memo mobile financial services - orange.com · mobile financial services and connected objects are...

TRANSCRIPT

Memo MobileFinancial Services

January 2017

Ambition and strategyMobile financialservices are an opportunity

■ Increase customer loyalty.

■ New income-generating activity.

■ Strategic axis for new customer acquisition.

Orangehas many assets

■ A strong brand.

■ An extensive customer base.

■ A distribution network with a high customer-interaction rate.

■ Technological and marketing know-how.

■ Unique advantages for Orange and Orange Bank customers.

The Orange financial services ambition

Mobile financial servicesand connected objects are the Group’s two diversification levers.

02

Global

Europe

Africa

400 millions eurosturnover in 2018

Banklaunch

30 million Orange Money customers in 2018

Mobile Financial Services

Make mobile financial services available for all

Mobile Money

Mobile Banking

Europe

NFC Mobile Payment

Europe

Orange Cashavec Visa

Africa

03Mobile Financial Services

Since 2008, an improved mobile financial services offer to meet our customers’ new needs.

Africa

Useyour mobile

to pay and

send money

Poland

Subscribe to banking services*

on your mobile* In partnership

with mBank

France, Spain

Usecontactless

paymentwith your mobile

The African diaspora in France

Sendmoney

to Africa fromyour mobile

France

Subscribe to Orange Bank

services on your mobile

2008 2014 2015 2016 2017

Orange Finanse

Orange Cash

Orange Bank

Why diversify into banking?

■ Banking is a telecoms- related activity because bank services are increa-singly accessible via smart-phones (85% of banking interactions are carried out on smartphones).

■ Orange is trusted by our clients and close to them: both advantages have been identified by our customers when choosing a bank.

Orange is now a bank operator with Orange Bank which will be launched in France in 2017, and subsequently in Spain and Belgium.

Favourable environment

■ Booming mobile use.

■ Increasing customer adoption of online banking.

■ Changes in the regulatory environment making bank switching easier.

Why choose a partnershipwith Groupama?

■ Aligned strategy and joint vision.

■ Robust banking processes saving time for launching an offer.

■ A distribution network with 3,000 Groupama and Gan agencies and their 13 million customers.

■ An exportable model to Belgium and Spain.

What do Orange customers think?

A third of customers are interested in opening an Orange Bank account and a third would like to be contacted at the launch (in-store customer survey - 920 replies).

Mobile Banking in Europe

05Mobile Financial Services

What is the Orange Bank offer?

■ An offer for individuals, Orange customers and non-Orange customers.

■ 100% mobile for easy, everyday banking.

■ Simple, transparent, different.

■ Real time.

■ Comprehensive offer: current account, loan, savings and insurance at a later stage.

■ Unique customer experience.

■ And specific benefits for Orange and Orange Bank customers.

Orange Bank in a nutshell

• An agile bank.

• A «Phygital» model. Physical and digital acquisition. Innovative mobile services.

At the launch:

• 800 advisors trained and certified IOBSP (Intermediary in Banking and Payment Services).

• 140 Orange stores with a dedicated area for subscription.

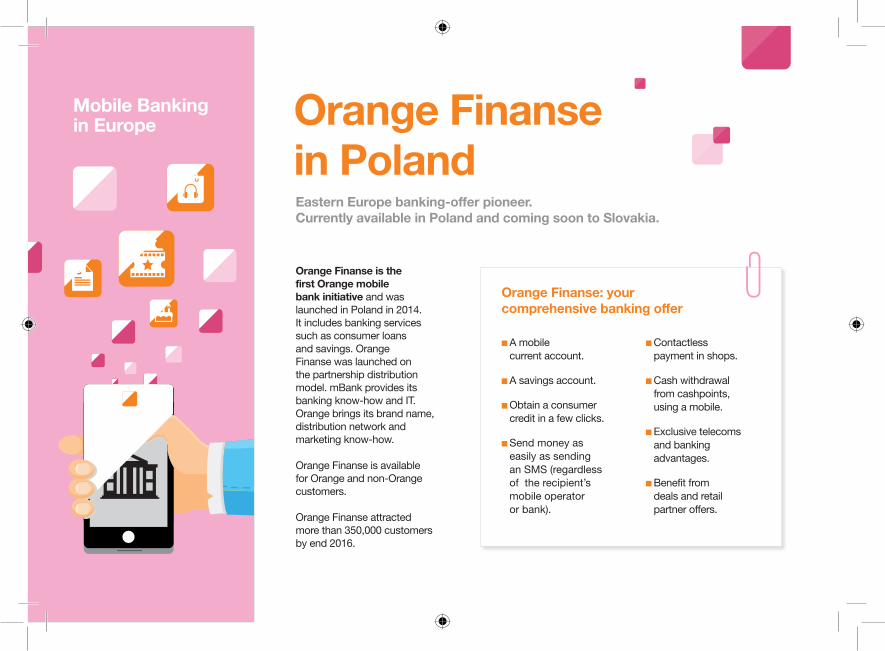

Orange Finansein Poland

Orange Finanse is thefirst Orange mobile bank initiative and was launched in Poland in 2014. It includes banking services such as consumer loans and savings. Orange Finanse was launched on the partnership distribution model. mBank provides its banking know-how and IT. Orange brings its brand name, distribution network and marketing know-how.

Orange Finanse is available for Orange and non-Orange customers.

Orange Finanse attracted more than 350,000 customers by end 2016.

■ A mobile current account.

■ A savings account.

■ Obtain a consumer credit in a few clicks.

■ Send money as easily as sending an SMS (regardless of the recipient’s mobile operator or bank).

■ Contactless payment in shops.

■ Cash withdrawal from cashpoints, using a mobile.

■ Exclusive telecoms and banking advantages.

■ Benefit from deals and retail partner offers.

Orange Finanse: your comprehensive banking offer

Eastern Europe banking-offer pioneer.Currently available in Poland and coming soon to Slovakia.

Mobile Banking in Europe

07Mobile Financial Services

Orange Cash

To subscribe to Orange Cash, customers

must have a postpaid Orange contract (incl. capped, Sosh and corporate tariffs), own an NFC mobile which is compatible with Orange Cash and an NFC SIM card.

With Orange Cash, customers can open

a prepaid account:

■ Reloaded with a Visa or Mastercard, according to each customer’s needs.

■ Regardless of the customer’s bank.

■ Limited user spending for an amount which the customers themselves decide via their smartphones.

Orange Cash is an application

for all Orange customers which can be easily downloaded for free (on Android, Windows Phone and iOS from iPhone 6 onwards).

21

3

Orange Cashavec Visa

Orange Cashavec Visa

NFC mobile payment in Europe

■ Locate the shops near you.

■ Contactless mobile payment in shops.

■ Take advantage of special offers.

■ Pay for purchases of up to 300 euros with your mobile.

■ You can also pay for your purchases online without disclosing your bank card number.

■ Your teenagers can pay with their mobile and benefit from special offers whilst learning how to manage their budgets with Orange Cash Teens.

Easier shopping and increased special offers with Orange Cash.

NFC mobile payment. Available in France and Spain.

■ With flat rates of 0,79 euros per top-up whatever the amount.

■ Commitment and subscription-free solution which does not require the presentation of documents (2,500 euros top-up limit per year).

Orange Cashis retail smartshopping:

■ Orange Cash can be used in any sales point around the world accepting Visa contactless payment. Over 500,000 retailers in France (30%) and over 800,000 (70%) in Spain.

Orange Cash is a secure

payment method: ■ Orange Cash is in partnership with Visa: Orange Cash offers the same level of security as a the chip in the bank card.

■ A secret code,or digital fingerprintfor iPhones, is required for all payments over 20 euros and online payments. It can be activated on user request for all payments above one euro.

Orange Cashis a prepaid

payment service, launched in partnership with Wirecard and Visa Europe. The service is currently available in France and Spain.

4

5

6

09Mobile Financial Services

11.5 million users in France own an NFC mobile*

*AFSCM juin 2016

500,000 Orange Cash customers 400,000 in France and 100,000 in Spain

12 euros per average purchase

Key figures

Orange Money

Orange Moneyis key to economic

and societal development.

■ It makes trade easier. It improves access to remote territories.

■ It promotes female entrepreneurship: this is highest in Sub-Saharan Africa where 25% of women create businesses (source: 2014 Global Entrepreneurship Monitor global report).

International money transfer extends

Orange Money benefits to the diasporas.

■ Sub-Saharan Africa transfer between Ivory Coast, Mali, Senegal and Burkina Faso.

■ Transfer between France and Africa (to Ivory Coast, Mali and Senegal).

In 2016, Orangecreated 5 EMIs

(Electronic Money Institution)in 5 countries (Ivory CoastGuinea, Mali, Senegal and the Democratic Republic of Congo). Orange will gain increased autonomy and agility from this status and will be able to launch new services.

Orange safeguards customers’ funds and guaranties bank compliance through the CECOM (Expertise Center for Orange Money Compliance based in Abidjan).

Orange Money is an electronic money

account linked to an Orange mobile number.

It is a universal solution which is available on

any mobile and works when there is no data network. There is also an Orange Money application for smartphone owners.

1

2

3

4

5

Mobile Money in Africa

Mobile payment and money transfer in Africa. This service was extended to France in 2016. It enables our customers to sendmoney to Africa via their mobiles.

11Mobile Financial Services

Initially, Orange Money met the urgent needs of unbanked customers

■ Transfer money to your family.

■ Top-up your airtime credit.

Orange Money’s success has enabled it to develop its services

■ Pay your bills.

■ Pay your taxes.

Orange Money waslaunched in IvoryCoast in 2008

Orange Money is present in 17 African and Middle-Eastern countries:Botswana, Burkina Faso*,Cameroon, Ivory Coast, Egypt, Guinea, Guinea- Bissau**, Mauritius Island, Liberia**, Madagascar,Mali, Niger, Central African Republic, Democratic Republic of Congo, Senegal, Sierra Leone*, Tunisia.

* Under the brand name Airtel Money

** Under the brand name Smile Money

Orange Moneystrategy

■ Develop international destinations.

■ Develop the partnership ecosystem (utilities, banks and distributors, etc.).

■ Develop financial services: pico loan, savings.

■ Make Orange Money a universal means of online payment thanks to Orange Money APIs.

December 2016 key figures

29 million Orange Money customers

8 million customers use it every month

160,000 sales points

■ Receive your salary or your pension.

■ Withdraw cash with your mobile.

■ Own an Orange Money Visa card.

Orange Money is extending its services to customers with bank accounts

■ Make transfers between your bank account and your Orange Money mobile account.

12 Mobile Financial Services

Orange and fintechsOrange Fab

■ A global startup accelerator programme (France, Silicon Valley, south-east Asia, Poland, Ivory Coast, Israel).

■ Several fintechs have benefited from the Orange Fab programme, such as Pumpkin in France: a refund solution between friends; or Token in the Silicon Valley: a secure exchange solution between banks and payment service providers.

Orange Digital Ventures: a fintech portfolio

As part of the Group’s strategy, Orange Digital Ventures is continuing early-stage startup investments, especially in its banking activity. Invested funds raised range from 500,000 to 3 million euros.

■ Afrimarket With “cash-to-goods” money transfer in association with partner retailers (food, health, education, etc.), users in Europe can pay for their friends and family’s everyday purchases in Africa. It is one of the leading international

money transfer markets. Users can choose how they wish to help friends or family and benefit from reduced rates, in comparison to traditional solutions, and also rest assured that quality fund-tracking products are used.

What is a fintech?

Put “Finance” and “Technology” together and you come up with fintech: banking startups which combine technology and banking services for individuals and companies. These companies use disruptive technologicaland economical models which aim to deal with existing or future issues in the financial services industry.

Afrimarket in a nutshell

CEO: Rania Belkahia, Jérémy Stoss.

Created in 2013.

Previous funding: 10 million euros in September 2016.

Country: France.

13Mobile Financial Services

Chain in a nutshell

CEO: Adam Ludwin.

Created in 2014.

Previous funding: 30 million dollars in September 2015, in particular with Visa, Fiserv and NASDAQ.

Country: United States.

■ Chain Chain is the first international technological blockchain solutions provider and is a new digital information or asset transfer model. The blockchain can facilitate, for example, the emission and transfer of financial shares, vouchers, mobile credit and also fully secure immediate transactions.

Lendopolis in a nutshell

CEO: Vincent Ricordeau.

Created in 2014.

Previous funding: 5 million euros in Kiss Kiss Bank Bank, February 2016.

Country: France.

■ LendopolisLendopolis (Kiss Kiss Bank Bank Group) is a French SOHO/SME online crowdfunding platform which pays for itself directly via individuals who wish to boost their savings. This new funding model gives new meaning to savings as it contributes to French SOHO/SME development. According to project type and time scale, the gross interest rate can generate 5 to 12%. Each project is initially approved by chartered accountants and financial analysts who monitor and ensure project reliability.

The word on the street…New technologiesare transformingthe world of banking

■ Blockchain technology, made famous by Bitcoin emoney, is used to save and check real time transactions. By reducing the level of intermediaries Blockchain challenges current economic models and reduces running costs.

■ Artificial intelligence understands and interprets natural language. In the banking sector, robot advisors offer high-quality added value services and operational cost management.

■ Biometric technology is used to provide new secure customer banking service authentication methods. Customers can now sign in to a banking application using a digital fingerprint or make payments using voice or facial recognition.

New market entrants

■ Fintechs Three main fintech categories

- Lending Platform (funding platform)

- Consumer Banking (everyday banking)

- Payment (payment method)

■ Neo banks Neo banks are based on a simplified mobile application and customer experience. Some have a banking licence and others do not. Many offer innovative mobile offers in Europe (UK, Germany, France).

■ The GAFA Sector giants like Apple, Samsung and Google offer mobile payment solutions: Apple Pay, Samsung Pay and Android Pay. They can now directly offer financial services upon banking licence acquisition.

Digital bankingdevelopment

■ Bank accounts and the weather channel are in the top 3 applications checked every morning (in France).

■ One third of new bank accounts are opened with online banks.

■ The number of customers who use internet and mobiles for their banking operations has increased by 50% in one year.

■ Online banks have gained 14% in market shares in the past 3 years in France.

■ Today, 85% of customer/bank dealings are now digital, 17% of customers go to their bank in comparison to 62% in 2007.

14 Mobile Financial Services

Regulations to boost mobile uses

■ In 2017, the PSD2(European Payment. Services Directive)will open the paymentmarket to newcomers. This will increase industrycompetition and reduce consumer payment method access costs.■

■ The European directive also aims to implement instant payment before end 2017. This is an electronic payment solution which is available at any given moment.This directive translates as a new revolution for the mobile payment sector.

January 2017

Orange Cashavec Visa