mergers, acquisitions, and restructuring. what is corporate restructuring corporate restructuring...

TRANSCRIPT

MERGERS, ACQUISITIONS, AND RESTRUCTURING

WHAT IS CORPORATE RESTRUCTURING

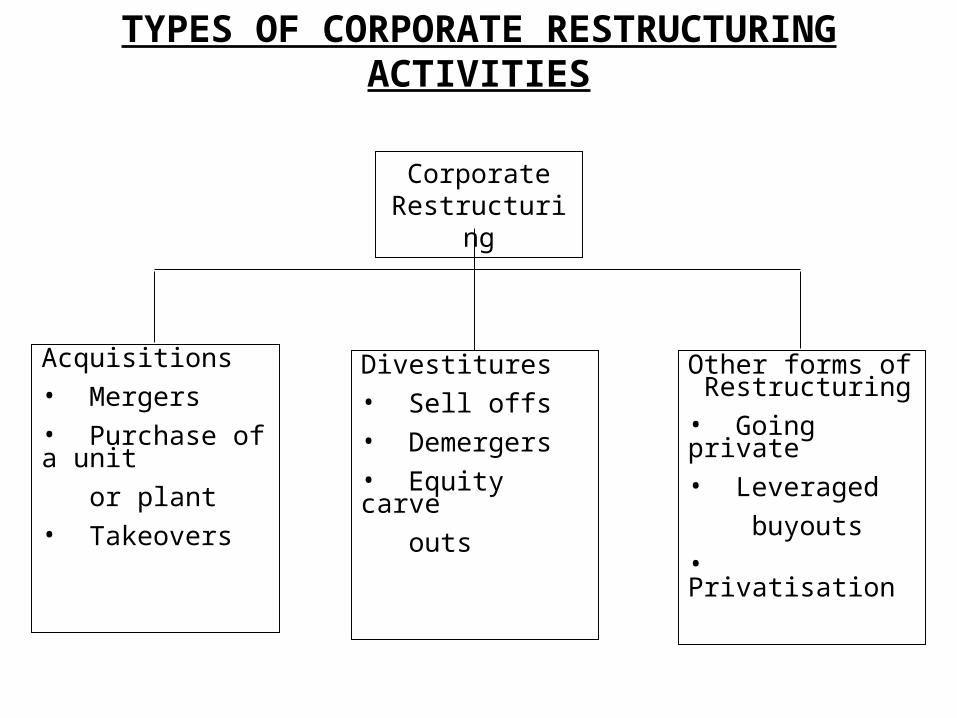

Corporate restructuring refers to a broad array of activities that expand or contract a firm’s operations or substantially modify its financial structure or bring about a significant change in its organisational structure and internal functioning. Inter alia, it includes activities such as mergers, purchases of business units, takeovers, slump sales, demergers, leveraged buyouts, organisational restructuring, and performance improvement initiatives. We will refer to these activities collectively as mergers, acquisitions, and restructuring (a widely used, though not a very accurate, term) or just corporate restructuring. Sacrificing some rigour, these activities may be classified as shown next.

TYPES OF CORPORATE RESTRUCTURING ACTIVITIES

Corporate Restructuring

Divestitures• Sell offs• Demergers• Equity carve

outs

Acquisitions• Mergers• Purchase of a unit

or plant• Takeovers

Other forms of Restructuring• Going private• Leveraged

buyouts• Privatisation

TYPES OF MERGER

Absorption

A + B = A

Consolidation

A + B = C

Horizontal Vertical Conglomerate Cogeneric

REASONS FOR MERGERS

• Strategic benefit• Economies of scale• Economies of scope• Economies of vertical integration• Complementary resources• Tax shields• Utilisation of surplus funds• Managerial effectiveness• Diversification• Lower financing costs• Earnings growth

LEGAL PROCEDURE FOR AMALGAMATION

• Examination of object clauses

• Intimation to stock exchanges• Approval of the draft amalgamation proposal by the respective

boards• Application to the High Court/s.• Despatch of notice to shareholders and creditors• Holding of meetings of shareholders and creditors• Petition to the High Court for confirmation and passing of High

Court orders• Filing the order with the Registrar of Companies• Transfer of assets and liabilities• Issue of shares and debentures

TAX ASPECTS OF AMALGAMATIONS

Tax concessions are granted to the amalgamated company only if the amalgamating company is an Indian company. Following deductions to the extent available to the amalgamating company and remaining unabsorbed or unfulfilled will be available to the amalgamated company:

• Capital expenditure on scientific research

• Expenditure on acquisition of patent right or copy right, know how

• Expenditure for obtaining license to operate

telecommunication services

• Amortisation of preliminary expenses

• Carry forward of losses and unabsorbed depreciation

ACCOUNTING FOR AMALGAMATIONS

According to the Accounting Standard 14 (AS-14) on

Accounting for Amalgamations issued by ICAI, an

amalgamation can be in the nature of either uniting of

interests which is referred to as ‘amalgamation in the

nature of merger’ or ‘acquisition’

CONDITIONS FOR AMALGAMATION

IN THE NATURE OF MERGER

• All assets and liabilities of the transferor transferee

• Shareholders 90%.. equity of the transferor company

become shareholders of the transferee company.

• Consideration is paid in shares

• The business of the transferor company is intended to be

carried on by the transferee company

AN AMALGAMATION .. NOT IN THE NATURE OF MERGER … IS TREATED AS AN ACQUISITION.

ACCOUNTING FOR A MERGER

For a merger, the ‘pooling of interest’ method, is used.

Under the ‘pooling of interest’ method, the assets and

liabilities of the merging companies are aggregated.

Likewise the reserves appearing in the balance sheet of the

transferor company carried forward into the balance sheet

of the transferee company. The difference in capital on

account of the share swap ratio (exchange ratio) is

adjusted in the reserves.

ACCOUNTING FOR AN ACQUISITION

For an acquisition the ‘purchase’ method is used. Under the ‘purchase’ method, the assets and outside liabilities of the transferor company are carried into the books of the transferee company at their fair market values. The difference between the purchase consideration and the net book value of assets over liabilities is treated as ‘goodwill’ that has to be amortised over a period not exceeding five years. Should the purchase consideration be less than the net book value of assets over liabilities, the difference is shown as ‘capital reserve’.

Since there is often an asset write-up as well as some goodwill, the reported profit under the purchase method is lower because of higher depreciation charge as well as amortisation of goodwill.

COST AND BENEFITS OF A MERGER

Benefit = PVAB – (PVA + PVB)

Cost = Cash – PVB

NPV to A = Benefit – Cost

= [(PVAB – (PVA + PVB)] – [Cash – PVB]

= PVAB – PVA – Cash

NPV to B = Cash - PVB

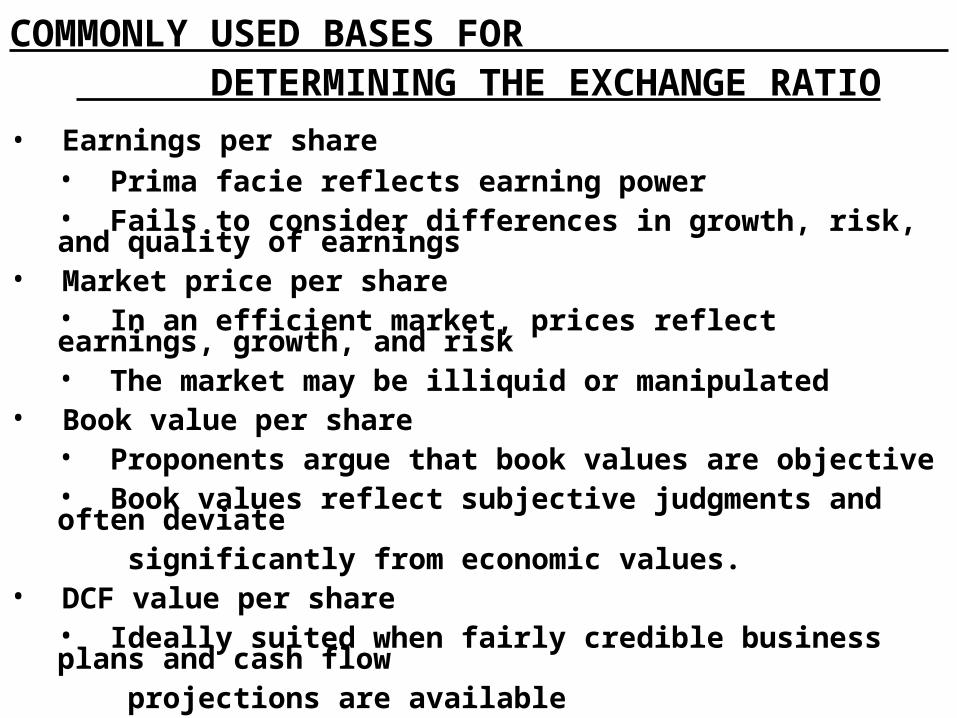

COMMONLY USED BASES FOR DETERMINING THE EXCHANGE RATIO

• Earnings per share• Prima facie reflects earning power• Fails to consider differences in growth, risk, and quality of earnings

• Market price per share• In an efficient market, prices reflect earnings, growth, and risk• The market may be illiquid or manipulated

• Book value per share• Proponents argue that book values are objective• Book values reflect subjective judgments and often deviate significantly from economic values.

• DCF value per share• Ideally suited when fairly credible business plans and cash flow projections are available• It overlooks options embedded in the business

TERMS OF MERGER• If firm 1 acquires firm 2, shares of firm 1 are given in exchange for shares of firm 2.

• Firm 1 would try to keep the exchange ratio as low as possible, whereas firm 2 would seek to keep it as high as possible

• Larson and Gonedes developed a model for exchange rate determination. Their model holds that each firm will ensure that its equivalent price per share will at least be maintained as a sequel to the merger

• In somewhat simpler terms, the following symbols may be used to explain their model. ER = exchange ratio

P = price per shareEPS = earnings per sharePE = price-earnings multipleE = earningsS = number of outstanding equity shares

• In the discussion that follows, the acquiring, acquired, and combined firms will be referred to by subscripts 1, 2, and 12 respectively.

TERMS OF MERGERS

• The maximum exchange ratio acceptable to the shareholders of firm 1 is:

- S1 (E1 + E2) PE12

ER1= +

S2 P1S2

• The minimum exchange ratio acceptable to the shareholders of firm 2 is:

P2 S1

ER2 =

PE12 (E1 + E2) – P2S2

PURCHASE OF A DIVISION/PLANT

With the step-up in corporate restructuring activity, purchase and sale of divisions or plants are becoming commonplace.

The counterpart of purchase is divestiture. If firm A purchases a plant or factory or business division of firm B, from the point of firm B it represents a divestiture. Purchases (and divestitures) are expected to grow in importance in the years to come as firms restructure themselves with greater freedom in the more liberalised industrial environment.

PROCEDURE FOR VALUING

A PURCHASE

1. Define the present value of the free cash flow from the

purchase.

2. Establish the horizon value and discount it to the

present time.

3. Add the present value of free cash flow and horizon

value to get the value of purchase.

VALUE OF SYNERGY

In most acquisitions, there is a potential for synergy which may come in one or more of the following ways:

• Lower operating costs due to economies of scale

• Savings in outlays on R & D, advertising, marketing, and

various shared services

• Higher growth rate because of greater market power of the

combined entity

• Longer growth period from enhanced competitive advantages

• Lower cost of capital due to higher debt capacity

• Better utilisation of tax shelters

Valuing synergy may not be easy because synergy is easy to imagine but difficult to realise.

TAKEOVERS

• A takeover generally involves the acquisition of a certain

block of equity capital of a company which enables the

acquirer to exercise control over the affairs of the

company

• A takeover may be done through the following ways

• Open market purchase

• Negotiated acquisition

• Preferential allotment

REGULATION OF TAKEOVERS

Takeovers may be regarded as a legitimate device in the market for corporate control provided they are regulated by the following principles:

• Transparency of the process

• Protection of the interest of small shareholders

• Realisation of economic gains

• No undue concentration of market power

TAKEOVER DEFENCES IN INDIA

• MAKE PREFERENTIAL ALLOTMENTS

• EFFECT CREEPING ENHANCEMENTS

• SEARCH FOR A WHITE KNIGHT

• SELL THE CROWN JEWELS

• AMALGAMATE GROUP COMPANIES

• RESORT TO BUYBACK OF SHARES

• LOBBY WITH GOVT AND SEBI

BUSINESS ALLIANCES

Business alliances such as joint ventures, strategic alliances, equity partnerships, licensing, franchising alliances, and network alliances have grown significantly. In many situations, well-designed business alliances are viable alternatives to mergers and acquisitions. No wonder they have become commonplace in diverse fields like high-technology, media and entertainment, automobiles, pharmaceuticals, oil exploration, and financial services.

COMMON FORMS OF BUSINESS ALLIANCES

• Joint ventures

• Strategic alliances

• Equity partnership

• Licensing

• Franchising alliance

• Network alliance

RATIONALE FOR BUSINESS ALLIANCES

• Sharing risks and resources

• Access to new markets

• Cost reduction

• Favourable regulatory treatment

• Prelude to acquisition or exit

DIVESTITURES

Mergers, asset purchases, and takeovers lead to expansion in some way or the other. They are based on the principle of synergy which says 2 + 2 = 5! Divestitures, on the other hand, involve some kind of contraction. It is based on the principle of “anergy” which says 5 – 3 = 3!

Among the various methods of divestiture, the more important ones are partial sell-off, demerger (spinoff and split-up), and equity carveout. Note that some scholars define divestitures rather narrowly as partial selloff. We define divestitures more broadly to include partial selloffs, demergers, and so on.

PARTIAL SELL-OFF

A partial selloff, also called slump sale, involves the sale of a business unit or plant of one firm to another. It is the mirror image of a purchase of a business unit or plant. From the seller’s perspective, it is a form of contraction; from the buyer’s point of view it is a form of expansion.

Motives for Sell off

• Raising capital

• Curtailment of losses

• Strategic realignment

• Efficiency gain

DEMERGERS

A demerger results in the transfer by a company of one or more of its undertakings to another company. The company whose undertaking is transferred is called the demerged company and the company (or the companies) to which the undertaking is transferred is referred to as the resulting company.

A demerger may take the form of a spinoff or a split-up. In a spinoff an undertaking or division of a company is spun off into an independent company. After the spinoff, the parent company and the spun off company are separate corporate entities. In a split-up, a company is split up into two or more independent companies. As a sequel, the parent company disappears as a corporate entity and in its place two or more separate companies emerge.

Rationale for Demergers

• Sharper focus• Improved incentives and accountability

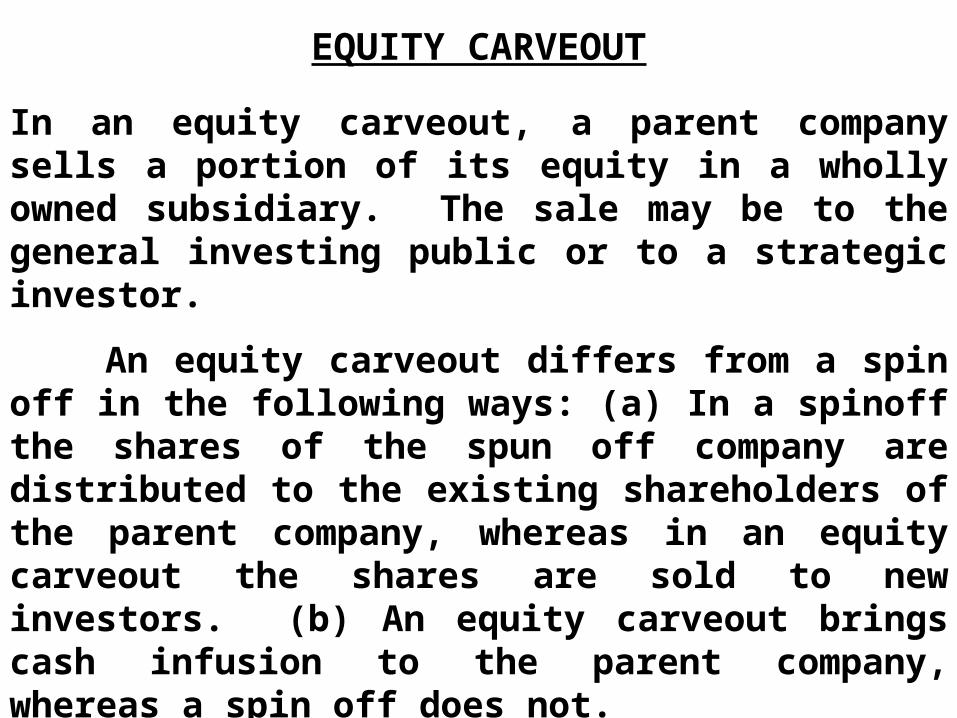

EQUITY CARVEOUT

In an equity carveout, a parent company sells a portion of its equity in a wholly owned subsidiary. The sale may be to the general investing public or to a strategic investor.

An equity carveout differs from a spin off in the following ways: (a) In a spinoff the shares of the spun off company are distributed to the existing shareholders of the parent company, whereas in an equity carveout the shares are sold to new investors. (b) An equity carveout brings cash infusion to the parent company, whereas a spin off does not.

Equity carveouts are undertaken to bring cash to the parent and to induct a strategic investor in a subsidiary.

LEVERAGED BUYOUT

A leveraged buyout involves transfer of ownership consummated mainly with debt. While some leveraged buyouts involve a company in its entirety, most involve a business unit of a company. Often the business unit is bought out by its management and such a transaction is called management buyout (MBO). After the buyout, the company (or the business unit) invariably becomes a private company.

RATIONALE FOR PRIVATISATION

• Improvement in Efficiency

• Autonomy

• Accountability

• Employee pride

• Generation of Resources

• Promotion of Popular Capitalism