mergers & acquisitions … state tax planning, traps and recent developments · ·...

TRANSCRIPT

26th Annual

Tuesday & Wednesday, January 24‐25, 2017 Hya Regency Columbus, Columbus, Ohio

Oh

io T

ax

Workshop L

Mergers & Acquisitions … State Tax Planning, Traps and Recent Developments

Tuesday, January 24, 2017 3:00 p.m. to 4:00 p.m.

Biographical Information

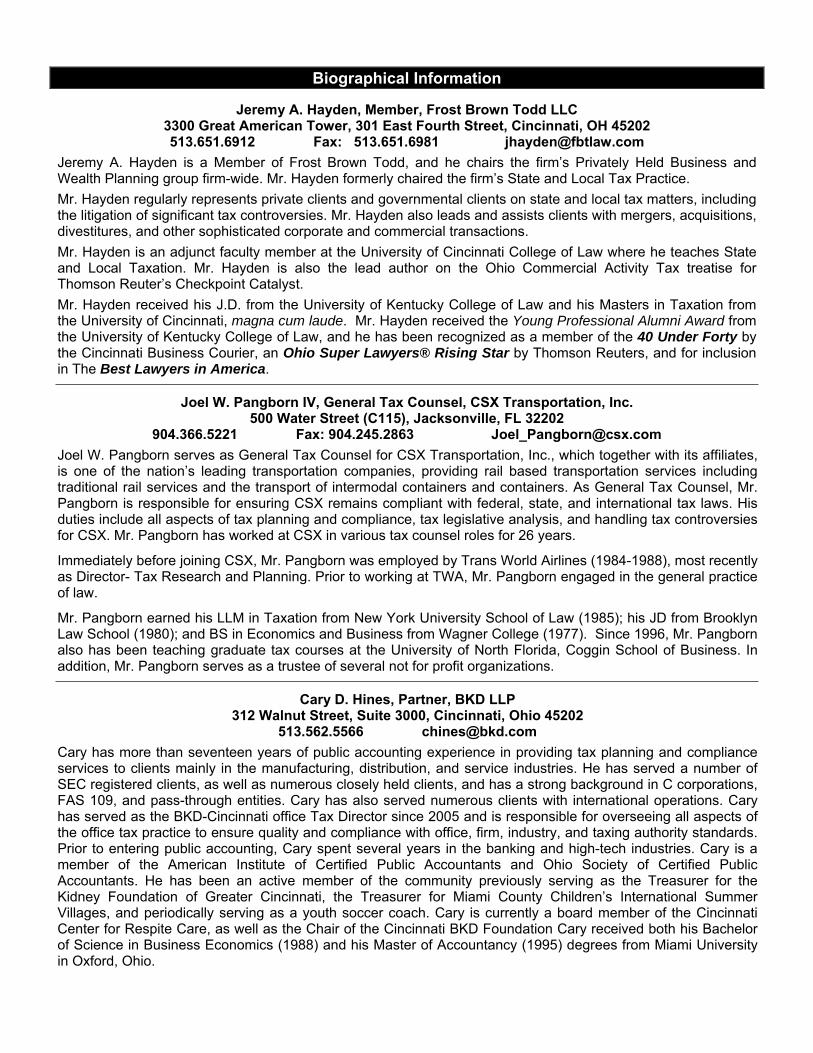

Jeremy A. Hayden, Member, Frost Brown Todd LLC 3300 Great American Tower, 301 East Fourth Street, Cincinnati, OH 45202 513.651.6912 Fax: 513.651.6981 [email protected]

Jeremy A. Hayden is a Member of Frost Brown Todd, and he chairs the firm’s Privately Held Business and Wealth Planning group firm-wide. Mr. Hayden formerly chaired the firm’s State and Local Tax Practice.

Mr. Hayden regularly represents private clients and governmental clients on state and local tax matters, including the litigation of significant tax controversies. Mr. Hayden also leads and assists clients with mergers, acquisitions, divestitures, and other sophisticated corporate and commercial transactions.

Mr. Hayden is an adjunct faculty member at the University of Cincinnati College of Law where he teaches State and Local Taxation. Mr. Hayden is also the lead author on the Ohio Commercial Activity Tax treatise for Thomson Reuter’s Checkpoint Catalyst.

Mr. Hayden received his J.D. from the University of Kentucky College of Law and his Masters in Taxation from the University of Cincinnati, magna cum laude. Mr. Hayden received the Young Professional Alumni Award from the University of Kentucky College of Law, and he has been recognized as a member of the 40 Under Forty by the Cincinnati Business Courier, an Ohio Super Lawyers® Rising Star by Thomson Reuters, and for inclusion in The Best Lawyers in America.

Joel W. Pangborn IV, General Tax Counsel, CSX Transportation, Inc. 500 Water Street (C115), Jacksonville, FL 32202

904.366.5221 Fax: 904.245.2863 [email protected]

Joel W. Pangborn serves as General Tax Counsel for CSX Transportation, Inc., which together with its affiliates, is one of the nation’s leading transportation companies, providing rail based transportation services including traditional rail services and the transport of intermodal containers and containers. As General Tax Counsel, Mr. Pangborn is responsible for ensuring CSX remains compliant with federal, state, and international tax laws. His duties include all aspects of tax planning and compliance, tax legislative analysis, and handling tax controversies for CSX. Mr. Pangborn has worked at CSX in various tax counsel roles for 26 years.

Immediately before joining CSX, Mr. Pangborn was employed by Trans World Airlines (1984-1988), most recently as Director- Tax Research and Planning. Prior to working at TWA, Mr. Pangborn engaged in the general practice of law.

Mr. Pangborn earned his LLM in Taxation from New York University School of Law (1985); his JD from Brooklyn Law School (1980); and BS in Economics and Business from Wagner College (1977). Since 1996, Mr. Pangborn also has been teaching graduate tax courses at the University of North Florida, Coggin School of Business. In addition, Mr. Pangborn serves as a trustee of several not for profit organizations.

Cary D. Hines, Partner, BKD LLP 312 Walnut Street, Suite 3000, Cincinnati, Ohio 45202

513.562.5566 [email protected]

Cary has more than seventeen years of public accounting experience in providing tax planning and compliance services to clients mainly in the manufacturing, distribution, and service industries. He has served a number of SEC registered clients, as well as numerous closely held clients, and has a strong background in C corporations, FAS 109, and pass-through entities. Cary has also served numerous clients with international operations. Cary has served as the BKD-Cincinnati office Tax Director since 2005 and is responsible for overseeing all aspects of the office tax practice to ensure quality and compliance with office, firm, industry, and taxing authority standards. Prior to entering public accounting, Cary spent several years in the banking and high-tech industries. Cary is a member of the American Institute of Certified Public Accountants and Ohio Society of Certified Public Accountants. He has been an active member of the community previously serving as the Treasurer for the Kidney Foundation of Greater Cincinnati, the Treasurer for Miami County Children’s International Summer Villages, and periodically serving as a youth soccer coach. Cary is currently a board member of the Cincinnati Center for Respite Care, as well as the Chair of the Cincinnati BKD Foundation Cary received both his Bachelor of Science in Business Economics (1988) and his Master of Accountancy (1995) degrees from Miami University in Oxford, Ohio.

Mergers and AcquisitionsState Tax Aspects

PANELISTS:

Jeremy A. Hayden Frost Brown Todd LLC Cary Hines BKD, LLP Joel W. Pangborn IV CSX Transportation, Inc.

Ohio Tax Conference – January 24, 2017

1

Presentation Overview

I. Business / Nonbusiness IncomeII. Successor LiabilityIII. Due DiligenceIV. Agreement TermsV. Compliance

2

I. Business / Nonbusiness IncomeA. Business Income is Apportioned

1. Normal apportionment methods – such as UDITPA property, payrolland sales factors

2. Strong presumption in favor of business income

3. Applicable only to assets that are part of the taxpayer’s unitarybusinesses (functional integration, centralized management, andeconomies of scale)

a. Be careful: passive assets have been found to serve operationalpurpose rather than investment purpose.

B. Nonbusiness Income is Allocated1. Based on nature of property

a. Real property – situs of propertyb. Tangible Personal Property – situs of property unless taxpayer is

not taxable in state, then to taxpayer’s commercial domicilec. Intangible Property – state of taxpayer’s commercial domicile

3

C. Tests Based on UDITPA definition of business income:

1. Transactional – Gain is business income and apportionable ifthe taxpayer regularly engages in transaction producing the gain.

a. Whether sale was part of the taxpayer’s principal businessactivity

b. Whether sales of similar property were common, even if notthe taxpayer’s normal business activity

c. Frequency of salesd. Whether sales proceeds are distributed in liquidation and not

reinvested in the businesse. Whether the sale was prompted by extraordinary

circumstancesf. Size of the transaction

4

I. Business / Nonbusiness Income

C. Tests Based on UDITPA definition of business income:

2. Functional – Gain is business income if the acquisition,management, and disposition of the property constitutes anintegral part of the corporation’s regular trade or businessoperations.

a. Is this separate test applicable? Depends on the State.i. Argument against functional test is that the word “and”

before the word “disposition” indicates that disposition(and not just use) of the property must be an integralpart of the taxpayer’s business

b. In response, some states have changed the “and” to an “or”c. Potential exception for liquidation of businessd. In addition to asset transactions, has been held applicable to

sale of a subsidiary’s stock and stock transactions in which a338(h)(10) election is made.

5

I. Business / Nonbusiness Income

D. Some States have repealed UDITPA definition in favor of broad Business Income definitions

1. All income that can be apportioned, within constitutional bounds

2. Only income not derived from the conduct of a trade or business is nonbusiness income

E. Lack of Uniformity can result in double taxation

1. Business Income in one State and nonbusiness income in another State

2. Similarly, taxpayer may not be required to use consistent treatment in every State

6

I. Business / Nonbusiness Income

F. Ohio’s Determination of Business/Nonbusiness Income

ORC 5747.01 (General Rule) provides in relevant part:

(B) "Business income" means income, including gain or loss, arising fromtransactions, activities, and sources in the regular course of a trade or businessand includes income, gain, or loss from real property, tangible property, andintangible property if the acquisition, rental, management, and disposition of theproperty constitute integral parts of the regular course of a trade or businessoperation. "Business income" includes income, including gain or loss, from apartial or complete liquidation of a business, including, but not limited to, gain orloss from the sale or other disposition of goodwill.

(C) "Nonbusiness income" means all income other than business income andmay include, but is not limited to, compensation, rents and royalties from real ortangible personal property, capital gains, interest, dividends and distributions,patent or copyright royalties, or lottery winnings, prizes, and awards.

7

I. Business / Nonbusiness Income

F. Ohio’s Determination of Business/Nonbusiness IncomeORC 5747.212 (Special Rule) “Apportioning gain recognized by nonresident equity investor selling an investment in a closely-held business” provides in relevant part: “Section 5747.212 entity" is any qualifying person if, on at least one

day of the three-year period ending on the last day of thetaxpayer's taxable year, any of the following apply:

(a) The qualifying person is a pass-through entity;

(b) Five or fewer persons directly or indirectly own all the equityinterests, with voting rights, of the qualifying person; or

(c) One person directly or indirectly owns at least fifty per cent ofthe qualifying person's equity interests with voting rights.

A "qualifying person" is any person other than an individual, estate, ortrust. 8

I. Business / Nonbusiness Income

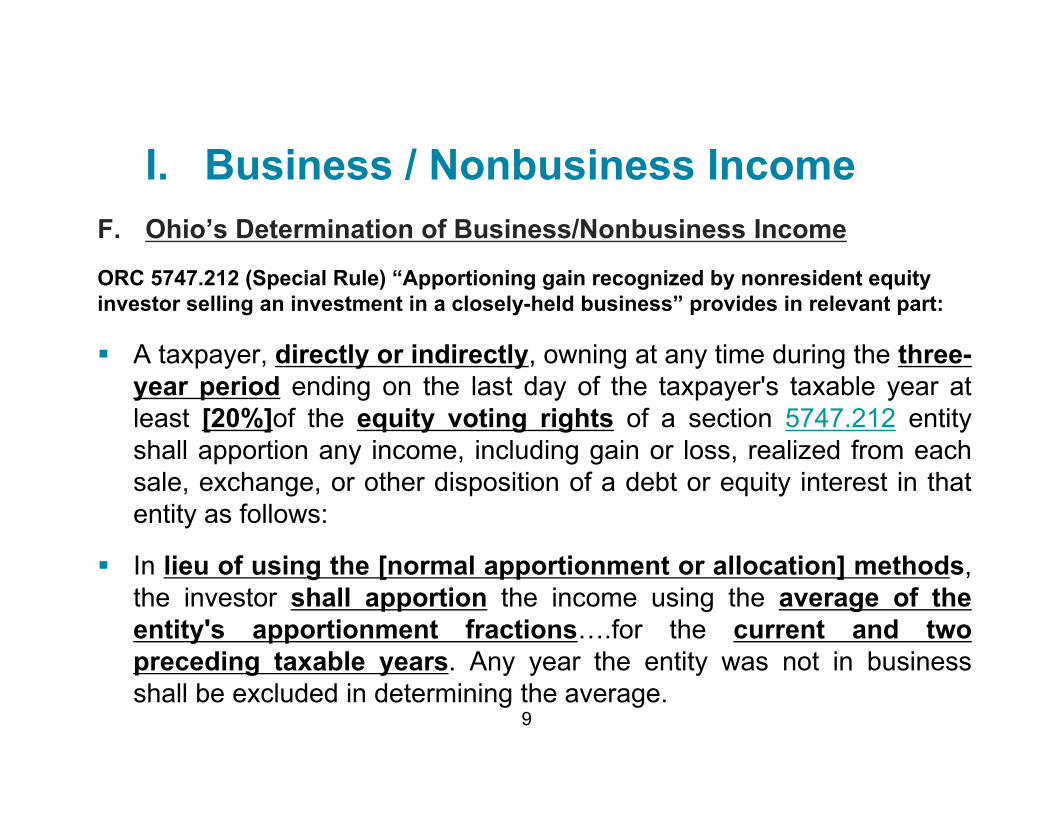

F. Ohio’s Determination of Business/Nonbusiness IncomeORC 5747.212 (Special Rule) “Apportioning gain recognized by nonresident equity investor selling an investment in a closely-held business” provides in relevant part:

A taxpayer, directly or indirectly, owning at any time during the three-year period ending on the last day of the taxpayer's taxable year atleast [20%]of the equity voting rights of a section 5747.212 entityshall apportion any income, including gain or loss, realized from eachsale, exchange, or other disposition of a debt or equity interest in thatentity as follows:

In lieu of using the [normal apportionment or allocation] methods,the investor shall apportion the income using the average of theentity's apportionment fractions….for the current and twopreceding taxable years. Any year the entity was not in businessshall be excluded in determining the average.

9

I. Business / Nonbusiness Income

G. Ohio’s Treatment of Business Income

1. Small Business Investor Income Deduction.

a. HB 64i. Passed in 2015 to allow for 75% deduction of the first $250k for tax

year 2015 and 100% deduction of the first $250k for tax year 2016 and thereafter.

ii. Upon initial enactment, it was unclear whether additional 25% up to $250k was subject to flat 3% rate or graduated rates.

iii. Legislative intent was for the graduated rates to apply.b. SB 208

i. Tax correction bill to clarify that the remaining 25% will be taxed at thegraduated tax rates and 3% flat rate on income greater than $250k.

ii. Signed into law by Governor Kasich on November 15, 2015.

10

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

1. Corrigan v. Testa, Case No. 2014-1836, 2016-Ohio-2805(Ohio Supreme Court May 4, 2016).

a. In 2000, Connecticut-domiciled private equity investor,acquired a nearly 80% ownership stake in MansfieldPlumbing business.

b. Mansfield conducted business in all 50 states.c. Undisputed that Ohio could tax Corrigan’s distributive share

for income earned by Mansfield in Ohio.d. Sole question was capital gain taxation on sale of ownership

interest.e. Reported losses from the business until it was sold to

Colombian firm in 2004 for $27 million capital gain.

11

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

1. Corrigan v. Testa (cont’d)

f. Corrigan was not “active” in the day-to-day activities of thebusiness.

g. However, he was active for purposes of the passive activityloss rules.i. Footnote stated that Corrigan used the losses from

Mansfield in prior years to offset income in other states.h. Corrigan spent time in Ohio “for board meetings and

management presentations regarding operations, labor,finance, strategic positioning and other matters important tothe goal of growing Mansfield’s market share.”

i. Corrigan testified that that involvement was “easily ahundred hours.”

j. He provided “stewardship” rather than active management.

12

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

1. Corrigan v. Testa (cont’d)

k. Taxpayer challenged the constitutionality of specialapportionment rules under R.C. 5747.212 via refund claimfor tax assessed on capital gain.

l. Absent special statute, capital gain would be allocated toConnecticut.

m. Court ruled that Due Process Clause of the United StatesConstitution, as applied to Corrigan, prohibits Ohio fromlevying an income tax on the capital gain from his sale of anownership interest in a pass-through entity.

n. His activities did not amount to a unitary business withMansfield and thus Mansfield’s activities could not beattributed to Corrigan on the sale of his equity.

13

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

1. Corrigan v. Testa (cont’d)

o. The court declined to adopt “investee apportionment”(Mansfield) like NY as an alternative to investorapportionment (Corrigan), since US Supreme Court haddeclined to address the issue in MeadWestvaco.

p. Commerce Clause Challenge ruled moot.q. Court left open whether Asset Sale in the liquidation of a

business could have the same effect (substantial equivalent)as the sale of corporate ownership and thus be subject tothe same constitutional challenge.

r. Hellerstein and others have criticized the court’s ruling inCorrigan.

14

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

2. Ohio Information Release 2016-01a. Department’s post-Corrigan guidance focuses on fact that

Corrigan’s challenge was an as-applied challenge and that“neither Mr. Corrigan nor the sale of the asset had a taxablelink to Ohio”

b. Not clear if “taxable link” used by the Department is intendedto be broader/more aggressive than Court-required unitarybusiness relationship.i. Corrigan spent significant time in the business (was not

passive) and he attended board meetings and otherfunctions in Ohio.

15

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

2. Ohio Information Release 2016-01 (cont’d)i. Consider whether anything changes if:

• taxpayer is employed by the business or manages itsday-to-day activities rather than its “stewardship”?

• business only conducts business in Ohio?c. Does not address asset sales.d. States that equity sales that are not subject to R.C. 5747.212

are considered nonbusiness income.

16

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

3. T. Ryan Legg Irrevocable Trust v. Testa, Case No. 2015-917,2016-Ohio-8418 (Ohio Dec. 28, 2016)

a. Irrevocable Delaware Trust established by Ohio co-founderof TQL (Ohio S corporation).

b. Commissioner assessed Ohio income tax for Trust’s capitalgain on sale of TQL stock, and apportioned income pursuantto special rule under R.C. 5747.212.

c. Commissioner’s position - gain is qualifying trust amount.d. BTA affirmed and also held that income was business

income due to partial liquidation.

17

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

3. T. Ryan Legg Irrevocable Trust v. Testa (cont’d)

e. Ohio Supreme Court affirmed in part.

• Affirmed that income was qualifying trust amount.

• “Qualifying trust amount” includes capital gainsrealized “from the sale, exchange, or other dispositionof equity or ownership interests in, or debt obligationsof, a qualifying investee to the extent included in thetrust’s Ohio taxable income” provided two conditionsare met.

18

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

3. T. Ryan Legg Irrevocable Trust v. Testa (cont’d)

• First, the requirements of R.C. 5747.011 must besatisfied—most notably, the requirement that thetrust’s ownership interest be at least 5 percent of thetotal outstanding ownership interests “at any timeduring the ten-year period ending on the last day ofthe trust’s taxable year in which the sale, exchange,or other disposition occurs.”

• The Trust did not dispute the 5% requirement wasmet.

19

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

3. T. Ryan Legg Irrevocable Trust v. Testa (cont’d)

• Second, “book value of the qualifying investee’sphysical assets in this state and everywhere, as ofthe last day of the qualifying investee’s fiscal orcalendar year ending immediately prior to the date onwhich the trust recognizes the gain or loss” must be“available to the trust.”

20

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

3. T. Ryan Legg Irrevocable Trust v. Testa (cont’d)

• Trust disputed that the book value of TQL’s assetswere available. Ohio Supreme Court held that theTrust had such access/availability to book value percorporate shareholder rights statute and per use ofshared accountant.

• Further, the trust would need the access to prepare itstax returns due to property factor calculation which isbased in part on investee’s assets (TQL).

• Legislature must have thought the record availabilityrequirement would normally limit the tax on qualifyingtrust amounts to instances when the trust owned aninterest in a closely-held business.

21

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

3. T. Ryan Legg Irrevocable Trust v. Testa (cont’d)

• Business/non-business income distinction was irrelevant.• Statutory definitions of modified business/non-business

income expressly excluded income that is qualifying trustamount.

f. Court said Commissioner, however, erred in apportioninggain based on special rule under R.C. 5747.212.• Instead, statute required special apportionment formula

using Ohio share of investee’s (TQL’s) physical assets as ofthe last day of the year ending immediately prior to therecognition of the qualifying trust amount.

22

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

3. T. Ryan Legg Irrevocable Trust v. Testa (cont’d)

g. In analyzing constitutional arguments, court first ruled thatBTA erred in finding that Trust was a resident trust.

• Commissioner had held trust was nonresident in his FD.Taxpayer did not challenge Commissioner’s priorfinding. Thus, BTA should have deferred toCommissioner’s finding.

• Residency depends on whether the assets weretransferred into a trust by an Ohio resident and whethera “qualifying beneficiary” is an Ohio resident.

23

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

3. T. Ryan Legg Irrevocable Trust v. Testa (cont’d)• Legg was an Ohio resident, but he was not a qualifying

beneficiary.• A qualifying beneficiary has to be a potential current

beneficiary under IRC 1361(e)(2), which providesthat such term does not include a person who firsthad the right to a distribution within the 1 yearpredating an ownership sale.

• Trust was structured to require accumulation ofincome during this period, and Commissioner’sargument on discretionary principal distributionswas not timely (raised for the first time at oralargument).

24

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

3. T. Ryan Legg Irrevocable Trust v. Testa (cont’d)• Due Process rights were not violated based on trust’s

and transaction’s connections with the state.• Rational basis review standard.• Acknowledged similarities with Corrigan (i.e.,

nonresident taxpayers selling ownershipinterests).

• Court held, however, that a “more comprehensivereview” revealed more differences thansimilarities.

• Legg was the co-founder of the company andactivity involved in the day-to-day operations ofthe business.

25

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

3. T. Ryan Legg Irrevocable Trust v. Testa (cont’d)

• Equal protection argument based on sale of C-corpshares being treated differently (no tax) also failed.

• Court found that legislature had the right to make thisdistinction.

• Tax-law classifications are afforded deference as theydo not involve fundamental rights or “suspect lines.”

• Further, there are many differences between C corpsand pass-throughs. For example, pass-throughs aremore likely to be closely-held.

• Thus, they are not similarly situated.

26

I. Business / Nonbusiness Income

H. Recent Ohio Cases and Developments on Business Income

3. T. Ryan Legg Irrevocable Trust v. Testa (cont’d)

h. Strong dissent by Lanzinger encourages overrulingCorrigan.

• Lanzinger said that laws should be presumed to beconstitutional, and Corrigan creates a burden on thestate to justify imposing tax and then a court mustanalyze each new case for “fine points of distinction.”

• Lanzinger believes that trust’s status as an investor inOhio assets or an Ohio business justifies tax and thisconnection is enough to warrant taxation.

27

I. Business / Nonbusiness Income

I. Planning Opportunities and Considerations after Corrigan

1. Prior Sales Subject to R.C. 5747.212

a. Apply for refund claim if within prior 4 years.

b. Refund may not be worthwhile if taxpayer is domiciled in astate with the same or higher tax as Ohio.

c. Residents are generally taxed on their worldwide incomesubject to credit for taxes paid to other states.

28

I. Business / Nonbusiness Income

I. Planning Opportunities and Considerations after Corrigan

2. Future Salesa. Ohio residents

i. Taxed by Ohio on worldwide income with deduction for taxes paid toother states.

ii. Thus, all things otherwise equal, would be better to structure asasset sale rather than equity sale so that gain is subject to SmallBusiness Investor Income Deduction and flat 3% tax thereafter.

iii. If equity sale and taxpayer was active in the business, then considerargument that Commissioner's position in T. Ryan Legg casecontrols rather than information release.a) Also argue per Ohio Supreme Court’s Due Process analysis:

Corrigan – taxpayer’s unitary position with business maywarrant business income treatment.

Legg - Legg was active in the business and thus incomecould have qualified as business income (distinguishingCorrigan).

29

I. Business / Nonbusiness Income

I. Planning Opportunities and Considerations after Corrigan

2. Future Sales

b. Non-Ohio residentsi. Generally only taxed in Ohio to the extent income is

business income (apportioned in part to Ohio).ii. Thus, all things otherwise equal, would be better to

structure as equity sale rather than asset sale so thatgain is allocated to residency state.a) If 20% or more owner, consider minimizing “links”

to Ohio prior to sale so that Ohio does not try toargue Corrigan does not apply.

b) Per Legg, interests owned by Trusts could betreated differently.

iii. If asset sale, then consider argument left open inCorrigan that asset sale may be economic equivalentof equity sale.

30

I. Business / Nonbusiness Income

II. Successor Liability

A. Buyer’s Point of Emphasis – Determining Exposure for Taxes Prior to Closing

1. Stock/merger vs. asset acquisition

2. Amount of exposure (could be unlimited and includepredecessors’ liabilities)

3. Rights to challenge successor liability vs. merit of taxesowed

4. Types of taxes

31

II. Successor Liability

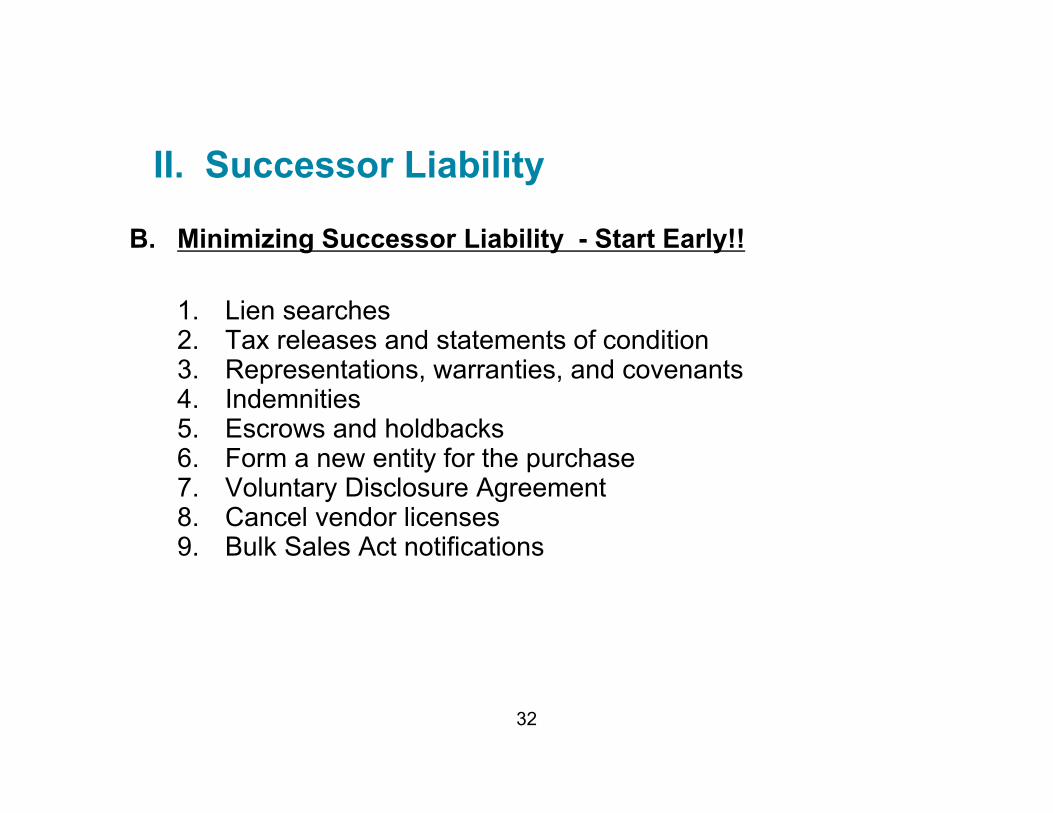

B. Minimizing Successor Liability - Start Early!!

1. Lien searches2. Tax releases and statements of condition3. Representations, warranties, and covenants4. Indemnities5. Escrows and holdbacks6. Form a new entity for the purchase7. Voluntary Disclosure Agreement8. Cancel vendor licenses9. Bulk Sales Act notifications

32

III. Due DiligenceA. Overview

1. Broad – Encompasses all state and local taxesa. Keeping organized - start with due diligence checklistb. Review and analysis of due diligence itemsc. Incorporate into due diligence memod. Sign and close vs. sign then close deal structures

2. Fully understand business(es) involveda. Goods or servicesb. Wholesaler or retailerc. Exempt or governmentd. Industry type

3. Acquisition structurea. Stock or assetb. Taxable or non-taxable

33

III. Due DiligenceB. Tax Returns and Specific Taxes

1. Overviewa. States in which the target is currently filing for all

tax matters and reasons for filing in those jurisdictions

b. How is the target’s business structured, and has it been appropriately reporting based on ownership and operational activities?

c. Open tax years for target including extensions and waivers of SOL

34

III. Due Diligence

2. Income and Franchise Tax Matters

a. Allocation and apportionment figures, whether the target has NOLs, depreciation adjustments, or state-specific adjustmentsi. Specifically determine sourcing of services of target

(cost of performance, customer’s address, market-based)

ii. Determine states in which the target has payroll expenses and real or personal property

iii. Goal is to minimize double taxation and maximize nowhere income

b. States in which the target files a separate return, a combined return, or a consolidated return

35

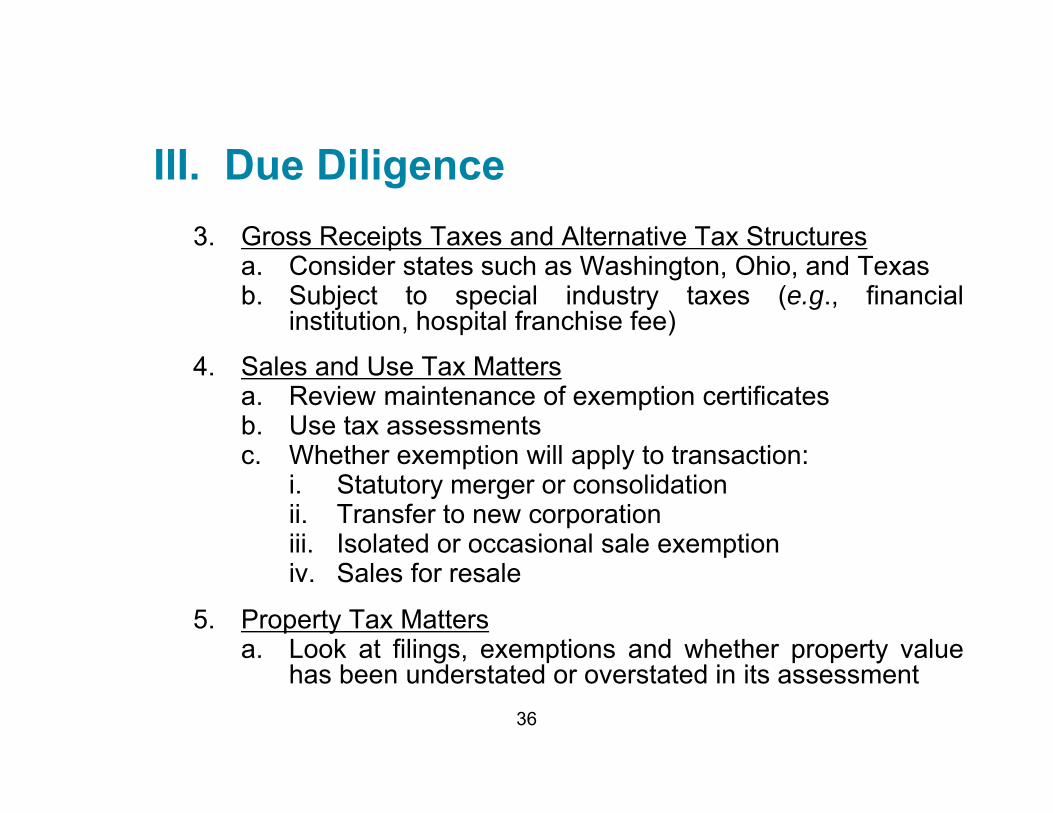

III. Due Diligence3. Gross Receipts Taxes and Alternative Tax Structures

a. Consider states such as Washington, Ohio, and Texasb. Subject to special industry taxes (e.g., financial

institution, hospital franchise fee)

4. Sales and Use Tax Mattersa. Review maintenance of exemption certificatesb. Use tax assessmentsc. Whether exemption will apply to transaction:

i. Statutory merger or consolidationii. Transfer to new corporationiii. Isolated or occasional sale exemptioniv. Sales for resale

5. Property Tax Mattersa. Look at filings, exemptions and whether property value

has been understated or overstated in its assessment36

III. Due Diligence6. Payroll, Unemployment, and Workers Compensation

a. Analyze worker classification issuesb. Review withholding tax filingsc. Review unemployment tax filingsd. Although workers compensation is not a tax matter,

certain aspects often may need to be reviewed by SALTpractitioners

7. Unclaimed Property.a. Often overlooked and exposure can be $$$b. Certain states (such as Delaware) have stepped-up

enforcement

8. Look-Through Rules.a. Some states apply transaction-based taxes (e.g.,

sales/use taxes) to equity sales involving passivecompanies whose assets include real property, boats,planes, motor vehicles, etc.

37

III. Due DiligenceC. Nexus

1. Analyze activities in states:a. Look for gaps in reporting and potential expansion of

required filingsb. Physical presencec. Employees or representatives working on behalf of target

to solicit salesd. Employees or representatives working on behalf of target

for activities beyond soliciting salese. Client locationsf. Any other affiliates, agents, etc. that may establish nexus

for target (e.g., Amazon law)g. States in which target is registered to do businessh. States in which target is registered for sales tax purposes

38

III. Due Diligence

D. Other Matters

1. Pending Audits, Appeals and Refund Claims

2. Incentives• State and local tax incentives applied for, denied or

received

3. Reserves.• Determine reserves for any state and local tax

liabilities

39

IV. Agreement Terms

A. Types of Taxes Addressed

1. Historic• Includes all prior taxes (should be broadly defined)

2. Acquisition• Sales taxes attributable to transaction, incremental

taxes due to 338(h)(10) election, etc.

3. Future• Filing responsibility for straddle periods, etc.

40

B. Representations and Warranties (the guarantees)1. Addresses tax matters arising prior to closing (historic tax

liabilities)2. Seller is verifying that such tax matters are true and correct

(e.g., all tax returns filed and taxes paid regardless of whethershown on a tax return or not, no ongoing audits)

3. Offers buyer further diligence and additional protection as riskshifts to seller via contractual representations and warranties

4. May be subject to qualifiers (e.g., materiality, knowledge)5. Seller should carefully review representations and warranties

and schedule any exceptions6. Address updates to schedules if sign then close transaction7. Incorporate due diligence (e.g., representation on tax attributes

to be acquired)

41

IV. Agreement Terms

C. Covenants1. Types: Negative (e.g., will not extend SOL, settle tax liabilities,

or make any new tax elections without buyer’s consent) oraffirmative (e.g., seller to make all required tax filings)

2. Timing: Pre-closing (if applicable) and post-closing3. Taxes Covered: May cover historic (between time of signing

and closing), acquisition (e.g. buyer’s promise to payincremental taxes associated with 338(h)(10) election), andfuture tax obligations

D. Contingencies, Indemnities, Escrows1. Provide remedies for compliance with representations,

warranties, and covenants2. May overlap with representations and warranties3. Caps, deductibles, timing, and other limitations on indemnities

usually not applicable to tax matters

42

IV. Agreement Terms

E. Other Tax Matters1. Responsibility for tax return filings, including straddle

periods2. Ownership of refunds, NOLs, and other tax attributes3. Special elections (e.g., S corporation, 338(h)(10), etc.)4. Purchase price allocation (timing can be important)5. Withholding provisions – could inadvertently require entire

purchase price to be withheld6. Responsibility for transfer taxes7. Closing of books for income taxes vs. allocation for net

worth taxes

43

IV. Agreement Terms

V. ComplianceA. Equity Transactions

1. Buyera. Nexus b. Structural considerationsc. Combined and consolidated reportingd. Net Operating Lossese. Deductibility of interest (debt placement)f. Management fees

2. Sellera. Gain/(Loss) apportionment (?)

44

V. ComplianceB. Asset Transactions

1. Buyera. Section 338 electionsb. Purchase price allocationc. Nexus

2. Sellera. Purchase price allocationb. Net Operating Loss utilizationc. Gain/(Loss) apportionment

45

V. Compliance

C. Mergers and Reorganizations

1. Most states follow federal treatment for income taxes

2. Same treatment does NOT necessarily apply to sales taxes

46

Questions?Thank you for your time today.

Jeremy A. Hayden, Esq.Frost Brown Todd [email protected]

Cary Hines, CPABKD, [email protected]

Joel W. Pangborn IV, Esq.General Tax CounselCSX Transportation, [email protected]

47