mergers and acquisitions as a growth strategy in the

TRANSCRIPT

MERGERS AND ACQUISITIONS AS A GROWTH STRATEGY IN THE PRIVATE

SECURITY INDUSTRY IN KENYA

BY

NGARI, ANNE WAIRIMU

UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA

SUMMER 2015

II

MERGERS AND ACQUISITIONS AS A GROWTH STRATEGY IN THE PRIVATE

SECURITY INDUSTRY IN KENYA

BY

NGARI ANNE WAIRIMU

A Research project Submitted to the Chandaria School of Business in Partial

Fulfillment of the Requirement for the Degree of Master of Business Administration

(MBA)

UNITED STATES INTERNATIONAL UNIVERSITY - AFRICA

SUMMER 2015

III

DECLARATION

I, the undersigned, declare that this is my original work and has not been submitted to any

other college, institution or university other than the United States International University in

Nairobi for academic credit.

Signed: Date:

Ngari Anne Wairimu (ID: 609873)

This project has been presented for examination with my approval as the appointed

supervisor.

Signed: Date:

Fred O. Newa

Signed: Date:

Dean, Chandaria School of Business

IV

COPYRIGHT

All rights reserved. No part of this project may be reproduced, stored in a retrieval system or

transmitted in any form or by any means, electronic, mechanical, photocopying, recording or

otherwise without permission from the author.

©Ngari Anne Wairimu 2015

V

ABSTRACT

The purpose of this study was to examine the mergers and acquisition as a growth strategy in

the Kenyan private security industry. The study narrowed down on two Kenyan private

security companies registered in the Kenya Security Industry Association (KSIA). The study

discussed the reasons for using mergers and acquisition as a growth strategy. The research

questions for this study were reason why organizations choose mergers as a growth strategy?,

why they choose acquisitions as a growth strategy?, the success factors for mergers and

acquisition.

The research design used in this study was a descriptive study and was guided by

questionnaires that were prepared online using Google forms. The link was emailed to the

target population of 40 where 32 employees filling in the forms. The sample was based on

three strata that is, top level managers, middle level management and the subordinates. The

data was cleaned then coded and input in the system using computer software. The data was

presented in form of tables, figures and graphs.

The following findings were revealed while looking at acquisition as a growth strategy.

Looking at the three variables, firstly acquisitions create value the study shows that there was

no correlation between growth and value creation. Secondly, acquisition provides access to

new channels there was a positive correlation between growth and new channels. This meant

that while using acquisition as a growth strategy, the organization would benefit from a

creation of new channels. Thirdly, acquisition helps in research & development and

innovation this can be a great motivation to participate in an acquisition but for this study

there was no link between growth and research, development and innovation.

The findings for the use of mergers as a growth strategy were derived from three variables.

The first attribute was mergers bring about economics of scale. The study showed that there

was a positive correlation between growth and economics of scale. Secondly mergers help

improve the market share, the study did not show any correlation between growth and the

market share and although there was some improvement in the market share, it was not

sufficient to promote growth. Thirdly, mergers achieve tax relief benefits for the

organization, the correlation between tax relief and growth was nonexistent.

VI

The findings for the success factors of mergers and acquisition looked at three attributes,

firstly was due diligence performed on the organization. There was a positive correlation

between due diligence and the success parameters. The findings showed that the key success

factors for mergers and acquisition in the private security industry in Kenya was performing

proper due diligence in the intended acquisition company. Secondly was the cultural

integration of the two organizations, although the corporate cultures are important, there was

no correlation with the success factors. In this case, it is safe to say that cultural integration

did not equal a successful merger or acquisition. Thirdly, there was no correlation between

the high cost of mergers and acquisition and the success attributes. This means that the cost

did not affect the success or any failures of the merger and acquisition.

In conclusion, the main reason for acquisition that promotes growth in the private security

industry in Kenya is access to new channels. Meanwhile the main reason for mergers that

promotes growth in the private security industry in Kenya is the economics of scale involved

in the combination of the two companies. Finally the key success factors for mergers and

acquisition in the private security industry in Kenya is performing proper due diligence in the

intended acquisition company. These are the points to consider when carrying out a merger

or acquisition in the private security industry in Kenya.

Recommendations derived from the study are linked to the research questions. Organizations

that use acquisition as a growth strategy need to be surgical and sell off loss making units,

and also departments that are duplicated this will help the organization create value that will

ensure growth. The study shows a positive correlation between using acquisition to gain new

channels and use it as a growth strategy. Organizations using acquisition stand to gain better

distribution and increase clientele. Although innovation, research and development allows

an organization to keep up with the growing needs of its clientele, the study shows that the

private security industry in Kenya has not embraced innovation as a reason to use acquisition

as a growth strategy. An international security company can be best suited to meet the gap of

innovation and research & development.

There is need to look at merger as a growth strategy as a way to consolidate companies

offering similar products, this will reduce the cost and maximize the growth. This can lead to

a monopolistic market, and create growth. The use of the BCG Matrix, to position the

VII

product on the depending on its growth against the market share before merging can help

anticipate the market share expected. Merging with a loss making organization earns the new

organization a tax relief. Although it will not achieve the expected growth, it will protect the

profits from the other organization from taxation.

The factors that have determined the success of mergers and acquisitions is clearly illustrated

as due diligence. An independent team needs to evaluate the merger and acquisition. Due

diligence takes long, thus reducing the effectiveness of the merger and acquisition especially

when it is a secret in the industry, it is the key to the success of the merger or acquisition.

Cultural integration is essential especially in order to reduce attrition of the top manager and

the talented staff. Overpriced organization can reduce the returns expected from the merger

or acquisition. Organizations should be willing to walk away rom highly priced mergers

when the goal is to achieve growth.

A recommendation for further study with a focus exclusively of each reason for merger and

acquisition was deduced. The variables do not explain 100% of this relationship. Therefore, it

is important that the managers of private security industries to consider that not all intended

benefits of mergers and acquisition are predetermined and obvious to begin with. With the

struggle to make profits in the industry, and the need to stay competitive, there will be an

ever-growing need to merge and acquire to foster fast growth.

VIII

ACKNOWLEDGEMENT

I would like to extend my sincere gratitude to Dr. Fred O Newa for his continued guidance in

preparation of the research project; I am also grateful for the unlimited support from my

family and friends. Their continued support and encouragement has brought me this far.

I am indebted to the G4S and KK Security Staff for their invaluable time to provide feedback

that has aided me to conduct an analysis of the mergers and acquisition as a growth strategy

in the private security industry. I appreciate their cooperation during period of research.

I Thank the Almighty God for His Mercies & Endless Grace during the learning period. It

has been a challenging experience and I am extremely humbled for completing this study.

IX

TABLE OF CONTENTS

DECLARATION................................................................................................................... III

COPYRIGHT ........................................................................................................................ IV

ABSTRACT ............................................................................................................................ V

ACKNOWLEDGEMENT ................................................................................................. VIII

TABLE OF CONTENTS ..................................................................................................... IX

LIST OF TABLES .............................................................................................................. XII

LIST OF FIGURES ........................................................................................................... XIV

ABBREVIATIONS .............................................................................................................. XV

CHAPTER ONE ..................................................................................................................... 1

1.0 INTRODUCTION........................................................................................................ 1

1.1 Background Of Problem............................................................................................. 1

1.2 Statement Of Problem ................................................................................................ 9

1.3 Purpose Of The Study .............................................................................................. 11

1.4 Research Questions .................................................................................................. 11

1.5 Importance Of The Study ......................................................................................... 11

1.6 Scope Of The Study ................................................................................................. 12

1.7 Definition Of Terms ................................................................................................. 13

1.8 Chapter Summary ..................................................................................................... 14

CHAPTER TWO .................................................................................................................. 16

2.0 LITERATURE REVIEW ......................................................................................... 16

2.1 Introduction .............................................................................................................. 16

2.2 Reasons Why Private Security Firms Use Acquisition as a Growth Strategy ......... 16

2.3 Reasons Why Private Security Firms Use Mergers as A Growth Strategy ............. 23

2.4 Factors That Have Determined The Success Of Mergers And Acquisitions ........... 28

X

2.5 Chapter Summary ..................................................................................................... 35

CHAPTER THREE .............................................................................................................. 36

3.0 RESEARCH METHODOLOGY ............................................................................. 36

3.1 Introduction .............................................................................................................. 36

3.2 Research Design ....................................................................................................... 36

3.3 Population and Sampling Design ............................................................................. 37

3.4 Data Collection Methods .......................................................................................... 39

3.5 Research Procedures ................................................................................................ 40

3.6 Data Analysis Methods ............................................................................................ 40

3.7 Chapter Summary ..................................................................................................... 41

CHAPTER FOUR ................................................................................................................. 42

4.0 RESULTS AND FINDINGS ..................................................................................... 42

4.1 Introduction .............................................................................................................. 42

4.2 Response Rate .......................................................................................................... 42

4.3 General Information ................................................................................................. 43

4.4 Acquisition as a Growth Strategy............................................................................. 48

4.5 Merger as a Growth Strategy ................................................................................... 53

4.6 Success Factor Of Mergers And Acquisition ........................................................... 60

4.7 Chapter Summary ..................................................................................................... 66

CHAPTER FIVE .................................................................................................................. 67

5.0 DISCUSSIONS, CONCLUSION AND RECOMMENDATIONS ........................ 67

5.1 Introduction .............................................................................................................. 67

5.2 Summary .................................................................................................................. 67

5.3 Discussion ................................................................................................................ 68

5.4 Conclusion ................................................................................................................ 78

XI

5.5 Recommendations .................................................................................................... 80

REFERENCES ...................................................................................................................... 83

APPENDICES ....................................................................................................................... 94

Appendix A: Cover Letter .................................................................................................. 94

Appendix B: Data Collection Instruments-Questionnaire .................................................. 95

XII

LIST OF TABLES

Table 3.1 Number of Employees ............................................................................................ 37

Table 4.1 Response Rate per Company .................................................................................. 42

Table 4.2: Response Rate per Former Company .................................................................... 43

Table 4.3: Comparison of Age and Education Level .............................................................. 44

Table 4.4 Level of Education .................................................................................................. 45

Table 4.5: Tabulates Previous Employer and Education Level .............................................. 46

Table 4.6: Job Levels against Previous Employer .................................................................. 47

Table 4.7 Motive for Using Acquisition as a Growth Strategy .............................................. 48

Table 4.8 Acquisition Creates Value Indicators ..................................................................... 49

Table 4.9: Correlation of Growth and Value Creation ........................................................... 49

Table 4.10 Access to New Channels Indicators ..................................................................... 50

Table 4.11: Correlation Between Growth And Creating New Channels ................................ 51

Table 4.12 Regression Of Growth And Creating New Channels ........................................... 51

Table 4.13 Anova Growth And Creating New Channels ....................................................... 51

Table 4.14 Coefficients Growth And Creating New Channels ............................................... 52

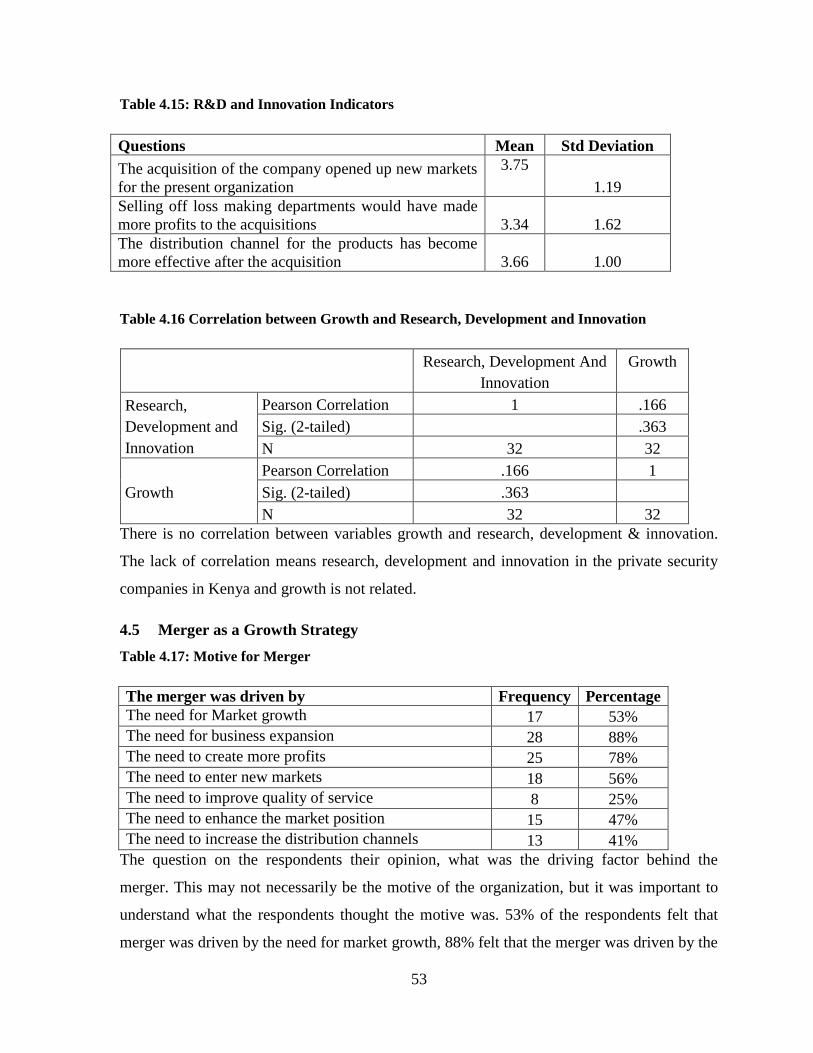

Table 4.15: R&D and Innovation Indicators........................................................................... 53

Table 4.16 Correlation between Growth and Research, Development and Innovation.......... 53

Table 4.17: Motive for Merger ............................................................................................... 53

Table 4.18: Merger Should Not Have Occurred Indicators .................................................... 54

Table 4.19: Merger as Growth Strategy Indicators ................................................................. 55

Table 4.20: Merger Driver’s Indicator .................................................................................... 55

Table 4.21: Economics of Scale Indicators............................................................................. 56

Table 4.22 Correlation Between Economics Of Scale And Growth ...................................... 57

Table 4.23 Regression Between Economics Of Scale And Growth ....................................... 57

Table 4.24 ANOVA Between Economics Of Scale And Growth .......................................... 57

Table 4.25 Coefficients Between Economics Of Scale And Growth ..................................... 58

Table 4.26: Market Share Indicators ....................................................................................... 58

Table 4.27 Correlation Between Market Share And Growth ................................................. 59

Table 4.28 Tax Relief Benefits Indicators .............................................................................. 59

Table 4.29 Correlation Of Tax Relief And Growth ................................................................ 60

XIII

Table 4.30 Merger / Acquisitions Shouldn’t Have Happened Indicators ............................... 60

Table 4.31 The Merger / Acquisition Should Not Have Happened ........................................ 61

Table 4.32: Value Of The Acquired Company ....................................................................... 61

Table 4.33 Due Diligence Indicators ...................................................................................... 62

Table 4.34 : Correlation Of Due Diligence and Success Factors ........................................... 62

Table 4.35 : Regression Of Due Diligence And Success Factors ........................................... 62

Table 4.36 : ANOVA Of Due Diligence And Success Factors .............................................. 63

Table 4.37 : Coefficients Of Due Diligence And Success Factors ......................................... 63

Table 4.38: Cultural Integration Indicators ............................................................................. 64

Table 4.39: Correlation Between Culture Integration And Success Factors .......................... 65

Table 4.40: High Costs Of Merger And Acquisition Indicators ............................................. 65

Table 4.41 Correlation between the Cost of the Acquisition and the Value after Acquisition65

XIV

LIST OF FIGURES

Figure 4.1 Age Bracket of Respondents ................................................................................. 44

Figure 4.2 Previous Employer Before The Merger / Acquisition ........................................... 45

Figure 4.3: Job Levels of Respondents ................................................................................... 47

Figure 4.4 Access to New Channel ......................................................................................... 50

Figure 4.5: Merger Shouldn’t Have Occurred ........................................................................ 54

XV

ABBREVIATIONS

BCG - Boston Consulting Group

CBK - Central Bank of Kenya

G4S - Group 4 Securicor

KK - Kenya Kazi Ltd

KRA - Kenya Revenue Authority

KSIA - Kenya Security Industry Association

M&A - Mergers and Acquisition

PSC - Private Security Company

PSIA - Protective Services Industry Association

ROI - Return on Investments

SPSS - Statistical Package for Social Scientists

K9 - Canine

1

CHAPTER ONE

1.0 INTRODUCTION

1.1 Background Of Problem

The purpose of the growth in business is to provide development opportunities of business

before their competitors and to help the resistance and give easy struggles in the moment

when face to face with difficulties (Akgöbek, 2012). Mergers and acquisitions have been

used over years as a way to grow business. Their activities around the world has been

booming for the last three decades, but the intense M&A activity is in sharp contrast with the

high rate of failure and dissatisfaction with its performance (Weber and Tarba, 2012).

Acquisitions and mergers are a national as well as global trend. They occur everywhere – in

organizations, administrative units and businesses in all industries and of all sizes (Balle,

2008).

Mergers and Acquisitions are the most effective and efficient ways to enter a new market,

add a new product line, or increase distribution reach. This is evident when large firms merge

in order to fill the gaps in their production pipeline or due to anticipated patent expirations,

while small firms merge as an exit strategy (Hassan, Patro, Tuckman and Wang, 2007).

Mergers and acquisitions have not always been successful, according to Galpin (2008)

overall poor M&A results may be attributed to a number of factors – poor strategic fit,

incomplete or haphazard due diligence, and ineffective integration efforts. Considering that

the motives of private security companies are different from the police, Bodnar (2012) notes

that ultimately private security companies are motivated by profits and seek to maximize

profits.

Many companies all over the globe consider M&A strategies to meet cost and increase

revenue especially in the competitive corporate world, price wars. The banking industry

worldwide has been consolidating at a dramatic rate over the past 30 years, and this trend is

ongoing (Lambkin and Muzellec, 2008). Over the past few decades, we have seen countless

examples of companies, such as General Electric, Google, and Cisco that have grown

dramatically and built revenues through aggressive acquisition programs (Sherman, 2011). A

2

look at Kenya according to the Central bank of Kenya, 33 banks have merged to form new

entities since 1989 to date, while four acquisitions have occurred since 2000 to 2008 (CBK,

2013).

Security companies originated during the middle Ages when lords needed to protect their

properties. According to Nemeth (2012), there was chaos and circumstances of medieval

England and Europe that led to the establishment of private, self-policing force. Regular

patrols of Citizens were established to stand watch nightly and to arrest criminals and

strangers found wondering at night. Nemeth (2012) continues to state that the expanding

trade and transportation of vital goods and services were temptations for criminals. It also

demanded the need for protection of private interest, proprietary and contract security.

Nemeth (2012) Individual merchants hired men to guard their property, and merchant

associations created merchant police to guard shops and warehouses. The essence of private

security was born in the chaos of the middle ages, especially that of the "contract" variety,

but the standardization of its organization hierarchy duties, and pay was yet to come.

Nemeth (2012) in Colonial America the first night watch was formed in Boston in 1634.

Serving as a guard was the duty of every male citizen over the age of 18. The need for

security entered on commercial interest, but on fear for fire, vagrants and attacks by the

Native Americans. One of the oldest security companies was Pinkerton Company. According

to Nemeth (2012) while Pinkerton officers were serving as the protectors of American

railroad and as basically, the only uniform system of law in the west, Pinketon was one of the

firms hired by business management to disrupt and disband labor activities (Nemeth, 2012).

In 2003 Pinkerton was acquired by Swedish security giant Securitas AB, and switched its

name to Securitas Critical Infrastructure (Chris, 2014).

According to Perry (2012), Securitas purchased of Burns, in 2000; then went on to make

about a dozen other acquisitions. Securitas continues to concentrate most of its recent

acquisition activity in the emerging markets. He also states that G4S uses the acquisition

strategy to enter new markets. G4S made its initial entry into the U.S. with the purchase of

Wackenhut in 2002, since that time, they have divested some of the traditional standing

security officer business and has limited its acquisition activity in the U.S. security market to

3

mostly electronics and high-end investigative type companies. Currently G4S has

concentrated most of its acquisition activity in the emerging markets (Perry, 2012).

The private security industry has evolved over the years today, it is responsible not only for

protecting many of the nation‘s institutions and critical infrastructure systems, but also for

protecting intellectual property and sensitive corporate information. U.S. companies also rely

heavily on private security for a wide range of functions, including protecting employees and

property, conducting investigations, performing pre-employment screening, providing

information technology security, and many other functions (Strom, Berzofsky, Shook-Sa,

Barrick, Daye, Horstmann, and Kinsey, 2010).

According to Weisbecker (2008), G4S in America has grown by acquisition with its top USA

holding being Florida based Wackenhut, a nationwide security firm that continues to operate

under its pre-merger name. Formed by the merger of two major European security firms in

2004, G4S, among other things, manages billions in cash for British commercial banks, runs

nine juvenile and adult "custody facilities" in the U.K. and U.S., and does risk management

consulting for a wide variety of clients. Weisbecker (2008) goes on to say that with the MJM

acquisition, G4S added insurance fraud to its already hefty catalog of business lines. As

MJM's growth curve suggests, insurance-fraud investigations could be a lucrative sector.

These illustrates that G4S has grown to be the second largest security company in America

by acquiring organizations.

Looking at Canada, GardaWorld is a Canadian security firm who’s headquartered is in

Montreal, Quebec. It employs around 45,000 people across North America, Europe, Africa,

Asia, Latin America and the Middle East (Chris, 2014). GardaWorld secures individuals and

resources in at least 140 cities and protects 28 North American airports (Chris, 2014). In

August 2013, GardaWorld acquired G4S’ Canadian cash management division in a deal

thought to be worth around $110 million (Chris, 2014). This shows that even large security

companies result to acquisition to increase their market share and diversify their product

portfolio.

In traditional African society, many rich people in various communities often hired the

services of private guards in ensuring the security of their lives and property (Kasali, 2008).

4

Uganda’s Department of Private Securities and Firearms at the police headquarters, by 2002

there were nearly 69 registered Private Security Companies and most had followed the

Control of Private Security Organizations Regulations of 1997 to acquire firearms (Mkutu

and Sabala, 2007). The Kenyan private security sector has expanded in recent years, and has

exported its services to other countries in the region, including the Democratic Republic of

Congo, Ethiopia, Rwanda, Sudan, Tanzania and Uganda (Mkutu and Sabala, 2007).

The private security sector in Africa is a reflection of a global trend, by which the post-Cold

War victory of neo-liberalism at the turn of the 1990's and its global expansion since then

have given thrust to a shift towards privatization (Thuranira and Munanye, 2013). This is

clearly seen in the privatization of prisons in Europe, and the outsourcing of prison wardens

to security companies like G4S. In more recent times, with the outsourcing of non-core

functions to Private Security Companies (PSCs) in the west and the exportation of these

privatized services to conflict and post-conflict settings example being Iraq and Afghanistan

(Thuranira and Munanye, 2013).

Private security industry in South Africa can be traced to the late 1970s and early 1980s. Its

development was encouraged by the governing political party at the time, the National Party,

as a way to address the political climate (Bodnar, 2012). The Government ordered that the

police engage in political duties and address political unrest, even if this meant they would

need to withdraw from traditional policing duties. This left a gap in the security sector for the

private security industry to fill (Bodnar, 2012).

There is a lot of competition between South African private security companies. There are

many small fly-by-night type security companies that provide a cheap but substandard

service, thereby tarnishing the image and reputation of the industry as a whole (Irish, 1999).

Through a number of mergers and takeovers, many of the larger private security companies

have consolidated their position even further. There is a danger that a few large companies

could end up dominating and even monopolizing the South African private security market

(Irish, 1999).

Government of South Africa tender procedures tends to favor companies with a racially

diverse or non-white racial make-up (Irish, 1999). As a result, the 1990s have witnessed the

5

formation of partnerships between small black-owned security companies and larger white

dominated companies, or mergers with and buy-outs of white-owned companies by black-

owned companies. Examples of this include Fabcos’ merger with Coin, and Khulani

Holdings’ purchase of Springbok Patrols (Irish, 1999).

Irish (1999) goes on to say that although such initiatives have worked in a number of cases

they have been a failure in some instances. Many smaller black companies complain that

they do not benefit fully from partnership agreements, but are being used simply to comply

with tender procedures. A number of partnership agreements have collapsed because of these

problems (Irish, 1999). Papadakis (2007) drew attention to mistakes that took place before

the merger. He argued that the seed of unsuccessful mergers was sown well before the deal

was signed. He goes on to point out “Among the main mistakes that usually take place before

the merger to be the managerial hubris problem, the lack of thorough due diligence, improper

selection of the target, the exceedingly high premiums paid.

The reasons for the drop in mergers and acquisitions were not clear but Mchale (2013)

speculated firstly that industry major restructuring from 2009 to 2011, and in the last two

years, had paused to consolidate that process. Secondly, lack of confidence and/or interest by

the major conglomerates to commit more investment to the industry, thirdly that there were a

lack of buyers from outside the business, particularly defense and it (Mchale, 2013).

In Congo, the majority of the 35–45 registered security companies are not operational.

Currently, a few security companies dominate the market for residential and commercial

clients in Kinshasa. Late in 2006, G4S bought DSA, thereby establishing a market-

dominating firm. G4S and DSA are international Private Security Companies, whereas most

other companies are Congolese (Goede, 2008).

Kenya has seen an increasing level of crime in recent years (Mkutu, 2007). Both the rise in

crime and the growth of the private security sector in Kenya are intimately connected to the

erosion of state capacities and services that began in the late 1980s and continued throughout

the 1990s (Abrahamsen and Williams, 2005). Between 2002 and January 2005, police

records showed 4,467 people killed by criminals (Mkutu, 2007). As a response to the feelings

of insecurity, the private security industry is growing fast (Mkutu, 2007).

6

The capital city of Kenya, Nairobi is home to a number of international organizations and

national embassies, including the second largest US embassy on the African continent

(Abrahamsen and Williams, 2005). Nairobi is also the regional headquarter for the United

Nations, and taken together international clients provide a substantial and particularly

lucrative market for private security companies (Abrahamsen and Williams, 2005).

Private security provision has a long history in Kenya, and companies like KK Security,

Factory Guards (now Security Group) and Securicor (acquired and renamed by G4S)

remained have operated in the country since the 1960s (Abrahamsen and Williams, 2005;

G4S, 2013a). The main expansion of the sector can be dated to the late 1980s and early

1990s, and private security continues to be one of the fastest growing sectors of the Kenyan

economy (Abrahamsen and Williams, 2005).

There is no special license is required and security companies are registered in the same

manner as any other business (Abrahamsen and Williams, 2005). There are currently two

rival industry associations in the Private Security industry in Kenya; these are Kenya

Security Industry Association (KSIA) and Protective Services Industry Association (PSIA)

(Abrahamsen and Williams, 2005). KSIA is the federation of private companies whose core

business is the supply of security products and services (KSIA, 2005). According to the

KSIA (2005), it has 29 registered members who strive to uphold the standards set by KSIA.

This is not the exact number of security companies in Kenya, since there are many security

companies not registered. The main reason for this discrepancy is that no special license is

required and security companies are registered in the same manner as any other business

(Abrahamsen and Williams, 2005).

Abrahamsen and Williams (2005) illustrates that top and second tier security companies in

Kenya will undergo a period of consolidation and mergers, since there is a high number of

companies’ competing for a relatively stable market. Example being KK Security acquired

EARS, and Securicor purchased Falcon Security. There is speculation that mergers of a

similar nature will occur in the future, and that a number of owner-mangers are looking to

sell their businesses as going concerns.

7

Mergers and acquisitions (M&A) in Kenya follow the usual paths adopted in other countries.

The majority of cases involve private companies, with relatively few transactions involving

public listed companies (Harney, and Khan, 2010). Thus the common forms are: acquisitions

of control of private companies; acquisitions of businesses as a going concern – asset

acquisitions; creation of joint ventures; acquisitions of minority or majority holdings by

strategic investors in particular sectors, such as banking or telecommunications; and mergers

involving the creation of new holding companies for existing entities (Harney and Khan,

2010).

The security industry in Kenya uses mergers and acquisitions differently. Unlike the

‘‘financial play’’ deals of bygone eras, the reasons for doing M&A’s today are ‘‘operational

leap’’ and a ‘‘shortcut to growth.’’ The targets are similar – in the same industry, have

similar products, and serve the same customers (Galpin, 2008). All this is aimed at capturing

the four c’s which are customer, competencies, channels, and content.

According to Sherman (2011) the sources of debt finance are looking at the M&A market

differently today from the way they did until 2006. The value of deals has decreased, with

conservative and tight valuation of target companies along with a decrease in the volume of

transactions. Due to many failures of M&A, many financers are shying away from such

deals.

An outlook of mergers and acquisitions in Kenya is that they are driven by the organization’s

need to gain more from a merged organization than what can be gained from an independent

organization. Through mergers and acquisitions, companies try to grow and expand their

assets, sales and market share, improve their scientific knowledge, technological

competences and product portfolio. Therefore, the benefits of consolidation extend beyond

pure financial motives, such as creating new market opportunities, building core

competences, expanding economies of scale and sustaining long-term competitive advantage

(Lodorfos and Boateng, 2006).

Furthermore, firms shift focus into higher value added production through changing the

emphasis of their research and development by buying firms that specialize in fields, which

8

they want to acquire. Therefore, mergers and acquisitions represent a strategic choice

(Lodorfos and Boateng, 2006).

Mergers and acquisitions are corporate strategies; corporate strategy is concerned with

arranging the business activities of the corporation as a whole, with a view to achieve certain

predetermined objectives at the corporate level (Sudarsanam, 2003). Corporate strategy is

how a firm creates value through the configuration and coordination of its multi-market

activities (Peng, 2009).

Mergers and acquisitions are corporate strategies used as a market entry strategy. The choice

for M&A depends on various factors, for example, the competition in a host market could be

high and there is excess capacity. Building new capacity is likely to invite retaliation from

the existing players thus; it makes more sense to acquire an existing firm to reduce the risk of

retaliation.

The main reasons organizations take part in Mergers and Acquisition is to grow the business,

this in turn increases revenue and profits while reducing the time it would take to grow

through internal growth. M&A brings similar resources that help to foster synergy, which

brings growth in revenue. Internal growth is usually slow due to the development of

resources needed to foster growth. The Private security industry in Kenya has grown rapidly

and almost monopolistic through mergers and acquisition.

Key growth indicators include revenue growth, increased market share, growth in sales,

increased employment, more sales, increased profits and innovations all these can be

achieved jointly or independently. Depending on the strategic intent of the organization

either can be an outcome of the growth strategy. Companies that are experiencing organic

growth tend to avoid M&A, but companies suffering from poor organic growth and suffer

from a lot of pressure for growth from the shareholders. These managers are more likely to

adopt aggressive strategies geared to growth maximization to release the pressure.

The merger or acquisition of two organizations that are servicing a homogenous customer

base and has similar customer facing jobs, overlapping distribution, and market is bound to

succeed. The combination of knowledge from the two organizations means that the new

formed entity has a higher competitive advantage over the rest. The combination with

9

organizations in the similar field tends to increase the market share and can bring about a

monopolistic monetary gain to the newly formed company.

1.2 Statement Of Problem

Mergers and acquisitions in the private security industry in Kenya are rarely documented; it

has become the culture of the industry to grow the business via acquisition or mergers. There

is a need to understand mergers and acquisitions in the private security industry in Kenya.

KK security began its work in Mombasa, moved to Nairobi to increase their market share. It

faced stiff competition from EARS security group and approached them for an acquisition in

order to gain their huge market share. The acquisition is only documented in a website article

from the year 2004. The consolidation in the local security industry escalated last week with

the acquisition of the EARS Group by KK Limited. The development creates what is clearly

an industry giant with billings expected to hit Sh2 billion a year (Akum, 2004). KK Security

acquired Lodgit to grow their cash solutions department and Knight Support to grow their

fire and rescue department (KK, 2014).

G4S Kenya has gone through a series of acquisitions and merges to reach the position it is

right now. It started in 1969 as Securicor after acquiring three companies K9 Guarding

Company, Night security and Guarding Services Company. Between 1991 and 2000,

Securicor Security Services Kenya Limited acquired Express Security and thus gained its

Cash Services department. Between 2000 to date, Securicor acquired Falcon Security, and

Group4 Falck Security merged with Securicor, but maintained the Securicor name. They

latter acquired Vera Security (Malindi), Polea Alarms (Kisumu), and Tanara Alarms

(Nairobi), increasing their market share in the three towns. Securicor was acquired by G4S

and changed its name to G4S. G4S acquired Armor Group, Urban Fire and Archive

solutions. From Urban Fire, they gained their fire unit and from Archive solutions, they

gained their secure data solution unit (G4S, 2013b).

Globalization has changed the face of business in the world. All organizations realize that

they need to grow within the shortest time possible. Merging and acquisition of competing

firms is aimed at improving the competitive advantage. Formed by the merger of two major

European security firms in 2004, G4S, among other things, manages billions in cash for

British commercial banks, runs nine juvenile and adult "custody facilities" in the U.K. and

10

U.S., and does risk management consulting for a wide variety of clients. The company also

provides on-site security for the Kennedy Space Center; a NASA research facility in

California; the Wimbledon tennis championships in London; various airports, including those

in Oslo and London; and political parties and events (Weisbecker, 2008). Many companies

believe that mergers or acquisitions are a key means for growth (Walker and Price, 2000).

The combining of resources, increase market share, coupled with a wider product range

means that Mergers and Acquisitions are one of the most preferred forms of market entry

strategies.

Mchale (2013) in his online article noted that in 2013 there was a 48% drop in the value of

mergers and acquisitions with the value in 2013 being approximately $5.0 billion. He goes

on to say that, there were 34 deals in 2013 compared to 56 in 2012. While the number of

deals and total value of acquisitions had fallen, the average value of a deal had actually

increased from $120 million in 2011 to $147 million in 2013 (Mchale, 2013).

Out of the 35 – 45 registered security companies in Congo, few are operational. The

ownership of these Congolese companies is in the hands of expatriates from Lebanon, Israel,

Belgium and South Africa. It appears that clients prefer to work with internationals rather

than Congolese PSCs and it is difficult for Congolese PSCs to acquire a firm footing on the

market (Goede, 2008) could this be the reason why many private security compaies opt to

merger or acquire exsisting companies, in order to have a competitive edge over other

companies.

When looking to enter the security industry, an organization can use many entry strategies.

With the above illustrations, one can clearly see that security companies favor mergers or

acquisitions as their entry and growth strategy. M&A’s are strategies for market entry that

are aimed at gaining a competitive advantage. Either what drives the choice for a merger or

acquisition is this trend unique to Kenya or is it a winning formula all over the world in the

security industry. Many M&A’s has been driven by the need to increase shareholder value

more than by sound strategic thinking. Simple momentum, imitative behavior, executive ego

or organization stagnation are among the other understandable, but questionable motives that

drive M&A activity (Lynch and Lind, 2002). There lies a gap in the choice between mergers,

acquisition and the success factor of mergers and acquisitions. This study aims to understand

11

the reasons why private security companies in Kenya use mergers and acquisitions as a

growth strategy.

1.3 Purpose Of The Study

The purpose of the study was to investigate the reason why mergers and acquisitions were

used as a growth strategy in the private security industry in Kenya and the success factors of

mergers and acquisitions in the private security industry in Kenya.

1.4 Research Questions

The research was guided by the following research questions:

1.4.1 Why Do Private Security Firms In Kenya Use Acquisition As A Growth Strategy?

1.4.2 Why Do Private Security Firms In Kenya Use Mergers As A Growth Strategy?

1.4.3 What Are The Factors That Determine The Success Of Mergers And Acquisitions?

1.5 Importance Of The Study

Key stakeholders to benefit from the study include

1.5.1 Investors

This study aims to be important to investors because they would need to understand what

affects the success of mergers and acquisitions in Kenya and especially the security industry.

1.5.2 Regulatory Bodies

This report aims to be beneficial to regulatory bodies that would gain a better understanding

on mergers and acquisitions. For them to be able to understand the success factors of M&A

and in future help these bodies to come up with regulations to govern M&A’s.

1.5.3 Staff In Merger And Acquisition Companies

This study aims to be important to staff that work in merger and acquisition companies to

allow them understand its importance and assist in the successful adoption of mergers and

acquisitions in Kenya

12

1.5.4 Government Of Kenya

This will equip the government especially the Kenyan investment council to educate

investors into the Kenyan market via mergers and acquisitions. The results of the studies can

benefit the government especially to set up policies on market entry strategies.

1.5.5 Academicians And Researchers

This study aims to help the academic world in future researches on success factors of

mergers and acquisitions. This research can one day be furthered by the academic world to

fill a knowledge gap.

1.6 Scope Of The Study

The study was carried out on private security companies in Kenya who are members of

KSIA, and have their head office in Nairobi. Focus was placed on studying security

companies that have used Mergers and Acquisition in Kenya. The two companies that meet

the criteria are G4S and KK Security.

The performance of merger and acquisition companies in developing countries especially in

Kenya is not well documented. There has been an increase in the use of mergers and

acquisitions to increase the market share. The study aimed to cover the performance

knowledge gap.

The research area of mergers and acquisitions in general is wide. Looking at Mergers and

Acquisitions, one can look at them from various functional disciplines i.e. finance,

accounting, management and marketing. This study focuses on the reasons why the private

security industry in Kenya chooses mergers or acquisitions as a growth strategy in Kenya. It

also looks at the success factors of mergers and acquisition in the private security industry in

Kenya.

The limitation is that the study is mainly based on secondary data. The study was confined to

only private security firms in Kenya. The study was limited to two corporate firms out of 29

firms registered by KSIA’s, the two firms have undergone mergers and acquisitions in the

last 10 years.

13

1.7 Definition Of Terms

1.7.1 Merger

According to Strategic Direction (2011), mergers typically occur when companies join forces

to create a new organization, which, because of complementary skills and expertise, will be a

stronger and more competitive outfit. According to Sherman (2011), a merger typically refers

to two companies joining (usually through the exchange of shares) as peers to become one.

Mergers usually involve full combination of two previously separate organizations into a

third new entity (Marks and Mirvis, 1998).

Merger implies a mutually agreed decision for joint ownership between organizations

(Johnson, Scholes, and Whittington, 2008). Mergers create a new organization out of two or

more organizations of more or less equal stature, pooling all resources (Strategic Direction,

2005).

1.7.2 Acquisitions

Acquisition is the purchase of one organization for incorporation into the new parent firm

(Marks and Mirvis, 1998). According to Sherman (2011), an acquisition typically has one

company, the buyer that purchases the assets or shares of another, the seller, with the form of

payment being cash, the securities of the buyer, or other assets that are of value to the seller.

Acquisition is where an organization takes ownership of another organization (Johnson,

Scholes, and Whittington, 2008). Acquisitions add a small firm onto the existing structure of

a larger organization. Deals tend to be based on market prices and can be risky, and usually

aim to increase sales, cut costs or enter new markets (Strategic Direction, 2005).

1.7.3 Horizontal M&A’s

This is a merger or acquisition of two companies in the same industry with similar products

or brands combine (Du˜ng Anh Vu˜ and Hanby, 2009).

1.7.4 Security Industry

Security can be improved through the provision of specialized services, such as cash and

valuables transport, as well as material means, such as large intelligence databases or

personal protective equipment. These goods and services can contribute to reduce the

14

vulnerability of society to terrorism and organized crime and mitigate the consequences of an

attack. The collection of economic agents that produce these goods and services is what is

known as the security industry (Marti, 2011).

1.7.5 Cross-Border M&A’s

Cross-border mergers and acquisitions take place when a firm follows the strategic objective

of expanding operations to foreign markets through a range of possible entry vehicles,

including de novo entry over acquisitions and mergers (Amoateng, 2006).

1.7.6 Entry Strategies

The continuing global upsurge in merger, acquisition, joint venture and other forms of

collaborative activity reflects the changing social, economic, technological and market

environments in which organizations now have to operate and respond (Cartwright and

Cooper, 1996).

1.7.7 Globalization

Globalization of markets refers to the merging of historical distinct and separate national

market into one huge global marketplace, while globalization of production refers to the

tendency among firms to source goods and services from different locations around the globe

to take advantage of national differences in the cost and quality factors of production (Hill,

2001).

1.7.8 Hubris

Hubris comes from a Greek methodology, considering a man who is extremely confident,

presumptuous, overly ambitions, and lacks in humility. Hubris applies to a merger, when

extremely confident managers are overly optimistic about their abilities to extract the benefits

anticipated from a merger, and consequently pay too large premium for Target Company.

(Anandalingam and Lucas, 2004).

1.8 Chapter Summary

The purpose of this study is to analyze the factors that affect the success of mergers and

acquisitions in Kenya. The focus of the study will be top 5 Kenyan organizations that have

gone through mergers and acquisition. The study will also concentrate on the mistakes that

take place before mergers and acquisitions will occur.

15

Chapter 2 dealt with literature review aims to show the researches done out there on topics of

mergers and acquisitions. It also the factors that affect the success of M&A, factors that lead

to the success of M&A and how to evaluate the signs of failure in an M&A. Chapter three

dealt with research methodology that will help the researcher in collecting and analyzing data

in respect to the research questions highlighted in the first chapter. Chapter four consists of

the results and findings of the study. This is the correlation analysis of the questionnaire. It

also included graphical representation of the findings and the analysis of the data. Chapter

five includes the discussion, summary and recommendations of the study. It analyses the

findings and compares with the literature review to come up with the summary and

recommendations derived from the study. There are also recommendations for and any future

studies on mergers and acquisition.

16

CHAPTER TWO

2.0 LITERATURE REVIEW

2.1 Introduction

The term mergers and acquisition has been used interchangeably but they are different.

Mergers occur when two companies join to form one while acquisition occurs when one

organization buys another organization and controls it. The aim for business is to grow and

achieve a profit, to evolve from a simple idea to a multimillion making venture. The growth

in business aims to develop opportunities ahead of competition, these helps in making profit.

Growth measured by an increase in revenue, profits, or assets. Growth is achievable by

buying other companies thus combining resources. Even with the need for growth,

organizations that look inward for growth through innovation still supplement their growth

by look towards mergers and acquisitions. Merger and acquisitions are one of the strategies

that an organization can apply to achieve growth.

2.2 Reasons Why Private Security Firms Use Acquisition as a Growth Strategy

Growth of an organization comes from increased revenue, reduced expenses that result to

higher profits. Increased revenue is within the company's control and can be achieved by

sales and market expansion. Growing by acquisition aims to take advantage of combined

synergy that can be better financing terms, instant new market share, having an upper hand

on the competition to increased resources. According to Halibozek & Kovacich (2005)

growth through acquisition, us a swift process compared with developing growth from

within.

Growth by acquisition is not restricted to companies offering homogenous products it also

occurs in companies offering complimentary products, or companies that supply or distribute

the acquiring company products. According to Unoki (2013) Coca-Cola viewed the

acquisition of Columbia as an opportunity to diversify its business portfolio as well as create

new sources of value through synergies obtained by combining different products and

businesses.

17

KK Security in 2009 buyout of Knight Support that gave it a presence in the fire-fighting

business (Business Daily, 2012). The sale was not of a security related services, but a fire

service that gave KK security the opening to the fire fighting services. It would have been

more expensive to set up a fire fighting business from scratch this way they could take

advantage of the already invested in resources. Nestlé’s business expanded in size and scope

through a series of acquisitions of US firms; Libby, the fruit juices company in late 1971;

Stouffer’s frozen foods in 1973; Carnation in 1985 (Jones, 2005).

For companies to grow they will need to do something different to achieve a new result.

They need to acquire existing business that will bring new technology or improve market

share. According to Strategic Direction (2005), Cisco Systems Inc, the networking giant is

known for its acquisition-led growth strategy, having taken over 36 smaller firms in ten

years. The acquisitions allow companies to penetrate into new markets that otherwise they

would not be able to enter. Other reason can be to follow clients. That is, when clients are

internationalizing suppliers may have to supply them materials in foreign countries. In

addition, companies can adopt a follower strategy, that is, follow the leader in the market.

The saturation of the local market can help to make the decision of going to other markets

(Martínez, 2004).

In some cases, the M&A involves unlikely mixtures like combining a company with excess

cash but few growth opportunities with a company boosting of high return projects but cash

hindrances. Usually it happens when big corporations buy small companies and when

companies are in different stages of their cycle, that is, one is focused on mature segments

and the other is immersed in a growth segment (Martínez, 2004).

2.2.1 Acquisition Creates Value

The aim of any business is to make a profit. Value creation occurs where the returns on the

investment exceed the return required (Bruner, 2004). A firm makes a profit if the price can

charge for its output is greater than its costs of producing that output, to do this; the firm

must produce a product that is valued by consumers (Hill, 2001). Firms can increase their

profits in two ways, by adding value to a product so consumers are willing to pay more for it

and by lowering the cost of value creation (Hill, 2001).

18

Firm value will increase by increasing market share, sales, and by reducing the operation

costs. Acquisition offer new opportunities to enhance the company’s competitive advantage,

operational efficiency, and financial performance, thereby increasing shareholder value

(Sudarsanam, 2003). An acquisition may also enable the firm to discover radically new paths

of resource combinations and thus open up new growth opportunities for the firm that are

different from those previously pursued (Davidsson and Wiklund, 2013).

Value creation is best illustrated using Potter’s value chain. A value chain represents the

breakdown of the value of the total output (sales revenue) into its component profit

(Sudarsanam, 2003). The Value chain helps to understand the behavior of cost.

Acquisitions are utilized by acquiring companies to gain monetary value from the acquired

companies. When one company buys the total assets of the other company, it does as it sees

fit with the assets to gain value to the acquiring company. According to Halibozek and

Kovacich (2005), an acquiring company may break up the company it purchases into

different business units or product lines and sell some or all of them. Causes of the breakup

may be that the company needs an immediate cash infusion and selling a business unit may

add cash to the company treasury, a method of eliminating a competitor (Halibozek and

Kovacich, 2005).

In some cases, the company will acquire another forming a symbiotic relationship where

each party bringing something to the table. Many small high-tech businesses need capital to

grow, and more-established firms need these start-ups to grow their top-line, hence the record

number of acquisitions in high-tech and other growth fields (Marks and Mirvis, 1998). Cost

savings are likely to be especially large when one company acquires another from the same

industry in the same country. SBC Communications realized substantial cost savings when it

acquired Pacific Telesis (Eccles, Lanes, and Wilson, 2001).

Even though few acquisitions produce the desired success, the market seems strong. Some of

the acquisitions transactions do also create significant returns for the acquiring firm and thus

confirm that acquisitions can be a profitable strategy for both the firms and its shareholders

(Hitt, Harrison, and Ireland, 2001). The cumulative spending on Cyber Security deals since

2008 totals nearly $22 billion, an average of over $6 billion in each year. Acquirers have

19

been from a range of sectors including Technology, IT services, Aerospace & Defense as

well as financial investors. With the acquisitions, the Cyber Security market was expected to

experience strong growth. Defense contractors have targeted acquisitions that provide access

to new customers primarily government agencies e.g. CIA, FBI, GCHQ, MI5/6, with new

capabilities and access to scarce security-cleared personnel (PWC, 2011).

Acquisitions have been used in organizations as a means to various strategic decisions from

defending an already existing company, making the company stronger by increasing

capacities or a forecast of a future opportunity that the company foresees. Protective value

and enhancing value are gained by defending existing business and building the existing

competitive position. Value sought by building capacities can be used in innovative ways in

markets that do not yet exist (CSBS, 1998). Sweat value describes the additional value

“squeezed out” of acquired companies by imposing strict financial and operational controls

(CSBS, 1998).

Before the acquisition there is, need to set targets to be achieved which help the

organization evaluate the success of the acquisition. During Unilever’s $26 billion

acquisition of Bestfoods in 2000, senior management understood that there was value

to be saved by setting a tight agenda to ensure the delivery of the targeted synergies

(Chanmugam, Shill, Mann, Ficery, and Pursche, 2005). Value derived from acquisitions

is evident in the U.S. acquirers of private firms or subsidiaries of publicly traded firms who

often realize positive excess returns of 1.5 to 2.6 percent (DePamphilis, 2011). Value created

has to be more than or equal to the forecasted value

Synergy motive is based on economic growth that results by merging the resources of the

two companies. This is the value creation and the aim is to increase the value of the firm

(Berkovitch and Narayanan, 1993). Synergy motive for an acquisition suggest that these

transactions take place in the anticipation of economic gain, which result from the acquisition

of the resources of both firms. The gain occurs to the acquirer firm shareholders.

2.2.2 Access To New Channels

The need to improve the chances of business success causes companies to look into

acquisition for survival. According to Gaughan (2007), companies that make a product but

20

do not have direct access to consumers need to develop channels to ensure that, their product

reaches the ultimate consumer in a profitable manner. Locking in dependable distribution

channels can be critical to a firm’s success.

According to Sherman, (2010) Acquisitions offer an ability to plug a weakness in the

organization. By extending product portfolio or strengthening the existing portfolio, an

acquisition can open up new market, customers, geographical regions or even distribution

channels. Disney in 2009 acquired Marvel, which gave it access to new contact channels and

product development (Sherman, 2010). When Mattel, the toy maker, acquired The Learning

Company, an interactive software maker, its aim was to extend its brands into software

products and reach older children who were no longer interested in Mattel's core brands such

as Barbie dolls. In addition, Mattel's corporate strategy intent was to evolve through

acquisition from a traditional toy company to a global children's products company.

(Gopinath, 2003) Mattel used the knowledge from the new company to revitalize its existing

business while at the same time having a common distribution system (Gopinath, 2003), they

increased their distribution channel and new markets in this acquisition.

New channels can be gained from a company expands its market share; this in turn improves

sales and grows the revenue. EPS Security in the USA, is one of the national's major

residential and business fire-and-burglary security firms, they acquired Grand Rapids-based

Eagle Security. The acquisition was for 1,000 Eagle Security accounts only. Half the

accounts were residential the rest are business accounts that will represent about 80% of

Annual revenue (Daly, 2012). This increased the market channel of EPS Security, improving

their standing in the industry and creating instant growth in customer acquisition.

Acquisitions provide the immediate access to the target market, including business network

and relationships, suppliers, distributors, and customers. Therefore, G4S made a conscious

decision to use acquisition as a means of growth (Chang and Rosenzweig, 2001; Simmonds,

1990). The merger of Group 4 Falck and Securicor in the year 2004 in Kenya created G4S

(G4S PLC, 2012). According to G4S annual report, acquisitions continue to be an important

part of the strategy, particularly in developing markets where they could improve either our

market share or where an acquisition can act as a catalyst to drive outsourcing opportunities.

21

Organizations set aside money in their budget that is solely geared to acquisitions. G4S set

budget each year dedicated to acquisition is £200m, they believe there are substantial growth

opportunities in these markets and they are targeting 50% of their revenues to come from

developing markets by 2019 (G4S PLC, 2012). The theory of growth of the firm suggests

that acquisitions enable firms to achieve a rapid speed of expansion (Hennart and Park,

1993).

An acquisition company may choose to keep the entire company it purchased and integrate it

into itself, creating a larger company from two smaller companies (Halibozek and Kovacich,

2005). The aim would be to capitalize on the capabilities of both companies as they are

shaped into a single new company.

2.2.3 Research, Development And Innovation

Due to the rapid technological change, innovation has becoming increasingly important in

organizations today. There is need for novel solutions and more advanced product in the

market. Acquisitions of major Swedish manufacturing groups by foreign owners have led to

increased investment in R&D in Sweden (Strandell, 2008). The acquisitions have shared the

innovative R&D and sharing technological advances to promote growth.

Acquisitions have been looked as an attempt by large organizations to grow by gaining

innovation from the companies they buy. Smaller organizations engage in R&D with the

hopes of acquisition by the large organizations. To extend its networking offerings, Cisco has

purchased 16 computer-networking companies and five computer security companies since

1999 (Phillips & Zhdanov, 2012). This illustrates that organization have grown via

acquisitions that have been geared to innovation, the motivation to innovate and carry our

R&D activities. The acquisition only occurs if the innovation has been successful.

Innovation can be in marketing i.e. to implement a new marketing process that changes the

products design; organizational changing the way the company works thus increasing

performance. According to Gaughan (2007) Johnson & Johnson between the periods 1995–

2005, the company engineered over 50 acquisitions as part of its growth through acquisitions

strategy. Rather than internally try to be on the forefront of every major area of innovation,

Johnson & Johnson, a $55 billion company, has sought to pursue those companies who had

22

developed successful products. They grew by acquiring companies that had innovative and

successful products.

Acquisition of a company can achieve growth. According to Phillips & Zhdanov (2012) with

the need to capture a greater fraction of the acquisition surplus, the small firm will tend to

invest in R&D to increase the odds of successful innovation and being acquired by the larger

firm.

The main point in the positive outcomes of acquisitions on innovation is the information

correlation among the acquiring and acquired company and, the ability to amalgamate the

information into the acquiring company. Typically, the acquirer pays a large premium for the

goodwill or brand equity of the acquired firm and the challenge then is not only to preserve

the existing equity under the new ownership but, ideally, to expand and enhance it (Lambkin

and Muzellec, 2008).

Acquiring technologies can also be a defensive weapon to keep important new technologies

out of the hands of competitors. In 2006, eBay acquired Skype Technologies, the Internet

phone provider, for $3.1 billion in cash, stock, and performance payments, hoping that the

move would boost trading on its online auction site and limit competitors’ access to the new

technology. By September 2009, eBay had to admit that it had been unable to realize the

benefits of owning Skype and was selling the business to a private investor group for $2.75

billion (DePamphilis, 2011).

The capacity to carry out successful R&D can be increased by acquisitions. By acquiring a

unique technology a company will grow in revenue and market share, this is preferred to

building the technology from scratch. Abbott’s $3.7 billion purchase of Piramal Healthcare

Abbot laboratories is US based drug manufacturer has acquired a domestic pharmaceutical

company Piramal Healthcare so as emerge as leaders in the generic drug market in India. One

of the benefits is that post acquisition both companies have benefitted in terms of huge

returns and increased sales of the pharmaceutical products in the global and the domestic

market alike. These have been primarily due to the amalgamation of the drug manufacturing

potential of Piramal and the ability of Abbott market effectively the products internationally

(Christopher and Arishma, 2013).

23

2.3 Reasons Why Private Security Firms Use Mergers as A Growth Strategy

Mergers are the most efficient method to add a new product line, enter a new market, or

increase distribution scope. A merger is a union of two companies. Together they

complement each other with each other’s inadequacy being reduced by the other’s capacity.

Neither company has an advantage after the merger, as both companies combine their people,

assets, and capabilities to form new entity. In mergers, each company seizes to exist and

instead forms a new entity. The 1999 combination of Daimler-Benz and Chrysler to form

DaimlerChrysler is an example of a consolidation (DePamphilis, 2011).

Mergers can take on two general forms: horizontal mergers, in which companies combine

with related companies and vertical mergers, in which companies of unrelated businesses

combine (Cheng, 2012). A merger is an important growth option. Merged enterprises are said

to gain from economies of scale, benefit from cash flow savings, procure new customer base

and eliminate business rivalry (Kasipillai, 2003).

Mergers have proven to be an important and more and more popular means of accomplishing

commercial diversity and growth. A merger strategy can be based on value-maximizing

motives, such as exploiting economies of scale and scope, or increasing profits through

geographic and product diversification. (Lambkin and Muzellec, 2008).

Reasons for mergers vary, as stated by Hisrich (2013), he talked about three factors that

include economics of scale, taxation and combined complementary resource. A firm buys

another in its line of business to get more market power, to acquire access to a new product

line, or even to bring in new employees. A merger with different kind of company can be

favored as a way of reducing risk (Anandalingam and Lucas Jr, 2004).

2.3.1 Economic Of Scale

Economic of scale can occur in any department in the organization. Although there are key

departments that benefit the organization than others especially in production, and sales,

since these increases the organizations revenue. According to Hisrich (2013), Economic of

scale occurs in production, coordination, and administration; sharing central services like

office management and accounting, financial control, and upper-level management.

24

Economics of scale increase operating, financial, and management efficiency, thereby

resulting in lower costs, fewer employees and better earnings.

Costs in organizations are split into fixed and variable costs. Fixed costs are present despite

production while variable costs depend on other variables to increase or decrease. Mergers

between two companies’ results in the new organization reducing its costs, by cutting fixed

cost that will come from reducing duplicate departments, staff and also operations. The aim

of any company is to reduce cost, increase revenue and in turn achieve huge profits. This in

turn will reduce the cost to the company and improve the profits margins. Hackett (1996)

notes that cost reduction can also occur through the rationalization of key clinical support,

such as pathology and radiology, services linked to investment in technology. In certain

activities where major economies were associated with the ways emergency workloads could

be organized and delivered across existing hospital sites and more effective scheduling of

elective workloads (Hackett, 1996).

Economies of scale exist when costs tend to increase on a less than proportionate rate from

the increase in output. One way of accomplishing this is to spread the axed costs over a larger

volume of output. When a merger has taken place, economies are supposed to be derived

from the sharing of services like management, accounting, research and development

(Evripidou, 2012). In 1994, the merger between Radisson diamonds Cruises and seven seas

cruises enabled the combined cruises to offer an extended product line in the form of more

ships, beds, and itineraries while lowering per-bed costs (Gaughan, 2007).

Many entrepreneurs will merge with other firms to ensure a source of supply for key

ingredients, to obtain a new technology, or to keep the other firm’s product from being a

competitive edge (Hisrich, 2013). It’s cheaper to merge with a company already possessing a

new technology instead of trying to replicate the technology. A merger can allow learning

from each other’s experience in the industry or even in technological advances. According to

Cento (2009), in 2004, KLM and Air France created a merger called Air France-KLM; the

merger benefited the consumer by offering superior services. They used their customer

knowledge to offer better services, which in turn brought new clients. . “After integrating its