mexico – beverages m soft drink industry · when job losses were rampant and competition...

TRANSCRIPT

Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

Latin American Equity Research Sector Report

New York, September 17, 2004 Mexico – Beverages

MEXICAN SOFT DRINK INDUSTRY A Closer Look at the Coke Bottlers: A Perfect Storm? Alexander Robarts Alonso Aramburú (212) 350-0723 (212) [email protected] [email protected]

In this report, we analyze the fundamentals of the Mexican bottling sector into 2005 and remain cautious despite an expected moderate recovery in consumption. We are lowering our earnings estimates on Coca-Cola Femsa (KOF), introducing our 2005 target price, and downgrading the stock to Hold from Buy. We are also initiating coverage on Arca and Contal, both with Underperform ratings.

• Our new sector concern is our expectation for incremental margin pressure in the next six months from rising raw material prices, particularly PET resin, and sugar, which account for approximately 40% of cash cost of sales. During the second half of 2004, we expect PET resin prices to be significantly higher year on year on the back of the surge in oil prices, leading to an estimated 160-170 basis point gross margin reduction on a pro forma basis.

• Prolonged intense competition leads us to estimate real price declines in 2005 for the third consecutive year (we had estimated in line with inflation). PBG Mexico has a new CEO and a new marketing campaign. B-brand producer Kola Real expects its new plant in Monterrey to be operational by February 2005 and to double its installed capacity by 2006.

• The ongoing industry shift toward lower margin one-way packages should further pressure gross margins.

• However, soft drink and water industry volume growth in Mexico should begin to recover during 2H04 after contracting 1.5% during 1H04, ending the year flat. Our Mexico-based economics team forecasts non-durable consumption spending growth to stabilize in 2H04, after a decelerating 1Q04 and a modest acceleration in 2Q04.

• In the current difficult operating environment, we believe revenue management and cost cutting will be even more critical to profit growth. Furthermore, we think industry consolidation could accelerate as economies of scale and financial resources become increasingly important competitive advantages.

• In the context of a weak bottling sector, we expect KOF to outperform Arca and Contal. In our view, KOF’s economies of scale, solid execution and revenue management capabilities give it a superior platform to outperform its peers in a highly competitive environment. We believe KOF has mostly contained the competitive threats, while Arca and Contal should begin to face intensifying competition from Kola Real in 1Q05. Also, KOF’s non-Mexican assets enjoy improving economic conditions and should post EBITDA growth faster than in Mexico. However, in our view, these positives are more than offset by new concerns that lead us to downgrade the stock to Hold from Buy. We now expect a significant increase in raw material costs in 2H04 and slower water volume growth. We also incorporate management’s warning on its 2Q04 results conference call that net cost synergies with Panamco would be US$20 million less than expected and that the expected US$50 million in savings from best practices should not be attainable in 2005.

Mexican Coca-Cola Bottlers (U.S. Dollars in Millionsa) Price Target Upside/ Net Earnings P/E FV/EBITDA Mkt. Company Rec. 09/14/04 Price Down 2003 2004E 2005E 2003 2004E 2005E 2003 2004E 2005E Cap Arca Uperf 1.89 1.90 6.1% 90 121 109 17.0 12.6 14.0 5.3 5.5 5.4 1,523 KOF Hold 20.71 23.00 12.4% 208 253 310 17.0 15.1 12.3 8.4 7.3 6.7 3,824 Contal Uperf 1.56 1.55 5.3% 102 83 84 11.4 14.0 13.9 5.3 5.8 5.8 1,168 Average NM NM NM 8.3% 133 152 168 14.5 13.0 12.9 6.0 6.0 5.8 NMa Except per share/ADR amounts. NM Not meaningful. Sources: Company reports and Santander Investment estimates.

A Closer Look at the Coke Bottlers: A Perfect Storm

2 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

TABLE OF CONTENTS

Water to Outpace Carbonated Soft Drinks ....................................................................... 4 Pricing Outlook: No Improvement Expected ................................................................... 7 Pepsi Bottling Group (PBG)............................................................................................. 7 Kola Real .......................................................................................................................... 8 Raw Material Prices to Pressure Gross Margins .............................................................. 9 Containing the Non-Returnable Packaging Trend.......................................................... 11 Industry Consolidation to Continue................................................................................ 12

Consumption Outlook............................................................................................................ 15 Arca........................................................................................................................................ 17

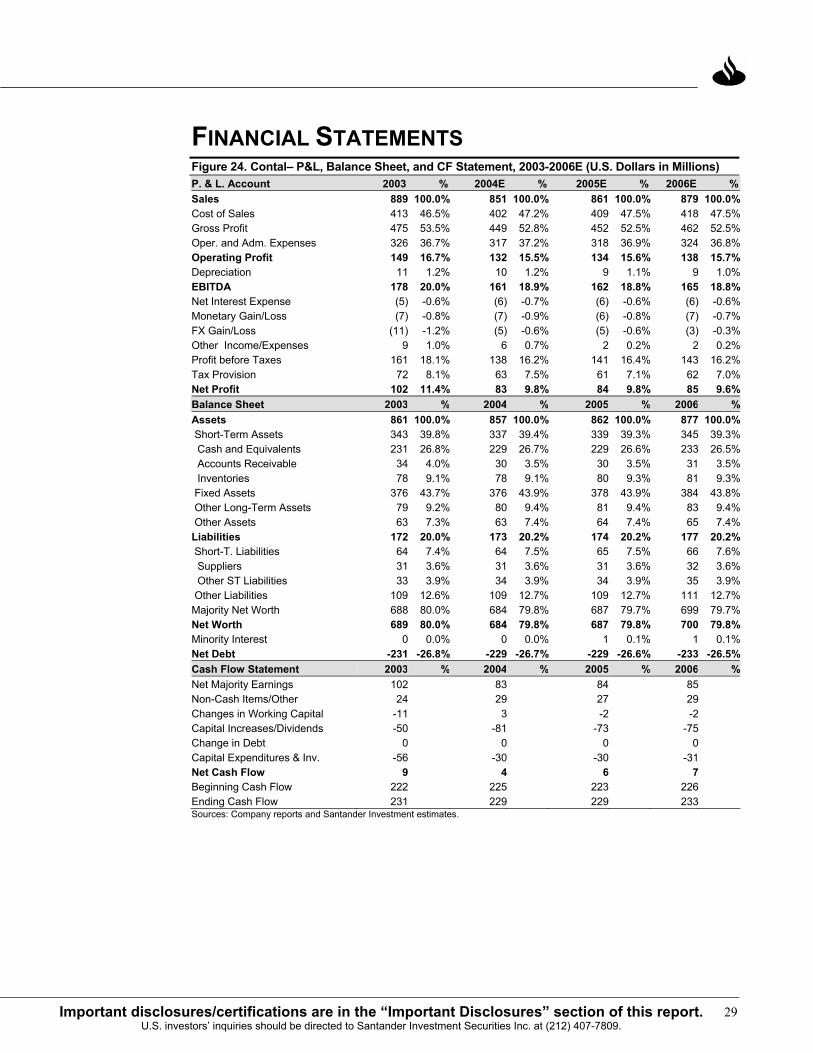

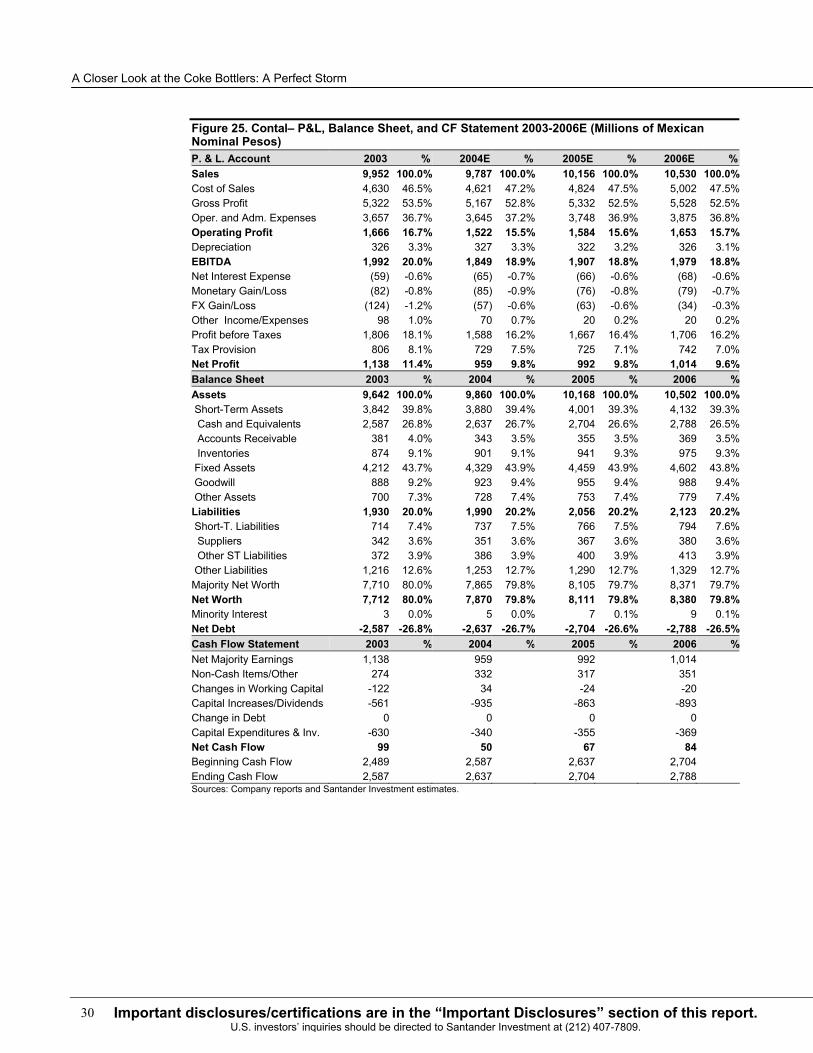

Financial Statements ................................................................................................. 22 Contal..................................................................................................................................... 25

Financial Statements ................................................................................................. 29

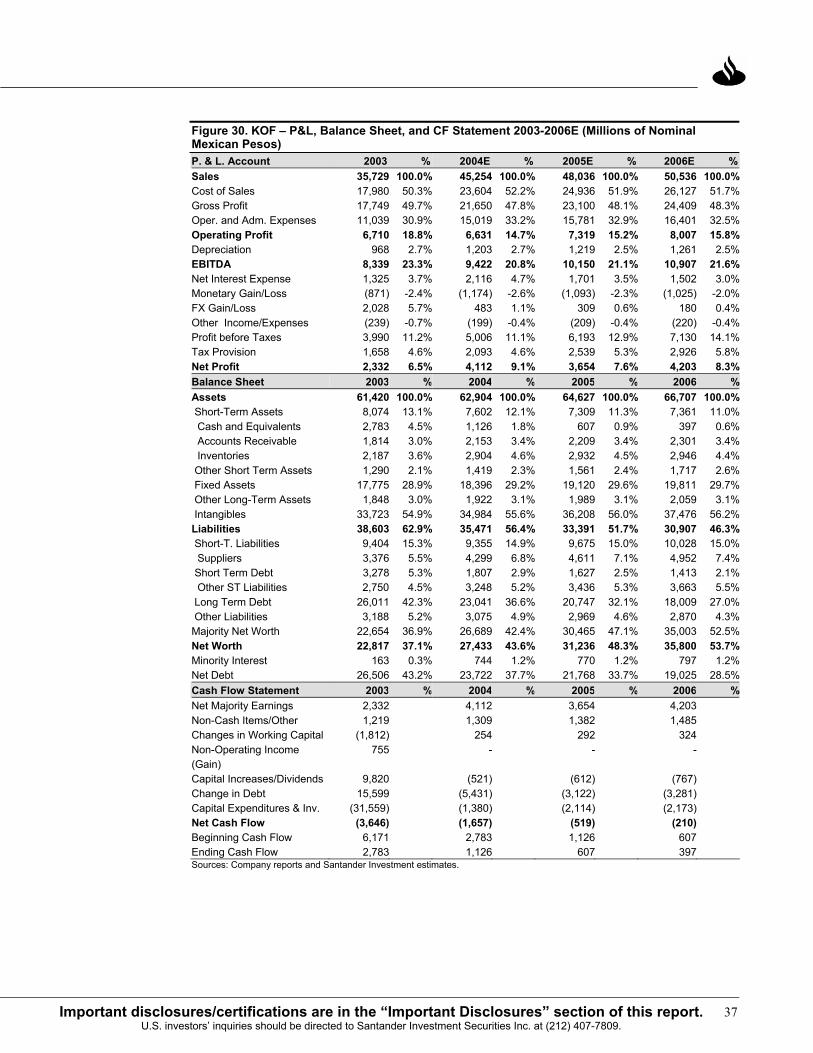

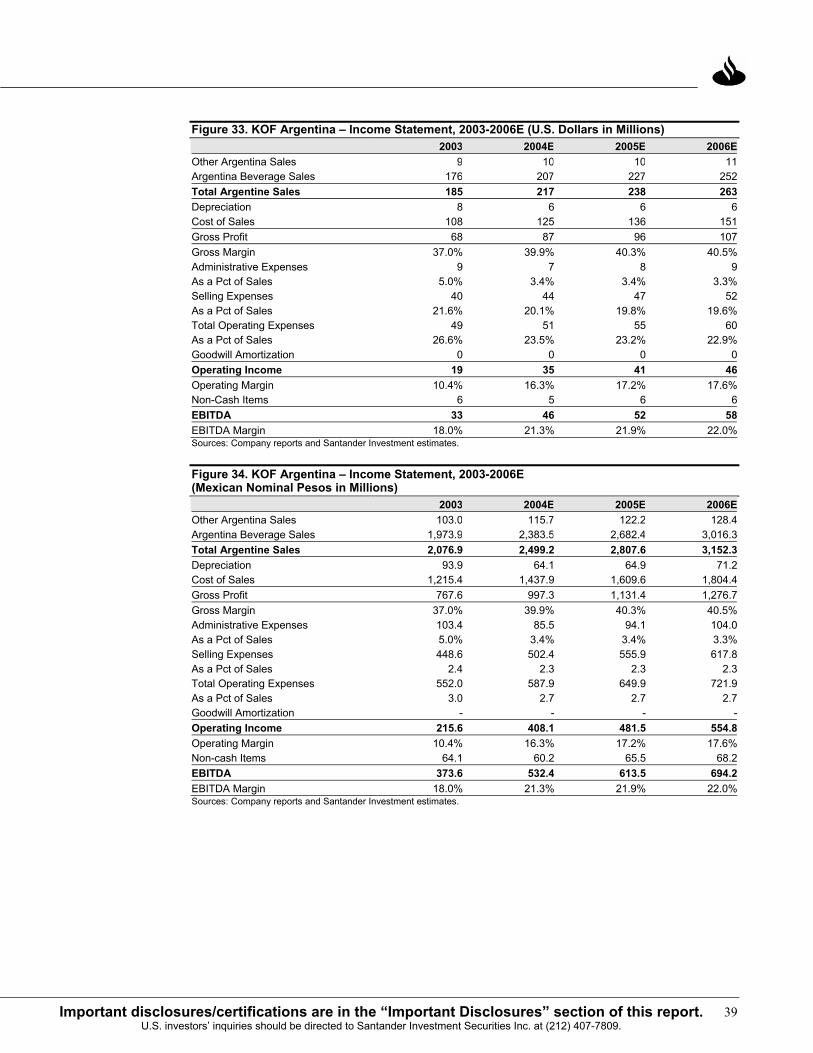

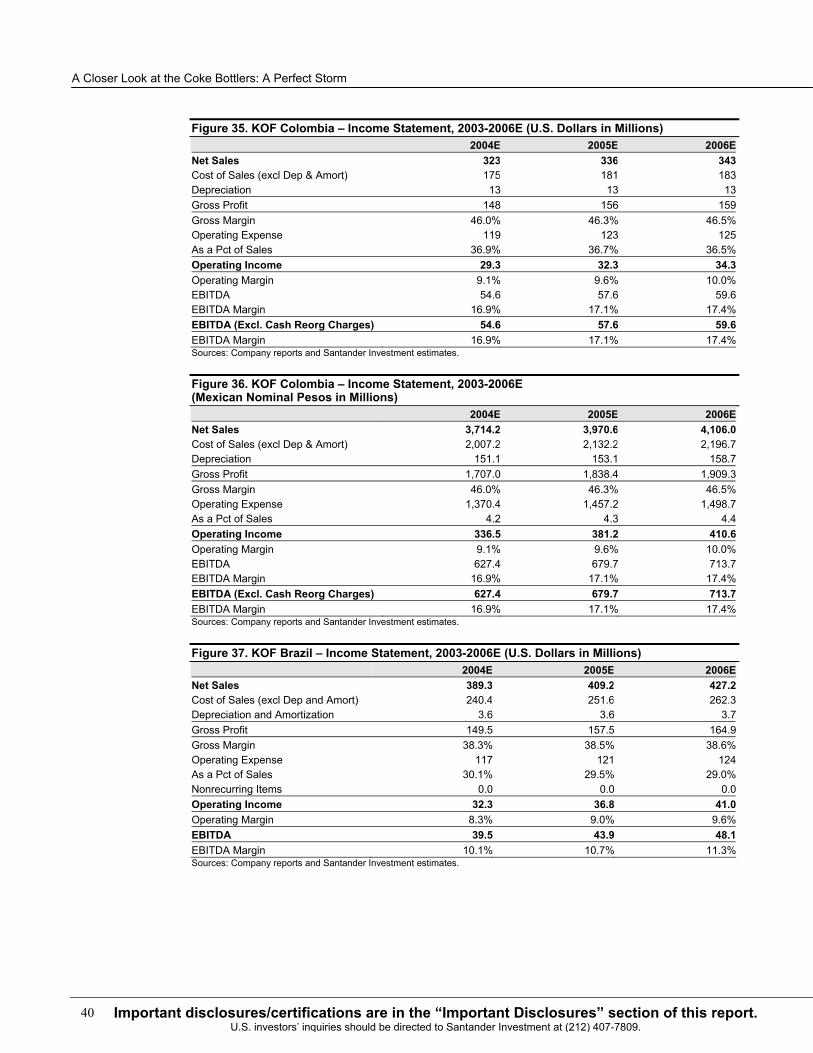

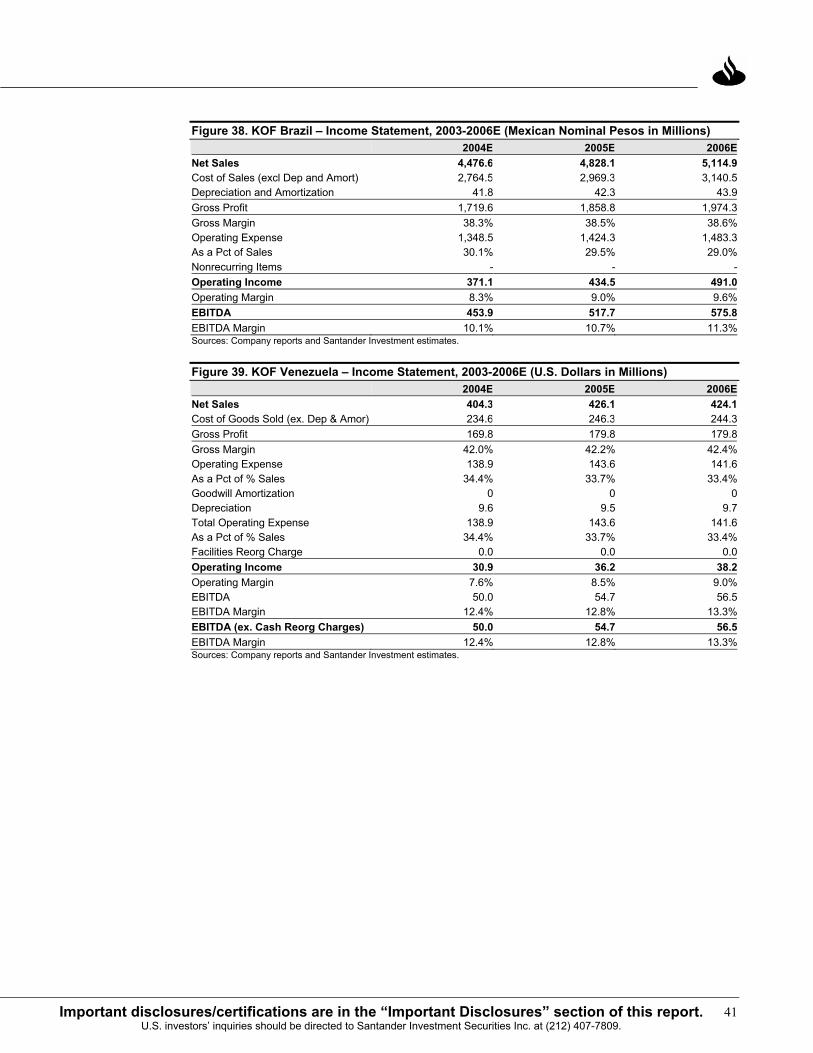

Coca-Cola Femsa................................................................................................................... 31 Financial Statements ................................................................................................. 36

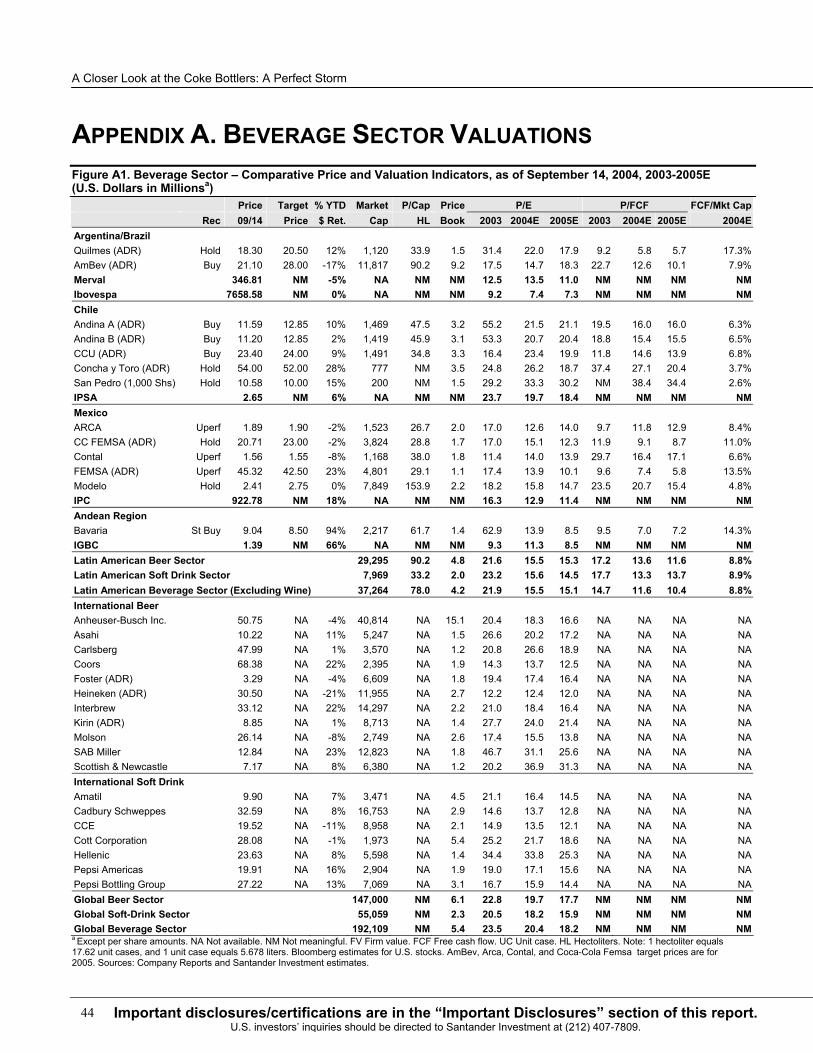

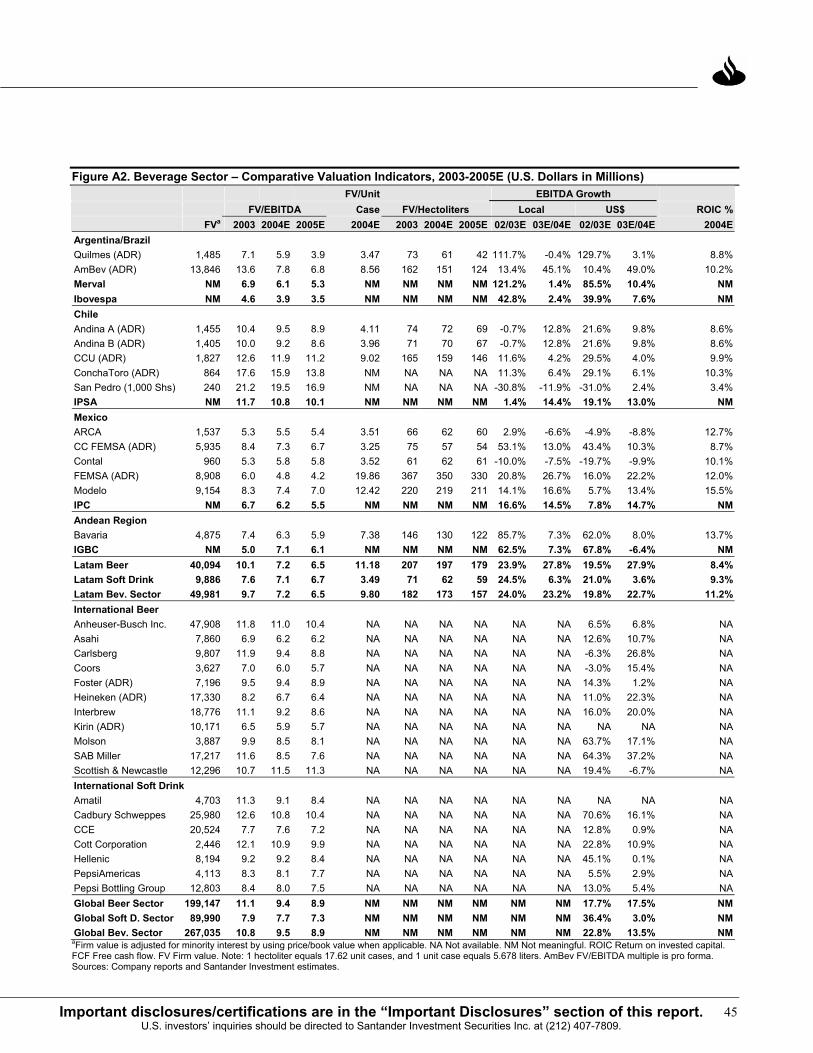

Appendix A. Beverage Sector Valuations ............................................................................. 43

3Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

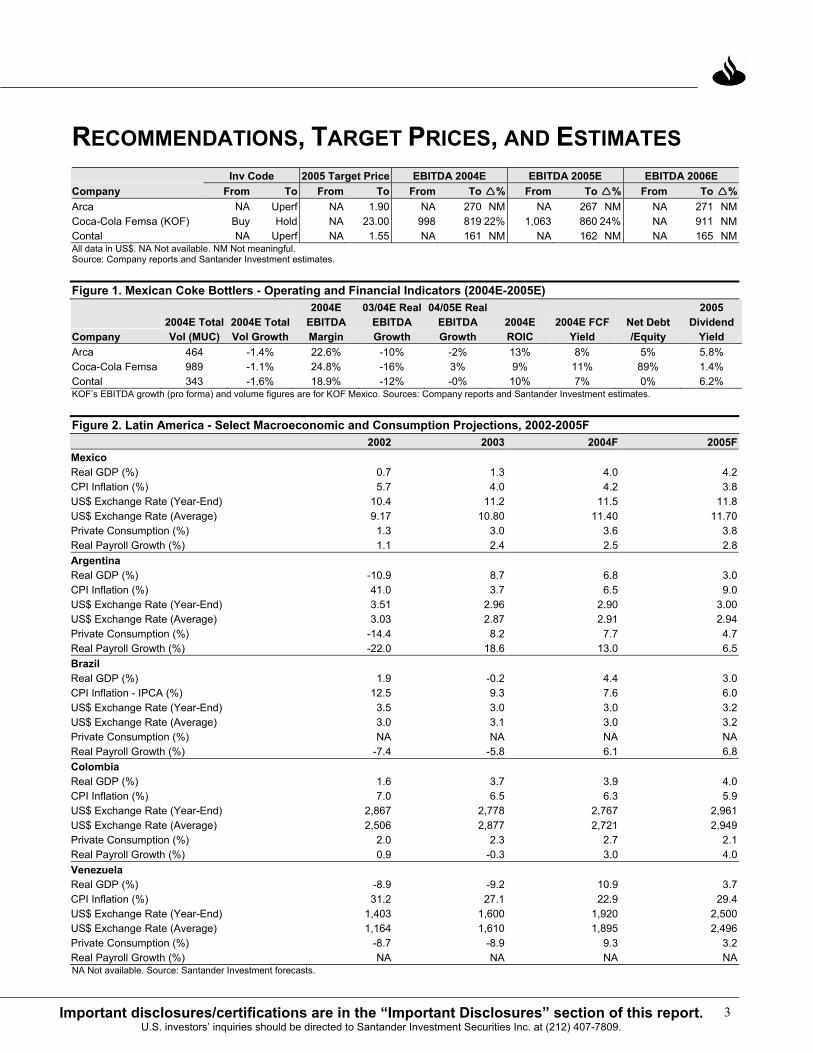

RECOMMENDATIONS, TARGET PRICES, AND ESTIMATES Inv Code 2005 Target Price EBITDA 2004E EBITDA 2005E EBITDA 2006E Company From To From To From To % From To % From To %Arca NA Uperf NA 1.90 NA 270 NM NA 267 NM NA 271 NMCoca-Cola Femsa (KOF) Buy Hold NA 23.00 998 819 22% 1,063 860 24% NA 911 NMContal NA Uperf NA 1.55 NA 161 NM NA 162 NM NA 165 NMAll data in US$. NA Not available. NM Not meaningful. Source: Company reports and Santander Investment estimates.

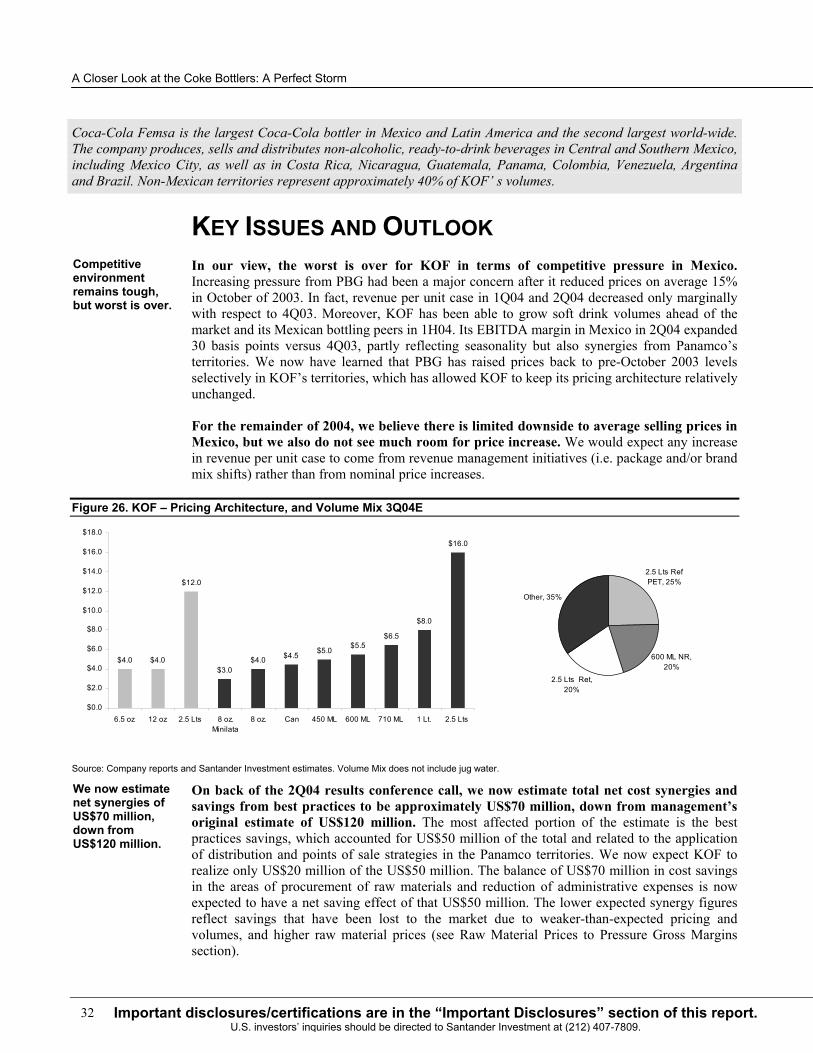

Figure 1. Mexican Coke Bottlers - Operating and Financial Indicators (2004E-2005E)

Company 2004E Total Vol (MUC)

2004E Total Vol Growth

2004E EBITDA Margin

03/04E Real EBITDA Growth

04/05E Real EBITDA Growth

2004E ROIC

2004E FCF Yield

Net Debt /Equity

2005 Dividend

Yield Arca 464 -1.4% 22.6% -10% -2% 13% 8% 5% 5.8% Coca-Cola Femsa 989 -1.1% 24.8% -16% 3% 9% 11% 89% 1.4% Contal 343 -1.6% 18.9% -12% -0% 10% 7% 0% 6.2% KOF’s EBITDA growth (pro forma) and volume figures are for KOF Mexico. Sources: Company reports and Santander Investment estimates.

Figure 2. Latin America - Select Macroeconomic and Consumption Projections, 2002-2005F 2002 2003 2004F 2005FMexico Real GDP (%) 0.7 1.3 4.0 4.2CPI Inflation (%) 5.7 4.0 4.2 3.8US$ Exchange Rate (Year-End) 10.4 11.2 11.5 11.8US$ Exchange Rate (Average) 9.17 10.80 11.40 11.70Private Consumption (%) 1.3 3.0 3.6 3.8Real Payroll Growth (%) 1.1 2.4 2.5 2.8Argentina Real GDP (%) -10.9 8.7 6.8 3.0CPI Inflation (%) 41.0 3.7 6.5 9.0US$ Exchange Rate (Year-End) 3.51 2.96 2.90 3.00US$ Exchange Rate (Average) 3.03 2.87 2.91 2.94Private Consumption (%) -14.4 8.2 7.7 4.7Real Payroll Growth (%) -22.0 18.6 13.0 6.5Brazil Real GDP (%) 1.9 -0.2 4.4 3.0CPI Inflation - IPCA (%) 12.5 9.3 7.6 6.0US$ Exchange Rate (Year-End) 3.5 3.0 3.0 3.2US$ Exchange Rate (Average) 3.0 3.1 3.0 3.2Private Consumption (%) NA NA NA NAReal Payroll Growth (%) -7.4 -5.8 6.1 6.8Colombia Real GDP (%) 1.6 3.7 3.9 4.0CPI Inflation (%) 7.0 6.5 6.3 5.9US$ Exchange Rate (Year-End) 2,867 2,778 2,767 2,961US$ Exchange Rate (Average) 2,506 2,877 2,721 2,949Private Consumption (%) 2.0 2.3 2.7 2.1Real Payroll Growth (%) 0.9 -0.3 3.0 4.0Venezuela Real GDP (%) -8.9 -9.2 10.9 3.7CPI Inflation (%) 31.2 27.1 22.9 29.4US$ Exchange Rate (Year-End) 1,403 1,600 1,920 2,500US$ Exchange Rate (Average) 1,164 1,610 1,895 2,496Private Consumption (%) -8.7 -8.9 9.3 3.2Real Payroll Growth (%) NA NA NA NANA Not available. Source: Santander Investment forecasts.

A Closer Look at the Coke Bottlers: A Perfect Storm

4 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

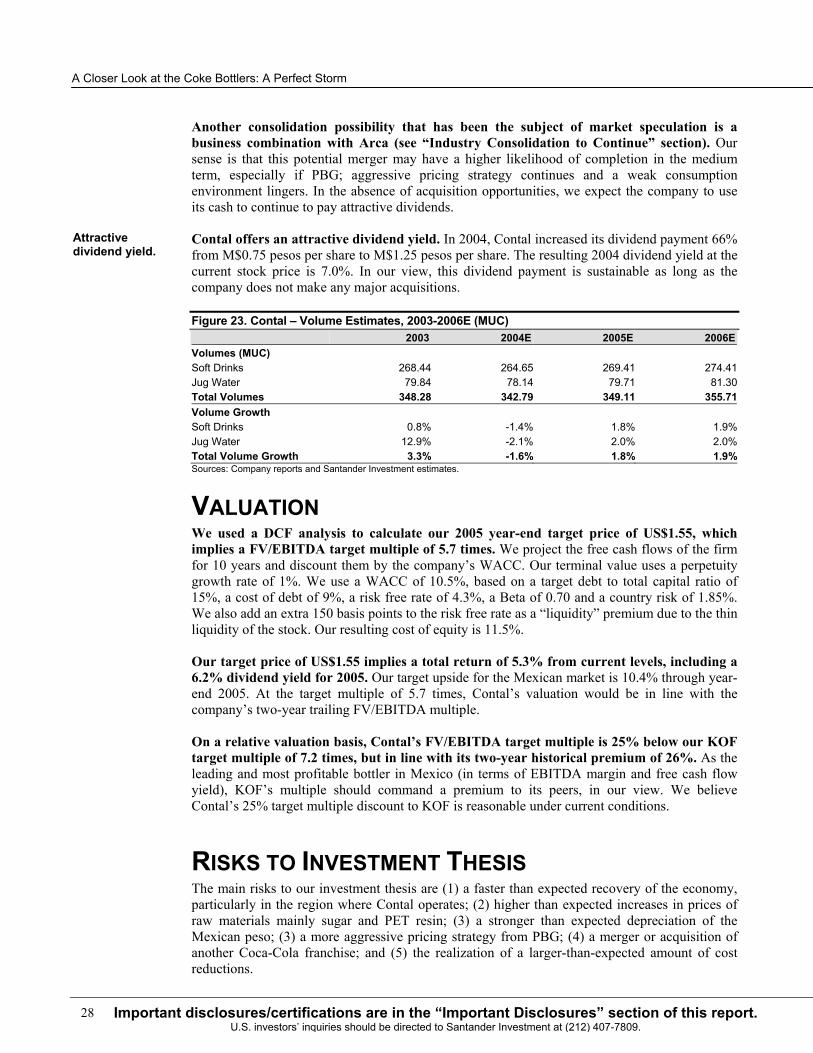

MEXICAN BOTTLING INDUSTRY OVERVIEW We expect Mexico’s soft drink and water industry volume sales to stabilize in 2H04 after contracting (about 1.5%) during the past two consecutive quarters for the first time in many years. By 2005, industry volumes should begin to accelerate modestly after several years of deceleration. According to our data, total soft drink and water industry volume sales grew at an average annual pace of 4.7% between 1999 and 2003, reaching 3.1 billion unit cases by 2003, 20% more than in 1999. However, this growth has two distinct stages. First, between 1999 and 2001, when macroeconomic indicators were relatively strong and competition was relatively tame, average annual volume growth was 7.8%. The second stage is between 2001 and 2003, when job losses were rampant and competition increased with the entrance of both Kola Real and the Pepsi Bottling Group (PBG). In this period, average annual volume growth decelerated considerably to an average of 1.8%. For 2004, we expect industry growth to be flat and reach 2.0% in 2005, for an average growth of 1% over these two years.

Figure 3. Soft Drink and Water Volume Growth in Millions of Unit Cases (1999-2005E)

-8%-6%-4%-2%0%2%4%6%8%

10%12%14%

1Q01

2Q01

3Q01

4Q01

1Q02

2Q02

3Q02

4Q02

1Q03

2Q03

3Q03

4Q03

1Q04

2Q04

2004

E

2005

E

Industry KOF Mx ARCA Contal PBG

Note: Arca volumes do not include jug water. PBG began operations in Mexico at end of 2002. Sources: Company Reports, INEGI and Santander Investment estimates.

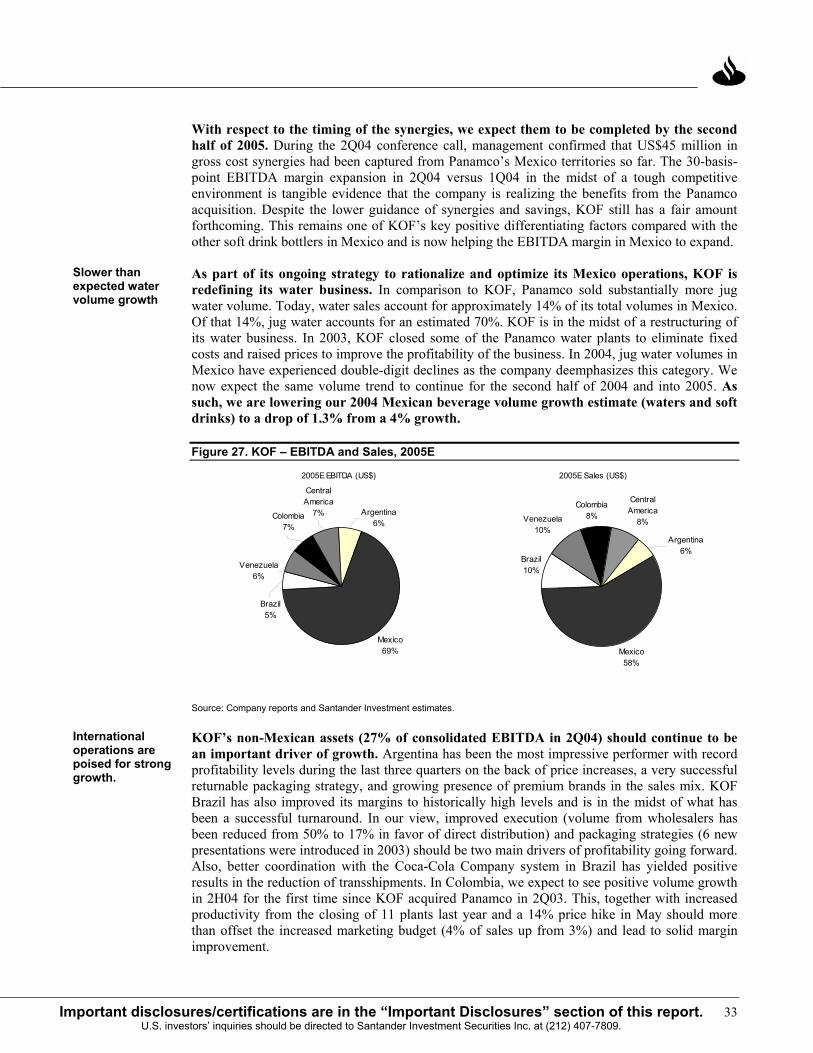

While the largest Coke bottlers in Mexico – Arca, Contal and KOF – mostly outperformed the decelerating period from 2001 to 2003, they underperformed during 1H04. During the 2001-2003 period, their outperformance versus the industry was supported by economies of scale and marketing muscle relative to the smaller Coca-Cola and PepsiCo bottlers in Mexico, in our view. Another factor could be the relative weakness of the competition. However, the underperformance in 1H04 suggests that their average selling prices may still be too high in light of the persistent competition from PBG and B-brands, including Kola Real. We also note that jug water volume growth at Arca and KOF have been particularly negatively impacted as they both seek to increase profitability in that category through price adjustments and outright distribution route closures.

WATER TO OUTPACE CARBONATED SOFT DRINKS We expect water to continue to be the fastest growing category in Mexico’s non-alcoholic beverage industry, while colas (rather than flavor carbonated drinks) should continue to be the laggards. This has been the trend for the past five years. As a result, colas’ share of the beverage industry has declined from 54% in 1999 to 47% in 2003. Meanwhile, purified water’s share of the total market volume has increased from 17% to 24% between 1999 and 2003.

Total industry volume growth contracted in 1H04, but only a modest recovery is expected.

Are selling prices too high?

Industry Ave Volume Growth 2001-2003: 1.8% 2003-2005E: 1.0%

5Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

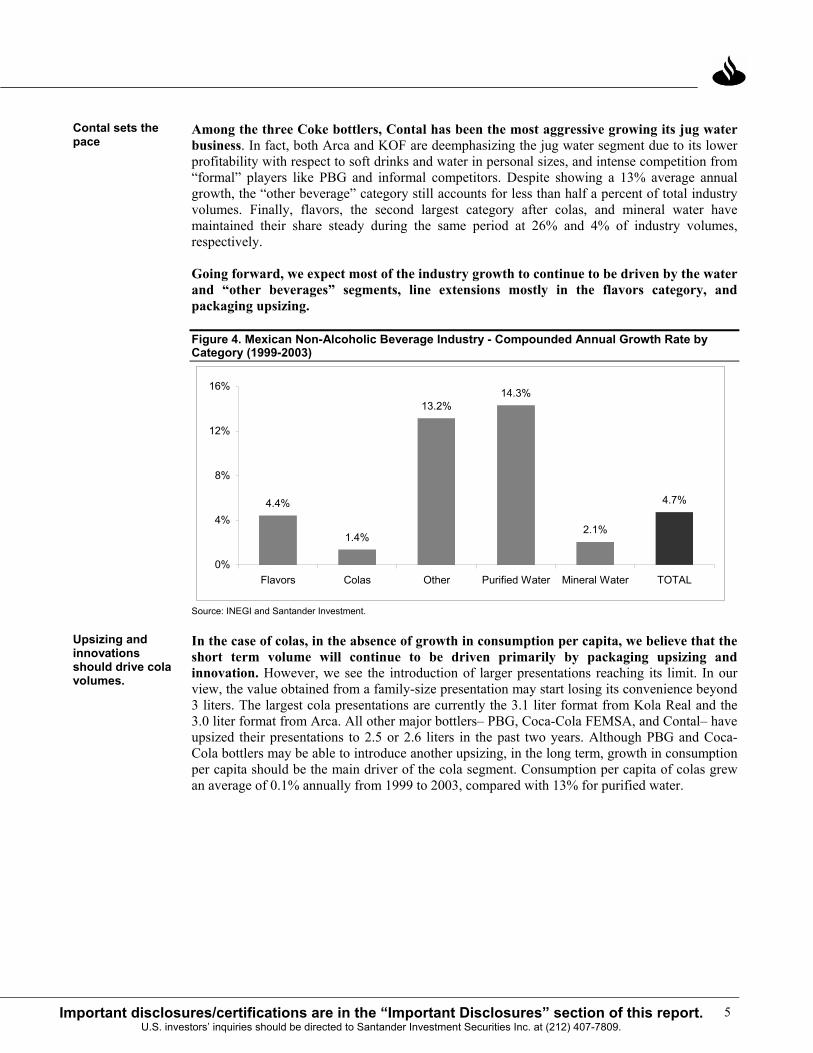

Among the three Coke bottlers, Contal has been the most aggressive growing its jug water business. In fact, both Arca and KOF are deemphasizing the jug water segment due to its lower profitability with respect to soft drinks and water in personal sizes, and intense competition from “formal” players like PBG and informal competitors. Despite showing a 13% average annual growth, the “other beverage” category still accounts for less than half a percent of total industry volumes. Finally, flavors, the second largest category after colas, and mineral water have maintained their share steady during the same period at 26% and 4% of industry volumes, respectively.

Going forward, we expect most of the industry growth to continue to be driven by the water and “other beverages” segments, line extensions mostly in the flavors category, and packaging upsizing.

Figure 4. Mexican Non-Alcoholic Beverage Industry - Compounded Annual Growth Rate by Category (1999-2003)

4.4%

1.4%

13.2%14.3%

2.1%

4.7%

0%

4%

8%

12%

16%

Flavors Colas Other Purified Water Mineral Water TOTAL

Source: INEGI and Santander Investment.

In the case of colas, in the absence of growth in consumption per capita, we believe that the short term volume will continue to be driven primarily by packaging upsizing and innovation. However, we see the introduction of larger presentations reaching its limit. In our view, the value obtained from a family-size presentation may start losing its convenience beyond 3 liters. The largest cola presentations are currently the 3.1 liter format from Kola Real and the 3.0 liter format from Arca. All other major bottlers– PBG, Coca-Cola FEMSA, and Contal– have upsized their presentations to 2.5 or 2.6 liters in the past two years. Although PBG and Coca-Cola bottlers may be able to introduce another upsizing, in the long term, growth in consumption per capita should be the main driver of the cola segment. Consumption per capita of colas grew an average of 0.1% annually from 1999 to 2003, compared with 13% for purified water.

Contal sets the pace

Upsizing and innovations should drive cola volumes.

A Closer Look at the Coke Bottlers: A Perfect Storm

6 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

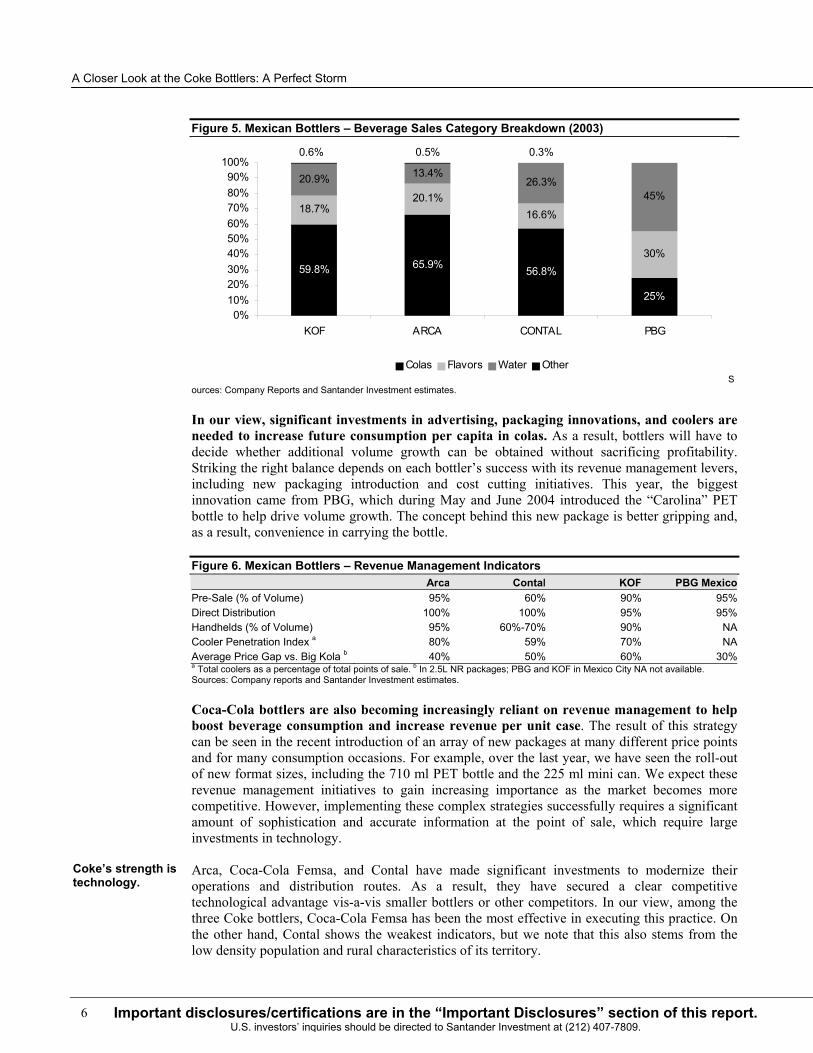

Figure 5. Mexican Bottlers – Beverage Sales Category Breakdown (2003)

59.8% 65.9% 56.8%

25%

18.7%20.1%

16.6%

30%

20.9% 13.4%26.3%

45%

0.6% 0.5% 0.3%

0%10%20%30%40%50%60%70%80%90%

100%

KOF ARCA CONTAL PBG

Colas Flavors Water OtherS

ources: Company Reports and Santander Investment estimates.

In our view, significant investments in advertising, packaging innovations, and coolers are needed to increase future consumption per capita in colas. As a result, bottlers will have to decide whether additional volume growth can be obtained without sacrificing profitability. Striking the right balance depends on each bottler’s success with its revenue management levers, including new packaging introduction and cost cutting initiatives. This year, the biggest innovation came from PBG, which during May and June 2004 introduced the “Carolina” PET bottle to help drive volume growth. The concept behind this new package is better gripping and, as a result, convenience in carrying the bottle.

Figure 6. Mexican Bottlers – Revenue Management Indicators Arca Contal KOF PBG MexicoPre-Sale (% of Volume) 95% 60% 90% 95%Direct Distribution 100% 100% 95% 95%Handhelds (% of Volume) 95% 60%-70% 90% NACooler Penetration Index a 80% 59% 70% NAAverage Price Gap vs. Big Kola b 40% 50% 60% 30%a Total coolers as a percentage of total points of sale. b In 2.5L NR packages; PBG and KOF in Mexico City NA not available. Sources: Company reports and Santander Investment estimates.

Coca-Cola bottlers are also becoming increasingly reliant on revenue management to help boost beverage consumption and increase revenue per unit case. The result of this strategy can be seen in the recent introduction of an array of new packages at many different price points and for many consumption occasions. For example, over the last year, we have seen the roll-out of new format sizes, including the 710 ml PET bottle and the 225 ml mini can. We expect these revenue management initiatives to gain increasing importance as the market becomes more competitive. However, implementing these complex strategies successfully requires a significant amount of sophistication and accurate information at the point of sale, which require large investments in technology.

Arca, Coca-Cola Femsa, and Contal have made significant investments to modernize their operations and distribution routes. As a result, they have secured a clear competitive technological advantage vis-a-vis smaller bottlers or other competitors. In our view, among the three Coke bottlers, Coca-Cola Femsa has been the most effective in executing this practice. On the other hand, Contal shows the weakest indicators, but we note that this also stems from the low density population and rural characteristics of its territory.

Coke’s strength is technology.

7Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

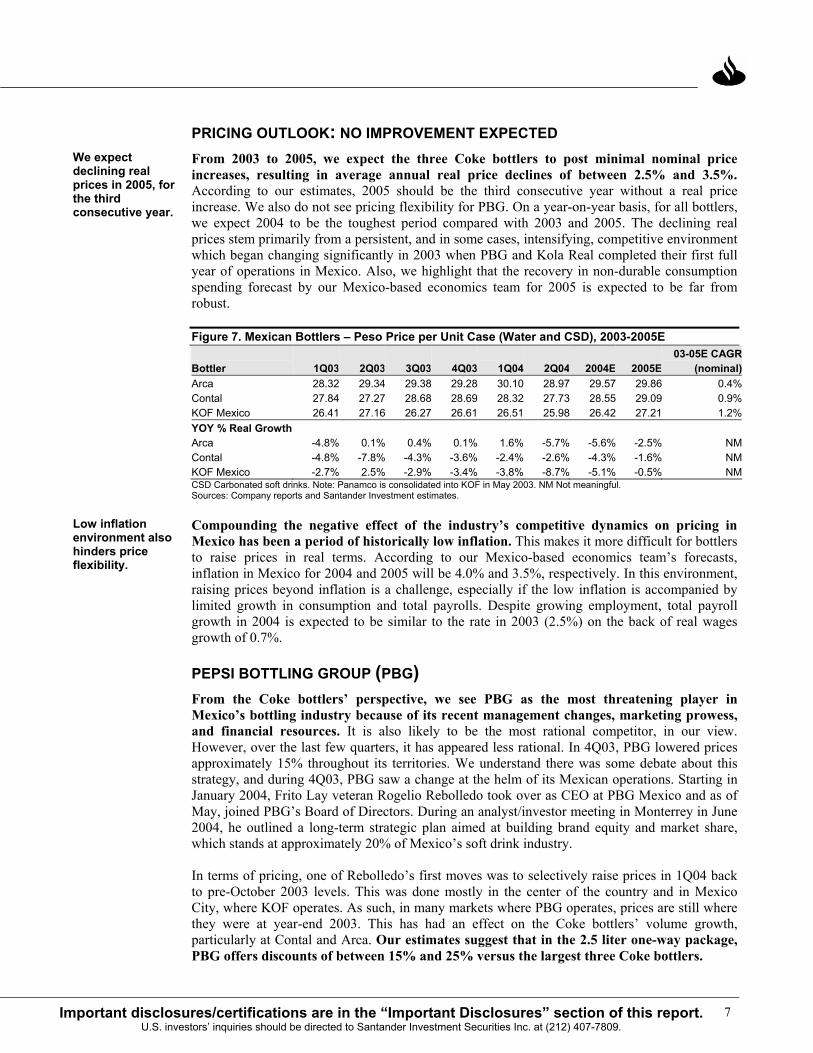

PRICING OUTLOOK: NO IMPROVEMENT EXPECTED From 2003 to 2005, we expect the three Coke bottlers to post minimal nominal price increases, resulting in average annual real price declines of between 2.5% and 3.5%. According to our estimates, 2005 should be the third consecutive year without a real price increase. We also do not see pricing flexibility for PBG. On a year-on-year basis, for all bottlers, we expect 2004 to be the toughest period compared with 2003 and 2005. The declining real prices stem primarily from a persistent, and in some cases, intensifying, competitive environment which began changing significantly in 2003 when PBG and Kola Real completed their first full year of operations in Mexico. Also, we highlight that the recovery in non-durable consumption spending forecast by our Mexico-based economics team for 2005 is expected to be far from robust.

Figure 7. Mexican Bottlers – Peso Price per Unit Case (Water and CSD), 2003-2005E Bottler 1Q03 2Q03 3Q03 4Q03 1Q04 2Q04 2004E 2005E

03-05E CAGR(nominal)

Arca 28.32 29.34 29.38 29.28 30.10 28.97 29.57 29.86 0.4%Contal 27.84 27.27 28.68 28.69 28.32 27.73 28.55 29.09 0.9%KOF Mexico 26.41 27.16 26.27 26.61 26.51 25.98 26.42 27.21 1.2%YOY % Real Growth Arca -4.8% 0.1% 0.4% 0.1% 1.6% -5.7% -5.6% -2.5% NMContal -4.8% -7.8% -4.3% -3.6% -2.4% -2.6% -4.3% -1.6% NMKOF Mexico -2.7% 2.5% -2.9% -3.4% -3.8% -8.7% -5.1% -0.5% NMCSD Carbonated soft drinks. Note: Panamco is consolidated into KOF in May 2003. NM Not meaningful. Sources: Company reports and Santander Investment estimates.

Compounding the negative effect of the industry’s competitive dynamics on pricing in Mexico has been a period of historically low inflation. This makes it more difficult for bottlers to raise prices in real terms. According to our Mexico-based economics team’s forecasts, inflation in Mexico for 2004 and 2005 will be 4.0% and 3.5%, respectively. In this environment, raising prices beyond inflation is a challenge, especially if the low inflation is accompanied by limited growth in consumption and total payrolls. Despite growing employment, total payroll growth in 2004 is expected to be similar to the rate in 2003 (2.5%) on the back of real wages growth of 0.7%.

PEPSI BOTTLING GROUP (PBG) From the Coke bottlers’ perspective, we see PBG as the most threatening player in Mexico’s bottling industry because of its recent management changes, marketing prowess, and financial resources. It is also likely to be the most rational competitor, in our view. However, over the last few quarters, it has appeared less rational. In 4Q03, PBG lowered prices approximately 15% throughout its territories. We understand there was some debate about this strategy, and during 4Q03, PBG saw a change at the helm of its Mexican operations. Starting in January 2004, Frito Lay veteran Rogelio Rebolledo took over as CEO at PBG Mexico and as of May, joined PBG’s Board of Directors. During an analyst/investor meeting in Monterrey in June 2004, he outlined a long-term strategic plan aimed at building brand equity and market share, which stands at approximately 20% of Mexico’s soft drink industry.

In terms of pricing, one of Rebolledo’s first moves was to selectively raise prices in 1Q04 back to pre-October 2003 levels. This was done mostly in the center of the country and in Mexico City, where KOF operates. As such, in many markets where PBG operates, prices are still where they were at year-end 2003. This has had an effect on the Coke bottlers’ volume growth, particularly at Contal and Arca. Our estimates suggest that in the 2.5 liter one-way package, PBG offers discounts of between 15% and 25% versus the largest three Coke bottlers.

We expect declining real prices in 2005, for the third consecutive year.

Low inflation environment also hinders price flexibility.

A Closer Look at the Coke Bottlers: A Perfect Storm

8 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

Figure 8. Mexican Bottlers – Cola Pricing by Region and Package, 3Q04E (Mexican Pesos) Bottler 2.5 Liter Returnable 2.5 Liter Non-ReturnableArca NA 14Coca-Cola Femsa 12 16Contal 13 15PBG (Mexico City) NA 12PBG NA 11-12Big Cola (Kola Real) NA 8-9Coca-Cola Femsa prices in Mexico City only. Sources: Company reports and Santander Investment estimates.

Data in 1H04 support this view as Arca and Contal suffered a decline in soft drink volumes of 3.5% (pro forma estimate) and 4.5% in 1H04, respectively, while KOF grew volumes 0.8%. Although part of the declines could be attributed to unfavorable weather, mainly in the North, we believe the main cause has been stepped-up competition from PBG particularly in the multi-serve category. We also note that Arca and Contal’s lower volumes occurred despite both companies lowering prices during 2Q04 in some presentations, potentially showing a less competitive picture in the center of the country, but also better execution from KOF. In the case of Contal specifically, regional competitive disparity is evident as the company’s volumes had a much steeper decline in the areas of operations where it competes directly with PBG (see Map of Coke and PepsiCo franchises in Figure 14).

PBG has also increased its aggressiveness in northern Mexico with its “Descubrela” (“Discover it”) marketing campaign, mainly impacting Arca’s territories. For example, PBG’s 2.5L one-way presentation which was being priced at 12 to 13 pesos in some of Arca’s territories is now being priced as low as 11 pesos in some channels. This forced Arca to respond by lowering prices in its 2.0L returnable presentation from 12 pesos to 10 pesos, the same price as PBG’s 2.0L one-way presentation. Contal also initiated a low-price campaign in March 21, 2004, “Campaña Primavera” (“Spring Campaign”) in the company’s main franchise territories in Guadalajara, San Luis and Aguas Calientes. The goal was to boost volumes in 2Q04 after the very sharp drop in volumes in 1Q04. However, on the back of disappointing volume growth in 2Q04, the campaign continues in effect in 3Q04.

KOLA REAL The pending construction of Kola Real’s new plant in northern Mexico could be the most threatening competitive event in terms of industry pricing next year, given that its discount to the Coke bottlers ranges between 25% and 50%. The plant, 18 km outside of Monterrey, is expected to be completed by 1Q05 and have 50 million unit cases of production capacity. This should double Kola Real’s total Mexican capacity, which is currently one plant in Puebla with approximately 50 million units of capacity. Undoubtedly, this new plant will strengthen Kola Real’s presence in the north of the country and improve profitability by saving freight costs. It also could pose a new threat to Arca, which sells approximately 30% of its volume in Monterrey. Contal is also likely to be impacted since many of its territories in central Mexico are within striking distance.

We expect Kola Real, driven by its main Big Cola brand, to reach a 5-6% share of the national soft drink market in Mexico over the medium term, up from an estimated 2-3% at present. The growth should come from two sources: Flavor brand extensions from the First brand family which has already enjoyed success in the grapefruit segment, and further geographical expansion, spurred by its new plant in the north. Of Mexico’s 32 states, Kola Real has no (or almost no) presence in 11 states. The company’s current stronghold is in Puebla, where it competes against KOF. There, its market share once reached 7%; however, KOF believes that it is now below 3%. According to Arca’s and Contal’s management, Kola Real’s

Kola Real expected to build a plant near Monterrey.

Kola Real to reach 5-6% market share by 2006, in our view.

9Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

market share is less than 3% in the territories where they overlap. We estimate that Kola Real is present in approximately 75% of Contal and Arca’s territories and 100% in KOF’s territories.

Over the longer term, we see Kola Real’s growth in Mexico constrained by the industry’s structure and its lack of a direct point of sale distribution network. First, and mainly, without a fleet of trucks and a pre-sale system, building relations with the majority of the points of sales is very difficult. That makes B-brand producers including Kola Real dependent on supermarkets for volume growth. Currently, supermarkets account for approximately 20% of Kola Real’s volume sales. However, Mexico’s industry is characterized by a very low penetration of supermarkets, which should continue to limit the ability of Kola Real to reach the mass market efficiently. In Mexico, supermarkets account for less than 4% of total volume sold. As a result, reaching a larger number of consumers requires large investments in distribution assets, something that to date only the largest Coke and PepsiCo bottlers can afford.

Second, the absence of soft drink excise taxes in Mexico puts every bottler on an equal footing. In markets such as Brazil, where B-brands have market shares above 30%, many B-brand producers gain a cost advantage by paying fewer taxes due to the difficulty in collecting from small producers. Finally, although to a lesser extent, the high proportion of returnable packages puts a ceiling on the market for B-brands, as they rely almost exclusively on non-returnable presentations. As discussed later in this report, we continue to see a significant shift towards one-way packaging in Mexico. However, we think the Mexican market is many years away from reaching the levels of one-way packaging seen in countries like Brazil.

We have recently seen more targeted, higher profile efforts in Kola Real’s advertising to increase brand awareness and gain consumer loyalty. Kola Real recently sponsored Big Brother’s Spanish version in Mexico, a program drawing a big audience of young consumers. It is also planning to advertise in Mexico’s upcoming Teleton, a high profile national charity event. Previously, Kola Real had relied mainly on price as its main marketing tool and advertising had focused on emphasizing this advantage. We view Kola Real’s new advertising strategy as an important step towards obtaining consumer loyalty, a crucial attribute to boost market share.

Over the long term, this advertising strategy may diminish its low operating cost advantage, which helps it to sustain deep discounts to the Coke bottlers. Although we understand that there has not been any increase in Kola Real’s advertising budget, in our view, a campaign designed to increase brand loyalty will require increasing and continued amounts of advertising in the medium to long term to be effective. This added cost could eat into the company’s margins if prices are maintained at low levels.

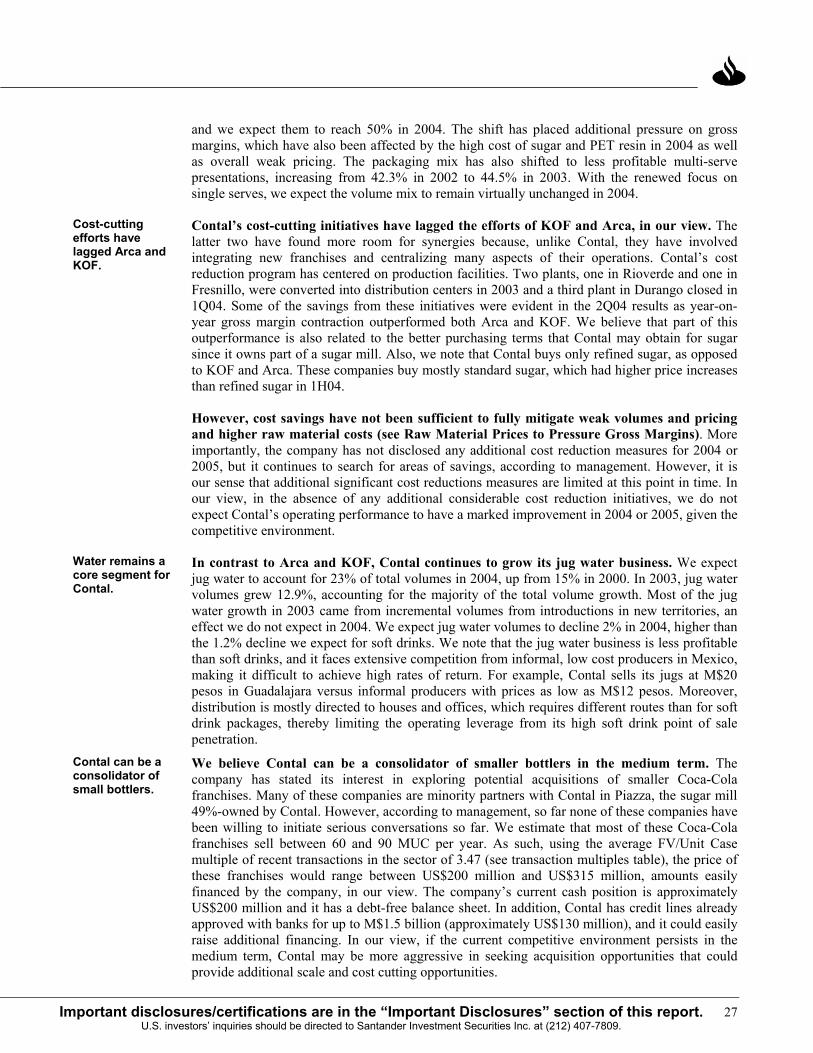

RAW MATERIAL PRICES TO PRESSURE GROSS MARGINS We estimate that on a year on year basis, 2H04 will likely show higher raw material price increases than in 1H04, particularly for PET and sugar, putting additional pressure on gross margins. We estimate PET and sugar represent approximately 40% of total cash cost of sales for bottlers. Therefore, movements in the prices of these raw materials can significantly impact on gross margins. Our conclusion is that Coke bottlers Arca, Contal and KOF (Mexico) will experience double-digit increases in raw material prices during the second half of 2004 on a year-on-year basis. The annual impact should correspond to almost 4% of cash cost of sales and reduce the bottlers’ gross margins between 160 and 170 basis points on a stand alone basis.

B-brands do have their limits in Mexico.

Kola Real’s new marketing push.

Sugar and PET represent 40% of cost of sales.

A Closer Look at the Coke Bottlers: A Perfect Storm

10 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

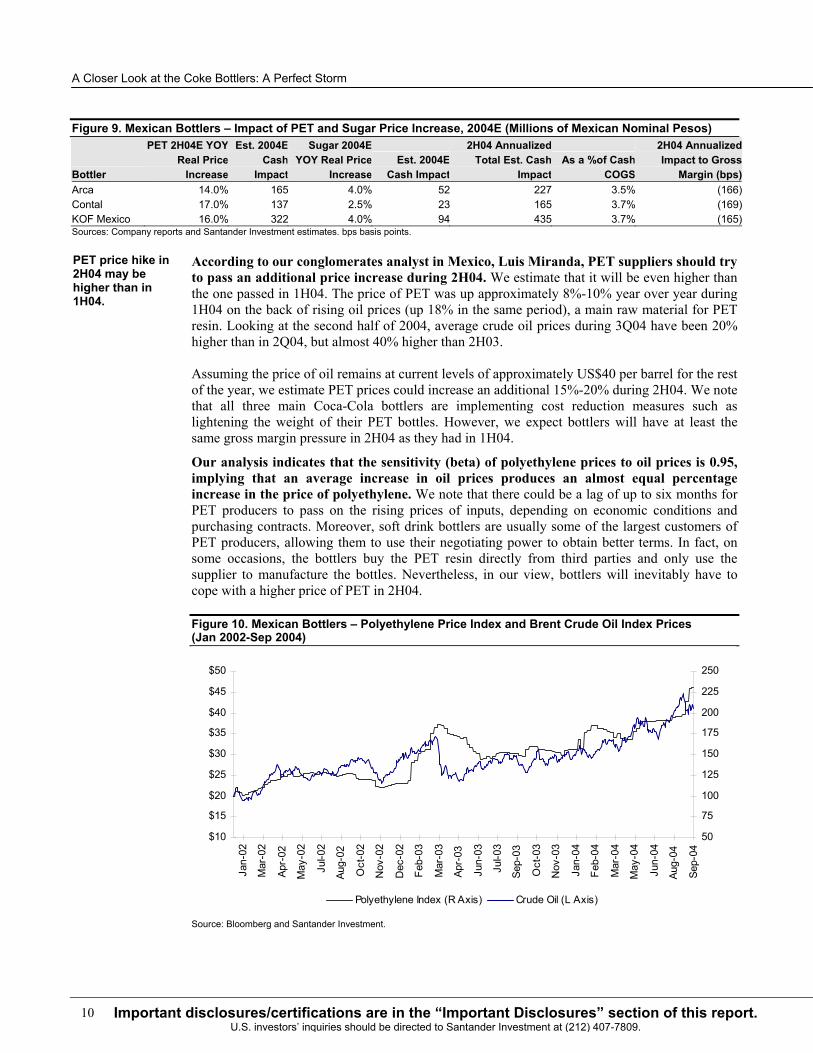

Figure 9. Mexican Bottlers – Impact of PET and Sugar Price Increase, 2004E (Millions of Mexican Nominal Pesos)

Bottler

PET 2H04E YOY Real Price

Increase

Est. 2004E Cash

Impact

Sugar 2004EYOY Real Price

IncreaseEst. 2004E

Cash Impact

2H04 Annualized Total Est. Cash

ImpactAs a %of Cash

COGS

2H04 Annualized Impact to Gross

Margin (bps)Arca 14.0% 165 4.0% 52 227 3.5% (166)Contal 17.0% 137 2.5% 23 165 3.7% (169)KOF Mexico 16.0% 322 4.0% 94 435 3.7% (165)Sources: Company reports and Santander Investment estimates. bps basis points.

According to our conglomerates analyst in Mexico, Luis Miranda, PET suppliers should try to pass an additional price increase during 2H04. We estimate that it will be even higher than the one passed in 1H04. The price of PET was up approximately 8%-10% year over year during 1H04 on the back of rising oil prices (up 18% in the same period), a main raw material for PET resin. Looking at the second half of 2004, average crude oil prices during 3Q04 have been 20% higher than in 2Q04, but almost 40% higher than 2H03.

Assuming the price of oil remains at current levels of approximately US$40 per barrel for the rest of the year, we estimate PET prices could increase an additional 15%-20% during 2H04. We note that all three main Coca-Cola bottlers are implementing cost reduction measures such as lightening the weight of their PET bottles. However, we expect bottlers will have at least the same gross margin pressure in 2H04 as they had in 1H04.

Our analysis indicates that the sensitivity (beta) of polyethylene prices to oil prices is 0.95, implying that an average increase in oil prices produces an almost equal percentage increase in the price of polyethylene. We note that there could be a lag of up to six months for PET producers to pass on the rising prices of inputs, depending on economic conditions and purchasing contracts. Moreover, soft drink bottlers are usually some of the largest customers of PET producers, allowing them to use their negotiating power to obtain better terms. In fact, on some occasions, the bottlers buy the PET resin directly from third parties and only use the supplier to manufacture the bottles. Nevertheless, in our view, bottlers will inevitably have to cope with a higher price of PET in 2H04.

Figure 10. Mexican Bottlers – Polyethylene Price Index and Brent Crude Oil Index Prices (Jan 2002-Sep 2004)

50

75

100

125

150

175

200

225

250

Sep-

04

Aug-

04

Jun-

04

May

-04

Mar

-04

Feb-

04

Jan-

04

Nov

-03

Oct

-03

Sep-

03

Jul-0

3

Jun-

03

Apr-

03

Mar

-03

Feb-

03

Dec

-02

Nov

-02

Oct

-02

Aug-

02

Jul-0

2

May

-02

Apr-

02

Mar

-02

Jan-

02

$10

$15

$20

$25

$30

$35

$40

$45

$50

Polyethylene Index (R Axis) Crude Oil (L Axis)

Source: Bloomberg and Santander Investment.

PET price hike in 2H04 may be higher than in 1H04.

11Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

Figure 11. Average Crude Oil Prices, Brent Crude Oil (US Dollars) 1H02 2H02 1H03 2H03 1H04 2H04a

Price 23.47 26.65 28.27 28.69 33.27 39.86 YOY Increase NA NA 20.5% 7.7% 17.7% 38.9%Sources: Bloomberg. A Through September 10, 2004

Since its is priced in U.S dollars, PET resin is also sensitive to currency fluctuations and can see sharp price increases in periods of local currency depreciation. However, for the rest of 2004, our Mexico-based economics team expects the Mexican peso to depreciate less than 1%. As such, we expect most of the PET price increases to be driven by higher oil prices.

We expect sugar prices to increase an additional 4% in real terms in 2H04, on the back of a 5% rise in 1H04. This follows an average 8% rise in prices in 2003. Not only is the industry growing but prices are mostly controlled by the government which owns half of the sugar mills. Current prices of sugar stand at approximately M$6,300 per ton. An important development for bottlers in the purchasing of sugar has been the use of clarification facilities. This practice has been beneficial due to the estimated 20% gap between the prices of standard and refined sugar. However, the proliferation of clarification facilities has increased demand for standard sugar and, as a result, the price of standard sugar is rising more rapidly, closing the price gap between standard and refined sugar.

Arca and KOF have both been very aggressive in clarifying sugar. As a result, we believe these two companies may be experiencing a steeper increase in the price of sugar. Contal, in turn, only buys refined sugar. In our view, the different practices may stem from the fact that Contal buys sugar from a sugar mill, Piazza, where it is the largest shareholder and may obtain better purchasing terms.

Short purchasing cycles are accelerating the impact in the price increase of raw materials. On average, we estimate that bottlers purchase one month of inventory at a time. Although this makes for a more efficient use of working capital, in the current environment it has also made bottlers more susceptible to short term fluctuations in prices of raw materials, particularly since none of the Mexican bottlers have a hedging policy for these inputs.

With the proliferation of PET bottles, glass has become a less meaningful input cost of production for bottlers. However, we note that we expect the price of glass to have a moderate increase in the second half of 2004 owing mainly to higher natural gas prices, the main input cost. We note that glass bottles are not directly expensed, but capitalized in the balance sheet and amortized over time. We estimate that glass accounts for less than 5% of the cost of sales.

CONTAINING THE NON-RETURNABLE PACKAGING TREND Another significant industry trend in Mexico is the ongoing growth of lower-margin non-returnable (one-way) presentations, namely PET plastic bottles. The major factor driving this shift is consumer preference for convenience. Despite the lower profitability of non-returnable presentations, bottlers have had to react to the growing preference of one-way packaging. Developed markets, such as the United States, consume soft drinks predominantly in non-returnable presentations. In Latin America, one way presentations are slightly more preferred than the returnable formats.

In our view, B-brands and PBG, who use one-way packages in Mexico almost exclusively, are another factor driving growth of these presentations. In countries where B-brands have obtained a high market share, the use of non-returnable presentations is significantly higher than in other countries in the region. The reasoning is clear: returnable presentations are supposed to offer a value proposition to customers because the bottlers can pass along the cost advantages

Sugar prices could increase an additional 4% in 2H04.

Consumer convenience continues to drive the packaging shift.

A Closer Look at the Coke Bottlers: A Perfect Storm

12 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

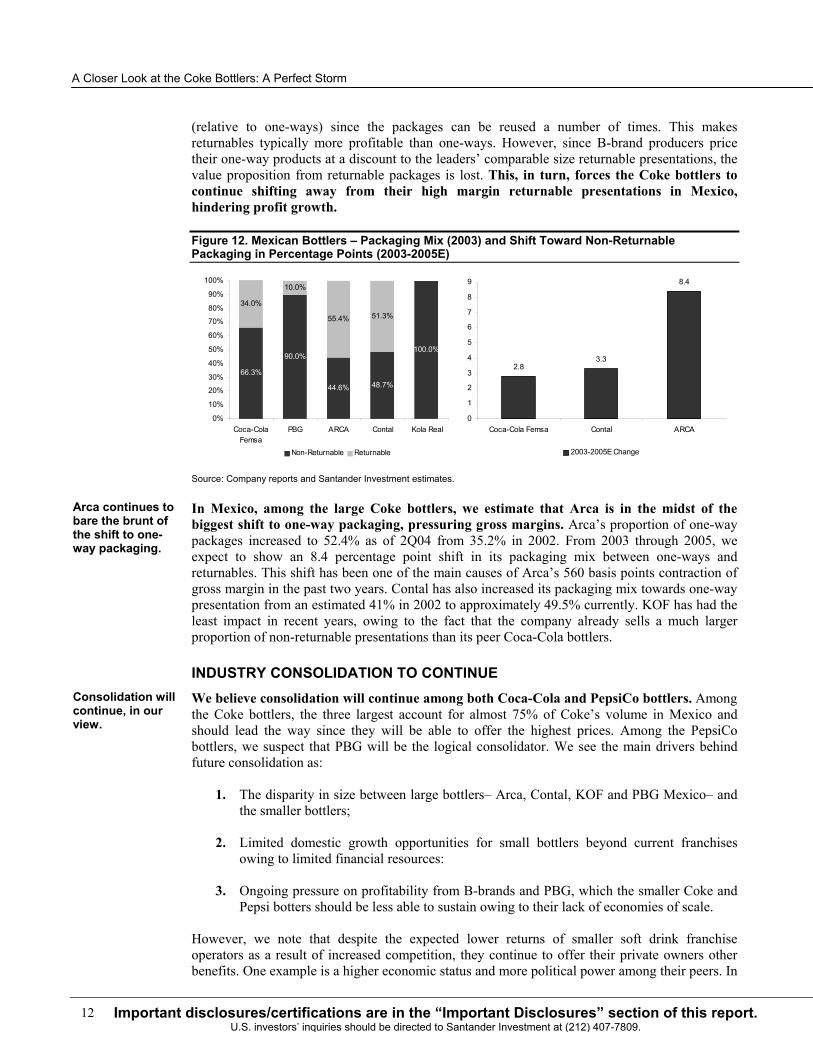

(relative to one-ways) since the packages can be reused a number of times. This makes returnables typically more profitable than one-ways. However, since B-brand producers price their one-way products at a discount to the leaders’ comparable size returnable presentations, the value proposition from returnable packages is lost. This, in turn, forces the Coke bottlers to continue shifting away from their high margin returnable presentations in Mexico, hindering profit growth.

Figure 12. Mexican Bottlers – Packaging Mix (2003) and Shift Toward Non-Returnable Packaging in Percentage Points (2003-2005E)

66.3%

90.0%

44.6% 48.7%

100.0%

34.0%

10.0%

55.4% 51.3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Coca-ColaFemsa

PBG ARCA Contal Kola Real

Non-Returnable Returnable

2.83.3

8.4

0

1

2

3

4

5

6

7

8

9

Coca-Cola Femsa Contal ARCA

2003-2005E Change

Source: Company reports and Santander Investment estimates.

In Mexico, among the large Coke bottlers, we estimate that Arca is in the midst of the biggest shift to one-way packaging, pressuring gross margins. Arca’s proportion of one-way packages increased to 52.4% as of 2Q04 from 35.2% in 2002. From 2003 through 2005, we expect to show an 8.4 percentage point shift in its packaging mix between one-ways and returnables. This shift has been one of the main causes of Arca’s 560 basis points contraction of gross margin in the past two years. Contal has also increased its packaging mix towards one-way presentation from an estimated 41% in 2002 to approximately 49.5% currently. KOF has had the least impact in recent years, owing to the fact that the company already sells a much larger proportion of non-returnable presentations than its peer Coca-Cola bottlers.

INDUSTRY CONSOLIDATION TO CONTINUE We believe consolidation will continue among both Coca-Cola and PepsiCo bottlers. Among the Coke bottlers, the three largest account for almost 75% of Coke’s volume in Mexico and should lead the way since they will be able to offer the highest prices. Among the PepsiCo bottlers, we suspect that PBG will be the logical consolidator. We see the main drivers behind future consolidation as:

1. The disparity in size between large bottlers– Arca, Contal, KOF and PBG Mexico– and the smaller bottlers;

2. Limited domestic growth opportunities for small bottlers beyond current franchises owing to limited financial resources:

3. Ongoing pressure on profitability from B-brands and PBG, which the smaller Coke and Pepsi botters should be less able to sustain owing to their lack of economies of scale.

However, we note that despite the expected lower returns of smaller soft drink franchise operators as a result of increased competition, they continue to offer their private owners other benefits. One example is a higher economic status and more political power among their peers. In

Arca continues to bare the brunt of the shift to one-way packaging.

Consolidation will continue, in our view.

13Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

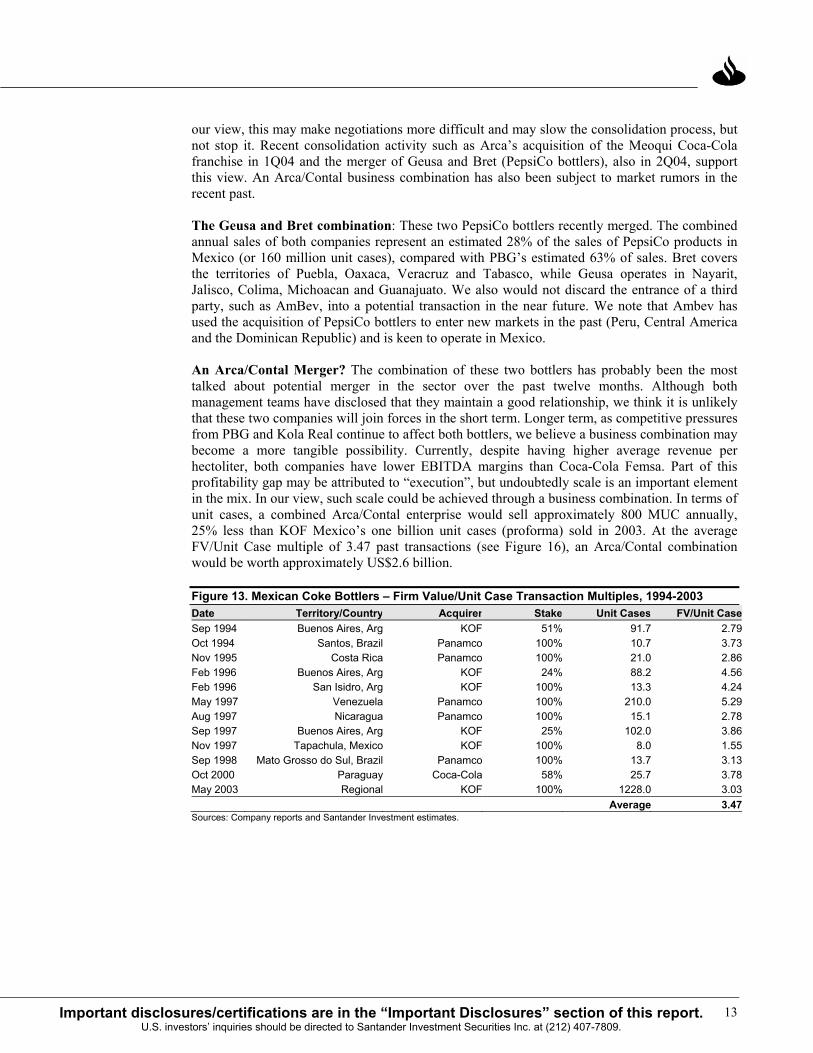

our view, this may make negotiations more difficult and may slow the consolidation process, but not stop it. Recent consolidation activity such as Arca’s acquisition of the Meoqui Coca-Cola franchise in 1Q04 and the merger of Geusa and Bret (PepsiCo bottlers), also in 2Q04, support this view. An Arca/Contal business combination has also been subject to market rumors in the recent past.

The Geusa and Bret combination: These two PepsiCo bottlers recently merged. The combined annual sales of both companies represent an estimated 28% of the sales of PepsiCo products in Mexico (or 160 million unit cases), compared with PBG’s estimated 63% of sales. Bret covers the territories of Puebla, Oaxaca, Veracruz and Tabasco, while Geusa operates in Nayarit, Jalisco, Colima, Michoacan and Guanajuato. We also would not discard the entrance of a third party, such as AmBev, into a potential transaction in the near future. We note that Ambev has used the acquisition of PepsiCo bottlers to enter new markets in the past (Peru, Central America and the Dominican Republic) and is keen to operate in Mexico.

An Arca/Contal Merger? The combination of these two bottlers has probably been the most talked about potential merger in the sector over the past twelve months. Although both management teams have disclosed that they maintain a good relationship, we think it is unlikely that these two companies will join forces in the short term. Longer term, as competitive pressures from PBG and Kola Real continue to affect both bottlers, we believe a business combination may become a more tangible possibility. Currently, despite having higher average revenue per hectoliter, both companies have lower EBITDA margins than Coca-Cola Femsa. Part of this profitability gap may be attributed to “execution”, but undoubtedly scale is an important element in the mix. In our view, such scale could be achieved through a business combination. In terms of unit cases, a combined Arca/Contal enterprise would sell approximately 800 MUC annually, 25% less than KOF Mexico’s one billion unit cases (proforma) sold in 2003. At the average FV/Unit Case multiple of 3.47 past transactions (see Figure 16), an Arca/Contal combination would be worth approximately US$2.6 billion.

Figure 13. Mexican Coke Bottlers – Firm Value/Unit Case Transaction Multiples, 1994-2003 Date Territory/Country Acquirer Stake Unit Cases FV/Unit CaseSep 1994 Buenos Aires, Arg KOF 51% 91.7 2.79Oct 1994 Santos, Brazil Panamco 100% 10.7 3.73Nov 1995 Costa Rica Panamco 100% 21.0 2.86Feb 1996 Buenos Aires, Arg KOF 24% 88.2 4.56Feb 1996 San Isidro, Arg KOF 100% 13.3 4.24May 1997 Venezuela Panamco 100% 210.0 5.29Aug 1997 Nicaragua Panamco 100% 15.1 2.78Sep 1997 Buenos Aires, Arg KOF 25% 102.0 3.86Nov 1997 Tapachula, Mexico KOF 100% 8.0 1.55Sep 1998 Mato Grosso do Sul, Brazil Panamco 100% 13.7 3.13Oct 2000 Paraguay Coca-Cola 58% 25.7 3.78May 2003 Regional KOF 100% 1228.0 3.03

Average 3.47Sources: Company reports and Santander Investment estimates.

A Closer Look at the Coke Bottlers: A Perfect Storm

14 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

Figure 14. Mexican Coke Bottlers Franchise Map

CHIHUAHUA

MONTERREY

GUADALAJARA

SAN LUIS POTOS

PUEBLAMEXICO CITY

VERACRUZ

Arca

Contal

Coca Cola Femsa

CANCUN

Embotell. de Guerrero

Independ.

Grupo Tampico

Cimsa

Bepensa

Jordan

Fomento Queretaro

Rica

CHIHUAHUA

MONTERREY

GUADALAJARA

SAN LUIS POTOS

PUEBLAMEXICO CITY

VERACRUZ

Arca

Contal

Coca Cola Femsa

CANCUN

Embotell. de Guerrero

Independ.

Grupo Tampico

Cimsa

Bepensa

Jordan

Fomento Queretaro

Rica

Source: Santander Investment.

Figure 15. Mexican Pepsi Bottlers Franchise Map

GEUSA/BRET

PBGGASEOSAS S.A.

GRUPO EMB. SURESTEBEBIDAS PURIFICADAS

CHIHUAHUA

MONTERREY

GUADALAJARA

SAN LUIS POTOS

PUEBLAMEXICO CITY

VERACRUZ

CANCUN

GEUSA/BRET

PBGGASEOSAS S.A.

GRUPO EMB. SURESTEBEBIDAS PURIFICADAS

CHIHUAHUA

MONTERREY

GUADALAJARA

SAN LUIS POTOS

PUEBLAMEXICO CITY

VERACRUZ

CANCUN

Source: Santander Investment.

15Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

CONSUMPTION OUTLOOK Mexican macroeconomic indicators show modest improvement in the second half of 2004. The economy grew 3.9% in 2Q04 supported by growth of the service and industrial sectors. Our Mexico-based economics team sees GDP growth reaching 4%, up from 1.3% in 2003 on back of increased government spending and exports. As has been the case during previous economic upturns, the growth of the U.S. economy has driven the recovery in the maquilas sector, where employment is showing an encouraging positive trend both in northern Mexico as well as nation-wide during 1H04. Despite the encouraging macroeconomic data, we remain cautious as to the magnitude of the forecast recovery in non-durable consumption spending growth for the remainder of 2004 and into 2005.

Figure16. Mexico, Maquiladora Industry Employment (Year-on-Year Growth), Oct 2000-Jun 2004

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

Oct

-00

Dec

-00

Feb-

01

Apr-

01

Jun-

01

Aug-

01

Oct

-01

Dec

-01

Feb-

02

Apr-

02

Jun-

02

Aug-

02

Oct

-02

Dec

-02

Feb-

03

Apr-

03

Jun-

03

Aug-

03

Oct

-03

Dec

-03

Feb-

04

Apr-

04

Jun-

04

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

National Border States

Source: INEGI and Santander Invesmtent.

As a result of the recent upturn in exports, employment at the national level in the maquilas sector reversed a 10-month negative year-on-year growth trend in 2Q04. We note that the most important U.S. industries for the maquilas sector, such as the auto industry, have underperformed the growth of the U.S. economy. In addition, some exports in textiles and electronics have been lost to China’s more competitive industries. As a result, the boost from the U.S. economic recovery may not be as strong for the Mexican economy as it has been in previous economic upturns. Furthermore, Mexican exports may have limited upside if the U.S. starts to show softer data on the back of a tightening monetary cycle. Finally, structural reforms that could increase the country’s competitiveness seem unlikely under the current political environment.

Economic Indicators point to a modest improvement in 2H04.

A Closer Look at the Coke Bottlers: A Perfect Storm

16 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

Figure 17. Mexico, Insured Employees by Region (Year on Year Growth), Dec 2000, Jun 2004

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Dec

-00

Feb-

01

Apr-

01

Jun-

01

Aug-

01

Oct

-01

Dec

-01

Feb-

02

Apr-

02

Jun-

02

Aug-

02

Oct

-02

Dec

-02

Feb-

03

Apr-

03

Jun-

03

Aug-

03

Oct

-03

Dec

-03

Feb-

04

Apr-

04

Jun-

04

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

Mexico Center North

Source: INEGI and Santander Investment.

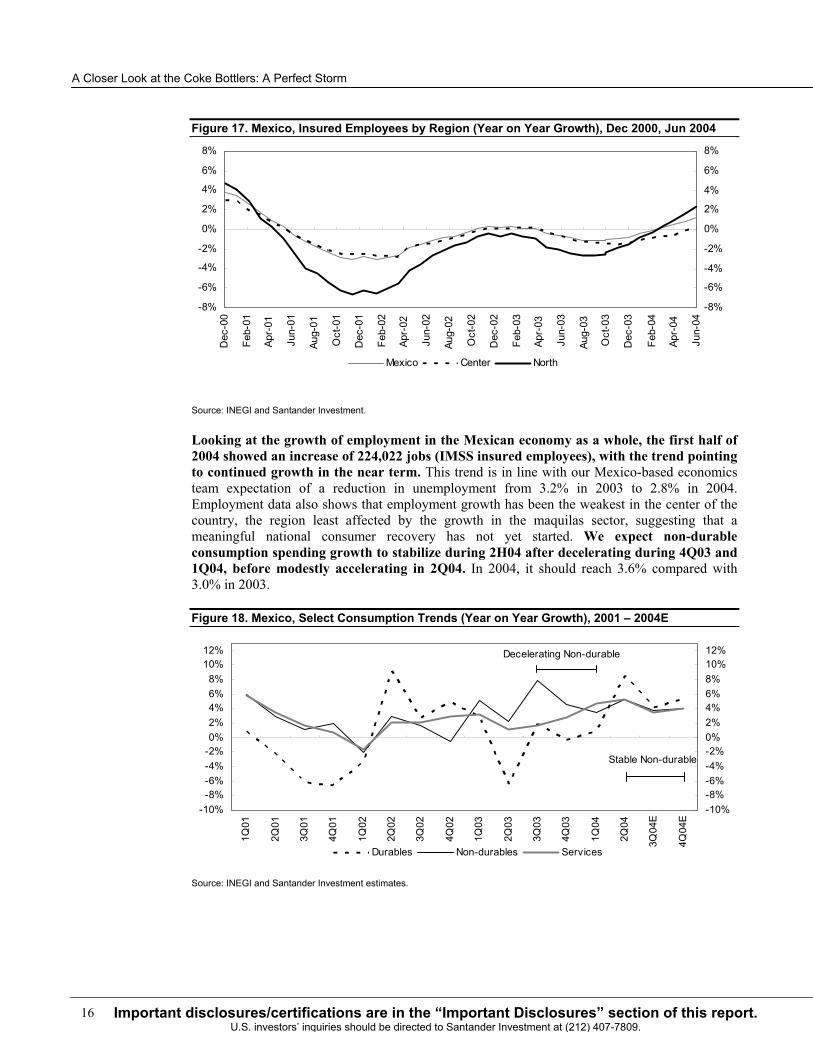

Looking at the growth of employment in the Mexican economy as a whole, the first half of 2004 showed an increase of 224,022 jobs (IMSS insured employees), with the trend pointing to continued growth in the near term. This trend is in line with our Mexico-based economics team expectation of a reduction in unemployment from 3.2% in 2003 to 2.8% in 2004. Employment data also shows that employment growth has been the weakest in the center of the country, the region least affected by the growth in the maquilas sector, suggesting that a meaningful national consumer recovery has not yet started. We expect non-durable consumption spending growth to stabilize during 2H04 after decelerating during 4Q03 and 1Q04, before modestly accelerating in 2Q04. In 2004, it should reach 3.6% compared with 3.0% in 2003.

Figure 18. Mexico, Select Consumption Trends (Year on Year Growth), 2001 – 2004E

-10%-8%-6%-4%-2%0%2%4%6%8%

10%12%

1Q01

2Q01

3Q01

4Q01

1Q02

2Q02

3Q02

4Q02

1Q03

2Q03

3Q03

4Q03

1Q04

2Q04

3Q04

E

4Q04

E

-10%-8%-6%-4%-2%0%2%4%6%8%10%12%

Durables Non-durables Services

Decelerating Non-durable

Stable Non-durable

Source: INEGI and Santander Investment estimates.

17Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

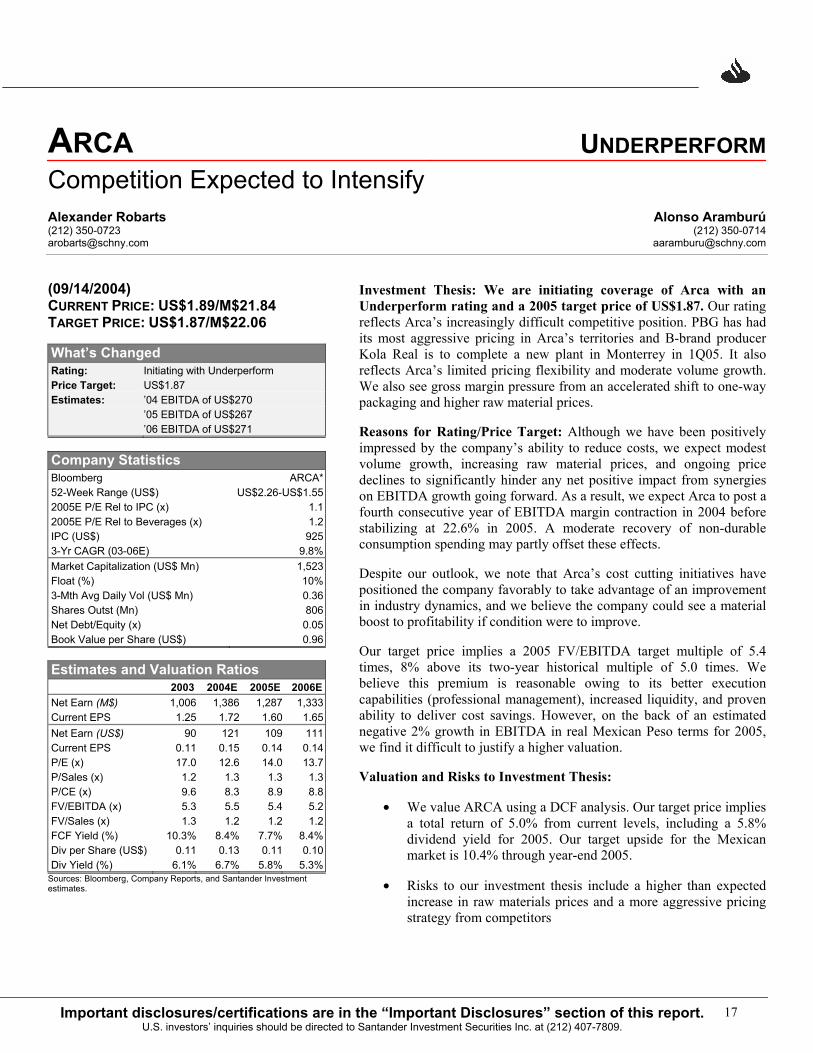

ARCA UNDERPERFORMCompetition Expected to Intensify Alexander Robarts Alonso Aramburú (212) 350-0723 (212) [email protected] [email protected]

(09/14/2004) CURRENT PRICE: US$1.89/M$21.84 TARGET PRICE: US$1.87/M$22.06

What’s Changed Rating: Initiating with Underperform Price Target: US$1.87 Estimates: ’04 EBITDA of US$270 ’05 EBITDA of US$267 ’06 EBITDA of US$271

Company Statistics Bloomberg ARCA* 52-Week Range (US$) US$2.26-US$1.55 2005E P/E Rel to IPC (x) 1.1 2005E P/E Rel to Beverages (x) 1.2 IPC (US$) 925 3-Yr CAGR (03-06E) 9.8% Market Capitalization (US$ Mn) 1,523 Float (%) 10% 3-Mth Avg Daily Vol (US$ Mn) 0.36 Shares Outst (Mn) 806 Net Debt/Equity (x) 0.05 Book Value per Share (US$) 0.96

Estimates and Valuation Ratios 2003 2004E 2005E 2006E Net Earn (M$) 1,006 1,386 1,287 1,333 Current EPS 1.25 1.72 1.60 1.65 Net Earn (US$) 90 121 109 111 Current EPS 0.11 0.15 0.14 0.14 P/E (x) 17.0 12.6 14.0 13.7 P/Sales (x) 1.2 1.3 1.3 1.3 P/CE (x) 9.6 8.3 8.9 8.8 FV/EBITDA (x) 5.3 5.5 5.4 5.2 FV/Sales (x) 1.3 1.2 1.2 1.2 FCF Yield (%) 10.3% 8.4% 7.7% 8.4% Div per Share (US$) 0.11 0.13 0.11 0.10 Div Yield (%) 6.1% 6.7% 5.8% 5.3%

Sources: Bloomberg, Company Reports, and Santander Investment estimates.

Investment Thesis: We are initiating coverage of Arca with an Underperform rating and a 2005 target price of US$1.87. Our rating reflects Arca’s increasingly difficult competitive position. PBG has had its most aggressive pricing in Arca’s territories and B-brand producer Kola Real is to complete a new plant in Monterrey in 1Q05. It also reflects Arca’s limited pricing flexibility and moderate volume growth. We also see gross margin pressure from an accelerated shift to one-way packaging and higher raw material prices.

Reasons for Rating/Price Target: Although we have been positively impressed by the company’s ability to reduce costs, we expect modest volume growth, increasing raw material prices, and ongoing price declines to significantly hinder any net positive impact from synergies on EBITDA growth going forward. As a result, we expect Arca to post a fourth consecutive year of EBITDA margin contraction in 2004 before stabilizing at 22.6% in 2005. A moderate recovery of non-durable consumption spending may partly offset these effects.

Despite our outlook, we note that Arca’s cost cutting initiatives have positioned the company favorably to take advantage of an improvement in industry dynamics, and we believe the company could see a material boost to profitability if condition were to improve.

Our target price implies a 2005 FV/EBITDA target multiple of 5.4 times, 8% above its two-year historical multiple of 5.0 times. We believe this premium is reasonable owing to its better execution capabilities (professional management), increased liquidity, and proven ability to deliver cost savings. However, on the back of an estimated negative 2% growth in EBITDA in real Mexican Peso terms for 2005, we find it difficult to justify a higher valuation.

Valuation and Risks to Investment Thesis:

• We value ARCA using a DCF analysis. Our target price implies a total return of 5.0% from current levels, including a 5.8% dividend yield for 2005. Our target upside for the Mexican market is 10.4% through year-end 2005.

• Risks to our investment thesis include a higher than expected increase in raw materials prices and a more aggressive pricing strategy from competitors

A Closer Look at the Coke Bottlers: A Perfect Storm

18 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

Arca is the second- largest Coca-Cola bottler in Mexico. The company produces, distributes and sells beverages under The Coca-Cola Company brand name, as well as proprietary and third party brands. The company was formed in 2001 through the merger of three bottlers in Mexico. Arca distributes its products in Northern Mexico, primarily in the states of Nuevo Leon, Chihuahua, Tamaulipa, Coahuila, Sonora, Sinaloa, Baja California and Baja California Sur.

KEY ISSUES AND OUTLOOK We expect modest volume growth, increasing raw material prices (see Raw Material Prices to Pressure Gross Margins section), and ongoing price declines to significantly erode any net positive impact from synergies on EBITDA growth going forward. According to management, Arca’s gross cost savings from the synergies program may reach M$700 million. The M$700 million is more than twice the initial management estimate announced in March 2003, which called for M$320 million of synergies. According to management, M$500 million of synergies were attained by March 2004, with an additional M$100 million expected to be achieved by 4Q04 and another M$100 projected for 2005. On a net synergy basis, however, we expect the total amount since 2003 could be as low as M$100 million.

The bulk of the synergies have come from the closing of 8 plants and 11 distribution centers. Other sources of savings have come from changes in the corporate structure. The number of legal entities has been reduced from 40 to 21, the workforce has been trimmed by 15% to 16,400 employees, operations has been simplified with the designation of one COO (versus two before), and the human resources and administrative functions have been centralized. Moreover, the operation has become more efficient through a 19% reduction in the number of routes from 2,026 to 1,701 and a 7% increase in the number points of sale. Finally, management has been able to reduce costs through outsourcing of PET bottles (through a partnership with Amcor) and other packaging materials, the installation of sugar clarification facilities, and a reduction in the cost of freight.

We view ARCA’s push to modernize its information infrastructure as a necessary long term project to remain competitive. We believe that under the current competitive environment, which is increasingly relying on price competition from both B-brands and PBG, combined with a low inflation environment, companies with superior revenue management capabilities will gain a competitive advantage. Access to accurate and updated market information will be a key tool to execute such market-driven strategies. We view ARCA’s investment in technology as an important step in gaining ground against the competition in this area. Arca recently completed the installation of four basic SAP modules, finance, production, procurement and warehousing and launched the installation of the human resources and supply chain modules in 1Q04. Management expects to complete the installation of these modules by March 2005.

Our main new concern is that Kola Real’s new plant will increase and prolong the pricing and volume pressure felt in Arca’s territories. Kola Real is expected to sell product from its new plant by February 2005. It is located 18 km outside of Monterrey, with an estimated installed capacity of 50 million unit cases by 2006. Kola Real’s low prices have disrupted Arca’s profit growth, albeit to a lesser degree than PBG’s aggressive pricing strategy, in our view. In fact, Kola Real recently raised its prices in Monterrey in its 3.1 liter presentation from 11 pesos to 12 pesos and in its 2.6 liter presentation from 9 pesos to 10 pesos. Nevertheless, the building of a plant in Arca’s backyard, Monterrey, which accounts for approximately 30% of Arca’s sales, and despite Kola Real already having a wide coverage of that territory, can only intensify the competitive threat, in our view. We estimate that Kola Real has approximately a 4% share of the Monterrey market, but we also believe that market share gains from Kola Real have stopped and we expect them to remain at current levels for the rest of 2004 and 2005.

Net impact from synergies on EBITDA may be only marginal.

ARCA is upgrading its technology.

Kola Real is building a plant in Monterrey.

19Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

The new Kola Real plant comes at a time when the competitive environment is already intense. The tough competitive environment in the first half of 2004 forced Arca to lower prices of its cola multi-serve presentations an average of 12%. As a result, EBITDA margin contracted 170 basis points year over year in 2Q04 after two consecutive quarters of EBITDA margin expansion. Unfavorable weather conditions also mitigated volume growth, particularly in 2Q04, but we anticipate a moderate improvement in the second half of 2004 and 2005 on the back of lower prices and a pick-up in consumption.

We expect Arca’s average price per unit case (excluding jug water volumes) to have a real decline of 5.6% in 2Q04 and 2.5% in 2005. In 2Q04, Arca realigned its prices in its 2.0 liter one-way, 2.0 liter returnable, and 2.5 liter one-way presentations from 14 pesos to 12 pesos, 12 pesos to 10 pesos and 15 pesos to 14 pesos, respectively. Together, these three presentations account for approximately 40%-45% of Arca’s total volumes. Arca also reduced prices in its 2.5 liter one-way flavors presentation from 15 pesos to 13 pesos at the beginning of 2004. Arca’s prices compare with PBG’s 2.5 liter one-way cola price of between 11 to 12 pesos, depending on the sales channel. In 3Q04, PBG reduced the pricing of its 2.0 liter one-way presentation from 11 pesos to 10 pesos, signaling the continuance of an aggressive pricing policy.

We do not expect any easing of the competitive environment in the short term. In fact, we would expect any potential price movements upward to be a reflection of higher raw material prices, not to be strategically driven. Finally, we expect Arca’s total soft drink volumes to be flat in 2004, including approximately 1% incremental volume from the new Meoqui territories, below management’s guidance of 1%-2% at the beginning of the year. In 2005, we expect soft drink volumes to increase 1.5% (1.1% pro forma), but total volumes to be flat on the back of a 9% decline in jug water volumes.

Figure 19. Arca– Pricing Architecture and Volume Mix, 3Q04

$3.0$4.0

$10.0

$4.5 $4.5$5.5

$12.0

$14.0

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0

$14.0

$16.0

12 ozGlass

0.5L Glass 2.0L RefPET

Can 500 ml NR 600 ml NR 2.0L NR 2.5L NR

2.0L NR, 9.0%

2.5L NR, 9.0%

2.0L Ref PET, 22.0%

12 oz & 0.5L Glass, 27.0%

600 ml NR, 15.0%

Other, 18.0%

Volume Mix does not include jug water. Sources: Company reports and Santander Investment estimates.

Part of Arca’s response to the competitive environment, in addition to realigning prices, has been the placement of coolers, increasing the penetration in the supermarket channel and pushing the sale of returnable and single serve presentations. The placement of coolers at the point of sale provides a competitive advantage, especially in a warm climate environment such as that found in Arca’s territories. The company plans to place 15,000 new coolers in 2004, the same amount as in 2003 and 8% higher than the 179,510 coolers at year-end 2003. Arca has also been pushing its presence in supermarkets to strengthen its position against B-brands and remains well-positioned for the potentially faster growth of this channel. Supermarkets currently account for approximately 4.2% of Arca’s sales. Finally, Arca is stimulating the consumption of single-serve and returnable presentations through promotions to push these more profitable packages and highlight the value-proposition from returnable packaging. In the water segment, Arca is emphasizing individual presentations while reducing its presence in the less profitable jug water business. In 2003, jug water volumes declined to approximately 20%, and we expect them to decline an additional 13% in 2004 and 9% in 2005.

We expect real decline in prices for 2004 and 2005.

A Closer Look at the Coke Bottlers: A Perfect Storm

20 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

The agreement to sell the Joya brand to The Coca-Cola Company for M$650 million will expand Arca’s portfolio of flavor drinks. The flavor market has become more competitive with the introduction of new flavor drinks from PBG and B-brand producers. Arca’s current flavor portfolio includes its proprietary brand Joya, which was sold primarily in the Northeast as well as The Coca-Cola Company brands Sprite and Fanta. Under the terms of the agreement Arca will continue to sell Joya, but will introduce List (Apple flavors) and Fresca (Grapefruit flavor) throughout its territories. The transaction is expected to close in 3Q04.

Shareholders should continue to benefit from a very attractive 2005 dividend yield, which we estimate to be 5.8% at current stock price levels. At the beginning of 2Q04, ARCA paid a dividend of M$0.70. We expect the company to complement this dividend payment with an extraordinary dividend of M$0.75 in 4Q04, on the back of the recent sale of the Joya brand to The Coca-Cola Company for approximately M$650 million and an estimated M$60 million payment from Amcor as part of their outsourcing of PET bottles agreement. In our view, in the absence of a large acquisition, we believe Arca can sustain a dividend payment close to our estimate of M$1.0 billion for 2005. We believe it is more likely that the company will close transactions similar to the one from Meoqui in the short term than a larger transaction, potentially with Contal. We estimate that adjacent territories such as Nogales sell approximately six million unit cases. Acquiring a territory of that size could require a disbursement of up to US$20 million according to our estimates, easily financed through the company’s own resources or through additional debt.

The Meoqui territories provide an estimated annualized 6.5 MUC of incremental volume. Arca acquired these territories in 1Q04, which required an initial investment of US$10 million in coolers, trucks, a distribution center and returnable bottles. We estimate that volumes on a pro-forma basis for 2004 and 2005 will decline 1% and increase 1.1%, respectively. Going forward, we believe it is more likely that the company will close transactions similar to the one from Meoqui in the short term than a larger transaction, potentially with Contal. We estimate that adjacent territories such as Nogales sell approximately six million unit cases. Acquiring a territory of that size could require a disbursement of up to US$20 million according to our estimates, easily financed through the company’s own resources or through additional debt.

VALUATION We used a DCF analysis to calculate our 2005 year-end target price of US$1.87, which implies a FV/EBITDA target multiple of 5.4 times. We project the free cash flows of the firm for 10 years and discount them by the company’s WACC. We use a WACC of 10.0%, based on a target equity to total capital ratio of 85%, a cost of debt of 9%, a risk free rate of 4.3%, a Beta of 0.86 and a country risk of 1.85%. Our cost of equity is 10.9%. Our terminal value uses a perpetuity growth rate of 1%.

Our target price of US$1.87 implies a total return of 5.0% from current levels, including a 5.8% dividend yield for 2005. Our target upside for the Mexican market is 10.4% through year-end 2005. At the target multiple of 5.4 times, ARCA’s valuation will be 8% above the company’s two-year trailing FV/EBITDA of 5.0 times. We believe this premium to its historical multiple is reasonable owing to its better execution capabilities (professional management), increased liquidity, and proven ability to deliver cost savings. On a relative valuation basis, Arca’s target multiple is 33% below our KOF 2005 target multiple of 7.2 times. This differential is slightly below Arca’s two-year historical discount to KOF of 35%, which we consider appropriate given Arca’s improved liquidity and management capabilities.

Arca offers an attractive dividend yield.

Newly acquired incremental volume.

21Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

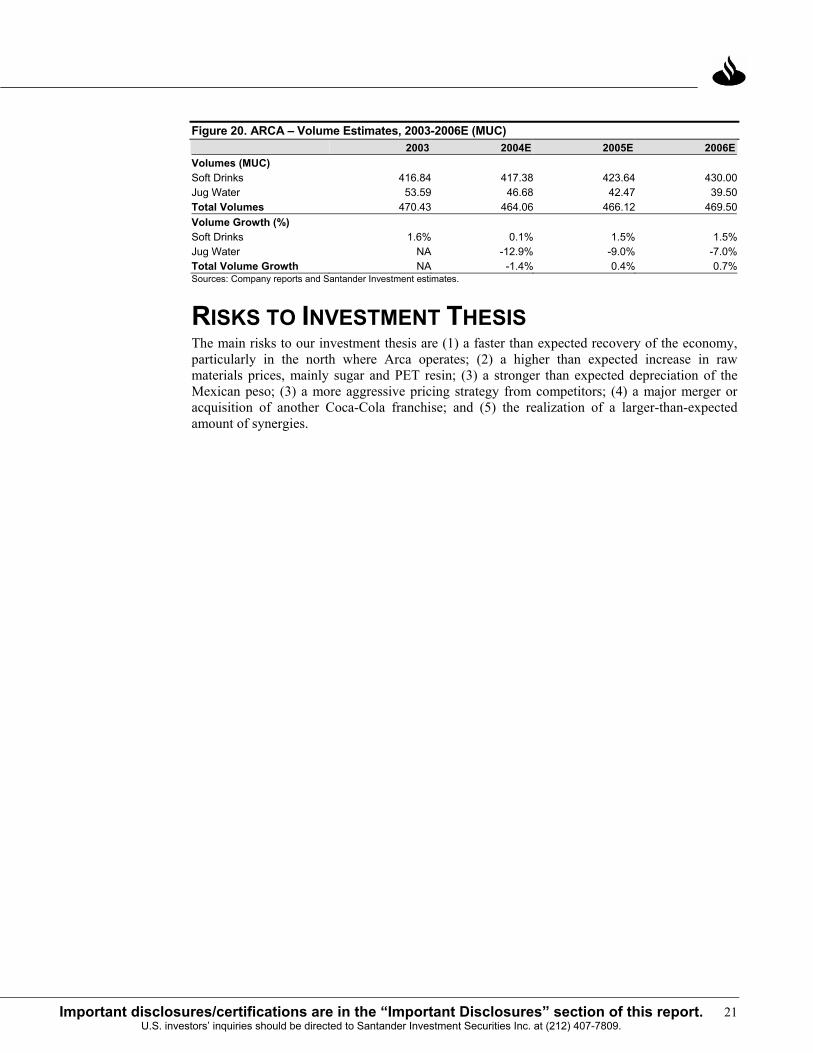

Figure 20. ARCA – Volume Estimates, 2003-2006E (MUC) 2003 2004E 2005E 2006EVolumes (MUC) Soft Drinks 416.84 417.38 423.64 430.00 Jug Water 53.59 46.68 42.47 39.50 Total Volumes 470.43 464.06 466.12 469.50 Volume Growth (%) Soft Drinks 1.6% 0.1% 1.5% 1.5%Jug Water NA -12.9% -9.0% -7.0%Total Volume Growth NA -1.4% 0.4% 0.7%Sources: Company reports and Santander Investment estimates.

RISKS TO INVESTMENT THESIS The main risks to our investment thesis are (1) a faster than expected recovery of the economy, particularly in the north where Arca operates; (2) a higher than expected increase in raw materials prices, mainly sugar and PET resin; (3) a stronger than expected depreciation of the Mexican peso; (3) a more aggressive pricing strategy from competitors; (4) a major merger or acquisition of another Coca-Cola franchise; and (5) the realization of a larger-than-expected amount of synergies.

A Closer Look at the Coke Bottlers: A Perfect Storm

22 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

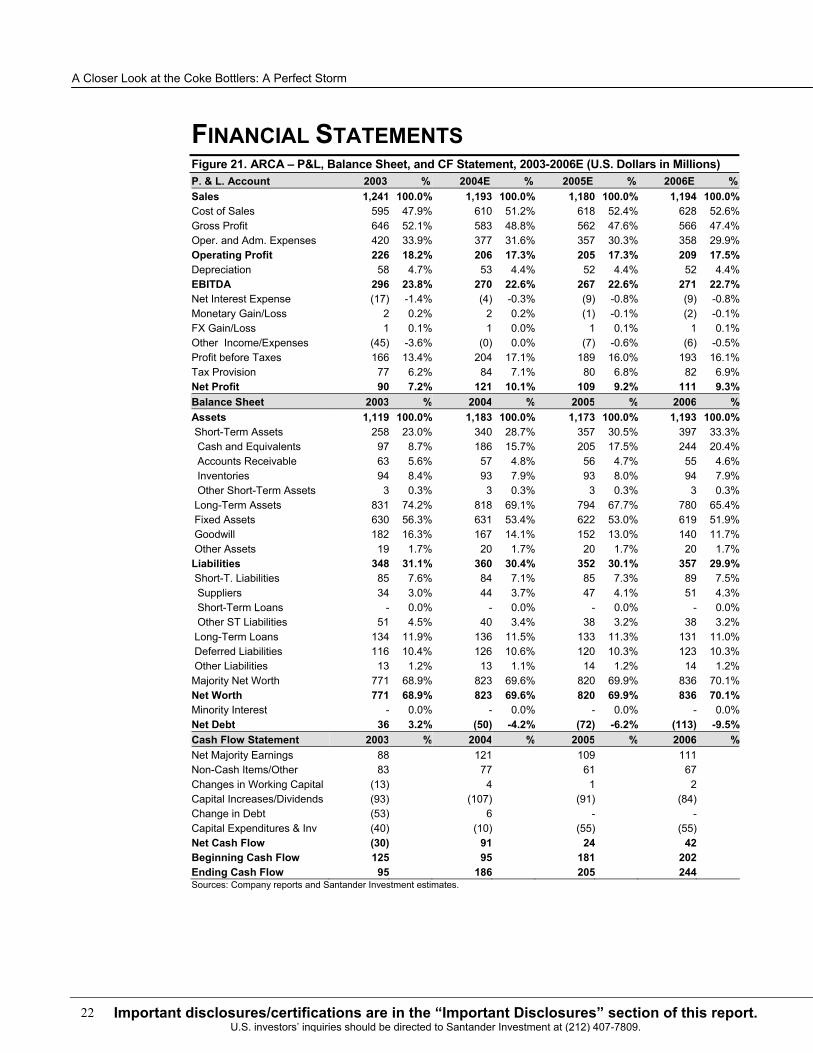

FINANCIAL STATEMENTS Figure 21. ARCA – P&L, Balance Sheet, and CF Statement, 2003-2006E (U.S. Dollars in Millions) P. & L. Account 2003 % 2004E % 2005E % 2006E %Sales 1,241 100.0% 1,193 100.0% 1,180 100.0% 1,194 100.0%Cost of Sales 595 47.9% 610 51.2% 618 52.4% 628 52.6%Gross Profit 646 52.1% 583 48.8% 562 47.6% 566 47.4%Oper. and Adm. Expenses 420 33.9% 377 31.6% 357 30.3% 358 29.9%Operating Profit 226 18.2% 206 17.3% 205 17.3% 209 17.5%Depreciation 58 4.7% 53 4.4% 52 4.4% 52 4.4%EBITDA 296 23.8% 270 22.6% 267 22.6% 271 22.7%Net Interest Expense (17) -1.4% (4) -0.3% (9) -0.8% (9) -0.8%Monetary Gain/Loss 2 0.2% 2 0.2% (1) -0.1% (2) -0.1%FX Gain/Loss 1 0.1% 1 0.0% 1 0.1% 1 0.1%Other Income/Expenses (45) -3.6% (0) 0.0% (7) -0.6% (6) -0.5%Profit before Taxes 166 13.4% 204 17.1% 189 16.0% 193 16.1%Tax Provision 77 6.2% 84 7.1% 80 6.8% 82 6.9%Net Profit 90 7.2% 121 10.1% 109 9.2% 111 9.3%Balance Sheet 2003 % 2004 % 2005 % 2006 %Assets 1,119 100.0% 1,183 100.0% 1,173 100.0% 1,193 100.0% Short-Term Assets 258 23.0% 340 28.7% 357 30.5% 397 33.3% Cash and Equivalents 97 8.7% 186 15.7% 205 17.5% 244 20.4% Accounts Receivable 63 5.6% 57 4.8% 56 4.7% 55 4.6% Inventories 94 8.4% 93 7.9% 93 8.0% 94 7.9% Other Short-Term Assets 3 0.3% 3 0.3% 3 0.3% 3 0.3% Long-Term Assets 831 74.2% 818 69.1% 794 67.7% 780 65.4% Fixed Assets 630 56.3% 631 53.4% 622 53.0% 619 51.9% Goodwill 182 16.3% 167 14.1% 152 13.0% 140 11.7% Other Assets 19 1.7% 20 1.7% 20 1.7% 20 1.7%Liabilities 348 31.1% 360 30.4% 352 30.1% 357 29.9% Short-T. Liabilities 85 7.6% 84 7.1% 85 7.3% 89 7.5% Suppliers 34 3.0% 44 3.7% 47 4.1% 51 4.3% Short-Term Loans - 0.0% - 0.0% - 0.0% - 0.0% Other ST Liabilities 51 4.5% 40 3.4% 38 3.2% 38 3.2% Long-Term Loans 134 11.9% 136 11.5% 133 11.3% 131 11.0% Deferred Liabilities 116 10.4% 126 10.6% 120 10.3% 123 10.3% Other Liabilities 13 1.2% 13 1.1% 14 1.2% 14 1.2%Majority Net Worth 771 68.9% 823 69.6% 820 69.9% 836 70.1%Net Worth 771 68.9% 823 69.6% 820 69.9% 836 70.1%Minority Interest - 0.0% - 0.0% - 0.0% - 0.0%Net Debt 36 3.2% (50) -4.2% (72) -6.2% (113) -9.5%Cash Flow Statement 2003 % 2004 % 2005 % 2006 %Net Majority Earnings 88 121 109 111 Non-Cash Items/Other 83 77 61 67 Changes in Working Capital (13) 4 1 2 Capital Increases/Dividends (93) (107) (91) (84)Change in Debt (53) 6 - -Capital Expenditures & Inv (40) (10) (55) (55)Net Cash Flow (30) 91 24 42 Beginning Cash Flow 125 95 181 202 Ending Cash Flow 95 186 205 244 Sources: Company reports and Santander Investment estimates.

23Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

Figure 22. Arca – P&L, Balance Sheet, and CF Statement 2003-2006E (Millions of Mexican Nominal Pesos) P. & L. Account 2003 % 2004E % 2005E % 2006E %Sales 13,936 100.0% 13,720 100.0% 13,919 100.0% 14,300 100.0%Cost of Sales 6,681 47.9% 7,018 51.2% 7,287 52.4% 7,520 52.6%Gross Profit 7,256 52.1% 6,702 48.8% 6,632 47.6% 6,780 47.4%Oper. and Adm. Expenses 4,721 33.9% 4,333 31.6% 4,218 30.3% 4,282 29.9%Operating Profit 2,535 18.2% 2,369 17.3% 2,413 17.3% 2,497 17.5%Depreciation 664 4.8% 608 4.4% 617 4.4% 624 4.4%EBITDA 3,323 23.8% 3,105 22.6% 3,149 22.6% 3,242 22.7%Net Interest Expense (192) -1.4% (45) -0.3% (110) -0.8% (110) -0.8%Monetary Gain/Loss 25 0.2% 25 0.2% (11) -0.1% (19) -0.1%FX Gain/Loss 9 0.1% 7 0.0% 14 0.1% 9 0.1%Other Income/Expenses (507) -3.6% (6) 0.0% (80) -0.6% (70) -0.5%Profit before Taxes 1,869 13.4% 2,349 17.1% 2,227 16.0% 2,308 16.1%Tax Provision 868 6.2% 970 7.1% 947 6.8% 981 6.9%Net Profit 1,006 7.2% 1,386 10.1% 1,287 9.2% 1,333 9.3%Balance Sheet 2003 % 2004 % 2005 % 2006 %Assets 12,571 100.0% 13,607 100.0% 13,836 100.0% 14,286 100.0% Short-Term Assets 2,894 23.0% 3,906 28.7% 4,217 30.5% 4,752 33.3% Cash and Equivalents 1,093 8.7% 2,142 15.7% 2,420 17.5% 2,919 20.4% Accounts Receivable 706 5.6% 658 4.8% 657 4.7% 664 4.6% Inventories 1,057 8.4% 1,068 7.9% 1,101 8.0% 1,129 7.9% Other Short-Term Assets 38 0.3% 38 0.3% 39 0.3% 40 0.3% Long-Term Assets 9,330 74.2% 9,404 69.1% 9,372 67.7% 9,336 65.4% Fixed Assets 7,072 56.3% 7,261 53.4% 7,340 53.0% 7,416 51.9% Goodwill 2,045 16.3% 1,917 14.1% 1,798 13.0% 1,678 11.7% Other Assets 214 1.7% 225 1.7% 234 1.7% 242 1.7%Liabilities 3,908 31.1% 4,140 30.4% 4,158 30.1% 4,275 29.9% Short-T. Liabilities 955 7.6% 969 7.1% 1,008 7.3% 1,065 7.5% Suppliers 383 3.0% 509 3.7% 560 4.1% 611 4.3% Short-Term Loans - 0.0% - 0.0% - 0.0% - 0.0% Other ST Liabilities 572 4.5% 460 3.4% 447 3.2% 454 3.2% Long-Term Loans 1,500 11.9% 1,568 11.5% 1,568 11.3% 1,568 11.0% Deferred Liabilities 1,305 10.4% 1,449 10.6% 1,420 10.3% 1,471 10.3% Other Liabilities 148 1.2% 155 1.1% 163 1.2% 171 1.2%Majority Net Worth 8,663 68.9% 9,466 69.6% 9,678 69.9% 10,011 70.1%Net Worth 8,663 68.9% 9,466 69.6% 9,678 69.9% 10,011 70.1%Minority Interest - 0.0% - 0.0% - 0.0% - 0.0%Net Debt 407 3.2% (574) -4.2% (852) -6.2% (1,352) -9.5%Cash Flow Statement 2003 % 2004 % 2005 % 2006 %Net Majority Earnings 1,007 1,386 1,287 1,333 Non-Cash Items/Other 950 887 715 804 Changes in Working Capital (147) 50 6 22 Capital Increases/Dividends (1,073) (1,233) (1,075) (1,000)Change in Debt (615) 68 - -Capital Expenditures & Inv (465) (109) (655) (660)Net Cash Flow (343) 1,048 278 499 Beginning Cash Flow 1,437 1,093 2,142 2,420 Ending Cash Flow 1,093 2,142 2,420 2,919 Sources: Company reports and Santander Investment estimates.

A Closer Look at the Coke Bottlers: A Perfect Storm

24 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

This page intentionally left blank.

25Important disclosures/certifications are in the “Important Disclosures” section of this report.

U.S. investors’ inquiries should be directed to Santander Investment Securities Inc. at (212) 407-7809.

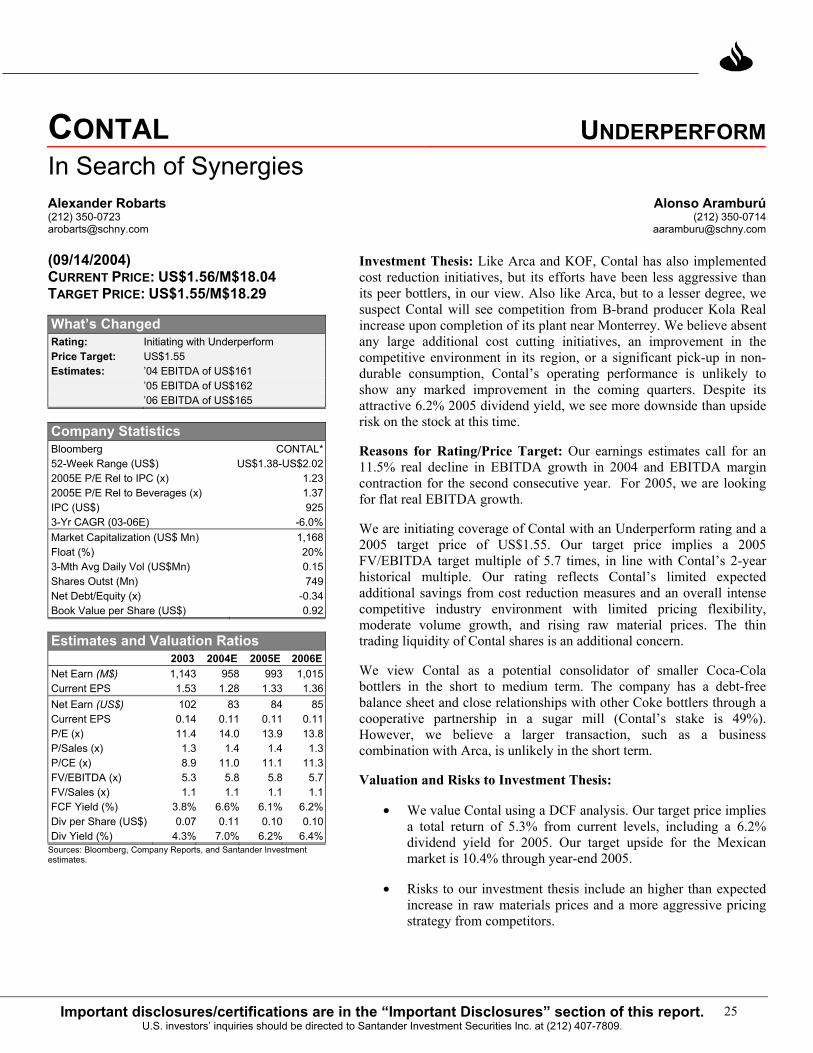

CONTAL UNDERPERFORMIn Search of Synergies Alexander Robarts Alonso Aramburú (212) 350-0723 (212) [email protected] [email protected] (09/14/2004) CURRENT PRICE: US$1.56/M$18.04 TARGET PRICE: US$1.55/M$18.29

What’s Changed Rating: Initiating with Underperform Price Target: US$1.55 Estimates: ’04 EBITDA of US$161 ’05 EBITDA of US$162 ’06 EBITDA of US$165

Company Statistics Bloomberg CONTAL* 52-Week Range (US$) US$1.38-US$2.02 2005E P/E Rel to IPC (x) 1.23 2005E P/E Rel to Beverages (x) 1.37 IPC (US$) 925 3-Yr CAGR (03-06E) -6.0% Market Capitalization (US$ Mn) 1,168 Float (%) 20% 3-Mth Avg Daily Vol (US$Mn) 0.15 Shares Outst (Mn) 749 Net Debt/Equity (x) -0.34 Book Value per Share (US$) 0.92

Estimates and Valuation Ratios 2003 2004E 2005E 2006E Net Earn (M$) 1,143 958 993 1,015 Current EPS 1.53 1.28 1.33 1.36 Net Earn (US$) 102 83 84 85 Current EPS 0.14 0.11 0.11 0.11 P/E (x) 11.4 14.0 13.9 13.8 P/Sales (x) 1.3 1.4 1.4 1.3 P/CE (x) 8.9 11.0 11.1 11.3 FV/EBITDA (x) 5.3 5.8 5.8 5.7 FV/Sales (x) 1.1 1.1 1.1 1.1 FCF Yield (%) 3.8% 6.6% 6.1% 6.2% Div per Share (US$) 0.07 0.11 0.10 0.10 Div Yield (%) 4.3% 7.0% 6.2% 6.4%

Sources: Bloomberg, Company Reports, and Santander Investment estimates.

Investment Thesis: Like Arca and KOF, Contal has also implemented cost reduction initiatives, but its efforts have been less aggressive than its peer bottlers, in our view. Also like Arca, but to a lesser degree, we suspect Contal will see competition from B-brand producer Kola Real increase upon completion of its plant near Monterrey. We believe absent any large additional cost cutting initiatives, an improvement in the competitive environment in its region, or a significant pick-up in non-durable consumption, Contal’s operating performance is unlikely to show any marked improvement in the coming quarters. Despite its attractive 6.2% 2005 dividend yield, we see more downside than upside risk on the stock at this time.

Reasons for Rating/Price Target: Our earnings estimates call for an 11.5% real decline in EBITDA growth in 2004 and EBITDA margin contraction for the second consecutive year. For 2005, we are looking for flat real EBITDA growth.

We are initiating coverage of Contal with an Underperform rating and a 2005 target price of US$1.55. Our target price implies a 2005 FV/EBITDA target multiple of 5.7 times, in line with Contal’s 2-year historical multiple. Our rating reflects Contal’s limited expected additional savings from cost reduction measures and an overall intense competitive industry environment with limited pricing flexibility, moderate volume growth, and rising raw material prices. The thin trading liquidity of Contal shares is an additional concern.

We view Contal as a potential consolidator of smaller Coca-Cola bottlers in the short to medium term. The company has a debt-free balance sheet and close relationships with other Coke bottlers through a cooperative partnership in a sugar mill (Contal’s stake is 49%). However, we believe a larger transaction, such as a business combination with Arca, is unlikely in the short term.

Valuation and Risks to Investment Thesis:

• We value Contal using a DCF analysis. Our target price implies a total return of 5.3% from current levels, including a 6.2% dividend yield for 2005. Our target upside for the Mexican market is 10.4% through year-end 2005.

• Risks to our investment thesis include an higher than expected increase in raw materials prices and a more aggressive pricing strategy from competitors.

A Closer Look at the Coke Bottlers: A Perfect Storm

26 Important disclosures/certifications are in the “Important Disclosures” section of this report. U.S. investors’ inquiries should be directed to Santander Investment at (212) 407-7809.

Grupo Continental, S.A. (Contal) is the third largest Coca-Cola bottler in Mexico and one of the 10 largest Coca-Cola bottling groups in the world. The company is dedicated to the production, sales and distribution of non-alcoholic, ready-to-drink beverages in the states of Durango, Coahuila, Zacatecas, Aguascalientes, San Luis Potosí, Jalisco, and Colima, covering 14.5% of Mexico's territory.