memory joggers fa 2015 - tolley.co.uk · 10 loan relationships ... 54 personal service companies...

TRANSCRIPT

Tolley® Exam Training

ATT

PAPER 4Corporate Taxation

MEMORY JOGGERS

FA 2015May and November 2016 Sittings

427

Tolley® Exam Training INTRODUCTION

© Reed Elsevier UK Ltd 2015 I FA 2015

INTRODUCTION

The Memory Joggers contain short bullet point summaries of the tax (and accounting where applicable) topics within ATT Paper 4.

The summaries are split into sections as follows:

• Useful Legislation • Corporation Tax • Other Taxes • Accounting Some wording has been highlighted in grey indicating a change from Finance Act 2014 to Finance Act 2015.

The Examination Paper

The paper will have two parts and a mixture of computational and written questions. There is no question choice.

Part 1 accounts for 40% of the marks and consists of “short form” questions worth between 2 and 4 marks each. There will be between 10 and 20 such questions in a paper.

Part 2 accounts for the remaining 60% of the marks and consists of between 3 and 5 longer questions carrying 10 to 20 marks each.

Law and Ethics for Paper 4

Also examinable in the ATT written tax papers are selected chapters from the text books "Professional Responsibilities and Ethics for Tax Practitioners" (2nd edition) and “Essential Law for Tax Practitioners” (4th edition) as detailed below.

The Law and Ethics text books are only available from the ATT and CIOT directly.

Law and Ethics can be tested either as a small part of a long question or as a short form question.

Examinable Law chapters for Paper 4:

Chapter 5 – only sections 5.1 to 5.10 inclusive Chapter 8 – only sections 8.1 to 8.3 Chapter 9 – all sections Chapter 10 – only section 10.9 Chapter 11 – all sections Chapter 12 – all sections Chapter 13 – only sections 1–6, and 11–12

Tolley® Exam Training INTRODUCTION

© Reed Elsevier UK Ltd 2015 II FA 2015

Chapter 14 – only sections 1–6 and 9–10 Chapter 16 – only sections 1–6 Examinable ethics chapters for all papers:

New clients and engagement letters Client service Conflicts of interest Other client handling issues Charging for services Complaints Ceasing to act Fundamental principles (of Professional Conduct in relation to Taxation) Tax returns Access to data by HMRC and other authorities Irregularities (including errors) Using your Memory Joggers

Your revision phase is all about practising questions. Put away your study manuals and instead practice the questions.

Remember you have your legislation to help and a useful legislation list is included here. However, at first, you may feel you need a little help remembering the key points of a topic to help you attempt the questions. Turn to these Memory Joggers rather than go back to your study manuals.

The Memory Joggers contain summaries of the study manual chapters and useful proformas.

After this introduction, there is a contents list referring to the original chapter from the study manual that the summary relates to. Therefore, if you did need some more detail from your study manuals you know where to look.

As you practise more questions and gain more confidence, you should start to rely on the Memory Joggers less.

Good luck with your studies and should you need to contact us, you can do so in one of the following ways:

• Phone 020 3364 4500 • Email [email protected] • Post a message on our ATT Papers 1-6 student forum on the Online Academy

Tolley® Exam Training INTRODUCTION

© Reed Elsevier UK Ltd 2015 III FA 2015

Please state your examination paper and related manual chapter/question to help us answer technical queries.

Tolley® Exam Training CONTENTS

© Reed Elsevier UK Ltd 2015 V FA 2015

CONTENTS

USEFUL LEGISLATION LISTS

Corporation Tax

Other Taxes

CORPORATION TAX

1 Introduction to Corporation Tax

2 Computation of Corporation Tax

3 Associated Companies

4 Long Periods of Account

5 Corporation Tax Self Assessment (CTSA)

6 Payment of Corporation Tax

7 Interest on Late Paid Tax and Repayments

8 CTSA Penalty Regime

9 Property Income

10 Loan Relationships – Basics

11 Loan Relationships – Connected Companies

12 Relief for Trading Losses

13 Relief for Other Losses

14 Corporate Capital Gains

15 Substantial Shareholding Exemption

16 Intangible Fixed Assets

17 Research and Development Expenditure

18 Companies with Investment Business

19 The Principles of Group Relief

20 Group Relief – Further Aspects

21 Consortium Relief

22 Group Consortium Companies

23 Group Administration

24 Group Capital Gains

Tolley® Exam Training CONTENTS

© Reed Elsevier UK Ltd 2015 VI FA 2015

25 Group Gains – Further Aspects

26 Change in Ownership of a Company

27 Transfer of Trades

28 Sale of Shares v Sale of Assets

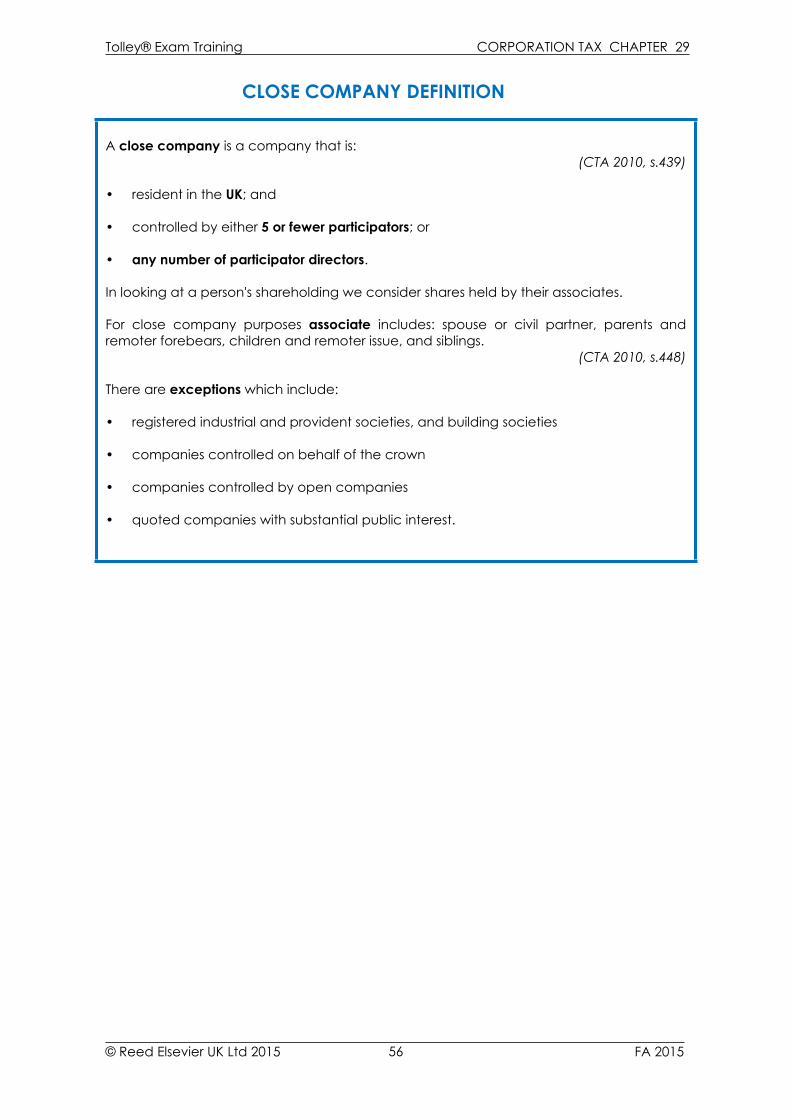

29 Close Company Definition

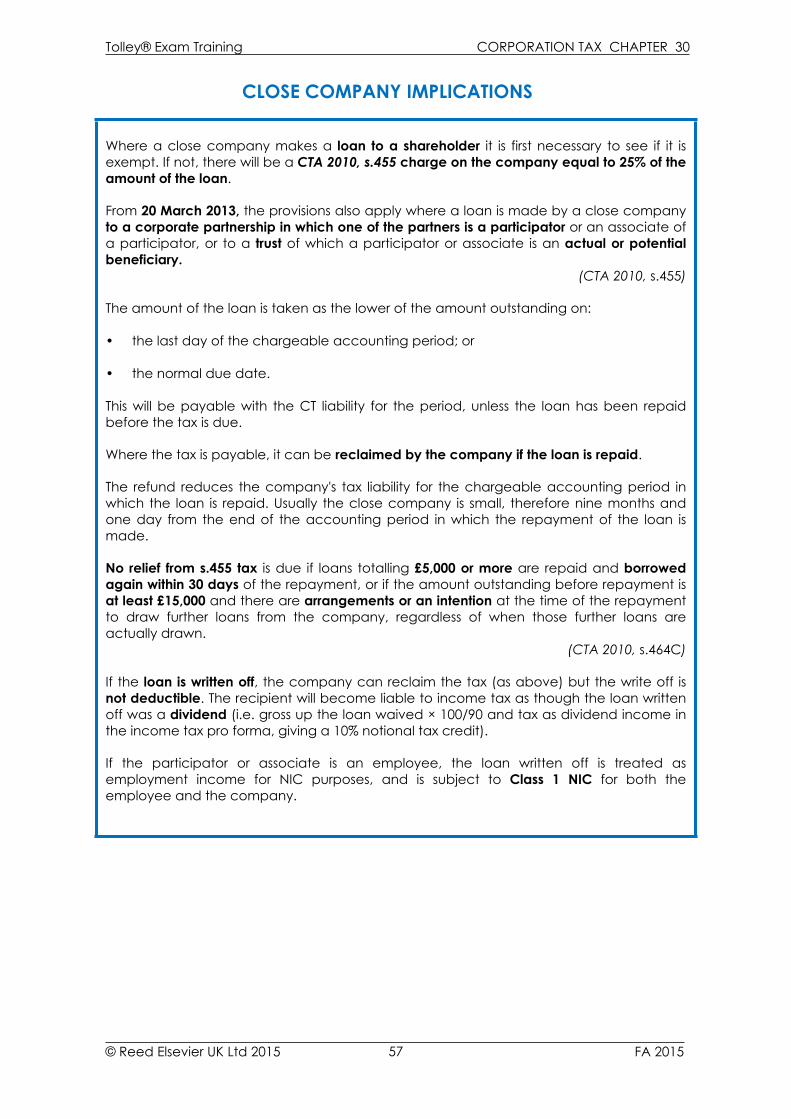

30 Close Company Implications

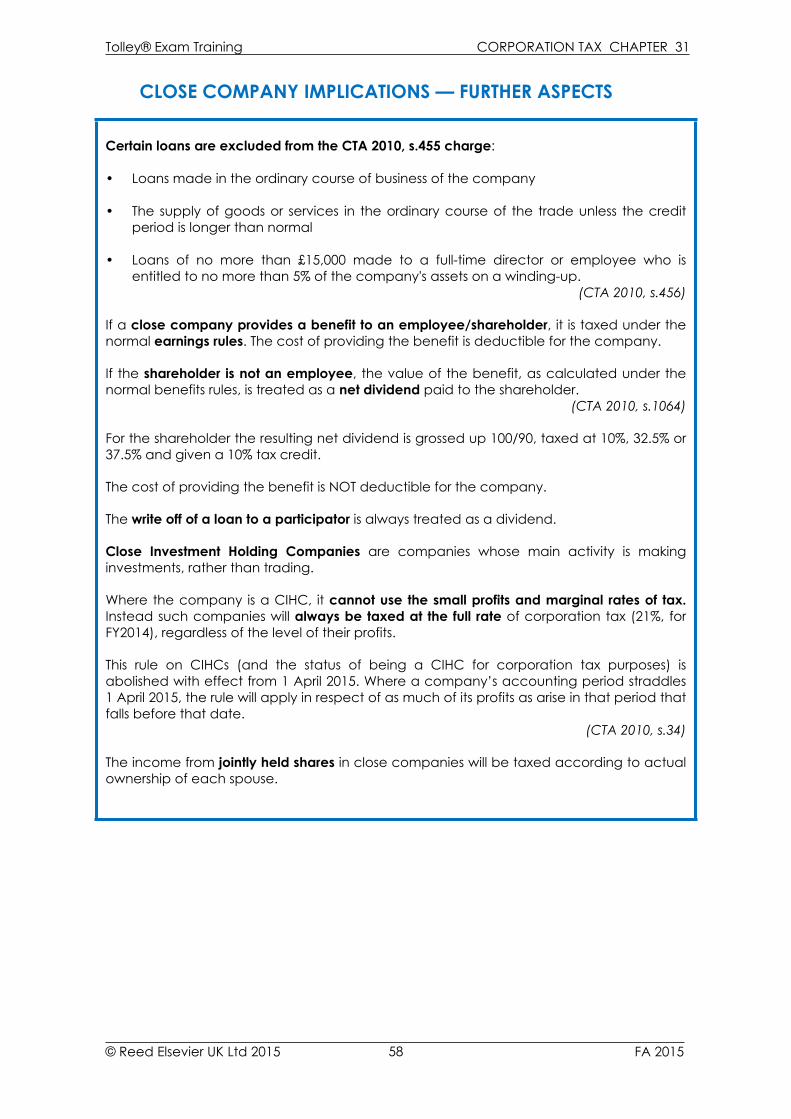

31 Close Company Implications – Further Aspects

32 Accounting for Income Tax

33 Overseas Matters for Companies

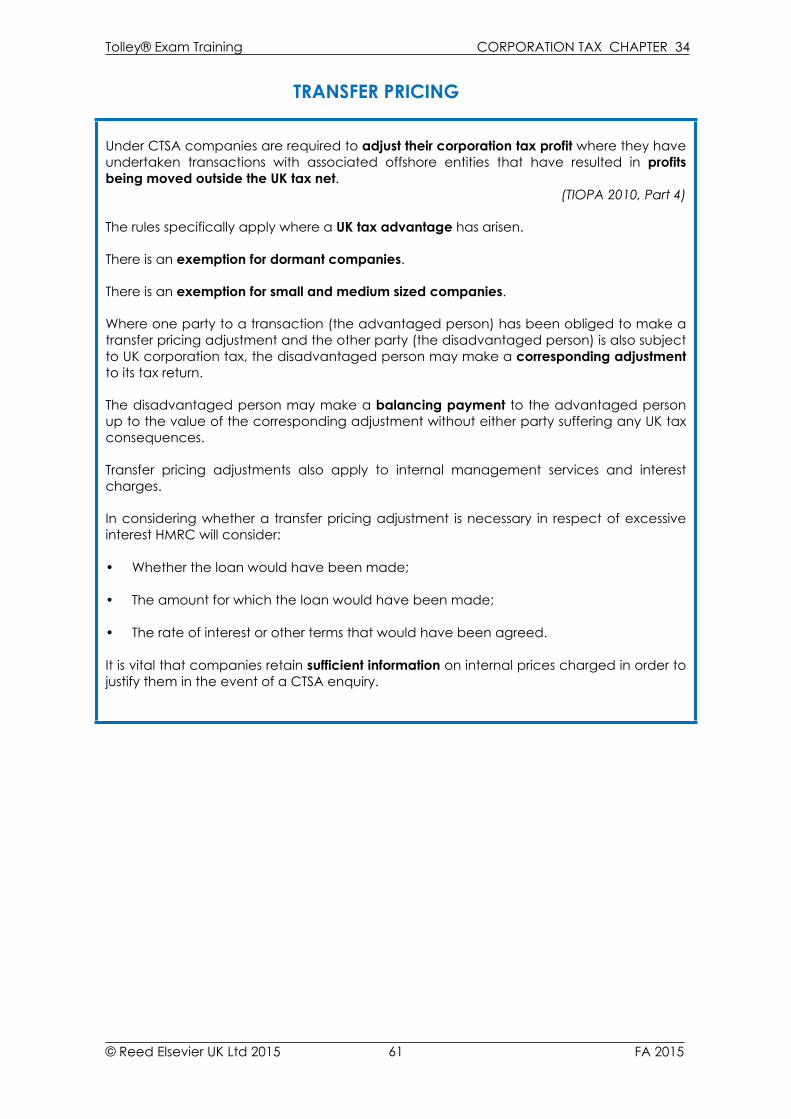

34 Transfer Pricing

35 Purchase of Own Shares

OTHER TAXES

Business Tax

1 Incorporation

2 Disincorporation Relief

3 Limited Liability Partnerships

4 Mixed Partnerships

Personal Income Tax

5 Termination Payments

6 Employed or Self Employed ?

7 Personal Service Companies

Capital Gains Tax

8 Connected Persons

Value Added Tax

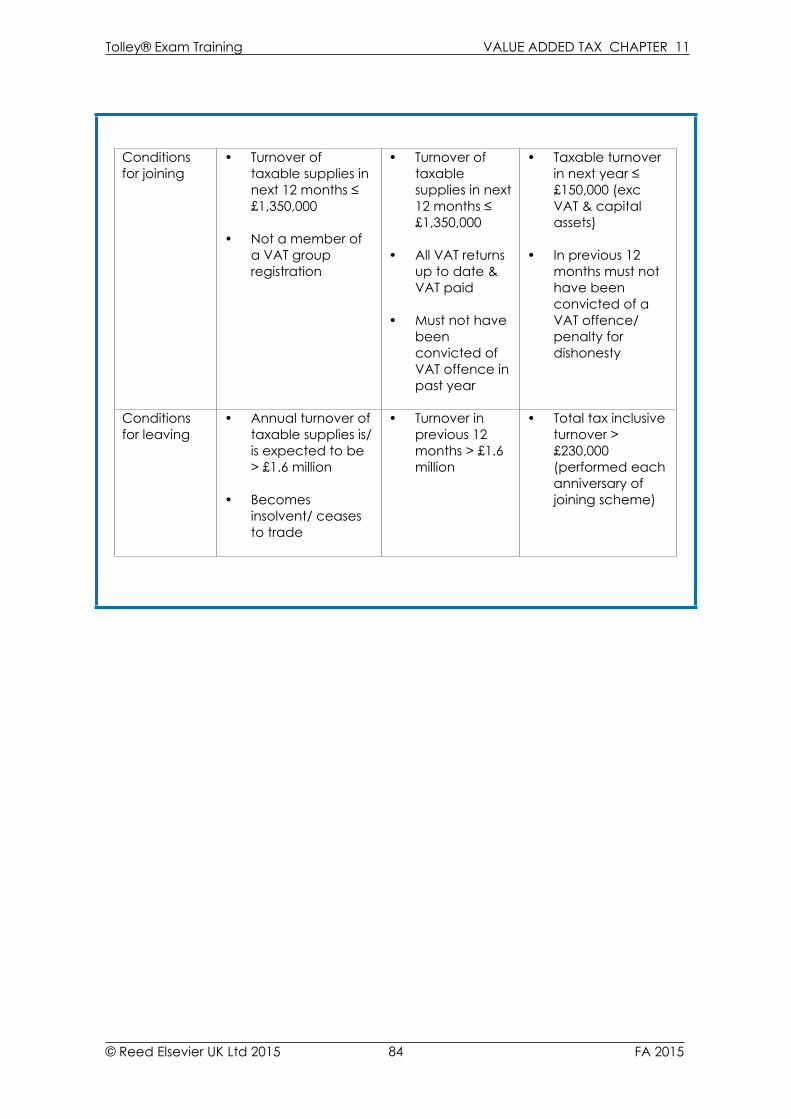

9 Bad Debt Relief

10 The Annual Accounting and Cash Accounting Schemes

11 The Flat-Rate Scheme

Accounting

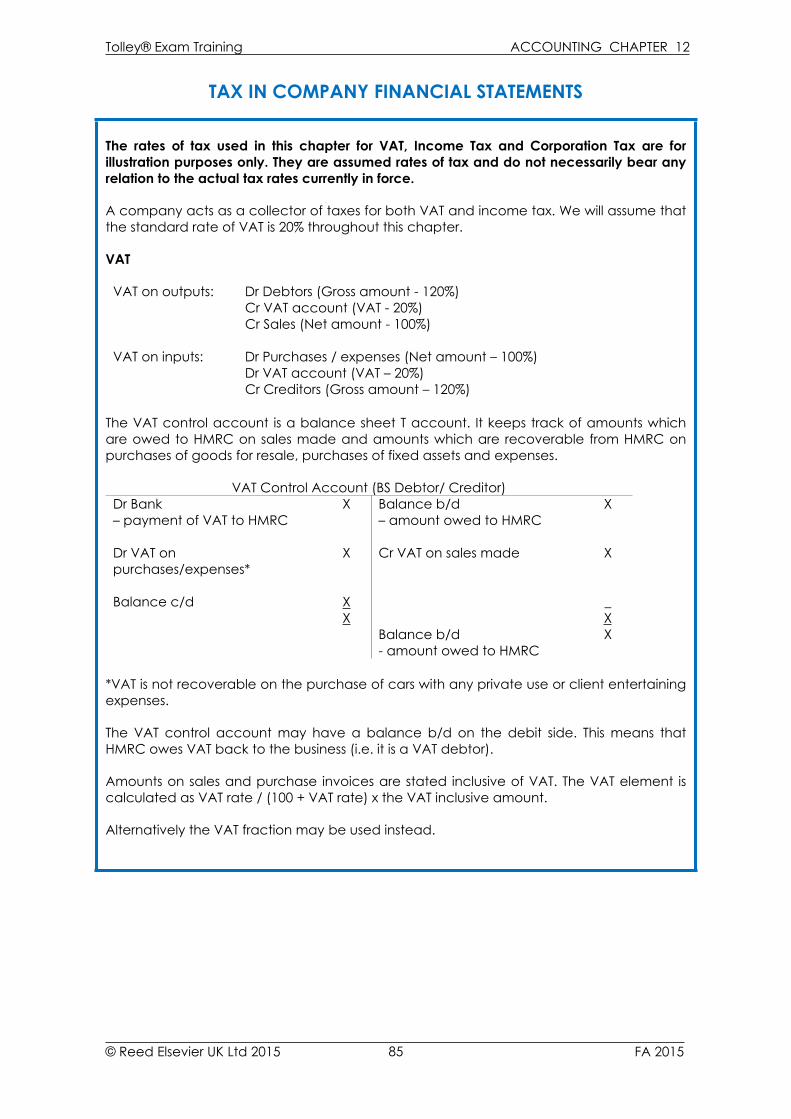

12 Tax in Company Financial Statements

Tolley® Exam Training USEFUL LEGISLATION LIST

© Reed Elsevier UK Ltd 2015 VII FA 2015

USEFUL LEGISLATION LIST

CORPORATION TAX

TCGA 1992152 - 155 Rollover relief170 Gains group definition179 (1, 3, 3A – 3H) Degrouping chargeSch 7AC Paras 3,7,8,9,10,18,19 Substantial shareholding exemption

FA 1998Sch 18 Paras 14–16, 21, 23, 24 CT AdministrationSch 18 Paras 67–75 Group relief

CAA 2001266, 267 Election to transfer P&M at tax wdv

FA 200455 Company notify of chargeability

FA 2007Sch 24 Paras 2, 3, 4, 5, 9, 10, 11, 14 Penalties for incorrect returns

FA 2008Sch 41 Paras 1, 6, 7(1–3) Penalties for late notification

CTA 20099-12 Rules on APs104A, 104M, 104N Research and development

expenditure credits for large companies

457, 458, 461– 463 Non-trading deficits from loan relationships

753 IFA loss relief1039, 1043, 1044, 1052,1054 –1056, 1074, 1123, 1124, 1126, 1140

R&D

FA 2009Sch 55 Paras 3–6 Penalties for late returnsSch 56 Paras 1,4 Penalties for late payments

CTA 201025-27 Associated company determination37 Trading losses current year and carry

back39 Terminal loss relief45(4) Trading losses carry forward relief62 UK property business loss relief66 Overseas property business loss relief131, 151, 152 Group relief definition279F—H Definition of related 51% group

company357A, 357B, 357G Patent box439 Definition of a close company455 Close company implications – loans to

participators518, 528, 530, 531 Real Estate Investment Trusts

Tolley® Exam Training USEFUL LEGISLATION LIST

© Reed Elsevier UK Ltd 2015 VIII FA 2015

673–674 MCINOCOT944 Transfer of trading losses with transfer

of trade948 Succession of CAs in transfer of trade963 Surrender of tax refund within group1033, 1034, 1035, 1036, 1037, 1042, 1062

Company buy back own shares

1122–1123 ’Connected person’ definition

Statutory Instruments:SI 1998/3175 Payment of tax by large companies

(instalments)SI 1999/2975 Simplified group relief arrangementsSI 2011/1784 Substantial commercial

interdependence

Statements of Practice:2/82 Purchase of own shares10/91 Changes allowed that do not give rise

to MCINOCOT

Tolley® Exam Training USEFUL LEGISLATION LIST

© Reed Elsevier UK Ltd 2015 IX FA 2015

OTHER TAXES

BUSINESS TAX

TCGA 1992162, 162A Incorporation relief & election to disapply165 (1 ,2, 4, 7, 8) Gift relief169 H, I, K-N, P Entrepreneur's relief CAA 2001266, 267 Election to transfer P&M at tax wdv

ITTOIA 2005173,175-178 Stock adjustments on cessation of trade850C-E Profits reallocated from corporate to

individual partners863A – C Disguised employment rules for members

of LLPs ITA 200786 Loss relief on incorporation107(1-5), 108(1, 2, 7) Restrictions re loss relief for member of LLP116A Loss relief to individual partners lost809AAZA Transfer of income streams through

partnerships FA 201358–60 Disincorporation relief PERSONAL INCOME TAX

ITEPA 200354 Personal Service Companies deemed

salary calculation401, 403, 413–414 Termination payments NICA 20141,2 National Insurance Contributions

Employment Allowance Miscellaneous V – IR35Misc V Personal Service Companies VALUE ADDED TAX

VATA 1994s.36 Bad debts Statutory Instruments

SI 1995/2518Reg.49 – 54 Annual AccountingReg.55A Flat-Rate SchemeReg.56 – 60 Cash Accounting

Tolley® Exam Training USEFUL LEGISLATION LIST

© Reed Elsevier UK Ltd 2015 X FA 2015

VAT Notices

Notice 731 Cash AccountingNotice 733 Flat-rate Scheme

Tolley® Exam Training CORPORATION TAX CHAPTER 1

© Reed Elsevier UK Ltd 2015 FA 2015

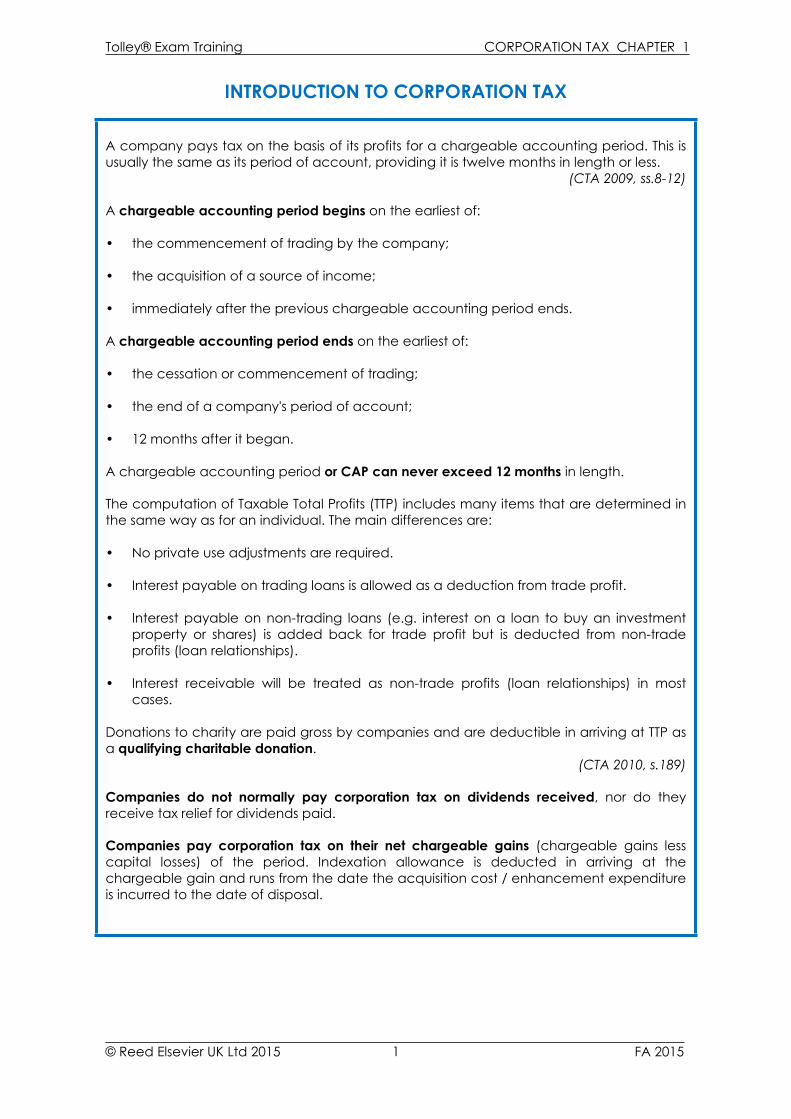

INTRODUCTION TO CORPORATION TAX

A company pays tax on the basis of its profits for a chargeable accounting period. This is usually the same as its period of account, providing it is twelve months in length or less.

(CTA 2009, ss.8-12)

A chargeable accounting period begins on the earliest of:

• the commencement of trading by the company;

• the acquisition of a source of income;

• immediately after the previous chargeable accounting period ends.

A chargeable accounting period ends on the earliest of:

• the cessation or commencement of trading;

• the end of a company's period of account;

• 12 months after it began.

A chargeable accounting period or CAP can never exceed 12 months in length.

The computation of Taxable Total Profits (TTP) includes many items that are determined in the same way as for an individual. The main differences are:

• No private use adjustments are required.

• Interest payable on trading loans is allowed as a deduction from trade profit.

• Interest payable on non-trading loans (e.g. interest on a loan to buy an investment

property or shares) is added back for trade profit but is deducted from non-trade profits (loan relationships).

• Interest receivable will be treated as non-trade profits (loan relationships) in most

cases.

Donations to charity are paid gross by companies and are deductible in arriving at TTP as a qualifying charitable donation.

(CTA 2010, s.189)

Companies do not normally pay corporation tax on dividends received, nor do they receive tax relief for dividends paid.

Companies pay corporation tax on their net chargeable gains (chargeable gains less capital losses) of the period. Indexation allowance is deducted in arriving at the chargeable gain and runs from the date the acquisition cost / enhancement expenditure is incurred to the date of disposal.

1

Tolley® Exam Training CORPORATION TAX CHAPTER 1

© Reed Elsevier UK Ltd 2015 FA 2015

PROFORMA CORPORATION TAX COMPUTATION

Company name

Corporation tax computation for the chargeable accounting period

£Trading IncomeAdjusted profits before capital allowances XLess: Capital allowances (X)Trade profit X

Other IncomeNon-trading profits (loan relationships) XNon-trading gains (IFAs) XMiscellaneous income XUK property business XOverseas property business XNet chargeable gains X

Less: Qualifying charitable donations (X)Taxable Total Profits (TTP) X

TTP × appropriate rate XLess: Marginal relief (not applicable for CAP beginning on/after 1 April 2015) (X)Corporation tax liability X

2

Tolley® Exam Training CORPORATION TAX CHAPTER 1

© Reed Elsevier UK Ltd 2015 FA 2015

REMINDER OF COMMON ADJUSTMENTS TO PROFITS IN CALCULATION OF TRADING INCOME FOR A COMPANY

£Profit before tax per accounts per period of account X

Add back disallowable expenditure:Depreciation of fixed assets(unless finance lease) XCapital expenditure XLosses on disposal of fixed assets XEntertaining (unless staff entertaining) XGifts (unless cost ≤ £50 and are not food/drink/tobacco and bear a clear advert)

X

15% of hire cost of cars with CO2 emissions > 130 g/km XFines and penalties XBribes X

Less income not taxed as trading income:Rental income/ interest income/ dividend income (usually exempt) (X)Profits on disposal of fixed assets (X)Tax adjusted profit before capital allowances X

Less: Capital allowances (calculated for the CAP — NO private use adjustments)

(X)

Trade profit X

The following expenses are allowable in calculating trade profits:

Legal fees re renewal of a short lease

Maximum of 4 × statutory redundancy payments on the cessation of trade

Pension contributions paid in the period

Wages and salaries accrued provided paid ≤ 9 months from period end

3

Tolley® Exam Training CORPORATION TAX CHAPTER 1

© Reed Elsevier UK Ltd 2015 FA 2015

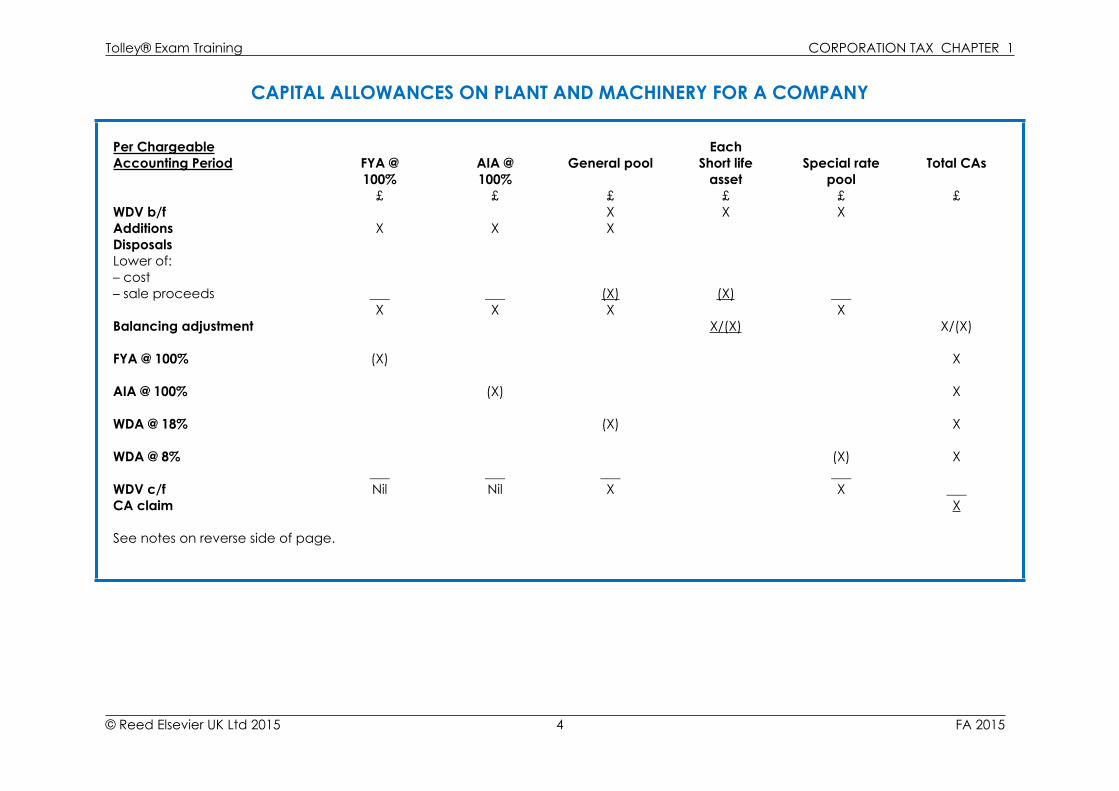

CAPITAL ALLOWANCES ON PLANT AND MACHINERY FOR A COMPANY

Per Chargeable EachAccounting Period FYA @ AIA @ General pool Short life Special rate Total CAs

100% 100% asset pool£ £ £ £ £ £

WDV b/f X X XAdditions X X XDisposalsLower of:– cost– sale proceeds ___ ___ (X) (X) ___

X X X XBalancing adjustment X/(X) X/(X)

FYA @ 100% (X) X

AIA @ 100% (X) X

WDA @ 18% (X) X

WDA @ 8% (X) X___ ___ ___ ___

WDV c/f Nil Nil X X ___CA claim X

See notes on reverse side of page.

4

Tolley® Exam Training CORPORATION TAX CHAPTER 1

© Reed Elsevier UK Ltd 2015 FA 2015

Notes:

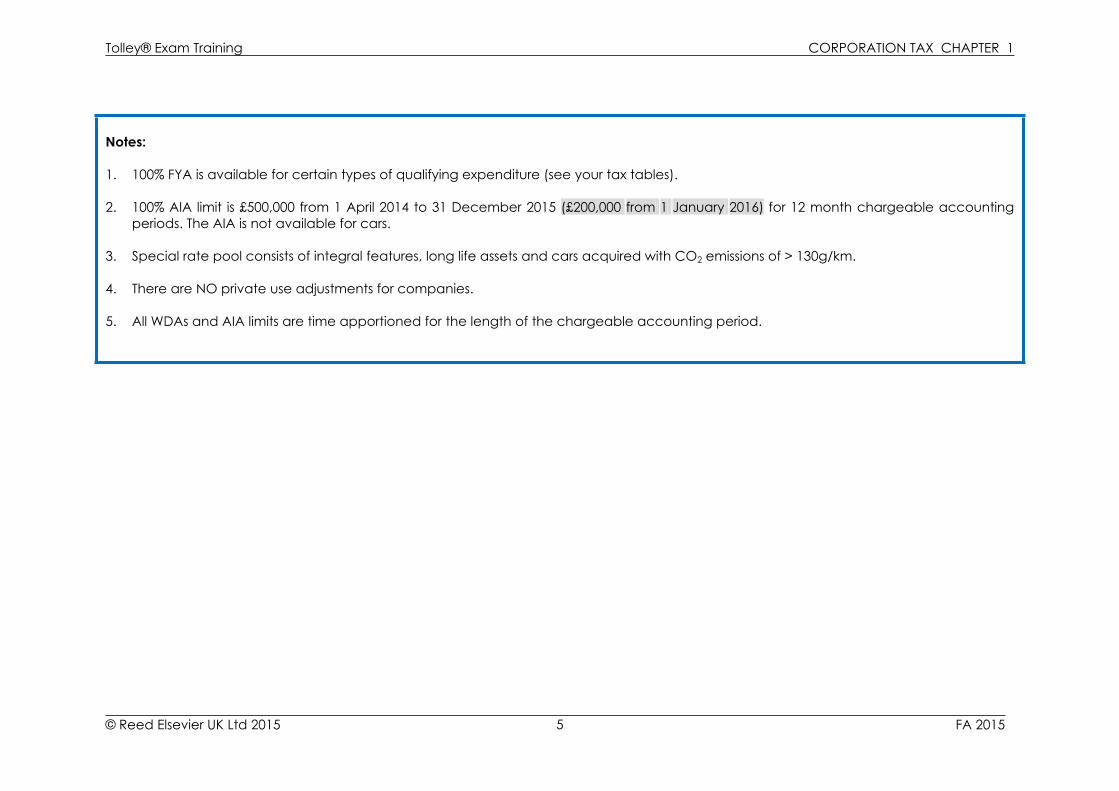

1. 100% FYA is available for certain types of qualifying expenditure (see your tax tables).

2. 100% AIA limit is £500,000 from 1 April 2014 to 31 December 2015 (£200,000 from 1 January 2016) for 12 month chargeable accounting periods. The AIA is not available for cars.

3. Special rate pool consists of integral features, long life assets and cars acquired with CO2 emissions of > 130g/km.

4. There are NO private use adjustments for companies.

5. All WDAs and AIA limits are time apportioned for the length of the chargeable accounting period.

5

Tolley® Exam Training CORPORATION TAX CHAPTER 1

© Reed Elsevier UK Ltd 2015 FA 2015

LEASES SUMMARY

Finance Lease Operating Lease Hire PurchaseLegal No legal ownership

but bears all risks and rewards of ownership

No legal ownership, short term rental agreement only

Legal ownership at end of agreement

Accounting Fixed asset on the balance sheet

Not on balance sheet

Fixed asset on the balance sheet

Depreciate through P&L

Rental expense through P&L

Depreciate through P&L

Finance lease interest through P&L

Hire purchase interest through P&L

Tax No capital allowances

No capital allowances

Capital allowances

Allow depreciation and FL interest in P&L but restrict where:

Allow rental expense in P&L but restrict where:

For cars:

Car and CO2 >130 g/km (disallow 15%)

Car and CO2 >130 g/km (disallow 15%)

• CO2 ≤75* g/km or electrically propelled: FYA 100%• CO2 76–130 g/km: general pool 18% WDA• CO2 >130 g/km: special rate pool 8% WDA

Allow interest expense in P&L

* - for expenditure incurred on/after 1 April 2015 (≤ 95g/km pre 1 April 2015)

6

Tolley® Exam Training CORPORATION TAX CHAPTER 2

© Reed Elsevier UK Ltd 2015 FA 2015

COMPUTATION OF CORPORATION TAX

Companies pay corporation tax for a chargeable accounting period on TTP.

The rate of corporation tax for FY 2015 is 20%.

For FY 2014, there are two rates of tax:

Main rate 21%Small profits rate 20%

For FY 2014, companies pay tax based on the level of their augmented profits:

TTP XFII = dividends received × 100/90 XAugmented profits X

However, it is always the TTP that is subject to corporation tax.

UK and foreign dividends received from non-associated compares form part of FII and not TTP. Dividends should be grossed up by 100/90.

The upper limit is £1,500,000 for a company with a 12 month chargeable accounting period and no associated companies. Where augmented profits are above the upper limit corporation tax is charged at the main rate (21% for FY 2014) on the whole TTP.

The lower limit is £300,000 for a company with a 12 month chargeable accounting period and no associated companies. Where augmented profits are below the lower limit corporation tax is charged at the small profits' rate (20% for FY 2014) on the whole TTP.

“Marginal relief” applies to companies whose augmented profits are between the relevant limits.

The formula for marginal relief is:(CTA 2010, s.19)

Fraction × (Upper Limit – Augmented Profits) × (TTP/Augmented Profits)

The standard fraction for FY 2014 is 1/400.

The marginal relief amount is deducted from the initial calculation of corporation tax at the main rate to give the actual corporation tax liability.

Where a company makes up its accounts for less than 12 months, it is necessary to adjust the corporation tax limits on a pro-rata basis.

(CTA 2010, s.24(4))

Limits × n/12

n = number of months in the short chargeable accounting period.

These adjusted limits are used in the marginal relief calculations.

7

Tolley® Exam Training CORPORATION TAX CHAPTER 2

© Reed Elsevier UK Ltd 2015 FA 2015

Where a chargeable accounting period straddles FY 2014 and FY 2015, the period is split into two notional accounting periods.

8

Tolley® Exam Training CORPORATION TAX CHAPTER 3

© Reed Elsevier UK Ltd 2015 FA 2015

ASSOCIATED COMPANIES

For FY 2014 (and earlier years) it is necessary to determine the number of associated companies in order to calculate the corporation tax payable.

The rules in respect of associated companies have been repealed from 1 April 2015.

Associated companies are companies under common control (i.e. >50%).

Common control can be by another company or an individual.(CTA 2010, s.450)

Dormant companies are excluded.(CTA 2010, s.25(3))

Overseas companies are included.

The profits limits are divided by the number of associated companies.

Dividends received from associated companies are ignored in determining FII.

If a company has a short chargeable accounting period together with associated companies the corporation tax limits are apportioned both for the short chargeable accounting period and the number of associates.

(CTA 2010, s.24(3)(4))

Companies which become associates or cease to be associates during the chargeable accounting period count as associates for the whole chargeable accounting period.

(CTA 2010, s.25(1))

When looking at sub-subsidiaries there is no need to multiply through to find an effective interest – the sub-subsidiaries will be associated with the top company in the group provided there is control (i.e. > 50%) at each level.

It is only necessary to aggregate holdings of an individual's associates, for the purposes of determining associated companies, where there is “substantial commercial interdependence” (i.e. financial, economic or organisational interdependence) between the companies under consideration.

(CTA 2010, s.27)

A pure holding company will be treated as dormant provided that all of the following apply:

(CTA 2010, s.26)

• It has no assets other than shares in 51% subsidiaries.

• It is not entitled to any deductions for qualifying charitable donations or management expenses in respect of any outgoings.

• It has no income or gains other than dividends which it has distributed in full to its

members.

9

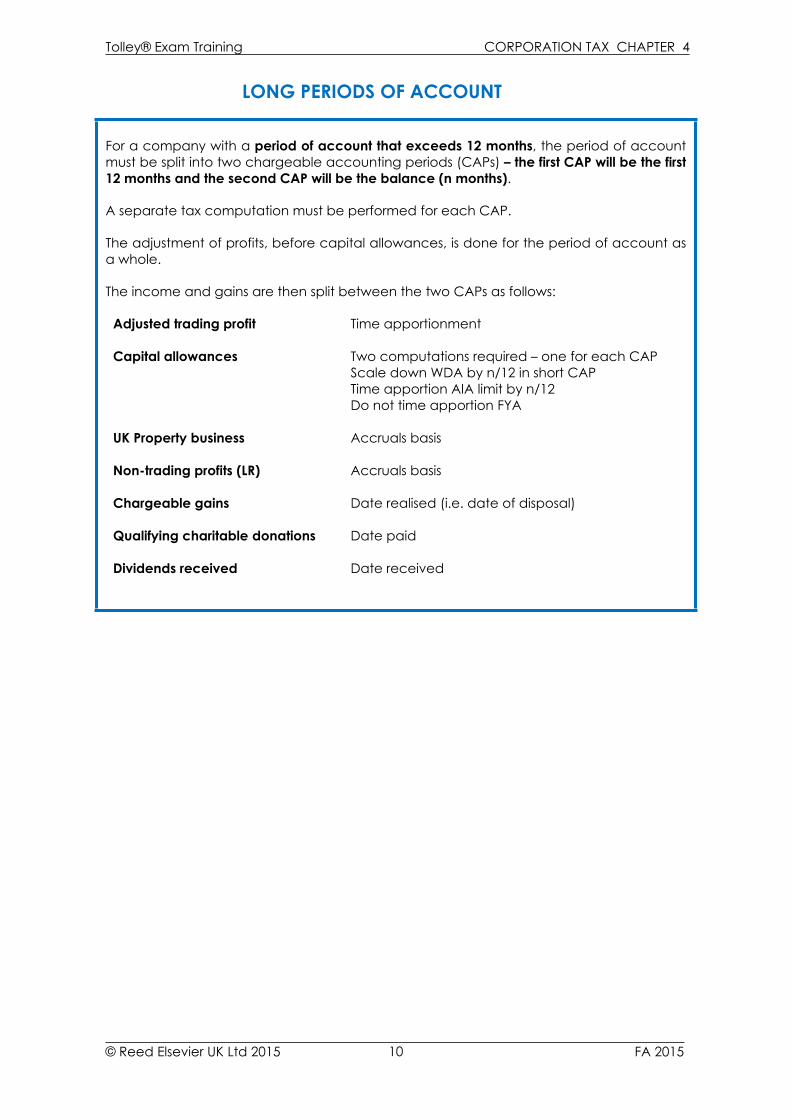

Tolley® Exam Training CORPORATION TAX CHAPTER 4

© Reed Elsevier UK Ltd 2015 FA 2015

LONG PERIODS OF ACCOUNT

For a company with a period of account that exceeds 12 months, the period of account must be split into two chargeable accounting periods (CAPs) – the first CAP will be the first 12 months and the second CAP will be the balance (n months).

A separate tax computation must be performed for each CAP.

The adjustment of profits, before capital allowances, is done for the period of account as a whole.

The income and gains are then split between the two CAPs as follows:

Adjusted trading profit Time apportionment

Capital allowances Two computations required – one for each CAPScale down WDA by n/12 in short CAPTime apportion AIA limit by n/12Do not time apportion FYA

UK Property business Accruals basis

Non-trading profits (LR) Accruals basis

Chargeable gains Date realised (i.e. date of disposal)

Qualifying charitable donations Date paid

Dividends received Date received

10

Tolley® Exam Training CORPORATION TAX CHAPTER 5

© Reed Elsevier UK Ltd 2015 FA 2015

CORPORATION TAX SELF ASSESSMENT (CTSA)

NOTIFICATION OF CHARGEABILITY:For first coming in/coming back into the charge to Corporation Tax

Company must notify HMRC within 3 months of the start of its 1st CAP.

(FA 2004, s55)

For existing company If no CT603 received notify HMRC within 12 months of end of CAP.

(FA 1998, Sch 18 para 2)

FILING THE CORPORATION TAX RETURN (CT600):

The CT600 return and the financial statements of the company must be submitted to HMRC by the later of:

• 12 months after the end of the accounting period, and

• 3 months from the receipt of the filing notice (CT603)

(FA 1998, Sch 18 para 14)Corporation tax returns must be filed online, with a full copy of the company accounts, suitably ‘tagged’ in iXBRL format.

For a long period of accounts there are two CAPs and two CT600s but both are due on the same day.

AMENDING AND CORRECTING RETURN:By HMRC 9 months from date of receipt

(FA 1998, Sch 18 para 16)By company 12 months from due filing date to

correct errors or change claims(FA 1998, Sch 18 para 15)

TIME PERIOD FOR ENQUIRIES:Filed on time 12 months from actual filing date*

Late filing 12 months from next quarter day following late filing (31 Jan, 30 April, 31 July, 31 October)

(FA 1998, Sch 18 para 24)

* This deadline only applies for single companies and companies in a small group. The deadline for large groups of companies is 12 months from the due filing date.

RECORDS: Records must be kept by a company for 6 years from the end of CAP

(FA 1998, Sch 18 para 21)

11

Tolley® Exam Training CORPORATION TAX CHAPTER 5

© Reed Elsevier UK Ltd 2015 FA 2015

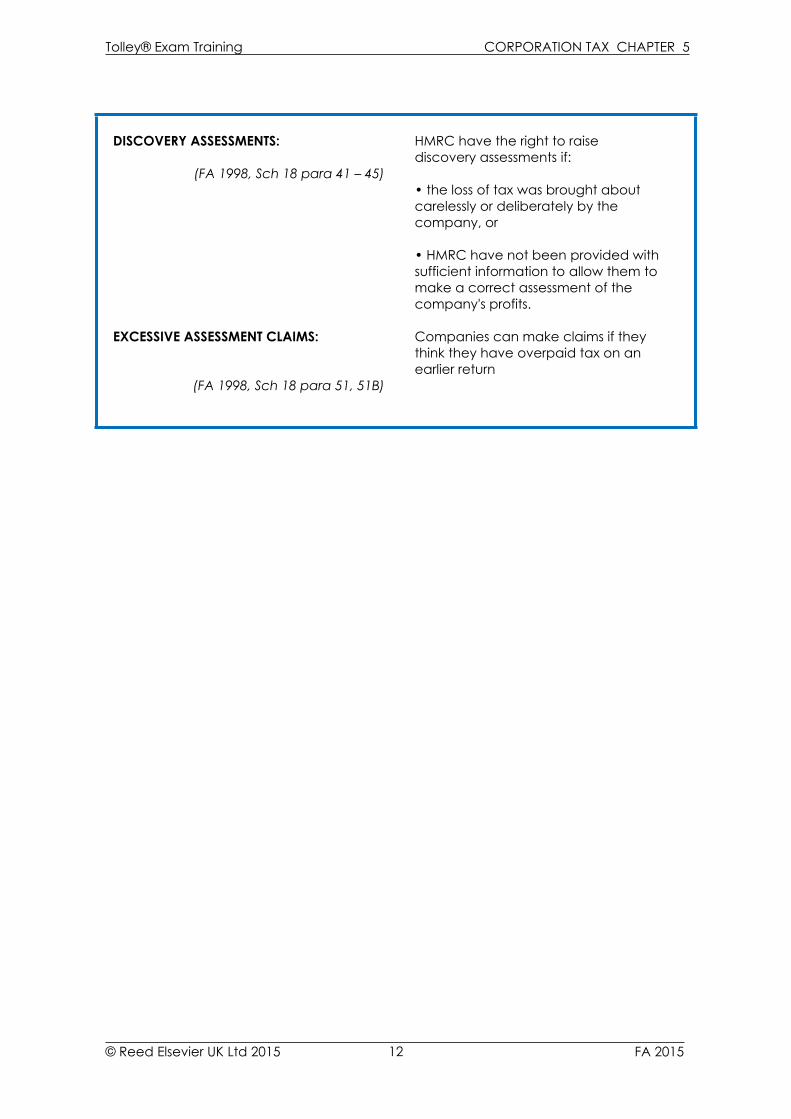

DISCOVERY ASSESSMENTS: HMRC have the right to raise discovery assessments if:

(FA 1998, Sch 18 para 41 – 45)• the loss of tax was brought about carelessly or deliberately by the company, or

• HMRC have not been provided with sufficient information to allow them to make a correct assessment of the company's profits.

EXCESSIVE ASSESSMENT CLAIMS: Companies can make claims if they think they have overpaid tax on an earlier return

(FA 1998, Sch 18 para 51, 51B)

12

Tolley® Exam Training CORPORATION TAX CHAPTER 6

© Reed Elsevier UK Ltd 2015 FA 2015

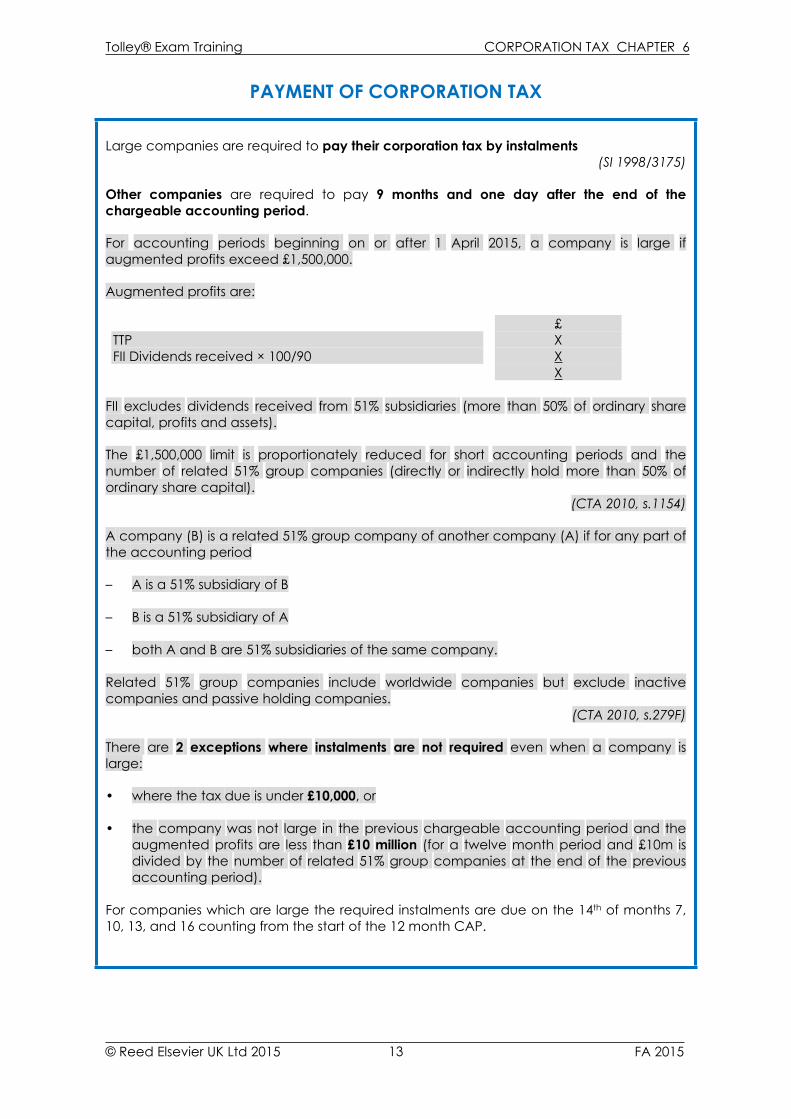

PAYMENT OF CORPORATION TAX

Large companies are required to pay their corporation tax by instalments(SI 1998/3175)

Other companies are required to pay 9 months and one day after the end of the chargeable accounting period.

For accounting periods beginning on or after 1 April 2015, a company is large if augmented profits exceed £1,500,000.

Augmented profits are:

£TTP XFII Dividends received × 100/90 X

X

FII excludes dividends received from 51% subsidiaries (more than 50% of ordinary share capital, profits and assets).

The £1,500,000 limit is proportionately reduced for short accounting periods and the number of related 51% group companies (directly or indirectly hold more than 50% of ordinary share capital).

(CTA 2010, s.1154)

A company (B) is a related 51% group company of another company (A) if for any part of the accounting period

– A is a 51% subsidiary of B

– B is a 51% subsidiary of A

– both A and B are 51% subsidiaries of the same company.

Related 51% group companies include worldwide companies but exclude inactive companies and passive holding companies.

(CTA 2010, s.279F)

There are 2 exceptions where instalments are not required even when a company is large:

• where the tax due is under £10,000, or

• the company was not large in the previous chargeable accounting period and the augmented profits are less than £10 million (for a twelve month period and £10m is divided by the number of related 51% group companies at the end of the previous accounting period).

For companies which are large the required instalments are due on the 14th of months 7, 10, 13, and 16 counting from the start of the 12 month CAP.

13

Tolley® Exam Training CORPORATION TAX CHAPTER 6

© Reed Elsevier UK Ltd 2015 FA 2015

The amount of corporation tax due for each instalment is calculated as:

3/n × estimated CT liability

Where n = number of months in CAP.

The first instalment is due on the 14th day of month 7 from the start of CAP.

The final instalment is always due 3 months + 14 days after the end of CAP.

Any further instalments are 3 months from the previous instalment.

14

Tolley® Exam Training CORPORATION TAX CHAPTER 6

© Reed Elsevier UK Ltd 2015 FA 2015

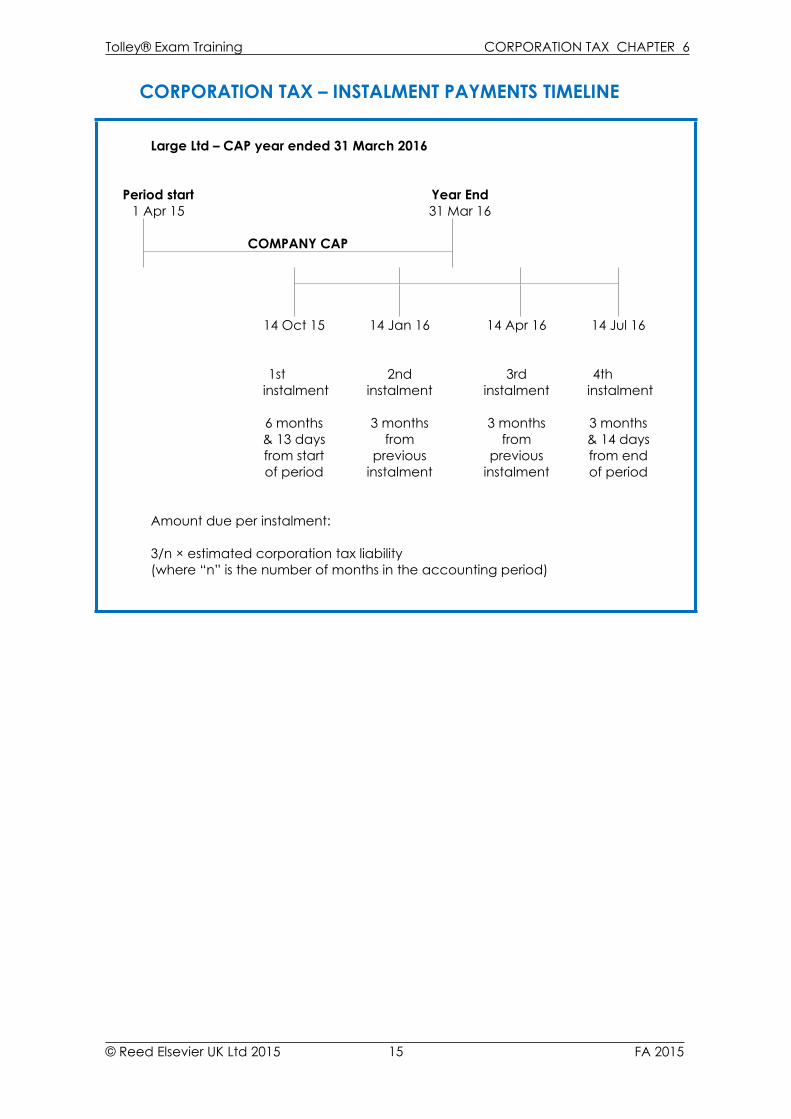

CORPORATION TAX – INSTALMENT PAYMENTS TIMELINE

Large Ltd – CAP year ended 31 March 2016

Period start Year End1 Apr 15 31 Mar 16

COMPANY CAP

14 Oct 15 14 Jan 16 14 Apr 16 14 Jul 16

1st instalment

2nd instalment

3rd instalment

4th instalment

6 months 3 months 3 months 3 months& 13 days from from & 14 daysfrom start previous previous from endof period instalment instalment of period

Amount due per instalment:

3/n × estimated corporation tax liability(where “n” is the number of months in the accounting period)

15

Tolley® Exam Training CORPORATION TAX CHAPTER 7

© Reed Elsevier UK Ltd 2015 FA 2015

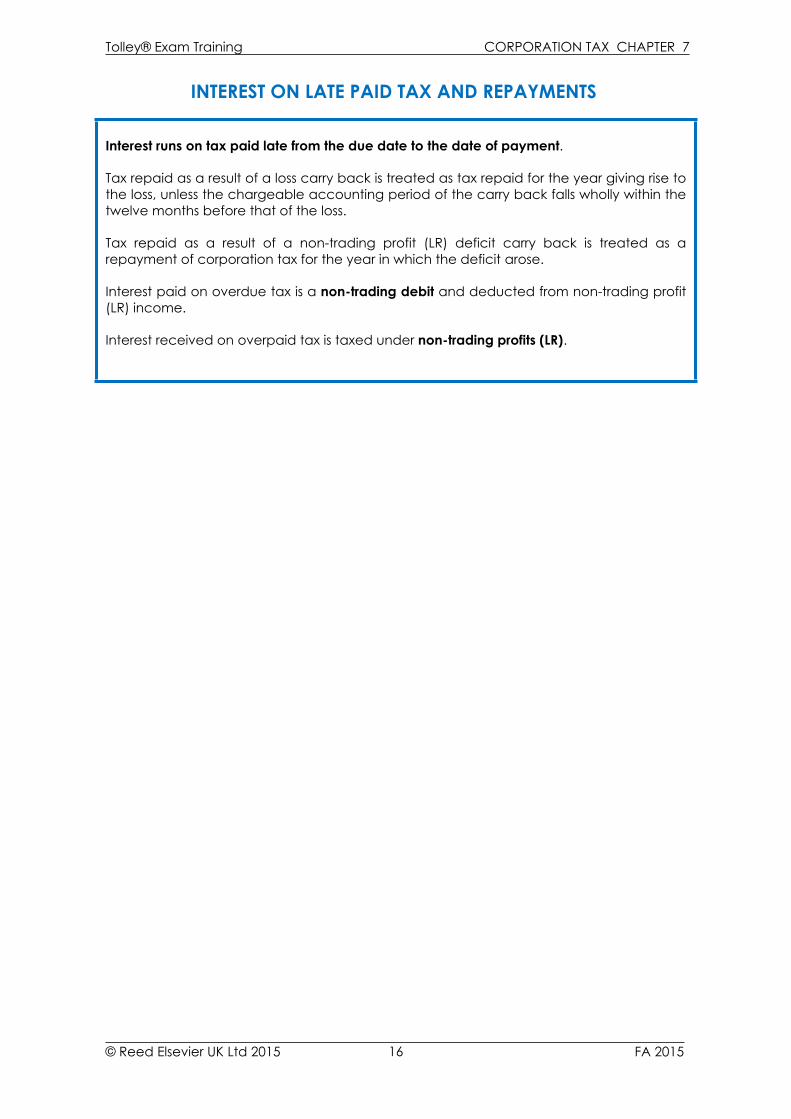

INTEREST ON LATE PAID TAX AND REPAYMENTS

Interest runs on tax paid late from the due date to the date of payment.

Tax repaid as a result of a loss carry back is treated as tax repaid for the year giving rise to the loss, unless the chargeable accounting period of the carry back falls wholly within the twelve months before that of the loss.

Tax repaid as a result of a non-trading profit (LR) deficit carry back is treated as a repayment of corporation tax for the year in which the deficit arose.

Interest paid on overdue tax is a non-trading debit and deducted from non-trading profit (LR) income.

Interest received on overpaid tax is taxed under non-trading profits (LR).

16

Tolley® Exam Training CORPORATION TAX CHAPTER 8

© Reed Elsevier UK Ltd 2015 FA 2015

CTSA PENALTY REGIME

PENALTIES FOR FAILURE TO NOTIFY CHARGEABILITY The penalty is charged as a % of the amount of corporation tax which is unpaid 12 months after the end of the chargeable accounting period as a result of the failure to notify.

(FA 2008, Sch 41 para 7(3))

The following table details the maximum and minimum penalties that could apply;(FA 2008, Sch 41 para 13)

Behaviour Maximum penalty

Minimum penalty with unprompted

disclosure

Minimum penalty with prompted

disclosure

Deliberate and concealed

100% 30% 50%

Deliberate but not concealed

70% 20% 35%

<12m* ≥12m* <12m* ≥12m*Any other case 30% Nil 10% 10% 20%

*from the date of the tax becoming unpaid

The penalty is due within 30 days of the assessment being raised. Failure to pay will result in interest being charged on the penalty.

(FA 2008, Sch 41 para 16)

The penalty can be avoided if there is a reasonable excuse or can be reduced if special circumstances apply.

(FA 2008, Sch 41 para 20 & 14)

PENALTIES FOR LATE RETURNS The penalties are:

(FA 2009, Sch 55 paras 3–6)

• immediate £100 fixed penalty where return is filed late, plus

• potential penalties of £10 per day for a maximum of 90 days where return > 3 months late; plus

• penalty of 5% of the liability to tax (or £300 if greater) if return > 6 months late; plus

• additional penalties where returns filed > 12 months late, as follows:

17

Tolley® Exam Training CORPORATION TAX CHAPTER 8

© Reed Elsevier UK Ltd 2015 FA 2015

Behaviour Max penalty

Min penalty with unprompted

disclosure

Min penalty with prompted disclosure

Deliberate and concealed

100% 30% 50%

Deliberate but not concealed

70% 20% 35%

Any other case 5% N/A N/A

Minimum penalty of £300 if greater.

The penalty for late filing is charged in addition to the penalty for late payment if both apply.

PENALTIES FOR FAILURE TO KEEP RECORDS A penalty of £3,000 per chargeable accounting period applies where there has been a failure to keep records for 6 years from the end of the chargeable accounting period.

(FA 1998, Sch 18 para 23)

PENALTIES FOR INCORRECT RETURNS The penalties are a percentage of lost revenue:

(FA 2007, Sch 24 paras 4 & 10)

Behaviour Maximum penalty

Min penalty with unprompted

disclosure

Min penalty with prompted disclosure

Deliberate and concealed

100% 30% 50%

Deliberate but not concealed

70% 20% 35%

Careless 30% 0% 15%

A penalty for a careless error may be suspended for two years.(FA 2007, Sch 24 para 14)

Both the penalties for late filing and incorrect returns are due within 30 days of the assessment being raised. Failure to pay will result in interest being charged on the penalty.(FA 2007, Sch 24 para 13 )

(FA 2007, Sch 55 para 18 )

The penalties can be avoided if there is a reasonable excuse or they can be reduced if special circumstances apply.

18

Tolley® Exam Training CORPORATION TAX CHAPTER 8

© Reed Elsevier UK Ltd 2015 FA 2015

PENALTIES FOR LATE PAYMENT OF TAX For corporation tax, a 5% penalty of the outstanding tax is charged in respect of each of:

(FA 2009, Sch 56 paras 1 & 4)

• tax outstanding after the filing date of the return; and

• tax outstanding more than 3 months after the filing date of the return; and

• tax outstanding more than 9 months after the filing date of the return.

If the taxpayer has entered into an agreed time to pay arrangement, late payment penalties will not be charged.

The penalty is due within 30 days of the assessment being raised. Failure to pay will result in interest being charged on the penalty.

(FA 2009, Sch 56 para 11)

The penalty can be avoided if there is a reasonable excuse or it can be reduced if special circumstances apply.

(FA 2009, Sch 56 paras 16 & 9)

19

Tolley® Exam Training CORPORATION TAX CHAPTER 9

© Reed Elsevier UK Ltd 2015 FA 2015

PROPERTY INCOME

UK property business income is taxed on an accruals basis.

Relief is given for expenses incurred wholly and exclusively for the UK property business.

Interest on loans taken out to buy properties is never a UK property business expense for companies, it is instead relieved under the loan relationship rules.

Dividends from Real Estate Investment Trusts (REITs) are taxed as UK property business income and are received gross by companies.

20

Tolley® Exam Training CORPORATION TAX CHAPTER 10

© Reed Elsevier UK Ltd 2015 FA 2015

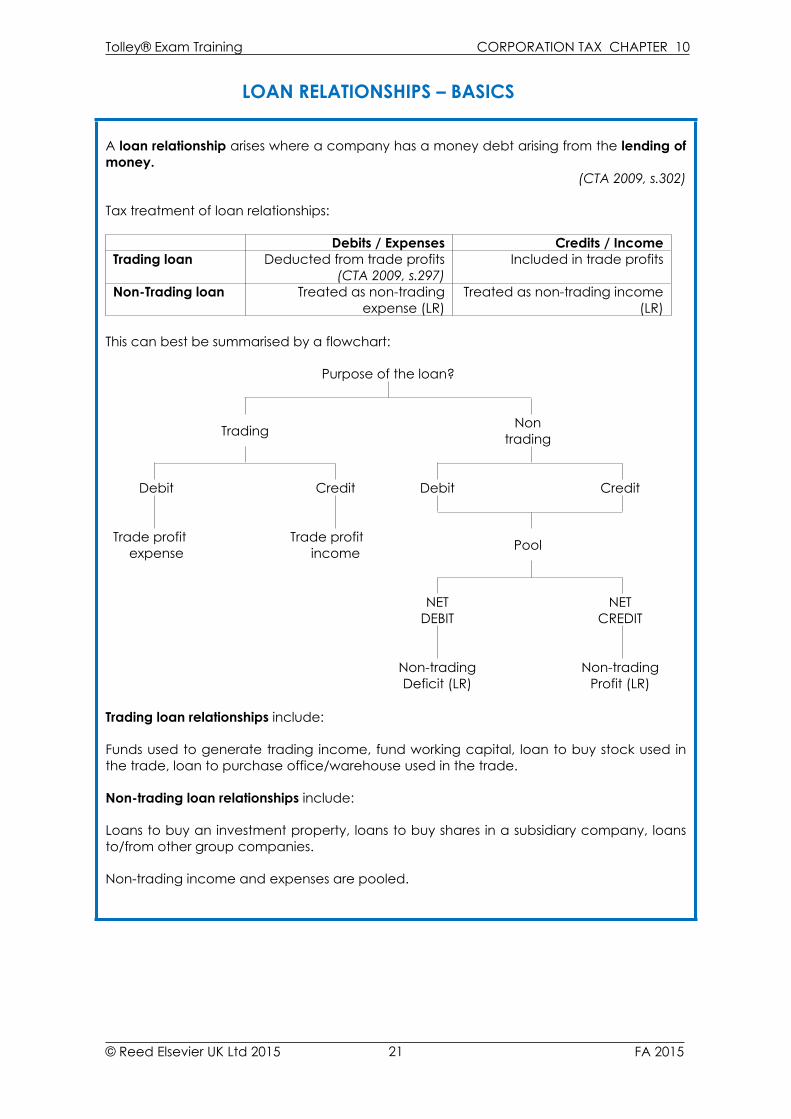

LOAN RELATIONSHIPS – BASICS

A loan relationship arises where a company has a money debt arising from the lending of money.

(CTA 2009, s.302)

Tax treatment of loan relationships:

Debits / Expenses Credits / IncomeTrading loan Deducted from trade profits

(CTA 2009, s.297)Included in trade profits

Non-Trading loan Treated as non-trading expense (LR)

Treated as non-trading income (LR)

This can best be summarised by a flowchart:

Purpose of the loan?

Trading Non trading

Debit Credit Debit Credit

Trade profit Trade profitexpense income Pool

NET NETDEBIT CREDIT

Non-trading Non-tradingDeficit (LR) Profit (LR)

Trading loan relationships include:

Funds used to generate trading income, fund working capital, loan to buy stock used in the trade, loan to purchase office/warehouse used in the trade.

Non-trading loan relationships include:

Loans to buy an investment property, loans to buy shares in a subsidiary company, loans to/from other group companies.

Non-trading income and expenses are pooled.

21

Tolley® Exam Training CORPORATION TAX CHAPTER 11

© Reed Elsevier UK Ltd 2015 FA 2015

LOAN RELATIONSHIPS – CONNECTED COMPANIES

Loan Relationships are accounted for at fair value or amortised cost – connected companies must use amortised cost.

(CTA 2009, s.349)

This will involve adjustments in the period companies become connected if the loans are held at fair value.

(CTA 2009, s.350)

No income or expense is recognised in respect of impairments or released debts between connected companies.

(CTA 2009, s.354 & 358)

If companies become connected, impairment losses up to the date of connection are recognised, with corresponding income in the debtor company.

(CTA 2009, s.362 & 358)

If an unconnected consortium member has a deduction for an impairment on a loan to a consortium company and claims consortium relief, restrictions apply to prevent double economic relief.

(CTA 2009, s.364)

Interest is deductible when payment is made if it is payable to:

• a participator (or his associate) in a close company(CTA 2009, s.375)

and

• it has not been paid within 12 months of the end of the accounting period,

and

• it has not been taxed in the hands of the recipient.(CTA 2009, s.373)

22

Tolley® Exam Training CORPORATION TAX CHAPTER 12

© Reed Elsevier UK Ltd 2015 FA 2015

RELIEF FOR TRADING LOSSES

When a company makes a trading loss it can relieve it against:

i. total profits of the same chargeable accounting period then,(CTA 2010, s.37(3)(a))

ii. total profits of the previous 12 months, and any unused loss is then automatically(CTA 2010, s.37(3)(b))

iii. carried forward against future trade profits only(CTA 2010, s.45(4))

Total profits means income and gains before deducting qualifying charitable donations.

A carry back claim can only be made after a current year claim has been made.

Care needs to be taken if there is a short chargeable accounting period, as the carry back must be against 12 months worth of profits, if the loss is large enough.

Where the company ceases to trade, the trading loss of the final 12 months can be carried back against total profits of the 36 months ending immediately before the loss making period rather than the normal 12 months.

(CTA 2010, s.39)

When a loss is carried back it will generate a repayment of CT paid for the earlier accounting period.

Both current year and carry back claims are ‘all-or-nothing’ – partial claims are not permitted.

The time limit for these claims is two years from the end of the loss making chargeable accounting period.

23

Tolley® Exam Training CORPORATION TAX CHAPTER 12

© Reed Elsevier UK Ltd 2015 FA 2015

CORPORATION TAX TRADING LOSS PROFORMA

Period ended£

Trade profit XLess: Losses b/fwd - S.45(4) (X)

XUK property business income XNon trading profit (LR) XOverseas property business income XNon trading gains (IFAs) XChargeable gains X

XLess: Current year loss - S.37(3)(a) (X)

X

Less: Carried back loss - S.37(3)(b) (X)X

Less: Qualifying charitable donations (X)TTP X

24

Tolley® Exam Training CORPORATION TAX CHAPTER 13

© Reed Elsevier UK Ltd 2015 FA 2015

RELIEF FOR OTHER LOSSES

Losses from a UK property business must be set off against total profits of the current period. If excess losses remain these can be carried forward against future profits.

(CTA 2010, s.62)

Overseas property business losses are pooled together with profits on overseas properties. Losses are then carried forward and set against profits of the overseas property business of future accounting periods.

(CTA 2010, s.66)

Non-trading income and expenses are pooled. If the non-trading debits exceed the non-trading credits then loss relief is available for the resulting deficit.

Deficits (or losses) from a non-trading loan relationship can be offset against any profits in the period, although a 12 month carry back against non-trading profits (LR) is also possible. These claims can be done in any order and are very flexible.

(CTA 2009, s.461 and s.462)

Unused non-trading (LR) deficits are automatically carried forward against future non-trading income and gains unless the company elects for them not to be offset in this way.

(CTA 2009, s.457)

25

Tolley® Exam Training CORPORATION TAX CHAPTER 13

© Reed Elsevier UK Ltd 2015 FA 2015

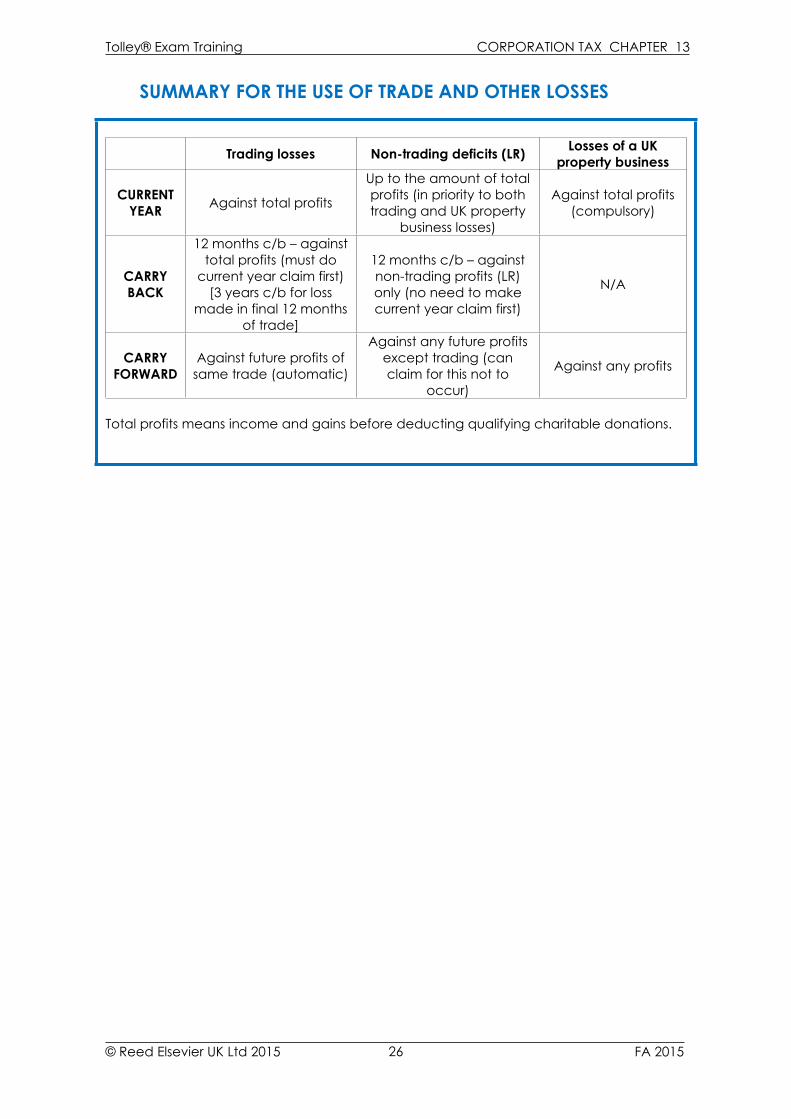

SUMMARY FOR THE USE OF TRADE AND OTHER LOSSES

Trading losses Non-trading deficits (LR) Losses of a UK property business

CURRENT YEAR Against total profits

Up to the amount of total profits (in priority to both trading and UK property

business losses)

Against total profits (compulsory)

CARRY BACK

12 months c/b – against total profits (must do

current year claim first) [3 years c/b for loss

made in final 12 months of trade]

12 months c/b – against non-trading profits (LR) only (no need to make current year claim first)

N/A

CARRY FORWARD

Against future profits of same trade (automatic)

Against any future profits except trading (can claim for this not to

occur)

Against any profits

Total profits means income and gains before deducting qualifying charitable donations.

26

Tolley® Exam Training CORPORATION TAX CHAPTER 14

© Reed Elsevier UK Ltd 2015 FA 2015

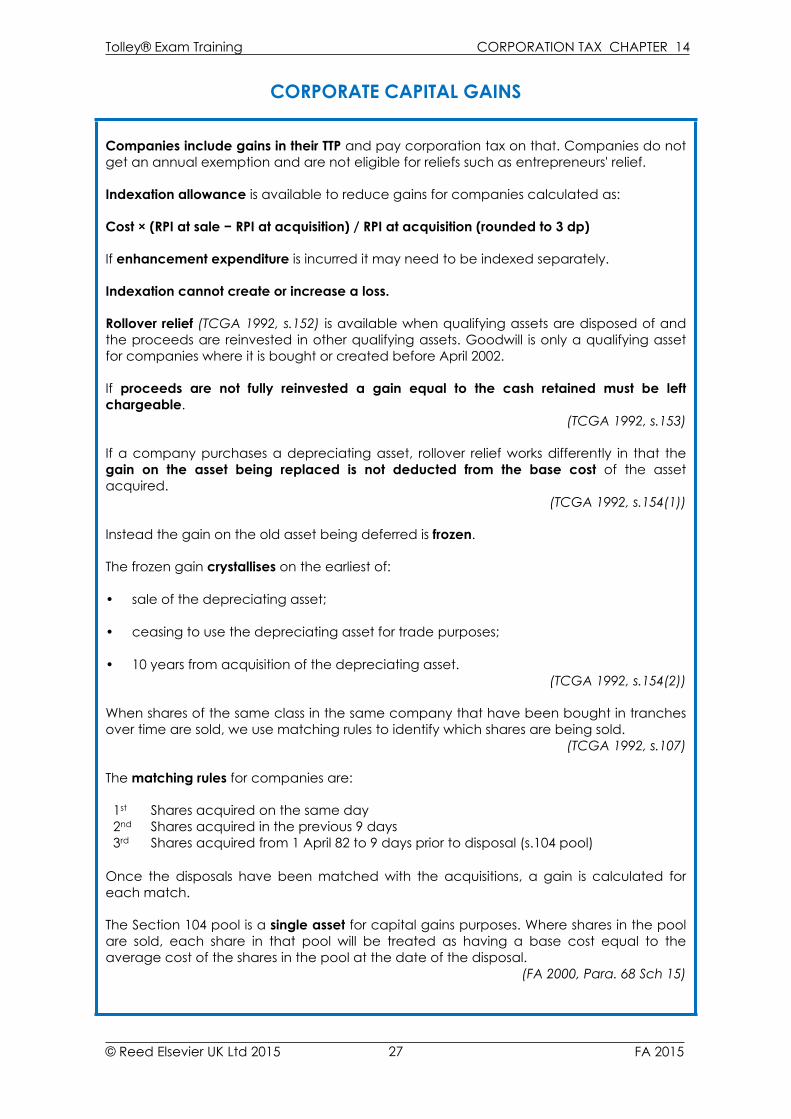

CORPORATE CAPITAL GAINS

Companies include gains in their TTP and pay corporation tax on that. Companies do not get an annual exemption and are not eligible for reliefs such as entrepreneurs' relief.

Indexation allowance is available to reduce gains for companies calculated as:

Cost × (RPI at sale − RPI at acquisition) / RPI at acquisition (rounded to 3 dp)

If enhancement expenditure is incurred it may need to be indexed separately.

Indexation cannot create or increase a loss.

Rollover relief (TCGA 1992, s.152) is available when qualifying assets are disposed of and the proceeds are reinvested in other qualifying assets. Goodwill is only a qualifying asset for companies where it is bought or created before April 2002.

If proceeds are not fully reinvested a gain equal to the cash retained must be left chargeable.

(TCGA 1992, s.153)

If a company purchases a depreciating asset, rollover relief works differently in that the gain on the asset being replaced is not deducted from the base cost of the asset acquired.

(TCGA 1992, s.154(1))

Instead the gain on the old asset being deferred is frozen.

The frozen gain crystallises on the earliest of:

• sale of the depreciating asset;

• ceasing to use the depreciating asset for trade purposes;

• 10 years from acquisition of the depreciating asset.(TCGA 1992, s.154(2))

When shares of the same class in the same company that have been bought in tranches over time are sold, we use matching rules to identify which shares are being sold.

(TCGA 1992, s.107)

The matching rules for companies are:

1st Shares acquired on the same day2nd Shares acquired in the previous 9 days3rd Shares acquired from 1 April 82 to 9 days prior to disposal (s.104 pool)

Once the disposals have been matched with the acquisitions, a gain is calculated for each match.

The Section 104 pool is a single asset for capital gains purposes. Where shares in the pool are sold, each share in that pool will be treated as having a base cost equal to the average cost of the shares in the pool at the date of the disposal.

(FA 2000, Para. 68 Sch 15)

27

Tolley® Exam Training CORPORATION TAX CHAPTER 14

© Reed Elsevier UK Ltd 2015 FA 2015

CHARGEABLE GAINS PROFORMA – COMPANY

COST£

Gross sale proceeds XLess: Incidental selling cost (X)Net sale proceeds XLess: Original acquisition cost (X)Less: Incidental costs of acquisition (X)Less: Enhancement expenditure (X)Unindexed Gain X

Less: Indexation allowance* on cost (X)Less: Indexation allowance on enhancement (X)

Indexed gain X

Less: Roll over relief (if available and claimed) (X)Gain after relief X

Less: Current year capital losses (X)Less: Brought forward capital losses (X)Net chargeable gain (included in TTP and charged to corporation tax)

X

* Indexation allowance (3dp) = (RPI disposal − RPI acquisition) / RPI acquisition × cost

RPI at acquisition is replaced by RPI at enhancement when calculating indexation allowance on enhancement expenditure.

28

Tolley® Exam Training CORPORATION TAX CHAPTER 14

© Reed Elsevier UK Ltd 2015 FA 2015

SOLE TRADERS V COMPANIES

Sole Traders/partners CompaniesTax rates set for tax years: Tax rates set for financial years:6 April – 5 April 1 April – 31 MarchTaxed on income and gains for a tax year

Taxed on income and gains for a chargeable accounting period

Basis period rules used to allocate results to tax years (opening years, closing year, change of accounting date rules with overlaps)

Chargeable accounting periods (“CAP”) (can never be more than 12 months and no overlaps)

No deduction from trade profits for private expenditure by sole traders/partners

Deduction from trade profit allowed for employee/director as private expenditure is taxed on employee/director as employment benefit

Capital allowances per accounting period (can be > 12 months)

Capital allowances per CAP (can never be more than 12 months)

Restrict capital allowances for private use by sole traders/partners

No restriction of capital allowances for private use by employee/director

Trade profits included in net income and charged to income tax

Trade profits included in TTP and charged to corporation tax

Trade losses: Trade losses:CY – against net income CY – against TTP before donationsCB – against net income (CY/CB any order)

CB – against TTP before donations (but CY must be done first)

Extend CY/CB against gains CF – against trade profitsCF – against trade profits On cessation – CB against TTP for 3 yearsEarly years – losses in first 4 years carry back (FIFO) against previous 3 years net incomeTerminal losses – carry back (LIFO) 3 years against trade profitsNIC – Class 2 and 4 NIC Class 1 Secondary, Class 1A and

Class 1B (payable by company as employer) but allowed as a corporation tax deduction

Due dates for returns: 31 Jan following tax year (electronic)

Due dates for returns: 12 months following CAP (unless period of account > 12 months then 12 months from end of period of account)

Can self assess or HMRC to calculate tax Must self assessDue dates for payments: Due dates for payments:POA 1: 31 Jan in tax yearPOA 2: 31 July after tax year Large – instalments Balance: 31 Jan after tax year (instalment amount 3/n × estimated CT

liability)(POA 50% prior year IT and Class 4 NIC due)

Others – 9 months 1 day from end of CAP

Capital gains charged to CGT – no indexation but AE given

Capital gains included in TTP - indexation but no AE given

Range of CGT deferral reliefs available Only deferral relief available for capital gains is rollover relief.

29

Tolley® Exam Training CORPORATION TAX CHAPTER 15

© Reed Elsevier UK Ltd 2015 FA 2015

SUBSTANTIAL SHAREHOLDING EXEMPTION

Under SSE gains on shares held by companies are exempt from corporation tax and losses are not allowable provided that:

• at least 10% stake has been held throughout a period of 12 months in the last 24

months of ownership.(TCGA 1992, paras 7 & 8 Sch 7AC)

• both companies are trading companies (or members of a trading group) throughout the 12 month holding period AND immediately after the disposal.

(TCGA 1992, paras 18 & 19 Sch 7AC)

Shareholdings of all group companies (51% holdings) are aggregated to determine whether the conditions have been satisfied.

(TCGA 1992, para 9)

30

Tolley® Exam Training CORPORATION TAX CHAPTER 16

© Reed Elsevier UK Ltd 2015 FA 2015

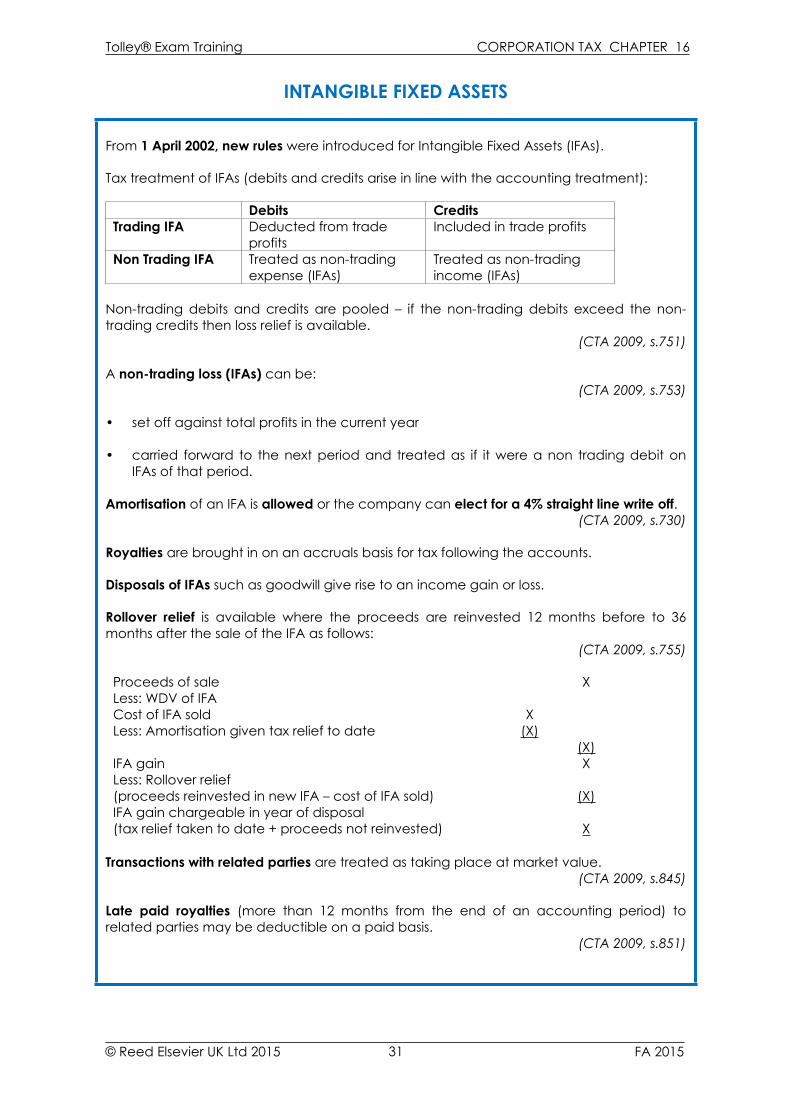

INTANGIBLE FIXED ASSETS

From 1 April 2002, new rules were introduced for Intangible Fixed Assets (IFAs).

Tax treatment of IFAs (debits and credits arise in line with the accounting treatment):

Debits CreditsTrading IFA Deducted from trade

profitsIncluded in trade profits

Non Trading IFA Treated as non-trading expense (IFAs)

Treated as non-trading income (IFAs)

Non-trading debits and credits are pooled – if the non-trading debits exceed the non-trading credits then loss relief is available.

(CTA 2009, s.751)

A non-trading loss (IFAs) can be:(CTA 2009, s.753)

• set off against total profits in the current year

• carried forward to the next period and treated as if it were a non trading debit on IFAs of that period.

Amortisation of an IFA is allowed or the company can elect for a 4% straight line write off.

(CTA 2009, s.730)

Royalties are brought in on an accruals basis for tax following the accounts.

Disposals of IFAs such as goodwill give rise to an income gain or loss.

Rollover relief is available where the proceeds are reinvested 12 months before to 36 months after the sale of the IFA as follows:

(CTA 2009, s.755)

Proceeds of sale XLess: WDV of IFACost of IFA sold XLess: Amortisation given tax relief to date (X)

(X)IFA gain XLess: Rollover relief (proceeds reinvested in new IFA – cost of IFA sold) (X)IFA gain chargeable in year of disposal (tax relief taken to date + proceeds not reinvested) X

Transactions with related parties are treated as taking place at market value.

(CTA 2009, s.845)

Late paid royalties (more than 12 months from the end of an accounting period) to related parties may be deductible on a paid basis.

(CTA 2009, s.851)

31

Tolley® Exam Training CORPORATION TAX CHAPTER 16

© Reed Elsevier UK Ltd 2015 FA 2015

For goodwill acquired on/after 3 December 2014, corporation tax relief is not available where it is acquired from an individual who is a related party in relation to the company.

(CTA 2009, s.849B-D)

Companies can elect for profits from IP and patents to be taxed at a lower rate. Rules commenced 1 April 2013 and are being phased in over 5 years to give an effective rate of 10%.

Relief is given by allowing a deduction to be made in calculating the trade profits for the period as follows:

Relevant IP profits x (Main rate of CT — IP Rate of CT)/Main Rate of CT(CTA 2010, s.357A)

The relevant IP profits used in the above calculation are reduced as follows:

Financial Year % of IP Profits2013 60%2014 70%2015 80%2016 90%

32

Tolley® Exam Training CORPORATION TAX CHAPTER 17

© Reed Elsevier UK Ltd 2015 FA 2015

RESEARCH AND DEVELOPMENT EXPENDITURE

For expenditure incurred on or after 1 April 2015, SMEs can claim a tax deduction of 230% for qualifying R&D (for expenditure incurred pre 1.4.15, the deduction was 225%).

The relief relates to “qualifying” expenditure on:(CTA 2009, s.1052)

• staff costs

• software and consumable items

• relevant payments to subjects of clinical trials

• externally provided workers

For expenditure incurred on/after 1 April 2015, relief is not available for consumables reflected in goods/services sold as part of the company’s trade.

SMEs with losses can surrender them to HMRC and receive a tax credit/repayment(CTA 2009, s.1058)

The surrenderable amount is the lower of:

• Qualifying R&D × 230% (225% for expenditure incurred pre 1.4.15).

• Unrelieved trading losses.

The tax credit is 14.5% of the surrenderable loss for the period since 1 April 2014.

Large companies can claim a tax deduction of 130% for qualifying R&D. This deduction will be available until 31 March 2016.

For expenditure from 1 April 2013, an R&D expenditure credit (RDEC) of is available. This may be claimed instead of the 130% deduction, which it replaces from 1 April 2016.

(CTA 2009, s.104A)

The RDEC is treated as a taxable receipt in calculating the profits of the trade for the accounting period. The company will also receive a credit against its tax liability of the same amount. This credit is equal to 11% of the company’s qualifying R&D expenditure incurred on or after 1 April 2015. The credit is 10% of expenditure incurred prior to this date.

33

Tolley® Exam Training CORPORATION TAX CHAPTER 18

© Reed Elsevier UK Ltd 2015 FA 2015

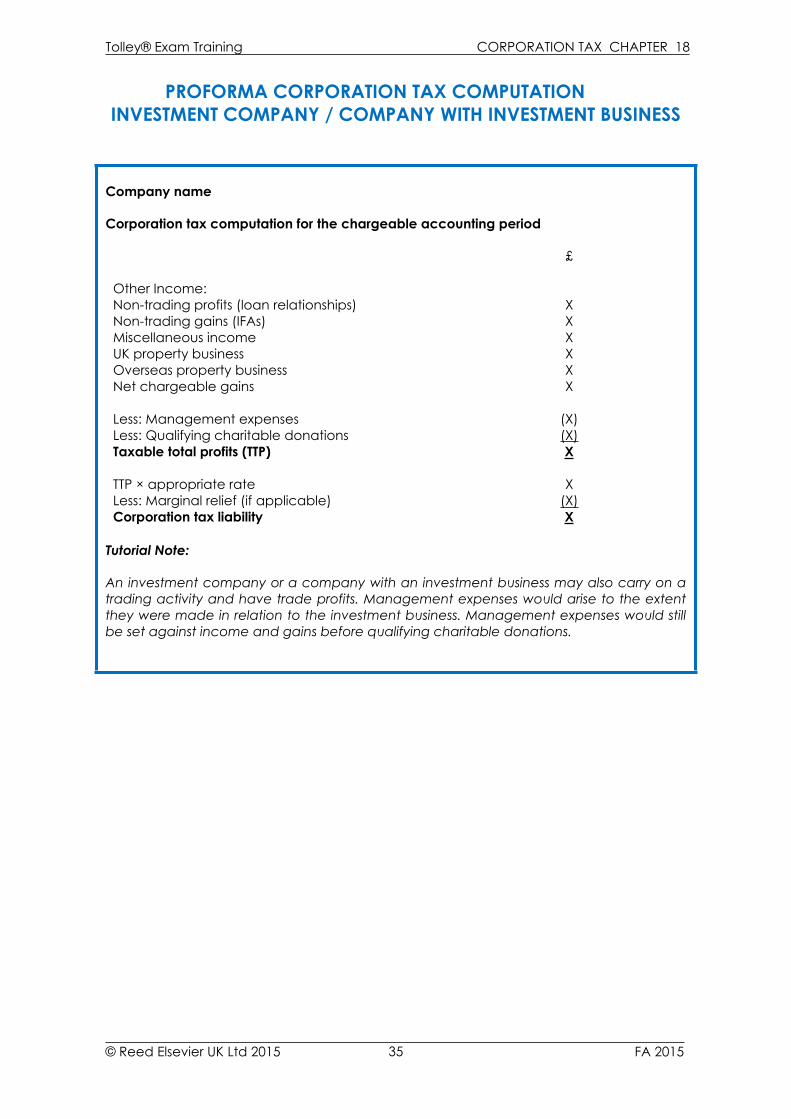

COMPANIES WITH INVESTMENT BUSINESS

A company with investment business is a company deriving its income wholly or partly from the making of investments.

(CTA 2009, s.1218B)

The Taxable Total Profits (TTP) of a company with investment business are found by adding together income and gains and deducting management expenses before any other deductions and reliefs.

Management expenses include agents' commissions, professional fees, premises costs and reasonable directors' salaries, but exclude expenses of a capital nature or for an unallowable purpose.

(CTA 2009, s.1219)

Management expenses are deductible based on when they are debited in the accounts.(CTA 2009, s.1224)

If management expenses exceed profits, a company has “excess management expenses”. These excess management expenses can be carried forward.

(CTA 2009, s.1223)

When an investment company has a capital loss on the disposal of shares that it subscribed for in a qualifying company, it can claim to set that loss off against income of that period or the previous period.

(CTA 2010, s.68)

An investment company is a company whose business consists wholly or mainly in the making of investments and the principal part of whose income is derived therefrom.

(CTA 2010, s.90(1))

34

Tolley® Exam Training CORPORATION TAX CHAPTER 18

© Reed Elsevier UK Ltd 2015 FA 2015

PROFORMA CORPORATION TAX COMPUTATIONINVESTMENT COMPANY / COMPANY WITH INVESTMENT BUSINESS

Company name

Corporation tax computation for the chargeable accounting period

£

Other Income:Non-trading profits (loan relationships) XNon-trading gains (IFAs) XMiscellaneous income XUK property business XOverseas property business XNet chargeable gains X

Less: Management expenses (X)Less: Qualifying charitable donations (X)Taxable total profits (TTP) X

TTP × appropriate rate XLess: Marginal relief (if applicable) (X)Corporation tax liability X

Tutorial Note:

An investment company or a company with an investment business may also carry on a trading activity and have trade profits. Management expenses would arise to the extent they were made in relation to the investment business. Management expenses would still be set against income and gains before qualifying charitable donations.

35

Tolley® Exam Training CORPORATION TAX CHAPTER 19

© Reed Elsevier UK Ltd 2015 FA 2015

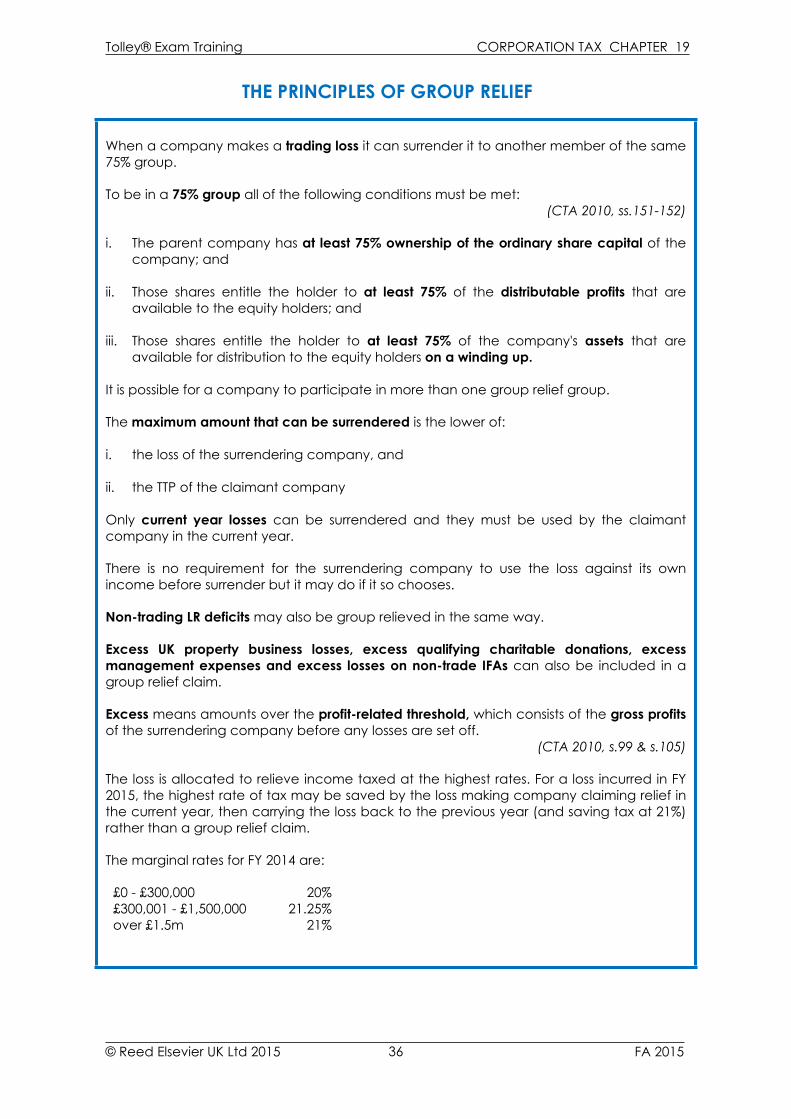

THE PRINCIPLES OF GROUP RELIEF

When a company makes a trading loss it can surrender it to another member of the same 75% group.

To be in a 75% group all of the following conditions must be met:(CTA 2010, ss.151-152)

i. The parent company has at least 75% ownership of the ordinary share capital of the company; and

ii. Those shares entitle the holder to at least 75% of the distributable profits that are

available to the equity holders; and

iii. Those shares entitle the holder to at least 75% of the company's assets that are available for distribution to the equity holders on a winding up.

It is possible for a company to participate in more than one group relief group.

The maximum amount that can be surrendered is the lower of:

i. the loss of the surrendering company, and

ii. the TTP of the claimant company

Only current year losses can be surrendered and they must be used by the claimant company in the current year.

There is no requirement for the surrendering company to use the loss against its own income before surrender but it may do if it so chooses.

Non-trading LR deficits may also be group relieved in the same way.

Excess UK property business losses, excess qualifying charitable donations, excess management expenses and excess losses on non-trade IFAs can also be included in a group relief claim.

Excess means amounts over the profit-related threshold, which consists of the gross profits of the surrendering company before any losses are set off.

(CTA 2010, s.99 & s.105)

The loss is allocated to relieve income taxed at the highest rates. For a loss incurred in FY 2015, the highest rate of tax may be saved by the loss making company claiming relief in the current year, then carrying the loss back to the previous year (and saving tax at 21%) rather than a group relief claim.

The marginal rates for FY 2014 are:

£0 - £300,000 20%£300,001 - £1,500,000 21.25%over £1.5m 21%

36

Tolley® Exam Training CORPORATION TAX CHAPTER 20

© Reed Elsevier UK Ltd 2015 FA 2015

GROUP RELIEF – FURTHER ASPECTS

Where the two companies do not have the same year-end, it is necessary to time apportion the profits and losses. The group relief becomes the lower of:

i. the loss, and

ii. TTP

of the corresponding (same) chargeable accounting period.

A corresponding chargeable accounting period starts when a company joins the group. Therefore group relief is not available for losses made before the company joined the group.

Similar rules apply when a company leaves the group, with the date of leaving being the date that “arrangements for sale” come into being.

Relief is available between two UK companies if they are 75% connected via a non-resident company.

37

Tolley® Exam Training CORPORATION TAX CHAPTER 21

© Reed Elsevier UK Ltd 2015 FA 2015

CONSORTIUM RELIEF

A consortium exists where 75% of the shares of the company (the consortium company) are owned by other companies (the consortium members). The consortium members must each own 5% or more of the consortium company.

(CTA 2010, s.153(1) & (2))

A consortium can be established using non UK resident companies, but losses cannot be claimed from or transferred to companies which are not trading in the UK (i.e. not within the charge to UK corporation tax).

Where the consortium company makes a loss, each member may claim its share of that loss, providing it is not greater than its profits for the same period.

(CTA 2010, s.143 (2))

The consortium company must relieve (or is deemed to have done so) its own income in the current period before the consortium relief is calculated.

(CTA 2010, s.147)

If the consortium member makes a loss, it can surrender the loss to the consortium company, up to its share of the consortium company's profits. No deemed current period claim is required.

(CTA 2010, s.144 (2))

38

Tolley® Exam Training CORPORATION TAX CHAPTER 22

© Reed Elsevier UK Ltd 2015 FA 2015

GROUP CONSORTIUM COMPANIES

If the consortium company is a group consortium company then any losses which could be group relieved are deemed to have been group relieved when calculating the loss available for consortium relief. If any actual group relief claims are made between the subsidiaries of the group consortium company, these are taken into account when calculating the deemed group relief claim.

(CTA 2010, ss.148–149)

If the consortium company is a consortium holding company then losses can flow between its 90% trading subsidiaries and the consortium members.

(CTA 2010, s.153)

39

Tolley® Exam Training CORPORATION TAX CHAPTER 23

© Reed Elsevier UK Ltd 2015 FA 2015

GROUP ADMINISTRATION

GROUP RELIEF

A group relief claim must be made on the claimant company's tax return.(FA 1998, Sch 18 para 67)

It must specify the amount claimed, the name of the surrendering company and the accounting period of the claimant to which the claim relates.

(FA 1998, Sch 18 para 68)

A claim requires the written consent of the surrendering company.(FA 1998, Sch 18 para 70)

The basic time limit for making and withdrawing group relief claims is the first anniversary of the filing date of the claimant.

(FA 1998, Sch 18 para 74)

There are simplified arrangements for group relief available. Under these the claim for group relief is made by the authorised company and does not have to include a consent to surrender.

(SI 1999/2975)

GROUP PAYMENT ARRANGEMENTS

Where there is a 51 % group, the group can apply for the nominated company to make all payments of tax for the group and allocate the payments after the closing date. This is called a group payment arrangement.

(TMA 1970, s.59F(3))

GROUP TAX SURRENDERS

If the group payment arrangements are not used, amounts of tax overpaid can be surrendered within a 75% group (75% direct and indirect relationship). This is called group tax surrenders.

(CTA 2010, ss.963–966)

40

Tolley® Exam Training CORPORATION TAX CHAPTER 23

© Reed Elsevier UK Ltd 2015 FA 2015

GROUP PAYMENT ARRANGEMENTS

A

51% 51%B C

51% 51% 51%

D E F

51%

G

HOW GROUP PAYMENT ARRANGEMENTS WORK:

• Group above eligible for and submits a group payment arrangement

• B is the nominated company here and pays CT to HMRC for all the group

• Nominated company can be any member of the group, does not need to be

ultimate parent

• B apportions the CT payments amongst the group members 30 days from the closing date (later of last filing date of the group and HMRC receipt of last return)

CONDITIONS FOR GROUP PAYMENT ARRANGEMENTS:

• 51% subsidiaries

• One or more companies liable to CT by instalment payments

• Usually all companies have same period of account

• Submit application for group payment arrangements at least 1 month before 1st

instalment due

EFFECT:

• Reduce interest on over/under payments

• Reduce group's administration

41

Tolley® Exam Training CORPORATION TAX CHAPTER 23

© Reed Elsevier UK Ltd 2015 FA 2015

GROUP TAX SURRENDERS

Overpays £5,000 A

Asurrenders£5,000 to

B

100% 75%Underpays £5,000 B C

75% 75%

E D

HOW GROUP SURRENDERS WORK:

• Group with A, B, C and E only eligible for group surrenders

• A and B submit a joint notice to make the surrender

• A surrenders its overpayment to B and so treated as if A did not overpay and B did not

underpay

CONDITIONS FOR GROUP SURRENDER ARRANGEMENTS:

• 75% direct relationship AND

• 75% indirect relationship

• Not in a group payment arrangement

• All companies have same CAP

• Member of group throughout period

EFFECT:

• Reduce interest on over/under payments

42

Tolley® Exam Training CORPORATION TAX CHAPTER 24

© Reed Elsevier UK Ltd 2015 FA 2015

GROUP CAPITAL GAINS

A gains group requires a 75% relationship between companies. However, unlike group relief groups it is possible to include sub-subsidiaries of 75% subsidiaries, providing the effective holding is more than 50%.

(TCGA 1992, s.170)

Assets transferred between members of a gains group automatically move on a no gain no loss basis under TCGA 1992, s.171, i.e. the new company inherits the indexed cost of the old one.

Companies can elect to treat current year gains or losses as accruing to another group member.

(TCGA 1992, s.171A)

Gains groups can claim rollover relief on a group wide basis.(TCGA 1992, s.175)

43

Tolley® Exam Training CORPORATION TAX CHAPTER 24

© Reed Elsevier UK Ltd 2015 FA 2015

CORPORATION TAX GROUPS

1. ASSOCIATES (For FY 2014 and earlier years only) a. Companies under common control at any time during CAP

b. Include overseas resident companies

c. Ignore companies that are dormant for whole CAP

d. Include shareholdings owned by individuals

e. Control is demonstrated by > 50% of either

i. Votes, or

ii. Ordinary issued shares, or

iii. Distributable profits, or

iv. Assets when winding up

f. Divide corporation tax limits by number of associates

g. Ignore dividends received from associates in calculating FII

2. GROUP RELIEF GROUP a. 75% direct holding (each direct holding) and ≥ 75% indirect holding

b. 75% applies to all three of:

i. Ordinary shares, and

ii. Distributable profits, and

iii. Assets when winding up

c. Ignore shareholdings owned by individuals

d. Can be a member of more than 1 group relief group

e. Can only surrender current period trading losses, non-trading deficits (LR), excess UK

property business losses, excess management expenses, excess non-trading losses on IFAs and excess qualifying charitable donations.

f. Maximum loss that can be surrendered is the lower of the current period loss and the

available taxable total profits of the claimant company for the corresponding CAP

g. Can surrender current CAP losses only to other members of group relief group if an election is made (2 years from end of claimant company's CAP)

44

Tolley® Exam Training CORPORATION TAX CHAPTER 24

© Reed Elsevier UK Ltd 2015 FA 2015

3. CAPITAL GAINS GROUP a. 75% direct holding (each direct holding) and > 50% indirect holding

b. 75% applies to ownership of Ordinary shares only

c. Ignore shareholdings owned by individuals

d. Can NOT be a member of more than 1 group

e. Transfers of chargeable assets automatically at no gain no loss within the gains group

(intra group transfers)

f. Can make election to reallocate a current period chargeable gain or loss to another group company (2 years from end of CAP in which gain was made)

g. Can claim group wide rollover relief 4 years from later of end of CAP in which gain

was made or CAP in which new asset is acquired.

4. CONSORTIUM COMPANY a. Consider for any company NOT in group relief group

b. Consortium if owned ≥ 75% by companies with each company holding ≥ 5%

(consortium members)

c. Can surrender current CAP losses between consortium member and consortium company (based on consortium member's ownership of consortium company)

45

Tolley® Exam Training CORPORATION TAX CHAPTER 25

© Reed Elsevier UK Ltd 2015 FA 2015

GROUP GAINS – FURTHER ASPECTS

If a company leaves the group within 6 years of receiving an asset in a no gains no loss transfer there will be a degrouping charge. This is calculated by treating the asset as having been sold for its open market value at the date of the original transfer.

(TCGA 1992, s.179)

This degrouping charge is assessed on the vendor of the company’s shares, as an adjustment to the sale consideration.

(TCGA 1992, s.179 (3D))

As the degrouping charge now forms part of the gain arising on the disposal of the company's shares, it is subject to the Substantial Shareholding Exemption, if the conditions for the exemption are met. It can also be reallocated to another group member under s.171A.

Where IFAs are transferred intragroup, the transfer is tax-neutral. (CTA 2009, s.775)

If the transferee leaves the group within 6 years of the IFA transfer, a degrouping charge arises on the transferee in the accounting period in which it leaves the group. This is calculated as the profit or loss that would have arisen if the transfer had taken place at market value at the date of the transfer. This can be rolled over or reallocated.

(CTA 2009, s.780)

IFA rollover relief is available on a group wide basis provided the company that buys the new asset is within the same group at the time of the IFA purchase as the company that has made the IFA income gain. In addition, the new asset must be bought from outside the group.

(CTA 2009, s.777)

There are anti-avoidance rules to prevent a company acquiring another company in order to utilise its capital losses or gains.

When a company joins a group there is restriction on how its capital losses can be used by the new group. Realised pre-entry capital losses can only be set against:

i. gains on assets held by the company at the time it joined the group; and

ii. gains on assets bought from non-group members after joining the group for use in the

company's trade and/or business. This category includes gains on assets bought from non-group members by any group company which is continuing to undertake the trade or business of the new joiner company (post a s.171 transfer of assets).

(TCGA 1992, Sch 7A para 7(1A))

“Realised” pre-entry capital losses are losses on assets sold before joining the group.

There is no longer a restriction on the use of “unrealised” pre-entry capital losses.

46

Tolley® Exam Training CORPORATION TAX CHAPTER 26

© Reed Elsevier UK Ltd 2015 FA 2015

CHANGE IN OWNERSHIP OF A COMPANY

Where there has been a change in ownership of a company, the use of trading losses will be blocked from the date of the change of ownership if in a period of three years either side of the change there has been a major change in the nature or conduct of the company’s trade.

(CTA 2010, s.673 and SP 10/91)

A “major change” includes a major change in:

• property dealt in

• services provided

• facilities provided

• customers

• outlets

• markets

The anti-avoidance rules also apply where the company’s trade was small or negligible immediately before the change in its ownership, and the trade undergoes a considerable revival in any period following the change in ownership. This provision is not confined to 3 years.

Similar rules apply to the carry forward of management expenses, losses from UK and overseas property businesses, non trade deficits on loan relationships and non trading losses on Intangible Fixed Assets, following a change in ownership of a company with an investment business.

(CTA 2010, s.677)

47

Tolley® Exam Training CORPORATION TAX CHAPTER 27

© Reed Elsevier UK Ltd 2015 FA 2015

TRANSFER OF TRADES

When a trade is transferred, the following occurs:

• Trade in the transferor ceases (end of accounting period)

• Trade in the transferee commences, if no existing trade, new accounting period starts

• Capital allowance balancing adjustments will arise in the transferor as pools cease

• Two connected companies can jointly elect for the assets to transfer between them at TWDV under s.266 CAA 2001

• Trading losses stay with transferor – possible terminal loss claim

• Capital gains disposal of chargeable assets – possible rollover provisions may apply

where assets qualifying and used in the trade

• Stock will be transferred at the price paid unless it is transferred to a connected party in which case market value will apply

(CTA 2009, s.162)• Connected parties can elect to have stock treated as transferred at the higher of

cost and price paid, provided that the market value is greater than both cost and selling price

(CTA 2009, s.167)

TRANSFERS UNDER COMMON OWNERSHIP

Successions apply automatically for a transfer of trade without a change in ownership.

Where a trade within the charge to UK tax is transferred from one company to another, and there is at least 75% common ownership of it (at some point in the year before the transfer and at some point in the two years following the transfer) then:

• Trading losses are transferred to the new owner; and

(CTA 2010, s.944)• Capital allowance pools transfer at TWDV.

(CTA 2010, s.948)

There is a restriction on the transfer of losses where net liabilities are left behind in the transferor.

(CTA 2010, s.945)

Where there is a succession followed by a change in ownership of the transferee company, the major change in nature or conduct of trade rules apply, and losses may be restricted.

48

Tolley® Exam Training CORPORATION TAX CHAPTER 28

© Reed Elsevier UK Ltd 2015 FA 2015

SALE OF ASSETS VERSUS SALE OF SHARES

When considering “buying” another company, there is a choice over how the acquisition is structured. The purchaser can either buy the shares of the target company (Co B) or buy the trade and assets from the target company.

Below is an outline of the tax implications of structuring such a transaction as firstly, a sale of shares, then as a comparison, as a sale of the trade and assets. The tax implications of both will vary depending on whether the parties involved are connected or not.

Before After

Seller →→→→ BuyerSale of B shares

100% 100%

Co B Co B

SALE OF SHARES IF UNCONNECTED BUYER AND SELLER Seller

• Gain on sale of shares?

• Consider entrepreneurs’ relief for an individual shareholder / SSE for a corporate

shareholder

Co B

• No break in CAP, keeps going as normal

• Trade losses: c/fwd of losses may be restricted by CTA 2010, s.673 (“MCINOCOT”) – SP 10/91

Buyer

• One extra related 51% group company where the buyer is a company

• Buying a company with ‘history’ (a “DIRTY” company)

– Warranty from Seller confirming no undisclosed liabilities

– Indemnity – Seller agreeing to repay any tax suffered by Buyer if there is any

49

Tolley® Exam Training CORPORATION TAX CHAPTER 28

© Reed Elsevier UK Ltd 2015 FA 2015

SALE OF SHARES IF UNCONNECTED COMPANIES

Before After

Co A →→→→ Co CSale of B shares

100% 100%

Co B Co B

Co A

• Gain on sale of shares? – SSE may apply

• Possible de-grouping charge (TCGA 1992, s.179). Adjustment to gain or loss calculation for sale of Co B.

• One less related 51% group company from next CAP

Co B

• No break in CAP, keeps going as normal

• Trade losses: c/fwd of losses may be restricted by CTA 2010, s.673 (MCINOCOT) – SP

10/91

• Group relief – time apportion for period in group with Co A (up to the date “arrangements” come into force) and period in new group with Co C (from date Co C acquires shares)

• Co B may have pre-entry capital losses which cannot be used by new gains group

with Co C

• IFAs – may be degrouping charge in Co B on leaving group with Co A

• A related 51% group company of both Co A and Co C in CAP of sale

Co C

• One extra related 51% group company

• Buying a company with ‘history’

– Warranty from A confirming no undisclosed liabilities

– Indemnity – Co A agreeing to repay any tax suffered by Co C if there is any

50

Tolley® Exam Training CORPORATION TAX CHAPTER 28

© Reed Elsevier UK Ltd 2015 FA 2015

SALE OF SHARES IF CONNECTED (75%)

Before After

Co A →→→→→→→→→→→→→ Co ASale of B shares

100% 100%

Co B Co C Co C

100%

Co B

Co A

• No gain no loss – automatic

Co B

• No issues re arrangements – still in same group relief group

• No degrouping charges – does not leave gains group

• No degrouping charges on IFAs

Co C

• No implications – acquires Co B at no gain no loss value

TRANSFER OF TRADE AND ASSETS

Seller Buyer↑↑↑

Co B ↑Trade & assets →→→→→→ Trade & assets

TRANSFER OF TRADE & ASSETS IF UNCONNECTED BUYER AND SELLER Seller

• No implications

Co B

• Transfers L&B, goodwill, P&M, stock, debtors, creditors to buyer

• Trade ceases = end of CAP

• Trade Profits:

51

Tolley® Exam Training CORPORATION TAX CHAPTER 28

© Reed Elsevier UK Ltd 2015 FA 2015

– P&M = balancing adjustments using agreed price

– Income gains/ losses on IFAs using agreed price

– Losses – CTA 2010, s.37 & s.39 terminal loss relief, losses stay within Co B (no c/fwd available as Co B has ceased to trade)

• Chargeable gains on L&B and goodwill using agreed price (if bought/created pre 1

April 02) – can set trading losses against chargeable gain as part of CTA 2010, s.37 claim

• Stock sold at agreed price

Buyer

• Acquires trade & assets, therefore no history (“CLEAN” assets)

• Goodwill = IFA if purchaser is a company, new rules apply (i.e. tax relief for

amortisation of agreed price). Goodwill is capital asset if buyer is individual

• AIA on agreed price of P&M (but no FYAs as second hand assets)

• Don't get any trade losses – they remain with Co B

• No extra related 51% group company if buyer is a company

• If buyer is a person – commence a trade (opening year rules / notify HMRC)

• If buyer is a company and no other existing trade start of CAP for company / notify HMRC

TRANSFER OF TRADE & ASSETS IF BUYER AND SELLER CONNECTED (>50%) For example Mr Smith owns 51% of selling company Co B and buying company Co C

IN ADDITION TO THE POINTS MADE ABOVE

Mr Smith - shareholder

• No implications

Co B – Selling Company

• Trade Profits:

– P&M = sale at lower of cost or actual sales proceeds or can jointly elect to transfer at TWDV under s.266 CAA 2001

– IFA’s transferred at MV as connected persons (e.g. “new” goodwill)

– Losses – stay with Co B to use for current year/terminal loss claims

• L&B and Goodwill (if bought/ created before 1 April 2002 within Co B) – must use

open market value for sales proceeds as connected persons

52

Tolley® Exam Training CORPORATION TAX CHAPTER 28

© Reed Elsevier UK Ltd 2015 FA 2015

• Stock is sold at market value but seller and buyer can elect to use higher of cost and agreed price

Co C – Buying Company

• Goodwill = not IFA, remains a chargeable gain on disposal (if bought/ created before

1 April 02 within Co B)

• P&M transferred at TWDV if CAA 2001, s.266 election made, or for price paid if not

TRANSFER OF TRADE & ASSETS IF BUYER AND SELLER CONNECTED (75%) For example Mr Smith owns 75% of selling company Co B and buying company Co C

IN ADDITION TO THE POINTS MADE ABOVE

Mr Smith - Shareholder

• No implications

Co B – Selling company

• Trade Profits:

– P&M = CTA 2010, s.948 automatically transferred at TWDV

– Losses – CTA 2010, s.944 transferred with the trade (but may be restricted). No terminal loss relief available

Co C – Buying company

• P&M transferred at TWDV

• Get trade losses – losses transferred to Co C with the trade of Co B

TRANSFER OF TRADE AND ASSETS BETWEEN COMPANIES

Co A Co C↑↑↑

Co B ↑Trade & assets →→→→→→ Trade & assets

TRANSFER OF TRADE & ASSETS IF UNCONNECTED COMPANIES Co A

• No implications

Co B

• Transfers L&B, goodwill, P&M, stock, debtors, creditors to Co C

• Trade ceases = end of CAP

53

Tolley® Exam Training CORPORATION TAX CHAPTER 28

© Reed Elsevier UK Ltd 2015 FA 2015

• Trade Profits:

– P&M = balancing adjustments using agreed price

– Income gains/ losses on IFAs using agreed price

– Losses – CTA 2010, s.37 & s.39 terminal loss relief, losses stay within Co B (no c/fwd

available as Co B has ceased to trade)

• Chargeable gains on goodwill (if bought/created pre 1 April 02) and L&B – can set trading losses against chargeable gain as part of CTA 2010, s.37 claim

Co C

• Acquires trade & assets, therefore no history

• If no other existing trade already in Co C = start of CAP for Co C

• Goodwill = IFA, new rules apply (i.e. tax relief for amortisation of agreed price)

• AIA on agreed price of P&M (no FYAs as second hand assets)

• Don't get any trade losses – they remain with Co B

• No extra related 51% group company

TRANSFER OF TRADE & ASSETS IF CONNECTED (>50%) Co A

• No implications

Co B

• Trade Profits:

– P&M = sale at lower of cost or actual sales proceeds or can jointly elect to transfer

at TWDV under CAA 2001, s.266 .

– Losses – stay with Co B to use for current year/terminal loss claims

• Goodwill (if bought/ created before 1 April 02 within Co B) and L&B = must use open market value for sales proceeds as connected persons

Co C

• Goodwill = not IFA, remains a chargeable gain on disposal (assuming bought/

created before 1 April 02 within Co B)

• P&M transferred at TWDV if CAA 2001, s.266 election made, or for price paid if not

54

Tolley® Exam Training CORPORATION TAX CHAPTER 28

© Reed Elsevier UK Ltd 2015 FA 2015

TRANSFER OF TRADE & ASSETS IF CONNECTED (75%) Co A

• No implications

Co B

• Trade Profits:

– P&M = CTA 2010, s.948 automatically transferred at TWDV

– IFAs transferred = tax neutral

– Losses – CTA 2010, s.944 transferred with the trade (but may be restricted)

• Goodwill (if bought/ created before 1 April 02 within Co B) and L&B = No gain no loss

(automatic)

Co C

• Goodwill = not IFA, remains a chargeable gain on disposal (assuming bought/created before 1 April 02 within Co B)

• P&M transferred at TWDV