michael clarfeld, clearbridge investments kevin mccarthy ... · michael clarfeld, clearbridge...

TRANSCRIPT

Is the MLP Model Broken?

Michael Clarfeld, Clearbridge Investments

Kevin McCarthy, Kayne Anderson Fund Advisors

Ed Russell, Tortoise Capital Advisors

©2016 Tortoise Capital Advisors, L.L.C. MLP Asset Manager Panel Discussion | June 2, 2016

Tortoise MLP Index®

MLP YTD total return performance

Source: Bloomberg as of 5/31/2016.

Price return Total return12/31/2015 - 2/11/2015 -31.6% -29.9%2/11/2016 - 5/31/2016 52.9% 56.2%YTD 4.6% 9.5%

-30% +56%

600

650

700

750

800

850

900

950

1000

12/31/2015 1/31/2016 2/29/2016 3/31/2016 4/30/2016 5/31/2016

Closed-end funds Exchange traded products Open-end funds

MLP fund net flows by quarter (2010-present)

Source: US Capital as of 4/30/2016.

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Mar

-10

Jun-

10

Sep

-10

Dec

-10

Mar

-11

Jun-

11

Sep

-11

Dec

-11

Mar

-12

Jun-

12

Sep

-12

Dec

-12

Mar

-13

Jun-

13

Sep

-13

Dec

-13

Mar

-14

Jun-

14

Sep

-14

Dec

-14

Mar

-15

Jun-

15

Sep

-15

Dec

-15

Apr

-16

Cap

ital i

nflo

ws

($ in

mill

ions

)

Exchange traded products Open-end funds

YTD MLP fund net flows by month

Source: US Capital as of 4/30/2016.

-200

0

200

400

600

800

1,000

Jan-16 Feb-16 Mar-16 Apr-16

Cap

ital i

nflo

ws

($ in

mill

ions

)

1

For institutional investors only.

Not for distribution to the general public.

Confidential and proprietary information.

For institutional investors only.

Not for distribution to the general public.

Confidential and proprietary information.

Simplification Transactions:

What’s Old is New Again

Michael Clarfeld, CFA

Managing Director, Portfolio Manager

June 2, 2016

2

For institutional investors only.

Not for distribution to the general public.

Confidential and proprietary information.

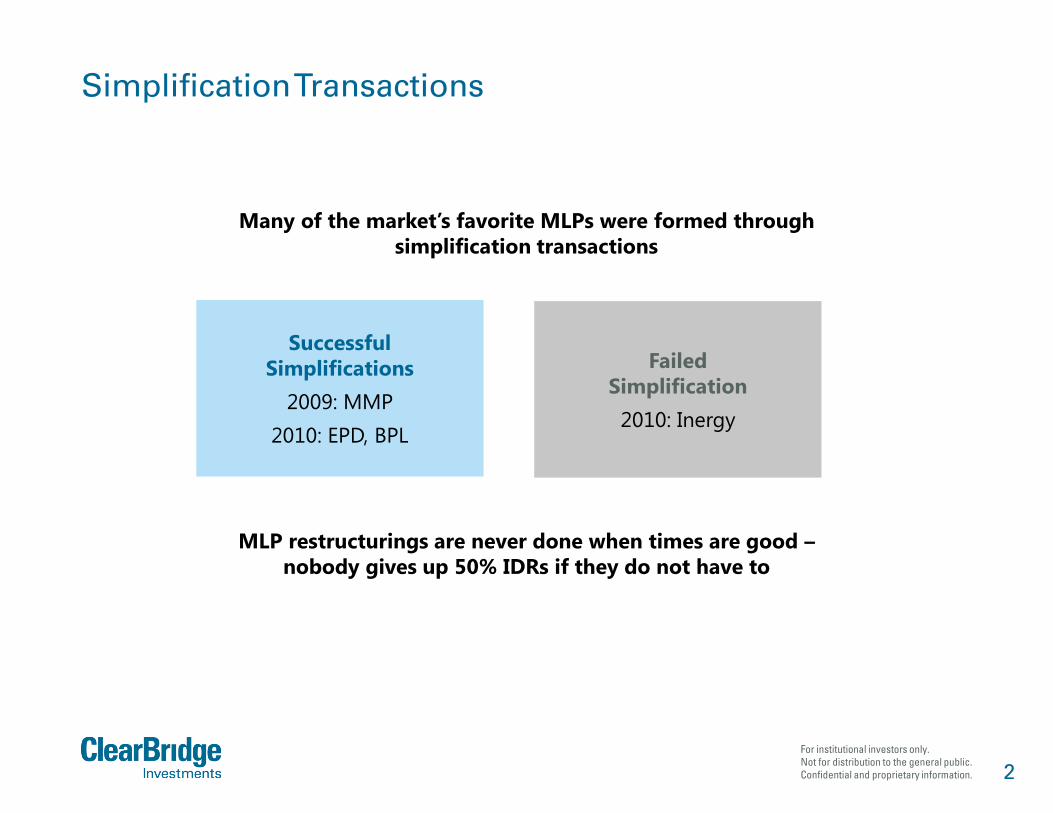

Simplification Transactions

MLP restructurings are never done when times are good –

nobody gives up 50% IDRs if they do not have to

Successful

Simplifications

2009: MMP

2010: EPD, BPL

Failed

Simplification

2010: Inergy

Many of the market’s favorite MLPs were formed through

simplification transactions

3

For institutional investors only.

Not for distribution to the general public.

Confidential and proprietary information.

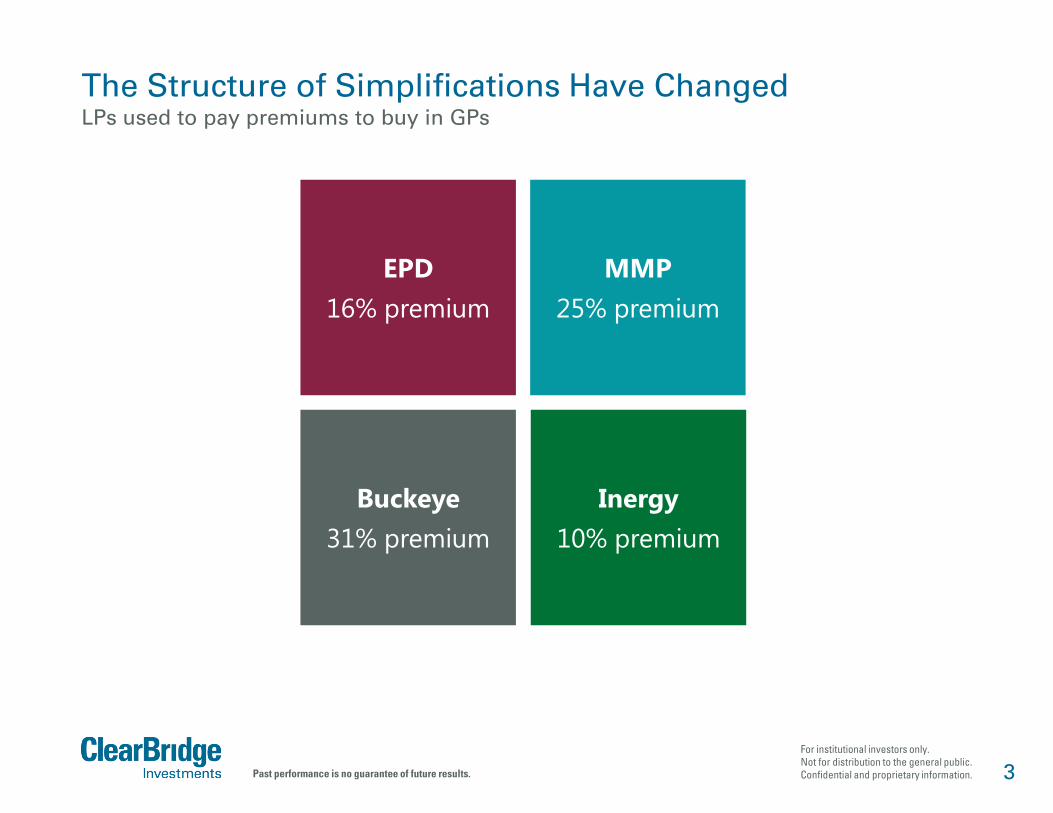

The Structure of Simplifications Have Changed LPs used to pay premiums to buy in GPs

EPD

16% premium

MMP

25% premium

Buckeye

31% premium

Inergy

10% premium

Past performance is no guarantee of future results.

4

For institutional investors only.

Not for distribution to the general public.

Confidential and proprietary information.

Lately GPs Have Been Paying Premiums to Buy in Their LPs

Past performance is no guarantee of future results.

2014

Kinder

11-16%

premium

2015

Crestwood

5%

premium

2016

Targa

18%

premium

5

For institutional investors only.

Not for distribution to the general public.

Confidential and proprietary information.

The GP/LP Model

The GP/LP model is

challenged when:

Growth slows

Cost of equity is high

The GP/LP model

works when:

Growth is strong

Cost of equity is cheap

6

For institutional investors only.

Not for distribution to the general public.

Confidential and proprietary information.

Is the GP/LP Model Broken?

• The model clearly isn’t “broken” – many of the best-performing MLPs are LPs with GP

Source: Bloomberg.

Past performance is no guarantee of future results.

Bottom Line:

The model can work

and work across various lines

of business

(G&P, Long haul pipes,

Refinery logistics)

Overriding Similarities:

Visible Growth

Big Differences:

AM and RMP:

G&Ps for non-IG EPs

CQP: Management issues

Performance

as of April 29, 2016 (%)

Name TTM Relative

to AMZ Index

Valero Energy Partners, LP -3.9 25.0

Phillips 66 Partners, LP -22.3 6.6

Shell Midstream Partners, LP -6.2 2.7

Antero Midstream Partners, LP 4.0 32.9

Rice Midstream Partners, LP 11.6 40.5

Cheniere Energy Partners, LP -3.2 25.7

Spectra Energy Partners, LP -1.5 27.4

Tallgrass Energy Partners, LP -12.2 16.7

7

For institutional investors only.

Not for distribution to the general public.

Confidential and proprietary information.

Conclusion

• GP/LP structure isn’t going away – this is America and the upside to being a successful GP isa powerful incentive

• There will not be a mass move to get rid of or cap IDRs – nobody will give up 50% unlessthey have to

• Simplification transactions are not new – they happen in downcycles

• The “MLP” universe is becoming more diverse

– C-corps like KMI or TRGP

– Unified Partnerships like EPD or MMP

– Classic GP/LP like WGP and WES or TEP and TEGP

• As investment universe changes, MLP products likely to change too (harder to own C-corpMLPs like Kinder and TRGP in C-corp mutual funds and ETFs)

• Payout ratio philosophy may differ by structure

– High payout ratio is a must in GP/LP structure

– High payout ratio may not make sense over the long term in C-corps like KMI, TRGP andPAGP/PAA

Product Development Research led to the following conclusions:

Combinations of different ClearBridge strategies using appropriate

reallocation triggers and weights generate higher risk-adjusted returns

(as measured by Sharpe Ratios) than the underlying products or an equal-

weighted combination

Lower-correlating products generate higher risk-adjusted returns

Optimized reallocation weights vary based on strategy combinations

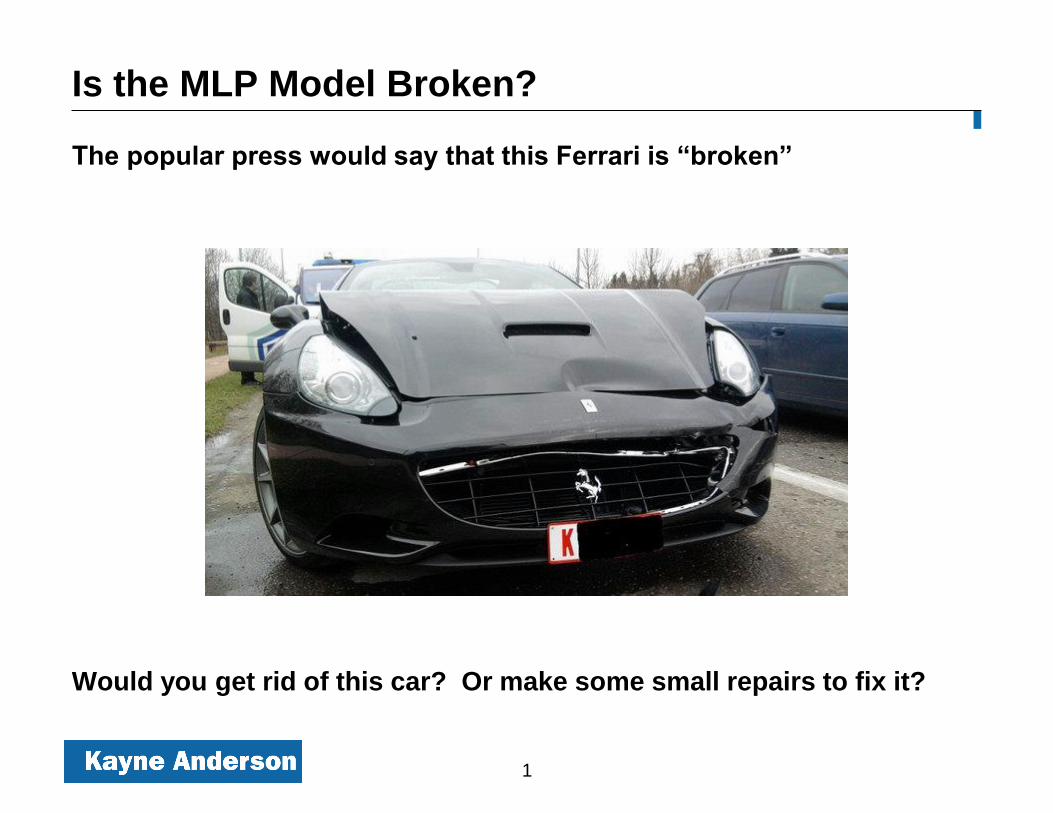

Is the MLP Model Broken?

The popular press would say that this Ferrari is “broken”

Would you get rid of this car? Or make some small repairs to fix it?

1

We strongly believe the MLP model isn’t broken!

Like the Ferrari, the MLP model was probably driving a little too fast…

…and probably deserved a speeding ticket….

So what happened?

Our view is that any problems we’ve seen in the MLP market were the result

of companies straying from the MLP model:

• In terms of how companies finance themselves

• What types of companies form MLPs – both the size and the type of

assets

• Structural protections for investors – which got whittled away in the bull

market

2

So… What Exactly is the “MLP Model”?

There are a few basic characteristics of MLPs

1) Full payout model

– “Finance as you go” model for acquisition and growth projects

2) Growth must be financed externally

– Instills discipline: if you do a bad deal, you can’t get financing

3) Predominantly fee based assets

– Minimal direct commodity risk preserves the level of cash flow

4) Incentives for General Partners to grow distributions

– Incentivize management both on the upside and the downside

3

How did we stray from the model?

Moving from an acquisition-based model to project-based model had

big challenges

– “Synchronized” financing became more difficult as capex requirements

were spread out over 2-4 years

– MLPs did not pre-finance equity portion of capex – wanted to wait until

the cash flowed

• Negative drag on DCF

– MLPs caught with huge capex obligations at a time when the capital

markets were very challenged

• Balance sheets were already stretched

4

What Should Have Happened??

In the next cycle, MLPs need to learn from the past

– Capex requirements can’t be outsized

• Have to be able to be proportionate with access to capital

– Big projects should be financed at the GP and dropped when ready

• MLPs with strong sponsors should receive a higher valuation

– Need to run leverage below target

• Leverage can fill the gap when the equity markets close

5

What Happened to Quality Control?

MLP market – both bankers and investors – strayed from the model

– More commodity risk, more volume risk and more service company risk

– Upstream model clearly doesn’t work – this is the second “blow up”

• Blew up in the 1986-1989 time frame for the exact same reasons

• Been there, done that……

– Read the fine print – what exactly does “fee based midstream mean??”

6

Non-Midstream IPOs were Frequent After 2008

40% of IPOs since 2008 were in non-midstream businesses

7

IPOs Since 2008

60%

40%

Midstream Non-Midstream

Non-Midstream Sub-Sectors

Marine (Shipping & Offshore)

Upstream

Refining

Coal

Retail Gas Distribution

Chemicals & Fertilizer

Frac Sand & Proppants

Propane Dehydrogenation

Wood Pellets

Saltwater Disposal

Ethanol Storage

Trona / Soda Ash Processing

What Happens when Quality Control Deteriorates?

No one should be surprised by the results…..

8

Relative Performance Since IPO(1) Median Relative Performance Since IPO

30%

25%

(11%)

(27%)

(40%)

(30%)

(20%)

(10%)

0%

10%

20%

30%

40%

Top 25% byMarket Cap

Top 50% byMarket Cap

Bottom 50%by Market

Cap

Bottom 25%by Market

Cap

20%

(17%)

(40%)

(30%)

(20%)

(10%)

0%

10%

20%

30%

40%

"Core Midstream" MLPs Other MLPs

___________________________

(1) Median relative performance versus the AMZ price return over the same time period. Includes 77 MLP IPOs since 2008. Return statistics as of May 18, 2016. Market capitalizations groupings as of June 30, 2015.

IDRs – Friend or Foe??

Incentive Distribution Rights have definitely worked

– MLP IDRs have been in existence since 1987

• Has been a primary driver of growth rate of 8% over the past 16 years

– IDRs provide a valuable incentive for the management – both on the

upside and the downside

• IDRs incentivize GPs to increase distributions - which in turn drives

stock price performance

• Also works on the downside, as the GP is hurt much more when an

MLP has to cut distributions

9

IDRs are Not Perfect

GP IDRs have - in some ways - worked too well

– The GP’s split of distributable cash flow is too high in the most

successful MLPs

• This effectively increases the cost of capital, and that has come under

great scrutiny lately

– Some MLPs trying to solve this issue through a “roll-in” of the LPs into

the GP

• Investors should be very wary of this – is often just a back door

distribution cut that disproportionately hurts the LPs

• That’s not how the high splits are supposed to work – the GP is

supposed to suffer more!

10

So…How Can We Solve IDR Issues?

There are several potential solutions – roll-ups not the only option!

– Giving “IDR holidays” on equity issued in times of distress is an easy fix

• Take the pledge: IDR waivers for the remainder of 2016

– Capping IDRs at 25% is also a step in the right direction

• IDRs weren’t designed with the expectation that they get this deep into the

splits – and 50%, quite frankly, looks excessive

– Could provide – at the time of IPO – an automatic reset of the IDRs at a certain

distribution amount

• Still need to give incentive to the GP – just don’t make IDRs a burden

– Finally, should consider eliminating IDRs on new equity – just on distribution

increases

11