mf0003 taxation

TRANSCRIPT

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 1/169

MR0003-Unit-01-Basic Concepts

Unit 1 Basic Concepts

1.1 Introduction

Learning objectives:

1.2 Tax Planning and Management

· Tax avoidance

· Tax evasion

· Tax planning

· Tax management

1.3 Terminology

1.4 Agricultural Income

1.5 Residence and Tax Liability

1.6 Scope of total income

1.7 Tax incidence in brief

1.8 Illustrations on incidence of tax

1.9 Total taxable income: how it is computed: tax liability

1.10 Summary

1.11 Terminal Questions

1.12 Answers to TQs

1.1 Introduction

The theory of taxation depends upon the definition of the term ―tax‖. According to Seligman, ‗Atax is a compulsory contribution from the person to the Govt. to defray the expenses incurred in

the common interest of all, without reference to special benefits conferred‘.

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 2/169

Bastable defines a tax as‘ a compulsory contribution of the wealth of person or body of persons

for the service of the public powers‘.

The Indian Taxation Enquiry Committee adopted the definition as ‗taxes are compulsory

contributions made by the members of a community to the governing body of the same towards

the common expenditure without any guarantee of a definite measured service in return‘.

The above definitions emphasize certain common features of tax such as:

1. It is a compulsory levy.2. Its proceeds are utilized for the common purpose.

3. The extent of the levy does not depend upon the benefits derived from state expenditure

by the tax payer.

4. Its object is to raise revenue to the state

Learning objectives:

· After studying this unit, you will be able to know:

· The difference between tax evasion and tax avoidance

· Basic concepts of taxation

· Terminologies

· Concept of agricultural income and concept of total income

1.2 Tax Planning and Management

The goal of the tax payers is to minimize his tax liability. To achieve this goal the following

three methods are commonly used by him:

1. Tax avoidance

2. Tax evasion

3. Tax planning

· Tax avoidance

Tax avoidance can be defined as the art of dodging tax without breaking the law. Objective of tax avoidance is minimizing the incidence of tax by adjusting the affairs in such a manner that

although it is within the four corners of the taxation laws but the advantage is taken by findingout loopholes in the laws. but where the main purpose is to defer, reduce or completely avoid the

tax payable under the law.

· Tax evasion

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 3/169

In the tax evasion, facts are deliberately misrepresented and tax liability is understated by

employing the following means:

a) concealment of income;

b) Inflation of expenses;

c) Falsification of accounts

d) violation of rules

These devices are unethical. Evasion, once proved, not only attracts heavy penalties but may alsolead to prosecution.

· Tax planning

Tax Planning is an arrangement of one‘s financial affairs in such a way without violating thelegal provisions of the Act. Full advantage is taken of all exemptions, deductions, rebates, reliefsetc. permitted under the Act, reducing the burden of taxation to the least.

The aim of tax planning is to minimise the incidence of tax. It is a guide in decision making. Itlooks at future benefits arising out of present actions.

· Tax management:

Tax management refers to the compliance with the statutory provisions of law. Tax planning isoptional, tax management is mandatory. It covers a wider field like maintenance of accounts,

filling of return, payment of taxes, TDS, timely payment of advance tax, etc., poor taxmanagement may lead to levy of interest, penalty, prosecution, etc.

Difference between tax planning and tax evasion

Tax planning Tax evasion

Objective is to reduce the tax liability Objective is to avoid the tax liability by

misrepresentation of facts and

falsification of accounts.

It works within the permissible rangeof the Act

It is achieved by violation of the act

Tax planning is a legal right Tax evasion is a legal offence which may

lead to penalty and prosecution.

Tax planning accelerates development

of the economy of a country bygenerating funds for investment in

desired sectors

Tax evasion retards the development of

economy and accelerate the developmentof parallel economy

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 4/169

Difference between tax avoidance and tax evasion

Tax avoidance Tax evasion

The objective is to minimising the taxliability by finding the loop holes in

the act

Objective is to avoid the tax liability bymisrepresentation of facts and falsification

of accounts.

2) Tax avoidance takes into accountsvarious gaps of law

Tax evasion involves use of unfair means

3) Tax avoidance is lawful butinvolves the element of mala fide

intention

Tax evasion is unlawful

4) Tax avoidance is planning beforethe actual liability for tax comes into

existence

Tax evasion involves avoidance of payment of tax after the liability of tax has

arisen

Difference between tax planning and tax management

Tax planning Tax management

Tax planning a wider term andincludes tax management

Tax management is narrow term and isthe first step towards tax planning.

Objective is to reduce the tax liability It emphasizes on compliance of legalformalities for minimisation of tax

It is optional Tax management is essential for every

person.

Tax planning helps in decisionmaking

Tax management helps in complying theconditions for effective decision making

Tax planning helps to claim variousbenefits of tax

Tax management involves maintenance of accounts in prescribed for, filing of return,

payment of tax, etc.

Tax planning involves comparison of

various alternatives before selecting

the best one.

Tax management involves maintenance of

accounts in prescribed form, filing of

return, payment of tax, etc.

Tax planning looks at future befits Tax management relates to past present

Who is liable to pay income tax?

Every person, whose taxable income for the previous financial year exceeds the minimum

taxable limit, is liable to pay to the Central Government the income tax during the current

financial year on the income of the previous financial year at the rates in force during the currentfinancial year.

1.3 Terminologies

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 5/169

Income [Sec 2 (24)]

In general sense ―It means any monitory receipt either in cash or in kind (Should be

quantifiable), may be real or notional, regular or casual or legal or illegal or own‘s own or

somebody else‘s from a definite source. These sources may be Income from salary, H.P,

Business or profession, other sources or Capital Gains‖ excluding anything in the nature of amere windfall.

Assesses [Sec. 2(7)] An Assesses means a person:

(i) Who is liable to pay any tax; or

(ii) Who is liable to pay any other sum of money under this Act. (Ex: interest, penalty, etc.); or

(iii) In respect of whom any proceeding under this act has been taken for the assessment of his

income; or

(iv) In respect of whom any proceeding under this act has been taken for the assessment of the

income of any other person in respect of which he is assessable; or

(vii) Who is deemed to be an assesses under any provision of this Act; or

(viii) Who is deemed to be an assesses in default under any provision of this Act.

Deemed Assesses: A person, who is deemed to be assesses for some other person, is called

deemed assesses

Assesses in Default: When a person responsible for doing any work under the Act, fails to do so,he is termed an ‗Assesses in Default‘.

For Ex: If a person while making any payment to other person, is liable to deduct income tax

thereon at source, does not deduct income tax therefrom, or having deducted at it, does not

deposit it in the Government treasury, he will be treated as an ‗Assesses in Default‘ for thatincome tax.

Assessment [Sec 2 (8)] It is a process of computing taxable income of the assesses, calculating

tax on such taxable income and imposing tax liability on the assesses

Assessment Year [Sec. 2 (9)]: Assessment Year means the period of twelve monthscommencing on the first day of April every year and ending on 31st March of next year. This

period is fixed by law and never changes. An assesses is liable to pay tax on the income of the

previous year during the next following assessment year.

Person [Sec. 2 (31)]

‗Person‘ includes the following:

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 6/169

(i) An Individual: means a natural person or human being,

(ii) A Hindu Undivided Family (H.U.F)

(iii) A Company

(iv) A Firm: It means a partnership firm; which is defined under the partnership Act.

(v) An Association of Person (A.O.P): It means two or more persons joining for a commonpurpose for the purpose of earning income.

(vi) Body of Individuals (B.O.I)

(vii) A Local Authority: It includes Municipality, Municipal Corporation, District Board

(viii) Every artificial Juridical Person, not falling within any of the preceding sub – classes: An

Idol or Deity, university.

Gross Total Income [Sec 80B (5)] It is the Total income computed in accordance with the

provisions of the income tax Act, before making deductions under sections 80C to 80U

Total Income: [Sec 2 (45)] It means amount left after making the deductions under sections 80C

to 80U

Previous Year [Sec 3]: Previous year is a period of twelve months, immediately preceding the

Assessment Year. Or any financial year immediately preceding the Assessment Year

Exceptions to the general rule of year

Income earned in any year will be assessed in its following year. This is called general rule of

Previous Year, However in the following cases the assessee is liable to be assessed to tax in the

same year in which he earns the income:

(i) Income of non – resident from shipping business [Sec 172]

(ii) Income of persons leaving India either permanently or for a long period of time [Sec 174]

(iii) Income of bodies formed for short duration [174A]

(iv) Transfer of property to avoid tax [175]

(v) Income of a discontinued business or profession [176]

Self Assessment Questions I

1) Mr. Suresh is a partner of a firm. He is assessable as —————— .

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 7/169

2) For previous year 2008-09, assessment year is —————– .

3) Indian Income Tax Act was passed in ———— -.

4) Income of discontinued business in the year 2008-09 is taxable in the year

Casual Income: Any receipts, which is of a casual, and non-recurring in nature is called casualincome i.e., it is that income the receipt of which is accidental and without any stipulation and is

in the nature of an unexpected windfall.

Heads of Income [Sec 14]

All taxable income of an assessee fall under any of the following five heads of income. Those

incomes, which do not find place under the first four heads and are taxable fall under the fifth

head of income.

1. Salaries [Sections 15 to 17]2. Income from House Property [Sections 22 to 27]

3. Profits and Gains of Business or Profession [Sections 28 to 44]4. Capital Gains [Sections 45 to 55] and

5. Income from Other Sources [Sections 56 to 59].

Rates of Tax for an Individual

Note: Surcharge: In all the above cases, If total income exceeds Rs. 10,00,000 – @ 10%

Education cess: On the amount of Income Tax + Surcharge – @ 3%

(Primary education cess at 2% + Secondary and Higher education cess at 1%)

1.4 Agricultural Income (Sec. 2(1A)

Agricultural income is totally exempt from liability to income tax. However, agricultural income

is factor in determining the tax on the non-agricultural income of an Individual, Hindu undivided

family, Association of persons and Body of individuals whose total income (excludingagricultural income) exceeds the minimum taxable limit and the agricultural income exceeds Rs.

5,000.

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 8/169

It is necessary to understand clearly the meaning of the term agricultural income which can be

done with the help of the following chart:

(A) (i) And (ii) Rent or revenue derived from land situated in India. When one person grants to

another a right to use his land situated in India for agricultural purposes; the former receives

from the latter rent or revenue in consideration of such user. Such rent or revenue is treated as

agricultural income.

(i) Used for agricultural purposes. It means cultivation of a field, tilling of the land, watering it,

sowing of the seeds, planting and similar operations on the land.

(B) (i) Income derived from such land by agricultural operations.

(ii) Income derived from such land by the performance of any process ordinarily employed by a

cultivator to render the produce raised by him fit to be taken to market. The process employed incuring of coffee, flue curing of tobacco, ginning of cotton, etc., is such a process.

(iii) Income derived from such land by a sale by a cultivator or receiver of rent-in-kind theproduce raised or received by him.

(C) Income from farm house. The income from a farm house is treated as agricultural income if the following conditions are satisfied

(i) It is situated on or in the immediate vicinity of the agricultural land;

(ii) The building is, by reason of his connection with the land, used as dwelling house or a store-house or an out-house by the cultivator or receiver of rent-in-kind;

(iii) The land is either assessed to land revenue in India or is subject to local rate assessed andcollected by the officers of the government, or alternatively;

(iv) If the land is situated in ‗non-urban‘ area, i.e., an area which though, is within municipalityor cantonment board jurisdiction, has a population of less than 10,000; or is beyond a notified

distance (maximum 8 kilometer) from the local limits of any such municipality; or cantonment

board.

However, the income derived from any building or land [mentioned in (C)] arising from the use

of such building or land for any purpose (including letting form residential purpose or for the

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 9/169

purpose of any business or profession) other than agricultural [mentioned in (A) or (B)] shall not

be agricultural income.

Examples of Agricultural Incomes:

(i) Income from growing flowers and creepers.

(ii) Rent from agricultural land.

(iii) Profit on sale of standing crops or produce after harvest by the cultivating owner or tenant of

agricultural land.

(iv) Income from leasing out agricultural land for grazing cattle required for agricultural

purposes.

(v) Interest on capital received by a partner from his firm engaged in agricultural operations.

(vi) Conversion of latex into smoked sheets.

(vii) Rent from agricultural land received from sub-tenants by the mortgagee in possession.

(viii) Income from sale of mulberry leaves grown on agricultural land.

(ix) Compensation received from an insurance company for damages caused by hailstorm or

floods to the tea plantations.

(x) Income from conversion of timber into planking.

Examples of Non-Agricultural Incomes

The following incomes are a not derived from land used for agricultural purposes hence they arenon-agricultural incomes:

(i) Income from markets;

(ii) Income from stone quarries;

(iii) Income from mining royalties;

(iv) Income from land used for storing agricultural produce;

(v) Income from supply of water for irrigation purposes (e.g., income from supply of water forirrigation from a tube-well, as it does not involve any agricultural operation);

(vi) Income from self-grown grass, trees or bamboos;

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 10/169

(vii) Income from fisheries;

(viii) Income from the sale of earth for brick-making;

(ix) Remuneration received as manager of an agricultural farm;

(x) Dividend from a company engaged in agriculture;

(xi) Income of the buyer of a ripe crop;

(xii) Income from dairy farm, poultry farming, etc.; and

(xiii) Income from interest on arrears of rent of agricultural land.

When the individual has net agricultural income exceeding Rs. 5,000, in addition to the non-agricultural income exceeding the exemption limit (Rs, 1,35,000 for women assesses, 1,85,000

for senior citizens, Rs. 1,00,000 for other individual), agricultural income is included in theincome only for rate of tax.

1.5 Residence and Tax Liability

The scope of total income of an assessee is determined with reference to his residence in India in

the previous year (Sec. 5). It is immaterial what type of resident an assessee is during theassessment year. Residence and citizenship are two different things. The incidence of tax has

nothing to do with citizenship. An Indian may be non-resident and a foreigner may be resident

for income tax purposes. The residence of a person may change from year to year but citizenship

cannot be changed every year.

Different Types of Residents

On the basis of residence, the assessees are divided into three categories, viz.:

a. Persons who are resident in India, Popularly known as ‗ordinarily resident‘.

b. Persons who are ‗not ordinarily resident in India‘.

c. Persons who are ‗non-resident‘.

Residential status of Individuals

Resident (Ordinarily Resident). Sec. 6 (1) and 6 (6) (a)

Basic Conditions: Sec. 6 (1):

An individual is said to be resident in India in any previous year if he satisfies any one of thefollowing basic conditions:

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 11/169

(a) He is in India in the previous year for a period of 182 days or more, or

(b) He has been in India for at least 365 days during the four years proceeding the previous year

and is in India for at least 60 days during the previous year.

Exceptions to the above rules of 60 days stay in India

(i) An individual who is a citizen of India and leaves India in any previous year for the purpose

of employment or as a member of the crew of an Indian ship must have stayed in India for at

least 182 days during the previous year instead of 60 days.

(ii) If any citizen of India or a foreign national of Indian origin, who is living outside India,comes on a visit of India in the previous year, he must have stayed in India for at least 182 days

during the previous year instead of 60 days.

In other words, in the case of an individual covered by the above two exceptions only condition

(a) is to be satisfied to become a resident in India and condition (b) has no significance at all.

Note:

1. It means that a non-resident Indian will not lose his non-residential status even if he visitsIndia and stays here up to 181 days in a previous year.

2. For calculating number of days stay in India, days of entry and exit should be included in theperiod of stay in India.

‗Indian origin‘ means that either he or either of his parents or any of his grandparents was born in

undivided India. Further, ‗comes on a visit to India in the previous year‘ means that he maycome to India for any purpose. Whatsoever, it may be business purpose or personal purpose of

any nature or he may come to meet his relations or he may come for a pleasure trip also.

Stay in India for 182 days or more during the previous year. It is not at all necessary that he

should stay at a stretch for 182 days. His total stay for at least 182 days may be with gaps. It isalso not necessary that the entire stay should be at one place. It may be at different places in

India.

Stay in India for at least 365 days during the four years preceding the previous year and for at

least 60 days or 182 days, as the case may be, during the previous year

Here again, it not necessary that he should stay during the previous year in India at a stretch for

60 days or 182 days, as the case may be, or the entire stay need not be at one place only.

Additional Conditions: Sec. 6 (6) (a):

In fact, in order that an individual may become ordinarily resident in India, he is to satisfy both

the following conditions besides satisfying any one of the above mentioned basic conditions:

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 12/169

(i) He has been resident in India in at least two out of the ten previous years preceding the

relevant previous year, and

(ii) He has been in India for at least 730 days in all during the seven previous years proceeding

the relevant previous year.

In condition (i) resident of two years out of ten years preceding the previous year means that theassessee must have satisfied at least one of the basic conditions for two years out of ten years

preceding the previous year.

In condition (ii) the assessee must be physically present in India for at least 730 days during the

seven previous years preceding the relevant previous year.

Resident but not ordinarily resident: Sec. 6(1), 6 (6) (a)

An individual who satisfies at least one of the basic conditions laid down in Sec. 6 (1), but does

not satisfy the two additional conditions of Sec. 6 (6) (a), is treated as ‗a resident but notordinarily resident‘.

Non-resident:

An individual is a non-resident in India if he satisfies none of the basic conditions. In the case of

non-resident, additional conditions are not relevant.

Residential Status of Hindu Individed Family, Firm or Association of Persons

Resident:

A Hindu Undivided family, firm or association of persons are residents in India in any previous

year if the control and management of its affairs is situated wholly or partly in India during therelevant previous year. i.e., even if a part of their control and management is situated in India

during the previous year, they will be called resident in India.

A resident H.U.F. will be ordinarily resident only when its kartha satisfies both the additional

conditions of ordinarily resident as an individual.

Not Ordinarily Resident:

Firm and Association of persons cannot be ‗not ordinarily resident‘. A Hindu Undivided Familyis ―not ordinarily resident‖ in India, if, its Karta or manager (as an individual) is not ordinarily

resident in India.

In this connection it is important to note that where during the last ten years preceding the

previous year the managers of Karta of H.U.F. had been different from one another, the totalperiod of stay of successive kartas of the Family should be aggregated to determine the

residential status of the Karta and consequently it‘s H.U.F.

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 13/169

Non-Resident:

All the three types of assessees (i.e., H.U.F., Firm of A.O.P.) are non-resident‘ only when the

control management of their affairs is situated wholly outside India.

Self Assessment Questions II

1) A Ltd. Company cannot be a ————— -.

2) Income from poultry farming is an agricultural Income.: True/ false

3) To become a Resident but ordinarily Resident, an individual must satisfy the conditions laiddown in ————— , in addition to the conditions laid down in —–

4) Income from house property is ———— in the hands of a Non resident.

Residential Status of Companies

Resident. A company is said to be resident in India in any previous year, if,

(i) It is an Indian company; or

(ii) During that year, the control and management of its affairs is situated wholly in India.

A company may be resident here even though its entire trading operations are carried on abroad.

If the management and control is situated wholly in India, the company is resident here.

Normally, control and management of a company‘s affairs is situated at the place where

meetings of its board of directors are held.

Not Ordinarily Resident. A company is never an ‗not ordinarily resident‘.

Non-resident. If a company does not satisfy both the aforesaid conditions of residence, it is said

to be a ‗non-resident‘ company. It means neither the company is an Indian Company nor thecontrol nor management of its affairs is situated wholly in India.

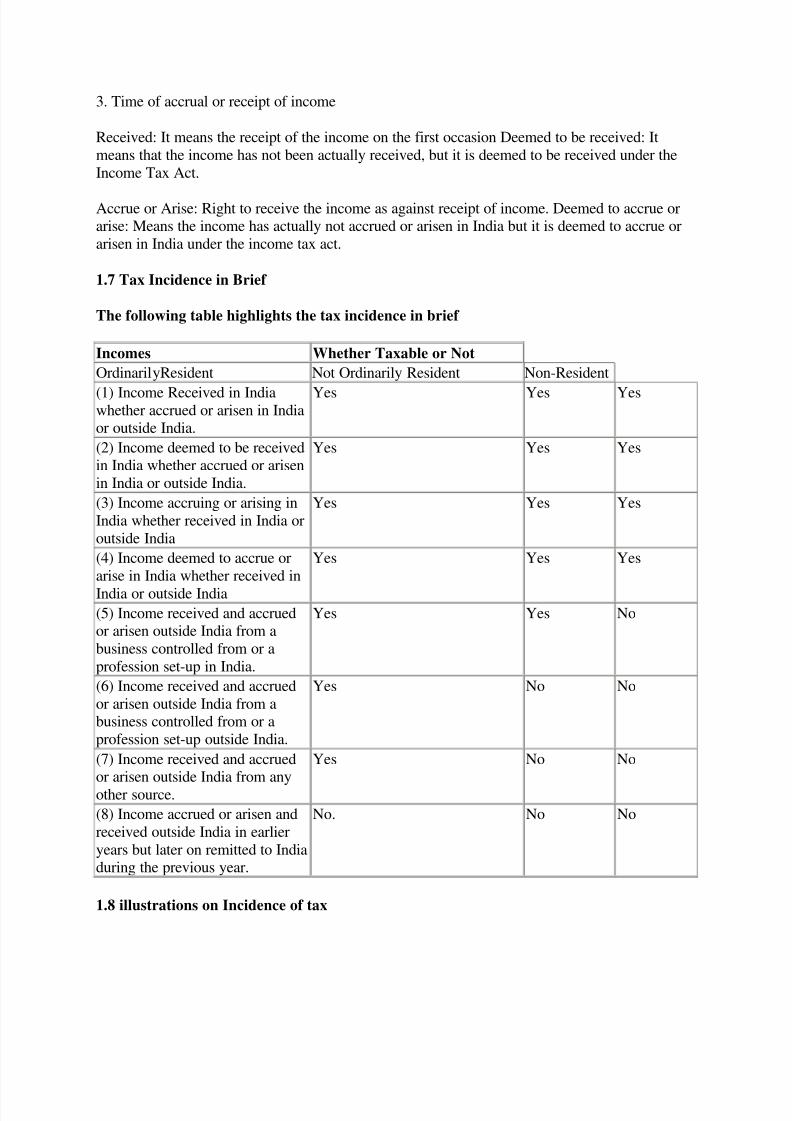

1.6 Scope of total income or incidence of tax

Incidence of Tax: It refers to chargeability of incomes based on the residential status of the

assessee and also on the place and time of accrual or receipt of income.

Factors of incidence:

1. Residential Status

2. Place

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 14/169

3. Time of accrual or receipt of income

Received: It means the receipt of the income on the first occasion Deemed to be received: It

means that the income has not been actually received, but it is deemed to be received under the

Income Tax Act.

Accrue or Arise: Right to receive the income as against receipt of income. Deemed to accrue orarise: Means the income has actually not accrued or arisen in India but it is deemed to accrue or

arisen in India under the income tax act.

1.7 Tax Incidence in Brief

The following table highlights the tax incidence in brief

Incomes Whether Taxable or Not

OrdinarilyResident Not Ordinarily Resident Non-Resident

(1) Income Received in Indiawhether accrued or arisen in Indiaor outside India.

Yes Yes Yes

(2) Income deemed to be receivedin India whether accrued or arisen

in India or outside India.

Yes Yes Yes

(3) Income accruing or arising in

India whether received in India or

outside India

Yes Yes Yes

(4) Income deemed to accrue or

arise in India whether received in

India or outside India

Yes Yes Yes

(5) Income received and accruedor arisen outside India from a

business controlled from or a

profession set-up in India.

Yes Yes No

(6) Income received and accrued

or arisen outside India from abusiness controlled from or a

profession set-up outside India.

Yes No No

(7) Income received and accruedor arisen outside India from any

other source.

Yes No No

(8) Income accrued or arisen and

received outside India in earlier

years but later on remitted to Indiaduring the previous year.

No. No No

1.8 illustrations on Incidence of tax

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 15/169

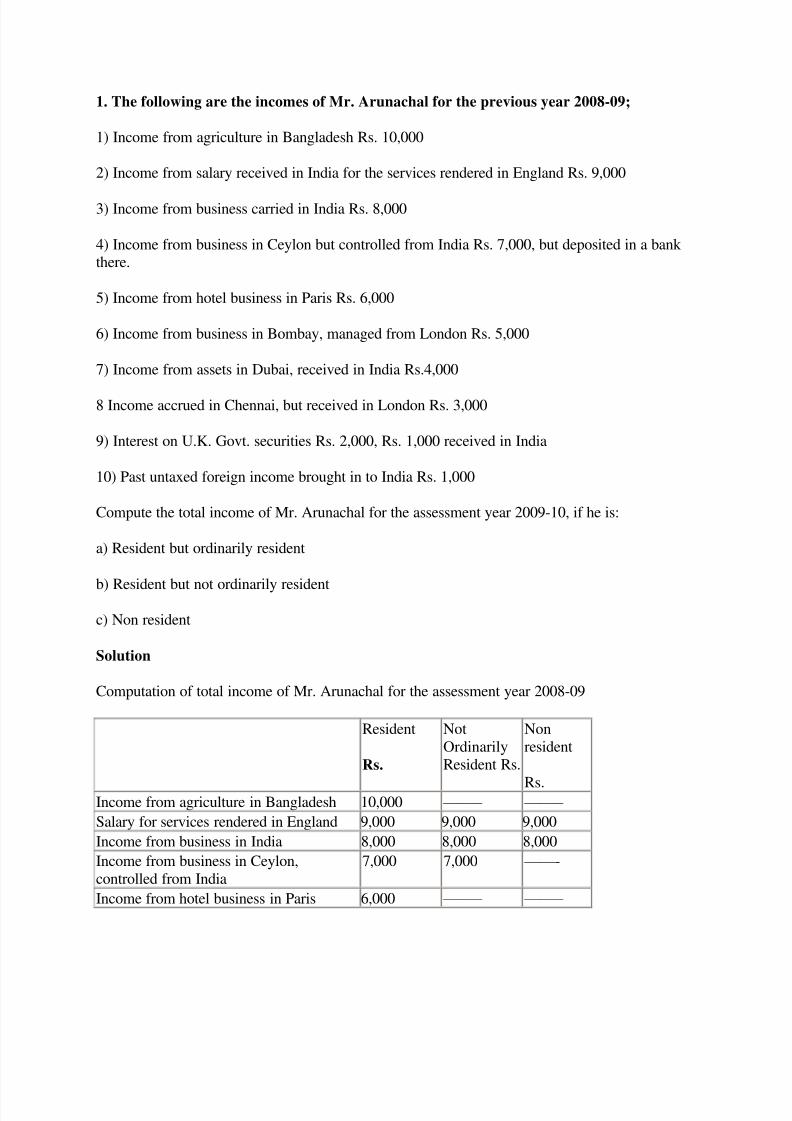

1. The following are the incomes of Mr. Arunachal for the previous year 2008-09;

1) Income from agriculture in Bangladesh Rs. 10,000

2) Income from salary received in India for the services rendered in England Rs. 9,000

3) Income from business carried in India Rs. 8,000

4) Income from business in Ceylon but controlled from India Rs. 7,000, but deposited in a bank there.

5) Income from hotel business in Paris Rs. 6,000

6) Income from business in Bombay, managed from London Rs. 5,000

7) Income from assets in Dubai, received in India Rs.4,000

8 Income accrued in Chennai, but received in London Rs. 3,000

9) Interest on U.K. Govt. securities Rs. 2,000, Rs. 1,000 received in India

10) Past untaxed foreign income brought in to India Rs. 1,000

Compute the total income of Mr. Arunachal for the assessment year 2009-10, if he is:

a) Resident but ordinarily resident

b) Resident but not ordinarily resident

c) Non resident

Solution

Computation of total income of Mr. Arunachal for the assessment year 2008-09

Resident

Rs.

Not

Ordinarily

Resident Rs.

Non

resident

Rs.Income from agriculture in Bangladesh 10,000 ——– ——–

Salary for services rendered in England 9,000 9,000 9,000

Income from business in India 8,000 8,000 8,000

Income from business in Ceylon,

controlled from India

7,000 7,000 —— -

Income from hotel business in Paris 6,000 ——– ——–

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 16/169

Income from business in Bombay 5,000 5,000 5,000

Income from assets in Dubai, received inIndia

4,000 4,000 4,000

Income accrued in Chennai received inLondon

3,000 3,000 3,000

Interest on U.K Govt. securities, receivedin India

2,000 1,000 1,000

Past untaxed income brought in to India ––– ––– –––

Total income taxable 54,000 37,000 30,000

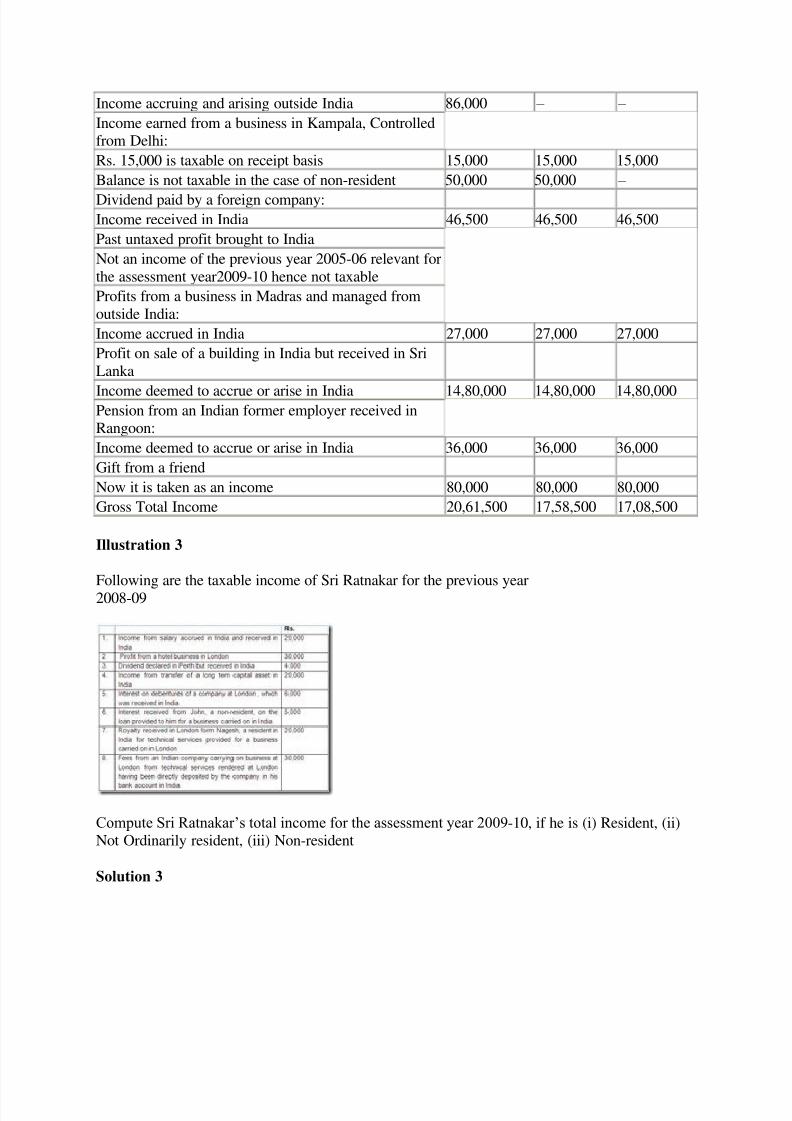

Illustration 2

Mr. Sumantha furnishes the following particulars of his income earned during the previous year

relevant to the assessment year 2008-09.

Solution 2

Resident and

ordinarily

resident

Rs.

Resident but

not

ordinarilyresident

Rs

Non-

resident

Rs.

Interest on German Development Bonds:Two fifths is taxable on receipt basis 24,000 24,000 24,000

Three-fifths is taxable in the case of resident andordinarily resident on accrual basis

36,000 – –

Income from agriculture in Bangladesh:

Income accrued and received outside India 1,81,000 – –

Income from property in Canada received outside India

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 17/169

Income accruing and arising outside India 86,000 – –

Income earned from a business in Kampala, Controlledfrom Delhi:

Rs. 15,000 is taxable on receipt basis 15,000 15,000 15,000

Balance is not taxable in the case of non-resident 50,000 50,000 –

Dividend paid by a foreign company:Income received in India 46,500 46,500 46,500

Past untaxed profit brought to India

Not an income of the previous year 2005-06 relevant for

the assessment year2009-10 hence not taxable

Profits from a business in Madras and managed from

outside India:

Income accrued in India 27,000 27,000 27,000

Profit on sale of a building in India but received in Sri

Lanka

Income deemed to accrue or arise in India 14,80,000 14,80,000 14,80,000Pension from an Indian former employer received inRangoon:

Income deemed to accrue or arise in India 36,000 36,000 36,000

Gift from a friend

Now it is taken as an income 80,000 80,000 80,000

Gross Total Income 20,61,500 17,58,500 17,08,500

Illustration 3

Following are the taxable income of Sri Ratnakar for the previous year

2008-09

Compute Sri Ratnakar‘s total income for the assessment year 2009-10, if he is (i) Resident, (ii)Not Ordinarily resident, (iii) Non-resident

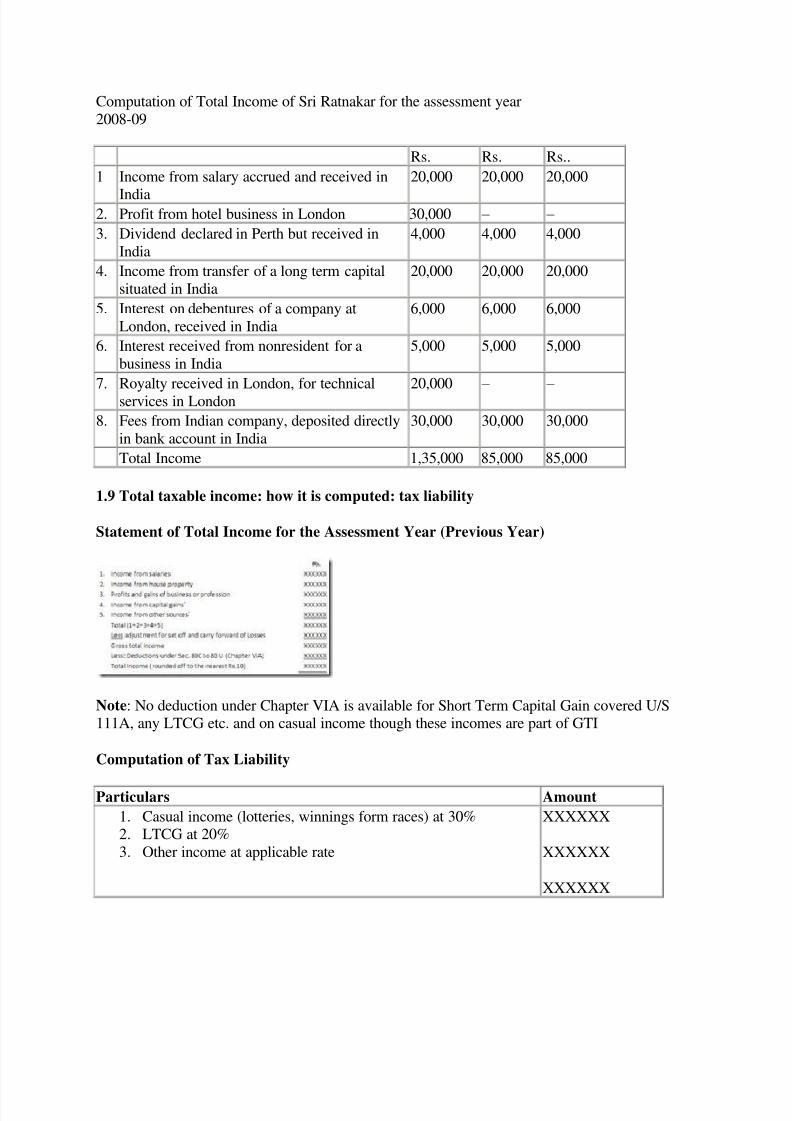

Solution 3

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 18/169

Computation of Total Income of Sri Ratnakar for the assessment year

2008-09

Rs. Rs. Rs..

1 Income from salary accrued and received in

India

20,000 20,000 20,000

2. Profit from hotel business in London 30,000 – –

3. Dividend declared in Perth but received in

India

4,000 4,000 4,000

4. Income from transfer of a long term capital

situated in India

20,000 20,000 20,000

5. Interest on debentures of a company at

London, received in India

6,000 6,000 6,000

6. Interest received from nonresident for a

business in India

5,000 5,000 5,000

7. Royalty received in London, for technical

services in London

20,000 – –

8. Fees from Indian company, deposited directly

in bank account in India

30,000 30,000 30,000

Total Income 1,35,000 85,000 85,000

1.9 Total taxable income: how it is computed: tax liability

Statement of Total Income for the Assessment Year (Previous Year)

Note: No deduction under Chapter VIA is available for Short Term Capital Gain covered U/S111A, any LTCG etc. and on casual income though these incomes are part of GTI

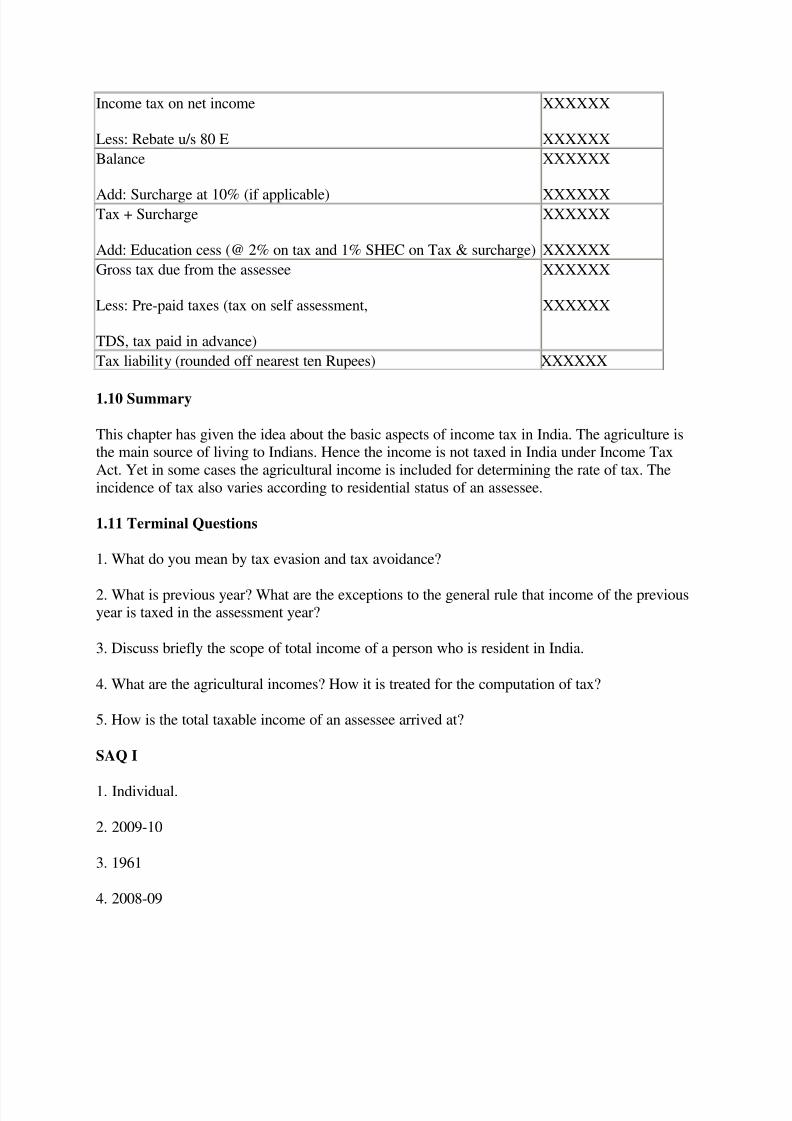

Computation of Tax Liability

Particulars Amount

1. Casual income (lotteries, winnings form races) at 30%2. LTCG at 20%

3. Other income at applicable rate

XXXXXX

XXXXXX

XXXXXX

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 19/169

Income tax on net income

Less: Rebate u/s 80 E

XXXXXX

XXXXXX

Balance

Add: Surcharge at 10% (if applicable)

XXXXXX

XXXXXXTax + Surcharge

Add: Education cess (@ 2% on tax and 1% SHEC on Tax & surcharge)

XXXXXX

XXXXXX

Gross tax due from the assessee

Less: Pre-paid taxes (tax on self assessment,

TDS, tax paid in advance)

XXXXXX

XXXXXX

Tax liability (rounded off nearest ten Rupees) XXXXXX

1.10 Summary

This chapter has given the idea about the basic aspects of income tax in India. The agriculture isthe main source of living to Indians. Hence the income is not taxed in India under Income Tax

Act. Yet in some cases the agricultural income is included for determining the rate of tax. The

incidence of tax also varies according to residential status of an assessee.

1.11 Terminal Questions

1. What do you mean by tax evasion and tax avoidance?

2. What is previous year? What are the exceptions to the general rule that income of the previousyear is taxed in the assessment year?

3. Discuss briefly the scope of total income of a person who is resident in India.

4. What are the agricultural incomes? How it is treated for the computation of tax?

5. How is the total taxable income of an assessee arrived at?

SAQ I

1. Individual.

2. 2009-10

3. 1961

4. 2008-09

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 20/169

SAQ II

1. Not ordinarily Resident

2. False

3. 6(1),6(6)

4. Not taxable

1.12 Answers to TQs

1. Refer to Section 1.2

2. Refer to Section 1.3

3. Refer to Section 1.6

4. Refer to Section 1.4

5. Refer to Section 1.9

Copyright © 2009 SMU

Powered by Sikkim Manipal University

.

MF0003-Unit-02-Deductions from Gross

Total Income

Unit 2 Deductions from Gross Total Income

and Exempted Incomes

Structure:

2.1 Introduction

Objectives

2.2 Deductions u/s 80C

2.3 Deduction in Respect of Medical Insurance Premium (sec 80D)

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 21/169

2.4 Deduction in Respect of Interest on Loan taken for Higher Education (Sec 80E)

2.5 Deduction in Respect of Donations to certain funds & Charitable Institutions

(Sec 80G)

2.6 Deduction in Respect of Profits and Gains from Industrial Undertaking Engaged inInfrastructure Development (Sec 80I)

2.7 Deduction in Respect of Profits and Gains from Business of Collecting and Processing of

Bio-Degradable Waste (Sec 80JJA)

2.8 Deduction in Respect of Certain Incomes of Offshore Banking Units (Sec 80LA)

2.9 Deductions in the Case of a Person with Disability (Sec 80U)

Self assessment question

2.10 Exemptions: Tax-Free Incomes

2.11 Exemptions U/S 10A, 10AAA, 10B

2.12 Rebate U/S 88E

2.13 Summary

2.14 Terminal Question

2.15 Answers to SAQ and TQ

2.1 Introduction

After computing the income under each head separately, the incomes of the various heads areadded together. The total of incomes of the various heads is called Gross Total Income. From the

gross total income, certain allowable deductions are made. The purpose of these deductions is to

encourage savings, industrialization and to assist tax payers in meeting their essentialexpenditures.

The resulting balance is the total income of the assessee.

The deductions from gross total income are allowed :

(i) In respect of certain investments and payments made by the assessee and

(ii) In respect of certain incomes received by the assessee

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 22/169

The deductions from gross total income are provided in Sections 80CCC to 80U. i.e., under

Chapter VI-A of the income-Tax Act of 1961.

As per Section 80A of the Income-tax Act, the aggregate (i.e., total) amount of various

deductions from gross total income allowed in Section 80 CCC to 80U should not exceed the

gross total income. (i.e. G.T.I. after excluding long-term capital gains, short term capital gainstaxable u/s 111A, winnings from lotteries, races etc.)

Learning objectives:

After reading this chapter you will learn:

· Various deductions allowable under the Act.

· To prepare proper tax plans.

· To claim exemptions given under the Act.

· Various tax concessions available for the entrepreneurs.

2.2. Deductions u/s 80C

Deductions under Section 80C: Deductions in respect of certain investments made or certainpayments, deposits made

Eligible assessee: An Individual and HUF

Quantum of Exemption: Rs. 1, 00,000 or Amount invested or Payment made, whichever isless.

Conditions: The maximum amount of exemptions under Sections 80C, 80CCC and 80CCD

should not exceed Rs. 1, 00,000

Eligible Investments, Contributions and Payments

Life Insurance Premium: Premium paid for insurance on his own life or on the life of hiswife or her daughter, or his or her child (minor or major) of any status including married

daughter.

1. Condition: The qualifying amount of any premium or other payment made on an

insurance policy shall not exceed 20% of the actual capital sum assured.

2. Payment made for a contract of deferred annuity

3. Deduction from the salary payable to a government servant by the government –

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 23/169

securing to him a deferred annuity (should not exceed 1/5 th of salary)

4. Contribution to the Statutory Provident Fund, Public Provident Fund or to a RecognisedProvident Fund and to an Approved Superannuating Fund.

5. Purchase National Savings Certificates VIII Issue (Interest accrued on VIII Issue isdeemed to have been re-invested)

6. Contributions towards Unit Linked Insurance Plan, (ULIP) of the UTI and of LICMutual Fund (notified)

7. Any sum paid annuity plan of LIC or any other insurer

8. Subscription to any notified units of any Mutual Fund or UTI

9. Contribution to any pension fund set-up by any Mutual Fund or by the UTI

10. Subscription to Home Loan Account or contribution to pension fund set-up by the

National Housing Bank.

11. Any subscriptions to any scheme PSU engaged in Long term financing of acquisitions

and constructions of residential houses

12. Tuition fees paid other than donations for full time education (max: two children)

13. Any payment made towards any loan taken to meet the cost of purchase or construction

of a new residential house

14. Amount invested in approved debentures and equity shares of PSUs engaged in

infrastructure facilities including power sectors or subscription of Units of MFs proceeds of

which are invested in infrastructure facilities

Deduction in respect of contribution to certain Pension Funds (80CCC)

Eligible assessee: Individual

It is allowed in respect of any amount paid or deposited in the P. Y. for an annuity plan of LIC or

any other insurer (approved by IRDA) for receiving pension

Deductible amount: the amount so paid or Rs.1, 00,000, whichever is less

The contribution made by the central government to the account of an employee under a

pension scheme referred to in Section 80CCD

Section 80CCD is applicable if the following conditions are satisfied

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 24/169

Eligible assessee: Individual

He is employed by the central Government on or after 1 – 1 – 2004

Amount should be deposited any amount in his account under a pension scheme notified by the

central Government during the P. Y.10% of employee‘s contribution (to the extent of Basic Pay+ D. A. given in terms of employment) to the above scheme is deductible 10% of Contributionby the Central Government to the above scheme is deductible in the year in which the

contribution is made Note: In both the cases the contribution amount should not exceed 10% of

salary

2.3 Deduction in respect of Medical Insurance Premium [Sec 80D]

Eligible assessee: Individual and HUF.

Deductible amount: the maximum deductible amount is Rs.10, 000, or actual amount paid

whichever is less (In case of senior citizen it is Rs. 15,000)

Certain conditions:

(i) Premium must be paid by cheque (Cash not allowed)

(ii) The medical insurance scheme of GIC (Ex: Mediclaim Policy) or any other scheme approved

by the Central Government or IRDA

(iii) Insurance on his health or on the health of his spouse or parents or dependant children.

Deduction in respect of maintenance including Medical treatment of a, handicappedDependant (Sec. 80DD)

Eligible assessee: Resident individual and HUF

Quantum of Deduction: For disability fixed sum of Rs. 50,000 irrespective of the amount

incurred or deposited further in case of a dependent with severe disability (80% disability or

more) the deduction shall be Rs. 75,000.

Note: If deduction u/s 80U is claimed no deduction is available under section 80DD

Deduction in respect of MedicalTreatment, etc. (Sec. 80DDB)

Eligible assessee: Individual and HUF

Deductible amount: i) Amount paid or Rs. 40,000, whichever is less (ii) Where the payment is inrelation to a senior citizen the deduction shall be amount paid or Rs. 60,000, whichever is less.

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 25/169

Note: However, the deduction shall be reduced by the amount received, if any, by under an

insurance from an insurer or reimbursed by the employer for the medical treatment of personmentioned in this section.

Specified diseases: Neurological diseases, cancer, AIDS, chronic renal failure, Hemophilia etc

2.4 Deduction in respect of interest of loan taken for Higher Education (Sec. 80E)

Eligible assessee: Individual

An individual is entitled to a deduction of amount paid by him in previous year by way of

repayment of loan (including interest) taken by‘ from any financial institution or an approvedcharitable institution for t purpose of pursuing his higher education Conditions:

(i) The repayment should be done out of his income chargeable to tax.

(ii) The deduction will be allowed for the previous year in which the assessee starts repaying theloan.

The deduction is available for a maximum period of 8 years till the loan together with inter

thereon is fully paid (whichever is earlier) by the assessee.

Only interest is allowed not repayment of any installments

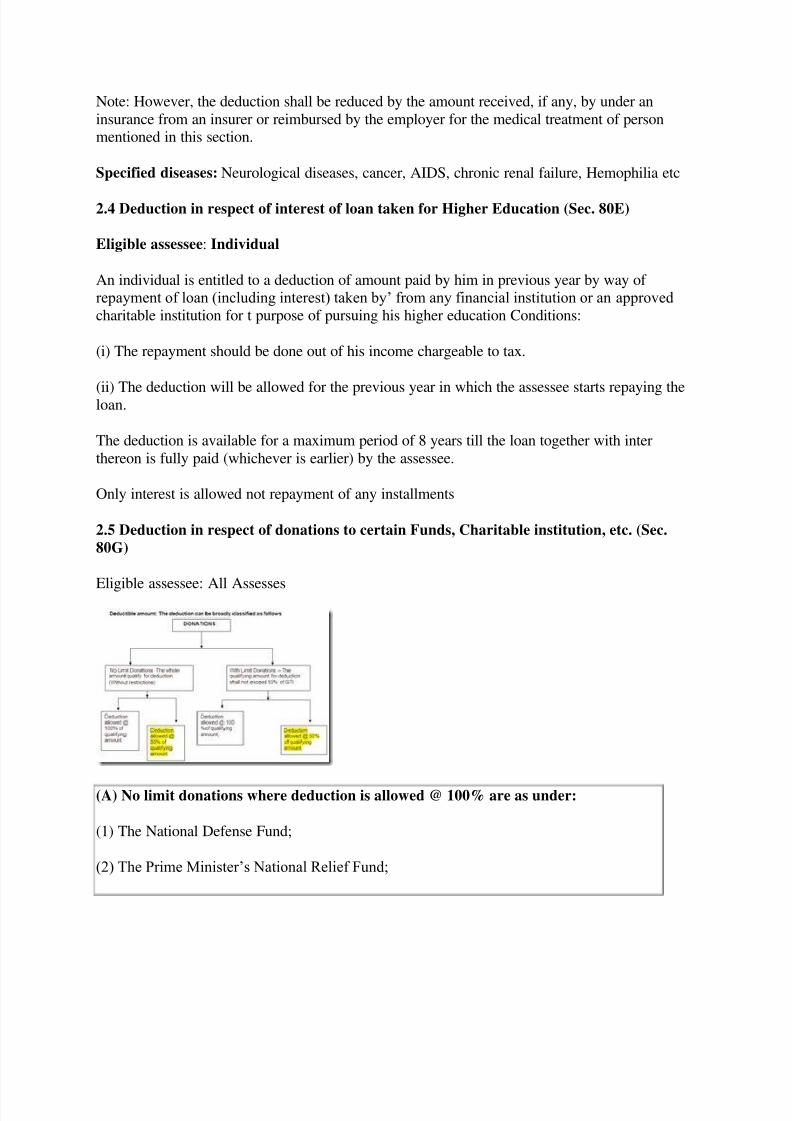

2.5 Deduction in respect of donations to certain Funds, Charitable institution, etc. (Sec.

80G)

Eligible assessee: All Assesses

(A) No limit donations where deduction is allowed @ 100% are as under:

(1) The National Defense Fund;

(2) The Prime Minister‘s National Relief Fund;

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 26/169

(3) The Prime Minister‘s Armenia Earthquake Relief Fund;

(4) The Africa (Public Contributions-India) Fund;

(5) The National Foundation for Communal Harmony;

(6) A University or Educational Institution of national eminence (approved)

(7) The Maharashtra Chief Minister‘s Relief Fund

(8) Zila Saksharta Samitis constituted in any district

(9) The National Blood Transfusion Council

(10) Any Fund set-up by State Govt. to provide medical relief to the poor

(11)The Central Welfare Fund of the Army and Air Force and the Indian Naval BenevolentFund

(12) The Andhra Pradesh Chief Minister‘s Cyclone Relief Fund

(13) The National illness Assistance Fund

(14) The Chief Minister‘s Relief Fund or the Lt. Governor‘s Relief Fund

(15) National Sports Fund

(16) National Cultural Fund

(17)The Fund for Technology Development and Application set-up by the Central

Government; or

(18)Any fund set-up by the State Government of Gujarat exclusively for providing relief to

the victims of earthquake in Gujarat

(19)The National Trust for welfare of persons with Autism, Cerebral Palsy, Mental

Retardation and Multiple Disabilities.

(B) No limit donations where deduction is allowed @ 50% are as under:

(1) Jawahar Lal Nehru Memorial Fund;

(2) Prime Minister‘s Drought Relief Fund;

(3) National Children‘s Fund;

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 27/169

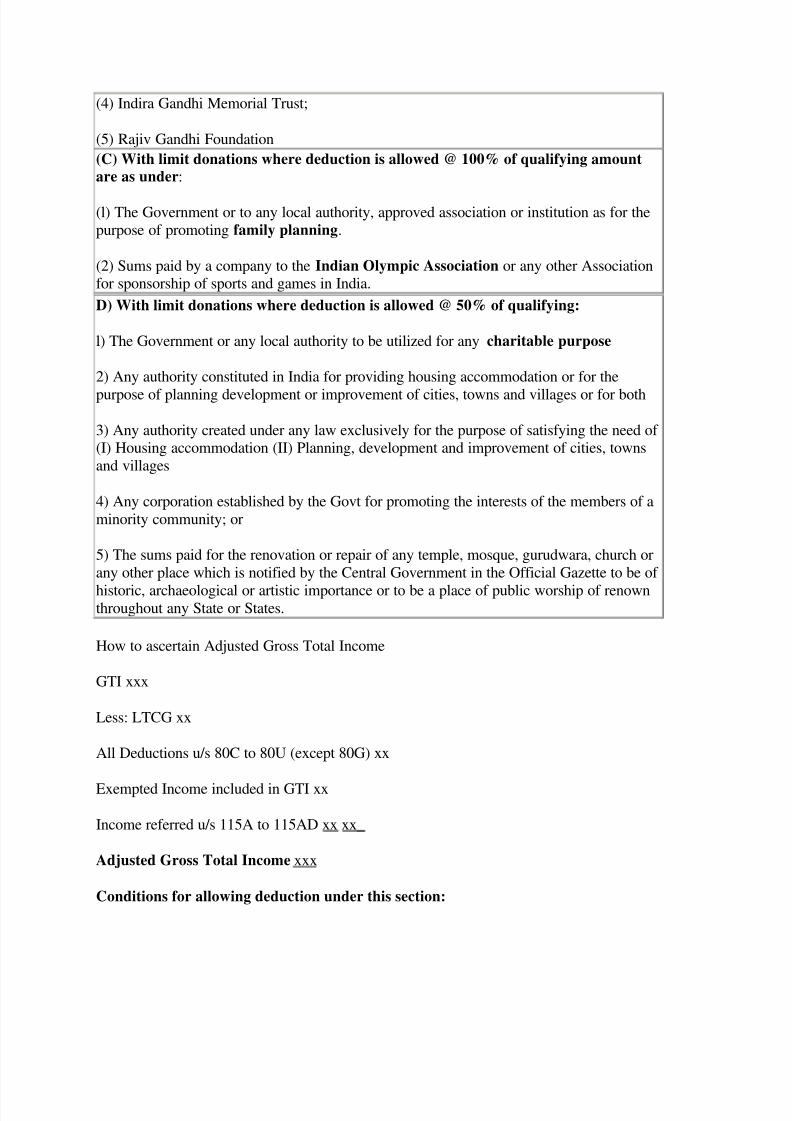

(4) Indira Gandhi Memorial Trust;

(5) Rajiv Gandhi Foundation

(C) With limit donations where deduction is allowed @ 100% of qualifying amount

are as under:

(l) The Government or to any local authority, approved association or institution as for the

purpose of promoting family planning.

(2) Sums paid by a company to the Indian Olympic Association or any other Associationfor sponsorship of sports and games in India.

D) With limit donations where deduction is allowed @ 50% of qualifying:

l) The Government or any local authority to be utilized for any charitable purpose

2) Any authority constituted in India for providing housing accommodation or for the

purpose of planning development or improvement of cities, towns and villages or for both

3) Any authority created under any law exclusively for the purpose of satisfying the need of (I) Housing accommodation (II) Planning, development and improvement of cities, towns

and villages

4) Any corporation established by the Govt for promoting the interests of the members of a

minority community; or

5) The sums paid for the renovation or repair of any temple, mosque, gurudwara, church or

any other place which is notified by the Central Government in the Official Gazette to be of

historic, archaeological or artistic importance or to be a place of public worship of renownthroughout any State or States.

How to ascertain Adjusted Gross Total Income

GTI xxx

Less: LTCG xx

All Deductions u/s 80C to 80U (except 80G) xx

Exempted Income included in GTI xx

Income referred u/s 115A to 115AD xx xx_

Adjusted Gross Total Income xxx

Conditions for allowing deduction under this section:

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 28/169

i) Donations should be in cash, not in kind.

ii) Donation should not be given for the benefit of any particular religion, class, creed,

community, etc. Donation given for the benefit of scheduled castes, scheduled tribes, backward

class or women o children are not for any particular religious community or caste.

Deduction in respect of Rent Paid [80GG]

Eligible assessee: Individual and HUF

An employee who is not in receipt of house Rent Allowance (H R A) from his employer during

the previous year or an individual who is a self employed

Least of the following amounts shall be allowed

(i) Excess of rent paid over 10% of Total Income;

(ii) 25% of Total Income; or

(iii) Rs. 2,000 p.m.

The total income for this purpose means Gross Total Income minus the deductions allowable u/s

80C to 80U (except u/s 80GG)

Deductions for scientific research or Rural development [80GGA]

Eligible Assessee: All Assessees

Deductible amount: 100% of such donation.

Deductions in respect of contributions given by any person to political parties: 80GGB

Only to a company – entire amount is exempt from tax

Deductions in respect of contributions given by any person to political parties: 80GGC

Available to all assessees other than a local authority and any authority or organisation or person

funded by the government – entire amount is exempt from tax

2.6 Deduction in respect of profits and gains from Industrial Undertaking engaged in

infrastructure development [Sec 80- IA]

Deduction under section 80-IA is available only to the following undertakings:

Case 1 Provision of infrastructure facility

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 29/169

Case 2

Case 3

Case 4

Case 5

Telecommunication services

Industrial Parks

Power generation, transmission and distribution or substantial

renovation and modernisation of existing distribution lines

Undertaking set up for reconstruction of a power unit.

An undertaking providing infrastructure facility must satisfy the following conditions-

Conditions 1

Conditions 2

Condition 3

Condition 4

Condition 5

It should provide infrastructure facility

It should be owned by an Indian company

There should be an agreement which the central

Government

It should start operation on or after April 1, 1995

Return of income should be submitted on or before

due date of Submission of return of income

Particulars AMOUNT OF DEDUCTION

1. Provision of infrastructure facility 100 per cent of the profit is deductible for the

first 10 years.

2. Telecommunication services

Assessee- enterprises % of profit deductible Period of deduction

commencing from

the initial assessmentyear

Owned by a company or any

other person

100

30

First 5 years

Next 5 years

3. Industrial parks / Special

economic Zone

100 per cent of profit is

deductible for 10 years

commencing from initialassessment year.

4. Power generation / distribution

100 per cent of profit isdeductible for 10 years

commencing from initial

assessment year.

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 30/169

Deductions in respect of profits and gains by an undertaking or enterprise engaged in

development of Special Economic Zone [Section 80- IAB]

The following conditions should be satisfied-

1.

The taxpayer is a developer of special economic zone2. The gross total income of the taxpayer includes profits and gains derived by anundertaking from any business of developing a special economic zone.

3. Such special economic zone is notified

Amount of deduction- If the above conditions are satisfied, the taxpayer can claim 100 per cent

deduction in respect of the aforesaid profit.

Period of Deduction- The aforesaid deduction is available for 10 consecutive assessment years.

The deduction may be claimed, at the option of the taxpayer, for any 10 consecutive assessment

years out of 15 year beginning from the year in which the special economic zone has been

notified by the central Government.

Deduction in respect of profits and gains from certain industrial undertakings other than

infrastructure development undertakings- [Sec. 80-IB]

Case 1 Business of an industrial undertaking

Case 2 Operation of ship

Case 3 Hotels

Case 4 Industrial research

Case 5 Production of mineral oilCase 6 Developing and building housing projects

Case 7 Business of processing, preservation and packaging of fruits or vegetables

or integrated handling, storage and transportation of food grains units

Case 8 Multiplex theatres

Case 9 Convention centre

Case 10 Operating and maintaining a hospital in rural area

Case 1: Business of an industrial undertaking

Amount of Deduction:

Assessee SSI Industrial Unit or

Cold Storage in

Backward State

Same in

Backward

District

Cold Chain for

Agri goods

Any Other

Company 25% for fist

12 years

100% for first 5 years

and 25% for next 7years

Same Same 25% for first

12 years

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 31/169

Any otherPerson

25% for first10 years

100% for first 5 yearsand 25% for next 5

years

Same Same 25% for first10 years

2. Operation of ship – 30 percent of the profit is deductible for the first 10 years.

3. Hotel –

Assessee % of profit deductible Period of deduction

in a notified area

Any other hotel

50

30

First 10 years

First 10 years

4. Engaged in Indusial Research

approved by the prescribed

authority at any time beforeApril 1, 1999

If the company is approved

by the prescribed authorityafter March 31, 200 but

before April 1, 2007

Amount of deduction

Period of deduction

100 per cent of profit from

such business

5 years beginning with the

initial assessment year

100 per cent of profit from

such business

10 years beginning with the

initial assessment year

5. Production of mineral oil: Amount of deduction- 100 per cent of the profit is deductible forthe first 7 years

6. Developing and building housing projects - If all the aforesaid conditions are satisfied 100per cent of the profit derived in any previous year relevant to any assessment year from such

housing project is deductible.

7. Business of processing, preservation and packaging of fruits or vegetables or integrated

handling, storage and transportation of food grains units

Amount of Deduction- The amount of deduction is given below :

Enterprises % of profit deductible PeriodOwned by a company

Owned by any other person

100

30

100

25

First 5 years

Next 5 years

First 5 years

Next 5 years

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 32/169

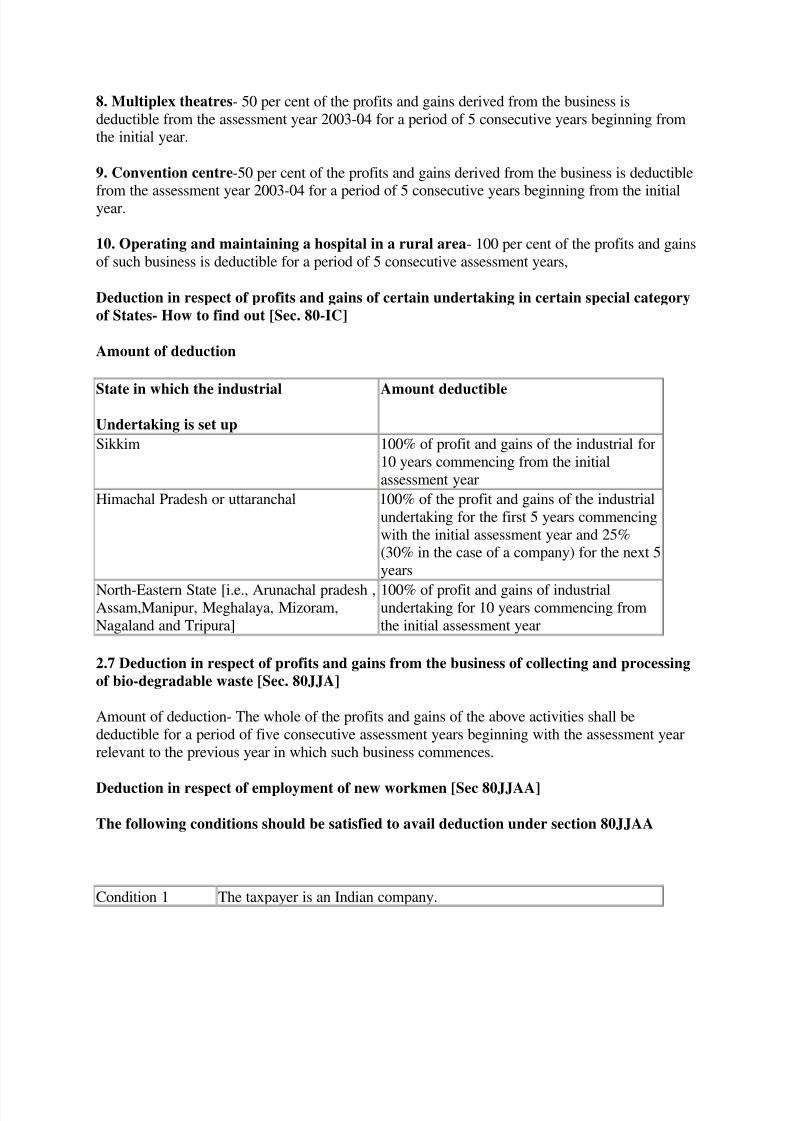

8. Multiplex theatres- 50 per cent of the profits and gains derived from the business is

deductible from the assessment year 2003-04 for a period of 5 consecutive years beginning fromthe initial year.

9. Convention centre-50 per cent of the profits and gains derived from the business is deductible

from the assessment year 2003-04 for a period of 5 consecutive years beginning from the initialyear.

10. Operating and maintaining a hospital in a rural area- 100 per cent of the profits and gains

of such business is deductible for a period of 5 consecutive assessment years,

Deduction in respect of profits and gains of certain undertaking in certain special category

of States- How to find out [Sec. 80-IC]

Amount of deduction

State in which the industrial

Undertaking is set up

Amount deductible

Sikkim 100% of profit and gains of the industrial for

10 years commencing from the initial

assessment year

Himachal Pradesh or uttaranchal 100% of the profit and gains of the industrial

undertaking for the first 5 years commencing

with the initial assessment year and 25%(30% in the case of a company) for the next 5

years

North-Eastern State [i.e., Arunachal pradesh ,Assam,Manipur, Meghalaya, Mizoram,

Nagaland and Tripura]

100% of profit and gains of industrialundertaking for 10 years commencing from

the initial assessment year

2.7 Deduction in respect of profits and gains from the business of collecting and processing

of bio-degradable waste [Sec. 80JJA]

Amount of deduction- The whole of the profits and gains of the above activities shall be

deductible for a period of five consecutive assessment years beginning with the assessment year

relevant to the previous year in which such business commences.

Deduction in respect of employment of new workmen [Sec 80JJAA]

The following conditions should be satisfied to avail deduction under section 80JJAA

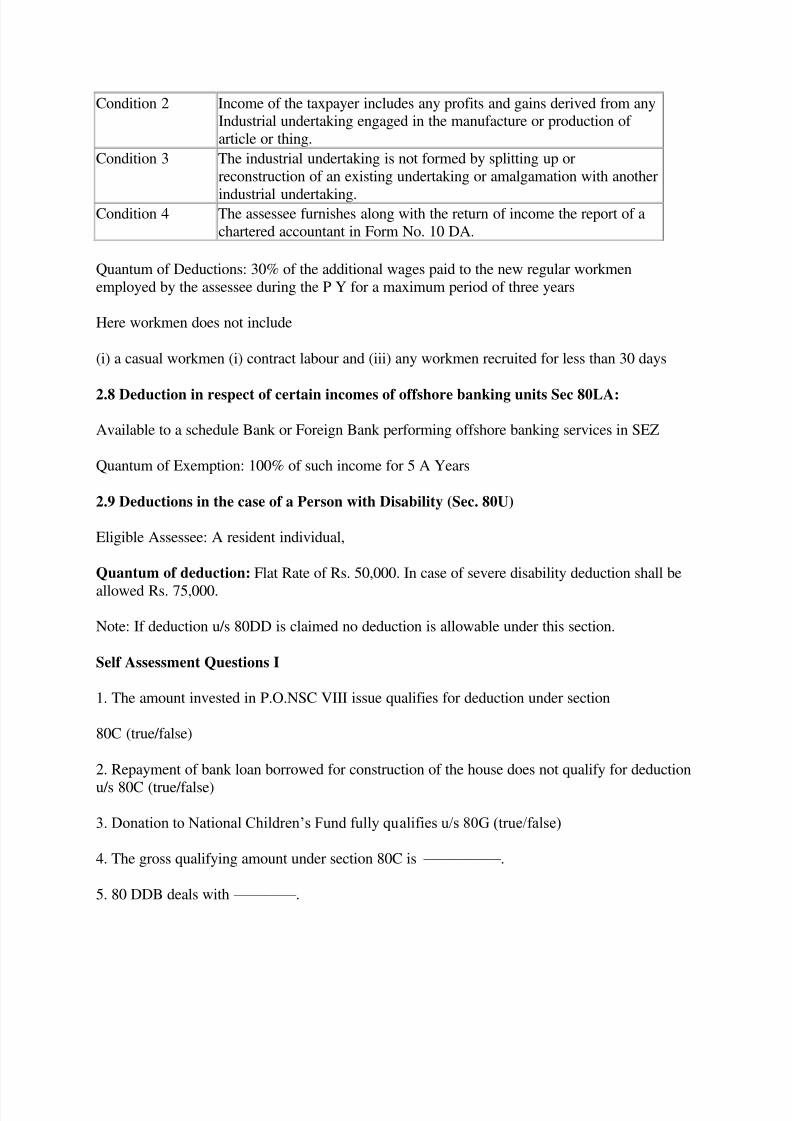

Condition 1 The taxpayer is an Indian company.

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 33/169

Condition 2 Income of the taxpayer includes any profits and gains derived from anyIndustrial undertaking engaged in the manufacture or production of

article or thing.

Condition 3 The industrial undertaking is not formed by splitting up or

reconstruction of an existing undertaking or amalgamation with another

industrial undertaking.Condition 4 The assessee furnishes along with the return of income the report of a

chartered accountant in Form No. 10 DA.

Quantum of Deductions: 30% of the additional wages paid to the new regular workmen

employed by the assessee during the P Y for a maximum period of three years

Here workmen does not include

(i) a casual workmen (i) contract labour and (iii) any workmen recruited for less than 30 days

2.8 Deduction in respect of certain incomes of offshore banking units Sec 80LA:

Available to a schedule Bank or Foreign Bank performing offshore banking services in SEZ

Quantum of Exemption: 100% of such income for 5 A Years

2.9 Deductions in the case of a Person with Disability (Sec. 80U)

Eligible Assessee: A resident individual,

Quantum of deduction: Flat Rate of Rs. 50,000. In case of severe disability deduction shall be

allowed Rs. 75,000.

Note: If deduction u/s 80DD is claimed no deduction is allowable under this section.

Self Assessment Questions I

1. The amount invested in P.O.NSC VIII issue qualifies for deduction under section

80C (true/false)

2. Repayment of bank loan borrowed for construction of the house does not qualify for deduction

u/s 80C (true/false)

3. Donation to National Children‘s Fund fully qualifies u/s 80G (true/false)

4. The gross qualifying amount under section 80C is ————— .

5. 80 DDB deals with ———— .

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 34/169

6. A person with severe disability is given deduction u/s 80U which is equal to Rs. —–

2.10 Exemptions: Tax-Free Incomes

An assessee need not pay tax on all his incomes. Some of his incomes are exempt from tax. Such

incomes are called incomes exempt from tax or tax-free incomes. Tax-free incomes are coveredby Section 10 of the Income-tax Act.

The various incomes exempt from income-tax are:

Sec. 10 (1): .Agricultural income is exempt from income-tax. In some cases agricultural income

is taken into consideration to find out tax on non- agricultural income.

Sec.10 (2): any sum received by a member of the Hindu undivided family either out of the

income of the H.U.F. or out of the income of the estate belonging to the H.U.F. is fully exempt

from income-tax. Such receipts are not taxable in the hands of an individual member, even if

they have not been taxed in the hands of the H.U.F.

Sec.10 (2A): The share of income of a partner in the total income of the firm, which is separatelyassessed to tax, is fully exempt from tax.

Sec. 10(5 ): Leave travel concessions.

Sec. 10 (7): Any allowance paid or allowed outside India by the Govt. to an Indian citizen forrendering service outside India is wholly exempt from tax.

Sec. 10 (10): Gratuity: See Unit 3

Sec. 10 (10A), 10 (AA): Pension and leave salary: See Unit 3

Sec. 10 (10B): Retrenchment compensation; See unit 3

Sec. 10 (10C): Compensation received at the time of voluntary retirement: See unit 3

Sec. 10 (10CC): Tax on perquisite paid by the employer:

Sec. 10 (10D): Amount paid by life insurance companies:

Sec. 10 (11), (12), (13): payment from provident fund, superannuation fund: See unit 3.

Sec. 10 (13A): House rent allowance: See unit 3

Sec. 10(14): Special allowance; See unit 3

Sec. 10 (15): Interest on securities. See unit: 7

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 35/169

Sec. 10 (16): Educational scholarships:

Sec. 10 (17): Daily allowance to Members of Parliament

Sec. 10 (17A): Scientific and artistic work awards instituted by the Central Government or by

any State Government are exempt from Income-tax.

Sec. 10 (18), (19): i) Pension received by an individual who has been in the service of the

Central or State Government and has been awarded ―Param Vir Chakra‖ or ―Maha Vir Chakra‖

or ―Vir Chakra‖ or such other gallantry award as the Central Government may, by notification inthe official gazette, specify in this behalf, and ii) family pension received by any member of the

family of such individual, will be exempt from tax .

Sec 10 (31): Subsidy received by an assessee engaged in the business of growing and

manufacturing rubber, coffee, cardamom or such other plantation crops as may be notified by the

Central Government is exempt from tax, provided the subsidy is received from the concerned

Board, it (i.e., the subsidy) is used for re plantation or replacement of rubber plants, coffee plantsor cardamom plants or for rejuvenation or consolidation of areas, and the assessee furnishes to

the assessing officer, along with the return of income, a certificate from the concerned Board

stating the amount of subsidy received during the previous year.

Sec. 10 (32): Income of minor child included in the income of individual is exempted up to Rs.

1,500 in respect of each such minor child or income of such minor child whichever is lower.

Sec.10 (33): Capital gains on the transfer of US64

Sec. 10 (34), (35): Income by way of dividends from domestic company or any income from the

units of Unit Trust of India, and the income received from the units of mutual funds specifiedunder Section 10 (23D) of the Income-tax Act are exempt from tax.

Sec. 10 (37): Capital gain on compulsory acquisition of urban agricultural land: only toindividuals and HUFs., provided such agricultural land was used by the assessee (or by his

parents) for agricultural purposes during 2 years immediately prior to transfer.

Sec. 10 (38): Long term capital gains on transfer of listed equity shares/ units covered by

securities transaction tax.

2.11 Exemptions U/s 10A, 10AAA, 10B

Newly established Under takings in Free trade zone: Electronic hardware technology park orsoftware technology park, special economic zone Sec. 10A

Subject to the fulfillment of certain conditions the profits and gains calculated as below is

allowed to be deducted from his total income for a period of 10 consecutive assessment years

beginning with the assessment year relevant to the previous year in which the undertaking begins

to manufacture or produce such articles or things or computer software.

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 36/169

Newly established units in Special Economic Zone: Sec. 10AA

Income from export of articles or thing or from services from such unit is deducted to the

following extent, subject to the fulfillment of certain conditions.

100% of the profit is deductible for a period of five assessment years, 50% for next five

assessment years.

Newly established 100% export oriented undertakings: Sec. 10B

Undertakings approved by the Board, is eligible for the deduction for a period of 10 consecutive

assessment years beginning with the assessment year relevant to the previous year in which the

undertaking begins to manufacture or produce such articles.

The profit eligible for deduction is calculated as per deduction computed u/s 10A (previous para)

2.12 Rebate u/s 88 E

Rebate of income tax in respect of securities Transaction Tax:

Tax paid on taxable securities transactions; or tax payable on income from taxable securitiestransactions at an average rate of tax, whichever is lower is allowed as a rebate and shall be

deducted from the amount of income tax.

2.13 Summary

Various deductions are available for savings, certain expenses, certain sources of incomes. Allthese savings, investments, incomes subject to certain conditions, can be claimed by the assessee

as deductions and see that his taxable total income is reduced hence his tax liability also.

2.14 Terminal Questions

2.15 Answers to SAQs and TQs

SAQ’s

1) True

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 37/169

2) False

3) True

4) 1, 00,000

5) Deduction in respect to Medical Treatment

6) Rs. 75,000

TQs

1) Refer 2.2

2) Refer 2.5

3) Refer 2.4

4) Refer 2.11

Copyright © 2009 SMU

Powered by Sikkim Manipal University

.

MF0003-Unit-03-Income from Salaries Unit 3 Income from Salaries

Structure:

3.1 Introduction

Objectives

3.2 Chargeability

3.3 Basis of charge of salary income

· Salary [Sec. 17(1)

3.4 Different Forms of salaries

· Advance salary

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 38/169

· Arrear salary

· Fees and commission

· Bonus

· Death Cum Retirement gratuity

· Leave salary of encashment of earned leave

· Compensation for retrenchment

· Tax paid by the4 employer on the value of perquisites [sec 10(10CC)]

· Salary and Pension from UNO

3.5 Allowances

3.6 Perquisites

Self Assessment Question

3.7 Who are specified employees?

3.8 Profits in Lieu of Salary

3.9 Deductions from cross income from salary

3.10 Provident Fund

3.11 Summary

3.12 Terminal Questions

3.13 Answers to SAQs and TQs

3.1 Introduction

Major number of assessees is from salaried class. Though they receive their dues in the form of cash or in kind, much of the receipts and value received in kind are not taken for tax purpose.

Hence it necessary to understand the meaning of salary and its chargeability.

Any remuneration paid by an employer to his employee in consideration of his services in called

salary. It also includes monetary value of those benefits and facilities provided by the employerwhich are taxable.

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 39/169

Objectives:

· After studying this unit you will be able to understand the concept of salary income

· The various concepts involved in computation of taxable salary

· The relevance of provident fund in savings

· The application of bargaining techniques with the employer

Under Section 15, the following incomes are taxable under the head ‘Salaries’:

(a) The salary due from an employer or former employer to an assessee in the previous year,

whether paid or not;

(b) The salary paid or allowed to him in the previous year by or on behalf of an employer or a

former employer though not due or before it becomes due to him; eg. Advance Salary

(c) Any arrears of salary paid or allowed to him in the previous year by or on behalf of an

employer or a former employer, if not charged to income tax for any earlier previous year.

Tax planning hints

While fixing the salary to his employee, the employer has to keep two factors in his mind. First

factor, make sure that the compensation payable to the employee must be a deductible

expenditure while computing the income from business or profession of the employer. On otherhand, make sure even the package received by the employee is taxable in their hand at lesser

rates to reduce their overall tax liability i.e., focus should be reduction of their tax liability and tomaximise their take home salary.

3.2 Chargeability

Any Remuneration paid by an employer to his employee in consideration of his services is called

salary. It includes monetary values of those benefits and facilities provided by the employer,

which are taxable

3.3 Basis of charge of salary income

Income is chargeable under this head on due basis or receipt basis whichever is earlier

· Salary [Sec. 17(1)

Salary includes;

· Wages; bonus; fees; commission

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 40/169

· any annuity or pension;

· any gratuity;

· taxable allowances;

· value of perquisites

· profit in lieu of salary;

· any advance of salary; but not loan for purchasing a car, cycle, scooter or a house; etc

· any arrears of salary;

· Employer‘s contribution to Recognised Provident fund account of employee in excess of 12%

of the employee‘s salary and interest credited during the year on provident fund in excess of

9.5%.

· The contribution made by the Central Government in the previous year, to the account of an

employee (who joins on or after 1.1.2004), under a pension scheme.

Tax Planning: Where employee takes salary in advance, it is added in the salary income of the

previous year in which it is taken. This increases tax liability of the employee. Hence, instead of advance salary, a loan may be taken from employer. (Loan is not added in the salary income for

tax purpose. Even interest free loan or interest on concessional loan is tax free, if the amount of

loan in aggregate does not exceed Rs. 20,000 during the previous year.)

3.4 Different Forms of salaries

=>Advance Salary Advance salary is taxable on receipt basis, in the year, which it is drawn.

=>Arrear Salary It is taxable on receipt basis, if the same has not been subjected to tax earlieron due basis.

=>Fees and Commission

This is paid by an employer to his employee for doing any extra work (not over time) other than

the job assigned to him as an employee. It will be included under the head salaries in

computation income of the employee.

=>Bonus: It is taxable as salary in the year of receipt, if it has not been taxed earlier on due

basis.

=>Death cum Retirement Gratuity

Death cum Retirement Gratuity [Sec.17 (1) iii]

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 41/169

Tax planning: If an employee is due for retirement shortly, it is better to go for commutation of

pension as per the above stated rules. Because pension (un-commuted) received by all employees

(govt. and non govt.) during their life time is included in the salary income and chargeable to tax.

=>Leave Salary or Encashment of earned leave Cash equivalent of leave salary payable to an

employee of the central and the sate government in respect of the earned leave at his credit at thetime of his retirement whether on superannuation or otherwise (e.g. by resigning), is exempt

from tax.

The least of the following is exempt from tax:

Particulars Amount

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 42/169

1. Maximum of 10 month‘s salary on the basis of theaverage salary drawn by the employee during 10

months preceding his retirement on superannuation

or otherwise2. Average salary x Approved Period Maximum or

Statutory limit3. Amount actually received

xxx

xxx

Rs. 3,00,000

xxx

Approved period: Earned leave entitlement cannot exceed 30 days for every year of actualservice

Salary: Basic pay + Dearness Allowance (given in terms of employment) + Commission

achieved on fixed percentage of turnover

Tax Planning

If a Govt. employee is due for retirement shortly, it is better for him not to encash his salary

while he is in service. This is because he can avoid paying tax on leave encashment which he

receives at the time of retirement. Even an employee in private service gets exemption for amajor part of the amount received as leave encashment. In this connection employee should also

consider the loss of interest on the amount which is not taking to save tax.

=>Compensation for Retrenchment [Sec10 (10B)]

Any compensation received by a workman under Industrial Disputes Act, 1947; at the timeretrenchment is exempt from the tax to the extent of the least of the following:

Particulars Amount

1. An amount calculated in accordance

with Sec 25F(b) of the industrial

dispute act 1947; or2. Statutory Limit (as the central

government notified in this behalf)

3. Actual amount of compensationreceived by the employee

XXX

5,00,000

XXX

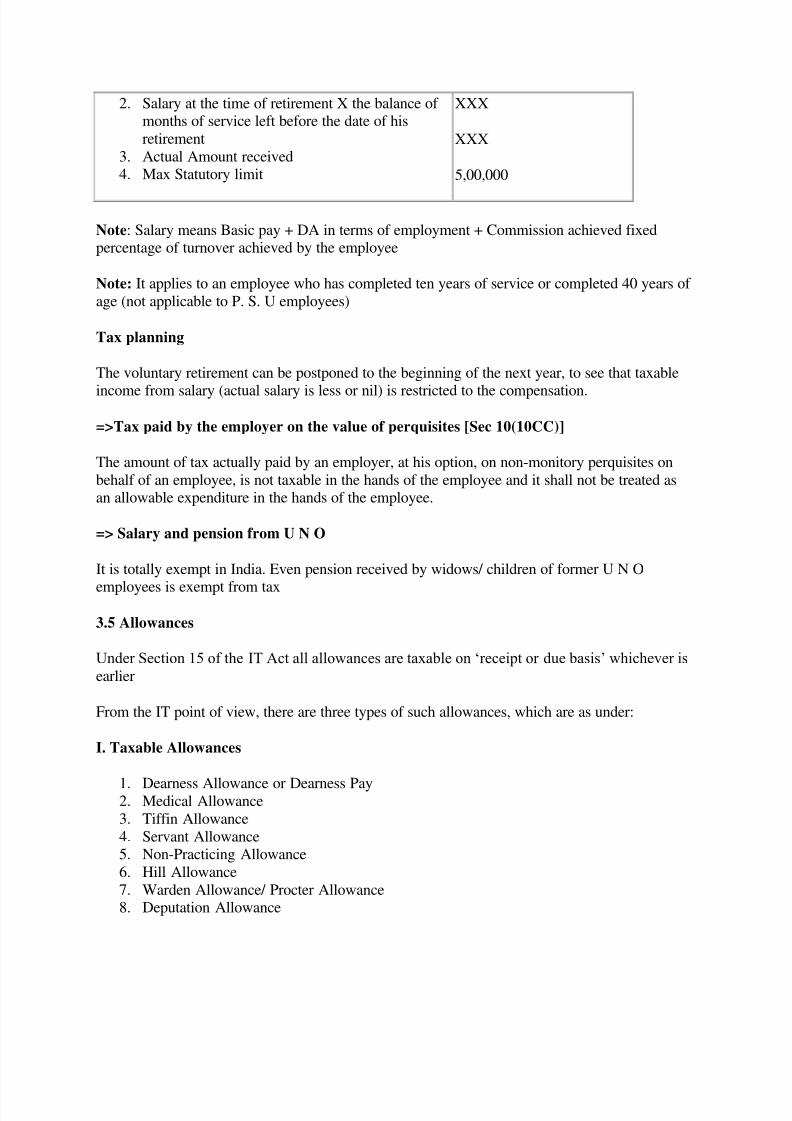

Receipts of employees on voluntary retirement [Sec10 (10C)]

The least of the following is exempt from tax:

Particulars Amount

1. Three months salary X Each completed year of

service

XXX

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 43/169

2. Salary at the time of retirement X the balance of months of service left before the date of his

retirement

3. Actual Amount received4. Max Statutory limit

XXX

XXX

5,00,000

Note: Salary means Basic pay + DA in terms of employment + Commission achieved fixedpercentage of turnover achieved by the employee

Note: It applies to an employee who has completed ten years of service or completed 40 years of

age (not applicable to P. S. U employees)

Tax planning

The voluntary retirement can be postponed to the beginning of the next year, to see that taxable

income from salary (actual salary is less or nil) is restricted to the compensation.

=>Tax paid by the employer on the value of perquisites [Sec 10(10CC)]

The amount of tax actually paid by an employer, at his option, on non-monitory perquisites on

behalf of an employee, is not taxable in the hands of the employee and it shall not be treated asan allowable expenditure in the hands of the employee.

=> Salary and pension from U N O

It is totally exempt in India. Even pension received by widows/ children of former U N O

employees is exempt from tax

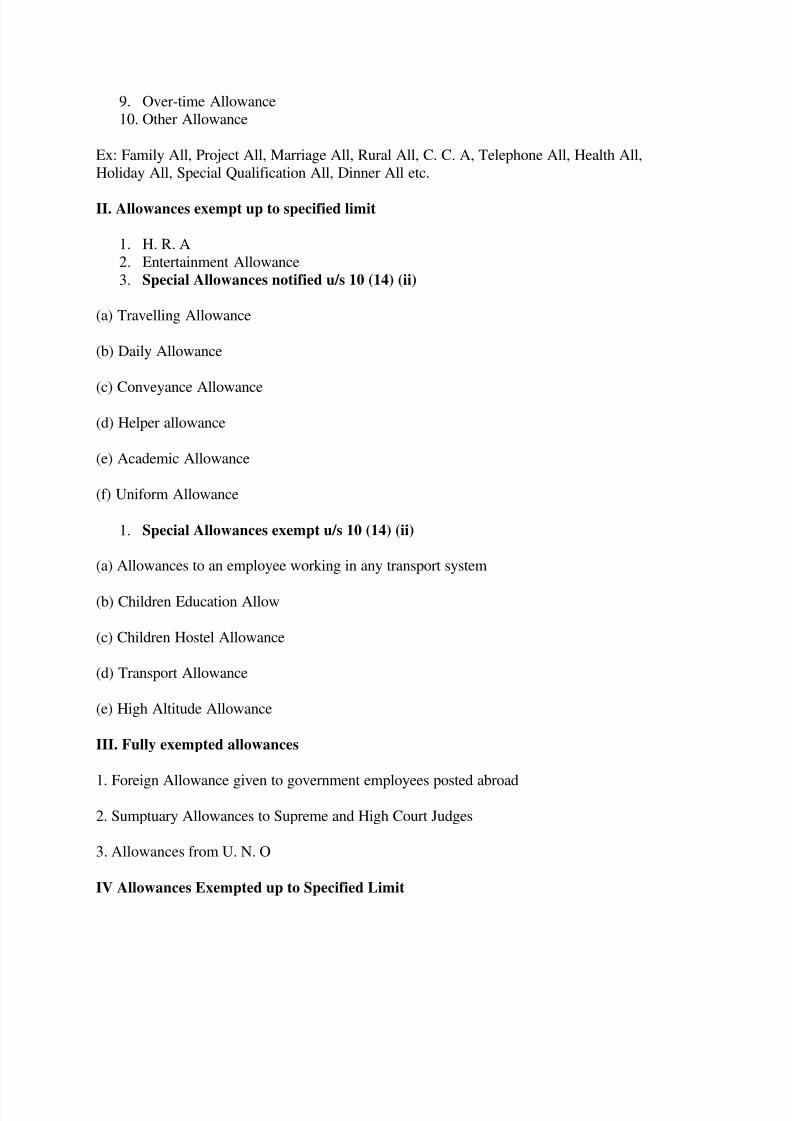

3.5 Allowances

Under Section 15 of the IT Act all allowances are taxable on ‗receipt or due basis‘ whichever is

earlier

From the IT point of view, there are three types of such allowances, which are as under:

I. Taxable Allowances

1. Dearness Allowance or Dearness Pay2. Medical Allowance

3. Tiffin Allowance

4. Servant Allowance5. Non-Practicing Allowance

6. Hill Allowance

7. Warden Allowance/ Procter Allowance8. Deputation Allowance

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 44/169

9. Over-time Allowance

10. Other Allowance

Ex: Family All, Project All, Marriage All, Rural All, C. C. A, Telephone All, Health All,

Holiday All, Special Qualification All, Dinner All etc.

II. Allowances exempt up to specified limit

1. H. R. A

2. Entertainment Allowance

3. Special Allowances notified u/s 10 (14) (ii)

(a) Travelling Allowance

(b) Daily Allowance

(c) Conveyance Allowance

(d) Helper allowance

(e) Academic Allowance

(f) Uniform Allowance

1. Special Allowances exempt u/s 10 (14) (ii)

(a) Allowances to an employee working in any transport system

(b) Children Education Allow

(c) Children Hostel Allowance

(d) Transport Allowance

(e) High Altitude Allowance

III. Fully exempted allowances

1. Foreign Allowance given to government employees posted abroad

2. Sumptuary Allowances to Supreme and High Court Judges

3. Allowances from U. N. O

IV Allowances Exempted up to Specified Limit

8/3/2019 MF0003 Taxation

http://slidepdf.com/reader/full/mf0003-taxation 45/169

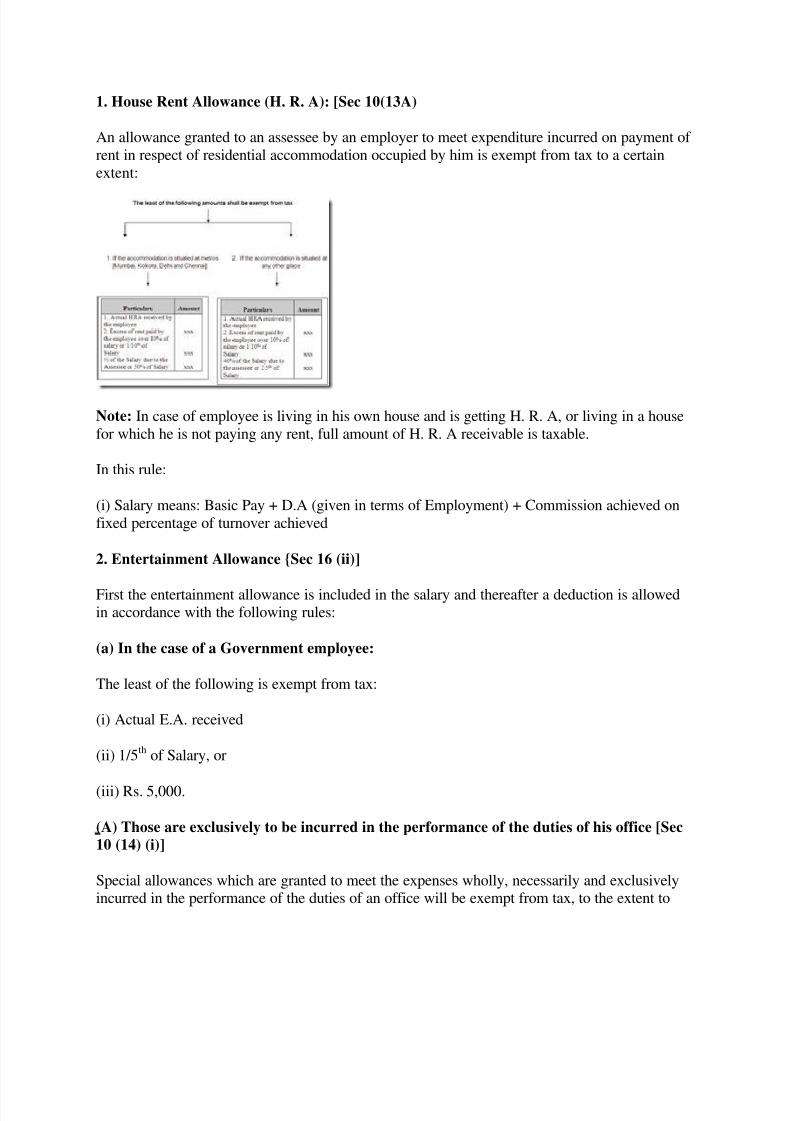

1. House Rent Allowance (H. R. A): [Sec 10(13A)

An allowance granted to an assessee by an employer to meet expenditure incurred on payment of

rent in respect of residential accommodation occupied by him is exempt from tax to a certain

extent:

Note: In case of employee is living in his own house and is getting H. R. A, or living in a house

for which he is not paying any rent, full amount of H. R. A receivable is taxable.

In this rule:

(i) Salary means: Basic Pay + D.A (given in terms of Employment) + Commission achieved on

fixed percentage of turnover achieved

2. Entertainment Allowance {Sec 16 (ii)]

First the entertainment allowance is included in the salary and thereafter a deduction is allowedin accordance with the following rules:

(a) In the case of a Government employee:

The least of the following is exempt from tax:

(i) Actual E.A. received

(ii) 1/5th of Salary, or

(iii) Rs. 5,000.