Corr R Rx x xσ σ σ σ+ − + − =⇔

2 1 2 1 2

1 2 1 2 1 2

( ) ( ) ( ) ( , )

( ) ( ) 2 ( ) ( ) ( , )

V R R R Corr R R

V R V R R R Corr R Rx

σ σ

σ σ+

−−

=

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

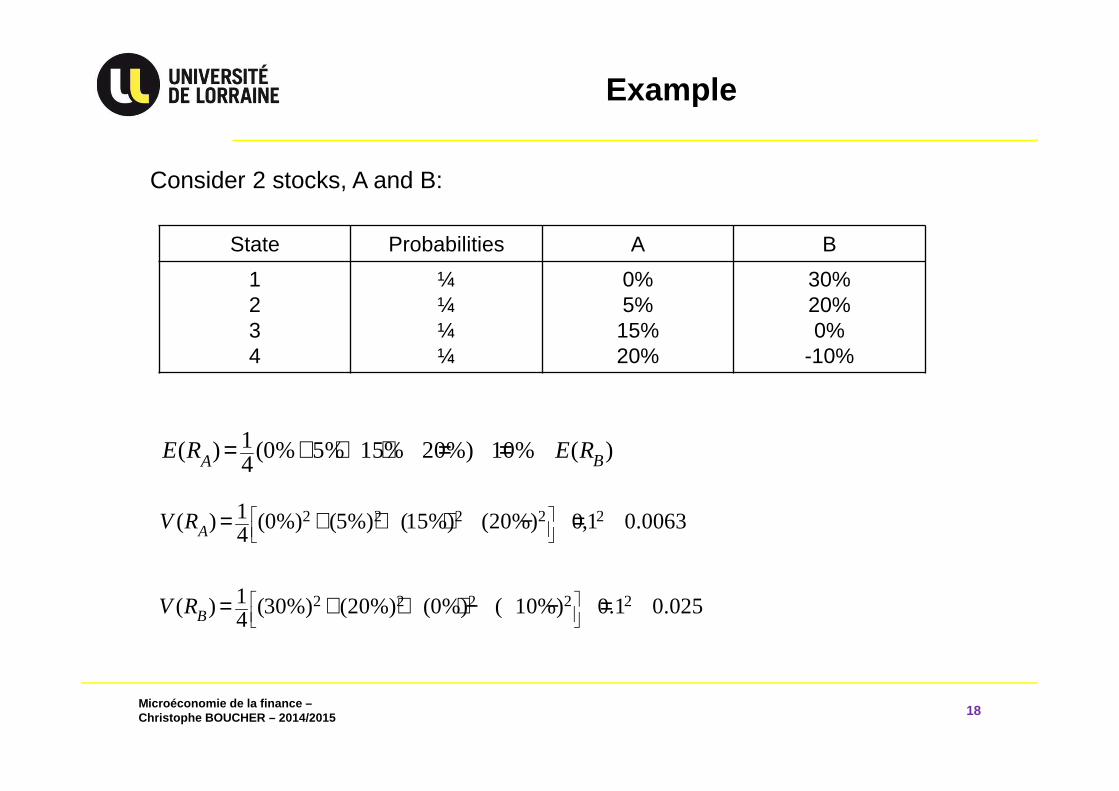

Example

18

Consider 2 stocks, A and B:

State Probabilities A B

1234

¼¼¼¼

0%5%

15%20%

30%20%0%

-10%

1( ) (0% 5% 15% 20%) 10% ( )4 BAE R E R= + + + = =

2 2 2 2 21( ) (0%) (5%) (15%) (20%) 0,1 0.00634AV R

= + + + − =

2 2 2 2 21( ) (30%) (20%) (0%) ( 10%) 0.1 0.0254BV R

= + + + − − =

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

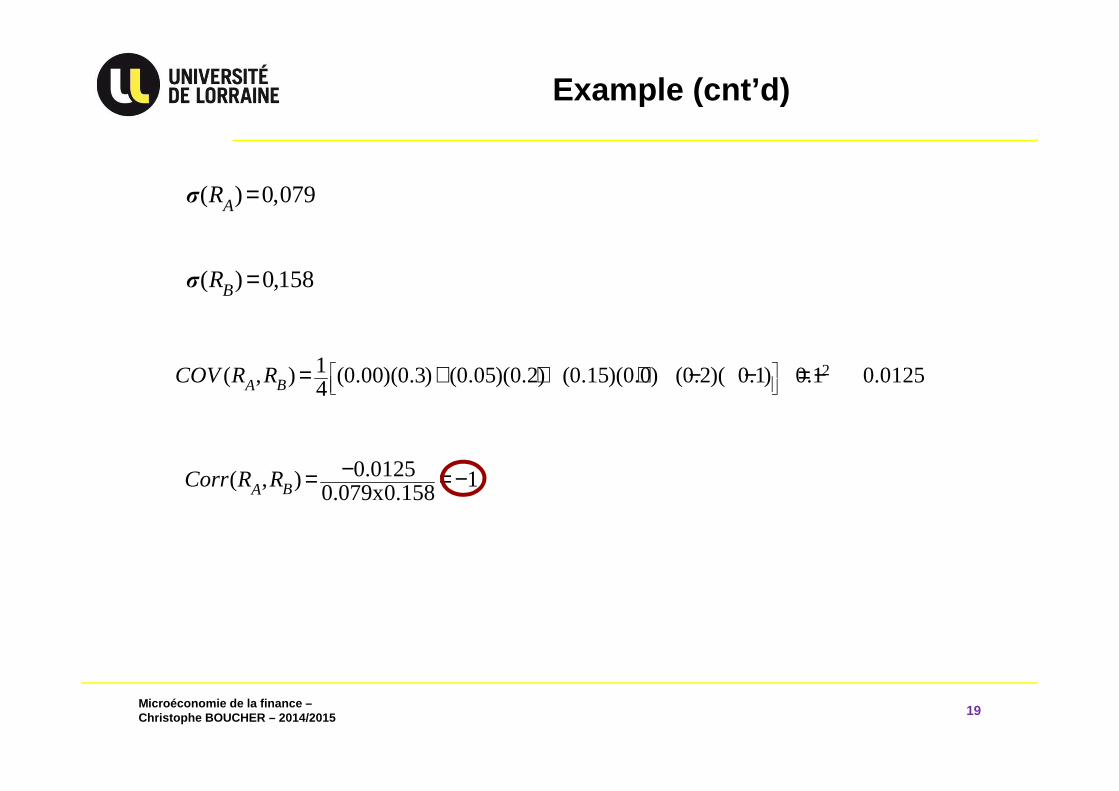

Example (cnt’d)

19

( ) 0,079AR =σ

( ) 0,158BR =σ

21( , ) (0.00)(0.3) (0.05)(0.2) (0.15)(0.0) (0.2)( 0.1) 0.1 0.01254BACOV R R

= + + + − − = −

0.0125( , ) 10.079x0.158BACorr R R −= = −

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

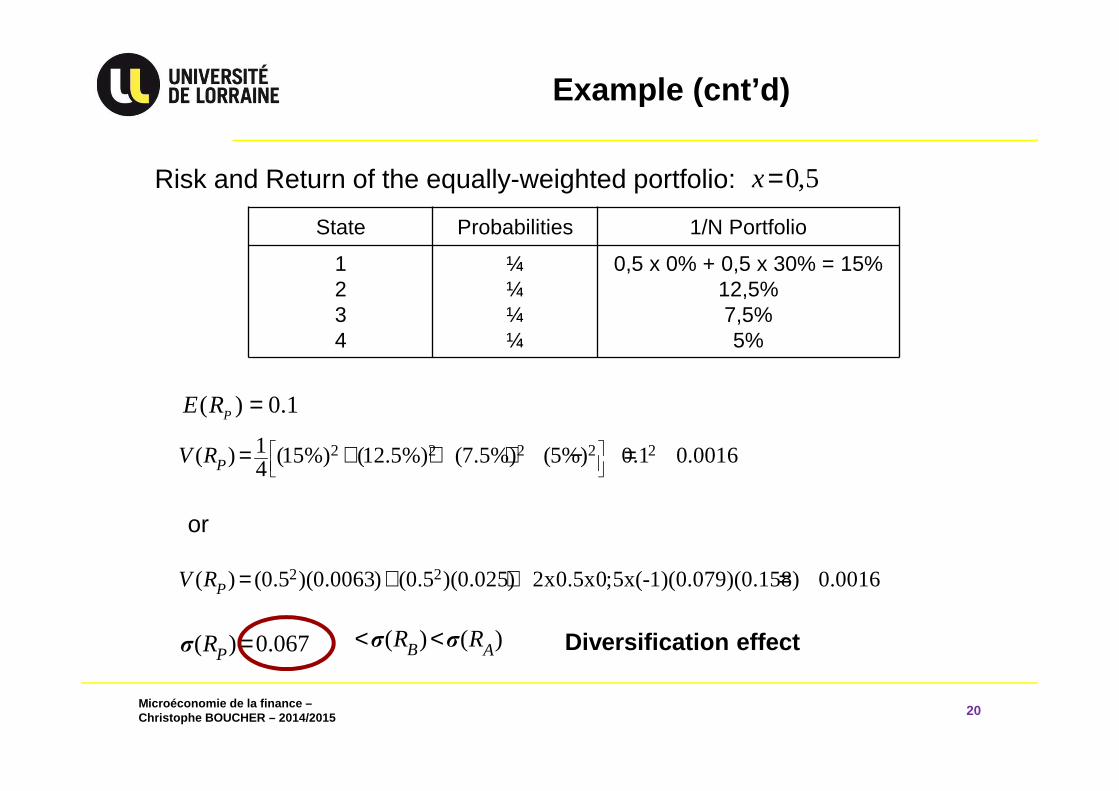

Example (cnt’d)

20

Risk and Return of the equally-weighted portfolio: 0,5x=

State Probabilities 1/N Portfolio

1234

¼¼¼¼

0,5 x 0% + 0,5 x 30% = 15%12,5%7,5%5%

( ) 0.1PE R =

2 2 2 2 21( ) (15%) (12.5%) (7.5%) (5%) 0.1 0.00164PV R

= + + + − =

or

2 2( ) (0.5 )(0.0063) (0.5 )(0.025) 2x0.5x0;5x(-1)(0.079)(0.158) 0.0016PV R = + + =

( ) 0.067PR =σ ( ) ( )B AR R< <σ σ Diversification effect

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

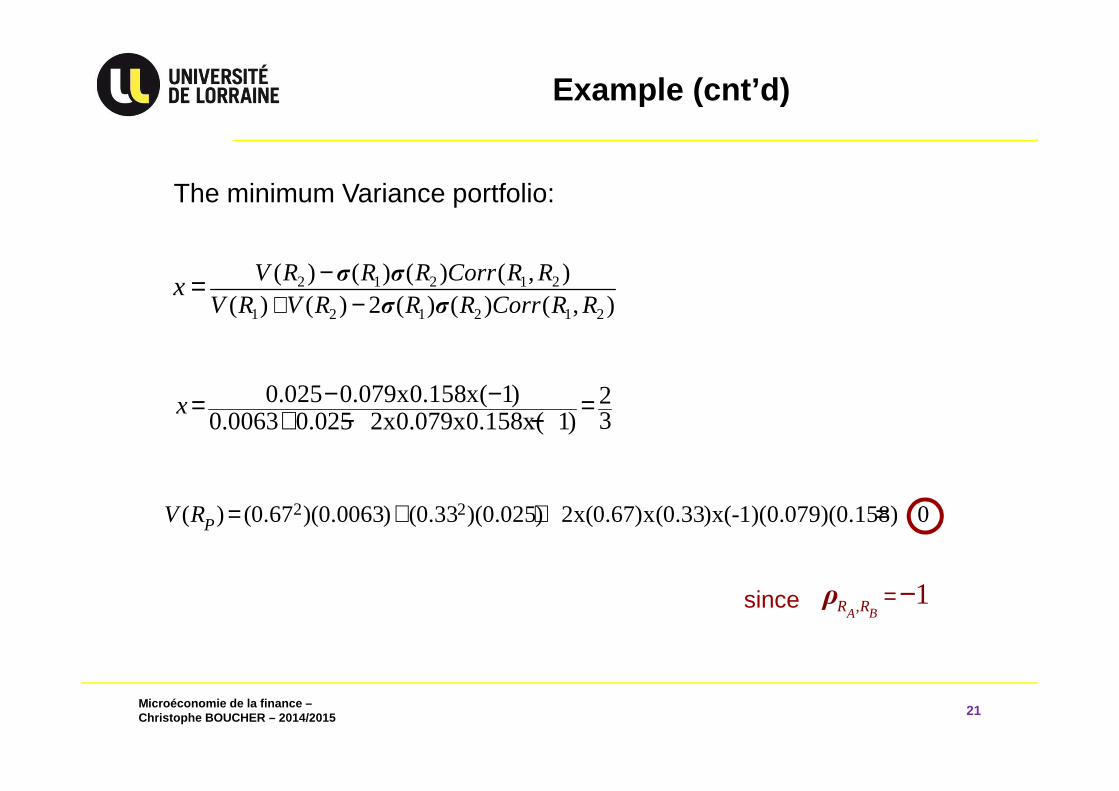

Example (cnt’d)

21

The minimum Variance portfolio:

2 1 2 1 2

1 2 1 2 1 2

( ) ( ) ( ) ( , )( ) ( ) 2 ( ) ( ) ( , )

V R R R Corr R RV R V R R R Corr R R

x+

−−

= σ σ

σ σ

0.025 0.079x0.158x( 1) 230.0063 0.025 2x0.079x0.158x( 1)

x − −= =+ − −

2 2( ) (0.67 )(0.0063) (0.33 )(0.025) 2x(0.67)x(0.33)x(-1)(0.079)(0.158) 0PV R = + + =

since , 1BAR R =−ρ

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

4.2 Asset Allocation with 2 Risky Assets

22

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

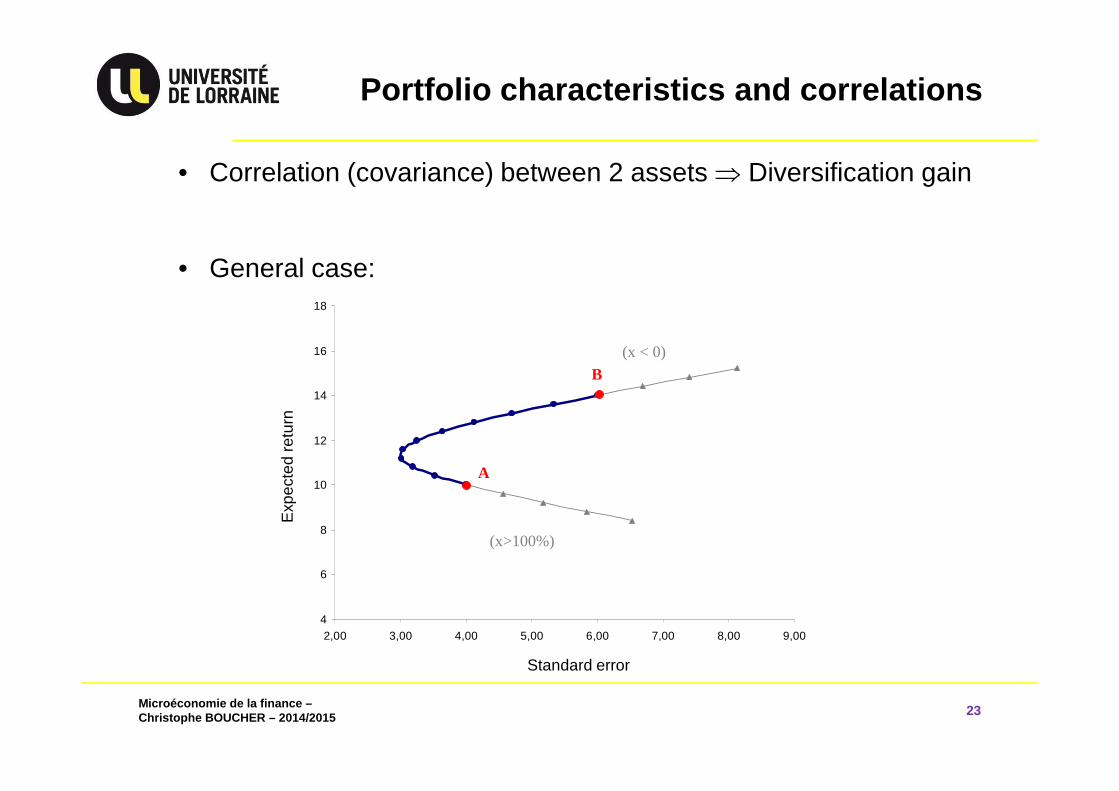

Portfolio characteristics and correlations

23

• Correlation (covariance) between 2 assets ⇒ Diversification gain

• General case:

4

6

8

10

12

14

16

18

2,00 3,00 4,00 5,00 6,00 7,00 8,00 9,00

A

B

(x>100%)

(x < 0)

4

6

8

10

12

14

16

18

2,00 3,00 4,00 5,00 6,00 7,00 8,00 9,004

6

8

10

12

14

16

18

2,00 3,00 4,00 5,00 6,00 7,00 8,00 9,00

A

B

(x>100%)

(x < 0)

Exp

ecte

d re

turn

Standard error

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

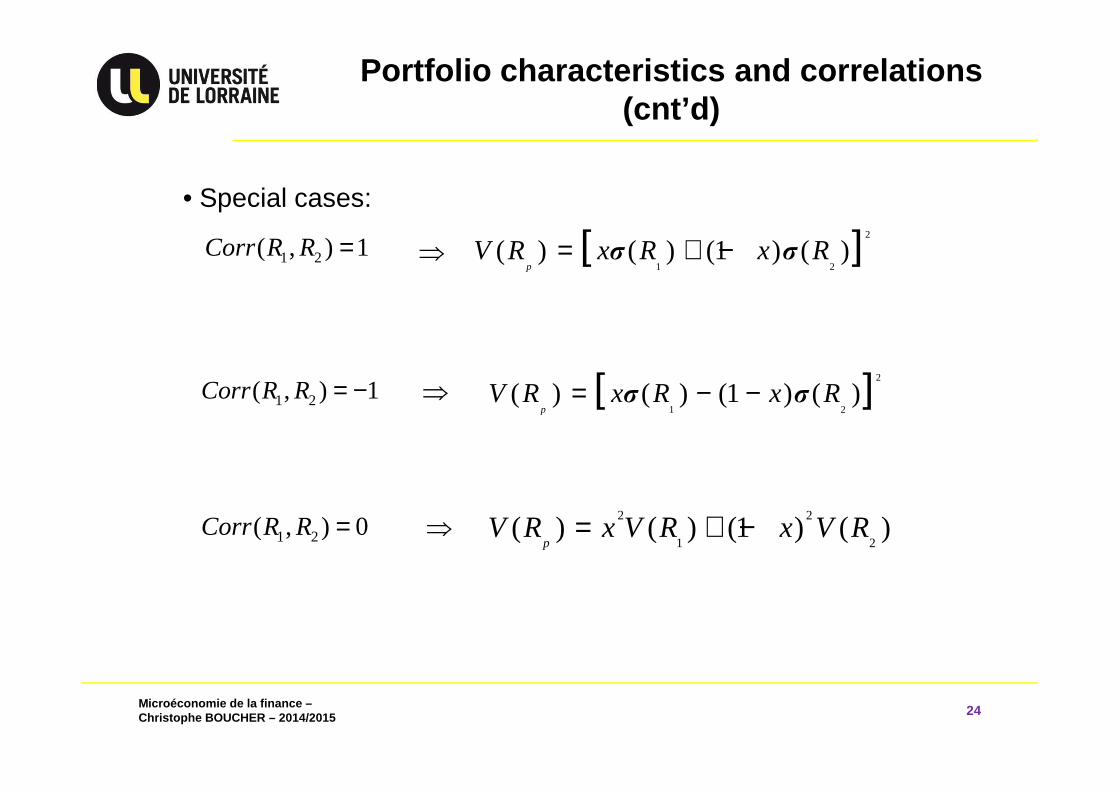

Portfolio characteristics and correlations (cnt’d)

24

• Special cases:

1 2( , ) 1Corr R R =

1 2( , ) 1Corr R R = −

1 2( , ) 0Corr R R =

[ ]2

1 2( ) ( ) (1 ) ( )

pV R x R x R= + −σ σ⇒

[ ]2

1 2( ) ( ) (1 ) ( )

pV R x R x Rσ σ= − −⇒

2 2

1 2( ) ( ) (1 ) ( )

pV R x V R x V R= + −⇒

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

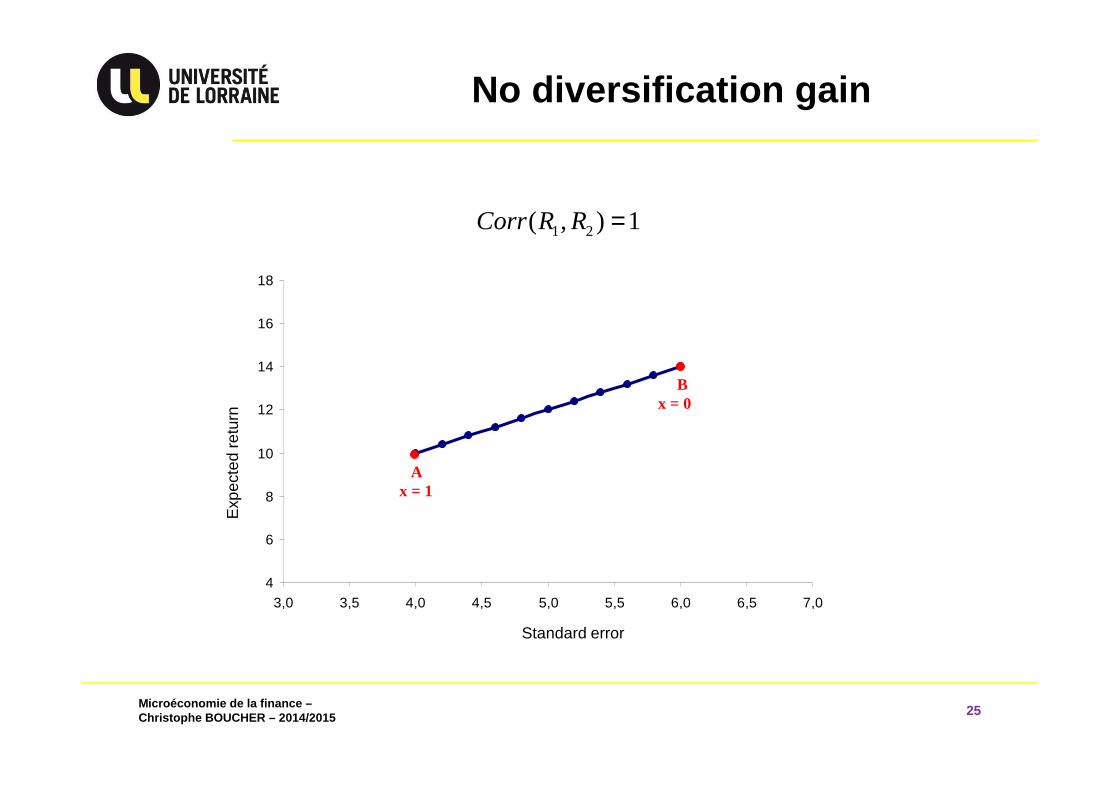

No diversification gain

25

1 2( , ) 1Corr R R =

4

6

8

10

12

14

16

18

3,0 3,5 4,0 4,5 5,0 5,5 6,0 6,5 7,0

Ren

dem

ent e

spér

é du

por

tefe

uille

(%

)

A

B

x = 1

x = 0

Exp

ecte

d re

turn

Standard error

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

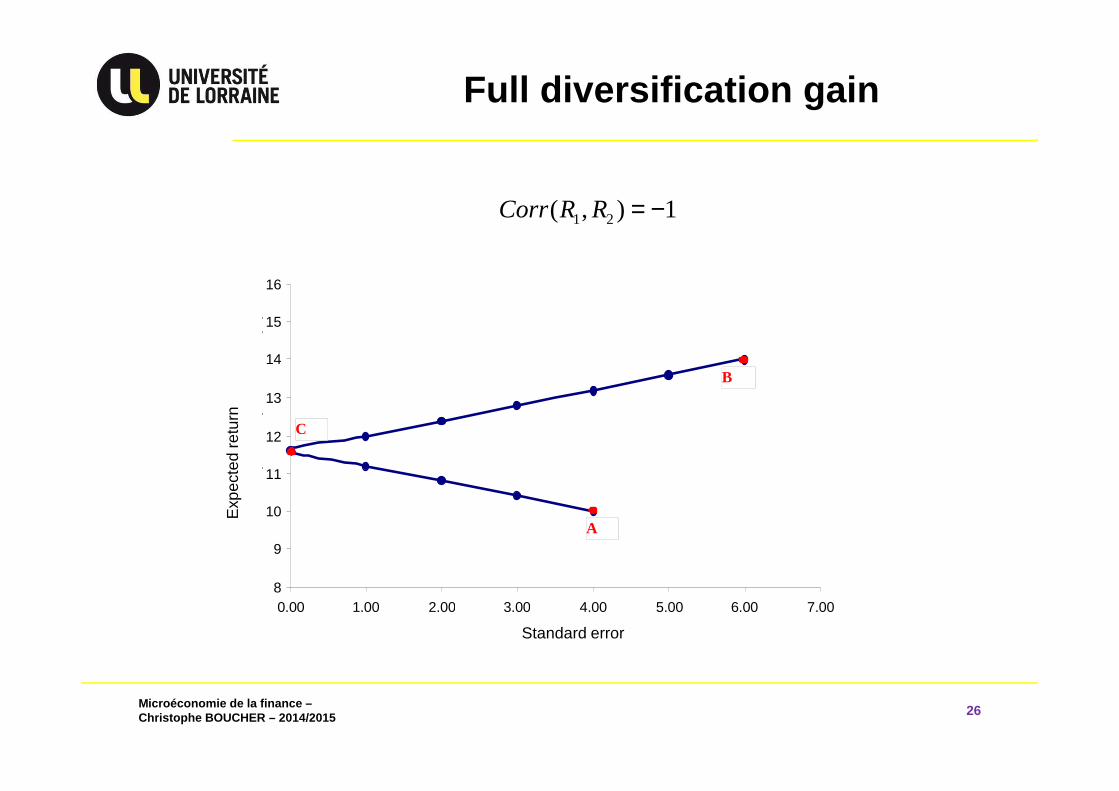

Full diversification gain

26

1 2( , ) 1Corr R R = −E

xpec

ted

retu

rn

Standard error

8

9

10

11

12

13

14

15

16

0,00 1,00 2,00 3,00 4,00 5,00 6,00 7,00Ecart type du portefeuille (%)

Ren

dem

ent e

spér

é du

por

tefe

uille

(%

)

A

B

C

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

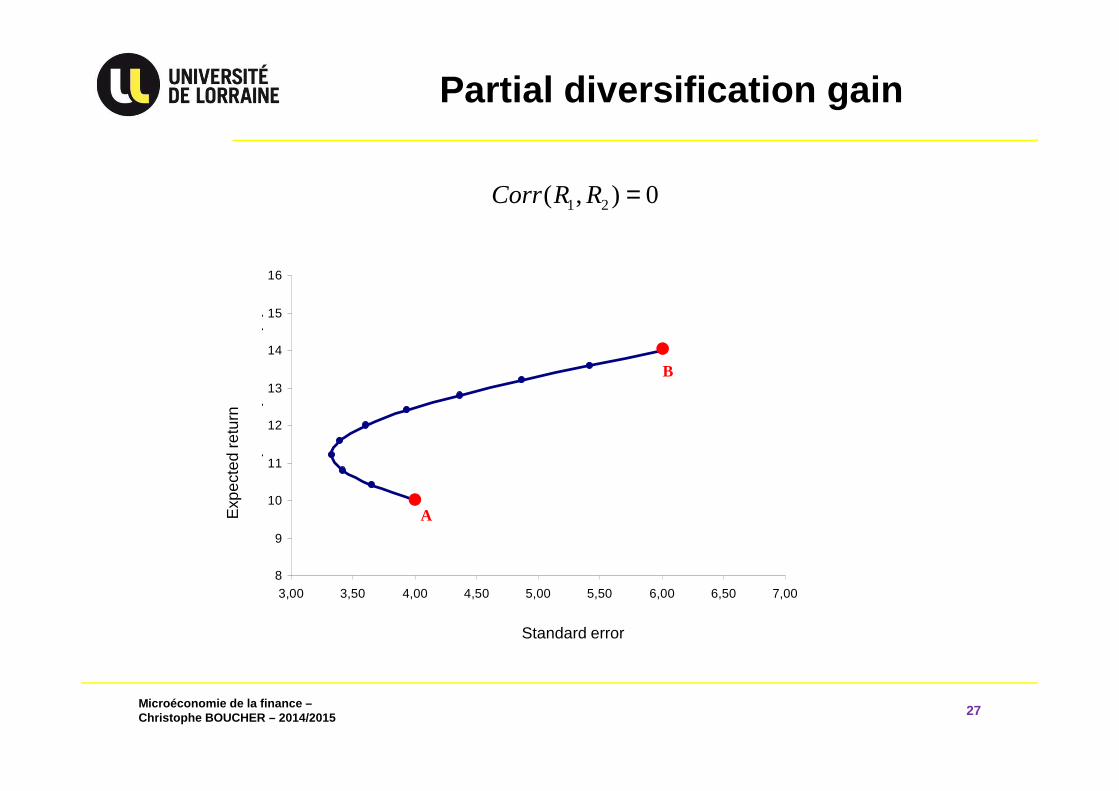

Partial diversification gain

27

1 2( , ) 0Corr R R =E

xpec

ted

retu

rn

Standard error

8

9

10

11

12

13

14

15

16

3,00 3,50 4,00 4,50 5,00 5,50 6,00 6,50 7,00

Ren

dem

ent e

spér

é du

por

tefe

uille

(%

)

A

B

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

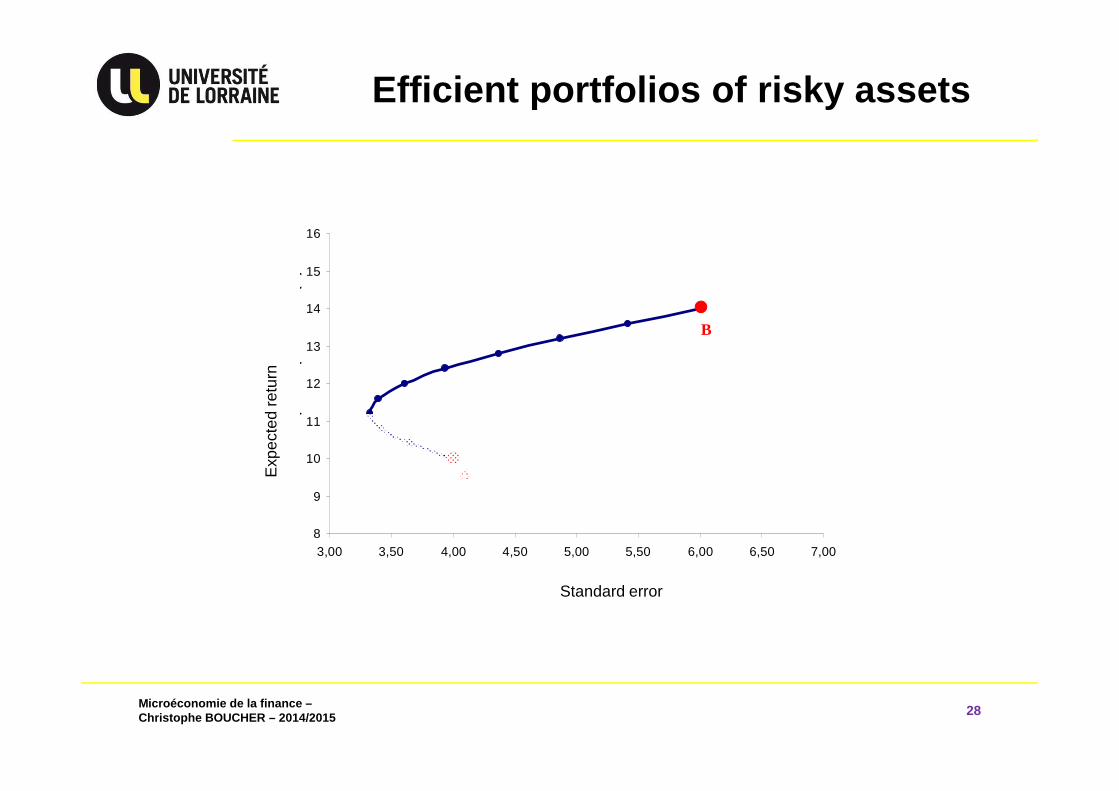

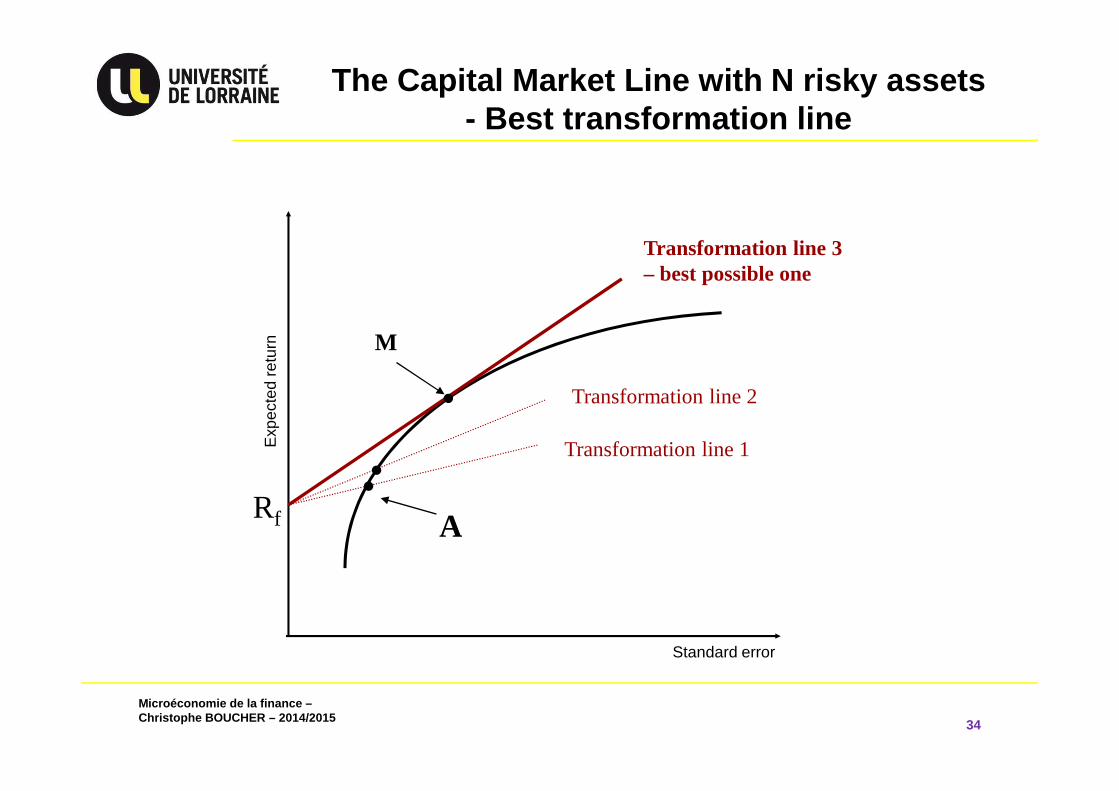

Efficient portfolios of risky assets

28

Exp

ecte

d re

turn

Standard error

8

9

10

11

12

13

14

15

16

3,00 3,50 4,00 4,50 5,00 5,50 6,00 6,50 7,00

Ren

dem

ent e

spér

é du

por

tefe

uille

(%

)

A

B

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

4.3 Introducing a Risk Free Asset and the Tobin’s Separation Theorem

29

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Introducing borrowing and lending:Risk free asset

30

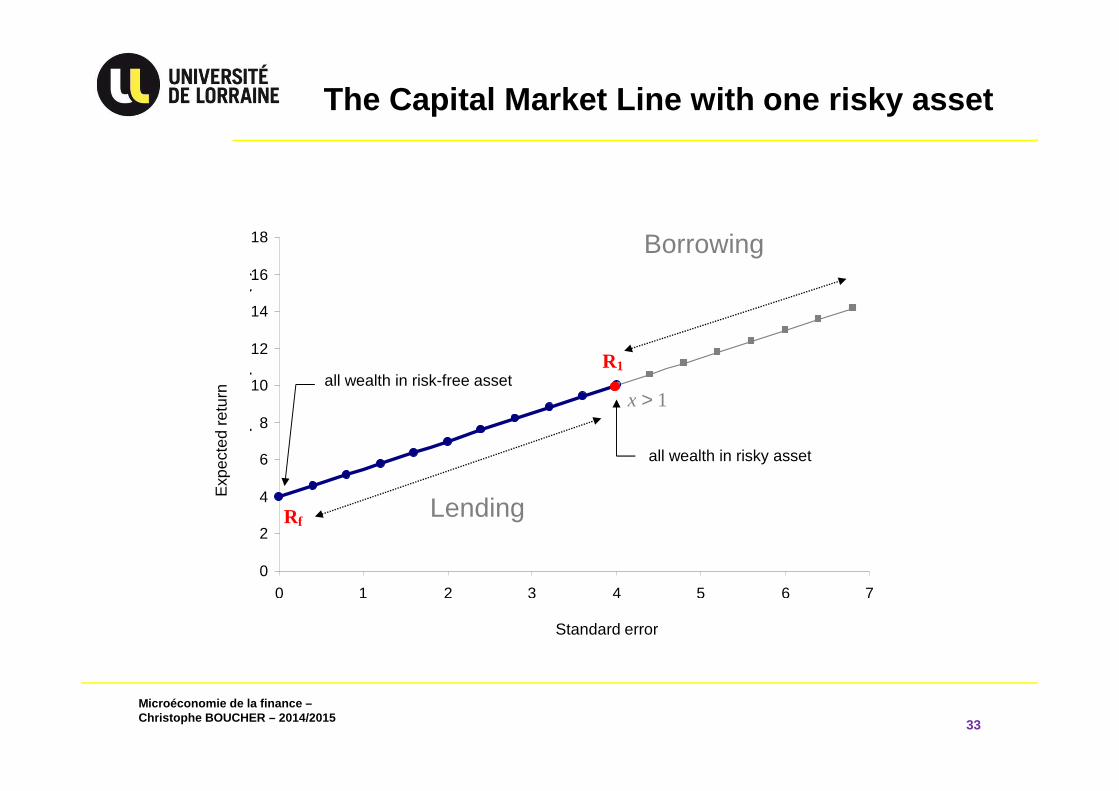

• You are now allowed to borrow and lend at the risk free rate Rf while still investing in any SINGLE ‘risky bundle’ on the efficient frontier.

• For each SINGLE risky bundle, this gives a new set of risk return combination known as the ‘transformation line’.

• The risk-return combination is a straight line (for each single risky bundle) - transformation line.

• You can be anywhere you like on this line.

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

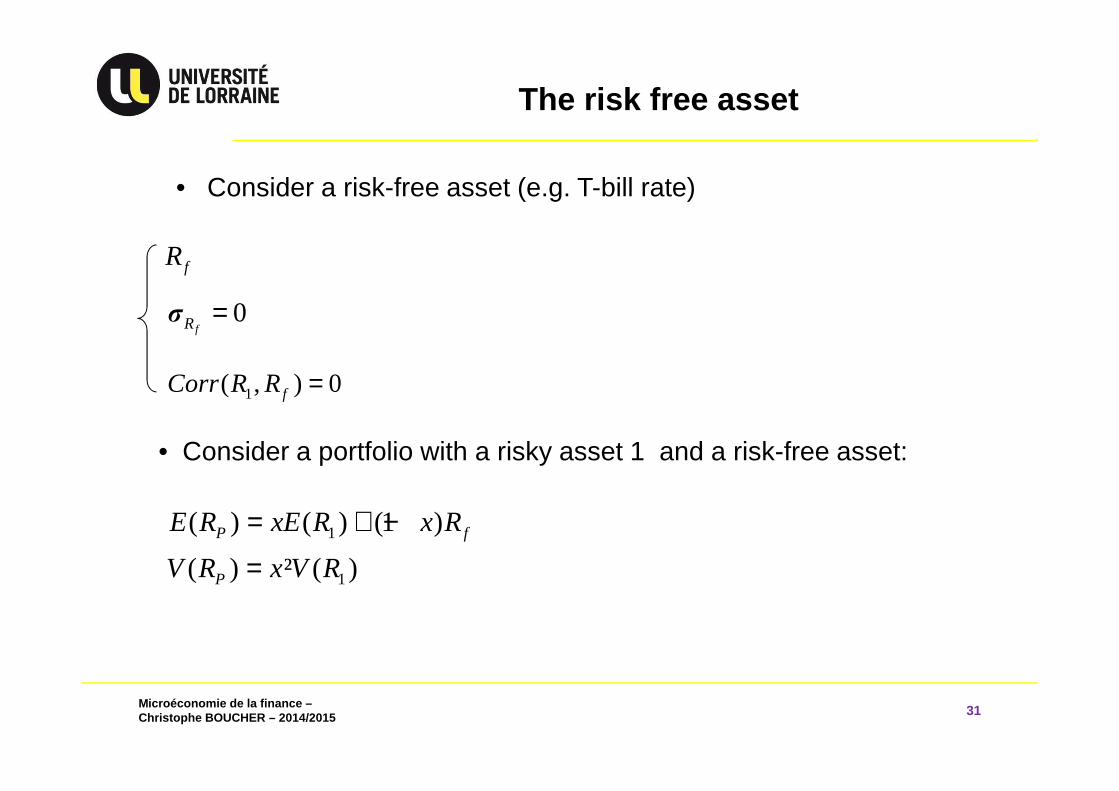

The risk free asset

31

• Consider a risk-free asset (e.g. T-bill rate)

fR

0fRσ =

1( , ) 0fCorr R R =

• Consider a portfolio with a risky asset 1 and a risk-free asset:

1

1

( ) ( ) (1 )

( ) ² ( )P f

P

E R xE R x R

V R x V R

= + −

=

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

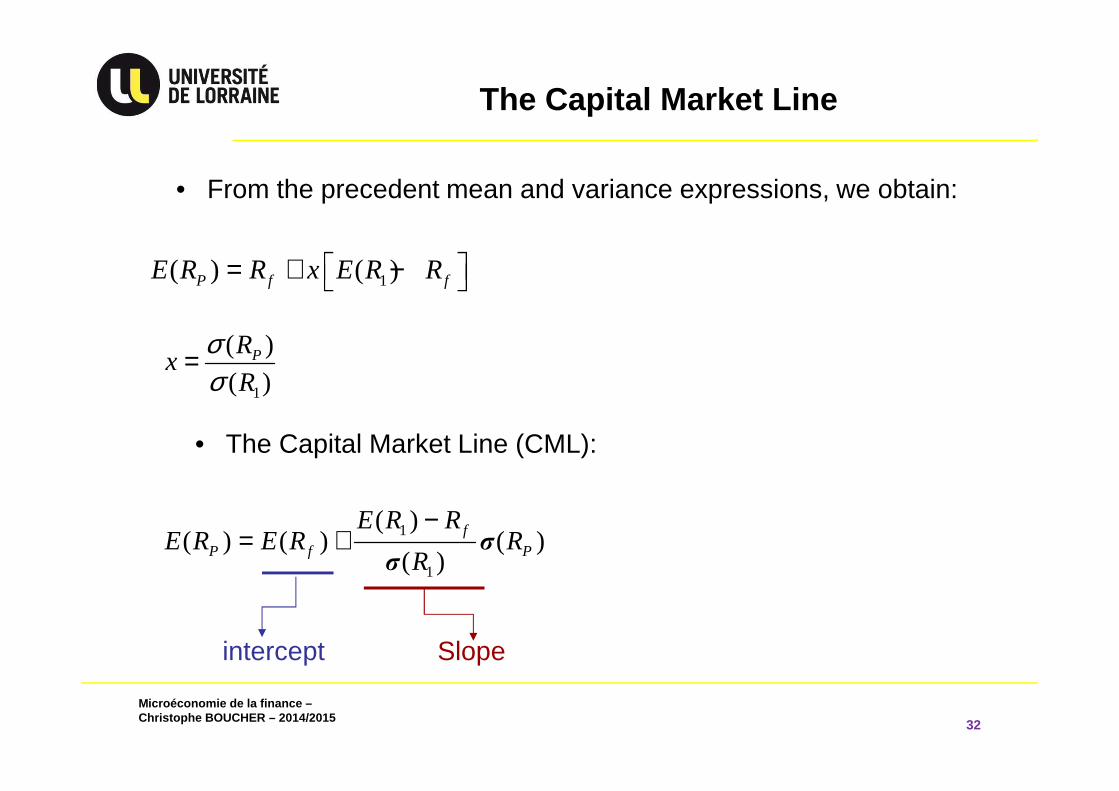

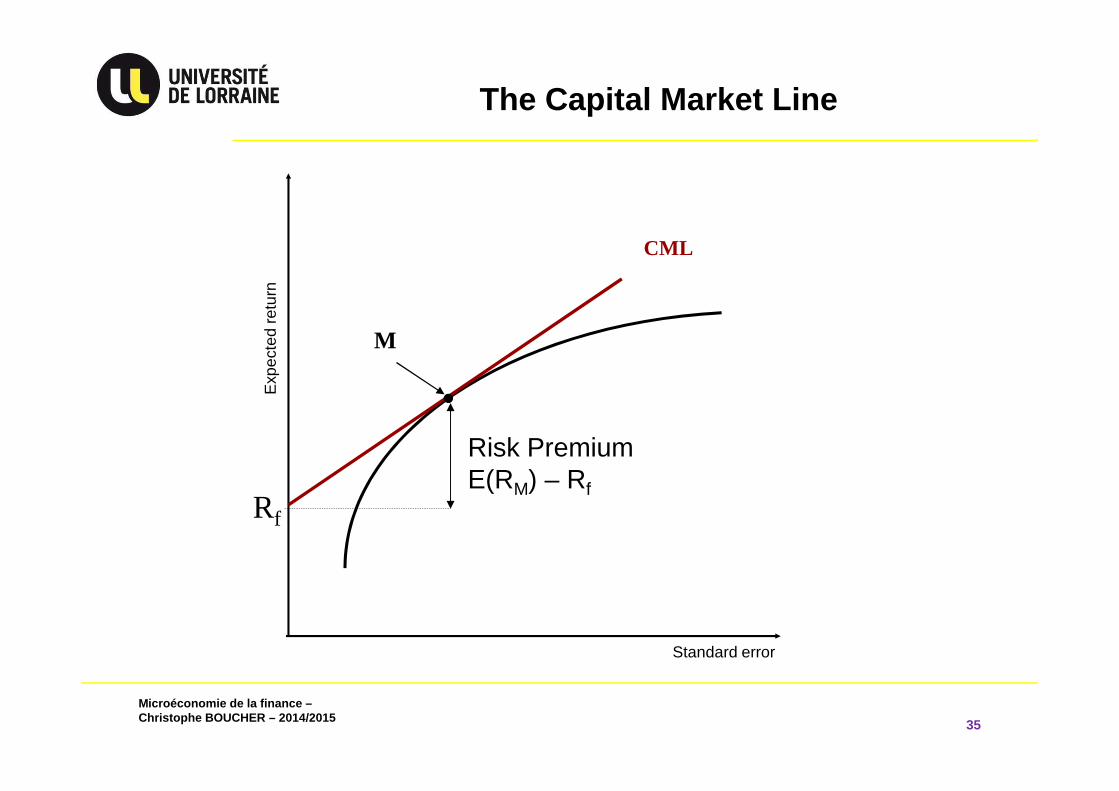

The Capital Market Line

32

• From the precedent mean and variance expressions, we obtain:

1( ) ( )P f fE R R x E R R = + −

1

( )

( )PR

xR

σσ

=

• The Capital Market Line (CML):

1

1

( )( ) ( ) ( )

( )f

P f P

E R RE R E R R

R

−= + σ

σ

Slopeintercept

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

The Capital Market Line with one risky asset

33

0

2

4

6

8

10

12

14

16

18

0 1 2 3 4 5 6 7

Ren

dem

ent e

spér

é du

por

tefe

uille

(%

)

R1

Rf

x > 1

all wealth in risky asset

Exp

ecte

d re

turn

Standard error

all wealth in risk-free asset

Lending

Borrowing

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

The Capital Market Line with N risky assets- Best transformation line

34

Exp

ecte

d re

turn

Standard error

Transformation line 1

Transformation line 2

Transformation line 3 – best possible one

Rf A

M

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

The Capital Market Line

35

Exp

ecte

d re

turn

Standard error

CML

Rf

M

Risk PremiumE(RM) – Rf

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

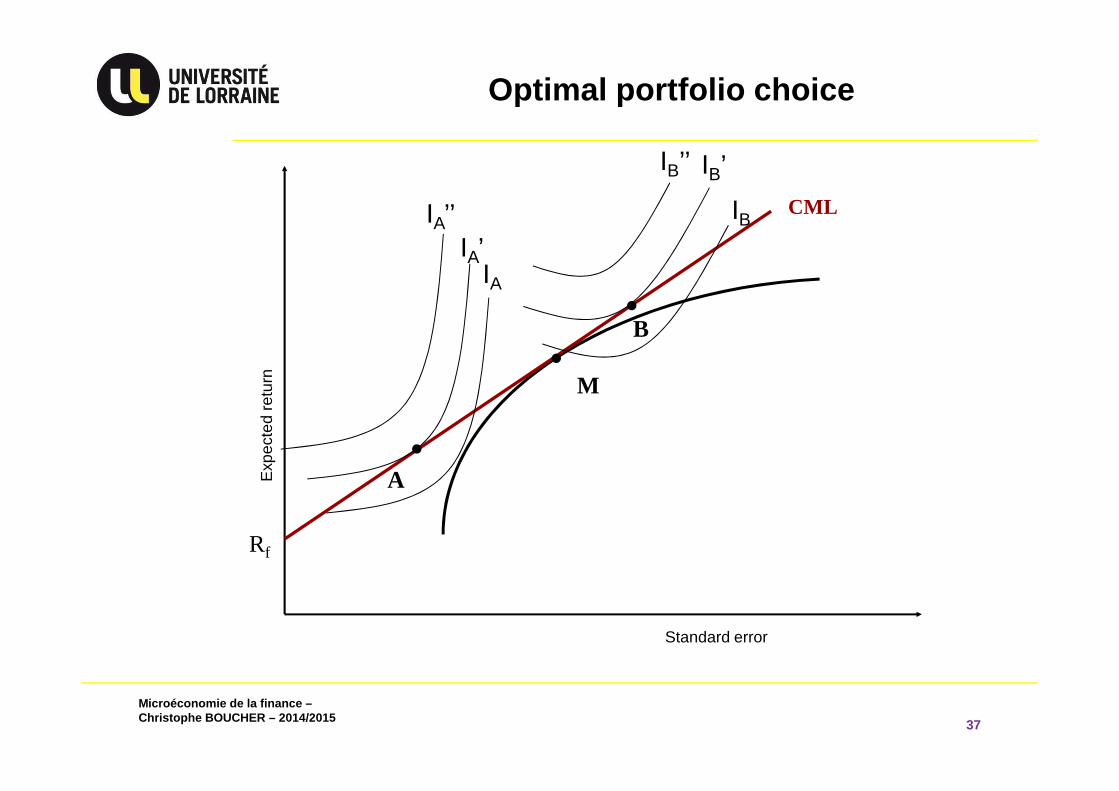

The CML and the separation theorem

36

• The CML dominates all other possible portfolios

• An agent invests along the CML (where ? ⇒ risk preferences)

• James Tobin’s separation theorem:

- Invest in a risky portfolio (optimal combination of risky securities)

- Borrow-lend at the risk-free rate

• Depending on your attitude toward risk: how much lend or borrow

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Optimal portfolio choice

37

Exp

ecte

d re

turn

CML

Rf

M

Standard error

A

B

IA’IA’’ IB

IA

IB’’ IB’

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

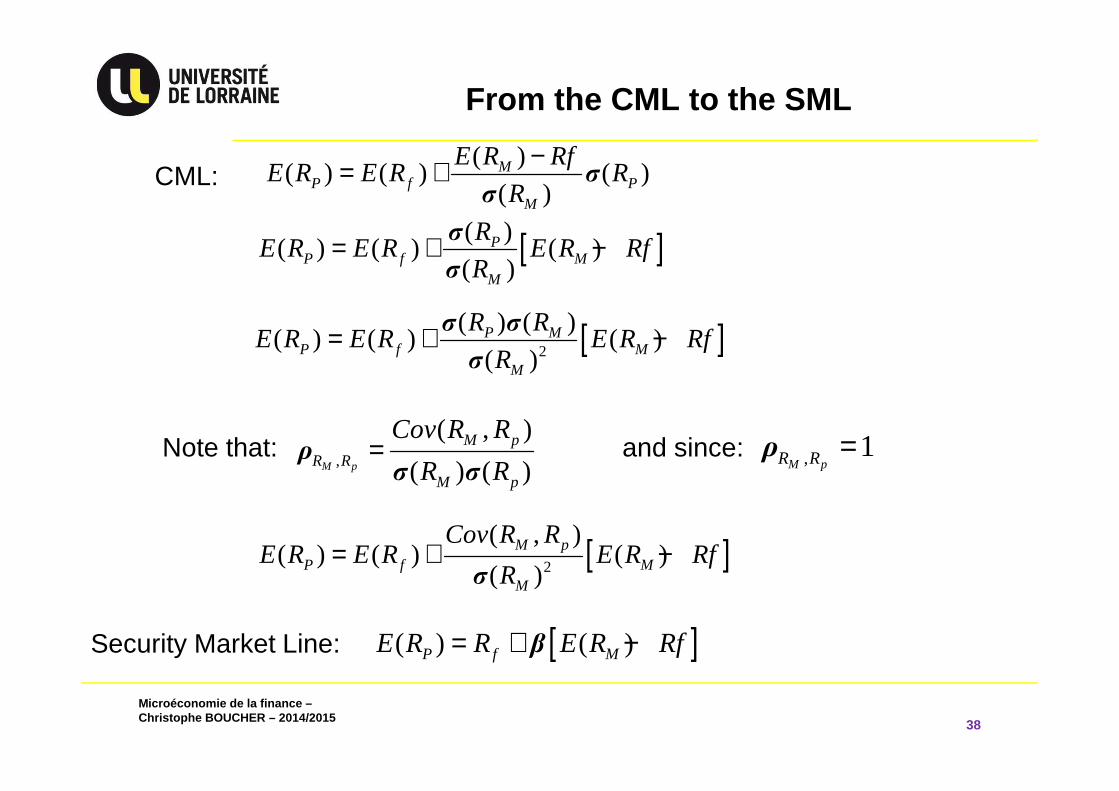

From the CML to the SML

38

( )( ) ( ) ( )

( )M

P f PM

E R RfE R E R R

R

−= + σσ

CML:

[ ]( )( ) ( ) ( )

( )P

P f MM

RE R E R E R Rf

R= + −σ

σ

Note that:,

( , )

( ) ( )M p

M pR R

M p

Cov R R

R R=ρσ σ

and since: , 1M pR R =ρ

[ ]2

( ) ( )( ) ( ) ( )

( )P M

P f MM

R RE R E R E R Rf

R= + −σ σ

σ

[ ]2

( , )( ) ( ) ( )

( )M p

P f MM

Cov R RE R E R E R Rf

R= + −

σ

Security Market Line: [ ]( ) ( )P f ME R R E R Rf= + −β

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

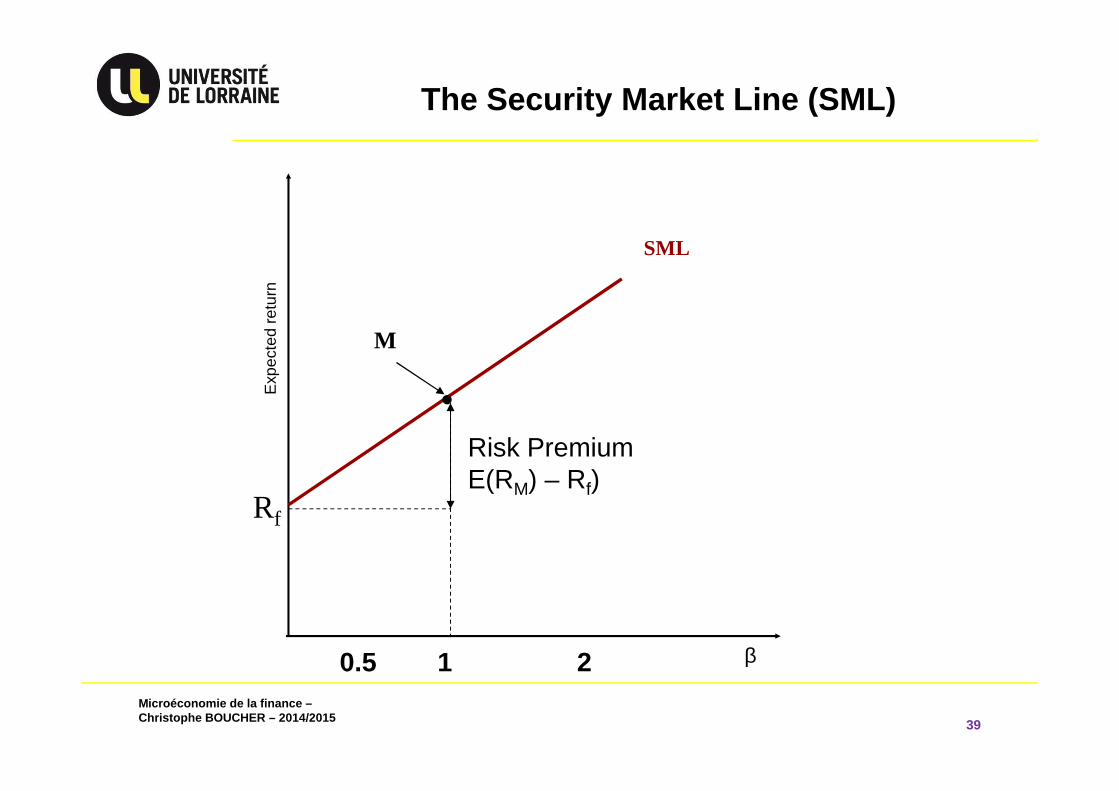

The Security Market Line (SML)

39

Exp

ecte

d re

turn

SML

Rf

M

β10.5 2

Risk PremiumE(RM) – Rf)

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

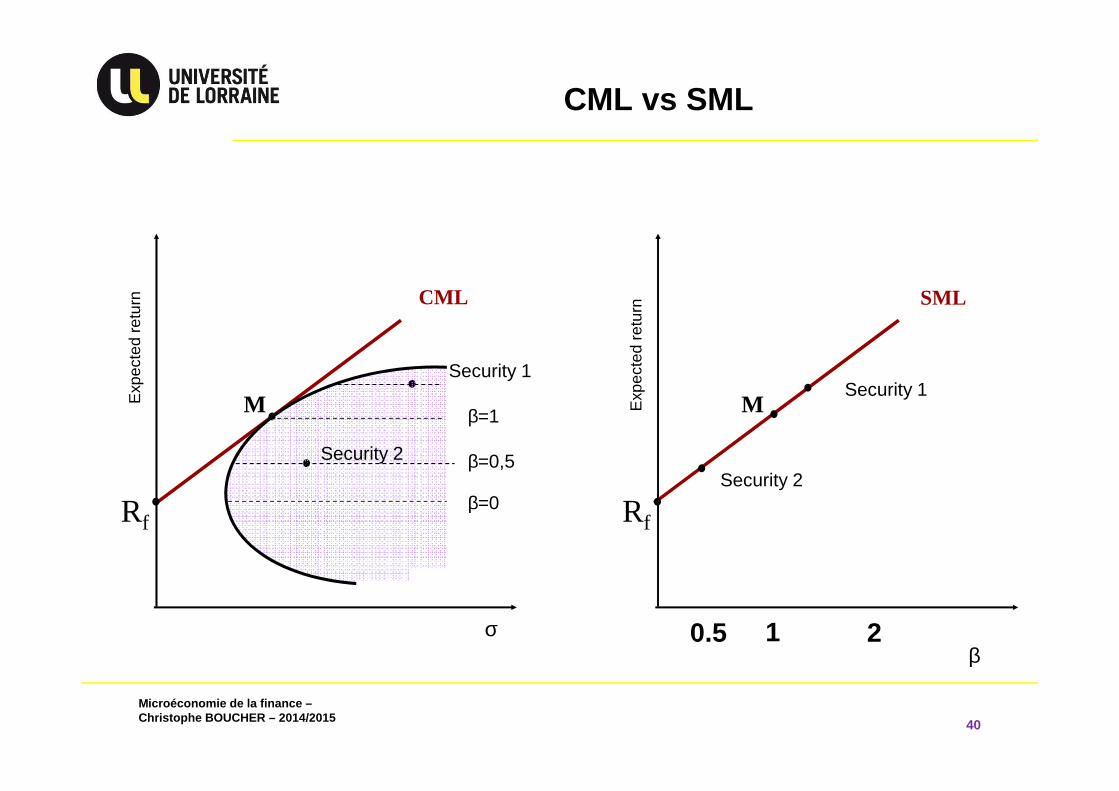

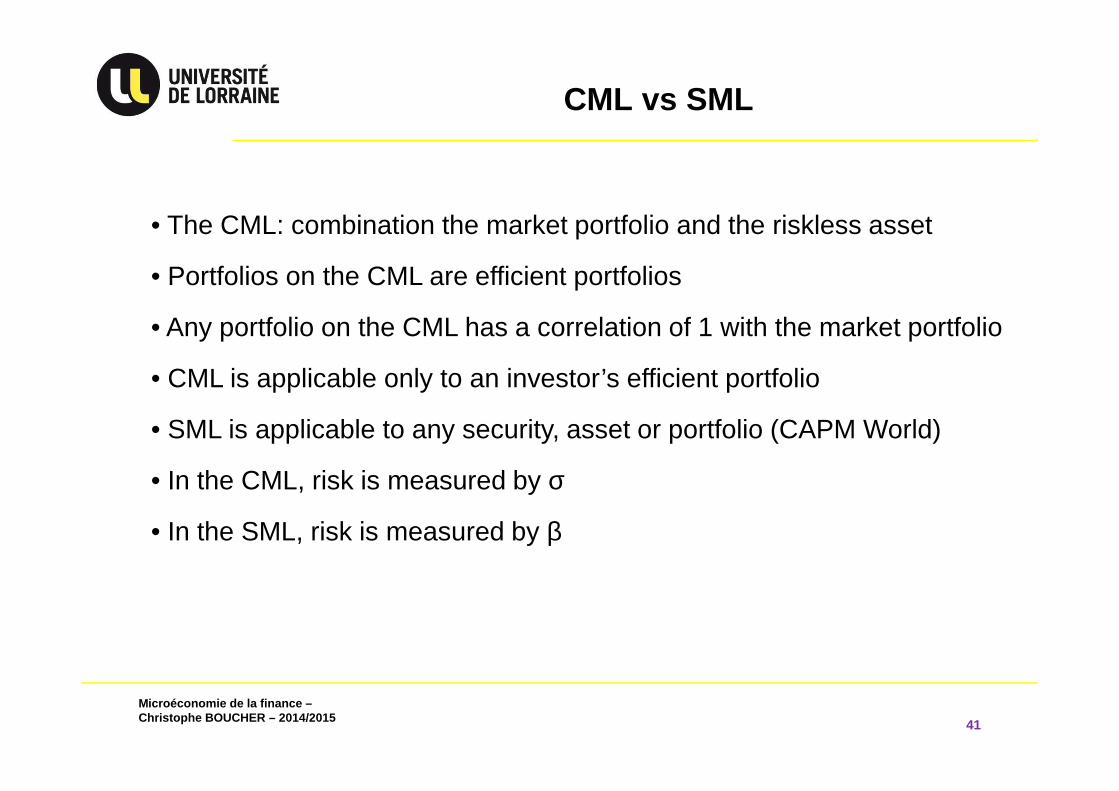

CML vs SML

40

βE

xpec

ted

retu

rn SML

Rf

M

10.5 2

Security 1

Security 2

σ

Exp

ecte

d re

turn CML

Rf

M

Security 2

Security 1

β=0

β=0,5

β=1

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

CML vs SML

41

• The CML: combination the market portfolio and the riskless asset

• Portfolios on the CML are efficient portfolios

• Any portfolio on the CML has a correlation of 1 with the market portfolio

• CML is applicable only to an investor’s efficient portfolio

• SML is applicable to any security, asset or portfolio (CAPM World)

• In the CML, risk is measured by σ

• In the SML, risk is measured by β

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

4.4 Asset Allocation with N risky Assets

42

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

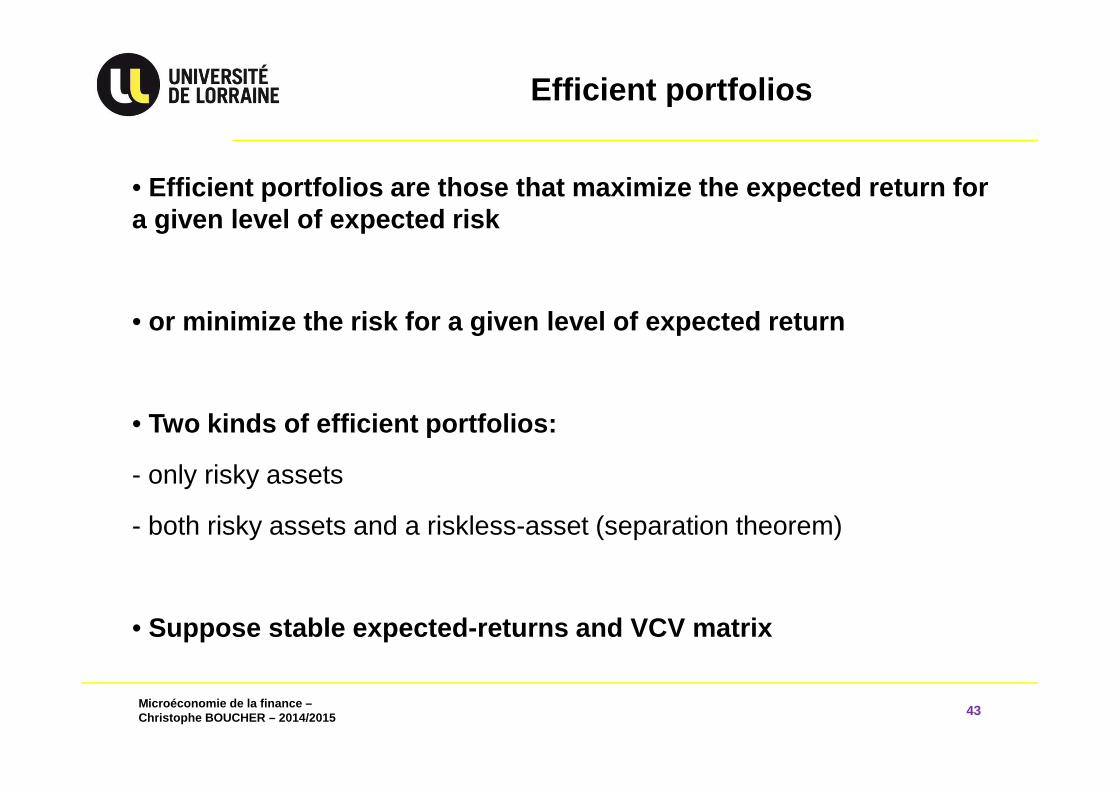

Efficient portfolios

43

• Efficient portfolios are those that maximize the ex pected return for a given level of expected risk

• or minimize the risk for a given level of expected return

• Two kinds of efficient portfolios:

- only risky assets

- both risky assets and a riskless-asset (separation theorem)

• Suppose stable expected-returns and VCV matrix

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

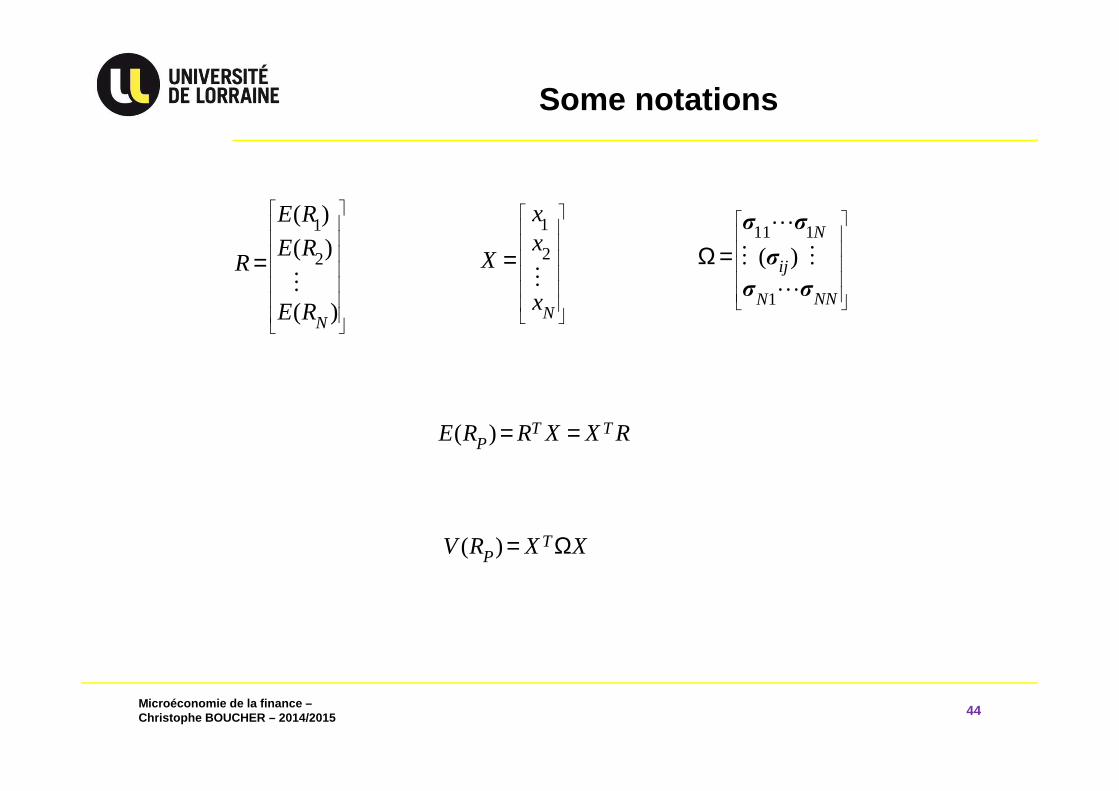

Some notations

44

1

2

( )

( )

( )N

E R

E RR

E R

=⋮

1

2

N

xx

X

x

=⋮

11 1

1

( )N

ij

NNN

Ω =⋯

⋮ ⋮

⋯

σ σ

σ

σ σ

( ) T TPE R R X X R= =

( ) TPV R X X= Ω

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

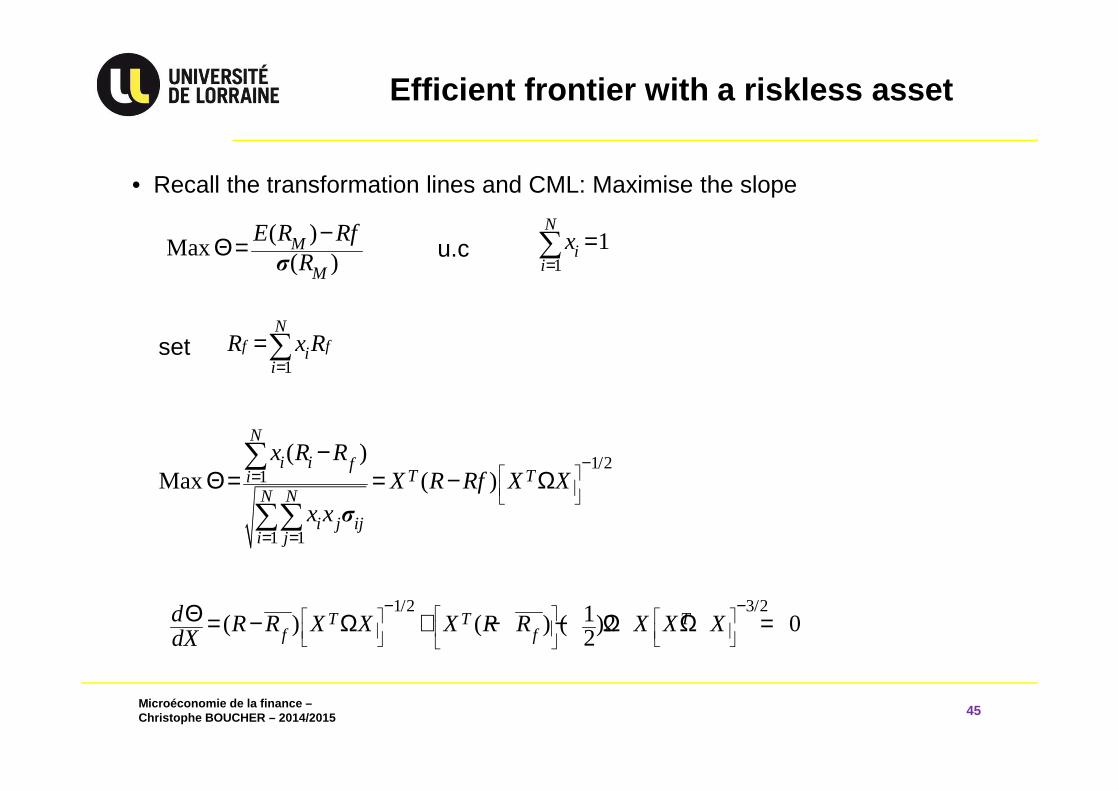

Efficient frontier with a riskless asset

45

( )Max

( )M

M

E R RfR

−Θ =σ

• Recall the transformation lines and CML: Maximise the slope

11

N

ii

x=

=∑u.c

1f f

N

ii

R x R=

=∑set

1/21

1 1

( )Max ( )

N

i i fT Ti

N N

i j iji j

x R RX R Rf X X

x x

−=

= =

−Θ = = − Ω

∑

∑∑ σ

1/2 3/21( ) ( ) ( )2 02

T T Tf f

d R R X X X R R X X XdX

− −Θ = − Ω + − − Ω Ω =

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

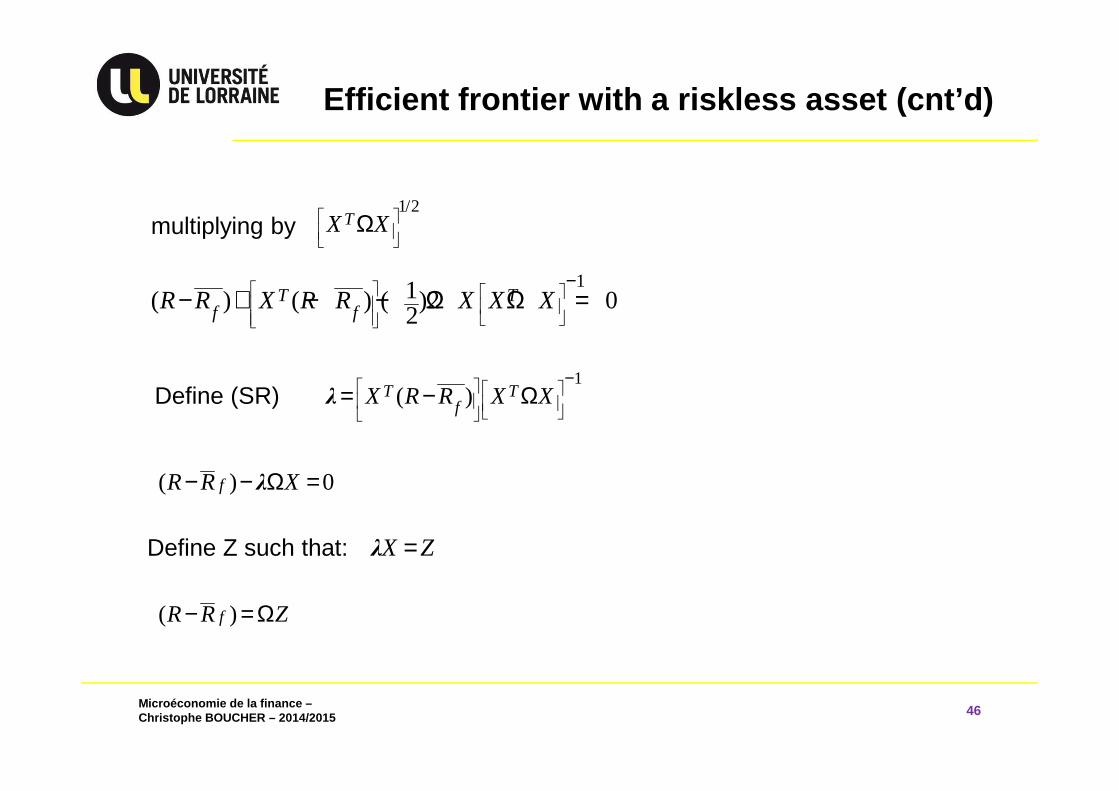

Efficient frontier with a riskless asset (cnt’d)

46

multiplying by1/2

TX X

Ω

11( ) ( ) ( )2 02

T Tf fR R X R R X X X

−− + − − Ω Ω =

1( )T T

fX R R X X

−= − ΩλDefine (SR)

( ) 0fR R X− − Ω =λ

X Z=λ

( )fR R Z− = Ω

Define Z such that:

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Efficient frontier with a riskless asset (cnt’d)

47

1 1 11 2 12 1

2 1 21 2 22 2

1 1 2 2

...

...

...

N Nf

N Nf

N N NNN Nf

R R Z Z Z

R R Z Z Z

R R Z Z Z

− = + + +− = + + +

− = + + +⋮

σ σ σ

σ σ σ

σ σ σ

1

ii N

ii

ZX

Z=

=∑

Since: 1 1 1

N N N

i i ii i i

X Z Z= = =

= ⇒ =∑ ∑ ∑λ λ

Then we can calculate: ( )ME R ( )MRσand

1

1

( )( ) ( )

( )P Pf

E R RfE R R R

R−= + σ

σand the CML

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

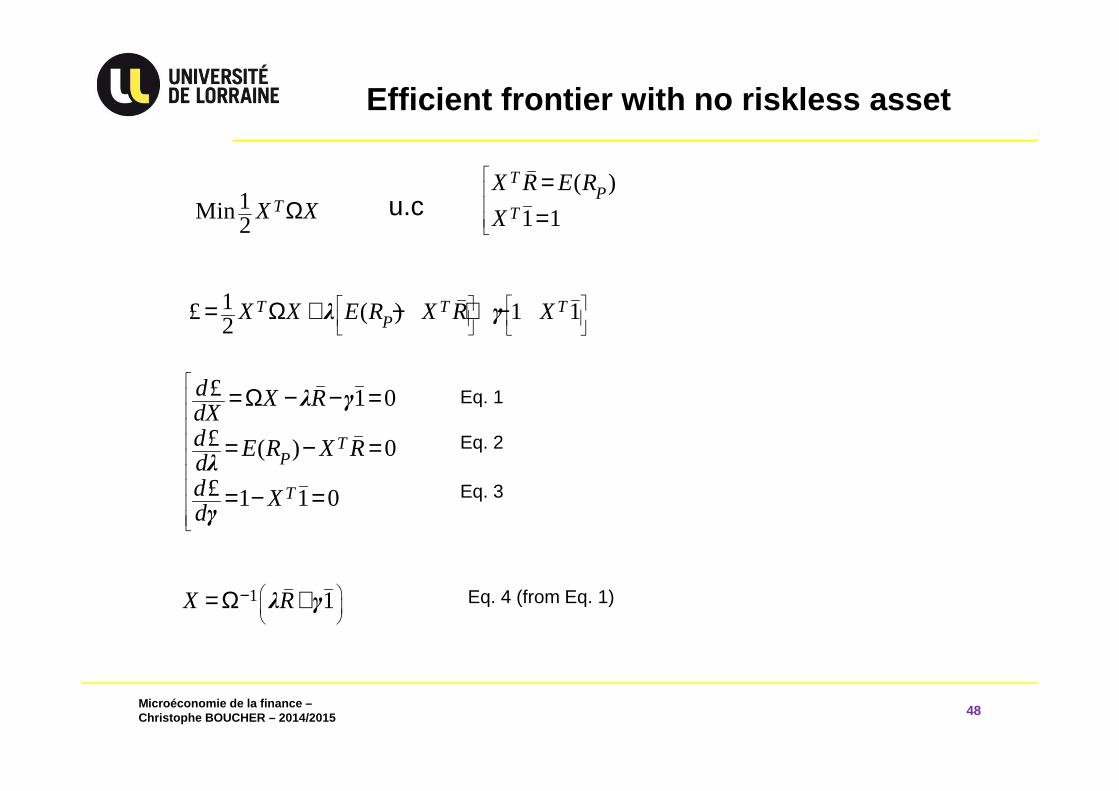

Efficient frontier with no riskless asset

48

1Min2

TX XΩ( )

1 1

TP

T

X R E R

X

==u.c

1£ ( ) 1 12

T T TPX X E R X R X

= Ω + − + −λ γ

£ 1 0

£ ( ) 0

£ 1 1 0

TP

T

d X RdXd E R X Rdd Xd

=Ω − − =

= − =

= − =

λ γ

λ

γ

1 1X R

−= Ω +λ γ

Eq. 1

Eq. 2

Eq. 3

Eq. 4 (from Eq. 1)

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

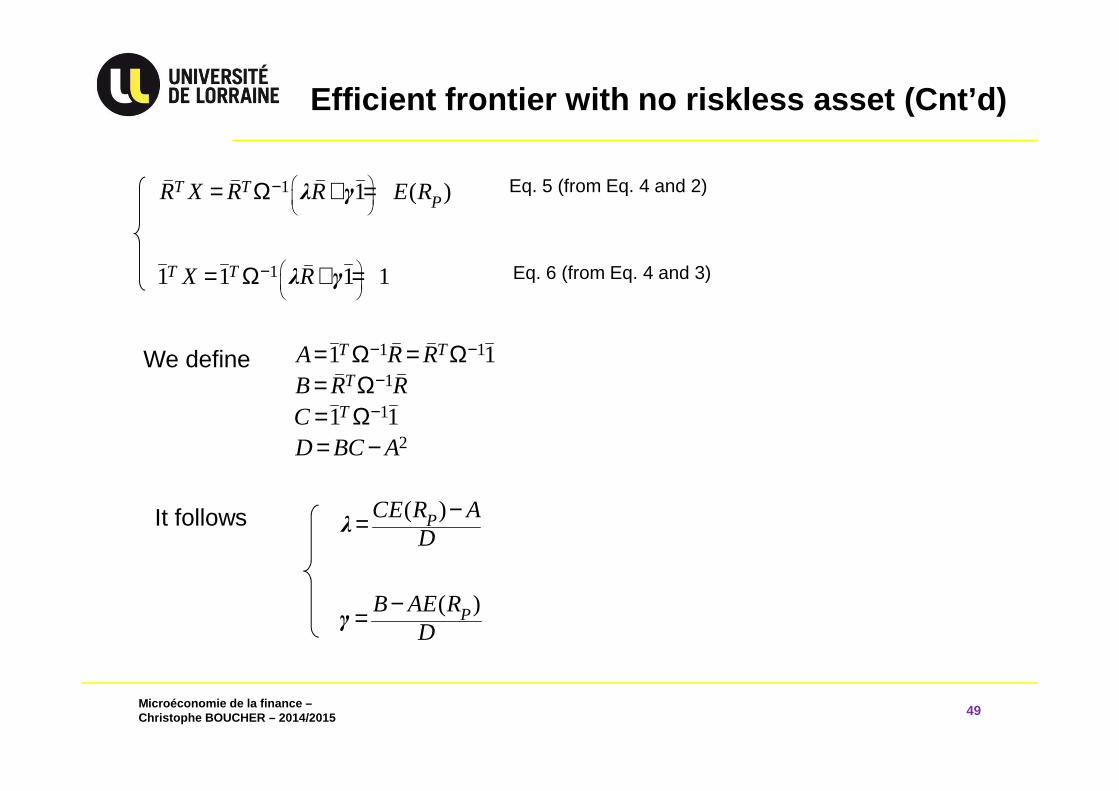

Efficient frontier with no riskless asset (Cnt’d)

49

1 1 ( )T TPR X R R E R

−= Ω + =λ γ

11 1 1 1T TX R

−= Ω + =λ γ

1 1

1

1

2

1 1

1 1

T T

T

T

A R RB R RCD BC A

− −

−

−

= Ω = Ω= Ω= Ω= −

We define

( )PCE R AD

−=λ

( )PB AE RD

−=γ

Eq. 5 (from Eq. 4 and 2)

Eq. 6 (from Eq. 4 and 3)

It follows

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

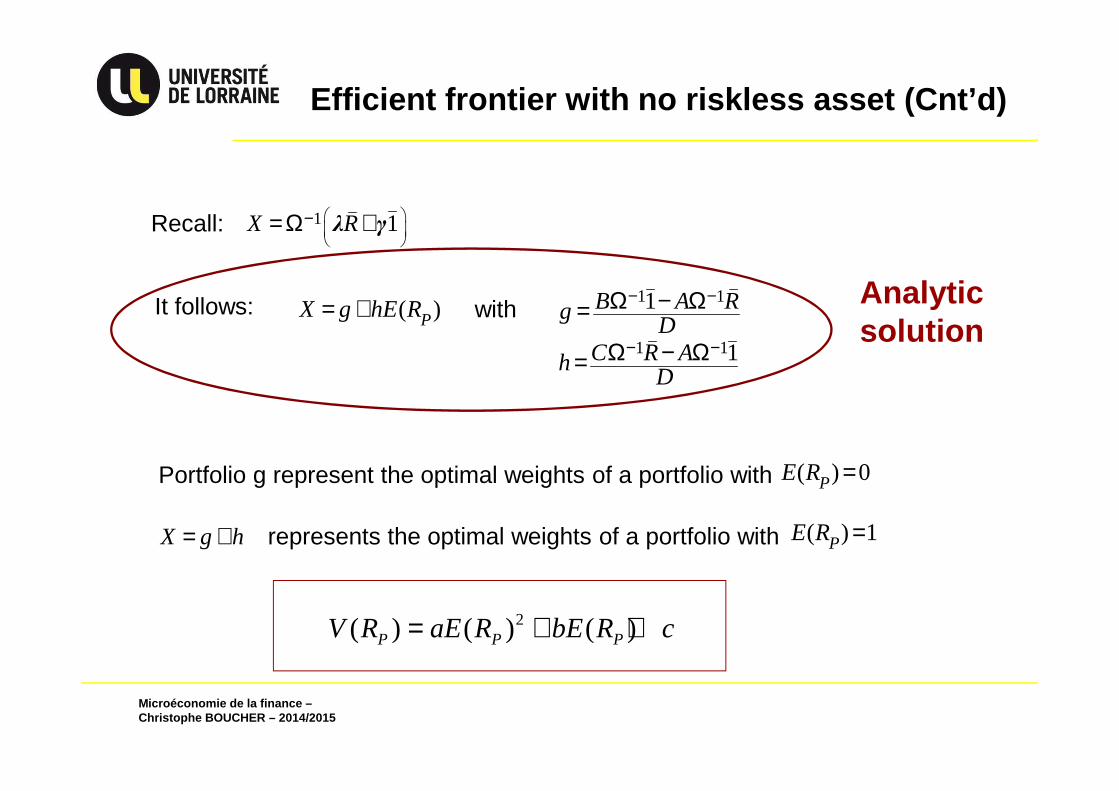

Efficient frontier with no riskless asset (Cnt’d)

Recall: 1 1X R

−= Ω +λ γ

( )PX g hE R= + 1 1

1 1

1

1

B A RgD

C R AhD

− −

− −

Ω − Ω=

Ω − Ω=

with

Portfolio g represent the optimal weights of a portfolio with ( ) 0PE R =

X g h= + represents the optimal weights of a portfolio with ( ) 1PE R =

2( ) ( ) ( )P P PV R aE R bE R c= + +

It follows: Analytic solution

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

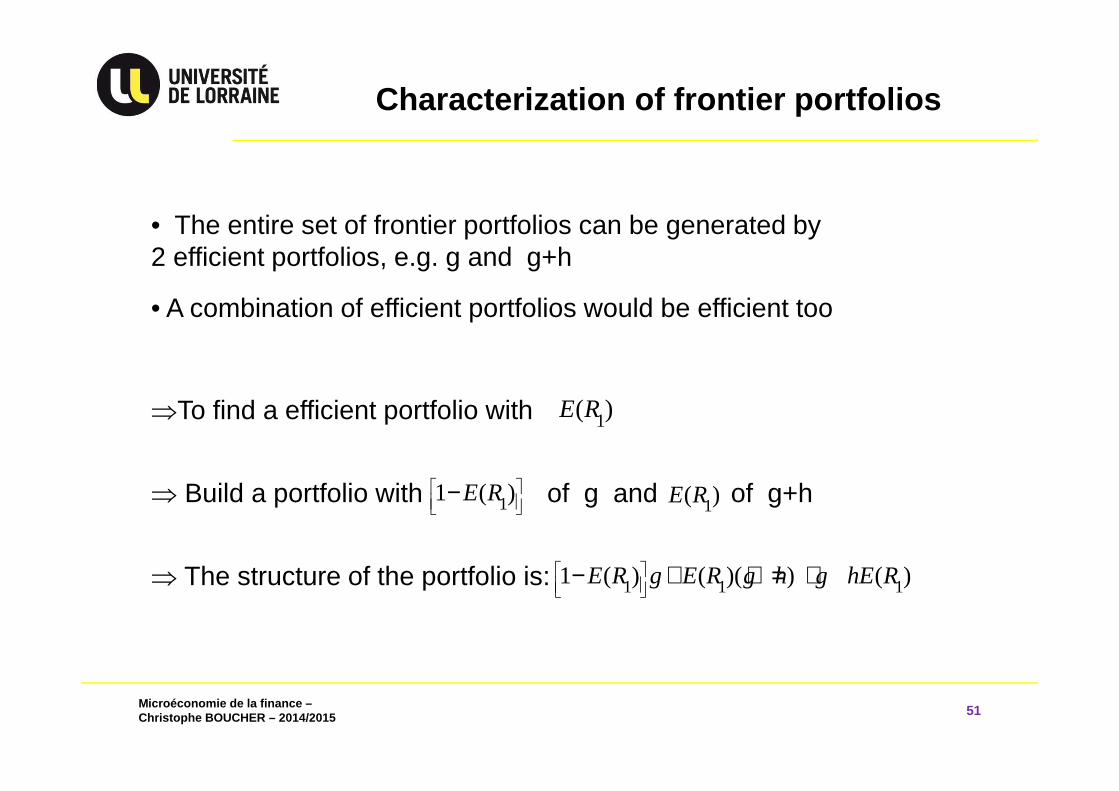

Characterization of frontier portfolios

51

• The entire set of frontier portfolios can be generated by 2 efficient portfolios, e.g. g and g+h

• A combination of efficient portfolios would be efficient too

⇒To find a efficient portfolio with

⇒ Build a portfolio with of g and of g+h

⇒ The structure of the portfolio is:

1( )E R

11 ( )E R

−1( )E R

1 1 11 ( ) ( )( ) ( )E R g E R g h g hE R

− + + = +

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

3.5 Portfolio Diversification

52

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

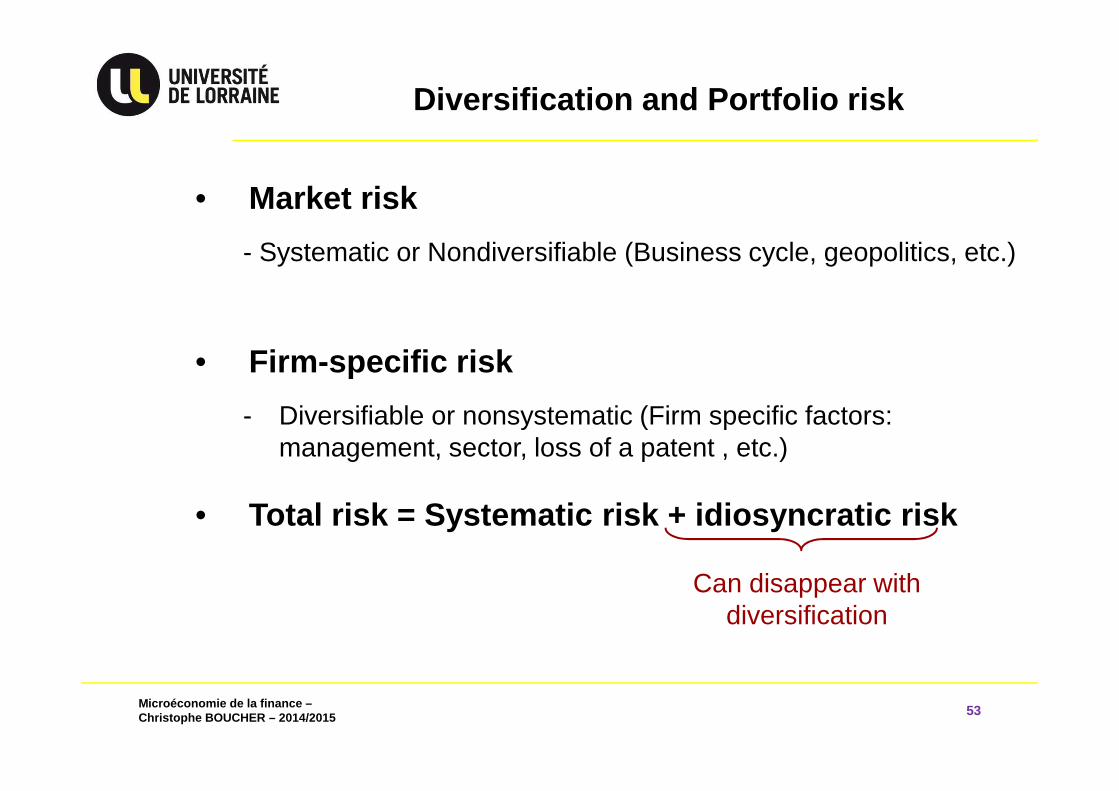

Diversification and Portfolio risk

53

• Market risk

- Systematic or Nondiversifiable (Business cycle, geopolitics, etc.)

• Firm -specific risk

- Diversifiable or nonsystematic (Firm specific factors: management, sector, loss of a patent , etc.)

• Total risk = Systematic risk + idiosyncratic risk

Can disappear with diversification

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

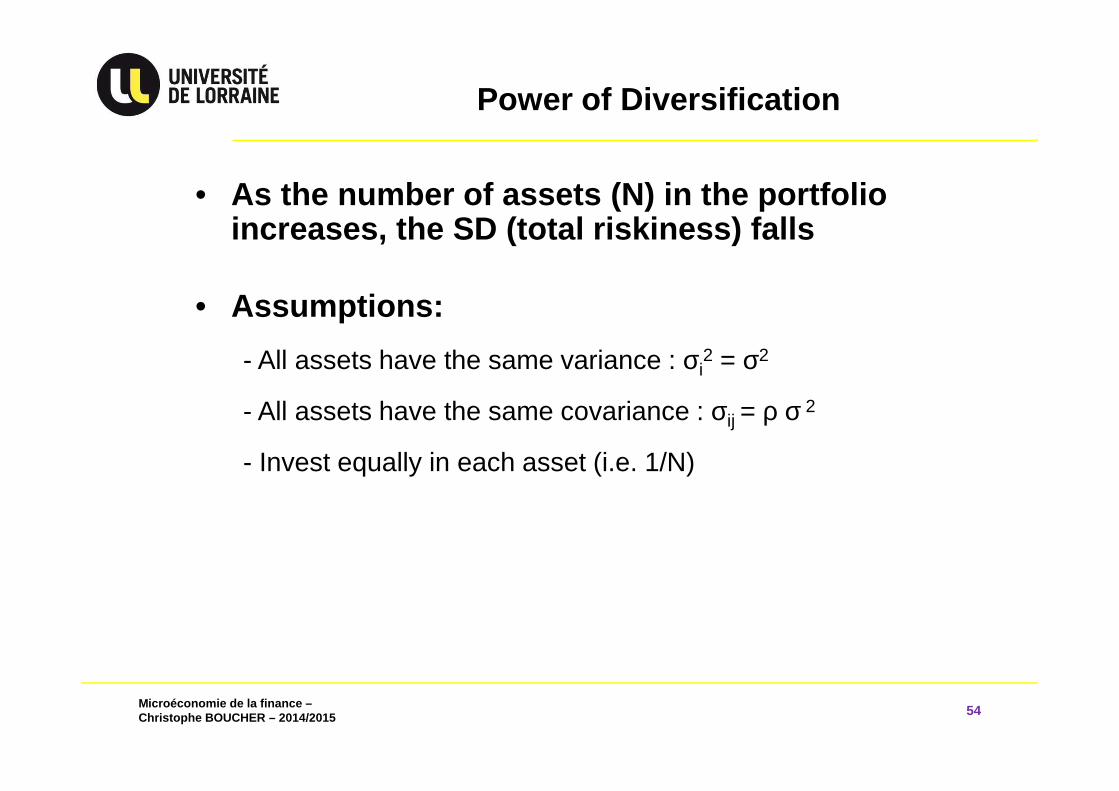

Power of Diversification

54

• As the number of assets (N) in the portfolio increases, the SD (total riskiness) falls

• Assumptions:

- All assets have the same variance : σi2 = σ2

- All assets have the same covariance : σij = ρ σ 2

- Invest equally in each asset (i.e. 1/N)

Microéconomie de la finance –Christophe BOUCHER – 2014/2015

Power of Diversification

55

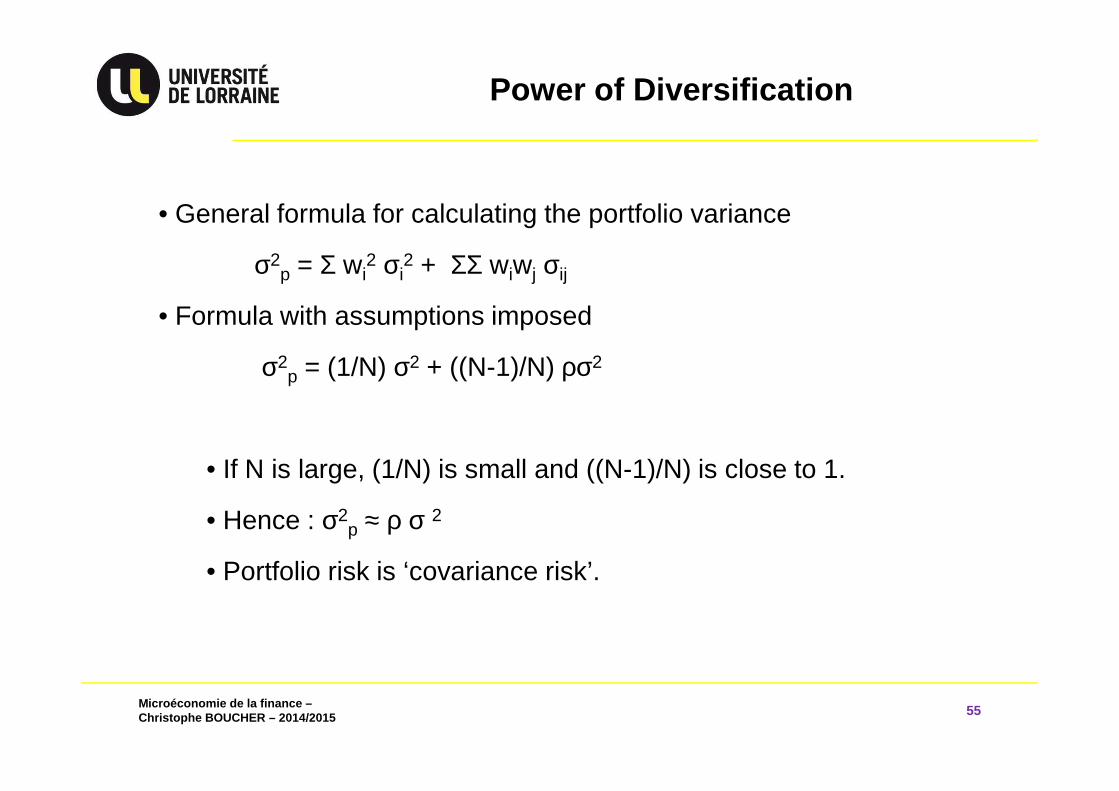

• General formula for calculating the portfolio variance

σ2p = Σ wi

2 σi2 + ΣΣ wiwj σij

• Formula with assumptions imposed

σ2p = (1/N) σ2 + ((N-1)/N) ρσ2

• If N is large, (1/N) is small and ((N-1)/N) is close to 1.

• Hence : σ2p ≈ ρ σ 2

• Portfolio risk is ‘covariance risk’.

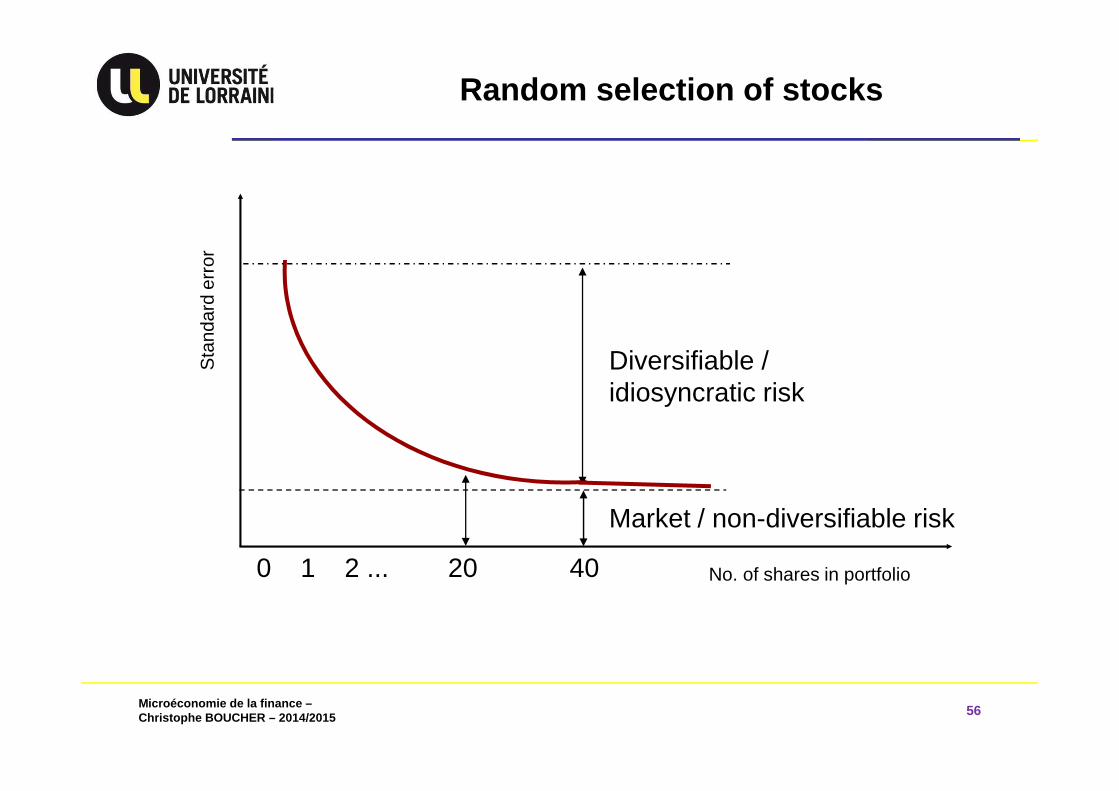

Microéconomie de la finance –Christophe BOUCHER – 2014/2015 56

Sta

ndar

d er

ror

No. of shares in portfolio

Diversifiable / idiosyncratic risk

Market / non-diversifiable risk

20 400 1 2 ...

Random selection of stocks

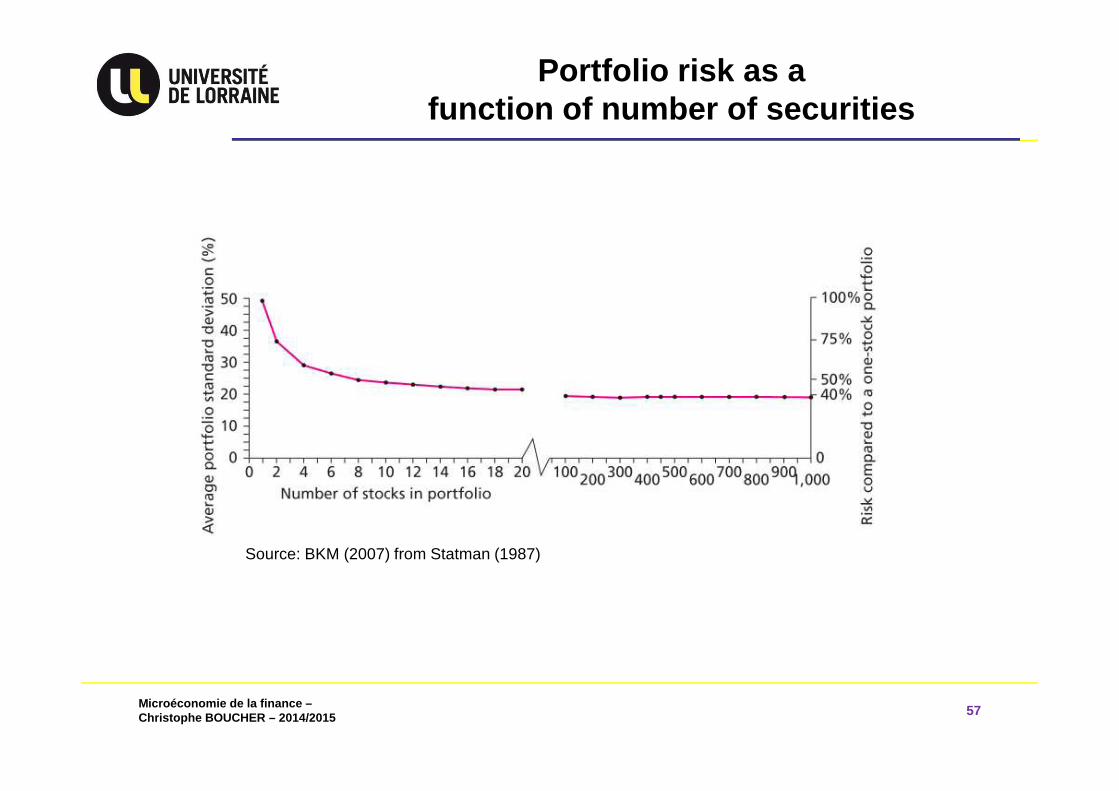

Microéconomie de la finance –Christophe BOUCHER – 2014/2015 57

Portfolio risk as a function of number of securities

Source: BKM (2007) from Statman (1987)

Microéconomie de la finance –Christophe BOUCHER – 2014/2015 58

Thank you for your attention…

See you next week